29

EP Energy's Flagship - The Eagle Ford Optimizing Spacing to Maximize Value Greg Givens Vice President, Eagle Ford October 15, 2012

| Date post: | 13-Jan-2015 |

| Category: |

Documents |

| Upload: | nickster66 |

| View: | 321 times |

| Download: | 3 times |

EP Energy's Flagship - The Eagle Ford Optimizing Spacing to Maximize Value

Greg Givens Vice President, Eagle Ford

October 15, 2012

2

Cautionary Statement In this presentation, EP Energy has disclosed its proved reserves using the SEC's definition of proved reserves under rules effective December 31, 2009. Proved reserves are estimated quantities of hydrocarbons that geological and engineering data demonstrate with reasonable certainty to be recoverable in the future from known reservoirs under the assumed economic conditions. In this presentation, EP Energy has provided estimates of its “net risked resources,” “unproved resources” or “inventory” which are different than probable and possible reserves as defined by the SEC. Net risked resources, unproved resources or inventory are estimates of potential reserves that are made using accepted geological and engineering analytical techniques. This presentation presents certain production and reserves-related information on an "equivalency" basis. Equivalent volumes are computed with oil and natural gas liquid quantities converted to Mcf at a ratio of one Bbl to six Mcf, and natural gas converted to barrels at a ratio of six Mcf to one Bbl. A Boe conversion ratio of six Mcf of natural gas to one Bbl, and a Mcfe conversion ratio of one Bbl of crude oil or NGLs to six Mcf, is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Although these conversion factors are industry accepted norms, they are not reflective of price or market value differentials between product types. Certain of the production information in this presentation includes the production attributable to EP Energy’s 48.8 percent interest in Four Star Oil and Gas Company (“Four Star”). In addition, the proved reserves attributable to its interest in Four Star represent estimates prepared by EP Energy and not those of Four Star. This presentation refers to the non-GAAP financial measures “Cash Operating Costs” and “Adjusted Cash Operating Costs”. Definition of these measures and reconciliation between U.S. GAAP and non-GAAP financial measures is included in the Appendix to this presentation.

3

Company Update

May 24, 2011 – Announced EPE spin-off

October 16, 2011 – Kinder Morgan announced acquisition of El Paso Corporation (with intent to sell E&P assets)

May 25, 2012 – Launched EP Energy

Closed sale to private equity group

More information on our new website

epenergy.com

4

Strategy: How We’ll Get There

5

Purpose: What We Do

At EP Energy, we have a passion for finding and producing the

oil and natural gas that enriches people's lives

6

Vision: Where We're Going

7

Values: How We Behave

8

Competitive Advantages 4.0 Tcfe of proved reserves – PV-10 of ~$7 billion1

Rapidly growing oil shale plays -- onshore U.S. unconventional

Producing wells currently 77% operated1

20+ year drilling inventory -- ~4,500 locations, 85% oil - related1

Natural gas inventory is largely held-by-production

2011 drilling success rate of 100% (233 gross wells)

1 As of 12/31/11. Pre-tax PV-10 value assumes SEC pricing, as of 12/31/11 2As of 6/30/12, proforma for the Financing Transaction completed on 8/13/12

Large, Diverse High Quality Asset Base

Industry leading well cost performance in key programs

Top tier lease operating expense performance

Manage returns and margin through commodity price cycles

Base PDP assets (1.7 Tcfe)1 provide predictable cash flow

Favorable hedge position

~$1.6 billion liquidity2

Leadership team comprised of former El Paso employees

Focused – build assets with repeatable programs/inventory

Asset teams and culture remain in place

Strong Financial Position

Experienced Team

Extensive Low-Risk Inventory

Efficient Operations

9

EAGLE FORD

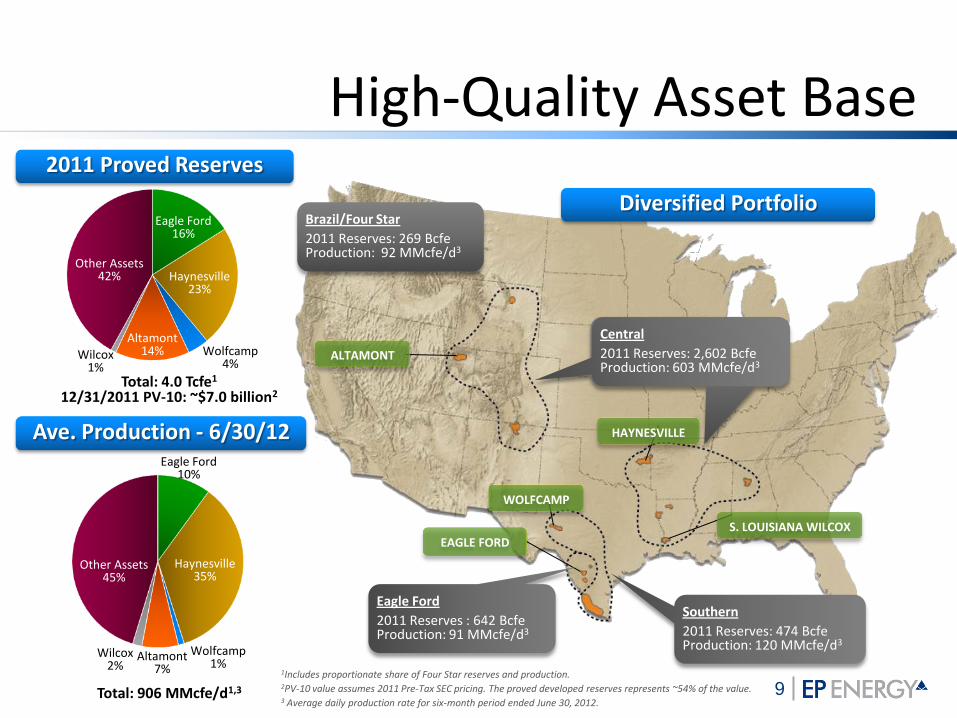

High-Quality Asset Base 2011 Proved Reserves

Total: 4.0 Tcfe1

12/31/2011 PV-10: ~$7.0 billion2

Total: 906 MMcfe/d1,3

Ave. Production - 6/30/12

Altamont 7%

Other Assets 45%

Wolfcamp 1%

Wilcox 2%

Eagle Ford 10%

Haynesville 35%

1Includes proportionate share of Four Star reserves and production. 2PV-10 value assumes 2011 Pre-Tax SEC pricing. The proved developed reserves represents ~54% of the value. 3 Average daily production rate for six-month period ended June 30, 2012.

Altamont 14%

Other Assets 42%

Wolfcamp 4%

Wilcox 1%

Eagle Ford 16%

Haynesville 23%

Central

2011 Reserves (Bcfe): 1,110 4Q 2011 Production (MMcfe/d): 153

Central

2011 Reserves: 2,602 Bcfe Production: 603 MMcfe/d3

Southern

2011 Reserves: 474 Bcfe Production: 120 MMcfe/d3

Brazil/Four Star

2011 Reserves: 269 Bcfe Production: 92 MMcfe/d3

Eagle Ford

2011 Reserves : 642 Bcfe Production: 91 MMcfe/d3

Diversified Portfolio

ALTAMONT

WOLFCAMP

S. LOUISIANA WILCOX

HAYNESVILLE

10

Low-Risk 90% 97% 100%

Drilling Inventory Growth

Liquids 6:1 34% 48% 59%

Domestic 82% 90% 99%

Core Prog1 46% 61% 78%

2009 2010

1Core programs include Altamont, Eagle Ford, Haynesville (includes Middle Bossier), Wolfcamp and South Louisiana Wilcox

Note: Inventory includes unproved resources and proved undeveloped reserves; All inventory is risked, net to EP Energy’s interest

Net Risked Resources Excluding PDP and PDNP (Tcfe)

Significant oil and natural gas inventory with high ownership and control

2011

0.9 1.3 1.9

2.5

4.2

6.2 2.0

2.2

1.6

0.6

0.2

0.0

2009 YE 2010 YE 2011 YE

PUD Unconventional Conventional Lower Risk Conventional Higher Risk

6.0

8.0

9.7

11

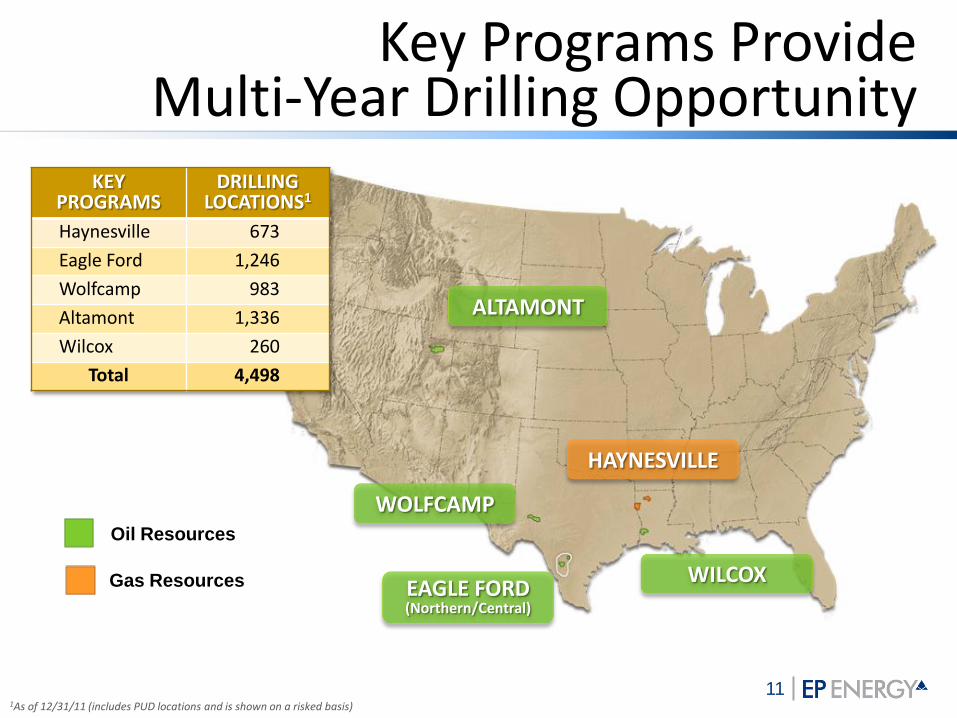

Key Programs Provide Multi-Year Drilling Opportunity

HAYNESVILLE

EAGLE FORD (Northern/Central)

WOLFCAMP

ALTAMONT

WILCOX

1As of 12/31/11 (includes PUD locations and is shown on a risked basis)

KEY PROGRAMS

DRILLING LOCATIONS1

Haynesville 673

Eagle Ford 1,246

Wolfcamp 983

Altamont 1,336

Wilcox 260

Total 4,498

Oil Resources

Gas Resources

12

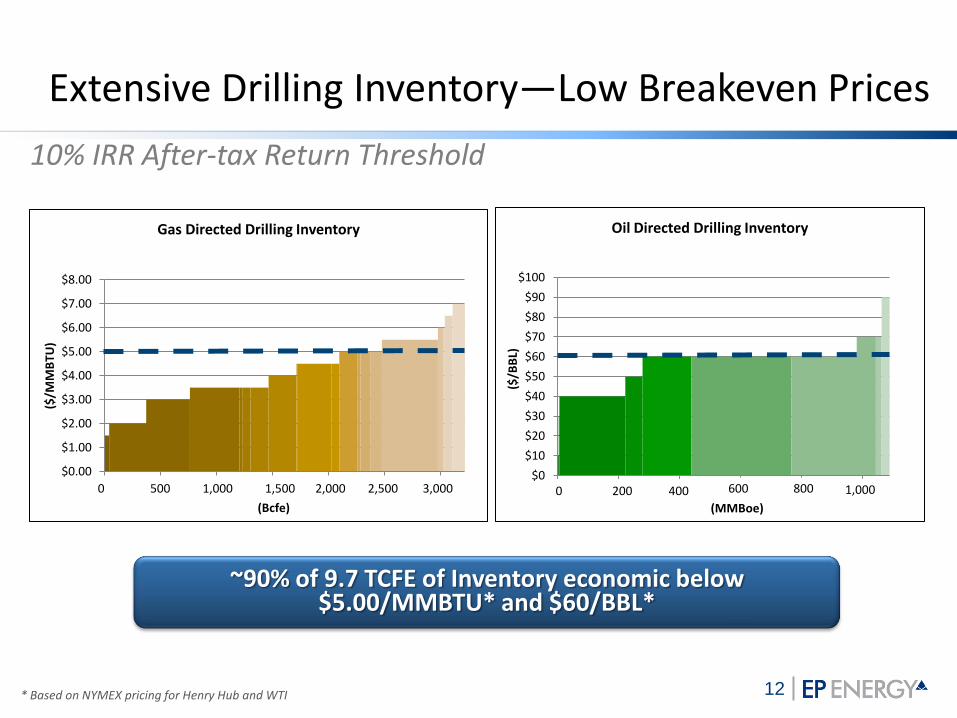

Extensive Drilling Inventory—Low Breakeven Prices

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

0 500 1,000 1,480 1,980 2,480 2,980

($/M

MB

TU)

(Bcfe)

Gas Directed Drilling Inventory

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

0 200 399 599 799 999

($/B

BL)

(MMBoe)

Oil Directed Drilling Inventory

500 1,000 1,500 2,000 2,500 3,000 0 0 200 400 600 800 1,000

~90% of 9.7 TCFE of Inventory economic below $5.00/MMBTU* and $60/BBL*

* Based on NYMEX pricing for Henry Hub and WTI

10% IRR After-tax Return Threshold

13

2012 Capital Budget

> 90% allocated to oil-focused key programs

3% 6%

8%

12%

13%

$1.5 - $1.6 Billion1

1Includes ~$100 MM of capitalized interest, information technology and capitalized direct labor costs

14

Favorable Program Economics

Capital

($MM) 1 EUR

(Mboe) 1

Initial Production (Boe/d)1,2 IRR3

Average Working Interest

Eagle Ford, Central 8.0 – 8.4 500 – 600 750 – 900 45 – 65% 92%

Wolfcamp 8.0 – 8.4 465 – 510 575 – 675 20 – 30% 100%

Altamont 4.6 – 7.7 300 – 450 400 – 600 20 – 40% 89%

Wilcox 6.0 – 7.0 320 – 440 500 – 900 30 – 70% 85%

1 Based on 100 percent working interest 2 Based on initial 24 hours of production 3 After-tax internal rate of return net to EP Energy interest based on $3.50 per MMBtu (HH) and $90.00 per Bbl (WTI)

Focused investments delivering excellent returns

15

Continuous Improvement

9.8

10.9

6.6

8.28.2 8.2

6.2 6.5

Eagle Ford Wolfcamp Altamont Wilcox

First 3 Wells Current (median)

Gross Capital Cost Per Well ($MM)

$1.72 $1.71

$1.69

$1.66 Adjusted Cash Operating Costs ($/Mcfe)

16

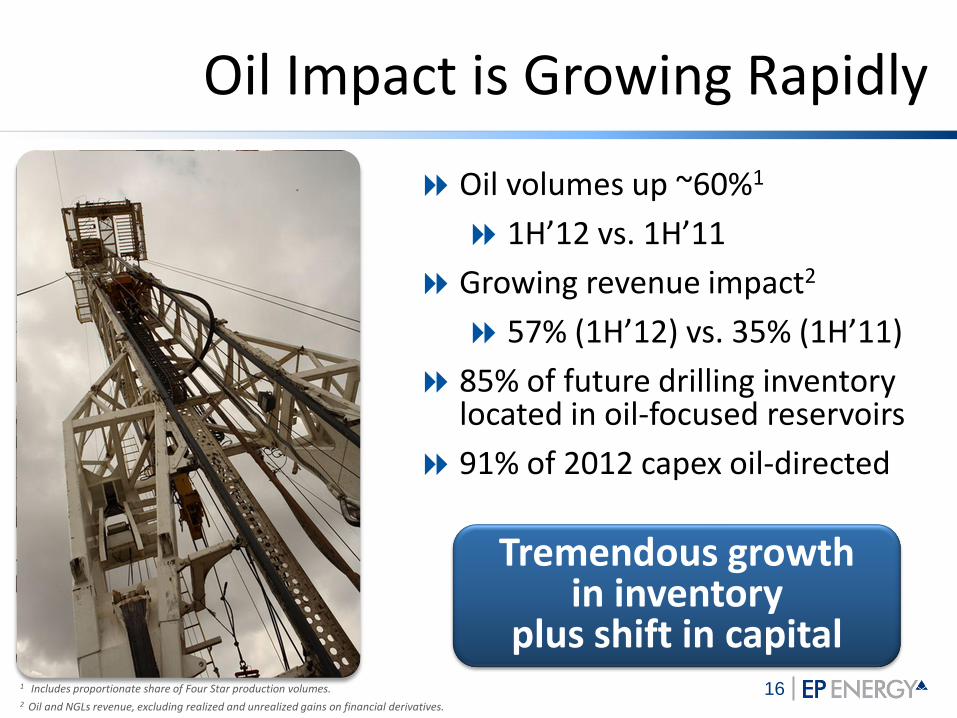

Oil Impact is Growing Rapidly

Tremendous growth in inventory

plus shift in capital

Oil volumes up ~60%1

1H’12 vs. 1H’11

Growing revenue impact2

57% (1H’12) vs. 35% (1H’11)

85% of future drilling inventory located in oil-focused reservoirs

91% of 2012 capex oil-directed

1 Includes proportionate share of Four Star production volumes. 2 Oil and NGLs revenue, excluding realized and unrealized gains on financial derivatives.

17

Eagle Ford

Highest return and highest value asset in portfolio

Advantaged acreage position in Central Area (La Salle/Dimmit Co.)

Significant inventory of oil opportunities (1246 locations1)

Major source of future oil production and reserve adds

2012 Program

Drilling 86 wells

Currently running 5 rigs

~$896 MM capex

Avg. Net Production Growth

0.0

3.0

6.0

9.0

12.0

15.0

18.0

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

MB

oe/

d

Gas NGL Oil

157,000 total net acres1

77,000 in Central area

642 Bcfe estimated net proved reserves1

88 net producing wells2

1 As of December 31, 2011 2 As of June 30, 2012

18

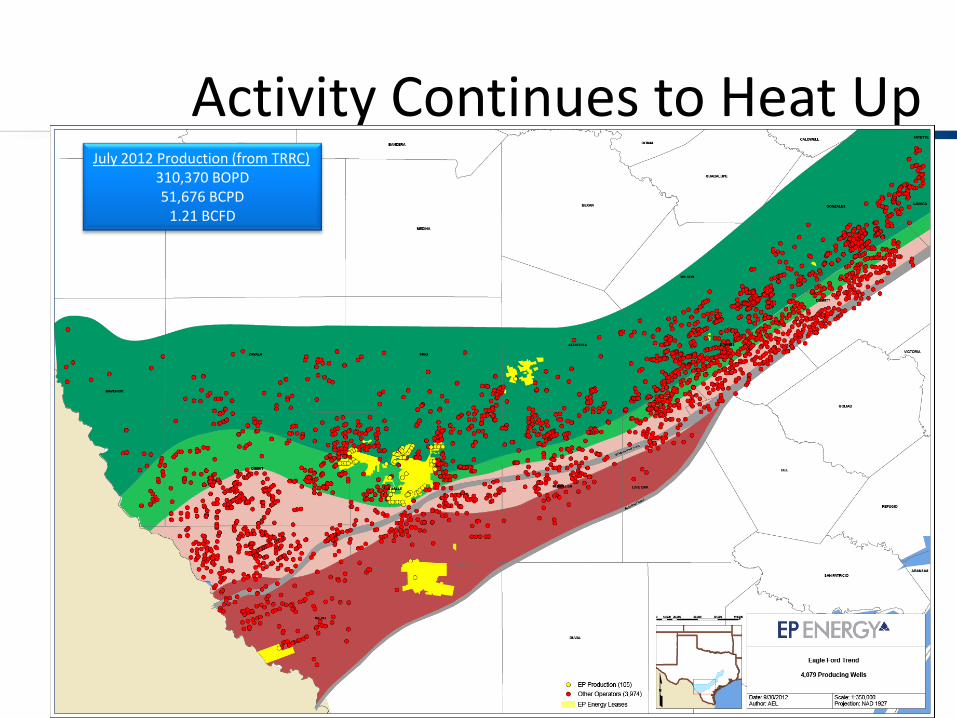

Activity Continues to Heat Up July 2012 Production (from TRRC)

310,370 BOPD 51,676 BCPD

1.21 BCFD

19

21

16 15 14

2010 1H 2011 2H 2011 1H 2012

Rig Days (Spud to Rig Release)

2.3

2.9

3.7

4.5

2010 1H 2011 2H 2011 1H 2012

Stimulation (Stages/Day)

Operational Efficiency Improves over time

1 Rig line now drills >20 wells per year

Higher efficiency lowers total well cost

763 723 721

1036

2010 1H 2011 2H 2011 1H 2012

Initial 24 hr rate1 (BOE/Day)

Well performance continues to improve

1 Maximum continuous 24 hours Note: Based on Central Area wells only

20

Field Gathering/Central Facilities

LACT

Well Paths

Frac Pond

Oil, Gas & Water Flow

Lines

Potential Future Well Locations

Road

Common Facility

Midstream Oil & Gas

Lines

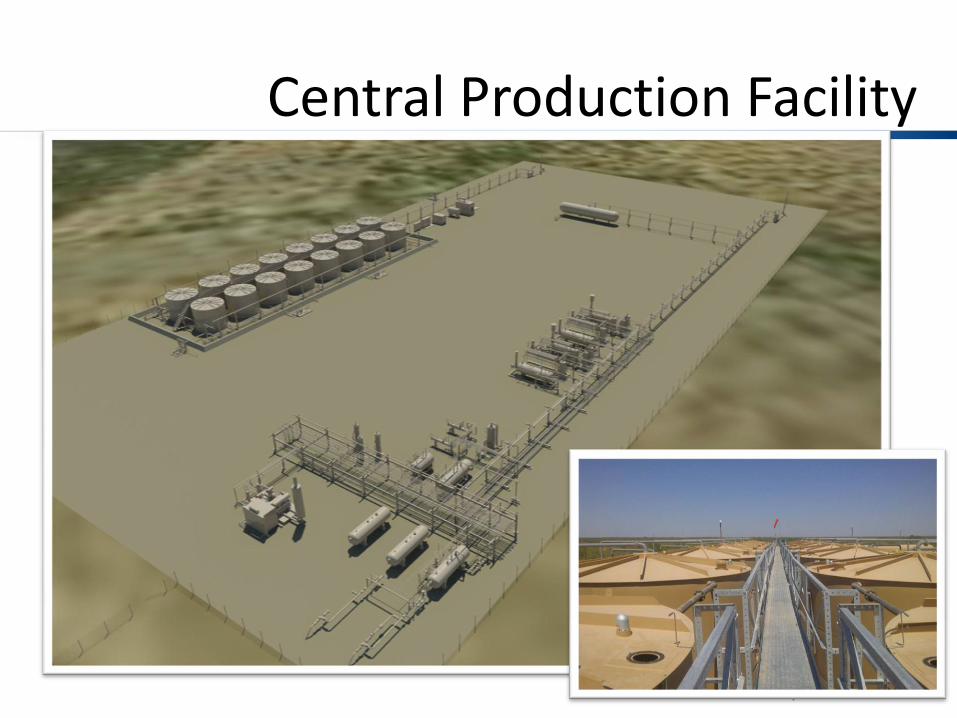

Wells within 3-4 miles gathered at Central Production Facility (CPF)

Oil and Gas connected to regional pipelines through midstream gathering lines

Maintain option to truck oil

30-40 wells connected to each CPF at full development

21

Central Production Facility

22

Eagle Ford Oil & Gas Infrastructure

In-field Gathering

Owned and operated by EP Energy

Wellhead gathering to 12 central batteries currently; additional batteries under construction

Camino Real Gathering System*

Natural gas system capacity of 150–170 MMcf/d

Oil system capacity of 90,000 Bbls/d, with blending capability

Additional connections to new lines under construction in area would substantially increase capacity

Takeaway

Sufficient downstream processing and transportation capacity to accommodate aggressive gas volume growth

Long-term oil sales agreements with premium pricing to WTI

Began oil deliveries to downstream markets via pipeline 1Q 2012

*Camino Real is owned and operated by Kinder Morgan

DIMMI

T

LA SALLE OIL

VOLATILE OIL

WET GAS

DRY GAS

EP acreage

Camino Real Gas line

Gas interconnects

Camino Real Oil line

Oil interconnects

Oil terminal

Gardendale Rail

Facility

Enterprise

Kinder/Copano

ETC

Regency

Hilcorp Gardendale

Hilcorp Cotulla

DIMMIT

23

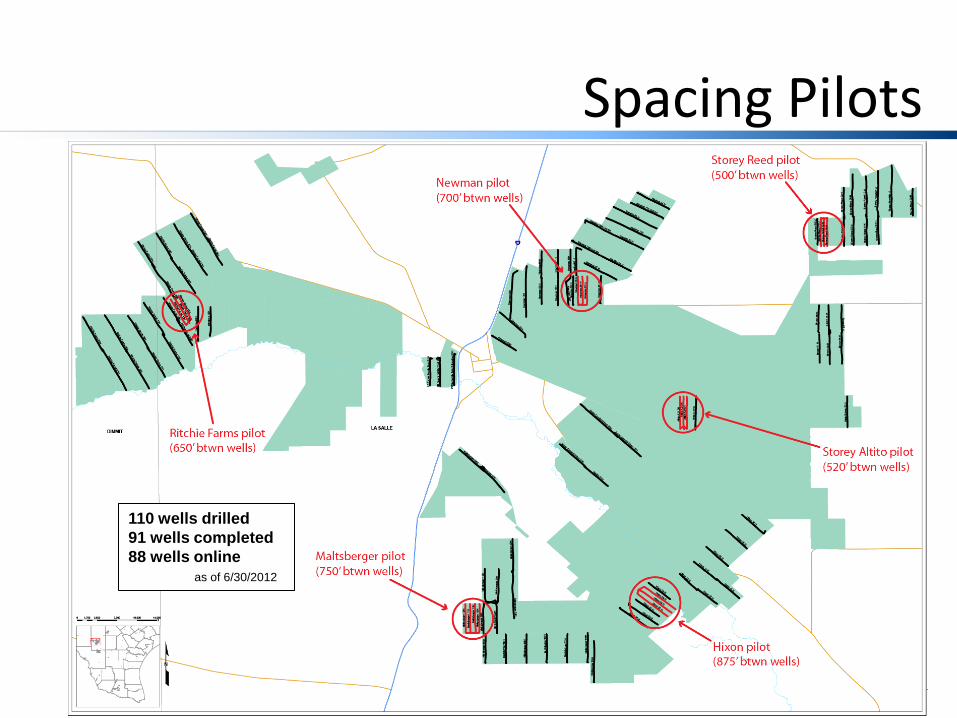

Spacing Pilots

110 wells drilled

91 wells completed

88 wells online

as of 6/30/2012

24

700 ft well spacing

875 ft well spacing

60 acre drainage area

Microseismic used to determine extent of fracture network

Production testing and reservoir simulation aid in selecting the optimal between well spacing

Microseismic Surveys

25

Initial Pilots holding up well

26

Increased density successful to date

27

Keys to success

Sound development strategy

Long range planning

Infrastructure build-out takes time

Evaluate & test options early

Continuous improvement culture

Cost management

Utilize latest technology

“Little things add up when you are drilling 1000 wells”

28

Thank you

29

Additional Non-GAAP Information EP Energy uses the non-GAAP financial measures of Cash Operating Costs and Adjusted Cash Operating Costs. We believe these supplemental

measures provide meaningful information to our investors; however, due to the limitations of these measures as analytical tools, we rely primarily

on our GAAP results.

Cash Operating Costs and Adjusted Cash Operating Costs. We monitor cash operating costs required to produce our oil and natural gas

production volumes. Cash operating costs is a non-GAAP measure calculated on a per Mcfe basis and includes total operating expenses less

depreciation, depletion and amortization expense, ceiling test and other impairment charges, exploration expense and transportation costs and

costs of products. Adjusted cash operating costs reflects cash operating costs adjusted for non-recurring transition and restructuring costs,

advisory fees paid to our sponsors, and non-cash equity based compensation expense. We believe cash operating costs and adjusted cash

operating costs per unit are valuable measures to provide management and investors reflecting operating performance and efficiency; however, as

non-GAAP measures, these measures may not be comparable to similarly titled measures used by other companies, have limitations as analytical

tools, and should not be considered in isolation.