Growth and profit drivers in non-life R/I Accomplishing profitable growth in a challenging environment Jürgen Gräber, Member of the Executive Board/COO non-life 15th International Investors' Day 2012 London, 18 October 2012

Transcript

Growth and profit drivers in non-life R/IAccomplishing profitable growth in a challenging environment

Jürgen Gräber, Member of the Executive Board/COO non-life

15th International Investors' Day 2012London, 18 October 2012

Introduction Target markets Specialty lines Global R/I Conclusion

Growth and profit drivers in non-life reinsurance

1. Introduction

2. Growth and profit drivers by non-life divisions

a) Selected Target Market - North America Business

b) Specialty Lines example - Agency Business

c) Global Reinsurance examples – Facultative, Agricultural and ReTakaful Business

3. Conclusion

Growth and profit drivers in non-life R/I

Agenda

Recapturing Investors' Day 2010 and 2011: We remain on track

� 2010 – 2012F est. GWP growth of our Chinese business: 22%

� 2011 – 2012F est. GWP growth of our Specialty Lines: 12%

Introduction Target markets Specialty lines Global R/I Conclusion

Introduction

� World real GDP growth expected to slow down from 4.0% (2011) to 3.5% (2012)

� Real GPD growth of emerging and developing economies expected to slow down

from 6.2% (2011) to 5.6% (2012)

� Recession in Europe is likely to continue through 2013

� Uncertainty about the economic situation in Europe remains global key risk

� Nonetheless, non-life insurance premium increased during 2011 by 1.9%

� Demand for top-rated reinsurance companies remains high

Growth and profit drivers in non-life R/I

Sources: Towers Watson – Global Markets Overview, July 2012, International Monetary Fund - World Economic Outlook April 2012,

International Monetary Fund – World Economic Outlook Update July 2012, The World Bank – Global Economic Prospects January 2012,McKinsey Global Institute – Mapping global capital markets 2011

HR well positioned - high performance in a challenging economic environment

1

Introduction

Introduction Target markets Specialty lines Global R/I Conclusion

Non-life insurance market premium development

Growth and profit drivers in non-life R/I

Emerging markets lead the way

Source: Swiss Re Sigma 3/2012

Non-life insurance premium in bn. USD 2011 change vs. 2010

North America 736 -1.1%

Latin America and Caribbean 89 10.7%

Western Europe 642 0.7%

Central and Eastern Europe 72 6.7%

Japan and new advanced Asian economies 208 5.0%

South and East Asia 119 10.2%

Middle East and Central Asia 30 8.9%

Africa 22 3.3%

Oceania 53 8.1%

World 1,971 1.9%

Advanced markets 1,639 0.5%

Emerging markets 332 9.1%

2

Introduction

Introduction Target markets Specialty lines Global R/I Conclusion

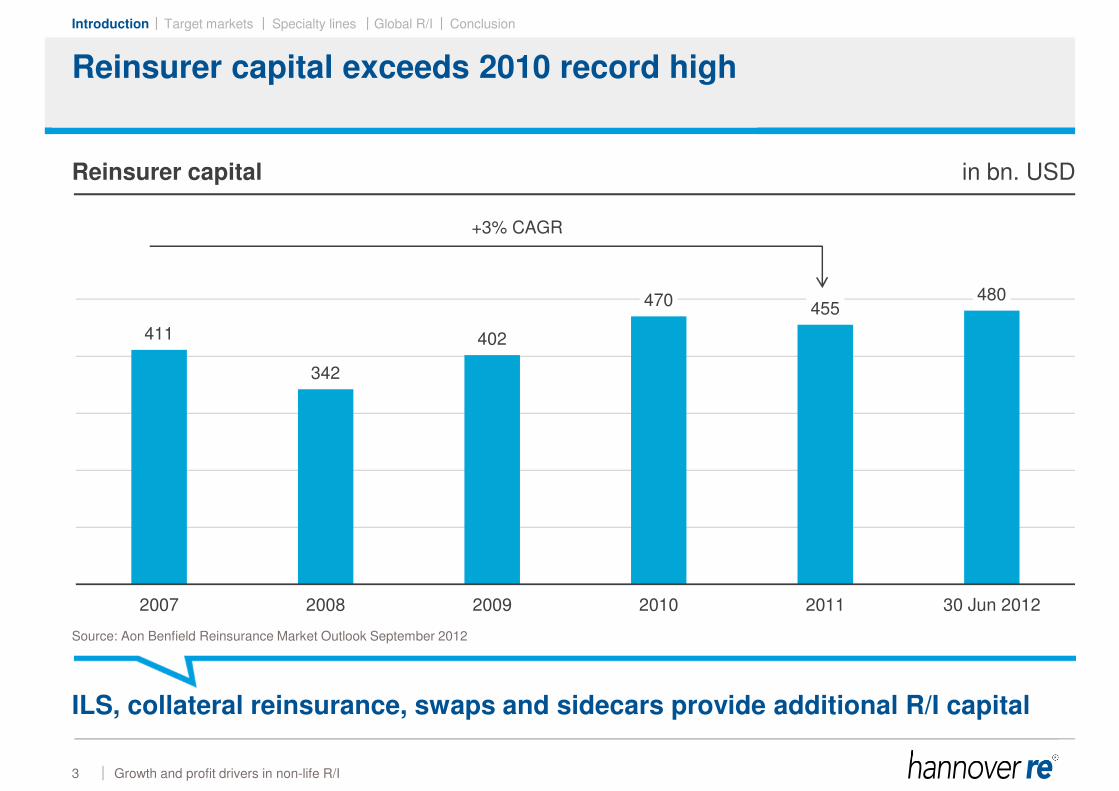

411

342

402

470455

480

2007 2008 2009 2010 2011 30 Jun 2012

Reinsurer capital exceeds 2010 record high

Growth and profit drivers in non-life R/I

Reinsurer capital in bn. USD

Source: Aon Benfield Reinsurance Market Outlook September 2012

ILS, collateral reinsurance, swaps and sidecars provide additional R/I capital

+3% CAGR

3

Introduction

Introduction Target markets Specialty lines Global R/I Conclusion

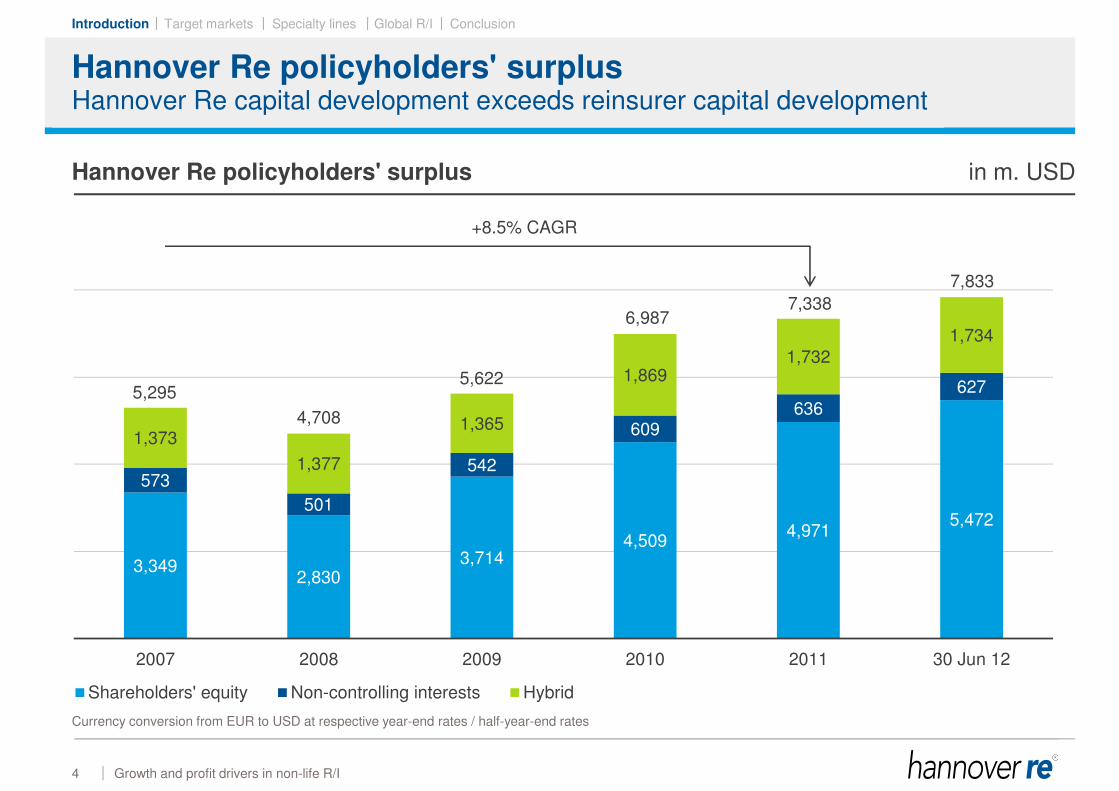

Hannover Re policyholders' surplus

Growth and profit drivers in non-life R/I

Hannover Re policyholders' surplus in m. USD

Hannover Re capital development exceeds reinsurer capital development

Inforce premium as at 1 January ≠ U/Y perspective!

12

Target markets

Introduction Target markets Specialty lines Global R/I Conclusion

North America Business

� The US non-life insurance market seems to be slowly hardening and will continue

to maintain this gradual momentum, barring the occurrence of any catastrophes

(we noticed a shift of business from the admitted to the surplus lines market)

� Although there is no firm hardening in the reinsurance market yet,

the reinsurance market is technically oriented and unwilling to compromise on

technical prices

� Selected, individual opportunities are presenting themselves offering the

chance to grow

Growth and profit drivers in non-life R/I

The reinsurance perspective

Strong brand awareness and efficient CRM further important drivers of growth

13

Target markets

Introduction Target markets Specialty lines Global R/I Conclusion

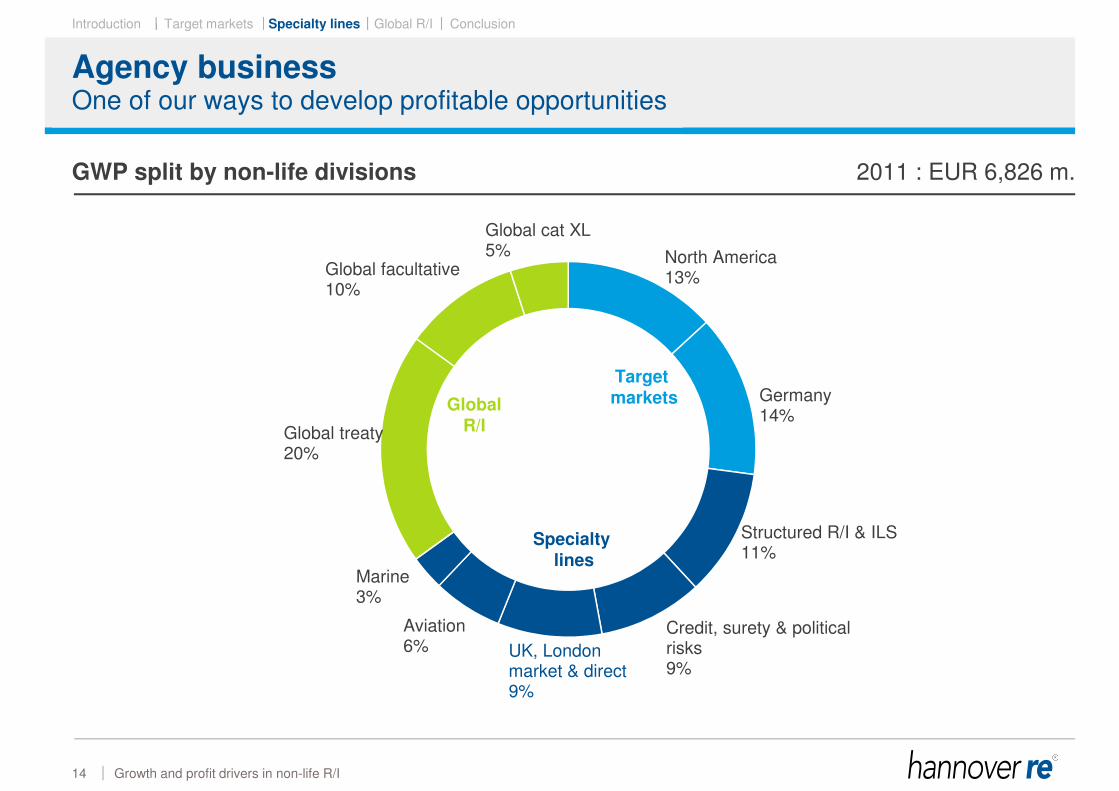

Agency business

North America13%

Germany14%

Structured R/I & ILS11%

Credit, surety & political risks9%

UK, London market & direct9%

Aviation6%

Marine3%

Global treaty20%

Global facultative10%

Global cat XL5%

Target markets

Specialty lines

Global R/I

Growth and profit drivers in non-life R/I

GWP split by non-life divisions 2011 : EUR 6,826 m.

One of our ways to develop profitable opportunities

14

Specialty lines

Introduction Target markets Specialty lines Global R/I Conclusion

Agency business

� Based on our strategy we underwrite direct insurance in selected markets in

addition to our core reinsurance business

� Emphasis lies on underwriting profitable business which we cannot access as

reinsurer

� On the one hand this refers to large risks that are underwritten on a co-insurance

basis similar to our facultative reinsurance business. By using our primary

insurance companies we can be independent of the proportion of facultative risks

our reinsurance customers are willing to cede

� On the other hand we conduct business via agents. In general, this would be

niche business such as mining or medical liability

� Especially in our non-life segment we expect our direct insurance business to

grow faster than our core reinsurance business

Growth and profit drivers in non-life R/I

Gaining access to profitable niche business

15

Specialty lines

Introduction Target markets Specialty lines Global R/I Conclusion

Agency business

� In general, we select partners who can conduct the main tasks of the direct

insurance administration themselves i.e. issuing policies, claims handling or sales

� Partners are direct insurance companies or in the case of co-insurance,

agents or brokers

� We underwrite exclusively to retain the business net within the Hannover Re

group (contrary to fee-income-model)

Growth and profit drivers in non-life R/I

Characteristics of our direct insurance activities

16

Specialty lines

Introduction Target markets Specialty lines Global R/I Conclusion

Agency business

Growth and profit drivers in non-life R/I

Gross written premium* FY in m. EUR

Gross written premium development

135

163

280

431

484

2007 2008 2009 2010 2011

* Agency business of Hannover Re's primary carriers

17

Specialty lines

Introduction Target markets Specialty lines Global R/I Conclusion

Agency Business

� Inter Hannover is mandated to enable Hannover Re to access selected direct

markets with the business sustainable only via direct insurance licenses

� Especially in agency business, a trustful business-relationship between agents

and Inter Hannover is emphasized to ensure alignment of interest

� Partners are existing agencies as well as start-ups and insurance companies that

are in transition to an MGA

� Mainly niche business is written

� Providing an access to large single risk business – particularly London market

� 2012 strategy updated to maintain growth and profitability

� Further development of lineslip and binder business

� Improving access to specialty lines

Growth and profit drivers in non-life R/I

Inter Hannover: actively driving profitable growth

18

Specialty lines

Introduction Target markets Specialty lines Global R/I Conclusion

Facultative business, agricultural business and ReTakaful

Growth and profit drivers in non-life R/I

GWP split by non-life divisions 2011: EUR 6,826 m.

Examples from our global reinsurance division

19

North America13%

Germany14%

Structured R/I & ILS11%

Credit, surety & political risks9%

UK, London market & direct9%

Aviation6%

Marine3%

Global treaty20%

Global facultative10%

Global cat XL5%

Target markets

Specialty lines

Global R/I

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

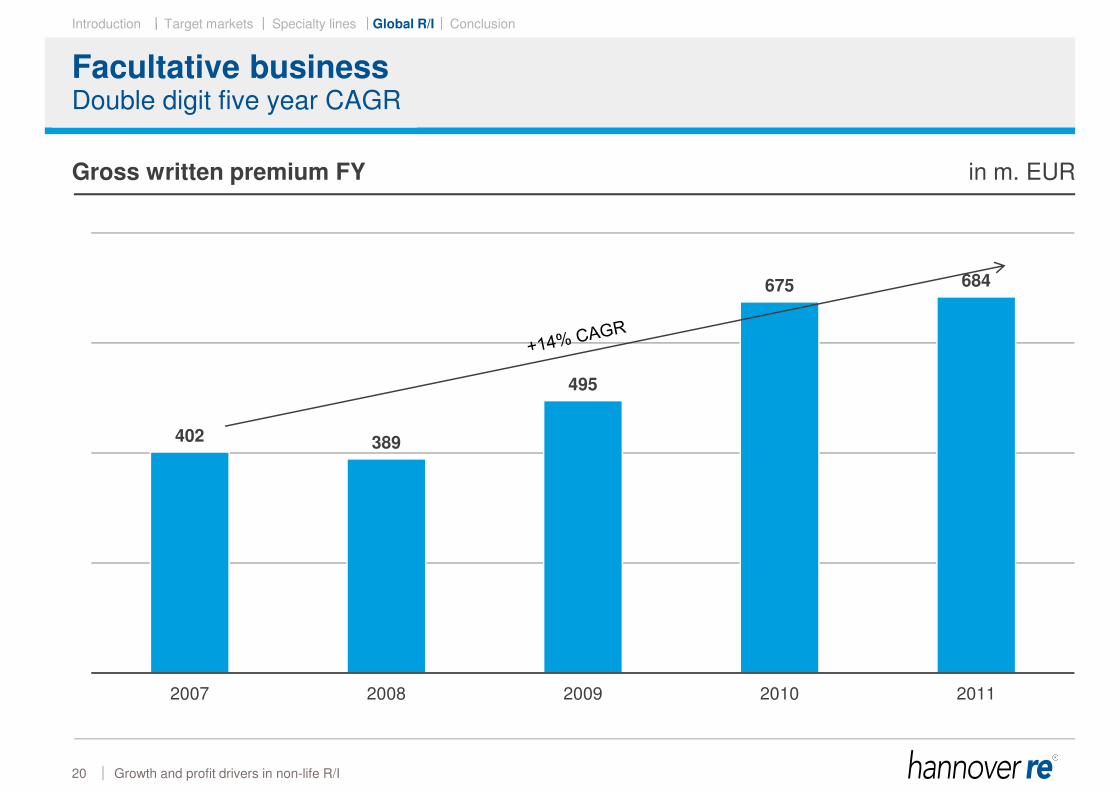

Facultative business

Growth and profit drivers in non-life R/I

Gross written premium FY in m. EUR

Double digit five year CAGR

402 389

495

675 684

2007 2008 2009 2010 2011

20

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Facultative business

Growth and profit drivers in non-life R/I

Facultative split by lob Facultative split by region

Well diversified by line of business and region

2011 gross written premium: EUR 683 m.

21

Liability36%

Fire Property34%

Marine10%

Engineering8%

Motor7%

Personal Accident3%

Other fin. losses 2%

Other Property0%

United Kingdom32%

Europe(ex UK)21%

North America19%

Australasia12%

Others16%

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Facultative business

� CAGR of 14% over the past 5 years

� Positive technical results of EUR 52 m. on average in the last ten years

� Low costs with max. 7.5 % on gross premium

• (ca. 5% during hard market and ca. 10% during soft market, market average between

12% and 15%)

� Further growth for 2013 expected in the low double digit percentage range

� 120 experienced underwriters worldwide and 6 centres of competence – i.e. one

of the leaders in IDI (inherent defect insurance) and one of the leaders in sports &

entertainment reinsurance

� Organic growth is taking place in Asia / CIS and for engineering single risk

business in Europe

Growth and profit drivers in non-life R/I

Global expert knowledge ensures sustainable competitive advantage

Special expertise & presence worldwide i.e. leading R/I for the mining industry

22

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Agricultural business

Market premium development FY in bn. RMB � Agricultural insurance under

public private partnership

� Constantly growing market

� Hannover Re market share is

currently below average

� Our market share will be

increased by

• development of new products

• provision of high quality service to

Hannover Re customers

� AIR MPCI model launched for

China which will drive

awareness for NatCat risks

throughout the agricultural

insurance market

Growth and profit drivers in non-life R/I

Increasing our share in the growing market in China

5,3

11,1

13,4 13,6

17,4

0,41,3

2,0 2,02,6

2007 2008 2009 2010 2011

Premium R/I premiumSources:

Introduction to Agricultural Insurance in China, April 2012, Aon Benfield;China Statistical Yearbook 2007 – 2011; China Insurance Regulatory Commission

23

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Agricultural business

Growth and profit drivers in non-life R/I

Turkey market premium FY in m. TL

Over-proportional growth due to high market presence

0

100

200

300

400

500

2007 2008 2009 2010 2011

Brazil market premium FY in m. BRL

Our agricultural insurance market share in these countries is significant

Sources: Turkish Agriculture Insurance Pool (TARSIM); Ses-Susep, www.susep.gov.br

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011

Premium RI Premium

24

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Hannover ReTakaful

� In Islamic jurisprudence, Sharia has certain points that oppose the deployment of

conventional insurance

� Several cultural and religious barriers were lifted with the introduction of a Sharia-

compliant alternative: takaful and by extension: retakaful

� Key takaful markets: Middle East and South East Asia (specifically Malaysia,

Indonesia and Brunei). Relatively young population at the beginning of work lives

with increased awareness of risk and the benefits of insurance

� Saudi Arabia is key Sharia-compliant market (a third of world takaful volumes)

Between 2011 and 2014 it is planned to spend about USD 400 bn., the largest

proportion of which on infrastructure development

� The Arab Spring brought more Islamic-leaning cabinets in Tunisia and Egypt. This

change is likely to enable further promotion and development of Islamic finance

Growth and profit drivers in non-life R/I

Low insurance penetration and demographic factors are fuelling growth

25

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

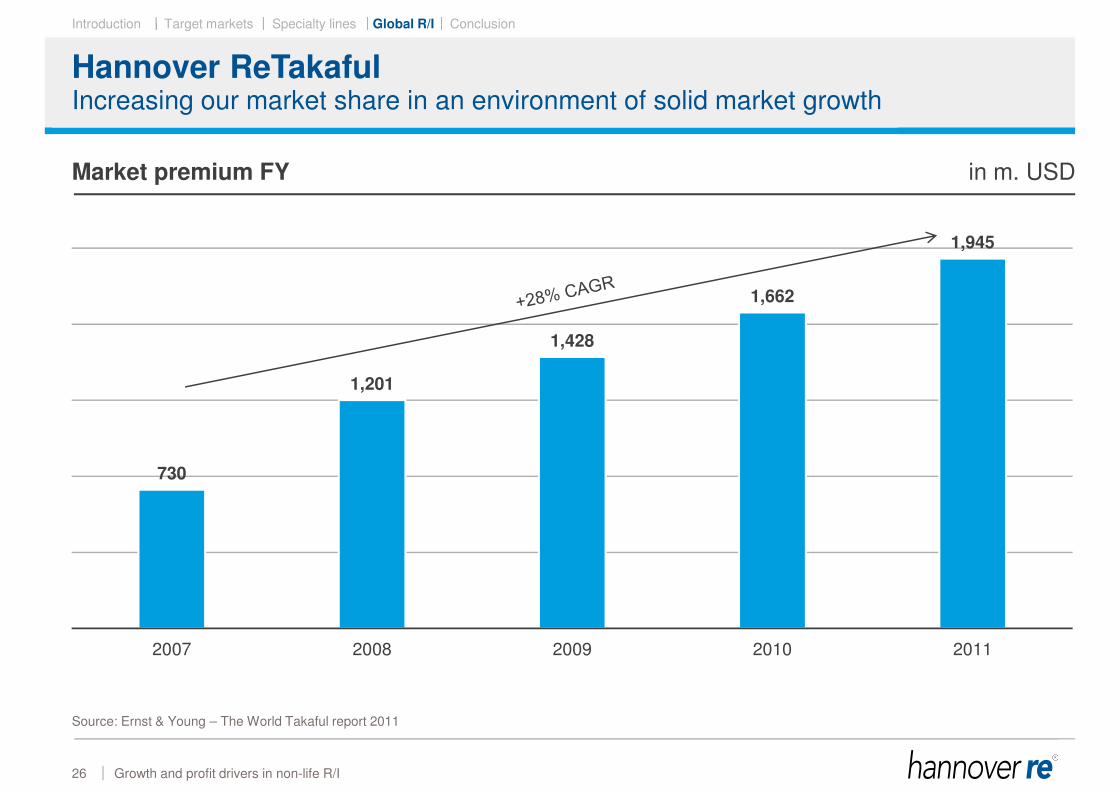

Hannover ReTakaful

Growth and profit drivers in non-life R/I

Market premium FY in m. USD

Increasing our market share in an environment of solid market growth

730

1,201

1,428

1,662

1,945

2007 2008 2009 2010 2011

Source: Ernst & Young – The World Takaful report 2011

26

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Hannover ReTakaful

� During August 2009, the Sharia supervisory board of Hannover ReTakaful gave

its approval to the pooling system of Hannover ReTakaful

� Hannover ReTakaful maintains four separate sub-pools namely Proportional

Treaty, Non-proportional Treaty, Facultative and Family/Health Retakaful

� Hannover ReTakaful charges certain level of wakalah fee for managing and a

mudarabaha fee for investing the retakaful pools assets. These fees are agreed

with the Sharia advisory board at regular intervals

� Surplus of the pools may be distributed to participants of retakaful pools, after

consideration of previous deficits (if any) and all appropriate provisions and

reserves

� Investment return is credited to the pools for invested assets

� Hannover ReTakaful will support the pool financially through Qard Hassan

(interest free loan), should the combined pool result in a deficit

Growth and profit drivers in non-life R/I

Pooling: a unique business model

27

Global R/I

Introduction Target markets Specialty lines Global R/I Conclusion

Conclusion

� Hannover Re has continuously grown above market average as a result of

selective underwriting

� Hannover Re is strategically very well positioned, particularly with regard to

• Maintaining substantial expert knowledge for facultative underwriting

• Opportunities arising out of emerging markets (CRM approach)

• Utilising a unique franchise model in the Sharia-compliant market

Growth and profit drivers in non-life R/I

Strategically well positioned to meet a dynamic market environment

28

Conclusion

Introduction Target markets Specialty lines Global R/I Conclusion

Conclusion (cont'd)

29

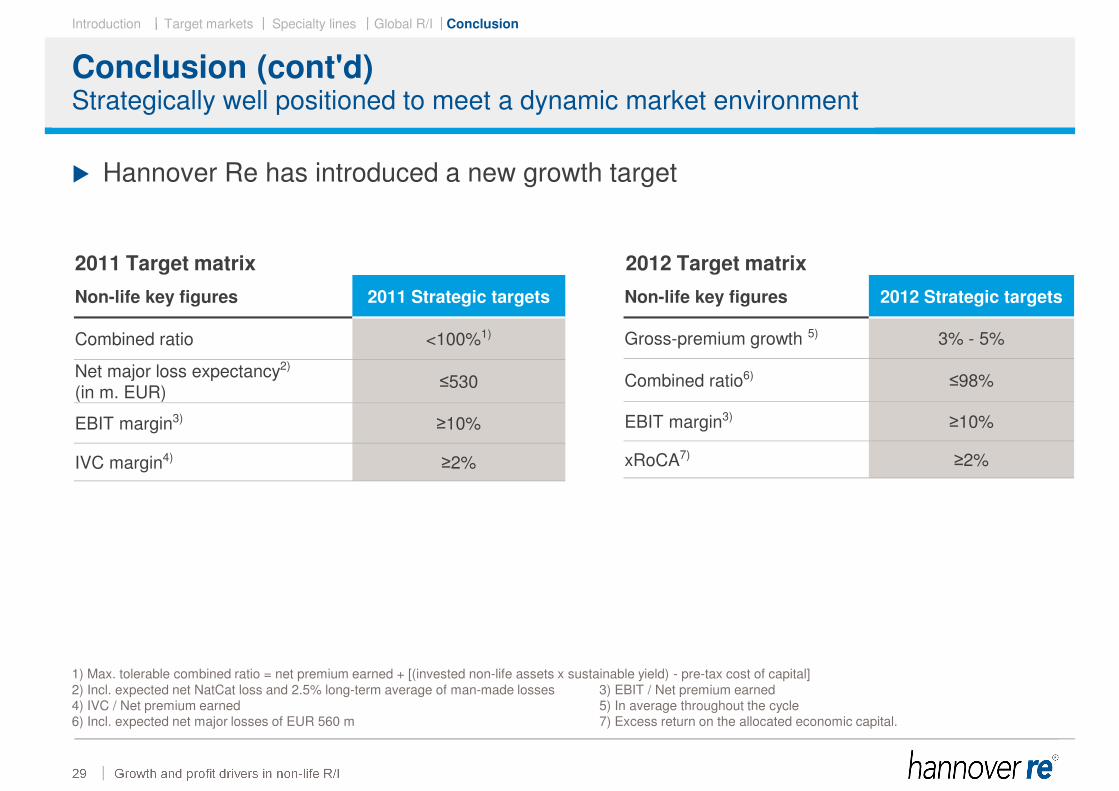

� Hannover Re has introduced a new growth target

Growth and profit drivers in non-life R/I

Strategically well positioned to meet a dynamic market environment

Non-life key figures 2011 Strategic targets

Combined ratio <100%1)

Net major loss expectancy2)

(in m. EUR)≤530

EBIT margin3)≥10%

IVC margin4)≥2%

Non-life key figures 2012 Strategic targets

Gross-premium growth 5) 3% - 5%

Combined ratio6)≤98%

EBIT margin3)≥10%

xRoCA7)≥2%

2011 Target matrix 2012 Target matrix

1) Max. tolerable combined ratio = net premium earned + [(invested non-life assets x sustainable yield) - pre-tax cost of capital]

2) Incl. expected net NatCat loss and 2.5% long-term average of man-made losses 3) EBIT / Net premium earned4) IVC / Net premium earned 5) In average throughout the cycle6) Incl. expected net major losses of EUR 560 m 7) Excess return on the allocated economic capital.

Conclusion

Introduction Target markets Specialty lines Global R/I Conclusion

Disclaimer

This presentation does not address the investment objectives or financial situation of any particular person or

legal entity. Investors should seek independent professional advice and perform their own analysis regarding

the appropriateness of investing in any of our securities.

While Hannover Re has endeavoured to include in this presentation information it believes to be reliable,

complete and up-to-date, the company does not make any representation or warranty, express or implied,

as to the accuracy, completeness or updated status of such information.

Some of the statements in this presentation may be forward-looking statements or statements of future

expectations based on currently available information. Such statements naturally are subject to risks and

uncertainties. Factors such as the development of general economic conditions, future market conditions,

unusual catastrophic loss events, changes in the capital markets and other circumstances may cause the

actual events or results to be materially different from those anticipated by such statements.

This presentation serves information purposes only and does not constitute or form part of an offer

or solicitation to acquire, subscribe to or dispose of, any of the securities of Hannover Re.