Page 1

1

Growth OK

Cautious consumers

Michael Workman

Senior Economist

Commonwealth Bank of Australia - (612) 9118 1019

[email protected]

Not For Profit Conference

Adelaide

October 2012

www.research.commbank.com.au

Page 2

2

Important Information

This advice has been prepared without considering your objectives, financial situation or needs, and

before acting on the advice, you should consider its appropriateness to your circumstances.

Commonwealth Bank of Australia (“CBA”) as a provider of investment, borrowing and other financial

services undertakes financial transactions with many corporate entities in Australia. This may include any

corporate issuer referred to in this report.

For US and US investors: If you would like to speak to someone regarding the subject securities

described in this report, please contact Commonwealth Australia Securities LLC (the “US Broker-Dealer”),

a broker-dealer registered under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”) and a

member of the Financial Industry Regulatory Authority (“FINRA”) at 1 (212) 336-7737. This report was

prepared, approved and published by Global Markets Research, a division of Commonwealth Bank of

Australia ABN 48 123 123 124 AFSL 234945("the Bank") and distributed in the U.S. by the US Broker-

Dealer. The Bank is not registered as a broker-dealer under the Exchange Act and is not a member of

FINRA or any U.S. self-regulatory organization. Commonwealth Australia Securities LLC (“US Broker-

Dealer”) is a wholly owned, but non-guaranteed, subsidiary of the Bank, organized under the laws of the

State of Delaware, USA, with limited liability.

Please see further disclaimers at the back of this document. Please also view our website at

www.research.commbank.com.au for a more detailed disclaimer.

Page 3

3

Agenda

Australian growth outlook:

– NFP – income sources & risks

– Growth drivers

– Employment & population

– Consumer spending & leakages.

Interest rates & Housing

– Prices & lending.

Currencies:

– USD to stay weak, AUD above parity.

Page 4

4

CBA TEI & THE CASH RATE

3.8

4.4

5.1

5.7

6.4

7.0

Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

-8

-5

-2

2

5

8

Cash

rate

(lhs)

CBA TEI*

(adv 9 mnths ,rhs)

%pa %pa

* Deviat ion from trend

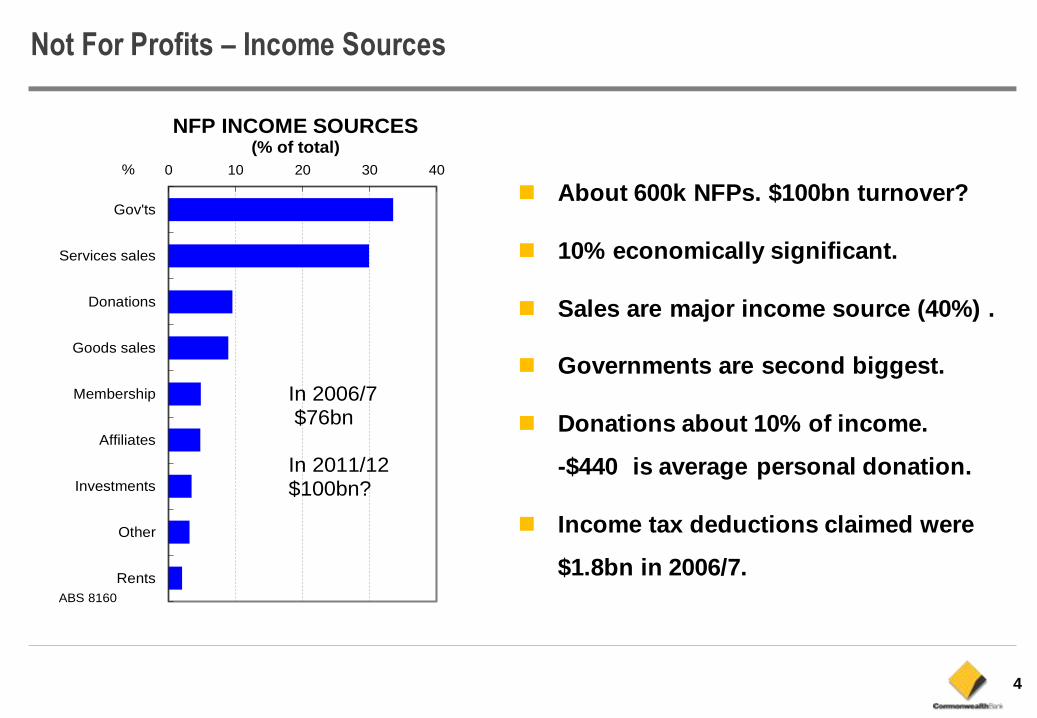

Not For Profits – Income Sources

About 600k NFPs. $100bn turnover?

10% economically significant.

Sales are major income source (40%) .

Governments are second biggest.

Donations about 10% of income.

-$440 is average personal donation.

Income tax deductions claimed were

$1.8bn in 2006/7.

0 10 20 30 40

Gov'ts

Services sales

Donations

Goods sales

Membership

Affiliates

Investments

Other

Rents

NFP INCOME SOURCES(% of total)

%

In 2006/7$76bn

In 2011/12$100bn?

ABS 8160

Page 5

5

CBA TEI & THE CASH RATE

3.8

4.4

5.1

5.7

6.4

7.0

Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

-8

-5

-2

2

5

8

Cash

rate

(lhs)

CBA TEI*

(adv 9 mnths ,rhs)

%pa %pa

* Deviat ion from trend

Not For Profits – Shares of Incomes by Sector

Education and research groups

receive largest (22%) share of

income.

Services receive a rising share of

consumer incomes.

0 5 10 15 20 25

Ed'n & Res

Cult & Rec

Social Serv

Environ. et al.

Other

Health

Hospitals

Bus. & Unions

Religion

SHARES OF INCOME BY SECTOR(% of total) %

In 2006/7$76bn

In 2011/12$100bn?

ABS 8160

Page 6

6

CBA TEI & THE CASH RATE

3.8

4.4

5.1

5.7

6.4

7.0

Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

-8

-5

-2

2

5

8

Cash

rate

(lhs)

CBA TEI*

(adv 9 mnths ,rhs)

%pa %pa

* Deviat ion from trend

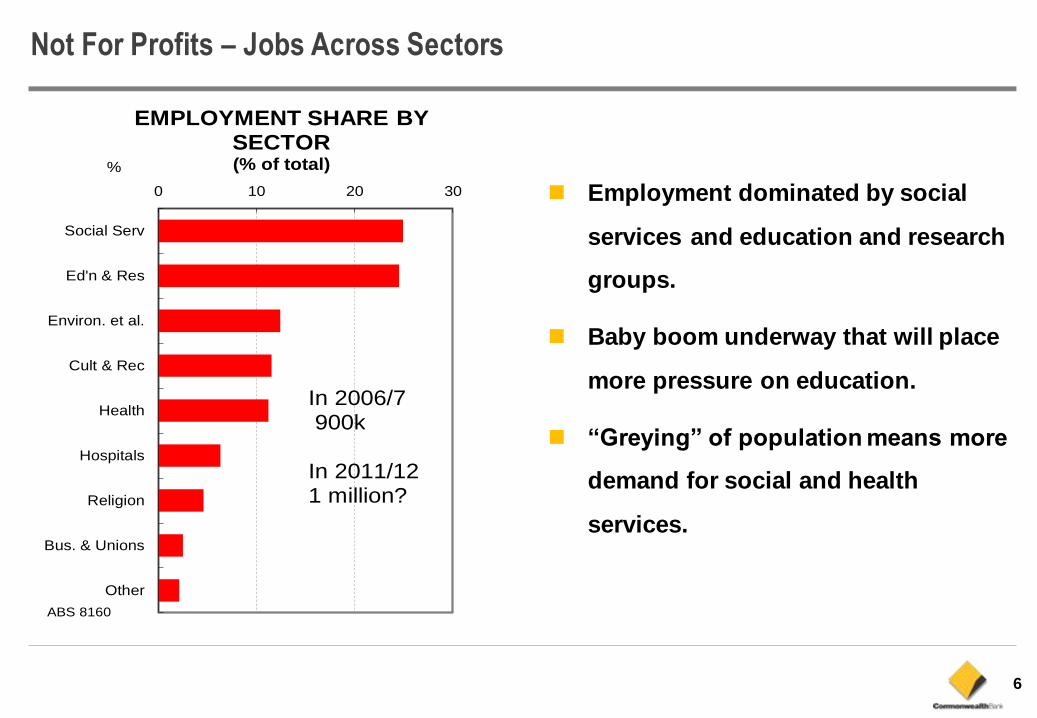

Not For Profits – Jobs Across Sectors

Employment dominated by social

services and education and research

groups.

Baby boom underway that will place

more pressure on education.

“Greying” of population means more

demand for social and health

services.

0 10 20 30

Social Serv

Ed'n & Res

Environ. et al.

Cult & Rec

Health

Hospitals

Religion

Bus. & Unions

Other

EMPLOYMENT SHARE BY SECTOR(% of total) %

In 2006/7900k

In 2011/121 million?

ABS 8160

Page 7

7

Asian protection

CBA TEI & THE CASH RATE

3.8

4.4

5.1

5.7

6.4

7.0

Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

-8

-5

-2

2

5

8

Cash

rate

(lhs)

CBA TEI*

(adv 9 mnths ,rhs)

%pa %pa

* Deviat ion from trend

Australia & The Global Economy

Australia’s GDP growth highly correlated to China’s growth.

-9

-6

-3

0

3

6

9

12

-9

-6

-3

0

3

6

9

12

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

REAL GDP(annual % chg)%pa

Australia

US

%pa

China

UKEU

Japan

GFC

Page 8

8

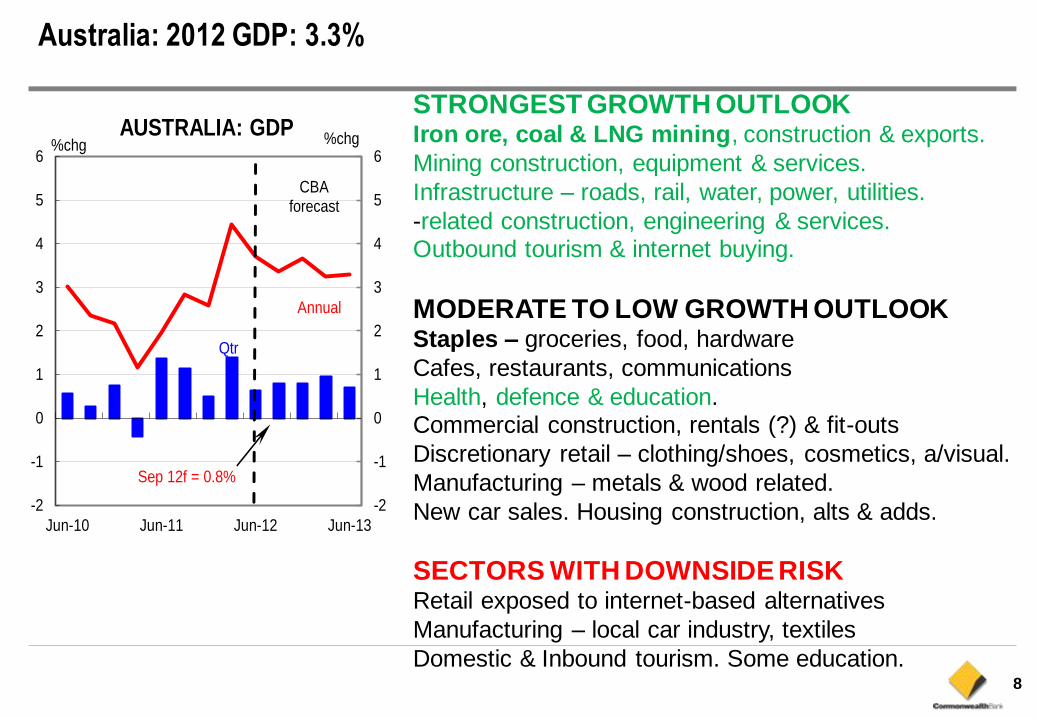

Australia: 2012 GDP: 3.3%

STRONGEST GROWTH OUTLOOK Iron ore, coal & LNG mining, construction & exports.

Mining construction, equipment & services.

Infrastructure – roads, rail, water, power, utilities.

-related construction, engineering & services. Outbound tourism & internet buying.

MODERATE TO LOW GROWTH OUTLOOK Staples – groceries, food, hardware

Cafes, restaurants, communications

Health, defence & education. Commercial construction, rentals (?) & fit-outs

Discretionary retail – clothing/shoes, cosmetics, a/visual.

Manufacturing – metals & wood related.

New car sales. Housing construction, alts & adds.

SECTORS WITH DOWNSIDE RISK Retail exposed to internet-based alternatives

Manufacturing – local car industry, textiles

Domestic & Inbound tourism. Some education.

-2

-1

0

1

2

3

4

5

6

-2

-1

0

1

2

3

4

5

6

Jun-10 Jun-11 Jun-12 Jun-13

AUSTRALIA: GDP

Annual

Qtr

%chg

Sep 12f = 0.8%

CBAforecast

%chg

Page 9

9

Growth: Mining v Rest

Consensus has trend GDP growth

over next few years and resources

accounting for ½-⅔ of that growth.

Implications:

– mining-related economy to expand at

≈16%pa over next two years;

– non-mining economy to grow at just 1½%pa if overall economy to be kept

within the “speed limits”;

– high AUD to keep driving structural change;

– AUD exposed sectors like tourism,

education, manufacturing, and

retailing to keep underperforming.

100

115

130

145

100

115

130

145

2010/11 2011/12 2012/13

ECONOMIC ACTIVITY(2010/11 = 100) Index

Source: RBA , CBA

MiningGDP

GDP

Non-miningGDP

Index

The “patchwork” economy

Page 10

10

Inflation at 1.2%....below 3% in 2012/13.

CPI running at 1.2%pa & underlying measures at 2.0%pa.

CPI has 58% goods and 42% services.

“AUD effected” inflation at -2.0%pa. Local (mainly services) inflation at 3.4%pa.

-2

0

2

4

6

-2

0

2

4

6

Mar-06 Mar-08 Mar-10 Mar-12

INFLATION(annual % change) %

AUD influenced prices

Local services

%

1

2

3

4

5

1

2

3

4

5

Mar-04 Mar-06 Mar-08 Mar-10 Mar-12

INFLATION(annual % change)% %

RBA target

Underlyinginflation

Headlineinflation

Page 11

11

Wages growth near 3.7%pa.

Business surveys suggest slower wages growth coming as unemployment rate rises.

Wages: Up 3.7%pa.

0.0 1.4 2.8 4.1 5.5

Mining

Mfg

Utilities

Construct.

Wholesale

Retail

Accom. etc

Transp

Communic.

Fin & insur

Rent & Hiring

Prof Serv.

Admin Serv.

Gov't

Education

Health

Cult & rec

Pers & other

WAGE PRICE INDEX(% annual growth)

Total = 3.7%

2

3

4

5

2

3

4

5

Sep-98 Dec-01 Mar-05 Jun-08 Sep-11

AUSTRALIAN WAGES(annual % change)

% %

Public

Total

Private

Page 12

12

Jobs: slowing………..unemployment rate to rise, except in WA.

Jobs growth expected to slow to 10k/mth, mainly in Victoria & NSW.

National unemployment rate likely to rise to 6 5.6% in late 2012.

3000

3250

3500

3750

7500

7750

8000

8250

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

EMPLOYMENT'000

Full-time(lhs)

Part-time(rhs)

'000

-50

0

50

100

150

3.8

4.4

4.9

5.5

6.0

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

LABOUR MARKET

Employmentgrowth(rhs)

Unemployment rate (lhs)

% '000

Page 13

13

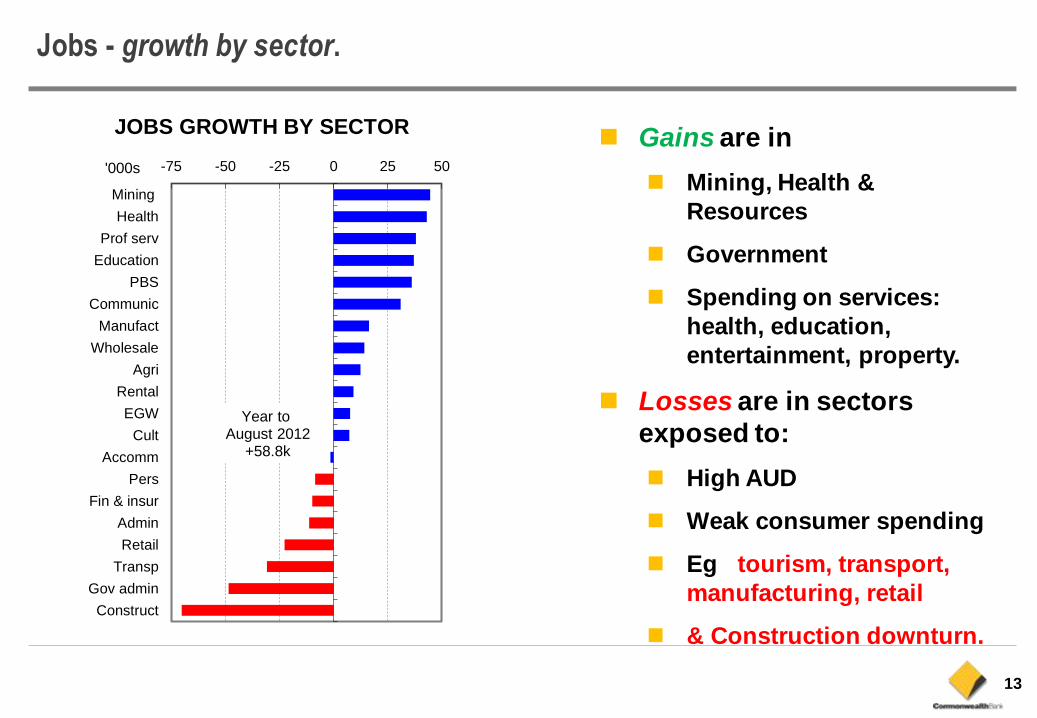

Jobs - growth by sector.

Gains are in

Mining, Health &

Resources

Government

Spending on services:

health, education,

entertainment, property.

Losses are in sectors

exposed to:

High AUD

Weak consumer spending

Eg tourism, transport,

manufacturing, retail

& Construction downturn.

-75 -50 -25 0 25 50

Mining

Health

Prof serv

Education

PBS

Communic

Manufact

Wholesale

Agri

Rental

EGW

Cult

Accomm

Pers

Fin & insur

Admin

Retail

Transp

Gov admin

Construct

JOBS GROWTH BY SECTOR

Year to August 2012

+58.8k

'000s

Page 14

14

Population: National 1.4%.......WA 3.0%.

National population growth at 331k (1.4%pa) gives underlying housing demand of 170k.

WA’s population growth strong at 3.1%pa. Boosted by interstate & overseas migration.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jun-00 Jun-02 Jun-04 Jun-06 Jun-08 Jun-10 Jun-12

POPULATION GROWTH(annual % change)

Tas

QldWA

SA

%pa

NSW

Vic

%pa

ABS3101

0

50

100

150

200

250

300

350

400

450

Dec-97 Dec-00 Dec-03 Dec-06 Dec-09

POPULATION GROWTH

Nat Increase

Net Overseas

Moving annual total

'000s

ABS

Page 15

15

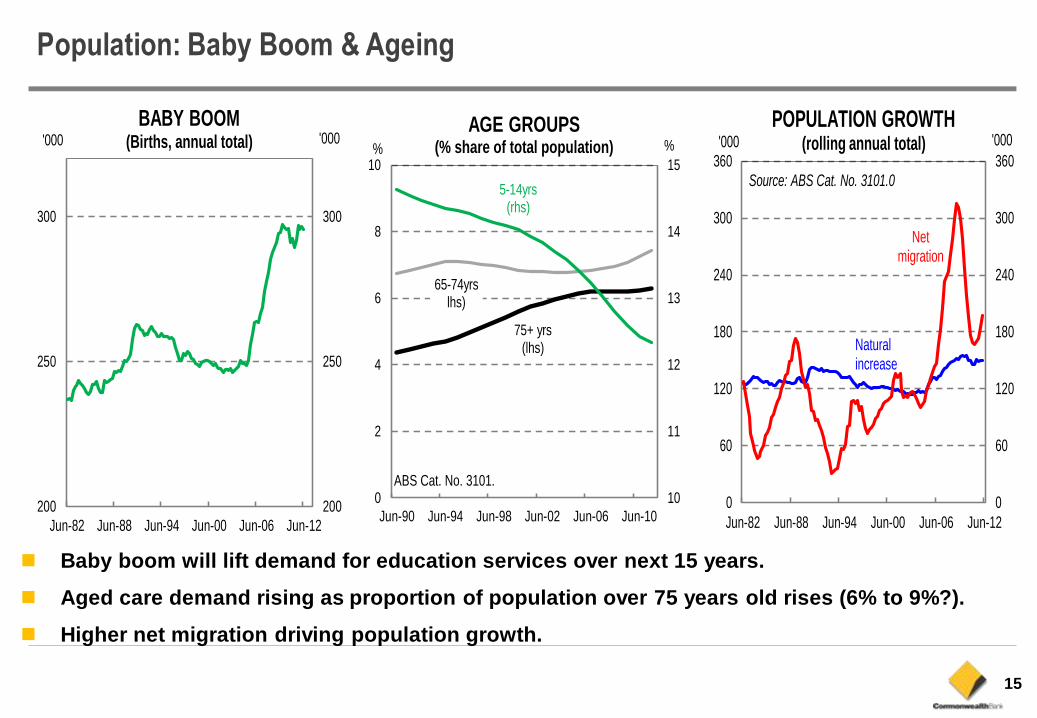

Population: Baby Boom & Ageing

Baby boom will lift demand for education services over next 15 years.

Aged care demand rising as proportion of population over 75 years old rises (6% to 9%?).

Higher net migration driving population growth.

200

250

300

200

250

300

Jun-82 Jun-88 Jun-94 Jun-00 Jun-06 Jun-12

'000 '000BABY BOOM

(Births, annual total)

0

60

120

180

240

300

360

0

60

120

180

240

300

360

Jun-82 Jun-88 Jun-94 Jun-00 Jun-06 Jun-12

'000 '000POPULATION GROWTH

(rolling annual total)

Netmigration

Naturalincrease

Source: ABS Cat. No. 3101.0

10

11

12

13

14

15

0

2

4

6

8

10

Jun-90 Jun-94 Jun-98 Jun-02 Jun-06 Jun-10

% %

AGE GROUPS(% share of total population)

75+ yrs(lhs)

65-74yrslhs)

5-14yrs(rhs)

ABS Cat. No. 3101.

Page 16

16

Consumers: Cautious About Spending

Ability to spend is OK

– Household incomes rising by 5%......with wages up 3.5% and jobs up 1.5%.

– BUT…..Wealth position: house prices and shares are weak.

– Strong growth in services, internet-based retail, & overseas travel.

Willingness is in doubt

– Consumer or retail caution prevails.

– Households still saving more.

– Bad news more often than goods. Especially on Europe and jobs.

– Government handed out $2.8bn in May & June, plus tax cuts.

Spending leakages were also important

– Power costs, health and rents up.

– Mortgage rates lower. Petrol flat. Olympics are good…. or bad for retail?

– More overseas travel, less inbound tourism. Both mean less local retail.

– Higher AUD means falling imported goods prices.

Page 17

17

Confidence: Not Happy, Jan.

Consumer confidence weak……are more rate cuts required?

Business confidence also poor. Big business worse than small business.

Are we in Athens yet?

-30

-15

0

15

30

Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

-30

-15

0

15

30

CONFIDENCE & CONDITIONS(smoothed)Index Index

Source: NAB

Businessconditions Business

confidence

60

100

140

60

100

140

Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12

CONSUMER SENTIMENT

Source: Melbourne Institute

Index Index

Time to buy a dwelling

Personal Finances

12mo ahead

Consumersentiment

Page 18

18

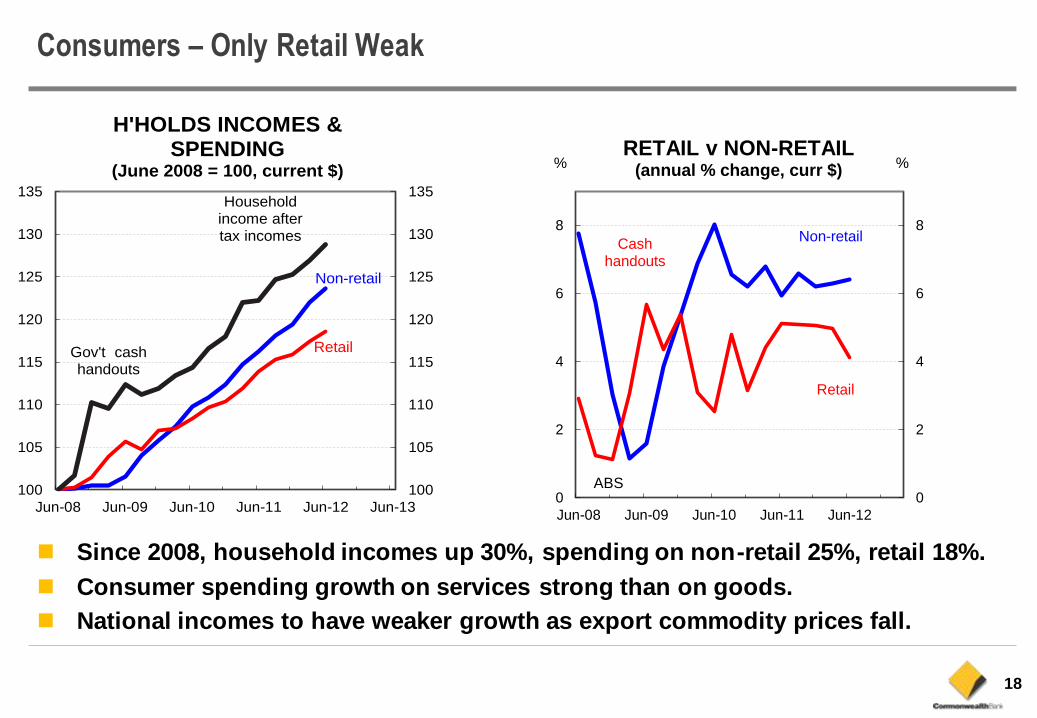

Consumers – Only Retail Weak

Since 2008, household incomes up 30%, spending on non-retail 25%, retail 18%.

Consumer spending growth on services strong than on goods.

National incomes to have weaker growth as export commodity prices fall.

100

105

110

115

120

125

130

135

100

105

110

115

120

125

130

135

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13

H'HOLDS INCOMES & SPENDING

(June 2008 = 100, current $)

Retail

Non-retail

Household income after tax incomes

Gov't cash handouts

0

2

4

6

8

0

2

4

6

8

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

RETAIL v NON-RETAIL(annual % change, curr $)

Retail

Non-retail

% %

Cash handouts

ABS

Page 19

19

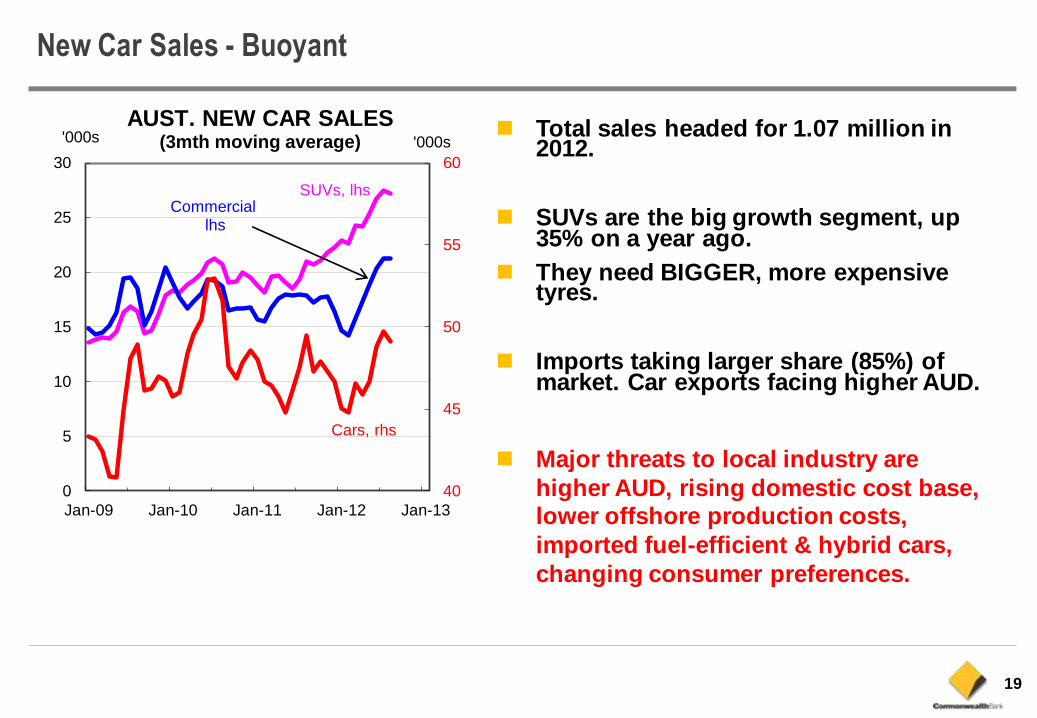

New Car Sales - Buoyant

Total sales headed for 1.07 million in 2012.

SUVs are the big growth segment, up 35% on a year ago.

They need BIGGER, more expensive tyres.

Imports taking larger share (85%) of market. Car exports facing higher AUD.

Major threats to local industry are

higher AUD, rising domestic cost base, lower offshore production costs,

imported fuel-efficient & hybrid cars,

changing consumer preferences.

40

45

50

55

60

0

5

10

15

20

25

30

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

AUST. NEW CAR SALES(3mth moving average)

Cars, rhs

Commerciallhs

SUVs, lhs

'000s '000s

Page 20

20

Overseas departures were 691k in June, up 8%pa. 40% above arrivals.

Higher charges in some areas are reducing discretionary spending ability.

Utility (electricity, gas & water) prices are 50% higher over the past 5 years.

More travel, higher bills.

Consumer Caution – leakages?

0.0

2.5

5.0

7.5

1.5

2.0

2.5

3.0

Mar-81 Mar-87 Mar-93 Mar-99 Mar-05 Mar-11

UTILITIES SPEND($bn & % of after tax income)% $bn/qtr

Spending as % ofafter tax income,,lhs

Spending,rhs

0

4

8

12

16

0

4

8

12

16

Sep-02 Sep-04 Sep-06 Sep-08 Sep-10 Sep-12

% %

Utilities

Purchase, rates &

maintenance

RENTS, UTILITIES & RATES(annual % change)

Rents

0.6

0.7

0.8

0.9

1

1.1

450

500

550

600

650

700

Jan-09 Jan-10 Jan-11 Jan-12

AUD/USD & TOURISM'000s AUD/USD

Departures, lhs

AUD/USD, rhs

Arrivals, lhs

Page 21

21

Credit card usage rising slowly…..debit cards as well.

Higher cash deposits shows precautionary savings rising firmly.

Saving ratio at 10%, highest since 1980s.

Consumer Caution – deposits to $700bn, up 8% pa.

-5

0

5

10

15

20

-5

0

5

10

15

20

Sep-72 Sep-80 Sep-88 Sep-96 Sep-04

SAVING RATIO% %

-3

0

3

6

9

12

-3

0

3

6

9

12

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

CREDIT CARD ACTIVITY(%pa smthd)

Balances

Avge balanceper card

Total Accounts

source RBA

400

500

600

700

800

2500

3000

3500

4000

4500

Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

HOUSEHOLD ASSETS

Dwellings,lhs

Deposits, rhs

$bn $bn

RBA

Page 22

22

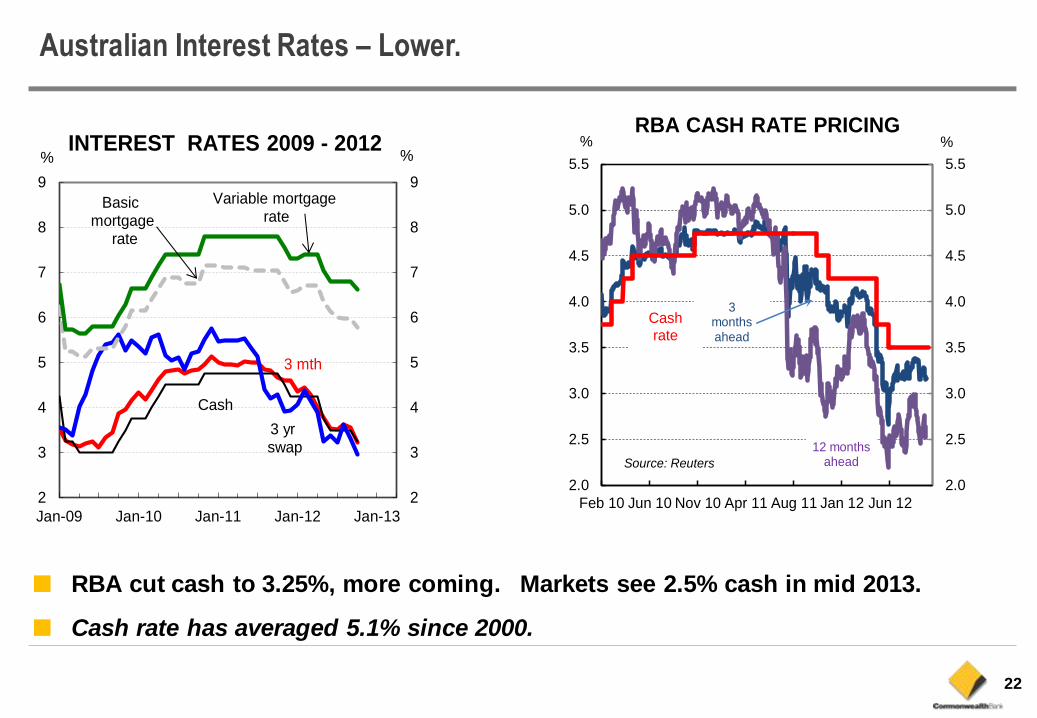

Australian Interest Rates – Lower.

■ RBA cut cash to 3.25%, more coming. Markets see 2.5% cash in mid 2013.

■ Cash rate has averaged 5.1% since 2000.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Feb 10 Jun 10 Nov 10 Apr 11 Aug 11 Jan 12 Jun 12

%

3 months ahead

12 monthsaheadSource: Reuters

RBA CASH RATE PRICING%

Cashrate

2

3

4

5

6

7

8

9

2

3

4

5

6

7

8

9

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

INTEREST RATES 2009 - 2012

Cash

3 mth

Variable mortgagerate

% %

3 yrswap

Basic mortgage

rate

Page 23

23

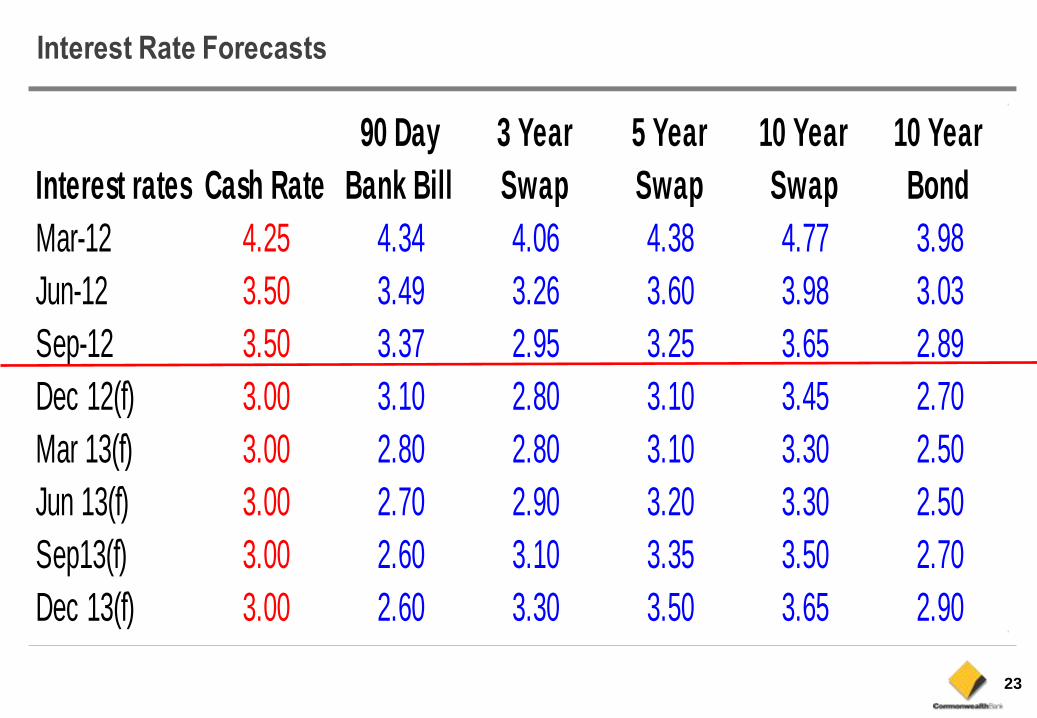

Interest Rate Forecasts

Interest rates Cash Rate

90 Day

Bank Bill

3 Year

Swap

5 Year

Swap

10 Year

Swap

10 Year

Bond

Mar-12 4.25 4.34 4.06 4.38 4.77 3.98

Jun-12 3.50 3.49 3.26 3.60 3.98 3.03

Sep-12 3.50 3.37 2.95 3.25 3.65 2.89

Dec 12(f) 3.00 3.10 2.80 3.10 3.45 2.70

Mar 13(f) 3.00 2.80 2.80 3.10 3.30 2.50

Jun 13(f) 3.00 2.70 2.90 3.20 3.30 2.50

Sep13(f) 3.00 2.60 3.10 3.35 3.50 2.70

Dec 13(f) 3.00 2.60 3.30 3.50 3.65 2.90

Page 24

24

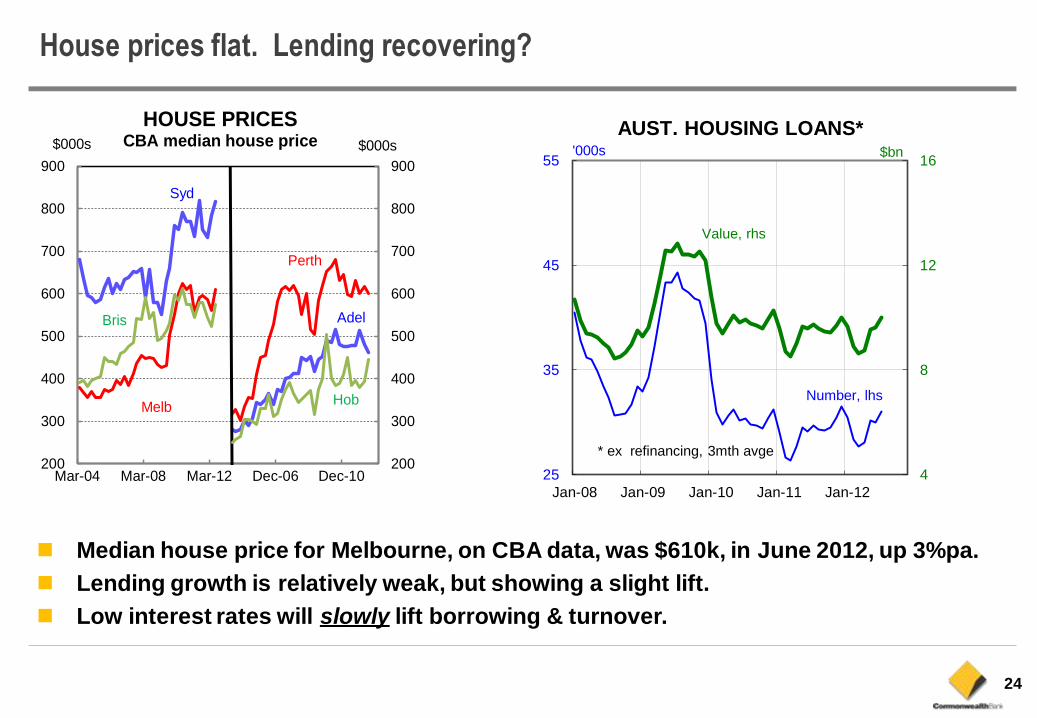

House prices flat. Lending recovering?

Median house price for Melbourne, on CBA data, was $610k, in June 2012, up 3%pa.

Lending growth is relatively weak, but showing a slight lift.

Low interest rates will slowly lift borrowing & turnover.

200

300

400

500

600

700

800

900

200

300

400

500

600

700

800

900

Mar-04 Mar-08 Mar-12 Dec-06 Dec-10

HOUSE PRICESCBA median house price

Syd

Adel

Melb

Bris

Perth

Hob

$000s $000s

4

8

12

16

25

35

45

55

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

AUST. HOUSING LOANS*$bn'000s

Number, lhs

* ex refinancing, 3mth avge

Value, rhs

Page 25

25

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

Jan-84 Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

USD USD

The AUD cycles 1983 - 2012

AUD floats 12 Dec83 at USD0.9090

5 March 1983:

Labor Party wins election.

8 March 1983:

AUD devalued

10% to USD 0.8549

6-8 February 1985:

MX Missile Crisis

14 May 1986

Keating “Banana

Republic”

comment on radio

Commodity prices

at record lows

28 July 1986:

Keating changes

foreign investment

rules and RBA raises

rediscount rate to 16%.

AUD hits record low of

USD 0.5712 during day

and closes at

USD0.6155

20 October 1987:

Stockmarket crash

in Australia

Rising interest

rates and

higher commodity

prices

14 February 1989:

Keating comments

talk down AUD

Kuwait

invaded by

Iraq Aug 90

19 December 1991:

Keating becomes

Prime Minister

August 1991:

Failed Russian

coup

26 February 1992:

One Nation

Statement

Interest rates cut

15 times from

Jan 1990 to Dec 1993,

from 18% to 4.75%

October 1993:

Metals prices reach

record lows. AUD low

of USD 0.6410

RBA lifts rates 3 times

from 4.75% to 7.5%,

from July to Dec 1994.

Commodity

prices rising

September 1986 :

First downgrade of Australian

sovereign debt rating

October 1989 :

Second downgrade of

Sovereign debt rating

AUD peaks at USD0.9653

on 16 March 1984

Strong USD & AUD

falls Oil

prices

spike in

Gulf War I

July 1998:

Metals prices reach

record lows. AUD low

of USD 0.5815

Interest rates cut

5 times from

July 1996 to July 1997,

from 7.5% to 5.0%

June 1997:

Asia crisis begins,

THB floats

Commodity prics

falling from June 97

IMF packages for Asia: Markets rally, Jan 98

Japan in recession:

JPY & AUD weaken

March 1996

Howard

Gov’t

elected

Federal election dates: 5 March

1983

1 Dec 1984

11 July 1987

24 March 1990

13 March 1993

16 March 1996

3 Oct 1998

10 Nov 2001

9 Oct 2004

24 Nov 2007

21 August 2010

Average Annual Trading Range AUD/USD, 1983 - 2011: 13USc

Russian debt crisis

Ruble devalued

Gold falls to USD273/oz

AUD low of USD0.5530

on 28 Aug ‘99.

LTCM on 23 Sept 98

Commoditie

s

recover

April 99

May 1999

S&P Upgrade

Y2K related

selling

Oct 99

RBA lifts

rates: Nov

1999,

Feb, April,

May &

August

2000

AUD falls to USD0.5075

as USD rises.

US stockmarkets fall.

Oil hits $37/bbl

AUD low of USD0.4775

on 2 April 2001

RBA cash rate changes

2 Mar 05 5.50

3 May 06 5.75

2 Aug 6.0

6 Nov 6.25

8 Aug 07 6 .50

7 Nov 6.75

5 Feb 08 7.0

5 Mar 7.25

3 Sep 08 7.0

8 Oct 6.0

5 Nov 5.25

3 Dec 4.25

4 Feb 09 3.25

8 Apr 3.0

7 Oct 09 3.25

4 Nov 3.5

2 Dec 3.75

3 Mar 10 4.0

7 Apr 10 4.25

3 May 10 4.5

3 Nov 10 4.75

1 Nov 11 4.50

6 Dec 11 4.25

2 May 12 3.75

6 June 12 3.50

RBA lifts

rates in May

& June ‘02

WTC 11 Sep 01

AUD dip,

0.4840

USD

weakens

as US

shares

fall

Oct ‘02

Moody’s upgrades

Australia to Aaa

Uridashis

lift AUD

March ‘03

S&P

upgrades

Australia

to AAA

Oil prices

spike until

Gulf War 2

ends 10

April 2003

S&P Sovereign Debt

Rating changes

AA+ 6 Dec 86

AA 24 Oct 89

AA+ 17 May 99

AAA 17 Feb 03

RBA lifts

rates 5 Nov ‘03

& 3 Dec.’ 03

Commodity

prices rising

12 December 1983:

AUD floats at

USD0.9090

9 Oct ‘04

Howard Gov’t

re-elected

Oil prices

hit $75/bbl

Aug 07

Mineral

commodity

prices at

50yr highs

AUD at 30 year

high of 1.108,

27 July 2011.

US sub-prime

Problems

Aug 07 on

USD weaker

Fed cuts rates

24 Nov 07

Rudd Gov’t

elected

Oil prices hit

$142/bbl

AUD collapses

as USD rises on

Sub-prime crisis

RBA cuts

rates

3 Sep 08, to

8 Apr 09

Commodity

prices

slump.

AUD low of

USD0.6010

on 27 Oct

08

Sep 08

Lehman Bros

collapse, US

Fed cuts to

zero, Dec 08.

USD falls as

Fed does

Quantitative

Easing, Mar 09

Commodities

& shares

recover

strongly

RBA lifts

rates

Oct 09 to Nov 10

World bond

markets sell-off on

US inflation fears

US & EU growth

data weakens,

USD up.

RBA cuts rates

on 1 Nov ,

6 Dec. 2011,

then May & Jun

‘12

Page 26

26

AUD Forecasts – peak in December?

Exchange ratesAUD/USD AUD/JPY AUD/EUR AUD/GBP AUD/NZD AUD/CHF

Mar-12 1.03 86 0.78 0.65 1.26 0.93

Jun-12 1.02 82 0.81 0.65 1.28 0.97

Sep-12 1.03 81 0.84 0.66 1.26 1.01

Dec 12(f) 1.05 83 0.84 0.66 1.27 1.01

Mar 13(f) 1.04 83 0.82 0.65 1.25 0.98

Jun 13(f) 1.04 84 0.80 0.64 1.24 0.96

Dec 13(f) 1.04 85 0.79 0.63 1.27 0.95

Dec 13(f) 1.04 86 0.79 0.63 1.27 0.95

Page 27

27

CBA TEI & THE CASH RATE

3.8

4.4

5.1

5.7

6.4

7.0

Jul-97 Jul-99 Jul-01 Jul-03 Jul-05

-8

-5

-2

2

5

8

Cash

rate

(lhs)

CBA TEI*

(adv 9 mnths ,rhs)

%pa %pa

* Deviat ion from trend

CBA Australian Economic Forecasts - October 2012 Fiscal Years Calendar Years

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2007 2008 2009 2010 2011 2012 2013

(a) (a) (a) (a) (f) (f) (a) (a) (a) (a) (a) (f) (f)

Economic Activity

Private final demand 0.1 1.0 3.3 6.8 5.3 4.6 6.9 3.0 -0.4 2.0 5.5 6.1 5.3

Of which: Household spending 0.1 2.5 3.1 3.7 3.3 3.3 5.6 1.9 1.0 2.9 3.3 4.0 3.1

Dwelling investment -1.5 1.2 3.0 -3.3 -0.2 4.8 2.0 2.7 -4.4 4.1 1.3 -5.1 4.9

Business investment 2.2 -5.2 6.1 22.1 13.0 8.1 14.9 9.4 -4.7 -1.5 17.1 16.9 12.2

Public final demand 3.7 6.6 3.1 0.7 0.4 0.2 3.4 6.8 0.7 8.7 0.1 1.9 -0.9

Domestic final demand 0.9 2.3 3.3 5.3 4.2 3.6 6.1 3.9 -0.2 3.5 4.2 5.1 3.9

Inventories (contrib to GDP) -0.7 -0.1 0.5 0.2 0.1 0.0 0.8 -0.3 -0.7 0.4 0.4 0.1 0.1

GNE 0.2 2.3 3.8 5.5 4.2 3.6 6.9 3.5 -0.9 3.9 4.6 5.2 4.0

Exports 1.7 5.3 0.4 3.7 5.0 5.2 3.2 3.8 2.1 5.9 -1.3 5.1 5.9

Imports -3.3 5.6 10.4 11.8 6.6 7.8 12.6 11.2 -8.6 14.1 11.5 7.8 7.7

Net exports (contrib to GDP) 1.0 -0.1 -2.0 -1.8 -0.6 -0.9 -1.6 -1.4 2.2 -1.5 -2.7 0.0 0.0

GDP 1.4 2.3 1.9 3.4 3.7 3.0 4.7 2.5 1.4 2.5 2.1 3.9 3.6

Prices & Wages

CPI 3.1 2.3 3.1 2.3 2.6 2.7 2.3 4.4 1.8 2.8 3.4 1.7 2.9

Underlying CPI 4.4 3.3 2.6 2.3 2.7 2.8 3.0 4.6 3.8 2.8 2.6 2.2 2.9

AWOTE 5.5 5.6 4.2 4.4 3.0 3.8 4.8 4.8 5.7 4.9 4.4 3.6 3.3

WPI 4.1 3.0 3.8 3.6 3.8 3.9 4.0 4.2 3.6 3.3 3.7 3.7 3.9

Real h/hold disposable income 7.4 1.0 3.8 3.5 2.7 3.0 7.7 4.2 5.9 1.0 4.4 3.0 2.7

Labour Market

Employment 1.6 1.4 2.9 0.7 1.1 1.8 3.1 2.8 0.7 2.7 1.7 0.7 1.5

Unemployment rate 4.9 5.5 5.1 5.2 5.5 5.3 4.4 4.3 5.6 5.2 5.1 5.3 5.5

External Accounts

Current Account: $bn -36.7 -56.1 -33.3 -40.8 -68.4 -77.8 -69.8 -54.2 -52.4 -38.8 -32.5 -57.7 -73.6

% of GDP -2.9 -4.3 -2.4 -2.8 -4.4 -4.8 -6.2 -4.4 -4.2 -2.9 -2.3 -3.9 -4.6

Page 28

28

All Investors: Unless otherwise noted, all data is sourced from Australian Bureau of Statistics material. (www.abs.gov.au) The Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945 (the “Bank”, is incorporated in Australia with limited liability. Commonwealth Securities Limited ABN 60 067 254 399 AFSL 238814 ("CommSec"), is a wholly owned, but non-guaranteed, subsidiary of the Bank and is incorporated in Australia with limited liability.

Please view our website at www.research.commbank.com.au for more information. The Bank and its subsidiaries, including CommSec, Commonwealth Australia Securities LLC, CBA Europe Ltd and Commonwealth Research, are domestic or foreign entities or business areas of the Commonwealth Bank Group of Companies

(CBGOC). CBGOC and their directors, employees and representatives are referred to in this Appendix as “the Group”. This report is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy any securities or financial instruments. This report has been prepared without taking account of the objectives, financial situation and capacity to bear loss, knowledge, experience or needs of any specific person who may receive this report. No member of the Group

does, or is required to, assess the appropriateness or suitability of the report for recipients who therefore do not benefit from any regulatory protections in this regard. All recipients should, before acting on the information in this report, consider the appropriateness and suitability of the information, having regard to their own objectives,

financial situation and needs, and, if necessary seek the appropriate professional, foreign exchange or financial advice regarding the content of this report. We believe that the information in this report is correct and any opinions, conclusions or recommendations are reasonably held or made, based on the information available at the time of its compilation, but no representation or warranty, either expressed or implied, is made or provided as to accuracy, reliability or completeness of any statement

made in this report. Any opinions, conclusions or recommendations set forth in this report are subject to change without notice and may differ or be contrary to the opinions, conclusions or recommendations expressed elsewhere by the Group. We are under no obligation to, and do not, update or keep current the information

contained in this report. The Group does not accept any liability for any loss or damage arising out of the use of all or any part of this report. Any valuations, projections and forecasts contained in this report are based on a number of assumptions and estimates and are subject to contingencies and uncertainties. Different assumptions and estimates could result in materially different results. The Group does not represent or warrant that any of these valuations, projections or forecasts, or any of the

underlying assumptions or estimates, will be met. Past performance is not a reliable indicator of future performance. The Group has provided, provides, or seeks to provide, investment banking, capital markets and/or other services, including financial services, to the companies described in the report and their associates. This report

is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject any entity within the Group to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to the Group. None of the

material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior written permission of the appropriate entity within the Group. In the case of certain products, the Bank or one of its related bodies corporate is or may be the only market maker. The Group, its

agents, associates and clients have or have had long or short positions in the securities or other financial instruments referred to herein, and may at any time make purchases and/or sales in such interests or securities as principal or agent, including selling to or buying from clients on a principal basis and may engage in transactions in a manner inconsistent with this report.

All investors – Analyst Certification: Each research analyst, primarily responsible for the content of this research report, in whole or in part, certifies that with respect

to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the report. The analyst(s) responsible for the preparation of this report may interact with trading desk personnel, sales personnel and other constituencies for

the purpose of gathering, synthesizing, and interpreting market information. Directors or employees of the Group may serve or may have served as officers or directors of the subject company of this report. The compensation of analysts who prepared this report is determined exclusively by research management and senior management

(not including investment banking). No inducement has been or will be received by the Group from the subject of this report or its associates to undertake the research or make the recommendations. The research staff responsible for this report receive a salary and a bonus that is dependent on a number of factors including their performance and the overall financial performance of the Group, including its profits derived from investment banking, sales and trading revenue.

Important Disclosures and Disclaimer