44

| Date post: | 16-Apr-2017 |

| Category: |

Automotive |

| Upload: | frost-sullivan |

| View: | 3,210 times |

| Download: | 0 times |

2

Today’s Presenter

Functional Expertise10+ years of global commercial vehicle technologies and markets expertise, which include particular focus on areas such as

- Global commercial vehicle industry growth opportunities, and market penetration and growth strategy development

- Advanced truck technologies- powertrain, chassis, safety, telematics and regulation compliance technologies

- Global research and consulting management, global business development and team-building, CXO level revenue and market share growth strategy development

Sandeep Kar, Global Vice President

Frost & Sullivan

Follow me on:

ca.linkedin.com/pub/sandeep-kar/1/942/958/en

Disclosure: Sandeep serves in the advisory board of Transfix and Vaahika, and board of South End Travels

3

2015 Key HighlightsGlobal MD-HD truck sales declined by 5 percent over 2014 on account of weak demand in China

1China Changed the Game, LATAM’s Rise Got Overshadowed by Brazil’s Weakness

China and LATAM dealt a 120 Thousand unit blow to overall global medium-heavy duty truck sales.

2

Low Oil Prices Both a Boon and Bane

Low and volatile oil prices had both a positive impact (driving sales in emerging markets such as India, enablingfleets in diverting opex towards capex, and improving margins in markets such as North America and Europe) anda negative impact (several economies such as Russia, Canada, South America experienced recessionarypressures).

3

Daimler Extended Dominance; Asian OEMs on the Rise

Daimler continues to dominate the global market through effective product and brand strategies across the world.Asian manufacturers started to gain traction as product focus slowly moved from low-cost to value trucks in theglobal market.

4

Initiative towards CO2/GHG Reduction

OEMs and engine suppliers activities for reaching fuel efficiency targets for Euro 7 and EPA 2018 centeredaround technologies such as powertrain-optimization, driveline-optimization, light weighting, down-speeding,downsizing, and aerodynamics.

5Mobile and Online Freight Brokering Revolution Gained Traction

2015 experienced rapid growth of mobile based freight brokering (aka Uber for Trucks) in markets such as NorthAmerica and Brazil, while online freight aggregation gained traction in markets such as India and Europe.

4

Note: Data collected from 2014-2015 interviews and discussions with Sr. Managers to CEO-level executives of truck OEMs and tier-1 suppliers in North America, Europe, Asia-Pacific, China, India, Latin America, and other regions

Source: Frost & Sullivan.

CV Outlook 2016: Senior Management Top-of-Mind Issues, Global, 2015-2016

2015–2016 CV Industry Senior Management Top-of-Mind IssuesDespite a weak global economic outlook and fuel price volatility, proliferation of electronics-enabled service-oriented business models will propel the global MD-HD truck market towards new and lucrative revenue streams.

5

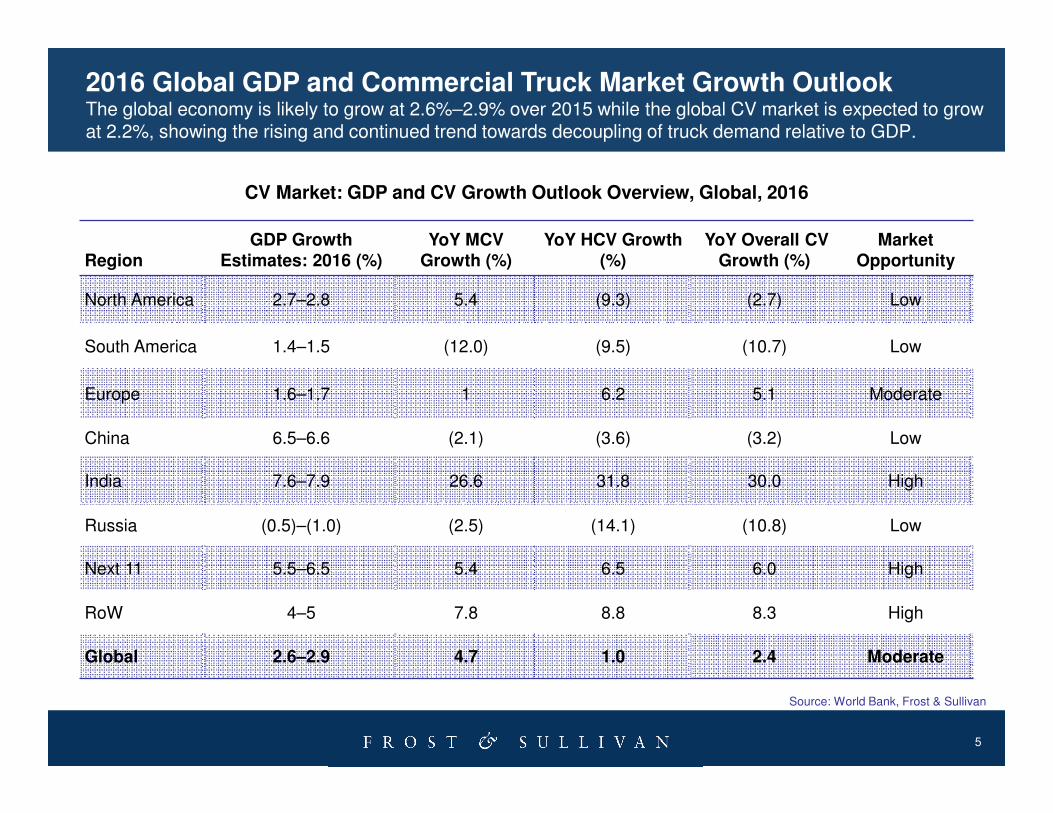

Source: World Bank, Frost & Sullivan

RegionGDP Growth

Estimates: 2016 (%)YoY MCV

Growth (%)YoY HCV Growth

(%)YoY Overall CV

Growth (%)Market

Opportunity

North America 2.7–2.8 5.4 (9.3) (2.7) Low

South America 1.4–1.5 (12.0) (9.5) (10.7) Low

Europe 1.6–1.7 1 6.2 5.1 Moderate

China 6.5–6.6 (2.1) (3.6) (3.2) Low

India 7.6–7.9 26.6 31.8 30.0 High

Russia (0.5)–(1.0) (2.5) (14.1) (10.8) Low

Next 11 5.5–6.5 5.4 6.5 6.0 High

RoW 4–5 7.8 8.8 8.3 High

Global 2.6–2.9 4.7 1.0 2.4 Moderate

CV Market: GDP and CV Growth Outlook Overview, Global, 2016

2016 Global GDP and Commercial Truck Market Growth OutlookThe global economy is likely to grow at 2.6%–2.9% over 2015 while the global CV market is expected to grow at 2.2%, showing the rising and continued trend towards decoupling of truck demand relative to GDP.

6

CV Market: Medium and Heavy Trucks-Unit Shipment, Global, 2015 and 2016

2.4% YoY Growth

2016 Regional Shares2.62 million 2.68 million

48%

48%

27%

52%

41%

22%

51%

55%

38%37%

63%

52%

52%81%

73%59%

78%49%

45%

62%

Next 11 includes the following countries: Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, the Philippines, Turkey, South Korea, Vietnam, and Bangladesh.

Un

its

MCV: 6T to 16THCV: 16T and above

19%

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

Global Medium and Heavy Truck Market Forecast 2016The global MD-HD truck market will absorb 60,000 additional units in 2016; MCV’s share will increase marginally by 1% on account of slumping demand in HD-heavy markets of China and North America.

7

GVWR (kilogram)

Pri

ce

($

)

CV Outlook 2016: Highest-selling Weight Segment in Each Region, Global, 2015 and 2016

Bubble size: Sales units of the top segments in each region

Bubble with map: Data points for 2016

Bubble shadow: Data points for 2015

Attractive MD-HD Truck Segments by RegionSlowdown in HD demand in China and North America and rise in value truck and MD Truck demand will push weighted average global GVWR to 22-23 MT; $40-65 thousand will emerge as the most active price bandwidth

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

8

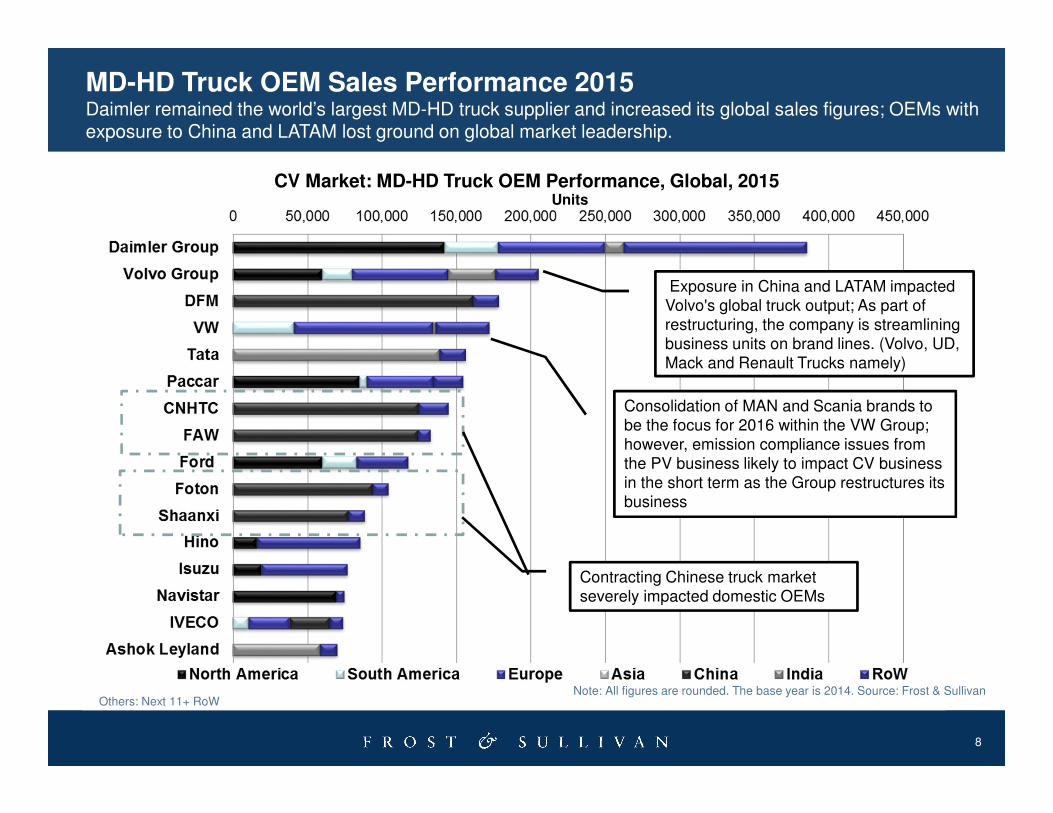

CV Market: MD-HD Truck OEM Performance, Global, 2015

Others: Next 11+ RoW

Units

Exposure in China and LATAM impacted Volvo's global truck output; As part of restructuring, the company is streamlining business units on brand lines. (Volvo, UD, Mack and Renault Trucks namely)

Contracting Chinese truck market severely impacted domestic OEMs

Consolidation of MAN and Scania brands to be the focus for 2016 within the VW Group; however, emission compliance issues from the PV business likely to impact CV business in the short term as the Group restructures its business

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

MD-HD Truck OEM Sales Performance 2015Daimler remained the world’s largest MD-HD truck supplier and increased its global sales figures; OEMs with exposure to China and LATAM lost ground on global market leadership.

9

Key 2016 Market Introductions—Truck Platforms, Powertrain LaunchesGlobal OEMs to focus more on soft technology upgrades that target mid-market (value truck) than new product launches

VO

LV

O

Gro

up

Ind

ia FMX 520 dump truck

FMX 480 dump truck

PA

CC

AR

No

rth

Am

eri

ca

Kenworth & Peterbilt trucks with MX-11 engine

DA

F

Eu

rop

e

New LF series distribution trucks

Tata

M

oto

rs

Ind

ia

Signa range of value Trucks

Isu

zu

No

rth

A

meri

ca

New NPR Diesel MD trucks

Fo

rd

No

rth

A

meri

ca

F 650-750 Class 6 & 7 Trucks

Daim

ler

No

rth

A

meri

ca

/Eu

rop

e

Mercedes-Benz Econic

dual control trucks

AP

AC

/Th

e M

idd

le E

ast/

Afr

ica

Fuso super low roof canter

New Actros

Arocs super heavy duty trucks

Unimog U4000 and U5000

Freigthliner Coronado with Cummins ISX e5

MA

N

AP

AC

TGX-D38

Navis

tar

No

rth

A

meri

ca

Premium vocational trucks C

um

min

s/

Westp

ort

No

rth

Am

eri

ca ISL G Near Zero (NZ)

NOx Natural gas engines

Westport ISB6.7 G, medium duty Natural Gas (NG) engine

Image Source: Company Brochures. Source: Frost & Sullivan

10

CV Market: Powertrain Technology Split by Region, Global, 2016

Po

we

rtra

in S

pli

t (%

)

Next 11 includes the following countries: Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, the Philippines, Turkey, South Korea, Vietnam, and Bangladesh. Source: Frost & Sullivan

Global MD-HD Truck Powertrain Technology ForecastChina and NA will show greater preference for alternative fuel powertrain systems; despite strong head winds, NG penetration will reach 4.8%.

11

Engine Platform Design Harmonization 2016-2022Emission compliance above Euro 4 standards, displacement range of 9 to 11.5L, power rating of 280-420 HP and price range of $7,000-14,000 emerging as ideal specifications for truly global platforms for 2016-2022 period

Price ($)Power Range (HP)Displacement (L)Emission Norms

Strong Trend Towards 2022 Moderate Trend Towards 2022

CV Market: HD Truck Engine Platform Requirements, Global, 2016–2022

Best Fit Latin America China India North America Europe Africa

200

100

300

4.0

2.0

8.0

6.0

12.0

10.0

400

600

500

Euro II

Euro I

Euro IV

Euro III

Euro VI

Euro V

14.0

10,000

5,000

15,000

20,000

30,000

25,000

Source: Frost & Sullivan

12

Product Segments Outlook-2016Mid-market value truck segment to gain 2 percent segment share in 2016; Despite Challenging Market Environment, China to Account for 40 Percent of Global Value Truck Market

17%

36%

47%

35%

19%

46%

CV Market: Unit Shipment by Product Segment, Global, 2015 and 2016

~2.61 Million

~2.68 Million

Value Truck Sales, Global, 2016

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

13

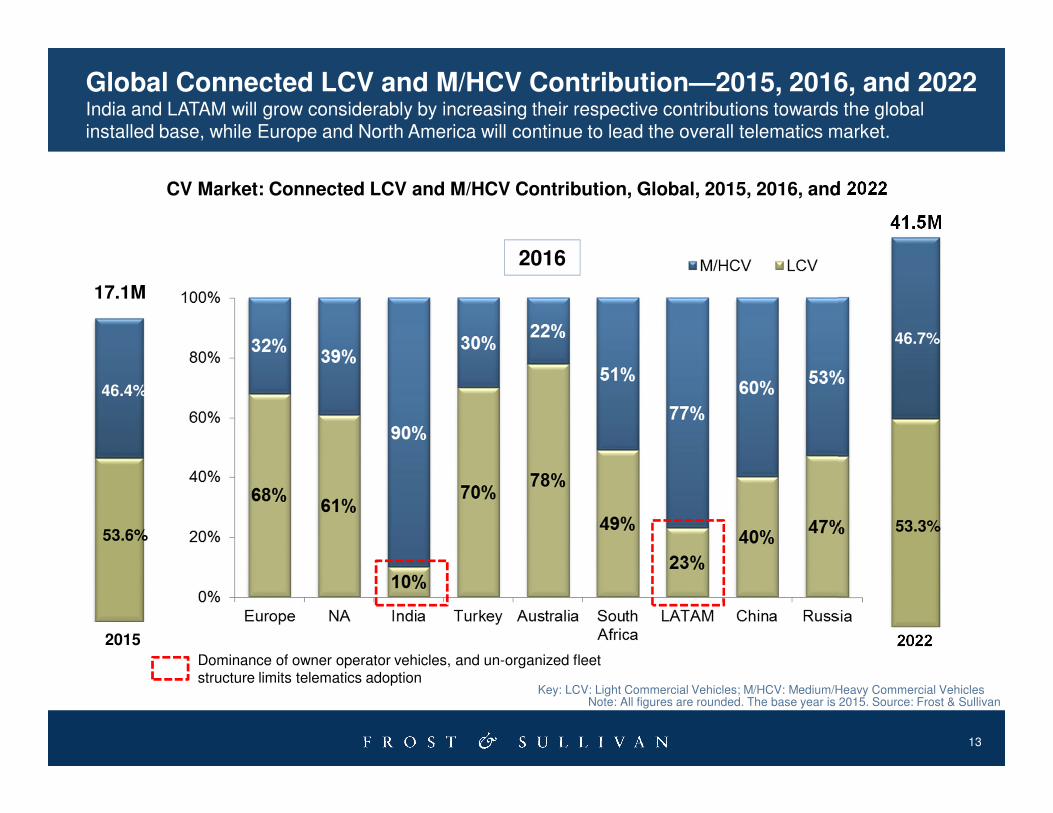

CV Market: Connected LCV and M/HCV Contribution, Global, 2015, 2016, and 2022

Key: LCV: Light Commercial Vehicles; M/HCV: Medium/Heavy Commercial Vehicles

2015 2022

53.6%

46.4%

2016

17.1M

41.5M

Dominance of owner operator vehicles, and un-organized fleet structure limits telematics adoption

53.3%

46.7%

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

Global Connected LCV and M/HCV Contribution—2015, 2016, and 2022India and LATAM will grow considerably by increasing their respective contributions towards the global installed base, while Europe and North America will continue to lead the overall telematics market.

14

Driver

Mgt.

Fuel

Mgt.

Vehicle

Management

Order

Management

Warranty

Optimization Prognostic & Repair

Management

Driver

Behaviour and Training

Advanced Driver

Assistance System

Integration

Usage based

Insurance

Automated Driving

/ Platooning

Transport

Management - TMS

ENVIRONMENTSAFETY

ACCESSIBLE AFFORDABLE

Re

ve

nu

e

Ge

ne

rati

on

Pro

fit

Ge

ne

rato

r

Evolving Service OpportunityBusiness model of connected truck is like an “Iceberg”; most important revenue generators are not yet seen

$3.5 Billion Today

15

2016 Top 6 PredictionsAs sales increases by 60 thousand units in 2016, the industry will increasingly focus towards offering cost-effective business ready solutions for fleet industry

1Global Sales to Hit 2.68 Million as the World Economy Grows in the Range of 2.6-2.9%

Growth from India, Europe and RoW (rest of world) markets to increase global truck out put by 2.4 percent.China to contract marginally by 3.2 percent to reach 750K units in 2016, a 300K drop from 2014 peak.

2OEMs Now Concentrating on Both Truck and Powertrain Platforms

By 2022, more than ½ of the global heavy duty truck engine production slated to feature platform basedlineage.

3Fuel Price Volatility to Impact Green Technologies In the Short-term

Short term headwinds from the fuel market to impact adoption of advanced powertrain technologies such asNatural Gas and Hybrid-Electric. Global natural gas adoption to reach 4.8 percent in 2016.

4Telematics Solutions to Become Top Differentiation Strategy

Developed markets will draw attention towards advanced services such as driver behavior management, videosafety and prognostics, while emerging regions will experience a shift from basic to mid-tier services.

5Global Truck Manufacturers and Suppliers Shifting Focus from Products to Services

Rise in interest and adoption of technologies such as telematics, safety, video based monitoring, prognostics,asset maintenance, platooning, online freight aggregation, mobile based brokering, etc

6Low-Cost and Premium Trucks to Lose Market Share to Value Trucks

After gaining market share for over 8 years, low-cost and premium trucks will cede 2 percent market share tovalue trucks (mid-market trucks that are higher priced than low-cost trucks but lower than premium trucks)

Source: Frost & Sullivan.

NORTH AMERICAN COMMERCIAL VEHICLE HEAVY TRUCK OUTLOOK

Frost & Sullivan Live

Webcast

March 24, 2016

Eric StarksPresidentChairman & CEO

888.988.1699 [email protected]@EricMStarks

www.FTRintel.com

17

WHY DO YOU BUY A TRUCK?

1818

U.S. TRUCK FREIGHT LEVELS ARE EASING BACK ON GROWTH

Sources: FTR, ATA - Copyright 2015

19

CLASS 8 ORDER ACTIVITY

Source: FTR Truck and Trailer Outlook Service

2020

N.A. CLASS 8 ORDERS HAVE CLEARLY WEAKENED

Source: FTR, Copyright 2016

2121

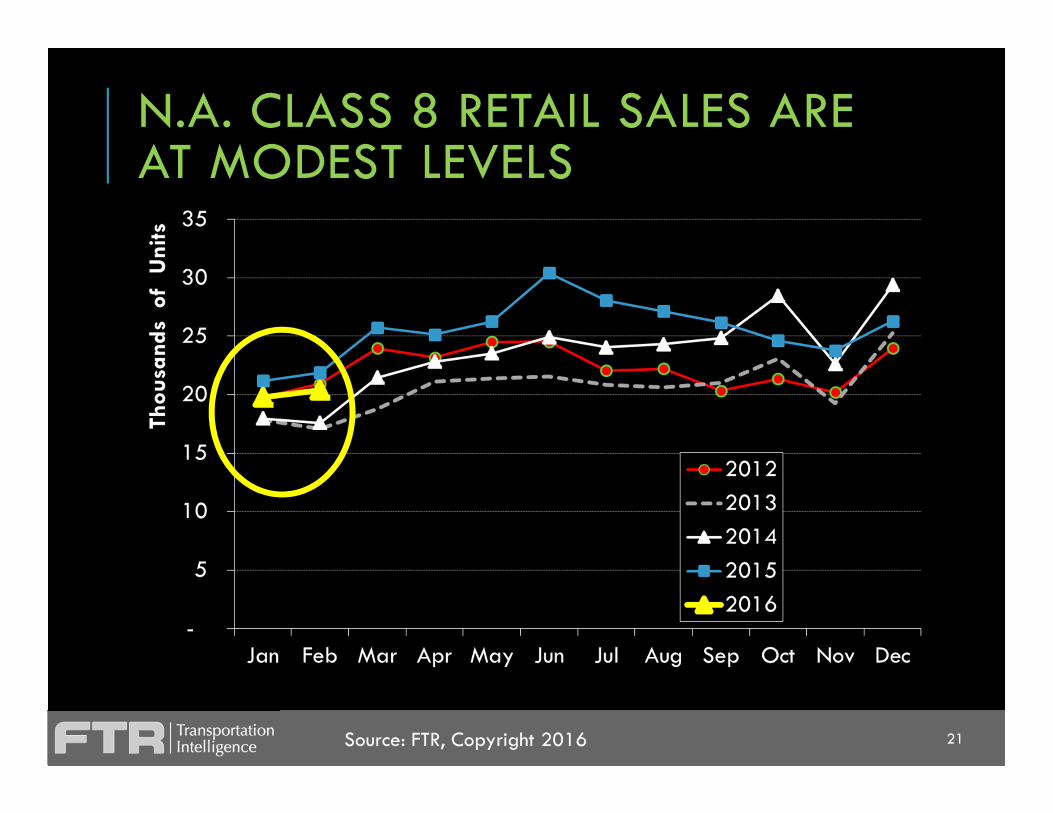

N.A. CLASS 8 RETAIL SALES ARE AT MODEST LEVELS

Source: FTR, Copyright 2016

2222

N.A. CLASS 8 BUILD ACTIVITY IS EASING BACK

Source: FTR, Copyright 2016

2323

N.A. CLASS 8 BACKLOGS HAVE PEAKED BUT ARE HEALTHY

Source: FTR, Copyright 2016

24

TOTAL CLASS 8 CAPACITY UTILIZATION

Source: FTR

25

BUILD VS ORDERS –LINING UP HISTORICALLY

Source: FTR Truck and Trailer Outlook Service

Net Orders

9 month moving avg

Monthly Build

26

NEW TRUCK LEAD TIME

Months

Source: FTR Truck and Trailer Outlook Service

Likely Production Cuts

Likely Increase In Production

27

CLASS 8 INVENTORY/RETAIL SALES RATIO – NORTH AMERICA

Months

Source: FTR Truck and Trailer Outlook Service

Likely Production Cuts

Likely Increase In Production

28

CLASS 8 INVENTORIES –EASING BACK FROM RECORD HIGHS

Source: FTR Truck and Trailer Outlook Service

29

New Freight Demand

Replacement Demand

New Equipment Demand

ECONOMICALLY DERIVED DEMAND (EDD)

30

U.S. CLASS 8 DEMAND: NORMAL CYCLE TIMING…EDD IS BELOW SALES

Sources: FTR N.A. Commercial Truck & Trailer Outlook ReportSales history ties to Ward’s Automotive Group

3131

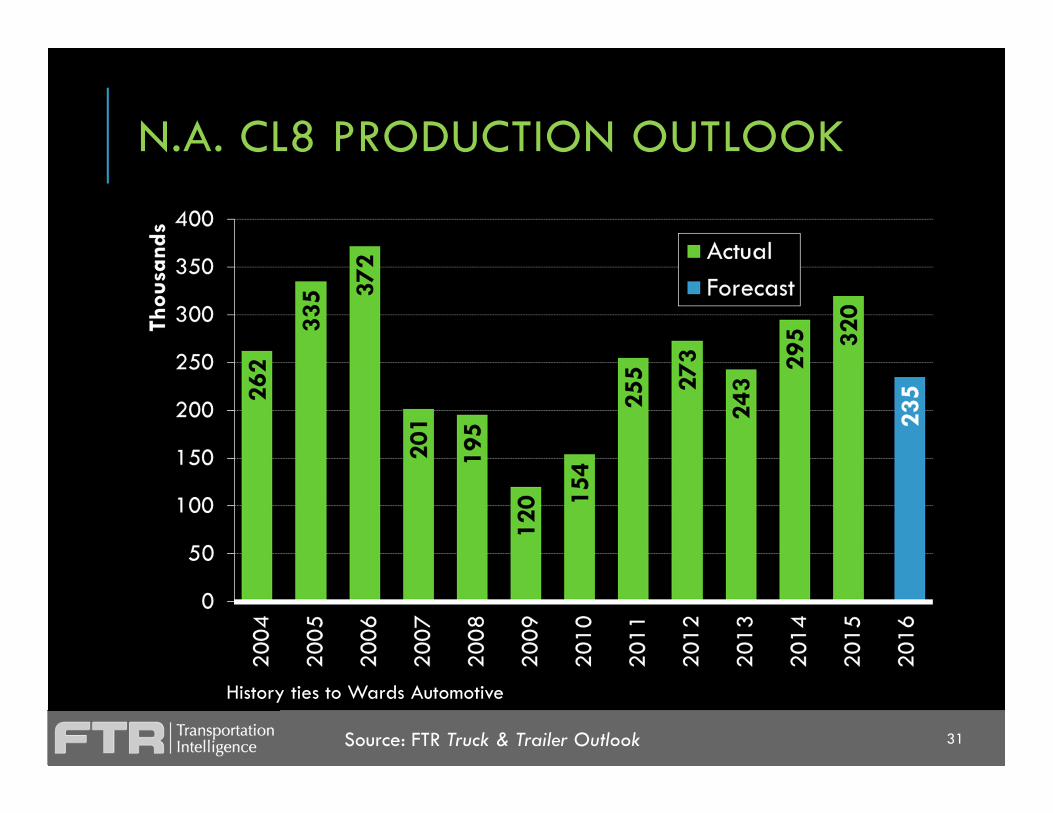

N.A. CL8 PRODUCTION OUTLOOK

History ties to Wards Automotive

Source: FTR Truck & Trailer Outlook

32

© 2016 Eaton. All Rights Reserved..

Eaton Corporation2016 Global Medium-Heavy Truck Outlook

Jeff WalkerMarch 2016

34© 2016 Eaton. All Rights Reserved..

Eaton is a global power management company

Eaton Truck industry

Electrical Fluid Mechanical

$20.9Bn

35© 2016 Eaton. All Rights Reserved..

U.S. Linehaul Fuel Consumption walk, “Reg-to-Reg” 2018-2030

Imp

rove

me

nt

in F

ue

l C

on

su

mp

tio

n

(lit

ers

/10

0 k

m, p

en

etr

ati

on

-we

igh

ted

)

vs

. 2

01

7 b

as

elin

e

Origin = 2017 truck with 15%

improvement over 2010

U.S. Regulatory environment

Expect to fill with Advanced

Powertrain, Advanced Engine

36© 2016 Eaton. All Rights Reserved..

Advanced powertrain

Mechanical Systems Controls

• Parasitic losses

• Gear friction

• Oil churn

• Dual clutch

• Customized ratios to match engine sweet spot

• Down-speeding

• Narrow-banding

• Power-shifting & hybridization

• Intelligent shift points• GPS-based

• Engine transient matching

37© 2016 Eaton. All Rights Reserved..

Advanced powertrains to meet specific customer needs

• Utilizing tailored integration to enhance fuel economy

• Optimizing fuel map efficiency with customized ratios and shift points

• Leveraging transmission overall ratio to enable down-speeding without sacrificing performance

Powertrain optimization Tailored solutions

• 6 platforms

• >30 models

The right tool for the job

38© 2016 Eaton. All Rights Reserved..

Impact of “ICA”Intelligent, Connected, & Autonomous

*SWEC = Software, Electronics, & Controls

OEMs’ focus

for differentiation

Significant resource

implications

39© 2016 Eaton. All Rights Reserved..

40

Next Steps

Growth Partnership ServiceBecome a Growth Partner to

develop your visionary and innovative skillsJoin our GIL Global Community

Share your growth thought leadership and ideas

Growth Consultinghttp://ww2.frost.com/consulting/

Phone: 1-877-GOFROST (463-7678) Email: [email protected]

GIL UniversityArrange a GIL Workshop at your company

EventsJoin our Board of Advisors to discuss your next project or training & learning

needs

41

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

What would you like to see from Frost & Sullivan?

42

www.twitter.com/FS_Automotive

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/groups?gid=4480787&trk=hb_side_g

http://www.slideshare.net/FrostandSullivan

43

* sponsorship does not include Parliamentary event

Overview of the Upcoming 2016 EventJune 28-30, 2016, inclusive of access to our 3rd day flagship GIL event

Frost and Sullivan Workshops

Key networking opportunity with Industry and government

stakeholders

Over 350 global senior executives from all spectrums of the industry

expected to attend

1st day at the House of Lords/Common chaired by Member

of Parliament*

Thought leadership keynote presentations

Highly Informative Panel discussions, interactive sessions

and knowledge sharing on Intelligent and Urban mobility trends

and future vision

Opportunity to display or witness latest technologies and products

Access to our flagship Growth, Leadership and Innovation Event

44

For Additional Information

Kayla Belcher

Corporate Communications

210.247.2450

Sandeep Kar

Global Vice President-Research

Mobility

+1 (416) 4907796

Bharani Lakshminarasimhan

Program Manager

Commercial Vehicle, Mobility

+91 44 6681 4459

Cyril Cromier

Vice President Sales

Intelligent Mobility

+33 1 42 81 22 44

![Bosch ESI[truck] Heavy Duty Truck Software Update – Q1 ...€¦ · Bosch ESI[truck] Heavy Duty Truck Software Update | Ver 2019/1 6 | 41 41135 42908 45411 47482 37000 38000 39000](https://static.documents.pub/doc/80x56/600ed0e779e62601223e82fb/bosch-esitruck-heavy-duty-truck-software-update-a-q1-bosch-esitruck-heavy.jpg)