104

GRUPPO DE ECCHER 2011

GRUPPO DE ECCHER 2011

RIZZANI DE ECCHER S.P.A.

Via Buttrio, 36

33050 Cargnacco (UD) Italy

Tel. +39 0432 6071

Fax +39 0432 522336

Joint Stock Company incorporated in Italy

Share Capital

Euro 20,000,000.00 fully paid up

Member, Udine Chamber of Commerce

Registration no.115684

Department of Foreign Trade UD 002577

Companies Register of Udine

Tax ID & VAT Number IT00167700301

rizzanideeccher.com

1

Annual Report and Consolidated Financial Statements for the Financial Year 2011(1st January – 31st December)

During the Financial Year under reviewno material changes have occurredthat require corrections or adjustmentsto the Annual Reports of preceding years.The 2011 Annual Report was approved by theShareholders’ Annual General Meetingheld in Udine, Italy on 14th June 2012.

This Annual Report was printed in 2500 copies in July and circulated to shareholders and the public, including the financial community, employees of the company,main customers and suppliers.

For further information:[email protected]

Table of Contents

3 Letter from the Chairman

4 2011 at a glance

10 History

13 Strategies

15 Organisation

18 Quality is Innovation

20 Sustainable Development

23 Areas of business activity

24 General Building

28 Infrastructures

31 Engineering and Special Equipment for Bridges and Viaducts

32 Real Estate Development

33 Focus

45 Management Report

50 Notes to the 2011 Annual Report

51 Contents of the Consolidated Financial Statements

56 Balance Sheet Analysis

68 Income Statement Analysis

71 Independent auditors’ report

73 Consolidated Financial Statements

81 Appendices

89 Statutory Financial Statements of the Parent Company

3

LETTER FROM THE CHAIRMAN OF THE BOARD OF DIRECTORS

Dear Shareholders,

Notwithstanding an increase in order backlog, the continuing economic

and financial crisis that erupted globally in 2008 and the political upheavals

of the spring of 2011 in the Mediterranean basin have caused a temporary

reduction in Group turnover.

At € 359 million, the revenues marks a decrease of 26% as opposed to 2010,

which is mostly due to the cancellation or delays of important overseas

projects owing to the unfavourable global economic situation. Conversely,

operating income (EBIT) of € 21,7 million and net profit of € 14.7 million

emphasise an excellent performance.

The order backlog, notwithstanding the cancellation of contracts in Libya and

(partially) in Kuwait, increased from € 1,641 million to € 1,979 million, of

which roughly 1/3 in Italy and 2/3 abroad. This should be enough to ensure

the comeback in the next years to the levels of production of 2010 at least.

This Annual Report and the enclosed Financial Statements have been drawn

according to principles of transparency, independence, accuracy, complete-

ness and reliability. These principles will provide any reader (whether mem-

bers of the public, the financial community, customers, suppliers or Group

employees) with a fair and accurate picture of results achieved.

In closing, I would like to convey my sincere thanks to our employees for

their commitment and hard work towards the attainment of our corporate

objectives. I would also like to thank all our business and financial partners

for their continued support and contributions towards the Group’s success.

The Chairman

Marco de Eccher

Preceding page:Office building Santa Monica, Udine (Italy)

4

2011 AT A GLANCE

As evidenced by the foregoing data, the economic and financial

position of the Group remains excellent from a structural

standpoint, with EBITDA and EBIT marking yet a slight

reduction in absolute terms but a significant increase relative

to revenues, and – more importantly – with a significant

improvement of the Group net financial position (inclusive of

short term and long-term debt relating to an ongoing leasing

contract), which is a positive € 80.6 million (as opposed to

€ 61.5 million in 2010). The sum of net current assets (NCA)

and net short term financial position (NFP) is € 45.8 million

(as opposed to € 26.8 million in 2010) and the corresponding

ratio is 1.15. The constant improvement of such financial

indicators over the preceding years bears testimony to the

Group’s ability to negotiate construction contracts that allow

for operational and financing needs to be funded directly by

payments from clients (advances and progress payments).

20102007

483,724

(447,761)35,963

7.4%(10,201)

25,7625.3%(947)

24,814(8,419)16,396

2,87313,523

80%23,724

2011

358,930

(326,249)32,681

9.1%(11,022)

21,6596.0%2,762

24,421(6,271)18,150

3,45314,697

67%25,719

488,618

(444,089)44,529

9.1%(7,653)36,876

7.5%95

36,971(13,268)

23,703531

23,172

70%30,825

492,628

(463,386)29,243

5.9%(6,773)22,470

4.6%(4,738)17,732(5,286)12,446

98111,465

74%18,238

2008

408,668

(377,270)31,398

7.7%(5,460)25,938

6.3%(2,355)23,583(7,387)16,196

69915,497

74%20,957

2009

Total revenues*

Total costs of production*Gross operating income (EBITDA) **% EBIDTA Depreciation and amortizationOperating income (EBIT)% EBITFinancial income/(expenses) and valuation adjustment of investmentsProfit or (loss) before income taxes (EBT)Income taxProfit or (loss) for the financial periodMinority share of profit for the financial periodConsolidated Group profit or (loss) for the financial period

Share value of production from overseasCash flow ***

* extraordinary income/charges included** EBITDA is conventionally calculated as the earning before depreciation and amortization, net financial income/(expenses), valuation adjustment of investment and income tax. Since the composition of EBITDA is not defined by the reference accounting standards, the criterion for its determination applied by the Group might not be consistent with that used by others and therefore not be comparable.*** consolidated Group profit + depreciation and amortization

economic and financial indicators[Euro thousand]

92,27691,209

163,396254,605199,132113,601312,733

(58,128)4,9881,2436,231

27,917108,497

23,357(103,937)

27,917

45,8091.15

82,43670,056

193,859263,915187,475122,395309,870

(45,955)4,5993,9798,578

27,90389,38111,228

(72,706)27,903

26,7511.09

38,77252,084

239,188291,272201,720

84,032285,752

5,5205,695

16,53722,232

22,06053,454

7,500(38,894)

22,060

44,4141.16

31,59576,652

194,949271,601178,031122,559300,591

(28,990)5,5042,1687,672

(5,067)58,762

9,100(72,929)

(5,067)

43,9391.15

70,86061,332

156,276217,608160,956106,207267,163

(49,555)4,9793,3308,309

12,99676,031

9,034(72,069)

12,996

22,5141.08

**** negative number = positive net short term financial position / positive number = negative short term financial position

Total non current assetsInventoryAccounts receivable Total current assetsDebts and other payables Advances from customersTotal current liabilities

Net current assets (NCA)Employees' severance indemnityProvision for contingencies and other liabilities Total non current liabilities

Net capital investedShareholders' equityNet medium and long term financial position Net short term financial position (NFP) ****

Total shareholders' equity and net financial position

NCA + NFPCurrent ratio

5

2010

25.8

13.5

23.2

36.9

2007 2008 2009

22.5

25.9

11.5

15.5

2010

80%

70%74%

74%

483.7

2011

358.9

67%

488.6

2007

492.6

2008

408.7

2009 2011

21.7

14.7

Revenues(millions of Euros)

= revenues = percentage generated abroad

net profit= EBIT

Income from operations (millions of Euros)

=

2007 2008 2009 2010

0.1 0.10.02

0.3

19.5 20.4

48.3

43.4

15.1

30.8 29.4

25.0

2007 2008 2009 2010

= ROI= ROE

2011

0

13.516.4

2011

Financial charges as a % of revenues Profitability [%]

2007 2008 2009 2010

2160

364 349

1219 793350801

1583

1142 1151

3771783

2007 2008 2009

11691081 1072

1641

92%

77%

68%

2010 2011

82%

1979

2011

439746

1185

= order book= percentage abroad

Number of employees = employees abroad= employees in Italy

Order book (millions of Euros)

66%

6

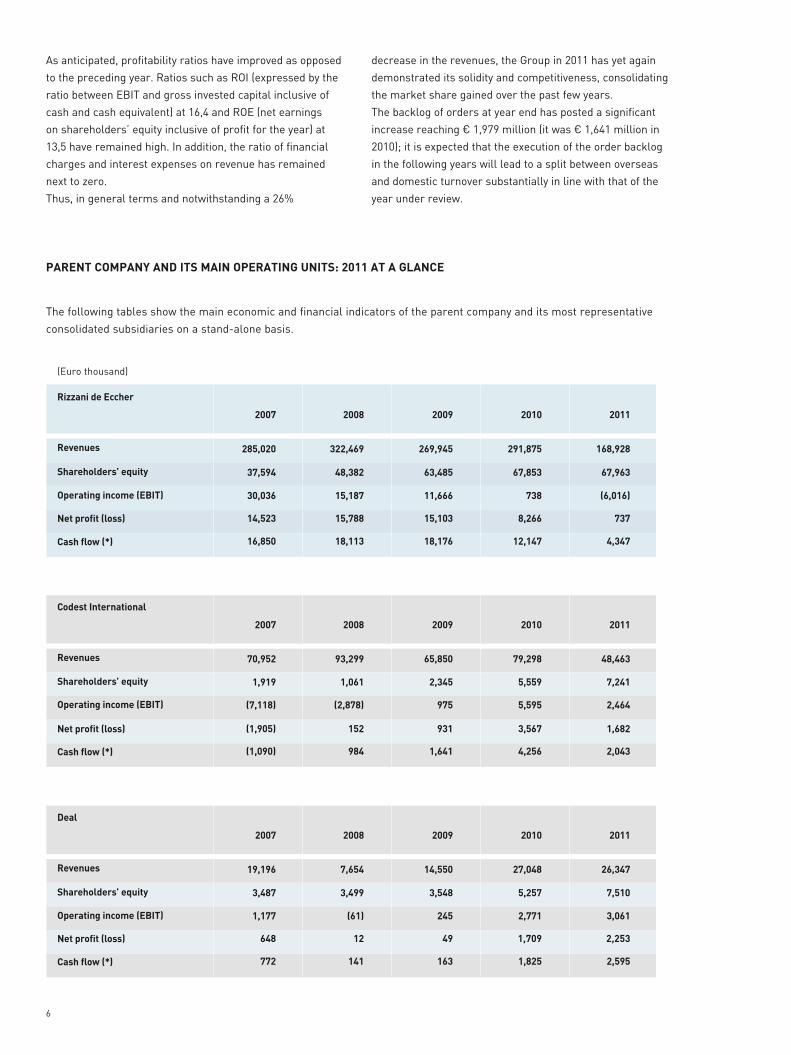

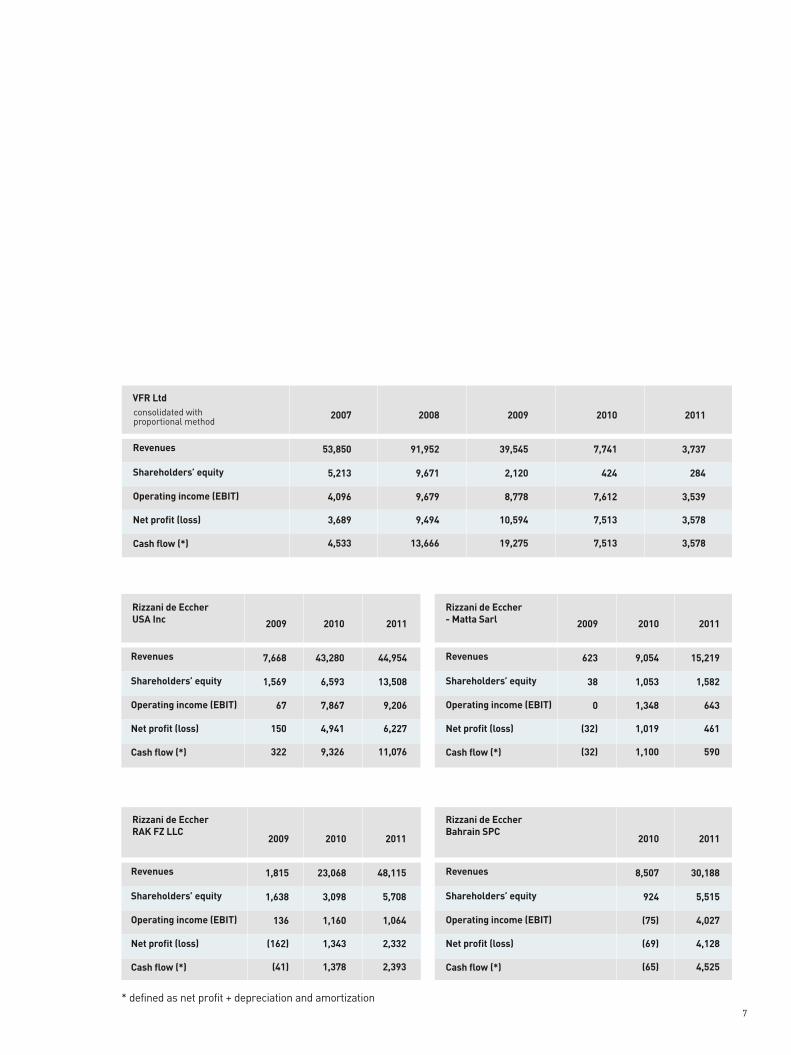

The following tables show the main economic and financial indicators of the parent company and its most representative

consolidated subsidiaries on a stand-alone basis.

PARENT COMPANY AND ITS MAIN OPERATING UNITS: 2011 AT A GLANCE

2009

269,945

63,485

15,103

18,176

11,666

2010

291,875

67,853

8,266

12,147

738

2007

285,020

37,594

14,523

16,850

30,036

2008

322,469

48,382

15,788

18,113

15,187

Rizzani de Eccher

2008

7,654

3,499

12

141

(61)

2009

14,550

3,548

49

163

245

2010

27,048

5,257

1,709

1,825

2,771

2007

19,196

3,487

648

772

1,177

Deal

2009

65,850

2,345

931

1,641

975

2010

79,298

5,559

3,567

4,256

5,595

2007

70,952

1,919

(1,905)

(1,090)

(7,118)

2008

93,299

1,061

152

984

(2,878)

Codest International

2011

168,928

67,963

737

4,347

(6,016)

2011

26,347

7,510

2,253

2,595

3,061

2011

48,463

7,241

1,682

2,043

2,464

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

As anticipated, profitability ratios have improved as opposed

to the preceding year. Ratios such as ROI (expressed by the

ratio between EBIT and gross invested capital inclusive of

cash and cash equivalent) at 16,4 and ROE (net earnings

on shareholders’ equity inclusive of profit for the year) at

13,5 have remained high. In addition, the ratio of financial

charges and interest expenses on revenue has remained

next to zero.

Thus, in general terms and notwithstanding a 26%

decrease in the revenues, the Group in 2011 has yet again

demonstrated its solidity and competitiveness, consolidating

the market share gained over the past few years.

The backlog of orders at year end has posted a significant

increase reaching € 1,979 million (it was € 1,641 million in

2010); it is expected that the execution of the order backlog

in the following years will lead to a split between overseas

and domestic turnover substantially in line with that of the

year under review.

(Euro thousand)

7

2008

91,952

9,671

9,494

13,666

9,679

2009

39,545

2,120

10,594

19,275

8,778

2010

7,741

424

7,513

7,513

7,612

2007

53,850

5,213

3,689

4,533

4,096

VFR Ltd

2011

44,954

13,508

6,227

11,076

9,206

Rizzani de Eccher USA Inc

Rizzani de Eccher- Matta Sarl

2009

7,668

1,569

150

322

67

2010

43,280

6,593

4,941

9,326

7,867

2011

15,219

1,582

461

590

643

2011

3,737

284

3,578

3,578

3,539

2010

9,054

1,053

1,019

1,100

1,348

2009

623

38

(32)

(32)

0

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

consolidated with proportional method

2011

48,115

5,708

2,332

2,393

1,064

Rizzani de Eccher RAK FZ LLC

Rizzani de Eccher Bahrain SPC 2011

30,188

5,515

4,128

4,525

4,027

2010

8,507

924

(69)

(65)

(75)

2010

23,068

3,098

1,343

1,378

1,160

2009

1,815

1,638

(162)

(41)

136

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

Revenues

Shareholders’ equity

Net profit (loss)

Cash flow (*)

Operating income (EBIT)

* defined as net profit + depreciation and amortization

8

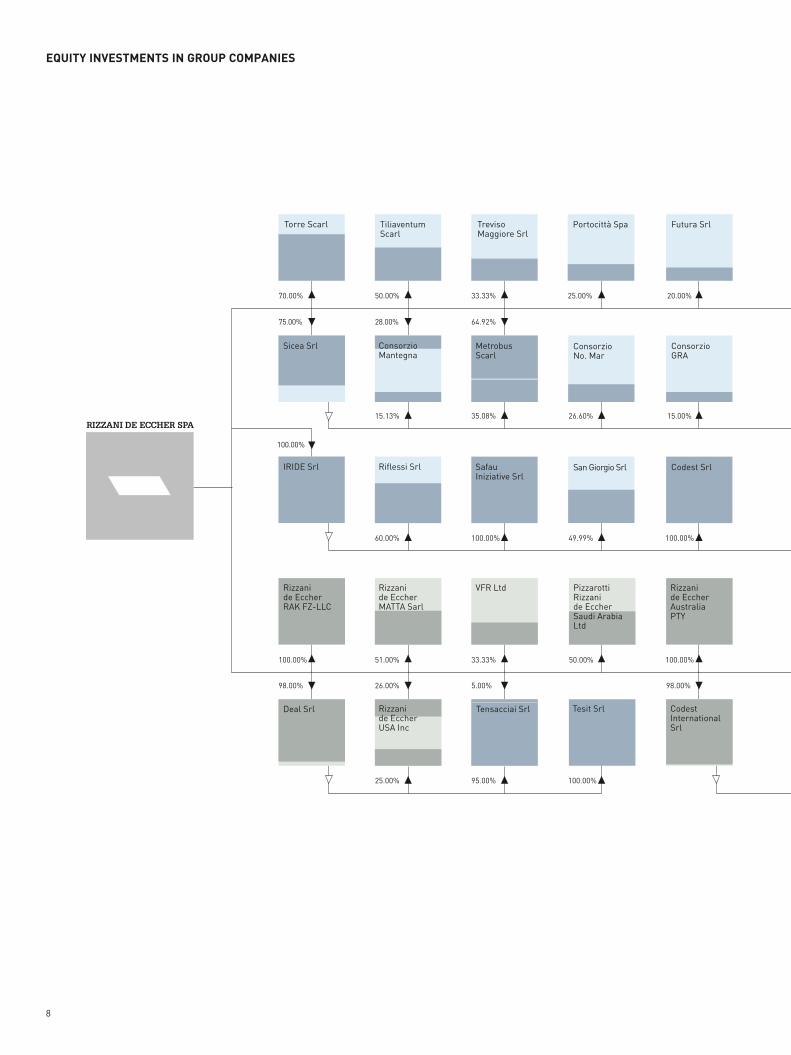

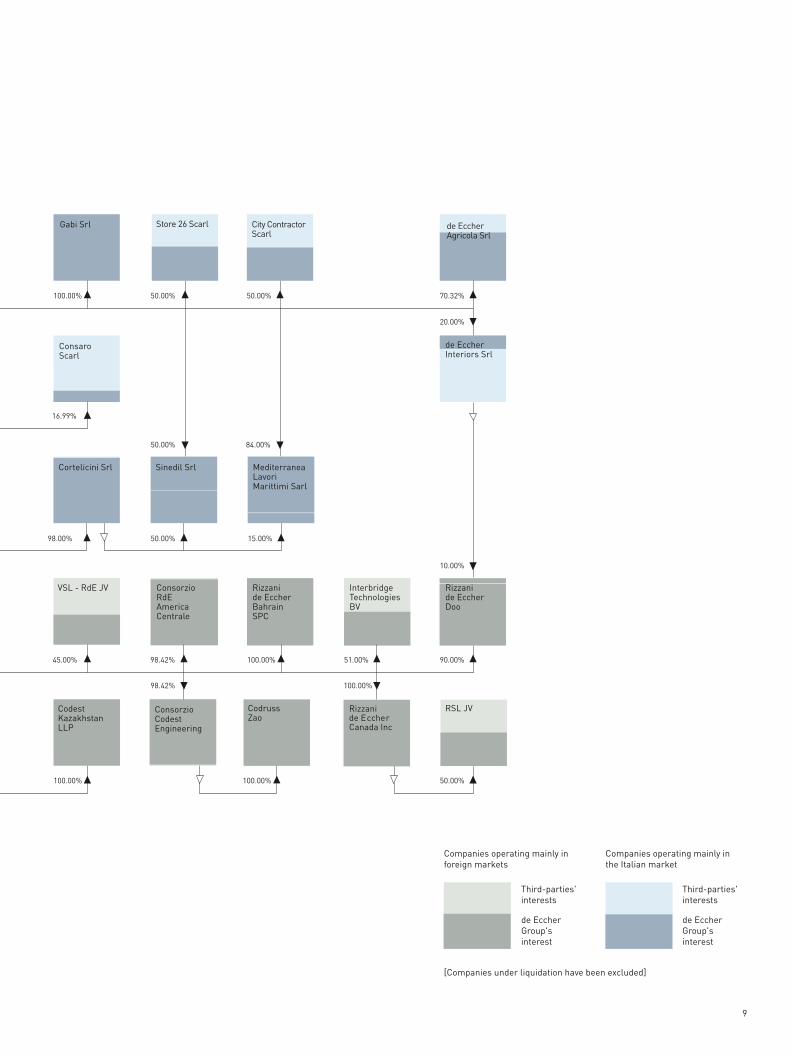

EQUITY INVESTMENTS IN GROUP COMPANIES

25.00%

Tiliaventum Scarl

26.00%

51.00%

Rizzani de EccherMATTA Sarl

28.00%

50.00%

15.13%

60.00%

Riflessi Srl

Rizzanide EccherUSA Inc

ConsorzioMantegna

26.60%

25.00%

Portocittà Spa

50.00%

PizzarottiRizzani de EccherSaudi ArabiaLtd

49.99%

San Giorgio Srl

Tesit Srl

100.00%

ConsorzioNo. Mar

20.00%

Futura Srl

98.00%

100.00%

Rizzani de EccherAustralia PTY

15.00%

100.00%

Codest Srl

CodestInternationalSrl

ConsorzioGRA

64.92%

33.33%

Treviso Maggiore Srl

33.33%

VFR Ltd

35.08%

5.00%

100.00%

Safau Iniziative Srl

Tensacciai Srl

MetrobusScarl

95.00%

IRIDE Srl

75.00%

70.00%

98.00%

100.00%

Rizzani de EccherRAK FZ-LLC

100.00%

Deal Srl

Torre Scarl

Sicea Srl

9

de EccherGroup'sinterest

Third-parties'interests

de EccherGroup'sinterest

Companies operating mainly inthe Italian market

Companies operating mainly inforeign markets

[Companies under liquidation have been excluded]

Third-parties'interests

50.00%98.00% 15.00%

100.00%

50.00%

20.00%

70.32%

10.00%

de EccherInteriors Srl

100.00%

Gabi Srl de Eccher Agricola Srl

50.00%100.00%

100.00%98.42%

98.42% 100.00% 51.00% 90.00%45.00%

Consorzio RdE AmericaCentrale

Rizzani de EccherBahrainSPC

InterbridgeTechnologiesBV

VSL - RdE JV Rizzani de EccherDoo

16.99%

ConsaroScarl

50.00%

City Contractor Scarl

50.00% 84.00%

Store 26 Scarl

Cortelicini Srl Sinedil Srl Mediterranea LavoriMarittimi Sarl

RSL JVConsorzioCodestEngineering

CodrussZao

Rizzani de EccherCanada Inc

CodestKazakhstanLLP

international tender for the construction of five school

complexes in Algeria. Two years later, the Company is

awarded a further five projects for the construction of two

tanneries and three shoe factories in the former Soviet

Union. This initial success ushers in a period of significant

growth in Eastern Europe and Central Asia, which continues

to this day. 1986 Thanks to the courage and commitment

of the de Eccher family, aided by a bright and talented

management team, the Group posts an extraordinary

growth in turnover, topping revenues of 228 billion

Italian liras in 1990, up from 37 billion liras in 1986. 1994

Difficult conditions in the domestic infrastructure market

in the mid-90s - partly caused by the high profile anti-

graft ‘clean hands’ campaign - shift the Company’s focus

towards overseas markets. Revenues from international

projects exceed 50% of total turnover for the first time.

2004 Rizzani de Eccher becomes one of the ten leading

construction companies in Italy, and is also listed among

the Top 100 International Contractors by Engineering New

Record Magazine solely on the basis of the share of turnover

generated abroad. 2005 From this year onward - thanks

to its established presence in many countries (Russia and

other CIS countries, Middle East, Mediterranean Basin

and North and Central America) - the share of revenue

from overseas operations remains consistently above 70%.

2010 With the acquisition of the South Road Superway in

Adelaide, Australia, the Group extends its operations to

Oceania and the Pacific. 2011 The third generation of de

Eccher family begins to work in the Group.

Today, the Group is one of the world’s premier construction

businesses and a market leader in its field, operating in four

areas of activity with specialised and innovative know-how:

general building construction, infrastructure construction,

engineering services and equipment solutions for bridges

and viaducts and real estate development.

HISTORY

1831 Rizzani is established in Udine, as a general

contracting and construction company. Within a few years,

it earns a prestigious reputation for carrying out large

engineering projects in Italy and in several countries in

Africa, Asia and Latin America. 1948 Riccardo de Eccher

establishes a construction and real estate development

company bearing his name, in the North Eastern Italian

region of Trentino Alto Adige. 1970 Riccardo de Eccher

takes over Rizzani, combining the track records and

capabilities of the two firms into a new company, Rizzani de

Eccher, managed by the de Eccher family. The merger and

integration process of these two companies is completed in

the early 1970s, laying the foundations for today’s corporate

structure. 1976 - The second generation of the de Eccher

family joins the management and the Company expands

its focus and market share in infrastructure projects and

public works. Following a devastating earthquake in the

Friuli region in the same year, the Company’s resources

are immediately devoted to the reconstruction process,

including the careful restoration of the medieval town of

Venzone, which, from icon of destruction rose to become a

symbol of reconstruction, not only of historical buildings,

but also of the whole urban and social fabric of the town.

1980 The construction of two large sections of the Carnia-

Tarvisio highway provides the Company with the opportunity

to develop innovative construction techniques for the

prefabrication and erection of pre-cast concrete segments.

The latter technology is further developed in the following

years, as the Group completes many important highway

and motorway projects. This invaluable technological

expertise is eventually consolidated with the establishment

of Deal, a company dedicated to vanguard technologies for

the construction of elevated bridges and viaducts, utilising

mass-production industrialised systems. 1982 Towards

the end of this year, Rizzani de Eccher wins its first large

Nella pagina a fianco:Palazzo Tergesteo, Trieste

13

The Group’s continuous expansion in new geographic areas

with high potential and the consolidation of its position in

those areas where it already operates are objectives that are

achieved through improvements in management efficiency

and effectiveness of production methods, so as to guarantee

quality and reliability in delivering products to customers.

To achieve these objectives, the Group focuses on its

organization, composed of people and processes, as the

key driver. In an industry, such as general contracting, that

is characterized by markedly tangible aspects, the Group

instead leverages its intangible assets, the effectiveness

of its processes and the skills of its human resources, in

order to provide customers with fast response times and

significantly higher quality standards than the industry

average.

In particular, the Group places strong emphasis on two

critical aspects:

Human Resources Development, which focuses on the

organic development of resources internally, with the aim of

developing the specific skill-sets to deal with the particular

areas or markets where the Group operates. This policy

hinges on a careful process of search and selection, the

offering of career advancement opportunities, such as the

Master course jointly organized by Rizzani de Eccher and the

University of Triest, and the constant investment in internal

training programs. Over the past few years, the Group has

actively hired directly in the countries where it operates, so

as to integrate more effectively with the local environment

thus improving efficiency and effectiveness.

Process Optimization, aimed at securing better coordination

within project teams as well as between project teams and

head office.

STRATEGIES

14

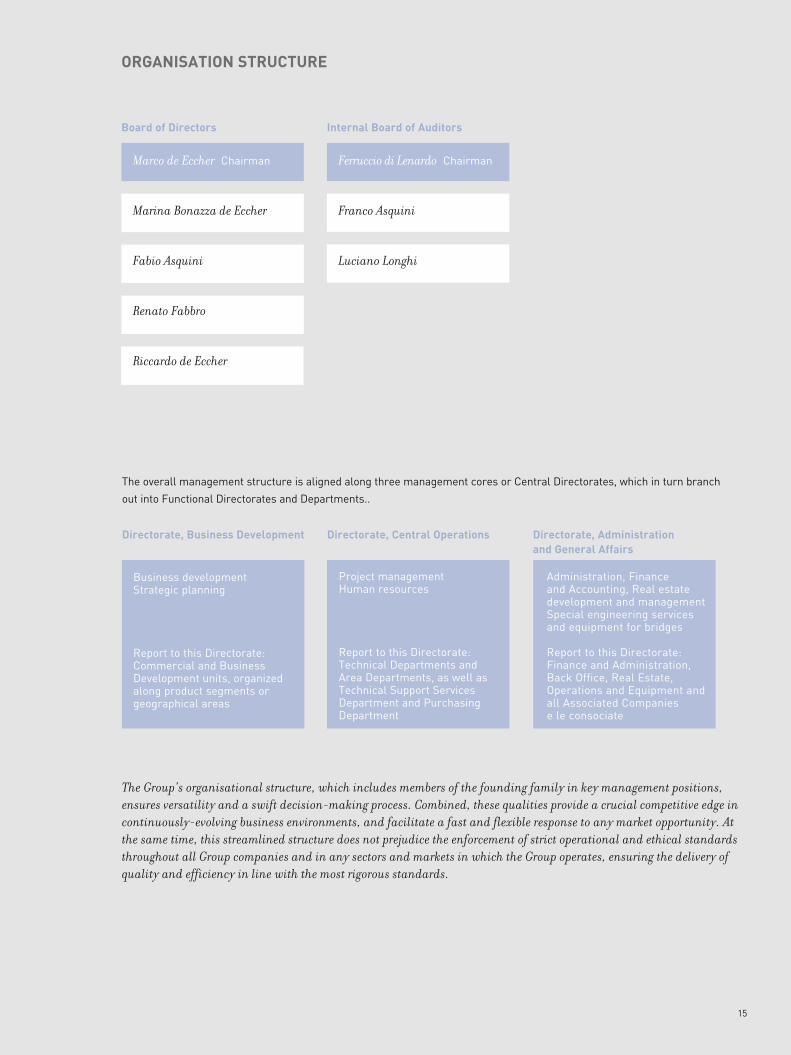

15

Directorate, Business Development Directorate, Central Operations Directorate, Administration and General Affairs

Board of Directors

Ferruccio di Lenardo Chairman

Franco Asquini

Luciano Longhi

Internal Board of Auditors

Project managementHuman resources

Report to this Directorate: Technical Departments and Area Departments, as well as Technical Support Services Department and Purchasing Department

Administration, Finance and Accounting, Real estate development and managementSpecial engineering services and equipment for bridges

Report to this Directorate: Finance and Administration, Back Office, Real Estate, Operations and Equipment and all Associated Companiese le consociate

Business developmentStrategic planning

Report to this Directorate: Commercial and Business Development units, organized along product segments or geographical areas

ORGANISATION STRUCTURE

The overall management structure is aligned along three management cores or Central Directorates, which in turn branch

out into Functional Directorates and Departments..

The Group’s organisational structure, which includes members of the founding family in key management positions,

ensures versatility and a swift decision-making process. Combined, these qualities provide a crucial competitive edge in

continuously-evolving business environments, and facilitate a fast and flexible response to any market opportunity. At

the same time, this streamlined structure does not prejudice the enforcement of strict operational and ethical standards

throughout all Group companies and in any sectors and markets in which the Group operates, ensuring the delivery of

quality and efficiency in line with the most rigorous standards.

Marco de Eccher Chairman

Marina Bonazza de Eccher

Fabio Asquini

Renato Fabbro

Riccardo de Eccher

16

Health and Safety

The most important goal achieved in 2011 was to obtain

certification of the safety management system according to

the international standards BS: OHSAS 18001:2007.

The certification process involved a comprehensive audit

carried out by Bureau Veritas, the appointed independent

certification body, at the headquarters as well as at many

construction sites. The audit focused on the regularity and

the correct application of national laws and compliance

with the mandatory provisions and standards imposed by

OHSAS.

A series of activities that mainly concern prevention and

protection and HSE personnel have been introduced

and subsequently fully implemented into systems. Such

activities involve periodic audits, equipment maintenance,

health training and supervision of personnel, control on

Human resources

The Group places the development of its human resources

as one of its main corporate objectives, placing particular

emphasis on training, career growth and organization.

The Group’s main competitive asset is composed of well

prepared, dedicated professionals who are capable of

dealing with different environments and solve any type

of problems. The business in which the Group operates

requires organized teams capable of expediting the project

tasks assigned by various clients.

These goals can only be achieved by the Group through

a corporate policy that is strongly oriented towards the

development of its human resources potential, attracting

only the best candidates, nurturing their professional

growth at all levels and emphasizing merit and

performance over seniority.

As at 31 December 2011, the Group employs 1,185

individuals from a variety of ethnic, cultural and religious

backgrounds, in different locations worldwide. Diversity is

actively encouraged as it contributes towards enriching the

competitive edge of the Group in its line of business.

Overseas-based (i.e. outside Italy) employees are 746,

of which 711 hired locally. 439 employees are Italian

nationals, of which 15% are based overseas. Educational

qualifications are very high on average, with 43%

possessing university degrees and 51% holding secondary

school diplomas.

2009

AFI ASI

0.462.16

AFI ASI

2010

0.622.27

AFI ASI

2011

0.190.92

Ay = number of accidents in the year under reviewDLA = days lost to accidentMh = cumulative man-hours during the year under review

Where:

Group consolidated dataCalculation based on the following algorithms:

Accident Frequency Index (AFI):AFI = (Ay x 100,000) / Mh

Accident Severity Index (ASI):ASI = (DLA x 1,000) / Mh

2011

29

145

176

350

22

281

498

801

1,151

53,228

50

187

202

439

21

326

399

746

1,185

60,308

20092010

35

147

167

349

16

252

525

793

1,142

45,687

Italy-based employees

Management

Staff

Workers

Total Italy

Overseas-based employees

Management

Staff

Workers

Total overseas

Total Group

Total employees’ costs(Euro thousand)

17

subcontractors and suppliers, as well as internal controls,

audit and review of implemented activities, with periodic

redefinition of objectives. This commitment finds reflection

in the drastic decrease in the number of reported injuries

during the year under review. In addition, the great majority

of reports involved light injuries.

Similarly, despite numerous inspections conducted by

regulatory bodies and supervisory authorities (ASL,

CPT, INAIL and Labour Department) no penalties or

prescriptions have been imposed in connection with the

building site operations of the Group. These results

represent a starting point from which to progress further

and ensure that the certifications are maintained, while

aiming for the continuous decline of reported accidents.

To achieve these objectives, the Group places the emphasis

on the training of personnel at all levels, as the best means

to raise the awareness of workers, supervisors and all

people involved in business processes on the risks and

critical issues associated with their job. For this reason,

2011 saw the commencement of the important training

programmes, which will continue throughout 2012. These

programmes will also introduce new concepts (related to

communication and staff management) and strengthen the

assessment of specific risks.

The foregoing concepts are numerically reported in the

accident frequency and severity indices in the table

of page 16.

Training and career development

Over the course of 2011 the Group has continued to

implement its knowledge-based programmes and training

courses, both internal and external, which are specifically

aimed at younger employees. Funds from the European

Social Fund (ESF) have been drawn to finance Project

Management, language and software courses. Great efforts

have been placed upon career development from within

the organization, and dedicated training programmes have

been put in place with the following objectives:

_development of technical engineering skills;

_development of management and organizational skills; and

_team-building and group bonding.

To assess needs and design training plans, role analyses have

been carried out by using appropriate tools, and these have

proved particularly useful. This process, with a view to increasing

staff motivation, also highlighted the possibility of undertaking

organizational changes to ensure improvements in efficiency and

a more complete response to growing market demands.

The Masters Degree course in Project Management – Advanced Applications in the Construction Industry remains

the flagship initiative. The course, which is now at its seventh

edition, is yielding excellent results in terms of applications

and recruiting opportunities. Alumni who have been hired

by the Group have risen to prominent positions in Italy and

abroad as project managers, finance managers, technical

office and project control specialists. The course is organized

in conjunction with the Universities of Triest and Udine and is

taught by faculty professors as well as reputed professionals

with proven track records in the engineering and construction

field, of which senior Rizzani de Eccher managers account

for about 50% and offer an unrivalled patrimony of insights

and experiences. The course curriculum complements theory

with practice, in the form of internships in construction sites

in Italy and abroad. With the 2011 edition, the number of

alumni who are now employed by the Group has risen to 28.

The collaboration with Academia is extended to agreements

with outside faculties for personnel training and to senior

managers of the Group holding professorships at the faculties

of engineering at the Universities of Udine and Padua.

18

To compete in the field of complex constructions requires thorough planning of all activities, careful optimisation of

resources and strict quality control. The main factors contributing to the Group’s success are the unending commitment to

investing in innovation, stringent quality control systems and the professionalism and dedication of its employees.

The emphasis and sensitivity placed on quality control

management has allowed the Group to improve consistently

on its qualitative benchmarks fulfilling stringent engineering

and architectural specifications, ensures constantly high

quality standards and achieving optimal levels of clients’ satisfaction. Rizzani de Eccher is a long-dated member

of UNI (the Italian National Agency for the unification of

production standards) which positions it at the forefront

of all new developments in production and quality control

techniques. In many occasions, this commitment to

performance has won the Group commendations as well as

performance fees. The Group’s constant focus on innovation

and its rich pool of technical knowledge in the infrastructure

sector has allowed Rizzani de Eccher to become a world

leader in the design and engineering of special equipment

for the construction of bridges and viaducts. The continuous

research and development activities of the design team of

Deal Srl have allowed this Group to expand its range of

products, which find application in other industrial sectors

where tailor-made solutions and customised equipment are

particularly appreciated.

A wide range of successful partnerships and affiliations

with other major international contractors (e.g. Bovis Lend

Lease, Cemea Investments Ltd, Six Construct Co. Ltd, John

Holland Pty Ltd, OHL Obrascon Huarte Lain SA) testify to

the status of Rizzani de Eccher as a robust and reliable

partner. These ties also represent solid stepping stones

towards the future growth of the Group in the global arena.

Another noteworthy development has been the year-end

acquisition by Deal Srl of majority control of Tensacciai

Srl and Tesit Srl, two companies operating in the design,

fabrication and installation of cable-stays, components

for tensile structures and post-tensioning systems. These

acquisitions constitute a valuable addition and complement

to the product range of Deal Srl and the Group, besides

representing a further step towards the realisation of an

integrated technological pole acting as depositary of the

Group’s know-how.

The quality policy pursued by the Group has led to the

following certifications and attestations:

Rizzani de Eccher Spa

_ISO 9001 Certification, certified 12 February 1999,

attested by Bureau Veritas Italia Spa in relation to Design

and Construction of civil engineering works, industrial

buildings, bridges, viaducts and transport infrastructure

works

_SOA Certification no. 6462/16/00 attested by SOA Nord Est

_Accreditation as pre-qualified General Contractor with

the Italian Ministry of Transportation and Infrastructure

no. 332/11 of 5 April 2011

_ BS OHSAS 18001:2007 Certification (health and

workplace safety management system) of 5 July 2011

by Bureau Veritas Italia Spa in respect of Design and

construction of civil and industrial engineering works,

bridges, viaducts and other transport infrastructure works

_ ISO 14001:2004 Certification (environment protection

system) of 28 September 2011 by Bureau Veritas Italia

Spa in respect of Design and construction of civil and

industrial engineering works, bridges, viaducts and other

transport infrastructure works

Deal Srl

_ISO 9001 Certification of 21 April 2005, attested

by Bureau Veritas Italia Spa in respect of Design,

QUALITY IS INNOVATION

19

construction, installation and operation of heavy

lifting equipment, including special equipment for the

construction of bridges, such as overhead gantry cranes,

pre-cast girder launching equipment, special elevated

formwork, cable-stayed erection equipment, post-

tensioning systems, caissons and other equipment for the

off-shore sector; design and engineering of bridges and

viaducts for road, railways or urban mass rapid transit

systems

Tensacciai Srl

_ISO 9001 Certification of 4 December 1999 by Bureau

Veritas Italia Spa in respect of Design, fabrication and

installation of cable-stay systems, post-tensioning

systems, rock anchors, ground anchors and associated

equipment and accessories; structural refurbishments

Sicea Srl

_ISO 9001 Certification certified on 30 July 2002, attested

by IGQ in respect of All activities and processes for

the construction, restoration and recovery of civil and

industrial buildings; architectural restoration of heritage

sites; construction and maintenance of roads; general

urbanization works

_SOA Certification no. 9688/16/00 attested by SOA Nord Est

Codest International Srl

_GOST P ISO 9001 Certification of 28 September 2006,

attested by Tektoplan - MosCert CMK, in respect of

All activities and processes for the provision of technical

and design services, site preparation and all construction

of buildings of any category; general civil and building

works; finishing and rendering; consulting and design

services for architectural and building purposes

Gabi Srl

_ISO 9001:2008 Certification (Quality Management

System) of 9 September 2009, attested by Bureau

Veritas Italia Spa in respect of Construction of tunnels,

underground works and roads

_SOA Certification n. 6929/16/00 attested by SOA

Nord Est

Torre Scarl

_ISO 14001:2004 Certification (Environment Protection

System) of 25 October 2011, attested by Bureau

Veritas Italia Spa, in respect of Management and

coordination of all activities associated with the provision

of goods and services by the consortium contractors of the

‘Torre’ high-rise building for Banca Intesa Sanpaolo Spa

in Torino

20

The environment

The integration of business management systems with

environmental issues was the starting point set by senior

management, which led during the course of 2011 to

obtaining the ISO 14001:2004 certification in respect of

environmental management systems.

This process has led to a deeper understanding of

all environmental issues related to the processes of

headquarters, the warehouse and the various construction

sites scattered around the globe.

New elements of evaluation (herein defined Initial

Environment Analyses) have been introduced with a view to:

_ identifying critical factors and aspects

_ prioritising the same factors and aspects in relation to

the particular context in which the local unit is immersed

_ defining the procedures to monitor these critical factors

_ obtaining the necessary authorizations

_ planning and adapting the overall project site

organization so as to ensure that all such factors are kept

under constant scrutiny.

The internal audit programs have been implemented

by introducing regular checks on all aspects of general

building construction, and particularly those with more

striking environmental impact.

Training sessions have commenced to deal with these

cogent environment issues and will continue throughout

2012 in anticipation of expected important changes in

environment protection legislation in Italy and abroad.

Code of ethics and compliance

With effect from December 2008 Rizzani de Eccher has

implemented its own organization and compliance manual,

thereby complying with the provisions of Legislative Decree

231/2001. To that effect, Rizzani de Eccher has drafted

and enacted, among the various documents that constitute

such manual, the so called Model 231, a Code of Ethics

(also available on www.rizzanideeccher.com) includes

preventive and specific protocols. The Company has

appointed a Supervisory Body entrusted with the functions

of supervising and enforcing compliance with Model 231

and ensuring that the Code of Ethics is up to date with

current legislation.

The aim of Model 231 is to prevent relevant offences under

the Law by all physical persons who are engaged in a

working relationship with the Company, be it employment

or simple cooperation. This starts from the mapping of

the areas of the firm that are ‘at risk’ and goes as far as

defining the pre-emptive protocols, which include the

organizational, physical and logical countermeasures set

forth by the same Model 231.

Through the prevention of the relevant offences, Model 231

is intended to forestall the emergence of any administrative

liability to the parent company of the Group, which may

affect its capital as a result of fines, pecuniary damages or

injunctions.

In addition to this, Rizzani de Eccher is fully aware of the

importance to educate and inform its employees and

partners so as to ensure their full knowledge of the law and

the obligations associated with it as expressed by Model 231.

Value creation and distribution

The integration between the traditional business values -

economic values expressed by production and profitability

- and the system of socio-political values - the centrality

of the individual, integrity, quality of life – which are

at once present inside and outside the organization,

poses new problems of consensus and legitimacy. The

progressive emergence in these past few years of the

so called ‘stakeholder’s view’ has raised the urgency to

have systems in place that are capable of measuring and

evaluating the ability of the firm to balance the disclosure

requirements of business partners, whether internal

or external (staff, shareholders, lenders, customers,

suppliers, public administration and the community at

large). To this end, the parameter of ‘value added’, which is

derived by reclassifying the items in the income statement

of this Annual Report, measures the wealth produced by

the firm for the benefit of the surrounding territory and its

stakeholders, thus expressing the relationship between the

firm and the socio-economic system with which it interacts.

SUSTAINABLE DEVELOPMENT

21

The value added is presented in two different dimensions:

_scheme of calculation of value added, which emerges

from comparing income and costs at each intermediate

level;

_scheme of distribution of value added comprising of the

sum of the remunerations received by stakeholders.

The value added to different stakeholders is identified as

follows:

_remuneration of human resources: it includes direct and

indirect remunerations of all those who have a working

relationship with the Group;

_remuneration of the public administration: it includes

direct and indirect taxes paid by the Group;

_remuneration of debt capital: it includes interest paid to

the banking system and financial institutions;

_remuneration of equity capital: it includes dividends paid

out to shareholders;

_remuneration of the enterprise: it includes any income

set aside as reserve or retained earnings to finance future

growth;

_acts of liberality: they include and distributions of benefits

for charity purposes.

Thus it emerges that the most substantial portions of value

added go towards the remuneration of human resources

and to the society at large through taxation. This underpins

the central role of the enterprise as a contributor to

human welfare. It is worth noting the Group’s commitment

to supporting humanitarian and cultural projects, as

witnessed by contributions and donations to various non-

profit organizations.

In 2011 the Group participated in the construction of a

cold storage facility for vaccines in Abechè, Chad, through

a donation of funds to UNICEF within a programme aimed

at rehabilitating the country’s cold chain and particularly

the logistics of vaccine distribution. Proper cold storage is

essential to the effectiveness of vaccines.

The value added was determined by reclassifying the items

in the income statement of this Annual Report, using the

methodology proposed by ‘Gruppo Bilancio Sociale’ (GBS),

an association which promotes ethical standards and

principles of social responsibility in accounting practices.

2011

480,078

390,139

89,939

91,174

(10,201)

80,973

2010

1,235

353,571

260,418

93,153

4,689

97,842

(11,022)

86,820

Value added calculation(Euro thousand)

Value of production(revenues)

Costs of production

Operating value added

Extraordinary and additional income/charges

Gross value added

Amortisation and depreciation

Net value added

%2011 %

54,868

9,372

76

181

16,395

81

80,973

2010

62,254

6,744

(431)

-

18,150

103

86,820

71.7%

7.8%

(0.5%)

0.0%

20.9%

0.1%

100%

Employees' remuneration

Public administration remuneration

Debt capital remuneration

Equity capital remuneration

Retained earnings

Charitable donations

Net value added

Value added distribution(Euro thousand)

67.8%

11.6%

0.1%

0.2%

20.2%

0.1%

100%

22

Railway Line Oued Tlèlat Tlemcen

Infrastructure Algeria 1,328,000,000 25.00

Jamal Abdul Nasser StreetKuwait City

Infrastructure Kuwait 600,000,000 48.90

Al Udeid Air Force BaseDoha

General building / Infrastructure Qatar 1,340,000,000 100.00

Multifunction complex CityLifeMilan

General building Italy 250,000,000 50.00

Headquarters of Intesa SanpaoloTurin

General building Italy 246,000,000 70.00

Multifunction complex Treviso MaggioreTreviso

General building / Real estatedevelopment

Italy 173,000,000 33.33

North Manama CausewayManama

Infrastructure / Special equipment /Engineering services

Bahrain 143,000,000 50.00

Residential complex Portopiccolo Sistiana - Triest

General building Italy 110,000,000 100.00

Requalification of Brescia hospital Brescia

General building / Project financing Italy 107,000,000 55.92

Summerland Hotel & ResortBeirut

General building Lebanon 103,000,000 51.00

95,000,000General buildingFour Seasons Hotel Baku

Azerbaijan 100.00

76,000,000Infrastructure works at Marjan IslandRas Al Khaimah

Infrastructure UAE 100.00

55,000,000Dulles Metrorail elevated lineWashington DC

Infrastructure USA 100.00

109,000,000Technological building for central hospitalUdine

General building / Project financing Italy 48.50

31,000,000Miami Orange Line LRTMiami

Infrastructure USA 100.00

19,000,000Banca Nazionale del LavoroMilano

General building Italy 61.44

17,900,000Residential complexAtyrau

General building Kazakhstan 100.00

12,800,000South Road SuperwayAdelaide

Special equipment /Engineering services

Australia 100.00

State Road 826 Palmetto ExpresswayMiami

Infrastructure / Special equipment /Engineering services

USA 38,000,000 100.00

Evraz South Mill plant Rostov

General building Russia 45,000,000 100.00

Project Business area Country Amount Share %

23

AREAS OF BUSINESS ACTIVITY

Over the years, the Group has consolidated its leading position in four main areas: General Building Contracting, Infrastructure Contracting, Engineering Services and Equipment for Bridge Construction and Real Estate Development. Apart from the

specific circumstances of certain individual markets, the Group is generally involved in all of the foregoing business areas, in every

country where it is active. The Group’s well-established presence in Russia and CIS countries of Central Asia, Middle East, the

Mediterranean Basin and Central and North America, combined with the vast international experience acquired with working for

many international clients ensure a solid and dominant market position, pointing to strong growth and a stable future. The table in

the previous page illustrates the main projects underway during the period under review, according to the four areas outlined above.

24

In general building contracting, the Group is well positioned in market segments which demand increasingly high

standards of technology and quality. Since each building is unique and construction site conditions differ greatly,

each project requires specific technical skills. Over the past few years, energy efficiency has become the underlying

theme of every new project. This is accomplished through a vast range of design solutions including purpose-

built volumes, the adoption of materials and technologies that facilitate heat transmission with the outside, the

installation of energy-efficient heating/cooling systems and the recourse to renewable energy sources (solar energy,

heat pumps). Furthermore, in order to compete in high-end market niches and to maintain the expected quality

levels in the design and construction process, the Group has established a number of vertically-integrated dedicated

subsidiaries, each of which specialises in particular steps of the production and delivery process. These steps include

design, prefabrication, plant engineering and interior decoration and furnishing. These companies work in synergy

within the framework of the general contracting business of the Group. The main sectors of activity in this area are:

residential buildings, office buildings, industrial and commercial buildings, hospitals, schools, luxury hotels, large-

scale renovations and recovery of heritage sites and finally military infrastructure.

Residential buildingsThe Group has always performed well in this area, leveraging

off the market knowledge of its real estate development unit

and the track record in high-quality construction projects. In

this segment, the Group focuses on large and complex projects

with high quality standards. In early 2011 Rizzani de Eccher

commenced construction of the Portopiccolo mixed use project

in Sistiana (Triest), a contract worth in excess of € 110 million.

The project calls for the recovery of a disused quarry facing the

sea, on whose site 420 residential units, retail outlets, hotels,

bars, restaurants, a 100-berth marina and a beach resort are

to be built. In February 2011, Codest International was awarded

the contract for the construction of a residential complex in

Kazan (Tatarstan, Russian Federation) comprising of 58 villas,

a kindergarten, office and technical buildings. The contract is

worth € 19 million. In December 2011, Rizzani de Eccher has

taken over the position of Immobiliare Lombarda Spa (a Gruppo

FonSai company) in the contracting consortium, which together

with Lamaro Appalti Spa, is entrusted with the construction

of the massive CityLife mixed-use development in Milan, a

project started in 2008. The consortium had a construction

backlog of € 160 million as at the date of Rizzani de Eccher

acquisition. The backlog increased by a further € 48.5 million

in January 2012 with the award of an additional contract for the

construction of the 100 m tall Park Tower, a residential high

rise designed by renowned architect Daniel Libeskind. In the

same month, Codest International has executed an important

contract agreement related to the 2018 Moscow World Cup;

this agreement includes the construction of a commercial area

consisting of a complex of 12 buildings (2 Hyatt hotels, 4 office

buildings, 6 residential buildings, for an amount in aggregate

of € 395 million) in connection with the VTB Arena Stadium Project.

Business Areas. General building contracting

Office buildingsThe construction of modern office buildings, which is rapidly

developing in many markets, is a key focus area for the

Group, characterized by a high level of sophistication. Each

office building project requires close cooperation with highly

qualified designers to achieve an effective convergence of

25

technical requirements and functionality. Rizzani de Eccher

is engaged in the design & build of the headquarters of

banks and multinational companies, as well as government

buildings and offices in Italy and abroad, with stages of

deliveries ranging from ‘shell and core’ to complete

‘fit out’, which includes the supply and installation of

interior furnishings. During the course of 2011, construction

activities have continued on the Banca Intesa Sanpaolo office

tower in Turin, a skyscraper over 160 m tall designed by

renowned architect Renzo Piano. Rizzani de Eccher has won

the project in joint venture with Swiss contractor Implenia.

As at 31 December 2011 the € 246 million project had

reached a progress of some € 34 million.

Industrial buildings The Group’s track record in this field dates back to large

industrial projects in Italy and abroad in the second half of

1800s. In the past few decades such wealth of experience

has been put to good use as evidenced by the successful

completion of industrial buildings in Italy and abroad in

several industries and sectors, such as steel plants, textile

factories, mechanical workshops, tanneries, shoe factories,

food processing and several other industrial buildings.

During the course of 2011, Codest won the contract for a

large-scale green field project consisting of the construction

of a steel mill at Ust-Donetskiy (Rostov, Russian Federation)

for € 45 million. The mill will have a rated output capacity of

600,000 tons per annum of reinforced concrete bars (rebars)

and other steel applications for the construction industry.

The plant will utilise Siemens technology installed by Codest.

HospitalsThis is an area characterized by the rapid evolution of

functional requirements, increasingly sophisticated MEP

components and ever more specific medical equipment.

The utilization of project financing to fund the construction

and operation of hospitals is becoming ever more frequent,

which demands strong skills and commitment not just in

respect of the design and construction challenges (with

which the Group is obviously very experienced in dealing) but

also in respect of the financial and legal challenges, which

the Group has amply demonstrated to be able to negotiate

with the required professionalism. During 2011, the project-

finance scheme in respect of the expansion of the facilities

of Spedali Civili di Brescia has reached several milestones

such as the completion and opening of the new kitchen

and canteen building and commencement of works on the

new basement plate. Meanwhile, the entire project, whose

contract amount has increased to € 107 million, has reached

a progress of € 21 million at year end. As regards another

hospital project-finance, the build & operate of several

hospital facilities for S. Maria della Misericordia in Udine, an

addendum to the main contract was finalised in 2011, with

the project budget now reaching € 109 million (excluding the

remote heating network). Progress as at year end reached €

32 million. Naturally, difficult conditions in capital markets

have resulted in financial closing for the project being

postponed several times. However, Siram (a Dalkia company)

and partners have continued to provide financing for the

execution of the project in order to respect the deadlines

imposed by the public sector owner.

Luxury hotelsThe experience in the field of large scale buildings combined

with traditional craftsmanship has enabled the Group to

compete effectively in the luxury hospitality segment. Works

have drawn to a close in 2011 at the lavish Four Seasons Hotel in Baku (Azerbaijan), a contract worth € 95 million,

while they have continued apace, reaching a progress of € 25

million (on € 103 total) at the Summerland Hotel & Resort in

Beirut, a luxury property on the waterfront of South Beirut,

which shall be operated by Kempinski.

Military infrastructureInfrastructure projects for the armed forces are

characterised the world over by their sheer size and

complexity. They usually include the construction of a

number of independent structures, each designated for

highly specialised functions. Military projects also require

thorough and complex plant-engineering over vast areas, but

need practical infrastructure for rapid and easy connections.

In all these projects, planning schedules and delivery times

are notoriously inflexible, since they are tightly linked to

the movement of troops and armaments, which are in turn

classified information. The Al Udeid Air Force Base, in Qatar

continues to be the Group’s flagship project in this field also

in 2011, with an additional extension. Billed works at the

end of 2011 topped € 1.291 billion. Construction is set to be

completed in 2012 for a final amount of € 1.340 billion.

Large scale building renovations and recovery of heritage sitesThe construction track record of more than a hundred

years and the specific skills gained from the experience

of the extensive post-earthquake reconstruction of the

Friuli region in 1976 provide Rizzani de Eccher with the

knowledge capital to undertake complex restorations

on monumental buildings adopting the most innovative

technologies. Works have been completed in 2011 on

Palazzo Tergesteo, a historical building in Triest, while

the Banca Nazionale del Lavoro Headquarters project

in Piazza S. Fedele in Milan, a € 19 million contract, is

nearing completion.

28

Environment and hydraulic engineering During past decades Rizzani de Eccher has completed

important projects in this sector in Italy and abroad. Some

of the most representative projects include sewerage pipe

networks; water purification systems equipped with underwater

pipelines for offshore discharge; aqueducts and water-

supply networks and dredging works on rivers and navigable

waterways. The infrastructure project at Marjan Island in Ras al Khaimah (UAE), which covers the complete urbanization

works comprising of roads, bridges, sewerage networks, an

aqueduct, high and low voltage power lines, telephone lines and

street lighting for a grand complex of artificial islands set to

host hotels and sports facilities, reached completion in 2011 for

a total contract value of € 76 million.

Highway networks, railways, subways and mass transit light railwaysAt present Rizzani de Eccher is increasingly engaged in the

construction of railways and in particular mass transit light

railway systems in Italy and abroad. Works for the dual track

Oued Tlélat Tlemcen railway line in Algeria have finally

resumed at the end of 2011, on the basis of the revised design

requested by the client. During the course of 2011 works have

continued, reaching € 10 million progress, on the € 31 million

Orange Metro Line in Miami, while the € 55 million Dulles Corridor Metrorail Project in Washington (DC) has almost

reached completion. Both projects link existing metro lines with

the respective international airports, while the latter project

also involves Deal as the supplier of all special equipment.

Again in the USA, 2011 witnessed substantial progress on the

Palmetto Interchange in Miami (Florida), a clover-leaf junction

on 5 levels and 4 overpasses worth € 38 million, including

special equipments provided by Deal. In early 2010, Rizzani

de Eccher in association with Pizzarotti won the contract for

the enlargement to three lanes (in each direction) of the A4 Highway, comprising of a first stretch of 25 km from the Bridge over the Tagliamento River to Gonars and the Palmanova interchange for a total contract value of € 300 million, of which

one third or € 100 million is under a private finance initiative

(PFI) arranged by the builders. Unfortunately construction

is still on hold pending the definition of the public portion of

the financing. As at 31 December 2011, works on the North Manama Causeway in Bahrain have reached a progress of € 86

million on a total of € 143 million, including special equipments

provided by Deal. This is a project carried out in joint venture

with Six Construct and a local contractor, which includes a

90,000 m2 viaduct made of prefabricated segments. Finally,

construction works continue on the massive prefabrication

plant for bridge segments, which is intended to feed the two-

level upgrade of Jamal Abdul Nasser Street at Kuwait City.

This project, worth in excess of € 600 million, covers a length of

14 km length and involves 395,000 m2 of prefabricated bridge

segments. The contract is being performed in joint venture with

OHL (Spain) Trevi (Italy) and Kuwaiti contractor Boodai.

Rizzani de Eccher excels at infrastructure building and transport engineering in particular, thanks to more than one

hundred years’ experience in this field. In the past few years most of the Group’s infrastructure projects have been outside

Italy, as the Italian market is experiencing a period of recession due to funding shortages and competitive pressures on

costs. Rizzani de Eccher is also actively involved in evaluating and securing project finance for infrastructure projects.

At home and abroad, emphasis is placed on Design & Build tenders where competitive pricing is just one aspect of the

overall offer, and where design and engineering solutions play an important role.

Business Area. Infrastructures

29

30

31

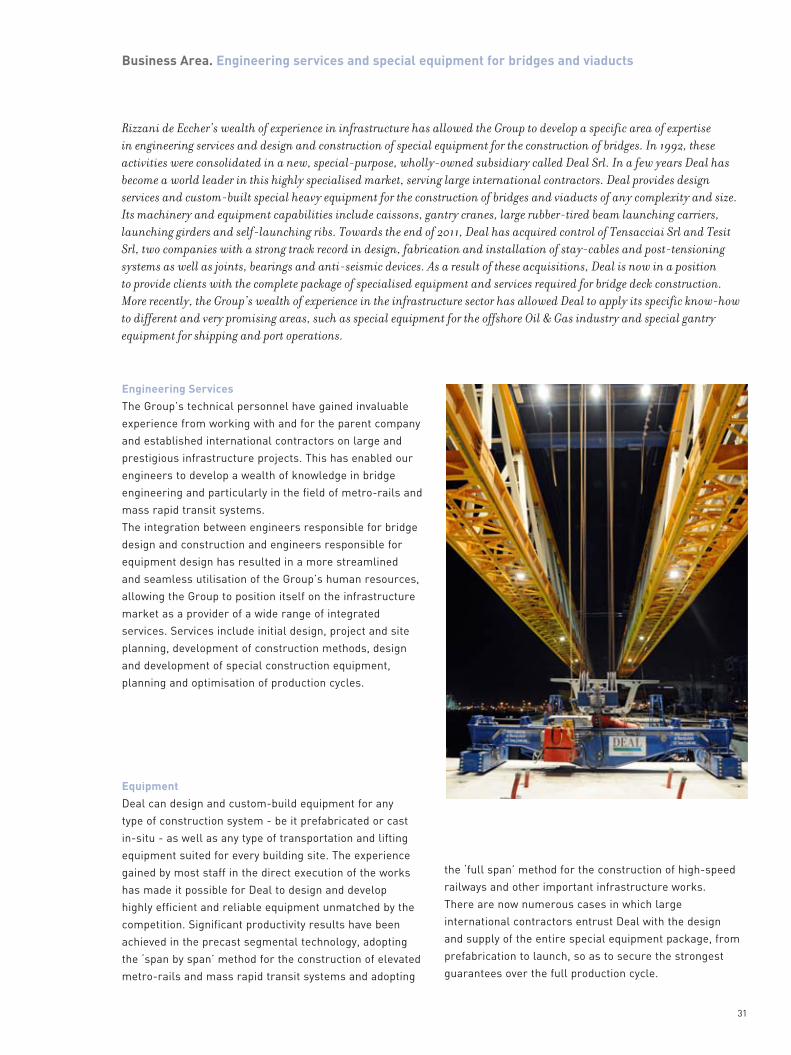

Engineering ServicesThe Group’s technical personnel have gained invaluable

experience from working with and for the parent company

and established international contractors on large and

prestigious infrastructure projects. This has enabled our

engineers to develop a wealth of knowledge in bridge

engineering and particularly in the field of metro-rails and

mass rapid transit systems.

The integration between engineers responsible for bridge

design and construction and engineers responsible for

equipment design has resulted in a more streamlined

and seamless utilisation of the Group’s human resources,

allowing the Group to position itself on the infrastructure

market as a provider of a wide range of integrated

services. Services include initial design, project and site

planning, development of construction methods, design

and development of special construction equipment,

planning and optimisation of production cycles.

EquipmentDeal can design and custom-build equipment for any

type of construction system - be it prefabricated or cast

in-situ - as well as any type of transportation and lifting

equipment suited for every building site. The experience

gained by most staff in the direct execution of the works

has made it possible for Deal to design and develop

highly efficient and reliable equipment unmatched by the

competition. Significant productivity results have been

achieved in the precast segmental technology, adopting

the ‘span by span’ method for the construction of elevated

metro-rails and mass rapid transit systems and adopting

Business Area. Engineering services and special equipment for bridges and viaducts

Rizzani de Eccher’s wealth of experience in infrastructure has allowed the Group to develop a specific area of expertise

in engineering services and design and construction of special equipment for the construction of bridges. In 1992, these

activities were consolidated in a new, special-purpose, wholly-owned subsidiary called Deal Srl. In a few years Deal has

become a world leader in this highly specialised market, serving large international contractors. Deal provides design

services and custom-built special heavy equipment for the construction of bridges and viaducts of any complexity and size.

Its machinery and equipment capabilities include caissons, gantry cranes, large rubber-tired beam launching carriers,

launching girders and self-launching ribs. Towards the end of 2011, Deal has acquired control of Tensacciai Srl and Tesit

Srl, two companies with a strong track record in design, fabrication and installation of stay-cables and post-tensioning

systems as well as joints, bearings and anti-seismic devices. As a result of these acquisitions, Deal is now in a position

to provide clients with the complete package of specialised equipment and services required for bridge deck construction.

More recently, the Group’s wealth of experience in the infrastructure sector has allowed Deal to apply its specific know-how

to different and very promising areas, such as special equipment for the offshore Oil & Gas industry and special gantry

equipment for shipping and port operations.

the ‘full span’ method for the construction of high-speed

railways and other important infrastructure works.

There are now numerous cases in which large

international contractors entrust Deal with the design

and supply of the entire special equipment package, from

prefabrication to launch, so as to secure the strongest

guarantees over the full production cycle.

32

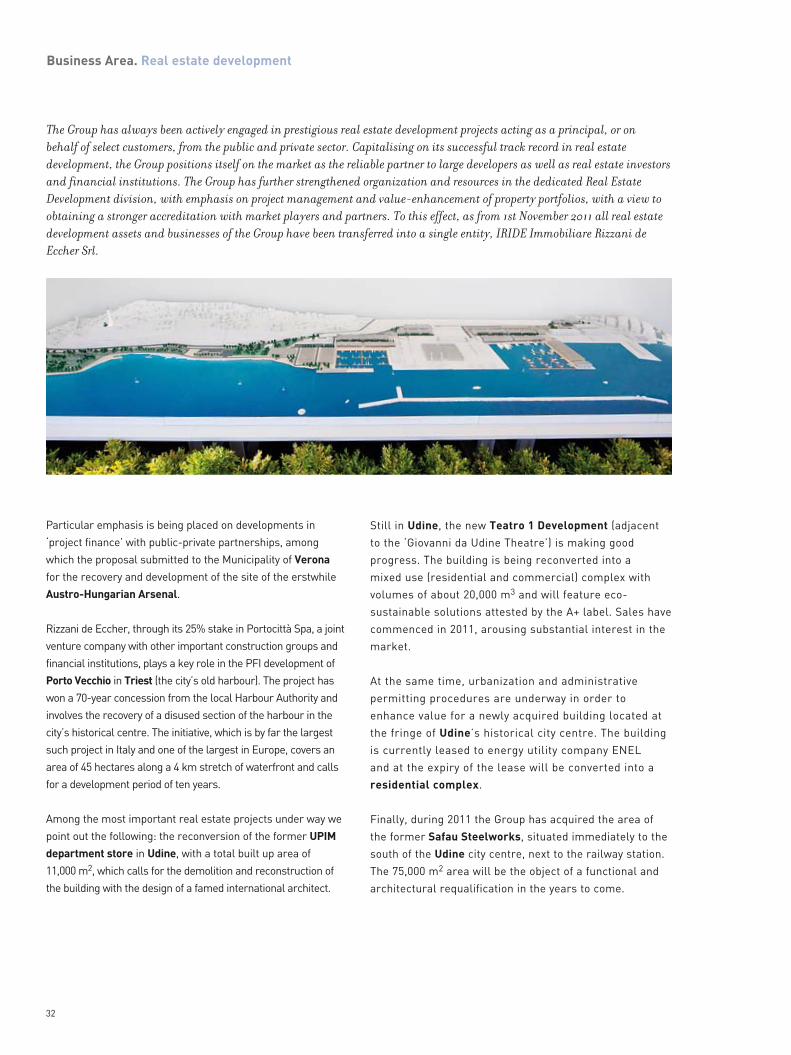

Business Area. Real estate development

The Group has always been actively engaged in prestigious real estate development projects acting as a principal, or on

behalf of select customers, from the public and private sector. Capitalising on its successful track record in real estate

development, the Group positions itself on the market as the reliable partner to large developers as well as real estate investors

and financial institutions. The Group has further strengthened organization and resources in the dedicated Real Estate

Development division, with emphasis on project management and value-enhancement of property portfolios, with a view to

obtaining a stronger accreditation with market players and partners. To this effect, as from 1st November 2011 all real estate

development assets and businesses of the Group have been transferred into a single entity, IRIDE Immobiliare Rizzani de

Eccher Srl.

Particular emphasis is being placed on developments in

‘project finance’ with public-private partnerships, among

which the proposal submitted to the Municipality of Verona

for the recovery and development of the site of the erstwhile

Austro-Hungarian Arsenal.

Rizzani de Eccher, through its 25% stake in Portocittà Spa, a joint

venture company with other important construction groups and

financial institutions, plays a key role in the PFI development of

Porto Vecchio in Triest (the city’s old harbour). The project has

won a 70-year concession from the local Harbour Authority and

involves the recovery of a disused section of the harbour in the

city’s historical centre. The initiative, which is by far the largest

such project in Italy and one of the largest in Europe, covers an

area of 45 hectares along a 4 km stretch of waterfront and calls

for a development period of ten years.

Among the most important real estate projects under way we

point out the following: the reconversion of the former UPIM department store in Udine, with a total built up area of

11,000 m2, which calls for the demolition and reconstruction of

the building with the design of a famed international architect.

Still in Udine, the new Teatro 1 Development (adjacent

to the ‘Giovanni da Udine Theatre’) is making good

progress. The building is being reconverted into a

mixed use (residential and commercial) complex with

volumes of about 20,000 m3 and will feature eco-

sustainable solutions attested by the A+ label. Sales have

commenced in 2011, arousing substantial interest in the

market.

At the same time, urbanization and administrative

permitting procedures are underway in order to

enhance value for a newly acquired building located at

the fringe of Udine’s historical city centre. The building

is currently leased to energy utility company ENEL

and at the expiry of the lease will be converted into a

residential complex.

Finally, during 2011 the Group has acquired the area of

the former Safau Steelworks, situated immediately to the

south of the Udine city centre, next to the railway station.

The 75,000 m2 area will be the object of a functional and

architectural requalification in the years to come.

Focus

1 Palazzo Tergesteo Triest

2 Treviso Maggiore Treviso

3 State Road 826 Palmetto Expressway Miami

3434

Rizzani de Eccher. Focus 1

Palazzo Tergesteo

Triest

Client: Cerep Italy U

Palazzo Tergesteo is a neoclassical building dating back to 1842 situated in the heart of Triest’s historic city centre (just a stone’s throw from Piazza Unità), which connects Piazza della Borsa (site of the former stock exchange and commercial heart of Habsburg Triest) with Piazza Verdi, the site of the renowned theatre of the same name.

Careful restoration work has brought old splendour back to the elegant neo-classical facade, the majestic entrances that lead to the gallery reconstructed in its original nineteenth century style, and the sculptures by Zandomeneghi and Bianchi. The variety of high quality materials used (marble, wood and ceramic), the use of the latest technologies and systems, the oak doors and shutters, have enhanced and made functional the building without detriment to the property’s historical charm.

The gallery, covered by a glass canopy and artfully restored, divides the building into four ‘towers’ that house 20 retail units located on the ground and mezzanine floors for a total of 4,000 m2.On the upper floors, one tower is devoted to offices, while the other three are intended for residential use.

contract amount 16,200,000

work commencement December 2008

final delivery April 2011

Volumes (excluding gallery) 53,300 m3

NLA 10,600 m2

covered area 2,440 m2

glass canopy area 640 m2

36

37

39

Rizzani de Eccher. Focus 2

Treviso Maggiore Treviso

Client: Fondazione Cassamarca

contract amount 173,000,000

work commencement September 2005

final delivery July 2012

total volumes 236,000 m3

area 60,000 m2

above-ground built up area 80,000 m2

below-ground built up area 55,000 m2

poured concrete 119,000 m3

reinforcement steel 16,600 t

exterior walls cladding 45,100 m2

bricks employed 2,660,000

doors and windows installed 2,430

curtain walling 15,200 m2

lifts 45

Treviso Maggiore was born just a few steps from the sixteenth century walls of Treviso, in the area where the historic factory of bricks and ceramics ‘Appiani’ has been operating since 1873.

The project, designed by the renowned architect Mario Botta with the aims of regenerating the area from an environmental and architectural perspective and linking the historic city centre with the most immediate outskirts, finds its centre of gravity in the large central square of over 11,000 m2, paved with Rosso Asiago marble and porphyry and dominated by a large marble fountain, in addition to the landscaping offered by 1,500 rose bushes.

Facing the square are 10 mixed-use buildings (office, retail and residential) of variable height between five and nine floors, a multipurpose auditorium with 500 seats and a small church. The basement, which extends for almost the entire surface of the complex, along with a parking garage located on the north end, hosts all technical installation and 2,000 parking spaces.

Treviso Maggiore was designed to become the new terminal for office and institutional buildings in the city and will host the prefecture, the police central precinct, the chamber of commerce, the manufacturers association, the confederation of craftsmen, the local tax office, another precinct for the financial police and the local headquarters of the builders association.

Arranged on the long sides of the square and complete with green areas, the residential buildings are developed on a lower area between ground floor and fourth floor, which includes 80 shops and offices, and a higher area on 4 towers, 9-storey each, yielding a total of 120 residential units. The residences include 16 duplex penthouses of 200 m2 each, with view over the Alps and the city centre to the north.

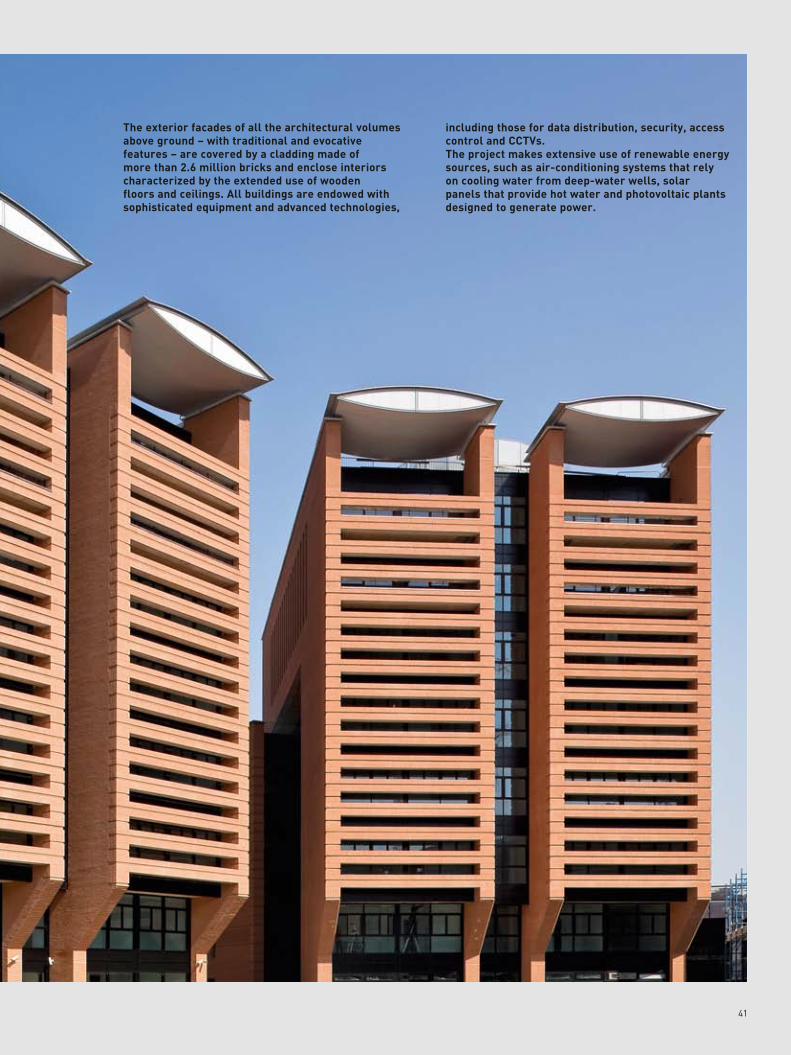

40

41

The exterior facades of all the architectural volumes above ground – with traditional and evocative features – are covered by a cladding made of more than 2.6 million bricks and enclose interiors characterized by the extended use of wooden floors and ceilings. All buildings are endowed with sophisticated equipment and advanced technologies,

including those for data distribution, security, access control and CCTVs.The project makes extensive use of renewable energy sources, such as air-conditioning systems that rely on cooling water from deep-water wells, solar panels that provide hot water and photovoltaic plants designed to generate power.

4242

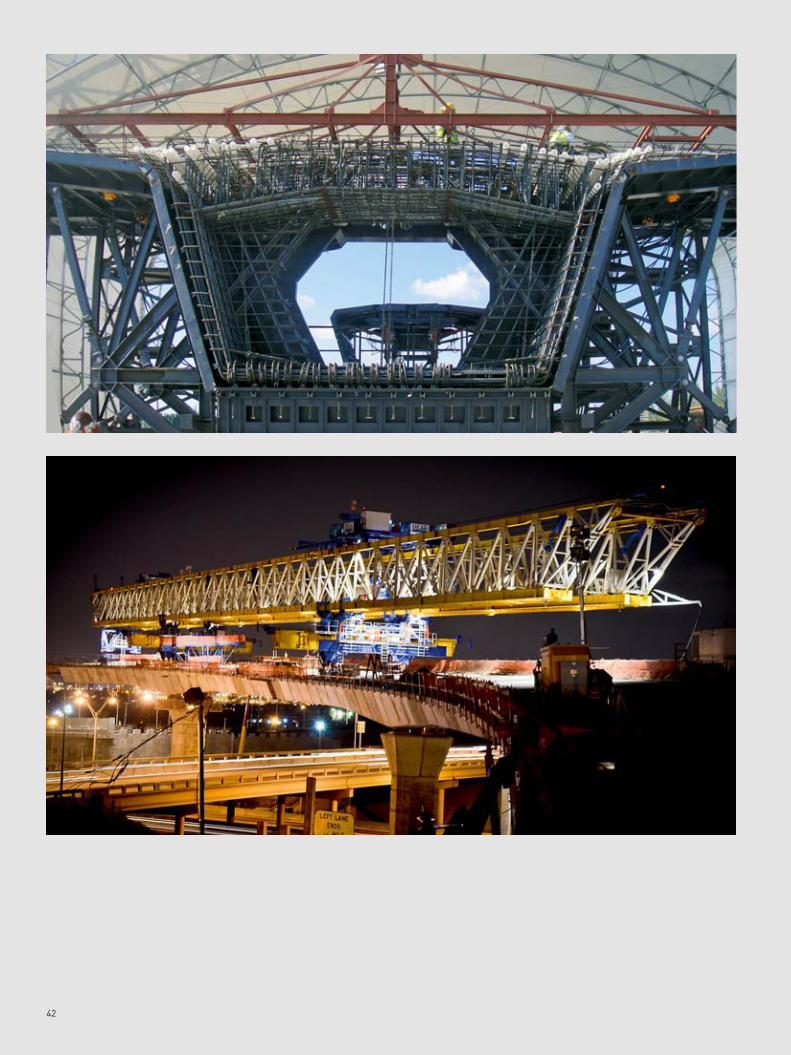

4343

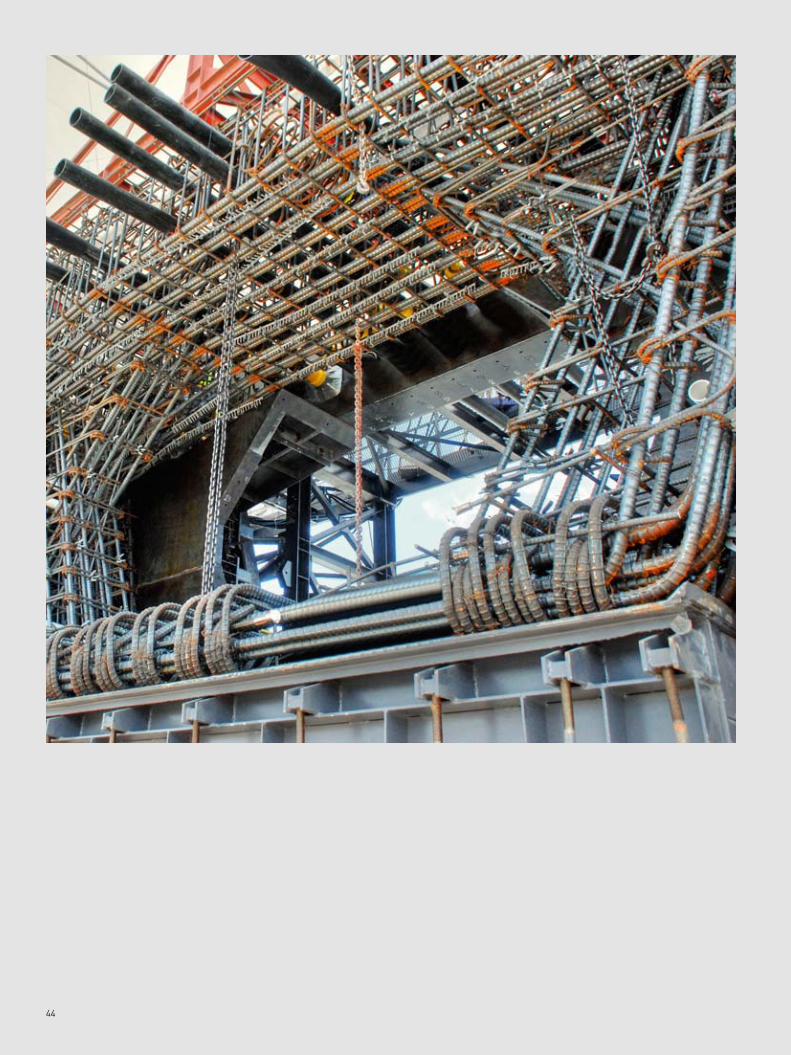

As part of a USD 558 million mega-project (the most expensive ever developed by the State of Florida) aimed at easing congestion on State Route 826 ‘Palmetto’, Rizzani de Eccher USA is currently building 4 viaducts with the pre-cast segmental method. The overlying viaducts serve as connecting ramps with State Route 836 ‘Dolphin’.

The precast segments are fabricated in the purpose-built prefabrication plant, which is the same one that had been previously served for the construction of the rapid transit Orange Line, and where two new sets of formwork dedicated to the new project have been installed.

The heavy congestion of the underlying area and the tight curvature radius of the viaducts have required special engineering solutions and the application of innovative construction methods. A particularly complex system was applied to temporary anchor between superstructure and piles.

The segments are launched by a launching beam specially designed and assembled to operate on this project. Launching activities take place mostly at night time to minimise traffic disruption.

In order to execute the project, Deal has supplied the following special equipment (worth in aggregate € 2.8 million):

_ two sets of formwork for segment prefabrication ‘balanced cantilever’ type

_ launching equipment set_ special accessories for expansion joints and pile-head

segments

Rizzani de Eccher / Deal. Focus 3

State Road 826Palmetto Expressway

Miami(Florida - USA)

Client: Florida Department of TransportationCommunity Condotte de Moya JV LLC

contract amount 38,000,000

start of segment prefabrication activities April 2011

start of segment launching activities September 2011

estimated completion of prefabrication August 2013

estimated completion of launching May 2014

total length of viaducts 2,365 m

width 14 m

minimum curvature radius 180 m

total number of prefabricated segments 783 total surface area of elevated decks 32,200 m2

concrete poured 19,000 m3

steel 2,000 tons

post-tensioning steel strands 960 tons

44

MANAGEMENT REPORT

4747

Economic and financial position

The consolidated financial statements for the accounting

period ending on 31 December 2011 show total revenues

(or value of production) of € 355.5 million (as opposed to

€ 482.6 million in FY2010), EBITDA of € 32.7 million (it was

€ 36.0 million in FY2010) and net profit of € 14.7 million

(against € 13.5 million in FY2010).

In the face of a sharp reduction in revenues (or value of

production), which was down 26.4%, the Group posted a

moderate reduction in operating profit (EBITDA) combined

with a slight improvement in net profit. This is a result that

bears testimony to Group’s ability to adjust its cost base in

relation to changes in demand deriving from such factors as

political upheavals and adverse macroeconomic conditions.

Uncertainty in the markets where the Group operates

has caused investment expenditure to stall. Tough

conditions in the construction market were exacerbated

in the second half of the financial year by the sudden, as

much as unpredictable, crisis that hit Eurozone financial

markets particularly hard. This had a significant impact

on the banking sectors and public finances of the weaker

countries of the Southern border of Eurozone, which face

mounting public debt, slowing GDP growth and rising

budget deficits.

Governments have dealt with the emergency primarily

by slashing spending and increasing taxes, wiping out