68

GST for Hospitality Industry – Practical Aspects in Implementation CA KURESH S KAGALWALA [email protected] +91 98201 69660 +91 22 43441717

| Date post: | 24-Jul-2018 |

| Category: |

Documents |

| Upload: | duongtuyen |

| View: | 221 times |

| Download: | 0 times |

GST for Hospitality Industry – Practical Aspects in

Implementation

CA KURESH S KAGALWALA [email protected]

+91 98201 69660

+91 22 43441717

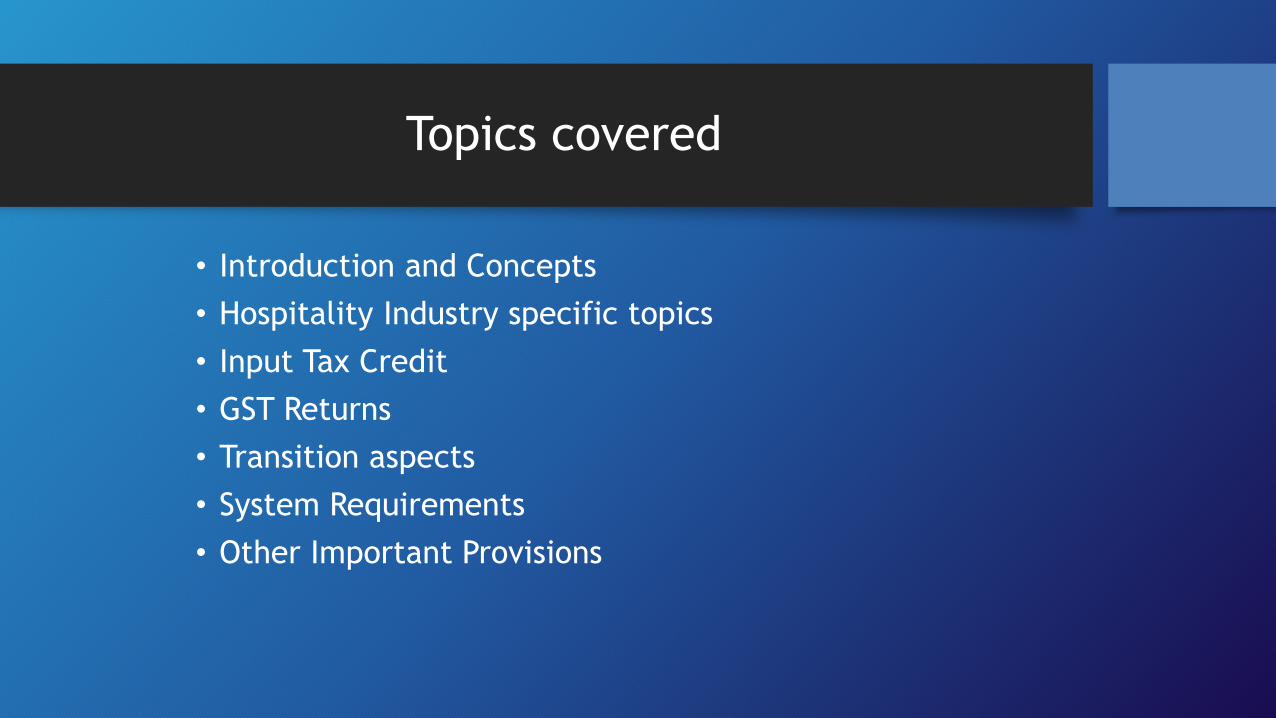

Topics covered

• Introduction and Concepts

• Hospitality Industry specific topics

• Input Tax Credit

• GST Returns

• Transition aspects

• System Requirements

• Other Important Provisions

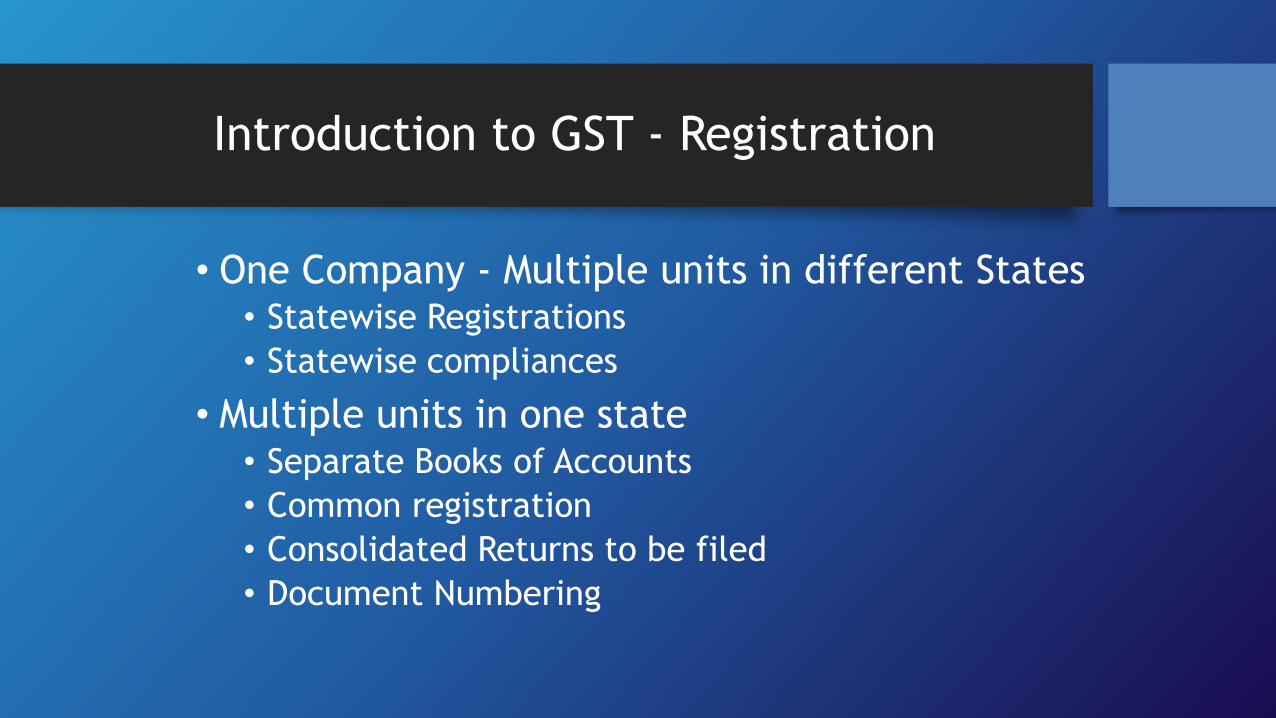

Introduction to GST - Registration

• One Company - Multiple units in different States • Statewise Registrations

• Statewise compliances

• Multiple units in one state • Separate Books of Accounts

• Common registration

• Consolidated Returns to be filed

• Document Numbering

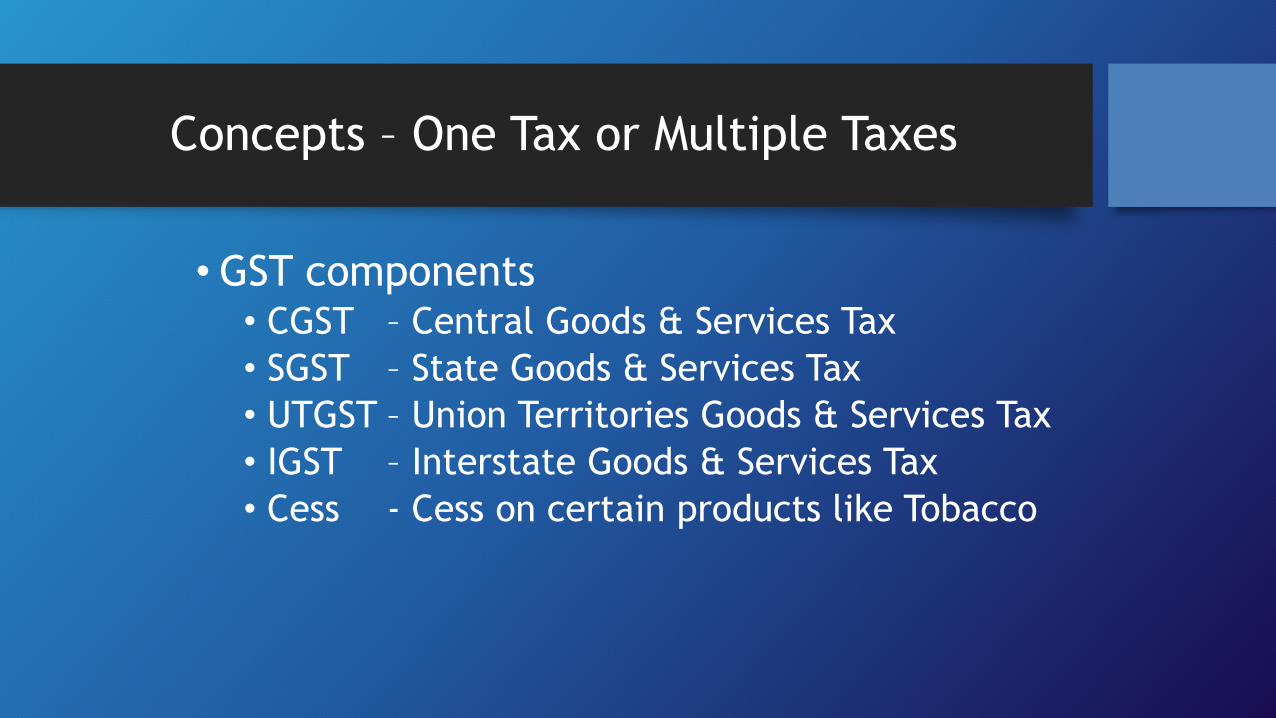

Concepts – One Tax or Multiple Taxes

• GST components • CGST – Central Goods & Services Tax

• SGST – State Goods & Services Tax

• UTGST – Union Territories Goods & Services Tax

• IGST – Interstate Goods & Services Tax

• Cess - Cess on certain products like Tobacco

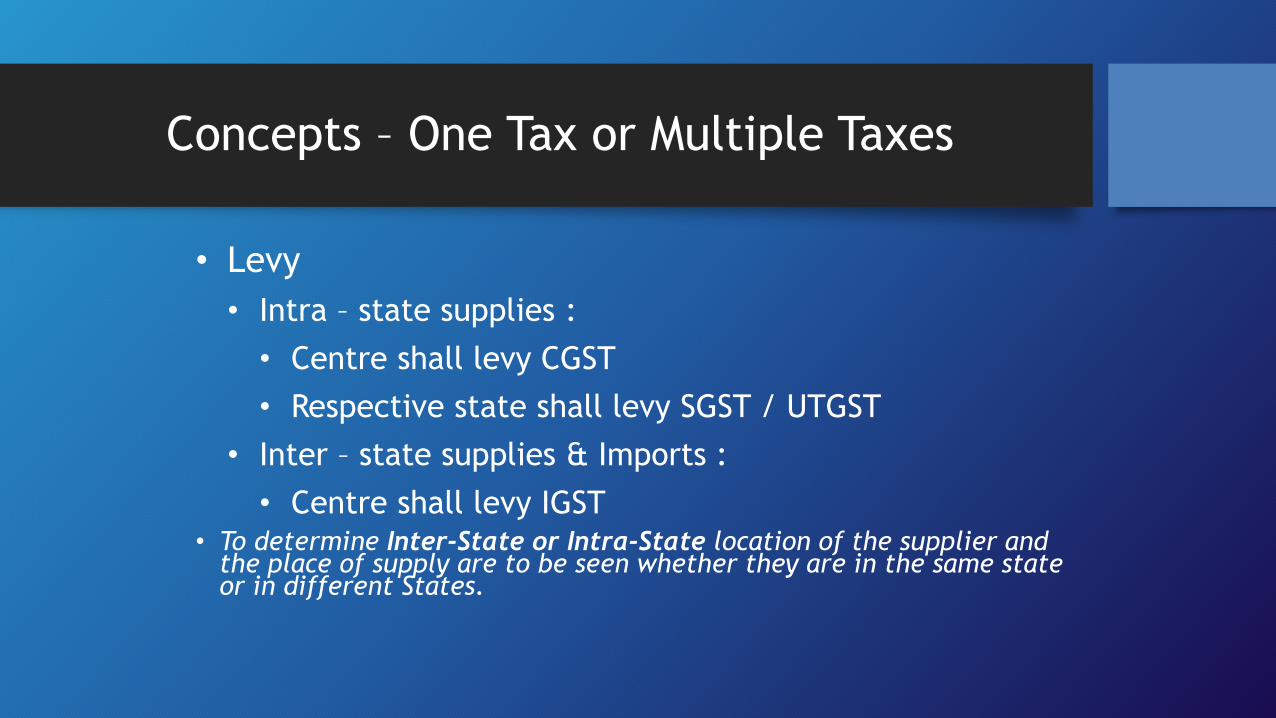

Concepts – One Tax or Multiple Taxes

• Levy

• Intra – state supplies :

• Centre shall levy CGST

• Respective state shall levy SGST / UTGST

• Inter – state supplies & Imports :

• Centre shall levy IGST • To determine Inter-State or Intra-State location of the supplier and

the place of supply are to be seen whether they are in the same state or in different States.

Hospitality Industry specific topics – SALES

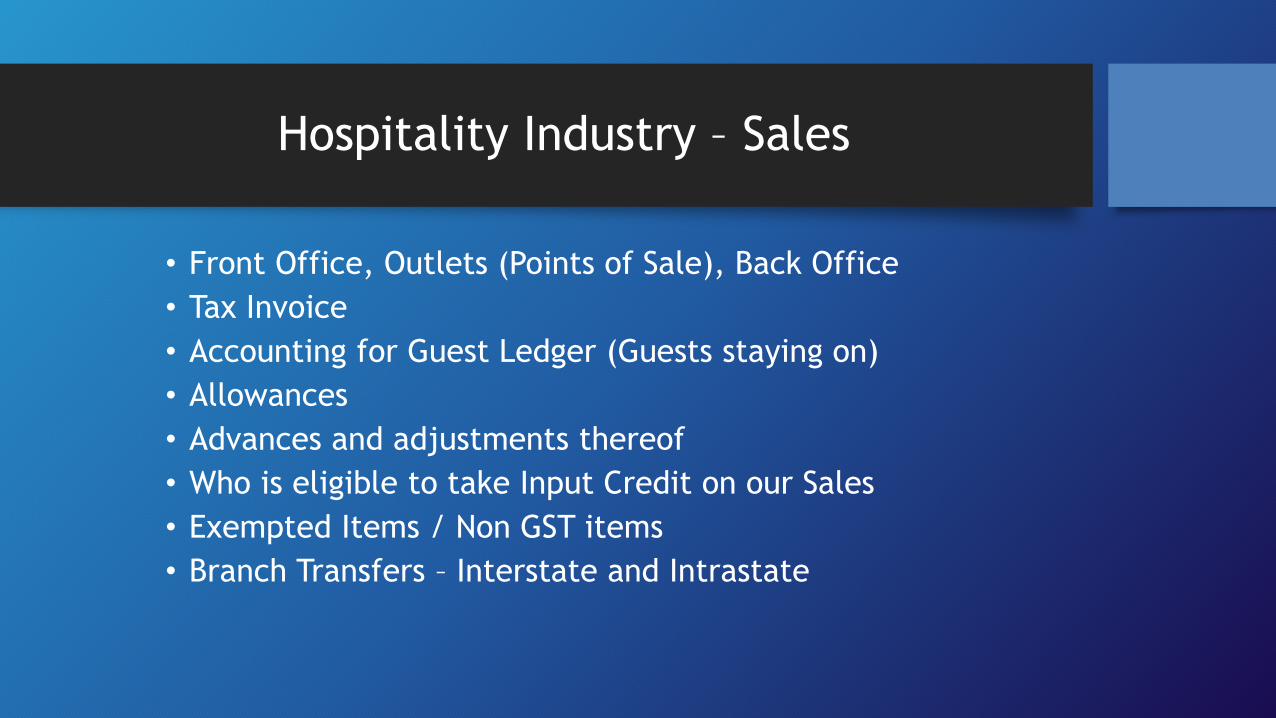

Hospitality Industry – Sales

• Front Office, Outlets (Points of Sale), Back Office

• Tax Invoice

• Accounting for Guest Ledger (Guests staying on)

• Allowances

• Advances and adjustments thereof

• Who is eligible to take Input Credit on our Sales

• Exempted Items / Non GST items

• Branch Transfers – Interstate and Intrastate

Hospitality Industry - Sales

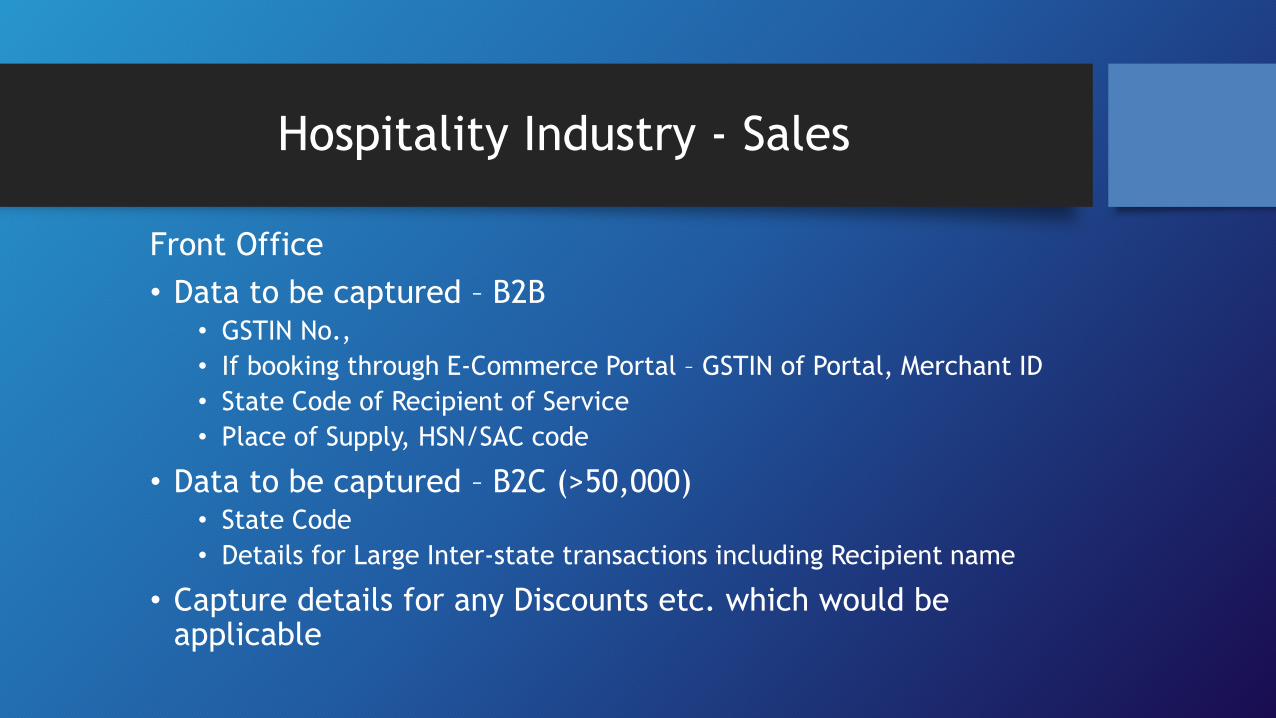

Front Office

• Data to be captured – B2B • GSTIN No.,

• If booking through E-Commerce Portal – GSTIN of Portal, Merchant ID

• State Code of Recipient of Service

• Place of Supply, HSN/SAC code

• Data to be captured – B2C (>50,000) • State Code

• Details for Large Inter-state transactions including Recipient name

• Capture details for any Discounts etc. which would be applicable

Hospitality Industry - Sales

Front Office

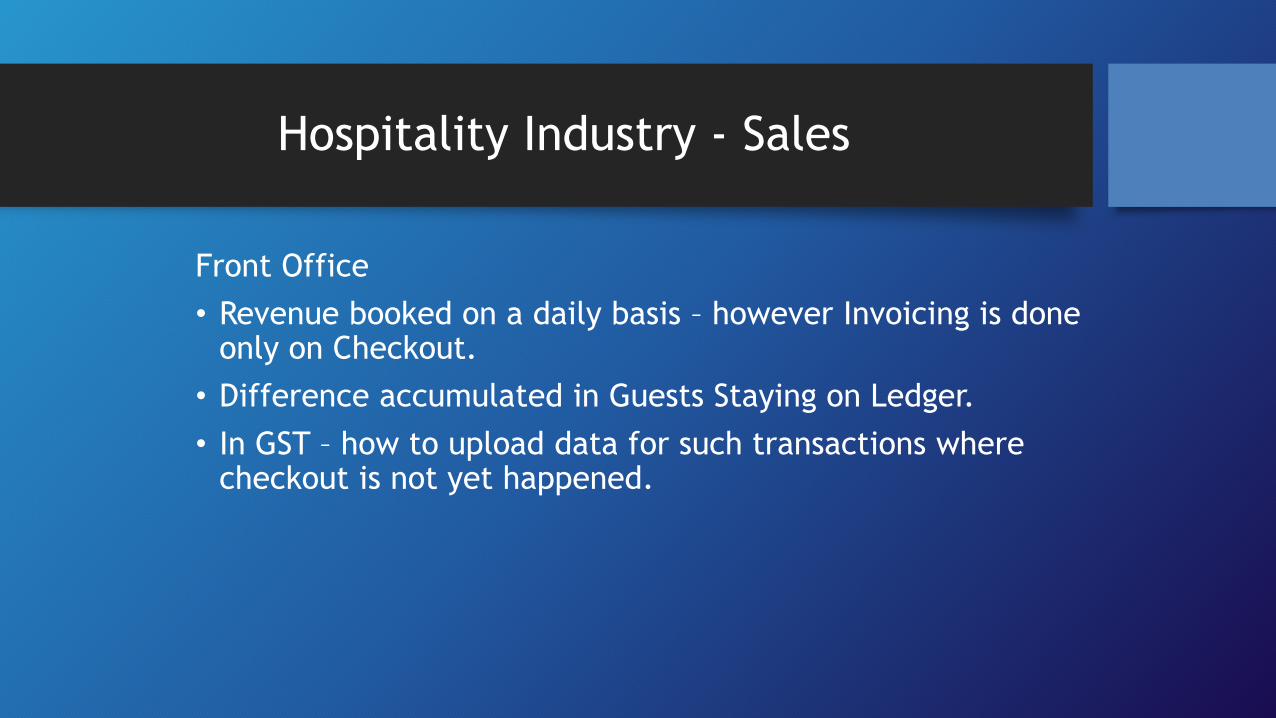

• Revenue booked on a daily basis – however Invoicing is done only on Checkout.

• Difference accumulated in Guests Staying on Ledger.

• In GST – how to upload data for such transactions where checkout is not yet happened.

Hospitality Industry - Sales

Outlets Sales (Point of Sales)

• Invoice nos to be unique – for each POS within one GST Regn. No.

• HSN/SAC codes to be printed on the Invoice

• Differentiate between Resident Guests and Non-Resident Guests

• Differentiate between B2B and B2C

• Accounting for Plans including Lodging and Meals

• F&B not eligible for Input Tax Credit

• Banquets – Data Capturing – GSTIN / Name

Hospitality Industry - SALES

Back Office

• Rental Income

• Scrap Sales

• Allowances

• Credit notes / Debit Notes

• Membership / Subscription Fees

• Penalties / Late Fees

Hospitality Industry - SALES

TAX INVOICE

• Only one Tax Invoice can be issued for a specific product / service

• Currently Invoice is made in POS even for In-house guests

• The same are again aggregated in the final check out bill

• For non-staying guests, GST Tax Invoice is mandatory.

• Options – Charge slip / Multiple Invoices in final statement of account.

Hospitality Industry - SALES

Accounting for Guest Ledger (Guests staying on)

• Currently Revenue is booked daily – however Invoice is made only on checkout.

• To balance the daily entry in the books, the difference is taken to Guest staying on or Guests Ledger.

• Since Invoice details are to be uploaded every month, what happens for a guest who is staying between 2 months

• Different Opinions and Options follow -

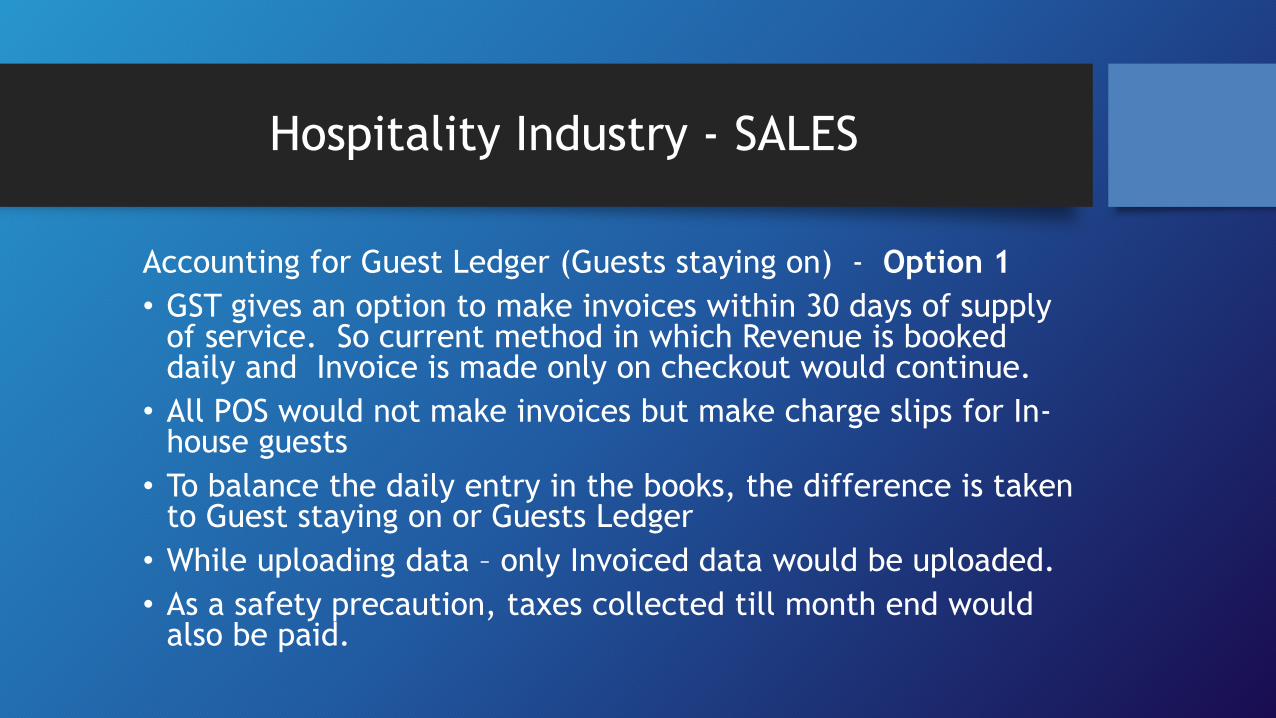

Hospitality Industry - SALES

Accounting for Guest Ledger (Guests staying on) - Option 1

• GST gives an option to make invoices within 30 days of supply of service. So current method in which Revenue is booked daily and Invoice is made only on checkout would continue.

• All POS would not make invoices but make charge slips for In-house guests

• To balance the daily entry in the books, the difference is taken to Guest staying on or Guests Ledger

• While uploading data – only Invoiced data would be uploaded.

• As a safety precaution, taxes collected till month end would also be paid.

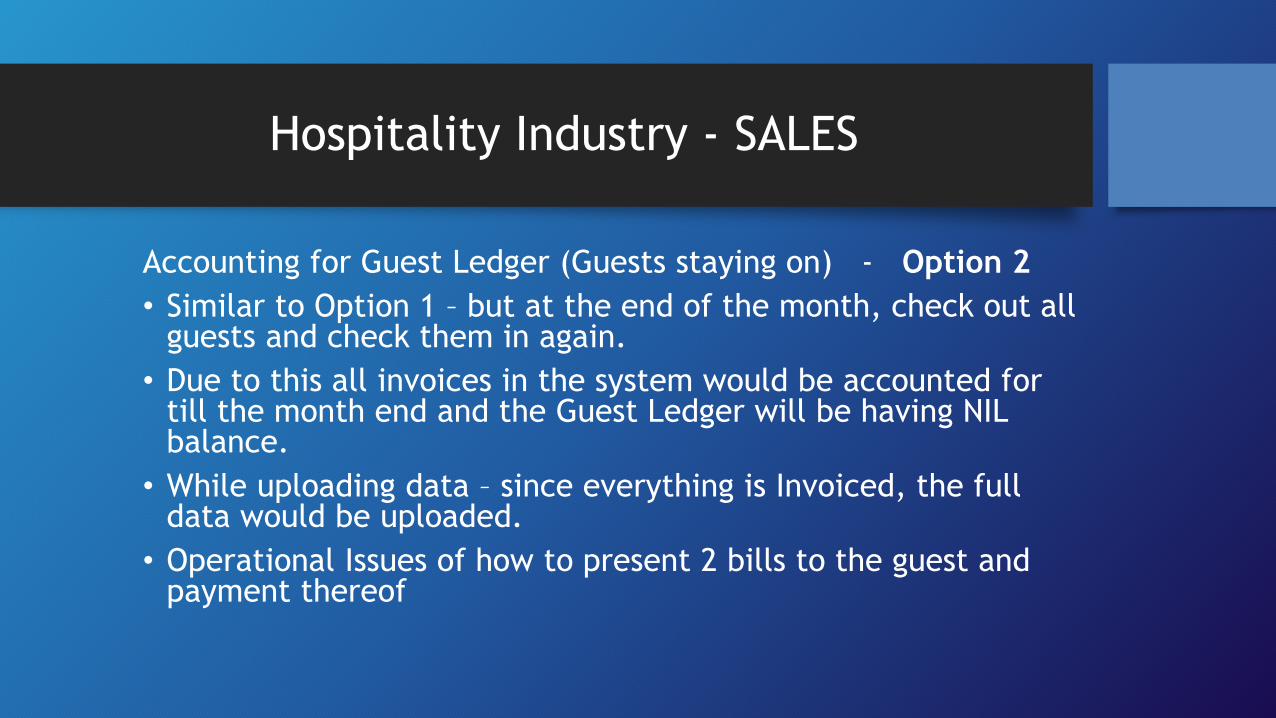

Hospitality Industry - SALES

Accounting for Guest Ledger (Guests staying on) - Option 2

• Similar to Option 1 – but at the end of the month, check out all guests and check them in again.

• Due to this all invoices in the system would be accounted for till the month end and the Guest Ledger will be having NIL balance.

• While uploading data – since everything is Invoiced, the full data would be uploaded.

• Operational Issues of how to present 2 bills to the guest and payment thereof

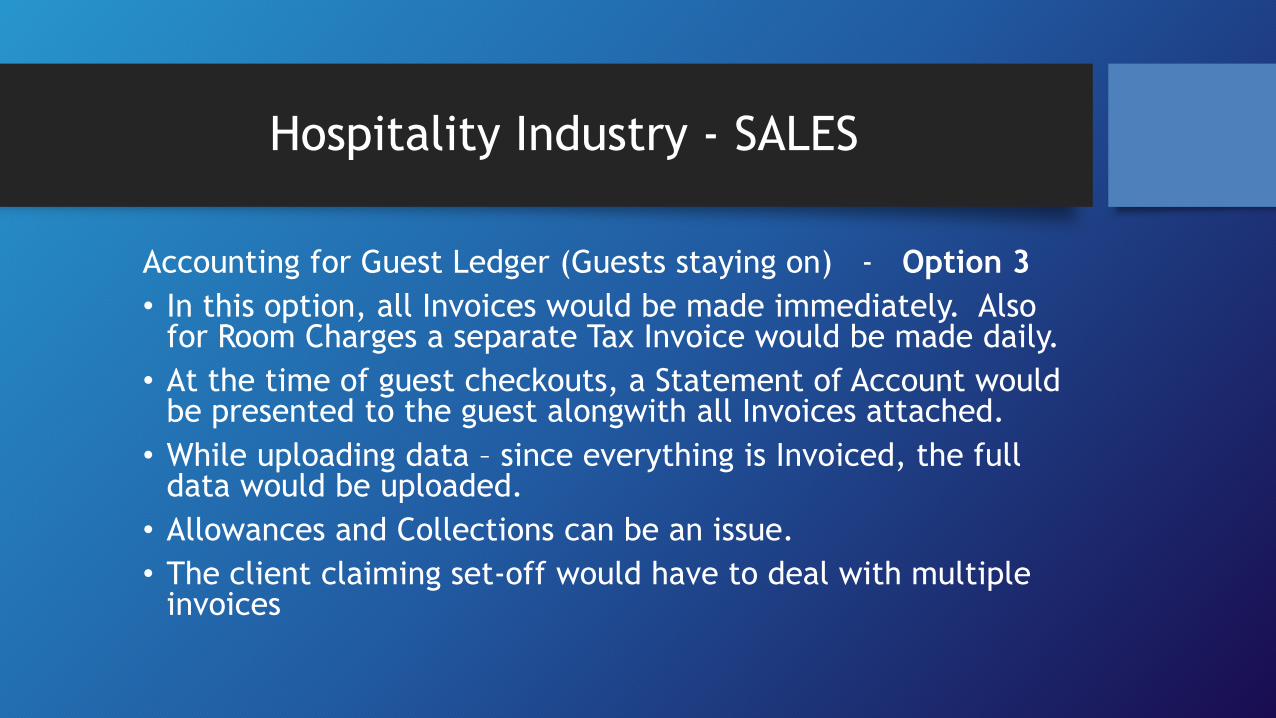

Hospitality Industry - SALES

Accounting for Guest Ledger (Guests staying on) - Option 3

• In this option, all Invoices would be made immediately. Also for Room Charges a separate Tax Invoice would be made daily.

• At the time of guest checkouts, a Statement of Account would be presented to the guest alongwith all Invoices attached.

• While uploading data – since everything is Invoiced, the full data would be uploaded.

• Allowances and Collections can be an issue.

• The client claiming set-off would have to deal with multiple invoices

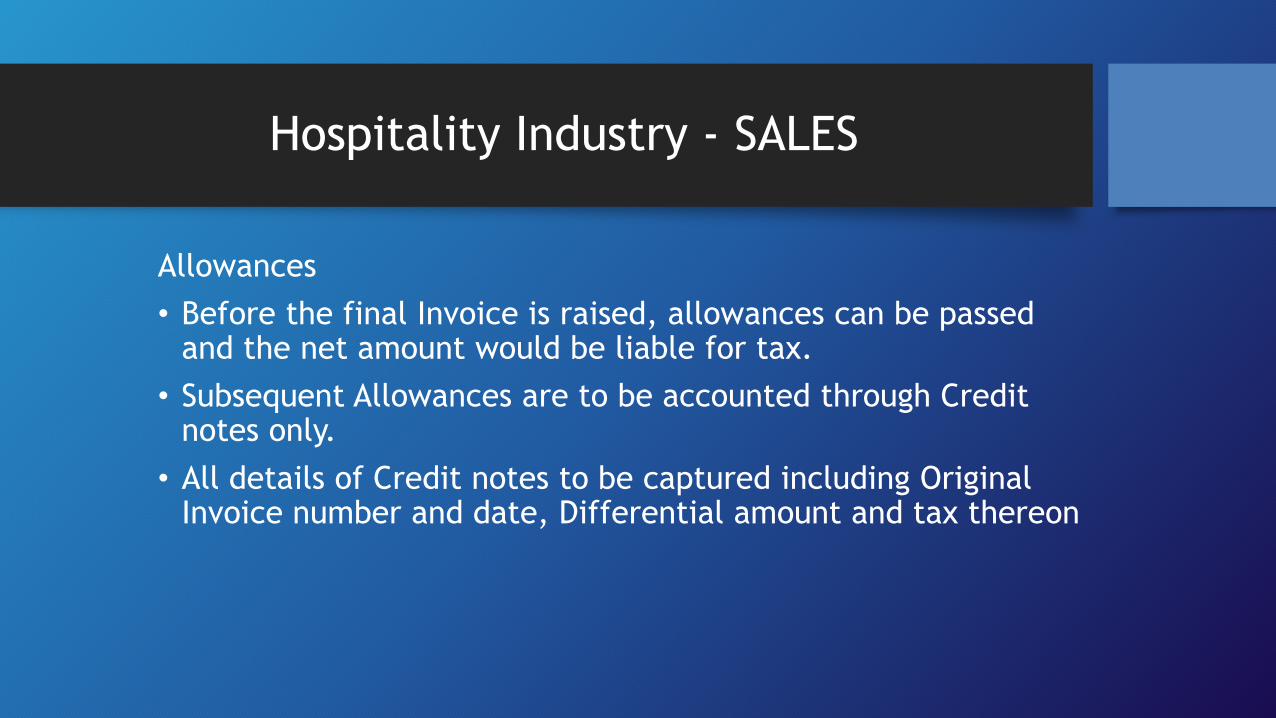

Hospitality Industry - SALES

Allowances

• Before the final Invoice is raised, allowances can be passed and the net amount would be liable for tax.

• Subsequent Allowances are to be accounted through Credit notes only.

• All details of Credit notes to be captured including Original Invoice number and date, Differential amount and tax thereon

Hospitality Industry - SALES

Advances

• All Advances received would have to be reported and the tax thereon to be offered for taxation

• The GSTN would generate a unique transaction id which would have to be updated in your system

• When subsequent Invoice is made and the advance is adjusted, the reporting of such adjustments (transaction id with Invoice no.) would have to be reported.

• How to take care if in the same month?

• What happens in case of refunds of advances – no current provision.

Hospitality Industry - Sales – Who can claim ITC?

• B2C

• Food Sales

• Rent a Cab

• B2B customers from outside the state

• So only B2B customers who are registered in the same state and who are staying in the hotel would be eligible.

• So the cost adds up to the end customer as he would not be able to take the Input Tax Credit.

Hospitality Industry - Sales

Exempted Items / Non GST items

• Reporting has to be done for the above too.

• Certain items are not covered under GST like Liqour, Petroleum products, electricity.

• Agricultural produce like Vegetables, Food grains are exempted.

Hospitality Industry specific topics – PURCHASES

Hospitality Industry – PURCHASES

• Supplier Types – GST Compliant, Composite, Unregistered, Imports

• Purchase Types – Normal Goods, Exempt Goods, Zero rate goods and Non-GST supplies

• Interstate or Intrastate.

• Composite and mixed supplies.

• Payments to be done within 6 months.

• Input Tax Credit conditions and calculation.

Hospitality Industry – PURCHASES

Supplier Types - GST Compliant

• Preferred to have such vendors as Input Tax Credit would be available from them.

• Proper Invoices would have to be procured from them containing our GSTIN no. mentioned on them. Also other details like HSN / SAC code, tax breakups etc.

• GSTIN will also issue Supplier Ratings from time to time.

Hospitality Industry – PURCHASES

Supplier Types – Composite

• Composite Suppliers would be those whose annual turnover in the preceding financial year is less than Rs. 50 lacs.

• These suppliers shall pay tax as a percentage of the turnover and they shall not collect any tax from their customers.

• They shall not be eligible for Input Tax Credit on their purchases.

• Interstate Suppliers or those supplying through ecommerce operators shall not be eligible for composition scheme

Hospitality Industry – PURCHASES

Supplier Types – Unregistered

• In case of receipt of supply from an unregistered person, the registered person who is receiving goods or services shall be liable to pay tax under reverse charge mechanism.

• The supplier would have to classify the item purchased as per the HSN / SAC code, determine the tax thereon, and pay the same.

• Details of such supplier – name and address would also have to be captured for upload in the returns

Hospitality Industry – PURCHASES

Supplier Types – Imports

• Imports of Goods and Services will be treated as inter-state supplies and IGST will be levied on import of goods and services into the country.

• The incidence of tax will follow the destination principle and the tax revenue in case of SGST will accrue to the State where the imported goods and services are consumed.

• Full and complete set-off will be available on the GST paid on import on goods and services.

Hospitality Industry – PURCHASES

Payments to be done within 6 months

• Details of all invoices to be submitted where payment is not made within 6 months.

• The input tax credit claimed earlier on that invoice would be reversed and interest would also be charged on the same

• Later when the payment for the same is made, the tax credit can again be availed off.

• The systems should be able to keep track of such cases and proper uploads made monthly.

Input Tax Credit

Input Tax Credit - Conditions for allowability

Input Tax Credit can be availed only if:

• It is a B2B transaction

• Purchaser possesses Tax Invoice, Debit note, Bill of Entry, ISD Invoice or Invoice issued by service recipient under Reverse charge mechanism.

• Prescribed particulars are mentioned on the Invoice

• Goods/Services have been received by such person

• Tax charged in respect to such supply has been actually paid to the Government.

• Seller has uploaded the relevant information in his returns

• Purchaser matches the corresponding entries in his Returns

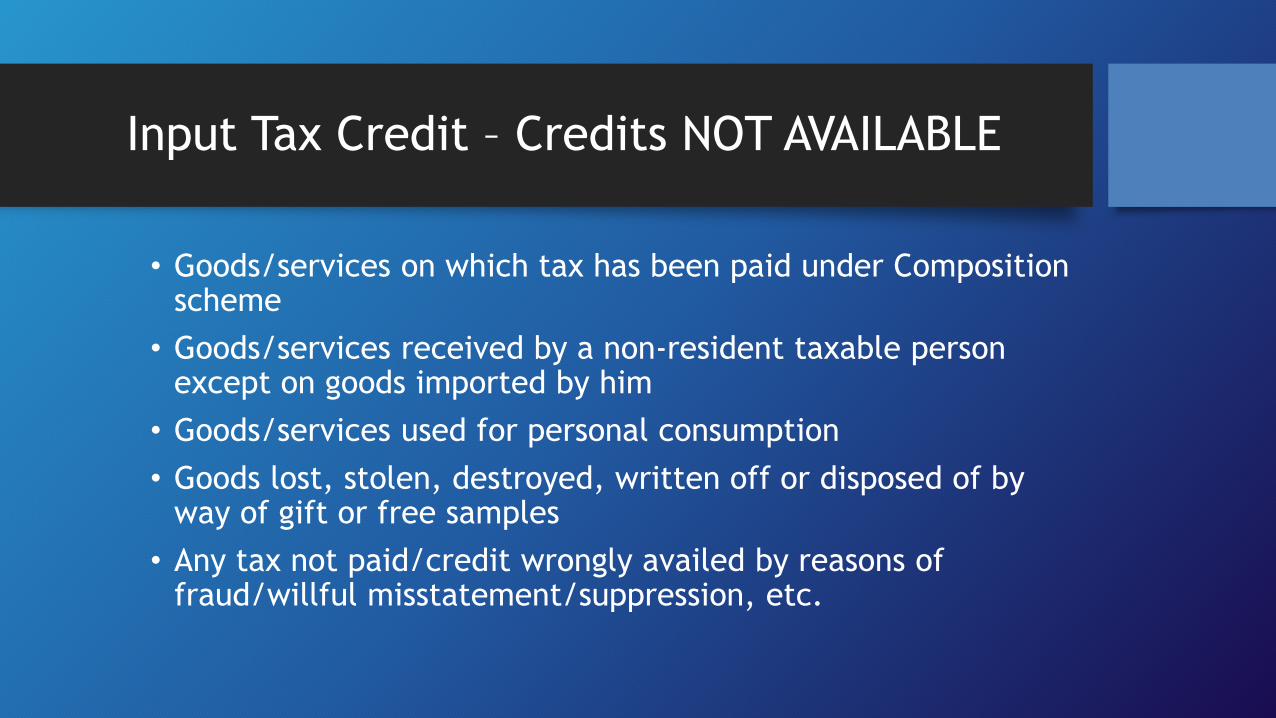

Input Tax Credit – Credits NOT AVAILABLE

• Motor vehicles and other conveyances, except when they are used for providing the taxable supplies of further supply of vehicles/conveyances

• Goods/services provided in relation to food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery except when used for providing similar taxable supplies

• Membership of club, health and fitness center

• Goods/services received for construction of immovable property (excluding plant & machinery) on own account

Input Tax Credit – Credits NOT AVAILABLE

• Goods/services on which tax has been paid under Composition scheme

• Goods/services received by a non-resident taxable person except on goods imported by him

• Goods/services used for personal consumption

• Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples

• Any tax not paid/credit wrongly availed by reasons of fraud/willful misstatement/suppression, etc.

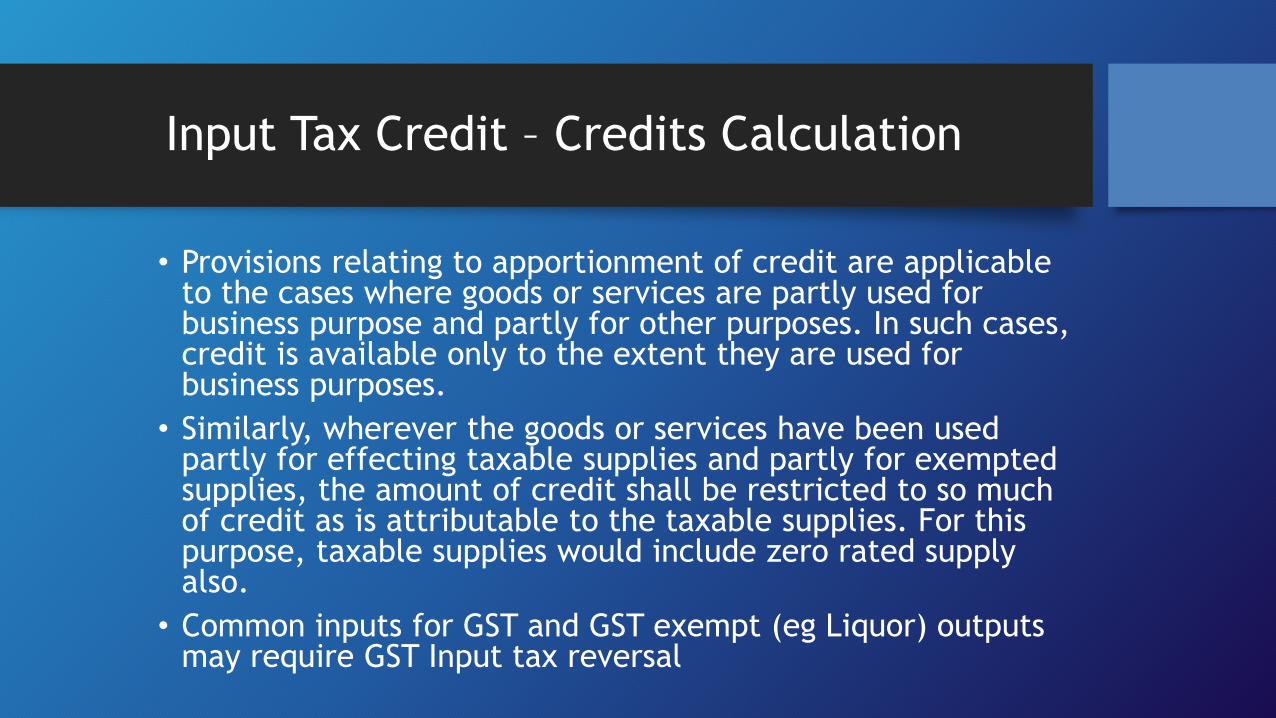

Input Tax Credit – Credits Calculation

• Provisions relating to apportionment of credit are applicable to the cases where goods or services are partly used for business purpose and partly for other purposes. In such cases, credit is available only to the extent they are used for business purposes.

• Similarly, wherever the goods or services have been used partly for effecting taxable supplies and partly for exempted supplies, the amount of credit shall be restricted to so much of credit as is attributable to the taxable supplies. For this purpose, taxable supplies would include zero rated supply also.

• Common inputs for GST and GST exempt (eg Liquor) outputs may require GST Input tax reversal

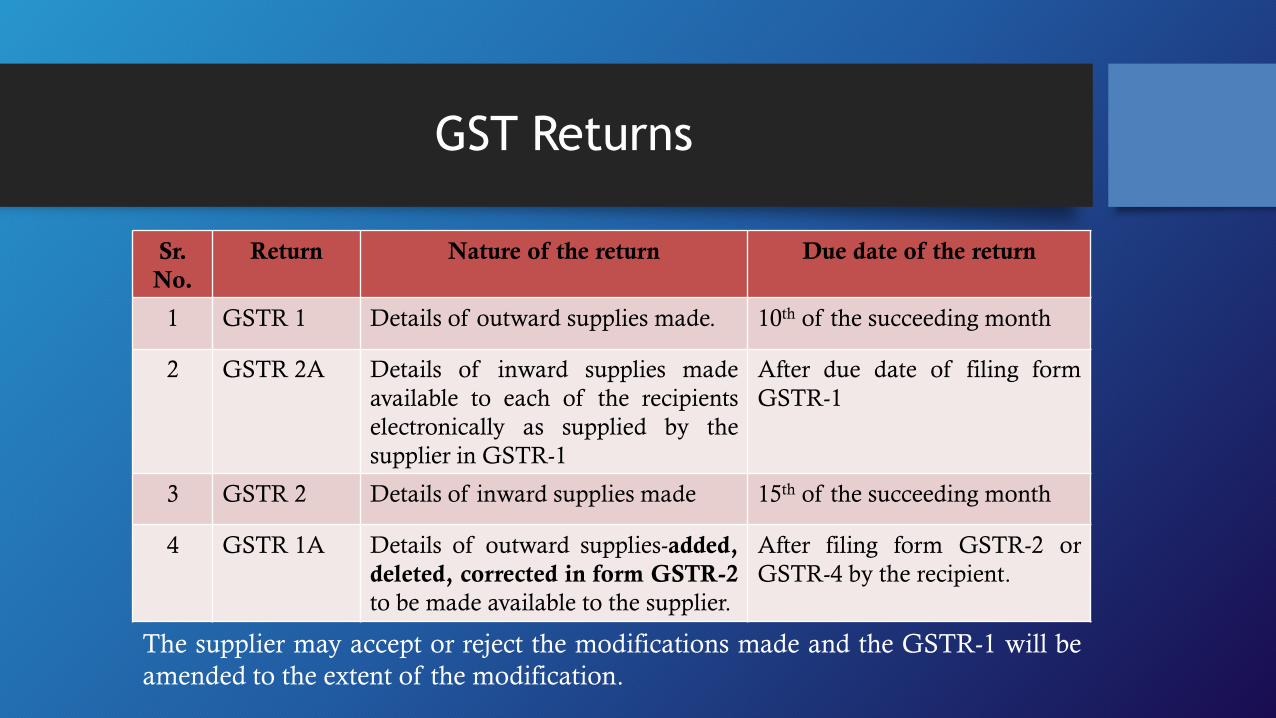

GST Returns

Sr.

No.

Return Nature of the return Due date of the return

1 GSTR 1 Details of outward supplies made. 10th of the succeeding month

2 GSTR 2A Details of inward supplies made

available to each of the recipients

electronically as supplied by the

supplier in GSTR-1

After due date of filing form

GSTR-1

3 GSTR 2 Details of inward supplies made 15th of the succeeding month

4 GSTR 1A Details of outward supplies-added,

deleted, corrected in form GSTR-2

to be made available to the supplier.

After filing form GSTR-2 or

GSTR-4 by the recipient.

The supplier may accept or reject the modifications made and the GSTR-1 will be

amended to the extent of the modification.

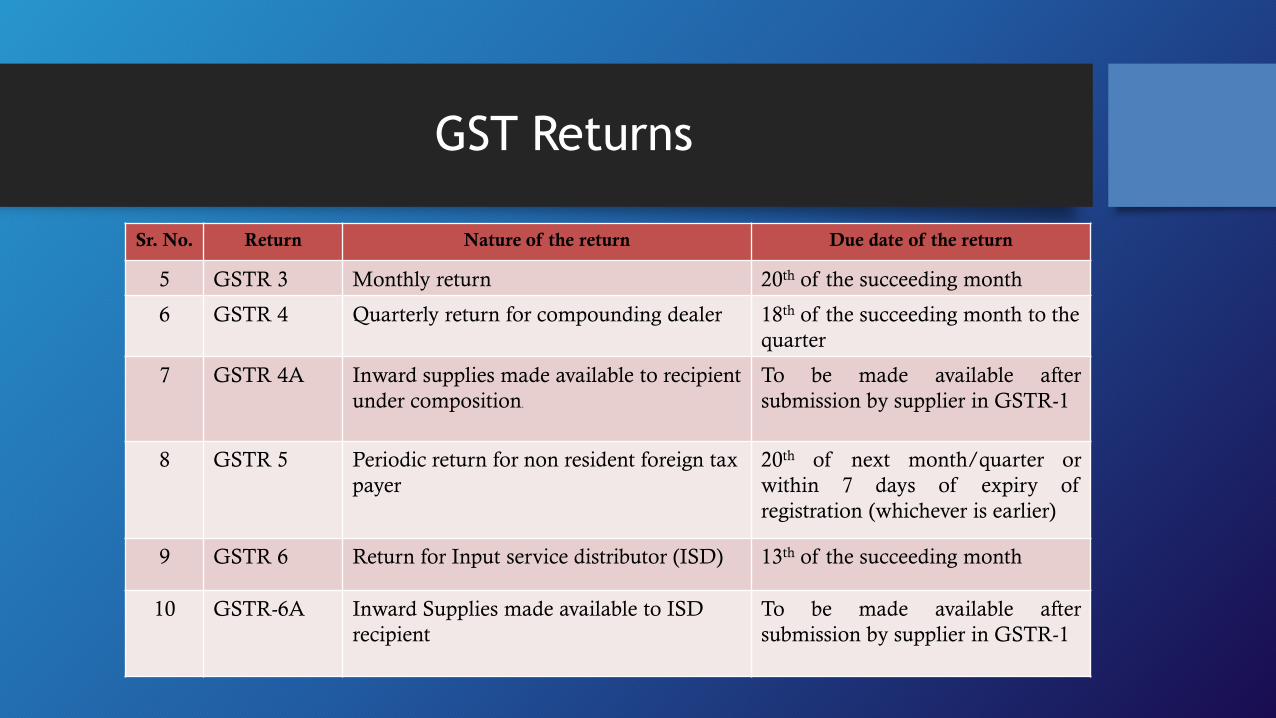

GST Returns

Sr. No. Return Nature of the return Due date of the return

5 GSTR 3 Monthly return 20th of the succeeding month

6 GSTR 4 Quarterly return for compounding dealer 18th of the succeeding month to the

quarter

7 GSTR 4A Inward supplies made available to recipient

under composition.

To be made available after

submission by supplier in GSTR-1

8 GSTR 5 Periodic return for non resident foreign tax

payer

20th of next month/quarter or

within 7 days of expiry of

registration (whichever is earlier)

9 GSTR 6 Return for Input service distributor (ISD) 13th of the succeeding month

10 GSTR-6A Inward Supplies made available to ISD

recipient

To be made available after

submission by supplier in GSTR-1

GST Returns

Sr. No. Return Nature of the return Due date of the return

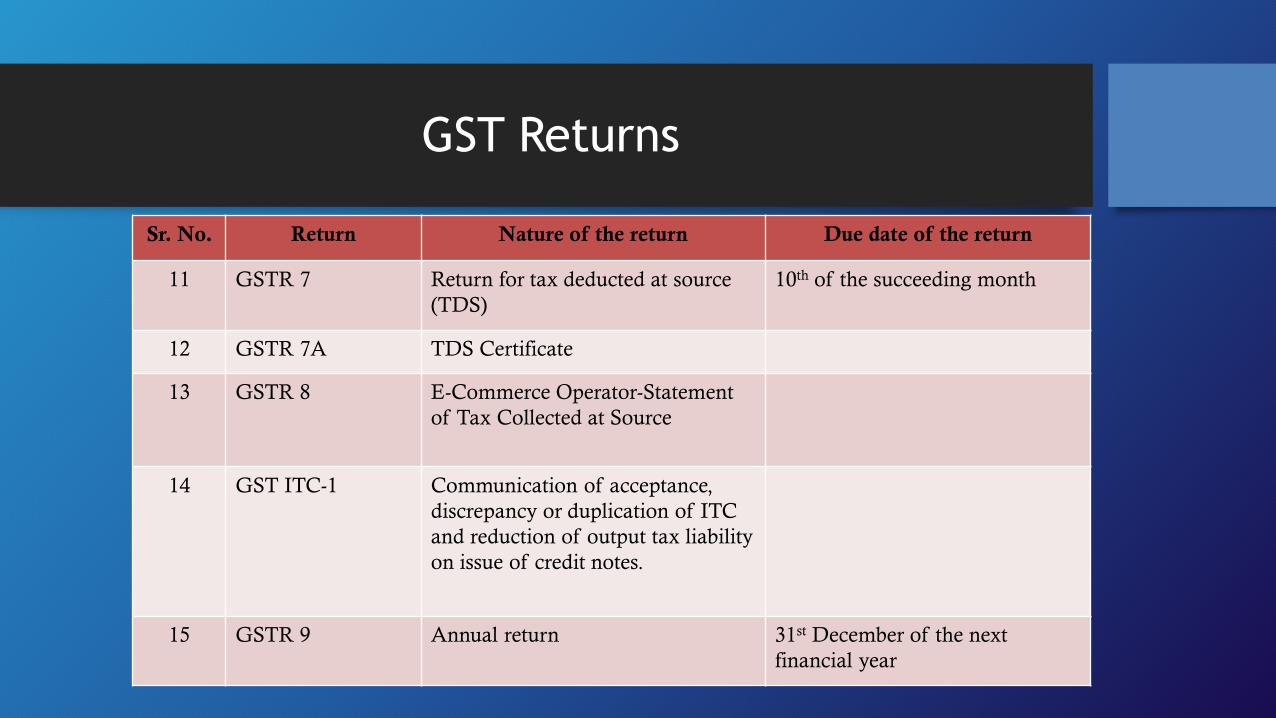

11 GSTR 7 Return for tax deducted at source

(TDS)

10th of the succeeding month

12 GSTR 7A TDS Certificate

13 GSTR 8 E-Commerce Operator-Statement

of Tax Collected at Source

14 GST ITC-1 Communication of acceptance,

discrepancy or duplication of ITC

and reduction of output tax liability

on issue of credit notes.

15 GSTR 9 Annual return 31st December of the next

financial year

GST Returns

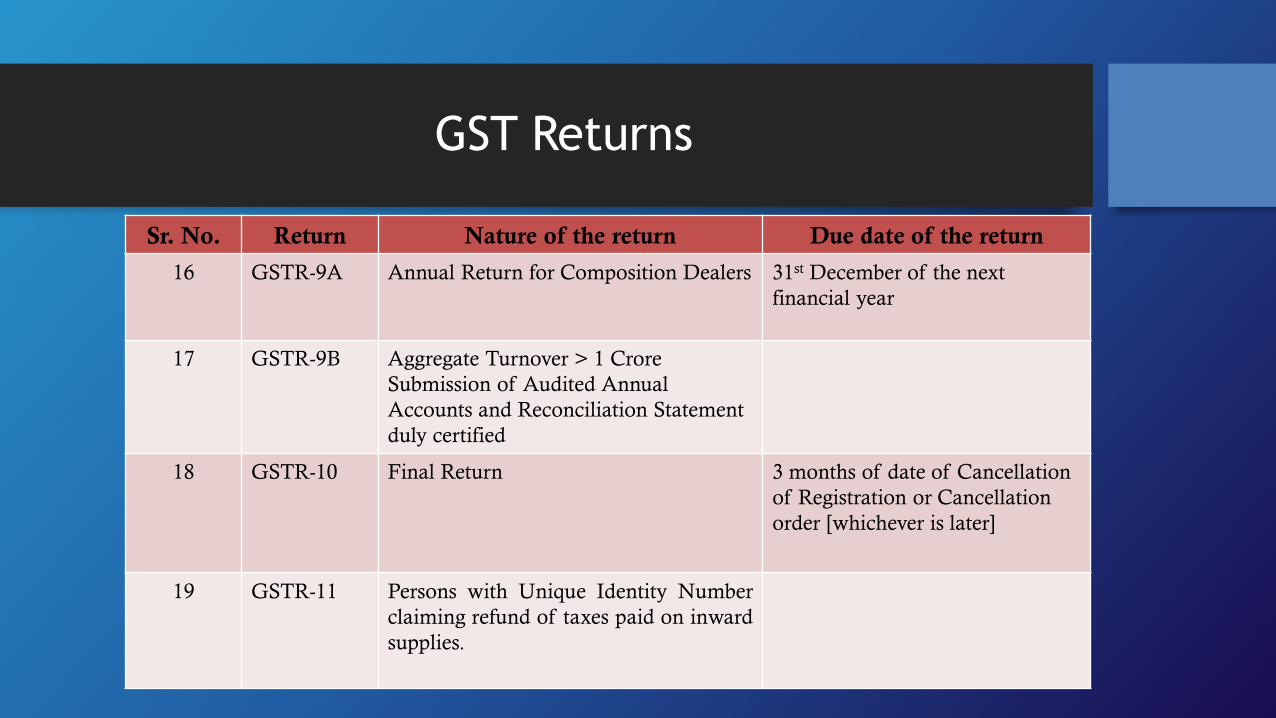

Sr. No. Return Nature of the return Due date of the return

16 GSTR-9A Annual Return for Composition Dealers 31st December of the next

financial year

17 GSTR-9B Aggregate Turnover > 1 Crore

Submission of Audited Annual

Accounts and Reconciliation Statement

duly certified

18 GSTR-10 Final Return 3 months of date of Cancellation

of Registration or Cancellation

order [whichever is later]

19 GSTR-11 Persons with Unique Identity Number

claiming refund of taxes paid on inward

supplies.

GST Returns

GST Returns

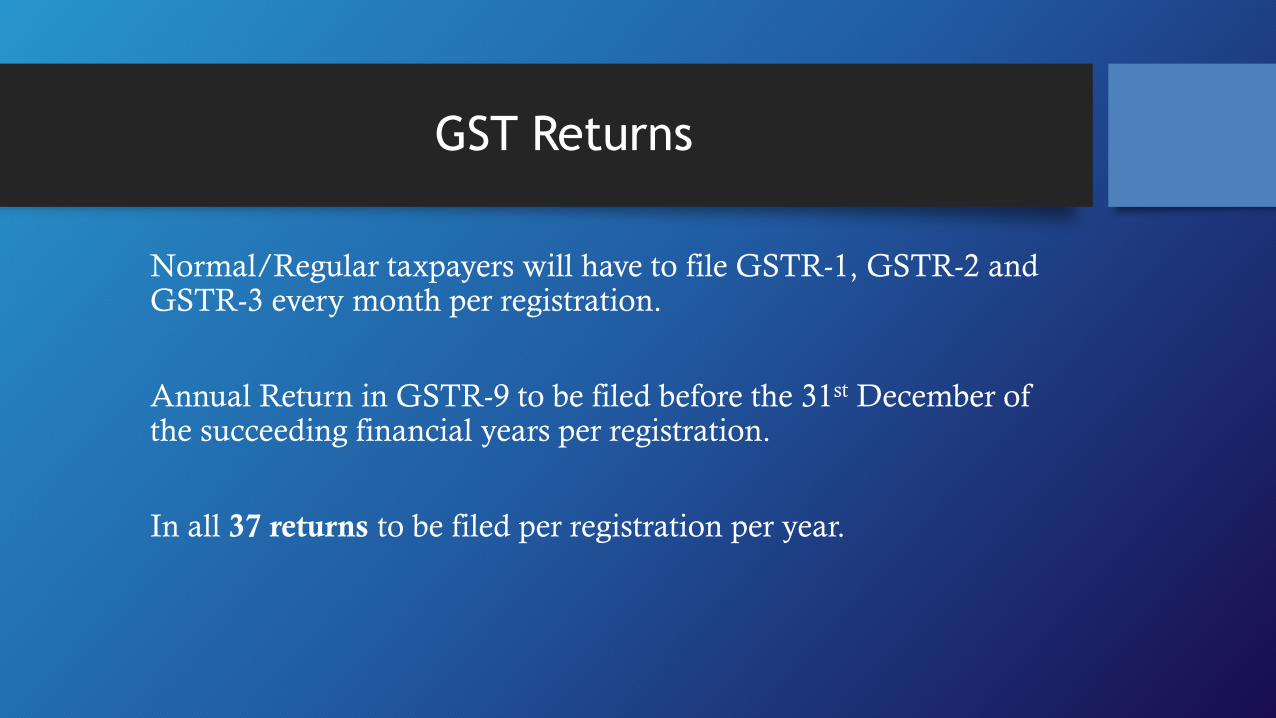

Normal/Regular taxpayers will have to file GSTR-1, GSTR-2 and GSTR-3 every month per registration.

Annual Return in GSTR-9 to be filed before the 31st December of the succeeding financial years per registration.

In all 37 returns to be filed per registration per year.

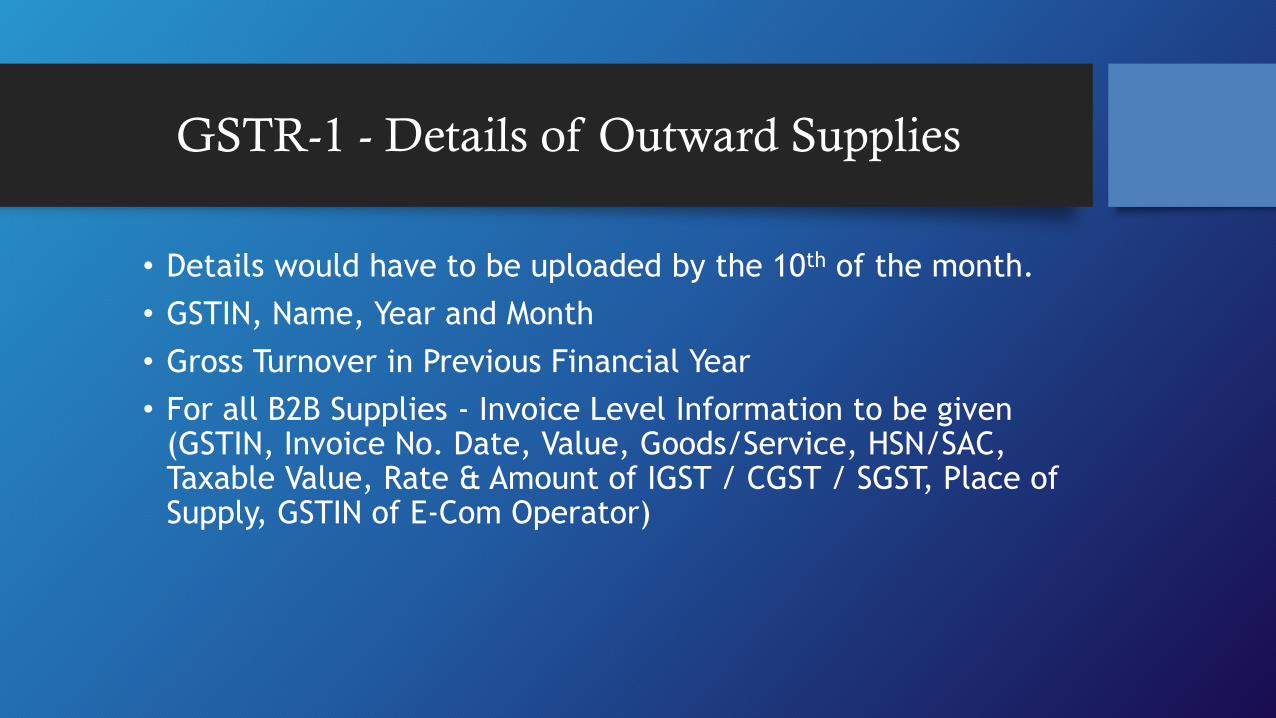

GSTR-1 - Details of Outward Supplies

• Details would have to be uploaded by the 10th of the month.

• GSTIN, Name, Year and Month

• Gross Turnover in Previous Financial Year

• For all B2B Supplies - Invoice Level Information to be given (GSTIN, Invoice No. Date, Value, Goods/Service, HSN/SAC, Taxable Value, Rate & Amount of IGST / CGST / SGST, Place of Supply, GSTIN of E-Com Operator)

GSTR-1 - Contents

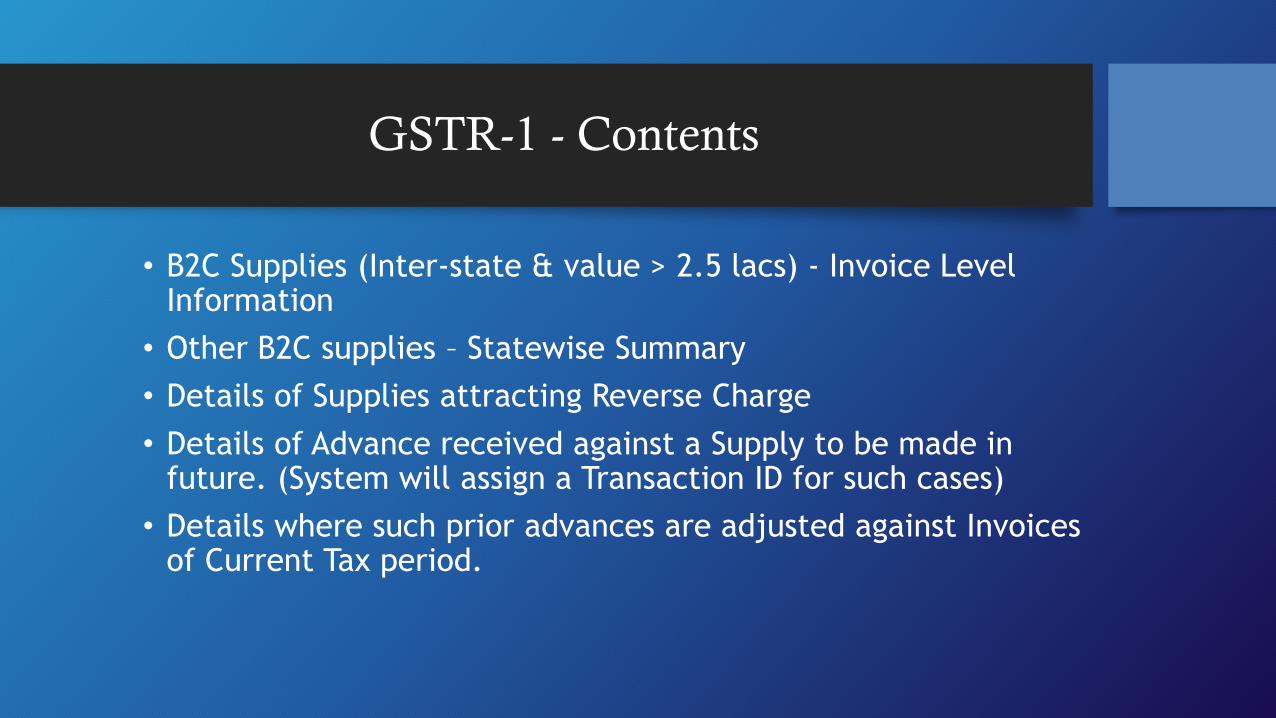

• B2C Supplies (Inter-state & value > 2.5 lacs) - Invoice Level Information

• Other B2C supplies – Statewise Summary

• Details of Supplies attracting Reverse Charge

• Details of Advance received against a Supply to be made in future. (System will assign a Transaction ID for such cases)

• Details where such prior advances are adjusted against Invoices of Current Tax period.

GSTR-1 - Contents

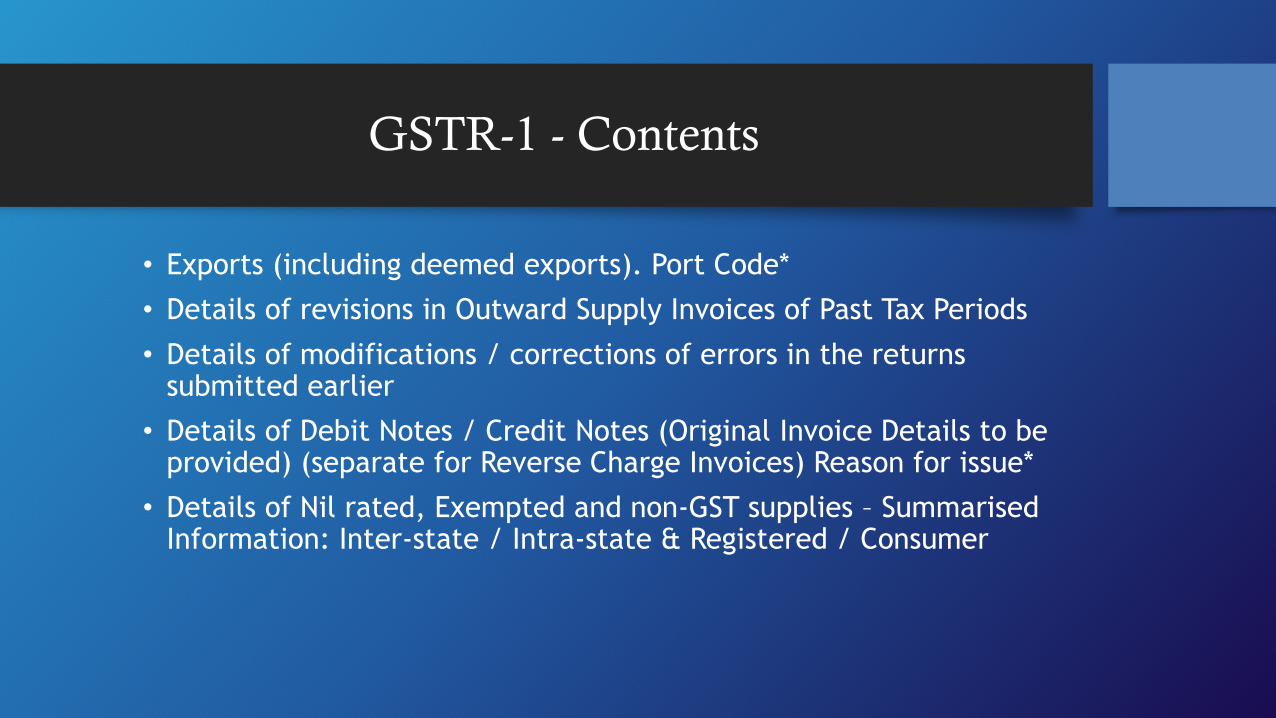

• Exports (including deemed exports). Port Code*

• Details of revisions in Outward Supply Invoices of Past Tax Periods

• Details of modifications / corrections of errors in the returns submitted earlier

• Details of Debit Notes / Credit Notes (Original Invoice Details to be provided) (separate for Reverse Charge Invoices) Reason for issue*

• Details of Nil rated, Exempted and non-GST supplies – Summarised Information: Inter-state / Intra-state & Registered / Consumer

GSTR-1 - Contents

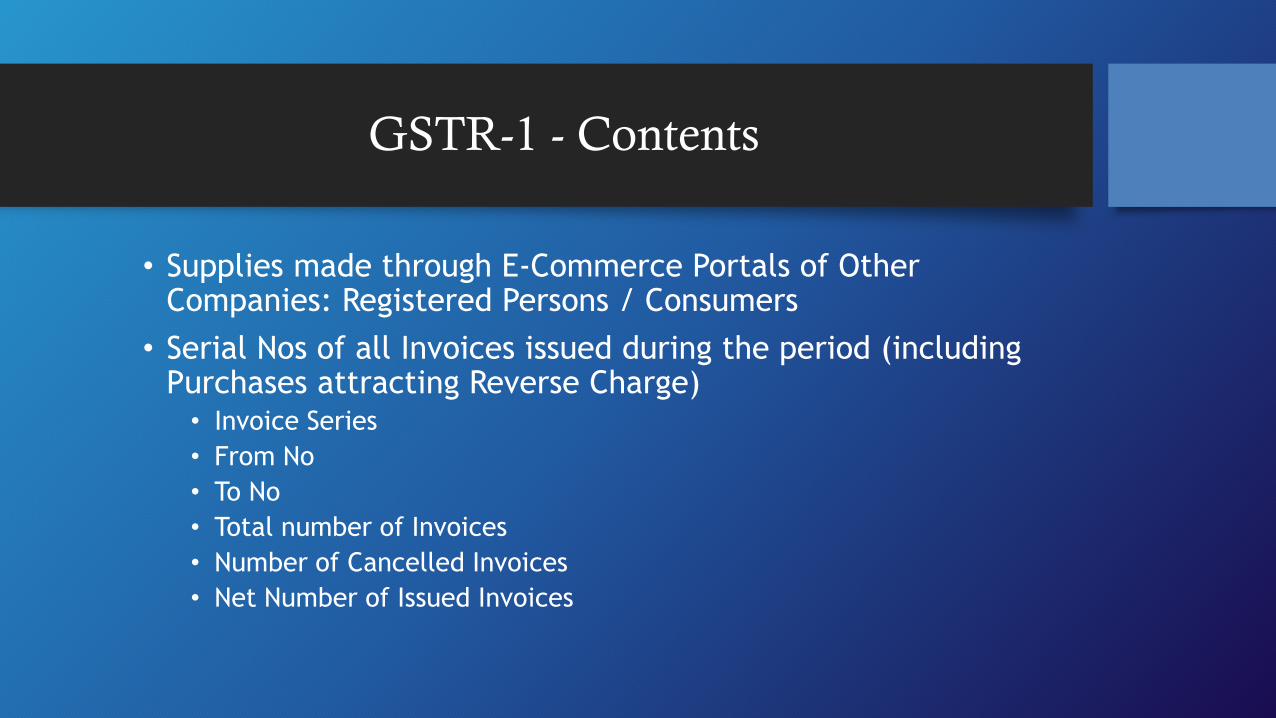

• Supplies made through E-Commerce Portals of Other Companies: Registered Persons / Consumers

• Serial Nos of all Invoices issued during the period (including Purchases attracting Reverse Charge) • Invoice Series

• From No

• To No

• Total number of Invoices

• Number of Cancelled Invoices

• Net Number of Issued Invoices

GSTR-1 - Contents

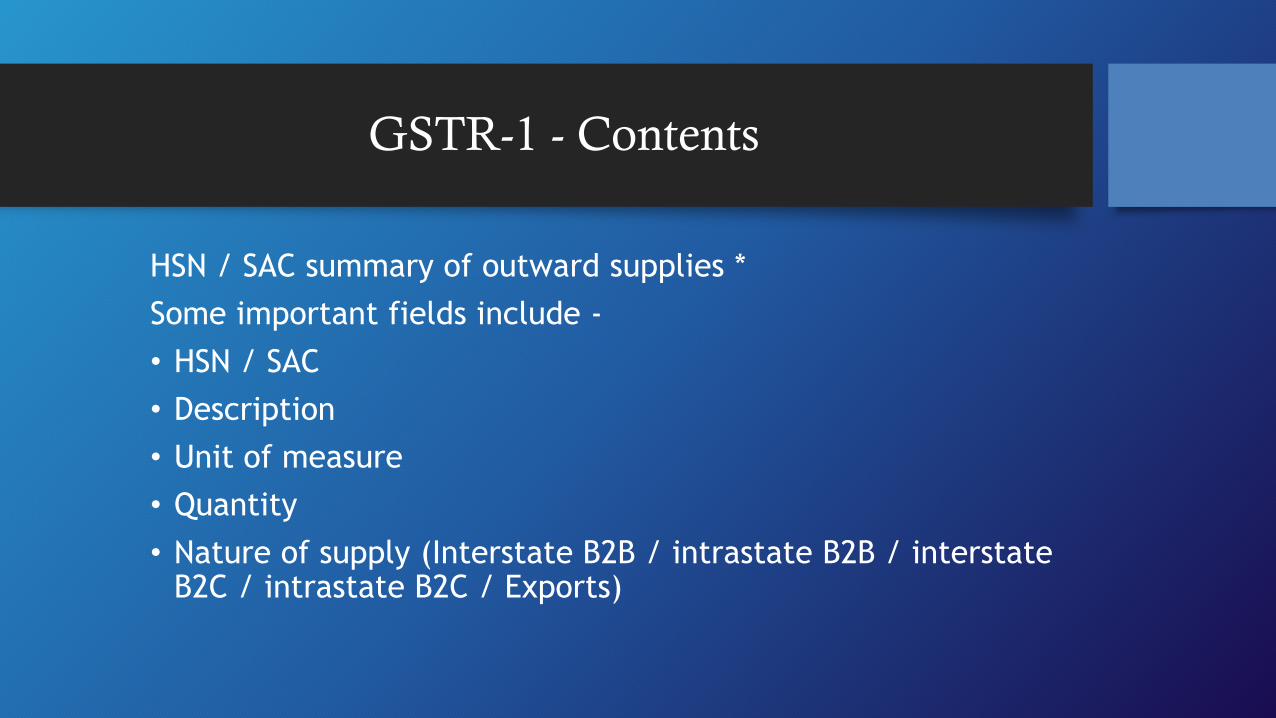

HSN / SAC summary of outward supplies *

Some important fields include -

• HSN / SAC

• Description

• Unit of measure

• Quantity

• Nature of supply (Interstate B2B / intrastate B2B / interstate B2C / intrastate B2C / Exports)

GSTR-1 - Contents

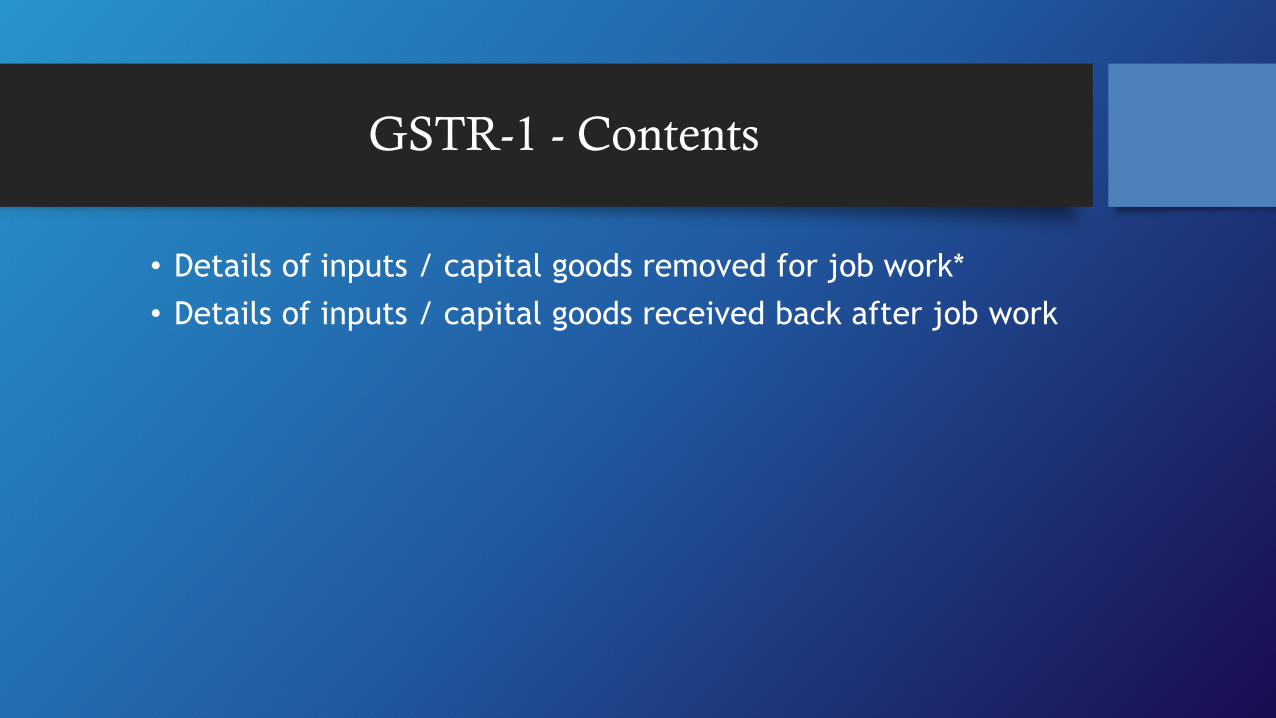

• Details of inputs / capital goods removed for job work*

• Details of inputs / capital goods received back after job work

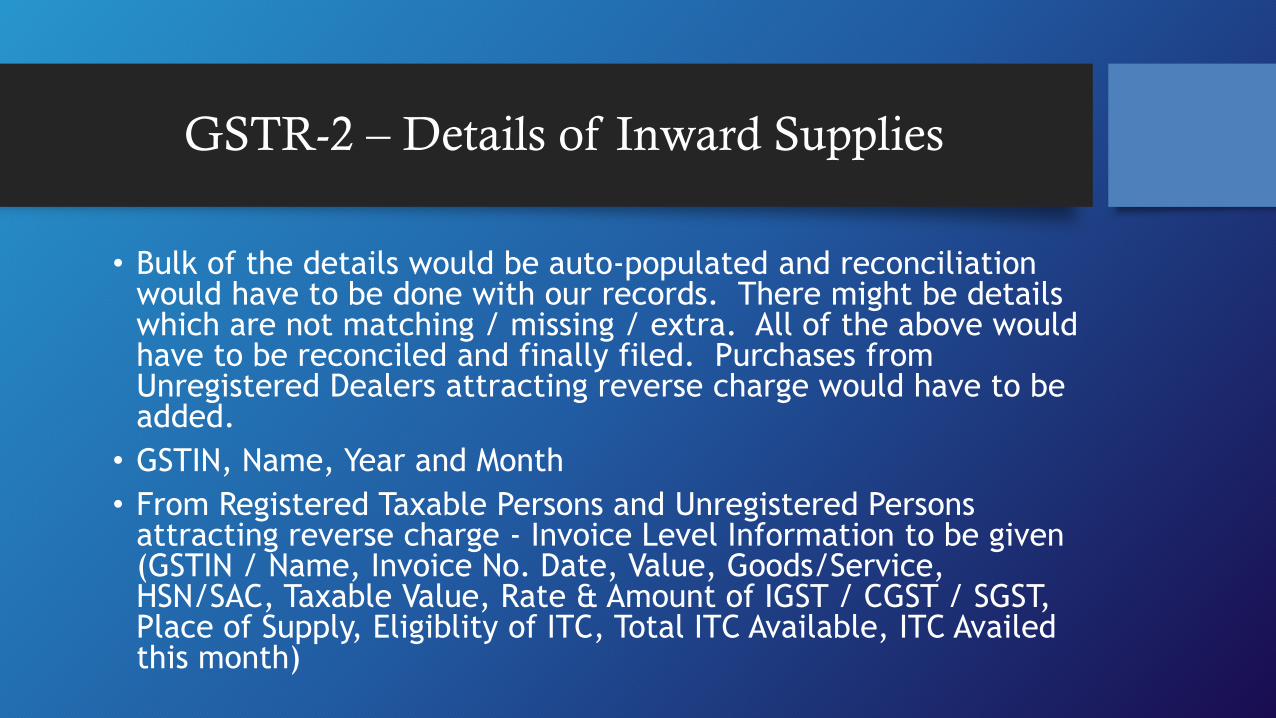

GSTR-2 – Details of Inward Supplies

• Bulk of the details would be auto-populated and reconciliation would have to be done with our records. There might be details which are not matching / missing / extra. All of the above would have to be reconciled and finally filed. Purchases from Unregistered Dealers attracting reverse charge would have to be added.

• GSTIN, Name, Year and Month

• From Registered Taxable Persons and Unregistered Persons attracting reverse charge - Invoice Level Information to be given (GSTIN / Name, Invoice No. Date, Value, Goods/Service, HSN/SAC, Taxable Value, Rate & Amount of IGST / CGST / SGST, Place of Supply, Eligiblity of ITC, Total ITC Available, ITC Availed this month)

GSTR-2 - Contents

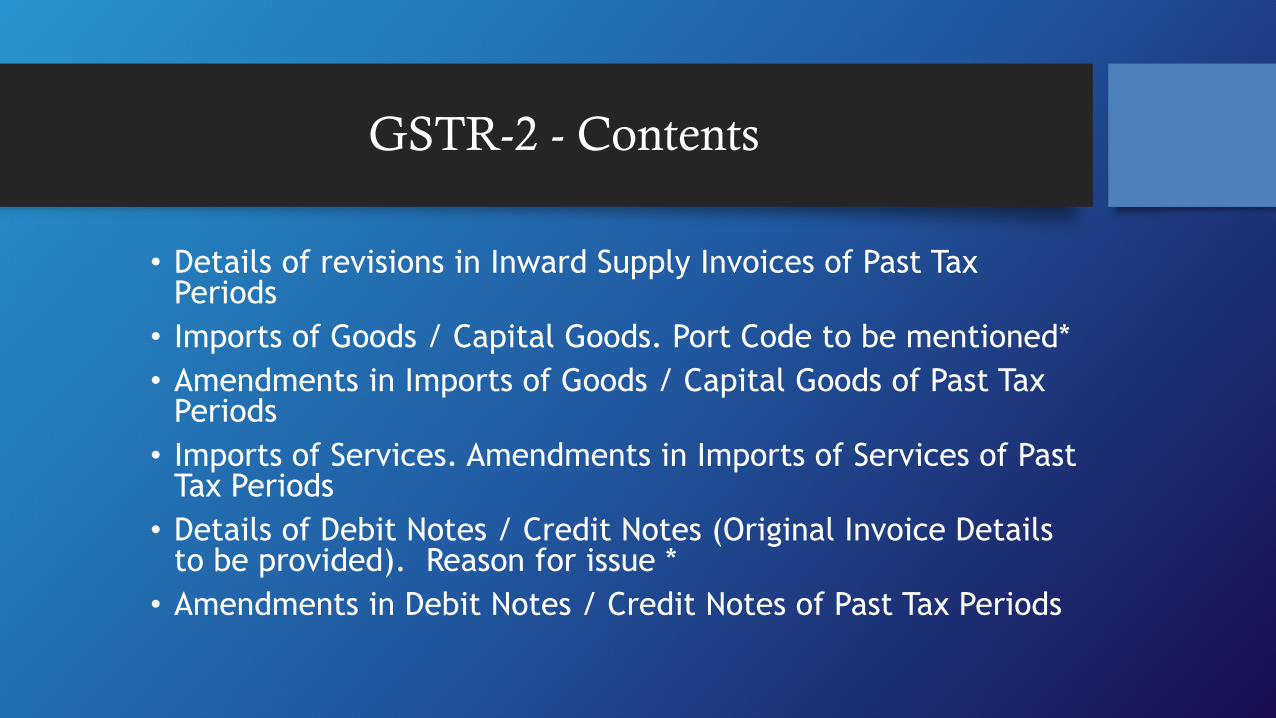

• Details of revisions in Inward Supply Invoices of Past Tax Periods

• Imports of Goods / Capital Goods. Port Code to be mentioned*

• Amendments in Imports of Goods / Capital Goods of Past Tax Periods

• Imports of Services. Amendments in Imports of Services of Past Tax Periods

• Details of Debit Notes / Credit Notes (Original Invoice Details to be provided). Reason for issue *

• Amendments in Debit Notes / Credit Notes of Past Tax Periods

GSTR-2 - Contents

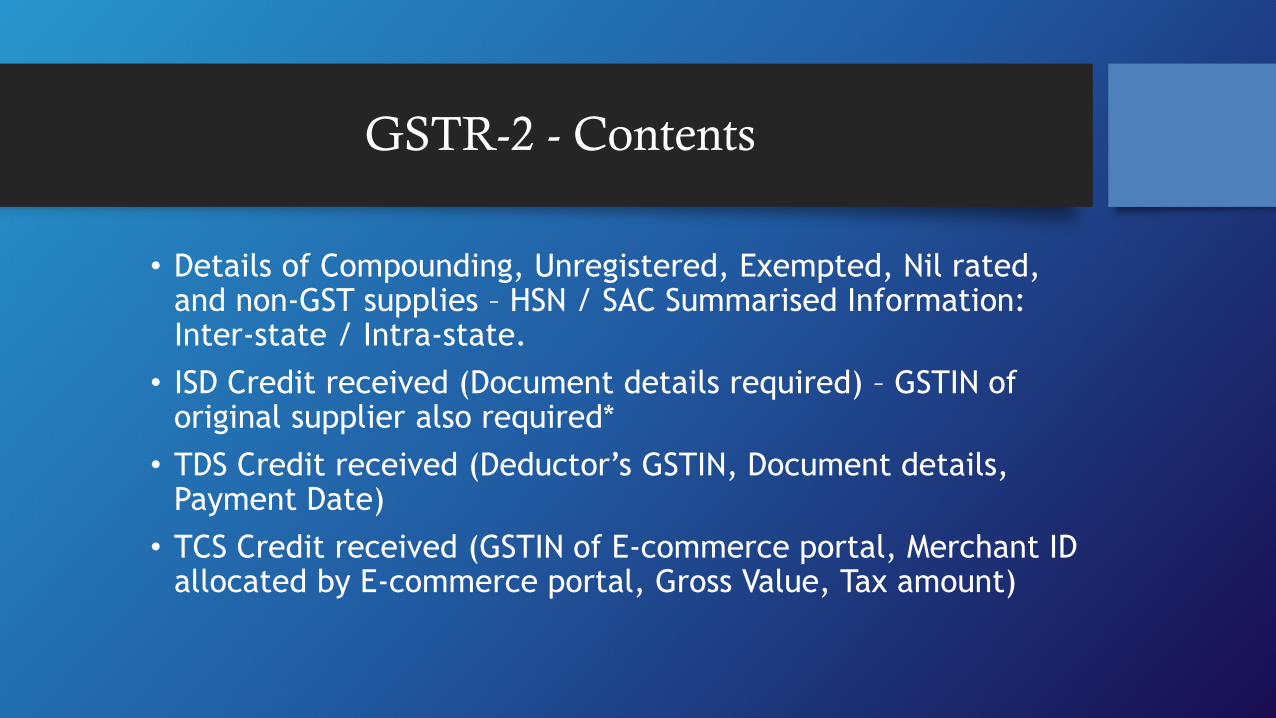

• Details of Compounding, Unregistered, Exempted, Nil rated, and non-GST supplies – HSN / SAC Summarised Information: Inter-state / Intra-state.

• ISD Credit received (Document details required) – GSTIN of original supplier also required*

• TDS Credit received (Deductor’s GSTIN, Document details, Payment Date)

• TCS Credit received (GSTIN of E-commerce portal, Merchant ID allocated by E-commerce portal, Gross Value, Tax amount)

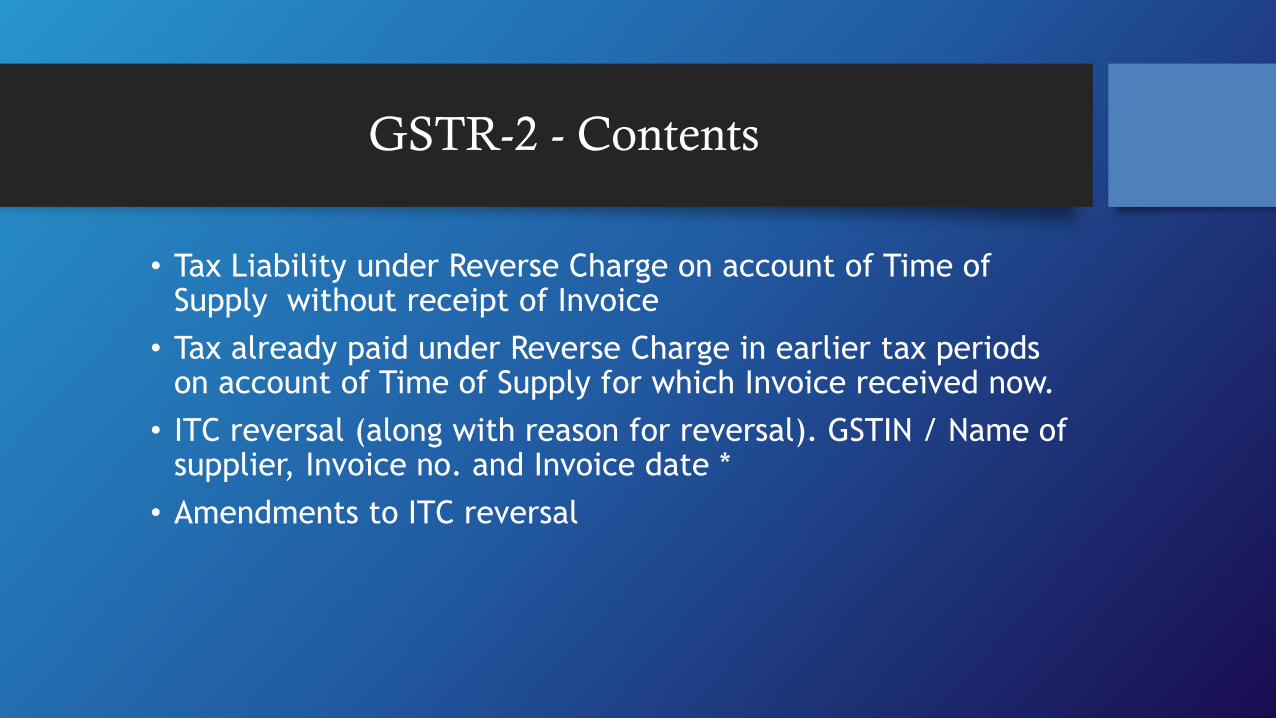

GSTR-2 - Contents

• Tax Liability under Reverse Charge on account of Time of Supply without receipt of Invoice

• Tax already paid under Reverse Charge in earlier tax periods on account of Time of Supply for which Invoice received now.

• ITC reversal (along with reason for reversal). GSTIN / Name of supplier, Invoice no. and Invoice date *

• Amendments to ITC reversal

GSTR-2 - Contents

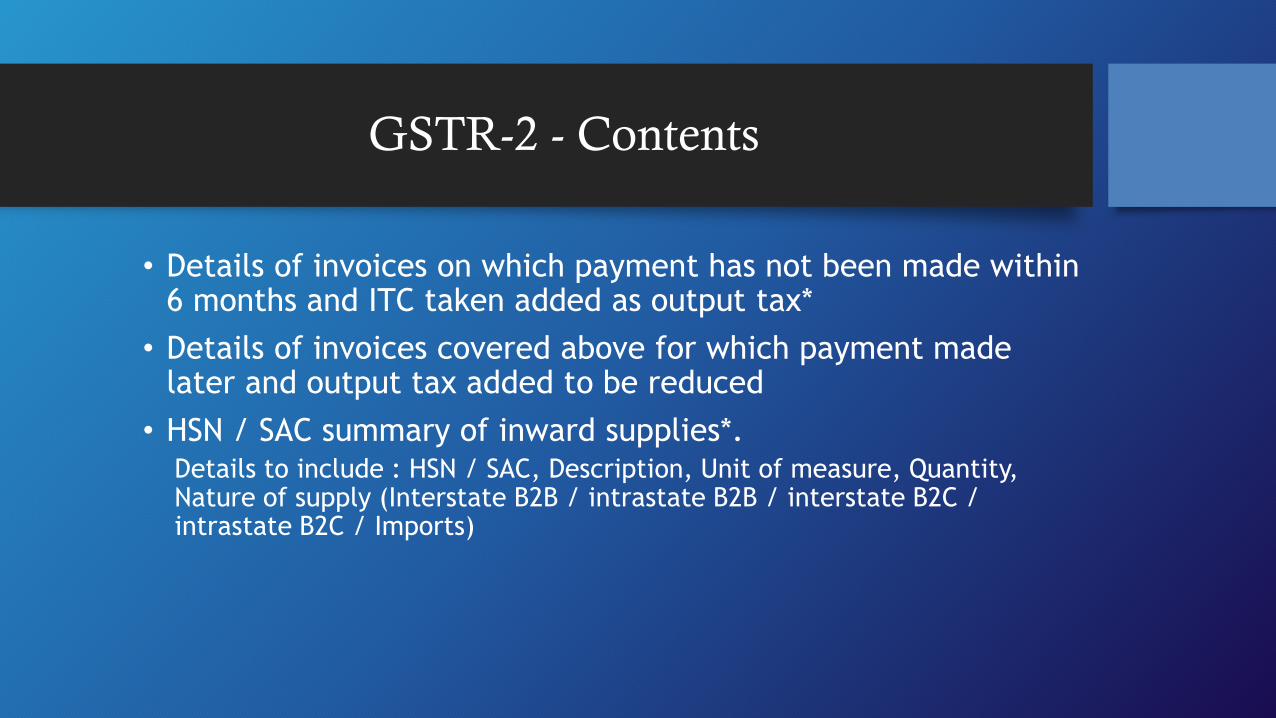

• Details of invoices on which payment has not been made within 6 months and ITC taken added as output tax*

• Details of invoices covered above for which payment made later and output tax added to be reduced

• HSN / SAC summary of inward supplies*. Details to include : HSN / SAC, Description, Unit of measure, Quantity, Nature of supply (Interstate B2B / intrastate B2B / interstate B2C / intrastate B2C / Imports)

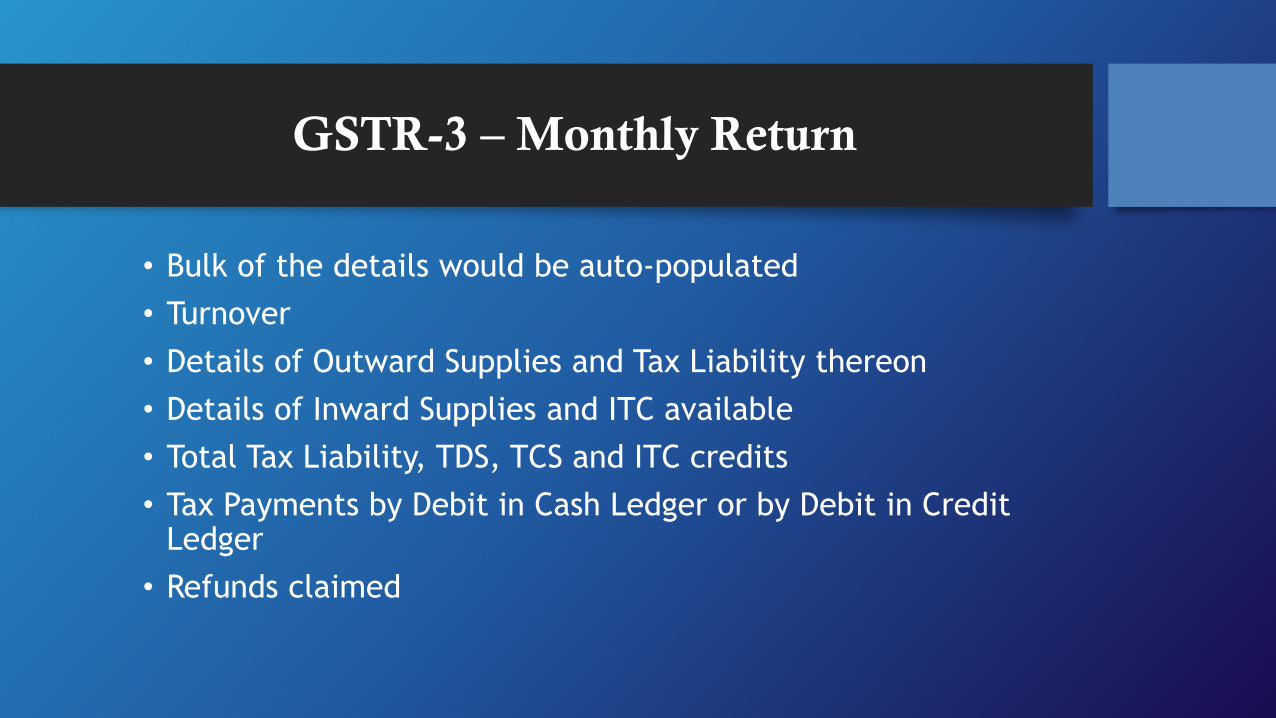

GSTR-3 – Monthly Return

• Bulk of the details would be auto-populated

• Turnover

• Details of Outward Supplies and Tax Liability thereon

• Details of Inward Supplies and ITC available

• Total Tax Liability, TDS, TCS and ITC credits

• Tax Payments by Debit in Cash Ledger or by Debit in Credit Ledger

• Refunds claimed

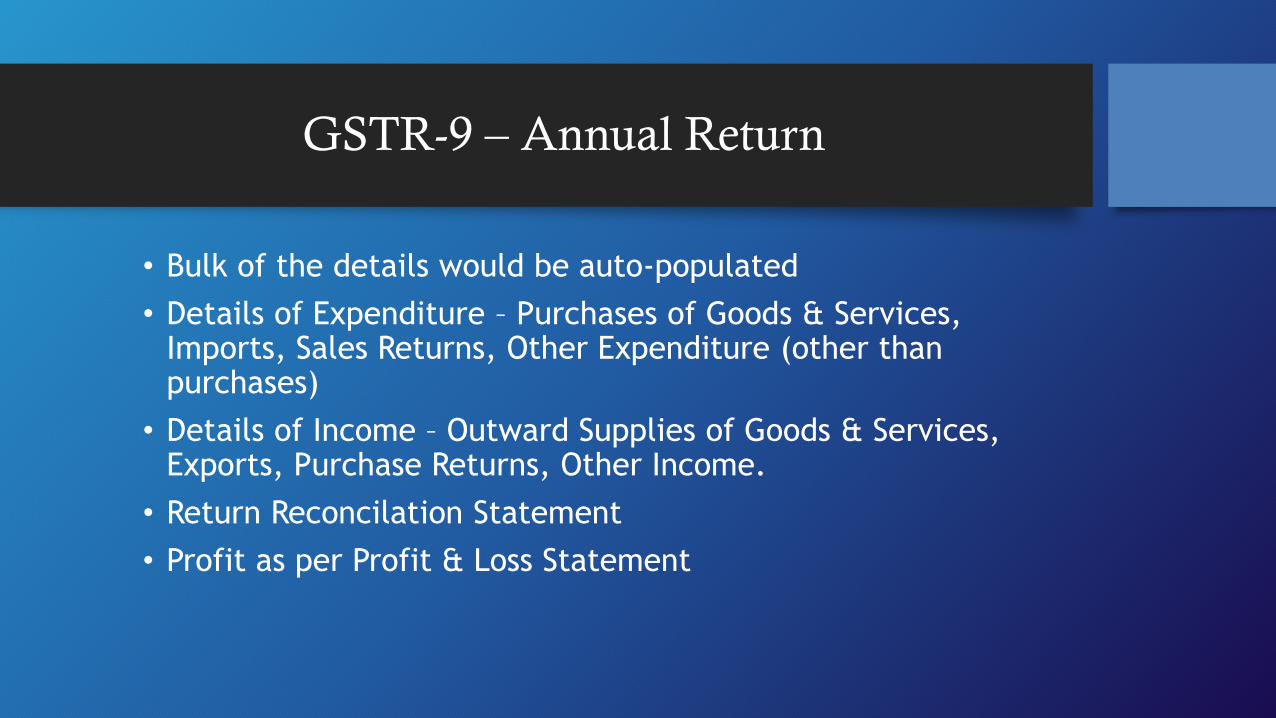

GSTR-9 – Annual Return

• Bulk of the details would be auto-populated

• Details of Expenditure – Purchases of Goods & Services, Imports, Sales Returns, Other Expenditure (other than purchases)

• Details of Income – Outward Supplies of Goods & Services, Exports, Purchase Returns, Other Income.

• Return Reconcilation Statement

• Profit as per Profit & Loss Statement

Transition Provisions

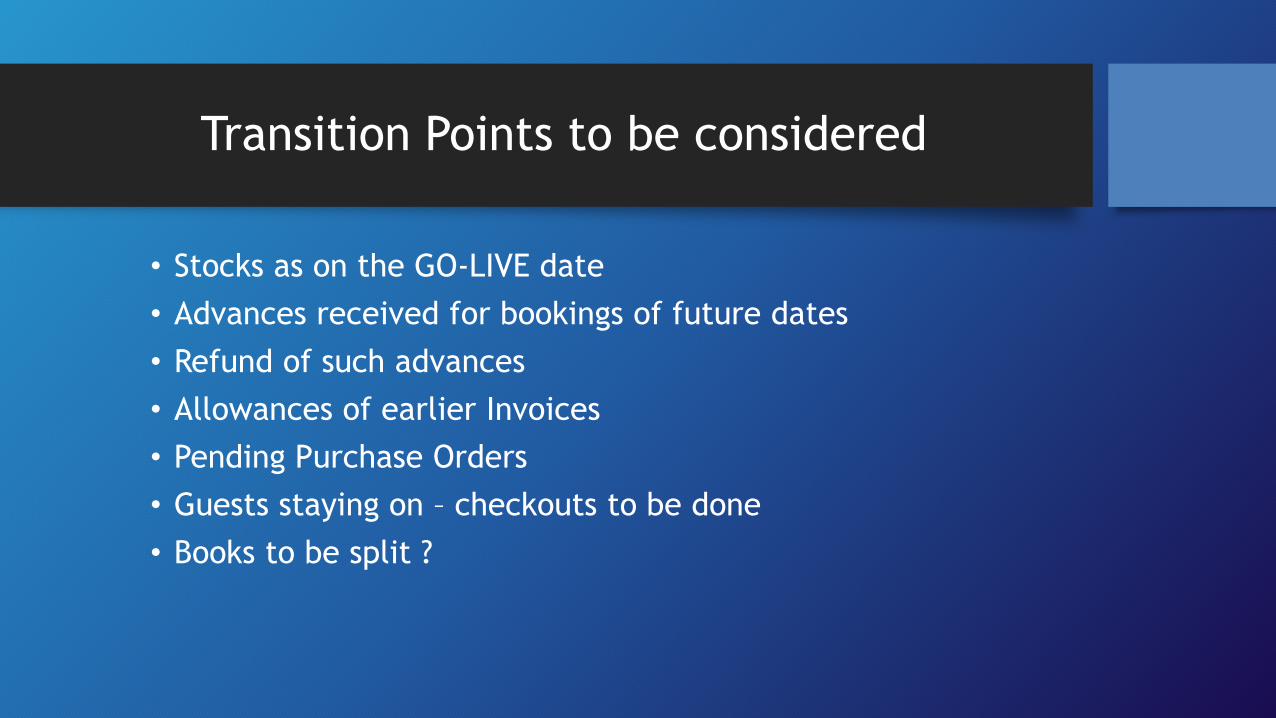

Transition Points to be considered

• Stocks as on the GO-LIVE date

• Advances received for bookings of future dates

• Refund of such advances

• Allowances of earlier Invoices

• Pending Purchase Orders

• Guests staying on – checkouts to be done

• Books to be split ?

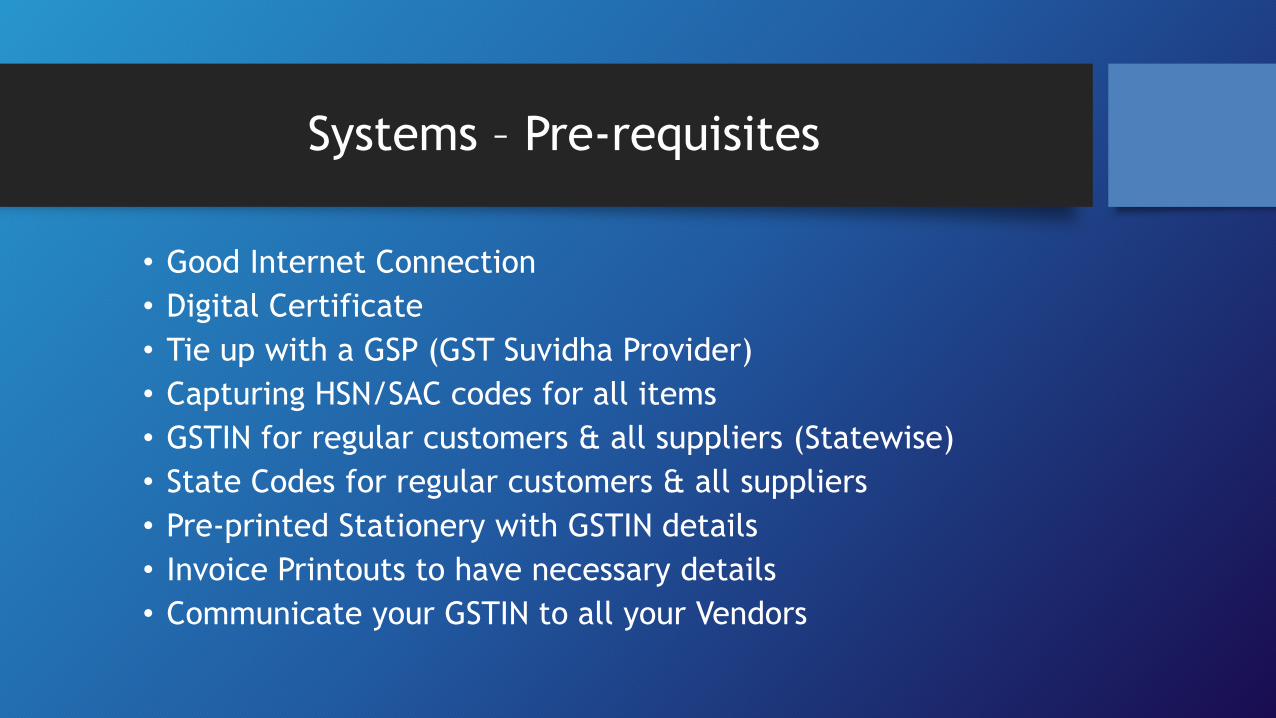

Systems – Pre-requisites

• Good Internet Connection

• Digital Certificate

• Tie up with a GSP (GST Suvidha Provider)

• Capturing HSN/SAC codes for all items

• GSTIN for regular customers & all suppliers (Statewise)

• State Codes for regular customers & all suppliers

• Pre-printed Stationery with GSTIN details

• Invoice Printouts to have necessary details

• Communicate your GSTIN to all your Vendors

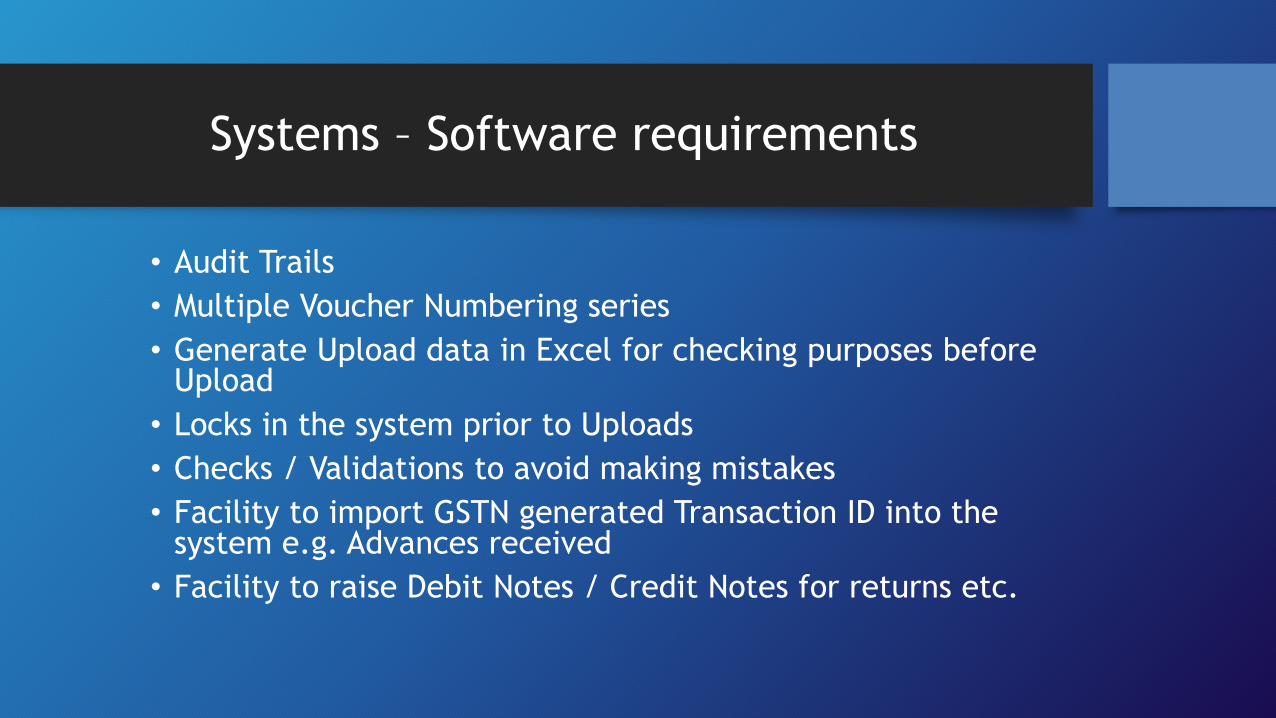

Systems – Software requirements

• Audit Trails

• Multiple Voucher Numbering series

• Generate Upload data in Excel for checking purposes before Upload

• Locks in the system prior to Uploads

• Checks / Validations to avoid making mistakes

• Facility to import GSTN generated Transaction ID into the system e.g. Advances received

• Facility to raise Debit Notes / Credit Notes for returns etc.

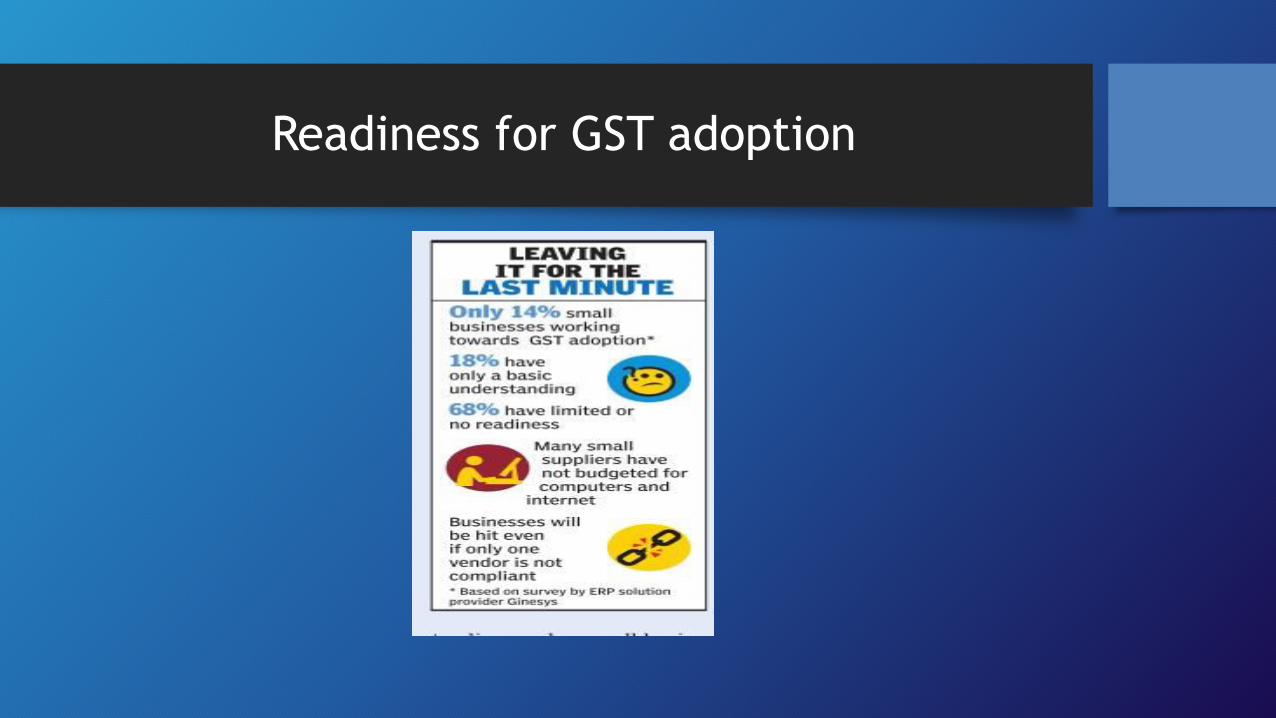

Readiness for GST adoption

Tax Rates applicable

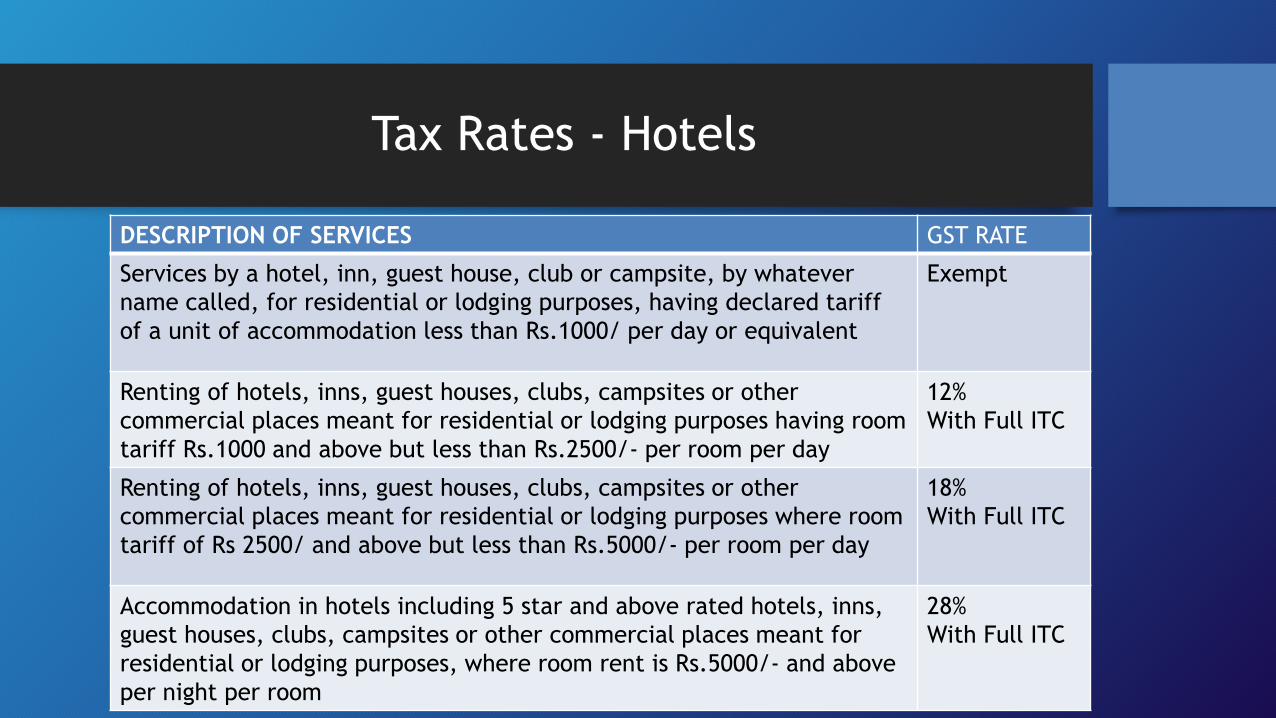

Tax Rates - Hotels

DESCRIPTION OF SERVICES GST RATE

Services by a hotel, inn, guest house, club or campsite, by whatever

name called, for residential or lodging purposes, having declared tariff

of a unit of accommodation less than Rs.1000/ per day or equivalent

Exempt

Renting of hotels, inns, guest houses, clubs, campsites or other

commercial places meant for residential or lodging purposes having room

tariff Rs.1000 and above but less than Rs.2500/- per room per day

12%

With Full ITC

Renting of hotels, inns, guest houses, clubs, campsites or other

commercial places meant for residential or lodging purposes where room

tariff of Rs 2500/ and above but less than Rs.5000/- per room per day

18%

With Full ITC

Accommodation in hotels including 5 star and above rated hotels, inns,

guest houses, clubs, campsites or other commercial places meant for

residential or lodging purposes, where room rent is Rs.5000/- and above

per night per room

28%

With Full ITC

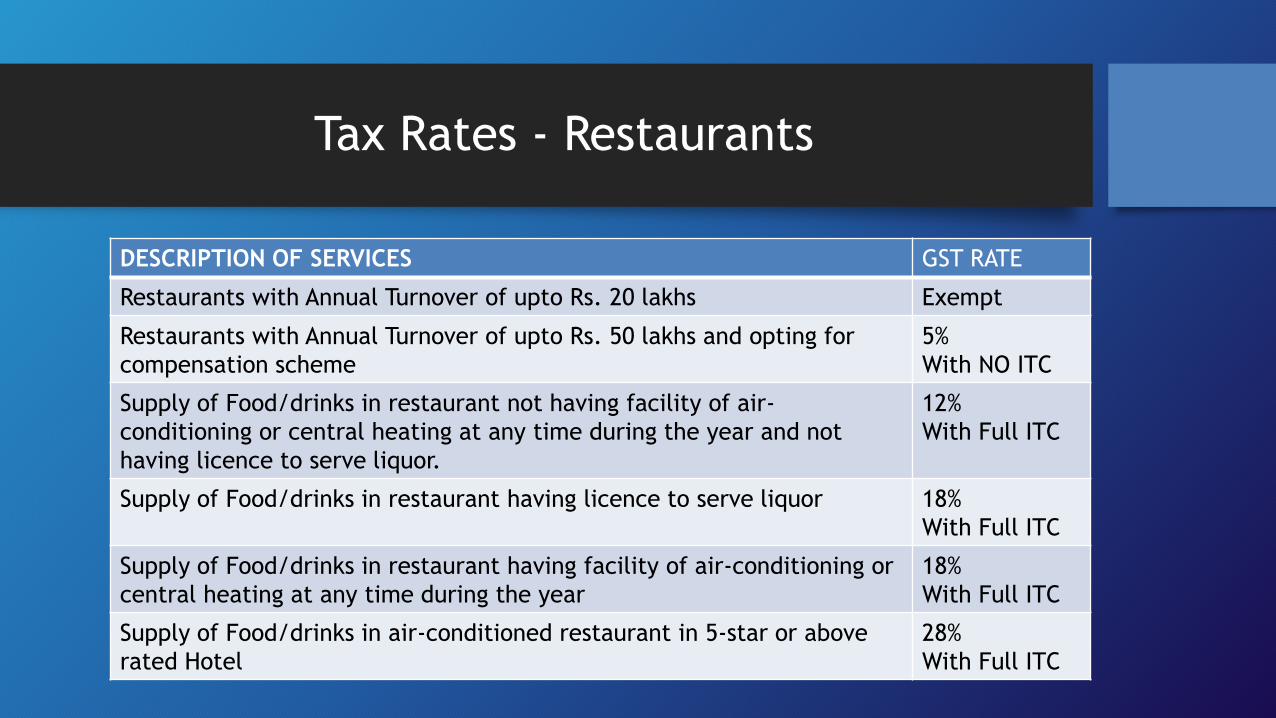

Tax Rates - Restaurants

DESCRIPTION OF SERVICES GST RATE

Restaurants with Annual Turnover of upto Rs. 20 lakhs Exempt

Restaurants with Annual Turnover of upto Rs. 50 lakhs and opting for

compensation scheme

5%

With NO ITC

Supply of Food/drinks in restaurant not having facility of air-

conditioning or central heating at any time during the year and not

having licence to serve liquor.

12%

With Full ITC

Supply of Food/drinks in restaurant having licence to serve liquor 18%

With Full ITC

Supply of Food/drinks in restaurant having facility of air-conditioning or

central heating at any time during the year

18%

With Full ITC

Supply of Food/drinks in air-conditioned restaurant in 5-star or above

rated Hotel

28%

With Full ITC

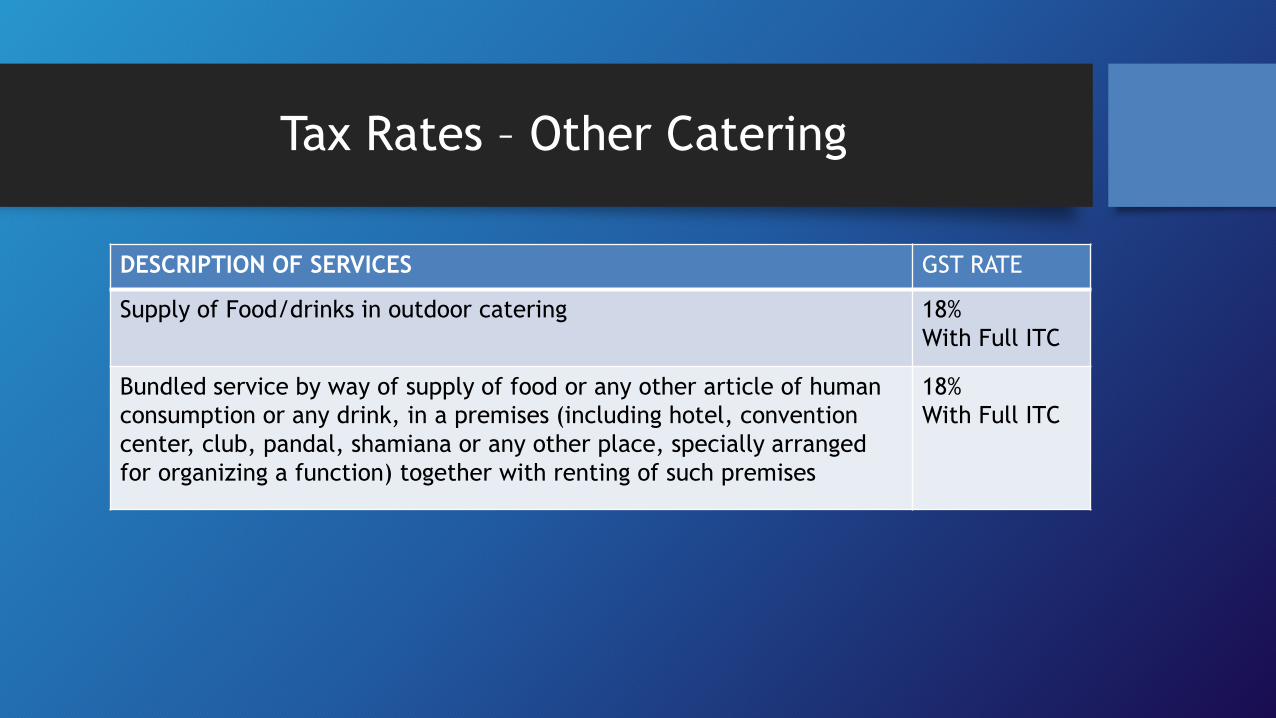

Tax Rates – Other Catering

DESCRIPTION OF SERVICES GST RATE

Supply of Food/drinks in outdoor catering 18%

With Full ITC

Bundled service by way of supply of food or any other article of human

consumption or any drink, in a premises (including hotel, convention

center, club, pandal, shamiana or any other place, specially arranged

for organizing a function) together with renting of such premises

18%

With Full ITC

Other Important Provisions

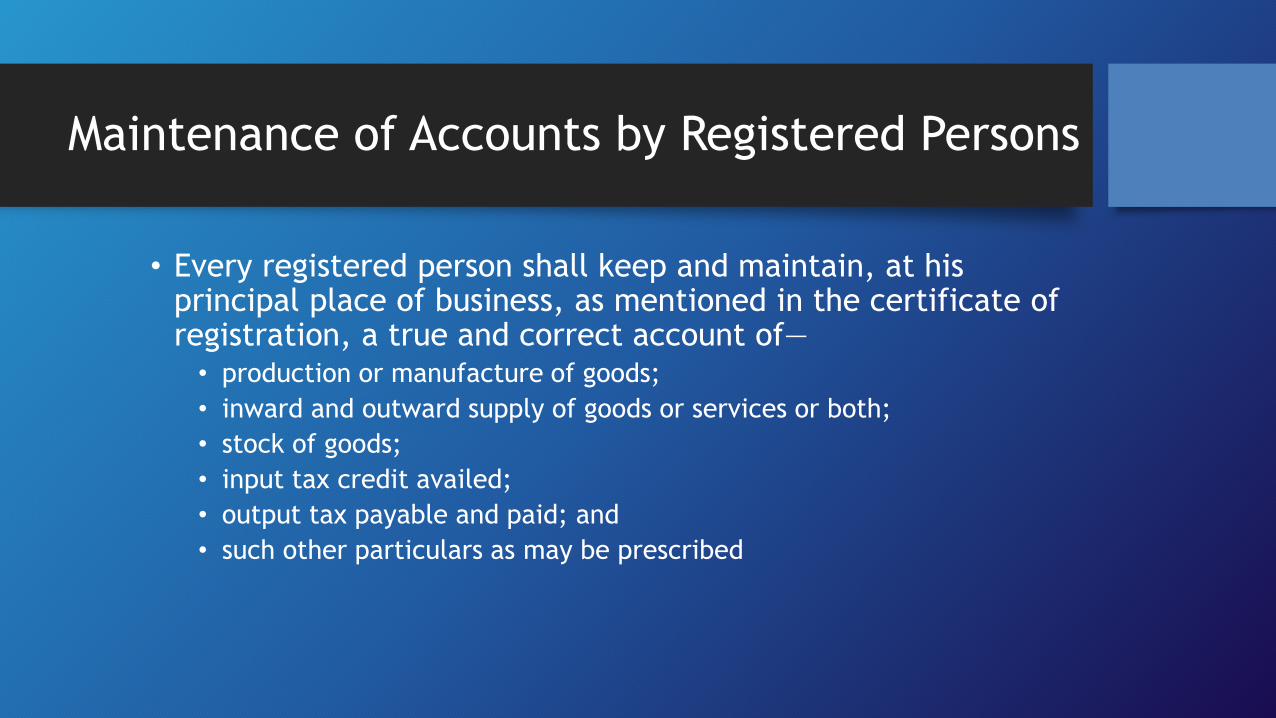

Maintenance of Accounts by Registered Persons

• Every registered person shall keep and maintain, at his principal place of business, as mentioned in the certificate of registration, a true and correct account of— • production or manufacture of goods;

• inward and outward supply of goods or services or both;

• stock of goods;

• input tax credit availed;

• output tax payable and paid; and

• such other particulars as may be prescribed

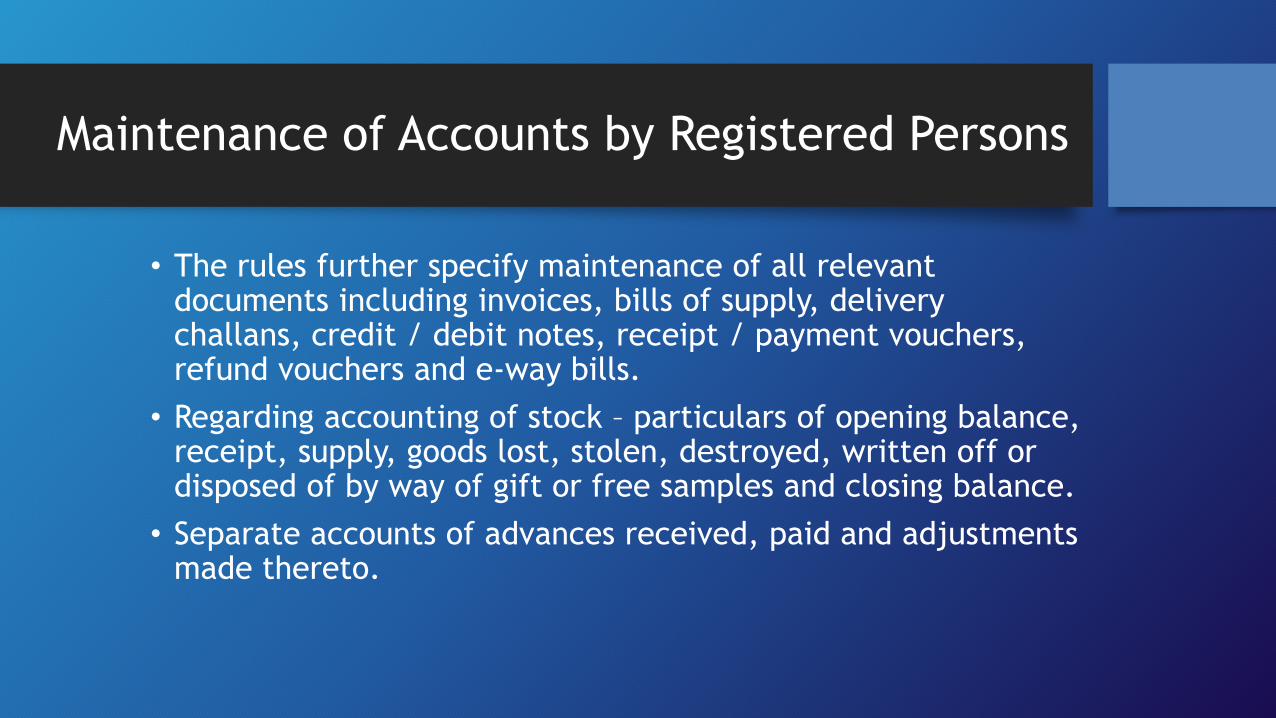

Maintenance of Accounts by Registered Persons

• The rules further specify maintenance of all relevant documents including invoices, bills of supply, delivery challans, credit / debit notes, receipt / payment vouchers, refund vouchers and e-way bills.

• Regarding accounting of stock – particulars of opening balance, receipt, supply, goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples and closing balance.

• Separate accounts of advances received, paid and adjustments made thereto.

Maintenance of Accounts by Registered Persons

• Details of tax payable, tax collected and paid, input tax, input tax credit claimed, together with a register of tax invoice, credit / debit note, delivery challan issued or received.

• Names and complete addresses of suppliers

• Names and complete addresses of persons to whom he has supplied goods / services

• Any entry in registers, accounts and documents shall not be erased or overwritten, and where the registers and other documents are maintained electronically, a log of every entry edited or deleted shall be maintained.

Maintenance of Accounts by Registered Persons

• Every registered person supplying services shall maintain the accounts showing the quantitative details of goods used in the provision of each service, details of input services used and the services supplied.

• The records under these rules may be maintained in electronic form and the record so maintained shall be authenticated by means of a digital signature.

Electronic Way Bills

• E-way bills would have to be generated on the GSTN (common portal) for movement of goods.

• ‘Movement’ of goods of more than Rs 50,000 in value cannot be made by any person without an e-way bill.

• The tax officials can inspect the same, anytime during the transit to check tax evasion.

• GSTN will generate e-way bills that will be valid for 1-15 days, depending on distance to be travelled.

• Flight Kitchens, Outdoor Catering may be affected

GST – A Simple Single Tax

What we thought it would be What it turns out to be

Thank You

CA KURESH S KAGALWALA

+91-9820169660

Disclaimer:

The information provided in this presentation is intended for informational purposes only and does not constitute legal opinion or advice. Readers are requested to seek formal legal advice prior to acting upon any of the information provided herein. This presentation is not intended to address the circumstances of any particular individual or corporate body. There can be no assurance that the judicial / quasi-judicial authorities may not take a position contrary to the views mentioned herein.