22

1 August 22, 2012 GSU Economic Forecasting Conference

1

August 22, 2012

GSU Economic Forecasting Conference

2

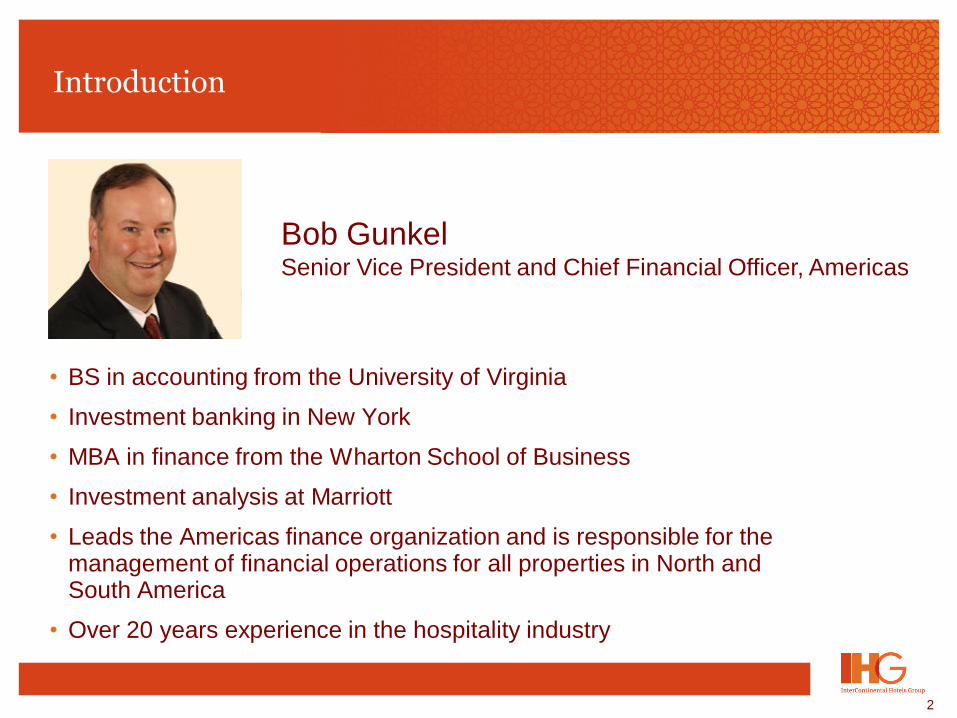

Introduction

• BS in accounting from the University of Virginia

• Investment banking in New York

• MBA in finance from the Wharton School of Business

• Investment analysis at Marriott

• Leads the Americas finance organization and is responsible for the management of financial operations for all properties in North and South America

• Over 20 years experience in the hospitality industry

Bob Gunkel Senior Vice President and Chief Financial Officer, Americas

3

Agenda

1. Introduction to IHG

2. Why lodging is important to the U.S. economy and where we are in the business cycle

3. The Southeast and Atlanta’s part in the lodging industry

4. Forecasts for the future

4

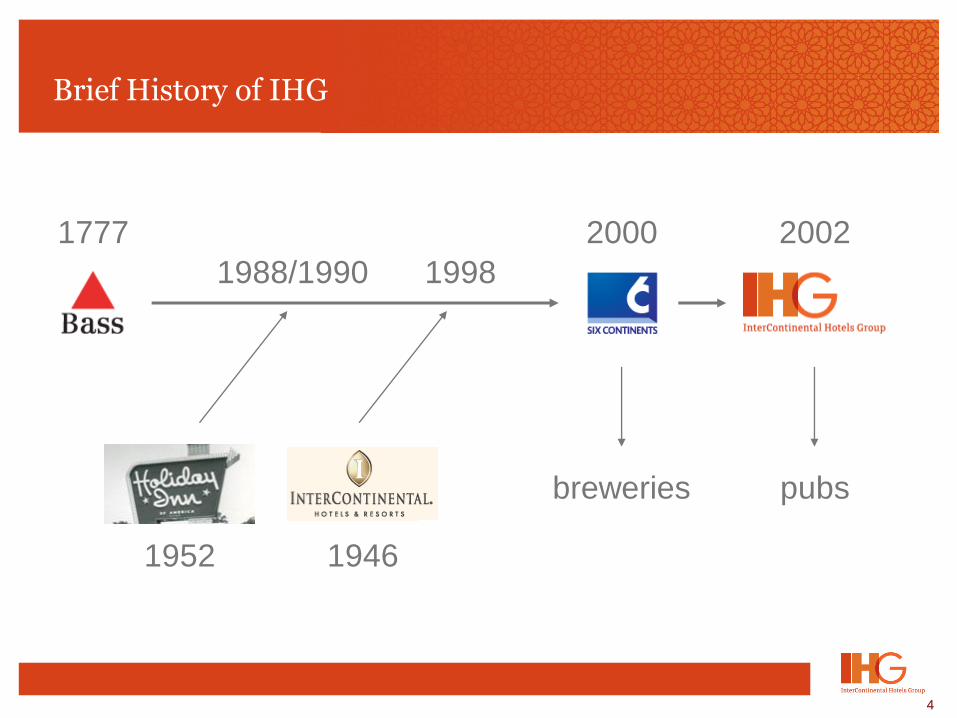

Brief History of IHG

1777

1988/1990 1998

2000 2002

breweries pubs

1946 1952

5

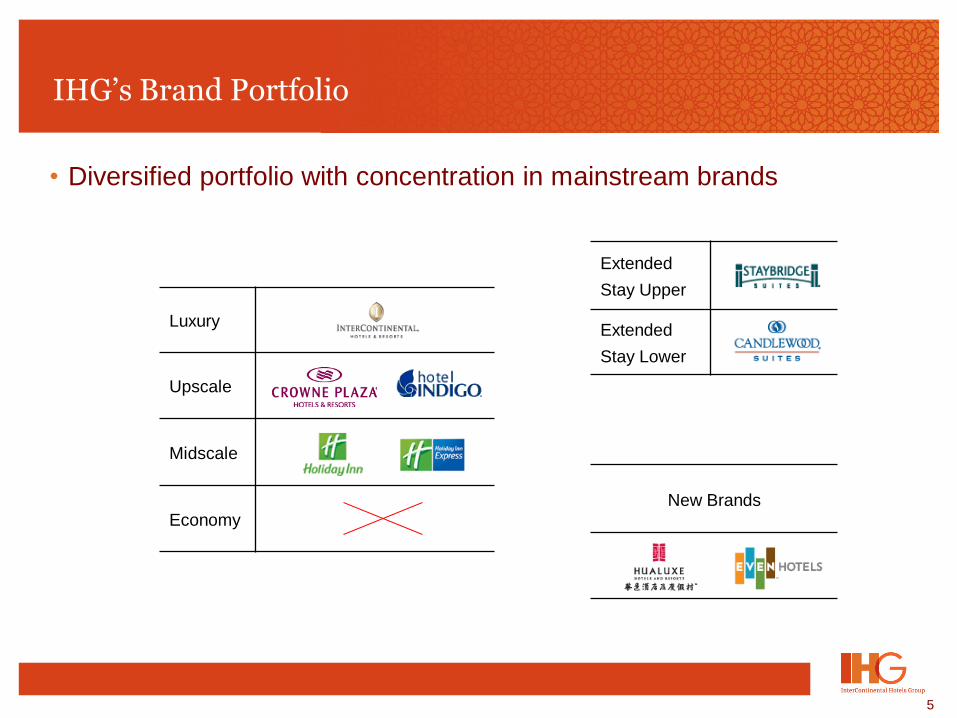

IHG’s Brand Portfolio

• Diversified portfolio with concentration in mainstream brands

New Brands

Luxury

Upscale

Midscale

Economy

Extended

Stay Upper

Extended

Stay Lower

6

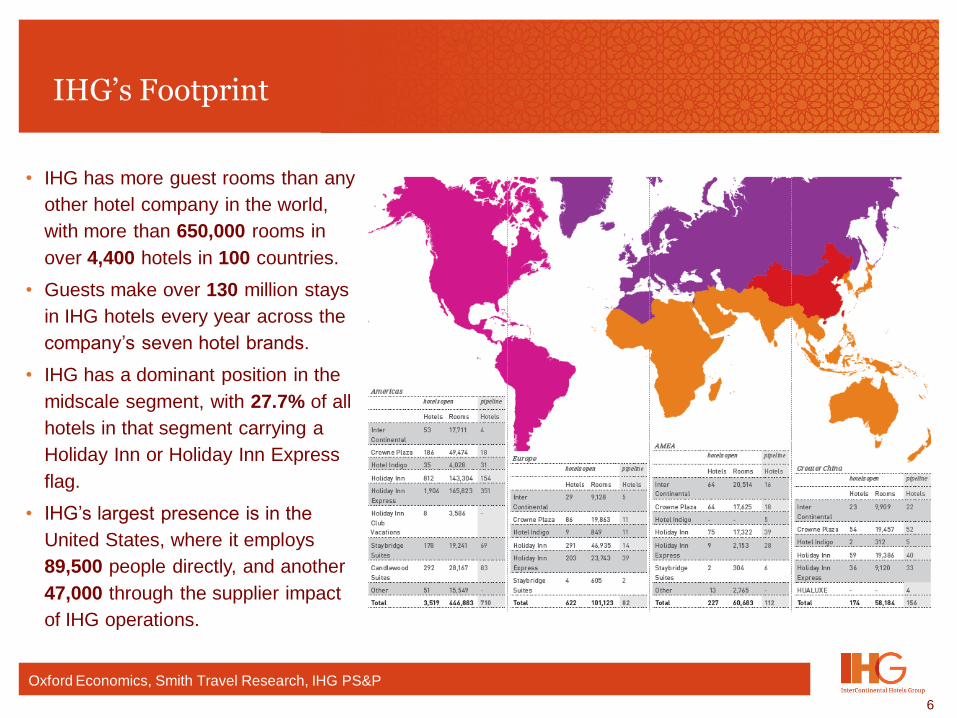

IHG’s Footprint

• IHG has more guest rooms than any

other hotel company in the world,

with more than 650,000 rooms in

over 4,400 hotels in 100 countries.

• Guests make over 130 million stays

in IHG hotels every year across the

company’s seven hotel brands.

• IHG has a dominant position in the

midscale segment, with 27.7% of all

hotels in that segment carrying a

Holiday Inn or Holiday Inn Express

flag.

• IHG’s largest presence is in the

United States, where it employs

89,500 people directly, and another

47,000 through the supplier impact

of IHG operations.

Oxford Economics, Smith Travel Research, IHG PS&P

7

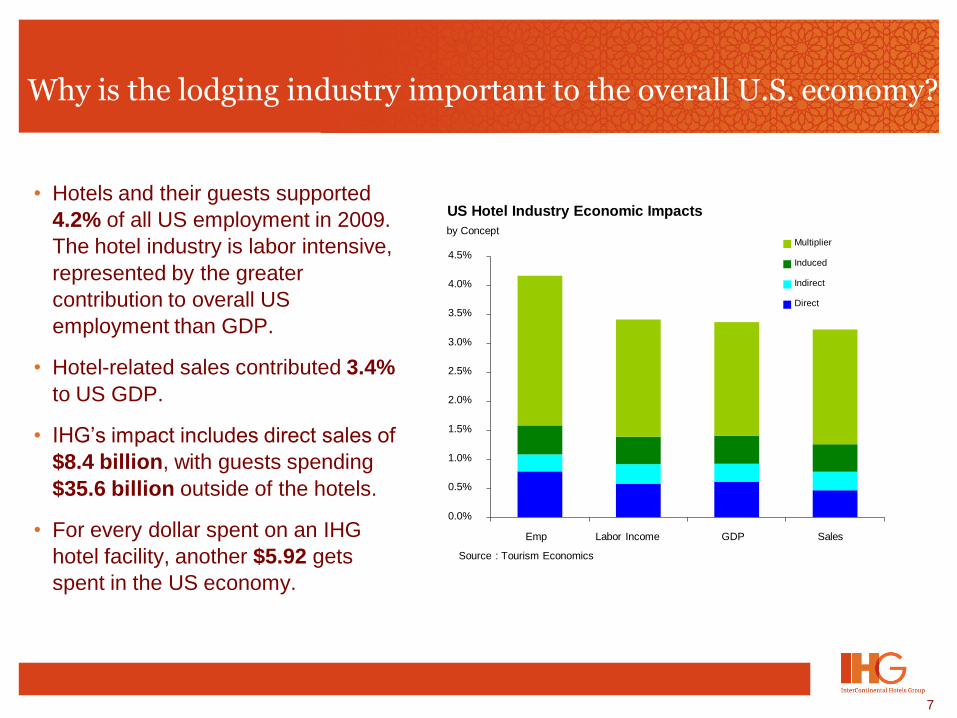

Why is the lodging industry important to the overall U.S. economy?

• Hotels and their guests supported

4.2% of all US employment in 2009.

The hotel industry is labor intensive,

represented by the greater

contribution to overall US

employment than GDP.

• Hotel-related sales contributed 3.4%

to US GDP.

• IHG’s impact includes direct sales of

$8.4 billion, with guests spending

$35.6 billion outside of the hotels.

• For every dollar spent on an IHG

hotel facility, another $5.92 gets

spent in the US economy.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Emp Labor Income GDP Sales

Multiplier

Induced

Indirect

Direct

US Hotel Industry Economic Impacts

by Concept

Source : Tourism Economics

8

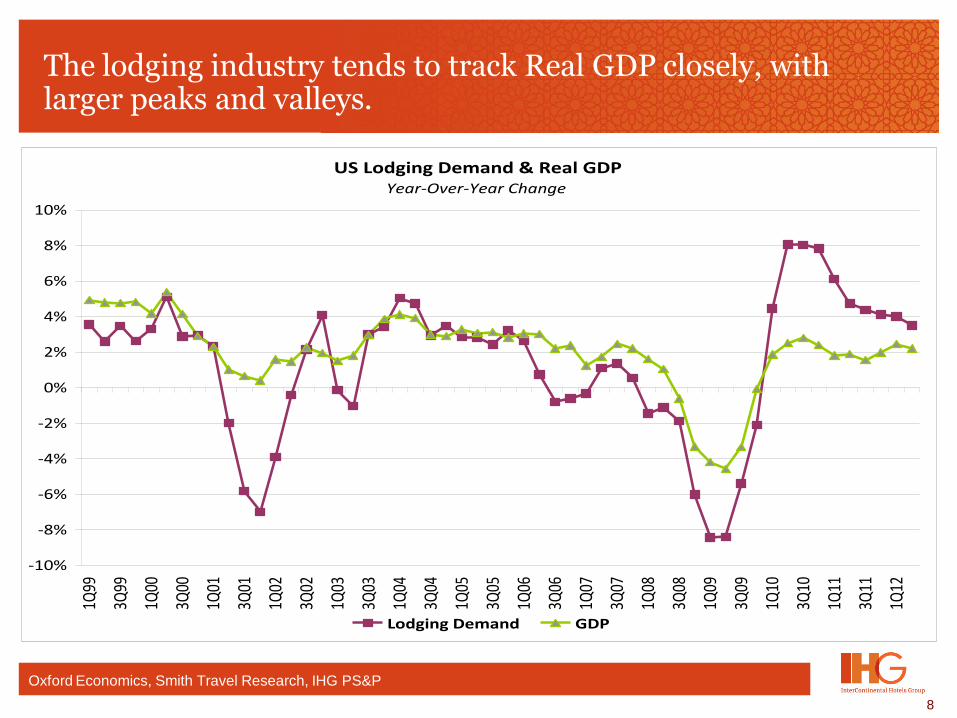

The lodging industry tends to track Real GDP closely, with larger peaks and valleys.

US Lodging Demand & Real GDPYear-Over-Year Change

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1Q99

3Q99

1Q00

3Q00

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

Lodging Demand GDP

Oxford Economics, Smith Travel Research, IHG PS&P

9

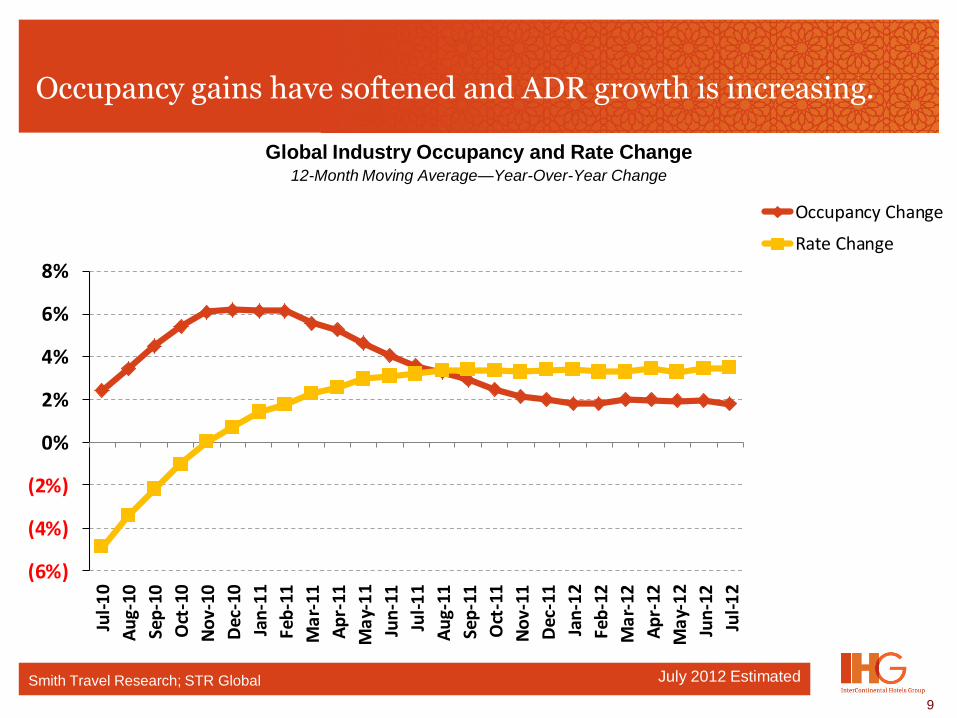

Occupancy gains have softened and ADR growth is increasing.

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

Jul-

10

Au

g-10

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan

-11

Feb

-11

Ma

r-11

Ap

r-11

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan

-12

Feb

-12

Ma

r-12

Ap

r-12

Ma

y-1

2

Jun

-12

Jul-

12

Occupancy Change

Rate Change

Smith Travel Research; STR Global

Global Industry Occupancy and Rate Change 12-Month Moving Average—Year-Over-Year Change

July 2012 Estimated

10

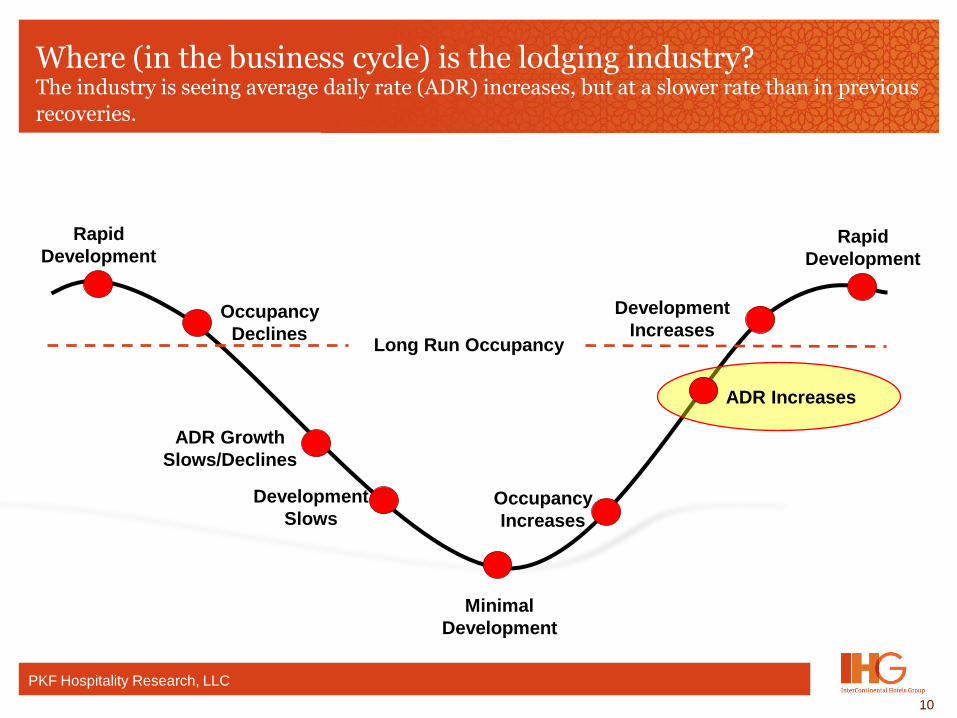

Where (in the business cycle) is the lodging industry? The industry is seeing average daily rate (ADR) increases, but at a slower rate than in previous

recoveries.

Rapid

Development

ADR Growth

Slows/Declines

Minimal

Development

Development

Increases

ADR Increases

Occupancy

Increases

Occupancy

Declines

Development

Slows

Long Run Occupancy

Rapid

Development

PKF Hospitality Research, LLC

11

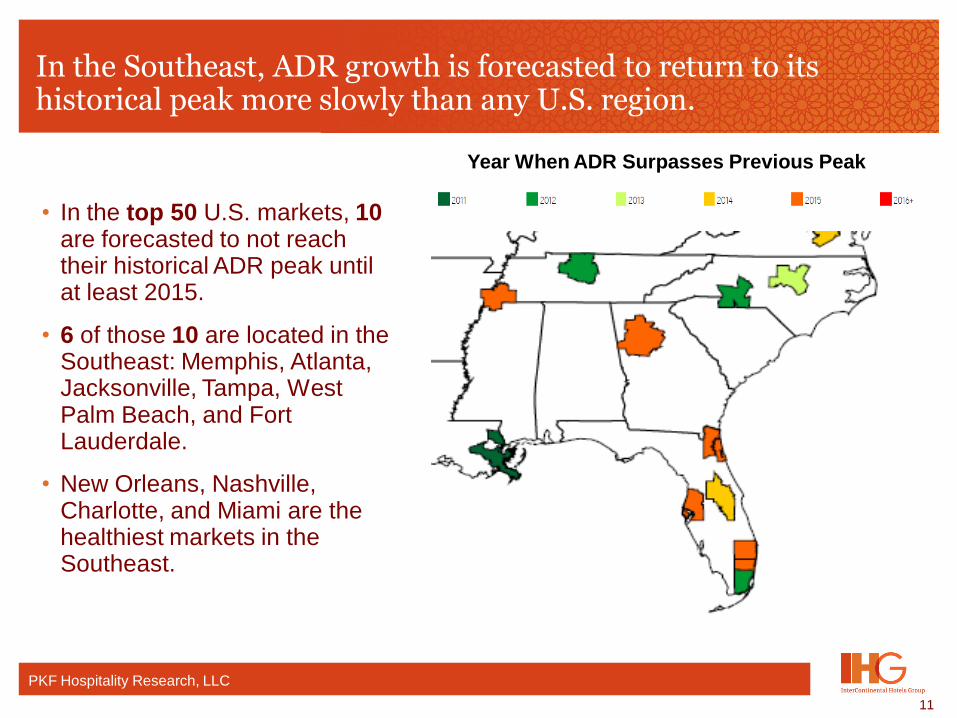

In the Southeast, ADR growth is forecasted to return to its historical peak more slowly than any U.S. region.

PKF Hospitality Research, LLC

• In the top 50 U.S. markets, 10 are forecasted to not reach their historical ADR peak until at least 2015.

• 6 of those 10 are located in the Southeast: Memphis, Atlanta, Jacksonville, Tampa, West Palm Beach, and Fort Lauderdale.

• New Orleans, Nashville, Charlotte, and Miami are the healthiest markets in the Southeast.

Year When ADR Surpasses Previous Peak

12

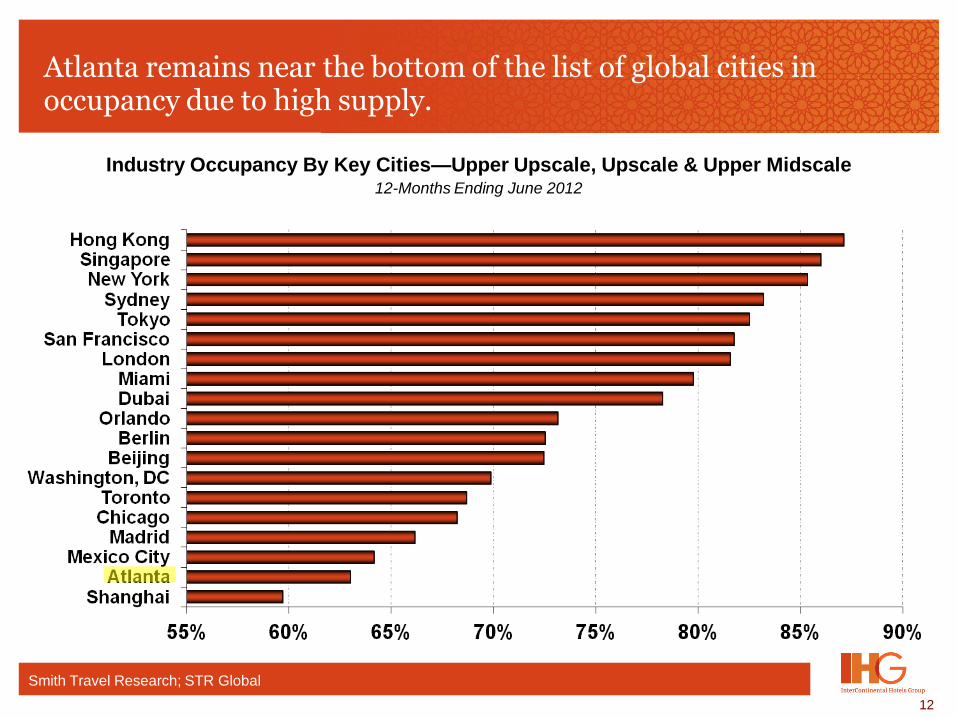

Atlanta remains near the bottom of the list of global cities in occupancy due to high supply.

Smith Travel Research; STR Global

Industry Occupancy By Key Cities—Upper Upscale, Upscale & Upper Midscale 12-Months Ending June 2012

13

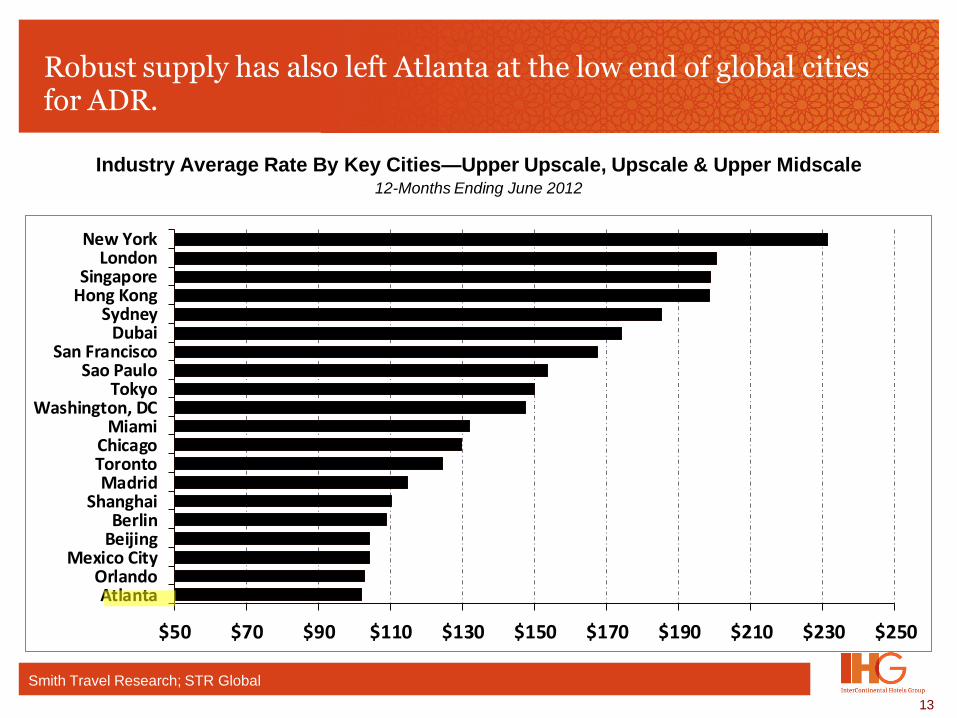

Robust supply has also left Atlanta at the low end of global cities for ADR.

Smith Travel Research; STR Global

Industry Average Rate By Key Cities—Upper Upscale, Upscale & Upper Midscale 12-Months Ending June 2012

$50 $70 $90 $110 $130 $150 $170 $190 $210 $230 $250

AtlantaOrlando

Mexico CityBeijingBerlin

ShanghaiMadrid

TorontoChicago

MiamiWashington, DC

TokyoSao Paulo

San FranciscoDubai

SydneyHong KongSingapore

LondonNew York

14

Specifically in the luxury market in Atlanta, new hotels have helped stall growth in that segment.

Loews Atlanta Hotel The St. Regis Atlanta Mandarin Oriental, Atlanta

(April 1st, 2010) (April 11th, 2009 ) (May 1st, 2008)

15

Why is much of the Southeast over-supplied (relative to other regions)?

• Pro-growth mindset

• Land availability/few “natural” barriers to entry

• Favorable zoning and entitlement process

• Good weather (longer construction “season”)

• Good airports including worldwide hub in Atlanta

(new international terminal)

• All the major brands want and need to be here

16

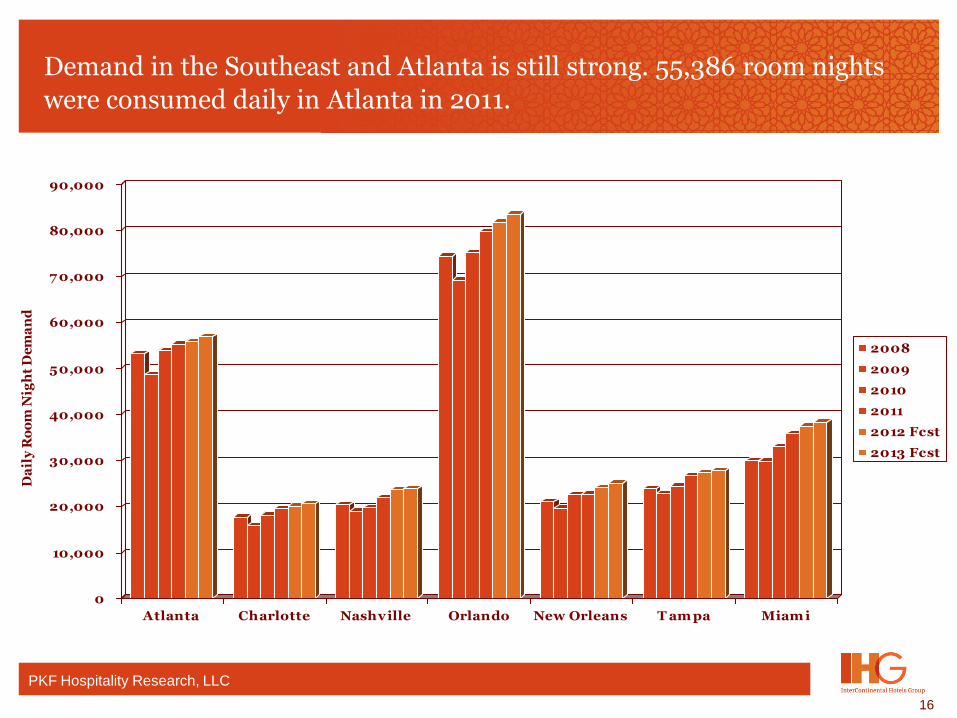

Demand in the Southeast and Atlanta is still strong. 55,386 room nights

were consumed daily in Atlanta in 2011.

PKF Hospitality Research, LLC

0

10,000

20,000

30,000

40,000

50,000

60,000

7 0,000

80,000

90,000

Da

ily

Ro

om

Nig

ht

De

ma

nd

Atlanta Charlotte Nashville Orlando New Orleans T am pa Miam i

2008

2009

2010

2011

2012 Fcst

2013 Fcst

17

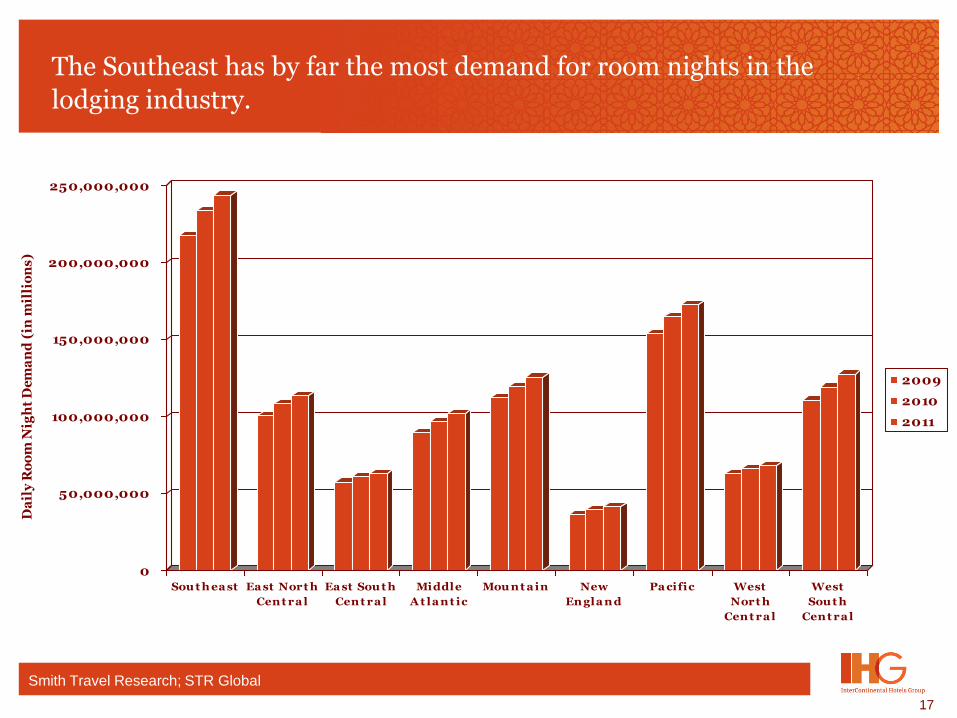

The Southeast has by far the most demand for room nights in the

lodging industry.

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

Da

ily

Ro

om

Nig

ht

De

ma

nd

(in

mil

lio

ns

)

Sou t h ea st Ea st Nort h

Cent ra l

Ea st Sou t h

Cent ra l

Middle

A t la nt ic

Mou nt a in New

Engla nd

Pa cific West

Nort h

Cent ra l

West

Sou t h

Cent ra l

2009

2010

2011

Smith Travel Research; STR Global

18

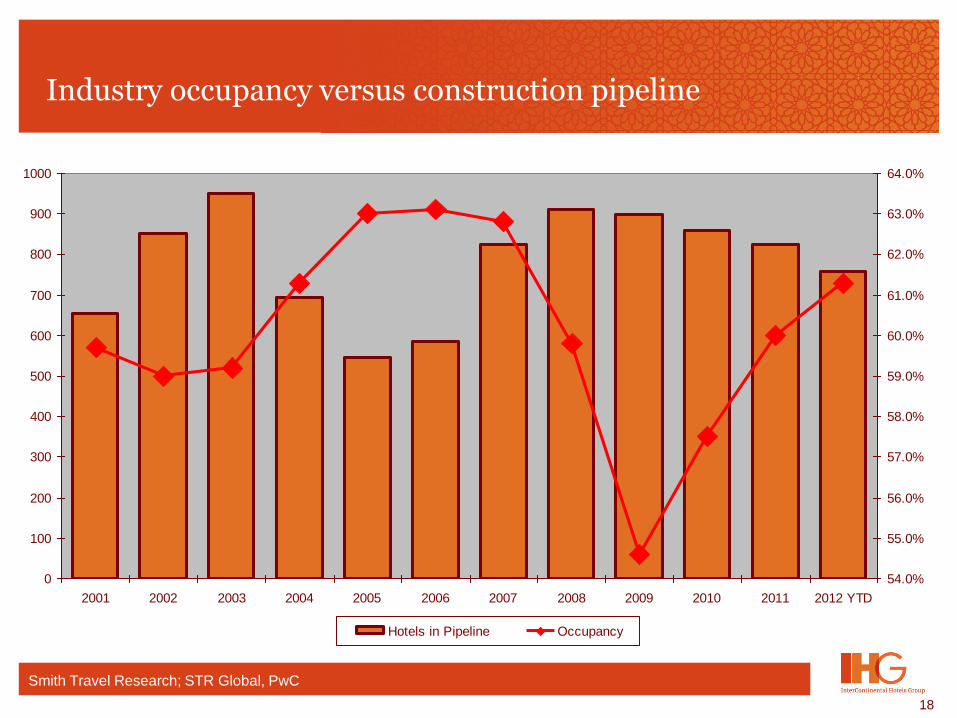

Industry occupancy versus construction pipeline

Smith Travel Research; STR Global, PwC

0

100

200

300

400

500

600

700

800

900

1000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 YTD

54.0%

55.0%

56.0%

57.0%

58.0%

59.0%

60.0%

61.0%

62.0%

63.0%

64.0%

Hotels in Pipeline Occupancy

19

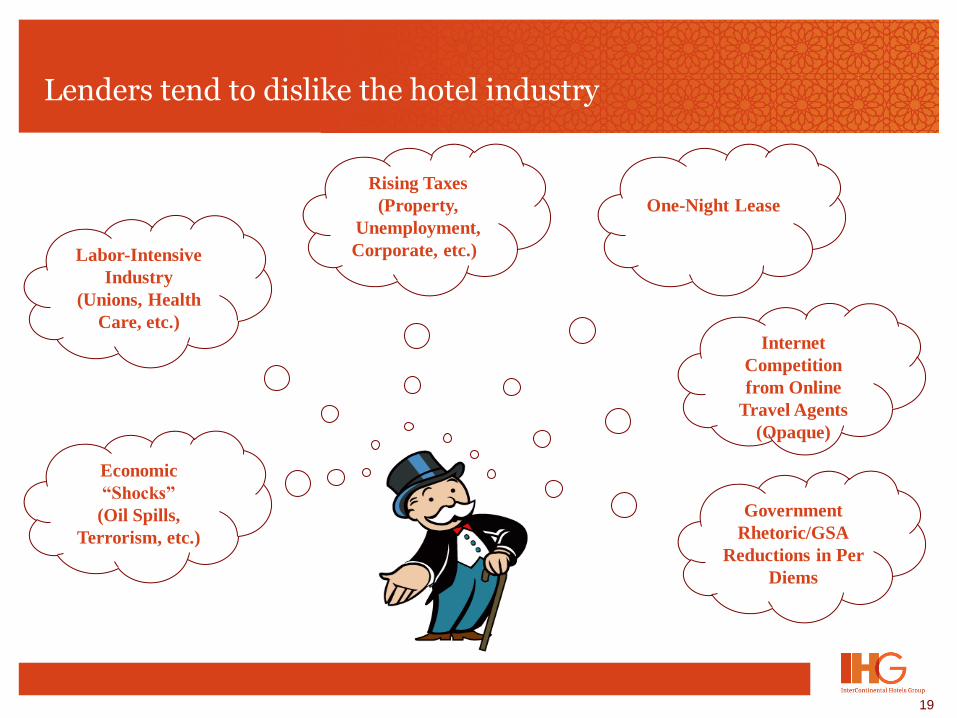

Lenders tend to dislike the hotel industry

One-Night Lease

Government

Rhetoric/GSA

Reductions in Per

Diems

Economic

“Shocks”

(Oil Spills,

Terrorism, etc.)

Rising Taxes

(Property,

Unemployment,

Corporate, etc.)

Labor-Intensive

Industry

(Unions, Health

Care, etc.)

Internet

Competition

from Online

Travel Agents

(Opaque)

20

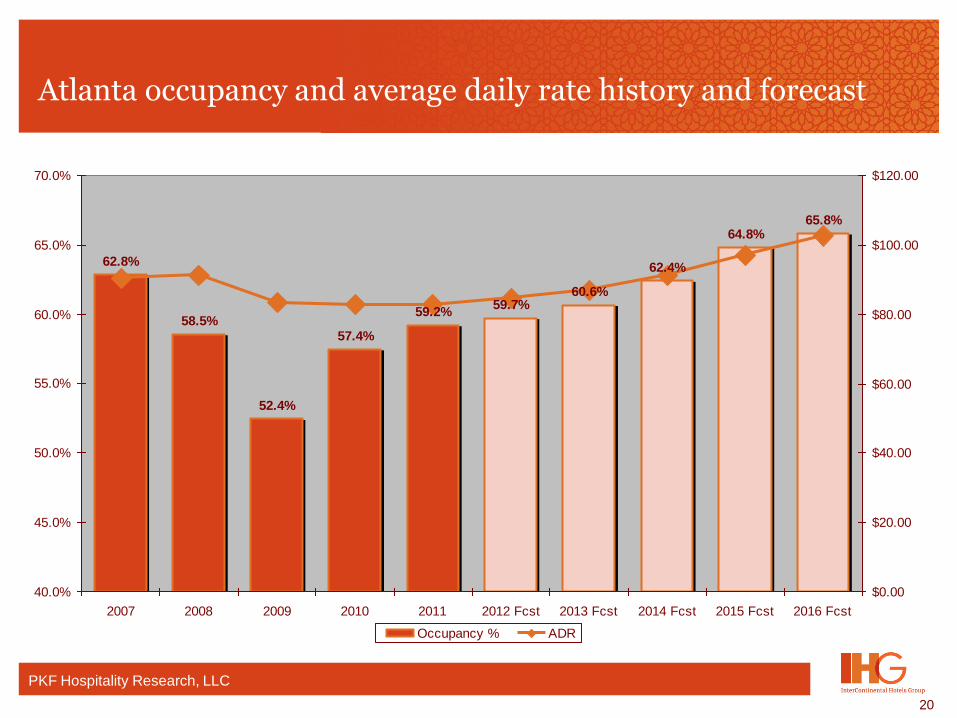

Atlanta occupancy and average daily rate history and forecast

62.8%

58.5%

52.4%

57.4%

59.2%59.7%

60.6%

62.4%

64.8%65.8%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

2007 2008 2009 2010 2011 2012 Fcst 2013 Fcst 2014 Fcst 2015 Fcst 2016 Fcst

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

Occupancy % ADR

PKF Hospitality Research, LLC

21

Summary

• Lodging is a significant contributor to the U.S. economy (that cannot be off-shored or outsourced).

• The lodging industry has rebounded well since 2008.

• Atlanta is a vibrant market, but is perpetually over-supplied with available rooms.

• Slower construction growth should begin to address over-supply over the coming years.

• Very little new supply due to lender apprehension.

• Room demand forecasts for Atlanta and the Southeast are robust.

22

Questions