48

Guidance Note on Connected Transactions A Practical Guide to Good Governance January 2016

Guidance Noteon Connected Transactions

A Practical Guide to Good Governance

January 2016

The Hong Kong Institute of Chartered Secretaries(Incorporated in Hong Kong with limited liability by guarantee)

The Hong Kong Institute of Chartered Secretaries (HKICS) is an independent professional body

dedicated to the promotion of its members’ role in the formulation and effective implementation

of good governance policies as well as the development of the profession of Chartered Secretary

in Hong Kong and throughout Mainland China.

HKICS was first established in 1949 as an association of Hong Kong members of the Institute of

Chartered Secretaries and Administrators (ICSA) of London. It became a branch of ICSA in 1990

before gaining local status in 1994.

HKICS is a founder member of Corporate Secretaries International Association (CSIA) which was

established in March 2010 in Geneva, Switzerland to give a global voice to corporate secretaries and

governance professionals.

HKICS has over 5,800 members and 3,200 students.

1Guidance Note on Connected Transactions | January 2016

Contents

1. Introduction

2. Types of CTs

3. Specified transactions with TPs: Financial assistance to commonly held entity.

LR14A.26

4. Specified transactions with TPs: Acquisition of target company & controller

relationship. LR14A.28

5. The main category: Transactions with CPs – Non-PRC listed issuers (Appendix A)

Step 1 – Is the person within the red boxes?

Step 2 – No other deemed CP relationship

Step 3 – No associates and other deemed CP relationship

Step 3. Box 1 – Immediate family member

Step 3. Box 2 – Family members

Step 3. Box 3 – Relatives

Step 3 – Majority controlled company

Step 3. Box 4 – Associate of a company

6. The main category: Transactions with CPs – PRC listed issuers (Appendix B)

Step 1 – Is the person within the red boxes?

Steps 2 and 3

7. Transactions

8. Compliance requirements

9. Exemptions

Exemption 1: De minimis exception. LR14A.76

Exemption 2: Transactions with connected persons at subsidiary level. LR14A.101

Exemption 3: Financial assistance exemption. LR 14A.87-91

Exemption 4: Issues of new securities by issuer or subsidiaries. LR14A.92

Exemption 5: Dealing in securities on stock exchanges. LR14A.93

Exemption 6: Repurchases of securities by listed issuer or subsidiary. LR14A.94

Exemption 7: Directors’ services contracts and insurances. LR14A.95 and 96

Exemption 8: Buying and selling consumer goods or services.LR14A.97

Exemption 9: Sharing of administrative services. LR14A.98

Exemption 10: Transactions with associates of passive investors. LR14A. 99-100

10. Waivers

11. Conclusion

Appendix A

Appendix B

Disclaimer and Copyright

4

5

6

7

9

20

22

23

24

37

38

40

42

44

Page no.

2

1. Hong Kong has its fair share of concentrated ownership companies, including family

and state-owned companies. The aim of the connected transaction (CT) rules is to

prevent those involved in such concentrated ownership companies from benefiting

from transactions between them and the listed issuers as part of shareholders’

protection, and otherwise for shareholders’ protection generally.

2. Hong Kong’s connected transaction rules which are set out in Chapter 14A of the

Listing Rules are amongst the most advanced globally, and precisely for this reason,

the most complex. It follows that no other area of the Listing Rules attracts more

vexed questions than that of the CT rules.

3. This Guidance Note is general in nature and is intended to provide an overview for

members to acquire a working knowledge of the main provisions of the CT rules. It

is not intended to be a substitute for the CT rules themselves. In addition to the CT

rules, there may be other compliance requirements which members should seek to

comply with.

4. We have used diagrams to make the subject of CT rules more comprehensible and

as quick references to various topics thereunder. We have assumed that the reader

has some knowledge of the Listing Rules and sought to keep explanations to a

manageable level.

5. The materials herein are updated to January 2016. The Main Board Listing Rules are

used as the basis for discussions. Please consult the equivalent GEM rules for a GEM

Board listed issuer.

6. The original version of this Guidance Note is in English. In case of discrepancy, as

and when the Chinese version is released, the English version will prevail.

7. Special gratitude is extended to the following persons from HKICS for their

contributions and suggestions during the preparation of this Guidance Note

(in surname alphabetical order):

April Chan FCIS FCS, Chairman of Technical Consultation Panel (TCP)

Jack Chow FCIS FCS, Chairman of Professional Development Committee (PDC) 2014/2015

Dr Maurice Ngai FCIS FCS(PE), Immediate Past President

Edith Shih FCIS FCS(PE), Past President

Paul Stafford FCIS FCS, Vice-President and Chairman of PDC 2015/2016

Samantha Suen FCIS FCS(PE), Chief Executive

Ivan Tam FCIS FCS, President

Wendy Yung FCIS FCS, member of TCP

PDC members 2014/2015

TCP members 2014/2015

Background

3Guidance Note on Connected Transactions | January 2016

8. Gratitude is also extended to The Stock Exchange of Hong Kong Limited (Exchange) for

permission to reproduce the Listing Rule diagrams (LR diagrams). HKEx has also issued

frequently asked questions (FAQs) and listing decisions relating to CTs (at www.hkex.

com.hk) which serve as useful reference materials.

Daniel Wan Mohan Datwani FCIS FCS (PE)LLB (First Class Honours) LLB LLM PCLL MBA (Iowa) (Distinction) CAMS

Solicitor Solicitor and Accredited Mediator

Joint Authors: (in alphabetical order)

Listing Rules (LR) Chapter 14A sets out 105 CT rules provisions. Why do we

need CT rules?

LR.14A.03 elaborates that there may need to be announcements, circulars, annual reports

disclosures and shareholders’ approvals. Continuing connected transactions (CCTs) further

requires annual reviews by INEDs and auditors

LR14A.04 acknowledges that these may be burdensome, and there will be exemptions and waivers where risk of

abuse by connected persons is low

LR.14A.01 explains CT rules are to protect shareholders as a whole where listed issuer’s

group enters into a CT. LR14A.02 makes it clear that they could include capital and revenue

transactions

4

1 Introduction1.1 Prior to becoming a director of a listed issuer1, an incumbent director would have

signed an undertaking to comply, and to ensure the director’s listed issuer comply

with the Listing Rules (LR). This undertaking extends to compliance with connected

transaction2 (CT) rules under LR Chapter 14A.

1.2 There are 105 CT rules under LR Chapter 14A. They are to protect shareholders

as a whole. Where CT rules apply they could lead to additional announcements,

circulars, annual reports disclosures and shareholders’ approvals requirements

for transactions3 which could be both capital and revenue nature transactions.

Additionally, for continuing connected transactions4 (CCTs), they may require

annual reviews by INEDs and auditors. These compliance requirements could be

burdensome and therefore exemptions are available where the risk of abuse by

connected persons5 (CPs) is low:

Rationale for CT Rules

1.3 Nevertheless, CT rules are complicated. For example, LR14A.06 set outs some 39

definitions relating to CT rules and some of them cross refer back to other LR

provisions. In the context of the complicated nature of CT rules, we hope to make the

topic more comprehensible and manageable.1 LR14A.06(21)2 LR14A.06(11) and 23 to 303 LR14A.06(38) and 244 LR14.06(12) and 315 LR14.06(7) and 7 to 11

Main Category: Transactions with connected persons

(CPs)

Transactions with third parties (TP) where CPs benefits from interests in

entities involved

These can be one off or continuing

connected transactions (CCT)

5Guidance Note on Connected Transactions | January 2016

2 Types of CTs2.1 The main category of CTs are (1) transactions between a listed issuer’s group6,

meaning the listed issuer and its subsidiaries or any of them, and a CP. In addition,

there are (2) transactions with third parties caught under CT rules because of

benefits to CPs from interests in entities involved in transactions. Finally, CTs could

be (3) one off or CCTs7.

Types of CTs

2.2 Before turning to the main category of the regulation of transactions between listed

issuer’s group and CPs, we mention the TP transactions caught under CT rules.

6 LR14A.06(22)7 Please see LR14A.23 generally

X

Company ACompany A

X

The listed issuer

The listed issuer

Subsidiaryof the listed issuer

Scenario 1 Scenario 2

Any shareholding

Any shareholding

>50%

≥10% ≥10%

• Xisaconnectedpersonatthe issuer level

• Boththelistedissuer’sgroupandXareshareholders of Company A,andXholds10%(ormore) of shareholding in Company A.

Company A is a commonly held entity.

Financial assistance provided by the listed issuer’s group to, or received by the listed issuer’s group from, Company A is a connected transaction.

6

3 Specified transactions with TPs: Financial assistance to commonly held entity. LR14A.26

3.1 Where the listed issuer’s group provides or receives financial assistance8, that is,

“granting credit, lending money, or providing an indemnity against obligations under

a loan, or guaranteeing or providing security for a loan”, to or from a commonly

held entity9 (CHE), the CT rules may apply.

3.2 A CHE has amongst its shareholders (1) CPs at the issuer level, who individually or

togetherexerciseorcontrol10%ormoreofthevotingrights,and(2)amemberof

the listed issuer’s group, and hence the commonly held nature of the CHE.

3.3 For such purpose, interests indirectly held10 through the listed issuer’s group are

excluded. The relationship is shown in the LR diagram 17:

The Commonly Held Entity (CHE)

Note: If X held 30% or more of Company A, Company A will be an associate of X and

regarded as a CP to attract the operations of CT rules. The effect of LR14A.26 is to

lower this threshold to 10% or more to attract the operations of the CT rules because

Company A is commonly held by a CP at the issuer level and the listed issuer’s group. It

does not extend to situations where X is a CP at the subsidiary level.

3.4 Please remember to consider CT rules implications when you have transactions

involving financial assistance along with relevant exemptions, if any.

8 LR14A.06(17) and 24(4)9 LR14A.06(6) and 2710 LR14A.06(19)

LR diagram 17

XX

Target CompanyTarget Company

The listed issuerThe listed issuer

Thirdparty

Thirdparty

Subsidiariesof the listed issuer

Subsidiariesof the listed issuer

After the acquisitionBefore the acquisition

15%5% 20% 10%≥10%≥10%

• Xisacontrollerorproposed controller of the listed issuer.

• Xisasubstantialshareholder of the Target Company.

The acquisition of an interest in the Target Company by the listed issuer’s group from the third party is a connected transaction.

7Guidance Note on Connected Transactions | January 2016

LR diagram 18

4 Specified transactions with TPs: Acquisition of target company & controller relationship. LR14A.28

4.1 In acquisition type situations, where a person who is a non-CP is a substantial

shareholderholding10%ormoreofthetargetcompanybeingacquired,theCTrules

may apply. This applies where the person who is a non-CP is, or will be proposed to

be a controller11 of the listed issuer, or an associate12 of a controller. This is shown in

LR diagram 18:

Acquisition and the Controller Relationship

Note: If X held 30% or more of the Target Company, then the Target Company will

be an associate of X and regarded as a CP to attract the operations of CT rules. The

effect of LR14A.28 is to lower this threshold to 10% or more to attract the operation

of the CT rules because of the common ownership of the Target Company with the

listed issuer’s group. It does not extend to situations where X is, or will be proposed

controller, at the subsidiary level.

11 LR14A.06(13) and 28(1)12 LR14A.06(2) and 12 to 15

≥30%

≥10%

X

Target Company

The listed issuer/

its subsidiary

• Xisacontrollerofthelisted issuer.

• Xonlyhasanindirectinterest in the Target Company through the listed issuer’s group.

The acquisition of an interest in the Target Company by the listed issuer’s group from any third party (who is not a connected person) is not a connected transaction.

8

4.2 LR14A.28 defines a controller as a director, chief executive or controlling

shareholder13 of the listed issuer. Any interests indirectly held through the listed

issuer’s group are excluded. This is shown in LR diagram 19:

Exclusion for Indirectly Held Interests

13 LR1.01 defines “controlling

shareholder” as “ any person

(including a holder of depositary

receipts) who is or group of

persons (including any holder

of depositary receipts) who are

together entitled to exercise or

controltheexerciseof30%(or

such other amount as may from

time to time be specified in the

Takeovers Code as being the

level for triggering a mandatory

general offer) or more of

the voting power at general

meetings of the issuer or who

is or are in a position to control

the composition of a majority

of the board of directors of the

issuer; or in the case of a PRC

issuer, the meaning ascribed to

that phrase by rule 19A.14”

LR diagram 19

Director,chief executive,

substantialshareholder

Directorin the last12 months

Supervisor(PRC issuer

only)

Connectedsubsidiary

Deemedconnected

person

Connected person

Associate

9Guidance Note on Connected Transactions | January 2016

5 The main category: Transactions with CPs – Non-PRC listed issuers (Appendix A)

5.1 The main category of CTs are transactions between a listed issuer’s group with

CPs. LR diagram 1, under LR14A.07, sets out the persons who are to be regarded as

connected persons in respect of the listed issuer’s group:

The CP Relationship

Note: If you juxtapose within LR diagram 1 that (1) a substantial shareholder,

holding 10% or more of a member of the listed issuer’s group, could be a person or a

company, and (2) a subsidiary could be wholly or partially owned, and where partially

owned, could have other substantial shareholders at the subsidiary level as CPs, the

above diagram would probably be an over-simplification of the relationships. This

is especially as the relationships extend to (3) associates, and (4) the supervisor, as

defined under LR19A.04, of a PRC listed issuer. Additionally, there is a (5) special

exception for an insignificant subsidiary to brings persons, who would otherwise

be CPs, out of the connected person relationship, and (6) the addition of connected

subsidiaries as connected persons.

5.2 It is with an understanding of these relationships referred under the note to section

5.1 that we have created the two charts relating to CPs of non-PRC listed issuer and

PRC listed issuer under Appendix A and Appendix B respectively. We will go through

Appendix A for non-PRC listed issuers and highlight the additions under Appendix B

for PRC listed issuers.

LR diagram 1

First Wave Connected PersonsLR14A.07(1)&(2)

Connected subsidiaries

Insignificant subsidiary

Any connected person at the issuer

level

>50%

>50%>50%

≥10%

≥10% 100%

100%

≥10%

≥10%

≥10%

SS

SS

SS

Dir /ex Dir CE Dir /ex Dir CE Dir /ex Dir CE

Dir /ex Dir CEDir /ex Dir CE

Corporate shareholder

SS

Dir /ex Dir CE

Non- PRC Listed Issuer

Corporate shareholder

Note: subsidiaries could be partially owned (with or without its own SS); wholly owned (which will not have any other SS); connected (which must have CP at issuer level as SS); and insignificant subsidiary (which can be at any subsidiary level). The diagram is illustrative to bring out these themes

Main Box

10

5.3 Even after you have been through the steps below and determined that there is

unlikely to be any CP relationship in respect of a transaction, please still try to seek

for confirmations from the relevant third parties that the CT rules under Chapter

14A do not apply to them in relation to the proposed transaction as an additional

safeguard, where possible. Please however remember that in the Exchange has the

right to deem any persons as connected persons in relation to a transaction for the

CT rules to apply. The ultimate discretion and interpretations under the Listing Rules

are with the Exchange.

5.4 If you have to determine whether a person is a CP, please start by considering

whether the person is within any of the red boxes of the Main Box of the chart

in Appendix A. If so, the person is a CP. This takes into account the relationships

referred to under the note to section 5.1 above and the discussions under the further

notes below; and all such CPs are called “First Wave Connected Persons”

The Main Box

Step 1 – Is the person within the red boxes?

Dir = Director CE = Chief Executive SS = Substantial Shareholder

Director,chief executive,

substantialshareholder

Directorin the last12 months

Supervisor(PRC issuer

only)

Connectedsubsidiary

Deemedconnected

person

Connected person

Associate

LR diagram 1

11Guidance Note on Connected Transactions | January 2016

Further notes:

The CP Relationship

(1) If you read LR14A.07, you will see that there are 5 types of CPs as set out under the LR

diagram 1 above. We will call the first two types on the left hand boxes corresponding

to LR14A.07(1) and (2) the “first wave connected persons”. That is, for the non-PRC

listed issuers and its subsidiaries, any director, chief executive, substantial shareholder,

and ex-director within the last 12 months. These are everyone within the red boxes in

the chart. As long as you can slot a person into one of the red boxes, the person is a CP.

For PRC listed issuers, the supervisor will be included, under the third box corresponding

to LR14A.07(3) as first wave connected persons. Please refer to Appendix B.

(2) You could also ascertain from the chart who are connected persons at the issuer

level14. These include the issuer’s directors, chief executive, substantial shareholders and

ex-directors within the last 12 months of the issuer and their respective associates.

(3) By the same token, you could ascertain from the chart who are connected person

at the subsidiary level15. These include the directors, chief executive, substantial

shareholders and ex-directors within the last 12 months of the issuer’s subsidiaries,

which could be wholly or partially owned by the issuer, and their respective associates.

(4) Where a person is connected at an insignificant subsidiary16 level, the person is

not to be regarded as a CP. That is, a subsidiary with whose total assets, profits and

revenue compared to that of the listed issuer’s group are less than: (1) 10% for each

of the latest 3 financial years; or (2) 5% for the latest financial year. If the person

is connected with two or more subsidiaries, the Exchange will aggregate them

14 LR14A.06(8)15 LR14A.06(9)16 LR14A.06(20) and 09

100%

The listed issuer

Subsidiary A

>50%

>50%

≥10%

Subsidiary A

Subsidiaryof the listed issuer

The listed issuer

>50%

>50% ≥30%

≥10%

Subsidiary A

Subsidiaryof the listed

issuer

The listed issuerX

LR diagram 13

LR diagram 14

• SubsidiaryAisasubstantial shareholder of another subsidiary of the listed issuer. However, this relationship will not make Subsidiary A a connected person of the listed issuer.

• SubsidiaryAisnotaconnected person.

• Xisasubstantialshareholder of a subsidiary of the listed issuer.

• Xholds30%(ormore)shareholding in Subsidiary A.

Subsidiary A is an associate of X.However,thisrelationship will not make Subsidiary A a connected person of the listed issuer becauseXisonlyaconnected person at the subsidiary level.

LR diagram 12

12

together, and it is 100% of the total assets, profits and revenue that will be used for

the purposes of calculations unless this produces an anomalous result whereby the

Exchange may consider alternative tests provided by the listed issuer.

(5) A subsidiary is not a connected person in general. For the avoidance of doubt,

LR14A.18 states that a subsidiary is not a CP where (1) it is a directly or indirectly

wholly-owned (100%) subsidiary (2) where its substantial shareholder is a subsidiary

of the listed issuer and/or (3) where the connection is with an associate of a

connected person at the subsidiary level. These are set out in LR diagrams 12 to 14:

The Subsidiary Relationship

>50%

>50%

X

Subsidiary E

The listed issuer

Subsidiary D

Scenario 1

≥10%

≥10%

>50%

>50%

X Y

Subsidiary E

The listed issuer

Subsidiary D

Scenario 2

≥10%

≥10%

• Xisaconnectedpersonat the issuer level, and he orithasa10%(ormore)shareholding in Subsidiary A.

Subsidiary A is a connected subsidiary. (See rule 14A.16(1))

• SubsidiariesBandCaresubsidiaries of Subsidiary A.

Subsidiaries B and C are also connected subsidiaries. (See rule 14A.16(2))

• Transactionsbetweenthelisted issuer or Subsidiary D with Subsidiary A/B/C are connected transactions.

• Transactionsbetweenany of Subsidiaries A, B and C are not connected transactions if Subsidiaries B and C are connected solely because of their relationship with Subsidiary A. (See rule 14A.17)

LR diagram 10

Subsidiary D Subsidiary A

Subsidiary B Subsidiary C

The listed issuer

X

>50% >50%

>50% >50%

≥10%

• XandYareconnectedpersons at the issuer level.

Subsidiaries D and E are connected subsidiaries.

• SubsidiaryEisasubsidiaryof Subsidiary D. However, the exemption in rule 14A.17 does not apply to transactions between them because Subsidiary E is a connected subsidiary not only because of its relationship with Subsidiary D but also its relationshipwithXorY.

LR diagram 11

13Guidance Note on Connected Transactions | January 2016

17 LR14A.06(10) and 16

(6) There is a special case in which a subsidiary has a substantial shareholder who

is a connected person at the issuer’s level. This subsidiary is called a connected

subsidiary17 and in itself regarded as a connected person. Please note that any

subsidiary of a connected subsidiary is also a connected subsidiary. These will be the

light blue shaded boxes in the chart. Even then, there is an exemption for transactions

between connected subsidiaries where the only CP relationship arises based on the

same connected person at the issuer level. Please see LR diagrams 10 and 11 for

further details as to the narrow scope of the exemption:

The Connected Subsidiaries Relationship

CONNECTED PERSONS (NON-PRC LISTED ISSUER)

M

“first wave” connected persons: LR14A.07

associates of the “first wave” connected persons such associates are connected persons: LR14A.07(4)

deemed connected persons: having agreement, arrangement, understanding or undertaking (whether formal or informal and whether express or implied) with (1) Dir, CE or SS of the listed issuer or any of its subsidiaries; and (2) ex-Dir of the listed issuer or any of its subsidiaries in the last 12 months: LR14A.20

deemed connected persons: LR14A.21

connected subsidiary and any subsidiary of such connected subsidiary: LR14A.16

chief executive, which is defined as a person who either alone or together with one or more other persons is or will be responsible under the immediate authority of the board of directors for the conduct of the business of a listed issuer. For example, CEO: LR1.01

director / former directors within the last 12 months

substantial shareholder, in relation to a company means a person (including a holder of depositary receipts) who is entitled to exercise, or control the exercise of, 10% or more of the voting power at any general meeting of the company

marriage

CE

SS

Dir /ex Dir

Any connected person at the issuer level (1) Dir, CE, SS of the listed Issuer; (2) ex-Dir of the listed issuer in the last 12 months; and (3) an associate of any of the above: LR14A.06(8)

Insignificant subsidiarysubsidiary whose total assets, profits and revenue compared to that of the listed issuer’s group are less than: (1) 10% for each of the latest 3 financial years; or (2) 5% for the latest financial year: LR14A.09

The Hong Kong Institute of Chartered SecretariesReproduce with suitable acknowledgement.

Last updated: 1 July 2015

Associates of Individual: Immediate Family Members

LR14A.12(1)(c)

LR14A.12(1)

≥30%

>50%

BOX 1

Trustee(s)

SS/Dir/exDir/CE

Beneficiary

Spouse

Child/Step-child (natural or adopted) under 18

M

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

30% - controlled company

Subsidiaries

Associates of company

LR14A.13(3)

LR14A.13

≥30%

>50%

Trustee(s)Holding

Companies

Fellows

Fellows

Corporate shareholder

Subsidiaries

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

BOX 4

>50% >50%

>50%>50%

beneficiary

SS

30% - controlled company

Subsidiaries

LR14A.12(2)(a)Associates of Individual: Family Members

BOX 2

Mother/ Step-mother

Father/ Step-Father

M

Brother/ Step-brother/

Sister/Step-sister

Person(s) cohabitingas a spouse

Son/Step-son/ Daughter/ Step-daughter aged 18 or above

SS/Dir/

exDir/CE

Spouse

M♥

= Already covered by Box 1[1]

[1][1]

First waveconnected person

BOX 3

LR14A.21(1)(a)Relatives

Grandfather Grandfather Grandmother Grandmother

M M

Grandson/Granddaughter = Already covered by Box 1[1] = Already covered by Box 2[2]

First waveconnected person

Spouse of Uncle/Aunt

Sister-in-law/ Brother-in-law

Spouse of Uncle/Aunt

Mother in law

Father in law

Uncle/Aunt

Uncle/Aunt

Cousin Cousin

Nephew/Niece

Daughter-in-law/

Son-in-law

Brother- in-law/

Sister-in-law

M

M M

M

M

Mother/ Step-

mother

Brother/ Step-brother/

Sister/ Step-sister

Son/Step-son/ Daughter/

Step-daughter aged 18 or above

Person(s) cohabitingas a spouse

Father/Step-father

M M[2]

[2] [2]

[2]

[2]

♥SS/Dir/

exDir/CE

[1] [1]Spouse

LR14A.12(2)(b)LR14A.21(1)(b)

>50%

>50%

Individually or together (directly or indirectly) exercise or control the exercise of more than 50% of the voting power at

general meetings or control the composition of a majority of the board of directors

Subsidiaries

Majority-controlled company

First Wave Connected PersonsLR14A.07(1)&(2)

Connected subsidiaries

Insignificant subsidiary

Any connected person at the issuer

level

>50%

>50%>50%

≥10%

≥10% 100%

100%

≥10%

≥10%

≥10%

SS

SS

SS

Dir /ex Dir CE Dir /ex Dir CE Dir /ex Dir CE

Dir /ex Dir CEDir /ex Dir CE

Corporate shareholder

SS

Dir /ex Dir CE

Non- PRC Listed Issuer

Corporate shareholder

Note: subsidiaries could be partially owned (with or without its own SS); wholly owned (which will not have any other SS); connected (which must have CP at issuer level as SS); and insignificant subsidiary (which can be at any subsidiary level). The diagram is illustrative to bring out these themes

Appendix A

Main Box

39

14

(7) A PRC Governmental Body18 is not normally treated as a CP19.

(8) A depository of the listing of a depository receipt will not be regarded as associate of the

holder of the depository receipt or SS or controlling shareholder of the listed issuer20.

(9) The Exchange has power to deem any person as a CP21.

18 LR14A.06(31) and 19A.0419 LR14A.1020 LR14A.1121 LR14A.19

5.5 If the person is not a CP under Step 1, please go on to consider if the person has

with any first wave CP (that is the red person in the Main Box) (1) any agreement,

arrangement, understanding or undertaking, whether formal or informal and whether

express of implied, to potentially be deemed a CP by the Exchange under LR14A.20.

These are the yellow persons under the chart to the first wave connected persons.

5.6 If a person has no CP relationship identified from Steps 1 and 2, you will still need

to go through the rest of the chart to see if the person is an “associate” or “deemed

connected person” and thereby regarded as a CP (which again is expanded from the

LR diagram 1 on pages 9 and 11 based on the LRs indicated). We will go through

each of the boxes in turn. Please note that persons within the red boxes are known

as “first wave connected persons”.

The Associate and Deemed CP Relationships Overview

Step 2 – No other deemed CP relationship

Step 3 – No associates and other deemed CP relationship

Associates of Individual: Immediate Family Members

LR14A.12(1)(c)

LR14A.12(1)

≥30%

>50%

BOX 1

Trustee(s)

SS/Dir/exDir/CE

Beneficiary

Spouse

Child/Step-child (natural or adopted) under 18

M

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

30% - controlled company

Subsidiaries

15Guidance Note on Connected Transactions | January 2016

(1) Step 3. Box 1 – Immediate family member22

The CP relationship extends to a first wave CP’s (that is, the red persons under the

Main Box) immediate family members as shown in the grey boxes. As could be

seen from the diagram, these include trustee, spouse, child, step-child, natural or

adopted, under 18, any 30%-controlled company23 and its subsidiaries. For detailed

definitions as to trustees24and30%-controlledcompany,pleaserefertoLR14A.12:

22 LR14A.12(1)(a)23 LR14A.06(1)24 LR14A.06(39) and 12(1)(b) or

13(2)

LR14A.12(2)(a)Associates of Individual: Family Members

BOX 2

Mother/ Step-mother

Father/ Step-Father

M

Brother/ Step-brother/

Sister/Step-sister

Person(s) cohabitingas a spouse

Son/Step-son/ Daughter/ Step-daughter aged 18 or above

SS/Dir/

exDir/CE

Spouse

M♥

= Already covered by Box 1[1]

[1][1]

First waveconnected person

16

(2) Step 3. Box 2 – Family members25

In addition to immediate family members already covered under Box 2 “[1]”,

the other family members under Box 2 within the grey boxes are also regarded

as associates of the first wave connected person (that is, the red persons under

the Main Box) and therefore CPs themselves. You will see these include a person

cohabiting as a spouse, etc. The grey boxes are self-explanatory:

25 LR14A.06 (16) and 12(2)(a)

BOX 3

LR14A.21(1)(a)Relatives

Grandfather Grandfather Grandmother Grandmother

M M

Grandson/Granddaughter = Already covered by Box 1[1] = Already covered by Box 2[2]

First waveconnected person

Spouse of Uncle/Aunt

Sister-in-law/ Brother-in-law

Spouse of Uncle/Aunt

Mother in law

Father in law

Uncle/Aunt

Uncle/Aunt

Cousin Cousin

Nephew/Niece

Daughter-in-law/

Son-in-law

Brother- in-law/

Sister-in-law

M

M M

M

M

Mother/ Step-

mother

Brother/ Step-brother/

Sister/ Step-sister

Son/Step-son/ Daughter/

Step-daughter aged 18 or above

Person(s) cohabitingas a spouse

Father/Step-father

M M[2]

[2] [2]

[2]

[2]

♥SS/Dir/

exDir/CE

[1] [1]Spouse

17Guidance Note on Connected Transactions | January 2016

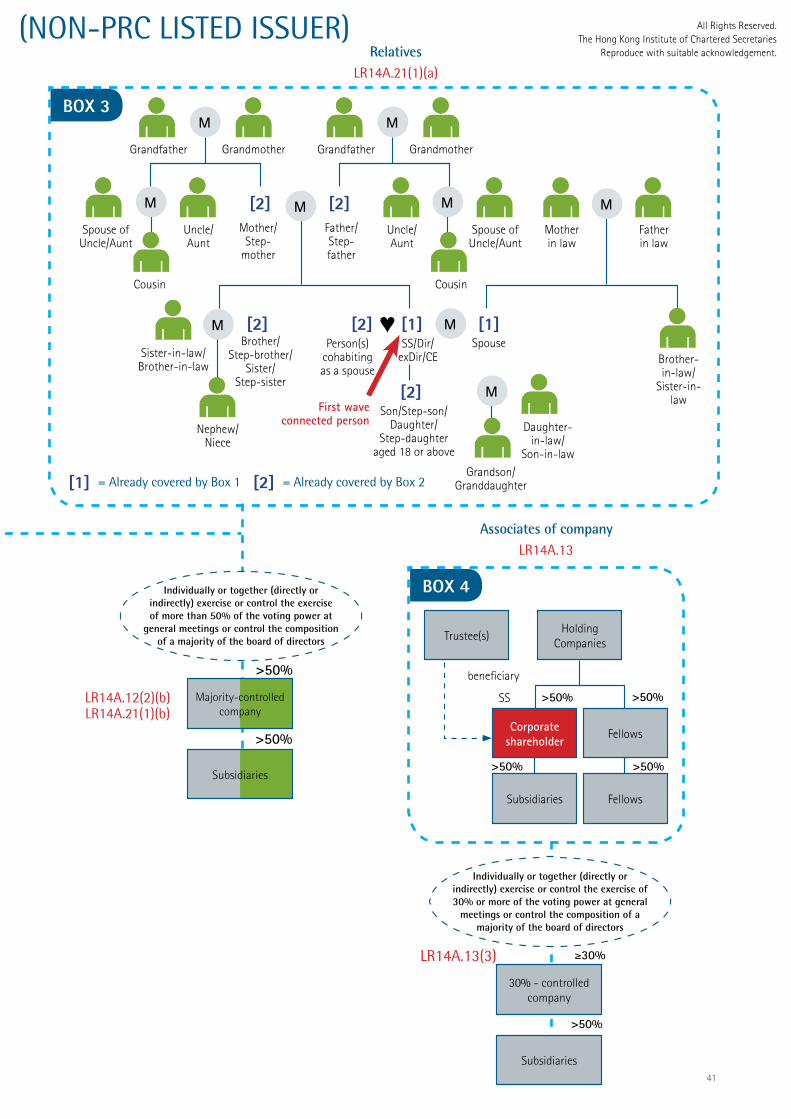

(3) Step 3. Box 3 – Relatives26

In addition to immediate family members and family members already covered under

Box 3 “[1]” and “[2]”, the other relatives under Box 3 within the green boxes are

deemed CPs. The green boxes are self-explanatory:

26 LR14A.06(37) and 21(1)(a)

LR14A.12(2)(b)LR14A.21(1)(b)

>50%

>50%

Individually or together (directly or indirectly) exercise or control the exercise of more than 50% of the voting power at

general meetings or control the composition of a majority of the board of directors

Subsidiaries

Majority-controlled company

18

(4) Step 3 – Majority controlled company27

As seen in the bottom of Box 1, if any immediate family member of first wave CPs

(thatis,theredpersonsundertheMainBox)hasa30%-controlledcompanythen

the company is deemed an associate. Another case is where all persons in Boxes 1, 2

and/or 3 together control a majority-controlled company, then that company and its

subsidiaries are CPs:

27 LR14A.06(23) means “a

company held by a person

who can exercise or control

the exercise of more than

50%ofthevotingpowerat

general meetings, or control

the composition of a majority

of the board of directors”

Associates of company

LR14A.13(3)

LR14A.13

≥30%

>50%

Trustee(s)Holding

Companies

Fellows

Fellows

Corporate shareholder

Subsidiaries

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

BOX 4

>50% >50%

>50%>50%

beneficiary

SS

30% - controlled company

Subsidiaries

19Guidance Note on Connected Transactions | January 2016

(5) Step 3. Box 4 – Associate of a company28

Where the first wave connected person is a company, by necessity as it is not a

natural person, it cannot be a director, chief executive or former director, and it must

be a substantial shareholder. This is because under LR only natural persons could

be directors of listed issuers. LR14A.13 extends the concept of a CP to its associates

shown in the grey boxes, namely trustees, holding company, fellows, subsidiaries and

30%-controlledentitiesandtheirsubsidiaries:

28 LR14A.06 and 13

First Wave Connected PersonsLR14A.07(1)&(2)&(3)

Connected subsidiaries

Insignificant subsidiary

Main Box

>50%

>50%>50%

≥10%

≥10% 100%

100%

≥10%

≥10%

≥10%

SS

SS

SS

ex-Dir

Corporate shareholder

SS

Dir /exDirSP CE

PRC Listed Issuer

Corporate shareholder

Dir /exDirSP CEDir /exDirSP CE Dir /exDirSP CE

Dir /exDirSP CEDir /exDirSP CE

Note: subsidiaries could be partially owned (with or without its own SS); wholly owned (which will not have any other SS); connected (which must have CP at issuer level as SS); and insignificant subsidiary (which can be at any subsidiary level). The diagram is illustrative to bring out these themes

20

6 The main category: Transactions with CPs – PRC listed issuers (Appendix B)

6.1 Please refer to the analysis under Section 5 for non-PRC listed issuers. The only

difference for PRC listed issuers is that a supervisor of a PRC listed issuer and any of

its subsidiaries is to be considered and regarded within the first wave CP.

The Main Box

Step 1 – Is the person within the red boxes?

Individually or together (directly or indirectly) hold 30% or more of the joint venture’s capital or assets

contributions or the share of its profits or income

X (the joint venture

partner)

LR14A.15

Cooperative or contractual

joint venture

Individually or together (directly or indirectly) hold 30% or more of the joint venture’s capital or assets

contributions or the share of its profits or income

X (the joint venture

partner)

LR14A.15

Cooperative or contractual

joint venture

21Guidance Note on Connected Transactions | January 2016

6.2 The similar thought process under Section 5 as with non-PRC listed issuers apply.

That is, you should go through the boxes in Appendix B. You will notice that there

is the additional need to consider the cooperative or contractual joint venture

relationships to identify if a joint venture partner would be regarded as an associate

of a first wave connected person. If it would, the joint venture partner is also a CP.

Steps 2 and 3

Acquisition, disposal, deemed

disposals (LR14A.06 and

LR14.29)

Granting, accepting, exercising,

transferring, or terminating

an option (except on

non-discretionary puts) over assets

or securities subscription,

or not exercising a call

Entering, terminating finance or

operating leases or sub-leases

Granting an indemnity or providing or

receiving financial assistance

Agreement, arrangement to set up joint

venture or joint venture arrangement

22

7 Transactions7.1 We have referred to the main category of CTs as transactions between the listed

issuer’s group and CPs. Thus, in addition to defining who is a CP, there is also the

need to consider what amounts to a transaction.

7.2 As to what constitutes a transaction is relatively straightforward. As set out under

LR14A.24, transactions could be of both capital and revenue nature, and whether in

the listed issuer group’s ordinary course of business or not and extends to:

Types of Transactions

7.3 We will not discuss the details of what amount to transactions, except to point out

that the more complicated area relates to options29, which you will in all likelihood,

be taking in professional advice. The Exchange is considering option pricing as part

of investor protection.

29 LR14A.61

Written Agreement

announcementISA and IBC

(with IFA) inputIssue circular

Disclosure in Annual Report

23Guidance Note on Connected Transactions | January 2016

8 Compliance requirements8.1 In accordance with LA14A.32 to 60, there are many additional compliance

requirements relating to CTs. Subject to exemptions, there may need to be written

agreement, announcement, independent shareholders’ approval with independent

board committee recommendations, usually based on independent financial adviser’s

advice, issue of circulars and disclosures in annual reports. The exemptions are

set out under section 9, and they relate to certain threshold amounts as well as

procedural safeguards for full or partial exemptions set out therein for exemption

from the onerous CT rules which would otherwise be applicable.

The Compliance Requirements Overview

Note: Under LR14A.81, the Exchange will aggregate a series of connected transactions

and treat them as one transaction if they were all entered into or completed within a

12-month period or otherwise related; and 24 months if the connected transactions

are a series of acquisitions of assets being aggregated which may constitute a reverse

takeover.

8.2 For CCTs, additionally, there are additional needs for the agreement to set out

the basis for calculation of the CCTs; not to exceed three years; and with pre-

approved annual caps30. There will be need for re-compliance with these CCT rules

requirements where the cap is exceeded or there is material change to the CCT.

Also auditors need to provide annual confirmation to the board to be filed with the

Exchange relating to compliance with the CCT rules.

8.3 Under LR14A.60, if a continuing transaction subsequently becomes a CCT, the listed

issuer must comply with the annual review and disclosure requirements including

the publishing an announcement and annual reporting, and upon renewal or

variation, comply with all requirements.

30 LR14A.06(4) and 53

Fully exempt from shareholders approval,

annual review by INEDs and auditors and all disclosure

requirements

Exempt from shareholders approval requirement only

Financial assistance

3Transactions with CPs at the subsidiary level

2De minimis

1

Repurchase of securities by issuer or subsidiaries

6Dealings in securities on

stock exchange

5Issues of new securities by issuer or subsidiaries

4

Sharing of administrative costs

9Buying or selling consumer

goods or services

8Directors service

contracts and insurances

7

Transactions with associates of passive investors

10

24

9 Exemptions9.1 Under the CT rules, there are various exemptions. These could range from full

exemptions to partial exemption from shareholders’ approval requirement only.

In most cases, your main task will be to identify if the person is a CP along

with applicable exemptions, if any, in relation to potential transactions with

CT implications. Please remember the need to comply with other compliance

requirements, including Chapter 14 on notifiable transactions.

The Extent of Exemptions

9.2 Under the LR, there are 10 types of exemptions, there are listed below:

Types of Exemptions

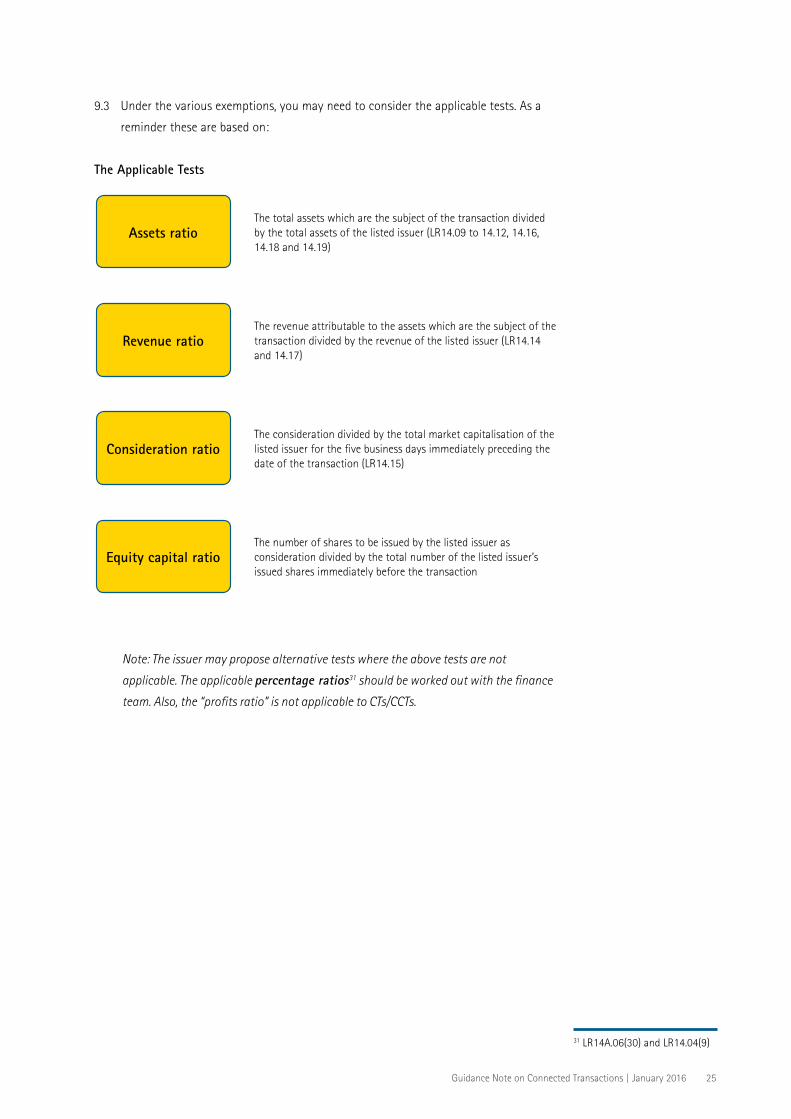

Assets ratioThe total assets which are the subject of the transaction divided by the total assets of the listed issuer (LR14.09 to 14.12, 14.16, 14.18 and 14.19)

Revenue ratioThe revenue attributable to the assets which are the subject of the transaction divided by the revenue of the listed issuer (LR14.14 and 14.17)

Consideration ratioThe consideration divided by the total market capitalisation of the listed issuer for the five business days immediately preceding the date of the transaction (LR14.15)

Equity capital ratioThe number of shares to be issued by the listed issuer as consideration divided by the total number of the listed issuer’s issued shares immediately before the transaction

25Guidance Note on Connected Transactions | January 2016

Note: The issuer may propose alternative tests where the above tests are not

applicable. The applicable percentage ratios31 should be worked out with the finance

team. Also, the “profits ratio” is not applicable to CTs/CCTs.

9.3 Under the various exemptions, you may need to consider the applicable tests. As a

reminder these are based on:

The Applicable Tests

31 LR14A.06(30) and LR14.04(9)

(LR 14A.76)De minimis

Partially exempt

normal commercial terms or better

<5%OR<25%and<$10m

LR14A.76(2)

Fully exempt

normal commercial terms or better:

<0.1%OR<1%withCP

atSubLevelOR <5%and<$3m

LR14A.76(1)

26

9.4 There could be full or partial exemption depending on the size tests and threshold

amounts involved with the CT. This exemption is commonly used in various instances

by listed issuers. Please see diagram below:

De minimis exemption

Note: The partial exemption under Rule 14A.76(2) is in respect of circular, including

independent financial advice and shareholders’ approval requirements.

Note: For CCT, the listed issuer must use the cap as the numerator. If the agreement

covers over one year, the transaction will be classified based on the largest cap during

the term of the agreement.”

9.5 You will see from the diagram that the extent of exemptions depends on the size

of the transactions, with relaxation for CTs at the subsidiary level. Please refer to

the applicable LR for further details where you have a relatively small CT as this

exemption may be applicable.

Exemption 1: De minimis exemption. LR14A.76

A CT between listed issuer’s group and CP at the subsidiary level

on normal commercial terms or better is exempt from the

circular, independent financial advice and

shareholders’ approval requirements if:

listed issuer’s board approved it, and INEDs confirmed the terms

are fair and reasonable on normal commercial

terms or better, and in the interests of the listed issuer and its

shareholders as a whole

Note: In the case of formation of a joint

venture by a qualified issuer and a qualified

connected person to make a qualified

property acquisition, the qualified issuer must announce the transaction as soon as practicable after

receiving notification of the success of the bid by

the joint venture

If any details of the acquisitions or the

joint venture required to be disclosed are not available when the qualified issuer publishes the initial

announcement, it must publish subsequent announcement(s) to

disclose the details as soon as practicable after

they have been agreed or finalized.

27Guidance Note on Connected Transactions | January 2016

9.6 Please remember that where a person is connected at an insignificant subsidiary

level the person is not to be regarded as a CP. This operates as an exclusion of the

person from being a CP. There will be no compliance requirements required under

CT rules. An insignificant subsidiary under LR14A.09 refers to a subsidiary whose

total assets, profits and revenue compared to that of the listed issuer’s group are

lessthan:(1)10%foreachofthelatest3financialyears;or(2)5%forthelatest

financial year.

9.7 Additionally, there is a partial exemption (from the circular, independent financial

advice and shareholders’ approval requirements) under the LR for a transaction with

CPs at the subsidiary level where the transaction is (1) on normal commercial terms

or better, and (2) independent non-executive directors (INEDs) have provided the

confirmation as set forth in the diagram below:

The Subsidiary Exemptions

9.8 In case of formation of joint venture by qualified issuer32 and a qualified

connected person33 to make a qualified property acquisition34, an announcement

will be required upon notification of the successful bid by the joint venture.

Note: Under the Exchange’s FAQ Series 28, FAQ No21B of 29th May 2015 the Exchange

clarifies that transactions or arrangements involving substantial shareholder of a

subsidiary and hence CP at subsidiary level in relation to placing of shares to such CP

is not exempt. Please see the FAQ for further analysis.

Exemption 2: Transactions with connected persons at subsidiary level. LR14A.101

32 LR14A.06(34) and 14.04(10B)33 LR14A.06(33) means a

connected person of the qualified issuer solely because he or it is a substantial shareholder (or its associate) in one or more of the qualified issuer’s non wholly-owned subsidiaries formed to participate in property projects, each of which is single purpose and project specific. This person may or may not have representation on the board of the subsidiary or subsidiaries.

34 LR14A.06(35) and 14.04(10C)

Corporate structure immediately after completion of the transactions

Listco

Target

Others

86% 14%

3 Vendors to sell their interests in Target to Listco (the 3 blue arrows)

Itisdiscloseabletransactionbecause%ratio>5%but<25%

It is connect transaction because the 3 Vendors are connected persons. It is subject to reporting and announcement requirements but not shareholders’ approval, because (a) Listco Board has approved, and (b) all INEDs gave confirmations that the terms of the transaction are fair and reasonable, on normal commercial terms and in the interests of the Listco and its shareholders as a whole

Corporate structure prior to completion of the transactions

Listco

Target

A

C D E F OthersB

Regular subsidiary

100%

6% 10% 10% 10% 14%

99.9%

100%

0.1%

50%

28

9.9 For example, this exemption was used in a recent transaction as follows:

An Illustrative Example

By BC to CP or CHE is fully exempt if on

OrdinaryTerms

By BC to CP or CHE is fully exemptifNOTonOrdinaryTerms but at <0.1%OR

<1%withCPatsublevelOR

<5%and<$3m

(inclusive of monetary advantage

(LR14A.06(25)))

By BC to CP or CHE is partially exempt from

circular ISA/IFA requirements

ifNOTonOrdinaryTerms

but<5%OR<25%and

<10m (inclusive of monetary advantage)

Received by a listed issuer’s group from a CP or CHE is fully exempt if on normal commercial

terms and not secured by the assets of the listed issuer’s

group

By listed issuer’s group

on normal commerical terms and in proportion

to its equity interest

directly held (LR14A.06(15))

in the CP or CHE, and in case of

guarantee on several basis

By listed issuer’s group

is fully exempt if as an indemnity for liabilities incurred in

the course of the director

performing his duties, and in

permitted form in Hong Kong

or place of incorporation

By Banking Companies

Received and Provided by Listed Issuers

29Guidance Note on Connected Transactions | January 2016

9.10 These range from financial assistance provided by a banking company35 (BC)

to CP or CHE; financial assistance provided by the listed issuer’s group to cover

certain liabilities to directors directly or through indemnities; financial assistance

provided by the listed issuer’s group to CP or CHE; and financial assistance received

by the listed issuer’s group from CP or CHE. Most of these have to be on normal

commercial terms or better36 and in ordinary and usual course of business37

(Ordinary Terms), and subject to certain size tests.

Types of Exemptions for Financial Assistance

Exemption 3: Financial assistance exemption. LR 14A.87-91

35 LR14A.06(3) and 8836 LR14A.06(26) 37 LR14A.06(28)

Fully exempt, if pro rata as shareholder,

or where the CP is an underwriter or sub-underwriter

in a rights issue or open offer

Fully exempt under top-up placings and

subscriptions

Fully exempt under apreorpostIPO

share option schemes

30

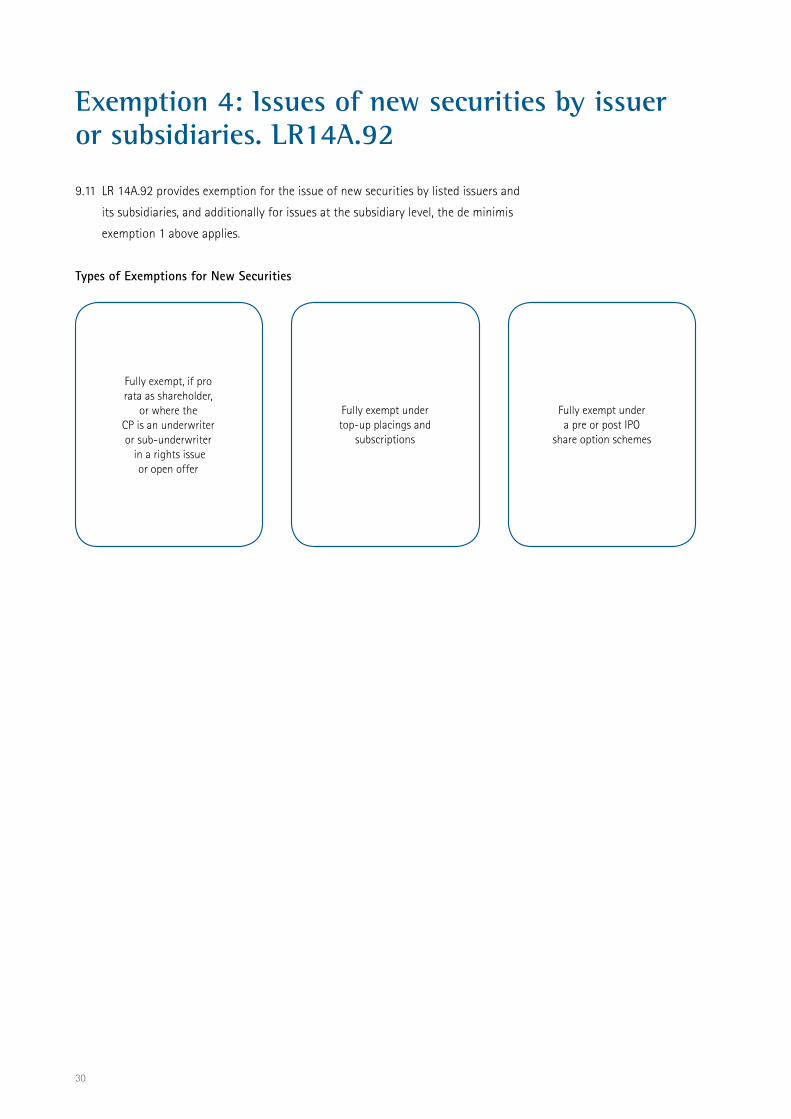

9.11 LR 14A.92 provides exemption for the issue of new securities by listed issuers and

its subsidiaries, and additionally for issues at the subsidiary level, the de minimis

exemption 1 above applies.

Types of Exemptions for New Securities

Exemption 4: Issues of new securities by issuer or subsidiaries. LR14A.92

Dealing by listed issuer’s group in

securities of a target company (acquired under

a LR14A.28 CT) is fully exempt

if in the listed issuer’s group’s ordinary and

usual course of business

The target company’s

securities are listed on HKSE or other recognised

exchanges

The dealings are carried out on market, or off

market with no consideration

moving to or from a connected

person

There is no direct or indirect

benefit to a CP who is a substantial

shareholder of the target company

31Guidance Note on Connected Transactions | January 2016

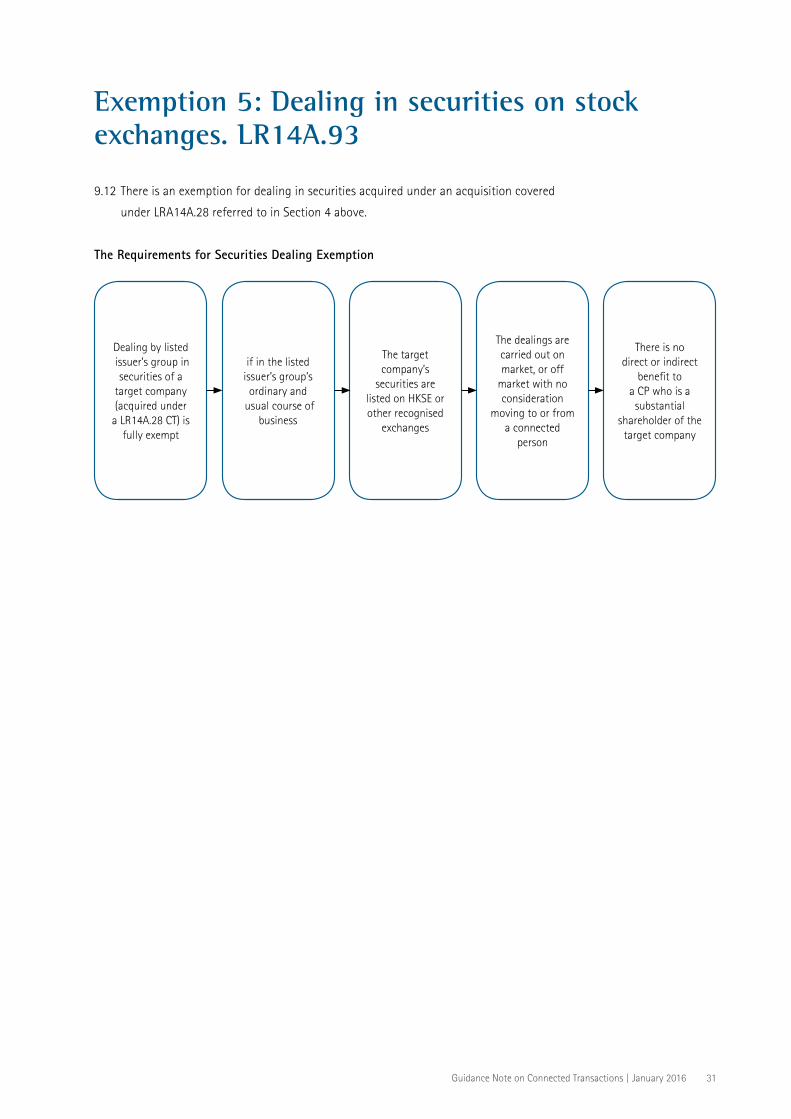

9.12 There is an exemption for dealing in securities acquired under an acquisition covered

under LRA14A.28 referred to in Section 4 above.

The Requirements for Securities Dealing Exemption

Exemption 5: Dealing in securities on stock exchanges. LR14A.93

Repurchases of own securities by a listed

issuer or its subsidiary from a connected person

is fully exempt if it is made:

(2) in a general offer made under the Code on Share Buy-backs.

(1) on HKSE or recognised stock

exchange (LR14A.06), except where the CP knowingly

sells the securities to the listed issuer’s group; or

32

9.13 There is an exemption for repurchases of securities under applicable rules. Please

refer to LR14A.94 for further details:

Types of Repurchases of Securities Exemption

Exemption 6: Repurchases of securities by listed issuer or subsidiary. LR14A.94

LR14A.95, a director entering into a service contract

with the listed issuer or its subsidiary is fully exempt

LR 14A.96, purchase and maintenance of insurance

for a director of the listed issuer or its subsidiaries against liabilities

to third parties that may be incurred in the course of

performing his duties are fully exempt if in

permitted form in Hong Kong or place of

incorporation

33Guidance Note on Connected Transactions | January 2016

9.14 The entering of service contract by directors with the listed issuer or its subsidiary

and purchase of insurances in permitted form under Hong Kong or place of

incorporation are fully exempt from operations of the CT rules.

Directors’ Related Exemptions

Exemption 7: Directors’ service contracts and insurances. LR14A.95 and 96

LR14A.97, a listed issuer’s group buying consumer goods or services as a customer from,

or selling consumer goods or services to, a connected person on normal

commercial terms or better in its ordinary and usual

course of business is fully exempt subject to a host of conditions

as set out therein

The examples are, Meals consumed by a director at a restaurant owned

by the listed issuer’s group, A director buying groceries for his

own use at a retail store operated by the listed issuer’s group, Utilities provided by the listed issuer’s

group to a director’s apartment, or provided by a connected

person to the listed issuer’s group where the prices are published or publicly quoted and apply

to other independent consumers

34

9.15 This is an exception to allow the CP to be in the position of any consumer in relation

to the goods or services of the listed issuer’s group.

The Consumer Exemption

Exemption 8: Buying and selling consumer goods or services. LR14A.97

LR14A.98 Administrative services shared between

the listed issuer’s group and a connected person on a

cost basis are fully exempt, provided

that the costs are identifiable and are allocated to the parties

involved on a fair and equitable basis.

Note: Examples of shared administrative services are shared secretarial,

legal and staff training services.

35Guidance Note on Connected Transactions | January 2016

9.16 This exemption allows the sharing of resources between a CP and a listed issuer’s

group at cost on fair and equitable basis, which is fully exempt from the operations

of the CT rules:

The Administrative Services Exemption

Exemption 9: Sharing of administrative services. LR14A.98

LR14A.100 “passive investor”

is a substantial shareholder of the listed issuer and/or any of its subsidiaries that

is a sovereign fund, or a unit trust or mutual fund authorised by the Securities and Futures

Commission or an appropriate overseas

authority

has a wide spread of investments other than

the securities of the listed issuer’s group and

the associate that enters into the

transaction with the listed issuer’s group

The passive investor (LR14A.06) is CP only as a substantial shareholder of the listed issuer and/or

any of its subsidiaries

It is not controlling shareholder, has no

board representative, not involved in management

or influence including through veto on material

matters of the listed issuer’s group

is independent of the directors, chief executive, controlling shareholder(s) and any other substantial

shareholder(s) of the listed issuer or its

subsidiaries

The transaction is of a revenue nature in

the ordinary and usual course of business of the listed issuer’s group, and

conducted on normal commercial terms or

better

36

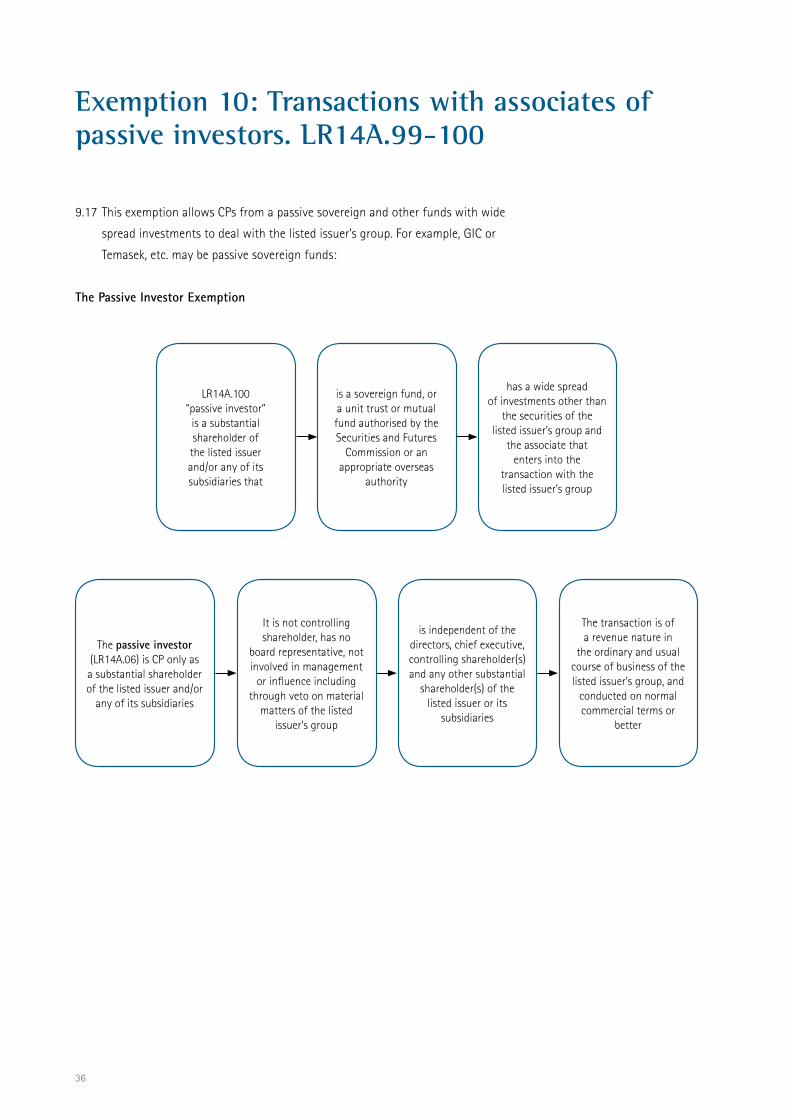

9.17 This exemption allows CPs from a passive sovereign and other funds with wide

spread investments to deal with the listed issuer’s group. For example, GIC or

Temasek, etc. may be passive sovereign funds:

The Passive Investor Exemption

Exemption 10: Transactions with associates of passive investors. LR14A.99-100

37Guidance Note on Connected Transactions | January 2016

10 Waivers 9.18 Please note that the Exchange has wide discretion to waive the application of CT

rules under LR14A.102. This could apply to transactions connected only because

of a non-executive director as CP with the listed issuer’s group. The Exchange may

require auditors and financial adviser’s opinion that the transaction is fair and

reasonable to the shareholders a whole before considering to grant any waiver from

the operations of the CT rules.

9.19 The Exchange may also grant waivers for joint and several guarantee or indemnity

to a TP creditor for obligations of connected subsidiary or a CHE in connection with

public sector contracts awarded by tender where the other shareholders provide

similar guarantee or indemnity, along with an indemnity to the listed issuer to the

extent of the other shareholders’ equity interest in the subsidiary or entity.

9.20 The Exchange may waive the requirements for CCT for a new applicant or its

subsidiaries where the CCT is disclosed in the listing document with sponsor’s

opinion that the CCT is in the ordinary and usual course of business of the listed

issuer’s group, on normal commercial terms or better, are fair and reasonable and in

the interests of the shareholders as a whole.

38

11 Conclusion11.1 We have sought to explain the CT rules with the assistance of diagrams. The above

analysis should assist you to comply with the checklist for CTs in accordance with

LR14A.66. However, we have not been through the detailed drafting requirements

under the CT rules as these are transaction specific and there are ready examples

from the Exchange’s website from disclosures by other listed issuers under CT rules.

39Guidance Note on Connected Transactions | January 2016

CONNECTED PERSONS (NON-PRC LISTED ISSUER)

M

“first wave” connected persons: LR14A.07

associates of the “first wave” connected persons such associates are connected persons: LR14A.07(4)

deemed connected persons: having agreement, arrangement, understanding or undertaking (whether formal or informal and whether express or implied) with (1) Dir, CE or SS of the listed issuer or any of its subsidiaries; and (2) ex-Dir of the listed issuer or any of its subsidiaries in the last 12 months: LR14A.20

deemed connected persons: LR14A.21

connected subsidiary and any subsidiary of such connected subsidiary: LR14A.16

chief executive, which is defined as a person who either alone or together with one or more other persons is or will be responsible under the immediate authority of the board of directors for the conduct of the business of a listed issuer. Forexample,CEO:LR1.01

director / former directors within the last 12 months

substantial shareholder, in relation to a company means a person (including a holder of depositary receipts) who is entitled to exercise, or control theexerciseof,10%ormoreofthevotingpower at any general meeting of the company

marriage

CE

SS

Dir /ex Dir

Any connected person at the issuer level (1) Dir, CE, SS of the listed Issuer; (2) ex-Dir of the listed issuer in the last 12 months; and (3) an associate of any of the above: LR14A.06(8)

Insignificant subsidiarysubsidiary whose total assets, profits and revenue compared to that of the listed issuer’s group are less than: (1)10%foreachofthelatest3financialyears;or(2)5%for the latest financial year: LR14A.09

Last updated: 1 July 2015

Associates of Individual: Immediate Family Members

LR14A.12(1)(c)

LR14A.12(1)

≥30%

>50%

BOX 1

Trustee(s)

SS/Dir/exDir/CE

Beneficiary

Spouse

Child/Step-child (natural or adopted) under 18

M

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

30% - controlled company

Subsidiaries

LR14A.12(2)(a)Associates of Individual: Family Members

BOX 2

Mother/ Step-mother

Father/ Step-Father

M

Brother/ Step-brother/

Sister/Step-sister

Person(s) cohabitingas a spouse

Son/Step-son/ Daughter/ Step-daughter aged 18 or above

SS/Dir/

exDir/CE

Spouse

M♥

= Already covered by Box 1[1]

[1][1]

First waveconnected person

First Wave Connected PersonsLR14A.07(1)&(2)

Connected subsidiaries

Insignificant subsidiary

Any connected person at the issuer

level

>50%

>50%>50%

≥10%

≥10% 100%

100%

≥10%

≥10%

≥10%

SS

SS

SS

Dir /ex Dir CE Dir /ex Dir CE Dir /ex Dir CE

Dir /ex Dir CEDir /ex Dir CE

Corporate shareholder

SS

Dir /ex Dir CE

Non- PRC Listed Issuer

Corporate shareholder

Note: subsidiaries could be partially owned (with or without its own SS); wholly owned (which will not have any other SS); connected (which must have CP at issuer level as SS); and insignificant subsidiary (which can be at any subsidiary level). The diagram is illustrative to bring out these themes

Appendix A

Main Box

CONNECTED PERSONS (NON-PRC LISTED ISSUER) All Rights Reserved.The Hong Kong Institute of Chartered Secretaries

Reproduce with suitable acknowledgement.

Associates of company

LR14A.13(3)

LR14A.13

≥30%

>50%

Trustee(s)Holding

Companies

Fellows

Fellows

Corporate shareholder

Subsidiaries

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

BOX 4

>50% >50%

>50%>50%

beneficiary

SS

30% - controlled company

Subsidiaries

BOX 3

LR14A.21(1)(a)Relatives

Grandfather Grandfather Grandmother Grandmother

M M

Grandson/Granddaughter = Already covered by Box 1[1] = Already covered by Box 2[2]

First waveconnected person

Spouse of Uncle/Aunt

Sister-in-law/ Brother-in-law

Spouse of Uncle/Aunt

Mother in law

Father in law

Uncle/Aunt

Uncle/Aunt

Cousin Cousin

Nephew/Niece

Daughter-in-law/

Son-in-law

Brother- in-law/

Sister-in-law

M

M M

M

M

Mother/ Step-

mother

Brother/ Step-brother/

Sister/ Step-sister

Son/Step-son/ Daughter/

Step-daughter aged 18 or above

Person(s) cohabitingas a spouse

Father/Step-father

M M[2]

[2] [2]

[2]

[2]

♥SS/Dir/

exDir/CE

[1] [1]Spouse

LR14A.12(2)(b)LR14A.21(1)(b)

>50%

>50%

Individually or together (directly or indirectly) exercise or control the exercise of more than 50% of the voting power at

general meetings or control the composition of a majority of the board of directors

Subsidiaries

Majority-controlled company

41

Associates of Individual: Immediate Family Members

LR14A.12(1)(c)

LR14A.12(2)(a)LR14A.12(1)Associates of Individual: Family Members

≥30%

>50%

BOX 1

Trustee(s)

SS/SP/Dir/exDir/CE

Beneficiary

Spouse

Child/Step-child (natural or adopted) under 18

M

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

30% - controlled company

Subsidiaries

“first wave” connected persons: LR14A.07

associates of the “first wave” connected persons such associates are connected persons: LR14A.07(4)

deemed connected persons: having agreement, arrangement, understanding or undertaking (whether formal or informal and whether express or implied) with (1) Dir, CE or SS of the listed issuer or any of its subsidiaries; and (2) ex-Dir of the listed issuer or any of its subsidiaries in the last 12 months: LR14A.20

deemed connected persons: LR14A.21

connected subsidiary and any subsidiary of such connected subsidiary: LR14A.16

chief executive, which is defined as a person who either alone or together with one or more other persons is or will be responsible under the immediate authority of the board of directors for the conduct of the business of a listed issuer. Forexample,CEO:LR1.01

director / former directors within the last 12 months

supervisor

substantial shareholder, in relation to a company means a person (including a holder of depositary receipts) who is entitled to exercise, or control theexerciseof,10%ormoreofthevotingpower at any general meeting of the company

marriageM

CE

SSSP

Dir /ex Dir

Any connected person at the issuer level (1) Dir, CE, SS of the listed Issuer; (2) SP of a PRC issuer; (3) ex-Dir of the listed issuer in the last 12 months; and (4) an associate of any of the above: LR14A.06(8)

Insignificant subsidiarysubsidiary whose total assets, profits and revenue compared to that of the listed issuer’s group are less than: (1)10%foreachofthelatest3financialyears;or(2)5%for the latest financial year: LR14A.09

Individually or together (directly or indirectly) hold 30% or more of the joint venture’s capital or assets

contributions or the share of its profits or income

X (the joint venture

partner)

LR14A.15

Cooperative or contractual joint venture

BOX 2

Mother/ Step-mother

Father/ Step-Father

M

Brother/ Step-brother/

Sister/Step-sister

Person(s) cohabitingas a spouse

Son/Step-son/ Daughter/ Step-daughter aged 18 or above

SS/SP/Dir/

exDir/CE

Spouse

M♥

= Already covered by Box 1[1]

[1][1]

First waveconnected person

First Wave Connected PersonsLR14A.07(1)&(2)&(3)

Connected subsidiaries

Insignificant subsidiary

Any connected person at the issuer

level

>50%

>50%>50%

≥10%

≥10% 100%

100%

≥10%

≥10%

≥10%

SS

SS

SS

ex-Dir

Corporate shareholder

SS

Dir /exDirSP CE

PRC Listed Issuer

Corporate shareholder

Dir /exDirSP CEDir /exDirSP CE Dir /exDirSP CE

Dir /exDirSP CEDir /exDirSP CE

Note: subsidiaries could be partially owned (with or without its own SS); wholly owned (which will not have any other SS); connected (which must have CP at issuer level as SS); and insignificant subsidiary (which can be at any subsidiary level). The diagram is illustrative to bring out these themes

Last updated: 1 July 2015

Main Box

CONNECTED PERSONS (PRC LISTED ISSUER)Appendix B

BOX 3

LR14A.21(1)(a)Relatives

Grandfather Grandfather Grandmother Grandmother

M M

Grandson/Granddaughter

LR14A.12(2)(b)LR14A.21(1)(b)

>50%

>50%

Associates of company

LR14A.13(3)

LR14A.13

≥30%

>50%

Trustee(s)Holding

Companies

Fellows

Fellows

Corporate shareholder

Subsidiaries

Individually or together (directly or indirectly) exercise or control the exercise of 30% or more of the voting power at general

meetings or control the composition of a majority of the board of directors

BOX 4

>50% >50%

>50%>50%

beneficiary

SS

30% - controlled company

Subsidiaries

= Already covered by Box 1[1] = Already covered by Box 2[2]

Spouse of Uncle/Aunt

Sister-in-law/ Brother-in-law

Spouse of Uncle/Aunt

Mother in law

Father in law

Uncle/Aunt

Uncle/Aunt

Cousin Cousin

Nephew/Niece

Daughter-in-law/

Son-in-law

Brother- in-law/

Sister-in-law

M

M M

M

M

Mother/ Step-

mother

Brother/ Step-brother/

Sister/ Step-sister

Son/Step-son/ Daughter/

Step-daughter aged 18 or above

Person(s) cohabitingas a spouse

Father/Step-father

M M[2]

[2] [2]

[2]

[2]

♥SS/SP/Dir/exDir/CE

[1] [1]

Individually or together (directly or indirectly) exercise or control the exercise of more than 50% of the voting power at

general meetings or control the composition of a majority of the board of directors

Individually or together (directly or indirectly) hold 30% or more of the joint venture’s capital or assets

contributions or the share of its profits or income

X (the joint venture

partner)

LR14A.15

Cooperative or contractual joint venture

First waveconnected person

Spouse

Subsidiaries

Majority-controlled company

All Rights Reserved.The Hong Kong Institute of Chartered Secretaries

Reproduce with suitable acknowledgement.

43

CONNECTED PERSONS (PRC LISTED ISSUER)

44

Disclaimer and Copyright

Notwithstanding the recommendations herein, this Guidance Note is not intended to constitute legal advice or to

derogate from the responsibility of HKICS members or any persons to comply with the relevant rules and regulations.

Members and readers should be aware that this Guidance Note is for reference only and they should form their own

opinions on each individual case. In case of doubt, they should consult their own legal or professional advisers, as

they deem appropriate. The views expressed herein do not necessarily represent those of HKICS and/or the joint

authors. It is also not intended to be exhaustive in nature, but to provide guidance in understanding the topic

involved. The Institute and/or the joint authors shall not be responsible to any person or organisation by reason

of reliance upon any information or viewpoint set forth under this Guidance Note, including any losses or adverse

consequences consequent therefrom.

The copyright of this Guidance Note is owned by HKICS. This Guidance Note is intended for public dissemination and

any reference thereto, or reproduction in whole or in part thereof, should be suitably acknowledged.

45Guidance Note on Connected Transactions | January 2016

The Hong Kong Institute of Chartered Secretaries 香港特許秘書公會(Incorporated in Hong Kong with limited liability by guarantee)

Hong Kong Office

3/F Hong Kong Diamond Exchange Building, 8 Duddell Street, Central, Hong Kong

Tel: (852) 2881 6177 Fax: (852) 2881 5050

E-mail: [email protected] Website: www.hkics.org.hk

Beijing Representative Office

Room.15A04,15A/F,DachengTower,No.127XuanwumenWestStreet,XichengDistrict,

Beijing, China PRC 100031

Tel: (8610) 6641 9368 Fax: (8610) 6641 9078

E-mail: [email protected] Website: www.hkics.org.cn

Chartered Secretaries. More than meets the eye.

![GUIDANCE NOTE ON REPORT ONkthemani.com/download/international_taxation/[G] Guidance Note on Report on Int...guidance note on report on international transactions under section 92e](https://static.documents.pub/doc/80x56/5e4e4b8f669779779131f887/guidance-note-on-report-g-guidance-note-on-report-on-int-guidance-note-on-report.jpg)

![Large diameter service connection (LDC) guidance note · Large diameter service connection (LDC) guidance note New connection . 2 Large diameter service connection guidance note [public]](https://static.documents.pub/doc/80x56/5e2019da8663ea0b12457bab/large-diameter-service-connection-ldc-guidance-note-large-diameter-service-connection.jpg)