1 Guidelines on Retirement and Death Section Page Retirement Benefits 1. Introduction 2 2. At a Glance 2 3. Pension Age 3 4. The Lifetime Allowance 3 5. Tax-free Lump Sums 5 6. Flexi-Access Drawdown 6 7. Uncrystallised Fund Pension Lump Sum 7 8. Small Pot Lump Sums 7 9. Annuities 8 10. Crystallised Funds Prior to 6 th April 2015 (Capped Drawdown) 9 11. Income Tax and Pension Payroll 9 12. Risk Warnings 10 13. In-Specie Payments 11 Death Benefits 14. Introduction 12 15. Beneficiaries and Successor Beneficiaries 12 16. Tax on Death Benefits 12 17. Death Benefit Pension Income Options 13 18. Death Benefit Lump Sum Options 13 Contents These guidelines have been produced to assist scheme Members and their Advisers with the options available for payment of benefits on retirement and death from the pension schemes we provide. It does not cover retirement and death benefit options from other types of pension scheme. Please note that neither Whitehall Group (UK) Limited nor Whitehall Trustees Limited give financial advice and nothing in these guidelines should be considered as financial advice. We strongly suggest that you seek advice from an Independent Financial Adviser (IFA) or guidance from the Government’s free advice service Money and Pensions Service www.moneyandpensionsservice.org.uk before making any decisions on your benefits. If you do not already have a Financial Adviser, information can be obtained from www.unbiased.co.uk 0800 020 9430.

Transcript

1

Guidelines on Retirement and Death

Section Page

Retirement Benefits

1. Introduction 2

2. At a Glance 2

3. Pension Age 3

4. The Lifetime Allowance 3

5. Tax-free Lump Sums 5

6. Flexi-Access Drawdown 6

7. Uncrystallised Fund Pension Lump Sum 7

8. Small Pot Lump Sums 7

9. Annuities

8

10. Crystallised Funds Prior to 6th April 2015 (Capped Drawdown)

9

11. Income Tax and Pension Payroll 9

12. Risk Warnings 10

13. In-Specie Payments 11

Death Benefits

14. Introduction 12

15. Beneficiaries and Successor Beneficiaries 12

16. Tax on Death Benefits 12

17. Death Benefit Pension Income Options 13

18. Death Benefit Lump Sum Options 13

Contents

These guidelines have been produced to assist scheme Members and their Advisers with the options available for payment of benefits on retirement and death from the pension schemes we provide. It does not cover retirement and death benefit options from other types of pension scheme.

Please note that neither Whitehall Group (UK) Limited nor Whitehall Trustees Limited give financial advice and

nothing in these guidelines should be considered as financial advice. We strongly suggest that you seek advice

from an Independent Financial Adviser (IFA) or guidance from the Government’s free advice service Money and

Pensions Service www.moneyandpensionsservice.org.uk before making any decisions on your benefits. If you do

not already have a Financial Adviser, information can be obtained from www.unbiased.co.uk 0800 020 9430.

The pension schemes we operate are known as “Money Purchase” or “Defined Contribution”. This means that the level

of benefits payable on retirement or death is not fixed or guaranteed, but is dependent on the amount of funds

available for you when you retire or die. You are able to choose which retirement option is best for you. Pensions paid in

the UK are subject to income tax but not National Insurance.

Your pension scheme will be geared to a Normal Retirement Date which is the expected date of your retirement under

your contract of employment. We will write to you between four and six months before your Normal Retirement Date.

At this point, we will remind you of your retirement options and the value of your pension plan with us. You are not

required to commence retirement benefits at this time and it is also important to stress that you do not have to draw

your retirement benefits from your pension arrangement and are free to shop around for the best deal to suit you. This

is known as the “Open Market Option”.

1. Introduction

2. At a Glance

Those Retiring After 5th April 2015

Those Retired Before 6th April 2015

Tax-free Lump Sum: Usually 25% of your pension fund

Continue receiving

Capped Drawdown

Convert to

Flexi-Access

Drawdown

Flexi-Access

Drawdown

Uncrystallised

Fund Pension

Lump Sum

Annuity

Small Pot Lump

Sum

• Your maximum

pension is

determined by

Government

Actuary rates.

• Your maximum

pension is

reviewed every

three years (and

every year from

age 75).

• Your maximum

ongoing

contributions are

not affected.

• Your pension

becomes

unrestricted.

• Your maximum

ongoing

contributions

are limited to

£4,000 p.a.

• 25% of your fund is paid tax-free.

• You can draw the balance how you choose with no restrictions on amount or frequency.

• The balance is subject to income tax at your marginal rate.

• Your maximum ongoing contributions are limited to £4,000 p.a. where you take a taxable income.

• One-off lump sums paid from your pension fund.

• 25% is tax-free.

• The balance is subject to income tax at your marginal rate.

• Your maximum ongoing contributions are limited to £4,000 p.a.

• This option continues to be available.

• New flexibility allows annuities to fluctuate (called Flexible Annuities).

• Guarantee periods are unlimited.

• Short term annuities are available.

• Your maximum ongoing contributions may be limited to £4,000 p.a. in some cases.

• Similar to Flexi- Access Drawdown.

• Designed for withdrawing all of a small fund.

• Up to three personal pensions or any number of occupational pensions can be paid where each does not exceed £10,000.

• Your maximum ongoing contributions are not affected.

• These options are available from age 55 or on ill-health early retirement.

• They can only be paid if there is available Lifetime Allowance.

3

Retirement benefits can commence at any age from age 55 (rising to age 57 from 6 April 2028). There is no upper limit

to the age at which retirement benefits must commence. Some people have what is known as a “Protected Pension

Age” and they can commence retirement benefits before age 55, i.e. sports people or the police. This right must have

existed before 6th April 2006.

Ill Health Early Retirement

Retirement benefits can be drawn before minimum pension age of 55 on grounds of ill health. To pay ill health early

retirement benefits, we must receive a letter from a registered medical practitioner confirming you are (and will

continue to be) incapable of carrying on your occupation because of physical or mental impairment. You must have

already ceased to carry on your occupation at this time. We also require full details of the impairment. Commencement

of ill health early retirement benefits will be tested against the Lifetime Allowance (see below).

Serious Ill Health Lump Sum

If you have a life expectancy of less than one year, all your uncrystallised funds can be paid as a serious ill health lump

sum. If this is paid after age 75, the lump sum will be subject to your marginal rate of tax. If paid prior to age 75, it is paid

tax-free. We must see a letter from a registered medical practitioner explaining the nature of the illness and confirming

life expectancy is less than one year. This must be provided before any benefits are paid. Payment of a serious ill health

lump sum will be tested against your Lifetime Allowance (see below).

This is the upper limit on the total value of your combined pension arrangements which qualifies for tax exempt

treatment. If your pension arrangements exceed this, you will pay a tax charge when you commence drawing retirement

benefits in excess of the Lifetime Allowance. The amount assessed is the combined value of your tax-free lump sums and

amounts used to pay pensions (even if you choose a nil pension). When you commence benefits, the amount used

towards payment is called a “benefit crystallisation”. The Lifetime Allowance has previously changed from year to year

but, is currently set at £1,073,100 from 2021/22 to 2025/26:

Tax Year Lifetime Allowance

2006/07 £1,500,000

2007/08 £1,600,000

2008/09 £1,650,000

2009/10 £1,750,000

2010/11 £1,800,000

2011/12 £1,800,000

2012/13 £1,500,000

2013/14 £1,500,000

2014/15 £1,250,000

2015/16 £1,250,000

2016/17 £1,000,000

2017/18 £1,000,000

2018/19 £1,030,000

4. The Lifetime Allowance

3. Pension Age

4

2019/20 £1,055,000

2020/21 £1,073,100

2021/22 £1,073,100

Your combined pension arrangements are tested against the Lifetime Allowance when you commence drawing

retirement benefits or at age 75 if you have any uncrystallised funds at that time. These are called “Benefit

Crystallisation Events”. If your benefits are drawn in stages, a separate test is carried out each time to establish whether

you have exceeded the Allowance.

Pension Protection

There are a number of ways in which excess funds over the Lifetime Allowance can be protected from the Lifetime

Allowance Charge. Apart from Individual Protection and Tax-free Lump Sum Protection, these mean no further

pension contributions can be paid for you or by you without losing the protection.

Date Protection Regime Amount Protected

6th April 2006 Enhanced or Primary Protection Any funds over £1,500,000

6th April 2006 Tax-free Lump Sum Protection Accrued entitlement to a tax-free lump sum over 25% of your accumulated pension fund

6th April 2012 Fixed Protection Funds up to £1,800,000

6th April 2014 Fixed Protection 2014 Funds up to £1,500,000

6th April 2014 Individual Protection 2014 Funds in excess of £1.25 million as at 5th April 2014. Your Lifetime Allowance will equal this figure with an overall maximum of £1.5 million. You will not lose Individual Protection if you make pension contributions, meaning if you suffer a fall in the value of your pension savings you can top this up to your Individual Protection figure by making pension contributions (subject to the Annual Allowance / carry-forward rules).

6th April 2016 Fixed Protection 2016 Funds up to £1,250,000

6th April 2016 Individual Protection 2016 This is the same as Individual Protection 2014 except it protects funds in excess of £1 million up to £1.25 million

You have to make an application to HM Revenue & Customs for protection and will receive a certificate from them

detailing the level of your protection. If you have not already applied for one of the earlier protection regimes the

opportunity has been lost however, applications for Fixed Protection 2016 and Individual Protection 2016 have no

closing date. Tax-free lump sum protection only had to be registered with your pension provider at the time. There are

other potential protection regimes where individuals have acquired UK registered pension benefits as a result of a

divorce or a transfer from an overseas pension scheme.

When you crystallise retirement benefits we will send you a statement detailing the percentage of the Lifetime

Allowance you have used-up. We will send you a reminder every year. You must keep these statements safely.

The Lifetime Allowance Charge This is the tax charge you pay where your combined crystallisation events mean you have exceeded your Lifetime Allowance. There are two choices of how to pay a Lifetime Allowance Charge:

5

• If you take the excess over the Lifetime Allowance as a lump sum, the Lifetime Allowance Charge is 55% of the excess.

• If you draw the excess as a pension which is subject to income tax, the up-front Lifetime Allowance Charge is 25%.

Responsibility for the Lifetime Allowance Charge falls jointly between the Scheme Administrator and the Member. The

Lifetime Allowance Charge is payable from the pension fund but must be reported via the member’s self-assessment tax

return. We will provide you with a computation of the charge deducted.

A tax-free lump sum of 25% of the value of your pension arrangements being crystallised can be paid at the point you

commence your retirement benefits. Please note the following points in connection with tax-free lump sums:

• Tax-free lump sums are also called “Pension Commencement Lump Sums” because they can only be paid at the point of commencing retirement benefits.

• A period of 12 months is allowed from benefit commencement to make actual payment of the tax-free sum.

• The overall tax-free lump sum is subject to a limit of 25% of the Lifetime Allowance unless you have registered for protection.

• As mentioned above, those with an entitlement to a tax-free lump sum greater than 25% on the 6th April 2006 were able to protect this if it had been registered.

• In some cases, your tax-free lump sum may have been restricted to less than 25%. For example, a transfer of a fund on divorce to a new scheme for the ex-spouse, where the transferring scheme had already paid a tax-free lump sum.

Tax-free Lump Sum Recycling Regulations do not allow you to receive your tax-free lump sum and use this to increase contributions to another

pension arrangement, thereby benefiting from tax relief on the tax-free lump sum. The rules are as follows:

5. Tax-free Lump Sums

Example: David has no pension protection. He had three pension arrangements.

In February 2017 he commenced retirement benefits from all of arrangement 1. At that time the fund was worth £500,000.

• He has used-up 50% of his Lifetime Allowance leaving him 50%.

In May 2017 he commenced retirement benefits from all of arrangement 2. At that time the fund was worth 200,000.

• He has used-up a further 20% of his Lifetime Allowance leaving him 30%.

In December 2018 he commenced retirement benefits from all of arrangement 3. At that time the fund was worth £400,000.

• He has used-up a further 38.83% of his Lifetime Allowance.

He has now used-up a total of 108.83% of his Lifetime Allowance. The excess amount crystallised was £90,949. He therefore pays

a Lifetime Allowance Charge of 55% on this amount: £50,021.95.

Note: If he had applied for Fixed Protection in April 2016 the Lifetime Allowance Charge would not apply but he would have to have ceased pension

contributions at that time.

6

If HM Revenue & Customs consider you have recycled a tax-free lump sum then the amount received will be taxable.

There are now five potential options available for drawing your retirement benefits. These are explained below:

The amount of fund you crystallise can pay a 25% tax-free lump sum. The balance is paid to you as a pension which is

subject to income tax at your marginal rate. You can choose the amount of pension and frequency you want to receive

from the balance of the fund. This will give you a number of options:

• You may crystallise your entire fund, receive the tax-free lump sum and draw a regular pension from the balance.

• You may crystallise your entire fund, receive the tax-free lump sum and draw the balance as ad-hoc pension payments

as and when you need them.

• You may crystallise a proportion of your fund which pays you a tax-free lump sum plus a pension and is treated as a

Flexi-Access Drawdown Fund where the rest of your fund remains uncrystallised and can be drawn at a later date.

• You may crystallise your entire fund, receive the tax-free lump sum and withdraw all the rest as a pension so you are

no longer a member of the pension scheme.

Please note the following:

You receive a tax-free lump

sum

You significantly increase the amount of

contributions paid to another pension scheme

The tax-free lump sum and

any other lump sums received in the last 12

months exceeds £7,500

The amount of the additional contributions

exceeds 30% of the tax-free lump sum

This recycling was pre-planned

Lifetime Allowance

• The amount of your fund that is crystallised for Flexi-Access Drawdown is tested against your available Lifetime Allowance.

• Any excess over the available allowance is subject to a Lifetime Allowance Charge.

Contributions

• When you commence Flexi-Access Drawdown your future maximum money purchase pension contributions are limited to £4,000 p.a. with no Carry-Forward allowance (please refer to our contribution guideline for details).

Reporting Requirements

• You will receive a statement from us confirming you have commenced Flexi-Access Drawdown.

• You must give this to any other pension scheme providers to which you are paying contributions (or pay in future) or are accruing benefits within 31 days.

6. Flexi-Access Drawdown

7

This is similar to crystallising part of your fund for Flexi-Access Drawdown but the parameters are fixed:

• You receive 25% of the amount crystallised as a tax-free lump sum.

• All of the balance is paid to you as a one-off pension payment which is subject to income tax at your marginal rate.

This option is not available to you if you have Tax-free Lump Sum Protection or Primary or Enhanced Protection and

an entitlement to a tax-free lump sum in excess of £375,000 as at 6th April 2006 (please see above).

Please note the following:

This is similar to an Uncrystallised Fund Pension Lump Sum but your total fund held with the pension scheme we

operate must not exceed £10,000. This means you cannot select this option for payment from the residual balance of a

Flexi-Access Drawdown Fund. The parameters are again fixed:

• You receive 25% of the amount crystallised as a tax-free lump sum.

• All of the balance is paid to you as a one-off pension payment which is subject to income tax at your marginal rate.

• You will cease to be a member of the pension scheme.

Please note the following:

Lifetime Allowance

• The amount of your fund that is paid to you as an Uncrystallised Fund Pension Lump Sum is tested against your available Lifetime Allowance.

• Any excess over the available allowance is subject to a Lifetime Allowance Charge.

Contributions

• When you receive an Uncrystallised Fund Pension Lump Sum your future maximum allowable money purchase pension contributions are limited to £4,000 p.a. with no Carry-Forward allowance (please refer to our contribution guideline for details).

Reporting Requirements

• You will receive a statement from us confirming you have received an Uncrystallised Fund Pension Lump Sum.

• You must give this to any other pension scheme providers to which you are paying contributions (or pay in future) or are accruing benefits within 31 days.

Lifetime Allowance

• The amount of your fund that is paid to you as a Small Pot Lump Sum is NOT tested against your available Lifetime Allowance. It is therefore possible to receive a small lump sum after you have exhuasted all of your lifetime allowance elsewhere.

Contributions

• With this option, your future maximum allowable pension contributions are NOT limited to £4,000 p.a. with no Carry-Forward allowance.

Reporting Requirements

• You will receive a statement from us confirming you have received a Small Pot Lump Sum.

• You DO NOT need to give this to any other pension scheme providers to which you are paying contributions (or pay in future) or are accruing benefits.

7. Uncrystallised Fund Pension Lump Sum

8. Small Pot Lump Sum

8

Your pension is secured with an insurance company. Purchasing an annuity involves removing funds from your scheme

with us and giving them to the insurance company who will pay your pension. You can do this with all or only part of

your fund. If you use your entire fund you will no longer be a member of the Scheme.

You are free to choose any insurance company based in the UK and this is known as the “Open Market Option”. The

insurance company will then pay your pension for the balance of your lifetime. Responsibility for payment of the

pension and income tax lies with the insurance company, and we are no longer accountable for these funds. With a

conventional annuity, when you die any of your fund that has not already been paid to you as a pension is kept by the

insurance company within its annuity pool and is used to pay pensions to other annuitants.

The level of pension paid by the insurance company is secured by using your fund to purchase Government Gilts. For this

reason the underlying level of pension is determined by long term Gilt yields at the time of the annuity purchase, but

with additional factors taken into account depending on the features you select.

There is a range of features you can select which include the following:

Once you have purchased an annuity, you are deemed to have secured your pension income and you cannot convert to

the other pension options described here.

Please note the following:

Features of Annuities

Annual Increases

These can be at a fixed percentage or can be linked to increases in the Retail Prices Index (RPI), but the rate of increase must not exceed the higher of 5% p.a. or the annual increase in RPI.

Beneficiary's Annuity

On your death, the pension continues to be paid to your beneficiaries.

A Guarantee Period

This is where the pension continues to be paid after your death to your beneficiaries for the remainder of the guarantee period.

With-Profit Annuities

The level of pension fluctuates in line with the performance of an underlying with-profits fund.

Unit-Linked Annuities

The level of pension fluctuates in line with the performance of underlying unit-linked funds.

Temporary Annuities

The pension is paid for a short-term only and then ceases.

Flexible Annuities

New flexibility will allow annuities to fluctuate.

).

Impaired Life Annuities

In cases of poor health, increased levels of annuity may be payable due to a shorter life expectancy.

These are assessedon an individualbasis and requiremedical evidence.

Lifetime Allowance

• An annuity purchase is tested against your available Lifetime Allowance.

• Any excess over the available allowance is subject to a Lifetime Allowance Charge

Contributions

• When you purchase a Flexible Annuity your future maximum allowable pension contributions are limited to £4,000 p.a. with no Carry-Forward allowance (please refer to our contribution guideline for details).

Reporting Requirements

• If you purchase a Flexible Annuity you will receive a statement from us to confirm this.

• You must give this to any other pension scheme providers to which you are paying contributions (or pay in future) or are accruing benefits within 31 days.

9. Annuity Purchase

9

Capped Drawdown is pension income drawdown that was available before 6th April 2015. The maximum Capped

Drawdown is determined by the Government Actuary’s rates and is reviewed every three years (every year after age 75).

Your options are:

You can also use your Capped Drawdown fund to purchase an annuity at any time.

Your pension must be subject to income tax, but not National Insurance and must be paid via PAYE.

We operate a pension payroll system used by many of our clients. Our fees are outlined in our Fee Schedule.

We will apply a rate of income tax using your existing tax code or P45 if you have one. If you do not know this we will

apply an emergency basic rate tax code until HMRC advise us of the tax code applicable, which is used from then on. Any

additional tax payable by you must be dealt with via your self-assessment tax return. If you have overpaid income tax via

PAYE there are forms available from HM Revenue & Customs for you to reclaim this.

It is your responsibility to ensure that sufficient cash is available to cover ongoing pension payments.

Our pension payroll can be paid monthly, quarterly, half yearly or annually, in advance or in arrears. Ad-hoc payments

can also be made if required although there is an additional fee for these. We pay pensions using a bank account with

the Royal Bank of Scotland. For regular payments we require a standing order for the gross amount to be set up from

the pension scheme account to the payroll account to reach the account on 15th of the month. We pay your pension by

BACS on 24th of the month. Please note that no amendments can be made to a regular pension and no one-off payments

can be arranged after 16th of March in each tax year due to the Government’s Real Time Information (RTI) requirements.

The reason for requiring funds early is to ensure they arrive on time, the amount is correct and they are cleared funds by

24th of the month. This gives us time to rectify any banking errors or underpayments.

If you choose not to use our pension payroll, the gross pension payable needs to be transferred to the relevant payroll

account in time for the payroll run. Please note that pension payments made as Flexi-Access Drawdown and

Uncrystallised Fund Pension Lump Sums must be reported separately to HM Revenue & Customs under RTI rules.

Continue with Capped Drawdown

(with reviews every three years)

• Your maximum ongoing contribution rate is NOT affected.

• If you have uncrystallised funds these can be used to pay Capped Drawdown without affecting your maximum ongoing contributions.

Convert to Flexi-Access Drawdown

• Your pension is unrestricted.

• There is no test against the Lifetime Allowance.

• Your maximum ongoing contributions WILL be restricted to £4,000 p.a. with no carry-forward allowance.

• You will receive a statement from us as outlined above.

11. Income Tax and Pension Payroll

10. Crystallised Funds Prior to 6th April 2015 (Capped Drawdown)

10

Overseas Residents

If you are a non UK Taxpayer who is resident in another country, then provided it has a double taxation agreement with

the UK, you should be eligible to receive your UK pension gross, without deduction of UK income tax. You will need to

complete a double taxation agreement claim form with the tax authorities in your country of residence and once

approved by them, this should be submitted to HMRC in the UK for authorisation. The HMRC guidance notes and

paperwork to apply for gross payments are known as HS304.

We will need a copy of your HMRC authorisation to commence making gross pension payments. There are bank charges

involved with making foreign payments which are deducted automatically from your cash account. It should also be

noted that payment of pensions abroad can be affected by currency fluctuations.

Unlike conventional annuities where the insurance company guarantees payment of your pension for the rest of your

life, it is important that if you are considering Flexi-Access Drawdown, Uncrystallised Fund Lump Sums or a Flexible

Annuity, you understand and appreciate the risks involved. Some of the key points are outlined as follows:

Are you aware of the implications if you withdraw your entire pension fund in the early stages of your retirement?

A pension scheme is designed to produce an income in your retirement for the rest of your life which could be many years. If you withdraw your entire fund early and spend it, you may have no source of income for your old age.

Are you aware of the income tax implications of the option you have chosen?

• You pay income tax on the amount withdrawn in excess of your tax-free lump sum. This may be paid at a higher rate than you presently pay.

• Once the funds are held by you personally, any income generated may be subject to income tax, which is not payable on income on funds in the pension scheme.

Are you aware of the inheritance tax implications of the option you have chosen?

Once funds are held by you personally they form part of your estate and may be subject to inheritance tax when you die, which is not payable on funds in the pension scheme.

Are you aware of the capital gains tax implications of the option you have chosen?

Once funds are held by you personally any capital gains on investments you make may be subject to capital gains tax, which is not payable on capital gains in the pension scheme.

Are you expecting your pension withdrawals to maintain your lifestyle throughout your retirement?

Your pension scheme may need to support you for many years and may not be sufficient to maintain your current lifestyle.

Are you aware of the effect your pension withdrawals may have on any means-tested benefits you receive?

Funds held by you personally will be included in any means-tested benefit calculations and you may no longer qualify for valuable means-tested benefits.

Are you aware that, in the event of your insolvency, your creditors will have a claim over the funds you withdraw from your pension?

Funds held in a pension scheme are usually protected from your creditors if you become insolvent. If you withdraw money from your pension fund, your creditors will be able to claim this.

Do you intend to pay future pension contributions in excess of £4,000 p.a.?

If you do, you will not be able to if you withdraw funds from your pension scheme as Flexi-Access Drawdown,

12. Risk Warnings

11

Uncrystallised Fund Lump Sums or a Flexible Annuity.

Are you aware that other pension products are available to pay your pension income?

There are many different pension options and products available to you. You need to be careful that you have chosen the best one to suit you.

Are you withdrawing funds from your pension to invest elsewhere?

It is possible you could make the investment with the pension scheme and do not have to withdraw the funds.

If you are withdrawing funds from your pension to invest elsewhere, are you aware of the tax treatment of these investments?

Most investment gains and income received by a pension scheme is tax-free. If you make investments personally, it is likely you will have to pay tax on these.

If you are withdrawing funds from your pension to invest elsewhere, are you aware of the fees and charges for these investments?

Some investments involve high fees and charges. You need to be sure you know all the costs involved before deciding to proceed.

Are you aware that investment scams exist and you should be careful where you invest money withdrawn from your pension?

You may be approached by individuals offering enticing investment opportunities who encourage you to withdraw all your pension savings to make the investment. You need to be wary of these opportunities as they may be fraudulent.

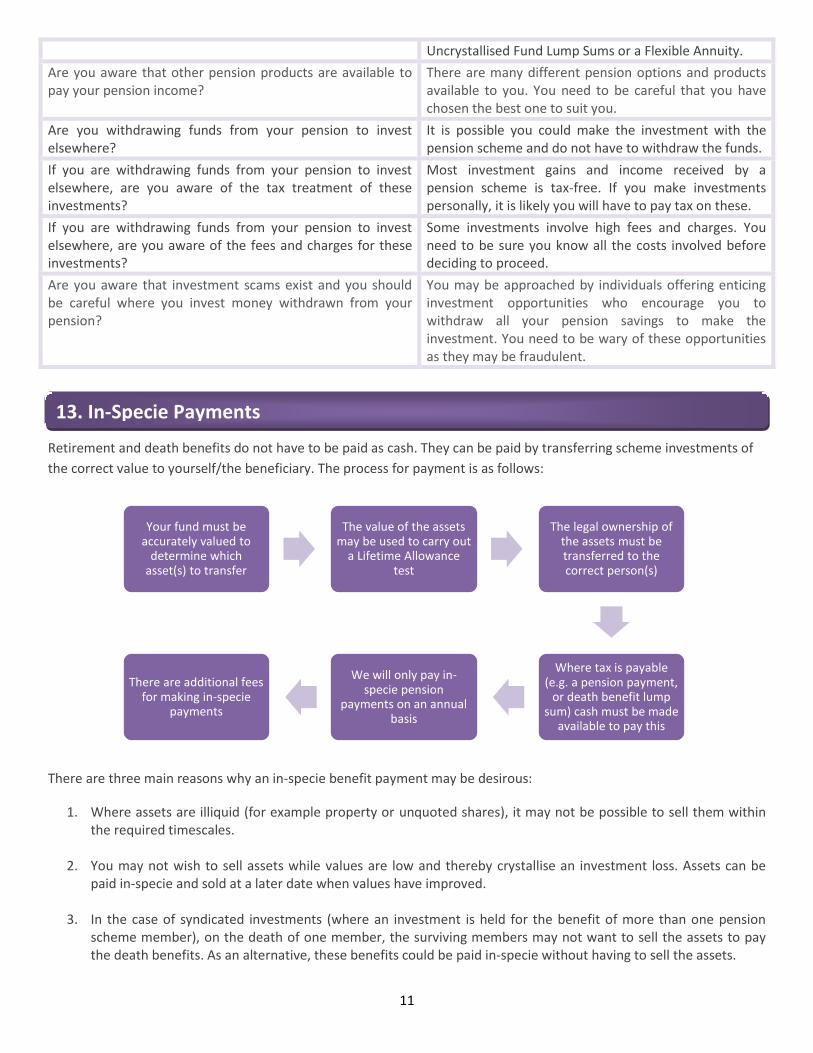

Retirement and death benefits do not have to be paid as cash. They can be paid by transferring scheme investments of

the correct value to yourself/the beneficiary. The process for payment is as follows:

There are three main reasons why an in-specie benefit payment may be desirous:

1. Where assets are illiquid (for example property or unquoted shares), it may not be possible to sell them within the required timescales.

2. You may not wish to sell assets while values are low and thereby crystallise an investment loss. Assets can be

paid in-specie and sold at a later date when values have improved.

3. In the case of syndicated investments (where an investment is held for the benefit of more than one pension scheme member), on the death of one member, the surviving members may not want to sell the assets to pay the death benefits. As an alternative, these benefits could be paid in-specie without having to sell the assets.

Your fund must be accurately valued to

determine which asset(s) to transfer

The value of the assets may be used to carry out

a Lifetime Allowance test

The legal ownership of the assets must be transferred to the correct person(s)

Where tax is payable (e.g. a pension payment,

or death benefit lump sum) cash must be made

available to pay this

We will only pay in-specie pension

payments on an annual basis

There are additional fees for making in-specie

payments

13. In-Specie Payments

12

Your pension scheme can pay benefits to beneficiaries on your death. They will inherit your remaining pension fund.

The amount and type of benefits depends on the amount held in your fund, your age when you die and the benefit

option chosen by your beneficiaries.

Funds held in your pension scheme do not form part of your estate when you die and have separate tax treatment.

We require an original or certified copy of the death certificate before we can commence paying death benefits.

Death benefits must be paid or “designated” for payment (i.e. the benefit option selected) within two years of death for those who die before age 75 otherwise any payments made will be subject to the same tax treatment as those who die after age 75. Beneficiaries

Death benefits can be paid to anyone so you are free to choose who you want to be your beneficiary(ies).

We ask you to nominate your beneficiary(ies) and the proportion of your fund you wish each one to receive when you

join your pension scheme. These can be amended at any time. We will then be guided by your nomination. If no

nomination is completed then we will pay benefits at our discretion.

When paying death benefits we require evidence of identity of the beneficiary(ies): please see our guideline on evidence

of identity for details.

Beneficiaries can choose either to withdraw the available fund on death as a lump sum or can select a pension option

whereby they become a trustee of the pension scheme and the relevant proportion of the deceased member’s fund is

allocated to them to pay the pension selected. The pension scheme then continues to operate and be invested in

accordance with the trustees’ decisions.

Successor Beneficiaries

Beneficiaries who select a pension option can nominate their own beneficiaries, known as “successor beneficiaries”.

When they die, any funds remaining in the pension scheme are then paid to the successor beneficiary(ies) in accordance

with their chosen benefit option.

Death before 75

• On death before age 75 all death benefits whether paid as lump sums or pensions are paid tax-free to the

beneficiary(ies).

Death After 75

• On death after age 75 all death benefits whether paid as lump sums or pensions are paid subject to the

beneficiary(ies) marginal income tax rate.

14. Death Benefits: Introduction

15. Beneficiaries and Successor Beneficiaries

16. Tax Treatment

13

Notes

• Any tax payable must be paid via PAYE (please see above).

Tax on benefits paid to successor beneficiaries is determined by the age of the original beneficiary when they

die.

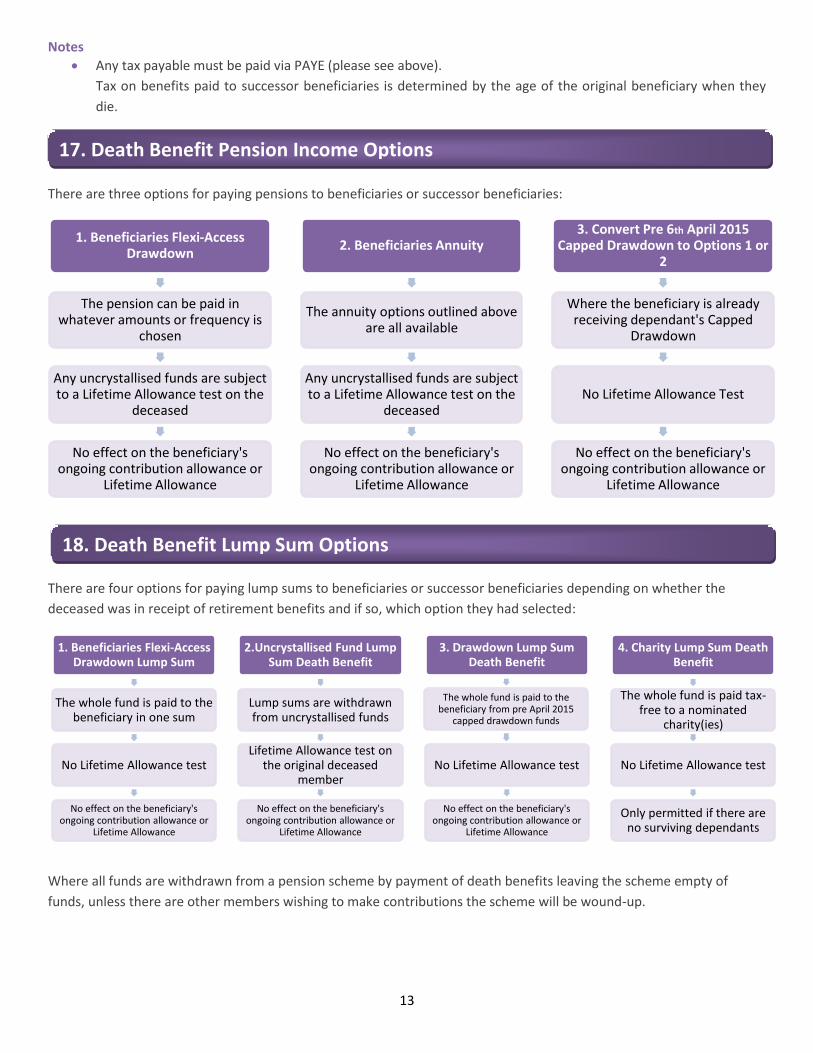

There are three options for paying pensions to beneficiaries or successor beneficiaries:

There are four options for paying lump sums to beneficiaries or successor beneficiaries depending on whether the

deceased was in receipt of retirement benefits and if so, which option they had selected:

Where all funds are withdrawn from a pension scheme by payment of death benefits leaving the scheme empty of

funds, unless there are other members wishing to make contributions the scheme will be wound-up.

1. Beneficiaries Flexi-Access Drawdown

The pension can be paid in whatever amounts or frequency is

chosen

Any uncrystallised funds are subject to a Lifetime Allowance test on the

deceased

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

2. Beneficiaries Annuity

The annuity options outlined above are all available

Any uncrystallised funds are subject to a Lifetime Allowance test on the

deceased

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

3. Convert Pre 6th April 2015 Capped Drawdown to Options 1 or

2

Where the beneficiary is already receiving dependant's Capped

Drawdown

No Lifetime Allowance Test

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

1. Beneficiaries Flexi-Access Drawdown Lump Sum

The whole fund is paid to the beneficiary in one sum

No Lifetime Allowance test

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

2.Uncrystallised Fund Lump Sum Death Benefit

Lump sums are withdrawn from uncrystallised funds

Lifetime Allowance test on the original deceased

member

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

3. Drawdown Lump Sum Death Benefit

The whole fund is paid to the beneficiary from pre April 2015

capped drawdown funds

No Lifetime Allowance test

No effect on the beneficiary's ongoing contribution allowance or

Lifetime Allowance

4. Charity Lump Sum Death Benefit

The whole fund is paid tax-free to a nominated

charity(ies)

No Lifetime Allowance test

Only permitted if there are no surviving dependants

17. Death Benefit Pension Income Options

18. Death Benefit Lump Sum Options

14

These guidelines are based on our understanding of current law and HM Revenue & Customs practice, which are subject to change.

April 2021 item code 06.1.8

To Proceed - Commencing Retirement or Death Benefits

Items Required

✓ You may need to arrange investment encashment to ensure sufficient funds are available to pay your retirement benefits.

Benefit Request Form

Current valuation of pension scheme assets

Evidence of identity for beneficiaries for payment of death benefits

Whitehall is the trading name of: Whitehall Group (UK) Limited, a company registered in England and Wales (Registered number 07625300), Whitehall Trustees Limited, a company

registered in England and Wales (Registered number 07625294) and Whitehall Corporate Limited, a company registered in England and Wales

(Registered number 7759590). All three companies have their registered office at 41 Greek Street, Stockport, Cheshire, SK3 8AX.