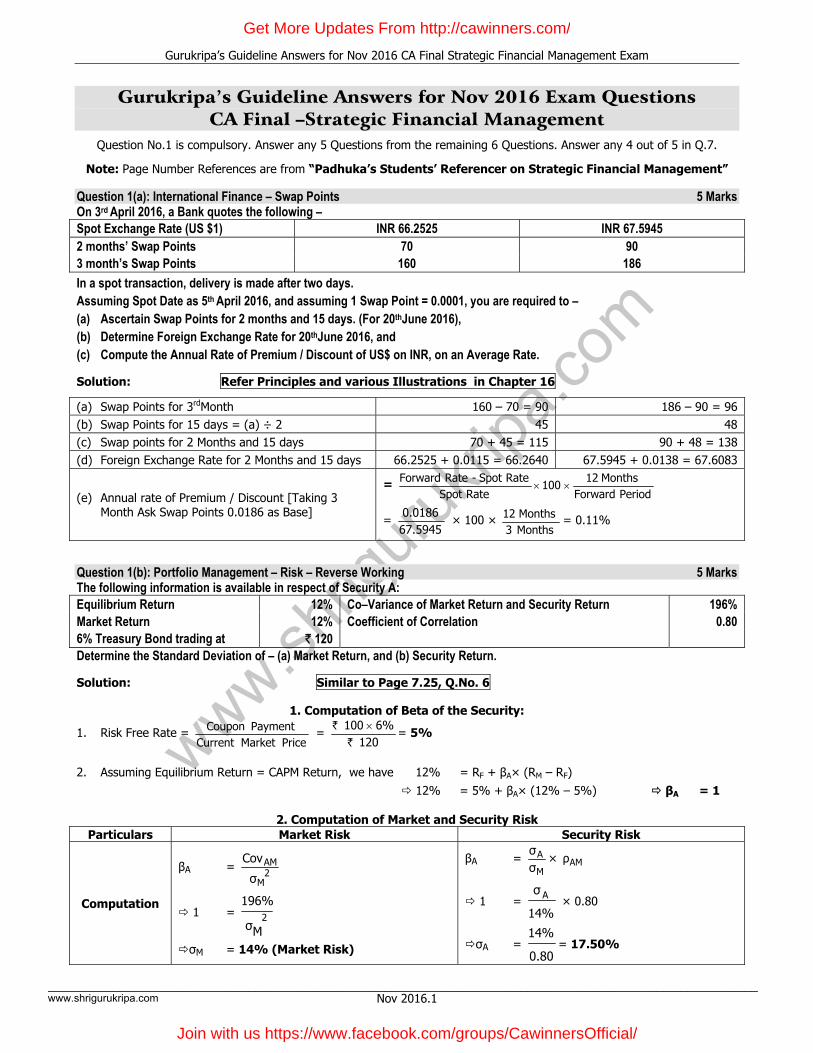

www.shrigurukripa.com Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam Nov 2016.1 Gurukripa’s Guideline Answers for Nov 2016 Exam Questions CA Final –Strategic Financial Management Question No.1 is compulsory. Answer any 5 Questions from the remaining 6 Questions. Answer any 4 out of 5 in Q.7. Note: Page Number References are from “Padhuka’s Students’ Referencer on Strategic Financial Management” Question 1(a): International Finance – Swap Points 5 Marks On 3 rd April 2016, a Bank quotes the following – Spot Exchange Rate (US $1) INR 66.2525 INR 67.5945 2 months’ Swap Points 70 90 3 month’s Swap Points 160 186 In a spot transaction, delivery is made after two days. Assuming Spot Date as 5 th April 2016, and assuming 1 Swap Point = 0.0001, you are required to – (a) Ascertain Swap Points for 2 months and 15 days. (For 20 th June 2016), (b) Determine Foreign Exchange Rate for 20 th June 2016, and (c) Compute the Annual Rate of Premium / Discount of US$ on INR, on an Average Rate. Solution: Refer Principles and various Illustrations in Chapter 16 (a) Swap Points for 3 rd Month 160 – 70 = 90 186 – 90 = 96 (b) Swap Points for 15 days = (a) ÷ 2 45 48 (c) Swap points for 2 Months and 15 days 70 + 45 = 115 90 + 48 = 138 (d) Foreign Exchange Rate for 2 Months and 15 days 66.2525 + 0.0115 = 66.2640 67.5945 + 0.0138 = 67.6083 (e) Annual rate of Premium / Discount [Taking 3 Month Ask Swap Points 0.0186 as Base] = Period Forward Months 12 100 Rate Spot Rate Spot - Rate Forward × × = 67.5945 0.0186 × 100 × Months 3 Months 12 = 0.11% Question 1(b): Portfolio Management – Risk – Reverse Working 5 Marks The following information is available in respect of Security A: Equilibrium Return 12% Co–Variance of Market Return and Security Return 196% Market Return 12% Coefficient of Correlation 0.80 6% Treasury Bond trading at ` 120 Determine the Standard Deviation of – (a) Market Return, and (b) Security Return. Solution: Similar to Page 7.25, Q.No. 6 1. Computation of Beta of the Security: 1. Risk Free Rate = Price Market Current Payment Coupon = 120 6% 100 ` ` × = 5% 2. Assuming Equilibrium Return = CAPM Return, we have 12% = R F + β A × (R M – R F ) 12% = 5% + β A × (12% – 5%) β A = 1 2. Computation of Market and Security Risk Particulars Market Risk Security Risk Computation β A = 2 M AM σ Cov 1 = 2 M σ 196% σ M = 14% (Market Risk) β A = M A σ σ × AM ρ 1 = 14% σ A × 0.80 σ A = 0.80 14% = 17.50% ________________________________________________________________________________________________________________________ www.shrigurukripa.com Get More Updates From http://cawinners.com/ Join with us https://www.facebook.com/groups/CawinnersOfficial/

Transcript

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.1

Gurukripa’s Guideline Answers for Nov 2016 Exam Questions CA Final –Strategic Financial Management

Question No.1 is compulsory. Answer any 5 Questions from the remaining 6 Questions. Answer any 4 out of 5 in Q.7.

Note: Page Number References are from “Padhuka’s Students’ Referencer on Strategic Financial Management” Question 1(a): International Finance – Swap Points 5 Marks On 3rd April 2016, a Bank quotes the following – Spot Exchange Rate (US $1) INR 66.2525 INR 67.5945 2 months’ Swap Points 70 90 3 month’s Swap Points 160 186 In a spot transaction, delivery is made after two days. Assuming Spot Date as 5th April 2016, and assuming 1 Swap Point = 0.0001, you are required to – (a) Ascertain Swap Points for 2 months and 15 days. (For 20thJune 2016), (b) Determine Foreign Exchange Rate for 20thJune 2016, and (c) Compute the Annual Rate of Premium / Discount of US$ on INR, on an Average Rate.

Solution: Refer Principles and various Illustrations in Chapter 16

(a) Swap Points for 3rdMonth 160 – 70 = 90 186 – 90 = 96 (b) Swap Points for 15 days = (a) ÷ 2 45 48 (c) Swap points for 2 Months and 15 days 70 + 45 = 115 90 + 48 = 138 (d) Foreign Exchange Rate for 2 Months and 15 days 66.2525 + 0.0115 = 66.2640 67.5945 + 0.0138 = 67.6083

(e) Annual rate of Premium / Discount [Taking 3 Month Ask Swap Points 0.0186 as Base]

= Period Forward

Months 12 100

RateSpot RateSpot - Rate Forward

××

= 67.59450.0186

× 100 × Months3Months12 = 0.11%

Question 1(b): Portfolio Management – Risk – Reverse Working 5 Marks The following information is available in respect of Security A: Equilibrium Return 12% Co–Variance of Market Return and Security Return 196% Market Return 12% Coefficient of Correlation 0.80 6% Treasury Bond trading at ` 120 Determine the Standard Deviation of – (a) Market Return, and (b) Security Return.

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.2

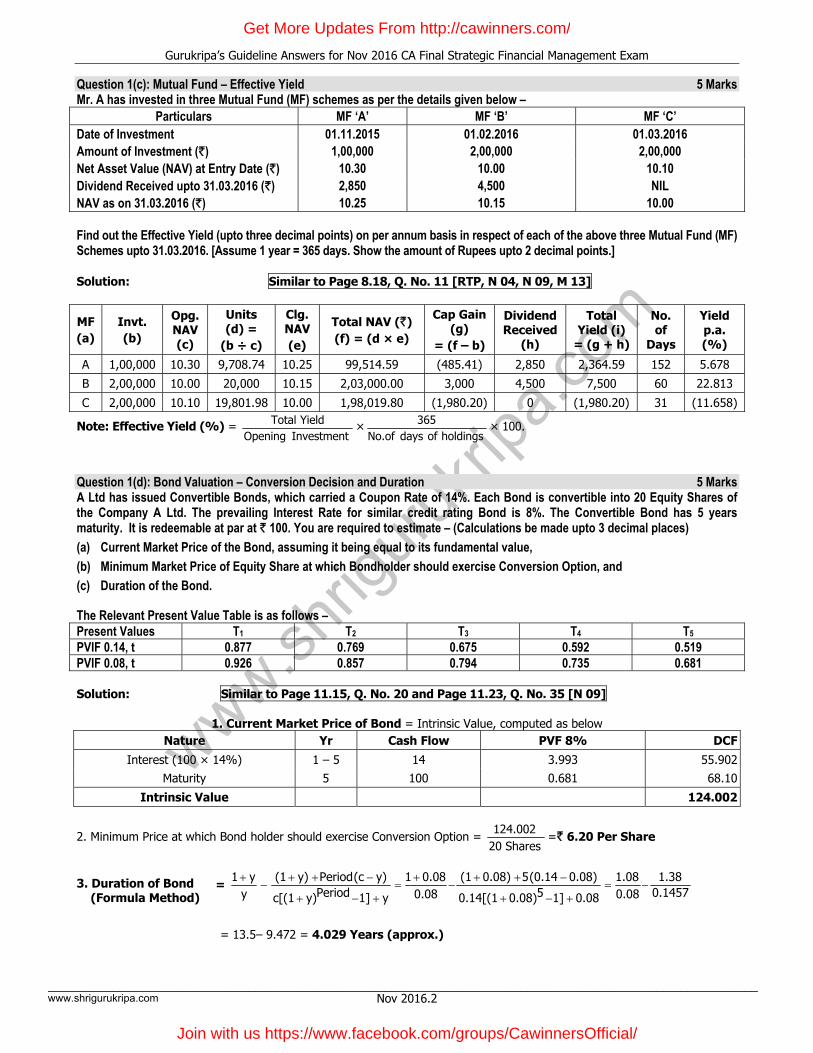

Question 1(c): Mutual Fund – Effective Yield 5 Marks Mr. A has invested in three Mutual Fund (MF) schemes as per the details given below –

Particulars MF ‘A’ MF ‘B’ MF ‘C’ Date of Investment 01.11.2015 01.02.2016 01.03.2016 Amount of Investment (`) 1,00,000 2,00,000 2,00,000 Net Asset Value (NAV) at Entry Date (`) 10.30 10.00 10.10 Dividend Received upto 31.03.2016 (`) 2,850 4,500 NIL NAV as on 31.03.2016 (`) 10.25 10.15 10.00 Find out the Effective Yield (upto three decimal points) on per annum basis in respect of each of the above three Mutual Fund (MF) Schemes upto 31.03.2016. [Assume 1 year = 365 days. Show the amount of Rupees upto 2 decimal points.] Solution: Similar to Page 8.18, Q. No. 11 [RTP, N 04, N 09, M 13]

Question 1(d): Bond Valuation – Conversion Decision and Duration 5 Marks A Ltd has issued Convertible Bonds, which carried a Coupon Rate of 14%. Each Bond is convertible into 20 Equity Shares of the Company A Ltd. The prevailing Interest Rate for similar credit rating Bond is 8%. The Convertible Bond has 5 years maturity. It is redeemable at par at ` 100. You are required to estimate – (Calculations be made upto 3 decimal places) (a) Current Market Price of the Bond, assuming it being equal to its fundamental value, (b) Minimum Market Price of Equity Share at which Bondholder should exercise Conversion Option, and (c) Duration of the Bond. The Relevant Present Value Table is as follows – Present Values T1 T2 T3 T4 T5 PVIF 0.14, t 0.877 0.769 0.675 0.592 0.519 PVIF 0.08, t 0.926 0.857 0.794 0.735 0.681 Solution: Similar to Page 11.15, Q. No. 20 and Page 11.23, Q. No. 35 [N 09]

1. Current Market Price of Bond = Intrinsic Value, computed as below Nature Yr Cash Flow PVF 8% DCF

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.3

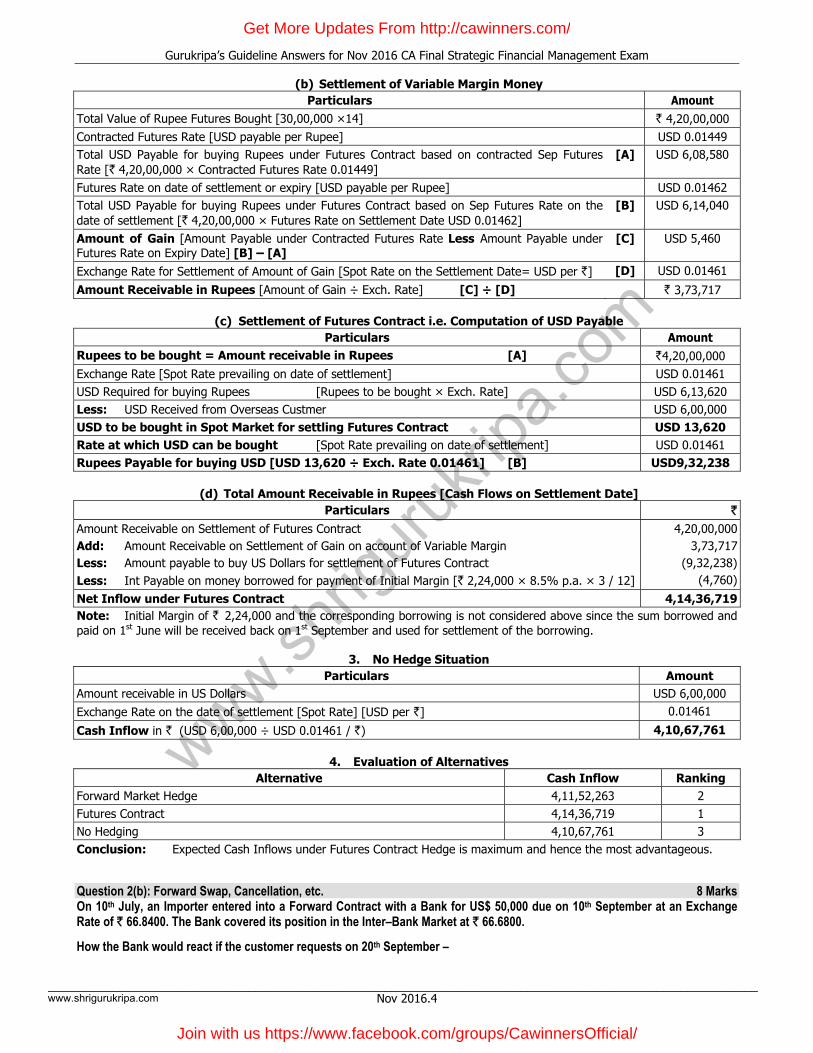

Question 2(a): International Finance 8 Marks LMN Ltd is an export oriented business house based in Mumbai. The Company invoices in Customer’s Currency. The receipt of US $ 6,00,000 is due on 1st September 2016. Market Information as at 1st June 2015 is –

Exchange Rate US $ / ` Exchange Rates US $ / ` Contract Size Spot 0.01471 Currency Future 1 Month Forward 0.01464 June 0.01456 ` 30,00,000 3 Months Forward 0.01458 September 0.01449

Initial Margin (`) Interest Rates in India % June 12,000 8.00 p.a. September 16,000 8.50 p.a. On 1st September 2016, the Spot Rate US $ / ` is 0.01461 and Currency Futures Rate is US $ / ` 0.01462.

It may be assumed that Variation in Margin would be settled on the maturity of the Futures Contract.

Which of the following methods would be most and advantageous for LMN Ltd? (a) Using Forward Contract, (b) Using Currency Futures, and (c) Not hedging Currency Risks. Show the calculations and comment. Solution: Similar to Page 17.80, Q. No. 76 [N 06]

1. Forward Contract Hedge Particulars Amount

Amount receivable in US Dollars USD 6,00,000Forward Rate USD per ` 0.01458

2. Hedging using Currency Futures Facts: USD 6,00,000 is receivable in 3–Months time. USD should be encashed into Rupees. Therefore, USD should be sold

and Rupee should be bought. Therefore, the Company should BUY Rupee Futures Contract Cash Flows: June 1 (Now) Payment of Initial Margin in by borrowing in Rupees

Sept 1 (3 Mths Later) Settlement of Variable Margin based on Contracted Futures Rate and Futures Rate on Settlement Date for September Futures

Sept 1 (3 Mths Later) Purchase of Rupee by paying in US Dollars (received from the Overseas customer) based on Spot Rate on the date of settlement.

Sept 1 (3 Mths Later) Settlement of money borrowed in Rupees for payment of Margin along with interest

(a) No. of Futures Contracts Required and Margin Money

Particulars Result Amount receivable in USD USD 6,00,000 Exchange Rate for September Futures [USD / `] USD 0.01449

Total Value Receivable in Rupees = Rupees to be bought [Amt Receivable USD 6,00,000 ÷ Futures Exchange Rate USD 0.01449 / `]

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.4

(b) Settlement of Variable Margin Money Particulars Amount

Total Value of Rupee Futures Bought [30,00,000 ×14] ` 4,20,00,000 Contracted Futures Rate [USD payable per Rupee] USD 0.01449 Total USD Payable for buying Rupees under Futures Contract based on contracted Sep Futures Rate [` 4,20,00,000 × Contracted Futures Rate 0.01449]

[A] USD 6,08,580

Futures Rate on date of settlement or expiry [USD payable per Rupee] USD 0.01462 Total USD Payable for buying Rupees under Futures Contract based on Sep Futures Rate on the date of settlement [` 4,20,00,000 × Futures Rate on Settlement Date USD 0.01462]

[B] USD 6,14,040

Amount of Gain [Amount Payable under Contracted Futures Rate Less Amount Payable under Futures Rate on Expiry Date] [B] – [A]

[C] USD 5,460

Exchange Rate for Settlement of Amount of Gain [Spot Rate on the Settlement Date= USD per `] [D] USD 0.01461

Amount Receivable in Rupees [Amount of Gain ÷ Exch. Rate] [C] ÷ [D] ` 3,73,717

(c) Settlement of Futures Contract i.e. Computation of USD Payable Particulars Amount

Rupees to be bought = Amount receivable in Rupees [A] `4,20,00,000 Exchange Rate [Spot Rate prevailing on date of settlement] USD 0.01461 USD Required for buying Rupees [Rupees to be bought × Exch. Rate] USD 6,13,620 Less: USD Received from Overseas Custmer USD 6,00,000 USD to be bought in Spot Market for settling Futures Contract USD 13,620 Rate at which USD can be bought [Spot Rate prevailing on date of settlement] USD 0.01461 Rupees Payable for buying USD [USD 13,620 ÷ Exch. Rate 0.01461] [B] USD9,32,238

(d) Total Amount Receivable in Rupees [Cash Flows on Settlement Date] Particulars `

Amount Receivable on Settlement of Futures Contract 4,20,00,000Add: Amount Receivable on Settlement of Gain on account of Variable Margin 3,73,717Less: Amount payable to buy US Dollars for settlement of Futures Contract (9,32,238)Less: Int Payable on money borrowed for payment of Initial Margin [` 2,24,000 × 8.5% p.a. × 3 / 12] (4,760)

Net Inflow under Futures Contract 4,14,36,719Note: Initial Margin of ` 2,24,000 and the corresponding borrowing is not considered above since the sum borrowed and paid on 1st June will be received back on 1st September and used for settlement of the borrowing.

3. No Hedge Situation Particulars Amount

Amount receivable in US Dollars USD 6,00,000 Exchange Rate on the date of settlement [Spot Rate] [USD per `] 0.01461

4. Evaluation of Alternatives Alternative Cash Inflow Ranking

Forward Market Hedge 4,11,52,263 2 Futures Contract 4,14,36,719 1 No Hedging 4,10,67,761 3 Conclusion: Expected Cash Inflows under Futures Contract Hedge is maximum and hence the most advantageous. Question 2(b): Forward Swap, Cancellation, etc. 8 Marks On 10th July, an Importer entered into a Forward Contract with a Bank for US$ 50,000 due on 10th September at an Exchange Rate of ` 66.8400. The Bank covered its position in the Inter–Bank Market at ` 66.6800.

How the Bank would react if the customer requests on 20th September –

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.5

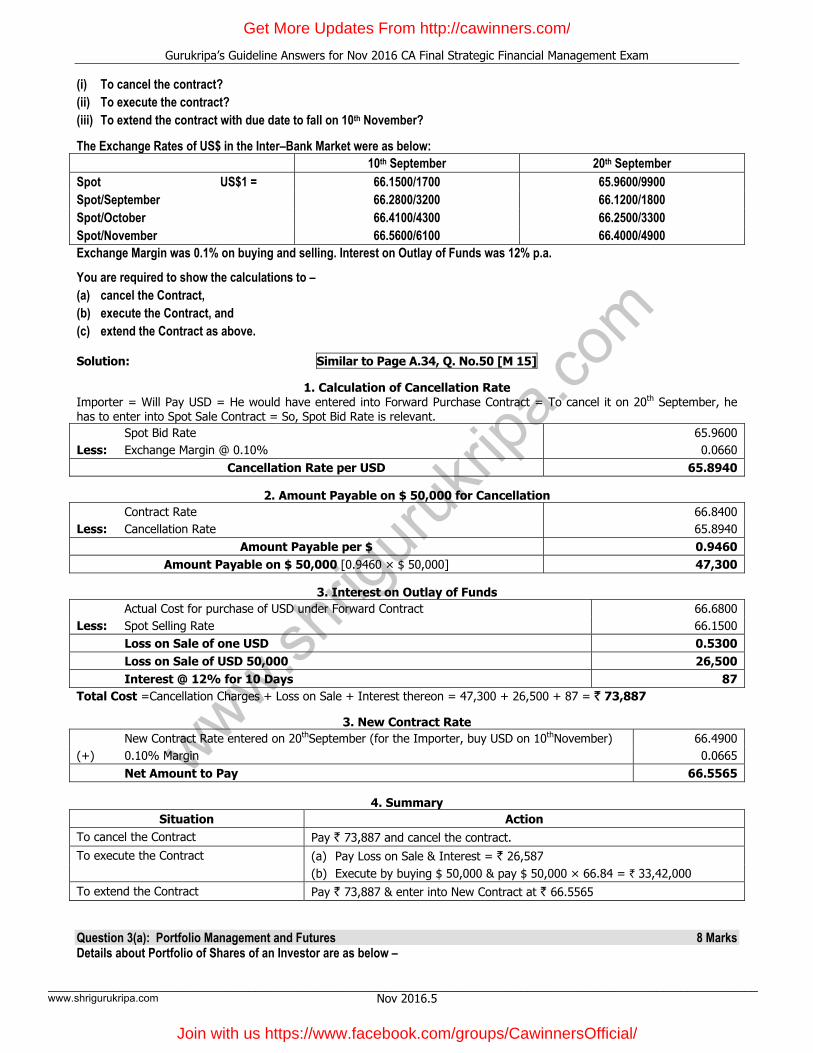

(i) To cancel the contract? (ii) To execute the contract? (iii) To extend the contract with due date to fall on 10th November? The Exchange Rates of US$ in the Inter–Bank Market were as below:

10th September 20th September Spot US$1 = 66.1500/1700 65.9600/9900 Spot/September 66.2800/3200 66.1200/1800 Spot/October 66.4100/4300 66.2500/3300 Spot/November 66.5600/6100 66.4000/4900 Exchange Margin was 0.1% on buying and selling. Interest on Outlay of Funds was 12% p.a.

You are required to show the calculations to – (a) cancel the Contract, (b) execute the Contract, and (c) extend the Contract as above. Solution: Similar to Page A.34, Q. No.50 [M 15]

1. Calculation of Cancellation Rate Importer = Will Pay USD = He would have entered into Forward Purchase Contract = To cancel it on 20th September, he has to enter into Spot Sale Contract = So, Spot Bid Rate is relevant. Spot Bid Rate 65.9600 Less: Exchange Margin @ 0.10% 0.0660

Cancellation Rate per USD 65.8940

2. Amount Payable on $ 50,000 for Cancellation Contract Rate 66.8400 Less: Cancellation Rate 65.8940

Amount Payable per $ 0.9460Amount Payable on $ 50,000 [0.9460 × $ 50,000] 47,300

3. Interest on Outlay of Funds

Actual Cost for purchase of USD under Forward Contract 66.6800 Less: Spot Selling Rate 66.1500 Loss on Sale of one USD 0.5300 Loss on Sale of USD 50,000 26,500 Interest @ 12% for 10 Days 87Total Cost =Cancellation Charges + Loss on Sale + Interest thereon = 47,300 + 26,500 + 87 = ` 73,887

3. New Contract Rate New Contract Rate entered on 20thSeptember (for the Importer, buy USD on 10thNovember) 66.4900(+) 0.10% Margin 0.0665 Net Amount to Pay 66.5565

4. Summary Situation Action

To cancel the Contract Pay ` 73,887 and cancel the contract. To execute the Contract (a) Pay Loss on Sale & Interest = ` 26,587

(b) Execute by buying $ 50,000 & pay $ 50,000 × 66.84 = ` 33,42,000 To extend the Contract Pay ` 73,887 & enter into New Contract at ` 66.5565 Question 3(a): Portfolio Management and Futures 8 Marks Details about Portfolio of Shares of an Investor are as below –

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.6

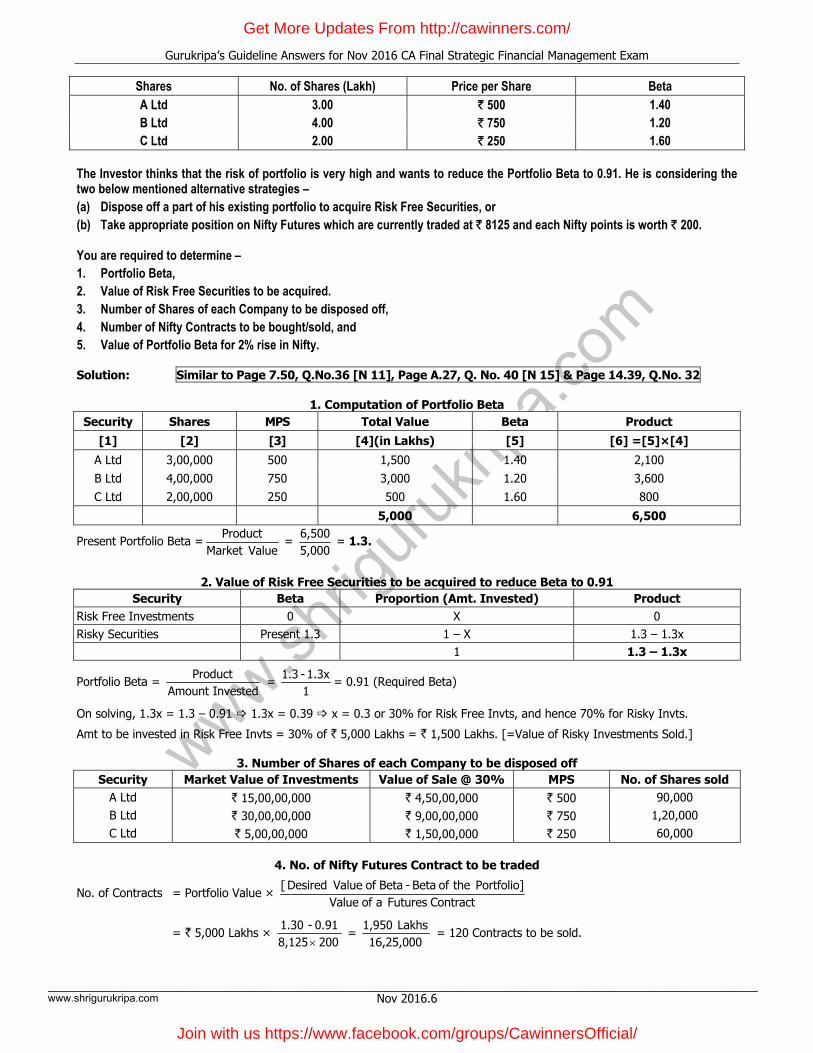

Shares No. of Shares (Lakh) Price per Share Beta A Ltd 3.00 ` 500 1.40 B Ltd 4.00 ` 750 1.20 C Ltd 2.00 ` 250 1.60

The Investor thinks that the risk of portfolio is very high and wants to reduce the Portfolio Beta to 0.91. He is considering the two below mentioned alternative strategies – (a) Dispose off a part of his existing portfolio to acquire Risk Free Securities, or (b) Take appropriate position on Nifty Futures which are currently traded at ` 8125 and each Nifty points is worth ` 200. You are required to determine – 1. Portfolio Beta, 2. Value of Risk Free Securities to be acquired. 3. Number of Shares of each Company to be disposed off, 4. Number of Nifty Contracts to be bought/sold, and 5. Value of Portfolio Beta for 2% rise in Nifty. Solution: Similar to Page 7.50, Q.No.36 [N 11], Page A.27, Q. No. 40 [N 15] & Page 14.39, Q.No. 32

1. Computation of Portfolio Beta Security Shares MPS Total Value Beta Product

[1] [2] [3] [4](in Lakhs) [5] [6] =[5]×[4]

A Ltd 3,00,000 500 1,500 1.40 2,100 B Ltd 4,00,000 750 3,000 1.20 3,600 C Ltd 2,00,000 250 500 1.60 800

5,000 6,500

Present Portfolio Beta =ValueMarket

Product=

5,0006,500

= 1.3.

2. Value of Risk Free Securities to be acquired to reduce Beta to 0.91

6,670.80= 1.3. [Note: Alternative assumptions exist for computation of Beta in this case.]

Question 3(b): Portfolio Management – Characteristic Line and Risk 8 Marks The Returns and Market Portfolio for a period of four years are as under:

Year % Return of Stock B % Return on Market Portfolio 1 10 8 2 12 10 3 9 9 4 3 –1

For Stock B, you are required to determine – (a) Characteristic Line, and (b) The Systematic and Unsystematic Risk. Solution: Similar to Page 7.30, Q. No. 12 [M 09]

Combination Market and Stock B Combination Market and Stock B

Covariance [ ]

nBDMD

BM,Cov

∑ ×= =

4

57= 14.25 Correlation B M,ρ =

BσMσ

BM,Cov

×=

3.354 4.387

14.25

×= 0.968

Beta of Stock B =2

Mσ

BM,Cov =

19.25

14.25= 0.740

2. Computation of Characteristic Line for Stock B Basic Values: y = BR = 8.5 Β= 0.74 x = MR (Expected Return on Market Index) = 6.5 For computing ‘a’ using Securities Market Line, Y = a + β Rm So, 8.5 = a + 0.74×6.5, So, a = 8.5–(0.74×6.5) = 3.69

Characteristic Line for Stock B= Y = a + β Rm = 3.69 + 0.74 RM

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.8

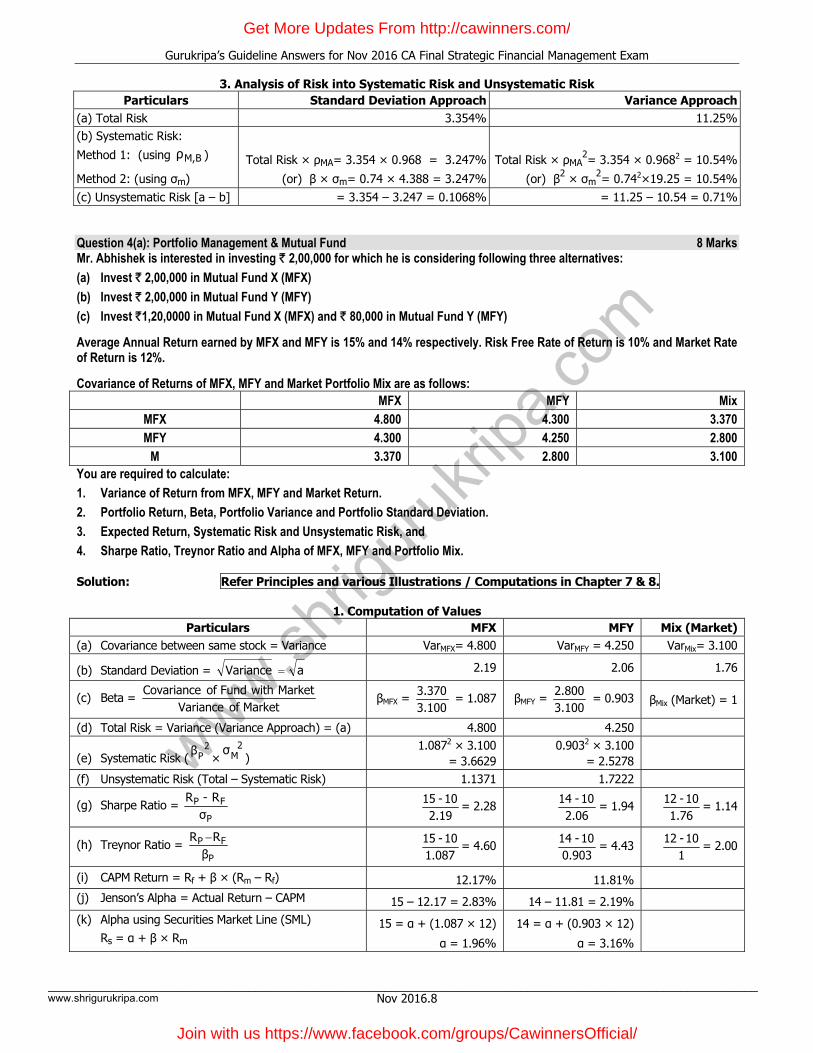

3. Analysis of Risk into Systematic Risk and Unsystematic Risk Particulars Standard Deviation Approach Variance Approach

(a) Total Risk 3.354% 11.25%(b) Systematic Risk:

Method 1: (using B M,ρ )

Method 2: (using σm)

Total Risk × ρMA= 3.354 × 0.968 = 3.247%

(or) β × σm= 0.74 × 4.388 = 3.247%

Total Risk × ρMA2= 3.354 × 0.9682 = 10.54%

(or) β2 × σm2= 0.742×19.25 = 10.54%

(c) Unsystematic Risk [a – b] = 3.354 – 3.247 = 0.1068% = 11.25 – 10.54 = 0.71% Question 4(a): Portfolio Management & Mutual Fund 8 Marks Mr. Abhishek is interested in investing ` 2,00,000 for which he is considering following three alternatives: (a) Invest ` 2,00,000 in Mutual Fund X (MFX) (b) Invest ` 2,00,000 in Mutual Fund Y (MFY) (c) Invest `1,20,0000 in Mutual Fund X (MFX) and ` 80,000 in Mutual Fund Y (MFY) Average Annual Return earned by MFX and MFY is 15% and 14% respectively. Risk Free Rate of Return is 10% and Market Rate of Return is 12%. Covariance of Returns of MFX, MFY and Market Portfolio Mix are as follows:

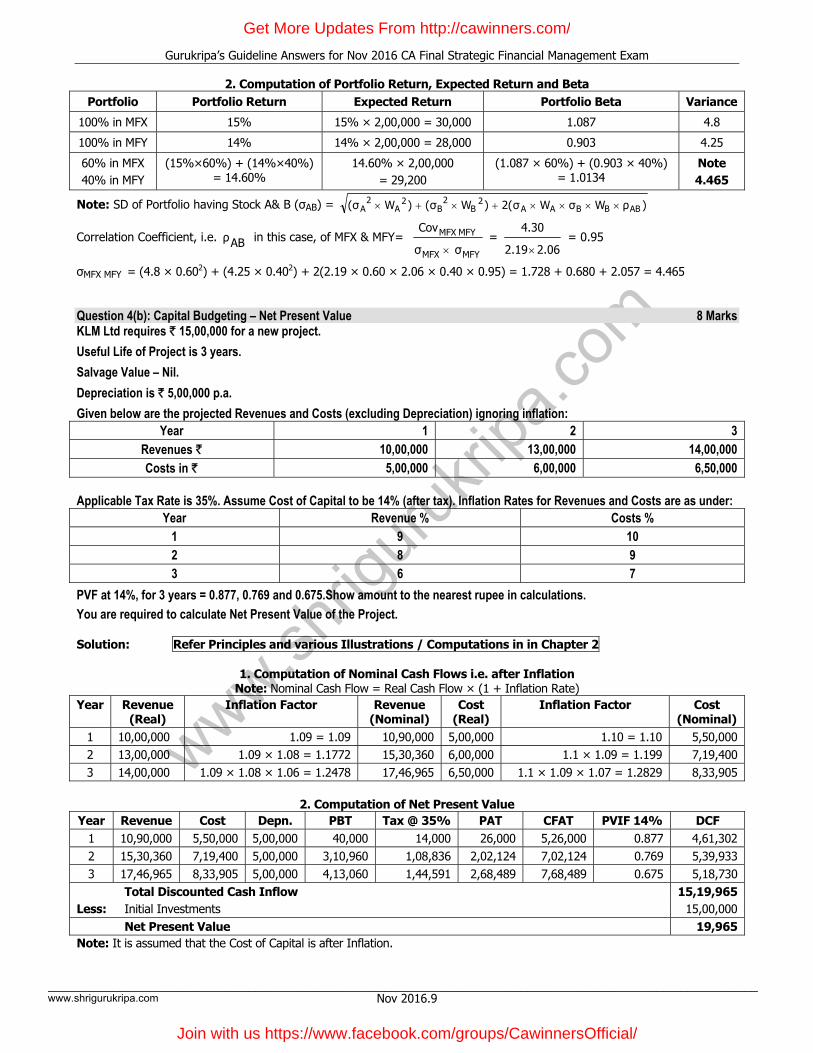

M 3.370 2.800 3.100 You are required to calculate: 1. Variance of Return from MFX, MFY and Market Return. 2. Portfolio Return, Beta, Portfolio Variance and Portfolio Standard Deviation. 3. Expected Return, Systematic Risk and Unsystematic Risk, and 4. Sharpe Ratio, Treynor Ratio and Alpha of MFX, MFY and Portfolio Mix. Solution: Refer Principles and various Illustrations / Computations in Chapter 7 & 8.

1. Computation of Values Particulars MFX MFY Mix (Market)

(a) Covariance between same stock = Variance VarMFX= 4.800 VarMFY = 4.250 VarMix= 3.100

(b) Standard Deviation = Variance a= 2.19 2.06 1.76

Note: SD of Portfolio having Stock A& B (σAB) = )ρWσW2(σ)W(σ)W(σ ABBBAA2

B2

B2

A2

A ××××+×+×

Correlation Coefficient, i.e. ABρ in this case, of MFX & MFY= MFYMFX

MFYMFX

σσ

Cov

× =

2.062.19

4.30

× = 0.95

σMFX MFY = (4.8 × 0.602) + (4.25 × 0.402) + 2(2.19 × 0.60 × 2.06 × 0.40 × 0.95) = 1.728 + 0.680 + 2.057 = 4.465 Question 4(b): Capital Budgeting – Net Present Value 8 Marks KLM Ltd requires ` 15,00,000 for a new project. Useful Life of Project is 3 years. Salvage Value – Nil. Depreciation is ` 5,00,000 p.a. Given below are the projected Revenues and Costs (excluding Depreciation) ignoring inflation:

Year 1 2 3 Revenues ` 10,00,000 13,00,000 14,00,000 Costs in ` 5,00,000 6,00,000 6,50,000

Applicable Tax Rate is 35%. Assume Cost of Capital to be 14% (after tax). Inflation Rates for Revenues and Costs are as under:

Year Revenue % Costs % 1 9 10 2 8 9 3 6 7

PVF at 14%, for 3 years = 0.877, 0.769 and 0.675.Show amount to the nearest rupee in calculations. You are required to calculate Net Present Value of the Project. Solution: Refer Principles and various Illustrations / Computations in in Chapter 2

1. Computation of Nominal Cash Flows i.e. after Inflation

Note: Nominal Cash Flow = Real Cash Flow × (1 + Inflation Rate) Year Revenue

Total Discounted Cash Inflow 15,19,965Less: Initial Investments 15,00,000 Net Present Value 19,965Note: It is assumed that the Cost of Capital is after Inflation.

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.10

Question 5(a): Factoring vs Own Management of Receivables – with / without Recourse 8 Marks Projected Sales for the next year of Z Ltd is ` 1,000 Crores. The Company manages its Accounts Receivables internally. Its present annual Cost of Sales Ledger Administration is ` 11 Crores. The Company finances its Investment on Debtors through a mix of Bank Credit and own Long Term Funds in the ratio of 60:40. Current Cost of Bank Credit and Long Term Funds are 10% and 12% respectively. The past experience indicates that Bad Debts Losses are 1.5% on Total Sales. The Company has a credit policy of 2/10, net 30. On an average, 40% of Receivables are collected within the discount period and rest are collected 70 days after the invoice date. Over the years, Gross Profit is maintained at 20% and the same is expected to be continued in future. To enable the Management focus on promotional activities and get rid of escalating cost associated with In–House Management of Debtors, the Company is considering the possibility of availing the services of Fairgrowth Factors Ltd for managing the Receivables of the Company. According to the proposal of the Factor, it would pay advance to the tune of 85% of Receivables with 20% interest and 81% of Receivables with 21% interest for the recourse and non–recourse agreements respectively. The proposal provides for guaranteed payment within 30 days from the date of invoice. The Factoring Commission would be 4% without recourse and 2% with recourse. If the Company goes for the factoring arrangement, the staff would be under burdened and concentrate more on promotional activities and consequently additional sales of ` 100 Crores would be achieved. Assume that all Sales of the Company are credit sales and the year is of 360 days. You are required to: (a) Calculate Cost of In–House Management of Receivables. (b) Compute Cost of Fairgrowth Factors Ltd proposal (with recourse and without recourse) (c) Calculate Net Benefits under Recourse Factoring and Non–Recourse Factoring, and (d) Decide the best option for the Company. Solution: Similar to Page A.11, Q. No. 13 [N 14]

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.11

3. Cost Comparison (` Crores) Particulars With Recourse Without Recourse

Present Own Cost [Note] 47.80 47.80 – 15 = 32.80 Cost of Factoring Proposal 39.11 61.42

Difference = Cost Saved / (Excess Cost) 8.69 (28.62)Note: Bad Debts `15 Crores not avoidable in case of “With Recourse” Factoring.

Conclusion: Fairgrowth Proposal with Recourse is most beneficial.

Question 5(b): International Finance – Hedging Profit / Loss 8 Marks A Company is considering hedging its Foreign Exchange Risk. It has made a purchase on 1st July 2016, for which it has to make a payment of US$ 60,000 on 31st December 2016. The present Exchange Rate is 1 US$ = ` 65. It can purchase forward 1 $ at ` 64. The Company will have to make an upfront premium at 2% of the Forward Amount purchased. The Cost of Funds to the Company is 12% per annum.

In the following situations, compute the Profit/ Loss the Company will make if it hedges its Foreign Exchange Risk with the Exchange Rate on 31st December 2016 as – (a)` 68 per US$, (b) ` 62 per US$, (c) ` 70 per US$, (d) ` 65 per US$. Solution: Similar to Page 17.55, Q. No. 44 [M 08]

1. Cash Flow in case of Forward Contract

Particulars ValueUSD to be purchased in Forward Market USD 60,000Forward Contract Purchase Price per USD ` 64 Total Value of Forward Contract [USD 60,000 × ` 64 per USD] 38,40,000 Upfront Premium at 2% of Contract Value [` 38,40,000 × 2%] 76,800 Interest on Upfront Premium for a period of 6 Months [` 76,800 × 12% p.a. × 6/12] 4,608

Total Cash Outgo on 31.12.2016 under Forward Contract Route 39,21,408Note: Upfront premium on Forward Contract is a transaction cost for entering into Forward Contract payable to the Foreign Currency Seller in the Forward Contract. It is assumed that this amount will be borrowed at 12% p.a. by the Company.

2. Notional Gain or Loss on 31.12.2016 If Exchange Rate on 31.12.2016 is (`/USD) ` 68 ` 62 ` 70 ` 65

Cash Outflow on 31.12.16 ($ 60,000 × `68 or `62 or `70 or `65) [Based on Spot Rate as at 31.12.2016]

40,80,000 37,20,000 42,00,000 39,00,000

Less: Cash Outflow under Forward Contract (39,21,408) (39,21,408) (39,21,408) (39,21,408) Profit / (Loss) on entering into Forward Contract 1,58,592 (2,01,408) 2,78,592 (21,408) Question 6(a): Valuation of Business& Shares 8 Marks XN Ltd reported a Profit of ` 100.32 Lakhs after 34% tax for the Financial Year 2015–2016. An analysis of the accounts reveals that the Income included Extraordinary Items of ` 15 Lakhs and an Extraordinary Loss of ` 5 Lakhs. The existing operations, except for the Extraordinary Items, are expected to continue in future. Further, a new product is launched and the expectations are as under:

Particulars `Lakhs Particulars `Lakhs Sales 70 Labour Costs 16 Material Costs 20 Fixed Costs 10 The Company has 50,00,000 Equity Shares of ` 10 each and 80,000, 9% Preference Shares of ` 100 each with P/E Ratio being 6 times. You are required to: (a) Compute the Value of the Business. Assume Cost of Capital to be 12% (after tax) and (b) Determine the Market Price per Equity Share. Solution: Similar to Page 18.34, Q. No. 13 [M 09, N 12]

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.12

1.Computation of Value of Business Particulars ` Lakhs

Earnings After Tax of 34% for the last year = ` 100.32 Lakhs. So EBT is 66%

100.32 152

Less: Extra Ordinary Income – Not to recur in the future (15)Add: Extra Ordinary Loss – Not to recur in the future 5Add: Additional Income from New Launch = (70 – 20 – 16 – 10) 24 Future Expected Earnings Before Tax 166Less: Taxes at 34% thereon 56.44 Future Expected Earnings After Tax 109.56Less: Preference Dividend (9% of ` 80 Lakhs) (7.20) Equity Earnings 102.36Valuation:

(a) Value of Whole Business assuming overall Capitalisation Rate = 12% = 12%

109.56 913.00

(b) Equity Expectations = Ke = RatioPE1

= 61 = 16.67%

(i) Value of Equity (Equity Earnings 16.67%102.36

) 614.04

(ii) Value of Pref. Capital (Face Value, in the absence of an identified Preference Expectation Rate) 100.00 Value of Business = Total under (b) 714.04

Note: Alternatively, Equity Expectations may also be assumed at given Ko =12%.

2. Value of Market Price Per Equity Share Based on Projected Earnings Past Year’s Earnings

(a) Equity Earnings (`Lakhs) 102.36 100.32 – 7.2 Pref. Dividend = 93.12(b) No. of Equity Shares (Lakhs) 50.00 50.00(c) Earnings Per Share (a ÷ b) ` 2.0472 ` 1.8624(d) PE Multiple 6 6(e) Market Price Per Equity Share = [c × d] ` 12.283 ` 11.174 Question 6(b): Capital Budgeting –Social Costs / Benefits 8 Marks The Municipal Corporation of a city with mass population is planning to construct a Flyover that will replace the intersection of two busy Highways X and Y. Average Traffic per day is 10,000 Vehicles on Highway X and 8,000 Vehicles on Highway Y. 70% of the Vehicles are private and rest are commercial vehicles. The flow to traffic across and between aforesaid Highways is controlled by traffic lights. Due to heavy flow, 50% of traffic on each of the highways is delayed. Average Loss of Time due to delay is 1.3 minute in Highway X and 1.2 minute in Highway Y. The Cost of time delayed is estimated to be ` 80 per hour for Commercial Vehicles and ` 30 for Private Vehicle.

The cost of stop and start is estimated to be ` 1.20 for Commercial Vehicles and ` 0.80 for Private Vehicle. The cost of operating the traffic lights is ` 80,000 a year. One Policeman is required to be posted for 3 hours a day at the crossing which costs ` 150 per hour.

Due to failure to obey traffic signals, eight fatal accidents and sixty non–fatal accidents occurred in last 4 years. On an average, Insurance Settlements per fatal and non–fatal accidents are ` 5,00,000 and ` 15,000 respectively.

To eliminate the delay of traffic and the accidents caused due to traffic light violations, the Flyover has been designed. It will add a quarter of kilometer to the distance of 20% of total traffic. No posting of Policeman will be required at the Flyover. The Flyover will require investment of ` 3 Crores. Extra Maintenance Cost would be ` 70,000 a year.

The incremental Operating Cost for Commercial Vehicle will be ` 5 per km and ` 2 for Non–Commercial Vehicle. Expected Economic Life of the Flyover is 30 years having no salvage value. The Cost of Capital for the Project is 8%. (Corresponding Capital Recovery is 0.0888).

You are required to calculate: 1. Total Net Benefits to Users, 2. Annual Cost to the State, and 3. Benefit Cost Ratio.

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.13

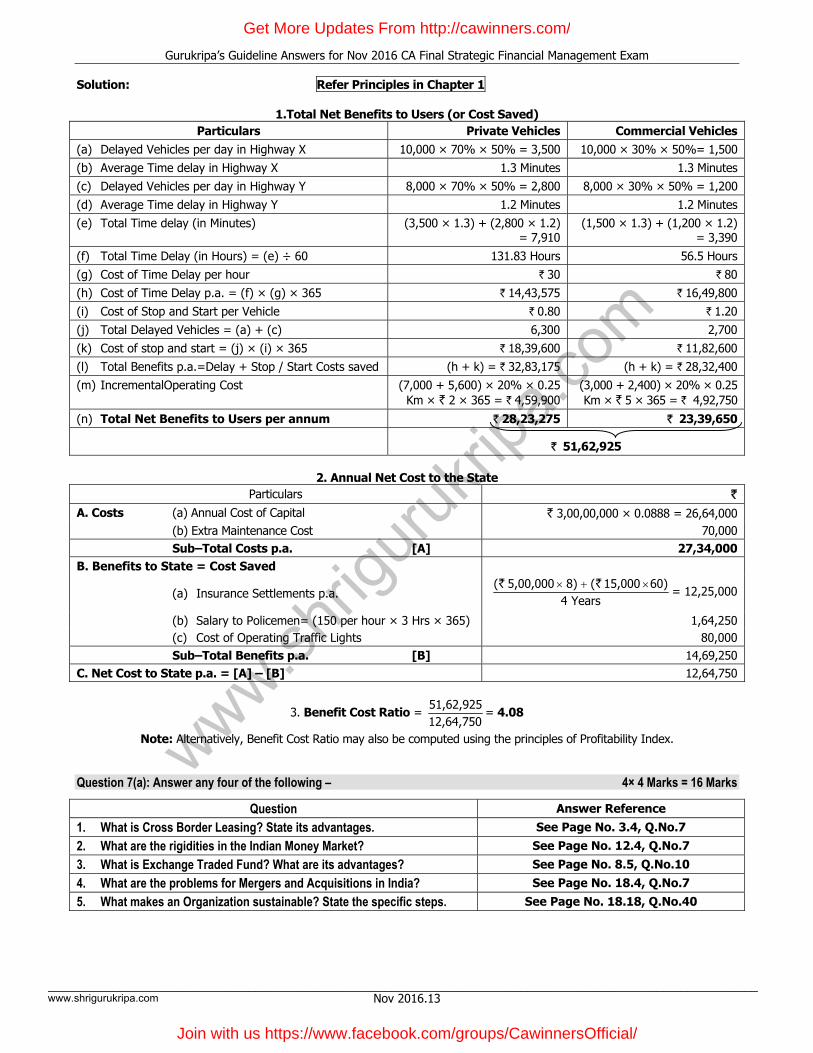

Solution: Refer Principles in Chapter 1

1.Total Net Benefits to Users (or Cost Saved) Particulars Private Vehicles Commercial Vehicles

(a) Delayed Vehicles per day in Highway X 10,000 × 70% × 50% = 3,500 10,000 × 30% × 50%= 1,500 (b) Average Time delay in Highway X 1.3 Minutes 1.3 Minutes (c) Delayed Vehicles per day in Highway Y 8,000 × 70% × 50% = 2,800 8,000 × 30% × 50% = 1,200 (d) Average Time delay in Highway Y 1.2 Minutes 1.2 Minutes (e) Total Time delay (in Minutes) (3,500 × 1.3) + (2,800 × 1.2)

= 7,910 (1,500 × 1.3) + (1,200 × 1.2)

= 3,390 (f) Total Time Delay (in Hours) = (e) ÷ 60 131.83 Hours 56.5 Hours (g) Cost of Time Delay per hour ` 30 ` 80 (h) Cost of Time Delay p.a. = (f) × (g) × 365 ` 14,43,575 ` 16,49,800 (i) Cost of Stop and Start per Vehicle ` 0.80 ` 1.20 (j) Total Delayed Vehicles = (a) + (c) 6,300 2,700 (k) Cost of stop and start = (j) × (i) × 365 ` 18,39,600 ` 11,82,600 (l) Total Benefits p.a.=Delay + Stop / Start Costs saved (h + k) = ` 32,83,175 (h + k) = ` 28,32,400 (m) IncrementalOperating Cost (7,000 + 5,600) × 20% × 0.25

(n) Total Net Benefits to Users per annum ` 28,23,275 ` 23,39,650

` 51,62,925

2. Annual Net Cost to the State Particulars `

A. Costs (a) Annual Cost of Capital ` 3,00,00,000 × 0.0888 = 26,64,000 (b) Extra Maintenance Cost 70,000 Sub–Total Costs p.a. [A] 27,34,000B. Benefits to State = Cost Saved

(b) Salary to Policemen= (150 per hour × 3 Hrs × 365) 1,64,250 (c) Cost of Operating Traffic Lights 80,000

Sub–Total Benefits p.a. [B] 14,69,250 C. Net Cost to State p.a. = [A] – [B] 12,64,750

3. Benefit Cost Ratio = 12,64,75051,62,925

= 4.08

Note: Alternatively, Benefit Cost Ratio may also be computed using the principles of Profitability Index. Question 7(a): Answer any four of the following – 4× 4 Marks = 16 Marks

Question Answer Reference

1. What is Cross Border Leasing? State its advantages. See Page No. 3.4, Q.No.7

2. What are the rigidities in the Indian Money Market? See Page No. 12.4, Q.No.7

3. What is Exchange Traded Fund? What are its advantages? See Page No. 8.5, Q.No.10

4. What are the problems for Mergers and Acquisitions in India? See Page No. 18.4, Q.No.7

5. What makes an Organization sustainable? State the specific steps. See Page No. 18.18, Q.No.40

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.14

Padhuka’s Publications

For CA Inter • Ready Referencer on Accounting – Group I • Law, Ethics and Communication – A Referencer • Students' Handbook on Cost Accounting and Financial Management • Cost Accounting and Financial Management – A Practical Guide • Handbook on Taxation • Question Bank for Taxation • Students' Handbook on Advanced Accounting – Group II • A Students' Handbook on Auditing and Assurance • Auditing and Assurance – A Ready Referencer • Students' Handbook on Information Technology and Strategic Management • Question Bank – Information Technology and Strategic Management • Students' Referencer on Standards on Auditing

For CA CPT • Basics of Accounting • Mercantile Law Guide • Basics of General Economics • Practical Guide on Quantitative Aptitude • MCQ Bank for CA CPT • Complete Guide for CA CPT

For Attractive Discounts with “Special Combo Offers” *,

visit www.shrigurukripa.com * Subject to availability of Offer at the time of order. Terms and Conditions apply.

Join with us https://www.facebook.com/groups/CawinnersOfficial/

www.shrig

urukri

pa.co

m

Gurukripa’s Guideline Answers for Nov 2016 CA Final Strategic Financial Management Exam

Nov 2016.15

Padhuka’s Publications

For CA Final • Students' Guide on Financial Reporting • Students' Referencer on Strategic Financial Management • Students' Handbook on Advanced Auditing • Easy Guide to Advanced Auditing • Students' Handbook on Corporate and Allied Law • A Ready Referencer on Advanced Management Accounting • Students' Handbook on Information Systems Control and Audit • Question Bank ISCA • Direct Taxes – A Ready Referencer • Practical Guide on Direct Taxes • Question Bank Direct Taxes • Students' Referencer on Indirect Taxes • Students' Referencer on Accounting Standards • Students' Referencer on Standards on Auditing For Professionals • Handbook on Direct Taxes – Compendium for Users • Practical Guide on TDS & TCS • Personal Income Tax – A Simplified Approach • A Professional Guide to Income Computation & Disclosure Standards • Professional Guide to Tax Audit • Professional Manual on Accounting Standards • Professional Guide to CARO 2016 • Audit Referencer

For Attractive Discounts with “Special Combo Offers” *,

visit www.shrigurukripa.com * Subject to availability of Offer at the time of order. Terms and Conditions apply.