132

Joel D. Montero Chief Executive Officer Hacienda La Puente Unified School District Fiscal Review April 12, 2007

Joel D. MonteroChief Executive Offi cer

Hacienda La PuenteUnifi ed School District

Fiscal ReviewApril 12, 2007

FCMATJoel D. Montero, Chief Executive Officer

1300 17th Street - CITY CENTRE, Bakersfield, CA 93301-4533 . Telephone 661-636-4611 . Fax 661-636-4647422 Petaluma Blvd North, Suite. C, Petaluma, CA 94952 . Telephone: 707-775-2850 . Fax: 707-775-2854 . www.fcmat.org

Administrative Agent: Larry E. Reider - Office of Kern County Superintendent of Schools

April 12, 2007

Dr. Barbara Nakaoka, SuperintendentHacienda La Puente Unifi ed School District15959 East Gale AvenueCity of Industry, California 91716-0002

Dear Superintendent Nakaoka,

In March 2006, the Fiscal Crisis and Management Assistance Team (FCMAT) entered into an agreement for a fi scal review with the Hacienda La Puente Unifi ed School District. The request specifi ed that FCMAT would:

1. Conduct a review of the district’s 2005-06 second interim fi nancial report for all the general fund, adult education and child development funds including revenue, expenditure, and ADA/enrollment information.

2. Prepare a general fund multiyear fi nancial forecast to identify the district’s fi nancial position in 2006-07 and 2007-08 if enrollment continues to decline and no changes other than statutory COLA, step and column, and consumer price index trends are applied.

3. Determine the current level of risk to the district’s fi scal health using the FCMAT Fiscal Health Risk Analysis model.

The attached fi nal report contains the study team’s fi ndings with regard to the above areas of review. We appreciate the opportunity to serve you, and we extend our thanks to all the staff of the Hacienda La Puente Unifi ed School District.

Sincerely,

Joel D. Montero, Chief Executive Offi cerFiscal Crisis and Management Assistance Team

TABLE OF CONTENTS i

Table of Contents

Foreword ...........................................................................iii

Introduction ...................................................................... 1

Study Guidelines ............................................................... 1

Study Team ......................................................................... 2

Executive Summary ......................................................... 5

Findings and Recommendations ................................... 9Declining Enrollment and Budget Reductions ...................................................................... 9

Communication ....................................................................................................................................11

Budget Development and Oversight .......................................................................................12

Position Control and Staffi ng .......................................................................................................16

Categorical Programs and Special Education ....................................................................17

Multiyear Financial Projection......................................................................................................21

Fiscal Health Risk Analysis ........................................................................................................... 29

Appendices ......................................................................43

Hacienda La Puente Unifi ed School District

FOREWORD iii

ForewordFCMAT BackgroundThe Fiscal Crisis and Management Assistance Team (FCMAT) was created by legislation in accordance with Assembly Bill 1200 in 1992 as a service to assist local educational agencies in complying with fi scal accountability standards.

AB 1200 was established from a need to ensure that local educational agencies throughout California were adequately prepared to meet and sustain their fi nancial obligations. AB 1200 is also a statewide plan for county offi ces of education and school districts to work together on a local level to improve fi scal procedures and accountability standards. The legislation expanded the role of the county offi ce in monitoring school districts under cer-tain fi scal constraints to ensure these districts could meet their fi nancial commitments on a multiyear basis. AB 2756 provides specifi c responsibilities to FCMAT with regard to dis-tricts that have received emergency state loans. These include comprehensive assessments in fi ve major operational areas and periodic reports that identify the district’s progress on the improvement plans

Since 1992, FCMAT has been engaged to perform more than 600 reviews for local educa-tional agencies, including school districts, county offi ces of education, charter schools and community colleges. Services range from fi scal crisis intervention to management review and assistance. FCMAT also provides professional development training. The Kern County Superintendent of Schools is the administrative agent for FCMAT. The agency is guided under the leadership of Joel D. Montero, Chief Executive Offi cer, with funding derived through appropriations in the state budget and a modest fee schedule for charges to re-questing agencies.

Management Assistance ............................. 594 (94.59%)Fiscal Crisis/Emergency ................................ 34 (5.41%)

Note: Some districts had multiple studies.

Districts (7) that have received emergency loans from the state.

(Rev. 2/7/07)

Total Number of Studies ................... 628Total Number of Districts in CA .......... 982

80

70

60

50

40

30

20

10

0

Study Agreements by Fiscal Year

92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07

Projected

Nu

mb

er o

f Stu

die

s

Hacienda La Puente Unifi ed School District

INTRODUCTION 1

IntroductionThe Hacienda La Puente Unifi ed School District (HLPUSD), located in the Los Angeles County community of La Puente, serves a diversifi ed population of approximately 25,000 pre-kindergarten through twelfth grade students and 30,000 adult students living in the communities of La Puente, Hacienda Heights, and portions of Valinda and West Covina. The district also provides instructional services for one of the largest correctional pro-grams in the nation. It is comprised of four comprehensive high schools, one alternative high school, one community day school, 20 K-5 elementary schools, four K-8 schools, six middle schools, one specialized orthopedic program for special needs students, and numerous child development and preschool programs. The large adult education program operates in over 32 satellite facilities.

In spring 2006, the district contacted the Fiscal Crisis and Management Assistance Team (FCMAT) requesting a management review of the budget and budgeting process after discovering that a budget shortfall was imminent due to defi cit spending brought about mainly because of declining enrollment that had not been discovered in a timely manner.

FCMAT was initially asked to perform services related to the 2005-06 fi nancial records after approval of the study agreement. The study agreement is attached as Appendix A to this report.

The scope and objectives of this study are to:

1. Conduct a review of the district’s second interim fi nancial report for all funds including revenue, expenditure, and ADA/enrollment information.

2. Prepare a general fund multiyear fi nancial forecast to identify the district’s fi nancial position in 2006-07 and 2007-08 if enrollment continues to decline and no changes other than statutory COLA, step and column, and Consumer Price Index (CPI) trends are applied.

3. Determine the current level of risk to the district’s fi scal health using the FCMAT Fiscal Health Risk Analysis model.

The scope of the study changed slightly after FCMAT’s initial visit because the district’s data was not in a format that could be used to prepare the multiyear projection. This mat-ter will be discussed further in another section of this report.

Fiscal Crisis & Management Assistance Team

INTRODUCTION2

Study TeamThe FCMAT study team was composed of the following members:

Michele McClowry Margaret RosalesFiscal Intervention Specialist FCMAT Fiscal ConsultantFiscal Crisis and Management Kingsburg, California Assistance TeamLa Verne, California Laura Haywood Public Information SpecialistCarleen Wing Chandler Fiscal Crisis and ManagementFCMAT Fiscal Consultant Assistance TeamSan Juan Capistrano, California Bakersfi eld, California

Study GuidelinesFCMAT consultants visited the district on several occasions to conduct interviews, collect data and review documentation. This report is the result of those activities. Findings and recommendations are presented in the following sections:

• Executive Summary• Background • Findings and Recommendations

o Declining Enrollment and Budget Reductionso Communicationo Budget Development and Oversighto Position Control and Staffi ngo Categorical Programs and Special Education

• Multiyear Financial Projection• Fiscal Health Risk Analysis

FCMAT fi rst visited the district in March 2006 to begin the study. The study team was asked to prepare a multiyear projection (MYP) based on the district’s working budget as of the 2005-06 second interim report. The MYP could not be completed at that time because some of the data in the second interim report had not been updated. The MYP process re-quires uploading budget information from a mainframe computer system into a software program, assuming that all budget line items are complete and accurate. The base data was deemed incomplete when various test assumptions did not produce plausible data.

This situation was discussed with the district administration on March 22, 2006, and it was mutually decided to adjust the study agreement and postpone the preparation of the multi-year projections for a few weeks to allow the district time to review all of the budget line items in question. It should be noted that the major budget components were deemed rea-sonable; it was specifi c line item detail that, when uploaded, was found to be incomplete.

Hacienda La Puente Unifi ed School District

INTRODUCTION 3

During the initial visit, FCMAT also reviewed records, interviewed employees, examined numerous fi nancial reports, and gathered other pertinent information to meet the objec-tives of the study agreement. The team was able to complete an analysis of the budgeting process and make other useful observations to help the district improve operations and move forward with making the budget reductions that were necessary to remain fi scally solvent. It was decided at that March 22 meeting that FCMAT would issue a management letter describing the preliminary fi ndings and recommendations. The full text of that man-agement letter is included as Appendix B to this report. FCMAT returned to the district for the second time in June 2006. By that time the district had completed the second interim report and also issued a third interim report to inform the community, employees and the Los Angeles County Offi ce of Education (LACOE) of the current budget status and project the ending balance for 2005-06. However, the data in the mainframe computer system still could not be uploaded into the FCMAT MYP software program. Since the year was almost over, FCMAT met with the district’s admin-istration on June 14, 2006 and it was once again mutually agreed that preparing the MYP would be postponed until late August, after the 2005-06 accounting records were closed, the state-required SACS unaudited actual documents were fi nalized, and the 2006-07 budget was approved by LACOE. The 2006-07 adopted budget would then become the base year for the multiyear projections rather than the 2005-06 second interim projected budget. A second management letter was sent to the district dated July 19, 2006, sum-marizing the context of this meeting. The full text of the second management letter is in-cluded as Appendix C to this report.

FCMAT returned for the third time on August 21 and 22, 2006, just prior to the departure of the former Assistant Superintendent of Business. Once again, FCMAT found that the data in the district’s fi nancial system was not in pristine condition, but with certain as-sumptions and adjustments made by FCMAT, the MYP could be prepared. The multiyear fi nancial projection included in this report is based on the fi nancial data that was available in August 2006. A third management letter summarizing FCMAT’s progress at this point in time was issued on August 6, 2006. The full text of that letter is included as Appendix D to this report.

In January 2007, FCMAT again met with district staff to gather as much information as possible as to the current fi nancial status of the district. This information included review of the 2006-07 fi rst interim report and the 2005-06 fi nancial audit report. It was reported to FCMAT that the district recently settled negotiations at 4% for all bargaining groups, but the cost of this settlement was not included in the district’s 2006-07 fi rst interim re-port.

Fiscal Crisis & Management Assistance Team

INTRODUCTION4

Hacienda La Puente Unifi ed School District

EXECUTIVE SUMMARY 5

Executive SummaryAs with nearly half of all California school districts, the Hacienda La Puente USD has experienced signifi cant declining enrollment over the past few years, forcing the district to make signifi cant budget reductions in 2005-06 and 2006-07. Enrollment and ADA must be carefully monitored monthly. Staffi ng should be adjusted as enrollment numbers change.

FCMAT was asked to review the budget development process and prepare a multiyear projection to help the board and administration determine the accuracy of the budget and the reductions necessary to remain fi scally solvent. Due to several unforeseen circum-stances related to the condition of the data in the fi nancial system, FCMAT visited the district on three different occasions between March and August 2006 to gather and pro-cess the information for the multiyear projection.

The district administration and board implemented over $3 million in cuts in 2005-06 and another $5.7 million in 2006-07. Because of these aggressive actions, the FCMAT MYP indicates that the district will adhere to the AB1200 requirements to meet its fi nancial ob-ligations in the current and two subsequent years. However, this FCMAT MYP was pre-pared prior to the district’s recent negotiations settlement of 4% with all bargaining units. FCMAT returned to the district again in January 2007 to review the 2005-06 audit report and the 2006-07 fi rst interim report, but the interim report did not include the cost of the negotiation settlement in the district-prepared multiyear projections.

FCMAT identifi ed several areas where the district could make changes to improve com-munication, keep key district stakeholders better informed, and improve overall opera-tions. Most of the employees interviewed by FCMAT expressed that they were caught completely by surprise when the administration announced that major cuts would be nec-essary.

The district should implement procedures to keep employees and the community in-formed. Regular meetings, newsletters, and the district Web site are ways to achieve this goal. Principals and department managers state that they are not involved in the budget-ing process. Continuing to utilize the budget committee, making regular board presenta-tions, discussing budget issues at management meetings, and working with managers to develop budgets for their sites will address that concern.

One of the most important budget monitoring tools is a fully integrated position control system to track and control employee salaries and benefi ts. The district’s position control system is manual and is not integrated between human resources, payroll and the budget-ing process. Budget preparation and monitoring rest almost entirely with the Director of Fiscal Services, whose workload is overwhelming. The district risks the chance of er-rors and untimely budget updates because the position control system is not totally reli-

Fiscal Crisis & Management Assistance Team

EXECUTIVE SUMMARY6

able and most of the responsibility is assigned to one person. Staffi ng ratios should be developed and followed to ensure fairness and prevent overstaffi ng and overspending. Evaluating and monitoring the assignments of special education instructional assistants may yield some savings.

The district uses multiple software systems, the in-house Business Operating Support System (BOSS) and the LACOE PeopleSoft and human resources systems for payroll, which fl ows directly into the PeopleSoft system but not into BOSS. Agencies using mul-tiple systems must constantly reconcile the data to maintain fi nancial integrity and reli-able records. FCMAT could not verify the accuracy of the data in either system because the reports did not match. The use of multiple computer systems creates a duplication of work for the Human Resources and Business departments. The district’s Business Offi ce does not have a process for reconciling the data in the two systems until the year-end closing of the fi nancial records.

The district receives considerable categorical funding each year. There has been a his-torical pattern of carrying over a large portion of the categorical funds each year. Better planning to use the categorical funds more effectively may help ease the burden on the unrestricted general fund.

The 2005-06 year end actual fi nancial report yielded a much larger ending balance than the administration had projected in the interim reports. The board should be kept in-formed monthly of the status of the budget, especially during times when the budget is under scrutiny by the community and employee bargaining groups. The district consis-tently meets the statutory requirements of preparing and submitting the budget for adop-tion and the interim reports on time, but beginning a monthly budget revision cycle would help to project a more accurate ending balance and facilitate better planning during the budget development cycle each year.

Hacienda La Puente Unifi ed School District

BACKGROUND 7

Background The district’s once-large reserve balance of $25 million dwindled over several years and has been used to cover the defi ciencies between revenues and expenditures. Until the recent budget reductions were implemented, the district continued to defi cit spend even though budget adjustments were made in prior years. The defi cit spending has largely been due to declining enrollment and the district’s inability to quickly respond by adjust-ing the budget. The decline in enrollment was even greater than anticipated in 2005-06, leaving the district facing budget reductions of at least $5.7 million in 2006-07 on top of $3 million in cuts implemented in 2005-06 to retain fi scal solvency.

At the time of the initial FCMAT fi eldwork, the district was in the process of submitting a qualifi ed 2005-06 second interim report to the Los Angeles County Offi ce of Education because the board and administration had not had suffi cient time to identify or approve appropriate budget reductions before the statutory deadline to submit the second interim report. The projected ending balance for 2005-06 would barely meet the minimum 3% reserve for economic uncertainties required by the state without signifi cant budget cuts. The district’s fi nancial situation was very serious.

Employee contract negotiations were in progress during the FCMAT fi eldwork. Only the smallest bargaining unit (SEIU) had settled its contract by August 2006. The budget in-cluded an allowance to cover a 2% increase for all employees in 2005-06. Subsequent to the FCMAT fi eldwork, the district settled negotiations for 2006-07 at 4% for all bargain-ing units. It may be diffi cult for the district to explain to the public why salary increases are awarded while budget reductions are being made.

Fiscal Crisis & Management Assistance Team

BACKGROUND8

Hacienda La Puente Unifi ed School District

DECLINING ENROLLMENT AND BUDGET REDUCTIONS 9

Findings and Recommendations

Declining Enrollment and Budget Reductions

As with many California school districts, Hacienda La Puente has been experiencing declining enrollment. The consequences of declining enrollment and defi cit spending must be regularly and carefully managed to avoid fi nancial insolvency. The district used excess ending reserves to balance the budget over the past several years. Using onetime ending reserves to balance the budget shortfall must cease. The administration and board have kept budget reductions as far away from the classroom as possible, but few future cuts can be made without drastically affecting student programs or amending bargain-ing agreements. With 90% of the unrestricted general fund budget devoted to employee compensation, the bargaining units and the administration must work closely to help the district avoid insolvency.

The Director of Human Resources prepares enrollment projections, which are reviewed by the Assistant Superintendent of Business. Student enrollment and the corresponding average daily attendance (ADA) are the key factors in the amount of state funding re-ceived in revenue limit funds. Enrollment levels were down more than projected, exacer-bating the budget shortfall in 2005-06. District staff must review and update enrollment projections at least three or more times per year and throughout the budget development process, and adjust staffi ng accordingly.

In the past, some budget reductions have not materialized due to subsequent decisions by the administration or Governing Board. One example is the last-minute 2005-06 change in the high school teacher staffi ng ratio from 34:1 to 33:1 that occurred just before the start of school in 2005. The budgeted savings from a teacher ratio of 34:1 were not real-ized, so onetime reserve funds were used to cover the defi cit. In the future, programs should not be added or enhanced without carefully identifying an ongoing funding source or negative impact to the budget.

FCMAT did not delve into the specifi c budget reductions being considered by the admin-istration and board of trustees, but it was noted that the district has several small elemen-tary schools with fewer than 300 students enrolled. The administrative and operational costs to maintain a small school are nearly as high as those of a larger campus. Other school districts facing critical budget defi cits have been faced with similar diffi cult deci-sions to close small schools or adjust boundaries to smooth out enrollment. The district should seriously consider closing small schools during the next budget development cycle if defi cit spending cannot be curbed.

The budget cuts and savings that were implemented in 2005-06 and 2006-07 must be accurately monitored to ensure that full implementation continues to result in expected

Fiscal Crisis & Management Assistance Team

DECLINING ENROLLMENT AND BUDGET REDUCTIONS10

savings. The LACOE requires the district to submit a detailed, accurate budget reduction plan and multiyear projection by June 30 each year indicating that the district could meet its fi nancial obligations in the current and two subsequent years, along with its adopted budget. The 2006-07 budget was submitted on time and approved by the County Offi ce. The 2006-07 fi rst interim report was prepared and submitted to LACOE on time but did not include the cost of the 4% salary increase approved by the Governing Board.

The district has taken a proactive, responsible approach to address the budget shortfall in 2005-06 and 2006-07. The administration and board must work diligently to fi nd ways to reduce the budget when necessary with as little impact to students and employees as pos-sible. As the district faces major budget reductions in future years if enrollment continues to decline, the availability of cash to cover current expenditures may be tight. Monthly cash fl ow projections should be prepared and cash regularly reconciled to better manage cash and plan the timing of certain types of expenses.

Employee contract negotiations were in progress at the time of the FCMAT study and were recently settled for 2006-07. Making sure that all bargaining groups understand the seriousness of budget issues is of utmost importance. The district must carefully explain to the public why salary increases may be approved while budget reductions are being considered, especially if the board should discuss closing small schools in the future. Hiring and retaining the best teachers, managers, and classifi ed employees is critical to the success of the instructional goals of the district. Balancing the needs of students and employees while maintaining fi scal solvency is essential for any school district.

RecommendationsThe district should:

1. Educate the public and employees about the effect of declining enrollment on district revenues.

2. Monitor enrollment monthly.

3. Regularly discuss and address enrollment and any enrollment changes with the Governing Board.

4. Provide the board with updated budget information on the actual savings achieved compared to the amounts approved as budget reductions.

5. Consider all options if future budget reductions are imminent, including the cost of operating small schools.

6. Include all managers and principals in the budget development process.

Hacienda La Puente Unifi ed School District

COMMUNICATION 11

Communication

Communication may not have been suffi cient to keep key stakeholders and employees informed about the budget shortfall. Most employees stated that the budget problems caught them by surprise and they were unaware that major budget reductions were being considered. The most common complaint from staff was that communication was spo-radic or inadequate and must be improved to ensure that all parties are kept apprised of the board’s decisions during any budget reduction process.

The perception is that the budget problem may not have been real because spending on major and facility and technology project is ongoing. Employees and the public may not completely understand the difference between unrestricted general fund operating dollars and the various restricted funding sources available for construction and other specifi c programs.

Interviews with various district employees revealed a lack of understanding of the dis-trict’s budget problems and funding sources. Most employees stated that the budget prob-lems caught them by surprise and that they were unaware that major budget reductions were being considered.

The Business Department must keep the lines of communication open with its principals and department heads. Many districts use a detailed budget calendar to help managers meet key deadlines and participate in the budget development process.

Open communication, beginning budget work early, and including stakeholders in the deci-sion-making enable school districts to effectively work through diffi cult budget reduction processes. All parties should be kept informed over the next few months to ensure that the budget savings are properly calculated and incorporated into the fi nal adopted budget.

RecommendationsThe district should:

1. Find ways to improve communication throughout the district.

2. Open lines of communication with all key stakeholders, including parents, bargaining units, management and supervisory employees, and community members.

3. Consider a series of voluntary workshops, community meetings at schools, newsletters, and use of the district’s Web site to communicate with district stakeholders, especially during times when the district faces budget reductions. Develop and use a detailed calendar to help meet deadlines and keep managers informed.

Fiscal Crisis & Management Assistance Team

BUDGET DEVELOPMENT AND OVERSIGHT12

4. Include all managers and principals in the budget development process.

5. Present facility information at board meetings to keep constituents and community members informed about funding sources and progress of construction projects.

6. Explain the restrictions on capital facilities funds and other restricted funding sources.

Budget Development and Oversight

Responsibility for developing a district’s budget generally resides with the business of-fi ce under the direction and oversight of the Chief Business Offi cer. Budget revisions, monitoring, and fi nancial reporting are usually the responsibility of the director of fi scal services, with changes submitted by budget managers throughout the district. Budget monitoring is essential to ensure that district funds are used correctly and effectively.

The Director of Fiscal services develops and monitors the district’s budget. Managing a budget as complex and intricate as that of HLPUSD is a daunting task. Five business of-fi ce employees are assigned to budget tasks, but three of them are reasonably new to their positions and have limited experience. The staff turnover and lack of experience have placed a heavy burden on the director, creating a major backlog in budget revisions. The high turnover in key personnel in 2005-06 may have kept the seriousness of the budget crisis from being adequately communicated to the board, staff and community.

The district’s multiple software systems have made budget development and monitor-ing diffi cult and time-consuming. The business offi ce must develop, manage, revise, and monitor the budget and fi nancial resources in a timely manner to retain the district’s fi scal viability. The budget should refl ect the district’s goal to provide a comprehensive instruc-tional program.

The level of student enrollment, number of sites, impact of contractual obligations, and past practices often determine the budgeting process used by a school district. A success-ful budget model establishes a level of fi nancial confi dence in the district. Throughout the process, budget managers must be provided with clear and concise procedures to follow. Budget development should begin early in the year, preferably in January after the gov-ernor proposes the budget for the upcoming fi scal year. The fi rst step in the process is to approve a budget calendar indicating the due dates that must be met to adopt the district’s budget by June 30 each year. A well-managed budget development calendar serves two purposes: It allows site and department budget managers to identify their needs for the upcoming year and it strengthens communications between the managers and the busi-ness offi ce.

Hacienda La Puente Unifi ed School District

BUDGET DEVELOPMENT AND OVERSIGHT 13

The district distributes an annual budget guide. However, budget managers may not al-ways be fully trained or included in budget development. This seems especially true with regard to federal and state categorical programs. Most budget managers at sites and de-partments can access their budgets online, but need more training to use the system more effectively. Budget managers need to be held accountable for budgeting accurately and not overspending their allocations. The business offi ce staff should meet with budget managers and principals at least once in the spring to discuss budget assumptions and assist in budget development, and again in the fall to review prior year carryovers.

As the district may begin considering reductions and further changes in the budget for next year, it should develop a process to fully defi ne anticipated increases or decreases in spending. Once the options are identifi ed and prioritized, a full cost analysis must be completed to determine the total savings of each. For example, when positions are cre-ated or eliminated, the cost of statutory benefi ts and health coverage must be calculated along with salaries to quantify the full dollar value of these changes. Once budget reduc-tions are approved by the board, the cuts must be implemented and monitored to ensure that the anticipated savings are realized. Proper planning and cost analysis will protect the district’s future fi nancial health.

The business staff should strive to complete any current budget adjustments quickly to facilitate the preparation of multiyear projections that will accurately verify and forecast the fi nancial condition of the district this year and in two subsequent years.

The district should continue using a budget committee. Many school districts use budget committees with members representing all employee groups and community stakeholders to review and prepare recommended budget reductions to the board. A budget committee helps communicate fi nancial information to constituents, and would enhance trust among the constituencies in the district. The district uses multiple computer systems: the in-house BOSS system and the Los Angeles County Offi ce (LACOE) PeopleSoft and Human Resources systems for pay-roll, which fl ows directly into the PeopleSoft System but not into BOSS. Agencies using multiple systems must constantly reconcile the data to maintain fi nancial integrity and reliable records. The use of multiple computer systems creates a duplication of work for the Human Resources and Business departments. The HLPUSD business offi ce does not have a process for reconciling the data in the two systems until the year-end closing of the fi nancial records.

The district does not have a reliable, ongoing budget monitoring process in place. When the study team visited the district in March, June, and August, many revenue and expen-diture accounts had not been reviewed to determine if the estimates should be adjusted

Fiscal Crisis & Management Assistance Team

BUDGET DEVELOPMENT AND OVERSIGHT14

based on changes in enrollment or federal or state allocations. Additionally, the 2006-07 fi rst interim report indicated the same restricted carryover as the prior year, indicating that categorical spending had not been well planned.

The overwhelming workload of the Director of Fiscal Services complicates routine budget monitoring, which could mean that the district does not have a good picture of changes that may have occurred during the year. Also, the district is not able to accurately refl ect its net ending fund balance throughout the year if budgets are not kept up to date. If possible, budget revisions should be taken to the board for approval more often than just at interim reporting deadlines. Budget-to-actuals summaries should be prepared and submitted to the board as a discussion item monthly. This should make interim reports more useful and give the board a more accurate idea of the district’s fi nances. Submitting the summaries monthly also would allow the board and community to understand why variances are occurring. The summaries should be presented to the board for information, comment and direction if action is needed. When interim reports are prepared, they must include the very latest information with projections of the district’s fi nancial condition at the end of the year. Interims should be considered the nearest thing to closing the books, which means updating budgets to annual estimates and reviewing general ledger accounts to ensure that the balances refl ected are accurate and that no balances need to be cleared. Valid, thorough budget updates with projections of the district’s ending fund balance will ensure an early warning of any discrepancies between the budget projections and actual revenues or expenditures.

The district does not have a computerized integrated position control system. This issue will be discussed later in this report, but the method used currently requires manual track-ing of employee placement with step and column movement and actual health benefi t costs budgeted, assuming that every certifi cated employee may move a column on the salary schedule. This practice likely has the effect of overstating budgeted salary costs. Additionally, because of the lack of a computerized position control and budget projec-tion system, the district uses an average amount to project health benefi ts. This practice could overstate or understate the budget for health benefi t costs. When the district pre-pares the cost estimate for step and column movement of teachers, it does not prepare the net cost of retirements and resignations. This practice tends to overstate the actual annual cost of step and column movement.

The cost of salaries and benefi ts makes up approximately 90% of the district’s unre-stricted general fund budget. Unanticipated increases in these categories can quickly change the fi scal stability of a district. An integrated position control system establishes authorized positions by site or department and ensures that staffi ng levels and payroll expenditures conform to the district formulas and standards, preventing overstaffi ng and overpayments.

Hacienda La Puente Unifi ed School District

BUDGET DEVELOPMENT AND OVERSIGHT 15

The district does not appear to have a budget allocation policy related to replacement of furniture and equipment at schools. Interviews with school administrators revealed that schools are expected to use discretionary funds or categorical funds to replace items such as computers, classroom furniture, lunch tables, etc. This process has led to a perception of unequal distribution of resources and could violate supplanting regulations for categor-ical programs.

The district currently pays retiree health benefi ts for employees to age 65. The unrestrict-ed general fund currently pays all costs for this program regardless of the employee’s original funding source. These expenditures should be charged to the program or fund where the employee originally worked.

The 2005-06 second interim report for the adult education fund was budgeted incorrectly. Revisions submitted to the business offi ce by the Assistant Superintendent were not promptly updated. Based on FCMAT’s interview with the child development program di-rector, the second interim report for that fund also was incorrect. All operating funds such as the adult education fund, child development fund and cafeteria fund should be updated every time the general fund budget is revised, especially at interim reporting periods.

RecommendationsThe district should:

1. Review the need to maintain dual fi nancial systems.

2. Schedule training sessions on district budgets for school administrators, managers and secretaries.

3. Ensure that the Business Department reviews the budget monthly and adjusts revenue and expenditures as needed.

4. Provide assistance for the Director of Fiscal Services to ensure that all funds and budget line items are reviewed regularly.

5. Ensure that schools and departments have access to up-to-date and accurate budget information, and hold them accountable for not overspending budgets and for following established purchasing procedures.

6. Present budget changes and monthly budget summaries for the board to review, discuss and approve at a public meeting, accompanied by the rationale for any changes.

7. Continue to utilize a budget committee. Many school districts’ budget committees include members from all employee groups and community stakeholders to review and prepare recommended budget reductions for the Governing Board.

8. Carefully prepare the interim reports to include the very latest information with projections of the district’s fi nancial condition through the end of the year.

Fiscal Crisis & Management Assistance Team

POSITION CONTROL AND STAFFING16

9. Work to establish a more accurate method to estimate annual column movement costs based upon the average actual column movement in several prior years.

10. Review the estimated health benefi t costs to actual health benefi ts costs to determine if the current budgeting method should be further refi ned.

11. Prepare step and column estimates to include new hires and the effect of retirements and resignations.

12. Charge retiree health benefi ts appropriately to all funds and categorical programs. Accomplish this by using a benefi ts account object code and charging a small percentage of retiree benefi ts against each payroll as allowed. Use these accumulated funds from all sources to pay for retiree health benefi t costs.

13. Develop a district-level budget process whereby schools sites can request funds for replacement of old, broken, vandalized or stolen furniture and equipment.

14. Identify a long-term funding plan for replacement and maintenance of the district’s signifi cant investment in technology.

15. Ensure that all fund and program budgets are updated at interim reporting periods.

Position Control and Staffi ng

One of the most critically essential budget development and monitoring tools is a posi-tion control system to monitor and authorize staffi ng, and identify employee salary and benefi t costs. A reliable position control system also is an integral part of the overall in-ternal accounting controls to ensure that only authorized positions are fi lled and salaries and benefi ts are budgeted and paid only as approved by the Governing Board. Salaries and benefi ts are approximately 90% of the district’s general fund budget. Unanticipated increases in these categories can quickly alter a district’s fi scal stability. An integrated po-sition control system establishes authorized positions by site and department and ensures that staffi ng levels and payroll expenditures conform to district formulas and standards, preventing overstaffi ng and overpayments.

The HLP position control system is not computerized or integrated with human re-sources, payroll and budget. Instead, employee tracking and budgeting for salaries and benefi ts is managed manually by the Human Resources Department and Fiscal Services. The Director of Fiscal Services uses an Excel spreadsheet based on payroll informa-tion to identify current employee salaries and benefi ts. Data in the Human Resources Department is managed using spreadsheets and by memory. Human Resources tracks and fi lls positions. Implementation and utilization of a reliable, computerized position con-trol system by human resources, budget and payroll should be a top priority. This would enable human resources and the business offi ce to jointly maintain salary and benefi t in-formation. It would only allow payroll to pay employees based on the information in the system. This separation of duties enhances internal control standards.

Hacienda La Puente Unifi ed School District

CATEGORICAL PROGRAMS AND SPECIAL EDUCATION 17

Staffi ng ratios must be carefully reviewed and strictly enforced. The district has reduced certifi cated staff as enrollment declined, but classifi ed positions may not have been ad-justed in a timely manner. The district’s small and large schools were reported to have similar classifi ed support staff regardless of the enrollment level. Staffi ng ratios should be reviewed and updated before the budget development cycle begins each year.

District staffi ng ratios for classifi ed staff and for certain certifi cated positions were es-tablished several years ago and have not been adjusted as enrollment has declined at a number of district schools. Interviews with school staff members revealed perceived dis-crepancies in staffi ng at schools and a perception that staffi ng allocations are not changed when enrollment changes. While many schools in the district are declining, several are growing and indicate they have not received additional staff. Involving site administrators will help to create buy-in and a transparency in the staffi ng allocation process. In creating this process, the district should look at an enrollment-based model as well as considering other unique needs and characteristics of individual schools.

Under the current HLPUSD dual computer system and lack of an integrated position con-trol module, positions are entered in payroll and then the budget is projected from payroll data. This creates an internal control weakness since there is no check and balance system that ensures that people being paid are actually fi lling budgeted and authorized positions.

RecommendationsThe district should:

1. Develop and use a computerized, integrated position control system.

2. Review and revise staffi ng allocation formulas for classifi ed staff and certain certifi cated positions to ensure fairness at all sites, whether enrollment is declining or increasing.

Categorical Programs and Special Education

The district receives considerable state and federal categorical funds that are designated by the granting agency for special projects. At the end of 2005-06, the district had over $6 million in unspent carryover categorical funds. Careful planning for the effective use of these funds may help ease the burden on the unrestricted general fund. The recent 2006-07 fi rst interim report shows that the restricted ending balance is projected to be the same as the prior year ending balance, indicating that categorical fund expenditures have not been reviewed or planned for use to provide services for students.

The study team noted that the district’s categorical (CAT) form for 2004-05 showed a restricted carryover for home-to-school transportation and special education transporta-tion. This is highly unusual since it would indicate the district incurred no encroachment

Fiscal Crisis & Management Assistance Team

CATEGORICAL PROGRAMS AND SPECIAL EDUCATION18

for transportation in the prior year. The current year’s budget showed that only personnel costs were budgeted in the transportation resource code. Expenditures may have been in-correctly coded, causing incorrect information to be entered on state and federal reports. This could result in the district not receiving appropriate funding in future years. The dis-trict should carefully review its account code structure for accuracy and make corrections as necessary. The district should also consider refi ling certain state and federal reports if revenues and/or expenditures have been reported incorrectly.

Categorical funds are an integral part of the district budget. Categorical program develop-ment should be integrated with the district’s goals and should be used to respond to stu-dent needs that cannot be met by unrestricted expenditures. The Superintendent and cabi-net should establish procedures to ensure that categorical funds are expended effectively to meet district goals. Carryover and unearned income of categorical programs should be monitored and evaluated in the same manner as general fund unrestricted expenditures.

The district has large unexpended carryover balances in numerous categorical programs. The revenues and expenditures for these programs must be reviewed and evaluated in the same manner as unrestricted general fund revenues and expenditures. Plans need to be made to budget categorical funds the district expects to receive early in the budget development cycle. These plans must be consistent with categorical funding guidelines and restrictions. Schools should consider all funding sources when addressing key strate-gies. Restricted funds should be used fi rst since they are allocated for students in the year they are received. Whenever there is doubt about whether to use unrestricted or restricted funds for an item that can come from either source, restricted funds should be used. Reports of categorical expenditures should be prepared monthly for the Chief Academic Offi cer and Chief Business Offi cer. They should review expenditures to date and remain-ing balances and determine whether any of these funds can be redirected to reduce car-ryover and unused balances. A review of effective categorical program supervision, deliv-ery and expenditure of funds should be included in evaluating managers with responsibil-ity over these specifi c funds. The use of AB 825 categorical fl exibility provisions as well as fl exibility provisions for federal programs should be reviewed to assist in alleviating the district’s budget crisis.

Interviews with district managers and employees indicated the need for budget training and for improved budget accountability for managers and principals. Principals indicated the desire for training on the use of categorical funds and on how the district and site budgets are developed. Additionally, concerns were expressed that categorical carryover information did not reach school sites until late in the year and then was often revised several times, causing schools to continually update school site plans.

As with most districts in California, the cost of Special Education has increased signifi -cantly. It was reported that the caseloads of Special Education teachers and staff may need realignment. In small schools the teacher caseloads may be below average. Careful

Hacienda La Puente Unifi ed School District

CATEGORICAL PROGRAMS AND SPECIAL EDUCATION 19

review of six-hour special education instructional assistant positions indicates that chang-ing some positions to part-time could reduce costs. Additionally, the district needs to formalize a tracking system to ensure that one-on-one instructional assistants follow the student to whom they are assigned and that the position is eliminated if the student leaves the district or services are no longer required.

RecommendationsThe district should:

1. Set up a training session for school administrators and key staff members on the allowable uses of various categorical funds.

2. Carefully review for accuracy the recording and reporting of transportation program charges to avoid any loss of funding.

3. Consider refi ling certain transportation reports if revenues and/or expenditures have been reported incorrectly.

4. Allocate school site carryover to the sites no later than September 30 and work with schools to review these carryover budgets.

5. Engage the instructional department, under the direction of the Chief Academic Offi cer, to develop and monitor the district’s categorical budget. Ensure compliance by having the Chief Academic Offi cer review and approve personnel and purchase requisitions that are charged to categorical programs.

6. Ensure that the Consolidated Application is developed and reviewed against actual revenue and expenditure transactions in the fi nancial records.

7. Set priorities for the use of categorical funds. Develop plans for the use of carryover funds.

8. Evaluate the caseloads of Special Education staff and reallocate positions or duties if caseloads are below average.

9. Review six-hour Special Education instructional assistant positions to determine if some positions might be converted to part-time status.

10. Ensure that Special Education one-on-one instructional assistants follow the students to whom they are assigned.

Fiscal Crisis & Management Assistance Team

CATEGORICAL PROGRAMS AND SPECIAL EDUCATION20

Hacienda La Puente Unifi ed School District

MULTIYEAR FINANCIAL PROJECTION 21

Multiyear Financial ProjectionMultiyear fi nancial projections (MYP) are an important part of the overall budget process and a major requirement of the AB1200 school district fi nancial oversight legislation. The district is required to submit multiyear projections along with the adopted budget and all interim reports. AB1200 requires school districts to be able to meet all fi nancial obliga-tions for the current and two subsequent years. FCMAT noted some inconsistencies in the district-prepared MYP at the time the 2006-07 budget was adopted. The independently prepared multiyear projections done by FCMAT in this report include certain corrections and assumptions that differ from those the district used in their original projections. The FCMAT MYP, which was prepared last fall, indicates that the district will be able to meet its obligations in the current and two subsequent years. FCMAT prepared the multiyear fi nancial projections that are in this report. An unrestrict-ed general fund summary appears at the end of this section of the report, and the detailed MYP is attached as Appendix E. After reviewing district records, interviewing employees and examining numerous fi nancial reports to gather pertinent information for the MYP, FCMAT developed certain assumptions that are identifi ed in the MYP narrative. The dis-trict has engaged in defi cit spending in the past and is likely to continue doing so even though signifi cant budget adjustments were made in 2005-06 and 2006-07 if the budget is not carefully and frequently monitored.

FCMAT’s MYP was prepared using the district’s 2006-07 adopted budget and other fi -nancial information but may contain assumptions different from other multiyear projec-tion assumptions prepared by district staff. At this time, based on the 2006-07 budget information the district provided to FCMAT, it appears that the district will comply with the AB1200 requirements of meeting its fi nancial obligations in the current and two sub-sequent years. This was determined before the 4% salary increases were awarded.

The district met the required 3% reserve for economic uncertainties and ended the 2005-06 fi scal year with unrestricted general fund reserves exceeding the projected ending fund balance on the 2005-05 third interim report by over $3 million. The unaudited actual fi -nancial statements indicated that all of the excess funds have been designated for specifi c future purposes as identifi ed in Section 5 of the Fiscal Health Risk Analysis included in this report.

In 2006-07, prior to the 4% increase, salaries and benefi ts were budgeted at approximate-ly 90% of the district’s unrestricted general fund. A cap on the cost of employee health benefi ts at $9,500 per employee was in effect at the time the FCMAT MYP was prepared. The adopted budget included projected step and column moves for both certifi cated and classifi ed employees. The ending fund balance of 2005-06 included a designation of 2% to offset a potential retroactive pay increase.

Fiscal Crisis & Management Assistance Team

MULTIYEAR FINANCIAL PROJECTION22

In developing and implementing a multiyear projection, the district’s primary objective is to achieve and sustain a balanced budget, improve academic achievement and maintain local governance. MYPs are required by AB 1200 and AB 2756 and should be timely and contain the most current fi scal information available. These projections allow the district and its major stakeholders to predict revenues and expenditures, and to ensure that the district will be able to meet its fi nancial obligations in the current and two subsequent fi s-cal years.

The following MYP was prepared based on the district’s adopted budget as of July 1, 2006, using information provided by management at that time. Although the district is in declining enrollment, it has been proactive in planning its resources for the future and has maintained a balanced budget. At the time this MYP was prepared, negotiations had not been settled for 2006-07. FCMAT has subsequently learned that the district settled negotiations with all bargaining units at 4% for 2006-07. The district is not experiencing any signifi cant fi nancial challenges at this time but could face further budget reductions if the budget is not monitored regularly. The district’s 2006-07 fi rst interim report did not include the cost analysis of the 4% salary increases.

If a district cannot meet its fi nancial obligations for the current or two subsequent fi scal years, the county superintendent of schools must notify the governing board of the district and the Superintendent of Public Instruction if the district falls below the required reserve level. The county offi ce adheres to Education Code 42127.6 when assisting any school district in this situation.

County assistance could include assigning a fi scal expert to advise the district on fi nancial problems, conducting a study of the fi nancial and budgetary conditions of the district, or requiring the district to submit a proposal for addressing its fi scal condition. If a district does not meet the required reserve levels, the intent of the MYP is to help the county and the district formulate a plan to regain fi scal solvency and restore the required ending bal-ance.

California school districts and county offi ces use many different methods and software products to prepare reliable multiyear fi nancial projections. The FCMAT MYP was pre-pared using FCMAT’s Budget Explorer multiyear software, a Web-based forecasting tool that is available to all California school districts at no cost. The MYP was prepared using district data that was uploaded into Budget Explorer from the district’s mainframe com-puter system.

Any forecast of fi nancial data has inherent limitations, including issues such as the tim-ing of the report, subsequent negotiated settlements, unanticipated changes in enrollment trends and changing economic conditions on a state and local level. Therefore, the budget forecasting model should be viewed as a tool to assess trends based on certain criteria and assumptions, not as a prediction of exact numbers. The projection should be updated

Hacienda La Puente Unifi ed School District

MULTIYEAR FINANCIAL PROJECTION 23

at each interim fi nancial reporting period to maintain the most accurate data. The district should consider using Budget Explorer for future multiyear projections to provide a more detailed analysis for the board and district stakeholders to review, particularly since the 4% salary increase may have long-term fi nancial consequences that will affect future years.

FCMAT reviewed the district’s budget assumptions as of August 2006 to validate the 2006-07 adopted budget report and multiyear fi nancial projections. Budget assumptions include conservative economic factors outlined by School Services of California (SSC) in its fi nancial dartboard and fi scal information available at the California School Finance and Management 2006-07 Conference.

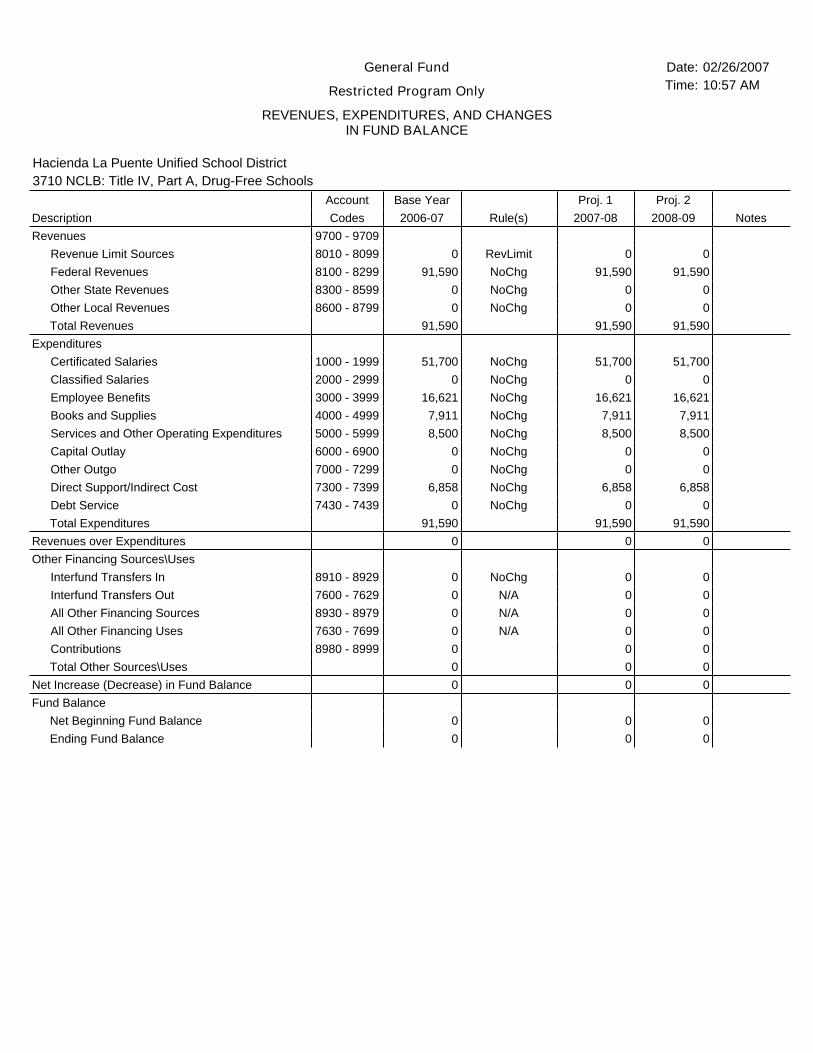

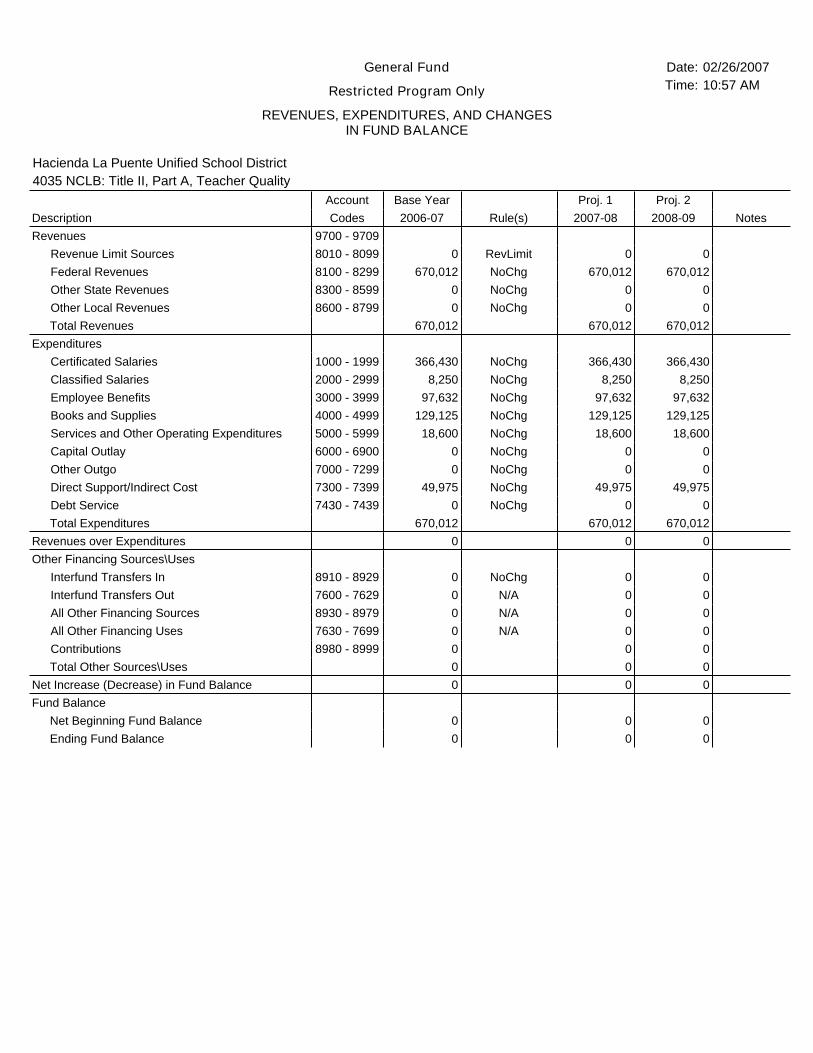

The following MYP represents FCMAT’s fi nancial projections as of August 2006 for the unrestricted general fund, which is where most of the district’s expenditures occur. (Please see next page.) The MYPs for the restricted and combined general fund are lo-cated in Appendix E to this report.

Fiscal Crisis & Management Assistance Team

MULTIYEAR FINANCIAL PROJECTION24

Notes

1, 2, 3

4

5, 6, 7

(1,276,721)(1,276,721)(1,276,721)3,302,3143,220,5361,997,600

2008-092007-082006-07Codes

General Fund

Restricted & Unrestricted Programs

REVENUES, EXPENDITURES, AND CHANGESIN FUND BALANCE

Date:Time:

02/26/200710:49 AM

Hacienda La Puente Unified School District

Proj. 2Proj. 1Base YearAccountDescription

129,943,858128,130,593125,252,2348010 - 8099Revenue Limit SourcesRevenues

12,893,71412,893,71412,893,7148100 - 8299Federal Revenues36,778,53135,925,53134,827,5668300 - 8599Other State Revenues1,673,2201,673,2201,673,2208600 - 8799Other Local Revenues

181,289,323178,623,058174,646,734Total Revenues

85,189,26484,367,94783,655,2661000 - 1999Certificated SalariesExpenditures

27,080,41026,655,08826,238,1022000 - 2999Classified Salaries37,574,61036,950,59536,168,0913000 - 3999Employee Benefits8,941,9278,718,0168,401,7934000 - 4999Books and Supplies

176,710,288174,125,801171,372,413Total Expenditures4,579,0354,497,2573,274,321Excess (Deficiency) of Revenues over Expenditures

16,348,45415,959,68715,540,2805000 - 5999Services and Other Operating Expenditures1,532,8501,492,8161,451,0286000 - 6900Capital Outlay2,324,9202,263,7992,200,0007000 - 7299Other Outgo

(2,282,147)(2,282,147)(2,282,147)7300 - 7399Direct Support/Indirect Cost

0008910 - 8929Interfund Transfers InOther Financing Sources\Uses

1,276,7211,276,7211,276,7217600 - 7629Interfund Transfers Out0008930 - 8979All Other Financing Sources0007630 - 7699All Other Financing Uses0008980 - 8999Contributions

Total Other Sources\Uses

24,397,12021,176,58519,178,985

Net Increase (Decrease) in Fund Balance

Net Beginning Fund BalanceFund Balance

27,699,43424,397,12021,176,585Ending Fund Balance

50,00050,00050,000

Components of Ending Fund Balance

300,000300,000300,0006,975,5846,975,5846,975,584

0006,429,4986,517,1496,622,2325,339,6155,262,0785,179,474

000

8,604,7375,292,3092,049,295

9711Reserve for Revolving Cash9712Reserve for Stores9719Reserve for All Others

9730 - 9739General Reserve9740 - 9759Legally Restricted Balance9770 - 9774Designated for Economic Uncertainty

9700 - 9709Fund Balance Reserved

9790Undesignated/Unappropriated

0007430 - 7439Debt Service

0009780Other Designated

0009790Negative Shortfall

Hacienda La Puente Unifi ed School District

MULTIYEAR FINANCIAL PROJECTION 25

2006-07 Projected Ending BalancesAs noted in the following table, there are differences between the projected ending bal-ance for the budget year 2006-07 as determined by the district and the projected ending balance determined by FCMAT.

2006-07 Projected Balances as of August 2006District FCMAT

Unrestricted 15,293,536 14,554,353Restricted 6,622,232 6,622,232Total 21,915,768 21,176,585

The following will explain the unrestricted difference of ($739,183) between the district’s and FCMAT’s MYPs for the unrestricted general fund:

• FCMAT used the July 25, 2006 updated equalization aid provided by SSC to cal-culate the district’s revenue limit sources. This updated information provided an additional $10.81 per ADA and will result in an increase of $240,817 in revenue limit sources funding.

• Prior year revenue limit is not normally budgeted. Any positive or negative fi nan-cial impact of the fi nal prior year calculation is typically handled as an accrual or liability and does not impact the current year revenues. Therefore, FCMAT did not include the current budgeted amount of $680,000 in this projection, resulting in a decrease in revenue.

• FCMAT was unable to verify the source of the unrestricted federal revenue. Therefore, FCMAT’s projection does not include the $300,000 budgeted for unre-stricted federal revenues in the district’s projection.

Multiyear Forecast AssumptionsFCMAT has focused attention on the unrestricted portion of the district’s general fund budget, including the impact of increasing special education, community day school, transportation and the routine restricted maintenance calculations. The FCMAT projec-tion does not assume expending the sizeable 2005-06 restricted ending balance, because at the time of FCMAT’s fi eldwork the district had not shared specifi c plans for the use of these funds. In fact, as of the 2006-07 fi rst interim report, the district does not appear to have made specifi c decisions as to how the categorical carryover funds will be allocated or spent.

Enrollment and Average Daily AttendanceThe FCMAT study team reviewed the enrollment and average daily attendance (ADA) trends of the district for the years 2001-02 through 2005-06. The review compared the October CBEDS student enrollment count to the April P2 ADA data. Revenues earned by

Fiscal Crisis & Management Assistance Team

MULTIYEAR FINANCIAL PROJECTION26

the district through the revenue limit calculations are based on either the current or prior year P-2 data, whichever is higher. With the exception of an increase of 315 students in 2003-04, the district’s enrollment has been declining for a net enrollment loss of 2,041 over the previous four years. FCMAT has continued that conservative trend in its mul-tiyear projection using historical CBEDS data, cohort survival classroom progression and county birth rates to develop the attendance projection. FCMAT’s projected CBEDS and ADA are shown below. More detail as to enrollment and ADA analysis is located in Appendix E to this report.

2002 2003 2004 2005 2006 * 2007 * 2008 *CBEDS 25,184 25,499 24,955 23,241 23,037 22,736 22,297P2 ADA 23,076 23,076 22,677 22,223 21,767 21,476 21,061CBEDS/ADA % 91.6% 90.5% 90.9% 95.6% 94.5% 94.5% 94.5%

* estimated

Although the district’s ratio of enrollment to ADA in 2005-06 was within the average range for schools, the prior years’ ratio was well below the state average. Keeping kids in school for more days each year will increase the district’s revenue limit funding by increasing the number of ADA used in the calculation. At this time, the district continues to be funded on prior year P2 ADA because of declining enrollment. Improvements to the ratio will be realized in the funding for the following year at such time as the district experiences a growth in current year ADA above the prior year level. An increase of 1% in the attendance of currently enrolled students above last year’s P2 level could bring an additional $1,256,000 in revenue limit funding.

RevenuesRevenue Limit SourcesAt the time this MYP was prepared, FCMAT calculated the district’s revenue limit for 2006-07 using the most current state budget information from the July 2006 California School Finance and Management Conference and factors from the fi nal budget version 2006 SSC Dartboard. These factors include the estimated statutory COLA, elimination of the defi cit, and lottery rates for the current and projected fi scal years.

Anticipated declining enrollment numbers have affected the amount of revenues the dis-trict will receive; however, an enhanced COLA, equalization aid and a fully funded defi -cit factor mitigate the loss of revenue limit funding in the projection years. The district’s revenue limit sources are made up of a combination of state aid and local tax revenues in the calculation. FCMAT did not increase the level of district property taxes in the calcula-tion. This does not impact the total funding level, only the proportion of state aid to prop-erty taxes.

Hacienda La Puente Unifi ed School District

MULTIYEAR FINANCIAL PROJECTION 27

Federal RevenuesFCMAT did not include any unrestricted federal revenues in the projection because the source of any such funds could not be verifi ed.

State RevenuesFCMAT projected K-3 class size reduction revenues with COLA plus adjustments for declining enrollment. No mandated cost reimbursement funding is included in the pro-jection years. Due to uncertainty in the state funding of mandated cost reimbursements and the high rate of disallowed claims audited by the State Controller’s Offi ce, budgets should be adjusted when funds are received.

Local RevenuesNo changes were made to this revenue category.

ExpendituresCertifi cated SalariesThe FCMAT multiyear projection includes the impact of step and column salary move-ment. FCMAT did not include any increase for salary compensation in the projec-tion, as salary increases had not yet been determined through negotiations. FCMAT did reduce the number of teachers funded with unrestricted dollars by 18 in the projection year 2007-08 and seven in 2008-09 to offset the anticipated declining enrollment. The 2005-06 ending balance indicated a 2% reserve for future salary increases.

Classifi ed SalariesAs noted above, FCMAT did not include any salary increase but did include the ongoing impact of step and column movement.

Employee Benefi tsFCMAT increased statutory benefi ts in proportion to certifi cated and classifi ed salary changes in the projection years and factored a small COLA increase in employer health contributions in 2006-07 and 2007-08.

Books and SuppliesFCMAT adjusted the budget for materials and supplies using the Consumer Price Index (CPI) infl ation factor from the SSC Dartboard.

Services and Other Operating ExpendituresBudget amounts for travel and dues were not adjusted in the projection years. All other expenditures in the 5000 object series were adjusted using CPI.

Capital OutlayThe equipment budget was increased by CPI.

Fiscal Crisis & Management Assistance Team

MULTIYEAR FINANCIAL PROJECTION28

Direct Support/Indirect CostsIndirect costs have been adjusted based on the changes in categorical budgets in the pro-jection years.

Other Financing Sources/UsesTransfers OutThe transfer out in 2006-07 is the required contribution of ½ of 1% of the total general fund budgeted expenditures to the deferred maintenance fund.

Contributions to Restricted ProgramsUnrestricted contributions to restricted programs are for community day school, special education and the routine restricted maintenance program. FCMAT adjusted the contribu-tions according to calculated shortfalls for community day school and the special education program based on the current service delivery model. The routine restricted maintenance contribution was adjusted based on the 3% of total general fund expenditures requirement.

Net Increase/Decrease in Fund BalanceThe difference in the 2006-07 budgeted unrestricted revenues and expenditures is a posi-tive $1,997,600, taking into account the necessary contribution to restricted programs. This budgeted positive balance is a conservative amount and equates to 1.5% of the dis-trict’s unrestricted revenues.

Reserve LevelThe FCMAT projection indicates that the district will be able to meet the 3% minimum required reserve level in 2007-08 and 2008-09. However, this could change based on the impact of the 4% salary settlement and any future negotiated settlements with bargaining unit groups. The district must continue to monitor the budget carefully and accurately and address potential shortfalls in a timely manner.

RecommendationsThe district should:

1. Monitor enrollment and ADA monthly.

2. Consider using FCMAT’s free Budget Explorer software to prepare future multiyear fi nancial projections.

3. Update the MYP to refl ect the impact of the recent 4% negotiated salary settlements.

4. Update the budget as changes occur, not just at interim reporting periods.

5. Address potential budget shortfalls in a timely manner.

6. Develop a plan to effectively use the categorical carryover funds.

Hacienda La Puente Unifi ed School District

FISCAL HEALTH RISK ANALYSIS 29

Fiscal Health Risk AnalysisIn 2005, FCMAT developed the Fiscal Health Risk Analysis as a tool for local educa-tional agencies to evaluate the fi scal impact of trends in 18 operational and management areas. Reviewed in isolation, these areas may not independently be considered detrimen-tal to fi scal solvency. However, when evaluated as the core composite elements of the district’s fi nancial condition, these areas provide a clear checklist for establishing and maintaining fi scal solvency.

To conduct the fi scal health and risk analysis for the Hacienda La Puente Unifi ed School District, the FCMAT study team requested and reviewed a comprehensive list of fi nancial re-ports, enrollment and ADA information, as well as supplemental documents and system print-outs. The team met with the district Assistant Superintendent, Business Services and Director of Fiscal Services, and interviewed other key administrators and staff in the district.

The district has been experiencing signifi cant defi cit spending and declining enrollment over the past few years. During the 2005-06 fi scal year, the CBEDS enrollment declined by 1,714 from the prior year. FCMAT conducted a multiyear comparison of the general fund for past, current, and projected revenues, expenditures, transfers and components of the ending fund balance for fi scal years 2001-02 through the unaudited actuals for 2005-06 along with the 2006-07 adopted and fi rst interim budgets. FCMAT’s projections show en-rollment declined by about 200 in 2006-07. The enrollment decline of 200 was accounted for in the 2006-07 adopted budget and FCMAT’s multiyear projections. In periods where enrollment and ADA are fl at or declining, the district must exercise extreme caution regard-ing budgetary issues such as negotiations, staffi ng, and defi cit spending to ensure fi scal solvency. Diligent planning will enable the district to more clearly understand its fi nancial objectives and strategies to sustain fi nancial solvency. The district must continuously update the budget as new information becomes available in the district or from other funding and regulatory agencies. Although the district complies with the mandated budget revisions at the fi rst and second interim reporting periods, budget revisions should be prepared and pre-sented to the board monthly to ensure that changes and updates are known quickly and that the savings expected from budget reductions actually materialize.

The following Fiscal Health and Risk Analysis was completed by the FCMAT study team and refl ects the fi nancial status of the district as of the completion of FCMAT’s fi eldwork in August 2006. The analysis also includes an update of certain key events subsequent to the FCMAT fi eldwork, such as the results of the 2006-07 bargaining unit settlements, which will affect the district both fi scally and operationally.

The analysis focuses on the district’s unrestricted general fund, representing the revenues and expenditures related to funding sources that allow full district discretion in how mon-ies are used. The analysis contains specifi c comments and recommendations to assist the district in measuring and improving its fi nancial solvency score.

Fiscal Crisis & Management Assistance Team

FISCAL HEALTH RISK ANALYSIS30

Fiscal Health Risk Analysis

Key Survival Questions

1. Defi cit Spending • Is this area acceptable? Yes• Is the district spending within its budget in the current year? Yes (after

implementing major budget reductions)

The district has adopted a budget for 2006-07 that includes approximately $5.7 million in budget reductions, following budget reductions implemented in 2005-06 of $3.5 million. These reductions include staffi ng reductions, program delivery changes, and reductions to department and school site discretionary budgets.

The district administration became aware of the need for signifi cant budget reductions during fall 2005. Budget reductions were identifi ed during the preparation of the 2005-06 fi rst interim report, with the goal to reduce the budget by at least $3 million that year. The district requested that FCMAT prepare an independent multiyear projection to verify the estimated budget shortfall in 2005-06 and subsequent years. FCMAT suggested that the district issue a third interim report for 2005-06 to better project the ending fund balance prior to FCMAT’s preparation of the multiyear projections. The third interim general fund budget refl ected an unrestricted ending balance of $9,287,149, which was signifi cantly lower than the actual unrestricted ending balance of $12,556,753. Although this difference refl ects budget savings and conservative spending, it also indicates that the budget monitoring and oversight functions had not been working properly.

• Has the district controlled defi cit spending over multiple years? No

FCMAT reviewed independent audit reports for Hacienda La Puente from 1997-98 through 2005-06 that identifi ed general fund defi cit spending in six of the nine years. The district showed excess revenues over expenditures in 2000-01, 2004-05, and 2005-06 and budgeted excess revenues in 2006-07, before the settlement of negotiations.

• Is the defi cit spending addressed by fund balance, ongoing revenues, or expenditure reductions? Yes

The district administration and board developed and implemented budget reductions of $3.5 million in 2005-06 and $5.7 million in 2006-07 that appear to have adequately addressed the defi cit spending in both years, before the settlement of employee bargaining unit negotiations. Much of the success of this planning will depend on the accuracy of the enrollment projections for the current and future years as well as the district’s ability to prepare accurate multiyear fi nancial

Hacienda La Puente Unifi ed School District

FISCAL HEALTH RISK ANALYSIS 31

projections after reaching negotiated settlements of approximately 4% in ongoing salary increases for all employees. The July 1, 2006 adopted budget for 2006-07 indicated a projected net increase in the unrestricted general fund balance of approximately $2.7 million. The 2006-07 fi rst interim report indicates a projected increase in the ending fund balance of $3 million but does not include the 4% general fund salary increases that were recently approved by the board, estimated to be about $4.5 million.

2. Fund Balance • Is this area acceptable? Yes• Is the district’s fund balance consistently increasing? No

The general fund ending balance has experienced both increases and decreases since 1997-98. However, the fund balance has continued to support the required 3% minimum reserve level. The district’s diligence in implementing budget reductions in 2005-06 and 2006-07 indicates improvement in the fund balance before the recently approved salary increases.

Ending Fund Balance* Combined General Fund1998-99 $12,710,9981999-00 $9,133,6892000-01 $22,228,9632001-02 $22,071,7512002-03 $13,318,8172003-04 $12,523,1872004-05 $15,559,0762005-06 $19,178, 9852006-07 $22,258,650

*source – annual independent audit balances include legally restricted categorical ending balances 2006-07 projected balance taken from fi rst interim report, 12/15/06

• Is the fund balance increasing due to ongoing revenues and/or expenditure reductions? Yes

The projected fund balance increases for 2005-06 and 2006-07 are due to increased revenues and decreased expenditures but do not refl ect any negative effect from the negotiated settlements for 2006-07.

3. Reserve for Economic Uncertainty • Is this area acceptable? Yes• Is the district able to maintain its reserve for economic uncertainty in the

current and two subsequent years based on current revenue and expenditure trends? Yes

Fiscal Crisis & Management Assistance Team

FISCAL HEALTH RISK ANALYSIS32

• Was the district able to maintain its reserve in 2003-04 and 2004-05 without using the state fl exibility? Yes

• Is the district aware that the reserves must be restored with the 2005-06 budget? N/A