50

1 Bioenergy in North-West Russia Challenges to export… Harald Birkeland & Francois Sammut Norsk Energi

| Date post: | 07-Apr-2018 |

| Category: |

Documents |

| Upload: | firdadimawarnita |

| View: | 227 times |

| Download: | 0 times |

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 1/50

1

Bioenergy in North-West RussiaChallenges to export…

Harald Birkeland & Francois Sammut

Norsk Energi

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 2/50

2

Bioenergy - NW Russia

• Energy status Russia, NW Russia

• Forest Resources• Possibilities & new developments

• Export of biofuels & ”climatic values”• Project Examples

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 3/50

NW-Russia / the Barents

Region

The Barents Euro-Arctic Region, © Finnbarents

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 4/50

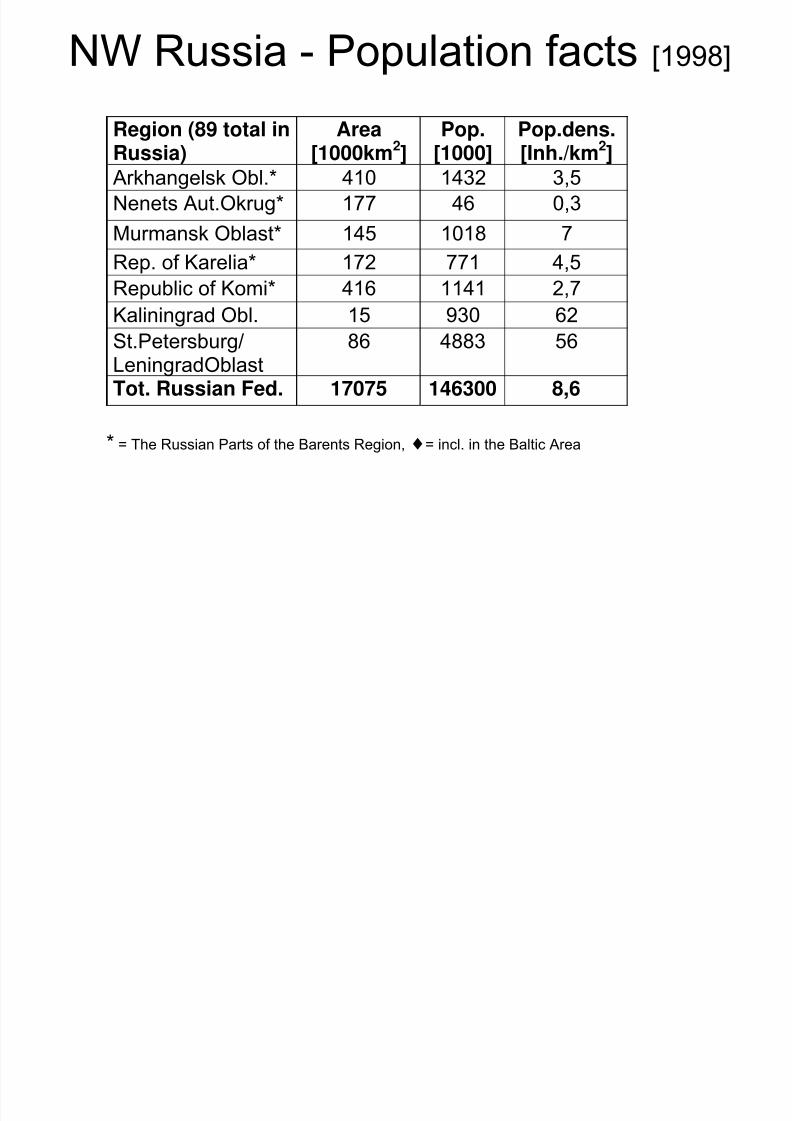

NW Russia - Population facts [1998]

Region (89 total inRussia)

Area[1000km2]

Pop.[1000]

Pop.dens.[Inh./km2]

Arkhangelsk Obl.* 410 1432 3,5

Nenets Aut.Okrug* 177 46 0,3Murmansk Oblast* 145 1018 7

Rep. of Karelia* 172 771 4,5

Republic of Komi* 416 1141 2,7

Kaliningrad Obl. 15 930 62St.Petersburg/LeningradOblast

86 4883 56

Tot. Russian Fed. 17075 146300 8,6

* = The Russian Parts of the Barents Region, ♦= incl. in the Baltic Area

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 5/50

5

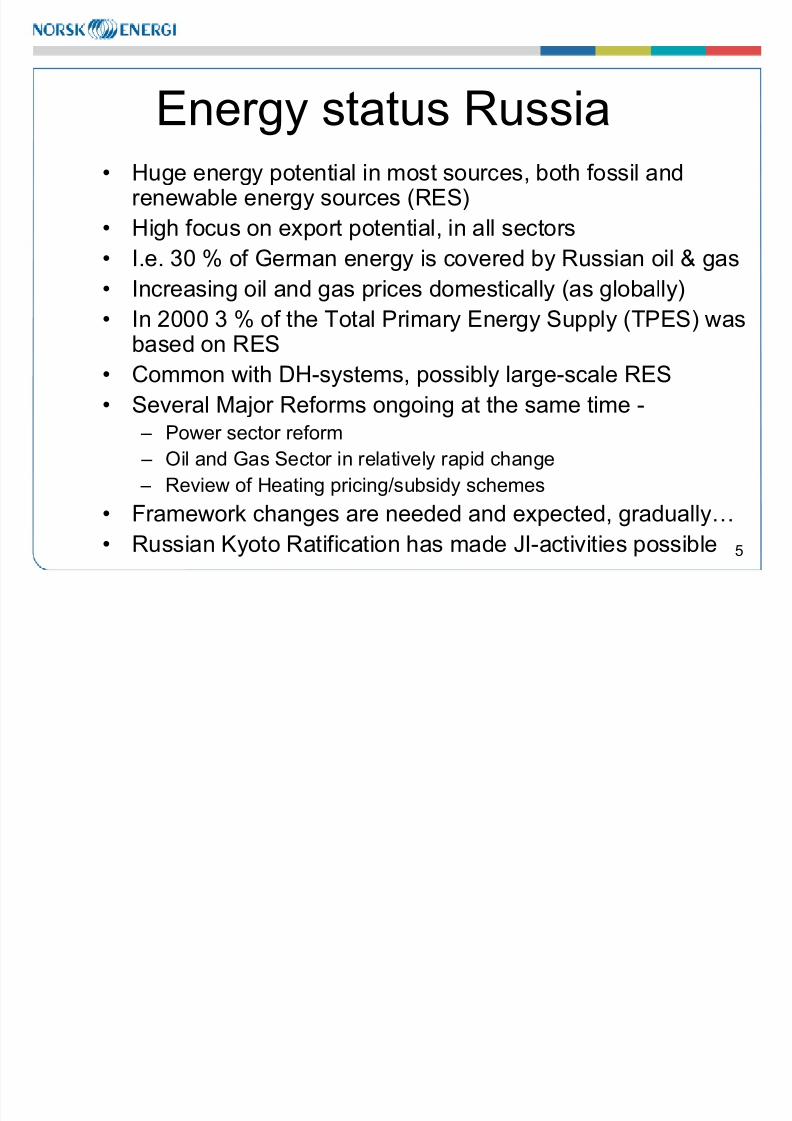

Energy status Russia• Huge energy potential in most sources, both fossil and

renewable energy sources (RES)• High focus on export potential, in all sectors

• I.e. 30 % of German energy is covered by Russian oil & gas

• Increasing oil and gas prices domestically (as globally)

• In 2000 3 % of the Total Primary Energy Supply (TPES) wasbased on RES

• Common with DH-systems, possibly large-scale RES

• Several Major Reforms ongoing at the same time - – Power sector reform

– Oil and Gas Sector in relatively rapid change

– Review of Heating pricing/subsidy schemes

• Framework changes are needed and expected, gradually…• Russian Kyoto Ratification has made JI-activities possible

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 6/50

6

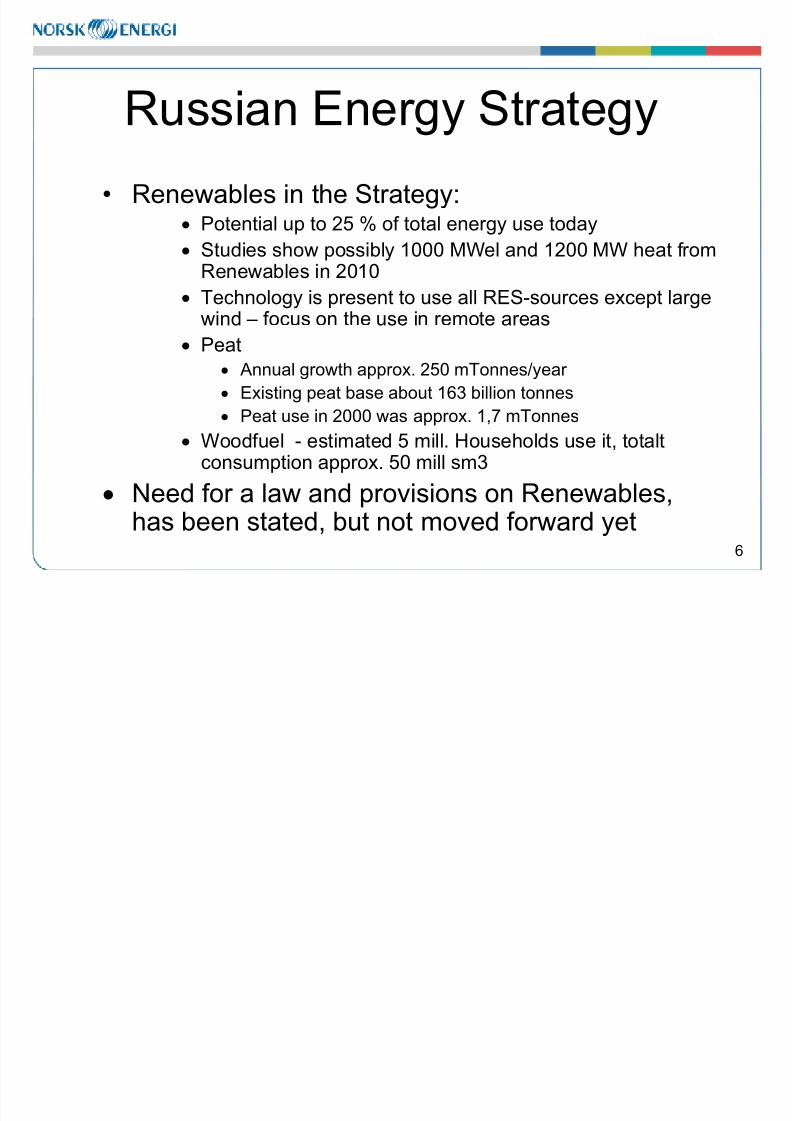

Russian Energy Strategy

• Renewables in the Strategy:• Potential up to 25 % of total energy use today

• Studies show possibly 1000 MWel and 1200 MW heat fromRenewables in 2010

• Technology is present to use all RES-sources except largewind – focus on the use in remote areas

• Peat• Annual growth approx. 250 mTonnes/year

• Existing peat base about 163 billion tonnes

• Peat use in 2000 was approx. 1,7 mTonnes• Woodfuel - estimated 5 mill. Households use it, totalt

consumption approx. 50 mill sm3

• Need for a law and provisions on Renewables,

has been stated, but not moved forward yet

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 7/50

7

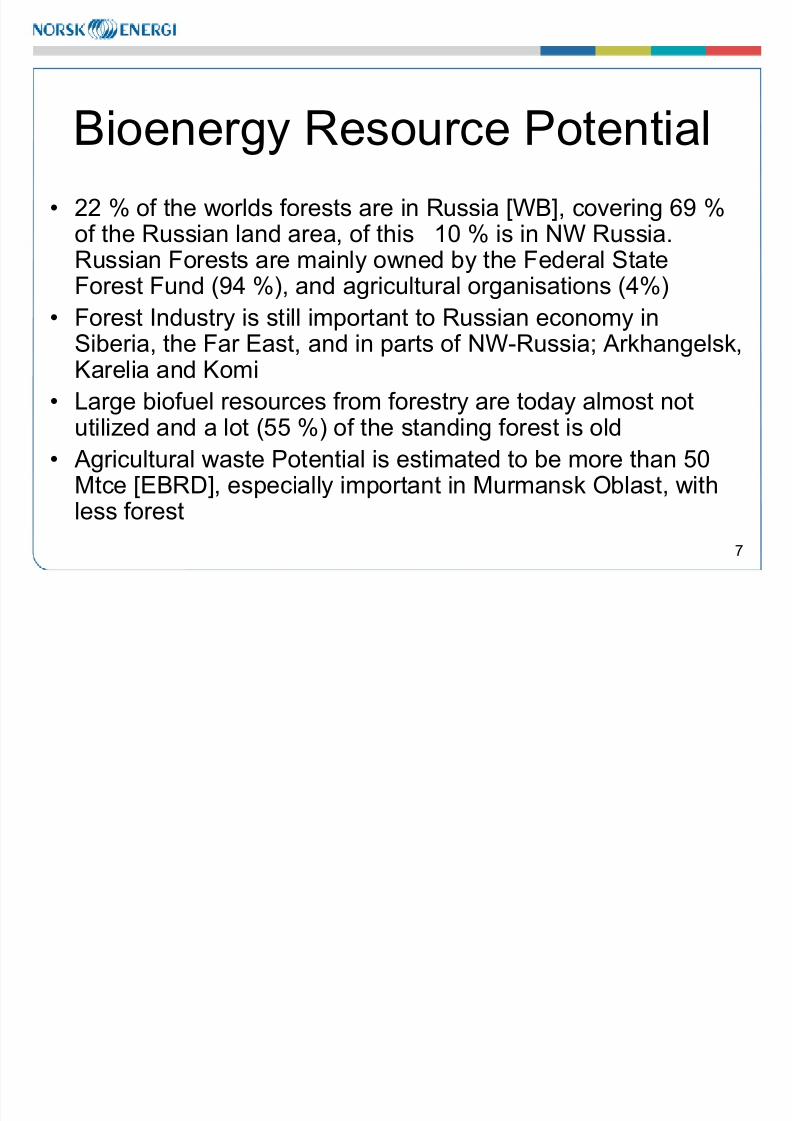

Bioenergy Resource Potential

• 22 % of the worlds forests are in Russia [WB], covering 69 %of the Russian land area, of this 10 % is in NW Russia.Russian Forests are mainly owned by the Federal StateForest Fund (94 %), and agricultural organisations (4%)

• Forest Industry is still important to Russian economy inSiberia, the Far East, and in parts of NW-Russia; Arkhangelsk,Karelia and Komi

• Large biofuel resources from forestry are today almost notutilized and a lot (55 %) of the standing forest is old

• Agricultural waste Potential is estimated to be more than 50Mtce [EBRD], especially important in Murmansk Oblast, with

less forest

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 8/50

8

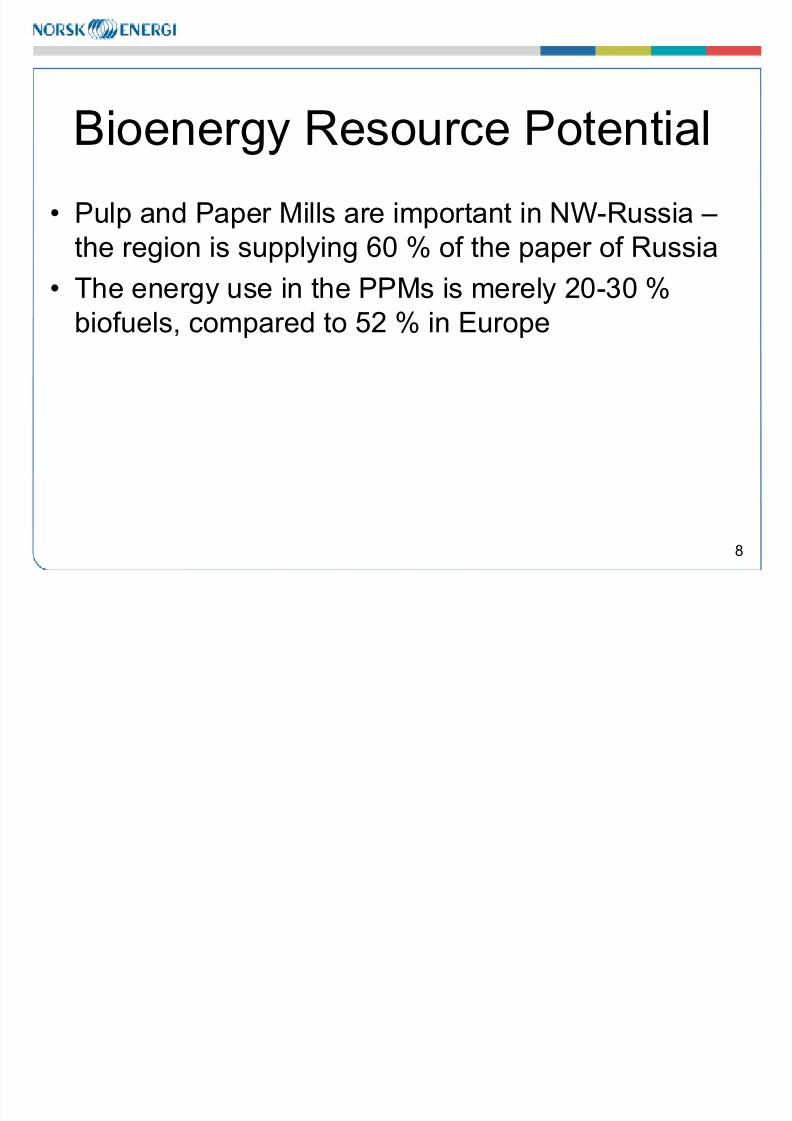

Bioenergy Resource Potential

• Pulp and Paper Mills are important in NW-Russia –the region is supplying 60 % of the paper of Russia

• The energy use in the PPMs is merely 20-30 %

biofuels, compared to 52 % in Europe

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 9/50

9

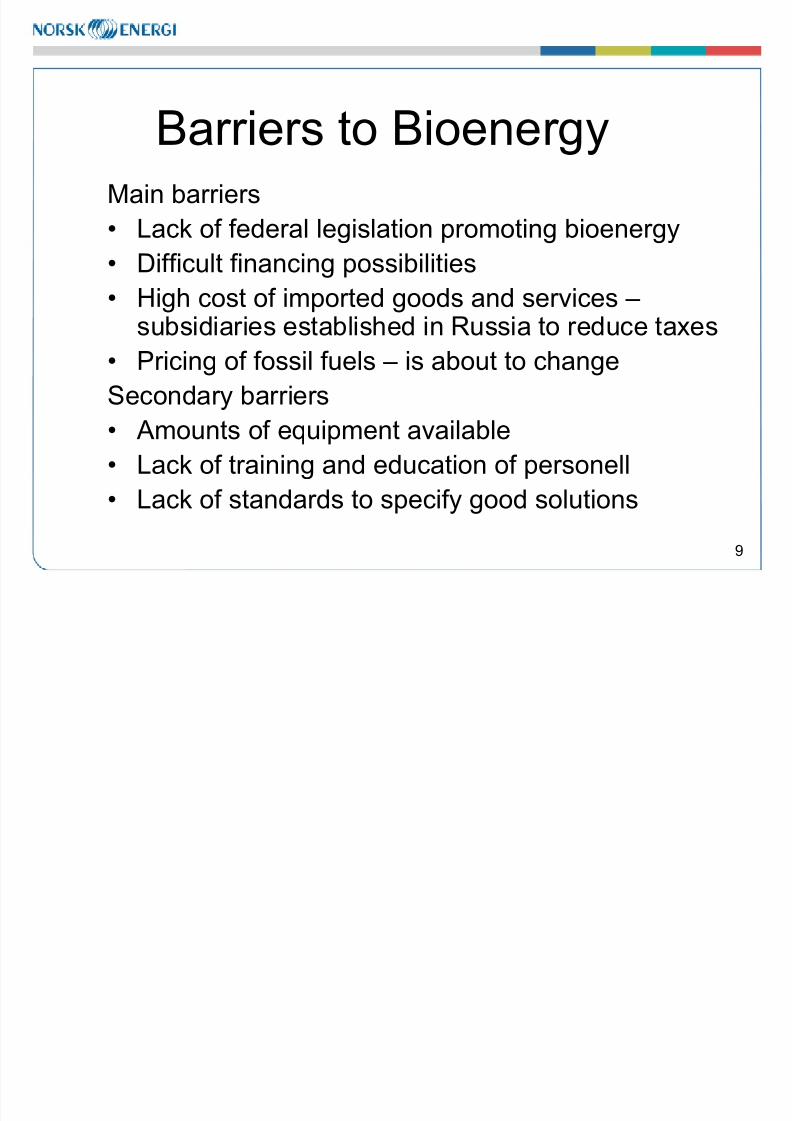

Barriers to BioenergyMain barriers

• Lack of federal legislation promoting bioenergy

• Difficult financing possibilities

• High cost of imported goods and services –subsidiaries established in Russia to reduce taxes

• Pricing of fossil fuels – is about to change

Secondary barriers

• Amounts of equipment available

• Lack of training and education of personell

• Lack of standards to specify good solutions

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 10/50

10

Bioenergy Project types

• Fuel swithcing projects, coal/mazut tobioenergy, connected to district heating

• Process improvements in sawmills• Off-grid society conversion projects

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 11/50

11

Arkhangelsk Oblast,Bioenergy Resources and Market

• Large forest resources,• High degree of fossil fuel import to the region

• Traditionally producing timber, wood processing, and

pulp and paper mill industry• More than1600 small med.size old boilers

• 200 wood cutting companies, supplying sawmills

• 25 % of wood fuel is used for heating, the rest is dumpedat landfills etc – increased local use.

• Potential to increase bioenergy by 30 % or more

• Large port/harbour, kept open with ice-breakers• No production of pellets so far

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 12/50

12

Possible northern shipping route

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 13/50

13

Murmansk Oblast, Resources andMarket

• Little Forest resources close to population• Much fossil fuel (gas/oil) import to the region

• Population decline since late 80s, slow economy

• No local biofuel market at present, partlybecause of transport and climate barriers

• Very low coal prices, even competitive at η=20%• Focus on waste utilization in DH-systems

• Large Wind Resources

• Open port/harbour in Murmansk

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 14/50

14

Republic of Karelia, Resources andMarket

• Significant biofuel potential, several x present use

• Emerging local biofuel market• Some wood fuel and peat export to Finland

• Defined ambition in 1998 by the Karelian

Government to increase use of wood chips, wastewood and mixed wood

• Local Government supports Biofuel, but notwithout some bureaucracy

• The Energy Policy ambition is to increase use of RES to 40-50 % in 2015

• Limited access to shipping routes in winter

• Some production of pellets for export

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 15/50

15

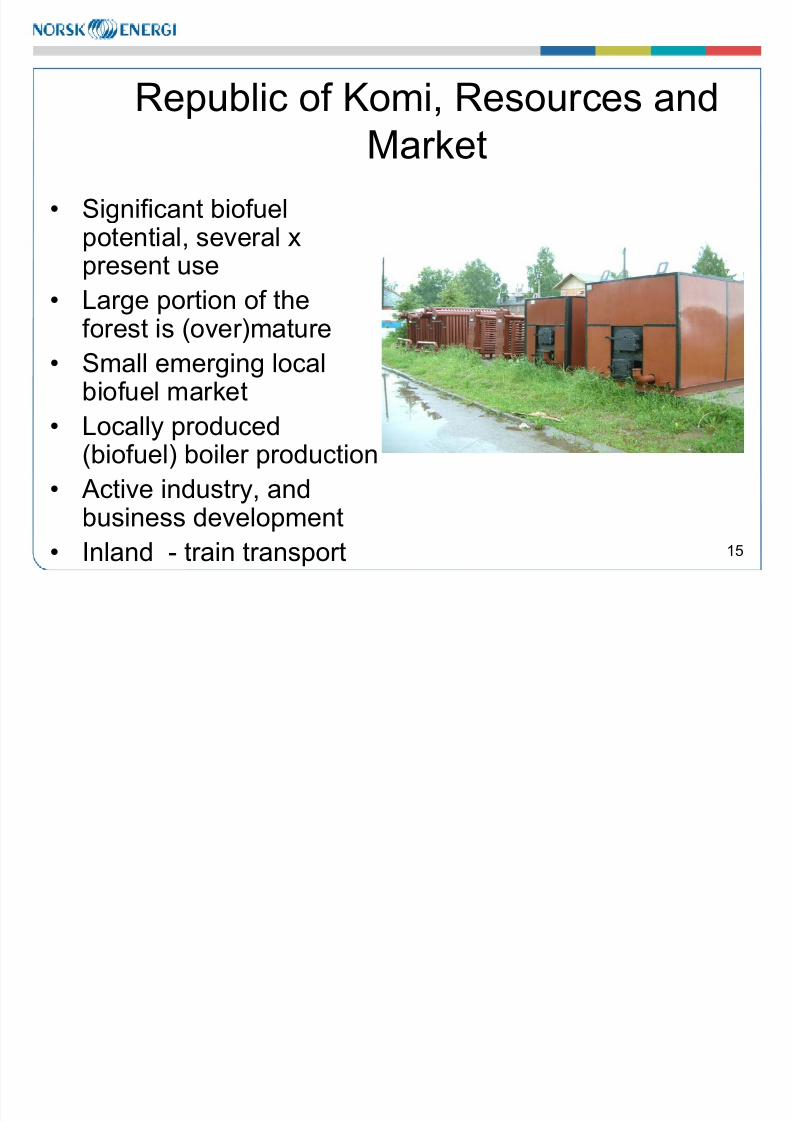

Republic of Komi, Resources andMarket

• Significant biofuelpotential, several xpresent use

• Large portion of theforest is (over)mature

• Small emerging localbiofuel market

• Locally produced(biofuel) boiler production

• Active industry, and

business development• Inland - train transport

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 16/50

16

Domestic use or Export ?

• In light of global CO2-balance it makes more sense toprocess wood as close as possible to the resource rather than to export wood from Russia. Thus, transport costs

and energy consumed to transport the wood areminimized.

• The place where carbon dioxide is emitted – the

processing plant – then remains as near as possible tothe place where these emissions can be absorbed – in

the forest.

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 17/50

17

Domestic use or Export ?

• Domestic use of bioenergy means job creation in Russia• Russia has a rather high scientific and engineering

potential which could secure further development of the

use of bioenergy• The present political and economic stability in Russiaproduces the favourable conditions for investments aswell as for import of up-to-date technologies. Taking into

account that the level of remuneration of labour willremain significantly lower in Russia than in WestEuropean countries, it would be quite promising to exportthe products of extended wood processing from Russia.

• It also favors export of climatic values through JI.

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 18/50

18

Domestic use or Export ?

• Thus, in the context of Kyoto Protocol implementation, itis advisable not only to increase felling volume* inRussia but also to achieve better wood processing near

the resource.• In so doing, this would increase wood residue output at

the woodworking and pulp and paper mills.

• *In the context of sustainable forest management,industrial wood and pulpwood logging must beaccompanied by logging waste utilization.

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 19/50

19

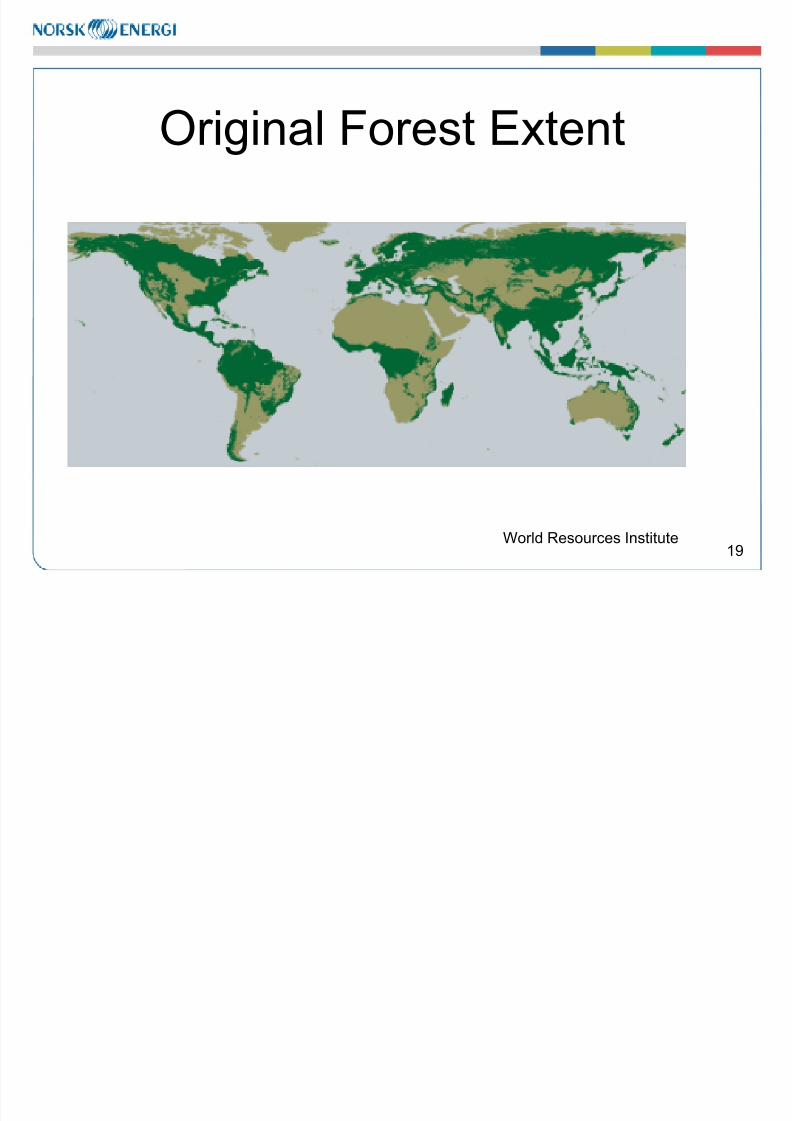

Original Forest Extent

World Resources Institute

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 20/50

20

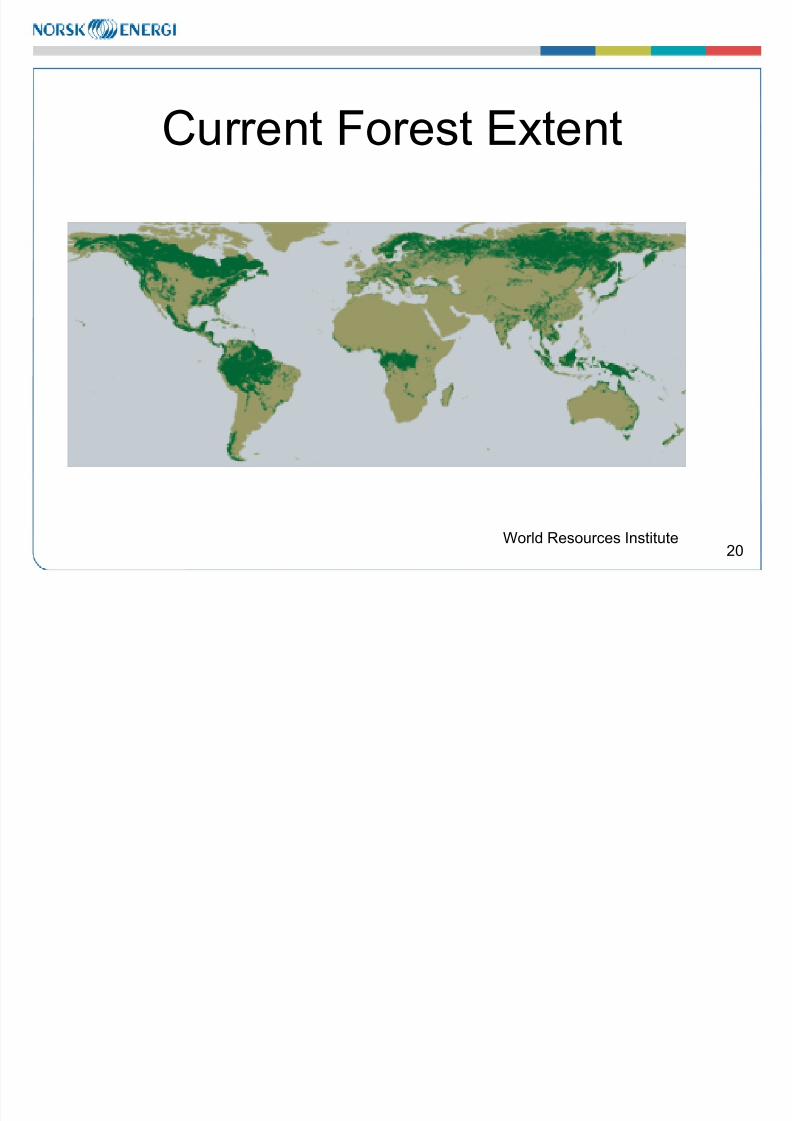

Current Forest Extent

World Resources Institute

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 21/50

21

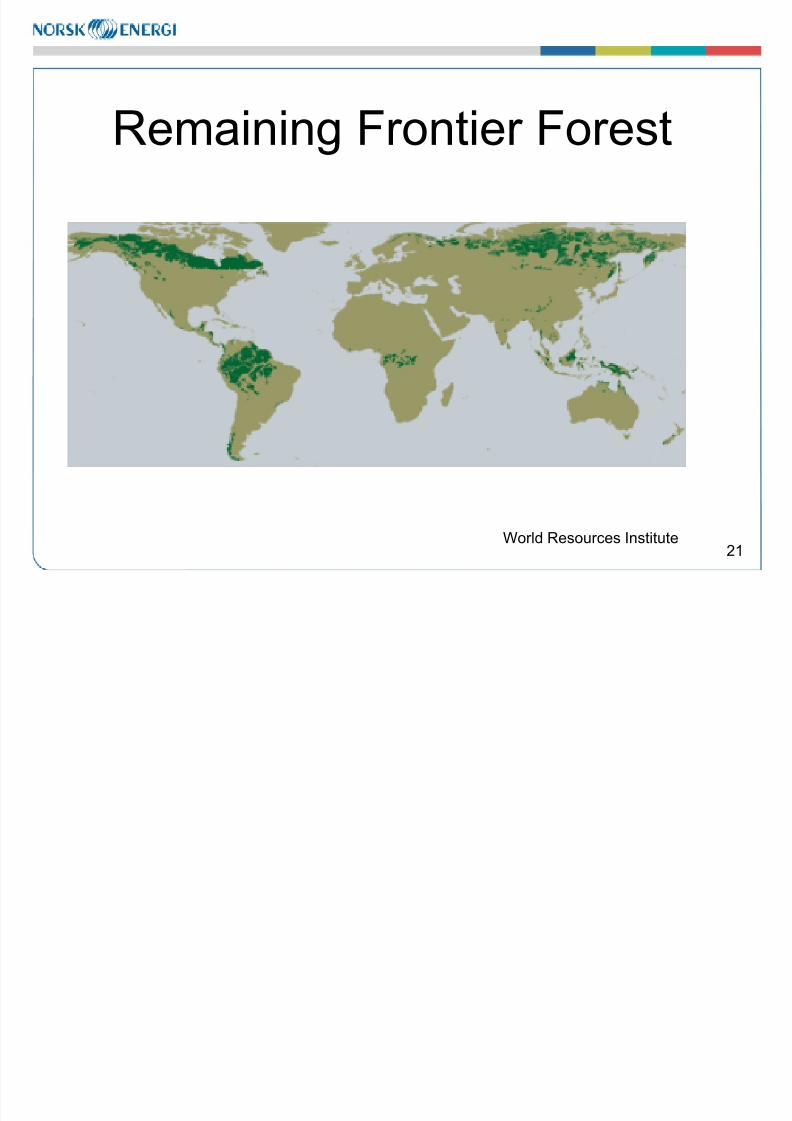

Remaining Frontier Forest

World Resources Institute

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 22/50

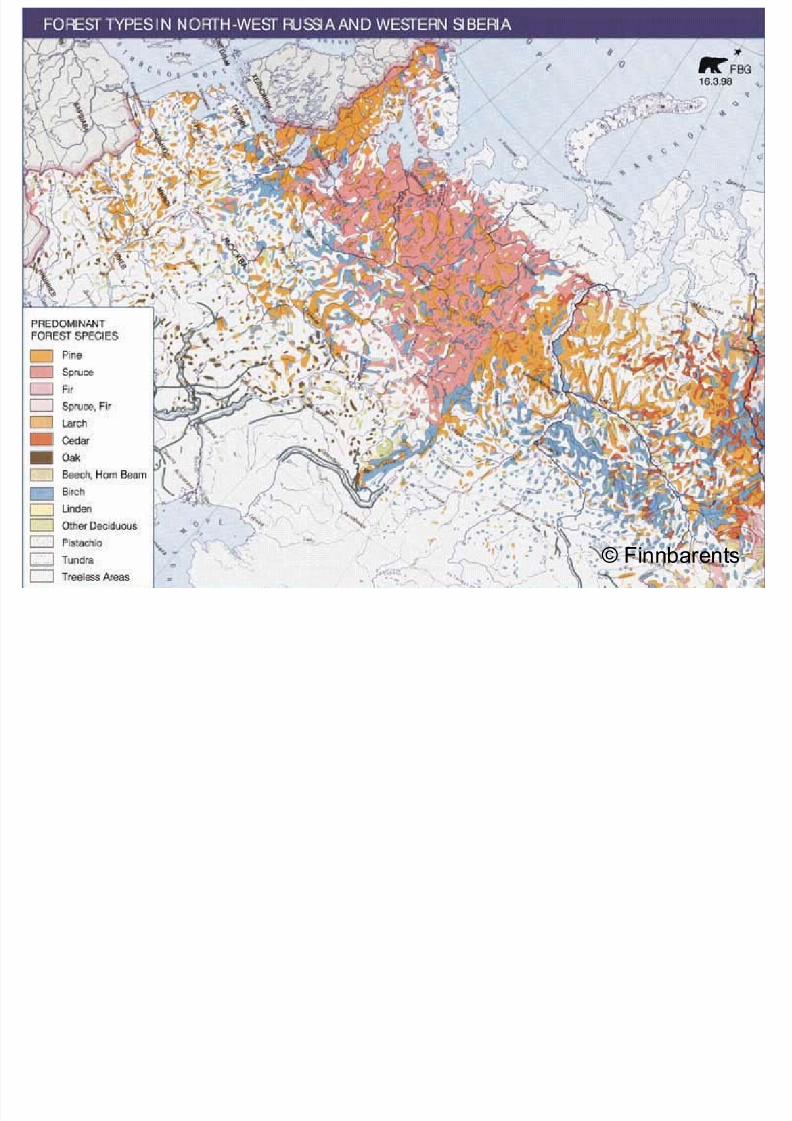

© Finnbarents

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 23/50

23

Russian National Parks and Protected areas

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 24/50

24

Changes in domestic Energy Prices

• The current gas prices on the Russian domestic markethave been known to differ from those on world marketsand from export prices for Russian gas by approximately

a factor of ten, this is now changing drastically• The increase in domestic prices for gas will result in

considerable changes in biofuel competitiveness and just

in a short time wood will become a competitive type of fuel in the North-Western Region of Russia.

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 25/50

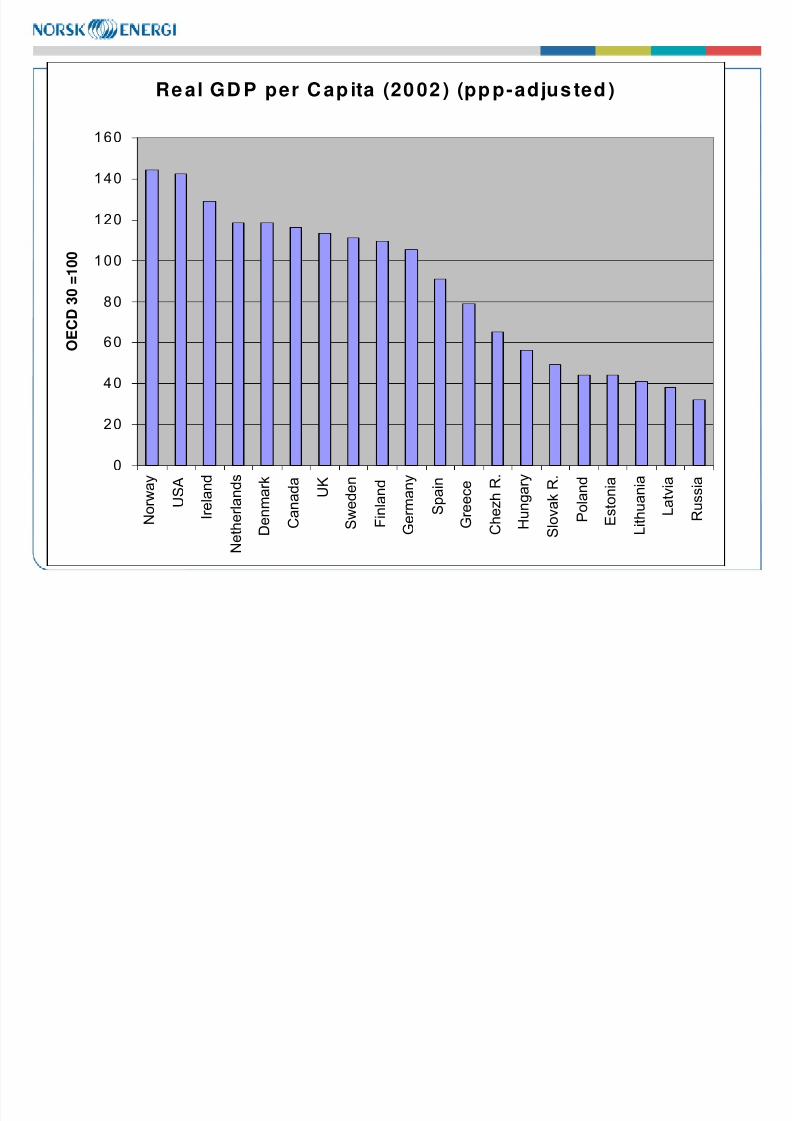

Re al GD P per C ap ita (20 02 ) (pp p-adjus ted )

0

20

40

60

80

100

120

140

160

N

o r w a y

U S A

I r e l a n d

N e t h e r l a n d s

D e

n m a r k

C

a n a d a

U K

S

w e d e n

F

i n l a n d

G e

r m a n y

S p a i n

G

r e e c e

C h

e z h R .

H

u n g a r y

S l o

v a k R .

P o l a n d

E

s t o n i a

L i t

h u a n i a

L a t v i a

R u s s i a

O E C D

3 0 = 1 0 0

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 26/50

26

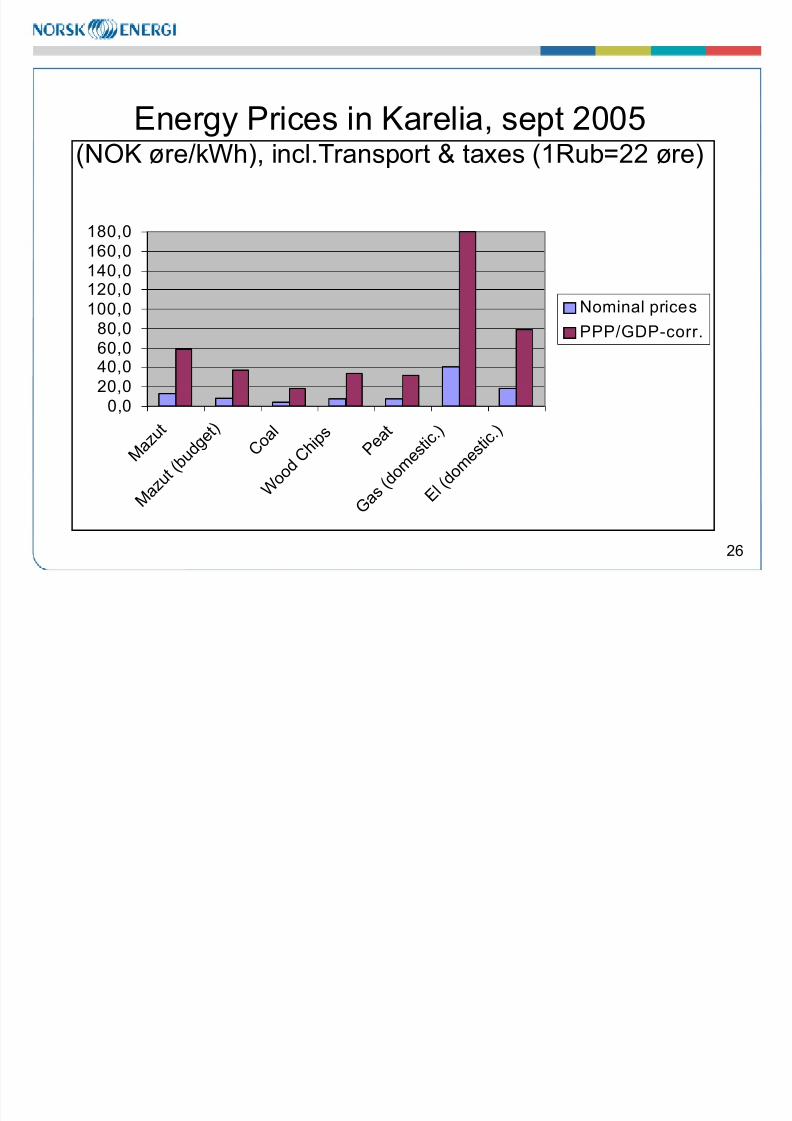

0,020,040,060,080,0100,0

120,0140,0160,0180,0

M a z u t

M a z u t ( b u

d g e t )

C o a l

W o o

d C h i p

s P e

a t

G a s ( d o m e

s t i c . )

E l ( d o

m e s t i c . )

Nominal prices

PPP/GDP-corr.

Energy Prices in Karelia, sept 2005(NOK øre/kWh), incl.Transport & taxes (1Rub=22 øre)

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 27/50

27

Russian business status

• A lot of the wood processing industry and thelarge PPMs are highly developed, commercialand competitive companies

• As domestic energy prices have increased, theuse of own biofuel is increasing,

• These companies are not desperate to sell

resources for export at low costs,• Some cases of export of high grade expensive

fibreboard woodchips have set high price

standards

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 28/50

28

Domestic use or Export ?

A number of Russian pulp and paper mills haveincreased the share of wood waste in their energy balance.

Arkhangelsk Pulp and Paper Mill in 2001 madea fundamental reconstruction of its bark boiler

of a capacity of 150 tonnes of steam per hour In August 2005 was completed a secondbiofuel boiler, total consumption 500 t.tons/year

of bark and wood waste

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 29/50

29

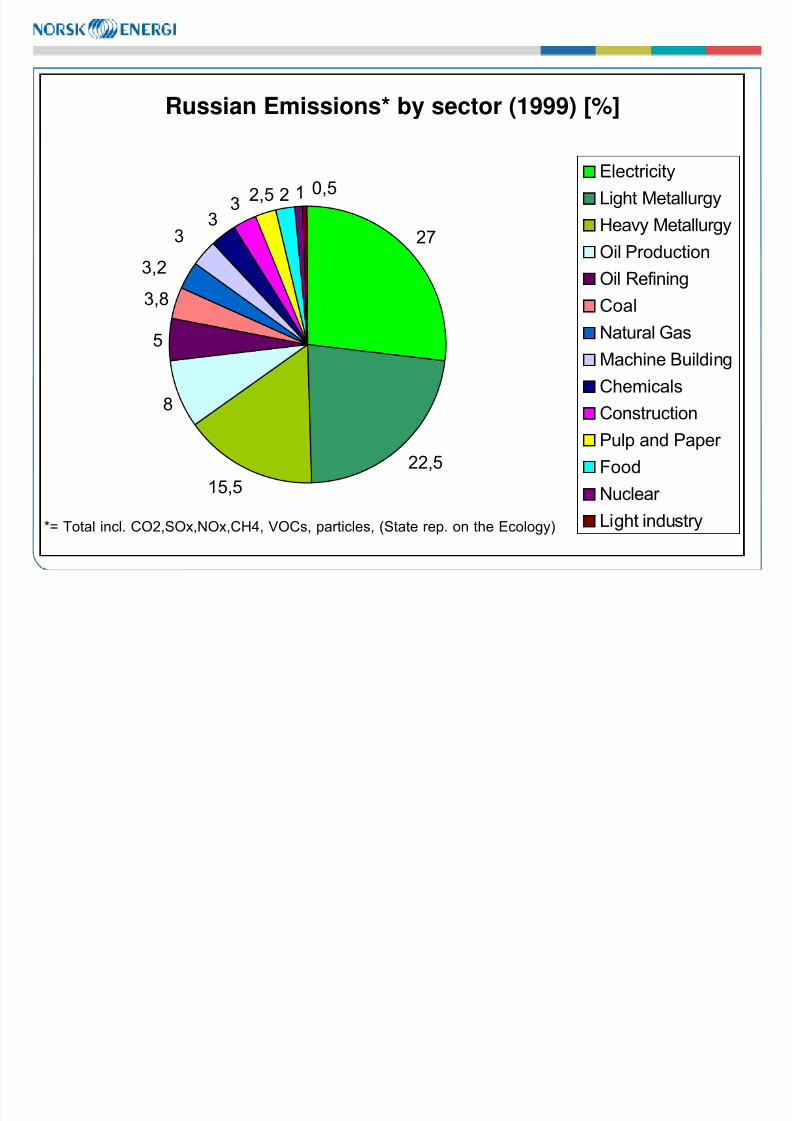

Russian Emissions* by sector (1999) [%]

22,5

15,5

8

5

3,8

3,2

33

32 12,5 0,5

27

Electricity

Light Metallurgy

Heavy Metallurgy

Oil Production

Oil Refining

Coal

Natural Gas

Machine Building

Chemicals

ConstructionPulp and Paper

Food

Nuclear

Light industry*= Total incl. CO2,SOx,NOx,CH4, VOCs, particles, (State rep. on the Ecology)

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 30/50

30

Heating Sector -characteristics

• DH-systems exist in most urban areas

• More than 250.000 km heating pipes in Russia

• Prices do not cover Costs – estimated 60 % of pipes need maintenance

• Poor or no metering• Poor insulation – high energy losses

• Often uneven heat distribution

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 31/50

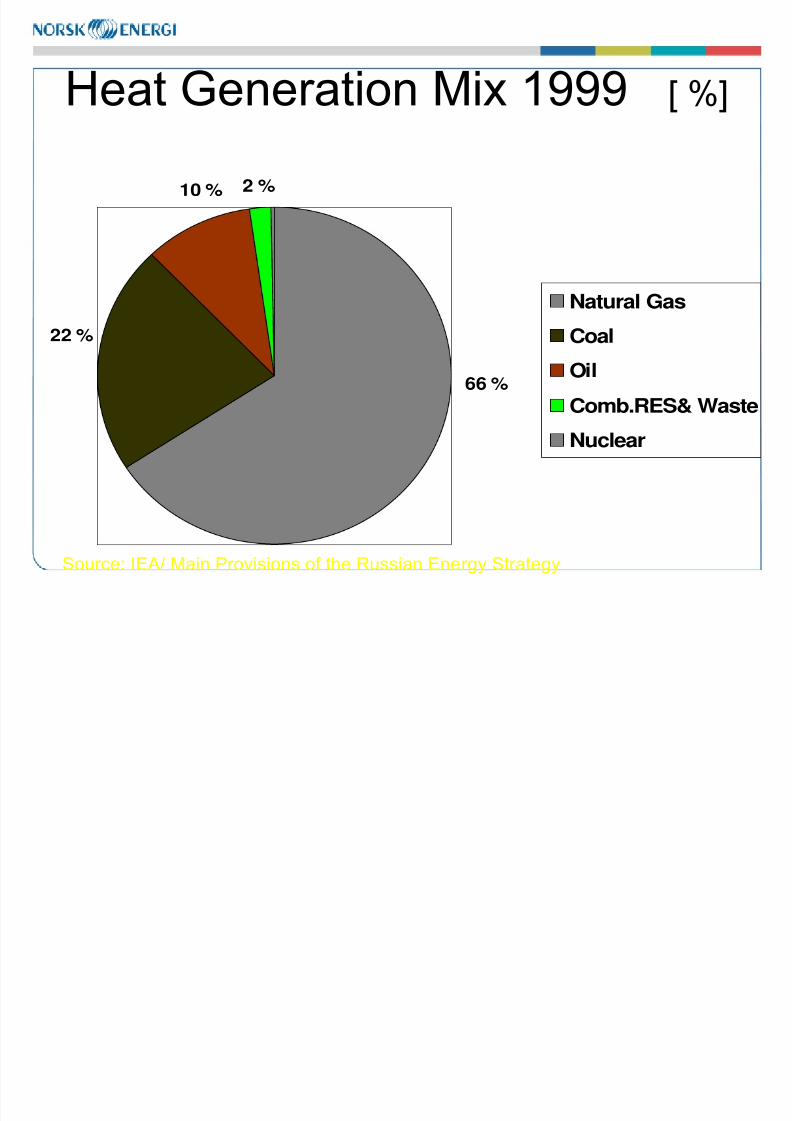

Heat Generation Mix 1999 [ %]

66 %

2 %10 %

22 %

Natural Gas

Coal

Oil

Comb.RES& Waste

Nuclear

Source: IEA/ Main Provisions of the Russian Energy Strategy

Russian Electric Power Generation Mix

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 32/50

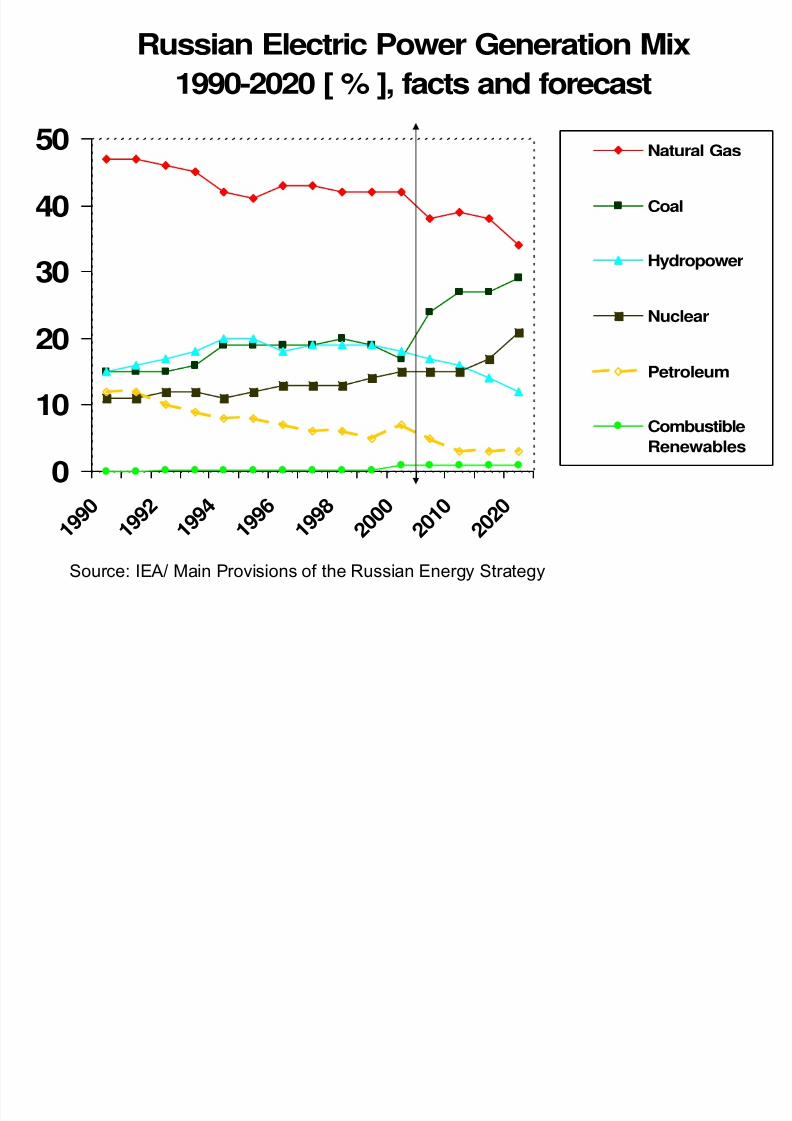

Russian Electric Power Generation Mix

1990-2020 [ % ], facts and forecast

0

10

20

30

40

50

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 1 0

2 0 2 0

Natural Gas

Coal

Hydropower

Nuclear

Petroleum

CombustibleRenewables

Source: IEA/ Main Provisions of the Russian Energy Strategy

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 33/50

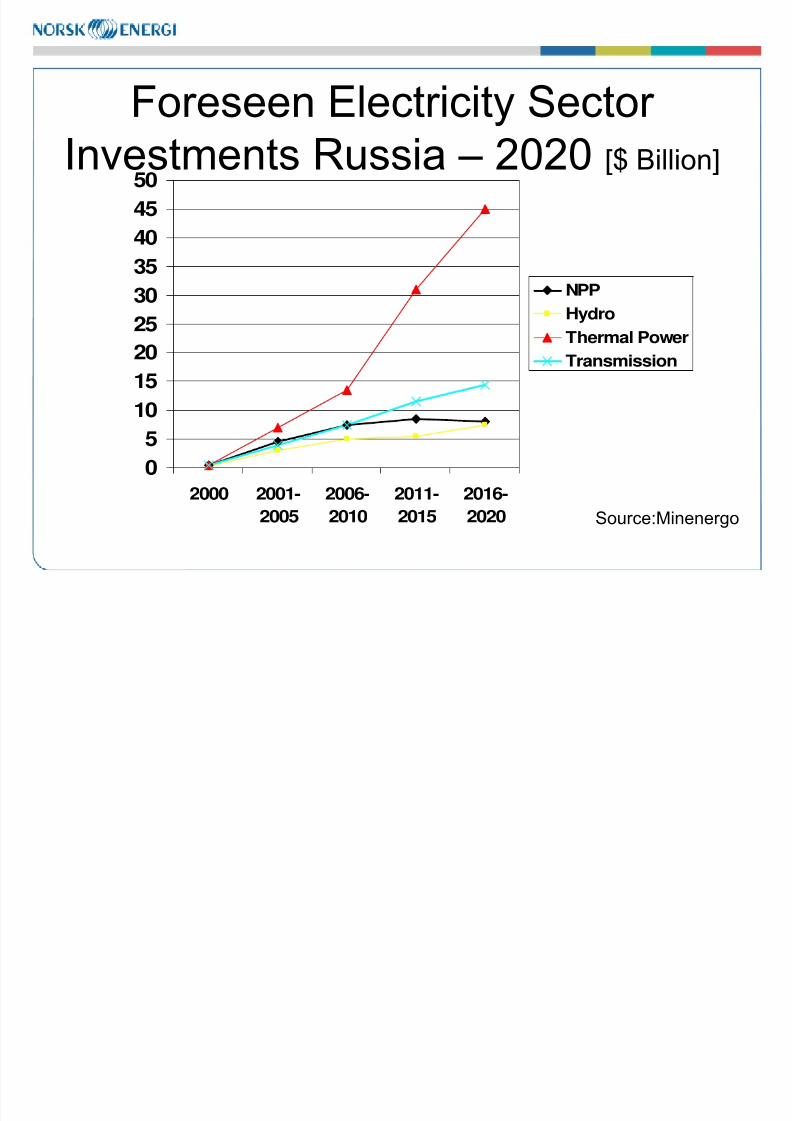

Foreseen Electricity Sector Investments Russia – 2020 [$ Billion]

0

5

10

15

20

25

30

35

4045

50

2000 2001-

2005

2006-

2010

2011-

2015

2016-

2020

NPP

HydroThermal Power

Transmission

Source:Minenergo

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 34/50

34

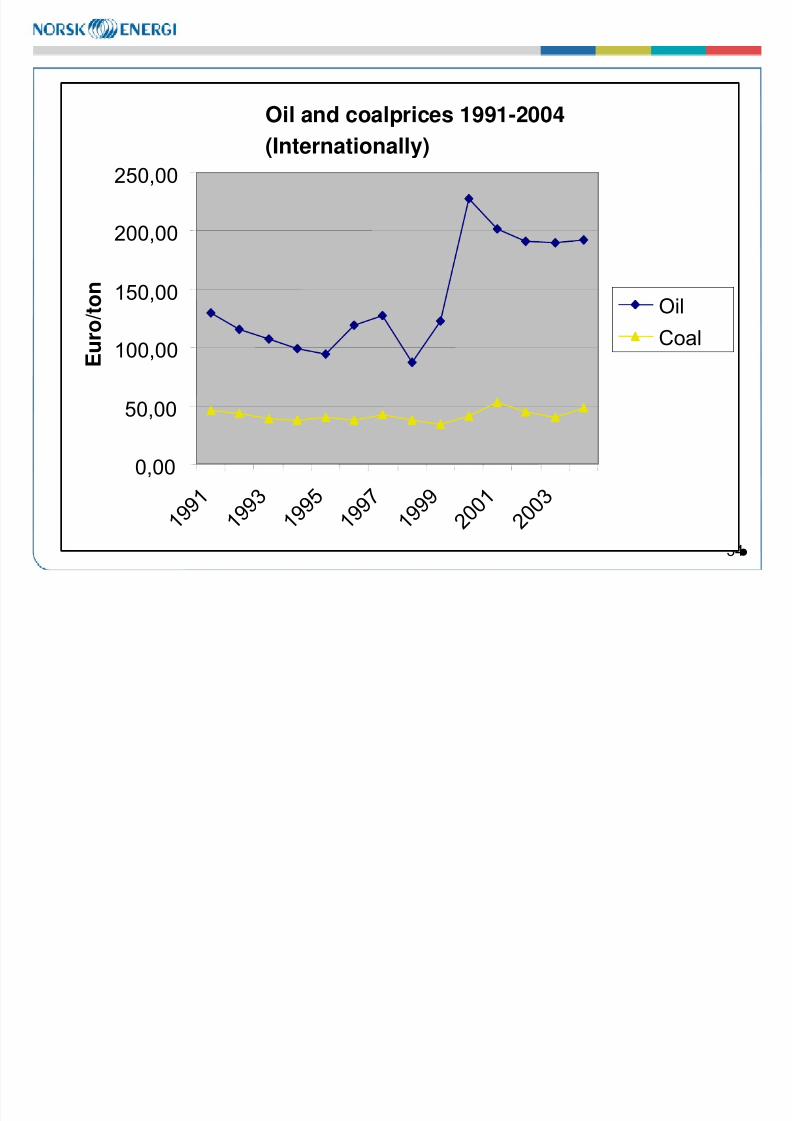

Oil and coalprices 1991-2004(Internationally)

0,00

50,00

100,00

150,00

200,00

250,00

1 9 9

1

1 9 9

3

1 9 9 5

1 9 9 7

1 9 9

9

2 0 0

1

2 0 0

3

E u r o / t o n

Oil

Coal

•

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 35/50

35

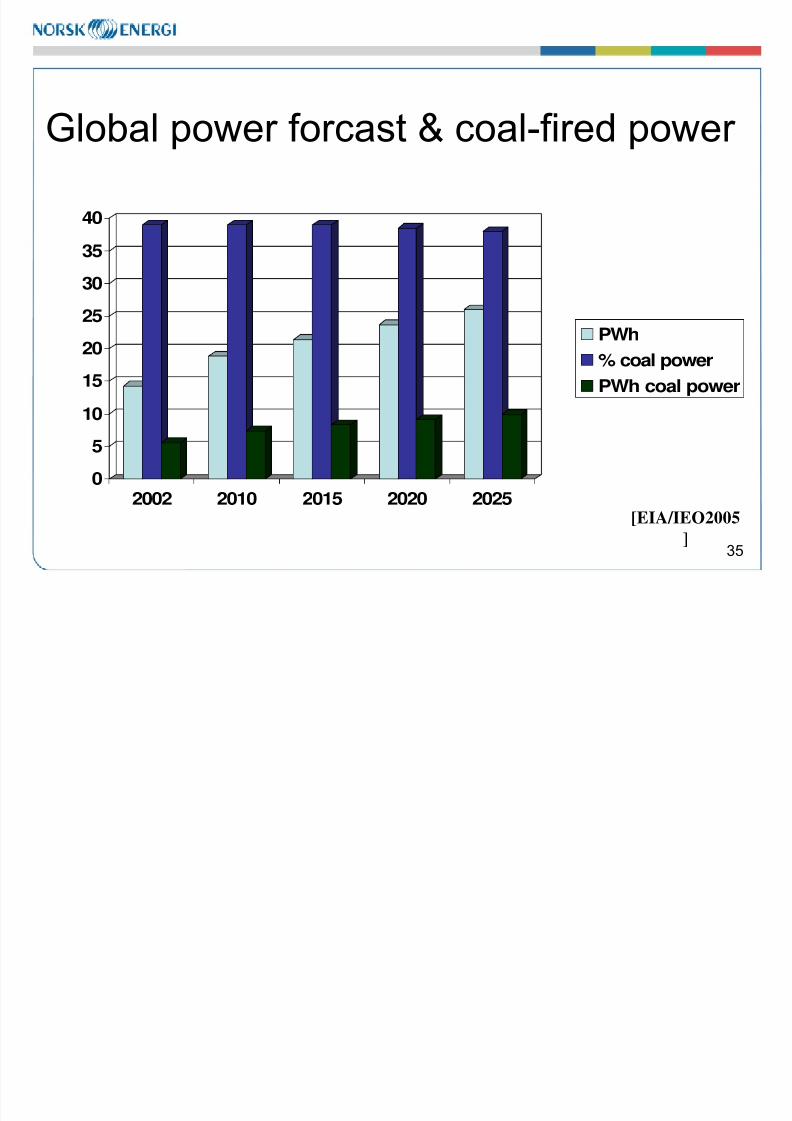

Global power forcast & coal-fired power

0

510

15

20

25

30

35

40

2002 2010 2015 2020 2025

PWh

% coal power

PWh coal power

[EIA/IEO2005]

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 36/50

36

Co-firing

• Coal power will most likely remain globally• The price of CO2 quotas might be as high as it alone

pays for the investment of re-building existing plants

• In countries with high price of coal local biofuel could becheaper than coal and thus outweigh the expense of re-building/conversion to co-firing

• In some countries with favorable support schemes to co-

firing, this is happening large-scale, especially in the• Co-firing is increasing, and often represents a cost-

effective climatic measure

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 37/50

37

Russia Cofiring Potential

•

Large coal reserves• Russian Energy strategy expects increased use

of coal power due to increased oil & gas export

• At present approx. 500 TPP installed (mean)capacity 300 MWel

• Enormous need for upgradings

• Increasing part of privatizing TPPs

• JI-prosjects : cofiring is an eligible type of project

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 38/50

38

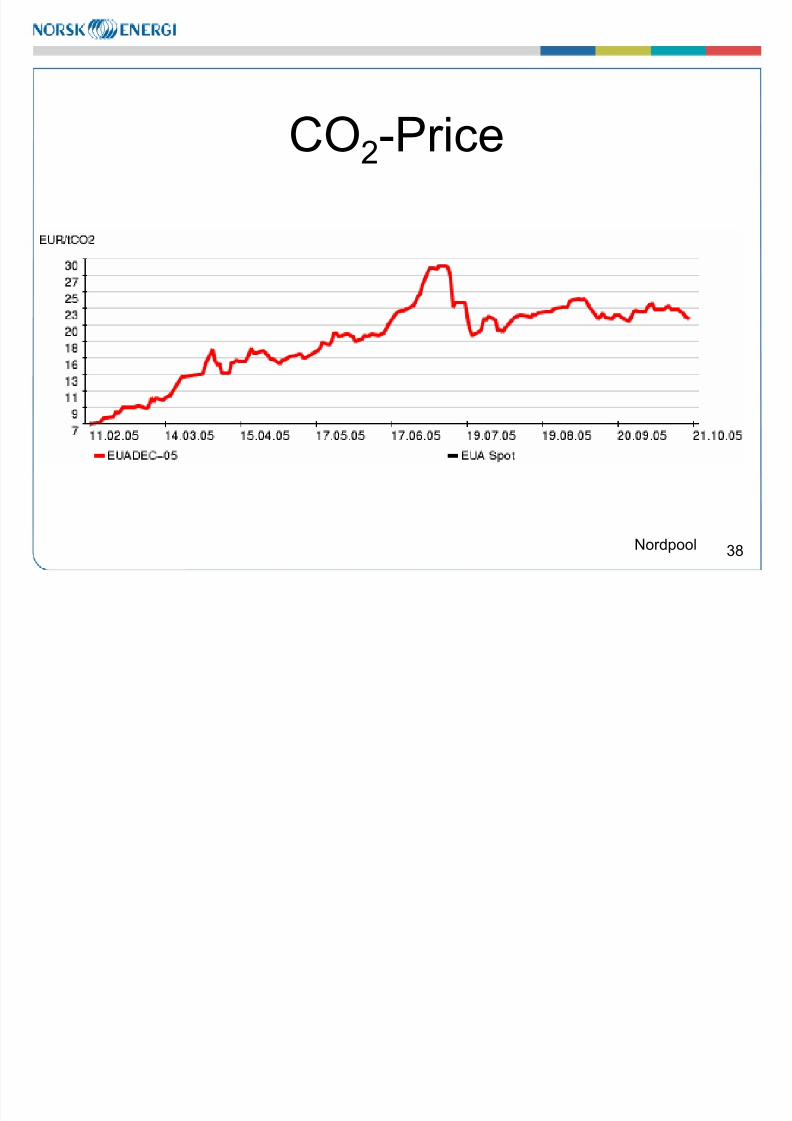

CO2-Price

Nordpool

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 39/50

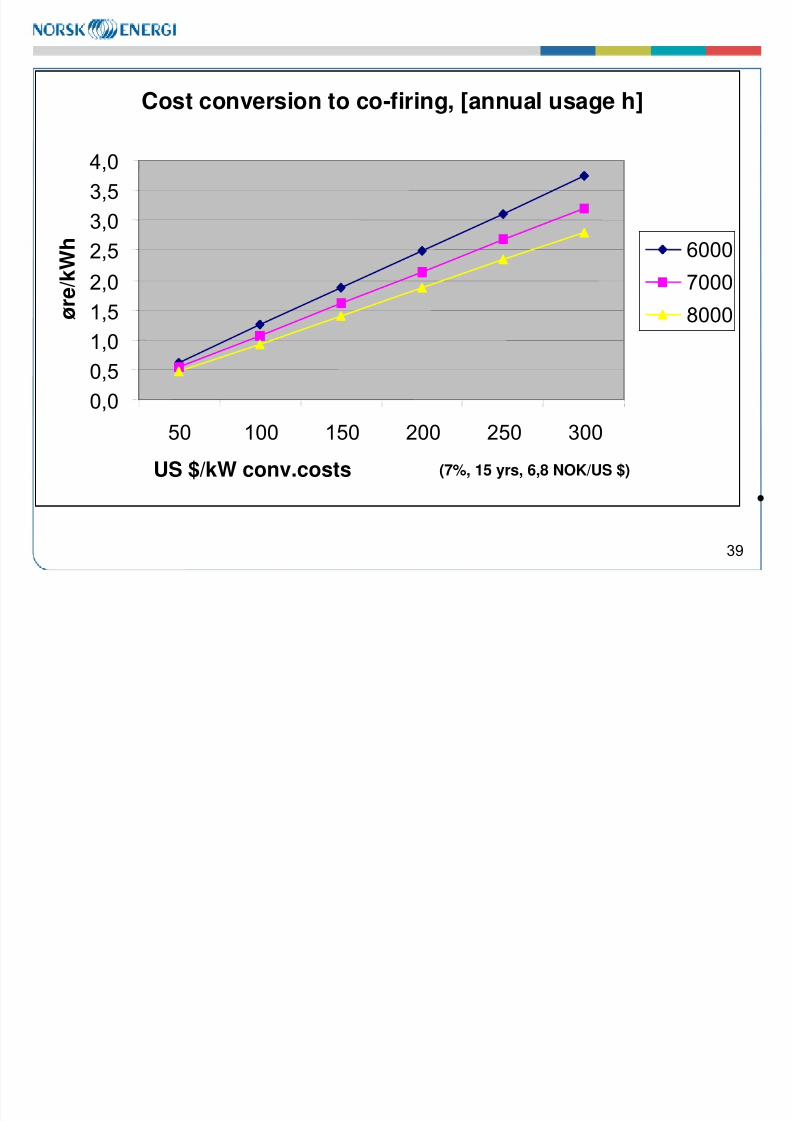

39

Cost conversion to co-firing, [annual usage h]

0,0

0,5

1,01,5

2,0

2,53,0

3,5

4,0

50 100 150 200 250 300

US $/kW conv.costs (7%, 15 yrs, 6,8 NOK/US $)

ø r e / k W h 6000

7000

8000

•

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 40/50

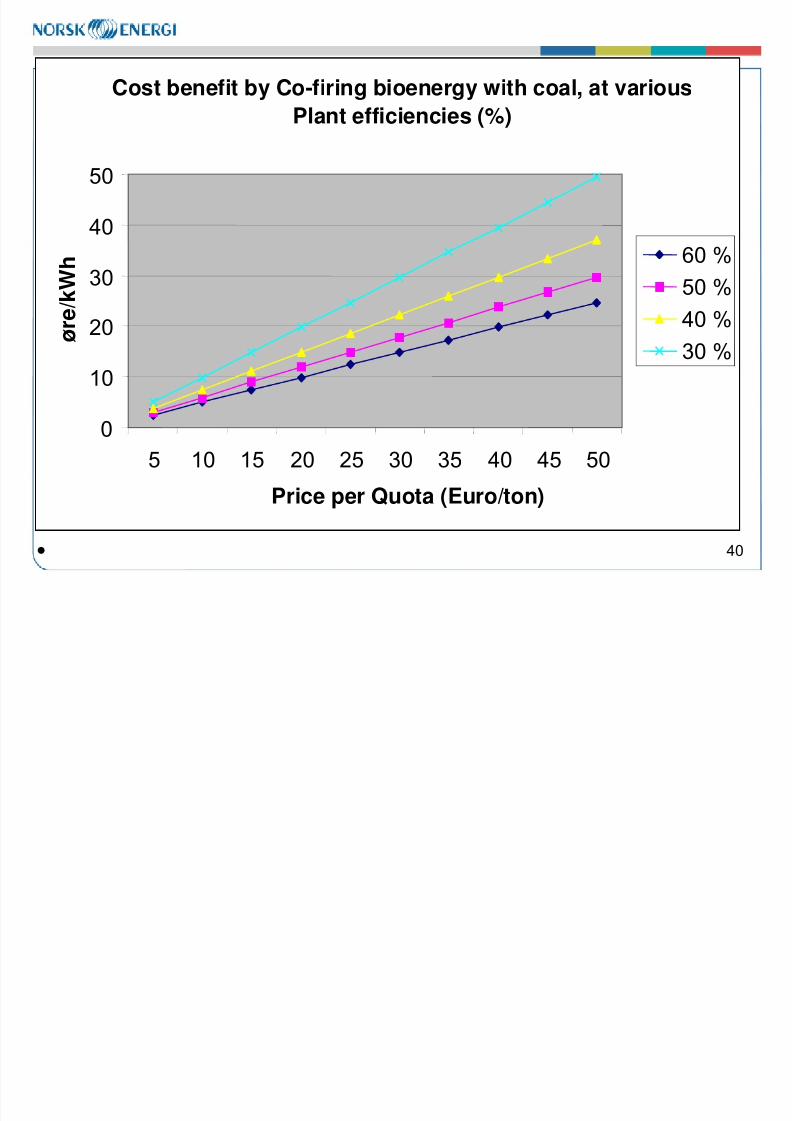

40•

Cost benefit by Co-firing bioenergy with coal, at various

Plant efficiencies (%)

0

10

20

30

40

50

5 10 15 20 25 30 35 40 45 50

Price per Quota (Euro/ton)

ø r e

/ k W h 60 %

50 %

40 %30 %

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 41/50

41

Testing Ground Facility TGF (1)

• Established by BASREC in 2002• Way of testing Joint Implementation (JI)

projects

• TGF invests in projects with cost-effectiveEmission Reduction Units ERUs and

Assigned Amount Units (AAUs)• Geographical focus is Poland, Lithuania,

Latvia, Estonia and Russia

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 42/50

42

Testing Ground Facility TGF (2)

• TGF handled by Nordic EnvironmentFinance Corporation, NEFCO, Helsinki

• Current funding 15 mEuro, possibly 30 mE• ERUs can be used with EU ETS

• Project owners can be private or public• Typical projects are fuel switching,

renewable energy, waste to energy

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 43/50

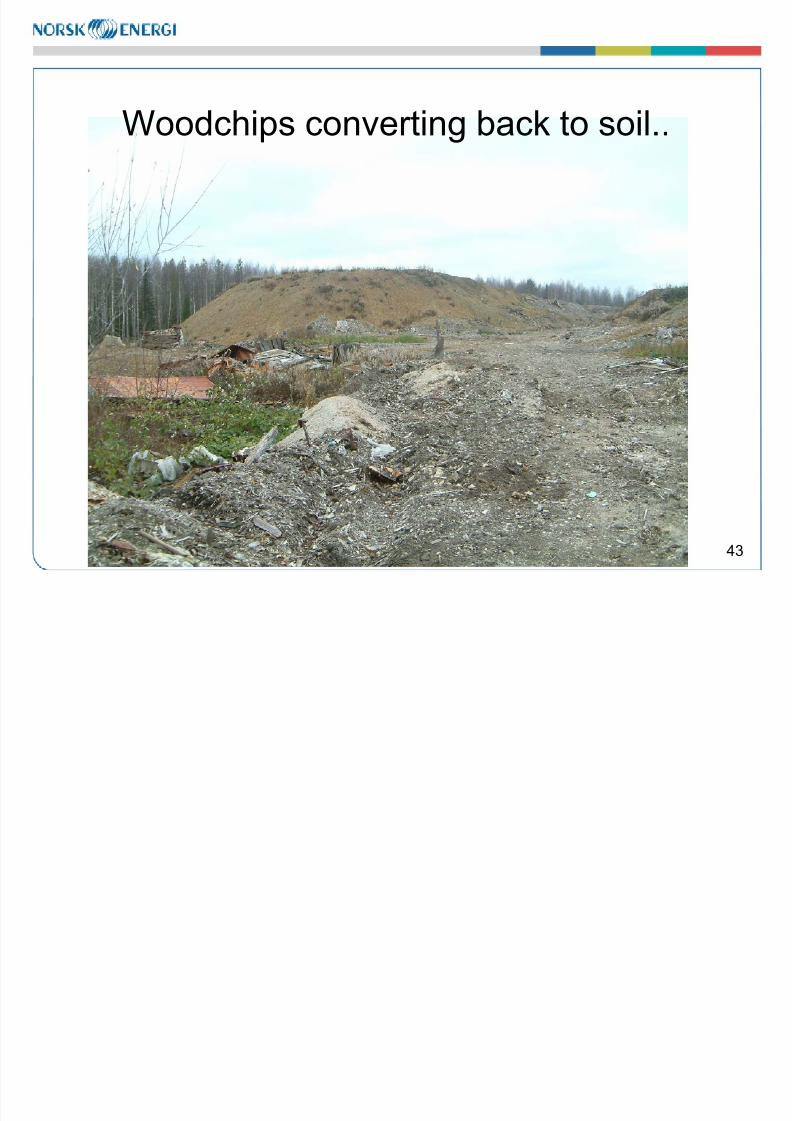

43

Woodchips converting back to soil..

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 44/50

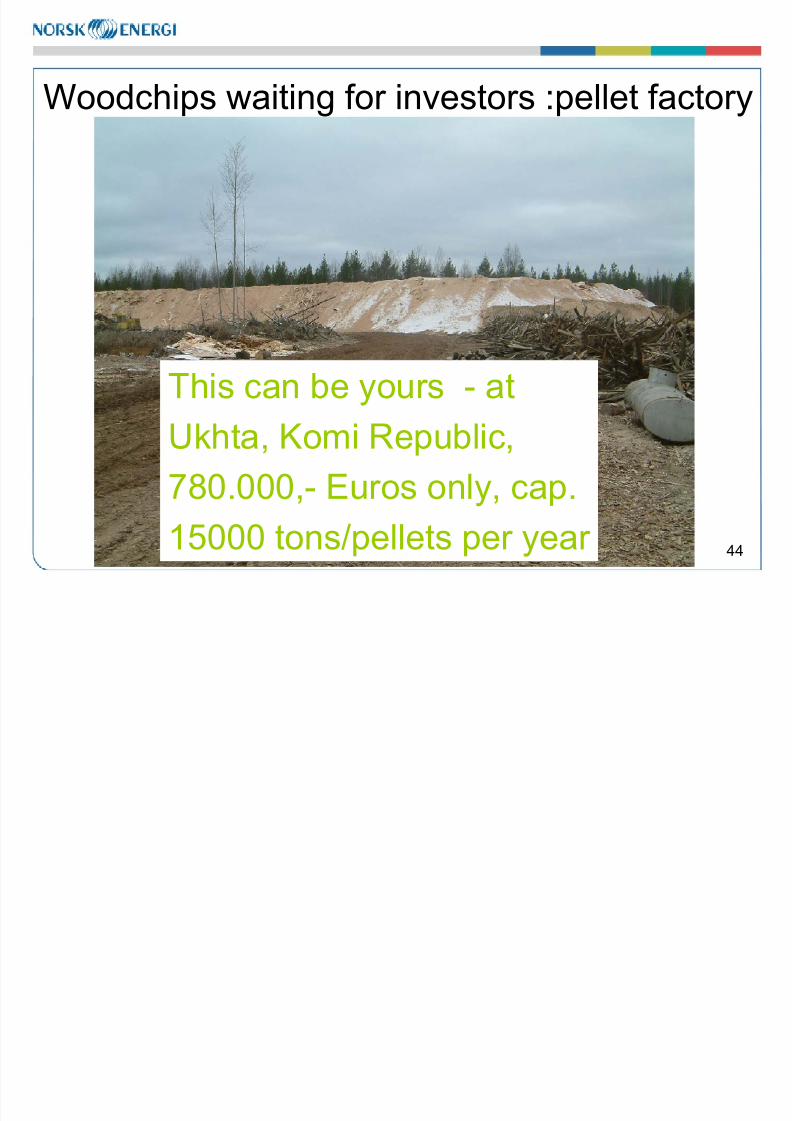

44

Woodchips waiting for investors :pellet factory

This can be yours - at

Ukhta, Komi Republic,

780.000,- Euros only, cap.

15000 tons/pellets per year

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 45/50

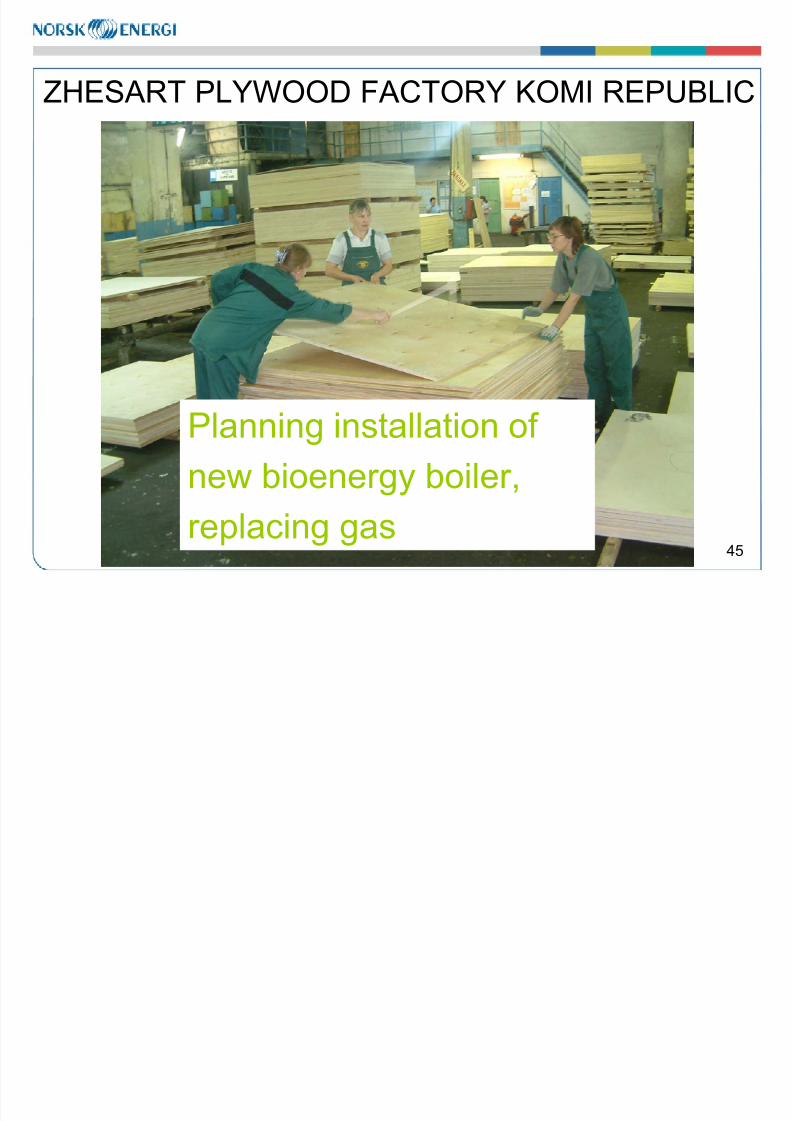

45

ZHESART PLYWOOD FACTORY KOMI REPUBLIC

Planning installation of new bioenergy boiler,

replacing gas

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 46/50

46

Typical VOLVO in KOMI REPUBLIC

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 47/50

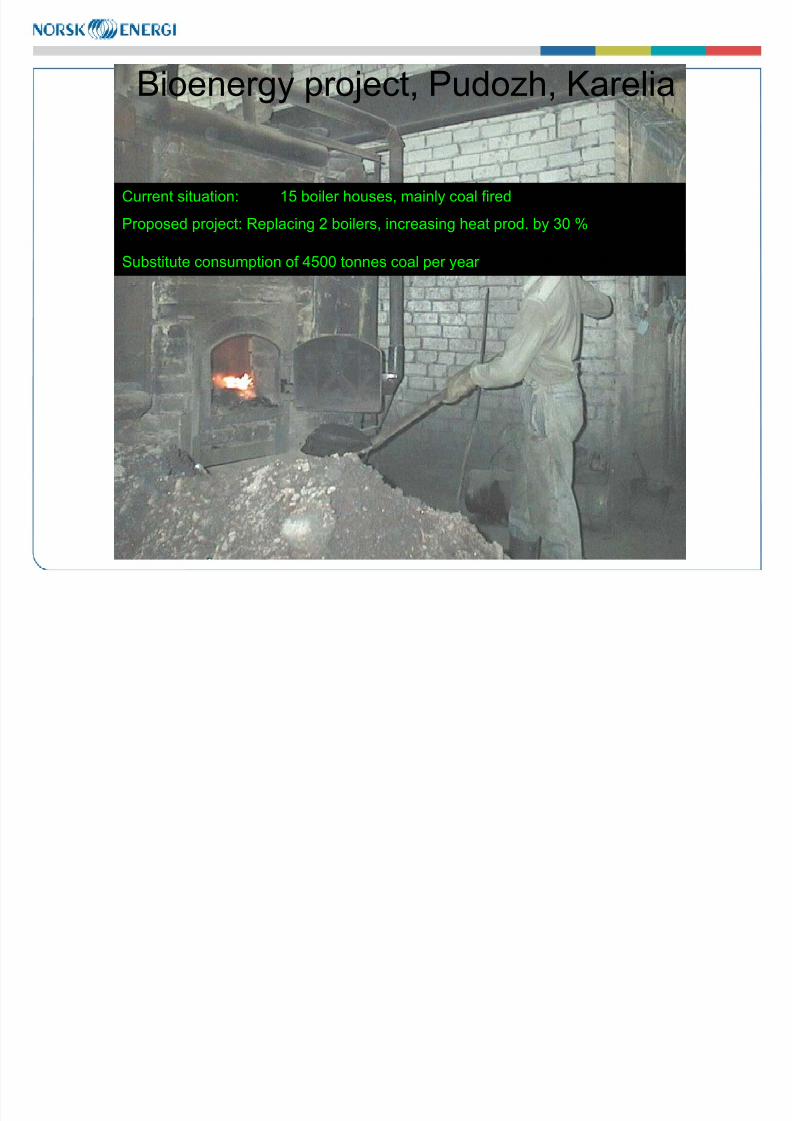

Current situation: 15 boiler houses, mainly coal fired

Proposed project: Replacing 2 boilers, increasing heat prod. by 30 %

Substitute consumption of 4500 tonnes coal per year coal per year

Bioenergy project, Pudozh, Karelia

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 48/50

48

Positive Conclusions I

Increased use of Bioenergy in NW Russia is feasible,and sustainable, with several possible positive effects

•Reduced CO2-emissions

•Reduced need for fossil fuel transport

•Reduction of waste and pollution to air, water and soil•Basis for production of equipment locally

•Possible export of biofuels such as pellets and briquettes –

however business development should be thorough

•Possible Creation of local positions

•Possible use of biofuel will improve local economy

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 49/50

49

Conclusions & Challenges II

•To obtain significant shares of RES, authorities must increasefocus and ease framework conditions further

•Financing projects is possible in several ways even today,however tailor made solutions are required, as well as quite muchendurance

•Numerous financing institutions available, WB, EBRD, NEFCONEFCO most suitable for small to medium sized loans;

30 000 – 4 MEuro – refer www.nefco.org

8/3/2019 Harald Birkeland

http://slidepdf.com/reader/full/harald-birkeland 50/50

50

Thank you for your attention !

• Additional information

– http://www.barentsenergy.org

– http://www.neeg.com

– http://www.forest.ru/

– Questions or comments welcome to [email protected]