16

Harbortouch Amex OptBlue Training Program HT2124

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | lucy-ashley-bell |

| View: | 218 times |

| Download: | 1 times |

HarbortouchAmex OptBlue

Training Program

HT2124

CONTENTS

History of Amex programs What happens on 4/17/2015? What are the interchange costs? Merchant pricing options FAQ

ESA (External Sales Agent) Referral program which has been around for almost two decades A one-time bonus used to be paid for acceptance, but was

discontinued by Amex several years ago All that remains is a limited number of basis points for a short time

period Most merchants in the HT portfolio are under the ESA program

HISTORY OF AMEX PROGRAMS

Amex OnePoint Introduced a few years ago Benefits included slightly better basis point revenue sharing and

combined deposits of Visa, MC, Discover, Amex, debit all in the same batches

Simplified reconciliation for merchants Only merchants with less than $500K/annual Amex volume can

participate American Express will discontinue the program with the release

of OptBlue

HISTORY OF AMEX PROGRAMS

Amex OptBlue This fully transitions American Express to the same type of

acquiring as we are used to with Visa, MC and Discover There is an Interchange cost, assessments, sponsorship, and

surcharges There is a lot of flexibility on how merchants can be priced Active sales partners can earn residuals the same as they would

with the other card types All deposits are combined, just like with Amex OnePoint, and risk

liability is transferred from American Express to the acquirer, Harbortouch

Only merchants with less than $1M/annual Amex volume can participate

HISTORY OF AMEX PROGRAMS

Existing Merchants on Amex OnePoint• Will convert automatically to Amex OptBlue on this date• Merchant pricing will be very close to what the merchant was paying with

Amex OnePoint• Active sales partners will start earning a residual on that processing volume • After 4/17/15, there will not be an Amex OnePoint program anymore

Existing Merchants still on Amex ESA These are merchants that were not converted to Amex one point These merchants will remain on Amex ESA until 10/17/15, when American

Express will automatically convert the merchants to OptBlue Existing ESA merchants can not be converted to OptBlue prior to this date

All New Merchants Going Forward• All merchants signed up from 4/17/15 forward will be eligible to be signed

directly to OptBlue

WHAT HAPPENS ON 4/17/2015?

American Express will typically have the highest Interchange costs out of all the card brands

American Express uniquely qualifies the Interchange based off of average ticket and merchant industry type

American Express pricing components include:

• Interchange = Varying costs based on merchant industry type and average ticket

• Assessments = 15 basis points

• Sponsorship and Risk = 25 basis points

- Revenue sharing would be over and above the costs above

- There are two surcharges for key-entry (30 basis points) and foreign issued cards (40 basis points), both of which cannot be marked-up

WHAT ARE THE INTERCHANGE COSTS?

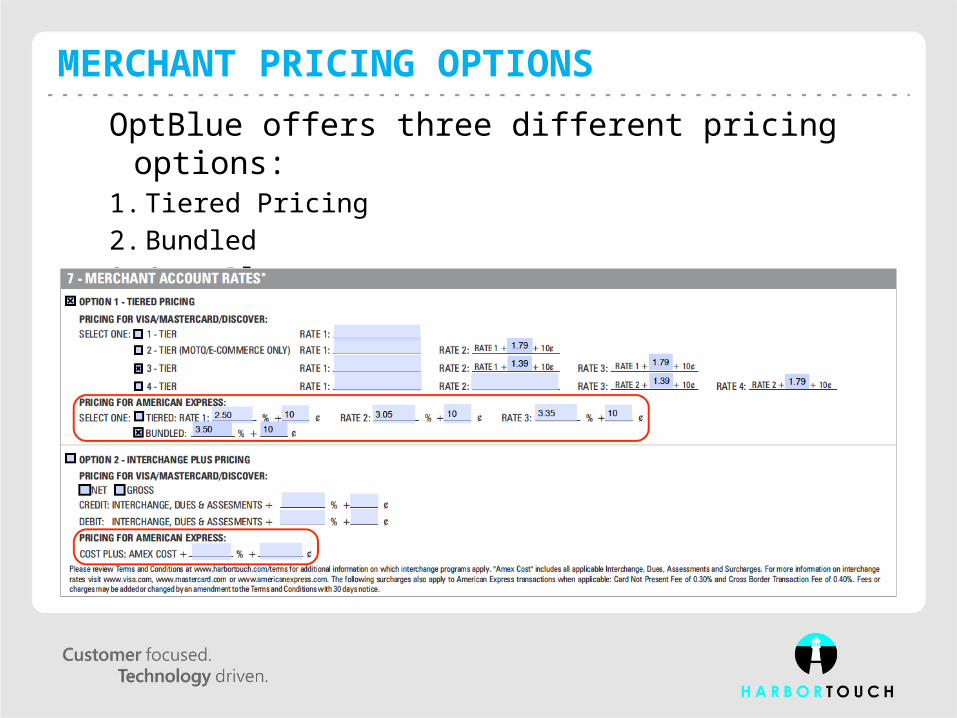

OptBlue offers three different pricing options: 1. Tiered Pricing2. Bundled3. Cost Plus

MERCHANT PRICING OPTIONS

1. Tiered Pricing Every Amex Interchange rate has a tier associated with it for each

industry type Rate 1, Rate 2, and Rate 3 on the merchant application correspond to

each Interchange tier• For example: When signing up a restaurant, you could

hypothetically charge Rate 1 = 2.5%, Rate 2 = 3.05% and Rate 3 = 3.35%.

The qualifying tier is determined by the transaction amount on the Interchange chart

In this case, there would be 25 basis points of margin in each tier, and the costs in all cases would be less than the typical American Express rate a merchant is paying now

MERCHANT PRICING OPTIONS

2. Bundled This would be continuing with how Amex has historically priced

merchants For example, 3.5% would be a good example of historical Amex

pricing for the merchant In the case of a restaurant, there could be upwards of 125 basis

points (1.25%) of margin, depending on the qualifying Interchange This would be the highest margin pricing strategy

MERCHANT PRICING OPTIONS

3. Cost Plus This is essentially an Interchange/Cost Plus pricing method The American Express Interchange, Assessments and BIN sponsorship

will all be passed through to the merchant plus your indicated percentage and transaction fee mark-up

If this is priced the same as how Visa/MC/Discover is often priced, it will likely result in the most dramatic cost savings to the merchant and the lowest residual margin

MERCHANT PRICING OPTIONS

What do I have to do to convert my existing merchants to OptBlue?

Nothing. Everything is automatic. If your merchants are on Amex OnePoint prior to 4/17/15 they will automatically be converted to OptBlue. If your merchants are still on ESA as of 4/17/15 then they will remain on ESA until 10/17/15.

I have a merchant that does a lot of Amex volume on ESA still; can I move them to OptBlue?

No, only merchants that were on Amex OnePoint prior to 4/17/15 will be moved to OptBlue. Merchants still on ESA as of 4/17/15 will need to wait until 10/17/15 to convert to OptBlue. These are American Express rules.

I have a merchant on Amex OnePoint that will convert to OptBlue on 4/17/2015; will their rates change?

For the most part, No, but there are new pricing components to OptBlue that include key-entry and foreign-card surcharges that the merchant will begin paying

FREQUENTLY ASKED QUESTIONS

What program will all my new merchants be signed up on after 4/17/15?

All new merchants are signed on Amex OptBlue after 4/17/15.

Are there any merchants that American Express does not allow on OptBlue?

Yes, the usual very high-risk merchants and any merchant that processes over $1 million per year in American Express volume will be excluded.

Will I make residual revenue on OptBlue?

Yes, much more than any other Amex program. For all purposes, Amex OptBlue makes American Express very similar to Visa, MC, and Discover. There is an Interchange cost, Assessments, Sponsorship, and active sales partners would share in the revenue over those costs.

FREQUENTLY ASKED QUESTIONS

What rates should I charge the merchant for Amex OptBlue?

This is entirely your preference. If you want to maximize margins, simply charge merchants similar rates to what they were paying Amex previously. In that case, the average merchant was paying between 3.25% and 3.75%. This would present great residual margin opportunities. If you want a middle of the road option, try the 3-tier pricing. Of course the option with the least amount of profitability would be Cost Plus.

What are the best opportunities with Amex OptBlue?

Considering our edge at Harbortouch is POS Systems, you should focus on the restaurant industry. Most restaurant owners are paying very high American Express rates. There will be plenty of opportunities where you could lower a restaurant owner from 3.5% to 3.2%. In that case, you are saving the merchant 30 basis points. If the merchant does $40,000/month in Amex volume that is $120.00/month in savings. It nearly pays for two POS Elite systems. Not to mention there will be healthy residual profit remaining.

FREQUENTLY ASKED QUESTIONS

Will American Express OptBlue get competitive?

Like all things in our industry, when it comes down to just price, it will inevitably face margin compression. For now, many acquirers do not yet participate in the OptBlue program. This presents a great opportunity to grow and expand margins, as well as sign up new customers for the POS program.

What are some of the advantages for the merchant to participate in Amex OptBlue?

Lower processing rates, faster deposits (same time as Visa/MC/Discover including next day funding), easier reconciliation of deposits and statements, and better reporting. The merchant deals with one vendor (Harbortouch), instead of Harbortouch plus American Express as it was before.

If a merchant is happy with Amex ESA or has a special Amex ESA deal, can I still submit ESA numbers?

Yes, you can still submit Amex ESA numbers in the old manner, though we highly encourage you to transition to OptBlue. Eventually, OptBlue will be the only Amex program other than the few high-volume exceptions that American Express works with directly.

FREQUENTLY ASKED QUESTIONS

Can I choose to keep my merchants on Amex OnePoint?

No. Amex OnePoint will be discontinued by American Express when OptBlue rolls out. That is a good thing, since OptBlue is a much better program for merchants and our sales partners.

Does Harbortouch now have to manage risk on American Express transactions?

Yes. The same liability and risk exposure that Harbortouch manages for Visa, MC, and Discover would now include Amex as part of the OptBlue program.

What are the most important things for me to know about Amex OptBlue?

It is a great program filled with opportunity. You will make more money in terms of residuals. You will have greater control over Amex pricing to permit you to be more competitive. Your merchants will love it since they can get deposits faster with easier reconciliation and pay less for Amex rates.

FREQUENTLY ASKED QUESTIONS