23

HARMFUL TAX COMPETITION: A SPECIAL REFERENCE TO MAURITIUS INVESTMENT A SPECIAL REF. TO MAURITIUS INVEST. HARMFUL TAX COMPETITION ssssss PRESENTED BY HILAL AHMAD MALLA

| Date post: | 10-Oct-2014 |

| Category: |

Documents |

| Upload: | danish-hilal |

| View: | 51 times |

| Download: | 2 times |

HARMFUL TAX COMPETITION: A SPECIAL REFERENCE TO

MAURITIUS INVESTMENT

A SPECIAL REF. TO

MAURITIUS INVEST.

HARMFUL

TAX

COMPETITION

ssssss

PRESENTED BY

HILAL AHMAD MALLA

2

Introduction

“Competition among nations tends to produce a race to the top rather than to the bottom by limiting the

ability of powerful and voracious groups and politicians in each nation to impose their will at the expense of

the interests of the vast majority of their populations.”

The growing globalization of the world economy and the consequent vanishing of national

borders in cross border trade have resulted in an increasing mobility of economic activities.

There are many different economic, social and institutional factors influencing the

competitive position of a country and the investment decision taken by companies and

individuals. Taxation is normally just one of these factors. However, the rise in mobility of

economic activities and the disappearance of various international and legal impediments to

cross border trade have significantly increased the importance of the tax factor. This has been

at the expense of other factors that have traditionally tendered to determine location

decisions, for example the infrastructure of a country. This is particularly true in the case of

economic activities, such as financial services, that can be easily relocated to another country.

In these situations, the differences between countries, national taxation rapidly result in

economic activities moving to the country with the lowest effective burden.

This increased mobility has resulted in sharp increase in the tax competition between

countries, with each government seeking to attract or retain economic activities by creating a

favorable tax climate able to compete with those of other countries. These developments

have been particularly marked within the European Union, partly because of the creation

of common market and the introduction of the euro and partly because of the ever-increasing

integration of the policy in other areas. As a result direct taxation is now one of the most

important economic tools left available to the member states available at National Level.

In certain countries, tax competition has laid to tax reform, with tax bases being broadened

and the tax rates cut. Other countries have introduced preferential tax regimes, which

provide low effective tax rates for specific mobile business activities such as group

financing? The increasing tax competition emphasized the direct effects of such competition,

for example a healthy downward pressure on overall tax levels and a reduction in govt. size,

whilst opponents pointed to the undesired or harmful effects of certain forms of tax

competition such as the erosion of tax bases, a shift of the tax burden from capital to labour

and distortion of the market mechanisms. According to these opponents, the later situation

should be combated by taking countermeasures.

3

So the aim and objective is to prevent the downward pressure on overall tax levels, erosion of

tax bases, a shift of tax burden from capital to labour and distortion of the market mechanism,

this is what we call Harmful Tax Competition.

MEANING AND DEFINITION OF TAX COMPETITION

Tax competition, a form of regulatory competition, exists when governments are encouraged

to lower fiscal burdens to either encourage the inflow of productive resources or discourage

the exodus of those resources. Often, this means a governmental strategy of attracting foreign

direct investment, foreign indirect investment (financial investment), and high value human

resources by minimizing the overall taxation level and/or special tax preferences, creating a

comparative advantage. Some observers suggest that tax competition is generally a central

part of a government policy for improving the lot of labour by creating well-paid jobs (often

in countries or regions with very limited job prospects). Others suggest that it is beneficial

mainly for investors, as workers could have been better paid (both through lower taxation on

them, and through higher redistribution of wealth) if it was not for tax competition lowering

taxation on corporation. Many economists also argue that tax competition is beneficial in

raising total tax intake due to low corporate tax rates stimulating economic growth.1

It has also been argued that just as competition is good for businesses, competition is good

for governments as it drives efficiencies and good governance of the public budget.2

HISTORY OF TAX COMPITITION

From the mid 1900s governments had more freedom in setting their taxes as the barriers to

free movement of capital and people were high. The gradual process of globalization is

lowering these barriers and results in rising capital flows and greater manpower mobility.

The European Union (EU) illustrates the role of tax competition. The barriers to free

movement of capital and people were reduced close to nonexistence. Some countries (e.g.

Republic of Ireland) utilized their low levels of corporate tax to attract large amounts of

foreign investment while paying for the necessary infrastructure (roads, telecommunication)

from EU funds. The net contributors (like Germany) strongly oppose the idea of

1 Brill, Alex; Hassett, Kevin (31 July 2007), "Revenue Maximising Corporate Income Taxes: The Laffer Curve in OECD Countries",

Working paper 137 (American Express Institute).

2Hines, James R. (2005), "Do Tax Havens Flourish?", Tax Policy and the Economy (Cambridge, MA: MIT Press)

4

infrastructure transfers to low tax countries. Net contributors have not complained, however,

about recipient nations such as Greece and Portugal, which have kept taxes high and not

prospered. EU integration brings continuing pressure for consumption tax harmonization as

well. EU member nations must have a value-added tax (VAT) of at least 15 percent (the main

VAT band) and limits the set of products and services that can be included in the preferential

tax band. Still this policy does not stop people utilizing the difference in VAT levels when

purchasing certain goods (e.g. cars). The contributing factor is the single currency (Euro),

growth of e-commerce and geographical proximity. The political pressure for tax

harmonization extends beyond EU borders. Some neighboring countries with special tax

regimes (e.g. Switzerland) were already forced to some concessions in this area.

With tax competition in the era of globalization politicians have to keep tax rates

“reasonable” to dissuade workers and investors from moving to a lower tax environment.

Most countries started to reform their tax policies to improve their competitiveness. However,

the tax burden is just one part of a complex formula describing national competitiveness. The

other criteria like total manpower cost, labor market flexibility, education levels, political

stability, legal system stability and efficiency are also important. Governments typically react

with "carrot-and-stick" policies such as:3

reduction of both personal and corporate income tax rates

tax breaks/holidays (i.e. time limited tax exemptions)

favorable tax policies for non-residents

raising the barriers to free movement of capital

not allowing companies domiciled in tax havens to bid for public contracts

Political pressure on lower tax countries to “harmonize” (i.e. rise) their taxes.

3 Ruding report. P.29

5

CHAPTER 1

TAX COMPETITION: A GLOBAL PHENOMENON

Introduction

Globalization is one of the greatest economic events of the 20th century. It has positive

effects on the development of tax systems and has encouraged countries to engage in base

broadening and rate reducing tax reforms. However, it has also created an environment in

which tax havens thrive and jurisdictions are induced to adopt harmful preferential tax

regimes to attract mobile activities. This tax competition in the form of harmful tax practices

can distort trade and investment patterns, erode national tax bases, thus adversely affecting

and undermining the fairness of tax structures. Further, if this undercutting continues,

business location and financing decisions could become primarily tax driven and real

economic factors would take a backseat in business decisions.

The impact of these developments has already been quite significant. For example, foreign

direct investment by G7 countries through low-tax jurisdictions, increased to more than

US$200 billion over the period 1985-1994 and the rate of increase is well above that of total

outbound foreign direct investment by the G7. The accelerating process of globalization of

trade and investment has fundamentally changed the relationship among domestic tax

systems. Globalization has also been one of the driving forces behind tax reforms, which

have focused on base broadening and rate reductions, thereby minimizing tax induced

distortions. Globalization has also encouraged countries to assess continually their tax

systems and public expenditures with a view to making adjustments where appropriate to

improve the “fiscal climate” for investment. Globalization and the increased mobility of

capital has also promoted the development of capital and financial markets and has

encouraged countries to reduce tax barriers to capital flows and to modernize their tax

systems to reflect these developments. Many of these reforms have also addressed the need to

adapt tax systems to this new global environment. The process of globalization has led to

increased competition among businesses in the global market place. Multinational enterprises

(MNEs) are increasingly developing global strategies and their links with any one country are

becoming more tenuous. In addition, technological innovation has affected the way in which

MNEs are managed and made the physical location of management and other service

activities much less important to the MNE. International financial markets continue to

6

expand, a development that facilitates global welfare-enhancing cross-border capital flows.

This process has improved welfare and living standards around the world by creating a more

efficient allocation and utilization of resources.

As mentioned above, globalization has had a positive effect on the development of tax

systems. Globalization has, however, also had the negative effects of opening up new ways

by which companies and individuals can minimize and avoid taxes and in which countries

can exploit these new opportunities by developing tax policies aimed primarily at diverting

financial and other geographically mobile capital. These actions induce potential distortions

in the patterns of trade and investment and reduce global welfare. As discussed in detail

below, these schemes can erode national tax bases of other countries, may alter the structure

of taxation (by shifting part of the tax burden from mobile to relatively immobile factors and

from income to consumption) and may hamper the application of progressive tax rates and

the achievement of redistributive goals. Pressure of this sort can result in changes in tax

structures in which all countries may be forced by spillover effects to modify their tax bases,

even though a more desirable result could have been achieved through intensifying

international co-operation. More generally, tax policies in one economy are now more likely

to have repercussions on other economies. These new pressures on tax systems apply to both

business income in the corporate sector and to personal investment income.4

Tax havens or harmful preferential tax regimes that drive the effective tax rate levied on

income from the mobile activities significantly below rates in other countries have the

potential to cause harm by:

Distorting financial and, indirectly, real investment flows;

Undermining the integrity and fairness of tax structures;

Discouraging compliance by all taxpayers;

Re-shaping the desired level and mix of taxes and public spending;

Causing undesired shifts of part of the tax burden to less mobile tax bases, such as

labour, property and consumption,

Increasing the administrative costs and compliance burdens on tax authorities and

taxpayers.

4 OECD report ,455

7

What is considered harmful tax competition in the different states of the

world?

Various developments have contributed to an increase in the phenomenon of tax competition,

as outlined in the introduction to the previous chapter. The main causes of competition are

discussed in more detail below, with a distinction being drawn between general, worldwide

developments on the one hand and specific developments within the EU on the other hand.

5Over the past few decades the economy has become increasingly globalized .the vanishing

of national borders in cross-border trade ,the lifting of restrictions on capital markets and also

technical innovation have all contributed to a massive growth in international trade and

capital flows. This growth has in turn led to an increase in the mobility of certain economic

activities. Globalization results in a variety of different consequences. On the one hand there

are the positive consequences such as a more efficient allocation of production factors,6 a

more extensive range of goods available, a reduction in the costs of capital, a reduction in

transport costs and greater exchange of information and knowledge7.on the other hand;

however there are also certain negative consequences. Rising international trade volumes and

greater mobility of economic activities have led to external factors and undesired side effects

having a cross border impact on production and consumption, for example increasing

pressure on environment. In this sense globalization has contributed to transforming what

were previously national issues into international issues. It has therefore, become more

difficult for governments to pursue purely national policies. This tendency can also be clearly

perceived in respect of the levying of taxes.

Many countries’ tax systems date back to an era when companies were largely closed, with

limited cross border movements of goods and capital. Cross border trade flows were

frequently discouraged by protectionist import duties or physical barriers (for example,

limited availability of transportation), whilst capital flows controlled. As a result businesses

and individuals normally generated almost all of their income from activities or investments

in their countries of residence. Income and expenditure flows were largely restricted to a

single national economy, thus enabling tax to be levied in one country without conflicting

5 "Organisation for European Economic Co-operation", OECD. Retrieved 2008-07.

6 Cf .OECD Report, 522

7 The impact of economic globalization on taxation by TANZI V

8

with the levying of tax with the other country. Globalization has fundamentally changed the

relationship between national tax systems and their impact upon each other. Whereas in the

past governments could pursue national tax policies without regard for development in other

countries, they have now lost an element of their freedom to make policy since they now

have to take account of the cross border consequences( spill-over effects )of any taxes they

may propose or levy. These effects are reflected in various ways and at various levels of

taxation.

There are many economic, social and institutional factors affecting a country’s competitive

position and therefore the willingness of businesses and individuals to invest. Tax is normally

just one of these factors.8 In addition to tax, the political and economic stability of a country,

its social physical and communication infrastructures, the existing and potential size of a

market sector, labour costs, the availability of a skilled workforce and the size of financial

sector etc. are all factors influencing the choice of location. Increased mobility has, however,

led to the sharp increase in the importance of a tax as a factor, and this has been at the

expense of the more traditional reason for choosing a location.9 The types of economic

activity concerned are mainly those which can easily be relocated from one country to

another, such as capital (i.e. investments and savings), financial services, insurance and

leasing activities, patents and licensing management and highly skilled work. (E.g. in the

field of management, information and communications technology and research and

development).In these cases, the rate of tax levied by a country can be of vital importance in

respect of investment and location decisions.

FORMS OF TAX COMPETITION

In general terms, tax competition can be defined as:

Improving the relative competition position of one country vis-à-vis other countries by

reducing the tax burden on businesses and individuals in order to retain, gain or regain mobile

economic activities and the corresponding tax base. Tax competition can arise many different

ways. Tax measures designed to reduce the effective tax burden can be introduced in a

country in the form of legislative or administrative provisions or administrative practices.

Such measures can relate to both direct and indirect taxes, levied at either national

8 See OECD report.s6 9 See pinto, c EU and OECD to find Harmful tax competition :has the right path been undertaken.vol 26-12..p

.394

9

government or local government (I.e. Provincial or municipal) levels. A distinction can be

drawn generic and specific tax measures. Generic measures are those designed to achieve an

overall improvement in a country’s fiscal competitive position, for example a wide- ranging

programme of tax reforms. These could take the form, for instance, of a general reduction in

a country’s corporation tax rate.

The most striking example of a generic tax measure in the EU is Ireland’s is Ireland’s

reduction in its corporation tax rate to 12.5% as of 1st January 2003. Specific measures, which

are also referred to as 12.5% as of first January 2003.specific measures which are also

referred to as preferential tax measures are in contrast designed to improve the competitive

position of specific sector in a country’s economy for the primary purpose of attracting

mobile economic activities.

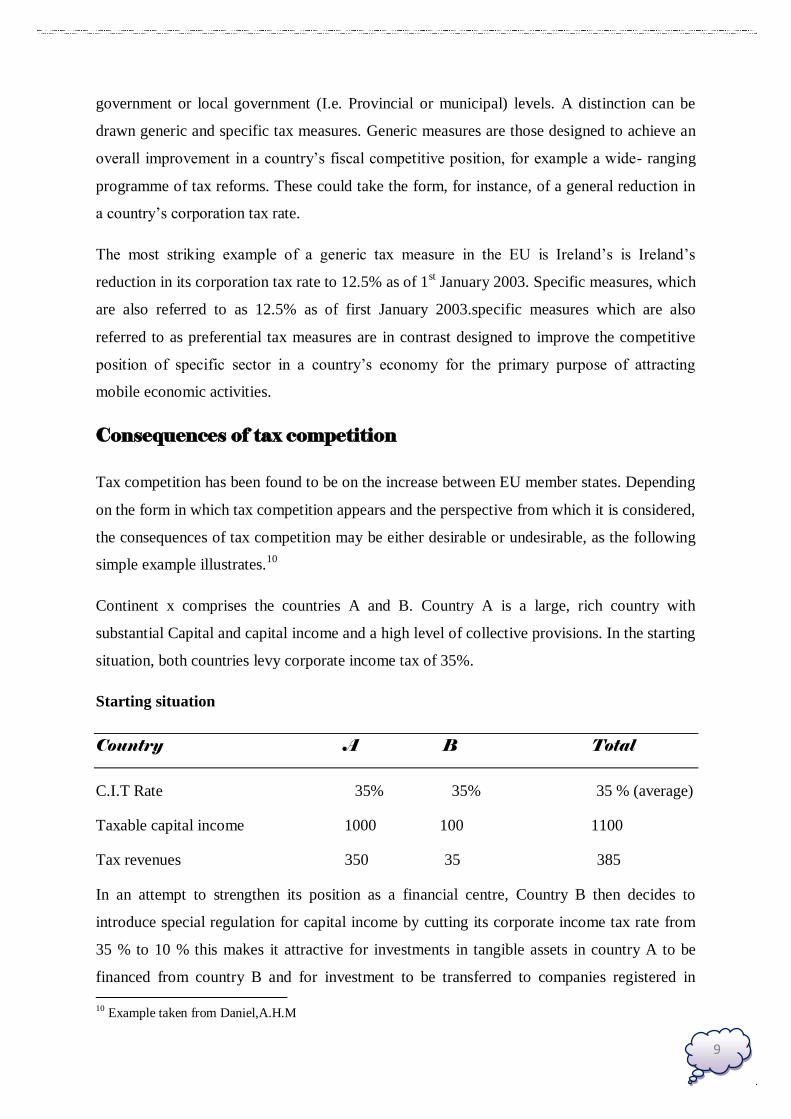

Consequences of tax competition

Tax competition has been found to be on the increase between EU member states. Depending

on the form in which tax competition appears and the perspective from which it is considered,

the consequences of tax competition may be either desirable or undesirable, as the following

simple example illustrates.10

Continent x comprises the countries A and B. Country A is a large, rich country with

substantial Capital and capital income and a high level of collective provisions. In the starting

situation, both countries levy corporate income tax of 35%.

Starting situation

Country A B Total

C.I.T Rate 35% 35% 35 % (average)

Taxable capital income 1000 100 1100

Tax revenues 350 35 385

In an attempt to strengthen its position as a financial centre, Country B then decides to

introduce special regulation for capital income by cutting its corporate income tax rate from

35 % to 10 % this makes it attractive for investments in tangible assets in country A to be

financed from country B and for investment to be transferred to companies registered in

10 Example taken from Daniel,A.H.M

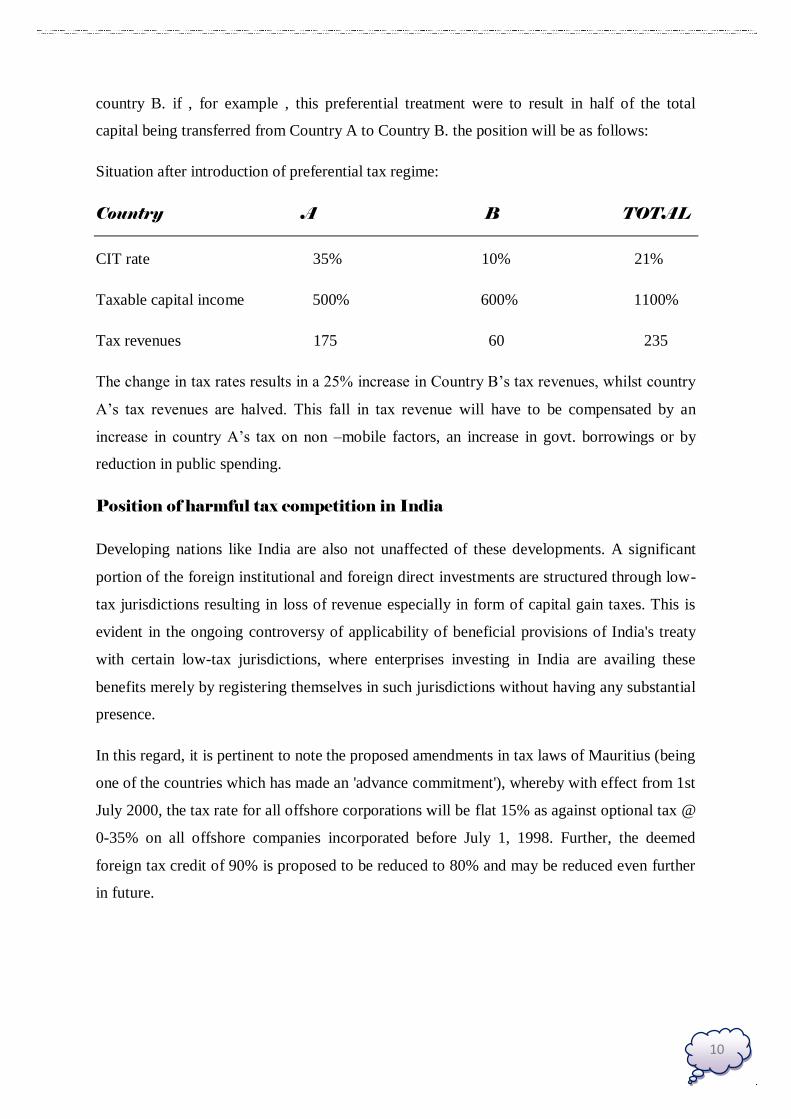

10

country B. if , for example , this preferential treatment were to result in half of the total

capital being transferred from Country A to Country B. the position will be as follows:

Situation after introduction of preferential tax regime:

Country A B TOTAL

CIT rate 35% 10% 21%

Taxable capital income 500% 600% 1100%

Tax revenues 175 60 235

The change in tax rates results in a 25% increase in Country B’s tax revenues, whilst country

A’s tax revenues are halved. This fall in tax revenue will have to be compensated by an

increase in country A’s tax on non –mobile factors, an increase in govt. borrowings or by

reduction in public spending.

Position of harmful tax competition in India

Developing nations like India are also not unaffected of these developments. A significant

portion of the foreign institutional and foreign direct investments are structured through low-

tax jurisdictions resulting in loss of revenue especially in form of capital gain taxes. This is

evident in the ongoing controversy of applicability of beneficial provisions of India's treaty

with certain low-tax jurisdictions, where enterprises investing in India are availing these

benefits merely by registering themselves in such jurisdictions without having any substantial

presence.

In this regard, it is pertinent to note the proposed amendments in tax laws of Mauritius (being

one of the countries which has made an 'advance commitment'), whereby with effect from 1st

July 2000, the tax rate for all offshore corporations will be flat 15% as against optional tax @

0-35% on all offshore companies incorporated before July 1, 1998. Further, the deemed

foreign tax credit of 90% is proposed to be reduced to 80% and may be reduced even further

in future.

11

CHAPTER 2

FACTORS TO IDENTIFY TAX HAVENS AND HARMFUL

PREFERENTIAL TAX REGIMES!

INTRODUCTION

This Chapter discusses the factors to be used in identifying, tax-haven jurisdictions and

harmful preferential tax regimes in non-haven jurisdictions. It focuses on identifying the

factors that enable tax havens and harmful preferential tax regimes in OECD Member and

non-member countries to attract highly mobile activities, such as financial and other service

activities. The Chapter provides practical guidelines to assist governments in identifying tax

havens and in distinguishing between acceptable and harmful preferential tax regimes.

The Chapter takes a necessary and practical step towards explaining further why governments

are concerned about harmful tax competition. It does this by first identifying and discussing

factors that characterize tax havens. It then discusses factors that may identify preferential tax

regimes that can be considered to lead to harmful tax competition.

At the outset, a distinction must be made between three broad categories of situations in

which the tax levied in one country on income from geographically mobile activities, such as

financial and other service activities, is lower than the tax that would be levied on the same

income in another country:11

The first country is a tax haven and, as such, generally imposes no or only nominal

tax on that income the first country collects significant revenues from tax imposed on

income at the individual or corporate level but its tax system has preferential features

that allow the relevant income to be subject to low or no taxation;

The first country collects significant revenues from tax imposed on income at the

individual or corporate level but the effective tax rate that is generally applicable at

that level in that country is lower than that levied in the second country.

11 http://www.oecd.org/document/58/0,3746,en_2649_201185_18894

12

All three categories of situations may have undesirable effects from the perspective of the

other country. Above, globalization has had a positive effect on the development of tax

systems, being, for instance, the driving force behind tax reforms which have focused on base

broadening and rate reductions, thereby minimizing tax induced distortions. Accordingly, and

insofar as the other factors referred to in this Chapter are not present, the issues arising in this

third category are outside the scope of this study. Any spillover effects for the revenue of the

other country may be dealt with by a variety of means at the unilateral or bilateral level It is

not intended to explicitly or implicitly suggest that there is some general minimum effective

rate of tax to be imposed on income below which a country would be considered to be

engaging in harmful tax competition.12

The first two categories, which are the focus of this chapter, are dealt with differently. While

the concept of “tax haven” does not have a precise technical meaning, it is recognized that a

useful distinction may be made between, on the one hand, countries that are able to finance

their public services with no or nominal income taxes and that offer themselves as places to

be used by non-residents to escape tax in their country of residence and, on the other hand,

countries which raise significant revenues from their income tax but whose tax system has

features constituting harmful tax competition. In the first case, the country has no interest in

trying to curb the “race to the bottom” with respect to income tax and is actively contributing

to the erosion of income tax revenues in other countries. For that reason, these countries are

unlikely to co-operate in curbing harmful tax competition. By contrast, in the second case, a

country may have a significant amount of revenues which are at risk from the spread of

harmful tax competition and it is therefore more likely to agree on concerted action. Because

of this difference, this Report distinguishes between jurisdictions in the first category, which

are referred to as tax havens, and jurisdictions in the second category, which are considered

as countries which have potentially harmful preferential tax regimes.. Many factors may

contribute to the classification of the actual or potential effects of tax practices as harmful.

Any evaluation should be based on an overall assessment of the relevant factors. The absence

of tax or a low effective tax rate on the relevant income is the starting point of any evaluation.

No or only nominal taxation combined with the fact that a country offers itself as a place, or

is perceived to be a place, to be used by non-residents to escape tax in their country of

residence may be sufficient to classify that jurisdiction as a tax haven. Similarly, no or only

12 "Shaping Policies for a Digital World". OECD (Retrieved 16-01-2010)

13

nominal taxation combined with serious limitations on the ability of other countries to obtain

information from that country for tax purposes would typically identify a tax haven. With

respect to preferential tax regimes, key factors, other than no or low effective taxation on the

relevant income, include: whether the regime is restricted to non-residents and whether it is

otherwise isolated from the domestic economy (i.e., ring-fencing), non-transparency and a

lack of access to information on taxpayers benefiting from a preferential tax regime.

TAX HAVENS

Many fiscally sovereign territories and countries use tax and non-tax incentives to attract

activities in the financial and other services sectors. These territories and countries offer the

foreign investor an environment with a no or only nominal taxation which is usually coupled

with a reduction in regulatory or administrative constraints. The activity is usually not subject

to information exchange because, for example, of strict bank secrecy provisions. Tax havens

generally rely on the existing global financial infrastructure and have traditionally facilitated

capital flows and improved financial market liquidity. Now that the non-haven countries have

liberalized and de-regulated their financial markets, any potential benefits brought about by

tax havens in this connection are more than offset by their adverse tax effects. Since tax and

non-tax advantages tend to divert financial capital away from other countries, tax havens

have a large adverse impact on the revenue bases of other countries. Because tax havens offer

a way to minimize taxes and to obtain financial confidentiality, tax havens are appealing to

corporate and individual investors. Tax havens serve three main purposes: they provide a

location for holding passive investments (“money boxes”); they provide a location where

“paper” profits can be booked; and they enable the affairs of taxpayers, particularly their

bank accounts, to be effectively shielded from scrutiny by tax authorities of other countries.

All of these functions may potentially cause harm to the tax systems of other countries as

they facilitate both corporate and individual income tax avoidance and evasion.13

A 1987 Report by the OECD recognized the difficulties involved in providing an objective

definition of a tax haven1. That Report concluded that a good indicator that a country is

playing the role of a tax haven is where the country or territory offers itself or is generally

recognized as a tax haven. While this is known as the “reputation test”, the present Report

sets out various factors to identify tax havens.

13 Text of the OECD Guidelines for Multinational Enterprises

14

HOW TO IDENTIFY TAX HAVENS

The necessary starting point to identify a tax haven is to ask (a) Whether a jurisdiction

imposes no or only nominal taxes (generally or in special circumstances) and offers itself, or

is perceived to offer itself, as a place to be used by non-residents to escape tax in their

country of residence. Other key factors which can confirm the existence of a tax haven (b)

laws or administrative practices which prevent the effective exchange of relevant information

with other governments on taxpayers benefiting from the low or no tax jurisdiction; (c) lack

of transparency and (d) the absence of a requirement that the activity be substantial, since it

would suggest that a jurisdiction may be attempting to attract investment or transactions that

are purely tax driven (transactions may be booked there without the requirement of adding

value so that there is little real activity, i.e. these jurisdictions are essentially “booking

centres”). 14

Only nominal taxation is a necessary condition for the identification of a tax haven. if

combined with a situation where the jurisdiction offers or is perceived to offer itself as a

place where non-residents can escape tax in their country of residence, it may be sufficient to

identify a tax haven.

14 "17 countries call for new 'tax haven blacklist'". EURO News. 2008-10-22. Retrieved 2008-10-22.

15

KEY FACTORS IN IDENTIFYING TAX HAVENS FOR THE

a) No or only nominal taxes

No or only nominal taxation on the relevant income is the starting point to classify a jurisdiction

as a tax haven.

b) Lack of effective exchange of information

Tax havens typically have in place laws or administrative practices under which businesses and

individuals can benefit from strict secrecy rules and other protections against scrutiny by tax

authorities thereby preventing the effective exchange of information on taxpayers benefiting

from the low tax jurisdiction.

c) Lack of transparency

A lack of transparency in the operation of the legislative, legal or administrative provisions is

another factor in identifying tax havens.

d) No substantial activities

The absence of a requirement that the activity be substantial is important since it would suggest

that a jurisdiction may be attempting to attract investment or transactions that are purely tax

driven.

In general, the importance of each of the other key factors referred to above very much

depends on the particular context. Even if the tax haven does impose tax, the definition of

domestic source income may be so restricted as to result in very little income being taxed.

16

CHAPTER 3

MAURITIUS INVESTMENT

INTRODUCTION

THE logic of a liberal economic regime can result in apparent paradoxes. Mauritius, a tiny

speck in the Indian Ocean, with a population of 1.2 million and an economy one-hundredth

the size of the Indian economy, is the biggest exporter of capital to India.

The use of Mauritius as a gateway to funnel foreign investments into India has always been

controversial. The island nation's financial regime, endowed with the key characteristics of a

quasi tax haven, has facilitated this. Curiously, successive Indian governments, which have

cried themselves hoarse about a runaway fiscal deficit and a resource crunch, have indulged

in self-denial and have refused to tax the earnings of these foreign entities. But the issue is

much more than lost revenues. The question is of equity. Can ordinary citizens be asked to

pay taxes even as a small body of foreign-based entities is not even asked to pay a fraction of

their earnings made through speculation on Indian soil? Although the Supreme Court on

October 7 quelled the legal challenge to the government's refusal to clamp down on the

Mauritius gateway, the controversy refuses to die.

The key to the apparent paradox lies in the provisions of a two-decade-old bilateral

agreement, the Double Taxation Avoidance Convention (DTAC). Foreign entities have set

up paper companies in Mauritius, claiming to be Mauritian residents. These companies,

masquerading as Mauritian companies, have invested in India. And, taking advantage of the

DTAC they avoid paying any taxes in India. They pay no taxes in Mauritius too.

MAURITIUS A SOURCE OF INVESTMENT

Mauritius is the single biggest source of foreign direct investment (FDI) in India - amounting

to $534 million in 2002-03 (about one-third of all FDI). But that is not all. Mauritius-based

foreign institutional investors (FII) are also believed to be major players in the Indian

bourses. FII investment in Indian stock markets between April and October this year

amounted to almost $5 billion - almost ten times what they invested in the whole of the last

financial year. Indeed, they are believed to be the ones leading the current boom in the stock

markets. But the Mauritius angle does not end there. Reports in the financial media indicate

that a substantial part of FII investment is believed to be coming from Non-resident Indians

17

(NRIs) bringing back funds to participate in the ongoing speculative orgy in the Indian stock

markets, much of which is said to be routed through Mauritius-based paper companies.

Mauritius is also reportedly the base of much of the hedge funds that are reported to be

active in the current boom. Hedge funds, which deploy large volumes of funds in thin

arbitrage deals made for very short-term gains, account for at least 30 per cent of the FII

activity in the ongoing boom in the bourses. These entities, using the device of Participatory

Notes, and dealing through the sub-accounts of the FIIs, which need not be registered with

regulatory agencies such as the Securities and Exchange Board of India (SEBI) or the

Reserve Bank of India (RBI), constitute the core of the speculative excess that is currently on.

This bout of speculation is not confined to the stock markets. In fact, from an economic

perspective, this boom is far more dangerous than previous episodes because these players

are betting simultaneously in several markets. While bringing in dollar denominated funds

and thereby adding to the burgeoning foreign exchange reserves, currently amounting to over

$90 billion, they are betting in stocks, the Indian currency and also speculating on the interest

rates, all at the same time. That Mauritius is a home base for all this is common knowledge.

The lack of regulatory oversight means that one is unable to quantify the funds coming in

from the tax haven. Although the losses to the government are difficult to estimate, primarily

because it is difficult to ascertain how much comes through the Mauritius route, it is reckoned

that the potential losses because of the loophole could run into several thousand crores since

1991, when India opened the floodgates to foreign investment. The government has

repeatedly fought shy of taking on foreign investors. Instead, it has restrained its own arm,

the Income Tax (I.T.) Department, from investigating the misuse of the bilateral agreement

by foreign investors.

ALTHOUGH successive governments have refused to plug the loopholes in the DTAC,

Indian regulators have always viewed them with suspicion. In late March 2000, officials in

the I.T. Department in Mumbai investigated 24 Mauritius-based entities and issued

"assessment orders" on them. The officers, racing against time to file their orders before the

March 31 deadline, were basically engaged in lifting the corporate veil covering these

entities. For instance, the I.T. Department's assessment of Cox and Kings Overseas Funds

(Mauritius), made on March 29, 2000 for the company's assessment year 1997-98, showed

that the company was in fact a subsidiary of Cox and Kings Overseas Fund Incorporated in

Luxembourg. The assessment order revealed that the company routed its investment through

18

Mauritius because "it realized that if it directly made investments in India, it will be liable to

pay Indian income tax on investment including capital gains". Aware that if investments were

made through a Mauritius-based company it would not have to pay taxes in India, it floated a

fully owned subsidiary in the island nation. In 1994, Cox and Kings incorporated the

subsidiary in Mauritius. It hired professional consultants, who were readily available for hire

in Mauritius, to serve on the subsidiary's board. The subsidiary's business of investing funds

in India was handled entirely by J. Henry Schroeder Bank AG, based in Switzerland.

The sole business of the subsidiary in Mauritius was to undertake investments outside

Mauritius. In fact, Mauritius laws proscribed it from acquiring property or raising funds in the

country. In fact it was not allowed to engage in any kind of business activity in Mauritius.

Thus, the I.T. Department found that the company's sole motive for existence as an entity in

Mauritius was to enable it to funnel investments overseas, particularly India. On the basis of

its investigation, the I.T. Department's assessment order observed that "the real control of

affairs of the Mauritian company is in the hands of the holding company incorporated outside

Mauritius". It also noted that "the Mauritian subsidiary has been created with the main

purpose to avoid tax". On the basis of its investigation of 24 cases, including Cox and Kings,

the I.T. Department thus issued show-cause notices to them. It pointed out that they were not

eligible for benefits of the DTAC since they were "not bona fide and genuine residents of

Mauritius". The department also alleged that the abuse of the DTAC by entities from third

countries amounted to "treaty shopping".

Soon after the orders were served on the FIIs, all hell broke loose. Amidst the controversy

there were also allegations that the then Union Minister for Finance Yashwant Sinha's

daughter-in-law was working for a Mauritius-based FII investing in India. The lobbies went

into overdrive and there were dark hints that the stock market would collapse because FIIs

would pull out of the Indian markets. On April 13, 2000, the Central Board of Direct Taxes,

the apex body governing the Income Tax Department, issued Circular Number 789, which

has since then been a subject of fierce litigation. The circular "clarified" that the production

of a "certificate of residence" issued by the Mauritius authorities would "constitute sufficient

evidence for accepting the status of residence as well as beneficial ownership for applying the

DTAC accordingly". It also clarified that FIIs and other entities based in Mauritius "should

not be taxable in India on income from capital gains arising in India".

19

The Joint Parliamentary Committee (JPC) probe into the 2001 stock market scam, in which

the broker Ketan Parekh was the kingpin, revealed large-scale abuse of Mauritius-based

entities. It revealed that Overseas Corporate Bodies (OCB), which are primarily vehicles

floated by NRIs but which can act as fronts for other foreign investors, acted in concert with

Ketan Parekh to siphon funds out of the country. In fact, there were allegations that Yashwant

Sinha kept the Mauritius gate wide open so that speculators could avoid paying taxes in India.

In fact, in his written submission to the JPC, after he was no longer Finance Minister, Sinha

said that the revenue losses on account of the abuse of the Mauritius route were only

"notional". In fact, he admitted that although he was aware of the abuse of the route, he did

not plug the holes in the DTAC because the inflow of foreign investments was considered

more important than raising revenue.

THE CBDT circular was challenged in the Delhi High Court by public interest petitions

filed by the Azadi Bachao Andolan (represented by Prashanth Bhushan) and a former Chief

Commissioner of Income Tax, Shiva Kant Jha. The latter, who is also an advocate with the

Supreme Court Bar, argued that the Government of Mauritius, through "reforms" undertaken

in the early 1990s, had transformed its legal and financial system into a veritable tax haven

(see interview). He said that third-country entities were using the provisions of the DTAC to

establish "conduit companies" in Mauritius and using them as vehicles to invest in India with

the sole objective of dodging tax in India. Shiva Kant Jha pointed out that the CBDT circular,

by asking I.T. officers to accept at face value the "certificate of residence" provided by the

Mauritian authorities, effectively curtailed their ability to investigate whether they were really

residents of Mauritius. He pointed out that the circular prevented officers from discharging

their duties by "investigating the matrix of facts to determine whether a company seeking

benefits under the convention was really a Mauritian resident". Shiva Kant Jha pointed out

that the Mauritius-based entities were not paying any capital gains tax either in India or in

Mauritius. He said that although Section 90 of the Income Tax Act provided the government

with the authority to enter into agreements with other countries, these powers were

specifically for entering into agreements on double taxation, that is, the elimination of a

similar tax on the same set of entities for identical transactions in two different locations. Jha

pointed out that the DTAC was meant to prevent double taxation, not tax evasion or

avoidance. He also said that the government had failed to discharge its duties by causing

wrongful revenue losses.

20

In May 2002, the Delhi High Court struck down circular 78915

. It observed that it was the

duty of the I.T. Department to find out whether an assessee was taking shelter under the

DTAC to avoid tax. In this, it was well within its right to make every endeavor to lift the

corporate veil to find the true intent of these entities. It also observed that the abuse of a

treaty or "treaty shopping" to "be illegal and thus necessarily forbidden".

The government filed an appeal against the High Court order in the Supreme Court in

October 2002. A consortium of international investors, represented by the Global Business

Institute (GBI), joined the government in filing the appeal. Interestingly, in February 2003,

Arun Jaitley, currently Union Minister for Law and Justice and Commerce and Industry, who

at that time was not a member of the Cabinet, donned his lawyer's robes to appear on behalf

of the GBI. In its judgment, the Supreme Court ruled that it was the sovereign right of the

state to enter into treaties with other countries. By taking a technical approach, the court ruled

that Mauritius-based companies were liable to pay tax in Mauritius; it just so happens that

they are not levied taxes there. It also ruled that the certificate of residence could not be

disputed because as a sovereign state Mauritius had the power to determine who ought to be a

resident of that nation. However, the Supreme Court observed that the Indo-Mauritius DTAC

was in marked contrast to the Indo-U.S. DTAC. Shiva Kant Jha had pointed out that the Indo-

U.S. DTAC provided for credits for taxes paid in either country, but had a specific provision

that barred third-country entities from taking advantage of the bilateral treaty.

HOW much has the Indian state lost in revenues? Data are hard to come by to make an

accurate estimate. However, one can hazard a guess on the basis of the value of securities

sold by FIIs. The long-term capital gains tax, applicable on investments sold after holding

them for more than a year, is at the rate of 10 per cent. Short-term rates are applied at the

rate of 30 per cent when investments are liquidated. It is well known that the bulk of the FII

investments are routed through Mauritius. Applying a uniform rate of 10 per cent capital

gains tax on the gross sales made by FIIs would give at the very least a ballpark figure.

Although it can be argued that this would overestimate the extent of lost revenue because it

would not account for losses that FIIs made when they made sales, the fact that short-term

capital gains are not being factored into the estimate offsets this reasonably.

15 Income Tax Department, issued Circular Number

21

On the basis of the figures presented in the table the losses to the exchequer on account of

lost capital gains tax in the last decade would amount to a whopping Rs.28, 139 crores. Even

if it is an admitted policy of the state to woo foreign capital at any cost, the question is

whether losses of this kind are acceptable to the polity at large. The average annual loss to the

exchequer amounts to over Rs.2, 300 crores. To get some idea of the magnitude of these

losses in relation to the Union Budget, these magnitudes amount to roughly 10 per cent of the

gross tax revenues of the Union projected for 2003-04. To put it more provocatively, in the

context of the ongoing controversy surrounding the privatization programme, the extent of

lost revenues could easily have saved companies such as Balco, VSNL, IPCL and several

others from being sold off to private parties; indeed, privatization as an option would appear

irrational if the executive chose not to forgo these taxes.

Tax havens are an important feature of the globalised world of financial speculation. Shiva

Kant Jha believes that there is tension between the needs of the globalised system and the

sovereignty of nation states. While financial entities want to move funds across a seamless

world at will, nation states are finding that their traditionally accepted sovereign right to tax

any economic entities active within their frontiers is increasingly coming under pressure from

powerful players in the financial world. The rise of Mauritius as a tax haven in the 1990s,

specializing in funneling investments into India, reflects this reality. It is obvious that

successive Indian governments have chosen to let this happen while creating two sets of tax

payers within India - a privileged set of foreign entities who pay no taxes even as they engage

in speculative excesses and ordinary Indians who have to pay taxes. Some would even regard

the "notional" tax losses as subsidies paid to the well-heeled.16

Conclusion

Based on the research done on this project the following overall conclusion can be drawn.

Harmful tax competition has become a major issue in the whole world. Globalization has

acted as a catalyst in integrating economies, dissolving political boundaries and changing

system of governance, politics, finance, trade and investment. Now the World is witnessing

reduced trade barriers, loosened exchange control, increased mobility of capital, skilled labor

and other factors of production. This has led to increased competition amongst countries

(similar to businesses competing domestically) to attract trade and investment.

16 http://www.frontlineonnet.com/fl2023/stories/20031121002108900.htm

22

There are many factors governing choice of the investors for e.g. stable currency, trustworthy

legal system, transparent financial markets, infrastructure, skilled labor, tax incentives etc .

Countries which are relatively less fortunate in terms of natural resources and geographical

locations stands at a disadvantageous position to attract investment to boost their economies.

Equity and fair competition demands that these countries should be provided with a level

playing field and stronger economies should be discouraged from interfering with the

capacity of these countries to pursue policies which are in their best interests. It is widely

accepted that with increased capital mobility tax considerations are playing a pivotal role in

deciding business locations and making investment choices. There seems to be no

justification in prohibiting countries (particularly the disadvantageous ones) to follow

aggressive tax policies except for some plausible reason such as terrorism, money laundering

etc. It is completely with in sovereign realms of the countries to pursue such aggressive tax

policies, suiting their own interests.

Suggestions

The rules regulating practices of countries to compete with each other should perpetuate

global interests rather than interests of some powerful nations intending to bully weak nations

and to grind their own axe. Any effort to regulate tax competition should be taken up by a

forum representing diverse interests of the world and not merely a particular group of

powerful nations like OECD, which has suo motto assumed the responsibility to correct the

world.

India should also take necessary steps to remove the loop holes embedded in the two-decade-

old bilateral agreement, the Double Taxation Avoidance Convention (DTAC), because this

Provides an open opportunity to the foreign investors to get in and take benefit of the

outdated treaties.

23

Bibliography

Books

Harmful tax competition in the European Union, code of conduct, counters measures

and EU Law, Kluwer law international publishing, 2004

Angharad Miller and Lynne Oats, Principles of International Taxation, Tottel

Publishing, 2006

Andrea Amatucci, International Tax Law, Kluwer Law International publishing,2007

OECD documents

OECD 1998 Report “ Harmful tax competition; An emerging global issue”, available

at <www.oecd.org/dataoecd/33/1/1904184.pdf>, OECD 2000 Report available at www.oecd.org/dataoecd/9/61/2090192.pdf OECD 2001 Report available at www.oecd.org/dataoecd/60/28/2664438.pdf OECD 2004 Report available at www.oecd.org/dataoecd/60/33/30901115.pdf Business and Industrial Advisory Committee to OECD, A Business View On Tax

Competition, June 1999 available at www.biac.org/statements/tax/htc.pdfBIAC OECD Revenue Statistics-Comparative tables available at

www.stats.oecd.org/wbos/Default.aspx

Journals and Articles

Alexander Townsend Jr., The Global Schoolyard Bully: The Organization Of

Economic Development’s coercive efforts to control tax competition, 25 Fordham

Int’l L.J 215 (2001-2002)

Michael Littlewood, Tax competition: Harmful to whom?, 26 Mich. J. Int’l L. 411

(2004-2005),

Mitchell B. Weiss, International Tax Competition; An efficient or inefficient

phenomenon?, 16 Akron J. 99 (2001)

Javier G. Salinas, The OECD tax competition initiative: A critique of its merits in the

global market place, 25 Hous. J. Int’l L. 531 (2002-2003)

Kimberley Carlson, When Cows have wings: An analysis of OECD’s tax haven work

as it relates to Globalization, Sovereignty and Privacy, 35 J. Marshall L. Rev. 163

(2001-2002)

Julie Roin, Competition and evasion: Another perspective on International tax

competition, 89 Geo L.J 543 (2000-2001)

Yoram Margolith, Tax competition, foreign direct investment and growth: Using tax

system in promoting developing countries, 23 Va. Tax Rev. 161 (2003-2004)

Almeida, Tax Havens: An Analysis of the OECD work with policy recommendations,