70

COUNTY AUDIT Haskell County For the fiscal year ended June 30, 2012 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE

COUNTY AUDIT

Haskell

County For the fiscal year ended June 30, 2012

Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE

This publication, issued by the Oklahoma State Auditor and Inspector’s Office as authorized by 19 O.S. § 171, has

not been printed, but is available on the agency’s website (www.sai.ok.gov) and in the Oklahoma Department of

Libraries Publications Clearinghouse Digital Collection, pursuant to 74 O.S. § 3105.B.

HASKELL COUNTY, OKLAHOMA

FINANCIAL STATEMENT

AND INDEPENDENT AUDITOR'S REPORT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

July 31, 2014

TO THE CITIZENS OF

HASKELL COUNTY, OKLAHOMA

Transmitted herewith is the audit of Haskell County, Oklahoma for the fiscal year ended June 30, 2012.

The audit was conducted in accordance with 19 O.S. § 171.

A report of this type can be critical in nature. Failure to report commendable features in the accounting

and operating procedures of the entity should not be interpreted to mean that they do not exist.

The goal of the State Auditor and Inspector is to promote accountability and fiscal integrity in state and

local government. Maintaining our independence as we provide this service to the taxpayers of Oklahoma

is of utmost importance.

We wish to take this opportunity to express our appreciation for the assistance and cooperation extended

to our office during our engagement.

Sincerely,

GARY A. JONES, CPA, CFE OKLAHOMA STATE AUDITOR & INSPECTOR

HASKELL COUNTY, OKLAHOMA

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

i

TABLE OF CONTENTS

INTRODUCTORY SECTION (Unaudited)

Statistical Information .................................................................................................................................. iii

County Officials ........................................................................................................................................... iv

Ad Valorem Tax Distribution ....................................................................................................................... v

Assessed Value of Property Trend Analysis ................................................................................................ vi

County Payroll Expenditures Analysis ...................................................................................................... vii

County General Fund Analysis ................................................................................................................. viii

County Highway Fund Analysis ................................................................................................................. ix

FINANCIAL SECTION

Report of State Auditor and Inspector .......................................................................................................... 1

Financial Statement:

Statement of Receipts, Disbursements, and Changes in Cash Balances—Regulatory Basis

(with Combining Information)—Major Funds ....................................................................................... 3

Notes to the Financial Statement ............................................................................................................ 4

OTHER SUPPLEMENTARY INFORMATION

Comparative Schedule of Receipts, Expenditures, and Changes in

Cash Balances—Budget and Actual—Budgetary Basis—General Fund ............................................. 10

Comparative Schedule of Receipts, Expenditures, and Changes in

Cash Balances—Budget and Actual—Budgetary Basis—County Health Department Fund .............. 11

Combining Statement of Receipts, Disbursements, and Changes in

Cash Balances—Regulatory Basis—Remaining Aggregate Funds ..................................................... 12

Notes to Other Supplementary Information ......................................................................................... 13

Schedule of Expenditures of Federal Awards ...................................................................................... 15

Note to the Schedule of Expenditures of Federal Awards .................................................................... 16

HASKELL COUNTY, OKLAHOMA

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

ii

INTERNAL CONTROL AND COMPLIANCE SECTION

Report on Internal Control Over Financial Reporting and on Compliance and Other Matters

Based on an Audit of Financial Statements Performed in Accordance With

Government Auditing Standards ................................................................................................................. 17

Independent Auditor's Report on Compliance With Requirements That Could Have a Direct

and Material Effect on Each Major Program and Internal Control Over Compliance in

Accordance With OMB Circular A-133 ..................................................................................................... 19

Schedule of Findings and Questioned Costs ............................................................................................... 21

Schedule of Prior Year Findings and Questioned Costs ............................................................................. 47

INTRODUCTORY SECTION

UNAUDITED INFORMATION ON PAGES iii -ix

PRESENTED FOR INFORMATIONAL PURPOSES ONLY

HASKELL COUNTY, OKLAHOMA

STATISTICAL INFORMATION

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

iii

Located in eastern Oklahoma, Haskell County was created at statehood and named for Charles N.

Haskell, a member of the Oklahoma Constitutional Convention and first governor of Oklahoma.

Haskell County was one of the first permanent Choctaw settlements in the Indian Territory. Many

Choctaws arrived by steamboat at Tamaha, and settled there along the Arkansas River. Haskell County

was also the site of several skirmishes during the Civil War. The county seat is located at Stigler. Belle

Starr, the bandit queen, frequented the area during the late 1800’s. She was reportedly killed near

present-day Hoyt.

There is an in-county transit system. Local industries include meat packing, milling, and trucking.

Recreational opportunities may be found at the Robert S. Kerr Lake, Sequoyah Wildlife Refuge and the

Haskell County Recreational Club. Annual events include Reunion Days during the third week in June,

the Christmas Parade on the first Saturday in December, and the Antique Car Show during late October.

Haskell County History: Indian Territory through 1988 is available from the Haskell County Historical

Society. For more information, call the county clerk’s office at 918-967-2884.

County Seat – Stigler Area – 625.27 Square Miles

County Population – 12,393

(2009 est.)

Farms –914 Land in Farms – 290,260 Acres

Primary Source: Oklahoma Almanac 2011-2012

HASKELL COUNTY OFFICIALS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

iv

Board of County Commissioners

District 1 – Kenny Short

District 2 – Mitch Worsham

District 3 – Paul Storie

County Assessor

Roger Ballard

County Clerk

Gail Brown

County Sheriff

Brian Hale

County Treasurer

Gale Dixon

Court Clerk

Robin Rea

District Attorney

Farley Ward

HASKELL COUNTY, OKLAHOMA

AD VALOREM TAX DISTRIBUTION

SHARE OF THE AVERAGE MILLAGE

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

v

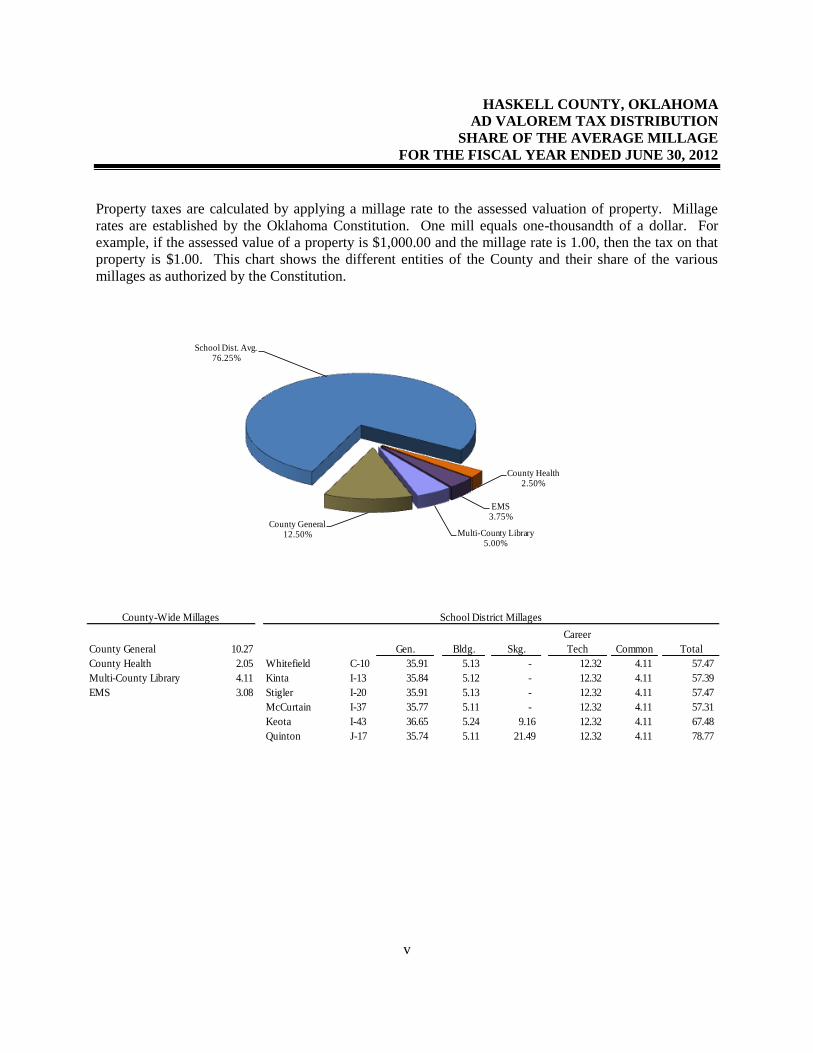

Property taxes are calculated by applying a millage rate to the assessed valuation of property. Millage

rates are established by the Oklahoma Constitution. One mill equals one-thousandth of a dollar. For

example, if the assessed value of a property is $1,000.00 and the millage rate is 1.00, then the tax on that

property is $1.00. This chart shows the different entities of the County and their share of the various

millages as authorized by the Constitution.

County General12.50%

School Dist. Avg.76.25%

County Health2.50%

EMS3.75%

Multi-County Library5.00%

County General 10.27 Gen. Bldg. Skg.

Career

Tech Common Total

County Health 2.05 Whitefield C-10 35.91 5.13 - 12.32 4.11 57.47

Multi-County Library 4.11 Kinta I-13 35.84 5.12 - 12.32 4.11 57.39

EMS 3.08 Stigler I-20 35.91 5.13 - 12.32 4.11 57.47

McCurtain I-37 35.77 5.11 - 12.32 4.11 57.31

Keota I-43 36.65 5.24 9.16 12.32 4.11 67.48

Quinton J-17 35.74 5.11 21.49 12.32 4.11 78.77

County-Wide Millages School District Millages

HASKELL COUNTY, OKLAHOMA

ASSESSED VALUE OF PROPERTY

TREND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

vi

Valuation

Date Personal

Public

Service

Real

Estate

Homestead

Exemption Net Value

Estimated

Fair Market

Value

1/1/2011 $12,596,505 $9,189,470 $35,337,133 $3,784,093 $53,339,015 $475,976,844

1/1/2010 $13,157,125 $10,569,856 $34,229,615 $3,752,170 $54,204,426 $477,046,121

1/1/2009 $13,295,747 $10,169,409 $33,499,270 $3,761,435 $53,202,991 $469,914,318

1/1/2008 $13,383,675 $9,839,566 $31,065,050 $3,670,620 $50,617,671 $447,140,876

1/1/2007 $14,120,230 $10,641,570 $29,001,935 $3,644,420 $50,119,315 $438,591,104

$438,591,104

$447,140,876

$469,914,318

$477,046,121 $475,976,844

$410,000,000

$420,000,000

$430,000,000

$440,000,000

$450,000,000

$460,000,000

$470,000,000

$480,000,000

1/1/2007 1/1/2008 1/1/2009 1/1/2010 1/1/2011

EstimatedFair Market

Value

HASKELL COUNTY, OKLAHOMA

COUNTY PAYROLL EXPENDITURES ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

vii

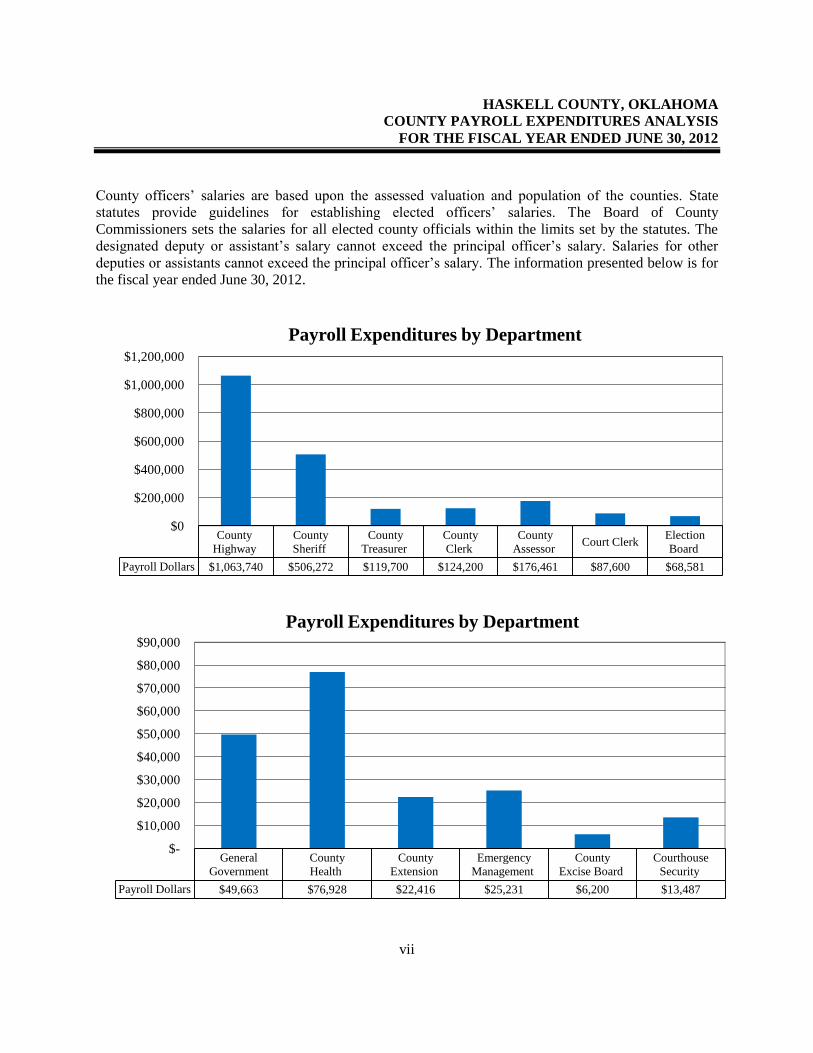

County officers’ salaries are based upon the assessed valuation and population of the counties. State

statutes provide guidelines for establishing elected officers’ salaries. The Board of County

Commissioners sets the salaries for all elected county officials within the limits set by the statutes. The

designated deputy or assistant’s salary cannot exceed the principal officer’s salary. Salaries for other

deputies or assistants cannot exceed the principal officer’s salary. The information presented below is for

the fiscal year ended June 30, 2012.

County

Highway

County

Sheriff

County

Treasurer

County

Clerk

County

Assessor Court Clerk

Election

Board

Payroll Dollars $1,063,740 $506,272 $119,700 $124,200 $176,461 $87,600 $68,581

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

Payroll Expenditures by Department

General

Government

County

Health

County

Extension

Emergency

Management

County

Excise Board

Courthouse

Security

Payroll Dollars $49,663 $76,928 $22,416 $25,231 $6,200 $13,487

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

Payroll Expenditures by Department

HASKELL COUNTY, OKLAHOMA

COUNTY GENERAL FUND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

viii

FYE 2008 FYE 2009 FYE 2010 FYE 2011 FYE 2012

Receipts Apportioned $2,116,139 $1,965,063 $1,789,971 $1,879,097 $2,040,058

Disbursements $1,906,896 $2,348,222 $2,228,078 $2,075,197 $1,748,560

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

County General Fund

The Oklahoma Constitution and the Oklahoma Statutes authorize counties to create a County General

Fund, which is the county’s primary source of operating revenue. The County General Fund is typically

used for county employees’ salaries plus many expenses for county maintenance and operation. It also

provides revenue for various budget accounts and accounts that support special services and programs.

The Board of County Commissioners must review and approve all expenditures made from the County

General Fund. The primary revenue source for the County General Fund is usually the county’s ad

valorem tax collected on real, personal (if applicable), and public service property. Smaller amounts of

revenue can come from other sources such as fees, sales tax, use tax, state transfer payments, in-lieu

taxes, and reimbursements. The chart below summarizes receipts and disbursements of the County’s

General Fund for the last five fiscal years.

HASKELL COUNTY, OKLAHOMA

COUNTY HIGHWAY FUND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

ix

FYE 2008 FYE 2009 FYE 2010 FYE 2011 FYE 2012

Receipts Apportioned $4,172,440 $4,440,200 $2,846,945 $3,296,546 $2,712,431

Disbursements $3,885,918 $3,911,126 $3,560,137 $2,990,118 $3,126,776

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

County Highway Fund

The County receives major funding for roads and highways from a state imposed fuel tax. Taxes are

collected by the Oklahoma Tax Commission. Taxes are imposed on all gasoline, diesel, and special fuel

sales statewide. The County’s share is determined on formulas based on the County population, road

miles, and land area and is remitted to the County monthly. These funds are earmarked for roads and

highways only and are accounted for in the County Highway Fund. The chart below summarizes receipts

and disbursements of the County’s Highway Fund for the last five fiscal years.

FINANCIAL SECTION

Independent Auditor’s Report

TO THE OFFICERS OF

HASKELL COUNTY, OKLAHOMA

We have audited the combined total—all county funds on the accompanying regulatory basis Statement

of Receipts, Disbursements, and Changes in Cash Balances of Haskell County, Oklahoma, as of and for

the year ended June 30, 2012, listed in the table of contents as the financial statement. This financial

statement is the responsibility of Haskell County’s management. Our responsibility is to express an

opinion on the combined total—all county funds on this financial statement based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of

America and the standards applicable to financial audits contained in Government Auditing Standards,

issued by the Comptroller General of the United States. Those standards require that we plan and perform

the audit to obtain reasonable assurance about whether the financial statement is free of material

misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statement. An audit also includes assessing the accounting principles used and

significant estimates made by management, as well as evaluating the overall financial statement

presentation. We believe that our audit provides a reasonable basis for our opinion.

As described in Note 1, this financial statement was prepared using accounting practices prescribed or

permitted by Oklahoma state law, which practices differ from accounting principles generally accepted in

the United States of America. The differences between this regulatory basis of accounting and accounting

principles generally accepted in the United States of America are also described in Note 1.

In our opinion, because of the effects of the matter discussed in the preceding paragraph, the financial

statement referred to above does not present fairly, in conformity with accounting principles generally

accepted in the United States of America, the financial position of Haskell County as of June 30, 2012, or

changes in its financial position for the year then ended.

In our opinion, the financial statement referred to above presents fairly, in all material respects, the

combined total of receipts, disbursements, and changes in cash balances for all county funds of Haskell

County, for the year ended June 30, 2012, on the basis of accounting described in Note 1.

In accordance with Government Auditing Standards, we have also issued our report dated July 30, 2014,

on our consideration of Haskell County’s internal control over financial reporting and on our tests of its

compliance with certain provisions of laws, regulations, contracts, and grant agreements and other

matters. The purpose of that report is to describe the scope of our testing of internal control over financial

reporting and compliance and the results of that testing, and not to provide an opinion on the internal

control over financial reporting or on compliance. That report is an integral part of an audit performed in

accordance with Government Auditing Standards and should be considered in assessing the results of our

audit.

2

Our audit was conducted for the purpose of forming an opinion on the combined total of all county funds

on the financial statement. The accompanying schedule of expenditures of federal awards is presented for

purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133,

Audits of States, Local Governments, and Non-Profit Organizations, and is not a required part of the

financial statement. The remaining Other Supplementary Information, as listed in the table of contents, is

presented for purposes of additional analysis, and is not a required part of the financial statement. Such

supplementary information has been subjected to the auditing procedures applied in the audit of the

combined total—all county funds on the regulatory basis Statement of Receipts, Disbursements and

Changes in Cash Balances and, in our opinion, is fairly stated, in all material respects, in relation to the

combined total—all county funds. The information listed in the table of contents under Introductory

Section has not been audited by us, and accordingly, we express no opinion on it.

GARY A. JONES, CPA, CFE OKLAHOMA STATE AUDITOR & INSPECTOR

July 30, 2014

REGULATORY BASIS FINANCIAL STATEMENT

HASKELL COUNTY, OKLAHOMA

STATEMENT OF RECEIPTS, DISBURSEMENTS, AND

CHANGES IN CASH BALANCES—REGULATORY BASIS

(WITH COMBINING INFORMATION)—MAJOR FUNDS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

The notes to the financial statement are an integral part of this statement.

3

Beginning Ending

Cash Balances Receipts Transfers Transfers Cash Balances

July 1, 2011 Apportioned In Out Disbursements June 30, 2012

Combining Information:

Major Funds:

County General Fund 361,527$ 2,040,058$ -$ -$ 1,748,560$ 653,025$

Gross Revenue - Operations and Expenses 78,465 12,166 - - 500 90,131

Gross Revenue - Bond 4 444,932 - - 444,932 4

T-Highway 1,075,339 2,712,431 246,000 - 3,126,776 906,994

T-Highway Road and Bridge - - 221,273 - 221,273 -

Resale Property 107,814 35,911 - - 20,684 123,041

County Health Department 138,914 166,429 - - 155,442 149,901

Sheriff County Jail Fund 171,259 356,254 - - 400,466 127,047

Sinking Fund 4,884 10 - - - 4,894

Hospital Sales Tax 54,448 - - - - 54,448

Hazard Mitigation 12,750 12,750 - - 25,500 -

County Road & Bridge Improvement Fund 582,457 368,993 - 366,000 59,652 525,798

Fire Department Sales Tax Fund - 192,747 - - 30,720 162,027

Remaining Aggregate Funds 278,535 171,437 - - 180,382 269,590

Combined Total - All County Funds 2,866,396$ 6,514,118$ 467,273$ 366,000$ 6,414,887$ 3,066,900$

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

4

1. Summary of Significant Accounting Policies

A. Reporting Entity

Haskell County is a subdivision of the State of Oklahoma created by the Oklahoma Constitution

and regulated by Oklahoma Statutes.

The accompanying financial statement presents the receipts, disbursements, and changes in cash

balances of the total of all funds under the control of the primary government. The general fund

is the county’s general operating fund, accounting for all financial resources except those required

to be accounted for in another fund, where its use is restricted for a specified purpose. Other

funds established by statute and under the control of the primary government are also presented.

The County Treasurer collects and remits material amounts of intergovernmental revenues and ad

valorem tax revenue for other budgetary entities, including emergency medical districts, libraries,

school districts, and cities and towns. The cash receipts and disbursements attributable to those

other entities do not appear in funds on the County’s financial statement; those funds play no part

in the County’s operations. Any trust or agency funds maintained by the County are not included

in this presentation.

B. Fund Accounting

The County uses funds to report on receipts, disbursements, and changes in cash balances. Fund

accounting is designed to demonstrate legal compliance and to aid financial management by

segregating transactions related to certain government functions or activities.

Following are descriptions of the county funds included as combining information within the

financial statement:

County General Fund – revenues are from ad valorem taxes, officer’s fees, sales tax, interest

earnings, and miscellaneous collections of the County. Disbursements are for the general

operations of the County.

Gross Revenue - Operations and Expenses – accounts for sales tax revenue and the

disbursement of funds as restricted by the sales tax resolution for the criminal justice facility.

Gross Revenue - Bond – accounts for sales tax revenue and the disbursement of funds as

restricted by the sales tax resolution for the criminal justice facility.

T-Highway – accounts for state, local, and miscellaneous receipts and disbursements for the

purpose of constructing and maintaining county roads and bridges.

T-Highway Road and Bridge – accounts for monies received from the Oklahoma Department

of Transportation and reflects activity related to the Circuit Engineering Districts’ Emergency

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

5

and Transportation Revolving Fund loan and disbursements for the purpose of constructing

and maintaining county roads and bridges.

Resale Property – accounts for the collection of interest and penalties on delinquent taxes and

the disposition of the same as restricted by statute.

County Health Department – accounts for monies collected on behalf of the county health

department from ad valorem taxes and state and local revenues. Disbursements are for the

operation of the county health department.

Sheriff County Jail Fund – accounts for monies received for housing prisoners to be used for

jail operating expenses.

Sinking Fund – accounts for debt service receipts derived generally from a special ad valorem

tax levy and from interest earned on investments of cash not immediately required for debt

service payments.

Hospital Sales Tax – accounts for the collection of the sales tax and disbursement of funds

used for general operations of the county hospital.

Hazard Mitigation – accounts for grant funds received from the Federal Emergency

Management Agency. Disbursements are made the county hazard mitigation plan.

County Road & Bridge Improvement Fund – accounts for monies collected through the

Oklahoma Tax Commission for the purpose of bridge repair and road resurfacing.

Fire Department Sales Tax Fund – accounts for the collection of sales tax revenue and the

disbursement of funds for the operation of the fire departments.

C. Basis of Accounting

The financial statement is prepared on a basis of accounting wherein amounts are recognized

when received or disbursed. This basis of accounting differs from accounting principles

generally accepted in the United States of America, which require revenues to be recognized

when they become available and measurable or when they are earned, and expenditures or

expenses to be recognized when the related liabilities are incurred. This regulatory basis financial

presentation is not a comprehensive measure of economic condition or changes therein.

Title 19 O.S. § 171 specifies the format and presentation for Oklahoma counties to present their

financial statement in accordance with accounting principles generally accepted in the United

States of America (U.S. GAAP) or on a regulatory basis. The County has elected to present their

financial statement on a regulatory basis in conformity with Title 19 O.S. § 171. County

governments (primary only) are required to present their financial statements on a fund basis

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

6

format with, at a minimum, the general fund and all other county funds, which represent ten

percent or greater of total county revenue. All other funds included in the audit shall be presented

in the aggregate in a combining statement.

D. Budget

Under current Oklahoma Statutes, a general fund and a county health department fund are the

only funds required to adopt a formal budget. On or before the first Monday in July of each year,

each officer or department head submits an estimate of needs to the governing body. The budget

is approved for the respective fund by office, or department and object. The County Board of

Commissioners may approve changes of appropriations within the fund by office or department

and object. To increase or decrease the budget by fund requires approval by the County Excise

Board.

E. Cash and Investments

For the purposes of financial reporting, “Ending Cash Balances, June 30” includes cash and cash

equivalents and investments as allowed by statutes. The County pools the cash of its various

funds in maintaining its bank accounts. However, cash applicable to a particular fund is readily

identifiable on the County’s books. The balance in the pooled cash accounts is available to meet

current operating requirements.

State statutes require financial institutions with which the County maintains funds to deposit

collateral securities to secure the County’s deposits. The amount of collateral securities to be

pledged is established by the County Treasurer; this amount must be at least the amount of the

deposit to be secured, less the amount insured (by, for example, the FDIC).

The County Treasurer has been authorized by the County’s governing board to make investments.

Allowable investments are outlined in statutes 62 O.S. § 348.1 and § 348.3.

All investments must be backed by the full faith and credit of the United States Government, the

Oklahoma State Government, fully collateralized, or fully insured. All investments as classified

by state statute are nonnegotiable certificates of deposit. Nonnegotiable certificates of deposit are

not subject to interest rate risk or credit risk.

2. Ad Valorem Tax

The County's property tax is levied each October 1 on the assessed value listed as of January 1 of

the same year for all real and personal property located in the County, except certain exempt

property. Assessed values are established by the County Assessor within the prescribed

guidelines established by the Oklahoma Tax Commission and the State Equalization Board. Title

68 O.S. § 2820.A. states, ". . . Each assessor shall thereafter maintain an active and systematic

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

7

program of visual inspection on a continuous basis and shall establish an inspection schedule

which will result in the individual visual inspection of all taxable property within the county at

least once each four (4) years."

Taxes are due on November 1 following the levy date, although they may be paid in two equal

installments. If the first half is paid prior to January 1, the second half is not delinquent until

April 1. Unpaid real property taxes become a lien upon said property on October 1 of each year.

3. Other Information

A. Pension Plan

Plan Description. The County contributes to the Oklahoma Public Employees Retirement Plan

(the Plan), a cost-sharing, multiple-employer defined benefit pension plan administered by the

Oklahoma Public Employees Retirement System (OPERS). Benefit provisions are established

and amended by the Oklahoma Legislature. The Plan provides retirement, disability, and death

benefits to Plan members and beneficiaries. Title 74, Sections 901 through 943, as amended,

establishes the provisions of the Plan. OPERS issues a publicly available financial report that

includes financial statements and supplementary information. That report may be obtained by

writing OPERS, P.O. Box 53007, Oklahoma City, Oklahoma 73105 or by calling 1-800-733-

9008.

Funding Policy. The contribution rates for each member category are established by the

Oklahoma Legislature and are based on an actuarial calculation which is performed to determine

the adequacy of contribution rates.

B. Other Post Employment Benefits (OPEB)

In addition to the pension benefits described in the Pension Plan note, OPERS provides post-

retirement health care benefits of up to $105 each for retirees who are members of an eligible

group plan. These benefits are funded on a pay-as-you-go basis as part of the overall retirement

benefit. OPEB expenditure and participant information is available for the state as a whole;

however, information specific to the County is not available nor can it be reasonably estimated.

C. Contingent Liabilities

Amounts received or receivable from grantor agencies are subject to audit and adjustment by

grantor agencies, primarily the federal government. Any disallowed claims, including amounts

already collected, may constitute a liability of the applicable fund. The amount, if any, of

expenditures which may be disallowed by the grantor cannot be determined at this time; although,

the County expects such amounts, if any, to be immaterial.

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

8

As of the end of the fiscal year, there were no claims or judgments that would have a material

adverse effect on the financial condition of the County; however, the outcome of any lawsuit

would not be determinable.

D. Sales Tax

The voters of Haskell County approved a permanent one percent (1%) sales tax effective March

1, 1984. One hundred percent (100%) of the sales tax proceeds are to be used for general

government. These funds are accounted for the County General Fund.

The voters of Haskell County approved a one-half percent (1/2%) sales tax effective April 1,

2005. This sales tax will expire April 1, 2035. This sales tax was established to provide revenue

for the City of Stigler Hospital Authority for renovation and expansion of the hospital and

purchase of capital equipment, fixtures, and furnishings necessary to support the expansion.

These funds are accounted for in the Hospital Sales Tax Fund.

The voters of Haskell County approved a one-half percent (1/2%) percent sales tax effective April

1, 2006. This tax will terminate after 25 years from the effective date of the tax or at the date of

retirement of any debt incurred related thereto, whichever is earlier. The sales tax was established

for the acquisition, remodeling, construction, financing, furnishing, and equipping of a new

county jail and criminal justice facility to be located in Haskell County, parking lots, streets and

other capital facilities associated therein, including design, construction, capital improvements,

expenses, operations, equipment, fixtures and furnishings; with one-fourth (1/4) of one-half (1/2)

cent to provide for the maintenance and operations of said facilities. These funds are accounted

for in the Gross Revenue - Operations and Expenses, and the Gross Revenue - Bond funds.

The voters of Haskell County approved a permanent one quarter (1/4%) sales tax effective July

11, 2011. The sales tax was established for the purpose of providing funding for the fire

departments in the following communities: Brooken, Hoyt, Keota, Kinta, LeQuire, Lona Valley,

McCurtain, Southside, Stigler, Tamaha, Whitefield or others herein established, for such fire

protection as may be deemed necessary. These funds are accounted for in the Fire Department

Sales Tax Fund.

E. Interfund Transfers

During the fiscal year, the County made the following transfers between cash funds:

The County transferred $246,000 from the County Road & Bridge Improvement Fund to

the T-Highway fund to reimburse for expenditures on bridge and road projects in the

County.

The County transferred $221,273 from the T-Highway Road and Bridge Emergency

Transportation Revolving Fund, a trust and agency fund, to the T-Highway Road and

Bridge to reimburse for expenditures on bridge and road projects in the County.

HASKELL COUNTY, OKLAHOMA

NOTES TO THE FINANCIAL STATEMENT

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

9

The County transferred $120,000 from the County Road & Bridge Improvement Fund to

the County Bridge Fund (CBRI) T & A, a trust and agency fund, for the repayment of

loans.

OTHER SUPPLEMENTARY INFORMATION

HASKELL COUNTY, OKLAHOMA

COMPARATIVE SCHEDULE OF RECEIPTS, EXPENDITURES, AND

CHANGES IN CASH BALANCES—BUDGET AND ACTUAL—BUDGETARY BASIS—

GENERAL FUND

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

10

Budget Actual Variance

Beginning Cash Balances 361,527$ 361,527$ -$

Less: Prior Year Outstanding Warrants (96,930) (96,930) -

Less: Prior Year Encumbrances (14,717) (14,480) 237

Beginning Cash Balances, Budgetary Basis 249,880 250,117 237

Receipts:

Ad Valorem Taxes 506,072 558,710 52,638

Charges for Services 46,250 49,558 3,308

Intergovernmental Revenues 1,008,750 1,223,543 214,793

Miscellaneous Revenues 161,913 208,247 46,334

Total Receipts, Budgetary Basis 1,722,985 2,040,058 317,073

Expenditures:

County Sheriff 197,679 197,640 39

County Treasurer 131,586 131,586 -

OSU Extension 43,123 40,830 2,293

County Clerk 129,785 128,309 1,476

Court Clerk 97,193 92,400 4,793

County Assessor 83,310 82,828 482

Revaluation 163,268 159,067 4,201

General Government 874,227 638,462 235,765

Excise Board 9,500 8,275 1,225

County Election Board 82,187 81,828 359

Sheriff Jail 101,935 101,232 703

County Audit Budget 10,741 - 10,741

Emergency Management 48,331 40,813 7,518

Total Expenditures, Budgetary Basis 1,972,865 1,703,270 269,595

Excess of Receipts and Beginning Cash

Balances Over Expenditures, Budgetary Basis -$ 586,905 586,905$

Reconciliation to Statement of Receipts,

Disbursements, and Changes in Cash Balances

Add: Current Year Outstanding Warrants 60,011

Add: Current Year Encumbrances 6,109

Ending Cash Balance 653,025$

General Fund

HASKELL COUNTY, OKLAHOMA

COMPARATIVE SCHEDULE OF RECEIPTS, EXPENDITURES, AND

CHANGES IN CASH BALANCES—BUDGET AND ACTUAL—BUDGETARY BASIS—

COUNTY HEALTH DEPARTMENT FUND

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

11

Budget Actual Variance

Beginning Cash Balances 138,914$ 138,914$ -$

Less: Prior Year Outstanding Warrants (3,178) (3,178) -

Less: Prior Year Encumbrances (9,229) (9,169) 60

Beginning Cash Balances, Budgetary Basis 126,507 126,567 60

Receipts:

Ad Valorem Taxes 101,017 111,524 10,507

Charges for Services 56,241 53,736 (2,505)

Miscellaneous Revenues - 1,169 1,169

Total Receipts, Budgetary Basis 157,258 166,429 9,171

Expenditures:

Health and Welfare 283,765 159,857 123,908

Total Expenditures, Budgetary Basis 283,765 159,857 123,908

Excess of Receipts and Beginning Cash

Balances Over Expenditures,

Budgetary Basis -$ 133,139 133,139$

Reconciliation to Statement of Receipts,

Disbursements, and Changes in Cash Balances

Add: Current Year Encumbrances 662

Add: Current Year Outstanding Warrants 16,100

Ending Cash Balance 149,901$

County Health Department Fund

HASKELL COUNTY, OKLAHOMA

COMBINING STATEMENT OF RECEIPTS, DISBURSEMENTS, AND

CHANGES IN CASH BALANCES—REGULATORY BASIS—

REMAINING AGGREGATE FUNDS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

12

Beginning Ending

Cash Balances Receipts Cash Balances

July 1, 2011 Apportioned Disbursements June 30, 2012

Remaining Aggregate Funds:

Assessor Visual Inspection 3,305$ 27$ 40$ 3,292$

County Clerk Lien Fees 10,278 8,064 16,230 2,112

Sheriff Service Fees 98,748 112,648 68,811 142,585

Mortgage Fees 14,406 1,855 - 16,261

Sheriff Donations 16,692 8,336 - 25,028

Lake Patrol 47,754 14,946 43,672 19,028

Community Service Sentencing Program Revolving 309 - - 309

Drug Fund 2,190 18 - 2,208

County Assessor Fees 21,272 3,675 1,874 23,073

County Clerk RM&P Revolving 40,783 15,105 21,739 34,149

Civil Defense Donation 155 200 - 355

Courthouse Security 22,643 6,563 28,016 1,190

Combined Total - Remaining Aggregate Funds 278,535$ 171,437$ 180,382$ 269,590$

HASKELL COUNTY, OKLAHOMA

NOTES TO OTHER SUPPLEMENTARY INFORMATION

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

13

1. Budgetary Schedules

The Comparative Schedules of Receipts, Expenditures, and Changes in Cash Balances—Budget

and Actual—Budgetary Basis for the General Fund and the County Health Department Fund

present comparisons of the legally adopted budget with actual data. The "actual" data, as

presented in the comparison of budget and actual, will differ from the data as presented in the

Combined Statement of Receipts, Disbursements, and Changes in Cash Balances with Combining

Information because of adopting certain aspects of the budgetary basis of accounting and the

adjusting of encumbrances and outstanding warrants to their related budget year.

Encumbrance accounting, under which purchase orders, contracts, and other commitments for the

expenditure of monies are recorded in order to reserve that portion of the applicable

appropriation, is employed as an extension of formal budgetary integration in these funds. At the

end of the year unencumbered appropriations lapse.

2. Remaining County Funds

Remaining aggregate funds as presented on the financial statement are as follows:

Assessor Visual Inspection – accounts for the collection and expenditure of monies by the

Assessor as restricted by state statute for the visual inspection program.

County Clerk Lien Fees – accounts for lien collections and disbursements as restricted by

statute.

Sheriff Service Fees – accounts for the collection and disbursement of sheriff process service

fees as restricted by statute.

Mortgage Fees – accounts for the collection of fees by the Treasurer for mortgage tax

certificates and the disbursement of funds as restricted by statute.

Sheriff Donations – accounts for donations from citizens made to the Sheriff’s Department

for the operation of the office.

Lake Patrol – accounts for monies received from the Corps of Engineers for patrolling

services.

Community Service Sentencing Program Revolving – accounts for the collection of funding

through the State Department of Corrections for administrative expenses and supervision of

offenders.

Drug Fund – accounts for local contributions, grants, or drug forfeitures and is used for

payments for confidential informants or purchases of illegal drugs in sting operations.

HASKELL COUNTY, OKLAHOMA

NOTES TO OTHER SUPPLEMENTARY INFORMATION

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

14

County Assessor Fees – accounts for the collection of fees for copies and disbursed as

restricted by state statute.

County Clerk RM&P Revolving – accounts for fees collected for instruments filed in the

County Clerk’s office as restricted by statute for preservation of records.

Civil Defense Donation – accounts for the receipt and disbursement of funds donated for civil

defense purposes.

Courthouse Security – accounts for monies allocated from the Court Fund for programs and

services related to Courtroom/Judicial Security.

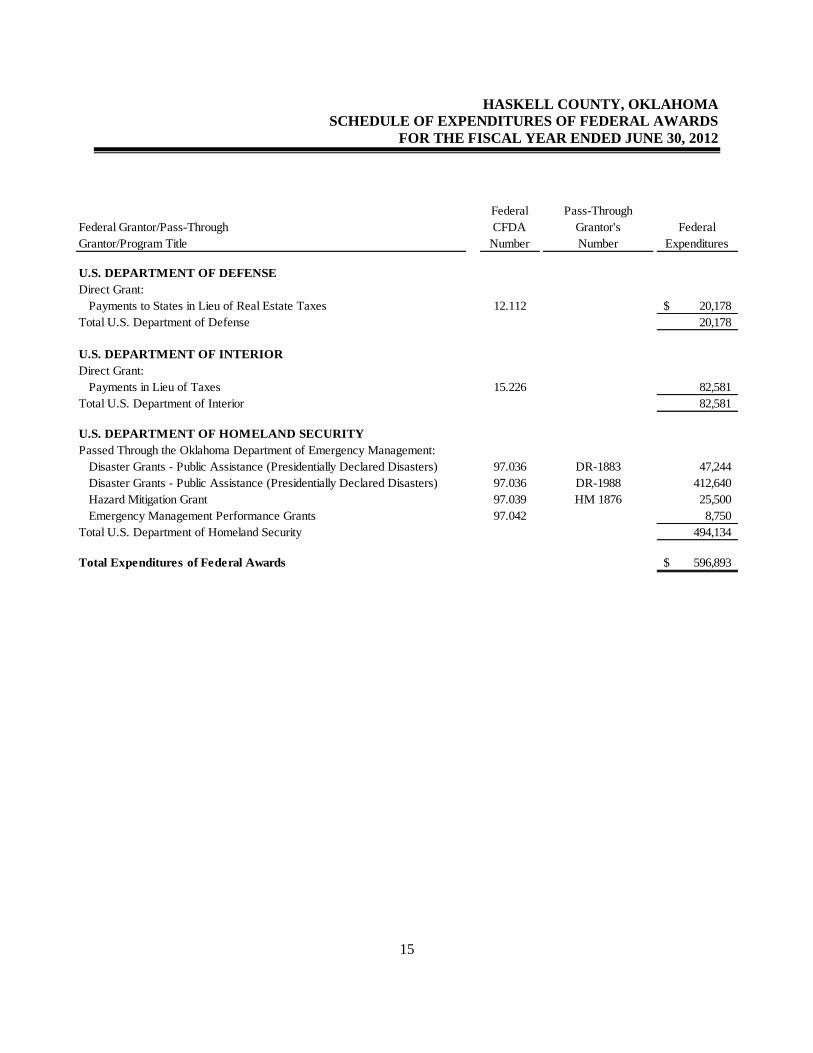

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

15

Federal Grantor/Pass-Through

Grantor/Program Title

Federal

CFDA

Number

Pass-Through

Grantor's

Number

Federal

Expenditures

U.S. DEPARTMENT OF DEFENSE

Direct Grant:

Payments to States in Lieu of Real Estate Taxes 12.112 20,178$

Total U.S. Department of Defense 20,178

U.S. DEPARTMENT OF INTERIOR

Direct Grant:

Payments in Lieu of Taxes 15.226 82,581

Total U.S. Department of Interior 82,581

U.S. DEPARTMENT OF HOMELAND SECURITY

Passed Through the Oklahoma Department of Emergency Management:

Disaster Grants - Public Assistance (Presidentially Declared Disasters) 97.036 DR-1883 47,244

Disaster Grants - Public Assistance (Presidentially Declared Disasters) 97.036 DR-1988 412,640

Hazard Mitigation Grant 97.039 HM 1876 25,500

Emergency Management Performance Grants 97.042 8,750

Total U.S. Department of Homeland Security 494,134

Total Expenditures of Federal Awards 596,893$

HASKELL COUNTY, OKLAHOMA

NOTE TO THE SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

16

Basis of Presentation

The schedule of expenditures of federal awards includes the federal grant activity of Haskell County, and

is presented on the cash basis of accounting. The information in this schedule is presented in accordance

with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit

Organizations.

INTERNAL CONTROL AND COMPLIANCE SECTION

Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based

on an Audit of Financial Statements Performed in Accordance With

Government Auditing Standards

TO THE OFFICERS OF

HASKELL COUNTY, OKLAHOMA

We have audited the combined totals—all funds of the accompanying Combined Statement of Receipts,

Disbursements, and Changes in Cash Balances of Haskell County, Oklahoma, as of and for the year

ended June 30, 2012, which comprises Haskell County’s basic financial statement, prepared using

accounting practices prescribed or permitted by Oklahoma state law, and have issued our report thereon

dated July 30, 2014. Our report on the basic financial statement was adverse because the statement is not

a presentation in conformity with accounting principles generally accepted in the United States of

America. However, our report also included our opinion that the financial statement does present fairly, in

all material respects, the receipts, disbursements, and changes in cash balances – regulatory basis of the

County for the year ended June 30, 2012, on the basis of accounting prescribed by Oklahoma state law,

described in Note 1. We conducted our audit in accordance with auditing standards generally accepted in

the United States of America and the standards applicable to financial audits contained in Government

Auditing Standards, issued by the Comptroller General of the United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered Haskell County’s internal control over financial

reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the

financial statement, but not for the purpose of expressing an opinion on the effectiveness of the County’s

internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness

of Haskell County’s internal control over financial reporting.

Our consideration of internal control over financial reporting was for the limited purpose described in the

preceding paragraph and was not designed to identify all deficiencies in internal control over financial

reporting that might be significant deficiencies or material weaknesses, and therefore, there can be no

assurance that all deficiencies, significant deficiencies, or material weaknesses have been identified.

However, as described in the accompanying schedule of findings and questioned costs, we identified

certain deficiencies in internal control over financial reporting that we consider to be material weaknesses

and other deficiencies that we consider to be significant deficiencies.

A deficiency in internal control exists when the design or operation of a control does not allow

management or employees, in the normal course of performing their assigned functions, to prevent, or

detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of

deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of

the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. We

consider the deficiencies in internal control described in the accompanying schedule of findings and

questioned costs to be material weaknesses in internal control over financial reporting. 2012-1, 2012-2,

2012-5, 2012-8, 2012-12, and 2012-13.

18

A significant deficiency is a deficiency, or combination of deficiencies, in internal control that is less

severe than a material weakness, yet important enough to merit attention by those charged with

governance. We consider the deficiencies in internal control described in the accompanying schedule of

findings and questioned costs to be significant deficiencies in internal control over financial reporting.

2012-3, 2012-10, 2012-17, and 2012-31.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Haskell County’s financial statement is free of

material misstatement, we performed tests of its compliance with certain provisions of laws, regulations,

contracts, and grant agreements, noncompliance with which could have a direct and material effect on the

determination of financial statement amounts. However, providing an opinion on compliance with those

provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The

results of our tests disclosed instances of noncompliance or other matters that are required to be reported

under Government Auditing Standards and which are described in the accompanying schedule of findings

and questioned costs as items 2012-8, 2012-17, and 2012-31.

We noted certain matters that we reported to the management of Haskell County, which are included in

Section 4 of the schedule of findings and questioned costs contained in this report.

Haskell County’s responses to the findings identified in our audit are described in the accompanying

schedule of findings and questioned costs. We did not audit Haskell County’s responses and,

accordingly, we express no opinion on the responses.

This report is intended solely for the information and use of management, those charged with governance,

others within the entity, and is not intended to be and should not be used by anyone other than the

specified parties. This report is also a public document pursuant to the Oklahoma Open Records Act (51

O.S. § 24A.1 et seq.), and shall be open to any person for inspection and copying.

GARY A. JONES, CPA, CFE OKLAHOMA STATE AUDITOR & INSPECTOR

July 30, 2014

Independent Auditors Report on Compliance with Requirements That Could Have a Direct and

Material Effect on Each Major Program

and Internal Control Over Compliance in Accordance With

OMB Circular A-133

TO THE OFFICERS OF

HASKELL COUNTY, OKLAHOMA

Compliance

We have audited the compliance of Haskell County, Oklahoma, with the types of compliance

requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133

Compliance Supplement that could have a direct and material effect on Haskell County’s major federal

program for the year ended June 30, 2012. Haskell County’s major federal program is identified in the

summary of auditor’s results section of the accompanying schedule of findings and questioned costs.

Compliance with the requirements of laws, regulations, contracts, and grants applicable to its major

federal program is the responsibility of Haskell County’s management. Our responsibility is to express an

opinion on Haskell County’s compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in the

United States of America; the standards applicable to financial audits contained in Government Auditing

Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of

States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133

require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance

with the types of compliance requirements referred to above that could have a direct and material effect

on a major federal program occurred. An audit includes examining, on a test basis, evidence about

Haskell County’s compliance with those requirements and performing such other procedures as we

considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our

opinion. Our audit does not provide a legal determination of Haskell County’s compliance with those

requirements.

As described in item 2012-30, in the accompanying schedule of findings and questioned costs, Haskell

County did not comply with requirements regarding Allowable Cost/Cost Principles that are applicable to

its Disaster Grants – Public Assistance (97.036). Compliance with such requirements is necessary, in our

opinion, for Haskell County to comply with the requirements applicable to that program.

In our opinion, except for the noncompliance described in the preceding paragraph, the County, complied,

in all material respects, with the requirements referred to above that could have a direct and material

effect on its major federal program for the year ended June 30, 2012.

20

Internal Control Over Compliance

Management of Haskell County is responsible for establishing and maintaining effective internal control

over compliance with the requirements of laws, regulations, contracts, and grants applicable to federal

programs. In planning and performing our audit, we considered Haskell County’s internal control over

compliance with the requirements that could have a direct and material effect on a major federal program

to determine the auditing procedures for the purpose of expressing our opinion on compliance and to test

and report on internal control over compliance in accordance with OMB Circular A-133, but not for the

purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly,

we do not express an opinion on the effectiveness of Haskell County’s internal control over compliance.

Our consideration of internal control over compliance was for the limited purpose described in the

preceding paragraph and was not designed to identify all deficiencies in internal control over compliance

that might be significant deficiencies or material weaknesses and therefore, there can be no assurance that

all deficiencies, significant deficiencies, or material weaknesses have been identified. However, as

discussed below, we identified certain deficiencies in internal control over compliance that we consider to

be material weaknesses.

A deficiency in internal control over compliance exists when the design or operation of a control over

compliance does not allow management or employees, in the normal course of performing their assigned

functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a

federal program on a timely basis. A material weakness in internal control over compliance is a

deficiency, or combination of deficiencies, in internal control over compliance, such that there is a

reasonable possibility that material noncompliance with a type of compliance requirement of a federal

program will not be prevented, or detected and corrected, on a timely basis. We consider the deficiencies

in internal control over compliance described in the accompanying schedule of findings and questioned

costs as items 2012-28, 2012-29, and 2012-30 to be material weaknesses.

Haskell County’s responses to the findings identified in our audit are described in the accompanying

schedule of findings and questioned costs. We did not audit Haskell County’s responses and, accordingly,

we express no opinion on the responses.

This report is intended solely for the information and use of management, those charged with governance,

others within the entity, and is not intended to be and should not be used by anyone other than the

specified parties. This report is also a public document pursuant to the Oklahoma Open Records Act (51

O.S., section 24A.1 et seq.), and shall be open to any person for inspection and copying.

GARY A. JONES, CPA, CFE OKLAHOMA STATE AUDITOR & INSPECTOR

July 30, 2014

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

21

SECTION 1—Summary of Auditor’s Results

Financial Statements

Type of auditor's report issued: ......................Adverse as to GAAP; unqualified as to statutory presentation

Internal control over financial reporting:

Material weakness(es) identified? ................................................................................................ Yes

Significant deficiency(ies) identified? ......................................................................................... Yes

Noncompliance material to financial statements noted? ........................................................................... Yes

Federal Awards

Internal control over major programs:

Material weakness(es) identified? ................................................................................................ Yes

Significant deficiency(ies) identified? ....................................................................... None reported

Type of auditor's report issued on

compliance for major programs: ............................................................................................... Qualified

Any audit findings disclosed that are required to be reported

in accordance with section 510(a) of Circular A-133? ....................................................................... Yes

Identification of Major Programs

CFDA Number(s) Name of Federal Program or Cluster

97.036 Disaster Grants - Public Assistance

(Presidentially Declared Disasters)

Dollar threshold used to distinguish between

Type A and Type B programs: .................................................................................................. $300,000

Auditee qualified as low-risk auditee? ....................................................................................................... No

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

22

SECTION 2—Findings related to the Report on Internal Control Over Financial Reporting and on

Compliance and Other Matters Based on an Audit of Financial Statements Performed in

Accordance With Government Auditing Standards

Finding 2012-1 – Inadequate County-Wide Controls (Repeat Finding)

Condition: County-wide controls regarding Risk Management and Monitoring have not been designed.

Cause of Condition: Procedures have not been designed to address risks of the County.

Effect of Condition: This condition could result in unrecorded transactions, undetected errors, or

misappropriation of funds.

Recommendation: The Oklahoma State Auditor and Inspector’s Office (OSAI) recommends that the

County design procedures to identify and address risks. OSAI also recommends that the County design

monitoring procedures to assess the quality of performance over time. These procedures should be written

policies and procedures and could be included in the County’s policies and procedures handbook.

Examples of risks and procedures to address risk management:

Risks Procedures

Fraudulent activity Segregation of duties

Information lost to computer crashes Daily backups of information

Noncompliance with laws Attend workshops

Natural disasters Written disaster recovery plans

New employee errors Training, attending workshops, monitoring

Examples of activities and procedures to address monitoring:

Monitoring Procedures

Communication between officers Periodic meetings to address items that should be

included in the handbook and to determine if the

County is meeting its goals and objectives.

Annual Financial Statement Review the financial statement of the County for

accuracy and completeness.

Schedule of Expenditures of Federal Awards

(SEFA)

Review the SEFA of the County for accuracy and

to determine all federal awards are presented.

Audit findings Determine audit findings are corrected.

Financial status Periodically review budgeted amounts to actual

amounts and resolve unexplained variances.

Policies and procedures Ensure employees understand expectations in

meeting the goals of the County.

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

23

Monitoring Procedures

Following up on complaints Determine source of complaint and course of

action for resolution.

Estimate of needs Work together to ensure this financial document is

accurate and complete.

Management Response: County Commissioner, District 1: We want to comply with these recommendations and work to design

controls regarding risk management and monitoring.

County Commissioner, District 2: We will work with the other County Officials to assess risks to the

County and monitor county financial activity.

County Commissioner, District 3: We will work with the other Officials to address these conditions.

Criteria: Internal control is an integral component of an organization’s management that provides

reasonable assurance that the objectives of effectiveness and efficiency of operations, reliability of

financial reporting and compliance with laws and regulations are being met. Internal control comprises

the plans, methods, and procedures used to meet missions, goals, and objectives. Internal control also

serves as the first line of defense in safeguarding assets and preventing and detecting errors and fraud.

County management is responsible for designing a county-wide internal control system comprised of

Control Environment, Risk Assessment, Information and Communication, and Monitoring for the

achievement of these goals.

Risk Assessment is a component of internal control which should provide for an assessment of the risks

the County faces from both internal and external sources. Once risks have been identified, they should be

analyzed for their possible effect. Management then has to formulate an approach for risk management

and decide upon the internal control activities required to mitigate those risks and achieve the internal

control objectives of efficient and effective operations, reliable financial reporting, and compliance with

laws and regulations.

Monitoring is a component of internal control which should assess the quality of performance over time

and ensure that the findings of audits and other reviews are promptly resolved. Ongoing monitoring

occurs during normal operations and includes regular management and supervisory activities,

comparisons, reconciliations, and other actions people take in performing their duties. It includes ensuring

that management know their responsibilities for internal control and the need to make control monitoring

part of their regular operating process.

Finding 2012-2 – Disaster Recovery Plan (Repeat Finding)

Condition: Upon inquiry, the following offices do not have a Disaster Recovery Plan:

County Commissioners

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

24

County Treasurer

County Clerk

Cause of Condition: Policies and procedures have not been designed and implemented to prepare a

formal Disaster Recovery Plan.

Effect of Condition: The failure to have a formal Disaster Recovery Plan could result in the County

being unable to function in the event of a disaster. The lack of a formal plan could cause significant

problems in ensuring County business could continue uninterrupted.

Recommendation: OSAI recommends the County Officials develop a Disaster Recovery Plan that

addresses how critical information and systems within their offices would be restored in the event of a

disaster.

Management Response:

County Commissioner, District 1: Chose not to respond.

County Commissioner, District 2: We will work with our Officials and see if we can implement a plan

to protect the County.

County Commissioner, District 3: We will work with our Officials and see if we can implement a plan

to protect the County.

County Treasurer: This is something all County Officers need to discuss together.

County Clerk: We will get in contact with OSU to get a copy of a Disaster Recovery Plan.

Criteria: An important aspect of internal controls is the safeguarding of assets which includes adequate

Disaster Recovery Plans. Internal controls over safeguarding of assets constitute a process, affected by an

entity’s governing body, management, and other personnel, designed to provide reasonable assurance

regarding prevention in a County being unable to function in the event of a disaster.

According to the standards of the Information Systems Audit and Control Association (CobiT Delivery

and Support 4), information services function management should ensure that a written disaster recovery

plan is documented and contains the following:

Guidelines on how to use the recovery plan;

Emergency procedures to ensure the safety of all affected staff members;

Roles and responsibilities of information services function, vendors providing recovery services,

users of services and support administrative personnel;

Listing of systems requiring alternatives (hardware, peripherals, software);

Listing of highest to lowest priority applications, required recovery times and expected

performance norms;

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

25

Various recovery scenarios from minor to loss of total capability and response to each in

sufficient detail for step by step execution;

Training and/or awareness of individual and group roles in continuing plan;

Listing of contracted service providers;

Logistical information on location of key resources, including back-up site for recovery operating

system, applications, data files, operating manuals, and program/system/user documentation;

Current names, addresses, telephone numbers of key personnel; and

Business resumption alternatives for all users for establishing alternative work locations once IT

services are available.

Finding 2012-3 – Inadequate Internal Controls Over Information Systems Security – County

Treasurer and County Clerk (Repeat Finding)

Condition: Upon review of the computer systems within the County Treasurer and the County Clerk’s

office, it was noted that there does not appear to be adequate controls in place to safeguard data from

unauthorized modification, loss, or disclosure. The following was noted:

Passwords are not required to be changed on a quarterly basis in the County Treasurer’s office.

Passwords are shared between users in the County Clerk’s office.

Computers do not lock out users after a period of inactivity in the County Treasurer’s and the

County Clerk’s offices.

The server is not in a secure location in the County Clerk’s office.

Cause of Condition: Policies and procedures have not been designed and implemented to prevent

unauthorized access to data.

Effect of Condition: These conditions could result in compromised security for the computers, computer

programs, and data.

Recommendation: OSAI recommends the County work with IT personnel or in conjunction with

software vendors to setup password requirements for length, character and an expiration of a minimum of

at least every ninety days. In addition, OSAI recommends passwords not be shared and access to servers

be limited.

Management Response:

County Treasurer: I will contact the ad valorem software provider regarding password

recommendations. As of July 1, 2012, my office began using a financial software program; the

passwords for the financial software are set up by the employee and the system automatically logs out of a

period of inactivity.

County Clerk: We will get in contact with our software vendor about changing our computer passwords.

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

26

Criteria: According to the standards of the Information Systems Audit and Control Association (CobiT, Delivery and Support DS5), the need to maintain the integrity of information and protect IT assets requires a security management process. This process includes establishing and maintaining IT security roles and responsibilities, policies, standards, and procedures. Security management also includes performing security monitoring and periodic testing and implementing corrective actions for identified security weaknesses or incidents. Effective security management protects all IT assets to minimize the business impact of security vulnerabilities and incidents.

Finding 2012-5 – Inadequate Segregation of Duties – County Treasurer (Repeat Finding) Condition: A lack of segregation of duties exists in the Treasurer’s office. All employees open mail,

total remittances, write official receipts, receive money, and mail billings. Further, all employees work

out of the same cash drawer. Also, one employee authorizes purchases, prepares claims, approves

payments, and writes and signs vouchers.

Cause of Condition: Internal controls have not been designed regarding segregation of duties.

Effect of Condition: A single person having responsibility for more than one area of recording,

authorization, custody of assets, and execution of transactions could result in unrecorded transactions,

misstated financial reports, clerical errors, or misappropriation of funds not being detected in a timely

manner.

Recommendation: OSAI recommends management be aware of these conditions and realize that

concentration of duties and responsibilities in a limited number of individuals is not desired from a

control point of view. The most effective controls lie in management's knowledge of office operations and

a periodic review of operations. OSAI recommends management provide segregation of duties so that no

one employee is able to perform all accounting functions. In the event that segregation of duties is not

possible due to limited personnel, OSAI recommends implementing compensating controls to mitigate the

risks involved with a concentration of duties. Compensating controls would include separating key

processes and/or critical functions of the office, and having management review and approval of

accounting functions.

Management Response:

County Treasurer: I segregate as well as I can with the employees that I have.

Criteria: Effective internal controls require that key functions within a process be adequately segregated

to allow for prevention and detection of errors and possible misappropriation of funds.

Finding 2012-8 – Inadequate Internal Controls and Noncompliance Over Purchasing (Repeat

Finding)

Condition: While testing seventy-four (74) purchase orders, we noted the following:

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

27

Twenty (20) were not timely encumbered.

Twelve (12) did not have proper supporting documentation.

Cause of Condition: The County did not follow the policies and procedures designed by state statutes

regarding the purchasing process.

Effect of Condition: This condition resulted in noncompliance with state statutes, laws, regulations or

legislative intent, and could result in inaccurate records, incomplete information, or a misappropriation of

assets.

Recommendation: OSAI recommends that the County adhere to state purchasing guidelines. Purchase

orders should be encumbered before goods or services are ordered and proper supporting documentation

should be maintained.

Management Response:

County Commissioner District 1: There are times that we cannot get a purchase order encumbered

before a purchase is made. We will work on this in the future.

County Commissioner District 2: This has been corrected. We will continue to make sure that all

purchase orders are timely encumbered and that we have all documentation attached.

County Commissioner District 3: I will better educate myself on the purchasing process to help rectify

these conditions.

County Clerk: I make a notation on the purchase order that it is not in compliance.

County Sheriff: Steps are being taken to comply with state requirements.

Criteria: Title 19 O.S. § 1505 prescribes the procedures established for the requisition, purchase, lease-

purchase, rental, and receipt of supplies, material, and equipment for maintenance, operation, and capital

expenditures of county government.

Finding 2012-10 – Inadequate Internal Controls Over Signature Stamp – County Commissioner

(Repeat Finding)

Condition: Upon inquiry, observation, and review of documents we noted the following control

weaknesses with regard to purchasing procedures:

The County Clerk’s office has control of the signature stamp for the Chairman of the Board of

County Commissioners.

Cause of Condition: The Chairman does not have physical control of his signature stamp.

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

28

Effect of Condition: This condition could result in the unauthorized transactions and misappropriation of

funds.

Recommendation: OSAI recommends that signature stamps only be used by the official. Officials who

utilize signature stamps should ensure that the stamp is adequately safeguarded from unauthorized use.

Management Response:

County Commissioner District 1: My signature stamp is only used for payroll purposes.

Auditor Response: The Chairman’s signature stamp is not adequately safeguarded from unauthorized

use.

Criteria: An aspect of internal control is the safeguarding of assets. Internal controls over safeguarding

of assets constitute a process, affected by the entity’s governing body, management, and other personnel,

designed to provide reasonable assurance regarding prevention or untimely detection of unauthorized

acquisition, use, or disposition of the entity’s assets from loss, damage, or misappropriation.

Finding 2012-12 – Inadequate Segregation of Duties Over Payroll (Repeat Finding)

Condition: A lack of segregation of duties exists in the County Clerk’s office because the County Clerk

performs the following:

Enters the lists of employees and salary information into the computer.

Calculates gross earnings of hourly employees using timesheets and hourly rates.

Runs a payroll verification report and compares the report to the payroll claims provided by

County Officers.

Prints the payroll checks.

Stamps checks with her signature and the signature of the Chairman of the Board of County

Commissioners.

The Commissioners sign the payroll totals report, not the individual payroll checks.

Cause of Condition: Procedures have not been designed to ensure adequate segregation of duties in the

County Clerk’s office with regards to the payroll process.

Effect of Condition: This condition could result in unrecorded transactions, misstated financial reports,

misappropriation of funds, or clerical errors that are not detected in a timely manner.

Recommendation: OSAI recommends that management be aware of these conditions and determine if

duties can be properly segregated. In the event that segregation of duties is not possible due to limited

personnel, OSAI recommends implementing compensating controls to mitigate the risks involved with a

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2012

29

concentration of duties. Compensating controls would include separating key processes and/or critical

functions of the office, and having management review and approval of accounting functions.

OSAI recommends management take steps to adequately segregate the following key accounting

functions:

Enrolling new employees and maintaining personnel files.

Reviewing time records and preparing payroll.

Approving payroll warrants.

Distributing payroll warrants to individuals.

Management Response:

County Clerk: I was not the County Clerk during this audit period. I am working to segregate the payroll

duties.

Criteria: Accountability and stewardship are overall goals of management in the accounting of funds.

Internal controls should be designed to analyze and check accuracy, completeness, and authorization of

payroll calculations and/or transactions to allow for prevention and detection of errors and abuse. To help

ensure a proper accounting of funds, key functions within the payroll process such as the duties of

processing, authorizing, and payroll distribution should be adequately segregated.

Finding 2012-13 – Reconciliation of the Appropriation Ledger to General Ledger (Repeat Finding)

Condition: Upon inquiry of the reconciliation process of apportioned receipts, disbursements, and cash

balances between the County Treasurer and the County Clerk, documentation of the reconciliation is not

maintained by either official.

Cause of Condition: Procedures have not been designed to ensure documentation of the reconciliation of

the County Clerk’s appropriation ledger to the County Treasurer’s general ledger is maintained.

Effect of Condition: These conditions could result in unrecorded transactions and undetected errors.

Recommendation: OSAI recommends management take steps to ensure reconciliations are performed

between the funds presented on the County Clerk’s appropriation ledger and the County Treasurer’s

general ledger on a monthly basis. Documentation of this reconciliation should be reviewed and

approved by someone other than the preparer.

Management Response:

County Treasurer: We will work with the County Clerk’s office to document the reconciliation of the

appropriation ledger to the general ledger.

County Clerk: We will initial and date account summary upon reconciliation with County Treasurer.

HASKELL COUNTY, OKLAHOMA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS