25

Shannon Okinaka - CFO HAWAIIAN HOLDINGS, INC. (HA) 1

Shannon Okinaka - CFO

HAWAIIAN HOLDINGS, INC. (HA)

1

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act

of 1995 that reflect the Company’s current views with respect to certain current and future events and financial

performance. Words such as “expects,” “anticipates,” “projects,” “intends,” “plans,” “believes,” “estimates,” variations of

such words, and similar expressions are also intended to identify such forward-looking statements. These forward-looking

statements are and will be, as the case may be, subject to many risks, uncertainties and assumptions relating to the

Company’s operations and business environment, all of which may cause the Company’s actual results to be materially

different from any future results, expressed or implied, in these forward-looking statements. These risks and uncertainties

include, without limitation, the Company’s ability to accurately forecast quarter and year-end results; economic volatility;

the price and availability of aircraft fuel; fluctuations in demand for transportation in the markets in which the Company

operates; the Company’s dependence on tourist travel; foreign currency exchange rate fluctuations; and the Company’s

ability to implement its growth strategy.

The risks, uncertainties and assumptions referred to above that could cause the Company’s results to differ materially from

the results expressed or implied by such forward-looking statements also include the risks, uncertainties and assumptions

discussed from time to time in the Company’s public filings and public announcements, including the Company’s Annual

Report on Form 10-K for the year ended December 31, 2015 and the Company’s Quarterly Reports on Form 10-Q, as well

as other documents that may be filed by the Company from time to time with the Securities and Exchange Commission. All

forward-looking statements included in this document are based on information available to the Company on the date

hereof. The Company does not undertake to publicly update or revise any forward-looking statements to reflect events or

circumstances that may arise after the date hereof even if experience or future changes make it clear that any projected

results expressed or implied herein will not be realized.

Forward-looking statements

2

3

• Successful travel carrier to and within Hawai‘i

– Unique business model• Neighbor Island shuttle service with 160 daily flights• Leisure carrier from North America to Hawai‘i serving 11 cities• Leisure carrier from International to Hawai‘i serving 7 countries

– Carried 10.7 million passengers in 2015– Our fleet of 48 aircraft are configured for the Hawai‘i mission– Industry leading service, safety and reliability

• Growing financial strength

– Profitable since 2007– Strong revenue growth with a diversified network– Strong financial performance– Strengthening balance sheet– Generating free cash flow

Hawai‘i’s Destination Carrier

MAUI

Seattle

Portland

New York/Kennedy

Sacramento

Oakland

Hilo

Kailua-Kona

Las Vegas

PhoenixLos Angeles

San Francisco

Kahului

MOLOKA‘I

NORTH AMERICA

Osaka/Kansai

Sapporo/Chitose

Beijing

Seoul/Incheon

Sydney

Brisbane

Auckland

Pago Pago

KAHO‘OLAWE

O‘AHU

KAUA‘I

Honolulu

Līhu‘e

Tokyo/Haneda

San Diego

SEASONAL SUMMER ROUTES

Kailua-Kona – OaklandLīhu‘e – OaklandKailua Kona – Los AngelesLīhu‘e – Los Angeles

Papeete

LĀNA‘I

San Jose

JAPAN

HAWAI‘I ISLAND

NI‘IHAU

SOUTHKOREACHINA

AUSTRALIA

NEWZEALAND

AMERICAN SAMOA TAHITI

Where we fly – Hawai‘i’s destination carrier

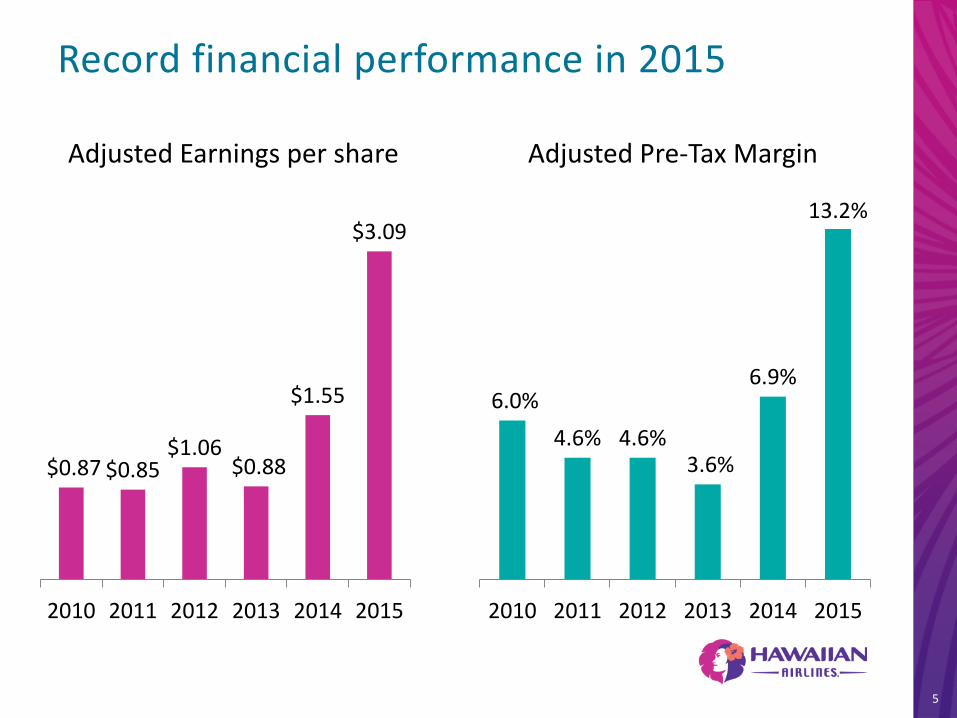

Record financial performance in 2015

$0.87 $0.85$1.06

$0.88

$1.55

$3.09

2010 2011 2012 2013 2014 2015

Adjusted Earnings per share Adjusted Pre-Tax Margin

6.0%

4.6% 4.6%3.6%

6.9%

13.2%

2010 2011 2012 2013 2014 2015

5

We are generating returns on our investments

15.6%

27.5%

2010 2011 2012 2013 2014 2015

Pre-Tax ROIC

6

• Solid demand for travel to Hawai‘i from all of our geographies

• Manageable industry capacity growth to Hawai‘i

• Maturation of routes

• Lapping of FX / fuel surcharge headwinds

• Continued growth of value-added products

• Cost control

• Low fuel prices

2016 is expected to be a better year than 2015

7

North America – improving unit revenue trend

8

Note: Capacity is defined as the industry seats from the West Coast to Hawai‘i in HA’s markets

11.3%

4.0%

-2.8% -3.3%

-9.5%-7.2%

-1.6%

2.8%

-1%

6%9%

11% 10%

13%

6% 5%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15PRASM yoy Annual capacity growth

Moderate industry capacity growth is driving better results

Neighbor Island – fleet optimization in 2015

9

0.0%

-5.0%

-1.7%

2.6%

1Q15 2Q15 3Q15 4Q15

PRASM Year over Year 18 B717 retrofitted to a standard seat count of 128 seats

125 additional seats

Equivalent to an additional very cost effective B717

Completion of interior modifications and refinement of capacity drove improvements

International – improving market performance with moderating FX headwinds

2014 MarketPerformanceand Network

Changes

FX FuelSurcharge

2015

International PRASM

¥100

¥105

¥110

¥115

¥120

¥125

Jan Mar May Jul Sep Nov

JPY / $

1.00

1.10

1.20

1.30

1.40

1.50

Jan Mar May Jul Sep Nov

2014 2015

AUD / $

Growing sales of value-added products

• Averaging $3.5M/month*

• Growth will come from additional inventory, pricing optimization, and new distribution channels

• >10% credit card portfolio growth

• >20% growth in credit card spend

$14.69

$19.72$22.01

2013 2014 2015

Other

Baggage

Sales of HawaiianMiles

Extra Comfort / Preferred Seat Sales

Value-added revenue per passenger

Note: “Other” includes ticket fees, first class upgrades, vacation commissions and on-board sales* Includes Extra Comfort and Preferred Seat revenue 11

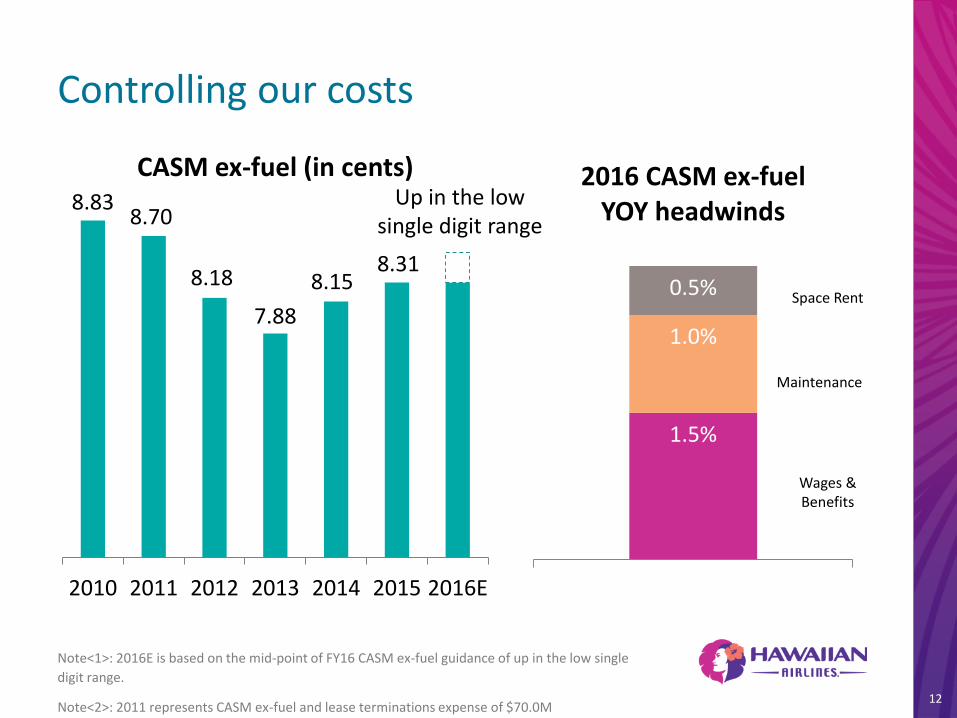

1.5%

1.0%

0.5%

2016 CASM ex-fuel YOY headwinds

Controlling our costs

Note<1>: 2016E is based on the mid-point of FY16 CASM ex-fuel guidance of up in the low single

digit range.

Note<2>: 2011 represents CASM ex-fuel and lease terminations expense of $70.0M

Maintenance

Wages & Benefits

Space Rent

12

8.838.70

8.18

7.88

8.158.31

2010 2011 2012 2013 2014 2015 2016E

CASM ex-fuel (in cents)Up in the low

single digit range

Lower fuel costs provide a tailwind

Note<1>: 2016E economic fuel cost per gallon estimates are based on the forward fuel curve as of

January 25, 2016.

Note<2>: Based on the Company’s hedge portfolio as of January 25, 2016

% Hedged Price

1Q16 60% $1.85

2Q16 46% $1.72

3Q16 30% $1.63

4Q16 15% $1.58

Heating Oil Hedge Position

$2.31

$3.13 $3.20 $3.15 $3.03

$2.04

2010 2011 2012 2013 2014 2015 2016E

Economic Fuel Cost per gallon

13

$1.35 - $1.45

Free cash flow strengthens our balance sheet

14

$476M

$101M

Sources of FCF

Aircraft SLB

Property, Equipment, and PDP

Cash from Operations

2015 FCF = $460M

$124M

$90M

$40M

$71M

$114M

Aircraft Debt before Maturity

Scheduled Principal Debt Repayment

Share Buy Back

Convertible Notes Buy Back: Original Principal Outstanding

Convertible Notes Outstanding: Equity

Uses of FCF = $440

$(118)M

Moderate capital expenditures in 2016

15

$80M

$45M

$40M

Pre-delivery PaymentsMaintenanceOther Modifications

2016 CapEx Breakdown

$140M

$282M$291M

$342M

$442M

$118M

2010 2011 2012 2013 2014 2015 2016E

$160M-$170M

Capital Expenditures

Early retirement of debt has lowered our leverage

Note: Aircraft Rent is capitalized at 7x.

16

$189M

$462M

$661M

$806M $772M

2010 2011 2012 2013 2014 2015 2014 2015

4.2x

2.7x

Debt Obligation Leverage

Optimize our capitalization and minimize cost of capital

$1,050M

Shareholder returns

Represents ~9% of our outstanding market cap

2015

Convertible Note – Equity Repurchase $114M

Share Repurchases $40M

Total Equity Repurchases $154M

17

30%

2014 2015

We’ve maintained a strong liquidity ratio

• Generating more excess cash with the current favorable operating environment

• Growing liquidity even with debt retirement and share repurchases

• 8% above our target is ~$185M

* Cash = cash, cash equivalents, short term investments and $175M availability under the revolving

credit facility

32%

18

Cash * / TTM revenue

• Hawai‘i’s leading airline

• Profitable with growing financial metrics

• Generating free cash flow and strengthening our

balance sheet

• Creating long-term value for our shareholders

Conclusion

19

Mahalo.20

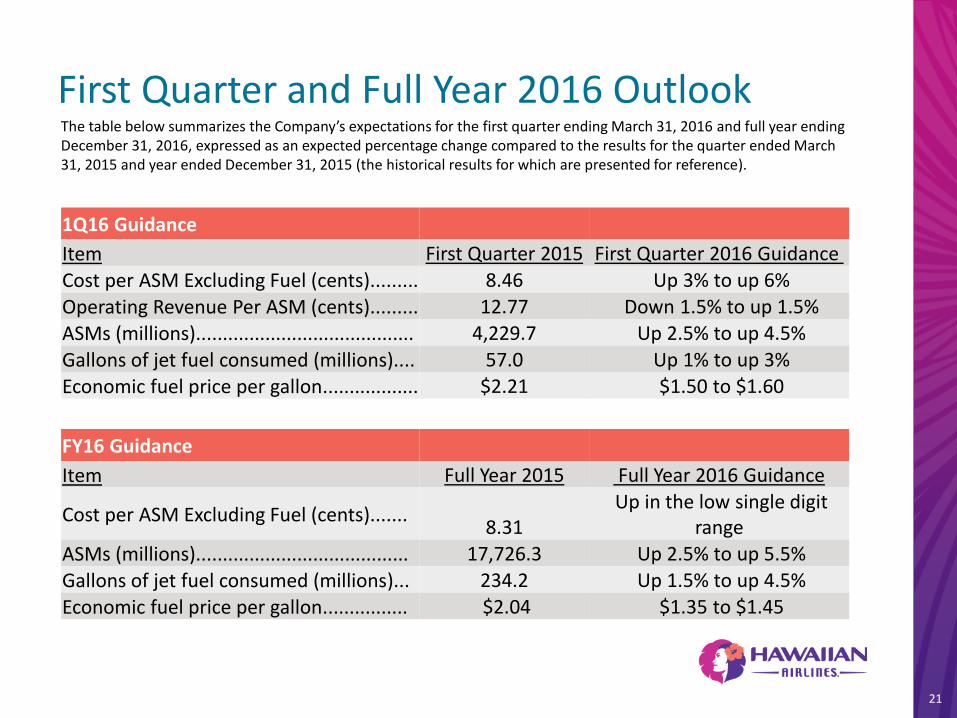

First Quarter and Full Year 2016 Outlook

21

FY16 Guidance

Item Full Year 2015 Full Year 2016 Guidance

Cost per ASM Excluding Fuel (cents).......8.31

Up in the low single digit range

ASMs (millions)........................................ 17,726.3 Up 2.5% to up 5.5%

Gallons of jet fuel consumed (millions)... 234.2 Up 1.5% to up 4.5%

Economic fuel price per gallon................ $2.04 $1.35 to $1.45

The table below summarizes the Company’s expectations for the first quarter ending March 31, 2016 and full year ending December 31, 2016, expressed as an expected percentage change compared to the results for the quarter ended March 31, 2015 and year ended December 31, 2015 (the historical results for which are presented for reference).

1Q16 Guidance

Item First Quarter 2015 First Quarter 2016 Guidance

Cost per ASM Excluding Fuel (cents)......... 8.46 Up 3% to up 6%

Operating Revenue Per ASM (cents)......... 12.77 Down 1.5% to up 1.5%

ASMs (millions)......................................... 4,229.7 Up 2.5% to up 4.5%

Gallons of jet fuel consumed (millions).... 57.0 Up 1% to up 3%

Economic fuel price per gallon.................. $2.21 $1.50 to $1.60

Non-GAAP Reconciliations

NON-GAAP RECONCILIATIONS

($ in thousands, except CASM data) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

GAAP Operating Expenses $1,218,815 $1,630,176 $1,832,955 $2,022,118 $2,069,747 $1,891,364

Less: aircraft fuel, including taxes and delivery (322,999) (513,284) (631,741) (698,802) (678,253) (417,728)

Less: lease termination expense - (70,014) - - - -

Adjusted operating expenses - excluding aircraft fuel and lease termination

$895,816 $1,046,878 $1,201,214 $1,323,316 $1,391,494 $1,473,636

Available Seat Miles 10,150,659 12,039,933 14,687,472 16,785,827 17,073,630 17,726,322

CASM - GAAP (in cents) 12.01 13.54 12.48 12.05 12.12 10.67

Less: aircraft fuel and lease termination expense (in cents) (3.18) (4.84) (4.30) (4.16) (3.97) (2.36)

CASM Excluding Fuel and lease termination expense (in cents)

8.83 8.70 8.18 7.88 8.15 8.31

NON-GAAP RECONCILIATIONS

($ in thousands) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Net Income (Loss), GAAP $110,255 $(2,649) $53,237 $51,854 $68,926 $182,646

Add: lease termination expense, net of tax - 42,008 - - - -

Add: loss on extinguishment of debt, net of tax - - - - 2,331 7,235

Add: changes in fair value of fuel derivatives, net of tax3,859 3,859

2,375 (5,210) 25,864 (609)

Add: non-recurring tax benefits (62,546) - - - - -

Adjusted Net Income, Non-GAAP $45,405 $43,218 $55,612 $46,644 $97,121 $189,272

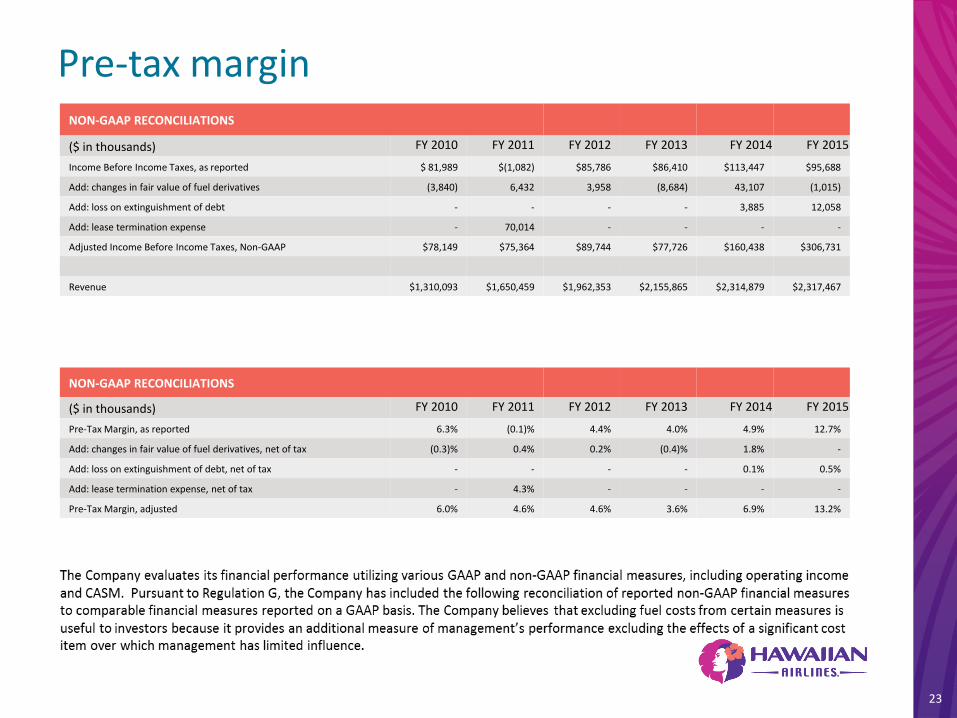

The Company evaluates its financial performance utilizing various GAAP and non-GAAP financial measures, including operating income and CASM. Pursuant to Regulation G, the Company has included the following reconciliation of reported non-GAAP financial measures to comparable financial measures reported on a GAAP basis. The Company believes that excluding fuel costs from certain measures is useful to investors because it provides an additional measure of management’s performance excluding the effects of a significant cost item over which management has limited influence.

22

Pre-tax marginNON-GAAP RECONCILIATIONS

($ in thousands) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Income Before Income Taxes, as reported $ 81,989 $(1,082) $85,786 $86,410 $113,447 $95,688

Add: changes in fair value of fuel derivatives (3,840) 6,432 3,958 (8,684) 43,107 (1,015)

Add: loss on extinguishment of debt - - - - 3,885 12,058

Add: lease termination expense - 70,014 - - - -

Adjusted Income Before Income Taxes, Non-GAAP $78,149 $75,364 $89,744 $77,726 $160,438 $306,731

Revenue $1,310,093 $1,650,459 $1,962,353 $2,155,865 $2,314,879 $2,317,467

NON-GAAP RECONCILIATIONS

($ in thousands) FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Pre-Tax Margin, as reported 6.3% (0.1)% 4.4% 4.0% 4.9% 12.7%

Add: changes in fair value of fuel derivatives, net of tax (0.3)% 0.4% 0.2% (0.4)% 1.8% -

Add: loss on extinguishment of debt, net of tax - - - - 0.1% 0.5%

Add: lease termination expense, net of tax - 4.3% - - - -

Pre-Tax Margin, adjusted 6.0% 4.6% 4.6% 3.6% 6.9% 13.2%

23

LeverageNON-GAAP RECONCILIATIONS

($ in thousands) FY 2014 FY 2015

Debt and capital lease obligations 1,049,637 772,144

Plus: Aircraft leases capitalized at 7x last 12 months’ aircraft rent 744,954 809,571

Adjusted debt and capital lease obligations 1,794,691 1,581,715

Income Before Income Taxes 112,634 295,688

Add back:

Interest and amortization of debt expense 64,420 55,678

Depreciation and amortization 96,374 105,581

Aircraft Rent 106,422 115,653

EBITDAR 379,850 572,600

Adjustments:

Add: changes in fair value of derivative contracts 43,108 (1,015)

Add: Loss on extinguishment of debt 3,885 12,058

Adjusted EBITDAR 426,843 583,643

Leverage Ratio 4.2x 2.7x

The Company evaluates its financial performance utilizing various GAAP and non-GAAP financial measures, including operating income and CASM. Pursuant to Regulation G, the Company has included the following reconciliation of reported non-GAAP financial measures to comparable financial measures reported on a GAAP basis. The Company believes that excluding fuel costs from certain measures is useful to investors because it provides an additional measure of management’s performance excluding the effects of a significant cost item over which management has limited influence.

24

25

Return on Invested CapitalHAWAIIAN AIRLINES – RETURN ON INVESTED CAPITAL (ROIC) – WORKING CAPITAL CASH METHODOLOGY 1

(in ‘000s) 2010 2011 2012 2013 2014 2015

Operating Income $91,278 $20,283 $129,400 $133,745 $245,132 $426,103

Add Back One-Time Charges $0 $70,014 $0 $0 $0 $0

Operating Income Less One-Time Charges $91,278 $90,297 $129,400 $133,745 $245,132 $426,103

Add Back Aircraft Rent Expense for Operating Leases $112,721 $112,883 $98,784 $108,535 $106,422 $115,653

Add Depreciation for Operating Lease Add Back 2 ($28,406) ($28,446) ($24,894) ($27,351) ($26,818) ($29,144)

Add Return on Invested Cash $197 $248 $294 $323 $347 $347

Adjusted Operating Income $175,790 $174,981 $203,585 $215,253 $325,083 $512,959

After Tax Adjusted Operating Income $108,990 $101,489 $122,130 $129,131 $195,050 $306,890

Average Total Debt and Capital Leases $225,170 $341,899 $616,704 $735,676 $1,017,084 $931,756

Common Equity $199,368 $286,499 $249,384 $302,141 $407,234 $361,014

Average Capitalized Operating Leases 3 $789,047 $790,180 $691,486 $759,747 $744,957 $809,575

Remove Average Excess Cash ($90,295) ($64,407) ($115,173) ($122,710) ($179,626) ($241,520)

Average Invested Capital $1,123,290 $1,354,171 $1,442,401 $1,674,855 $1,989,649 $1,860,827

Pre-Tax ROIC 15.6% 12.9% 14.1% 12.9% 16.3% 27.5%

After-Tax ROIC 9.7% 7.5% 8.5% 7.7% 9.8% 16.5%

Notes:1 All unrestricted cash removed from invested capital, except for working capital required to operate the business, defined as unrestricted cash equal to 15% of TTM total revenue2 Assumes 25 years useful life of aircraft and 10% salvage value3 Average capitalized operating leases equals TTM rent multiplied by 7

![THE HAWAIIAN PLANTERS' MONTHLY - University of Hawaii · 2012-09-05 · THE HAWAIIAN PLANTERS' MONTHLY PUBLISHED FOR THE HA WAIIAN SUGAR PLANTEHS' ASSOCIATION. Vol. XXI!.] HONOLULU,](https://static.documents.pub/doc/80x56/5f3c65e98c7b8c02031a6f17/the-hawaiian-planters-monthly-university-of-hawaii-2012-09-05-the-hawaiian.jpg)