31

Headline Verdana Bold Holiday shopping trends survey 2018 November 2018

Headline Verdana BoldHoliday shopping trends survey 2018November 2018

2

Content

Key Trends 3

Consumer Perception 5

Holiday Shopping 8

Omnichannel User Experience 20

3

Key Trends

ECONOMIC OVERVIEW

The Dutch population is significantly more positive about the current state and future of the economy than the European average

Although 4 out of 5 people are neutral or positive about the current state of the economy, only 65% thinks their spending power has increased compared to last year

WE’RE CONNECTED

1 out of 3 consumers uses the internet to search for ideas.

1 out of 4 actually purchases the products online, resulting in 30% of our spend through online channels

Mobile purchases increased by 21% compared to last year, showcasing its popularity

CONSUMER HABITS

Most holiday shopping is done in November or in the first half of December

The Netherlands scores second-lowest in terms of holiday spending, with only Russia spending less

Sinterklaas (5 December) spending makes up 21% of total holiday purchases. This is similar to last year but still 2.5 times less than Christmas spending

WHERE, WHEN, WHAT

The shopping street is still most valued by consumers for Holiday shopping, with 7 out of 10 purchasing products in-store, resulting in 70% of spend through the stores

When shopping online, there is a limited difference in preference between purchasing with pure online players or brick and click retailers. However, when searching for ideas, brick and click retailers are preferred almost twice as much

Black Friday popularity increased by almost 50% compared to last year. For the younger generation it’s even 68% who purchases during this sales event

3

4

Content

4

Key Trends 3

Consumer Perception 5

Holiday Shopping 8

Omnichannel User Experience 20

5

79% of the

participants in the Netherlands is positive or neutral about the current state of the economy

65% of those

participants rates the expected state of the economy in 2019 as positive or neutral

Compared to the rest of Europe, the Dutch population is significantly more positive about the current state of the economy, and next year’s state of the economy (18% and 16% more positive compared to cross country average for 2018 and 2019, respectively).

The Dutch population is less optimistic about next year’s economy compared to the current state. However, last year the respondents were also pessimistic about the 2018 state of the economy (32% was negative about the expected state of the economy), while the actual state is perceived similar (80% last year versus 79% this year).

Current state of the economy

+80% 80-70% 70-60% 60-50% 40-30%50-40%

European average: 67% European average: 56%

6

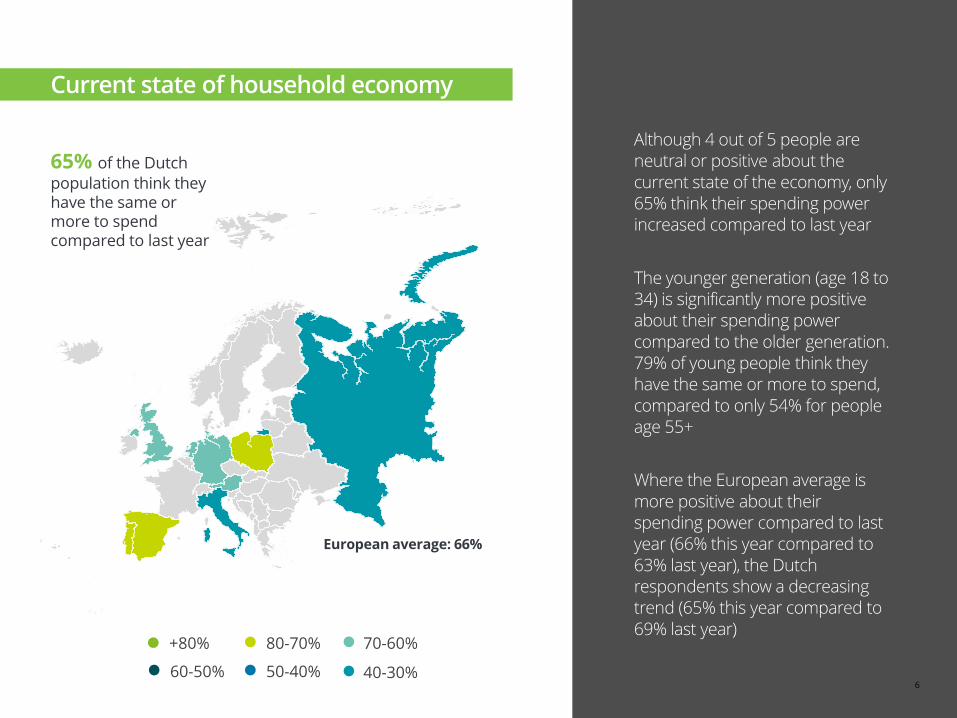

Current state of household economy

65% of the Dutch

population think they have the same or more to spend compared to last year

Although 4 out of 5 people are neutral or positive about the current state of the economy, only 65% think their spending power increased compared to last year

The younger generation (age 18 to 34) is significantly more positive about their spending power compared to the older generation. 79% of young people think they have the same or more to spend, compared to only 54% for people age 55+

Where the European average is more positive about their spending power compared to last year (66% this year compared to 63% last year), the Dutch respondents show a decreasing trend (65% this year compared to 69% last year)

+80% 80-70% 70-60%

60-50% 40-30%50-40%

European average: 66%

6

7

Content

7

Key Trends 3

Consumer Perception 5

Holiday Shopping 8

Omnichannel User Experience 20

8

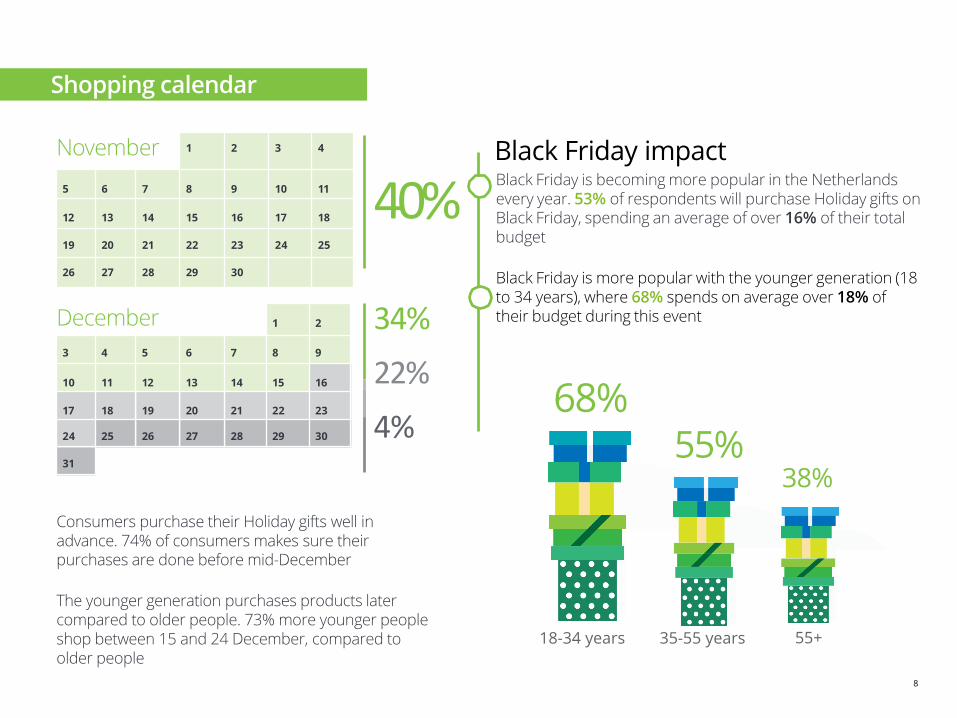

Shopping calendar

Black Friday is becoming more popular in the Netherlands every year. 53% of respondents will purchase Holiday gifts on Black Friday, spending an average of over 16% of their total budget

Black Friday is more popular with the younger generation (18 to 34 years), where 68% spends on average over 18% of their budget during this event

November 1 2 3 4

5 6 7 8 9 10 11

12 13 14 15 16 17 18

19 20 21 22 23 24 25

26 27 28 29 30

December 1 2

3 4 5 6 7 8 9

10 11 12 13 14 15 16

17 18 19 20 21 22 23

24 25 26 27 28 29 30

31

40%

34%

22%

4%

Black Friday impact

Consumers purchase their Holiday gifts well in advance. 74% of consumers makes sure their purchases are done before mid-December

The younger generation purchases products later compared to older people. 73% more younger people shop between 15 and 24 December, compared to older people

38%

68%

55+

55%

18-34 years 35-55 years

8

9

United Kingdom

Spain Austria Italy Germany

Gifts 341 240 268 216 219

Food 172 173 127 140 117

Socialising 75 82 47 66 51

Travel 58 105 100 119 89

Total 646 600 542 541 476

Belgium Portugal Poland Netherlands Russia

Gifts 194 161 124 118 94

Food 150 113 119 105 104

Socialising 37 39 29 31 25

Travel 60 77 51 67 61

Total 441 390 323 321 284

Gifts Food Socialising Travel Total

Total (%NL) 1975 (6%) 1320 (8%) 482 (6%) 787 (9%) 4562 (7%)

Estimated Holiday spending (by country) (€)

10

Estimated Holiday spending

Estimated

expense 2017

Estimated

expense 2018

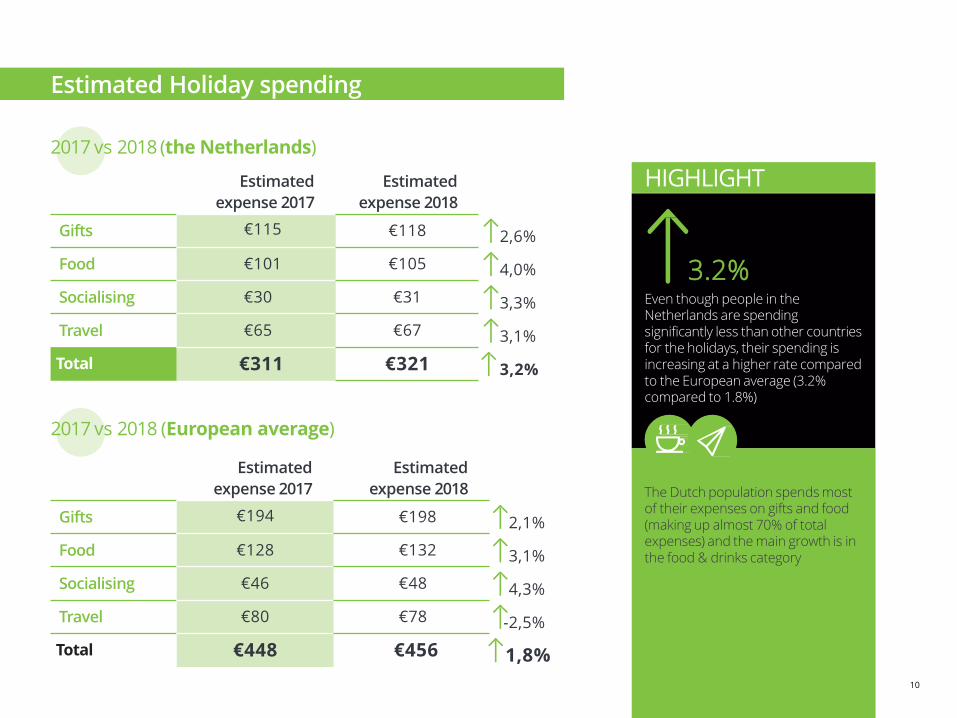

Gifts €115 €118 2,6%

Food €101 €105 4,0%

Socialising €30 €31 3,3%

Travel €65 €67 3,1%

Total €311 €321 3,2%

2017 vs 2018 (the Netherlands)

Estimated

expense 2017

Estimated

expense 2018

Gifts €194 €198 2,1%

Food €128 €132 3,1%

Socialising €46 €48 4,3%

Travel €80 €78 -2,5%

Total €448 €456 1,8%

2017 vs 2018 (European average)

3.2%Even though people in the Netherlands are spending significantly less than other countries for the holidays, their spending is increasing at a higher rate compared to the European average (3.2% compared to 1.8%)

The Dutch population spends most of their expenses on gifts and food (making up almost 70% of total expenses) and the main growth is in the food & drinks category

HIGHLIGHT

10

11

Estimated Christmas spending

The Dutch population spends a smaller percentage of their holiday expenses on gifts, while more is spent on food and drinks compared to the European average

Holiday budget composition 2018

UK

Spain

Austria

Italy

Germany

TOP 5

37%

10%

21%

The Netherlands

Europe

GIFTS FOOD SOCIALISING TRAVEL

43%

33%

11%

29%

17%

Estimated Holiday spending

12

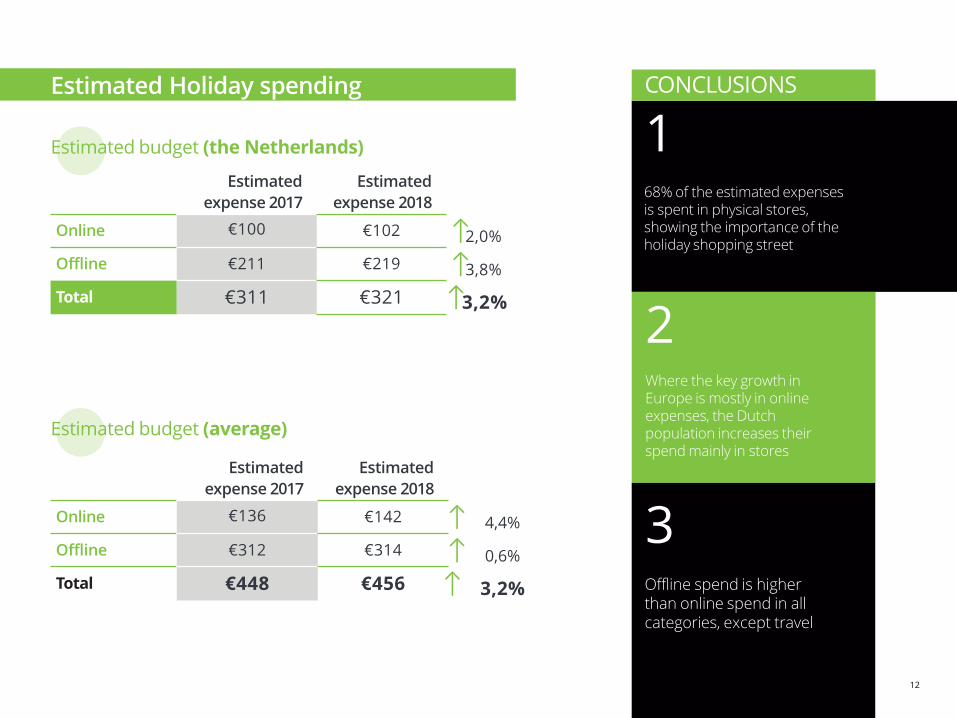

Estimated Holiday spending

Estimated

expense 2017

Estimated

expense 2018

Online €100 €102 2,0%

Offline €211 €219 3,8%

Total €311 €321 3,2%

Estimated budget (the Netherlands)

Estimated

expense 2017

Estimated

expense 2018

Online €136 €142 4,4%

Offline €312 €314 0,6%

Total €448 €456 3,2%

Estimated budget (average)

168% of the estimated expenses is spent in physical stores, showing the importance of the holiday shopping street

CONCLUSIONS

2Where the key growth in Europe is mostly in online expenses, the Dutch population increases their spend mainly in stores

3Offline spend is higher than online spend in all categories, except travel

12

13

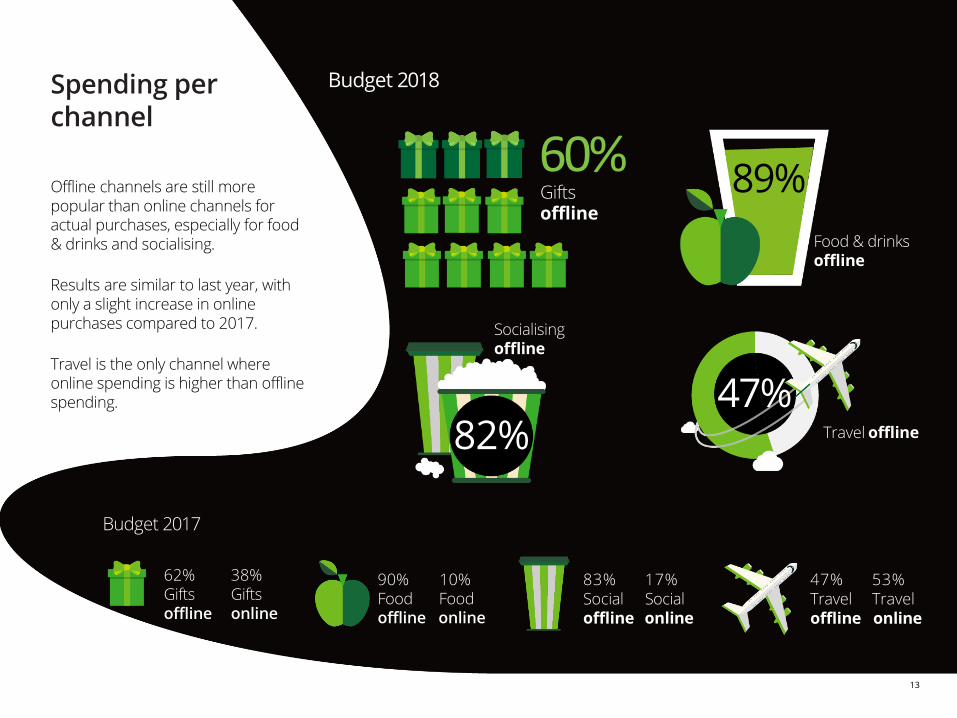

Spending per channel

Offline channels are still more popular than online channels for actual purchases, especially for food & drinks and socialising.

Results are similar to last year, with only a slight increase in online purchases compared to 2017.

Travel is the only channel where online spending is higher than offline spending.

60%Giftsoffline

Budget 2018

Budget 2017

62% 38%Gifts Giftsoffline online

90% 10%Food Foodoffline online

83% 17%Social Socialoffline online

Travel47% 53%

Traveloffline online

82%

Socialisingoffline

89%

Food & drinksoffline

47%Travel offline

14

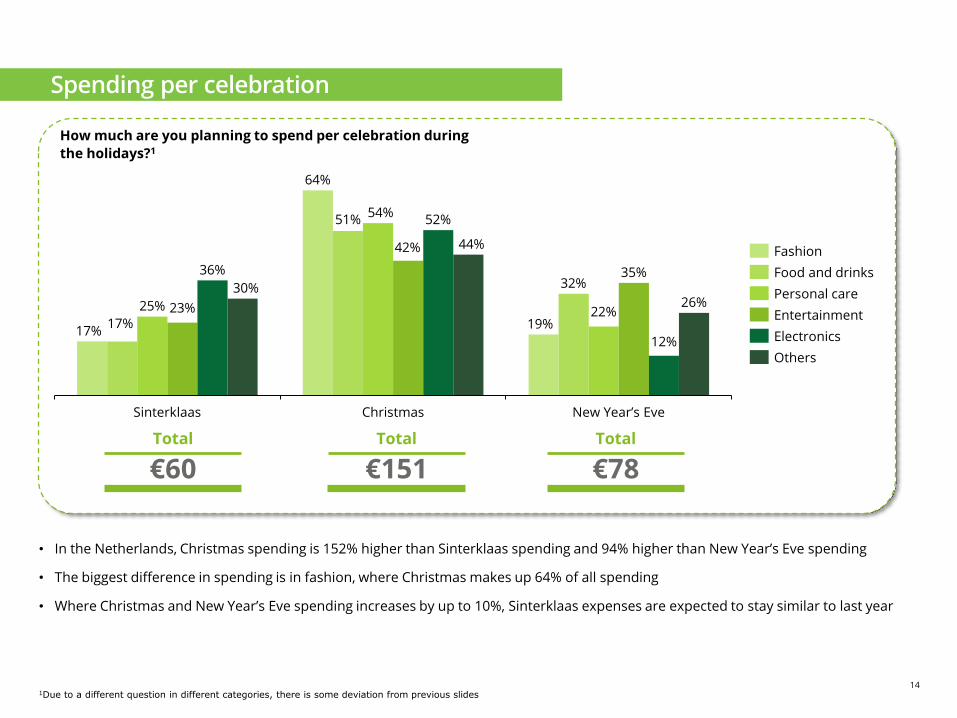

• In the Netherlands, Christmas spending is 152% higher than Sinterklaas spending and 94% higher than New Year’s Eve spending

• The biggest difference in spending is in fashion, where Christmas makes up 64% of all spending

• Where Christmas and New Year’s Eve spending increases by up to 10%, Sinterklaas expenses are expected to stay similar to last year

How much are you planning to spend per celebration during

the holidays?1

€60Total

€151Total

€78Total

1Due to a different question in different categories, there is some deviation from previous slides

26%

36%

25%

Sinterklaas

17%

Christmas New Year’s Eve

17%23%

30%

64%

51%54%

42%

52%

44%

19%

32%

22%

35%

12%

Fashion

Food and drinks

Entertainment

Personal care

Electronics

Others

Spending per celebration

15

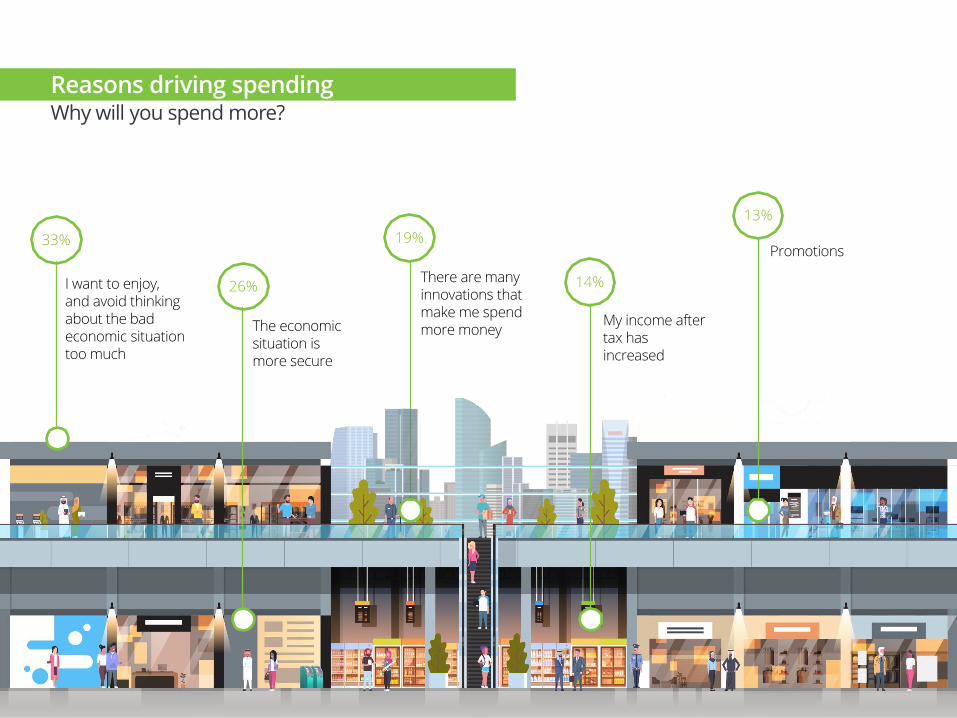

ing changesWhy will you spend more?

I want to enjoy, and avoid thinking about the bad economic situation too much

33%

The economic situation is more secure

There are many innovations that make me spend more money

My income after tax has increased

Promotions

26%

19%

14%

13%

15

Reasons driving spending

16

1 Chocolates 35%

2 Books 34%

3 Cosmetics/perfumes 26%

4 Gift vouchers 26%

5 Food & drink 24%

6 Beauty care 19%

7 Money (cash) 16%

8 Clothes/shoes 15%

9 CDs 13%

10 Games 13%

Most desired gifts for females and males

• The most popular gifts are chocolates (35%) and books (34%), similar to last year. Cosmetics/perfumes is third on the list of most desired gifts in 2018 with a 26% share

• Cosmetics, beauty & care, and CDs became more popular compared to last year, where food & drinks, money, and games declined in popularity

Position compared to 2017

Increase Same position Decrease

FEMALE MALE

1. Chocolates

2. Cosmetics/perfumes

3. Books

4. Gift vouchers

5. Beauty care

1. Books

2. Chocolates

3. Food & drink

4. Gift vouchers

5. Money (cash)

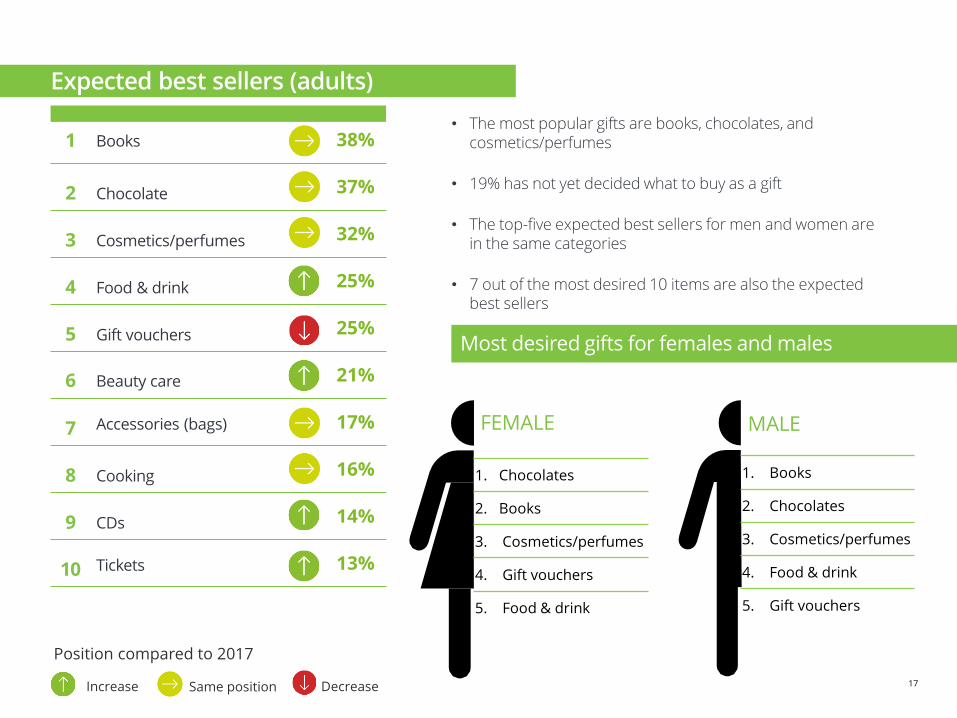

Most desired gifts (adults)

17

Most desired gifts for females and males

FEMALE MALE

1. Chocolates

2. Books

3. Cosmetics/perfumes

4. Gift vouchers

5. Food & drink

1. Books

2. Chocolates

3. Cosmetics/perfumes

4. Food & drink

5. Gift vouchers

Position compared to 2017

Increase Same position Decrease

1 Books 38%

2 Chocolate 37%

3 Cosmetics/perfumes 32%

4 Food & drink 25%

5 Gift vouchers 25%

6 Beauty care 21%

7 Accessories (bags) 17%

8 Cooking 16%

9 CDs 14%

10 Tickets 13%

• The most popular gifts are books, chocolates, and cosmetics/perfumes

• 19% has not yet decided what to buy as a gift

• The top-five expected best sellers for men and women are in the same categories

• 7 out of the most desired 10 items are also the expected best sellers

Expected best sellers (adults)

18

• The majority of respondents (39% or more) will purchase model construction toys or games for kids <12 years old

• For teens, the majority of respondents will also purchase games, but the rest of the best seller list for teens is similar to that for adults

• 12% has not yet decided what to purchase for teens

Position compared to 2017

Increase Same position Decrease

Under 12s

1 Model construction toys 46%

2Games (quiz games etc)

39%

3 Books 33%

4Education & toys

30%

5 Baby and infant articles 26%

6 Dolls & plush 24%

7 Action toys 20%

8 Arts and crafts, creative 18%

9Learning and experimenting

17%

10 Clothes/shoes 15%

12 to 18 years

1 Games 37%

2 Chocolates 30%

3 Books 23%

4 Gift vouchers 19%

5 Board games 19%

6 Clothes/shoes 18%

7 Cosmetics/perfumes 17%

8 Money (cash) 16%

9 Food & drink 15%

10 Sportswear 13%

Expected best sellers (kids and teens)

19

Content

19

Key Trends 3

Consumer Perception 5

Holiday Shopping 8

Omnichannel User Experience 20

20

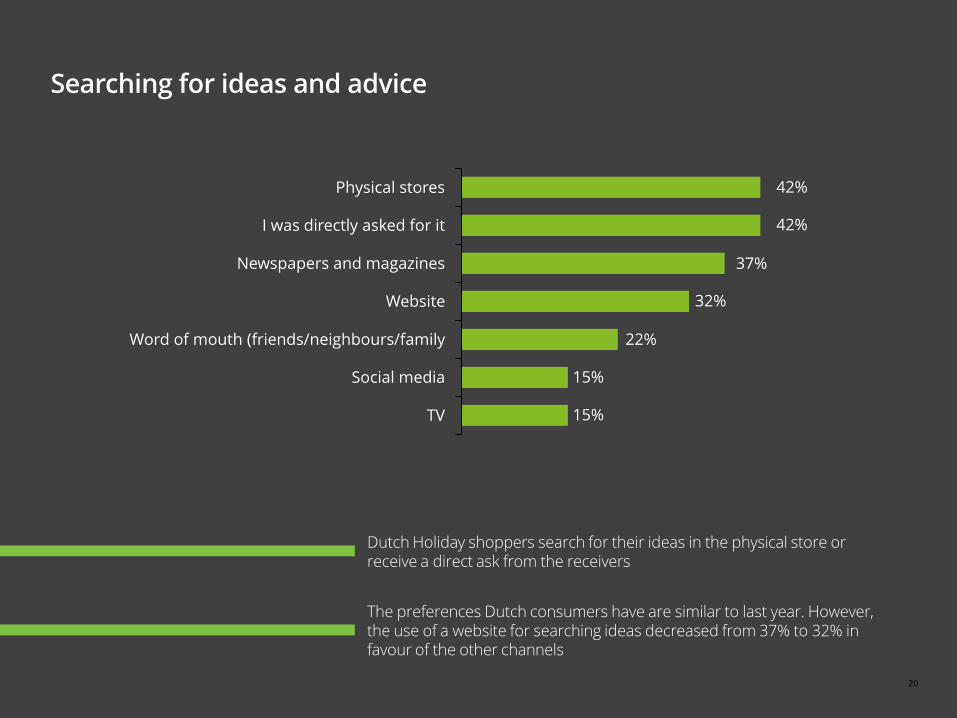

Searching for ideas and advice

Dutch Holiday shoppers search for their ideas in the physical store or receive a direct ask from the receivers

TV

Physical stores

I was directly asked for it

Newspapers and magazines

Social media

Word of mouth (friends/neighbours/family

Website

42%

42%

37%

32%

22%

15%

15%

The preferences Dutch consumers have are similar to last year. However, the use of a website for searching ideas decreased from 37% to 32% in favour of the other channels

21

Searching for ideas and advice(Internet sources)

Websites with coupons and offers

Website of stores with one or more physical stores

Search engines

Websites of brands/suppliers

Email newsletters and online leaflet I receive via email

Comparison site

Website of stores without physical stores

Forums and blogs

53%

45%

40%

32%

32%

31%

29%

16%

Internet sources are mainly websites of brick and click retailers, specific brands, or the use of search engines

22

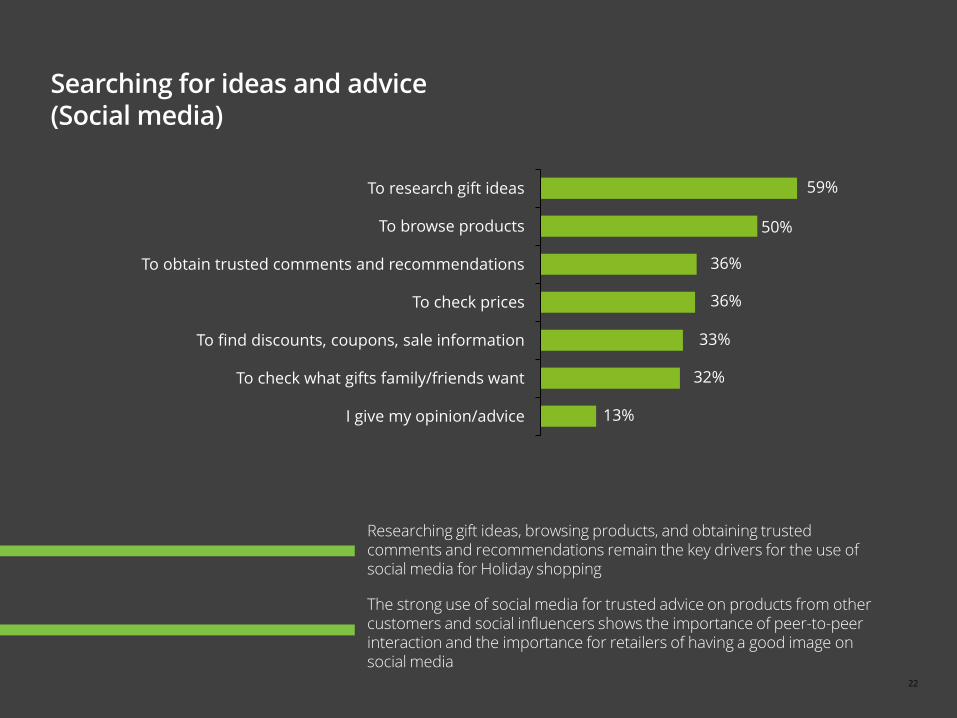

Searching for ideas and advice(Social media)

To obtain trusted comments and recommendations

I give my opinion/advice

To research gift ideas

To browse products

To check what gifts family/friends want

To check prices

To find discounts, coupons, sale information

59%

50%

36%

36%

33%

32%

13%

Researching gift ideas, browsing products, and obtaining trusted comments and recommendations remain the key drivers for the use of social media for Holiday shopping

The strong use of social media for trusted advice on products from other customers and social influencers shows the importance of peer-to-peer interaction and the importance for retailers of having a good image on social media

23

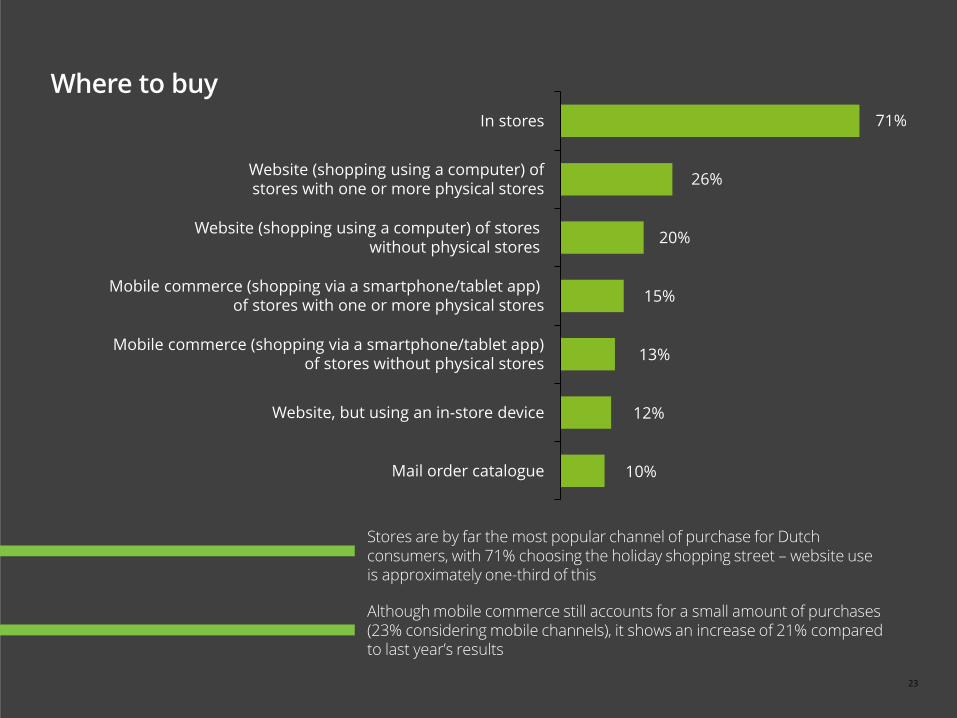

Stores are by far the most popular channel of purchase for Dutch consumers, with 71% choosing the holiday shopping street – website use is approximately one-third of this

Where to buy

Mobile commerce (shopping via a smartphone/tablet app) of stores with one or more physical stores

Website (shopping using a computer) of stores without physical stores

In stores

Website (shopping using a computer) ofstores with one or more physical stores

Mobile commerce (shopping via a smartphone/tablet app)of stores without physical stores

Website, but using an in-store device

Mail order catalogue

71%

26%

20%

15%

13%

12%

10%

Although mobile commerce still accounts for a small amount of purchases (23% considering mobile channels), it shows an increase of 21% compared to last year’s results

24

Where to buy (Physical stores)

45% Traditional local stores

50% Specialised chains

22% Traditional department stores

23% Hypermarket

Most popular channel per country

Considered Dutch purchasing channels

Hypermarket

Traditional local stores

Traditional department stores

Specialised chains

25

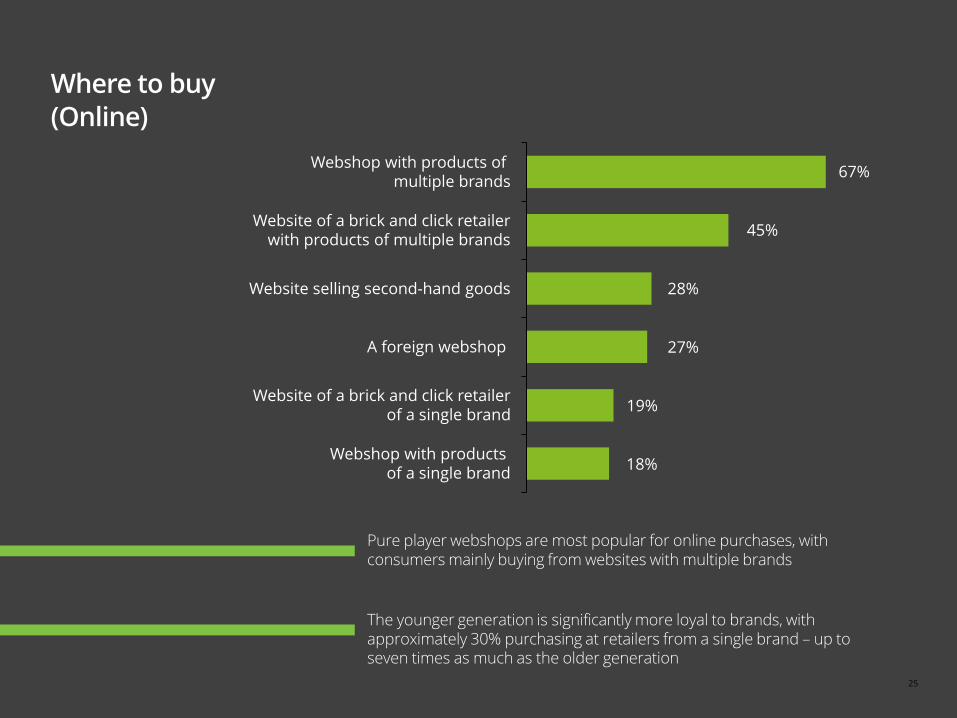

Pure player webshops are most popular for online purchases, with consumers mainly buying from websites with multiple brands

Where to buy (Online)

Website selling second-hand goods

Webshop with products of multiple brands

Webshop with products of a single brand

Website of a brick and click retailerwith products of multiple brands

A foreign webshop

Website of a brick and click retailerof a single brand

67%

45%

28%

27%

19%

18%

The younger generation is significantly more loyal to brands, with approximately 30% purchasing at retailers from a single brand – up to seven times as much as the older generation

26

Where do you spend more than budgeted?

When spending more than budgeted, the overspending is more often from purchases at physical stores than in webshops. It is also more often from multi-branded retailers than from single-branded retailers

Channels of overspending

27

ONLINE mobile OFFLINE

Competent and professional advice

Pleasure while shopping (nice experience)

I immediately get the products I purchased

After-sales services (repair)

Protection of my personal data

Price level

Following delivery

time to order

Products can be compared easily

Competent and professional advice

ONLINE web

Home delivery

Broad assortment

Access to other consumer reviews 62%

62%

61%

59%

57%

It’s easy to search for and choose what I need

24%

22%

20%

19%

18%

87%

82%

77%

74%

72%

Prices can be compared easily

Shopping when I want

Online shopping vs physical stores: advantages

28

1 al 15

50%

€7

Same day

41%

€5

Next day

30%

€5

In two days In a week In two weeks

50% of consumers are willing to pay on average €7 to ensure their package arrives in time for same-day orders

• Half of consumers would be willing to pay on average €7 to ensure the desired package arrives on the same day during the holiday

season

• The younger generation is more willing to pay for their delivery, with up to 75% willing to pay for same-day delivery. The younger

generation is up to three times more willing to pay for delivery compared to the older generation. However, the amount they want to

pay is up to 30% lower compared to the older generation

• In ‘non-holiday’ periods, a similar amount of consumers (50-60%) is willing to pay for same day delivery, but the amount they are

willing to pay is only €4 on average, showing the increased importance of a reliable same-day delivery option during the holiday

season1

1Source: Deloitte Digital Omnichannel Fulfilment 2017

Assuring on-time delivery

19%

€4

15%

€4

29

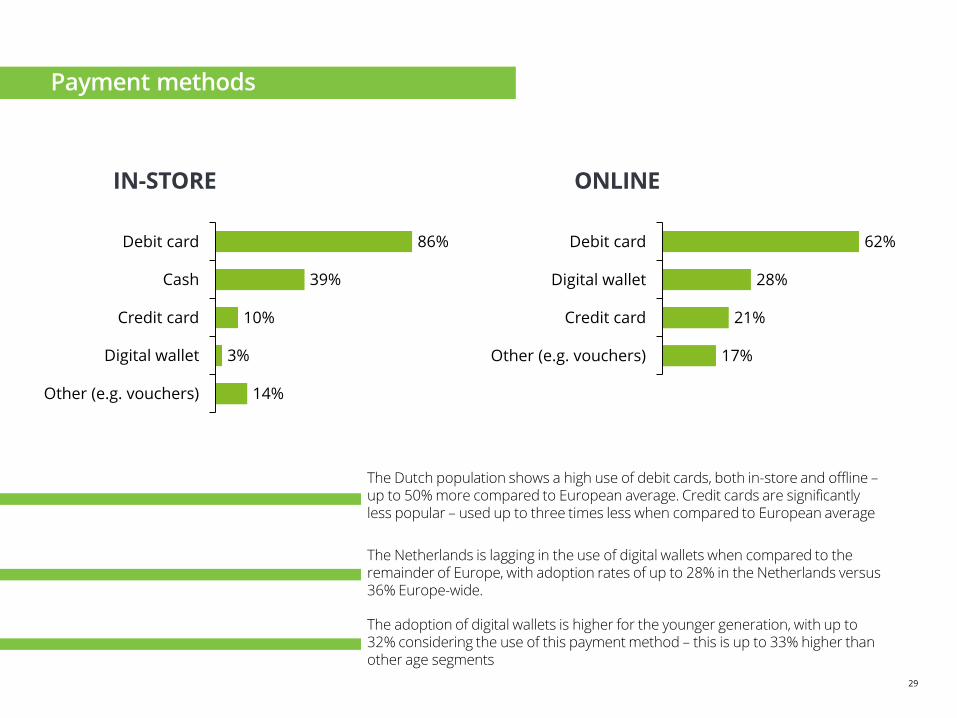

The Dutch population shows a high use of debit cards, both in-store and offline –up to 50% more compared to European average. Credit cards are significantly less popular – used up to three times less when compared to European average

IN-STORE ONLINE

Other (e.g. vouchers)

Debit card

Digital wallet

Cash

Credit card

86%

39%

10%

3%

14%

Debit card

21%

28%Digital wallet

62%

Credit card

Other (e.g. vouchers) 17%

The Netherlands is lagging in the use of digital wallets when compared to the remainder of Europe, with adoption rates of up to 28% in the Netherlands versus 36% Europe-wide.

The adoption of digital wallets is higher for the younger generation, with up to 32% considering the use of this payment method – this is up to 33% higher than other age segments

Payment methods

30

Holiday shopping trends survey 2018

Methodology

The conclusions of this study have been drawn from the results of a survey conducted over the internet to a population sample of more than 9,000 people

The data has been obtained through a structured questionnaire on a sample of the population between 18 and

65 years old within a controlled panel

The sample was chosen based on socio-demographic characteristics,

personal interests, income level and consumption behaviours

The information was collected between 3 and 15 October, 2018

Austria Belgium Germany Italy Netherlands Poland Portugal Russia Spain UK TOTAL

Participants 842 897 1,150 1,022 840 831 780 949 921 937 9169

This year, 10 countries participated, all of them European

31

Adgild HopPartner – Dutch Retail LeadTel: +31 (0)88 288 8721Mobile: +31 (06) 3463 5321Email: [email protected]

Patrick SchunckPartner – Dutch Consumer Business Consulting & Consumer Products LeadTel: +31 (0)88 288 1671Mobile: +31 (0)6 2126 7379Email: [email protected]

Wesley SnoerenConsultant – Strategy & Operations | Omnichannel Retail

Lars MulderAnalyst – Strategy & Operations | Omnichannel Retail

Contacts

Authors

Holiday shopping trends survey 2018