40

Small Employer Groups

| Date post: | 20-Aug-2015 |

| Category: |

Health & Medicine |

| Upload: | neacelukens |

| View: | 2,138 times |

| Download: | 1 times |

Small Employer Groups

Click the arrow to

open/close chat

panel

Type in a question

here and click

Send

� Director of Compliance for Neace Lukens Employee

Benefits

� 20+ years experience in the healthcare field

� Extensive clinical and management background

� Experience with both public and private sector funding

� RN degree from University of Miami

� Certified Professional in Healthcare Quality

� Small group definition

� Grandfathered plans

� Timeline for compliance

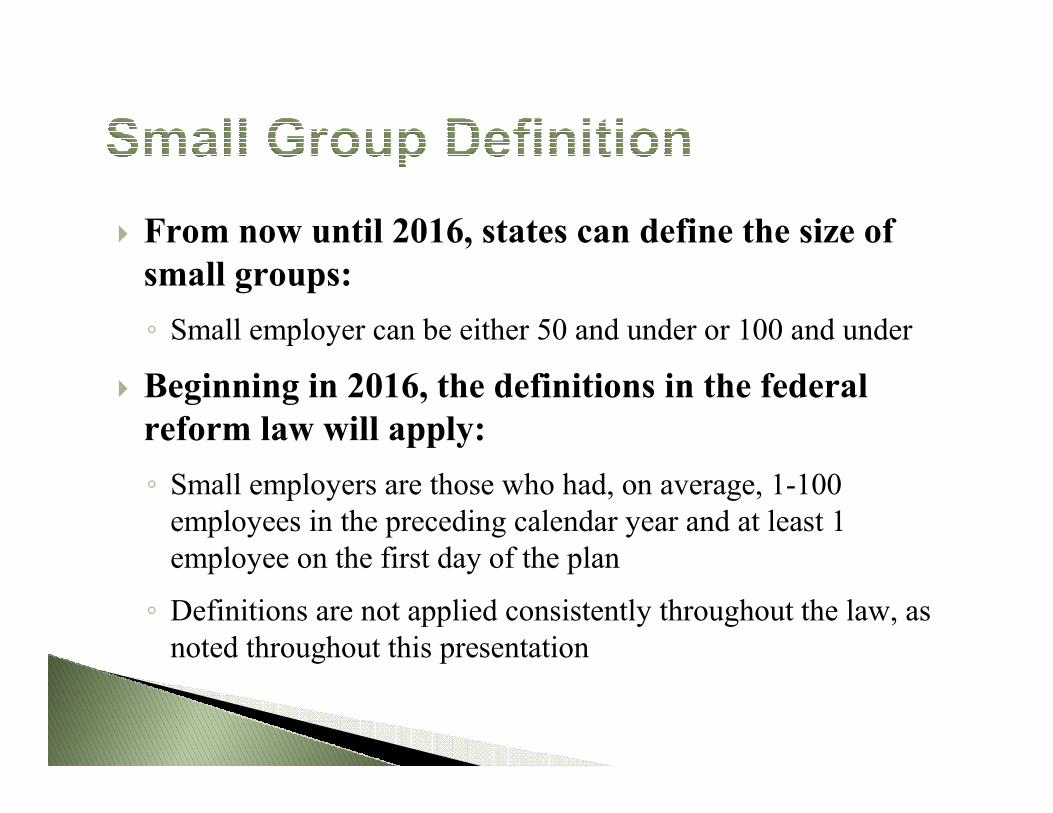

� From now until 2016, states can define the size of

small groups:

◦ Small employer can be either 50 and under or 100 and under

� Beginning in 2016, the definitions in the federal

reform law will apply:

◦ Small employers are those who had, on average, 1-100

employees in the preceding calendar year and at least 1

employee on the first day of the plan

◦ Definitions are not applied consistently throughout the law, as

noted throughout this presentation

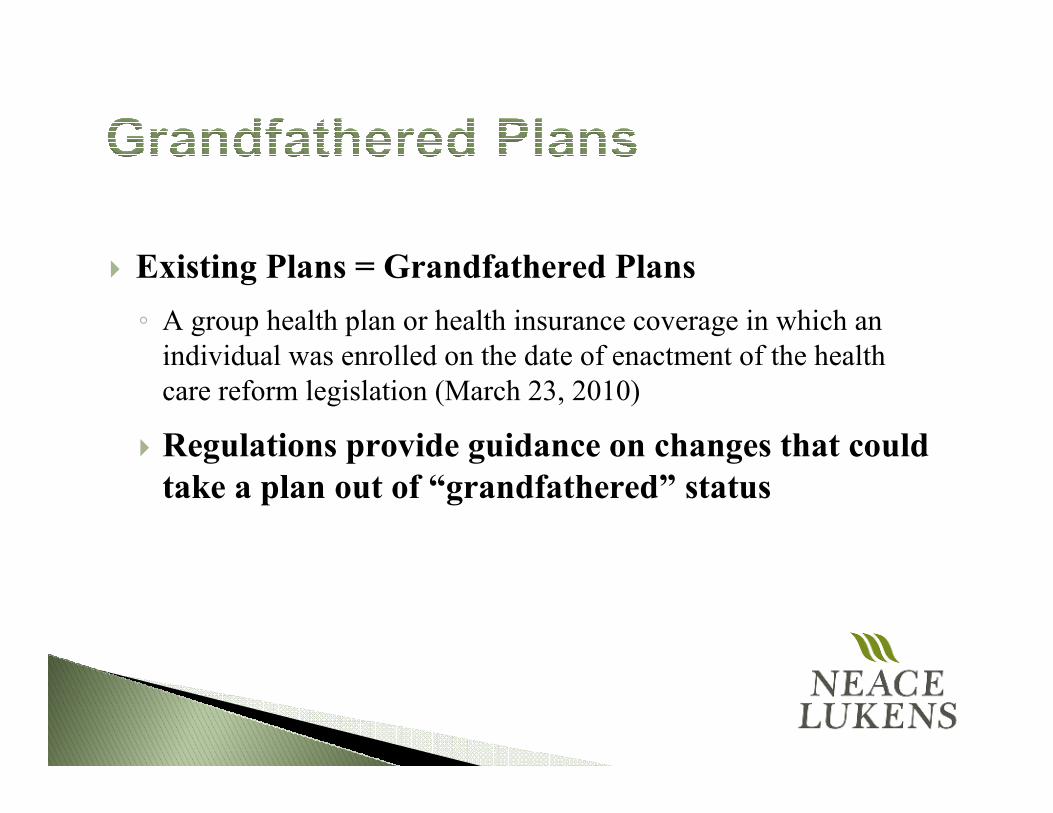

� Existing Plans = Grandfathered Plans

◦ A group health plan or health insurance coverage in which an

individual was enrolled on the date of enactment of the health

care reform legislation (March 23, 2010)

� Regulations provide guidance on changes that could

take a plan out of “grandfathered” status

� Health Insurance Changes – Prohibitions on:

◦ Lifetime and annual limits

◦ Pre-existing condition exclusions

◦ Rescissions

◦ Excessive waiting periods

� Required coverage of adult children up to age 26

� Summary of benefits and coverage

� Reporting medical loss ratio

� Qualifying small employers that provide health care coverage to employees are eligible for tax credit

◦ Have fewer than 25 full-time equivalent (FTE) employees

◦ Pay wages averaging less than $50,000 per employee per year

◦ Has a “qualifying arrangement” (pays premiums for each employee in a uniform percentage that is at least 50 percent of the cost of coverage)

◦ tax-exempt 501(c) organization also eligible

� Credit based on premiums paid by employer

� Claimed on employer’s annual income tax return

� Amount of credit

◦ Up to 35 percent of health (includes dental & vision) premium

costs paid in 2010 (25 percent for tax-exempt employers)

◦ On Jan. 1, 2014, increases to 50 percent (35 percent for tax-

exempt employers)

� Depends on employees and wages

◦ The credit phases out gradually for:

� Employers with average wages between $25,000 and $50,000 and

� Employers with the equivalent of between 10 and 25 full-time

workers

SMALL BUSINESS TAX CREDIT

� Employees taken into account

◦ Employees who perform services for the employer during the

tax year

◦ Exceptions:

� Partners and certain owners (and family members)

� Seasonal workers

� Employers not eligible

◦ Government employers

� Federal

� State

� Local

� Indian tribal

◦ Unless the employer is a tax-exempt 501(c) organization

� Temporary federal program for insuring high-risk

individuals

◦ $5 billion funding

◦ Expires Jan. 1, 2014

� High-risk individuals = pre-existing conditions and

no creditable coverage for 6 months

� Cannot have employees drop coverage to join high-

risk pool

◦ Sanctions/reimbursement requirement will be imposed

(Plan Years Beginning on or after September 23, 2010)

� Plans that cover dependent children must make

coverage available until child turns 26

◦ Includes grandfathered plans, unless child has own employer

coverage (before 2014)

◦ Covers married and unmarried children

◦ Children of covered adult children do not have to be covered

� State mandates above this level continue to apply

� Insurers complying early to avoid coverage gaps

� Definition of dependent restricted

◦ Can only be defined by relationship

◦ Other factors (financial dependence, residency, student status,

employment, eligibility for other coverage) generally can’t be

used as basis for denial

� Qualified dependents must be:

◦ Offered same coverage as similarly-situated individuals

◦ Given the same rates for coverage

◦ Provided with a 30-day special enrollment opportunity and

notice

� Apply to new and grandfathered plans

� No lifetime limits on essential benefits

� Restricted annual limits on essential benefits

◦ Allowed for plan years beginning before Jan. 1, 2014

� Essential benefits generally include: ◦ Ambulatory patient services, emergency services, hospitalization, maternity and

newborn care, mental health and substance abuse services, prescription drugs,

rehab services, lab services, wellness and disease management, pediatric care

� Some regulations issued, waiting on others

� No rescission of coverage

◦ Applies to group and individual coverage

◦ Applies to new and grandfathered plans

◦ Exception for fraud or intentional material misrepresentation

◦ Individual must be given prior notice of cancellation for

permitted reasons (including nonpayment of premium or plan

termination)

� No pre-existing condition exclusions or limitations

for children under age 19

◦ This prohibition will apply to everyone in 2014

◦ Applies to new and grandfathered group plans

� Apply to new plans

� Limits on preauthorization and cost-sharing

◦ No cost-sharing for some preventive care (including well-child

care) and immunizations

◦ No preauthorization or increased cost-sharing for emergency

services (in- vs. out-of-network)

� Patients can chose any available participating

primary care provider (or pediatrician)

◦ No preauthorization or referral for ob/gyn care

� Apply to new fully-insured plans

� Fully-insured plans must follow rules regarding

nondiscrimination in favor of highly-compensated

employees (HCE)

◦ Cannot discriminate with respect to eligibility or benefits

� HCE:

◦ 5 highest paid officers, more than 10% shareholder, or highest

paid 25% of all employees

� Apply to Health FSAs, HRAs, HSAs and Archer

MSAs

� Medicine or drugs only treated as qualified medical

expense for tax exclusion if they are prescribed or

are insulin

◦ This means no reimbursement for OTC medicine or drugs

without a prescription (except insulin)

� Applies to expenses incurred after Dec. 31, 2010

� Grants for health education, screenings, and

wellness programs

� Available only to eligible employers who implement

the programs after March 23, 2010

◦ Employers with up to 100 employees

� Employers must disclose aggregate cost of

employer-sponsored health coverage on Forms W-2

� Optional for 2011 tax year; mandatory for later

years

� Includes group health plan coverage, whether paid

by employer or employee

� Health FSA Limits: $2,500 per year

◦ Currently no FSA limit, although many employers impose

limit

◦ Limit is $2,500 for 2013; indexed for CPI after that

◦ Does not apply to dependent care FSAs

� Jan. 1, 2014: individuals must enroll in coverage or

pay a penalty

� Amounts indexed for CPI after 2016

� States will receive funding to establish health

insurance exchanges

� Individuals and small employers can purchase

coverage through an exchange (Qualified Health

Plans)

◦ Qualified employees use vouchers to buy coverage through

exchange

� Individuals can be eligible for tax credits

� Large employers subject to “Pay or Play” rule

� Applies to employers with 50 or more full-time

equivalent employees in prior calendar year

� Penalties apply if:

◦ Employer does not provide coverage and any FT employee

gets subsidized coverage through exchange ($2000 Penalty)

◦ OR

◦ Employer does provide coverage and any FT employee still

gets subsidized coverage through exchange ($3000 Penalty)

� Employers will have to report certain information

to the government

◦ Whether employer offers health coverage to full-time

employees and dependents

◦ Whether the plan imposes a waiting period

◦ Lowest-cost option in each enrollment category

◦ Employer’s share of cost of benefits

◦ Names and number of employees receiving health coverage

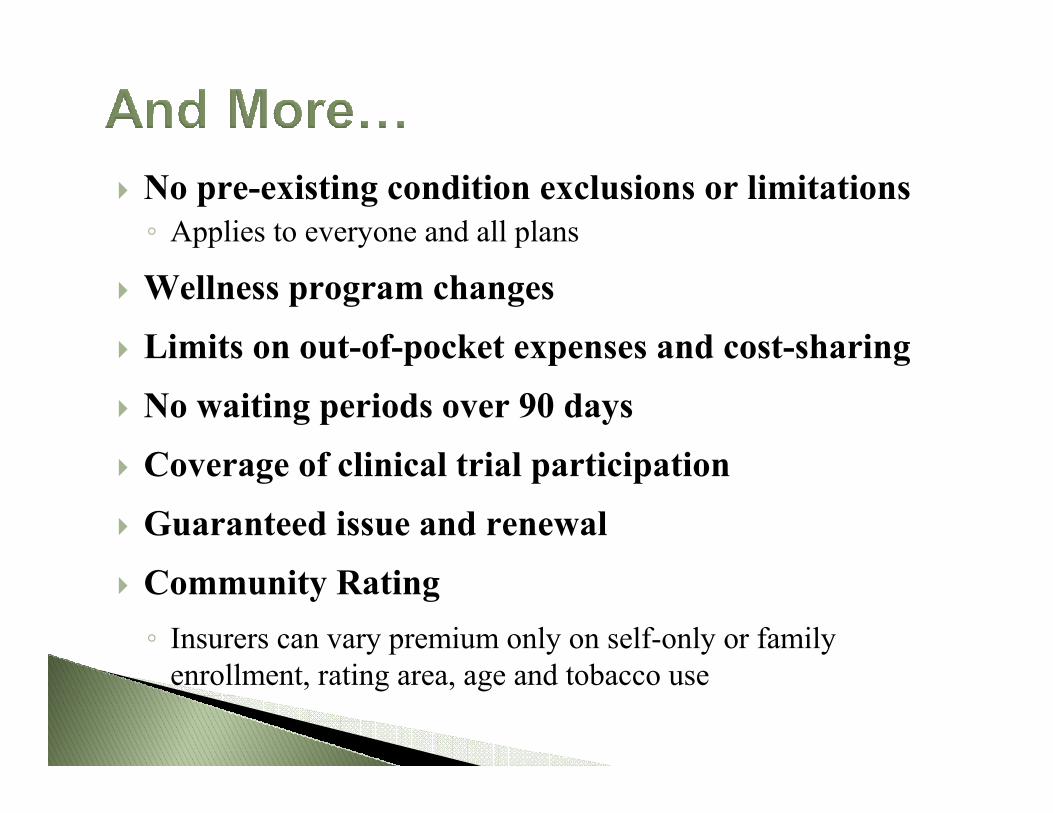

� No pre-existing condition exclusions or limitations

◦ Applies to everyone and all plans

� Wellness program changes

� Limits on out-of-pocket expenses and cost-sharing

� No waiting periods over 90 days

� Coverage of clinical trial participation

� Guaranteed issue and renewal

� Community Rating

◦ Insurers can vary premium only on self-only or family

enrollment, rating area, age and tobacco use

� 40 percent excise tax on high-cost health plans

� Based on value of employer-provided health

coverage over certain limits

◦ $10,200 for single coverage

◦ $27,500 for family coverage

� To be paid by coverage providers

◦ Fully insured plans = health insurer

◦ HSA/Archer MSA = employer

◦ Self-insured plans/FSAs = plan administrator

� More guidance expected

� Neace Lukens Compliance Information

◦ www.neacelukens.com

� US Department of Health & Human Services

◦ www.healthcare.gov

� Kaiser Foundation

◦ www.kaiserfoundation.org

� Small Business IRS tax credit FAQ

◦ www.irs.gov

� Model Notice Requirements

◦ www.dol.gov