Healthcare Reform: Winners and Losers May 20, 2010 John Boettiger, Principal Deloitte Financial Advisory Services LLP [email protected]Chuck Dowling, Senior Vice President of Regional Operations US Oncology [email protected]Jim Shannon, EVP Development LHP Hospital Group [email protected]Richard Rawson, President Administaff [email protected]

Transcript

Healthcare Reform:Winners and LosersMay 20, 2010

John Boettiger, PrincipalDeloitte Financial Advisory Services LLP [email protected]

Chuck Dowling, Senior Vice President of Regional Operations US [email protected]

Health care since the Clinton eraThe economy was beginning its downturn

* The Children’s Health Insurance Program, created in 1997, has significantly reduced the number of low-income children who are uninsured.

Sources: Employee Benefit Research Institute estimates of data from the Current Population Survey. Centers for Medicare & Medicaid Services, Office of the Actuary: Data from the National Health Statistics Group. Kaiser Family Foundation/HRET Survey of Employer-Sponsored Health Benefits, 1999–2008, and Kaiser analysis of data from bureau of Labor Statistics.

Health care spendingAs percentage of gross domestic product

Insurance premiumsCumulative growth

Cost of workersAverage monthly worker premium contributions

Declining reimbursementsUncertainty surrounding healthcare reformIncreasing regulationAccelerating uncompensated careConstraints on capital accessAging plant and equipmentIncreased competition from niche or specialty providers

These challenges are causing a widening divide between “haves” and “have nots”

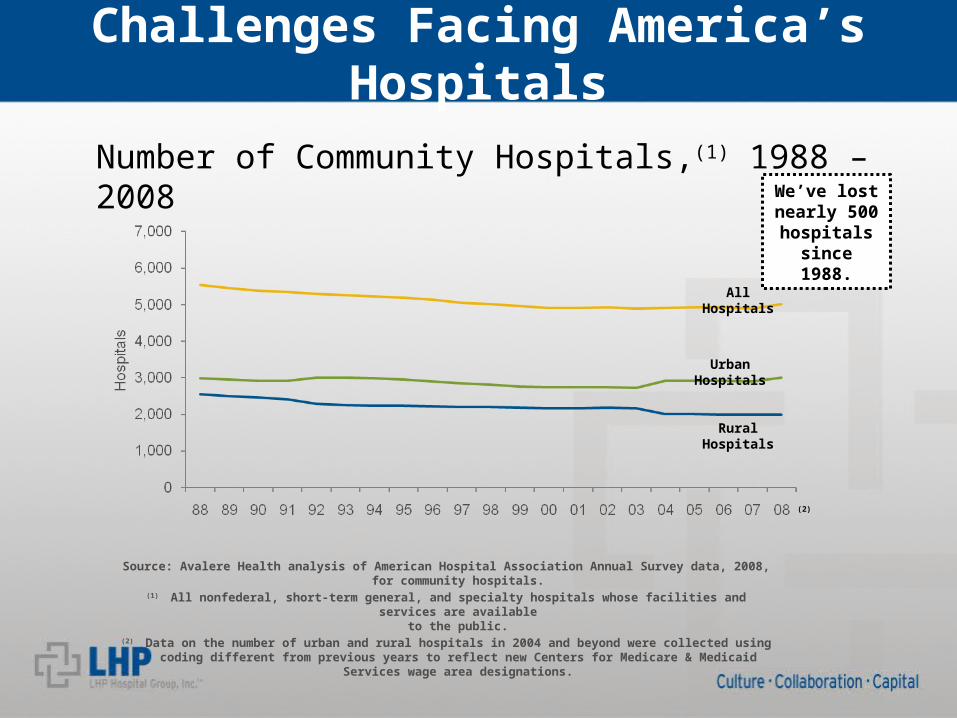

Number of Community Hospitals,(1) 1988 – 2008

Source: Avalere Health analysis of American Hospital Association Annual Survey data, 2008, for community hospitals.

(1) All nonfederal, short-term general, and specialty hospitals whose facilities and services are availableto the public.

(2) Data on the number of urban and rural hospitals in 2004 and beyond were collected using coding different from previous years to reflect new Centers for Medicare & Medicaid Services wage area designations.

(2)

All Hospitals

Urban Hospitals

Rural Hospitals

Challenges Facing America’s Hospitals

We’ve lost nearly 500

hospitals since 1988.

Percentage of Hospitals with Negative Total and Operating Margins, 1995 – 2008

Source: Avalere Health analysis of American Hospital Association Annual Survey data, 2008, for community hospitals.

Negative Operating Margin

Negative Total Margin

Challenges Facing America’s Hospitals

Approximately one third of

hospitals lose money

Aggregate Hospital Payment-to-cost Ratios for Private Payers, Medicare, and Medicaid, 1988 – 2008

Source: Avalere Health analysis of American Hospital Association Annual Survey data, 2008, for community hospitals.

(1) Includes Medicaid Disproportionate Share payments.

Challenges Facing America’s Hospitals

Commercial insurers

subsidize govt. payers

Number of Bond Rating Upgrades and Downgrades, Not-for-Profit Health Care(1), 1993 – 2008

Source: Moody’s U.S. Public Finance. Moody’s Not-for-Profit Healthcare 2008 Year End Ratings Monitor. Data released January 2009. (1) Includes stand-alone hospitals, health systems, and human service providers.

Upgrades

Downgrades

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

60

40

20

0

20

40

60

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

60

40

20

0

20

40

60

Challenges Facing America’s Hospitals

Downgrades have consistently

exceeded upgrades

Challenges Facing America’s Hospitals

protect their credit ratings;

stretch their capital spend;

preserve their liquidity.

And at the same time

grow, or at least protect, market share;

remain competitive in plant and equipment;

improve quality;

be opportunistic with regard to development.

These challenges are profoundly impacting hospitals across the board.

Hospitals in all categories are attempting to:

For many, if not most, this means at least considering some form of a joint venture or affiliation option.

LHP Response

LHP was formed as a direct response to these challenges.

Our purpose is to form joint ventures with not-for-profit partners to help community hospitals meet their strategic objectives.

Who is LHP Hospital Group?

A privately-held hospital company based in Plano, Texas

An experienced management teamFormer management team at Triad Hospitals, Inc. 54 hospitals (10 JVs)

Owners with financial and healthcare expertiseCCMP Capital Partners (former private equity arm of JP Morgan Chase)Canada Pension Plan Investment Board

A board with leading not-for-profit healthcare thought leaders

Our View on Health Reform

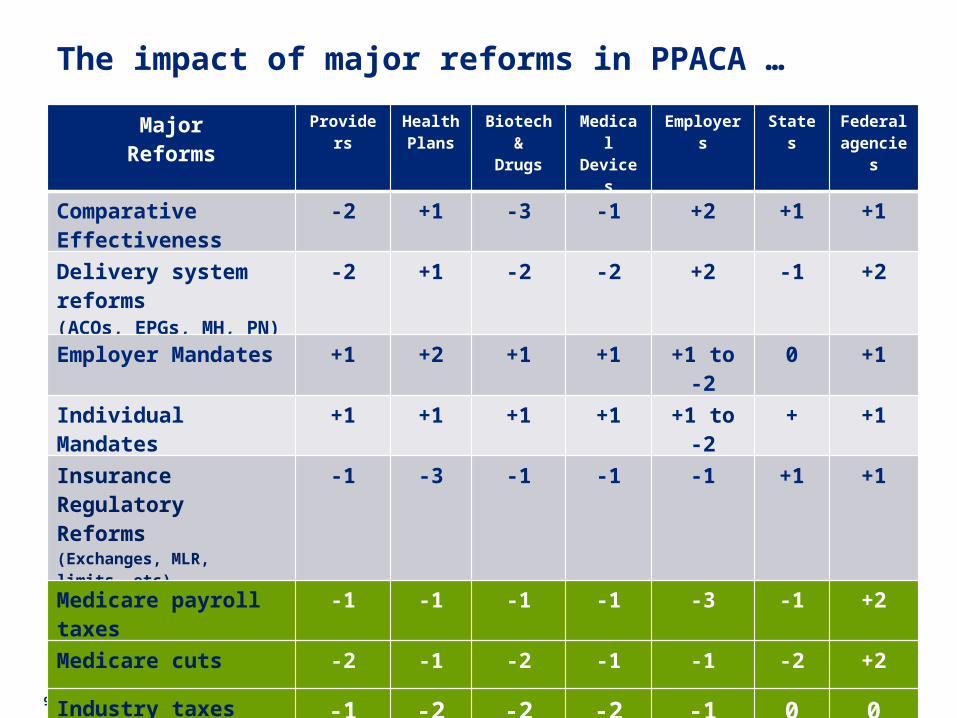

Likely accretive on average for hospitalsWinners and losersPricing pressureIncentives for coordinating careManaging the unintended consequences

Feels like another round of provider consolidation

Contact Information

If you would like to learn more about LHP Hospital Group please visit our website at www.lhphospitalgroup.com

If you would like to discuss specific points of this presentation or ask further detailed questions, please contact Jim Shannon, Executive Vice President of Development, at 972-943-1705 or by e-mail at [email protected].

ADA DFWAIRCATRA ’86 COBRADEFRAREATEFRAPDAERISAOSHAADEACRAFUTAFLSAFICANLRACommon LawCase LawLocal LawsState Laws

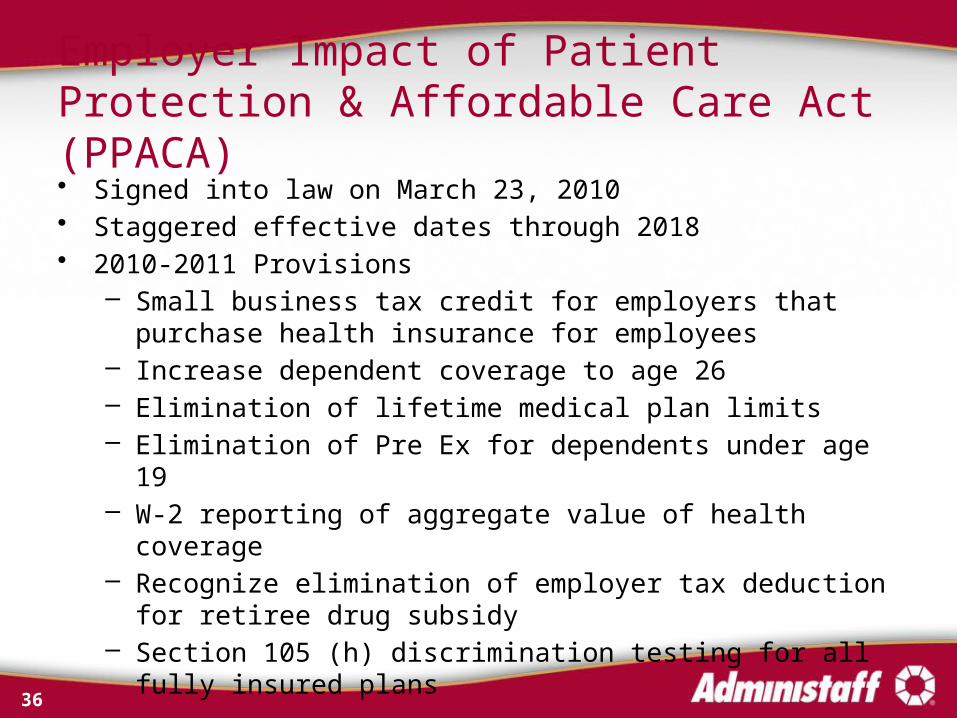

Employer Impact of Patient Protection & Affordable Care Act (PPACA)• Signed into law on March 23, 2010• Staggered effective dates through 2018• 2010-2011 Provisions

– Small business tax credit for employers that purchase health insurance for employees

– Increase dependent coverage to age 26– Elimination of lifetime medical plan limits– Elimination of Pre Ex for dependents under age 19– W-2 reporting of aggregate value of health coverage– Recognize elimination of employer tax deduction for retiree drug

subsidy– Section 105 (h) discrimination testing for all fully insured plans

36

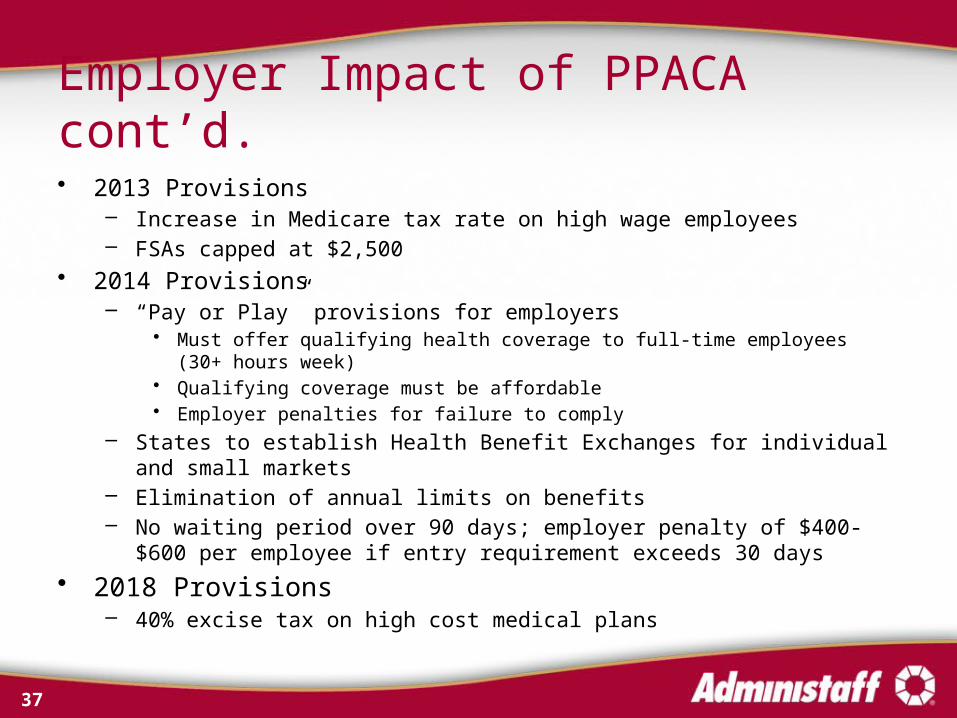

Employer Impact of PPACA cont’d.• 2013 Provisions

– Increase in Medicare tax rate on high wage employees– FSAs capped at $2,500

• 2014 Provisions– “Pay or Play” provisions for employers

• Must offer qualifying health coverage to full-time employees (30+ hours week)• Qualifying coverage must be affordable• Employer penalties for failure to comply

– States to establish Health Benefit Exchanges for individual and small markets– Elimination of annual limits on benefits– No waiting period over 90 days; employer penalty of $400-$600 per employee if

entry requirement exceeds 30 days

• 2018 Provisions– 40% excise tax on high cost medical plans

37

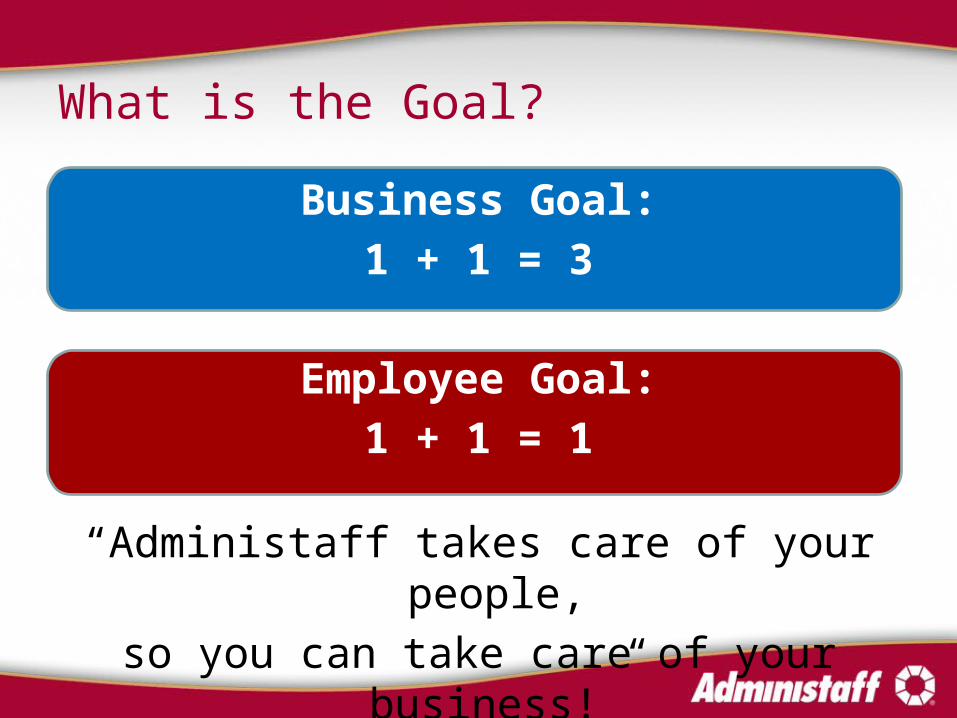

What is the Goal?

Business Goal:

1 + 1 = 3

Employee Goal:

1 + 1 = 1

“Administaff takes care of your people,

so you can take care of your business!”

What are the issues?

• Fast on-boarding of new employees• Risk management (compliance/liability)• Employee morale• Strategic alignment (culture/goals)