www.thefoodproject.org Healthy Food Accessibility in Underserved Boston Neighborhoods: The Affordability and Viability of Farmers’ Markets • Narrative report • PowerPoint presentation (“Getting to the Root of Popular Perceptions”) Robyn Lightner The Food Project / Amherst College The Food Project 10 Lewis Street, Lincoln, MA 01773 7812598621 (p) 7812599659 (f) [email protected]thefoodproject.org

Transcript

www.thefoodproject.org

Healthy Food Accessibil ity in Underserved Boston Neighborhoods:

The Affordability and Viability of Farmers’ Markets

• Narrative report • PowerPoint presentation (“Getting to the Root of Popular

Perceptions”)

Robyn Lightner The Food Project / Amherst College

The Food Project 10 Lewis Street, Lincoln, MA 01773 781-‐259-‐8621 (p) 781-‐259-‐9659 (f)

This whole process was truly a collective effort involving ideas, support, and knowledge from a whole basket full of people. First and foremost, I cannot begin to describe what wonderful mentors my “Boston advisors” Cathy Wirth and Cammy Watts have been throughout the entire course of this project. You both not only hosted me as an unexpected intern last summer, but taught me so much about what it means to have access to healthy food and what it means to work for a cause that you are absolutely passionate about. This report would not have been completed if you hadn’t devoted hours to collecting data in Boston and sending it to me in Amherst, and there’s no way I would have had the motivation and desire to take on the continuation of this study had I not felt your constant encouragement and guidance behind me. Many others deserve great appreciation for the time they spent collecting data for me over the summer and while at school: Cara Brumfield, Farmer Dave Dracut, Tim Diehl, Nebi Stephens, Cynthia Loesch and the B.O.L.D. Teens of Codman Square, and especially Phuong Luong, who could not have been more flexible and willing to help. Here at Amherst, my advisor Kate Sims was the one who proposed the then-‐crazy idea of turning my summer research into a thesis last fall, and she somehow accepted my endless questions and hesitations with remarkable knowledge and reassurance. Always excited to help, Professor Sims gave me the confidence to write and calculate like I never have before-‐ she pushed me to reach a level of academic potential I didn’t know I had and am so grateful to have uncovered. Professor Dizard, you have always managed to bring me back to reality and put such interesting thoughts into my already food-‐filled head-‐ perhaps your most timely piece of advice being “reading kills writing”. Professor Wagaman, had I not felt so confident stepping out of your Statistics class, I would have never agreed to develop this study for The Food Project-‐ your ability to explain new concepts to a humanities person has been invaluable all along. To my roommates and teammates-‐ thank you for always asking questions and at least pretending to be interested in what I was always doing in the library talking about farmers’ markets, and for putting up with all of my weariness and stress, you guys kept me somewhat grounded! And finally, to Mom, Dad, Jeff, and Ry-‐ you have put up with so much but continued to love and support me. I promise you will never have to hear the word “thesis” as an excuse from me ever, ever, again.

6

7

List of Abbreviations

BBB Boston’s Bounty Bucks

BCFF Boston Collaborative for Food and Fitness

EBT Electronic Benefit Transfer

FMNP Farmers’ Market Nutrition Program

FRAC Food Research and Action Center

SFMNP Senior Farmers’ Market Nutrition Program

SNAP Supplemental Nutrition Assistance Program

WIC Woman Infants and Children

8

9

Introduction

For many Americans, the words “clean your plate” conjure up memories of

having to eat those last few spoonfuls of cauliflower or ask for extra juice just to

force down that last brussel sprout. No matter how much gravy or, in my case

ketchup, covered those daunting final bites, day after day they always had in

common a certain despised nine-‐letter word-‐ vegetable. Often the villain in cartoon

shows, vegetables have traditionally become targets of childhood opposition,

subjected to the immature infamy associated with all things good for you. But no

matter how much picky young eaters loathe a side of peas and carrots, their colorful

presence on the daily table represents a nutritional privilege not easily within reach

of many low-‐income urban households.

An absence of fruits and vegetables on the dinner tables of the poor has much

more to do with a lack of access than it does with a lack of affinity for produce. The

current state of the American food system is such that unhealthy diets are more

often than not an economically and practically sensible choice. Attracted by the

relative price and convenience of processed junk foods, it’s no coincidence that a

national health crisis has erupted over a rapid increase in the prevalence of diet-‐

related diseases (Miller, 2010). Thrust into the public conscience, decisions about

what Americans should and should not be consuming have become a huge target of

aggressive research, debate, and reform. Parallel to this growing discussion on all

things food is an increasing emphasis on utilizing local systems of production,

10

particularly with regard to the popularity of fresh, local agricultural harvests.

Several nation-‐wide strategies have encouraged the integration of local farm

products into everyday meals as a method of supporting community economies

while increasing intake of fresh produce. Such programs would seemingly have

more ground to cover in low-‐income city neighborhoods that have historically

experienced reduced access to healthy foods, especially fruits and vegetables, and

consequentially suffered from increased frequencies of diet-‐related health

problems.

Yet many of these deprived neighborhoods are taking action to overcome the

obstacles that have kept fresh produce off their tables by confronting a series

accessibility issues and embracing what their local agriculture has to offer. Section

One of this report explores the national context of healthy food access in low-‐income

areas before focusing on specific characteristics of the Boston food access

environment. Contained in the concept of access are the separate but related

matters of physical availability, affordability, and practical awareness, all of which

are crucial to understanding the challenges facing the introduction of fresh fruits

and vegetables into healthy food deficient communities. Products of the heightened

energy behind local agriculture, farmers’ markets are highlighted as a growing

source of fresh produce across the United States. For low-‐income shoppers, federal

nutrition assistance programs currently include vouchers and coupons specifically

for use at farmers’ markets, and programs at the state level are rapidly expanding to

further incentivize the purchase and consumption of fresh, local produce. An

impetus for healthy food access in the Northeast, Boston Bounty Bucks is one such

11

program that offers SNAP (food stamps) users 50% off their purchase of up to

$20.00 at farmers’ markets and equips vendors with appropriate EBT terminals that

make purchasing with SNAP/EBT possible.

Though a great way to merge support for local environments and economies

with improvements in healthful dietary options, farmers’ markets are afflicted by a

widespread perception that their produce is much more expensive than

conventional grocery produce. As a result, it seems many price-‐sensitive shoppers

categorically reject shopping at farmers’ markets, in turn missing out on an

opportunity to purchase many of the nutritious foods their bodies need more of.

But is this commonly discussed perception true in Boston? With support from The

Food Project and the helpful curiosity of the communities involved, I developed an

observational study to examine this issue by comparing produce prices at farmers’

markets and supermarkets in two underserved Boston neighborhoods throughout

the 2010 summer season. Finding the few previous attempts at investigating

variation in price to prove inadequate-‐ especially for application in poor urban

areas, I confronted the need for an assessment of fruit and vegetable prices that

considers the unique context of farmers’ markets in areas that demand affordability.

Section Two begins with a careful explanation of the design process and

methodology of this study, covering the details of variable selection and data

collection procedures. The analysis component outlines a series of multivariate

regression tests to estimate the difference in price between farmers’ markets and

supermarkets in the defined neighborhoods of Dorchester and Roxbury, and

successively controls for the fixed effects of produce type, time, and quality rating.

12

The two principle findings resulting from this analysis were that 1) on average, the

mean price per pound of produce at farmers’ markets was 2.9% greater than at

supermarkets, after controlling for produce type, time, and quality, and 2) the

quality of produce at farmers’ markets scored significantly better than quality at

supermarkets. Subsequent analyses of seasonality by location and each produce

type separately help show patterns of fluctuation in price over the course of the 16-‐

week season and thus the importance of taking timing into account in similar future

studies. In discussing the results, I draw upon first-‐hand experience and

communication to make several inferences about factors that may have influenced

or caused our findings. With the intent of establishing a replicable method for

future studies of this kind, I also comment on strengths and weaknesses of this

research design throughout the discussion.

In Section Three, I reflect on the benefits of implementing farmers’ markets

in low-‐income areas, focusing on the opportunities for cost-‐savings, higher quality,

and community development, among others. I then go over several barriers that I

feel are most pertinent and crucial to the future viability of Boston farmers’ markets.

In addition to misperceptions about price, operational and administrative duties

impose a major burden on successful market functioning, just as low farmer

retention rates threaten the long-‐term growth of farmer-‐to-‐household relationships.

A brief list of recommendations for action complete my evaluation of healthy food

access in Boston and ideally stimulate further discussion about how the City can

perpetuate recent progress and remain an exemplary model of using local

producers to increase healthy food access for those who need it most.

13

Ultimately, the purpose of my first-‐hand observational research is to

accurately educate Boston communities about the affordability and accessibility of

healthy food in their neighborhoods and to inform the efforts of community groups,

policy advocates, and farmers so collective energies and funds are more efficiently

directed.

14

15

Section 1

Literature Review: Healthy Food Access in Underserved

Neighborhoods

A first step in this investigation is to review existing literature regarding food

accessibility to gain a better understanding of the national context in which this

debate falls. The contention that residents in low-‐income, urban neighborhoods are

disadvantaged by the limited accessibility of nutritious foods is based on the

separate, yet related, categories of healthy food availability and affordability. The

local effects of these issues are subsequently examined in the context of the

immediate Boston neighborhoods at the center of this report. As the focus of my

own research is to investigate differences in the cost of healthy food for a specific

area, I will introduce popular literature on availability and variety of healthy food

options before concentrating on material that more closely relates to the role of

affordability within healthy food accessibility. The second half of my review

narrows in on farmers’ markets, paying particular attention to three very different

studies that have attempted to compare costs between farmers’ markets and

conventional grocery outlets. Finally, I will summarize existing gaps in the

literature surrounding accessibility of healthy food and suggest areas for further

investigation.

16

1.1. Low-income neighborhoods have a higher rate of health problems

Nearly every piece of literature included in this review highlighted the well-‐

researched fact that low-‐income neighborhoods have higher rates of health

problems than more affluent neighborhoods (Larson et al., 2009; Neault et al., 2005;

Winne, 2008). The most frequently mentioned of these health risks are obesity,

childhood obesity, heart disease, malnutrition, hypertension, and type-‐2 diabetes.

Hendrickson et al. (2006) emphasizes the correlation between these health risks

and increased rates of mortality, successfully conveying the problem’s severity and

urgency. In “The Real Cost of a Healthy Diet”, Neault et al. (2008) effectively

juxtaposes rates of under-‐nutrition (consuming too few of some essential nutrients)

and over-‐nourishment (consuming an excess of calories) to highlight the troubling

paradox relating food insecurity and serious heath problems. Regardless of

presentation, the many studies featured in this literature review all underline the

disturbingly high incidences of diet-‐related disease in low-‐income areas that have

prompted such aggressive analysis of food accessibility.

From the Boston Public Health Commission’s annual “Health of Boston” report, it

is obvious that the national trend of increased health problems in low-‐income

neighborhoods is of major concern in Boston communities as well. In 2008, lower

income Boston residents (having household incomes of $25,000 or less) reported

higher rates of asthma, diabetes, heart disease, high blood pressure, and obesity

compared to higher income residents. Roxbury, North Dorchester, and South

Dorchester were three of the five neighborhoods with the highest annual heart

disease hospitalization rate; in particular, Roxbury’s rate was more than 50% higher

17

than the city’s rate overall1 (Health of Boston, 2010). Roxbury and North Dorchester

also reported two of the top three neighborhood rates for asthma hospitalization.

1.2. Low-income neighborhoods have reduced access to healthy food

Along with factors such as exercise level and time spent outdoors, the single

most important and studied factor related to the disparity of health concerns in low-‐

income urban neighborhoods is the accessibility of healthy food. Use of the term

access or accessibility can be interpreted as the physical distance from home to retail

outlets, the types and distribution of food retail located in the region, availability of

transportation to retail outlets, and/or affordability of healthy food. Other relevant

factors such as public food assistance, consumer behavior, community support, and

nutrition education are also explored to some extent. To identify a type of

neighborhood characterized by limited food access, researchers use the term “food

desert”, defined by the USDA as a neighborhood where residents do not have access

to affordable and nutritious food (Whitacre et al., 2009). Beyond this description,

both Walker et al. (2010) and Hendrickson et al. (2006) recognize persistent

inconsistency in the utilization of the term “food desert” and warn that such

significant lack of consensus about which measures are required for identifying food

deserts can only perpetuate the debate about the extent of their existence. Though a

densely populated, low-‐income urban environment is more commonly implied,

Winne’s extensive historical account Closing the Food Gap (2008) demonstrates,

1 Annual heart disease hospitalization rate for Boston was 19.8 per 1,000 population (Health of Boston, 2010)

18

given the multiple factors contributing to the meaning of “access”, a “food desert”

can also describe a rural area having a very small, widespread population.

Despite the confusion in nomenclature, connections between all of the factors

mentioned are important to understanding the accessibility of healthy food within a

certain neighborhood.

1.3. A Closer Look at Accessibility

Availability and variety

Food accessibility for inner-‐city residents is interpreted in this section as the

physical accessibility of food outlets based on geographical factors (i.e. where food

stores are located) and variety/ distribution of retail outlet types. It is widely noted

that in low-‐income urban neighborhoods fast-‐food restaurants and small

convenience stores have always been more prevalent than supermarkets or produce

stands (Winne, 2008). According to Hendrickson et al. (2006), the lack of

competition among the few grocery stores located in inner cities leads to fewer

varieties of healthy or fresh food for consumers, and the availability and variety of

certain food products, particularly fresh fruits and vegetables, varies greatly among

stores located in different neighborhoods. Additionally, the issue of lack of

transportation is echoed throughout the literature citing that many low-‐income

households do not have access to a car and cannot afford the costs associated with

getting to a supermarket outside of their immediate neighborhood (Walker et al.

2010). As a result of this lack of transportation, low-‐income households are less

likely to travel the distance to a supermarket outside of their neighborhood and will

purchase food items from the stores that are nearby, often possibly sacrificing cost

19

and quality for convenience (Hendrickson et al., 2006). Further, among households

with limited transportation, one survey uncovered a trend where families made one

or two trips per month outside their neighborhood to the supermarket to purchase

non-‐perishables, and relied on local suppliers (and their limited selection) for day-‐

to-‐day perishables (Whitacre et al., 2009). Though the limitations of smaller

convenience stores are well cited, at the more human level there also exists a

common inclination among residents to frequent their local store to maintain

loyalty and a relationship with the owner (Whitacre et al., 2009).

Such a pattern of reduced availability has been examined in the Boston area

and shown to exist in several dimensions. The “Real Cost of a Healthy Diet”, a report

published by the Boston Medical Center, investigated the availability and cost of the

USDA’s “Thrifty Food Plan”* in Boston food outlets and found that, on average, 16%

of the plan’s items were not available in surveyed stores. Similarly, a survey

conducted by the “Boston Collaborative for Food and Fitness” in six low-‐income

neighborhoods, including the three featured in our study, showed that an average of

33% of food retail locations did not carry any produce. Note: all types and sizes of

retail stores were included (bodegas, mega-‐markets, restaurants, fast food, etc.)

with the exception of direct retail farmers’ markets.

Affordability

The literature indicates a general consensus that low-‐income households pay

more for their food, largely due to the prevalence of higher priced small-‐sized

* The TFP consists of food lists and menu plans that serve as the national standard for a nutritious diet at the lowest possible cost. This cost-specific food plan guides national nutrition policy in the U.S. (such as determining maximum food stamp allotments) (Neault et al., 2008).

20

convenience stores in surrounding neighborhoods (Larson et al., 2009; Neault et al.,

2005; Whitacre et al., 2009). Likely reasons for higher prices in low-‐income, inner

city areas were suggested at “The Public Health Effects of Food Deserts” workshop

hosted by the Institute of Medicine and National Research Council in 2009

(Whitacre et al.). In these neighborhoods high crime and theft rates induce extra

security costs for businesses, while low employee-‐labor skills, lower sales volume,

and high turnover rates lead to higher operating costs. Additionally, inner cities

have less available land and more zoning restrictions so large chain stores prefer to

locate in the suburbs. Finally, low competition among the few grocery stores located

in urban areas may lead to higher prices for local residents (Walker et al., 2010).

USDA studies are widely used to validate this theory, finding that the prices in

smaller, independent markets are at least 10% higher than prices in larger

supermarkets (Whitacre et al., 2009; Walker et al., 2010). However, while these

USDA studies include all types of small (and large) food retail outlets in both high

and low-‐income urban neighborhoods, they fail to differentiate between

neighborhood income types. Because of such indiscriminate collection of price data,

this aspect of USDA research does not necessarily illustrate a relationship between

small retail stores in low-‐income neighborhoods and higher prices. Another USDA

report found that urban supermarket prices are higher than suburban prices, but

again did not break down the analysis to examine differences in socioeconomic

makeup of the urban (and suburban) areas. Most effectively, Hendrickson et al.

(2006) used an appropriately comprehensive approach of consumer surveys

combined with statistical analysis and found that food prices are higher and food

21

quality is poorer, often inedible, in areas where poverty is the highest, compared to

more affluent areas, concluding that residents living in areas without a supermarket

do in fact pay more for their food. Thus, healthy foods are less accessible to inner

city residents in terms of affordability in addition to geographical location and

variety of retail outlets.

The affordability of healthy food is a problem in Boston. The average

monthly cost of the Thrifty Food Plan in Boston was 39% higher than the USDA’s

reported cost. Several studies also demonstrate the fact that residents in poorer

Boston neighborhoods cannot afford their food. For example, of 574 people

interviewed by BCFF in low-‐income neighborhoods including Dorchester and

Roxbury, 59% said their household grocery purchases were affected by rising food

prices, 17% reported skipping meals, and 13% said they served fewer vegetables

(BCFF, 2010). When asked about the prevalence of fruits and vegetables in their

diets, 60% of respondents in these neighborhoods did not eat vegetables on a daily

basis and 14% reported no consumption at all (the numbers for fruit consumption

were equally dismal, at 65% and 16%, respectively) (Kim, 2010).

1.4. Impact of Rising Food Prices on Low-Income Households

With 2011 came a wave of increased commodity costs that struck Americans’

shopping carts hard, but rising prices were no newcomers to the produce section.

Over the last four years, one study in Seattle found that food prices rose significantly

and disproportionately-‐ 25% for the most nutritious foods (including produce) and

16% for the least nutritious and junk foods (Miller, 2010). According to the

Nationally-‐released Consumer Price Index-‐ which measures changes in costs for

22

dozens of living expenses, in December 2010 the overall food price index rose by 0.1

% while the fruit and vegetable price index rose 1.8 % (BLS, 2010). The number of

Americans receiving SNAP benefits has surged by 58.5% over the last three years

(Miller, 2010), and a report released by the Food Research and Action Center

(FRAC) earlier this month said almost 1 in 5 Americans struggled to afford food for

their families in 2010, with some of the highest rates of food hardship occurring just

last fall. Yet no relief is in sight for these households as an ominous release by the

Department of Agriculture expects overall food prices to rise 3 to 4% this year alone

(USDA, 2010). M. Fisher (2009) explains that rising food prices have the tendency

to affect lower income more than higher income consumers because they spend a

larger amount of their income on food. Limited budget households also react by

devoting a larger share of their food expenditures to non-‐perishable staple foods

like corn, wheat, and rice, leaving only a paltry share for nutritious fresh fruits and

vegetables (Fisher, M., 2009). And more substantially than for other types of food,

an increase in price of fresh produce correlates directly with a decline in

consumption, implying that when food prices rise, price-‐sensitive households may

further cut down on their already low intake of fruits and vegetables (Coleman et al.,

1968).

In addition to the recent rise in food prices, Boston has historically reported

more expensive food costs than most American cities, intensifying the burden for

consumers on limited incomes. In 1966, Boston had the 3rd highest retail food price

index across 20 major cities (Coleman, 1968) and the pattern continued as of

December 2010, when Boston reported the 2nd highest food price index (after New

23

York) and spent about 28% more than the national average on fruits and vegetables

(BLS, 2010). The city’s astounding 91.9% growth in SNAP participation between

May 2005 and May 2010 (enrollment of 57,052 and 109,049 person, respectively)

shows that Boston households are desperately trying to cope with the reality that

they can no longer afford to feed their families (Vollinger, et al., 2010). Particularly,

a substantial 17,000 (roughly one third of) Dorchester residents are currently

dependent on federal assistance for food, with $34 and $7 million in SNAP

redemptions at the neighborhood’s supermarkets and convenience stores,

respectively (Zarrell, 2011). A recent BCFF survey found that 51% and 63% of

surveyed residents in Dorchester and Roxbury claimed their grocery purchase were

affected by higher food prices; specifically, 12% and 8% of families in these

neighborhoods said they were serving fewer vegetables-‐ numbers that are even

more disturbing considering only 50% and 25% of residents reported eating

vegetables every day (BCFF, 2010). At a time when conventional food outlets are

forced to assume greater commodity costs that must be transferred to the customer

and eventually paid back into the massive food production industry, farmers’

markets take on the increasingly important role of local producers and suppliers,

helping to strengthen the economy of local communities by keeping money

circulating nearby.

1.5. Expansion of Direct Retail Outlets- “Farmers’ Markets”

With increasing attention around issues of healthy food accessibility,

communities around the United States are mobilizing to make fresh produce

available and affordable to low-‐income communities. One of the most effective ways

24

has been through the creation of farmers’ markets in low-‐income areas. When

paired with federal nutrition assistance program benefits, farmers’ markets are

becoming an increasingly important source of fresh, local produce for urban

residents (Winne, 2009). The most recent literature almost always mentions the

rapid growth of farmers markets over the last decade, as highlighted by the USDA

data indicating a 300% increase in the number of farmers markets between 1994

and 2009 (Pirog and McCann). Most recently, the 2010 National Farmers Market

Directory lists 6,132 operational markets, showing a 16% increase from 2009.

Research using consumer surveys has also verified a number of reasons why

individuals patronize farmers markets, such as perceived freshness and taste,

supporting local business and community building (Pirog and McCann, 2009),

enjoyment of relationships with producers, an opportunity to assist the small

producer (Sommer et al. 1980), perceived higher vitamin index, freshness, and

many others. The development and promotion of farmers’ markets is most

popularly emphasized as a strategy to increase neighborhood fruit and vegetable

consumption as part of a healthier lifestyle; more so, establishment of a farmers’

market is a way to foster community partnerships, support local agriculture,

develop leadership in youth, and reconnect urban areas with the natural food

system (Winne 2008).

While its healthy food access gap runs parallel to the problematic national

trend, Boston has become an outstanding leader at the front of a more promising

national movement-‐ the expansion of universal access to farmers’ markets.

According to Jeff Cole, executive director of the nonprofit Mass Farmers Markets,

25

Boston has “more farmers markets per capita than any other city in the United

States”, a claim backed by the city’s 2010 count of 27 markets, representing more

than a 30% increase since 2008 (Denison, 2010).

1.6. Expansion of Federal Assistance and Incentives to Farmers’ Markets

Though the significant increase in the prevalence of farmers’ markets is a

more recent trend, the government acknowledged affordability as a barrier to their

success with low-‐income populations nearly two decades ago (Schumacher et al.,

2009). To promote the consumption of fresh produce among low-‐income

Americans, the USDA created programs to supplement existing federal food

assistance dollars and encourage consumers to shop at farmers’ markets. The

Farmers Market Nutrition Program (FMNP) began providing additional subsidies

toward purchases at farmers’ markets for WIC participants (low-‐income Women

Infants and Children) in 1992 and later expanded those benefits to low-‐income

seniors in 2000 with the Senior Farmers Market Nutrition Program (SFMNP)

(Schumacher et al., 2009). To help make produce at farmers’ markets even more

affordable to low income populations, several states have recently implemented

pilot incentive programs that provide matching or bonus funds for SNAP, FMNP, and

SFMNP dollars used at farmers’ markets. Though most of these programs are still in

their infancy, Schumacher et al. report “early qualitative evidence shows these

programs to be successful at attracting low income customers to farmers’ markets,

getting low income customers into the routine of shopping at farmers markets, and

increasing sales for farmers’ market vendors” (Schumacher et al., 2009).

26

Confronting the affordability hurdle, Boston, with the support of Wholesome

Wave, Farm Aid, Mayor Menino, and The Food Project, introduced the “Boston

Bounty Bucks” farmers’ market subsidy program in 2008. To allow customers the

option of purchasing produce with their SNAP/EBT cards, this program first equips

vendors with wireless EBT terminals, along with proper training, funding for

terminal usage fees, and technical support. For the hundreds of Boston residents

that depend on federal nutrition assistance and have been previously limited to

conventional grocery and convenience stores, the ability to buy fresh, local fruits

and vegetables from a farm stand offers a different environment that makes buying

and consuming produce more appealing. The program’s main incentive is to

provide matching funds for customers that use SNAP/EBT dollars at participating

farmers’ markets (up to $20). In addition to increasing the purchasing power of

people with low incomes and broadening the customer base at farmers markets, this

double voucher program supports local farmers and producers willing to sell in low-‐

income neighborhoods (Schumacher et al., 2009). A 2009 survey on the progress of

the Boston Bounty Bucks program reported $20, 093.77 in SNAP and matching BBB

purchases at thirteen participating farmers’ markets, and found that customers

credited the subsidy program as an important factor in their increased consumption

of fruits and vegetables (Kim, 2010). By 2010, twenty-‐one farmers’ markets

throughout the Boston metropolitan area participated in the BBB program and the

usage of SNAP ($41,402.28) along with BBB matches ($36,409.46) combined for a

total of $77,811.74 in sales-‐ a 387% increase over the previous summer.

Representing 28.5% of total Boston sales, the ten markets located in Dorchester and

27

Roxbury reported a total of $21,699.58 in combined SNAP/BBB sales (The Food

Project, preliminary report, 2011).

1.7. Relative Cost of Direct Retail: Consumer Perceptions

There exists a widespread popular perception that farmers’ market produce

is more expensive than produce in conventional supermarkets (Jones, 2009).

Evidence comes from Grace et al.’s (2005) survey of shoppers at a farmers’ market

in Portland, Oregon. The study found that 22% of participants mentioned price

when asked what would influence them to use farmers’ markets regularly, claiming

that farmers’ markets were too costly for their budgets and decidedly more

expensive than conventional grocery options with statements like “markets offer

higher quality produce than grocery stores, but prices are unreasonable”, and

“farmers’ markets are for rich people”. Not surprisingly, nearly 42% of those who

discussed price as a major factor had never been to a farmers’ market before,

inferring that outside information-‐not personal experience-‐ caused them to form the

perception that farmers’ markets are expensive. The survey also impressively

identified that many shoppers believed farmers’ markets sold mostly organic

produce, which they identified was categorically beyond their price range and thus

not worth the trip.

These perceptions may be fed by the cultural popularity of buying local in

affluent communities, the placement of a higher premium on local produce with the

expectation that it has fewer chemical preservatives, the presence of expensive

artisanal and specialty goods at farmers’ markets, or possibly a reality of higher

prices. However, many proponents of direct-‐retail insist that lower prices are more

28

likely because farmers’ markets allow farmers to sell their produce directly to the

consumer, avoiding the expense of a middleman and rising fuel costs (Larsen et al.,

2009). Another common discussion emphasizes the impact of produce seasonality

on prices, as direct-‐retail outlets may be able to provide lower prices on in-‐season

produce than supermarkets (Sommer et al.).

1.8. Relative Cost of Direct Retail: Previous Research

The confusion over whether farmers’ market produce is indeed more or less

expensive that supermarket produce is perhaps most perpetuated by the

outstanding lack of relevant price comparison studies available. I shared this

frustration in my attempts at recovering appropriate literature and learned that

other researchers were equally disappointed at the underdevelopment of this

investigative cause (Larsen et al. 2009, Jones 2009, Pirog and McCann, 2009).

Undoubtedly the first study to compare the prices of produce at farmers’

markets with those at conventional supermarkets, Sommer et al.’s 1980 “Price

Savings to Consumers at Farmers Markets” is worth great attention. As the study

celebrates its 30-‐year anniversary, many statements seem ancient compared to the

sweeping farmers’ market trends of today and thus are difficult to relate to current

accessibility issues. Nonetheless, Sommer et al. (1980) showed similar enthusiasm

for the establishment of 24 Markets in California due to a renewed interest in

farmers’ markets for their direct marketing, “exciting shopping experience”, and an

“opportunity for city and country people to come together”. The results of the study

showed a statistically significant difference where overall unit costs at the farmers’

markets were 34% lower than overall unit costs at nearby supermarkets.

29

Sommer et al.’s methodology was carefully planned and succeeded in several

areas. The study was conducted at 15 out of 18 then current California Farmers’

markets and 2-‐3 nearby supermarkets over the summer and fall seasons which

allowed for the collection of many data points and adequately accounted for

seasonal variability. One drawback is that when different pricing systems were

used in corresponding retail outlets (ex. apples sold by the basket and apples by the

pound), these products were simply omitted from the study rather than using a

simple standardization calculation to avoid the loss of data. The study also cross-‐

compared city size with price; and though no significant findings resulted, it

indicates a realization that not all farmers’ market environments are comparable.

Although Sommer et al.’s study is dated, as one of the first contemporary studies of

its kind, it is crucial to analyze the design of these studies in order to develop a

better standard for this area of research.

A 2009 study conducted by Pirog and McCann employed the use of a “market

basket” sample of foods across farmers’ markets, supermarkets, natural foods

markets, and butcher shops in Iowa to compare the prices of locally grown foods

and foods procured from a national distributor. They found that the mean price per

pound of vegetables sold at farmers markets ($1.25) was 10% lower than at

supermarkets ($1.39), but the difference between these values proved statistically

insignificant.

Pirog and McCann credit competitive pricing of summer squash at farmers’

market (due to seasonality, supply, or weather) with skewing the advantage toward

locally grown foods. Regarding data collection methods, the developers enforced

30

very strict procedures in order to maintain consistency; however, I believe the

choice of collection period overshadows these efforts and is the prime reason

behind this study’s lack of significant data. By using only 5 data points between July

and August, which the authors admit represents the “height of local fresh fruit an

vegetable availability in Iowa”, along with a selection of crops that are particularly

abundant during that time, the locally-‐grown results were predisposed to reflect the

extreme variation in price related to crop production (non-‐local summer squash

was nearly twice the price of local varieties). Such results were likely expected and

may have been desired by the researchers in order to support their organization’s

local and sustainable agriculture initiatives.

A Seattle University Business class in partnership with the city’s

Neighborhood Farmers’ Market Alliance conducted another study with potentially

similar motivation. The May 2010 study, led by Professor Stacey Jones, concluded

that prices at the main Seattle farmers’ market were nearly 30 percent lower, on

average, than those at one supermarket, but did not differ significantly from prices

at the two other surveyed supermarkets. Having collected data only over the course

of five consecutive days in May and using very different types of supermarkets,

among other drawbacks, the students’ admission that their study is far from

comprehensive seems correct. Again, the condensed sampling period does not

provide for an analysis of a trend, but rather of a specific event.

These observational studies vary in process, purpose, and accuracy,

reinforcing a need for the development of better, more uniform methodology

31

comparing produce prices at supermarkets to prices at direct retail outlets, and

specifically at farmers markets.

1.9. Conclusion

This review demonstrates the breadth, complexity, and interconnectedness

of national food access issues that contribute to the confusion of public, and even

academic, perceptions about the ability of underserved neighborhoods to access

healthy foods. Still, noticeable gaps in the literature exist. While several studies

have examined supermarket access for low-‐income households, very few have

explored the impact on food prices or nutritional benefits or alternative food

purchasing options like farmers’ markets. Further research should be directed at

measuring the immediate impact of funding allocated to farmers’ markets in low-‐

income urban environments in order to demonstrate tremendous improvements in

food access and strengthen proposals for necessary future funding.

Finally, the need for a replicable methodology for comparing produce prices

at conventional grocery outlets with those at direct retail outlets is very clear. This

methodology should ideally include strategies that account for the hard to measure

effects of seasonality and quality, and also consider the impact of public food

assistance. Most importantly, it is clear there is a need for neighborhood-‐specific

price comparison studies to address the concerns of local consumers. Through the

creation of an agreed-‐upon, replicable method of price analysis, efforts to improve

food access in underserved neighborhoods across the nation will be made more

visible. By developing and conducting a pilot study in two Boston neighborhoods

32

that have become leaders in the community-‐guided healthy food access movement,

the observational phase of this report aims to contribute to this process.

33

Section 2

Observational Study: The Affordability of Farmers’ Markets in

Underserved Boston Communities

1. Overview

This study uses comparative price analysis of produce items to assess the

relative costs of produce at local farmers’ markets and supermarkets in the Boston

neighborhoods of North Dorchester, South Dorchester, and Roxbury. In this section,

I begin with the methodology of this study: the identification of direct-‐retail

(farmers’ markets) and conventional grocery outlets within the defined

neighborhoods, an explanation of how a variety of produce types were deemed most

appropriate for the time and demographic focus at hand, and a detailed description

of how price and quality data were collected. Next, I outline a series of regression

tests used in the statistical analysis of data, and present results on variation in

availability, quality, and price per pound. The final section is a comprehensive

discussion of statistical and observational results, along with conclusions and

inferences derived from relevant information about the circumstances surrounding

produce production and distribution at these retail environments. Cammy Watts

and Cathy Wirth, on behalf of The Food Project (Boston, MA), supervised the

development and completion of this study over the course of the summer of 2010;

hence, the plural “we” is used when referring directly to the study’s design and

fulfillment.

34

2. Objectives

The main goal of the study was to learn how the price of produce differs

between farmers’ markets and supermarkets in these neighborhoods, if at all. Since

farmer’s markets in low-‐income areas are unique and often feature different price

points than markets in more affluent areas, our efforts were focused entirely on the

retail options specific to a defined geographic area. While this limits generalization

of the results to a broader, more economically diverse area, it emphasizes the need

for food access research that is more concentrated on specific urban demographics

and communities. As low-‐income communities suffer disproportionately from diet

related disease, it makes sense to focus research on food access in these areas. A

second major goal of this study is to pilot a methodology for comparing produce

prices and other observational data for other researchers. Without a replicable

model, the compilation of a larger, more useful set of local and national price data

will not be possible. Additionally, I will include our secondary efforts to assess

produce quality at all locations, recognizing that the subjective nature of this

analysis makes it a more complex challenge.

3. Methodology

3.1. Variable Selection

The study identified the geographic area of interest as the neighborhoods of

North Dorchester, South Dorchester, and Roxbury. These neighborhoods were

chosen based on similar socio-‐economic statistics, proximity to one another, high

density of farmers’ markets, diversity of cultural backgrounds, and the nature of The

35

Food Project’s relationship with and past research into these communities. These

neighborhoods consist predominantly of people/ families on limited incomes

(Health of Boston, 2010). Recognizing the high rate of chronic disease related to

poor eating habits in this area, we also feel that this population could greatly benefit

from more information about the availability of fresh, healthy food within this

specific area (Health of Boston, 2010).

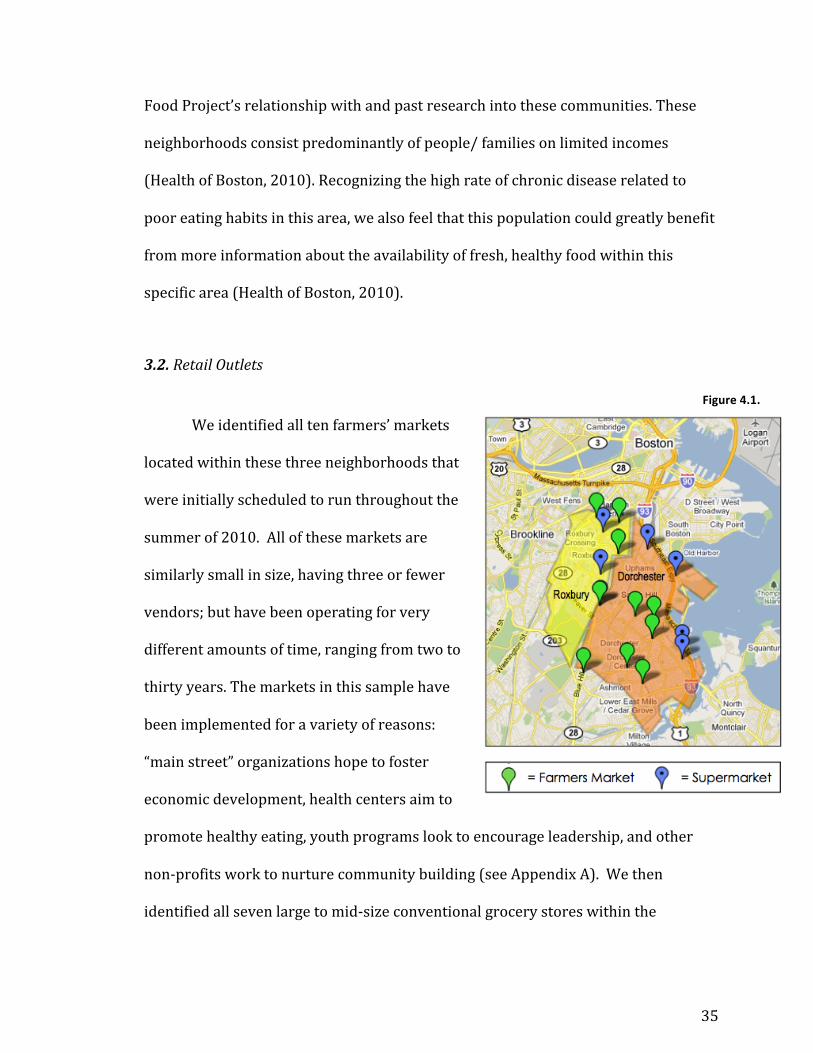

3.2. Retail Outlets

We identified all ten farmers’ markets

located within these three neighborhoods that

were initially scheduled to run throughout the

summer of 2010. All of these markets are

similarly small in size, having three or fewer

vendors; but have been operating for very

different amounts of time, ranging from two to

thirty years. The markets in this sample have

been implemented for a variety of reasons:

“main street” organizations hope to foster

economic development, health centers aim to

promote healthy eating, youth programs look to encourage leadership, and other

non-‐profits work to nurture community building (see Appendix A). We then

identified all seven large to mid-‐size conventional grocery stores within the

Figure 4.1.

36

geographic area based on conversations with residents regarding the most

frequented stores. All of the retail outlets accept EBT/ SNAP and WIC coupons; all of

the farmers’ markets also accept FMNP coupons, senior coupons (SFMNP), and

participate in the Boston’s Bounty Bucks double voucher program (which provides a

50% discount for EBT card users up to $20).

3.3. Time Periods

Using the anticipated starting and ending dates for the

markets, we identified a sixteen-‐week period from July 5 to October

24 during which all of the farmers’ markets would be open for the

2010 season. To account for predicted fluctuation in produce price

and availability throughout the market season, this period was

divided into eight separate 14-‐day periods. Data for each location

was collected exactly one time within the same time period, and is

assumed to be representative of average values during those 14

days.

3.4. Produce Types

The study identified ten types of produce that represented common “staple”

food items for the local population. This list also reflects a selection of items that we

found, through research and inquiry with vendors in the study, would be most

readily available at markets throughout the course of the season. Further, we chose

items for which specific type/ growing conditions are not as important (compared

to the price differences among varieties of apples, for instance). This list is very

Figure 4.2.

37

specific in its description of each item in order to ensure that the most consistent

samples of produce are being compared across all of our collection locations.

• Carrots: unpeeled, w/ green tops and w/o green tops

• Cucumbers: unwrapped, not English

• Onions (yellow): large, loose (not bagged)

• Tomatoes (field): about fist size, not hot house/ greenhouse, not heirloom, no

vine

• Zucchini: green summer squash

• White Potatoes: loose

• Scallions: green onions (not red bulb)

• Lettuce: green leaf, romaine/ Bibb variety, not bagged/washed/trimmed

• Bell Peppers (green): loose

• Green Beans: loose

3.5. Vendor Research

Realizing that some Farmers’ Markets feature more than one vendor, we

looked into a sample of vendors selling goods across all of the markets. For each

vendor, we researched and recorded information that would be relevant to the

quality of the items being sold at the markets; such as, organic certification (if any),

growing methods/ pesticide usage, amount of time elapsed between point of

harvest and point of sale, distance from point of harvest, non-‐profit status,

strategies/ methods of price variation at different places of vending, etc. (see

Appendix D). For each supermarket, we investigated similar factors related to the

quality and background of the items being sold.

3.6. Data Collection

38

The study consists of first person observations and data collection (see

Appendix B) at all farmers’ markets and supermarkets throughout the course of the

2010 summer market season, defined as July 5 to October 24. All observations per

time period were taken within the same 14-‐day span, each period beginning on a

Tuesday and ending on a Monday. Based on farmer and vendor interviews, we

assumed that farmers’ market prices were consistent throughout each respective

day the market was operating and did not fluctuate from market opening to closing

on the date observations were made2. All individuals who collected data at any

point throughout the survey went through a training workshop prior to collection in

order to ensure consistency of data collection at all times and locations (see

Appendix C). All vendors were notified of our study prior to collection in order to

enable cooperation and support.

For each item at a location, the price per pound was recorded as labeled;

however, many items were sold in a unit other than pounds (per head, per bunch,

per bag, per each). In this instance, a random sample of three units was weighed on

a scale to obtain an average weight for that item at that location. The price per unit

was then converted to a price per pound based on the average weight of the item in

each random sample. An average price per pound was collected for each vendor

independently and later combined into an overall mean price per pound for each

market. At each farmers’ market, prices from all vendors were observed to the best

of our ability but may have varied according to availability of item, cooperation of

2 Several vendors frequently dropped prices at the end of the market to move produce, but we did not have the capacity to capture time discrepancies in price for each market and hope staggered collection times account for some of this potential discount opportunity.

39

vendor, and precision/accuracy of scale(s) used. If an item was not available for any

reason, its price was not recorded, even if it had been available earlier in the market.

At each conventional market, the same process was implemented with

regard to non-‐pound units. In the case that more than one option of a produce type

is on display, we recorded data for the smallest, most conventional (i.e. non-‐organic)

unit sold. This means that if loose field tomatoes were available in both organic and

non-‐organic varieties, we would record data for the non-‐organic variety; or, if

carrots without greens were available only in 2 lb., 5 lb., or 10 lb. bags, we recorded

data for the 2 lb. bag. While aware that several conventional supermarkets have

volume or “loyalty card” discounts available, we did not take these into account

because such discounts were not consistent with farmers markets’ pricing schemes

and because low-‐income households are often cash-‐constrained and not able to take

advantage of such bulk purchasing.

Data collection also included recording an indicator of visual quality.

Collectors commented on and ranked the overall visual quality of the produce type

on display using a scale of 1 to 3 where 1= “wouldn’t buy the item”, 2= buy “item

only if necessary”, and 3= “excited to buy and use item” (see Appendix E for

examples). In some cases, collectors couldn’t decide between whole numbers and

resorted to using 1.5 or 2.5. In order to treat quality consistently, all half-‐number

values (50 total) were rounded toward the mode rating for the same produce item

at the same vendor or supermarket across all time periods.

There were a few occasions when it was found at the last minute that none of

the collection proxies were able to collect the data for a certain location for a time

40

period or there was a miscommunication where a market was missed entirely. In

these cases we conducted phone interviews with each vendor immediately upon

realizing the mistake in order to collect their availability and prices from the most

recent missed market. For example, the Ashmont farmers’ market was rained out

on the second Friday of collection period 3 and the data had not been collected on

the first Friday, so we acquired information about what was available at the first

Friday’s markets and what the prices were. Since we could not be present to weigh

items sold in units other than pounds, we interpolated unit weight by averaging

average unit weights for one unit of that item across all time periods and used the

period of interest’s unit price to calculate a standardized price per pound value. So

to approximate the price per pound of carrots sold for $2.50 per bunch by Spring

Brook Farm (Vendor) at the Ashmont Farmers’ Market during time period 3, we

calculated the average unit weight of a bunch across all time periods that it was

available [(.75+1.33+. 93)/3= 1.00 lb.], then followed the standardizing calculation

used for all data [$2.50/1.00 lb. = $2.50/lb.]. While we initially withheld data for

non pound units when corresponding unit weight was not provided, because of the

number of missing data points overall due to highly varying produce availability

from week to week, we felt it was reasonable to estimate these data points because

we were certain the item was available at the time but it was logistically impossible

to obtain a unit weight. The same averaging process was also done to obtain each

items estimated visual rating. Data for a certain price in a certain time period was

never interpolated for a produce item that was not available during that period, as

41

we recognize availability is an important factor in reviewing produce at both

farmers markets and supermarkets.

4. Statistical Analysis

4.1. Statistical Method

The primary goal of this analysis was to determine the difference, if any,

between price per pound of produce items at farmers’ markets and price per pound

of produce items at supermarkets. We also wanted to determine whether the

difference between price and retail location type could be explained by other

variables, namely produce type, time period, and quality rating. Multiple regression

was used to control for these other variables.

Regression analysis uses one response/dependent variable and one or more

predictor/independent variables to estimate a mathematical model that describes

the direction and strength of the relationship between these variables of interest

(Kleinbaum et al., 1998). Forming a model with various parameters based on a

research question allows for the construction of hypotheses that can be tested to

provide information about a certain parameter’s slope estimate and its significance.

After reviewing all of the collected data, I specified a series of models and

hypotheses for the effects of single and combined variables based around mean

price per pound as the important outcome variable of interest. Statistical analyses

were performed using STATA, version 9.0 (StataCorp, College Station, TX, 2008).

4.2. Defining the Regression Model

42

In defining the regression model, I concentrated on constructing a model

most relevant to the research question of “How does the mean price per pound

(PRICE) change with variation in location type (LOCATION), while produce type

(PRODUCE), time period (TIME), and quality rating (QUALITY) are held constant?”

For this model, the dependent variable throughout the succeeding regression tests

is the standardized mean price per pound [PRICE (Y)] of a fixed amount of a

produce item. All four independent variables of interest are categorical and are

added in succession to assess relative importance and individual trends. To

distinguish between the two options for the non-‐fixed independent variable

LOCATION, the codes 1=Farmers’ Market or “FM” and 0= Supermarket or “SM” were

used. The numbers 0-‐7 correspond to the eight periods of TIME, the numbers 0-‐9

identify the ten unique types of PRODUCE, and the numbers 0-‐2 are used

categorically to denote QUALITY rating along the previously described 1-‐3 scale of

assessment. These variables were then converted into sets of dummy or indicator

variables for each time period, produce, and quality category.

Note that if a nominal variable has k categories, then k-‐1 indicator variables

are assigned to index these categories because the first level of each nominal

variable is indicated by the presence of zeros in all of the hypothetical reference

cells (i.e. there are a total of 8 time periods, but only seven indicator variables are

used because “time1” is actually the indicator variable of time period 2, “time2” is

the indicator variable for time period 3, and so on). The complete population

regression model below represents the full model of price variation between

locations while controlling for fixed effects with each set of indicator variables. As

43

was mentioned earlier, fixed effects are added in succession to provide alternative

angles of analysis. The command “robust” is added to account for the fact that there

may be heteroskedasticity in the error terms.3

The value of β0 represents the intercept and varies according to the equation,

and the reported value of β1 represents the estimated coefficient of variation for the

variable of primary interest, which is the location of the sale.

4.3. Description of Sample

Preliminary descriptive statistics (Table 4.1) relate a helpful outline of the

data before introducing and controlling for other variables. Out of 1760 possible

observations of price (and quality) at both farmers markets and supermarkets at the

outset of this study, a total of 1032 data points were actually recorded. Despite the

initial over-‐representation of possible observations at farmers’ markets due to a

higher number of vendors and collection sites, both location types have fairly equal

representation in the final data set, with 52% from farmers markets and 48% from

3 This will tend to give more conservative estimates of the standard errors (and p-‐values).

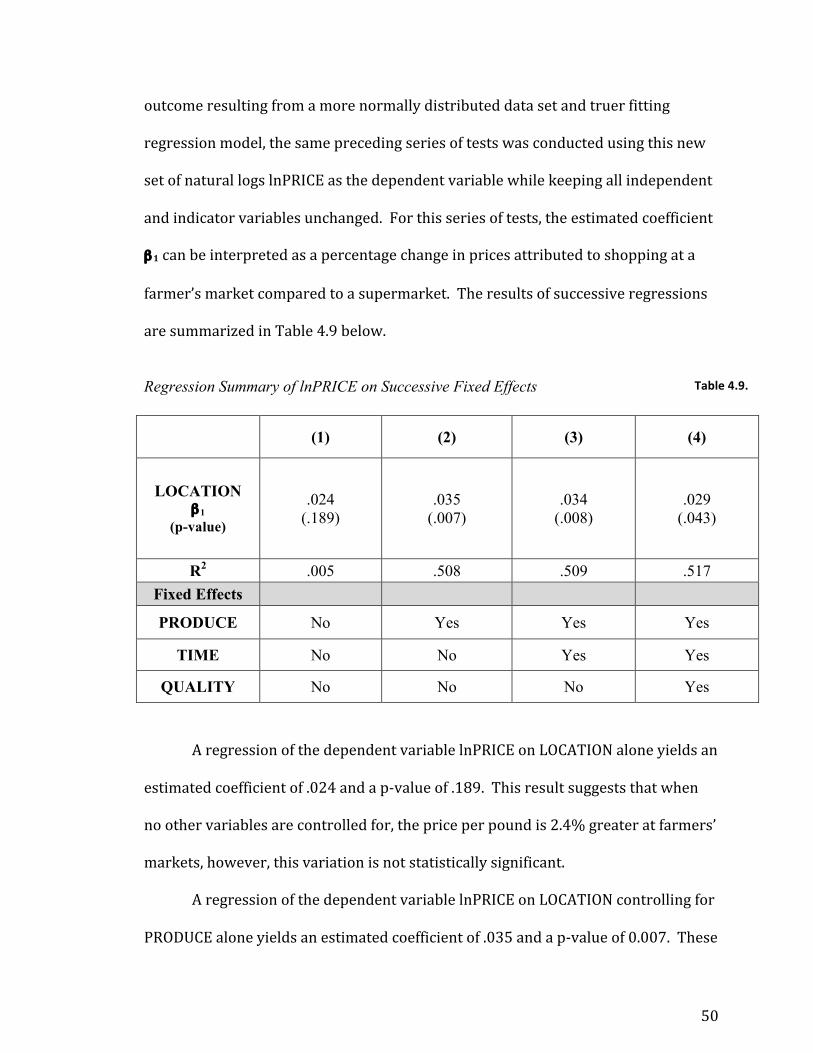

A chart of TIME vs. PRICE for each location type without accounting for

produce type or quality rating (Figure 4.4) illustrates how overall mean price at

each location type varies throughout the 8 time periods. An overall decreasing

trend in mean price per pound at farmers’ markets is contrasted with a relatively

constant and ultimately increasing trend at supermarkets. At farmers markets,

there was a 14% initial drop in mean price across time periods 1 and 2, followed by

a slight increase from period 3 to 4, and ending with another large decrease of 19%

over the final four time periods. Supermarkets reported a very constant mean price

from time periods 1 through 7, never deviating more than 0.03 from the mode 1.69,

but saw about a 10% increase during time period 8. Interestingly, the largest

differences in mean price per pound occurred during the very first and last time

periods. In time period one, mean price at farmers’ markets ($2.01) was about 18%

higher than at supermarkets ($1.70); while in time period 8, mean price at

supermarkets ($1.89) was a striking 28% higher than at farmers’ markets ($1.48).

Introduce Produce Type

Graphs of TIME vs. PRICE at each location type for each produce item

separately demonstrates how overall mean price for each type of produce varies by

location over the course of the summer season (see Appendix I). First, cucumbers

at farmers’ markets exhibited a slightly decreased price trend overall (though still

significantly more expensive than at supermarkets), marked by a notable sudden

decrease in mean price/lb. by about $0.40 during time period 6 (9/13-‐9/26). A very

similar pattern was followed by farmers’ market bell peppers, which exhibited a

momentary $0.60 decrease in mean price/lb. during the same time period 6 (see

57

figure 4.5). Interestingly, zucchini showed an opposite pattern, with an overall

increasing trend punctuated by a momentary $0.50 increase in mean price/lb.

during week 6. The mean price/lb. of carrots dropped rapidly by $0.50 during time

period 4 (8/16 -‐8/29), recovered, then dropped rapidly again by nearly $1.00

between periods 6 and 8 (9/13-‐ 10/24). The price/lb. of scallions spiked by $1.50

during time period 4 (8/16-‐8-‐29), and the price/lb. of lettuce spiked by about $1.25

during time period 5 (8/30-‐9/12) (see figure 4.6). Onions demonstrated a rapid

decline of about $1.40 from the start of the study until time period 3 (7/5-‐8/15),

and then remained relatively stable at the decreased price/lb (around $1.00).

Potatoes acted similarly, showing a decrease of nearly $1.00 (from $2.00) between

time periods 1 and 3 (7/5-‐8/15), and then staying between $1.00 and $1.50 for the

remainder of the market season. Interestingly, the mean price/lb. of green beans

increased at farmers’ markets and decreased at supermarkets during the same time

periods (4-‐7) by about the same margin.

5. Discussion of Results 5.1. Summary

These results offer some support to the widespread consumer perception that

produce costs more at farmers’ markets than at supermarkets in the underserved

Boston neighborhoods of Roxbury and Dorchester, but the difference is not very

large. I found that when time period, quality rating, and produce type were held

constant, the mean price per pound of produce at area farmers’ markets was a

marginally significant 8.6 cents greater than at supermarkets, on average. With the

dependent variable lnPRICE, the log of price, the results suggest a significant 2.9%

58

increase in price per pound on produce at farmers’ markets compared to

supermarkets. In addition, I found that bell peppers, cucumbers, and potatoes cost

significantly more per pound at farmers’ markets when the effects of time and

quality were controlled for. A plot of time period vs. mean price per pound by

location showed that prices at farmers markets decreased markedly throughout the

sixteen-‐week season, while supermarket prices remained nearly constant before a

noticeable increase during the final time period. As anticipated, overall quality

rating was significantly greater at farmers’ markets than at supermarkets. The

robustness of the statistical results on overall price differences was also confirmed

using a natural log transformation of price.

5.2. Magnitude of Price Differences

The statistically significant 2.9% increase in mean price per pound of

vegetables at farmers’ markets (from the log of price model) indicates that farmers’

market produce is more expensive, on average, than produce purchased from

traditional grocery outlets. But what is the practical significance of this variation to

the consumer? Several researchers have found that fruit and vegetable

consumption is lower when fruit and vegetable prices are higher (Powell and Bao,

2009), yet do these results imply a noteworthy obstacle to produce consumption via

a farmers market in certain Boston neighborhoods? It may be difficult to have a

concrete sense for how much “value” or weight about 3% carries, so I will translate

this amount into an estimated total cost increase if a consumer purchased produce

only at a farmers’ market throughout the summer season. The Economic Research

Service of the USDA recently published a report of fruit and vegetable prices

59

declaring that an adult on a 2,000-‐calorie diet could satisfy recommendations for

fruit and vegetable consumption (amounts and variety) in the 2010 Dietary

Guidelines for Americans at an average of $2 to $2.50 per day (Stewart et al., 2008).

By using the mean of this range, $2.25, an increase by 3% would increase daily cost

of consuming the recommended fruit and vegetable amount by about 7-‐cents to

$2.32. Over the course of the 16-‐week/112 day summer market season used in this

study, purchasing the recommended daily amount of produce would increase from

$252.00 to $259.84-‐ nearly $8.00. Though more weighty for a price-‐sensitive

shopper, I consider an additional $8 over the course of nearly four months to be a

relatively minimal cost to the average shopper’s wallet. Of course, the ERS

estimation does not provide an entirely precise basis for analysis given that it was

derived from national data (Boston has a history of food prices higher than the

national average), that most Americans do not consume recommended amounts,

and that it also includes fruits, which were not considered in this study. Even so,

this sort of extrapolation provides an approximate number that may be helpful in

conveying a more realistic message of actual cost differences to residents of

Dorchester and Roxbury and to policymakers responsible for incentivizing the

purchasing/consumption of fresh produce.

In its measurement of price per pound of produce, a few notable limitations

are encountered by this study’s methodology. First, data was recorded based on

standardized price per pound of produce as it would be presented to a customer at a

retail outlet and was not adjusted to represent an edible equivalent (stems, skins,

greens, and other non-‐edible parts removed). The USDA’s ERS examined the

60

importance of such an adjustment and found that retail prices appeared to be a poor

indicator of prices per edible cup equivalent, though great variation based on

produce type existed. Next, this study did not differentiate between produce sold on

a random weight basis ($1.29 per pound for loose tomatoes) and produce sold in

prepackaged containers bearing retailer’/manufacturer’s name or produce sold on a

“count basis” ($2.00 per 2 lb. bag of carrots or $1.50 per head of lettuce). Overall,

the USDA’s ERS suggested that a distinction in produce marketing form was not an

important factor in price, but often prepackaged containers or bags offered bulk

discounts that are important to mention. When collecting data, this study recorded

prices for the smallest amount of the conventional type of produce and did not

include prices for bulk packages (5 lb. bag of potatoes) because it was assumed that

customers on a limited budget may not be able to take advantage of volume

discounts, and also because farmers’ markets rarely offer such discounts. This

decision is backed by Kunreuther et al. (1973), who argued that the poor are

disadvantaged because they are unable to participate in the purchase of economy-‐

sized packaged goods due to the limits of available grocery money and storage

space. While this is a legitimate assumption, many shoppers are able to take

advantage of significant bulk discounts at supermarkets that are not as readily

available at farmers’ markets; for example, Shaw’s loose onions were sold for

$1.79/lb. compared with a 2 lb. package of onions for $0.92/lb (about a 50%

discount), and Tropical Foods sold loose potatoes for $0.79/lb. compared with a 5

lb. bag for $0.34/lb (nearly a 60% discount).

61

Lastly, special discount offers were available at both location types but were

not factored into price analysis. Supermarkets offered some sort of “frequent

shopper” discount almost weekly where shoppers with say, a “Stop and Shop Card”

could benefit from special price cuts like zucchini for $0.50/lb. (regular price =

$1.49) or green beans for $0.20/lb. (regular price = $1.69). Farmers’ market

shoppers receiving SNAP assistance frequently benefited from utilizing the city-‐

wide incentive program “Boston’s Bounty Bucks” to save 50% on purchases up to

$20.00. Interestingly, when shoppers took full advantage of the Bounty Bucks

program and selected $20.00 worth of produce, they were able to save $10.00 at a

farmers’ market in just one trip-‐ the same amount that my earlier extrapolation

suggested as the total additional cost at farmers’ markets over the course of the

summer. This comparison quite clearly implies that, for low-‐income residents of

Boston who receive federal SNAP assistance, shopping at a farmers’ market may in

fact be an extremely economical way to maximize monthly benefits while reaping

the greater nutritional advantages of fresh produce.

5.3. Availability

One major drawback of farmers’ markets highlighted by the data was the

relative frequency of unavailable items. Only 45% of the initially assigned data

points were available at farmers markets, compared with 88% at supermarkets.

This result is most likely influenced by heightened time and climate sensitivity at

farmers’ markets. Vendors are limited by what they can transport to the market

from the farm, usually only assign one vendor/vehicle for small markets in these

neighborhoods, and in many cases supply quantities reflective of low demand.

62

Consequently for collectors, the later data collection took place, the more likely it

was that an item was sold out and therefore excluded from the final data set.

Enhancing this obstacle is the fact that the markets included in this study were

usually scheduled to open only one day a week (two markets opened two times a

week) for a few hours, further limiting collectors as to when data could be recorded.

Also, it must be noted that data only reflects the availability of the ten chosen

produce items rather than overall produce stock, thus in most cases it does not

adequately express the wide variety and plentiful supply of other produce items at

farmers’ markets. For example, most vendors had some sort of green leafy produce

available (spinach, calaloo, arugula), but since these items are subject to vast price

variation at supermarkets and less certain availability at farmers’ markets, they

were not included and their availability not reflected. On many occasions when a

certain item was not recorded and thus deemed unavailable, closely similar items

were in fact available at farmers’ markets (plum or cherry tomatoes, red potatoes,

“salad mix”), but were not included because they did not fit the specific criteria for

comparison. Still, the limited supply and unpredictable availability of farmers’

markets are not only obstacles to data collection and analysis, but also more

significantly are a major hindrance to their utilization and popularity among

residents and shoppers.

While this expected pattern of decreasing availability due to limited supply at

farmers’ markets is clearly a disadvantage, it is further and perhaps unfairly

exaggerated by comparing it to the endless supply of produce available to larger

distributors and supermarkets. Unlike supermarkets that rely on a continental

63

network of greenhouses, massive farm operations, and refrigerated storehouses,

farmers’ markets are directly sensitive to the day-‐to-‐day growing conditions of

specific items and can only sell what is locally available for harvest. For a growing

number of Americans, this closeness with the farm and acceptance of nature’s

unpredictability is appreciated and even favored over the dependable stock of

supermarkets (Whitacre, 2009), but I speculate that such an attitude is not a reality

for residents in low-‐income neighborhoods. Though contemporary popular and

academic culture may suggest that the enormous network of processed agricultural

commodity crops is negatively affecting our health and environment, its ability to

create a consistent, reliable supply of fresh produce is highly valuable to the lower-‐

income consumer. The truth is that low-‐income shoppers in particular tend to make

fewer monthly trips to buy groceries due to transportation, federal support, and

proximity constraints (Whitacre, 2009); therefore, a larger distributor maximizes

options for those not likely or capable of making multiple trips to buy food.

On the other hand, however, the existence of these ten farmers’ markets in the

middle of dense neighborhoods puts fresh produce closer within the reach of

households that need it most. Larsen and Gilliland (2008) showed that for residents

of low-‐income urban communities that purchase food based on proximity due to

transportation constraints, the increased access to healthy foods provided by a

farmers’ market would likely improve some household diets. Regardless of how

small any market’s selection is, the quality, freshness, and nutrition of the produce

far surpasses that of the produce and food options at other neighborhood bodegas

and corner stores that supplement trips to larger, more distant supermarkets.

64

5.4. Quality

The incorporation of a quality rating into this study was meant to assess the

common hypothesis that farmers’ market produce, while more expensive, is

undoubtedly of better quality. Results support this hypothesis, showing that

farmers’ markets received a significantly greater proportion of highest quality

ratings than did supermarkets. While this difference in quality is certainly justified

by data and first-‐hand accounts, it is necessary to note the limitations inherent in

measuring produce quality. As quality is a subjective assessment prone to all sorts

of individual preferences, studies involving produce/foodstuffs often choose to

disregard it altogether for fear of jeopardizing the objective validity of their

research. I feel that quality is an extremely important aspect of a consumer’s

decision-‐making process and it must not be dismissed or ignored but rather handled

with caution. In designing a system for measuring quality, this study aimed to

minimize subjective influences by using a limited range of values (1-‐3) and training

all collectors using reference examples for each rating. Since most people rely on it

when selecting items to purchase, visual rating is a realistic and useful form of

quality assessment that plays a particularly strong role in the discussion on food

access. It is worthwhile to acknowledge that the measure of visual quality rating

used in this study is not necessarily a parallel indicator of taste, which has been

shown repeatedly to play the most influential role in fruit and vegetable

consumption decisions (Glanz and Goldberg, 1998; Reicks et al., 1994; Treiman et

al., 1996). However, in her discussion on food-‐purchasing decisions, Cummins

(2010) remarked that perceived quality of produce, (i.e. what a shopper infers about

65

taste, freshness, and nutrition based on visual presentation) is a very important

factor, and likely acts as a mediating variable in the decision to buy fresh produce.

Additionally, a similar survey by French (2002) concluded that individuals of lower

socioeconomic status -‐like those central to this study-‐ might place greater

importance on this perceived quality than on actual taste, freshness, or nutrition.

These references assert the importance of first impressions of produce quality in the

overall perception of value and verify the decision to incorporate perceived quality