Page 1

1

Hedging Palm Oil in Bursa

Malaysia Derivatives

Jeffrey Tan

General Manager, Product & Market Development

Bursa Malaysia Derivatives Berhad

2nd Palm Oil Internet-based Seminar

7-13 February 2011

Page 2

Hedging is the transfer of price risks associated with physical palm

oil market activities. For palm-oil based product distributors, the way

to control costs and margins is to hedge. For upstream producers,

the way to lock in desirable margins is to hedge.

By not hedging, a company is actually speculating that the market

will move favorably with respect to their market position! Recent

history suggests price peaks and troughs are unpredictable due to

unforeseen political events, weather, as well as supply and demand

imbalances.

A comprehensive hedging program provides risk management since

financial performance is materially impacted by fluctuating prices.

Concept of Hedging

Page 3

Who Should Hedge Palm Oil Products Exposure

• Any companies whose margins are impacted by increasing or

decreasing prices of palm oil products

• Examples : producers, millers, refiners, traders, wholesalers

and end-users

• Hedging is needed at every level of palm oil value chain, from

FFB harvesting to milling to refining and to the end products

Page 4

Malaysian Ringgit-Denominated Crude Palm Oil Futures

Crude Palm Kernel Oil Futures

USD-Denominated Crude Palm Oil Futures

Kuala Lumpur Composite Index Futures

Kuala Lumpur Composite Index Options

Single Stock Futures

3-Month KLIBOR Futures

3-Year Malaysian Government Bond Futures

5-Year Malaysian Government Bond Futures

Palm Oil Derivatives Products Offered

Page 5

0

500

1000

1500

2000

2500

3000

3500

4000

4500

01/0

1/1

981

01/1

0/1

981

01/0

7/1

982

01/0

4/1

983

01/0

1/1

984

01/1

0/1

984

01/0

7/1

985

01/0

4/1

986

01/0

1/1

987

01/1

0/1

987

01/0

7/1

988

01/0

4/1

989

01/0

1/1

990

01/1

0/1

990

01/0

7/1

991

01/0

4/1

992

01/0

1/1

993

01/1

0/1

993

01/0

7/1

994

01/0

4/1

995

01/0

1/1

996

01/1

0/1

996

01/0

7/1

997

01/0

4/1

998

01/0

1/1

999

01/1

0/1

999

01/0

7/2

000

01/0

4/2

001

01/0

1/2

002

01/1

0/2

002

01/0

7/2

003

01/0

4/2

004

01/0

1/2

005

01/1

0/2

005

01/0

7/2

006

01/0

4/2

007

01/0

1/2

008

01/1

0/2

008

01/0

7/2

009

01/0

4/2

010

Bursa CPO Settlement Price (RM)

FCPO Settlement Price (RM)

Page 6

Price Comparisons*

January 2011

(RM/MT)

October 2010

(RM/MT)

October 2005

(RM/MT)

Crude Palm Oil 3,771 2,853 1,456

RBD Palm Oil 3,819 2,951 1,510

RBD Palm Olein 3,828 2,978 1,558

RBD Palm Stearin 3,752 2,921 1,286

Palm Kernel Oil 6,440 4,224 2,076

* Source : MPOB

Page 7

Futures market – an auction market where participants

buy and sell CPO/PKO for delivery on a specific future

date

Futures contract – contract between buyer and seller

where buyer is obliged to take delivery and seller is

obliged to provide delivery of a fixed amount of CPO/PKO

at a predetermined price at a specified location

Everything is standardized except price. Already

determined include: commodity, quantity, quality, delivery

date

Futures Market

Page 8

Trade Flow

Broker A

Broker B

Bursa

Malaysia

Derivatives

Clearing

House

Surveillance

Clients notify their

brokers on their

trade orders

Brokers key in their

clients orders in the

trading system

Orders are routed

to the Exchange

and matched

Matched trades are sent to the

Clearing House to be cleared

and to Surveillance

Notification is sent

once trades are

matched

Page 9

Screen Shot of a Typical Trading Day

Open High Low Settlement Change

September, 2010 2,690 2,717 2,667 2,670 -47 885 4,619

October, 2010 2,620 2,633 2,569 2,570 -58 3,807 13,572

November, 2010 2,555 2,567 2,502 2,510 -50 17,235 23,114

December, 2010 2,533 2,543 2,477 2,481 -59 6,171 14,706

January, 2011 2,539 2,539 2,473 2,475 -59 697 6,527

February, 2011 0 0 0 2,461 -59 0 91

March, 2011 0 0 0 2,461 -59 0 1,817

May, 2011 2,526 2,526 2,510 2,448 -59 40 1,125

July, 2011 2,528 2,528 2,528 2,459 -59 1 488

September, 2011 0 0 0 2,460 -59 0 246

November, 2011 2,525 2,525 2,525 2,464 -59 20 156

January, 2012 2,535 2,535 2,518 2,481 -59 80 885

March, 2012 2,538 2,538 2,502 2,486 -59 2 628

May, 2012 0 0 0 2,486 -59 0 680

July, 2012 0 0 0 2,486 -59 0 0

Contract Prices (RM) Volume Open

InterestPrevious Average

2,717 2,691

2,628 2,597

2,560 2,535

2,540 2,513

2,534 2,514

2,520 0

2,520 0

2,507 2,521

2,518 2,528

2,519 0

2,523 2,525

2,540 2,530

2,545 2,520

2,545 0

2,545 0

Page 10

2,970

2,975

2,980

2,985

2,990

2,995

3,000

No

v-1

0

De

c-1

0

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

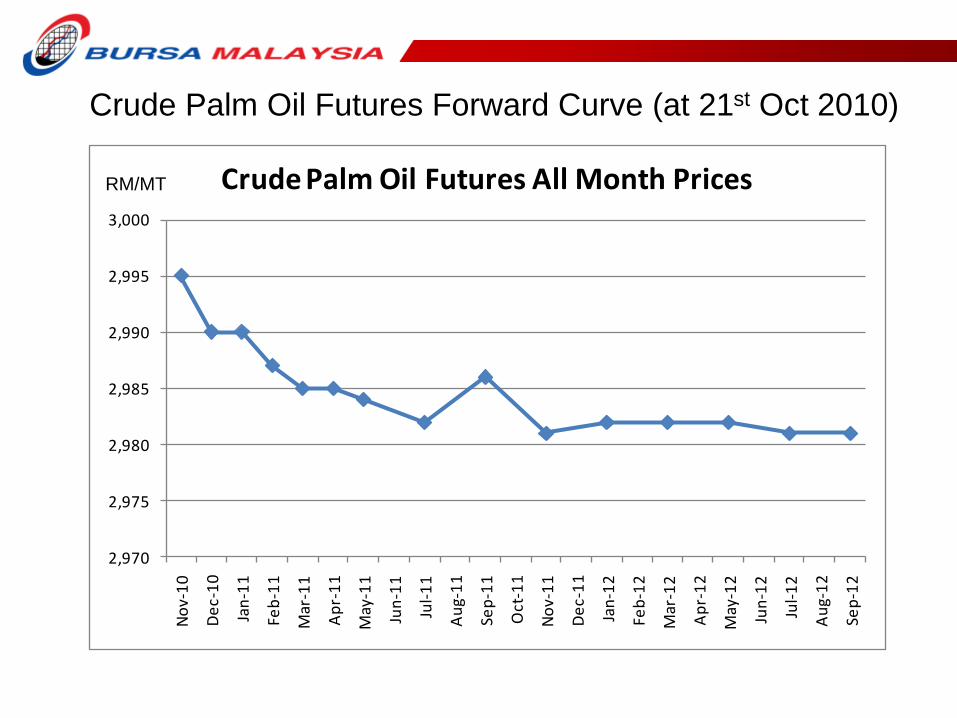

Crude Palm Oil Futures All Month Prices

Crude Palm Oil Futures Forward Curve (at 21st Oct 2010)

RM/MT

Page 11

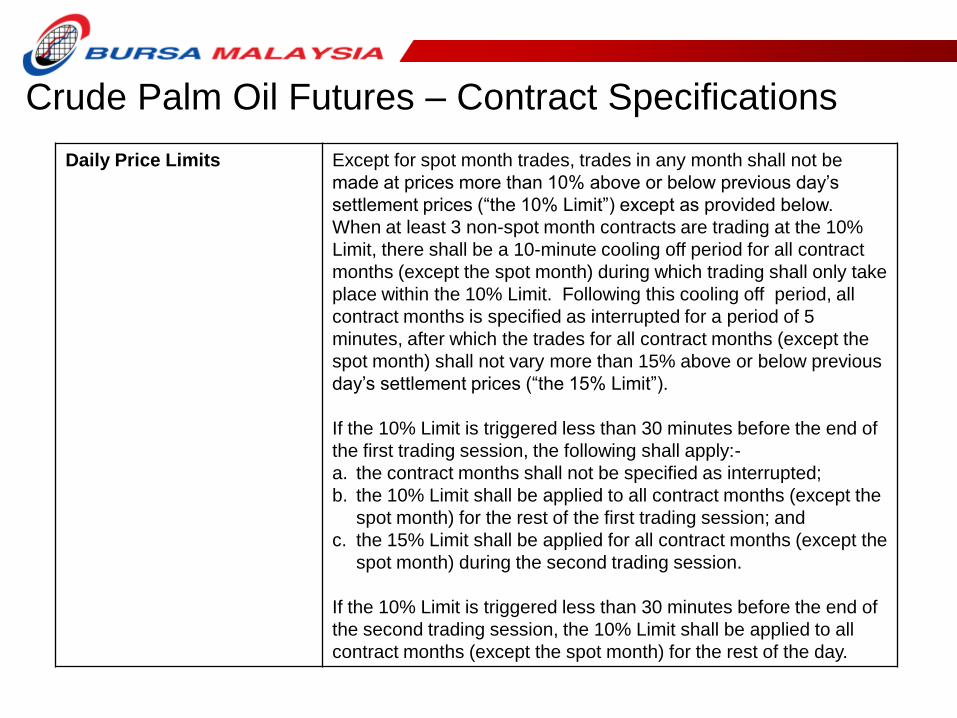

Crude Palm Oil Futures – Contract Specifications

Contract Code FCPO

Underlying Instrument Crude Palm Oil

Contract Size 25 metric tons

Minimum Price Fluctuation RM1 per metric ton

Contract Months Spot month and the next 5 succeeding months, and thereafter,

alternate months up to 24 months ahead

Trading Hours First trading session: Malaysian10:30 a.m. to 12:30 p.m.

Second trading session: Malaysian 3:00 p.m. to 6:00 p.m.

Speculative Position Limits 500 contracts net long or net short for the spot month

5,000 contracts for any single delivery month except for the spot

month

8,000 contracts for all contract months combined

Final Trading Day and

Maturity Date

Contract expires at noon on the 15th day of the delivery month, or if

the 15th is a non-market day, the preceding Business Day.

Tender Period 1st Business Day to the 20th Business Day of the delivery month,

or if the 20th is a non-market day, the preceding Business Day.

Page 12

Crude Palm Oil Futures – Contract Specifications

Daily Price Limits Except for spot month trades, trades in any month shall not be

made at prices more than 10% above or below previous day’s

settlement prices (“the 10% Limit”) except as provided below.

When at least 3 non-spot month contracts are trading at the 10%

Limit, there shall be a 10-minute cooling off period for all contract

months (except the spot month) during which trading shall only take

place within the 10% Limit. Following this cooling off period, all

contract months is specified as interrupted for a period of 5

minutes, after which the trades for all contract months (except the

spot month) shall not vary more than 15% above or below previous

day’s settlement prices (“the 15% Limit”).

If the 10% Limit is triggered less than 30 minutes before the end of

the first trading session, the following shall apply:-

a. the contract months shall not be specified as interrupted;

b. the 10% Limit shall be applied to all contract months (except the

spot month) for the rest of the first trading session; and

c. the 15% Limit shall be applied for all contract months (except the

spot month) during the second trading session.

If the 10% Limit is triggered less than 30 minutes before the end of

the second trading session, the 10% Limit shall be applied to all

contract months (except the spot month) for the rest of the day.

Page 13

Crude Palm Oil Futures – Contract Specifications

Contract Grade and

Delivery Points

Crude Palm Oil of good merchantable quality, in bulk, unbleached,

in Port Tank Installations approved by the Exchange located at the

seller’s option at Port Kelang, Penang/Butterworth and Pasir

Gudang (Johor).

Free Fatty Acids (FFA) of palm oil delivered into Port Tank

Installations shall not exceed 4% and from Port Tank Installations

shall not exceed 5%

Moisture and impurities shall not exceed 0.25%.

Deterioration of Bleachability Index (DOBI) value of palm oil

delivered into Port Tank Installations shall be at a minimum of 2.5

and of palm oil delivered from Port Tank Installations shall be at a

minimum of 2.31.

Deliverable Unit 25 metric tons, plus or minus not more than 2%.

Settlement of weight differences shall be based on the simple

average of the daily Settlement Prices of the delivery month from:

a. the 1st Business Day of the delivery month to the day of tender,

if the tender is made before the last trading day of the delivery

month; or

b. the 1st Business Day of the delivery month to the Business Day

immediately preceding the last day of trading, if the tender is made

on the last trading day or thereafter.

Page 14

FCPO is a physical delivered futures contract

C

Client

(Seller)

PTI

Seller

Delivers

CPO to

PTI

PTI conducts Appraisal:

• M&I

• FFA

• DOBI

PTI issues NSR

• Name & Location of PTI

• Date of Appraisal

• Certification of Quality

• Validity Date of NSR

Clearing

Broker (S)

Clearing

House

Notice of Tender (with NSR) must be submitted during tender period (1st – 20th)

Clearing

Broker (B1)

Clearing

Broker (B2)

Tender Advice will be

allocated to CPs on

proportionate basis

(based on OP)A

B

D

Client 1

(Buyer)

Client 2

(Buyer)

Tender Advice

allocated to CP is

onward allocated on

random basis at

client’s level

E

C

Client

(Seller)

PTI

Seller

Delivers

CPO to

PTI

PTI conducts Appraisal:

• M&I

• FFA

• DOBI

PTI issues NSR

• Name & Location of PTI

• Date of Appraisal

• Certification of Quality

• Validity Date of NSR

Clearing

Broker (S)

Clearing

House

Notice of Tender (with NSR) must be submitted during tender period (1st – 20th)

Clearing

Broker (B1)

Clearing

Broker (B2)

Tender Advice will be

allocated to CPs on

proportionate basis

(based on OP)A

B

D

Client 1

(Buyer)

Client 2

(Buyer)

Tender Advice

allocated to CP is

onward allocated on

random basis at

client’s level

E

Client

(Seller)

PTI

Seller

Delivers

CPO to

PTI

PTI conducts Appraisal:

• M&I

• FFA

• DOBI

PTI issues NSR

• Name & Location of PTI

• Date of Appraisal

• Certification of Quality

• Validity Date of NSR

Clearing

Broker (S)

Clearing

House

Notice of Tender (with NSR) must be submitted during tender period (1st – 20th)

Clearing

Broker (B1)

Clearing

Broker (B2)

Tender Advice will be

allocated to CPs on

proportionate basis

(based on OP)A

B

D

Client 1

(Buyer)

Client 2

(Buyer)

Tender Advice

allocated to CP is

onward allocated on

random basis at

client’s level

E

Page 15

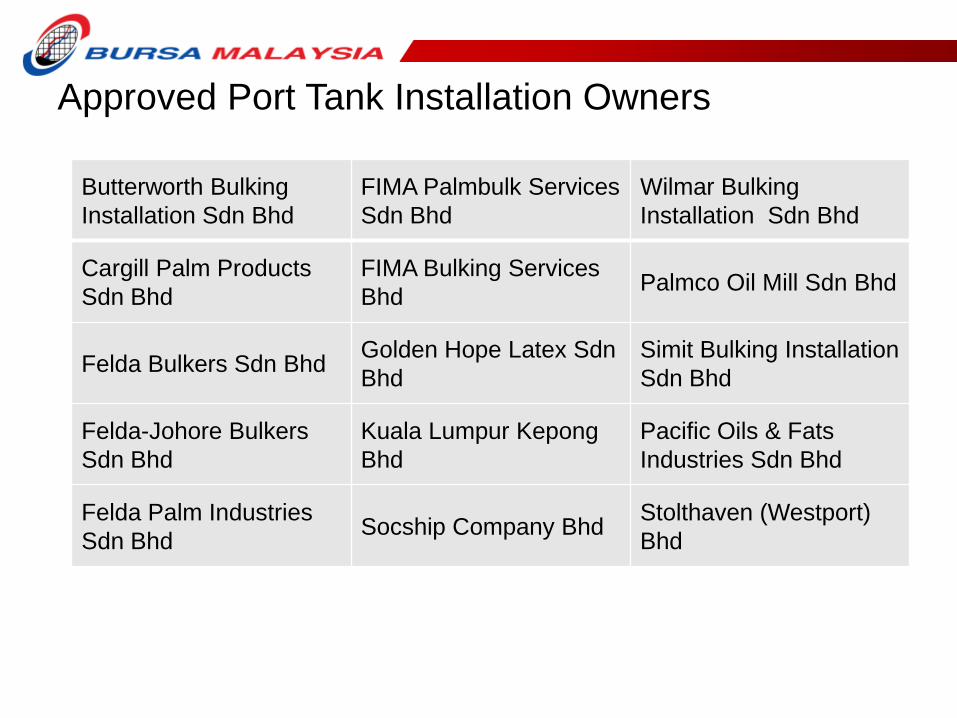

Approved Port Tank Installation Owners

Butterworth Bulking

Installation Sdn Bhd

FIMA Palmbulk Services

Sdn Bhd

Wilmar Bulking

Installation Sdn Bhd

Cargill Palm Products

Sdn Bhd

FIMA Bulking Services

BhdPalmco Oil Mill Sdn Bhd

Felda Bulkers Sdn BhdGolden Hope Latex Sdn

Bhd

Simit Bulking Installation

Sdn Bhd

Felda-Johore Bulkers

Sdn Bhd

Kuala Lumpur Kepong

Bhd

Pacific Oils & Fats

Industries Sdn Bhd

Felda Palm Industries

Sdn BhdSocship Company Bhd

Stolthaven (Westport)

Bhd

Page 16

In a rising spot price environment, a CPO trader who purchases and re-sells CPO may

have difficulty passing on his costs while protecting his profit margins. He decides to

purchase Bursa CPO for a percentage of his future commitments. He trades 300,000 tons

a year and decides to hedge 25,000 tons or 1 month’s commitment. He buys 1,000

contracts (equivalent to 25,000 tons) at RM3,700 per ton. Over the course of the next 10

days, prices rose to RM4,000 per ton. He sells out his Bursa at RM4,000 thereby realizing

a gain of RM300 per ton. The gain is offset by the higher cost of physical CPO he needs to

purchase.

Long Hedge Against Rising Prices

Physical Market Futures Market

21 Jan 2011 RM3,700 Buys 1,000 lots @ RM3,700/MT

= RM92.5m

31 Jan 2011 RM4,000 buys 25,000MT @

RM4,000/MT

= RM100.0m

Sells 1,000 lots @ RM4,000/MT

= RM100.0m

Futures Profit = RM100m – RM92.5m = RM7.5m

Effective Physical Price = RM100m – (RM100m – RM92.5m) = RM92.5m

Page 17

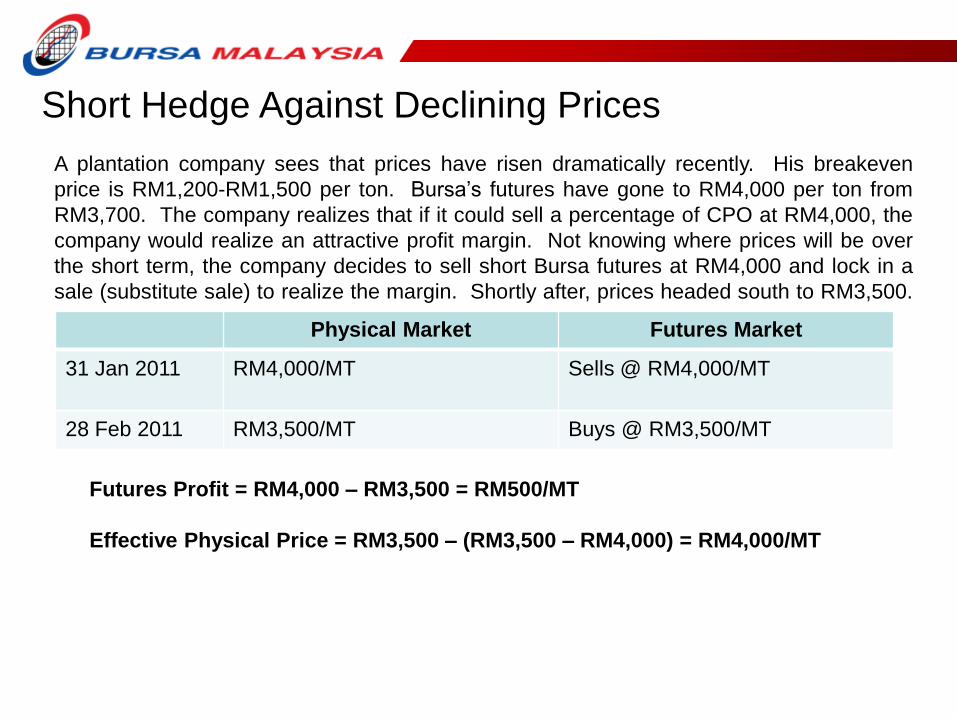

A plantation company sees that prices have risen dramatically recently. His breakeven

price is RM1,200-RM1,500 per ton. Bursa’s futures have gone to RM4,000 per ton from

RM3,700. The company realizes that if it could sell a percentage of CPO at RM4,000, the

company would realize an attractive profit margin. Not knowing where prices will be over

the short term, the company decides to sell short Bursa futures at RM4,000 and lock in a

sale (substitute sale) to realize the margin. Shortly after, prices headed south to RM3,500.

Short Hedge Against Declining Prices

Physical Market Futures Market

31 Jan 2011 RM4,000/MT Sells @ RM4,000/MT

28 Feb 2011 RM3,500/MT Buys @ RM3,500/MT

Futures Profit = RM4,000 – RM3,500 = RM500/MT

Effective Physical Price = RM3,500 – (RM3,500 – RM4,000) = RM4,000/MT

Page 18

• What is a crude palm oil futures contract?

It is a legally binding agreement guaranteed by Bursa

Malaysia Derivatives and regulated by Securities

Commission between a buyer and seller to make or take

delivery of a standardized quantity and grade of crude

palm oil. The price is agreed upon by the buyer and seller

in the form of bids and offers placed with a Bursa

Malaysia Derivatives broker or Trading Participant

Frequently Asked Questions (1)

Page 19

• If I purchase a Bursa CPO futures contract, will I have to

take physical delivery on the contract

No. While you can take delivery of Bursa’s futures

contracts at specified delivery points such as Port Klang,

Butterworth or Pasir Gudang, you do not have to take

delivery. By purchasing the contract and then selling an

equal number of contracts in the same month before the

expiration, you no longer have an obligation to fulfill the

contract. The majority of futures contracts traded do not

end up becoming physical transactions. The same

applies for sellers.

Frequently Asked Questions (2)

Page 20

• Does working with a Bursa Derivatives Trading Participant

or broker replace any relationships that a company may

have with regard to buying and selling oil palm products?

No. A palm oil-related company will still buy and sell oil

palm products to or from whomever they may currently be

buying or selling. Working with a Bursa Trading

Participant will complement those relationships.

Frequently Asked Questions (3)

Page 21

• When I call up to place an order to buy or sell a futures

contract, who is on the other side and how do I know that

they will fulfill their obligation on the

One of the benefits of trading futures contracts is

anonymity. The person who is on the other side of the

trade is represented by a broker (member of the

exchange) just like you are. The exchange acts as a

central clearinghouse for buyers and sellers. The party

who is on the other side of the contract may have an

inverse risk profile in your market, may be a speculator, or

may be liquidating (getting out of a contract). As for the

performance of the contract, the exchange ultimately

guarantees the performance of the contract regardless of

whether a counter party is able to meet its obligation.

Frequently Asked Questions (4)

Page 22

• How do I get started hedging with futures contracts?

First, you need to open a hedging account with a Bursa

Malaysia Trading Participant (a list of which can be found

in our website, www.bursamalaysia.com). Then you need

to deposit margin that is a good faith deposit for the

performance of the contract that you are going to buy or

sell. After this, you need to speak with a futures broker

representative (“FBR”) who can help you come up with a

game plan to accomplish your hedging goals.

Frequently Asked Questions (5)

Page 23

Summary

1. Hedging takes away the uncertainty of price fluctuations.

For downstream palmoil-based users, the only way to

control your costs is to hedge. For upstream producers,

protecting your margins is through hedging.

2. Not hedging means the company is actually speculating

that the market will move favorably with respect to its

market position.

3. Prices are volatile and uncertain. Hedging is imperative

for risk management in securing pricing and sales, enabling

more accurate and predictable cash flow projections and

enhanced inventory management control.

Page 24

List of Futures Brokers (www.bursamalaysia.com) 1. AmFutures Sdn Bhd

2. Innosabah Options Futures Sdn Bhd

3. Oriental Pacific Futures Sdn Bhd

4. JF Apex Securities Bhd

5. Inter-Pacific Securities Sdn Bhd

6. OSK Investment Bank Bhd

7. CIMB Futures Sdn Bhd

8. JPMorgan Securities (Malaysia) Sdn Bhd

9. Phillip Futures Sdn Bhd

10. ECM Libra Investment Bank Bhd

11. Kenanga Deutsche Futures Sdn Bhd

12. RHB Investment Bank Bhd

13. HDM Futures Sdn Bhd

14. LT International Futures (M) Sdn Bhd

15. Sunny Futures Sdn Bhd

16. HLG Futures Sdn Bhd

17. Okachi (M) Sdn Bhd

18. TA Futures Sdn Bhd

19. Interactive Futures Sdn Bhd

Page 25

Thank Youwww.bursamalaysia.com

[email protected] : +60320347084

Mobile: +60192615332