33

HEERF Accounting Refresher: A Year-End Guide July 29, 2021

HEERF Accounting Refresher: A Year-End GuideJuly 29, 2021

› Individuals• Participate in entire webinar• Answer polls when they are provided

› Groups• Group leader is the person who registered & logged on to the webinar• Answer polls when they are provided• Complete group attendance form • Group leader sign bottom of form• Submit group attendance form to [email protected] within 24 hours of webinar

› If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of webinar. Due to the large volume of certificates of completion issued, requests to reissue lost or misplaced certificates will be honored up to 60 days following the webinar

To Receive CPE Credit

Sara Grenier, [email protected]

Presenters

Jennifer Williams, [email protected]

Jackson Magdy, [email protected]

HEERF Refresher Agenda

1

2

3

4

Accounting for HEERF & SEFA Matters

5

HEERF Reminders

HEERF Examples

Questions

HEERF Reminders

84.425 Education Stabilization Fund (all alpha letters) is expected to be designated as higher risk in the 2021

Compliance Supplement

Lost revenue reminders

Reporting reminders

Procurement considerations

Drawdown considerations

HEERF – Compliance Update

› An institution may only estimate lost revenue “associated with coronavirus” as specified by CRRSAA section 314(c)(1)

• If the lost revenue is directly attributable to a cause other than the COVID-19 pandemic

• The institution may not include those lost revenues in its estimation of its lost revenue for the HEERF grant programs

› An institution may charge lost revenue to its grant at the end of the period that it is using to estimate lost revenue

› The institution may charge its HEERF grant award for the determined amount of lost revenue on or after the last day of the estimation period

› Lost revenue period ends at end of the HEERF grant performance period

› An institution does not need to assign specific costs once it has charged its HEERF grant award for its estimate of lost revenue

Lost Revenue

Lost Revenue: Acceptable Uses› Acceptable Academic Uses

• Tuitions, fees, & institutional charges

• Room & board

• Enrollment declines

• Supported research

• Summer terms & camps

› Acceptable Auxiliary Uses• Disruption of food service

• Bookstore revenue

• Parking revenue

• Canceled ancillary events

• Use of facilities or events › Other than facilities associated with

sectarian instruction or religious worship)

Source: Department of Education Lost Revenue FAQ #3: https://www2.ed.gov/about/offices/list/ope/heerflostrevenuefaqs.pdf

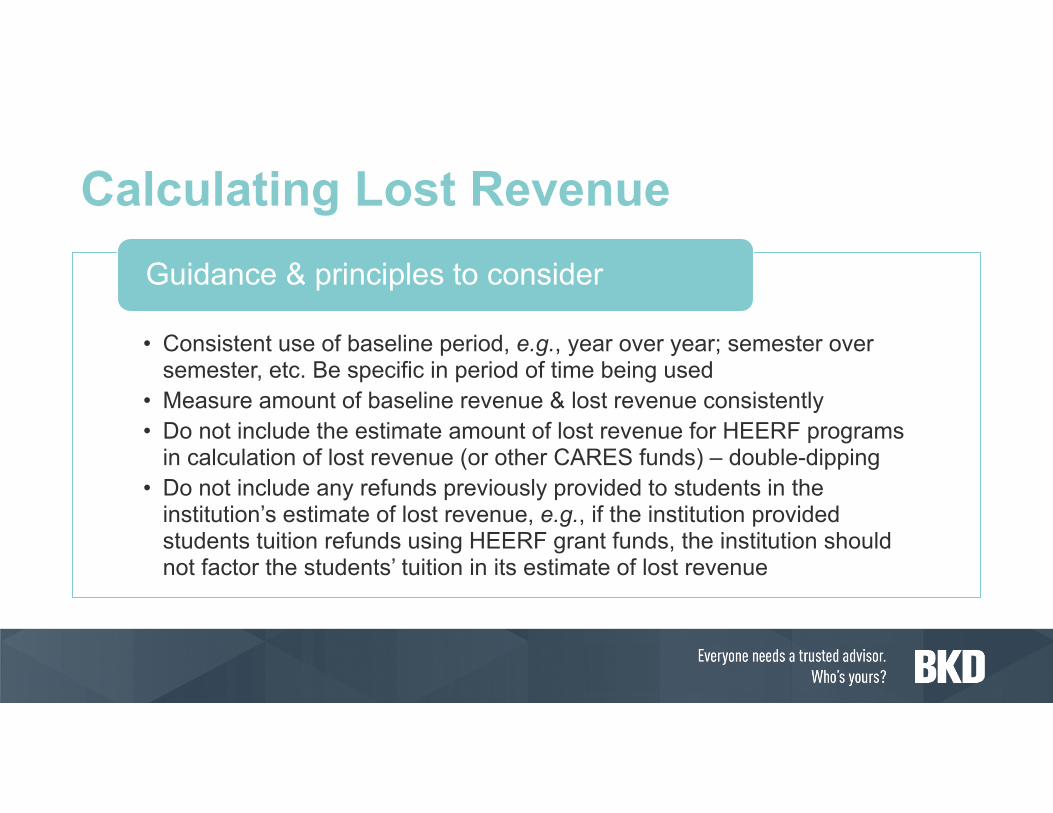

• Consistent use of baseline period, e.g., year over year; semester over semester, etc. Be specific in period of time being used

• Measure amount of baseline revenue & lost revenue consistently • Do not include the estimate amount of lost revenue for HEERF programs

in calculation of lost revenue (or other CARES funds) – double-dipping• Do not include any refunds previously provided to students in the

institution’s estimate of lost revenue, e.g., if the institution provided students tuition refunds using HEERF grant funds, the institution should not factor the students’ tuition in its estimate of lost revenue

Guidance & principles to consider

Calculating Lost Revenue

• To the extent possible lost revenue should be charged to the grant & recorded in the fiscal year in which it relates• Fall 2021 decisions & potential impact of going back & capturing lost revenue

• Document your methodology & support well• Make connection to COVID• Run by your team once calculation is drafted• Retain documentation for at least three years after date of final expenditure report • No indirect cost rate

Guidance & principles to consider

Other options – unpaid student debt

Calculating Lost Revenue

› Eligibility• Student must be enrolled on or after March 13, 2020, & other

factors such as …› Has a transcript withheld due to unpaid debt› Is blocked from enrolling due to unpaid debt› Cannot transfer credits due to an unpaid balance

• There are not (yet) specifically stated limitations on the age of the debt or timing of claim if the above criteria is met*

*You cannot claim lost revenue for a period in progress

Lost Revenue: Unpaid Balances

› Student balance(s) identified which meet the established criteria may include the student debt in lost revenue including penalties & fees

• This likely applies to …› Current students (on or after March 13, 2020) who were allowed to

enroll despite having an outstanding balance & then didn’t pay due to COVID-19

› Students who were enrolled on March 13, 2020, & are no longer at your institution & didn’t pay due to COVID-19

Lost Revenue: Unpaid Balances

› Institutions also have the ability to issue a grant for the student portion of HEERF for unpaid balances if you can obtain affirmative prior written consent from the student

› You are strongly encouraged to include a disclaimer that expressly notifies students that the student “has the ability to decline the emergency financial aid grant to pay off debts and instead may use the funds for any component of the student’s cost of attendance or for emergency costs that arise due to coronavirus, such as tuition, food, housing, health care (including mental health care), or childcare”

› The institution CANNOT condition the discharging of the balance based on any specific student actions, i.e., re-enrollment

Unpaid Balances: Student Portion

› HEERF II• Institutions must report publicly on their primary websites on a

quarterly basis for both student portion & institutional portion funds • Quarterly reporting deadline by which institutions must submit

retroactive reports for HEERF II is extended to the end of the second calendar quarter, June 30, 2021

• HEERF II funds will also be subject to the annual reporting requirement in early 2022 – details forthcoming

› HEERF III• Same quarterly reporting • Annual reporting requirement coming in 2022

Reporting

› Ensure grant agreements are reviewed to ensure all required reports are being submitted

› Maintain supporting documentation used to compile the report (should be supported by information within the general ledger)

› Ensure someone other than the preparer is reviewing & comparing information included in the report to supporting documentation

› To ensure effective internal control over reporting, all reviews should be clearly documented (even if report is submitted electronically)

Reporting Tips

Procurement – General Standards

Documented Policies

Necessary Purchases

Full & Open Competition

Conflict of Interest Documentation

Procurement – Allowable MethodsMicro

Purchases

Less than $10,000, can be raised to

$50,000 with self-certification qualification

No quote required

Equitable distribution

Current threshold: 48 CFR Subpart

2.101 – Micro purchase threshold

Small Purchases

Up to $250,000

Rate quotations required

No cost or price analysis

Current threshold: 48 CFR Subpart

2.101 – Simplified acquisition threshold

Sealed Bids

Greater than $250,000

(simplified acquisition threshold)

Construction projects

Price is a major factor

Current threshold: 48 CFR Subpart

2.101 – Simplified acquisition threshold

Competitive Proposals

Greater than $250,000

(simplified acquisition threshold)

Fixed price or cost reimbursement

RFP with evaluation methods

Current threshold: 48 CFR Subpart

2.101 – Simplified acquisition threshold

Noncompetitive Proposals

Also referred to as “sole source”

No dollar threshold

Certain circumstances

must exist to be allowable

Unique, public emergency, prior

approval or inadequate competition

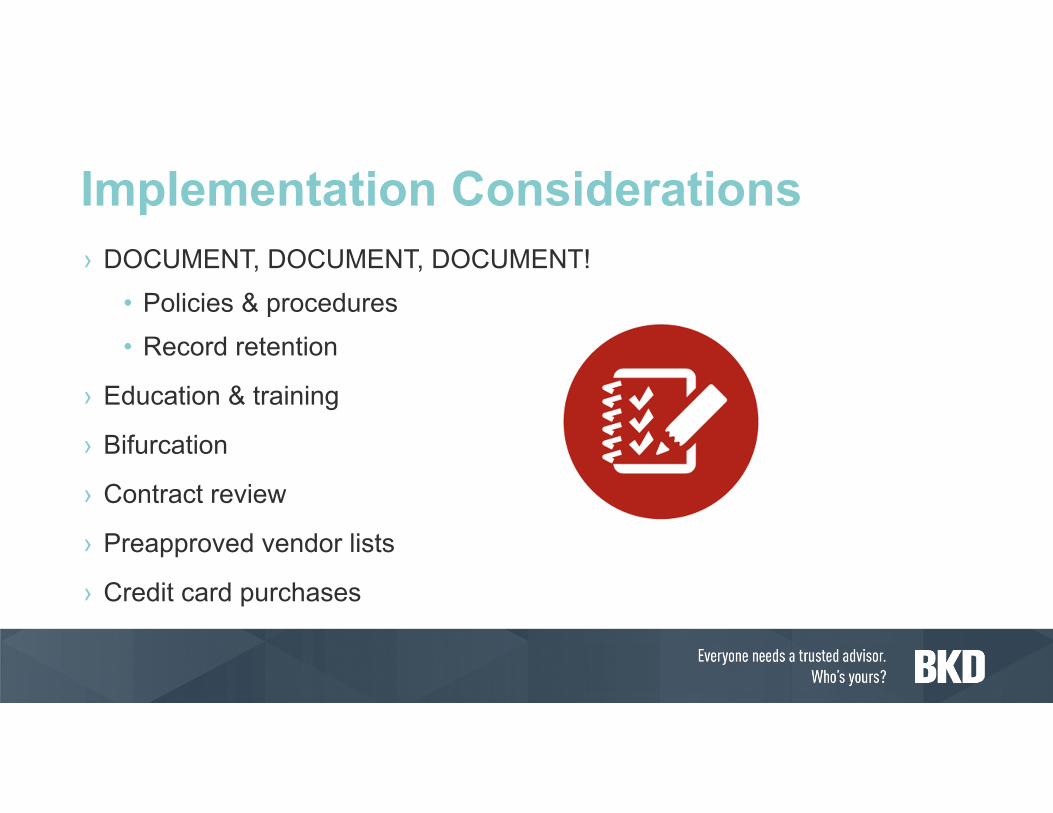

Implementation Considerations› DOCUMENT, DOCUMENT, DOCUMENT!

• Policies & procedures• Record retention

› Education & training

› Bifurcation

› Contract review

› Preapproved vendor lists

› Credit card purchases

› Draw funding within the first 90 days of the award

› Mindful of timing between drawdown & when the funds are spent

› Not precluded from drawing funds for institutional portion of HEERF III even if have not spent student portion – however, revenue recognition differences

Drawdown Considerations

Accounting for HEERF & SEFA Matters

› HEERF II operates differently than HEERF I & III

› HEERF II requires the higher education institution provide the same amount in grants to students that was required to provide under HEERF I. HEERF II is silent as to a percent for students versus institution & focuses on a pure dollar minimum to give to students (same amount as HEERF I)

› The U.S. Department of Education (ED) has not provided guidance on what amount of the institutional portion would be at risk of being required to be repaid to ED if the required student portion is not awarded to students by the end of the period of performance

› Very conservative approach – the institution would not recognize any revenue for the institutional portion under HEERF II until it has awarded all the required student portion

› However, since both HEERF I & III contain specific provisions that you must spend at least 50% of the funds on students, an institution may conclude it is appropriate to apply a pro rata methodology to revenue recognition under HEERF II

Accounting for HEERF II – FASB

› The determination of when an award is expended must be based on when the activity related to the federal award occurs

› Grants, cost reimbursement contracts, cooperative agreements under the Federal Acquisition Regulations (FAR), & direct appropriations

• When the expenditure or expense transactions occur

› May differ from revenue recognition criteria

SEFA Presentation for HEERF II

› If institution had signed GAN for HEERF III prior to FYE 2021

• If using any institutional portion of HEERF II or HEERF III for lost revenues for FY 20 or FY 21, must be included on SEFA

• If decide in FY 22 to go back & use FY 20 or FY 21 lost revenue, correction of an error

SEFA Presentation for HEERF

HEERF Examples

Example 1 – FactsPortion Awarded Expended DrawnStudent $5,000,000 $ - $ -Institutional $8,000,000 $8,000,000 $8,000,000

› Have not been able to distribute funds to students at June 30, 2021, due to timing issues

› Have enough lost revenue at June 30, 2021, to support using all $8,000,000

› Have drawn all $8,000,000 of institutional due to lost revenue

Example 1 – Journal EntryDebit Credit

Cash $8,000,000Refundable Advance – HEERF Institutional

$8,000,000

› Have not spent any student piece; therefore, cannot recognize revenue portion of institutional piece

› Defer what has already been drawn down

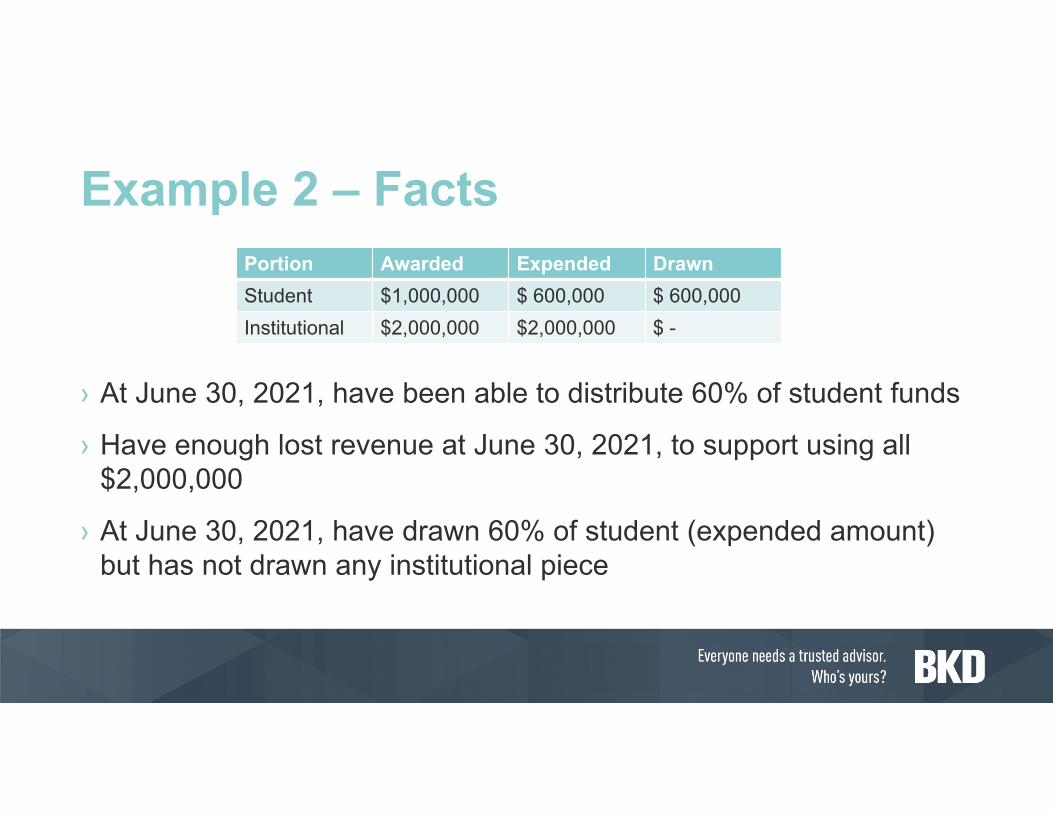

Example 2 – FactsPortion Awarded Expended DrawnStudent $1,000,000 $ 600,000 $ 600,000Institutional $2,000,000 $2,000,000 $ -

› At June 30, 2021, have been able to distribute 60% of student funds

› Have enough lost revenue at June 30, 2021, to support using all $2,000,000

› At June 30, 2021, have drawn 60% of student (expended amount) but has not drawn any institutional piece

Example 2 – Journal Entries

Debit CreditCash $600,000HEERF Student AP $600,000

Debit CreditHEERF Receivable – Institutional $1,200,000Grant Revenue – HEERF Institutional $1,200,000

Debit CreditHEERF Grant Revenue – Student $600,000HEERF Expense – Student $600,000HEERF Student AP $600,000Cash $600,000

Example 2 – ExplanationPortion Awarded Expended DrawnStudent $1,000,000 $ 600,000 $ 600,000Institutional $2,000,000 $2,000,000 $ -

› Record the student payments as grant income & expense

› Record proportional share of institutional portion (60% of $2,000,000)

› Because no money has been drawn for institutional portion, recognize receivable for proportionate share

Continuing Professional Education (CPE) Credit

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org

› CPE credit may be awarded upon verification of participant attendance

› For questions, concerns, or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]

CPE Credit

bkd.com | @BKDLLP

The information contained in these slides is presented by professionals for your information only & is not to be considered as legal advice. Applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor or legal counsel before acting on any matters covered