43

Company update March 2016

Company update

March 2016

1

Contents

• Introduction – Group Overview

• Strategy update

• Industry & market developments

• Strategic business units (SBUs)

• Appendix

Leading independent refiner in SEE with upgraded complex refining asset base;

sales evenly spread between domestic and international

• High complexity and net cash margin refineries

• Balanced sales channel mix with exports at

50% of total sales

• Regional footprint with international

subsidiaries

• > 60% of cashflows driven from international

sales and regional benchmark margins

• Leading domestic market position with c.60-

65% of wholesale and c.30% of retail

• Marketing and Petchems vertically integrated

with Refining; diversification in G&P

• Improved competitiveness position; €50m of

further upside in next 2 years

Nelson/Solomon complexity and benchmark margins

Group operational footprint

4*

(*) Average benchmark margins 2012-2015 ($/bbl)

Aspropyrgos

13.9

Thessaloniki

5.0 6.9

Elefsina

11.3

8.8 9.7

Solomon NCI

5* 1*

MONTENEGRO

BULGARIA

SERBIA

FYROM

GREECE

CYPRUS Power & Gas

2

Assets overview Core business around downstream assets with activities across the energy value chain

DESCRIPTION METRICS

• Exploration assets in Greece

• Complex (recently upgraded) refining system:

– Aspropyrgos (FCC, 148kbpd)

– Elefsina (HDC, 100kbpd)

– Thessaloniki (HS, 93kbpd)

• Pipeline fed refinery/terminal in FYROM

• Capacity: 16MT

• NCI: 9.6

• Market share: 65%

• Tankage: 7m M3

• Basel technology PP production (integrated with

refining) and trading

• > 60% exports in the Med basin

• Capacity (PP): 220 kt

• Leading position in all market channels (Retail,

Commercial, Aviation, Bunkering) through EKO and

HF (BP branded network)

• c.1,700 petrol stations

• 30% market share

• Sales volumes: 3.5MT

• Strong position in Cyprus, Montenegro, Serbia,

Bulgaria, FYROM

• Advantage on supply chain/vertical integration

• c.290 petrol stations

• Sales volumes: 1.2MT

• ELPEDISON: Second largest IPP in Greece (JV with

Edison/EdF)

• Capacity: 810 MW

(CCGT)

• DEPA/DESFA GROUP: 35% in Greece’s incumbent

NatGas supply company (DESFA in sale process) • Volumes (2015): 3.0bcm

Refining, Supply

& Trading

Exploration &

Production

Domestic

Marketing

International

Marketing

Petrochemicals

Power & Gas

3

Our Group in numbers – key financials

€ million, IFRS 2010 2011 2012 2013 2014 2015

Income Statement

Sales Volume (MT’000) - Refining 14,502 12,528 12,796 12,696 13,538 14,258

Net Sales 8,477 9,308 10,469 9,674 9,478 7,303

Segmental EBITDA

- Refining, Supply & Trading 338 259 345 57 253 561

- Petrochemicals 50 44 47 57 81 93

- Marketing 114 66 53 68 90 107

- Other (incl. E&P) -28 -6 0 -5 -7 -2

Adjusted EBITDA * 474 363 444 178 417 758

Adjusted associates’ share of profit 30 67 69 57 28 22

Adjusted Net Income * 213 140 229 -120 2 268

Balance Sheet / Cash Flow

Capital Employed 4,191 4,217 4,350 3,905 2,870 2,913

Net Debt 1,659 1,687 1,855 1,689 1,140 1,122

Capital Expenditure (incl. refinery upgrades) 709 675 521 112 136 165

(*) Calculated as Reported less the Inventory effects and other non-operating items 4

Our Group in numbers – key metrics

5

0

1

2

3

4

5

6

7

2010 2011 2012 2013 2014 2015

1.0

1.1

1.2

1.3

1.4

1.5

2010 2011 2012 2013 2014 2015

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 2015

Mogas Middle distillates Fuel oil

Benchmark system margin ($/bbl)

EUR/USD - €/$

Utilisation rate* (%)

Production yields (%)

758

417

178

363

444474

2010 2013 2014 2015 2011 2012

Adjusted EBITDA (€m)

(*) Total feed over crude capacity; 2011-1H12 Elefsina Refinery was not operating due to its upgrade project

Contents

• Introduction – Group Overview

• Strategy update

• Industry & market developments

• Strategic business units (SBUs)

• Appendix

6

2014-2018 Strategy Update Benefit of investments and competitiveness improvement initiatives to achieve deleverage and

increased cashflow; Emphasis on risk management, which remains a key priority

1

2

5

Rebalance market position and

de-risk business model

Improve financial position

3 Continue competitiveness

improvement

4 Manage business portfolio for

value

Integrate and realise benefit of

investments

- Vertical integration

- Increased exports (50%)

- Operating KPIs

- Solomon benchmarks

- Gas & Power

- Capture positive refining

cycles

- EBITDA €500-700m

STRATEGY TARGETS

- Deleverage balance-sheet

- De-risking

- Cost of funding

7

•85%

•60%

•60%

•50%

•65%

0

5

10

15

2011 2012 2013 2014 2015

IG int sales

293

6,414

2,914

5,031

2014

13,693

7,612

1,825

4,256

2013

12,961

7,771

1,269

3,920

2012

12,107

8,080

2,572

1,455

2011

8,635

7,061

1,282

Aspropyrgos

Thessaloniki

Elefsina

2015

14,359

(*) Total feed over crude capacity; 2011-1H12 Elefsina Refinery was not operating due to its upgrade project

New business model - Operations Business model transformed, post Elefsina upgrade, with increased production driving higher

exports with significant benefits (risk profile, economics, working capital)

Refining Sales by market (m MT)

21% 50%

Nameplate

capacity

8

50%

21%

Gross Production by refinery (MT’000)

54% Utilisation

Rate* (%) 76% 81% 85% 91%

Domestic Sales

Exports

New business model – Profitability drivers Reduced exposure to domestic economic environment; refining margins and operational

performance key drivers of profitability

9

30%

8%

12%

30%

19%

8%

Int’l* PetChems

5%

51%

Total Exports Aviation &

Bunkering*

Domestic

market*

Refining

38%

High Low None

Group Gross margin breakdown (%)

Greek market: contribution

(*) Includes both trading & marketing

Capex Significant step-down following completion of upgrade capex; no major growth project in 2016

10

136112

521

675

709

614

Stay in business capex

2015 2014 2013 2012 2011 2010 2009

165

2016

Capex evolution (€m) 2015 Overview

• Aspropyrgos full T/A included small

growth projects (PP splitter capacity,

energy efficiency projects)

• Elefsina decoking and Thessaloniki

debottlenecking works

• Retail network optimisation; growth of

COMO network

2016 Plan: Main projects

• Maintenance works at Elefsina in 1Q16

(Hydrocracker catalysts and VDU) and

Thessaloniki full T/A

• Selective expansion in Domestic and

International Marketing

Leverage* (x)

Credit facilities - liquidity Full repayment of $400m Eurobond during 1H16; plan to address other maturities, once market

conditions allow

Gross Debt overview (%)

9%

Banks (uncommitted)

30%

25%

Banks (committed)

EIB

36% Debt Capital Markets

Total:

€3.3bn

4Q15 Credit Lines Maturity Profile

11

Interest cover *(x) Gearing* (%)

0

100

200

300

400

500

600

700

2020+ 2019 2018 2017 2016

Debt Capital Markets Banks EIB

3.8 3.9

0 x

1 x

2 x

3 x

4 x

5 x

2013 1H14 2014 1H15 2015

Interest Coverage (x)

Interest Coverage (incl. Assoc.)

1.4 1.2

0 x

2 x

4 x

6 x

8 x

10 x

2013 1H14 2014 1H15 2015

Leverage (incl. Assoc.) Leverage (pro forma)

Leverage ratio is calculated as 12m trailing

Net Debt/Adjusted EBITDA;

Interest cover calculated as Adj. EBITDA over finance costs

(*) pro forma adjustment for DEPA group BV at reported capital structure

Gearing calculated as Net Debt/

Capital Employed

39%

31%

20%

30%

40%

50%

2013 1H14 2014 1H15 2015

Gearing (%) Gearing Pro forma

Framework Agreement with NIOC Iran payables agreement, positive for balance sheet and future crude supply options

12

• Following the removal of US/EU sanctions on 16 January 2016 (“Implementation day” according to the

P5+1 agreement reached on 7 July 2015), Hellenic Petroleum and the National Iranian Oil Company

(NIOC), reached a framework agreement on 22 January

• Recommencement of commercial relationship offering an additional source of crude, in line with existing

contract provisions; deliveries expected to start soon

• Agreement for the settlement of payables from 2011-2012 crude purchases which were frozen, (following

imposition of UN/US sanctions), de-risks balance sheet and is in line with the Group medium-term cash

flow plans

• Agreement implementation is subject to full compliance with current EU and International framework,

including surviving sanctions

Contents

• Introduction – Group Overview

• Strategy update

• Industry & market developments

• Strategic business units (SBUs)

• Appendix

13

Recent Industry developments Recent improvement in European refining environment; beginning of a new cycle?

• European refining margins benefited from improved Atlantic basin crude supply conditions (production

growth in US, as well as Iraq); lifting of Iran sanctions expected to impact crude supply in the region

• Strong demand in both OECD (Europe, US) and emerging markets (China) for products, notably gasoline

throughout 2015

• Developments in global refining capacity (Middle East, Russia) and inter-regional competitive position

(USGC) key drivers

• Weak crude prices and stronger USD positive for refiners, despite one-off inventory impact

Med complex margins - $/bbl (2012-2015)

Med FCC margins:

2.6

$/bbl

3.3 6.5

14 (*) Data updated as of 14/03/2016

4.3

FCC

Hydrocracking

0

1

2

3

4

5

6

7

8

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 QTD*

$/bbl

Regional market – Diesel shortage in the Med ELPE yields match increasing shortage in the region

Key DIESEL/GASOIL balances in the Med region, kb/d (2020)

-178

-103

-65 -28

-40

-40

-10 -11

-20

-6

-5

-18

-195

-34

-55

-16

-13

-87

+4

+8

+9

PORTUGAL

GIBRALTAR

MOROCCO

SPAIN

MED FRANCE

ALGERIA

TUNISIA MALTA

ITALY

CROATIA

SLOVENIA

SERBIA

BOSNIA

FYROM

ALBANIA

GREECE

MONTENEGRO

TURKEY

LIBYA

EGYPT ISRAEL

LEBANON

SYRIA

CYPRUS

Diesel/Gasoil surplus (2020)

Diesel/Gasoil deficit (2020)

-59

Source: Wood Mackenzie

15

953

805

765

751

930

10,125

3,722

2,518

2,932

2009

11,413

4,064

2,837

3,353

1,159

MOGAS

ADO

HGO

LPG & Others

2013

6,599

2,670

2,248

2012

7,727

2,913

2,066

1,983

2011

9,267

3,355

2,224

2,883

2010

813829

971

2015

7,103

2,458

2,427

1,389

2014

6,669

2,527

2,358

Domestic market environment Positive 1H15 trend reversed in 2H, following bank holiday and capital controls; auto-fuels flat y-o-

y, with heating gasoil driving overall market demand growth

16

(*) Does not include PPC and armed forces

Source: Ministry of Environment & Energy

Domestic Market demand* (MT ‘000)

+6%

-7% +6%

+22%

4Q

2,097 1,980

3Q

1,501 1,611

2Q

1,583 1,497

1Q

1,923

1,581

2015 2014

-3%

+43%

+3%

+3%

-11%

-8%

-17%

-15% +1% +7%

Contents

• Introduction - Group overview

• Strategy update

• Industry & market developments

• Strategic Business Units (SBUs)

• Appendix

17

Refining, Supply & Trading economics Combination of Refining economics, in-market trading and International export business;

export sales at 50% of total

Markets

(sales premia varying

across channels)

Refining

(Med benchmark returns

& operations performance)

Imported Products

(0.5-1.5m MT)

Aviation & Bunkering

(Med competitive pricing)

Exports, Intra-Group

(Platts Med FOB based + premia)

Domestic market

5.5 MT

2.5 MT

Exports, 3rd parties

(Platts Med FOB based)

2.0 MT

5.0 MT

Aspropyrgos

NCI 9.7

148kbpd

FCC

Thessaloniki

NCI 6.9

95kbpd

Hydroskimming

Elefsina

NCI 11.3

100kbpd

HDC

16 MT

0.5-1.5 MT

$ / €

Total ELPE capacity

12%

55%

25%

8%

Fuel oil Middle Distillates

Gasoline Other

Refined Products

(14.0 MT) $ $ $

11%

89%

High sulphur

Low sulphur

25%

8%

55%

12%

Other

Gasoline Fuel Oil

Middle Distillates

18

Other

8%

Egypt

9%

Libya

2%

CPC 20%

Iraq

28%

Urals 33%

FY15 crude slate (%)

19

ELPE realised vs benchmark* margin ($/bbl)

(*) System benchmark calculated using actual crude feed weights

(**) Includes PP contribution which is reported under Petchems

Refining, Supply & Trading economics – Performance vs benchmarks Operational excellence and trading premia account for consistent over-performance vs

benchmark of $5-5.5/bbl at normal operations

25 9 84 132 172 77 Adj.

EBITDA 163

8.0 7.5

10.2 10.2

12.3

8.3

11.8

9.5

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

ELPE system benchmark (on feed) ELPE realised margin**

143

Aspropyrgos

T/A

300

500

700

900

1100

1300

1500

1700

4Q14 1Q15 2Q15 3Q15 4Q15

Propane, FOB Propylene NWE, CIF Polypropylene NWE

Petrochemicals Operations centred on vertical integration for higher value product; trading geared to

exports markets

Polypropylene value chain

Propylene (refinery grade)

Propylene splitter

90%

Thessaloniki PP plant

(220 kt)

PP

Imports

10%

Propylene (polymer grade)

10%

90%

Domestic and international

market

BOPP film plant (26kt)

• Competitive advantage in polypropylene - vertical

integration at 85-90% of total production

• Exports account for >60% of total sales; strong export

markets in Turkey, Italy and East Med

• Domestic market share in petchems exceeds 50% in

all products, produced or traded

PP value chain contribution ($/T)

20

Integrated

PP

Margin Aspropyrgos splitter

contribution

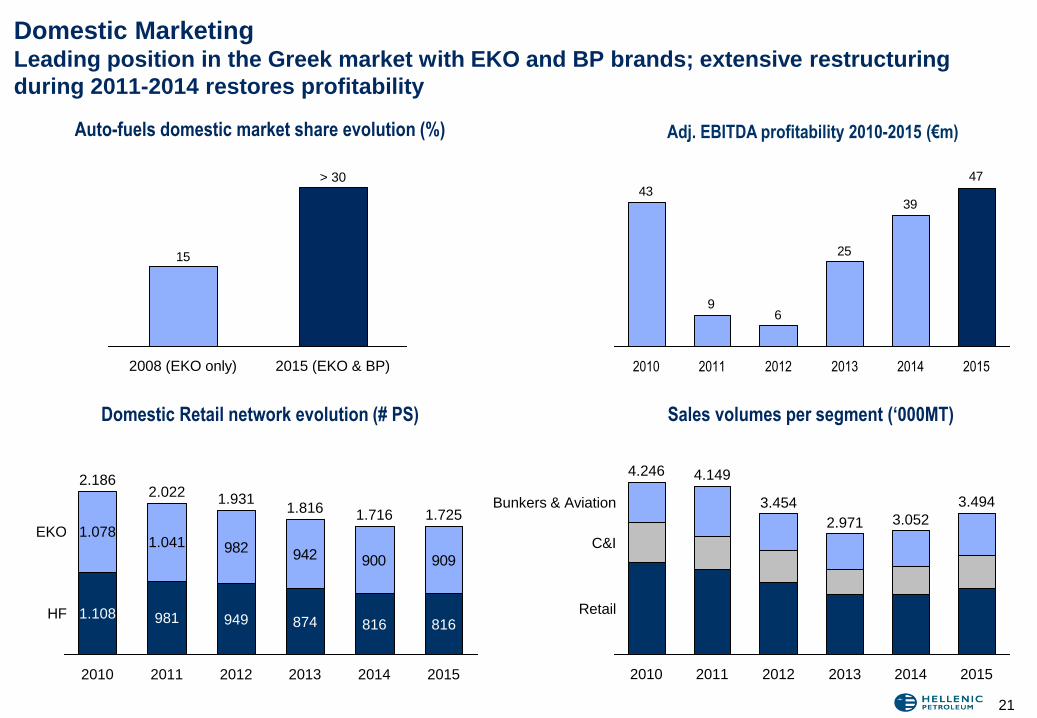

Domestic Marketing Leading position in the Greek market with EKO and BP brands; extensive restructuring

during 2011-2014 restores profitability

Auto-fuels domestic market share evolution (%)

15

2015 (EKO & BP)

> 30

2008 (EKO only)

Adj. EBITDA profitability 2010-2015 (€m)

47

39

25

69

43

2015 2014 2013 2012 2011 2010

21

2011

4.149

2010

4.246

Retail

C&I

Bunkers & Aviation

2015

3.494

2014

3.052

2013

2.971

2012

3.454

Sales volumes per segment (‘000MT)

982 942 900 909

1.078

2012

1.931

949

2011

2.022

981

1.041

2010

2.186

1.108 HF

EKO

2015

1.725

816

2014

1.716

816

2013

1.816

874

Domestic Retail network evolution (# PS)

International Marketing

Subsidiaries in neighboring markets increase downstream integration; selective expansion

to improve network control and increase presence in markets of focus

International Marketing: Regional footprint

Adj. EBITDA profitability 2010-2015 (€m) 59

51

4441

4548

2015 2014 2013 2012 2011 2010

22

CY

BU

SER

JPK

2015

1,178

2014

1,079

2013

1,072

2012

1,072

2011

1,041

2010

1,051

Sales volumes (MT‘000)

+5%

-1%

+19%

+5%

Group refineries

83%

3rd party

17%

2015

GREECE

BULGARIA SERBIA

MONTENEGRO

TURKEY

CYPRUS

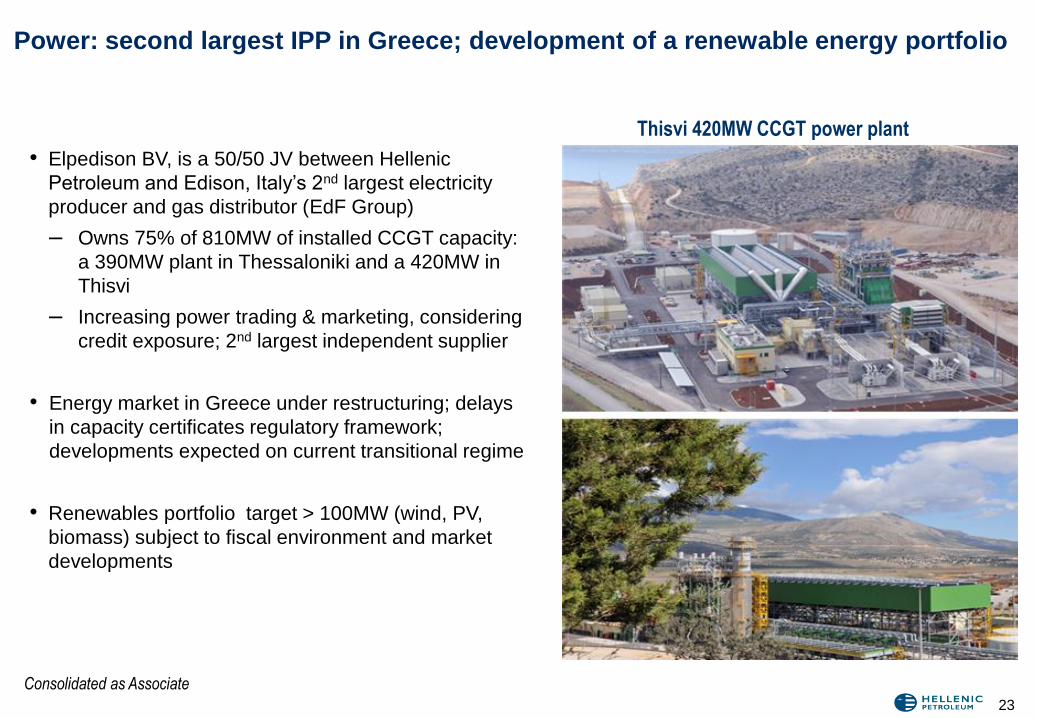

Power: second largest IPP in Greece; development of a renewable energy portfolio

Thisvi 420MW CCGT power plant

Consolidated as Associate

• Elpedison BV, is a 50/50 JV between Hellenic

Petroleum and Edison, Italy’s 2nd largest electricity

producer and gas distributor (EdF Group)

– Owns 75% of 810MW of installed CCGT capacity:

a 390MW plant in Thessaloniki and a 420MW in

Thisvi

– Increasing power trading & marketing, considering

credit exposure; 2nd largest independent supplier

• Energy market in Greece under restructuring; delays

in capacity certificates regulatory framework;

developments expected on current transitional regime

• Renewables portfolio target > 100MW (wind, PV,

biomass) subject to fiscal environment and market

developments

23

Gas: 35% participation in DEPA, Greece’s incumbent gas company

DEPA

– Long-term contracts on pipe gas (Russian & Azeri) and

capacity rights on two in-bound interconnecting pipelines

– Long-term contracts with power generators, eligible industrial

customers and existing EPAs

– Owns 51% of the local supply companies (EPAs), with rights

until 2036

– International pipelines: Participation in Greece-Bulgaria

Interconnector

DESFA (RAB) – in sale process

– Greece’s gas grid and LNG import terminal owner and

operator

• SPA for sale of 66% of DESFA to SOCAR for €400m signed

on 21 Dec 2013; regulatory approvals in process for

completion of transaction

DEPA snapshot financials (€m) 2009 2010 2011 2012* 2013 2014 2015

EBITDA 166 211 288 287 196 126 141

Net Income 61 91 191 197 147 83 66

* Adjusted for settlement with PPC

Natural gas transmission network

DEPA Volumes 2009-2015 (bcm)

Consolidated as Associate

2011 2009

3.3

2015

3.6

4.3

3.0

2013 2014

4.2

2012

3.8

3.0

2010

24

Contents

• Introduction - Group overview

• Strategy update

• Industry & market developments

• Strategic business units (SBUs)

• Appendix

25

Group Key financials: 2005 – 2015 Strong track record of consistent delivery and balance sheet resilience

(*) Calculated as Reported less the Inventory effects and other one-off non-operating items and special income taxes

26

€ million, IFRS (Published) 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Income Statement Figures

Sales Volume (MT'000) - Refining 16,525 16,952 17,130 16,997 15,885 14,557 12,528 12,796 12,696 13,538 14,258

Sales Volume (MT'000) - Marketing 4,727 4,790 5,236 4,910 4,787 5,735 5,126 4,434 4,043 4,131 4,672

Net Sales 6,653 8,122 8,538 10,131 6,757 8,477 9,308 10,469 9,674 9,478 7,303

EBITDA 671 502 617 249 390 501 335 298 29 -84 444

Adjusted EBITDA* 466 526 458 513 362 474 363 444 178 417 758

Net Income 341 271 365 29 176 187 118 81 -272 -369 45

Adjusted Net Income* 198 288 246 221 152 213 140 229 -120 2 268

Balance Sheet / Cash Flow Items

Capital Employed 2,956 3,442 3,557 3,153 3,927 4,191 4,217 4,350 3,905 2,870 2,913

Net Debt 699 1,044 977 679 1,419 1,629 1,687 1,855 1,689 1,140 1,122

Capital Expenditure 185 145 195 338 614 709 675 521 112 136 165

Free Cash flow -182 -177 204 512 -561 17 165 25 404 770 307

Dividend/Distributions (€/share) 0.43 0.43 0.50 0.45 0.45 0.45 0.45 0.15 n/a 0.21 n/a

Key drivers

Brent crude ($/bbl) 55.2 68.1 72.9 98.3 62.6 80.3 111.0 111.7 108.7 99.0 52.0

FCC cracking Med margins ($/bbl) 7.3 7.3 7.1 6.8 3.7 4.4 2.9 4.7 2.4 3.4 6.5

€/$ 1.24 1.26 1.37 1.47 1.39 1.33 1.39 1.29 1.33 1.33 1.11

Shareholding & Governance Controlling shareholders supported successful implementation of long-term strategy

Shareholding structure

6%

8%

36%

Greek State

Retail

7% Int’l institutionals

GR institutionals

POIH 43%

Corporate Governance

Board of Directors:

• Consists of 13 members appointed as per

Articles of Association

• Board Committees (Finance / Audit / HR)

Executive Committee:

• Key management executives with responsibility

for strategy and operations

27

Aviation &

Bunkering

C&I (Construction,

wholesale)

Retail

Greek petroleum market overview and route to market Leading domestic market position through vertical integration and competitive logistics

assets

3rd party

Imports

60-65% 30-35%

0-10%

Greek Refining capacity: 25MT

Domestic market: 11.5MT

ELPE Group

subsidiaries: 3.5MT

(30%)

MOH Group

subsidiaries: 2MT

(20%)

Independent

marketing

companies: 4.5MT

(35%)

ELPE exports: 6-8MT

3rd party exports:

5MT

16MT

ELPE Group

subsidiaries: 1-2MT

8%

9% 6%

20%

12%

24%

21%

Fuel Oil

Greek market product breakdown

Specialty markets

(PPC, public sector):

1.5MT (15%)

Gasoline

Diesel

Gasoil Jet

Bunkers

Other

28

€ million, IFRS 4Q FY

2014 2015 Δ% 2014 2015 Δ%

Income Statement

Sales Volume (MT'000) - Refining 3,981 4,070 2% 13,538 14,258 5%

Sales Volume (MT'000) - Marketing 1,075 1,211 13% 4,131 4,672 13%

Net Sales 2,383 1,803 -24% 9,478 7,303 -23%

Segmental EBITDA

- Refining, Supply & Trading 133 144 8% 253 561 -

- Petrochemicals 25 25 0% 81 93 14%

- Marketing 15 17 14% 90 107 19%

- Other -2 -2 -3% -7 -2 70%

Adjusted EBITDA * 171 184 8% 417 758 82%

Share of operating profit of associates ** 6 2 -66% 28 22 -24%

Adjusted EBIT * (including Associates) 121 131 8% 240 581 -

Finance costs - net -49 -48 3% -215 -201 7%

Adjusted Net Income * 52 65 24% 2 268 -

IFRS Reported EBITDA -206 31 - -84 444 -

IFRS Reported Net Income -228 -60 74% -369 45 -

Balance Sheet / Cash Flow

Capital Employed 2,870 2,913 1%

Net Debt 1,140 1,122 -2%

Capital Expenditure 51 34 -32% 136 165 22%

-60

-228

4Q15 4Q14

184171

+8%

4Q15 4Q14

131121

+8%

4Q15 4Q14

Adj. EBIT (€m)

4Q15 GROUP KEY FINANCIALS

(*) Calculated as Reported less the Inventory effects and other non-operating items

(**) Includes 35% share of operating profit of DEPA Group 29

IFRS Net Income (€m)

Adj. EBITDA (€m)

4Q15 KEY HIGHLIGHTS

30

• 4Q15 Adj. EBITDA at €184m (€171m LY) and Adj. Net Income at €65m (€52m LY):

– Robust refining margins and stable EUR/USD exchange rate

– Higher utilisation of all group refineries both q-o-q and y-o-y, improved performance post maintenance

– Record quarterly sales at 4m MT with exports at 53%

– Increased domestic fuels demand (+6%), driven by Heating GO, despite recession (GDP at -2%) in

4Q15

• Record high FY15 Adj. EBITDA at €758m and Adj. NI at €268m

• Oil price decline extended Inventory losses (€148m in 4Q15 and €301m in FY15), negatively affecting IFRS

Net results, at €-60m in 4Q15 and €45m in FY15

• Operating cashflow (Adj. EBITDA – Capex) of €593m supported uninterrupted operations during a most

challenging year, with Net Debt (€1.1bn), flat y-o-y

• Framework agreement with Iran for the settlement of payables from 2011-12 crude purchases and re-

commencement of commercial relationship reduces balance sheet risk

• May 2016 maturing Eurobond ($400m) to be repaid from Group’s existing reserves; Refinancing plans to be

implemented depending on market conditions later in the year

• Awarded exploration rights for Arta Preveza and NW Peloponisos areas (onshore) in Western Greece;

Geophysical studies (seismic 3D) in W. Patraikos have been completed

109 108 110 102

76

54 63

51 44

1.36 1.37 1.37 1.33

1.25

1.13 1.11 1.11 1.09

1.00

1.10

1.20

1.30

1.40

1.50

1.60

10

30

50

70

90

110

130

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Brent ($/bbl) EURUSD

INDUSTRY ENVIRONMENT Crude oil prices recorded new lows in 4Q15, leading to inventory losses; EUR/USD remained flat

at $1.1 level

31

• Global growth concerns and sustained

crude oversupply drive prices lower to

$44/bbl area

• Stable EUR/USD at $1.1 for 4th

consecutive quarter

• Further narrowing of Brent – WTI

spread, as US production declined

• Sour spreads at $1.5/bbl on increased

sour crude supply

ICE Brent and EUR/USD

Crude differentials ($/bbl) 11.8

9.4

6.7 6.2

4.0

6.6 5.6 5.6

2.6

0.3 0.8 1.4 1.0 0.8 1.0

0.5 0.7 1.5

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Brent-WTI Brent - Urals

2014 2015

31-Dec 55 36

4Q 76 44

Product Cracks* ($/bbl)

Hydrocracking & FXC

INDUSTRY ENVIRONMENT Robust refining benchmarks on sustained gasoline strength and wider crude spreads; middle

distillates performance was weaker y-o-y

32

Med benchmark margins** ($/bbl)

(*) Brent based.

(**) Revised benchmark margins set post-upgrades and secondary feedstock pricing adjustment

FCC

Diesel MOGAS

Naptha

HSFO

-30

-25

-20

-15

-10

-5

0

5

10

15

20

4Q14 1Q15 2Q15 3Q15 4Q15

$/bbl

1Q 2Q

3.4

7.2

3.1

5.8

4.7

6.2

3Q 4Q FY

4.5

6.7

3.9

6.5

2014 2015

1Q 2Q

2.2

6.8

2.6

7.3

4.2

7.3

3Q 4Q FY

4.3 4.8

3.3

6.5

-7 -2

253

561 81

93

200

145 65

30 1

90

107

20

80

FY14 BenchmarkRefiningMargins

FX Greek crisis(capital

controls)

Shut-down Assetutilisation

Supply Others FY15

CAUSAL TRACK & SEGMENTAL RESULTS OVERVIEW 2015 Record operating profitability reflects strong refining economics throughout 2015, despite

turnaround opportunity cost

33

Adjusted EBITDA causal track 2015 vs 2014 (€m)

758 417

Refining,

S&T

MK

Chems Refining,

S&T

MK

Chems

Other

(incl. E&P)

Environment Performance

Other

(incl. E&P)

CASH FLOW PROFILE Strong operating cashflow and prudent liquidity management allowed uninterrupted operations

during a most challenging year

Free Cashflow from Operations (Adj. EBITDA less capex- €m)

34

593

150188

68

188

281

120121

122766

FY14 4Q14 3Q14 2Q14 1Q14 FY13 FY15 4Q15 3Q15 2Q15 1Q15

Net Debt evolution FY14-FY15 (€m)

758

440

278

FY15 Net debt

1.122

Others

22

Working capital

(inventory

volumes, contago)

Interest, Tax,

Capex, Dividends

EBITDA FY14 Net Debt

1.140

4Q 2015 FINANCIAL RESULTS GROUP PROFIT & LOSS ACCOUNT

35 (*) Includes 35% share of operating profit of DEPA Group

IFRS FINANCIAL STATEMENTS 4Q FY

€ MILLION 2014 2015 Δ % 2014 2015 Δ %

Sales 2,383 1,803 (24%) 9,478 7,303 (23%)

Cost of sales (2,529) (1,702) 33% (9,334) (6,608) 29%

Gross profit (146) 101 - 145 695 -

Selling, distribution and administrative expenses (122) (123) (1%) (440) (458) (4%)

Exploration expenses (2) 1 - (4) (1) 87%

Other operating (expenses) / income - net* 8 (3) - 11 10 (9%)

Operating profit (loss) (262) (23) 91% (289) 245 -

Finance costs - net (49) (48) 3% (215) (201) 7%

Currency exchange gains /(losses) 1 (9) - (9) (27) -

Share of operating profit of associates** 6 2 (66%) 28 22 (24%)

Profit before income tax (305) (79) 74% (485) 39 -

Income tax expense / (credit) 77 19 (75%) 116 6 (95%)

Profit for the period (228) (60) 74% (369) 45 -

Minority Interest 1 2 28% 3 2 (50%)

Net Income (Loss) (227) (58) 74% (365) 47 -

Basic and diluted EPS (in €) (0.74) (0.19) 74% (1.20) 0.15 -

Reported EBITDA (206) 31 - (84) 444 -

4Q 2015 FINANCIAL RESULTS REPORTED VS ADJUSTED EBITDA

36

(€ million) 4Q FY

2014 2015 2014 2015

Reported EBITDA -206 31 -84 444

Inventory effect - Loss/(Gain) 375 148 484 301

One-offs 2 5 17 13

Adjusted EBITDA 171 184 417 758

37

4Q 2015 FINANCIAL RESULTS GROUP BALANCE SHEET

(*) 35% share of DEPA Group book value (consolidated as an associate)

IFRS FINANCIAL STATEMENTS FY FY

€ MILLION 2014 2015

Non-current assets

Tangible and Intangible assets 3,530 3,502

Investments in affiliated companies* 682 679

Other non-current assets 313 325

4,526 4,506

Current assets

Inventories 638 662

Trade and other receivables 708 744

Cash and cash equivalents 1,848 2,108

3,194 3,514

Total assets 7,719 8,020

Shareholders equity 1,618 1,684

Minority interest 110 106

Total equity 1,729 1,790

Non- current liabilities

Borrowings 1,812 1,598

Other non-current liabilities 162 170

1,974 1,768

Current liabilities

Trade and other payables 2,739 2,822

Borrowings 1,178 1,633

Other current liabilities 100 7

4,017 4,462

Total liabilities 5,991 6,230

Total equity and liabilities 7,719 8,020

4Q 2015 FINANCIAL RESULTS GROUP CASH FLOW

38

IFRS FINANCIAL STATEMENTS 12M

€ MILLION 2014 2015

Cash flows from operating activities

Cash generated from operations 876 478

Income and other taxes paid (23) (35)

Net cash (used in) / generated from operating activities 853 443

Cash flows from investing activities

Purchase of property, plant and equipment & intangible assets (136) (165)

Sale of property, plant and equipment & intangible assets 5 1

Expenses paid relating to share capital increase of subsidiary - (1)

Grants received - 1

Interest received 9 9

Dividends received 39 18

Proceeds from disposal of available for sale financial assets - 1

Net cash used in investing activities (83) (136)

Cash flows from financing activities

Interest paid (197) (201)

Dividends paid (2) (67)

Proceeds from borrowings 1,112 421

Repayment of borrowings (828) (227)

Net cash generated from / (used in ) financing activities 85 (74)

Net increase/(decrease) in cash & cash equivalents 854 233

Cash & cash equivalents at the beginning of the period 960 1,848

Exchange gains/(losses) on cash & cash equivalents 34 10

Net increase/(decrease) in cash & cash equivalents 854 233

Cash & cash equivalents at end of the period 1,848 2,091

(*) Calculated as Reported less the Inventory effects and other non-operating items

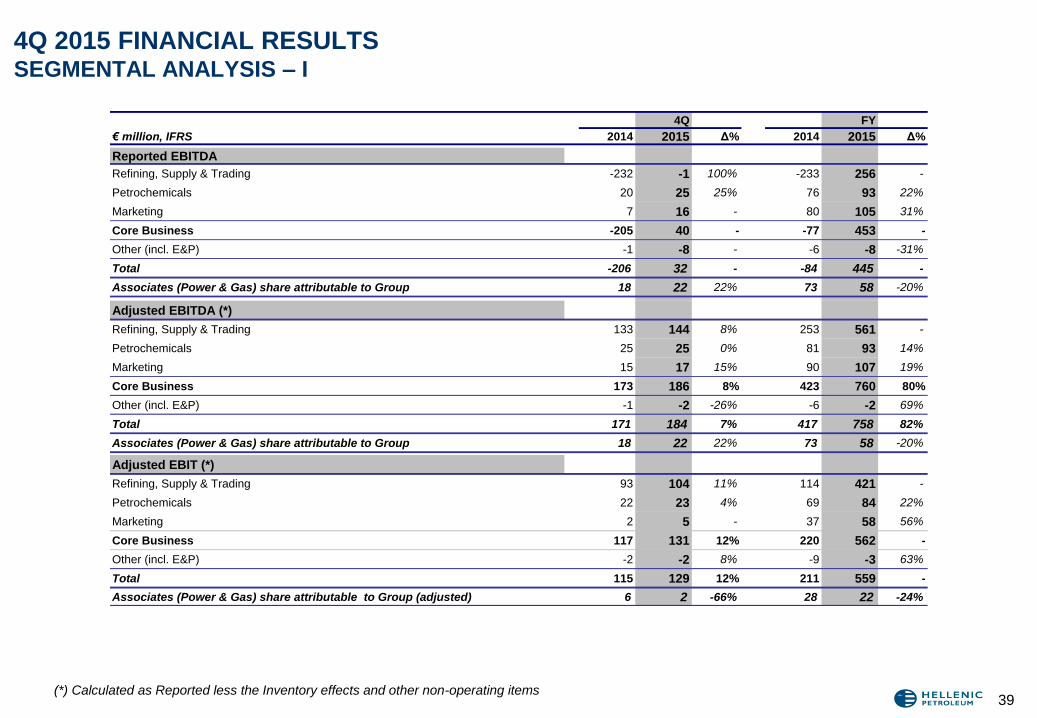

4Q 2015 FINANCIAL RESULTS SEGMENTAL ANALYSIS – I

39

4Q FY

€ million, IFRS 2014 2015 Δ% 2014 2015 Δ%

Reported EBITDA

Refining, Supply & Trading -232 -1 100% -233 256 -

Petrochemicals 20 25 25% 76 93 22%

Marketing 7 16 - 80 105 31%

Core Business -205 40 - -77 453 -

Other (incl. E&P) -1 -8 - -6 -8 -31%

Total -206 32 - -84 445 -

Associates (Power & Gas) share attributable to Group 18 22 22% 73 58 -20%

Adjusted EBITDA (*)

Refining, Supply & Trading 133 144 8% 253 561 -

Petrochemicals 25 25 0% 81 93 14%

Marketing 15 17 15% 90 107 19%

Core Business 173 186 8% 423 760 80%

Other (incl. E&P) -1 -2 -26% -6 -2 69%

Total 171 184 7% 417 758 82%

Associates (Power & Gas) share attributable to Group 18 22 22% 73 58 -20%

Adjusted EBIT (*)

Refining, Supply & Trading 93 104 11% 114 421 -

Petrochemicals 22 23 4% 69 84 22%

Marketing 2 5 - 37 58 56%

Core Business 117 131 12% 220 562 -

Other (incl. E&P) -2 -2 8% -9 -3 63%

Total 115 129 12% 211 559 -

Associates (Power & Gas) share attributable to Group (adjusted) 6 2 -66% 28 22 -24%

4Q 2015 FINANCIAL RESULTS SEGMENTAL ANALYSIS – II

40

4Q FY

€ million, IFRS 2014 2015 Δ% 2014 2015 Δ%

Volumes (M/T'000)

Refining, Supply & Trading 3,981 4,070 2% 13,538 14,258 5%

Petrochemicals 64 59 -8% 236 221 -7%

Marketing 1,075 1,211 13% 4,131 4,672 13%

Total - Core Business 5,119 5,340 4% 17,905 19,151 7%

Sales

Refining, Supply & Trading 2,217 1,613 -27% 8,818 6,644 -25%

Petrochemicals 84 64 -24% 322 263 -18%

Marketing 741 641 -14% 3,220 2,712 -16%

Core Business 3,042 2,318 -24% 12,361 9,620 -22%

Intersegment & other -659 -514 22% -2,882 -2,317 20%

Total 2,383 1,803 -24% 9,478 7,303 -23%

Capital Employed

Refining, Supply & Trading 1,344 1,164 -13%

Marketing 657 838 27%

Petrochemicals 164 144 -12%

Core Business 2,165 2,146 -1%

Associates (Power & Gas) 682 679 -1%

Other (incl. E&P) 23 88 -

Total 2,870 2,913 1%

Glossary of Key Terms

Adjusted EBITDA Reported EBITDA adjusted by inventory effect (impact of the fluctuation of crude prices on BS inventories and on the

value of products sold during the related period) and other one-off non recurring items

ADO Auto Diesel Oil

CCGT Combined Cycle Gas Turbine

COMO Company Owned Manager Operated

DCM Debt Capital Markets

FCC Fluid Catalytic Cracking

HDC Hydrocracking

HGO Heating Gasoil

HS Hydroskimming

HSFO High Sulfur Fuel Oil

IPP Independent Power Producer

MOGAS Motor Gasoline

LNG Liquefied Natural Gas

NatGas Natural Gas

Nelson Complexity Index (NCI) Index assessing the refinery conversion capacity by relating each processing unit capacity against the crude distillation

capacity and applying a weighting factor.

POIH Paneuropean Oil and Industrial Holdings

PP Polypropylene

Solomon Complexity Index Compares the relative refining configuration apart from throughput capacity. It is the total of EDC (Equivalent Distillation

Capacity) divided by the sum of the crude unit stream-day capacities.

ULSD Ultra-low-sulphur Diesel

41

Disclaimer

Forward looking statements

Hellenic Petroleum do not in general publish forecasts regarding their future financial

results. The financial forecasts contained in this document are based on a series of

assumptions, which are subject to the occurrence of events that can neither be reasonably

foreseen by Hellenic Petroleum, nor are within Hellenic Petroleum's control. The said

forecasts represent management's estimates, and should be treated as mere estimates.

There is no certainty that the actual financial results of Hellenic Petroleum will be in line

with the forecasted ones.

In particular, the actual results may differ (even materially) from the forecasted ones due

to, among other reasons, changes in the financial conditions within Greece, fluctuations in

the prices of crude oil and oil products in general, as well as fluctuations in foreign

currencies rates, international petrochemicals prices, changes in supply and demand and

changes of weather conditions. Consequently, it should be stressed that Hellenic

Petroleum do not, and could not reasonably be expected to, provide any representation or

guarantee, with respect to the creditworthiness of the forecasts.

This presentation also contains certain financial information and key performance

indicators which are primarily focused at providing a “business” perspective and as a

consequence may not be presented in accordance with International Financial Reporting

Standards (IFRS).

42