MGT (101) Prime ICS Collage (Virtual Campus) NOTES According to VU Syllabus Helping Material for Coaching Classes MBA (Semester -1) Lec# 1 to 5 Definition of Accounting Accounting is defined as “ The art ofrecording, classifying and summarizing in terms of money transactions and events of financial character and interpreting the results thereof” Recording: Recording means but the transaction to writing in the books of accounts. Recording is done in the book “Journal”, this book is further sub-divided books such as cash journal, purchases journal, sales journal etc. Classifying Classification is the process of grouping of transactions or entries of one nature at one place. The work of classification is done in the book termed as “Ledger” 2. • Financial Accounting It is the original form of accounting; it is mainly confined to the preparation of financial statements. The main function of financial accounting is to calculate profit or loss made by the business during the year and exhibit financial position of the business as on a particular date • Cost Accounting Its main function is to ascertain the cost of a product and to help the management in the control of cost. • Management Accounting Accounting which prov ides necessary information to th e management for discharging its functions. It is the reproduction of financial accounts in such a way as will enable the management to take decisions and to control activities. 1. Syste ms of accou nting There are two basic systems of accounting. I. Cash syst em of accou ntin g II. Accru al S ystem of Accoun ting I. Ca sh system of accounting It is the system in which accounting in which entries are made only when cash is received or paid. No entry is made when a payment or receipt is merely due. II . Accrual System of Ac counti ng It is the system in which accounting entries are made on the basis of amount having become due forpayment or receipt . Accounting Terminology To start the accounting we must have to familiar with some important accounting terms: Transaction: Prepared by: Syed Waseem HaiderBranches of Accounting Financial Accounting Cost Accounting Management Accounting

NOTES According to VU SyllabusAny dealing between two persons or things is a transaction.

Business:

It includes any activity undertaken for the purpose of earning profit e.g banking business, an insurancebusiness, a merchandise business etc.

Proprietor / Owner:

He is the owner of a business. He invests capital in it, gives his time and attention to it. He is entitled to

receive the profit. Or bear loss arising out of it.

Capital:

The resources invested by the investor to starts his business at any given time is known as CapitalPurchase:

Goods / things purchased in bundles are called Purchases. Purchases may be of two types: cash

purchase (purchased in cash payment) and Credit Purchases (purchases in which payment will have to

be made some future date it is known as credit purchases.

Purchase Return:

If goods purchased are found defective or unsatisfactory, the are sometimes returned to the persons

from whom they were purchased or to suppliers are called purchases returns or return outwards.

Sale:

Goods / things sold are called sale. Purchases may be of two types: cash purchase (purchased in cash

payment) and Credit Purchases (purchases in which payment will have to be made some future date it is

known as credit purchases.

Sales Return:If a person to whom goods have been sold finds that they are defective or unsatisfactory and returns

them are called sales returns or return inwards.

Expense

It means an expenditure whose benefit is finished or enjoyed immediately such as salaries, rent etc.

distinction between expense and expenditure is that the benefit of the former is consumed by the

business in present whereas in later case benefit will be available for future activities of the business.

Expenditure

Expenditure takes place when assets or service is acquired.

Account:

A summarized record of transactions relating to a person or thing is called an account.

Debtor (Account Receivable):

When we sell good on credit or somebody take a loan from us and he has to pay back in future, thoseare called our debtors or account receivable. These are also called our assets.

Creditor (Account Payable):

When we purchase goods on credit or take a loan from others, we are treated as creditors. Also called

account payable because we have to pay back the money in future date.

Assets:

The things which are in possession of the owner or proprietor or trader are called assets, like building

car, furniture etc.

Liabilities

These are the debts due by a business to its proprietor and other. The liabilities are may be a short term

based or long term based.

ing EquationThe accounting equation is

Assets = Liabilities + Owner's (Stockholders') Equity.The accounting equation should remain in balance at all times because of double-entry

accounting or bookkeeping. (Double-entry means that every transaction will affect at least twoaccounts in the general ledger.)

Here are some examples of how the accounting equation remains in balance.An owner's investment into the company will increase the company's assets and will alsoincrease owner's equity. When the company borrows money from its bank, the company'sassets increase and the company's liabilities increase. When the company repays the loan

NOTES According to VU Syllabusthe company's assets decrease and the company's liabilities decrease. If the company payscash for a new delivery van, one asset (cash) will decrease and another asset (vehicles) willincrease.If a company provides a service to a client and immediately receives cash, the company's

assets increase and the company's owner's equity will increase because it has earnedrevenue. If the company provides a service and allows the client to pay in 30 days, thecompany has increased its assets (Accounts Receivable) and has also increased its owner'sequity because it has earned service revenue. If the company runs a radio advertisement and

agrees to pay later, the company will incur an expense that will reduce owner's equity and hasincreased its liabilities.

From our examples, you can see that owner's equity increased when the owner made aninvestment in the business and also when revenues were earned. Owner's equity decreasedwhen the owner withdrew assets from the business and when expenses were incurred. Thisleads us to the expanded accounting equation:

epingIn years past, bookkeeping entailed writing/recording debit and credit entries into a

journal. Debits were entered on the left and credits on the right. After journalizing thetransactions, the amounts were posted to the proper accounts in the general ledger. Becausethis tedious and time consuming process usually resulted in errors, the bookkeeper prepareda trial balance. A trial balance showed that the debit balances in the accounts added to thesame total as the credit balances. After the bookkeeping errors were corrected, theaccountant prepared adjusting entries followed by the financial statements.

Today, computer software has eliminated much of the manual journalizing and posting. Thebookkeeping is still taking place, but it is being done within the accounting software. Forexample, each time a check is prepared the Cash account is credited and the softwareprompts the person at the computer to enter the account to be debited. When a sales invoiceis prepared using the accounting software, Accounts Receivable is automatically debited and

the Sales account is credited. In addition, the individual customer's record is updated as welas inventory and the cost of the goods sold.

Since the software demands that the debits and credits are equal in amount, and since thecomputer doesn't miscalculate balances, most of the clerical errors are eliminated.

At larger companies, there are now accounts receivable clerks, accounts payable clerkspayroll clerks, cost accounting clerks, and others to assist with the bookkeeping.

and CreditsDebits and credits are part of double entry accounting and bookkeeping. Recording a

transaction under double entry requires that at least one account will have an amount entered

as a debit-which means entered on the left side of an account. It also requires that at leastone account will have an amount entered as a credit -which means entered on the right side ofan account. Each transaction must have the total of the debits equal to the total of the credits.To increase the balance in an asset or expense account, you enter an amount as a debit. Todecrease the balance in an asset or expense account, you enter an amount as a credit.

Liabilities, revenues, and stockholders' (owner's) equity accounts are also increased with acredit. They are decreased with a debit.

Here are five examples to illustrate debits and credits:

NOTES According to VU Syllabus1. If a company borrows $5,000 from the bank, the company will debit Cash(because this asset increased) and will credit Notes Payable (because this liabilityincreased).2. When a company collects $400 from its customers who were billed earlier, thecompany will debit Cash (because this asset is increased) and will credit AccountsReceivable (because this asset decreased).3. If a company bills a client for a service, the company will debit AccountsReceivable (because this asset increased) and will credit Service Revenues (because

revenues increased and that in turn increases owner's equity).4. When a company pays $600 for the current month's rent, the company willdebit Rent Expense (because expenses increased and that in turn decreases owner'sequity) and will credit Cash (because this asset decreased).5. If J. Smith, a sole proprietor, withdraws $300 from the business for personaluse, the business will debit the account J. Smith, Drawing (because owner's equitydecreased) and will credit Cash (because the asset decreased).

Periodically, a trial balance is prepared to prove that the total of the debit balances in theaccounts is equal to the total of the credit balances in the accounts.

Rules of Debit and Credit

Follow these rules, this is the base of accounting

Assets Increases Debited

Decreases Credited

Liabilities Increases Credited

Decreases Debited

Capital Increases Credited

Decreases Debited

____________________________________________

Drills on Next Page

DRILLS for...

Accounting Equation

NOTE: For multiple-choice and true/false questions, simply place your cursor over what you think is the correct answer. (There is no

need to click the answer.) For fill-in-the-blank questions place your cursor over the _________ .

If you have difficulty answering the following questions, learn more about this topic by reading our Accounting Equation

Explanation.

Make the correct answer highlighted.

1. The basic accounting equation is Assets = Liabilities + __________ _______ .

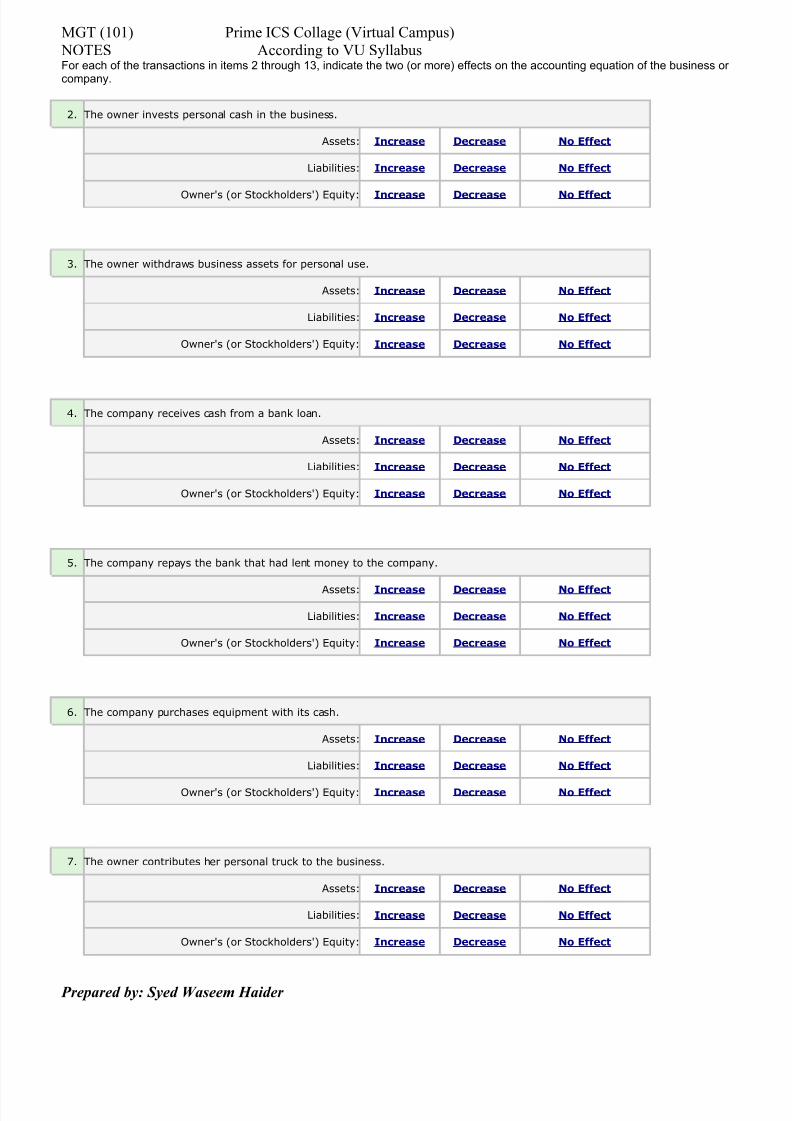

NOTES According to VU SyllabusFor each of the transactions in items 2 through 13, indicate the two (or more) effects on the accounting equation of the business or company.

2. The owner invests personal cash in the business.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

3. The owner withdraws business assets for personal use.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

4. The company receives cash from a bank loan.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

5. The company repays the bank that had lent money to the company.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

6. The company purchases equipment with its cash.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

7. The owner contributes her personal truck to the business.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

8. The company purchases a significant amount of supplies on credit.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

9. The company purchases land by paying half in cash and signing a note payable for the other half.

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

Information for Items 10 through 13:Company X provides consulting services to Client Q in May. Company X bills Client Q in May for the agreed upon amount of $5,000.The sales invoice shows that the amount will be due in June.

10. In May, Company X records the transaction by a debit to Accounts Receivable for $5,000 and a credit toService Revenues for $5,000. What is the effect of this entry upon the accounting equation for Company

X?

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

11. In June, Company X receives the $5,000. What is the effect on the accounting equation and whichaccounts are affected at Company X?

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

12.

What is the effect on Client Q's accounting equation in May when Client Q records the transaction as adebit to Consultant Expense for $5,000 and a credit to Accounts Payable for $5,000?

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

13. What is the effect on Client Q's accounting equation in June when Client Q remits the $5,000? Also, whichaccounts will be involved?

Assets: Increase Decrease No Effect

Liabilities: Increase Decrease No Effect

Owner's (or Stockholders') Equity: Increase Decrease No Effect

14. Which of the following will cause owner's equity to increase?

expenses owner draws revenues

15. Which of the following will cause owner's equity to decrease?

net income net loss revenues

16. The accounting equation should remain in balance because every transaction affects how many accounts?

only one only two two or more

17.A corporation's net income is eventually recorded in the following stockholders' equity account:___________ ___________ .

18.A corporation's quarterly _______________ will cause a reduction in the corporation's retained earnings,which in turn reduces the corporation's stockholders' equity. However, this will not reduce the corporation'snet income.

19.The financial statement with a structure that is similar to the accounting equation is the _____________ _____________ .

20.The financial statement that reports the portion of change in owner's equity resulting from revenues andexpenses during a specified time interval is the ____________ _______________ .