20

22/09/05 High frequency dynamics in financial markets State of the art of the project and of the national facility of financial data.

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 213 times |

| Download: | 0 times |

22/09/05

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

State of the art of the project and of the national

facility of financial data.

22/09/05 2

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

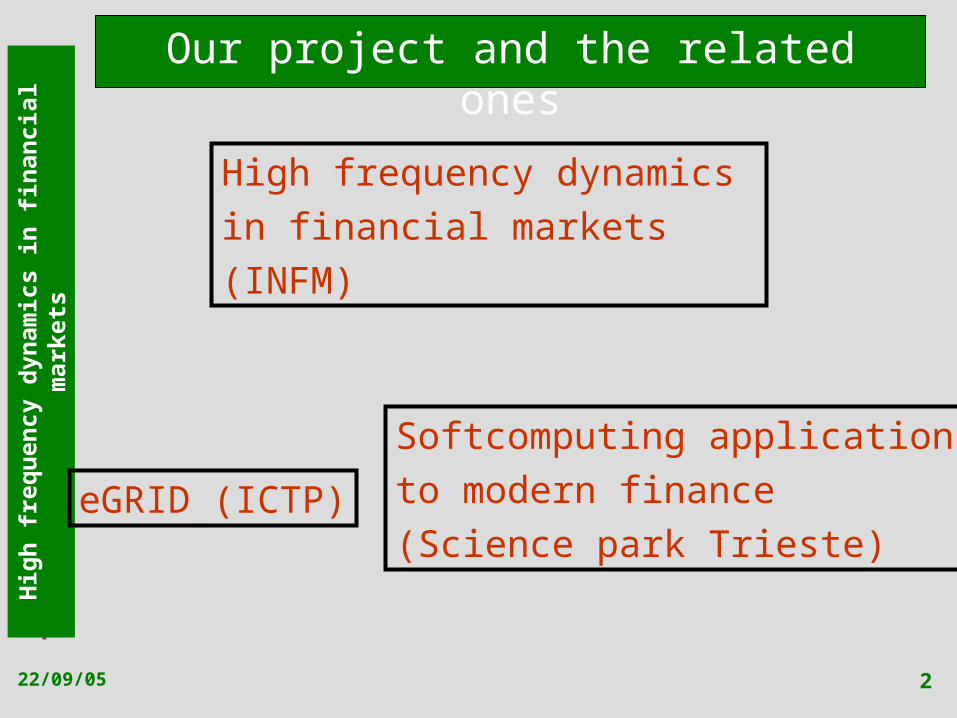

Our project and the related ones

High frequency dynamics in financial markets(INFM)

eGRID (ICTP)

Softcomputing applicationsto modern finance (Science park Trieste)

22/09/05 3

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Research institutions re-organization

INFM is now part of CNR. This re-organizationshould not affect the development of the project but will certainly affect future research possibilities.

22/09/05 4

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Work package 1

Contribution of INFM to the realizationof a “national facility” of financial data

The national facility is designed and maintainedby ICTP (within the eGRID project) but thefinal property of data is of INFM.

22/09/05 5

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Data of the facility

"Rebuild Order Book" of London Stock Exchange (LSE) year 2002

"Trades and Quotes" (1995-2003) and "Open Book" (2002) of the New York Stock Exchange (NYSE),

“Intraday Historical Euronext Data" of the Paris, Brussels andAmsterdam (year 2002). We are also trying to buy the orderbook related to these transactions

Intraday trades, best 5 quotes for the Milan Stock Exchangeyear (2002).

22/09/05 6

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Data of the facility

“Trades” of the Tokyo Stock Exchange, year 2002.

Money Exchange trough “Depositi Interbancari” of the electronic market E-MID S.p.a., year 2002.

S&P 500 Index and Future from TickData. Years 1982-2004 .

We have ordered the tick data of “MTS Time Series” fromEuroMTS l.t.d., from April 2003 to March 2004.

22/09/05 7

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

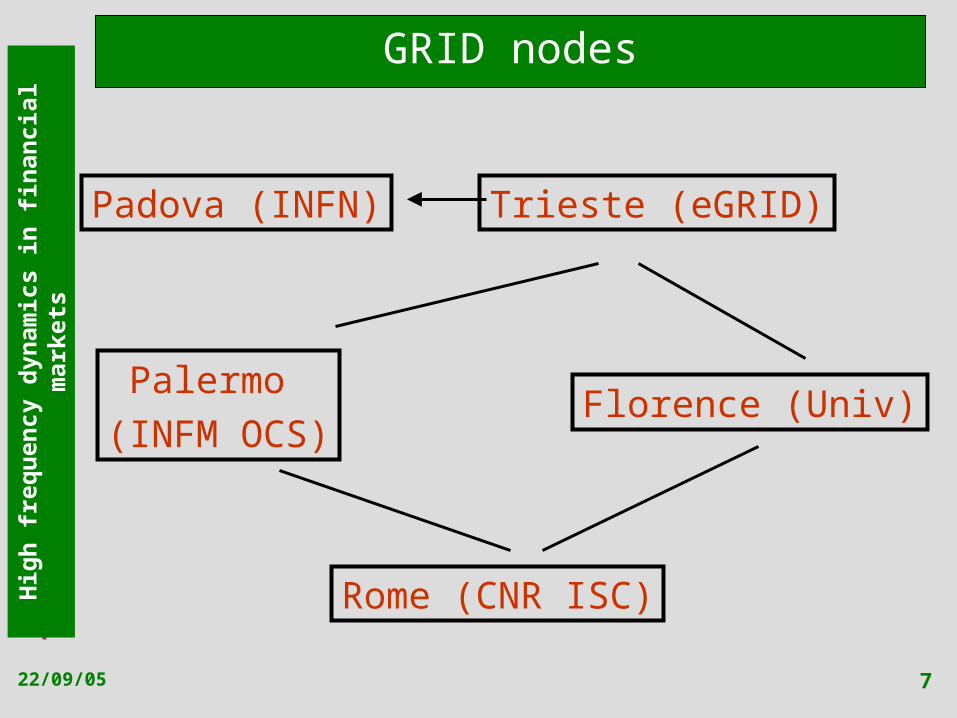

GRID nodes

Trieste (eGRID)Padova (INFN)

Palermo (INFM OCS)

Rome (CNR ISC)

Florence (Univ)

22/09/05 8

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Pre-processing of data

Flat files have been obtained for the LSE (A. Tedeschi, A. Ponzi)

An efficient sorting has been devised for NYSEand time series sampled at intraday fixed time intervals have been obtained (A. Tedeschi, C. Brownlees, C. Coronnello)

22/09/05 9

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Pre-processing of the data

A reconstruction of the LSE order book has been achieved for the Set 1 stocks of that market(A. Ponzi)

Correlation based graphs have been obtained for LSE, NYSE and Parigi stocks and a series of conditions and methods (S. Miccichè and C. Coronnello)

22/09/05 10

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Flat file exampleO

rder

ty

peHi

stor

y ty

pe

Ord

er

Code

Buy

Sell

Ind

Trad

e si

ze

Trad

e Pr

ice

Epoc

h Ti

me

Year

Mon

thDa

y

Hour

Min

ute

Seco

ndAg

ent

Id Tick

si

ze

Trad

e pr

ice

Rem

ain

ing

Size

Endi

ng

Hist

ory

Type

Endi

ng

Tim

e

Mat

chi

ngLO

Mat

chi

ng

Pric

eM

atch

ing

O

rder

Nu

mbe r

Agen

t ID

ofM

O

Best

Bi

d

Best

O

ffer

1 1 C01YD1CA02 2 0 341.0 1023265421 2002 6 5 10 23 41 0 1 0.0 2300 3 1023265421 0 341.0 0 0 343.5 350.01 2 C01YD1CA02 2 1000 341.0 1023265421 2002 6 5 10 23 41 0 1 343.5 1300 0 1023265421 1 343.5 701VLMAW02 0 343.5 350.01 3 701VLMAW02 1 1000 343.5 1023265421 2002 6 5 10 23 41 0 1 343.5 0 0 1023265421 1 341.0 C01YD1CA02 0 343.5 350.01 2 C01YD1CA02 2 1299 341.0 1023265421 2002 6 5 10 23 41 0 1 343.5 1 0 1023265421 1 343.5 E01WARGE02 0 343.5 350.01 3 E01WARGE02 1 1299 343.5 1023265421 2002 6 5 10 23 41 0 1 343.5 0 0 1023265421 1 341.0 C01YD1CA02 0 343.5 350.01 3 C01YD1CA02 2 1 341.0 1023265421 2002 6 5 10 23 41 0 1 343.5 0 0 1023265421 1 343.5 C01YD1C902 0 343.5 350.01 2 C01YD1C902 1 1 343.5 1023265421 2002 6 5 10 23 41 0 1 343.5 1000 0 1023265679 1 341.0 C01YD1CA02 0 343.5 350.0

22/09/05 11

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

The real behavior in a short time for a normal stock

- sell limit orders

- buy limit orders

○ sell market orders

x buy market orders

spread first sell gapfirst buy gap

Order book dynamics

22/09/05 12

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Order book dynamics

A slightly longer time interval

22/09/05 13

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

A rogue trade on September 20, 2005

22/09/05 14

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Correlation based networks

The “traditional” MST

22/09/05 15

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

The Planar maximally filtered graph

mst

22/09/05 16

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Work package 2

Modeling financial markets with Agent Based Models

- Ancona Unit

- Trieste Unit

22/09/05 17

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

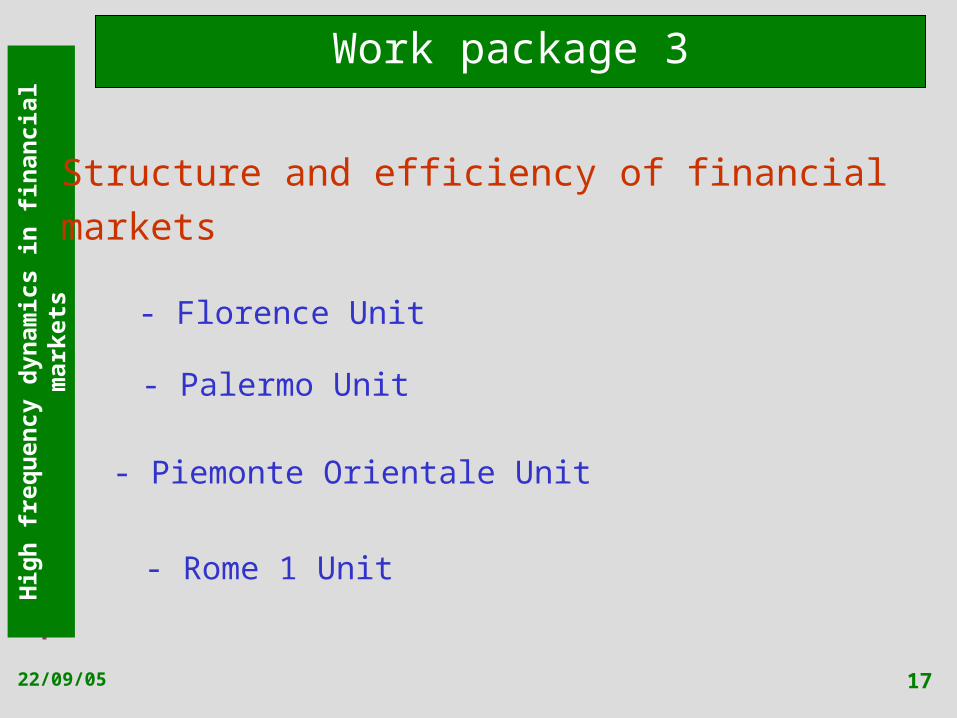

Work package 3

Structure and efficiency of financialmarkets

- Palermo Unit

- Piemonte Orientale Unit

- Rome 1 Unit

- Florence Unit

22/09/05 18

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

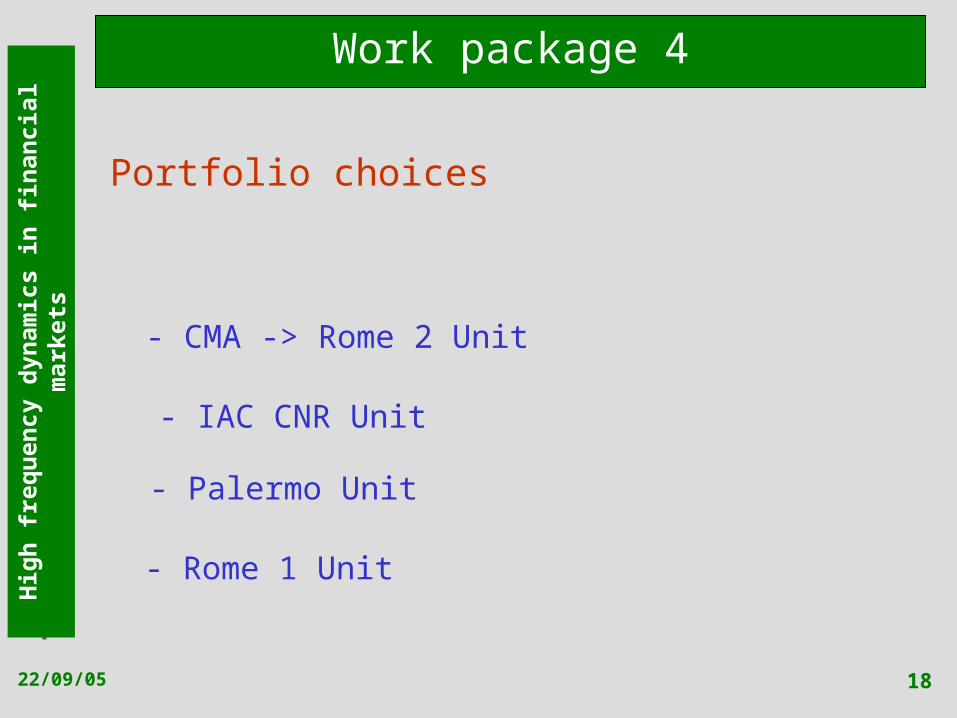

Work package 4

Portfolio choices

- Palermo Unit

- CMA -> Rome 2 Unit

- Rome 1 Unit

- IAC CNR Unit

22/09/05 19

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Conferences

Conference at Roma 2 December (5-7) with a session on “Physics in Finance”chairman Prof. M. Bagella

Workshop on Grid Technology for FinancialModeling and Simulation to be held in Palermo, Italy, from February 3 to 4, 2006 (Chairmen S. Cozzini, S. d’Addona, R.N.Mantegna)

22/09/05 20

Hig

h f

req

uen

cy d

yn

am

ics in

fin

an

cia

l m

ark

ets

Administration

Our first reference is always Stefania Scotto at INFM-CNR in Genova.