87

HIH Case Study on Provisioning Round 2 30 Aprl 2000 A Core Curriculum for Insurance Supervisors

�

HIH Case Studyon Provisioning

Round 230 Apr�l 2000

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organiza-tions with permission. Please contact the IAIS to seek permission.

�

HIH Case Study on Provisioning (Round 2)

The primary objective of this round of the case study is to ascertain what role, if any, poor measurement or misstatement of insurance liabilities played in the collapse of HIH; what warning signals, if any, were provided by the information that was available to the regulator; and what actions, if any, would be appropriate for a regulator in the face of such information.

It is relevant to note that, since round 1, HIH has successfully bid for and taken over FAI Insurance.

Attached is a briefing note prepared by the senior manager of the branch respon-sible for HIH.

Your tasks for this round are to assess the information provided in order to:

• Identify and list major concerns with HIH’s outstanding claims provision (OCP), identifying any particular portfolios that cause you concern

• Draft a brief memo to the APRA board (a bullet point outline is sufficient) indi-cating your concern, if any, regarding HIH’s OCP and its effect on HIH’s regula-tory solvency position. This memo should recommend and justify (in terms of the law) a course of supervisory action.

Insurance Superv�s�on Core Curr�culum

2

MEMORANDUM FOR GENERAL MANAGERBRIEFING NOTE ON HIH INSURANCE LIMITED

30 September 2000

At a recent industry function, two participants from another general insurance com-pany suggested that APRA should have a close look at the claims provisioning practices of HIH. In addition to this market intelligence, we have also received an anonymous document from an ex-HIH employee which criticizes the company’s approach in a number of areas, including provisioning. This information is somewhat at odds with our own risk rating of HIH as low risk (see Attachment 2).

In light of this information and given past concerns about the level of provisioning within FAI (now part of the HIH Group), I believe it is timely to closely review the ad-equacy of HIH’s outstanding claims provisions (OCP).

I have attached the following for your information:

• Attachment 1—Relevant extracts from the briefing note prepared for APRA’s first prudential visit to HIH earlier this month.

• Attachment 2—A file note prepared earlier this month in relation to the an-nual review of HIH C&G as at 30 June 1999. Appended to Attachment 2 are a printout from APRA’s Genesis Analytic System showing HIH’s claims assess-ment for June 1999 (based on Quarterly return data) and the HIH (C&G) an-nual returns (form 108) to APRA as at 30 June 1999 and 31 December 1997.

• Attachment 3—A file note providing extracts from an anonymous document received by APRA entitled “HIH Due Diligence”.

• Attachment 4—A memorandum from a meeting with HIH’s consulting actuary David Slee conducted as a follow up to the anonymous report.

• Attachment 5—Conclusions from a paper presented to the Institute of Actuaries of Australia seminar in November 1997 titled “Public and Products Liability—Experience, Expectations, Expensive?”

• Attachment 6—Extract from a paper entitled “Lack of Industry Profitability and Other Stories” by Peter McCarthy and Geoff Trahair (well respected company actuaries) presented to the Institute of Actuaries of Australia’s Twelfth General Insurance Seminar in November 1999. As with Attachment 5 the issues appear to be relevant to HIH.

Senior Manager

HIH Case Study on Prov�s�on�ng (Round 2)

3

Attachment 1

Memorandum

Extracts from Briefing Note on HIH for First Prudential Visit (Scheduled for 9 March)

7 March 2000

Introduction

HIH Insurance is currently the second largest General Insurance group in Australia, after NRMA/RACV (in terms of Inside Australia business). It has approximately 13% market share by Gross Earned Premium and 15% market share by Total Assets.

HIH Insurance Limited changed its financial year-end from 31 December to 30 June and the reporting period to June 1999 is therefore an 18-month period. APRA and ASIC both approved the above changes.

Acquisitions

A number of acquisitions took place in the 1998/1999 financial year. The most signifi-cant of these, in terms of impact on HIH’s asset structure, liabilities, product distribu-tion and many other areas, was the acquisition of FAI.

Investment Strategy

The takeover of FAI confirmed HIH’s strategies to secure a major market share position in Australia, change its business mix and to diversify distribution into every available distribution channel. HIH continues to adopt the strategy of selling non-core assets inherited from FAI. Recent media reports about the intention to sell its interest in the St Moritz Hotel in New York were confirmed on the 2nd of March, when HIH announced a deal to sell 50% of its stake in the property for US $65 million and lease the other 50% on a 75-year lease.

HIH’s investment strategy is based on the premise that the Group’s business risk should not be compounded by asset risk. HIH’s preferred strategy is to hold a large pro-portion of cash and fixed interest assets, the cashflows of which are matched with the expected cashflows of the liabilities.

Insurance Superv�s�on Core Curr�culum

�

Ratings

Standard & Poor’s has given a financial strength rating of A- (Strong) to all the core un-derwriting entities in the HIH Insurance Group. This includes all the major Australian subsidiaries: CIC Insurance, FAI General Insurance and HIH Casualty and General.

Solvency & Capital

HIH Insurance Group has net assets of $946.4 million (see summary balance sheet for June 1999 in Annex). This includes Intangibles and future income tax benefits which are excluded from the statutory solvency calculation. The assets that can be counted to-wards solvency total $572.7 million. The required solvency margin for the group, based on the 15% of Outstanding Claims Provision test (the operative test for HIH) is $397.4 million. This gives HIH Insurance Group a solvency surplus of $175.3 million (solvency coverage of 144%). The calculations are summarized below:

There are views in the market that HIH’s capital ratios are too low. These views were not supported by the Standard & Poor’s report (February 2000), which stated that:

“Capitalization is considered sound in the context of the nature of HIH’s insurance risk profile, the use of subordinated debt and hybrid instruments to support solvency, and the level of growth assets present”

S&P maintained its A- rating for the group. A recent report by ABN-AMRO ex-pressed an opinion that the capital problem lies in funding high levels of future growth. The report stated that modest organic growth can be met by existing capital resources and reinsurance, but faster (e.g. double-digit) growth in net premiums will need a cap-ital issue.

Overall, I believe that HIH’s capital levels are adequate provided future growth is predominantly organic rather than by takeover. There was mention in a recent news-

June �999 $m $m $m

Shareholders’ Equity 946.4

Less Statutory Exclusions

Intangibles –346.5

Future Income Tax Benefit –27.2 –373.7

Net Assets less Statutory Exclusions 572.7

OCP net of Reinsurance recoveries 2,649.3

Minimum solvency (15% x OCP) 397.4

Solvency Surplus 175.3

Solvency Coverage 1.44

HIH Case Study on Prov�s�on�ng (Round 2)

�

paper article that HIH may be considering a capital raising in the first half of 2000. At this point HIH still has a sizeable issue of Convertible and Converting Notes. These will need to convert to equity to support further growth.

Assets

For a break-down of some of HIH’s asset classes as at June 1999 see the summary bal-ance sheet in the attached annex.

According to their 1999 Annual Report all assets are measured at net market value (market less estimated selling costs) at balance date. Changes in market value between balance dates are recognized in the profit and loss account. Market values of non-traded assets are recorded at independent valuations or at the directors’ valuations based on current economic conditions.

With the exception of some investments taken over from FAI, HIH has a relatively conservative investment strategy. The group believes that an aggressive investment strategy would introduce volatility to performance.

The effect of the FAI acquisition on the investment portfolio has been to add sub-stantial amounts of property and equity as well as some other classes of investments. A recent article in the Sydney Morning Herald hinted that HIH is keen to reduce the amount of property in its investment portfolio. I believe this to be a move in the right direction.

Liabilities

HIH’s outstanding claims provision for the Group rose from $2 billion to $3.7 billion between 31/12/1997 and 30/6/1999. This was largely due to the acquisition of FAI. The ABN-AMRO report mentioned above, expressed some concerns regarding HIH’s claims reserves. It stated that some market analysts perceive them to be inadequate, but it stressed that these views are unproven. It is hard to assess the adequacy of HIH’s OCP without an actuarial review, but the recently signed agreement between HIH and Swiss Re and the $250 million deterioration in the current OCP cover should provide some comfort to APRA.

HIH has $0.5 billion in various borrowings including bond issues, various loans and convertible notes issue. There are a number of hybrid instruments issued by HIH and they include Converting Notes currently at $213.1 million all classified as equity and Convertible Notes at $121 million of which $65.3 million is equity and the re-maining $56 million is debt.

Insurance Superv�s�on Core Curr�culum

�

Reinsurance

The HIH Group has two sets of reinsurance arrangements in place. The first one is a tra-ditional reinsurance program and the second one a balance sheet protection program in the form of financial reinsurance with a profit-smoothing component.

APRA has recently approved a balance sheet protection agreement between HIH and Swiss Re as reinsurance. This is a five-year (from 1 July 1999 to 30 June 2004) multi-class agreement that sits on top of the existing reinsurance program. It provides some protection in case there is some deterioration in the current OCP as well as acts as a profit smoothing mechanism. It is a self-funding program with a small amount of risk transfer (which was deemed to be sufficient for the program to be treated as rein-surance) and it will have an effect of reducing the volatility in reported earnings of the Group and the Share Price.

Outlook

A number of events took place in recent months which should translate into a more positive outlook for HIH in terms of profitability. The recent rise in interest rates (and bond yields) and any further rises will have a positive effect on the group. A recent fall in the value of the bond portfolio was and will be offset by a similar fall in the OCP, as the group matches its assets and liabilities. Any new cash inflows will be invested at higher yields, and should thereby have a positive effect on operating results.

Diversification of the US worker’s compensation business out of California and rising premium rates in California will have a strong positive effect on the performance of the region. Performance in the UK market should also improve with reductions of net retentions on the catastrophe account and the unlikely scenario of continued fre-quency and severity catastrophes in the world.

The profit smoothing agreement with Swiss Re will reduce the volatility of earn-ings over the next few years. The most likely scenario is that HIH Insurance will report higher (than actual) earnings in the first two years of the agreement (i.e. 1999/2000 and 2000/2001) and lower (than actual) earnings in the remaining years. The expected strong rise in premium rates over the two to three years is expected to neutralize the effect of reduced earnings in the later years of the agreement.

There are a number of threats to HIH which have the potential to significantly af-fect its results in the future. Rising reinsurance premiums will undoubtedly have a large impact, especially for a company that cedes almost a third of its premiums. HIH will either have to increase its retentions (as they have indicated they might do with the first catastrophe layer—increasing event retentions to $20 million) or pay higher reinsur-ance premiums. Both strategies have disadvantages.

The new Goods and Services Tax (GST) system of indirect taxes (to be introduced on 1 July of this year) will also test HIH’s computer systems. The ability of computer

HIH Case Study on Prov�s�on�ng (Round 2)

�

systems to cope will be tested as will the adequacy of provisions raised to cope with the tax liability. The last and probably most significant threat is the possibility of a property and sharemarket correction in the future. The fall in property prices in Sydney would have a strong effect on the profit and loss statement as would a fall in stock prices. HIH has a significant exposure to the property market. The group has a hedging program in place for its equity book, but this might prove not to be enough.

Overall the outlook for HIH Insurance Group is strong and, provided no extraor-dinary event like a large market correction or another Sydney hailstorm occurs, the group should see improved results in the future.

Senior Analyst

Insurance Superv�s�on Core Curr�culum

�

Annex to File Note 7 March 2000

Summary of Audited Balance Sheet for HIH Group as at June 1999

June �999 $m $m

Current Assets 3,596.8

Cash 638.7

Receivables 1,427.0

Investments 803.5

Reinsurance recoveries receivable 415.5

Deferred acquisition costs 278.3

Other 33.8

Non-Current Assets 3,264.5

Receivables 35.0

Investments 1,790.1

Plant and equipment 147.8

Reinsurance recoveries receivable 634.7

Intangibles 346.5

Other 310.4

Plus:

NSW Workers Compensation Statutory Funds 864.1

Total Assets 7,725.4

Current Liabilities 3,289.1

Creditors and borrowings 754.5

Provisions 46.3

Outstanding Claims 1,415.5

Unearned premiums 1,038.9

Other 33.9

Non-Current Liabilities 2,625.8

Creditors and borrowings 335.8

Provisions 6.0

Outstanding claims 2,284.0

Plus:

NSW Workers Compensation Statutory Funds 864.1

Total Liabilities 6,779.0

Net Assets 946.4

Shareholders’ Equity

Share Capital 684.2

Convertible Notes 65.3

Converting Notes 213.1

Reserves –1.0

Retained profits –26.5

Total equity of Parent Entity 935.1

Outside equity interests in controlled entities 11.3

Total Shareholders’ Equity 946.4

HIH Case Study on Prov�s�on�ng (Round 2)

9

Attachment 2

Note for File APRA

Ref: HIH C&G Annual Review as at 30 June 199924 March 2000

IntroductionHIH Casualty and General Insurance Limited (HIH C&G) is one of three main un-derwriters in the HIH Group, which is the second largest general insurance group in Australia, after NRMA. The group writes business in all classes and in all states in Aus-tralia as well as UK, New Zealand, Hong Kong, Argentina and California. Total assets of the group are approximately $8 billion with net assets at $1 billion. The group’s net premium revenue is about $2 billion.

HIH has taken over a number of companies in recent times, including CIC Insur-ance, FAI Insurance and most recently World Marine and General Insurance (bought from BHP). Thus the group continues to face a number of challenges, trying to achieve as many benefits from these acquisitions as possible.

HIH C&G specializes in commercial underwriting, with casualty classes (PI, Public Liability, Worker’s Compensation (WC) and Commercial Motor Vehicle (CMV)) and Marine & Aviation being the main classes it underwrites. The company has paid up capital of $439.225 m and is categorized as low priority. An unqualified auditor’s state-ment was signed by the approved auditor Mr. Alan P. Davies of Arthur Anderson.

A consultation took place with HIH on March 9, 2000. It took the form of a number of presentations by the upper management of the company.

Solvency

Solvency Surplus $169.7 m (In Total); $278.1 m (Inside Australia)Solvency Coverage 2.5 (In Total); 4.66 (Inside Australia)The solvency surplus rose over the past 18 months from $130.2 m to $169.7 m.

Insurance Superv�s�on Core Curr�culum

�0

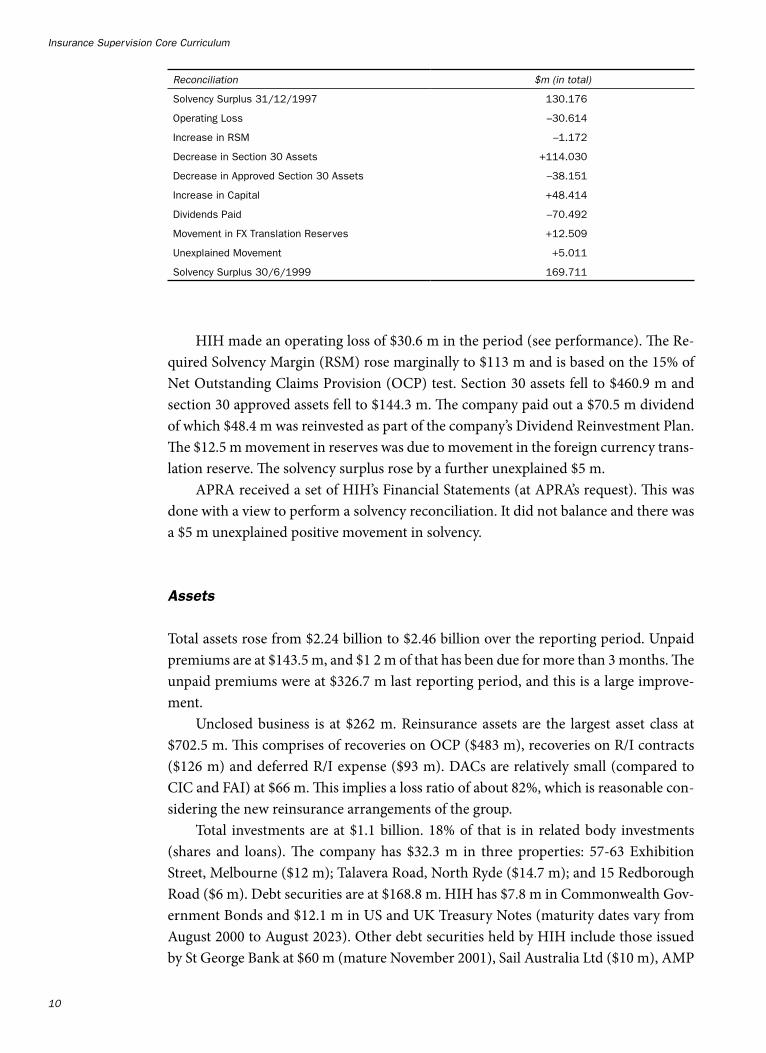

HIH made an operating loss of $30.6 m in the period (see performance). The Re-quired Solvency Margin (RSM) rose marginally to $113 m and is based on the 15% of Net Outstanding Claims Provision (OCP) test. Section 30 assets fell to $460.9 m and section 30 approved assets fell to $144.3 m. The company paid out a $70.5 m dividend of which $48.4 m was reinvested as part of the company’s Dividend Reinvestment Plan. The $12.5 m movement in reserves was due to movement in the foreign currency trans-lation reserve. The solvency surplus rose by a further unexplained $5 m.

APRA received a set of HIH’s Financial Statements (at APRA’s request). This was done with a view to perform a solvency reconciliation. It did not balance and there was a $5 m unexplained positive movement in solvency.

Assets

Total assets rose from $2.24 billion to $2.46 billion over the reporting period. Unpaid premiums are at $143.5 m, and $1 2 m of that has been due for more than 3 months. The unpaid premiums were at $326.7 m last reporting period, and this is a large improve-ment.

Unclosed business is at $262 m. Reinsurance assets are the largest asset class at $702.5 m. This comprises of recoveries on OCP ($483 m), recoveries on R/I contracts ($126 m) and deferred R/I expense ($93 m). DACs are relatively small (compared to CIC and FAI) at $66 m. This implies a loss ratio of about 82%, which is reasonable con-sidering the new reinsurance arrangements of the group.

Total investments are at $1.1 billion. 18% of that is in related body investments (shares and loans). The company has $32.3 m in three properties: 57-63 Exhibition Street, Melbourne ($12 m); Talavera Road, North Ryde ($14.7 m); and 15 Redborough Road ($6 m). Debt securities are at $168.8 m. HIH has $7.8 m in Commonwealth Gov-ernment Bonds and $12.1 m in US and UK Treasury Notes (maturity dates vary from August 2000 to August 2023). Other debt securities held by HIH include those issued by St George Bank at $60 m (mature November 2001), Sail Australia Ltd ($10 m), AMP

Reconc�l�at�on $m (�n total)

Solvency Surplus 31/12/1997 130.176

Operating Loss –30.614

Increase in RSM –1.172

Decrease in Section 30 Assets +114.030

Decrease in Approved Section 30 Assets –38.151

Increase in Capital +48.414

Dividends Paid –70.492

Movement in FX Translation Reserves +12.509

Unexplained Movement +5.011

Solvency Surplus 30/6/1999 169.711

HIH Case Study on Prov�s�on�ng (Round 2)

��

Infrastructure Trust ($17.9 m), Goldman Sachs ($3.7 m) and KFW International Fi-nance ($2.5 m). QTC, WATC and NSWTC (State issued Treasury Corporations) Bonds are at $53.8 m. They have various maturity dates and as seen above are issued by a number of different issuers.

$244 m (10%) is in various unlisted equity unit trusts including Lend Lease Invest-ment Trust ($134.8 m), First State Fund ($65.2 m), Macquarie Investment Limited ($8.9 m) and State Street Unit Trust ($23 m). HIH also has $20.3 m worth of direct share-holding in 29 companies. This portfolio appears well diversified with Keycorp Ltd ($3.9 m), News Corporation Ltd ($1.9 m), Rio Tinto Ltd ($1.36 m) and NAB ($1 m) being the four largest shareholdings.

HIH has $129 m (5.2%) in various deposits - $35 m is with SG, $31.2 m in BT Fu-tures account (all inside Australia) and $19.3 m is with AMP and $15.4 m with Courts (both in UK).

Total loans are at $152.4 m (2.2%). Staff loans are at $566K (excluded under sec-tion 30). Loans to non-related parties are at $55 m. The largest ones are to Lonplot Pty Ltd at $39.9 m, Wylde Street Potts Point at $9.6 m and Merwala P/L at $3.9 m. Loans to various related bodies are at $97 m

Related body shareholdings are a very significant item at $350.8 m (14.2%). There is a $197.7 m stake in CIC Insurance Ltd ($17.1 m of that has been section 30 approved - solvency surplus); $127.1 m stake in CIC General Insurance Holdings Ltd (all section 30 approved); $21.4 m stake in HIH (NSW) Pty Ltd (not approved); and various others (not approved).

HIH uses equity and bond futures as a hedging tool. They reported an aggregate exposure to all derivatives at $27.2 m. Currently the BT futures held have market value of $3.5 m.

Liabilities

Total liabilities rose from $1.6 billion to $1.865 billion. UPP is the second largest liability at $359.6 m (19.3%). After adjusting the total premium figure, to only reflect the last 12 months, the UPP to Total Premium ratio is at 48.6%. The OCP rose from $1.05 billion to $1.236 billion (17.8% rise). The inside Australia reported provision is lower than the actuarial estimate (there are no data about the outside Australia provisions). The classes of business with a deficit include Marine & Aviation ($5 m deficit), public & products liability ($77 m deficit), WC ($6 m) and other ($31 m). It is uncertain whether any pru-dential margins have been included in the actuarial estimates. It would appear prudent from APRA’s perspective to request an actuarial review of the OCP calculation.

The claims assessment form produced by Genesis (see Appendix) has produced a number of ‘alerts’. Average provisions for PI and WC are marginally below ‘standard amounts’; loss ratio for HH is lower and for PI, PL and I/T higher than the ‘standard range’; Average Provisioning divided by Average Settlement Cost is too low for PI, PL

Insurance Superv�s�on Core Curr�culum

�2

and WC; and Provisions divided by Net Claims Paid is too low for ISR, Aviation, PI, PL, Travel and LT. I do not consider any of the above to be too significant.

Other large liabilities include amounts due on R/I at $184 m (9.9%), bank balances at $22.3 m, all other provisions at $38 m and other creditors at $25.8 m.

Performance

Premium revenue rose from $715 m to $1,081 m. The second figure is for 18 months and misleading (changing it to a 12 months figure gives us $721 m, a marginal in-crease). R/I expense was high at $417.7 m ($278.5 m adjusted). NEP was at $663.6 m for the 18 months and net claims expense at $739.4 m giving the company a 111.4% loss ratio. Underwriting expenses were at $163.9 m (expense ratio of 24.7%; 25.4% if General and Admin expenses are included), giving HIH an underwriting loss of $239.7 m. This is significantly worse than the underwriting loss of $32.1 m experienced in the last reporting period (loss ratio of 88% and expense ratio of 18%).

The loss ratios for each class of business for the last two reporting periods (1997 and 1998/1999) are summarized below, with average percentage of total NEP for each class for the last 30 months calculated in column 2:

Investment revenue in the form of dividends (55.6%), interest (43.9%) and rent (0.5%) was at $116.2 m. After adjusting for the 18-month effect, the 12-month figure would be around $77.5 m (assuming the flow of revenue is steady throughout the year), which is lower than the $81.2 m revenue in 1997. The NMV of Investments rose over the 18 months by $63.2 m.

HIH* LR�99� LR 9�/99 Change

Fire/ISR 34.35% 42.62% 24.08%

HH 40.00% 42.86% 7.15%

CTP N/A N/A N/A

CMV 105.70% 112.57% 6.50%

DMV N/A N/A N/A

Marine 63.97% 82.07% 28.29%

PI 100.57% 93.98% -6.55%

Liability 121.74% 214.10% 75.87%

WC 128.13% 74.64% -41.75%

Travel 93.68% 82.18% -12.28%

Accident 47.55% 74.95% 57.62%

Other 87.81% 29.14% -66.81%

IT 304.40% >1000% N/A

Total 93.51% 103.54% 10.73%

* Inside Australia only

HIH Case Study on Prov�s�on�ng (Round 2)

�3

Overall the company made an operating loss of $30.614 m, which is significantly worse than the operating profit of $53 m made in 1997 and $72.6 m made in 1996.

Premiums

Total premiums for the 18-month period were $1.1 billion in total and $0.8bn inside Australia. Total Outwards R/I Premiums were very substantial at $511 m in total and $382 m inside Australia. Premium Revenue was at $1.08 billion in total and $786 m inside Australia.

Premium Income figures are at $58 m in total and $172 m inside Australia. These appear very small and this is due to the very large R/I premium paid by HIH. The Premium Income figure is an annual figure and is net of Reinsurance premium paid. Thus the unusual size of the figure reported this period. With regards to the required solvency margin, the 15% of OCP test appears sufficient.

Reinsurance

All the companies in the HIH Group (including this one) have Highest Risk Retention (HRR) at $5 m and Maximum Event Retention (MER) at $10 m. The HRR to adjusted NTA ratio is at 1.77% (in total) and the MER is covered 16.97 times by the solvency surplus (in total).

HIH has large acceptance limits in most classes (mostly due to the large amount of corporate business it writes). Some examples are ISR (Large commercial property cover) at $240 m, Public Liability at $100 m, PI at $25 m and construction at $120 m.

Net Prem�um Revenue ($’000) �99� % �99�/�999

Adj. �99�/�999* %

ISR 20,885 5.6% 46,538 31,025 9.7%

HH 5 0.0% 7 5 0.0%

CTP 0 0.0% 0 0 0.0%

CMV 27,077 7.3% 19,656 13,104 4.1%

DMV 0 0.0% 0 0 0.0%

Marine/Aviation 68,318 18.4% 128,976 85,984 26.9%

PI 87,219 23.5% 124,810 83,207 26.0%

Public Liability 73,286 19.7% 46,214 30,809 9.6%

WC 29.790 8.0% 31,790 21,193 6.6%

Travel 29,623 8.0% 50,654 33,769 10.5%

Other Accident 18,341 4.9% 15,597 10,398 3.2%

Other 9,464 2.5% 15,571 10,381 3.2%

Inward Treaty 7,623 2.1% 523 349 0.1%

Total 371,631 100.0% 480,336 320,224 100.0%

*Adjusted by multiplying times 2/3 in order to have an estimate of the 12 month figure.

Insurance Superv�s�on Core Curr�culum

��

The catastrophe cover arranged is $550 m and appears adequate considering the largest exposure for HIH is in Brisbane at $665.7 m and Sydney at $1.36 billion. This catas-trophe cover is for the whole group (the largest exposure of the group is to Brisbane at $7.8 billion at 5% probable maximum loss (i.e. $390 m exposure)). The cover purchased appears adequate.

In addition to the above, HIH (the group) has entered into a “smoothing arrange-ment” with Swiss Re. It is a multi-term (5 years), multi-class agreement, under which Swiss Re will cover losses above 70% (for the first 2 years), and above 71% (for the remaining 3 years). The premium for this cover is equal to 5% of NEP (equivalent to 5% in terms of loss ratio). This means that HIH has cover above 75%. The maximum limit of the cover in any one-year is 25% (i.e. to 95% loss ratio) and $1 billion over the 5 year period. This cover is taken in addition to the existing reinsurance program, which cannot be changed under the terms of the “smoothing arrangement”.

This “smoothing arrangement” should provide HIH with more stable earning over the next five years, which is very important from APRA’s perspective. Mr. Ray Gosling (Reinsurance Manager in HIH) has confirmed that the agreement with Swiss Re is al-most finalized and that APRA will receive a copy of the agreement in the near future. Mr. Gosling wants to organize another meeting with APRA to discuss any issues that might arise as a result of the review of the agreement.

Annual to Quarterly Comparisons

There are large discrepancies between the annual and quarterly return. It is important to keep in mind that the annual return is audited and thus more likely to be correct. Overall the assets on the quarterly return are $63.2 m smaller than on the annual return and liabilities are $108.3 m smaller.

Issues

Profitability is a large issue with large losses recorded by FAI and HIH ($155 m and $80 m loss respectively). Out of the three main companies, only CIC Insurance managed to record a positive operating result ($18 m). This is quite small compared to the large losses reported by HIH and FAI (-14.3% and -46.3% return on net assets). The net asset figure here is as at 30 June 1999 (end of period rather than beginning of period).

The profitability should return to the company in this financial for three reasons. The insurance premium rates are said to be rising. This has been reported by a number of sources (other companies, media and stockbrokers). Cost savings from the merger with FAI should begin to be fully realized in this financial year. Thirdly the “smoothing arrangement” with Swiss Re should make the results more stable over the next five years. Hopefully there will be no need for further increase in provisioning due to the

HIH Case Study on Prov�s�on�ng (Round 2)

��

Goods and Services Tax (introduced in Australia from 1/7/2000) and no more large extraordinary losses due to the sale of non-core assets inherited with FAI.

Recommendation

HIH complies with all the requirements and appears adequately solvent. No action is recommended and category low is appropriate.

Insurance Superv�s�on Core Curr�culum

��

Appendix—Tables

HIH Case Study on Prov�s�on�ng (Round 2)

��

Insurance Superv�s�on Core Curr�culum

��

HIH Case Study on Prov�s�on�ng (Round 2)

�9

Attachment 3

Note for File APRA

Ref: Anonymous Document entitled “HIH Due Diligence”2

24 March 2000

We have received a report entitled “HIH Insurance Due Diligence” from an ex-em-ployee of HIH criticizing the company’s approach in a number of areas such as provi-sioning, accounting policies, reinsurance arrangements, management skills and capital sufficiency. The employee is an accountant and was employed by HIH in their internal accounting group. We understand that he was of about middle level of seniority. He came to APRA after first going to the Insurance Council and being turned away.

Although the report has been sent to APRA as an anonymous document, the au-thor of the report had previously met with the analysts responsible for HIH to discuss his concerns. The report is in response to the analyst’s request for the concerns to be put into writing.

I have only included relevant sections of the document covering claims reserving practices and some other relevant aspects, including solvency.

HIH Insurance Due Diligence

In Australia, we have seen the consequences of failure of the buyer to undertake a com-plete due diligence process. Both AMP on GIO and HIH on FAI are classic cases of the buyer being caught unawares with severe consequences to share prices. More recently, there is now the case of HIH supposedly refusing two potential suitors the opportunity to undertake a full due diligence. In the cases of GIO and FAI, hindsight has shown that the acquisitions would probably not have proceeded if a full due diligence was under-taken or, at least, not at the price paid.

In the case of HIH, they have apparently denied other parties the opportunity of performing a due diligence. If one were to do a due diligence on HIH then what would be the main areas of review in order to ensure that the fair value of the net assets of the company could be ascertained with a greater degree of certainty? The following provides a discussion on the possible exposures, which exist or are likely to exist in an organization such as HIH, and addresses the due diligence process that may be applied in order to arrive at a possible range for a fair net asset value.

HIH is quite a diverse organization having been the result of mergers of CE Heath and CIC in 1995, CMG in 1996, and FAI in 1998. Both CIC and FAI had histories, also involving mergers, going back many decades. HIH also has a wide geographical pres-

2. It should be noted that, in real time, this report was not received until several months after the date of this round.

Insurance Superv�s�on Core Curr�culum

20

ence through the Americas, UK, and Asia. The areas requiring special consideration in a due diligence on HIH would include the following:

• Claims provisioning• Asset valuations• Accounting policies• Portfolio profitability and likely developments• Run-off exposures• Reinsurance arrangements—normal and one-off• Management stills and incentives• Capital sufficiency

It is only after having considered each of these matters that an informed view would be able to be taken on the fair value of the net assets of the HIH Group.

• Claims Provisioning Practices• The issues here would include:• Level of prudential margins• Run-off exposures• Technical adjustments• Actuarial valuations

It is generally accepted that most insurance companies should set claims provisions at a central estimate level and then hold a prudential margin on top of that to achieve a greater degree of confidence that the provisions are adequately stated. The adding of a prudential margin is considered particularly necessary in the case of long-tail port-folios. Most insurers would carry a prudential margin of in excess of 10% with some carrying up to 25%.

In the case of HIH, its net claims provisions total $2,561 m at December 1999.

Of this amount it is estimated that, given its portfolio mix, long-tail provisions would constitute around 85% of these provisions. A prudential margin of 10% would add a further $256 m to net provisions at December 1999.

The HIH position is possibly worsened with its constant difficulty in generating reasonable profits. This is not conducive to setting conservative provisions even at a central estimate level so it would be necessary to closely review the adequacy of the central estimate base. Ascertaining the external auditor’s and actuary’s view of the ad-

$m

Gross 4,065

Reinsurance 1,504

Net 2,561

HIH Case Study on Prov�s�on�ng (Round 2)

2�

equacy of provisions would be an essential phase of the due diligence process. If a low-end central estimate outcome were used, then greater concern would obviously exist.

A conservative increase for a prudential margin would, therefore, be $260 m (10%) and possibly as much as $390 m (15%).

The Group has inherited from both FAI and CIC a range of historical liability expo-sures from old group companies in those organizations. These would range from CIC’s asbestosis cover through CSR and US inward reinsurance liability business from FAI. On top of these, there is still a possibility of exposure to the Heath inward reinsurance liability business written in the US and UK. It would be necessary to quantify the extent of these exposures and what action, if any, has been taken to contain them. ACE, who as CIGNA was lead on the CSR account, are still seeing development of CSR asbestosis claims. Carlingford (part of CIC group) also participated on CSR. With the passing of time the collectibility of reinsurance increases the potential for a greater net exposure. Exposure to latent claims and uncollectible reinsurance needs to be closely examined. On those inward reinsurance exposures which have already been settled it would be necessary to review the terms of those settlements to ensure that none of the settlement cost is in the form of delayed payments, the expense for which will not be booked until a future period. On the remaining inward reinsurance liability exposures close care would need to be taken to undertake a full review of any potential exposures. Exposures on this inward reinsurance business could be in the range of $50 m to $100 m given the GIO and Reac scenarios.

The level of discounting of HIH provisions at December 1999 was at 6.8% which is at the high end of the range. Inflation at 5.7% is at the low end after allowing for the level of superimposed and economic inflation expected of a long tail dominated claims liabilities. A small decrease in discount and a small increase in inflation generating a 0.5% decrease in the real rate of return would add $35 m to net claims provisions. The basis of claims provision discounting, therefore, would need to be closely examined.

The asset/liability matching is an issue as the claims liabilities are not fully matched by fixed interest investments. It is necessary to bring into the matching process riskier assets such as equities and property. Cash and fixed interest investments at December 1999 totaled $1867 m and represented only 73% of net provisions. No risk adjustment would appear to have been made for the risk adjusted rate or return on equities and property investments, which are used to balance the match of liabilities and invest-ments. A 0.5% decrease in discounting to adjust for risk would add another $35 m to claims provisions. Again, a close examination of discount rates from this perspective would also be necessary.

HIH has indicated that it has put in place one-off reinsurance arrangements to protect the total provisions. The method of discounting recoveries on reinsurance con-tracts would need to be examined to ascertain if any exposure arose from the method of discount applied to aggregate stop-loss reinsurance recoveries. Exposure could be up to $10 m if inappropriate discounting methods have been applied to reinsurance recoveries.

Insurance Superv�s�on Core Curr�culum

22

The basis of determination of future claims handling provisions needs to be ascer-tained. If a run-off cost basis as opposed to the more correct ongoing operation method has been used, claims provisions could be artificially decreased. A 1% increase in FCHC (applied to gross discounted provisions) would add $40 m to claims provisions.

The HIH actuary, David Slee, has been associated with HIH over twenty years. With HIH being one of his main clients, the issue of total independence is a concern. Such a concern is exacerbated with the use of one-off reinsurance contracts, run-off exposures, and absence of prudential margins. As well, the long standing association with Arthur Andersen and the make up of the Audit Committee further the total inde-pendence concern scenario as recently expressed in the financial press.

Asset Valuation Practices

There are several asset categories in the HIH balance sheet that would require close examination in a due diligence. They include:

• Intangibles• Other assets• Fixed assets• Properties• Deferred acquisition costs

By far the major asset valuation exposure is that of goodwill. The goodwill is dom-inated by the FAI acquisition although the level of goodwill held for HIH America should also be examined given recent problems in this area.

In the six months to June 1999 the level of HIH’s goodwill increased by $312.5 m predominantly due to the acquisition of FAI ($275 m). The FAI goodwill would have been arrived at after taking account of such items including:

• Overvaluation of the FAI investment assets• Reinsurance exposures• Undervaluation on claims reserves• Underwriting results 30 June 1998 to 31 December 1998• Integration costs

These adverse net asset adjustments could have been offset by a future income tax benefit on them and the partial recognition of unbooked tax losses. The goodwill would have been even higher if the loss on Oceanic Coal was not reported as an abnormal item.

HIH Case Study on Prov�s�on�ng (Round 2)

23

The accounting for goodwill needs to be closely examined to ensure that firstly its method of determination is understood and the appropriateness of that method con-sidered.

The $275 m goodwill on FAI is being amortized over a period of twenty years. Given the underlying profitability and size of this business then its value is extremely doubtful. The initial market expectation of the goodwill on the acquisition was less than $100 m. At $275 m it is clearly overvalued. A reduction in net assets of $225 m would be not unrealistic.

The other goodwill built up in the year to June 1999 needs to be understood. If it related to HIH America then the value of this adjustment is particularly questionable given the profitability of this market even with rate increases. Under-provisioning in HIH America at the date of acquisition could have been partially offset by the booking of discount on provisions as the US does not discount provisions under US GAAP. The practice of providing for policyholder dividends in the US workers compensation market and the extent to which future exposures have been provisioned needs to be un-derstood. The end result could well be an abnormally high level of goodwill and an un-derstated policyholder dividend liability. Reinsurance arrangements for HIH America need to be examined with a view to ascertaining if an exposure also exists as regards future reinsurance contracts. Overall net tangible assets could need to be decreased by up to $20 m. Any goodwill reduction would be in addition to this.

Other assets consist of:

• Future income tax benefits—timing differences• Future income tax benefits—tax losses• Investments in associated companies• Prepayments and deferred expenses

The value of future income tax benefits in the Group at $150 m plus is question-able. Tax paid by the Group in the period 1 January 1997 to 31 December 1999 (3 years) has totaled $16.8 m. Given the level of under-provisioning and low profitability, it will be several years before any benefit can be gained from this asset (if ever). The one-off reinsurance contracts may assist in utilizing the losses to a certain degree but under-provisioning could well offset this benefit. There remains an exposure to the Group if the tax office were to view any one-off reinsurance contract as financial reinsurance as discussed in Ruling TR 96/2. If this were to be the case then there is a possible dividend imputation exposure.

The possible exposure on FITB could be up to $100 m.Investments in associates are dominated by Home Security International, Nam

Seng, a listed Thailand motor insurer, and a UK property holding. Valuation methods/basis of these investments are not disclosed. However, consistent with claims provi-sioning, it is possible that they would not be conservative. A due diligence process

Insurance Superv�s�on Core Curr�culum

2�

would closely consider these valuations and independent advice would certainly need to be taken.

The possible exposure on investments in associates could be up to $25 m.Prepayments and deferred expenses need to be examined for the deferral of com-

puter development expenditure, in particular, IS2. The future viability of this system would need to be closely considered given its development problems. The deferral or capitalization of IS2 expenditure would need to be considered given QBE’s rejection of this insurance system. The possible exposure on prepayments and deferred expenses could be up to $15 m. This decrease could be offset by a potential surplus, which ex-ists in the superannuation fund of $20 m, that is, if the benefit has not already been booked.

Fixed assets are comprised of leasehold improvements and computer and office equipment. The value of IS2 related items, again, needs to be closely considered.

The possible exposure on fixed assets could be up to $30 m.The valuation of the HIH property portfolio is subject to one’s view on the value of

St Moritz and the reliability of the valuations on the other property holdings. Properties have been valued at directors’ valuation having regard to the valuations carried out by registered valuers. If the same aggressive approach to claims reserving is taken to prop-erty valuations then close attention to the valuation of these assets would be required. A due diligence process would closely consider these valuations and independent advice would certainly need to be taken.

The possible exposure on property investments could be up to $25 m.Deferred acquisition costs comprise deferred commission and deferred under-

writing costs. The level of deferral of underwriting expenses is at the high end of rea-sonableness at 27.9% of unearned premiums. Given the net commission ratio is 10% and the total expense ratio is 14.7% then a deferral at 27.9% raises questions as to the overstatement of this asset. Assuming even 75% of underwriting expenses are defer-rable then the ratio to unearned premium should be around 21%. The due diligence process would need to closely examine the basis for the calculation of deferred indirect acquisition costs.

A conservative reduction of deferred expenses would be, therefore, around $70 m. This may be potentially overstated as net earned premium is artificially low due to the impact of smoothing reinsurance contracts.

Accounting PoliciesThe accounting approach to several areas would require close attention including

those covering:

• One-off reinsurance contracts• Goodwill amortization• Deferred expenses• Net discount rate adjustment• Superannuation surplus

HIH Case Study on Prov�s�on�ng (Round 2)

2�

• Reclassification of items within the profit and loss• Cash flow statement

The method of accounting for one-off reinsurance contracts as applied by FAI and HIH from June 1998 requires close review. It would be necessary to examine for the possibility of a reinsurance smoothing transaction being interpreted as a transfer of risk. All documentation relating to the one-off reinsurance transactions would need to be reviewed so as to understand their impact on the reported results for each of the reporting periods from June 1998.

Concern in this area arises from the extent of the loss on the reinsurance account for the recent reporting periods. For example, the HIH loss ratio on reinsurance for the six months to December 1999 was 125% compared with the gross loss ratio of 90%. The June 1998 FAI accounts depict a similar scenario.

Goodwill arising from the FAI acquisition is being amortized over a period of 20 years. Clearly both the period and quantum are questionable. The fading FAI di-rect market presence (advertising cut back significantly), potential deregulation of the Queensland CTP market, a disbanded corporate portfolio, deferral of NSW workers privatization and departure of the entire FAI executive and senior management tem significantly reduces the value in the name or business of FAI.

The expense deferral policy as regards underwriting expenses appears to take into account a higher than normal proportion of management costs, which is possibly stretching the definition of indirect acquisition costs to the limit. Again, the accounting policy and methodology would need to be closely examined for appropriateness.

Lloyd’s business profitability is usually recognized at the end of three years at the time the underwriting year is closed. The HIH method of accounting would need to be examined to ensure that is understood and considered for appropriateness. The treat-ment of discount on reinsurance to close would also need to be examined.

The net discount rate adjustment is a unique reporting line to HIH. It unclear defi-nition possibly enables adjustments to be made above or below the underwriting line to boost the underwriting result. The basis of calculation of this item in the P&L over recent years needs to be reviewed to consider its appropriateness.

The accounting treatment of the surplus in the superannuation fund needs to be understood.

In an environment of a wide range of one-off adjustments the quantum of the ben-efits of those adjustments needs to be examined in order to ascertain the real trend of the underlying results.

The cash flow statement is one of the truer indicators of the financial direction of HIH. A negative underwriting cash flow is now evident. As with accounting profit it is important to review basis of compilation of the cash flow statement. In particular, the treatment of payments under one-off reinsurance contracts would need to be closely examined to ensure that the correct cash flows are reflected in the statement.

Insurance Superv�s�on Core Curr�culum

2�

At June 1999 an abnormal item of $50 m was booked with respect to the estimated impact of the GST legislation on pre 30 June 2000 claims. The determination of this adjustment and subsequent appraisal thereof needs to be considered. In particular, it would be necessary to consider how any increase or decrease in this adjustment has been reflected through the P&L in subsequent periods.

Annual and quarterly reports to APRA returns need to be examined particularly in regard to the treatment of one-off transactions and the allocation of reinsurance and expense costs between the licensed Australian insurers and other companies in the Group.

The accounting treatment of major disputes/transactions that the Group has en-countered in recent years would need to be closely examined. There would include:

• US inward liability reinsurance• Charman inward reinsurance• FAI Life• One-Tel• St Moritz• OCAL

It is noted that Arthur Andersen were the signing auditors on the FAI June 1998 accounts and are the auditors of HIH. Obviously, they have been able to be comfortable with the accounting policies adopted by both FAI and HIH over recent years. Given the range and complexity of possible areas of concern then their rationale for agreeing to the treatment of these items would need to be closely considered in the due diligence process.

Capital Sufficiency

Australian insurance regulators currently apply several solvency tests to insurance com-panies. The ratio of net assets to net outstanding claims must be greater than 15% and the ratio of net assets to net written premium must be greater than 20%.

Net tangible assets in the case of HIH excluded goodwill ($330 m) but include sub-ordinated bond debt ($160 m). At December 1999 the net tangible assets of HIH were thus determined as follows:

HIH Case Study on Prov�s�on�ng (Round 2)

2�

The above indicates if the net tangible assets of HIH were to be decreased by more than $400 m then the Group would be below the current solvency requirements of APRA.

The possible adjustments to net tangible assets outlined herein are summarized as follows:

The bottom line is certainly uncomfortable. The impact of the potential net tangible asset adjustments outlined herein adds to between $750 m and $1,100 m. Obviously a full due diligence would be necessary to achieve a firmer view. Even if the best outcome is discounted 50% severe solvency concerns would still exist.

$m

Reported net assets 962

Less goodwill (330)

Add subordinated debt 160

Net tangible assets 792

Net outstanding claims 2,561

Claims solvency ratio 31%

Solvency margin (claims) 408

Net written premium 1,885

NWP solvency 42%

Solvency margin (premium) 415

Best$m

Worst$m

Claims provisions prudential margin

260 390

Claims historical exposures 50 100

Discounting 35 50

Asset risk adjustment 35 50

Reinsurance discounting 10 10

Claims handling 40 40

FITB 100 150

Investments in Associates 20 20

Deferred expenses 15 15

Fixed assets 30 50

Property valuations 25 25

Deferred acquisition costs 70 100

Reinsurance profit smoothing 40 80

Employment contracts 20 20

Total potential adjustments 750 1,100

Insurance Superv�s�on Core Curr�culum

2�

Conclusion

The extent of issues which need to be addressed in the due diligence process on a gen-eral insurer clearly indicates that it is a complex process. The potential range of out-comes is quite frightening as has been evidenced by GIO and to a lesser degree FAI. In the case of HIH similar scenarios could also exist. Unless an appropriate due diligence is undertaken on HIH by a potential bidder then clearly they are taking a major risk of over paying by a significant amount.

The problem for HIH is how to overcome present market perceptions of its finan-cial strength. Certainly allowing a due diligence to be undertaken would calm market concerns.

The issues raised in this due diligence document have broader implications for a number of parties other than investors including:

• APRA• Rating agencies• Auditors on general insurers• Actuaries of insurers• Financial analysts

It is essential for the stability of the general insurance industry and for shareholders and policyholders that these parties are able to properly interpret the financial posi-tion of the insurers. Confidence in these parties being able to achieve this is somewhat doubtful.

Anonymous

HIH Case Study on Prov�s�on�ng (Round 2)

29

Attachment 4

Memorandum for General Manager

Notes on Interview with David Slee —- Consulting Actuary to HIH Insurance

20 April 2000

The following notes summarize a meeting we held with David Slee, consulting actuary to HIH, in following up the anonymous “HIH Due Diligence” report. The note includes a brief background to his relationship with HIH and the way that his actuarial review of their OCP was conducted. It then raises a number of issues. A copy of Slee’s full Actu-arial Report for June 1999 is attached in the Appendix to this note.

1. Background

DaviD Slee anD hiS relationShip with hih

Slee is, and has been since 1967, a Fellow of both the Institute of Actuaries of Australia and the Institute of Actuaries (United Kingdom). He has approximately 40 years ex-perience in the insurance industry, both as a consulting actuary and as a director or manager of a number of insurance companies.

In 1989 Slee incorporated his actuarial practice and since that time has performed all his work through, and as the consulting actuary of, Slee Consulting. Slee was a long-term acquaintance of CE Heath’s CEO, Ray Williams, having provided both manage-rial and actuarial services to various insurance companies associated with Williams. For the 6 years in the early 1980s, prior to establishing his own practice, Slee had been an employee of Heath. At the time of incorporation, CE Heath Casualty and General Insurance Limited initially took a 49 per cent shareholding in the company, with Slee taking the remaining 51 per cent.

In 1992 he suggested to Williams that, because by that time Slee Consulting was carrying out a reasonable (and increasing) quantity of work for CE Heath, they should dissolve the relationship between the two companies so that they would not only be independent, but also be seen to be independent. Slee purchased CE Heath’s interest in the business.

Slee Consulting had clients other than CE Heath. During the period 1989 to 1995, Slee estimates that the work he performed for CE Heath accounted for about 20 per cent of his work. From about 1996 onwards HIH took up a growing proportion of Slee’s time. Slee estimated that during the year ending 30 June 1998 somewhere between 50 per cent and 80 per cent of Slee Consulting’s revenue was derived from HIH. In 1998

Insurance Superv�s�on Core Curr�culum

30

Slee was appointed consulting actuary for the entire HIH group and the percentage of revenue derived from HIH work has continued to grow.

In addition to his work on HIH outstanding claims liabilities (see below), Slee has, from time to time, been asked to provide advice and assistance in relation to a number of other discrete matters. He provides HIH with some limited actuarial assistance and advice in relation to pricing and premium levels in particular portfolios. He also as-sisted HIH in relation to various acquisitions and mergers (including CIC and CMG). In relation to reinsurance, he did some work on retention levels in 1994 and 1997. Slee also participated in several training programs for HIH staff to explain the actuarial pro-cess and the general method of operation of an insurance organization.

Up to December 1996, Slee’s instructions had been to assess the value of the specific classes of business identified in the terms of reference of his reports. In January 1998, Williams raised with Slee the possibility that he be instructed to prepare valuations for the purpose of ‘testing provisions on a global basis’. In discussing the terms of reference for the appointment Slee was told by CFO Dominic Fodera that he was not to include a prudential margin in his valuations, as this would be determined by the directors on a global basis.

Slee explained that the terms of reference for his valuations are agreed orally (usu-ally with Fodera) and then set out in his reports. There are no lengthy discussions on this topic. He understands, and believes the HIH executive directors understand, that his task is to test the aggregate of the net discounted claims provision which the com-pany proposes to book.

Slee emphasized that his task is to arrive at a central estimate (an estimate that has a 50% probability of adequacy) of HIH’s group or global OCL. He sees his task as being to determine an unbiased central estimate which can be compared with the proposed booked value.

Slee said that he understands his instructions to be to test the aggregate or global booked value, and not that of any of the individual companies or divisions. He also em-phasized the fact that his instructions were merely to test the booked provision, and not to make any recommendation as to the reserve or provision which ought to be booked. He regards the latter as a separate task.

the proviSion Setting proceSS at hih

The provision setting process within HIH differed in some respects from portfolio to portfolio. Essentially, however, the process appears to be as follows.

David Slee is retained to provide his assessment of the central estimate of the HIH group’s OCL. He does so through semi-annual reports. Slee’s total figure for each bal-ance date is intended to be a figure against which the reasonableness or adequacy of the total booked figure or provision proposed for HIH’s consolidated accounts can be

HIH Case Study on Prov�s�on�ng (Round 2)

3�

tested. As Slee’s total figure is a central estimate (in accordance with his instructions) it includes no prudential margin.

For each balance date, senior management put forward their estimate of the OCL for each division. Every six months there is a meeting at which both the management and actuarial estimates of each division’s OCL are discussed and considered. Those in attendance at the meetings vary over time, and from division to division, but the meet-ings always include Dominic Fodera, Terry Cassidy and David Slee. Following these meetings, senior management, led by Fodera, settle on a central estimate figure for each portfolio of business. The total of these figures is the figure that HIH books as its group OCP at the relevant balance date. It is argued to represent management’s assessment of the central estimate of the group’s OCL.

My impression from our discussion with Slee is that the consideration given to the adequacy of HIH’s proposed OCP at the various committee meetings is generally brief and seldom descends to particularity. From time to time there is some discussion of the discrepancies between the HIH, and actuary figures. However, given the corre-spondence between the total group HIH and actuary figures, the provisions proposed by management are usually the figures approved by the board.

inStructionS anD aSSumptionS in the Slee reportS

In addition to the overall instruction to test the proposed booked provision, Slee is in-structed to make a number of assumptions in preparing his valuations. The instructions or assumptions are disclosed in a relatively consistent manner in each of Slee’s reports. For example, in the 30 June 1999 report, under the heading ‘Terms of Reference’, after referring to his instruction to test the booked value of the proposed provision in the balance sheet of the Holding Company for all outstanding claims including claims in-curred but not reported (IBNR), and future claims handing costs (FCHC) as at 30 June 1999, Slee set out the following ‘conditions which were determined by the company:

• the rate of discount to be used is 6.42 per cent per annum;• the allowance for FCHC is generally to be 2 per cent of gross liabilities;• all reinsurance is to be considered fully recoverable;• where it is inappropriate to use actuarial methods, to use case estimates (par-

ticularly where there are individual items subject to law suits and in some short-term business);

• no prudential margin is to be included, nor should any allowance be made for mismatch of assets to liabilities;

• the portfolio is worldwide and in the time frame available other actuaries’ re-ports may be used to assist in the testing process; and

• the report should be as simple as possible, so that the essential features are easily understood.

Insurance Superv�s�on Core Curr�culum

32

Broadly equivalent instructions and assumptions are disclosed in each of the Slee reports.

The appropriateness and effect of a number of these individual instructions and assumptions are considered below. But, there are some matters of relevance to them all. For example, PS 300 (actuarial standard) relevantly provides:

• the actuary’s report should state the extent of compliance with this standard, the reasons for not complying fully with this standard, and any restrictions on the actuary;

• where the principal requires the actuary to use specific assumptions the actuary must clearly state the circumstances, discuss whether or not the assumptions are reasonable and consistent with this standard, and discuss the implications of divergence from this standard; and

• the actuary should not recommend or support a provision which is less than the central estimate of the liabilities.

In short, if an actuary is constrained in a way which leads to the valuation result being less than the central estimate of the liabilities, the actuary must clearly disclose that the result is less than the central estimate of the liabilities, and preferably quantify the shortfall.

Since Slee does not suggest anywhere in his reports that his valuations of the OCL were less than a central estimate,2 a reader of Slee’s reports would understand them to contain his central estimate of HIH’s OCL, notwithstanding the assumptions or con-straints imposed by the company.

When asked who his reports are circulated to Slee said that he assumed that his reports would be considered by all the directors, senior executives and possibly also APRA (in fact we have never before seen any of his reports). While he addresses his reports to the directors of HIH, he has had no contact with the board or directors of HIH (other than Williams, Cassidy and Fodera). He has received no requests for infor-mation, clarification or explanation from any of the directors.

2. Concerns Arising from our Review of Slee’s Actuarial Work

There were a number of matters raised during the course of our meeting with David Slee which are relevant to an assessment of the adequacy of HIH’s provisions across a number of portfolios, and in some cases, across all portfolios. These include the treat-ment of future claims handling costs, discounting, the use of prudential margins, the allowance for claims inflation, and the accuracy and flow of provisioning information.

2. On the contrary, in his June 1998 report Slee states: “I understand that this figure is to be booked in the balance sheet, and it represents [a] liability which has [a] 50% probability of being adequate.”

HIH Case Study on Prov�s�on�ng (Round 2)

33

Future claimS hanDling coStS

Both AASB 1023 and PS 300 are clear in their requirement that appropriate allowance be made for future claims handling costs (FCHC) in the estimate of a general insurer’s OCL. Since the allowance is intended to reflect the claims handling costs which the insurer expects to incur, there is a reasonable presumption that the allowance should be determined by reference to the insurer’s actual claims handling costs.

In his 31 December 1996 report, Slee provided for FCHC at differing rates across the various Australian portfolios. The rates varied between 2 per cent and 7 per cent, giving an approximate weighted average of just over 4 per cent. But in each of his subse-quent reports, Slee provided for FCHC at the lower and fixed rate of 2 per cent of gross liabilities across HIH’s entire global portfolio of liabilities. His reports made it clear that he was instructed to provide for FCHC at this rate.

We asked Slee whether he was provided with any statistics or analysis which would have enabled him to assess the actual costs of claims handling. He said he was informed that none were available.

While there may be occasions where lower allowances may be appropriate our ex-perience is that a range of 4 per cent to 8 per cent of expected future gross payments is a reasonable “benchmark” allowance for FCHC for the Australian general insurance industry. Given the size of HIH, it seems to me unlikely that there could be any claims handling practices or other factors which would enable HIH to reduce its claims han-dling costs below the standard industry range.

DiScounting

The relevant professional standards in Australia (AASB 1023 and PS 300) provide for the discounting of a general insurer’s OCL using a market-determined risk-adjusted rate of return appropriate to the insurer. This allows a departure from the risk-free rate of return where the insurer’s assets can reliably be expected to give rise to higher rate of return.

The discount rates adopted by Slee, upon instructions from HIH, have been con-sistently higher than the yields available on Commonwealth Government bonds with a three year maturity (three years being roughly representative of the mean term of HIH’s OCL). At the same time, Slee has made no allowance for HIH’s exposure to the risk arising from the mismatch in the term of HIH’s assets and liabilities. Again, this was upon instructions from HIH. His reports do, of course, make these instructions clear.

A particular concern arises in relation to the discounting of HIH’s OCL as at 31 December 1997. Note 19 to HIH’s consolidated accounts for the year ending 31 De-cember 1997 referred to HIH’s OCP as at 31 December 1997 as discounted at a rate of 6.2 per cent over an “average weighted term to settlement” for the outstanding claims liabilities of 2.7 years.

Insurance Superv�s�on Core Curr�culum

3�

Slee mentioned that he had written to HIH in April 1998 disclaiming any respon-sibility for the contents of this note on the basis both that it contained a mathematical error, and that on the figures given to him it would be difficult to justify a discount rate of 6.2 per cent. He said that his calculations had been done on the basis of a rate of 6 per cent, which was the rate which management had agreed was the actual rate being earned on the company’s assets.

However Slee did not subsequently discuss the matter with anyone from manage-ment or the auditors. Nor did he refer to the matter in his report. His reason for not including the matter in his report was that he believed the problem lay in the peculiar manner in which HIH had derived the undiscounted figure, and that his only task was to test the net discounted provision. The difference in the OCP arising from the math-ematical error and the extra .2 per cent on the discount rate is around $62 million on a total OCP of around $1.5 billion.

pruDential marginS

In its 31 December 1997 accounts, and subsequently, HIH adopted a policy of not in-cluding a general prudential margin in its OCP. In line with this policy, Slee was in-structed not to include any prudential margin in his valuations as at 31 December 1997 and subsequently.

Slee argued that he has provided valuations which he was prepared to put forward as central estimates as at the various balance dates. At the same time he made it clear in each of his reports that his valuations were heavily underpinned by the instructions he had been given, and hence assumptions he had made. Slee warned in his reports of the need for, and desirability of, a prudential margin in the face of risks such as those involved with the choice of discount rate, the rate of FCHC and other risks.

It is unfortunate that the Insurance Act 1973 does not mandate a prudential margin in provisioning—this is an area that we are addressing in our current reform of the law. AASB1023 allows a prudential margin and PS300 generally encourages one. More im-portantly, the industry practice is to include a margin, especially for long-tailed busi-ness.

In my view, in the absence of a more detailed appreciation of the risks inherent in the various assumptions made by Slee and his valuations more generally, best practice suggests that the directors of HIH should have resolved to include a prudential margin within their OCP.

claimS inFlation

Both AASB 1023 and PS 300 require that the estimate of an insurer’s OCL include an appropriate allowance for claims inflation. This includes both economic (that is, price

HIH Case Study on Prov�s�on�ng (Round 2)

3�

or wage) inflation and superimposed inflation for inflation of claims settlements in par-ticular portfolios.

In his reports, Slee has not always distinguished between economic inflation on the one hand, and superimposed inflation on the other. This makes it difficult to determine from the face of those reports the extent to which allowance was made for superim-posed inflation in respect of the individual portfolios.

Slee’s combined inflation allowance for the HIH C&G Liability, FAI Corporate, and FAI Professional Liability portfolios in 1997 and 1998 was 4.0%. For HIH C&G Professional Indemnity it was 3.5% and for Australian Workers Compensation it was 8.0%. This was at a time when general price inflation (CPI) was in the order of 3.5%. Our own internal actuary thinks that, for these portfolios, somewhere between 4 and 5 percentage points should be added to CPI.

accuracy anD Flow oF proviSioning inFormation

Assessment of a general insurance company’s OCL is, even in ideal circumstances, an inexact science. It is a truism that the accuracy of the assessment of the OCL depends upon the adequacy and accuracy of the data upon which it is based. In my view, it ap-pears highly likely that inadequate controls and procedures exist within HIH to ensure that accurate and complete information and data are available and communicated to the appropriate people (and in particular, to Slee).

Senior Manager

Insurance Superv�s�on Core Curr�culum

3�

Appendix—Copy of David Slee’s HIH Actuarial Report for June 1999

HIH Case Study on Prov�s�on�ng (Round 2)

3�

Executive Summary

The calculated discounted reserves net of all reinsurance expressed in Australian dollars as at 30th June 1999 excluding any prudential margin are as follows:

I understand that this figure is to be booked in the balance sheet, and it represents a liability which has a 50% probability of being adequate.

This represents a 7.05% increase over the reserve at 31st December 1998, largely due to increases in personal injury claims in Australia and USA.

Included in the above figures is A$42,100,000 for USA contractor’s liability rein-sured inwards. This figure is based on legal advice that HIH may be able to avoid certain claims, and that the management of HIH is confident that a settlement can be made for this figure. Such a judgement is not a matter for actuarial analysis and managements’ estimate of the outcome has been accepted. The eventual outcome of this dispute will impact on the results, at the time a settlement is reached.

DiScount

The valuation methods have allowed for all liabilities including short tail to be dis-counted. The rate of discount used for all business has been 6%. The auditors have cer-

Professional Indemnity $346,513,000

General Liability $463,249,000

Workers Compensation $212,895,000

CTP $873,100,000

Marine (excl UK) $81,440,000

Disability $4,942,000

Australian Short Tail $172,000,000

UK $294,522,000

HIH America $126,600,000

Great States $66,700,000

Hawaii $13,700,000

Argentina $11,200,000

Hong Kong $28,400,000

New Zealand $30,070,000

CMG $25,700,000

Charman $30,535,000

AAMI $44,987,000

FAI inwards Re $50,000,000

Miscellaneous $41,744,000

GST AND Y2K $35,400,000

Stop loss on 1998 reserves ($255,014,000)

Total $2,698,683,000

Insurance Superv�s�on Core Curr�culum

3�

tified that assets exist to support the claim provision and are currently earning at least 6%. The company expects to be able to sustain that rate.

I note however that whilst the investments are earning the above rates, they do carry a mis-match risk for which no allowance has been made. The long-term sustain-ability of 6% per annum is a matter of judgement, with which is associated risk.

Future claimS hanDling coStS

Future claims handling costs are included in the figures, at 2% of the claim costs, on the grounds that a third party would bid no more than this amount in a competitive ten-dering process. Whilst this is an acceptable proposition, I add that if the company does not contain its costs to 2%, then the company runs an expense over-run risk.

riSk

Actuarial standards require me to point out the uncertainty in all these calculations. The following risks are an inherent feature of this valuation and give rise to considerable uncertainty when taken in the aggregate:

• Currency conversion risk• Excess superimposed inflation risk• Expense over-run risk• Fluctuation risk• Investment capital risk• Investment income sustainability risk• Judicial interpretation risk• Regulatory interference risk• Reinsurance default risk

Whilst none of these items may in fact manifest as an adverse situation, the prob-ability that a combination of events will provide an adverse situation is not insignifi-cant.

Stop loSS

The company has purchased a stop loss of $400,000,000 excess of loss over the 1998 total reserves. It appears that this will all be used and the present value is deducted from the liability.

HIH Case Study on Prov�s�on�ng (Round 2)

39

Solvency teSt

The suggested reserve for testing solvency would usually have a higher probability of adequacy than 50%.

In that the group has a wide spread of business, I would expect to see shareholders funds of at least $600,000,000 supporting this claim reserve.

Introduction

This report was commissioned by Mr. Terry Cassidy, Director of HIH INSURANCE LTD, (ACN 008 636 575) and is not intended for use by any party other than the direc-tors of that company. The report should be read in its entirety, so that out of context conclusions are not drawn.

The actuary responsible for the report is Mr. David Slee FIA FIAA as principal of David Slee Consulting Pty Ltd, a disinterested party.

No constraints were put upon the actuary, other than as set out in the terms of reference.

The report does not exceed, nor falls short of its stated purpose and complies with actuarial standards in accordance with the terms of reference.

The terms of reference clearly require me to consider solvency as a separate exer-cise from adequacy for balance sheet purposes.

The company determines its own value for balance sheet purposed according to its won understanding of the position, and the actuarial central estimate is regarded as a test of the company’s results. It is highly unlikely that both the company calculated reserve based on case estimates plus allowance for IBNR will be exactly the same as the actuarial value, and indeed some years it should be expected that the actuarial basis will give a higher figure and some years a lower figure than case estimates.

Only when there is a wide discrepancy between the two figures would it be reason-able to reject the company calculated figure, given the uncertainty of all these calcula-tions.

However for purposes of testing the solvency of the company, it is desirable to use a reserve which does contain an allowance for subjective risk, and this is usually referred to as a prudential margin on top of the central estimate.

Terms of Reference

The object of my investigation has been to test the book value of the provision for out-standing insurance claims including IBNR and FCHC as at 30th June 1999.

I have been asked to assume that:

Insurance Superv�s�on Core Curr�culum

�0

1. All reinsurance is fully recoverable. (I have been advised that only 0.4% of re-insurance is with BBB rated companies and the remainder is with A or better. 39.5% is with AAA companies, 4.9% with AA, 46.5% with A rated companies and 8.7% with Lloyds. There is no reinsurance with unrated companies.)

2. The liability for certain USA contractors business and the Charman account be taken at an amount which the company in conjunction with its auditors con-siders to be a reasonable settlement in contested court cases.

3. The rate of discount to be used be 6% per annum.4. The allowance for future claims handling costs be 2% of liabilities

I have also been instructed not to include any prudential margins in my test of the balance sheet value, but to include a reasonable prudential margin in my test of solvency.

Reliance

Of necessity I have had to rely on the Company for the following:

• Underwriters’ estimates of all claims in excess of $1,000,000.• Underwriters’ estimates of outstanding claims for all short tail business. (This

represents only 10% of the liability.)• All data which has been supplies to me. The company’s auditors have advised me