• The objective of HKAS 2 is to prescribe– the accounting treatment for inventories.

• A primary issue in accounting for inventories is– the amount of cost to be recognised as an

asset and carried forward until the relatedrevenues are recognised.

• HKAS 2 provides guidance on– the determination of cost and its subsequent recognition as an expense,

including any write-down to net realisable value.– the cost formulas that are used to assign costs to inventories.

Objective and Scope of HKAS 2

Inventories are assets:a) held for sale in the ordinary course of business;b) in the process of production for such sale; orc) in the form of materials or supplies to be consumed in the production process

or in the rendering of services.

Inventories are assets:a) held for sale in the ordinary course of business;b) in the process of production for such sale; orc) in the form of materials or supplies to be consumed in the production process

• HKAS 2.3(b) states that HKAS 2 does not apply to:– commodity broker-traders who measure their inventories at fair value less

costs to sell. When such inventories are measured at fair value less costs to sell, changes in fair value less costs to sell are recognised in profit or loss in the period of the change.

• HKAS 2.5 clarifies that:– Broker-traders are those who buy or sell commodities for others or on their

own account.– The inventories referred to in HKAS 2.3(b) are principally acquired with the

purpose of selling in the near future and generating a profit from fluctuations in price or broker-traders’ margin.

– When these inventories are measured at fair value less costs to sell, they are excluded from only the measurement requirements of HKAS 2.

• The jewellery company can consider accounting for its golden anddiamond products at fair value less costs to sell and recognising such changes in profit or loss.

• HKAS 2.3(b) states that HKAS 2 does not apply to:– commodity broker-traders who measure their inventories at fair value less

costs to sell. When such inventories are measured at fair value less costs to sell, changes in fair value less costs to sell are recognised in profit or loss in the period of the change.

• HKAS 2.5 clarifies that:– Broker-traders are those who buy or sell commodities for others or on their

own account.– The inventories referred to in HKAS 2.3(b) are principally acquired with the

purpose of selling in the near future and generating a profit from fluctuations in price or broker-traders’ margin.

– When these inventories are measured at fair value less costs to sell, they are excluded from only the measurement requirements of HKAS 2.

• The jewellery company can consider accounting for its golden anddiamond products at fair value less costs to sell and recognising such changes in profit or loss.

• HKAS 2 does not apply to the measurement of inventories held by:a) producers of agricultural and forest products,

agricultural produce after harvest, and minerals and mineral products, to the extent that they are measured at net realisable value in accordance with well-established practices in those industries.When such inventories are measured at net realisable value, changes in that value are recognised in profit or loss in the period of the change.

Objective and Scope of HKAS 2

Producers of agriculture and

minerals

Producers of agriculture and

minerals

Commodity broker-traderCommodity

broker-trader

Using NRV (through P/L)Using NRV

(through P/L)

Using Fair Value (through P/L)

Using Fair Value (through P/L)

b) commodity broker-traders who measure their inventories at fair value less costs to sell. When such inventories are measured at fair value less costs to sell, changes in fair value less costs to sell are recognised in profit or loss in the period of the change.

Specific IdentificationSpecific Specific IdentificationIdentification

• The cost of inventories of items that are not ordinarily interchangeable and goods or services produced and segregated for specific projects– shall be assigned by using specific identification of

their individual costs.• Specific identification of cost means that

– specific costs are attributed to identified items of inventory.

Entity ST has the following accounting policy in its financial statements of 2006:• Inventories are stated at the lower of cost and net

realisable value. • In respect of unsold machines, cost is determined by

apportionment of the total development costs, including finance costs capitalised, attributable to unsold machines.

• In respect of other inventories, cost, comprising purchase cost from suppliers, is determined:• on first-in-first-out basis and• on the weighted average method.

• The cost of inventories, other than those dealt with by using specific identification, shall be assigned by using– the first-in, first-out (FIFO) or – weighted average cost formula.

• For all inventories having a similar nature and use to the entity,– an entity shall use the same cost formula.

• For inventories with a different nature or use,– different cost formulas may be justified.

Measurement of Inventories

Cost Formulas

FIFOFIFOFIFO

Weighted Average Weighted Weighted Average Average

Entity ST has the following accounting policy in its financial statements of 2006:• Inventories are stated at the lower of cost and net

realisable value. • In respect of unsold machines, cost is determined by

apportionment of the total development costs, including finance costs capitalised, attributable to unsold machines.

• In respect of other inventories, cost, comprising purchase cost from suppliers, is determined:• on first-in-first-out basis and• on the weighted average method.

Please comment.

ExampleExample

Are they having a similar nature and use to the entity?

Are they having a similar nature and use to the entity?

• In accordance with HKAS 2.25, an entity shall use the same cost formula for all inventories having a similar nature and use to the entity, • i.e. using either the first-in, first-out (FIFO) or weighted average cost

formula but not both (unless for inventories with a different nature or use, different cost formulas may be justified).

• In accordance with HKAS 2.25, an entity shall use the same cost formula for all inventories having a similar nature and use to the entity, • i.e. using either the first-in, first-out (FIFO) or weighted average cost

formula but not both (unless for inventories with a different nature or use, different cost formulas may be justified).

• The financial statements shall disclose:a) the accounting policies adopted in measuring inventories, including the

cost formula used;b) the total carrying amount of inventories and the carrying amount in

classifications appropriate to the entity;c) the carrying amount of inventories carried at fair value less costs to sell;d) the amount of inventories recognised as an expense during the period;e) the amount of any write-down of inventories recognised as an expense in

the period in accordance with HKAS 2.34;f) the amount of any reversal of any write-down that is recognised as a

reduction in the amount of inventories recognised as expense in the period in accordance with HKAS 2.34;

g) the circumstances or events that led to the reversal of a write-down of inventories in accordance with HKAS 2.34; and

h) the carrying amount of inventories pledged as security for liabilities.

Cost • is the amount of cash or cash equivalents paid or the fair value of other consideration given to acquire an asset at the time of its acquisition or construction, or

• where applicable, the amount attributed to that asset when initially recognised in accordance with the specific requirements of other HKFRSse.g. HKFRS 2 Share-based Payment

Hong Kong Aircraft Engineering Company Limited Annual Report 2005 states:– Property, plant and equipment are carried at cost less

accumulated depreciation and accumulated impairment losses.

– Cost includes expenditure that is directly attributable to the acquisition of the items.

– Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when • it is probable that future economic benefits

associated with the item will flow to the Group and• the cost of the item can be measured reliably.

– All other repairs and maintenance are expensed in the profit and loss account during the financial period in which they are incurred.

• 2005 Annual Report stated its accounting policy on cost of restoring and improving PPE as follows:– The plant components are depreciated over the period

to overhaul. – Major costs incurred in restoring the plant components

to their normal working condition to allow continued use of the overall asset are• capitalised and • depreciated over the period to the next overhaul.

– Improvements are capitalised and depreciated over their expected useful lives to the Group.

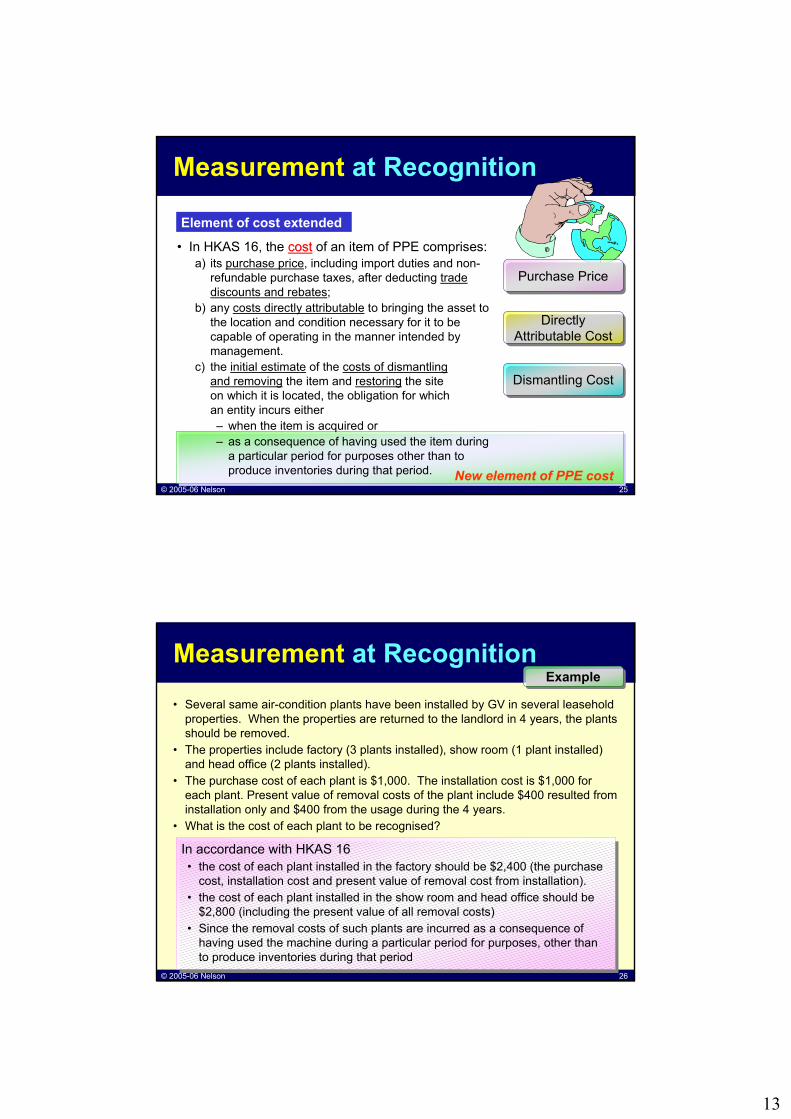

• In HKAS 16, the costcost of an item of PPE comprises:a) its purchase price, including import duties and non-

refundable purchase taxes, after deducting trade discounts and rebates;

b) any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management.

c) the initial estimate of the costs of dismantlingand removing the item and restoring the siteon which it is located, the obligation for whichan entity incurs either– when the item is acquired or– as a consequence of having used the item during

a particular period for purposes other than to produce inventories during that period.

• Several same air-condition plants have been installed by GV in several leasehold properties. When the properties are returned to the landlord in 4 years, the plants should be removed.

• The properties include factory (3 plants installed), show room (1 plant installed) and head office (2 plants installed).

• The purchase cost of each plant is $1,000. The installation cost is $1,000 for each plant. Present value of removal costs of the plant include $400 resulted from installation only and $400 from the usage during the 4 years.

• What is the cost of each plant to be recognised?

In accordance with HKAS 16• the cost of each plant installed in the factory should be $2,400 (the purchase

cost, installation cost and present value of removal cost from installation).• the cost of each plant installed in the show room and head office should be

$2,800 (including the present value of all removal costs)• Since the removal costs of such plants are incurred as a consequence of

having used the machine during a particular period for purposes, other than to produce inventories during that period

In accordance with HKAS 16• the cost of each plant installed in the factory should be $2,400 (the purchase

cost, installation cost and present value of removal cost from installation).• the cost of each plant installed in the show room and head office should be

$2,800 (including the present value of all removal costs)• Since the removal costs of such plants are incurred as a consequence of

having used the machine during a particular period for purposes, other than to produce inventories during that period

• As stated before, definition of Residual Value is revised as

the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset– were already of the age and– in the condition expected at the end of its useful life

Inflation may be incorporated in residual value

shall be reviewed at least at each financial year endif expectations differ from previous estimates, the change shall be accounted for as a change in an accounting estimate in accordance with HKAS 8No such requirement in SSAP 17

• New requirements (on both residual value and useful life)

• PPE’s residual value may increase toan amount equal to or greater than the asset’s carrying amount– If it does, the depreciation charge is zero – unless and until its residual value

subsequently decreases to an amount below the asset’s carrying amount

Be carefulBe careful• By referring to the definition of residual

value• It is still limited to the estimates that it

would receive currently for the asset if– the asset were already of the age and– in the condition expected at the end of

its useful life

Implication:• If

estimated residualvalue > carrying amount⇒ no depreciation is

required• But feasible only if

– the management clearly intends to dispose of the PPE before the end of its physical usage life

– otherwise, the estimated residual value is• minimal or even zero

Implication:• If

estimated residualvalue > carrying amount⇒ no depreciation is

required• But feasible only if

– the management clearly intends to dispose of the PPE before the end of its physical usage life

– otherwise, the estimated residual value is• minimal or even zero

• At 1 Jan. 1985, Entity A bought a flat in Tai Koo Shing at HK$ 0.5 million• Entity A aimed to use it for 50 years until the end of its estimated useful life• The original estimated residual value is zero• Depreciation is calculated on a straight-line basis• At 31 Dec. 2004, the depreciated historical cost (and carrying amount) of the

property was HK$0.3 million

• Now, the price of a similar flat in Tai Koo Shing is about HK$ 3M

• Shall A revise the residual value?

• If A changes its intention and aims to dispose of the flat in 10 years (i.e. 2015)

• Shall A revise the residual value?

ExampleExample

No!A has not changed its usage plan and the residual value after the estimated useful live would still be around zero

No!A has not changed its usage plan and the residual value after the estimated useful live would still be around zero

Yes!If A can demonstrate that it has an intention to dispose of it before the end of its economic life

Yes!If A can demonstrate that it has an intention to dispose of it before the end of its economic life

DisclosureHowever, in SME FRS, the requirement is the same (except no comparative requirement), but it gives the following illustrative notes: However, in SME FRS, the requirement is the same (except no However, in SME FRS, the requirement is the same (except no comparative requirement), but it gives the following illustrativcomparative requirement), but it gives the following illustrative notes: e notes:

Property, plant and equipment

4,104,0101,224,0102,880,000At 31 December 20x4

Net carrying amount:5,270,3002,470,3002,800,000At 31 December 20X5

• For those entities (charities and not-for-profit entities) that have previously taken advantage of the exemption under SSAP 17– They are permitted to deem the carrying amount

of an item of PPE immediately before applying HKAS 16 on its effective date (or earlier) as the cost of that item.

– Depreciation on the deemed cost of an item of property, plant and equipment commences from the time at which HKAS 17 is first applied.

– In the case where a carrying amount is used as a deemed cost for subsequent accounting, this factand the aggregate of the carrying amounts for each class of property, plant and equipment presented shall be disclosed.

• All the costs of PPE of an not-for-profit entity had been written off to income and expenditure statement before 2005.

The entity is permittednot to restate the costs of PPEto carry zero beginning balance on PPE in 2005to follow HKAS 16 from 2005

The entity is permittednot to restate the costs of PPEto carry zero beginning balance on PPE in 2005to follow HKAS 16 from 2005

• All the costs of PPE of an not-for-profit entity had not been depreciated before 2005.

The entity is permittedto begin depreciation from 2005to follow HKAS 16 from 2005

The entity is permittedto begin depreciation from 2005to follow HKAS 16 from 2005

ExampleExample

What is the implication on the following cases when HKAS 16 is adopted? What is the implication on the following cases What is the implication on the following cases when HKAS 16 is adopted? when HKAS 16 is adopted?

For both cases, the fact and the aggregate of the carrying amounts for each class of PPE presented shall be disclosed.

For both cases, the fact and the aggregate of the carrying amounts for each class of PPE presented shall be disclosed.

At each reporting date, an entity shall assess whether there is any indication that an asset may be impaired.If any such indication exists, the entity shall estimate the recoverable amount of the asset.

If, and only if, the recoverable amount of an asset is less than its carrying amount• The carrying amount of the asset shall be

reduced to its recoverable amount.• That reduction is an impairment loss.

andNet Selling Price Value in UseFair value less costs to sell

At each reporting date, an entity shall assess whether there is any indication that an asset may be impaired.If any such indication exists, the entity shall estimate the recoverable amount of the asset.

• For the purpose of impairment testing, goodwill acquired in a business combination shall– from the acquisition date, be allocated to each of the acquirer’s CGUs (or

groups of CGUs) that are expected to benefit from the synergies of the combination

– irrespective of whether other assets or liabilities of the acquiree are assigned to those units or groups of units.

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU

Hong Kong Aircraft Engineering Company Limited Annual Report 2005 states:– Goodwill is tested annually for impairment and

carried at costs less accumulated impairment losses. Any impairment arising on goodwill is recognised in the profit and loss account immediately ……

– Goodwill is allocated to cash-generating units for the purpose of impairment testing …….

– For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units).

• If goodwill has been allocated to a CGU and the entity disposes of an operation within that CGU– the goodwill associated with the operation disposed of shall be:

a) included in the carrying amount of the operation• when determining the gain or loss on disposal; and

b) measured on the basis of the relative values of• the operation disposed of, and• the portion of the CGU retained,

unless the entity can demonstrate that some other method better reflects the goodwill associated with the operation disposed of.

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU DisposalDisposal

• An entity sells for $100 an operation that was part of a CGU to which goodwill has been allocated.

• The goodwill allocated to the unit cannot be identified or associated with an asset group at a level lower than that unit, except arbitrarily.

• The recoverable amount of the portion of the CGU retained is $300.

ExampleExample

• Because the goodwill allocated to the CGU cannot be non-arbitrarily identified or associated with an asset group at a level lower than that unit, the goodwill associated with the operation disposed of is measured on the basis of the relative values of• the operation disposed of, and• the portion of the unit retained.

• Therefore, 25% of the goodwill ($100 / $400) allocated to the CGU is included in the carrying amount of the operation that is sold.

• Because the goodwill allocated to the CGU cannot be non-arbitrarily identified or associated with an asset group at a level lower than that unit, the goodwill associated with the operation disposed of is measured on the basis of the relative values of• the operation disposed of, and• the portion of the unit retained.

• Therefore, 25% of the goodwill ($100 / $400) allocated to the CGU is included in the carrying amount of the operation that is sold.

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU DisposalDisposal

• Assume S mainly involved in holding investment property to derive rental and had 2 properties managed independently.

• On 2.1.2006, S disposed of one property at $8,000 (cost $3,000) and the remaining property’s recoverable amount was $14,000 (cost $3,000).

On company level of S:Sales proceed of property $ 8,000Cost of property (3,000)Gain on disposal $ 5,000On consolidated level:Sales proceed of property $ 8,000Cost of property to the group ($11,000 ÷ 22,000 x 8,000) 4,000Gain on disposal at group level $ 4,000

On company level of S:Sales proceed of property $ 8,000Cost of property (3,000)Gain on disposal $ 5,000On consolidated level:Sales proceed of property $ 8,000Cost of property to the group ($11,000 ÷ 22,000 x 8,000) 4,000Gain on disposal at group level $ 4,000

That’s all?That’s all?Goodwill written off in accordance with HKAS 36($12,100 ÷ 22,000 x 8,000) $ 4,400

Goodwill written off in accordance with HKAS 36($12,100 ÷ 22,000 x 8,000) $ 4,400

Dr($) Cr($)Dr Retained earnings 2,500Cr Investment 2,500To restate the initial 20% investment in Subsidiary S to cost

Original consolidation journals:ExampleExample

Dr Property – fair value adjustment ($11,000 - $6,000) 5,000Issued equity – subsidiary (given) 5,000Retained earnings – subsidiary (given) 9,000Goodwill (as calculated in last slide) 12,100

Cr Investment – cost of combinations (twice) 25,500Minority interest (19,000 x 20%) 3,800Retaining earnings recognised (to the extent thatthey relate to the previously held ownership interests) 1,200Revaluation reserves 600

To recognise the goodwill and eliminate the investments with the equity shares

Dr($) Cr($)Dr Income statement (Retained earnings) 1,000Cr Property 1,000To adjust the gain recognised in S as fair value had been taken up atgroup level before

Additional consolidation journals:ExampleExample

Dr Retained earnings 800Cr Minority interest (4,000 x 20%) 800To allocate the gain on disposal of property to minority interest

Dr Income statement (Retained earnings) 4,400Cr Goodwill 4,400To write off the goodwill allocated to the “business” in accordance withHKAS 36

A portion of the fair value changes from 1st to 2nd acquisition relating to the 2 properties should also be realised when one of them was disposed of,$600 ÷ 22,000 x 8,000 = $218. Please suggest journal!

• If an entity reorganises its reporting structure in a way that changes the composition of one or more CGUs to which goodwill has been allocated– the goodwill shall be reallocated to the

CGUs affected.

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU ReorganiseReorganise

• Goodwill had previously been allocated to CGU A.

• The goodwill allocated to CGU A cannot be identified or associated with an asset group at a level lower than CGU A, except arbitrarily.

• A is to be divided and integrated into 3 other CGUs, namely B, C and D.

ExampleExample

• Because the goodwill allocated to CGU A cannot be non-arbitrarily identified or associated with an asset group at a level lower than CGU A.

• Goodwill is reallocated to CGU B, C and D on the basis of the relative values of the 3 portions of CGU A before those portions are integrated with CGU B, C and D.

• Because the goodwill allocated to CGU A cannot be non-arbitrarily identified or associated with an asset group at a level lower than CGU A.

• Goodwill is reallocated to CGU B, C and D on the basis of the relative values of the 3 portions of CGU A before those portions are integrated with CGU B, C and D.

Allocating Goodwill to CGUAllocating Goodwill to CGUAllocating Goodwill to CGU ReorganiseReorganise

• Entity A acquires 80% interest in GV at $1,600 on 1 Jan. 2005 • It implies that 100% interest of GV to Entity A would be $2,000.• Subsidiary GV has identifiable net assets at a fair value of $1,500

80% 100%Cost of combination $1,600 $2,000Fair value of GV 1,200 1,500Goodwill 400 500

• Goodwill recognised in the consolidation is $400.• Assume at 30 Jun. 2005, the carrying amount of all the balances are the

same but the recoverable amount of GV (a single CGU) is $1,900.• Compare the calculation with or without notional adjustment on goodwill

Without Notional AdjustmentCarrying amount of GV in A’s consolidation $ 1,500Goodwill recognised (attributable to A) 400Total carrying amount $ 1,900Recoverable amount of GV $ 1,900

Without Notional AdjustmentCarrying amount of GV in A’s consolidation $ 1,500Goodwill recognised (attributable to A) 400Total carrying amount $ 1,900Recoverable amount of GV $ 1,900

With Notional AdjustmentTotal carrying amount (as above) $ 1,900Notional adjustment• Goodwill attributable to minority interest 100Notionally adjusted carrying amount $ 2,000Recoverable amount of GV $ 1,900

With Notional AdjustmentTotal carrying amount (as above) $ 1,900Notional adjustment• Goodwill attributable to minority interest 100Notionally adjusted carrying amount $ 2,000Recoverable amount of GV $ 1,900

• Annual impairment test for a CGU to which goodwill has been allocated– may be performed at any time during an annual period, provided the test is

performed at the same time every year.• Different CGUs may be tested for impairment at different times.• However, if some or all of the goodwill allocated to a CGU was

acquired in a business combination during the current annual period,– that unit shall be tested for impairment before the end of the current annual

period.

Timing of Impairment TestsTiming of Impairment TestsTiming of Impairment Tests

• The most recent detailed calculation made in a preceding period of the recoverable amount of a CGU to which goodwill has been allocated– may be used in the impairment test of that CGU in the current period

provided all of the following criteria are met:a) the assets and liabilities making up the CGU have not changed

significantlyb) the most recent recoverable amount calculation resulted in an

amount that exceeded the carrying amount of the CGU by a substantial margin; and

c) the likelihood that a current recoverable amount determination would be less than the current carrying amount of the CGU is remote.

Timing of Impairment TestsTiming of Impairment TestsTiming of Impairment Tests

Corporate AssetsCorporate Assets are assets other than goodwill that contribute to the future cash flows of both• the CGU under review and• other CGUs.

• In testing a CGU for impairment– an entity shall identify all the corporate

assets that relate to the CGU under review.– The allocation approach of the corporate

assets is also amended ……

Examples include:• Building of a headquarter• EDP Equipment• Research centre

Examples include:• Building of a headquarter• EDP Equipment• Research centre

such portion shall be included as part of the carrying amount of the CGU for impairment test

Corporate AssetsCorporate Assets

Can be allocated on a reasonable and consistent basis

Cannot be allocated on a reasonable and consistent basis

The entity shall:1) compare the carrying amount of the CGU (excluding the

corporate asset) with its recoverable amount• recognise any impairment loss first

Firstly, test smaller CGU

Then, test larger CGU containing the goodwill

2) identify the smallest group of CGUs that includes the CGU under review and to which a portion of the carrying amount of the corporate asset can be allocated on a reasonable and consistent basis; and

3) compare the carrying amount of that group of CGUs, including the portion of the carrying amount of the corporate asset allocated to that group of CGUs, with the recoverable amount of the group of CGUs.

• An impairment loss– shall be recognised for a CGU

• if, and only if, the recoverable amount of the CGU (group of CGUs) is less than the carrying amount of the CGU (group of CGUs).

– shall be allocated to reduce the carrying amount of the assets of the CGU (group of CGUs) in the following order:a) first, to reduce the carrying amount of any goodwill

allocated to the CGU (group of CGUs); andb) then, to the other assets of the CGU (group of

CGUs) pro rata on the basis of the carrying amount of each asset in the CGU (group of CGUs).

These reductions in carrying amounts shall be treated as impairment losses on individual assets

• In allocating an impairment loss for a CGU, an entity shall not reduce the carrying amount of an asset below the highest of:a) its fair value less costs to sell (if determinable);b) its value in use (if determinable); andc) zero.

• The amount of the impairment loss that would otherwise have beenallocated to the asset shall be allocated pro rata to the other assets of the CGU (group of CGUs).

• A liability shall be recognised for any remaining amount of an impairment loss for a CGU– if, and only if, that is required by another HKAS/HKFRS.

• In respects of assets other than goodwill, an impairment loss is reversedif there has been a change in the estimates used to determine the recoverable amount and the circumstances and events leading to the impairment cease to exist.

• A reversal of impairment loss is limited to the asset’s carrying amount that would have been determined had no impairment loss been recognised in prior years.

• Reversal of impairment losses are credited to the profit and loss accountexcept when the asset is carried at valuation, in which case the reversal of impairment loss is treated as a revaluation movement.

• More extensive disclosure required now• Main additional disclosure requirements include:

– Extensive information for each CGU (or group of CGUs) for which the carrying amount of goodwill or intangible assets with indefinite useful lives allocated, including• Key assumptions used and the management approach to

measure the recoverable amounts (aligned with revised HKAS 1)• Period for cash flow projection, growth rate, discount rate ……• Certain other information when a reasonably possible change in

a key assumption would cause the carrying amount of CGUs to exceed its recoverable amount

– any portion of the goodwill acquired in a business combination during the period has not been allocated to a CGU (group of CGUs) at the reporting date• the amount of the unallocated goodwill shall be disclosed

together with the reasons why that amount remains unallocated.

Esprit Holdings LimitedEsprit Holdings Limited• In accordance with IAS 36, the Group completed its annual

impairment test for Esprit trademarks by comparing their recoverable amount to their carrying amount as at June 30, 2004.

• The Group appointed independent professional valuers to conduct a valuation of the Esprit trademarks as one corporate asset based on value-in-use calculation.

• The resulting value of the Esprit trademarks as at June 30, 2004was significantly higher than their carrying amount.

• This valuation uses cash flow projections based on financial estimates covering a three-year period, expected royalty ratesderiving from the Esprit trademarks in the range of 3% to 8% and a discount rate of 14%.

• The cash flows beyond the three-year period are extrapolated using a steady 3% growth rate.

• This growth rate does not exceed the long-term average growth rate for apparel markets in which the Group operates.

• Management has considered the above assumptions and valuation and also taken into account the business expansion plan going forward, the current wholesale order books and the strategic retail expansion worldwide and believes that there is no impairment in the Esprit trademarks.

• Management believes that any reasonably foreseeable change in any of the above key assumptions would not cause the aggregate carrying amount of trademarks to exceed the aggregate recoverable amount.

• A provision is– a liability of uncertain timing or amount

Definition →

• A liability is– a present obligation of the entity arising from past events,– the settlement of which is expected to result in an outflow from the entity

of resources embodying economic benefits• Not include those adjustments to the carrying amount of assets, say

provision for depreciation, provision for doubtful debt• Distinguished from other liabilities such as trade payables and

accruals because there is– Uncertainty about the timing or– Uncertainty about the amount of the future expenditure required in

• Entity A– gives warranties at the time of sale to buyers of its product– commits to make good (by repair or replacement)

manufacturing defects that become apparent within 3 years from the date of sale

• On past experience, it is probable (i.e. more likely than not) that there will be some claims under the warranties.

• Is there present obligation as a result of a past obligating event?

Present Present obligationobligation

ExampleExample

Yes• The obligating event is the sale of the product with a warranty,

which gives rise to a legal obligation.• As it is also probable to have an outflow of resources

embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of making good under the warranty products sold before the balance sheet date.

Yes• The obligating event is the sale of the product with a warranty,

which gives rise to a legal obligation.• As it is also probable to have an outflow of resources

embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of making good under the warranty products sold before the balance sheet date.

Legal obligation is an obligation that derives from:a) a contract (through its explicit or implicit terms);b) legislation; orc) other operation of law.

Present obligation

Definition → Recognition

Past eventPast event⇓⇓

Legal ObligationLegal Obligation

Constructive Obligation

Constructive Obligation

Constructive obligation is an obligation that derives from an entity’s actions where:a) by an established pattern of past practice, published

policies or a sufficiently specific current statement, the entity has indicated to other parties that it will accept certain responsibilities; and

b) as a result, the entity has created a valid expectationon the part of those other parties that it will discharge those responsibilities

• The only liabilities recognised in an entity’s balance sheet are those that exist at the balance sheet date.– Independent of future actions (i.e. the future

conduct of business)– Examples of such obligations are

• Penalties or clean-up costs for unlawful environmental damage

• Provision for the decommissioning costs of an oil installation (to the extent that the entity is obliged to rectify damage already caused)

• Entity A in the nuclear power industry causes contamination but cleans up only when required by the law.

• Country X in which Entity A operates has had no legislation requiring cleaning up, and Entity A has been contaminating land there for many years.

• At 31 Dec. 2000, it is virtually certain that a draft law requiring a clean-up of land already contaminated will be enacted shortly after the year end.

• Is there present obligation as a result of a past obligating event?

Yes• The obligating event is the contamination of the land because

of the virtual certainty of legislation requiring cleaning up.• As it is also probable to have an outflow of resources

embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of the clean-up

Yes• The obligating event is the contamination of the land because

of the virtual certainty of legislation requiring cleaning up.• As it is also probable to have an outflow of resources

embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of the clean-up

• Entity C operating power station– causes contamination and in Country Z where there is no

environmental legislation.– has a widely published environmental policy in which it

undertakes to clean up all contamination that it causes.– has a record of honouring this published policy.

• Is there present obligation as a result of a past obligating event?

Yes• The obligating event is the contamination of the land, which

gives rise to a constructive obligation because the conduct of the entity has created a valid expectation on the part of those affected by it that the entity will clean up contamination.

• As it is also probable to have an outflow of resources embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of the clean-up

Yes• The obligating event is the contamination of the land, which

gives rise to a constructive obligation because the conduct of the entity has created a valid expectation on the part of those affected by it that the entity will clean up contamination.

• As it is also probable to have an outflow of resources embodying economic benefits in settlement, a provision is recognised for the best estimate of the costs of the clean-up

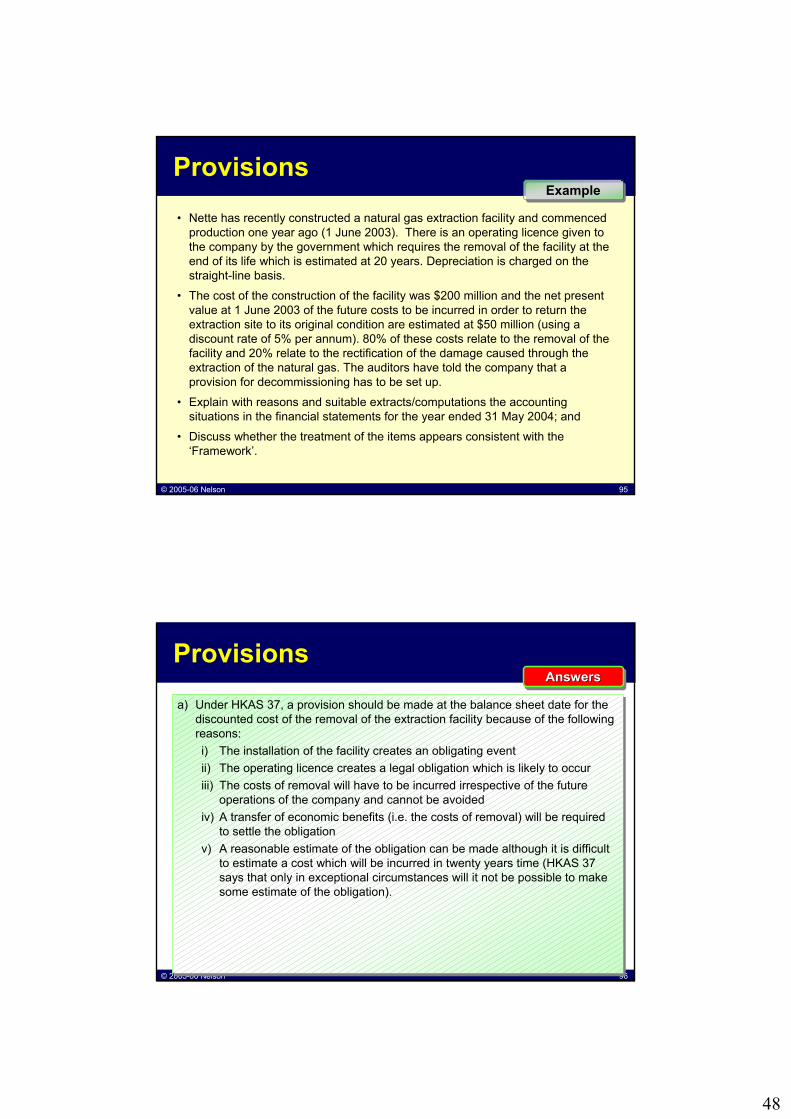

• Nette has recently constructed a natural gas extraction facility and commenced production one year ago (1 June 2003). There is an operating licence given to the company by the government which requires the removal of the facility at the end of its life which is estimated at 20 years. Depreciation is charged on the straight-line basis.

• The cost of the construction of the facility was $200 million and the net present value at 1 June 2003 of the future costs to be incurred in order to return the extraction site to its original condition are estimated at $50 million (using a discount rate of 5% per annum). 80% of these costs relate to the removal of the facility and 20% relate to the rectification of the damage caused through the extraction of the natural gas. The auditors have told the company that a provision for decommissioning has to be set up.

• Explain with reasons and suitable extracts/computations the accounting situations in the financial statements for the year ended 31 May 2004; and

• Discuss whether the treatment of the items appears consistent with the ‘Framework’.

a) Under HKAS 37, a provision should be made at the balance sheet date for the discounted cost of the removal of the extraction facility because of the following reasons:i) The installation of the facility creates an obligating eventii) The operating licence creates a legal obligation which is likely to occuriii) The costs of removal will have to be incurred irrespective of the future

operations of the company and cannot be avoidediv) A transfer of economic benefits (i.e. the costs of removal) will be required

to settle the obligationv) A reasonable estimate of the obligation can be made although it is difficult

to estimate a cost which will be incurred in twenty years time (HKAS 37 says that only in exceptional circumstances will it not be possible to make some estimate of the obligation).

a) Under HKAS 37, a provision should be made at the balance sheet date for the discounted cost of the removal of the extraction facility because of the following reasons:i) The installation of the facility creates an obligating eventii) The operating licence creates a legal obligation which is likely to occuriii) The costs of removal will have to be incurred irrespective of the future

operations of the company and cannot be avoidediv) A transfer of economic benefits (i.e. the costs of removal) will be required

to settle the obligationv) A reasonable estimate of the obligation can be made although it is difficult

to estimate a cost which will be incurred in twenty years time (HKAS 37 says that only in exceptional circumstances will it not be possible to make some estimate of the obligation).

The cost to be incurred will be treated as part of the cost of the facility to be depreciated over its production life. However, the costs relating to the damage caused by the extraction should not be included in the provision, until the gas is extracted which in this case would be 20% of the total discounted provision.

The accounting for the provision is as follows: $mPresent value of obligation at 1 June 2003 50Provision for decommissioning (80% x $50m) 40Provision for damage through extraction

(20% x $50m ÷ 20 years x 1·0520) (note) 1.33

Note: A simple straight line basis has been used to calculate the required provision for damage. A more complex method could be used whereby the present value of the expected cost of the provision ($10m) is provided for over 20 years and the discount thereon is unwound over its life. This would give a charge in the year of $0·5m + $10m x 5% i.e. $1m.

The cost to be incurred will be treated as part of the cost of the facility to be depreciated over its production life. However, the costs relating to the damage caused by the extraction should not be included in the provision, until the gas is extracted which in this case would be 20% of the total discounted provision.

The accounting for the provision is as follows: $mPresent value of obligation at 1 June 2003 50Provision for decommissioning (80% x $50m) 40Provision for damage through extraction

(20% x $50m ÷ 20 years x 1·0520) (note) 1.33

Note: A simple straight line basis has been used to calculate the required provision for damage. A more complex method could be used whereby the present value of the expected cost of the provision ($10m) is provided for over 20 years and the discount thereon is unwound over its life. This would give a charge in the year of $0·5m + $10m x 5% i.e. $1m.

b) The HK ‘Framework’ would require recognition of the full discounted liability for the decommissioning. The problem is that this can only be achieved by creating an asset on the other side of the balance sheet.This asset struggles to meet the Framework’s definition of an asset and is somewhat dubious by nature.An asset is a resource controlled by the company as a result of past events and from which future economic benefits are expected to flow. It is difficult to see how a future cost can meet this definition.The other strange aspect to the treatment of this item is that depreciation (and hence part of the provision) will be treated as an operating cost and the unwinding of the discount could be treated as a finance cost.This latter treatment could fail any qualitative test in terms of the relevance and reliability of the information.A liability is defined in the Framework as a present obligation arising from past events, the settlement of which is expected to result in an outflow of economic benefits.The idea of a ‘constructive obligation’ utilised in HKAS 37 is also included as a requirement in the Framework. Assets and liabilities are essentially a collection of rights and obligations. (ACCA 2004.06)

b) The HK ‘Framework’ would require recognition of the full discounted liability for the decommissioning. The problem is that this can only be achieved by creating an asset on the other side of the balance sheet.This asset struggles to meet the Framework’s definition of an asset and is somewhat dubious by nature.An asset is a resource controlled by the company as a result of past events and from which future economic benefits are expected to flow. It is difficult to see how a future cost can meet this definition.The other strange aspect to the treatment of this item is that depreciation (and hence part of the provision) will be treated as an operating cost and the unwinding of the discount could be treated as a finance cost.This latter treatment could fail any qualitative test in terms of the relevance and reliability of the information.A liability is defined in the Framework as a present obligation arising from past events, the settlement of which is expected to result in an outflow of economic benefits.The idea of a ‘constructive obligation’ utilised in HKAS 37 is also included as a requirement in the Framework. Assets and liabilities are essentially a collection of rights and obligations. (ACCA 2004.06)

Hong Kong Aircraft Engineering Company Limited Annual Report 2005 states:– Provisions are recognised when the Group has a

present legal or constructive obligation as a result of past events; it is more likely than not that an outflow

– of resources will be required to settle the obligation; and the amount has been reliably estimated.

– Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole.

– A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

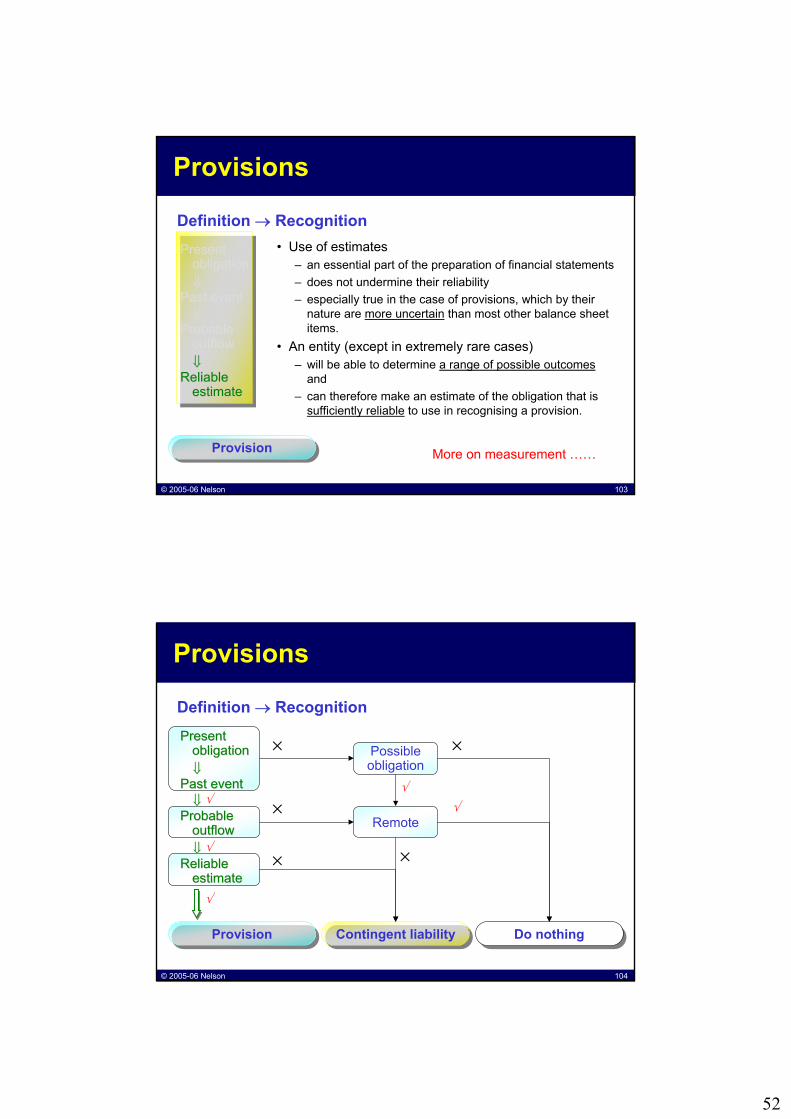

• Use of estimates– an essential part of the preparation of financial statements– does not undermine their reliability– especially true in the case of provisions, which by their

nature are more uncertain than most other balance sheet items.

• An entity (except in extremely rare cases)– will be able to determine a range of possible outcomes

and– can therefore make an estimate of the obligation that is

sufficiently reliable to use in recognising a provision.

a) a possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or

b) a present obligation that arises from past events but is not recognised because:i) it is not probable that an outflow of resources

embodying economic benefits will be requiredto settle the obligation; or

ii) the amount of the obligation cannot bemeasured with sufficient reliability.

→ No Recognition → Disclosed unless remote

Contingent liabilityContingent liability• An entity shall

• A contingent asset is:– a possible asset that arises from past events and whose

existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future eventsnot wholly within the control of the entity.

• An entity shall not recognise a contingent asset

3. Present Value– where the effect of the time value of money is material

• the amount of a provision shall be the present value of the expenditures expected to be required to settle the obligation

– the discount rate shall be a pre-tax rate that reflects• current market assessments of the time value of money and• the risks specific to the liability• not reflect risks for which future cash flow estimates have been

• Entity A is involved in a court case about the plagiarism of software.• Legal opinion seems to indicate that Entity A will lose the case.• Entity A estimates that

– the most likely outcome (60% chance) will be a settlement payment of costs and penalties of $1 million in 2 years’ time

– the best case scenario (30% chance) is deemed to be a settlementpayment of $500,000 in one year’s time and

– the worst case scenario (10% chance) will be a settlement payment of $2 million in 3 years’ time (discount rate is 5%)

• Discuss the implication on the financial position.

Annual Report 2004/05:• Provisions are recognised for liabilities of uncertain timing or

amount when the Board has a legal or constructive obligation arising as a result of a past event, it is probable that an outflow of economic benefits will be required to settle the obligation and a reliable estimate can be made.

• Where the time value of money is material,– provisions are stated at the present value of the

• Where some or all of the expenditure required to settle a provision is expected to be reimbursed by another party

– the reimbursement shall be recognised when, and only when, it is virtually certain that reimbursement will be received if the entity settles the obligation.

– The reimbursement shall be treated as a separate asset.

– The amount recognised for the reimbursement shall not exceed the amount of the provision.

– In the income statement, the expense relating to a provision may be presented net of the amount recognised for a reimbursement.

• 2005 Annual Report stated its accounting policy on provisions as follows:– Provisions are recognised when the Group has a present

legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation, and a reliable estimate of the amount can be made.

– Where the Group expects a provision to be reimbursed, • the reimbursement is recognised as a separate asset• but only when the reimbursement is virtually certain.

• Entity A operates profitably from a factory that it has leased under an operating lease.

• During the year, Entity A relocates its operations to a new factory.• The lease on the old factory continues for the next 4 years.• Entity A cannot cancel that lease and the factory cannot be re-let to

another user.• Discuss.

• The obligating event is the signing of the lease contract, which gives rise to a legal obligation.

• When the lease becomes onerous (unavoidable costs > economic benefits), an outflow of resources embodying economic benefits is probable.

• Until the lease becomes onerous, it is accounted under HKAS 17 Leases.

• A provision is recognised for the best estimate of the unavoidable lease payments.

• The obligating event is the signing of the lease contract, which gives rise to a legal obligation.

• When the lease becomes onerous (unavoidable costs > economic benefits), an outflow of resources embodying economic benefits is probable.

• Until the lease becomes onerous, it is accounted under HKAS 17 Leases.

• A provision is recognised for the best estimate of the unavoidable lease payments.

• A constructive obligation to restructure arises only when an entity:a) has a detailed formal plan for the restructuring identifying at least:

i) the business or part of a business concerned;ii) the principal locations affected;iii) the location, function, and approximate number of employees who will be

compensated for terminating their services;iv) the expenditures that will be undertaken; andv) when the plan will be implemented; and

b) has raised a valid expectation in those affected that it will carry out the restructuring by

i) starting to implement that plan orii) announcing its main features to those affected by it.

Provisions – ApplicationRestructuring

• A restructuring is a programme that is planned and controlled by management, and materially changes either:a) the scope of a business undertaken by an entity; orb) the manner in which that business is conducted

• No obligation arises for the sale of an operation until the entity is committed to the sale, i.e. there is a binding sale agreement.

• A restructuring provision shall include only the direct expendituresarising from the restructuring, which are those that are both:a) necessarily entailed by the restructuring; and

b) not associated with the ongoing activities of the entity.

• A restructuring provision does not include such costs as:a) retraining or relocating continuing staff;

b) marketing; or

c) investment in new systems and distribution networks.

• The directors of Desolve, planned and approved the closure of its glass making activity, a 100% owned subsidiary company, Glass. This decision was announced on 30 June 2001 and the subsidiary was closed down on 30 November 2001. The year end of the group is 31 July 2001 and the financial statements were approved on 10 December 2001.

• Desolve wished to make a provision of $15 million at 31 July 2001 for the costs of closing the glassmaking business. This amount has taken into account approximately $3 million for the potential profit on the disposal of the land and buildings of the subsidiary. Desolve has included this amount ($15 million) in non-current assets and not the income statement as the costs will berecoverable from the estimated disposal proceeds. The contracts for the sale of the land and buildings were signed on 1 Nov 2001 and were completed on 20 Dec 2001 for a price of $25 million at a profit of $4 million.

• It was anticipated that between 31 July 2001 and 30 Nov 2001 the subsidiary would make operating losses of $20 million before it is closed. Also there would be a cost of $5 million incurred in retraining and relocating the employees who accept employment in the refocused Group.

• A provision for the closure of the subsidiary is dealt with by HKAS 37, which classifies the sale or termination of a business as a restructuring and then provides specific guidance on how the general recognition criteria for provisions apply to restructuring.

• HKAS 37 describes the characteristics of an obligating event for a restructuring as being a detailed formal plan and a valid expectation on the part of those affected that the plan will be effected. It restricts a restructuring provision to direct expenditure necessarily incurred and not associated with the ongoing activities.

• There is no scope for providing for future operating losses, as there is no present obligation, nor scope, to include expected gains on disposal of assets.

• Thus, a provision should be recognised of $15 million + $3 million (potential profit on the disposal of land and buildings), i.e. $18 million.

• The amount of $15m should not have been included in non-current assets even though the sale proceeds of the land and buildings would cover this amount.

• Additionally the operating losses of $20 million cannot be provided for under HKAS 37 nor can the costs of retraining and relocating the employees ($5 million) who accept employment in the refocused group as these latter costs benefit the ongoing activities of the enterprise.

(ACCA 2001.12)

• A provision for the closure of the subsidiary is dealt with by HKAS 37, which classifies the sale or termination of a business as a restructuring and then provides specific guidance on how the general recognition criteria for provisions apply to restructuring.

• HKAS 37 describes the characteristics of an obligating event for a restructuring as being a detailed formal plan and a valid expectation on the part of those affected that the plan will be effected. It restricts a restructuring provision to direct expenditure necessarily incurred and not associated with the ongoing activities.

• There is no scope for providing for future operating losses, as there is no present obligation, nor scope, to include expected gains on disposal of assets.

• Thus, a provision should be recognised of $15 million + $3 million (potential profit on the disposal of land and buildings), i.e. $18 million.

• The amount of $15m should not have been included in non-current assets even though the sale proceeds of the land and buildings would cover this amount.

• Additionally the operating losses of $20 million cannot be provided for under HKAS 37 nor can the costs of retraining and relocating the employees ($5 million) who accept employment in the refocused group as these latter costs benefit the ongoing activities of the enterprise.

Disclosure – Provisions• For each class of provision, an entity shall disclose:

a) the carrying amount at the beginning and end of the period;b) additional provisions made in the period, including increases to existing

provisions;c) amounts used (i.e. incurred and charged against the provision) during the

period;d) unused amounts reversed during the period; ande) the increase during the period in the discounted amount arising from the

passage of time and the effect of any change in the discount rate. • Comparative information is not required.• An entity shall disclose the following for each class of provision:

a) a brief description of the nature of the obligation and the expected timing of any resulting outflows of economic benefits;

b) An indication of the uncertainties about the amount or timing of those outflows. Where necessary to provide adequate information, an entity shall disclose the major assumptions made concerning future events; and

c) the amount of any expected reimbursement, stating the amount of any asset that has been recognised for that expected reimbursement.

• Unless the possibility of any outflow in settlement is remote, an entity shall disclose for each class of contingent liability at the balance sheet date a brief description of the nature of the contingent liability and, where practicable:a) an estimate of its financial effect;b) an indication of the uncertainties relating to the amount or timing of any

outflow; andc) the possibility of any reimbursement.

• Where an inflow of economic benefits is probable, an entity shall disclose a brief description of the nature of the contingent assets at the balance sheet date, and, where practicable, an estimate of their financial effect, measured using the principles set out for provisions in paragraphs 36-52 of HKAS 37

• Where any of the information required in HKAS 37 is not disclosed because it is not practicable to do so, that fact shall be stated.

• In extremely rare cases, disclosure of some or all of the information can be expected to prejudice seriously the position of the entity in a dispute with other parties on the subject matter of the provision, contingent liability or contingent asset.

• In such cases, an entity need not disclose the information, but shall disclose the general nature of the dispute, together with the fact that, and reason why, the information has not been disclosed.

• The HK Building Management Ordinance S20(2) suggests the (Owners) Corporation to consider establishing a contingency fund to provide for any expenditure of an unexpected or urgent nature.

• In line with the above, a Maintenance and Repair Fund is normally established by a property management company in order to providefunds for the estimated cost of anticipated maintenance, redecoration and repair works which will be undertaken in the foreseeable future on the premises.

• Should the property management company recognise a provision for such repairs and maintenance in the financial statements?

ExampleExample

• There is no present obligation and no provision is recognised.• However, HKAS 37 neither encourages nor prohibits the segregation of

funds to meet future obligations as suggested by the Building Management Ordinance.

• There is no present obligation and no provision is recognised.• However, HKAS 37 neither encourages nor prohibits the segregation of

funds to meet future obligations as suggested by the Building Management Ordinance.

![[37-00-36] MyEnquiries Updated May 2017 - Revenue · PDF fileRevenue Operational Manual 37-00-36 1 [37-00-36] MyEnquiries Updated May 2017 1. Introduction](https://static.documents.pub/doc/80x56/5abe076c7f8b9a8e3f8c8766/37-00-36-myenquiries-updated-may-2017-revenue-operational-manual-37-00-36-1.jpg)