38

HMC Polymers Investor Roadshow Presentation 22 September 2020

HMC Polymers

Investor Roadshow Presentation

22 September 2020

Presenters

Chookiat K. Pornchai P. Angkanee S.

VP – Sales and Innovation

VP – Strategy, Business Management and

Supply Chain

VP – Finance, Accounting and

Corporate Support

Siridech K.

PRESIDENT

2

Joint Lead Arrangers’Representative

Prasert DeejongkitExecutive Vice President & Manager

Investment Banking Bangkok Bank Public Company Limited

Thitipong JurapornsirideeSenior Vice President

Corporate Finance and StrategyPTT Global Chemical Public Company Limited

Today’s Agenda

1. Company Profile

2. Financial Performance

3. Debentures Offering

3

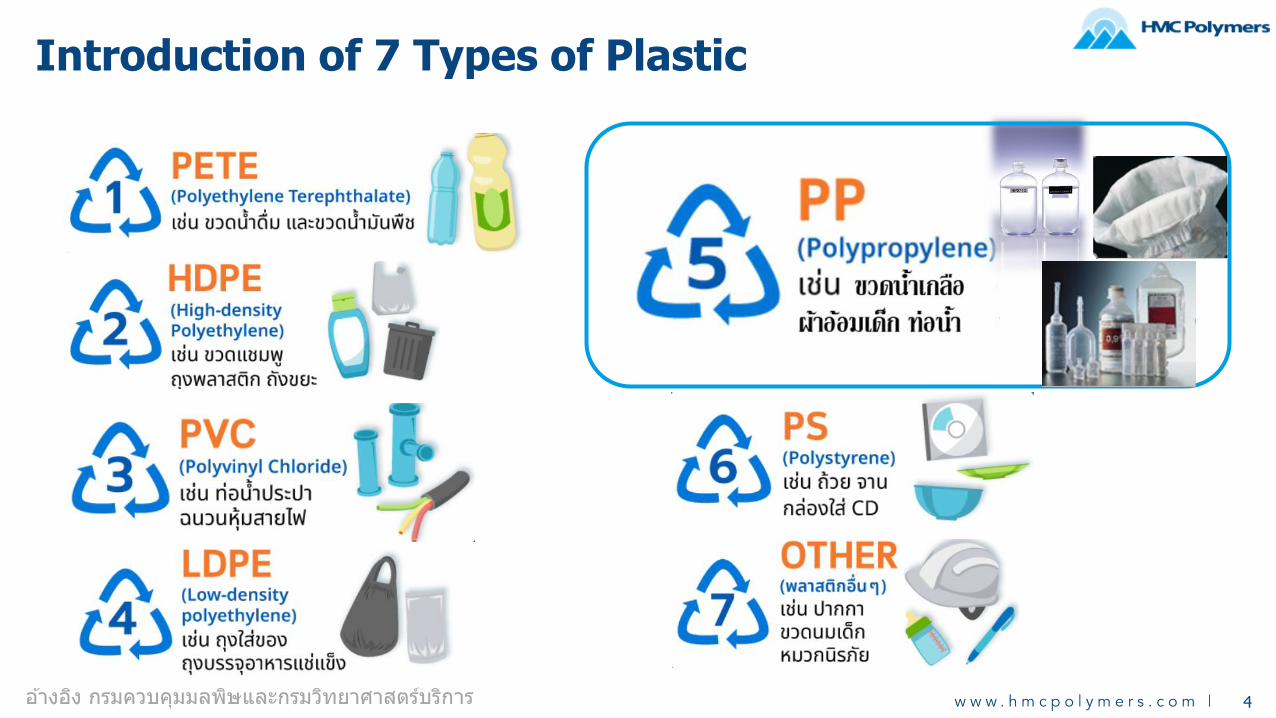

Introduction of 7 Types of Plastic

อา้งองิ กรมควบคมุมลพษิและกรมวทิยาศาสตรบ์รกิาร 4

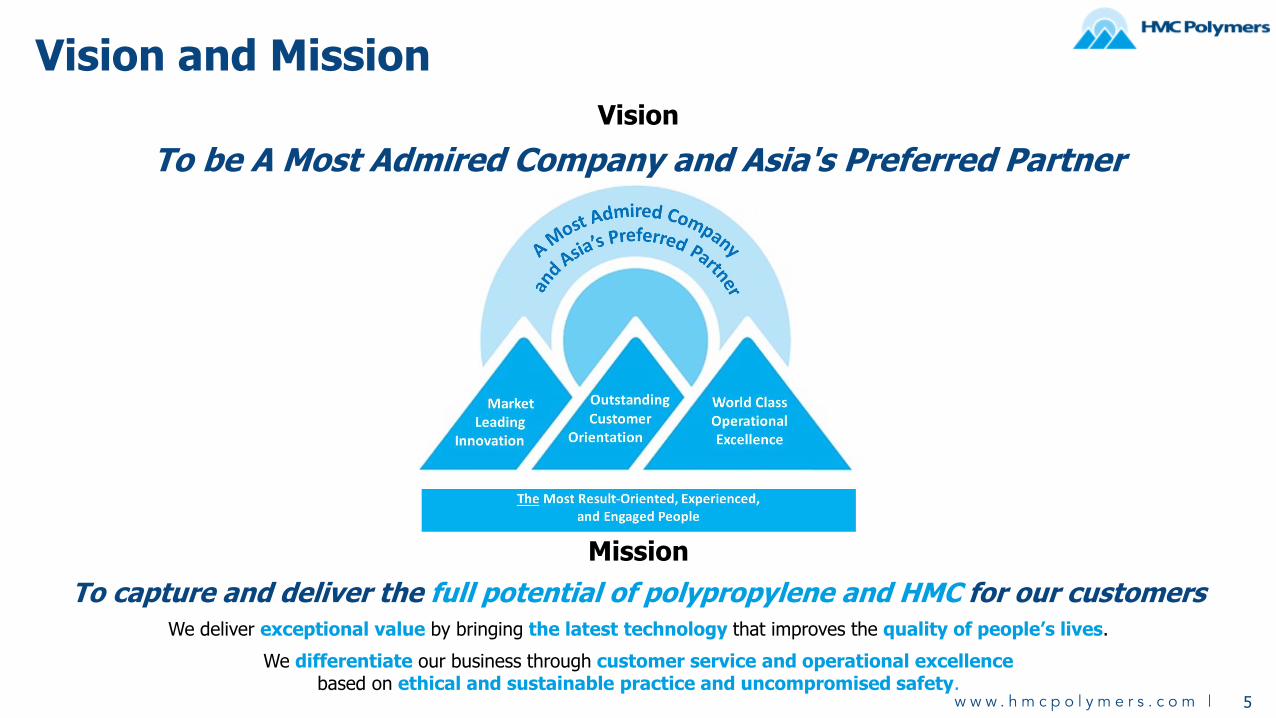

Vision and Mission

Vision

To be A Most Admired Company and Asia's Preferred Partner

Mission

To capture and deliver the full potential of polypropylene and HMC for our customersWe deliver exceptional value by bringing the latest technology that improves the quality of people’s lives.

We differentiate our business through customer service and operational excellencebased on ethical and sustainable practice and uncompromised safety.

5

HMC as “A Most Admired Company”

Reaching no. 1 in ASEAN in PP production capacity by 2022

No. 1 market share in Thailand

No. 1 product and service quality in the eyes of Thai customers

LyondellBasell’s best in class in Safe Work Hours Record

Success through strong and aligned shareholders

The polypropylene expert through the most advanced PP technology

Upstream integration and diversified feedstock

Strong financial position and operating cash flows

1st PP producer in Thailand with over 37 years of experience

PP flagship of GC Group

Strong financial position and operating cash flows

Long Heritage of Achievement2020s

▪ 2022 : PP Line 4

The most advanced PP plant

ever built.

2010s

▪ 2010 : PP Line 3 completed

▪ 2011 : PDH completed

▪ 2012 : CSR-DIW program be Department of

Industrial Work Works achieved

▪ 2015 : Debottlenecked PP Line 3 to 360 KTA

▪ 2017 : Transfer of PTT JV ownership to PTTGC

2000s

▪ 2001 : PP Line 2 debottlenecked to 250 KTA

▪ 2002 : PP Line 1 debottlenecked to 165 KTA

▪ 2006 : PTT became shareholder. Invested in PDH andPP (Spherizone) Projects – 300 KTA each

▪ 2007 : PDH and PP Line 3 construction started

▪ 2008 : New Corporate Identity launched

1990s

▪ 1995 : PP Line 1 debottlenecked to 125 KTA

Investment in Rayong Olefins.

PP Line 2 construction started.

▪ 1997 : PP Line 2 startup with 200 KTA

and Impact Copolymers capability.

▪ 1999 : ISO 9001 (1994 version) & ISO 14001

certification.

1980s

▪ 1983 : Himont, Metro (Srikrung) and Bangkok Bank established “HMC Polymers Company”.

▪ 1987 : Construction start of HMC’s first

plant - first PP manufacturing

facility in Thailand.

▪ 1989 : First plant completed in

September. Production startup

in Nov. for “Pro-fax” – 100 KTA

WORLD CLASS PRODUCTION TECHNOLOGY;

WESTERN INFLUENCE;

HIGHLY DIFFERENTIATED PRODUCT SLATE

7

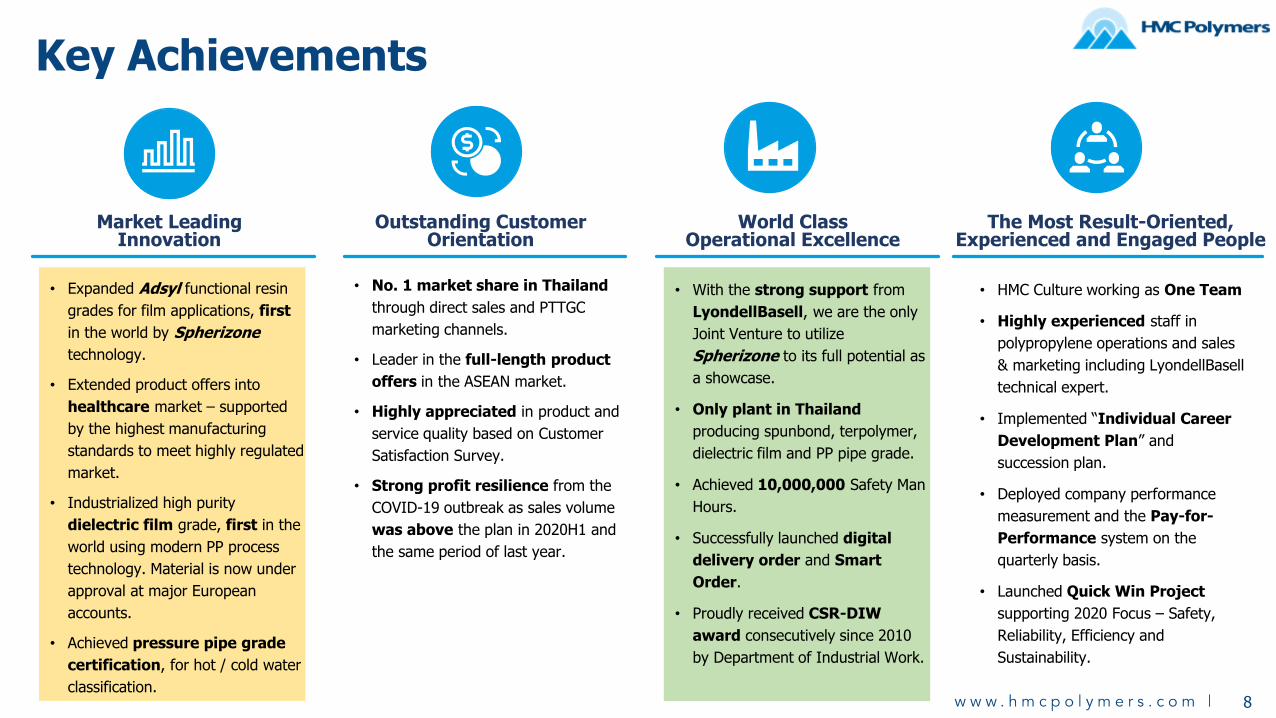

Key Achievements

Market Leading Innovation

Outstanding Customer Orientation

World ClassOperational Excellence

The Most Result-Oriented,Experienced and Engaged People

• Expanded Adsyl functional resin

grades for film applications, first

in the world by Spherizone

technology.

• Extended product offers into

healthcare market – supported

by the highest manufacturing

standards to meet highly regulated

market.

• Industrialized high purity

dielectric film grade, first in the

world using modern PP process

technology. Material is now under

approval at major European

accounts.

• Achieved pressure pipe grade

certification, for hot / cold water

classification.

• With the strong support from

LyondellBasell, we are the only

Joint Venture to utilize

Spherizone to its full potential as

a showcase.

• Only plant in Thailand

producing spunbond, terpolymer,

dielectric film and PP pipe grade.

• Achieved 10,000,000 Safety Man

Hours.

• Successfully launched digital

delivery order and Smart

Order.

• Proudly received CSR-DIW

award consecutively since 2010

by Department of Industrial Work.

• No. 1 market share in Thailand

through direct sales and PTTGC

marketing channels.

• Leader in the full-length product

offers in the ASEAN market.

• Highly appreciated in product and

service quality based on Customer

Satisfaction Survey.

• Strong profit resilience from the

COVID-19 outbreak as sales volume

was above the plan in 2020H1 and

the same period of last year.

• HMC Culture working as One Team

• Highly experienced staff in

polypropylene operations and sales

& marketing including LyondellBasell

technical expert.

• Implemented “Individual Career

Development Plan” and

succession plan.

• Deployed company performance

measurement and the Pay-for-

Performance system on the

quarterly basis.

• Launched Quick Win Project

supporting 2020 Focus – Safety,

Reliability, Efficiency and

Sustainability.

8

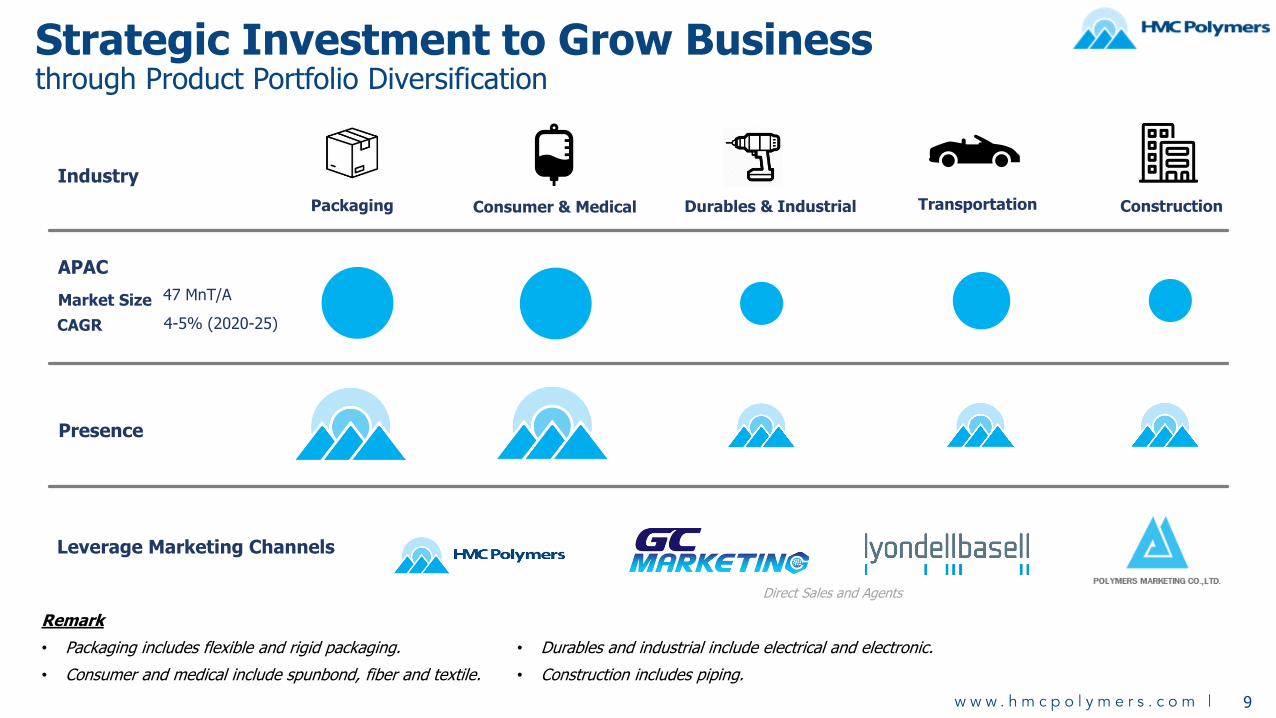

Strategic Investment to Grow Businessthrough Product Portfolio Diversification

Consumer & MedicalPackaging Transportation ConstructionDurables & Industrial

Leverage Marketing Channels

Presence

47 MnT/A

4-5% (2020-25)

APAC

Market Size

CAGR

Direct Sales and Agents

Remark

• Packaging includes flexible and rigid packaging.

• Consumer and medical include spunbond, fiber and textile.

• Durables and industrial include electrical and electronic.

• Construction includes piping.

Industry

9

Strong and Aligned Shareholders

• LyondellBasell (Moody’s Baa1 (international), S&P’s BBB (international)) as a Global leader in PP Technology and catalysto Spheripol : The most used PP technology

o Spherizone : The most advanced PP technology

• Second largest PP producer in the world

• Sales and marketing throughout the world with global grades and brands

THAI INVESTORS 30%

• Strong connections with industry and financial institutions

PTTGC 41%

• PTTGC (AA+(tha)/FITCH(tha)) as a Chemical Flagship of PTT Group with the market capitalization of Baht 0.3 trillion and ranked in SET50

• PTTGC leverages HMC as a PP Flagship to diversify product portfolio to high performance products

• Provide security in competitive feedstock, utilities and other services

• Deliver sales and marketing competencies throughout Asia Pacific

LyondellBasell 29%

10

Board of Directors

11

Mr. Patiparn Sukorndhaman(Chairman)

Mr. Varit Namwong Mr. Boonchai Chunhawiksit Mr. Wiboon Chuchepchunkamon

Ms. Tracey Doreen Campbell Mr. Mattheus Petrus Theodorus BeijkMr. Phirasilp Subhapholsiri

Mr. Suvij Suvaruchiphorn(Vice-Chairman) Dr. Pichit Nithivasin

Mr. Kanit Si

Thai Investors

Professional & Experienced Management Team

Chookiat K. Pornchai P. Angkanee S. Chatri P. Sawangpong K.

VP – Sales and Innovation

VP – Strategy, Business Management and

Supply Chain

VP – Finance, Accounting and

Corporate Support

VP – Operations and Manufacturing

VP – PP4 Project

Siridech K.

PRESIDENT

Board of Directors

Executive Committee

12

Graduated from Washington University, USA in Chemical Engineering with over 30 years of work

experience in refinery and petrochemical business from PTT Group

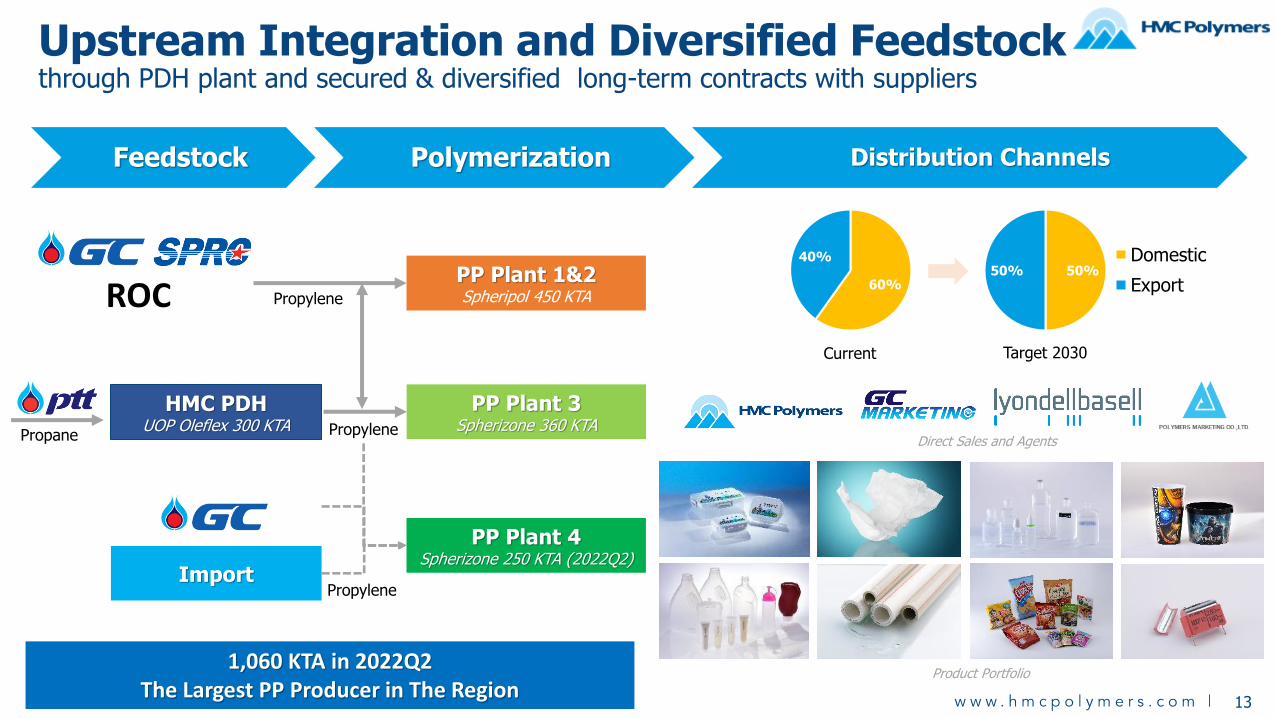

Upstream Integration and Diversified Feedstockthrough PDH plant and secured & diversified long-term contracts with suppliers

HMC PDHUOP Oleflex 300 KTA

PP Plant 1&2Spheripol 450 KTA

PP Plant 3Spherizone 360 KTA

PP Plant 4Spherizone 250 KTA (2022Q2)

Feedstock Polymerization Distribution Channels

60%

40%

Import

50%50%Domestic

Export

Current Target 2030

Propane

Propylene

Propylene

Propylene

Direct Sales and Agents

Product Portfolio

13

1,060 KTA in 2022Q2The Largest PP Producer in The Region

ROC

14

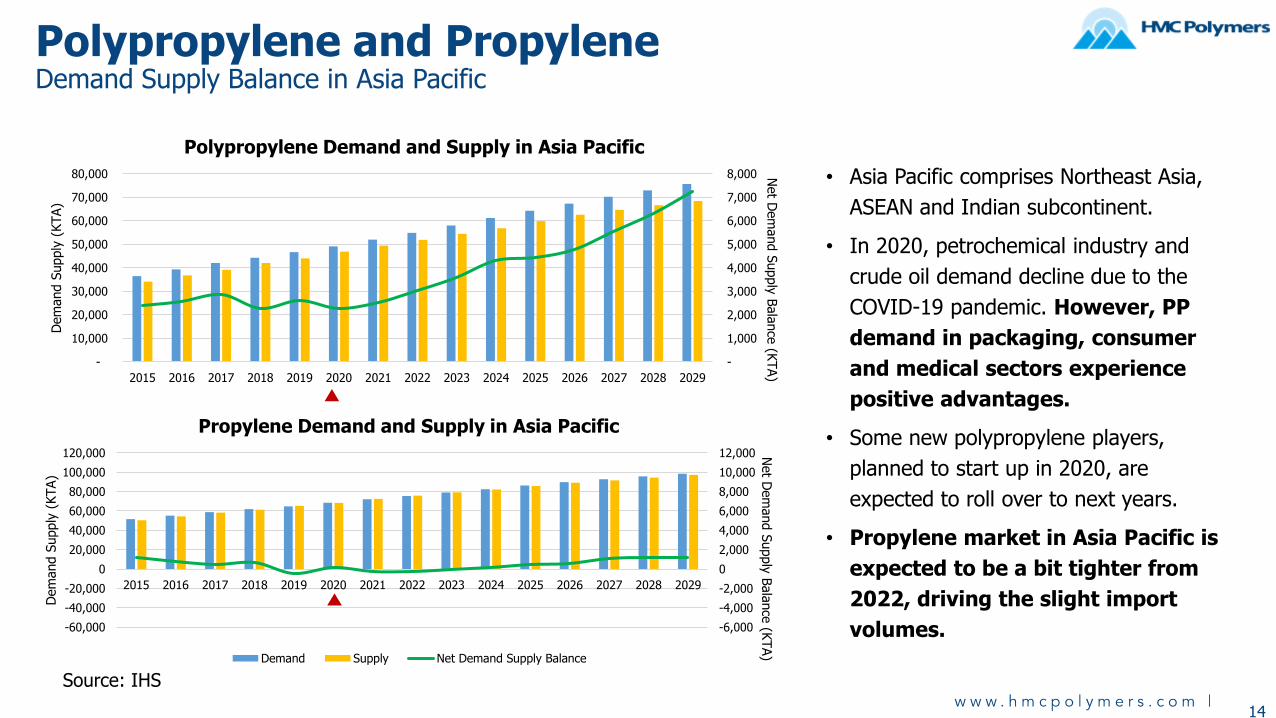

Polypropylene and PropyleneDemand Supply Balance in Asia Pacific

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Net D

em

and S

upply

Bala

nce

(KTA)

Dem

and S

upply

(KTA)

Polypropylene Demand and Supply in Asia Pacific

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Net D

em

and S

upply

Bala

nce

(KTA)

Dem

and S

upply

(KTA)

Propylene Demand and Supply in Asia Pacific

Demand Supply Net Demand Supply Balance

• Asia Pacific comprises Northeast Asia,

ASEAN and Indian subcontinent.

• In 2020, petrochemical industry and

crude oil demand decline due to the

COVID-19 pandemic. However, PP

demand in packaging, consumer

and medical sectors experience

positive advantages.

• Some new polypropylene players,

planned to start up in 2020, are

expected to roll over to next years.

• Propylene market in Asia Pacific is

expected to be a bit tighter from

2022, driving the slight import

volumes.

Source: IHS

15

Market Leading InnovationGrowth in specialty sales

Leveraging the capabilities

of Spherizone Technology

and/or innovative catalysts

from LYB. HMC is actively

developing materials to

further expand the product

portfolio into new

applications:

• Dielectric film for capacitors

• Pressure pipe and high stiffness sewage and drainage pipe

• Specialty resins for film functional layer

• Highly modified random copolymers for application requiring softness and transparency

Capacity will be further enhanced by PP4.

0

2000

4000

6000

8000

10000

12000

14000

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Q32019

Q42019

Q12020

Q22020

Sale

s p

er

Qu

arte

r /

mT

Adsyl5 Pipe High C2 RaCo Capacitor New Adsyl 3

COVID-19 pandemic

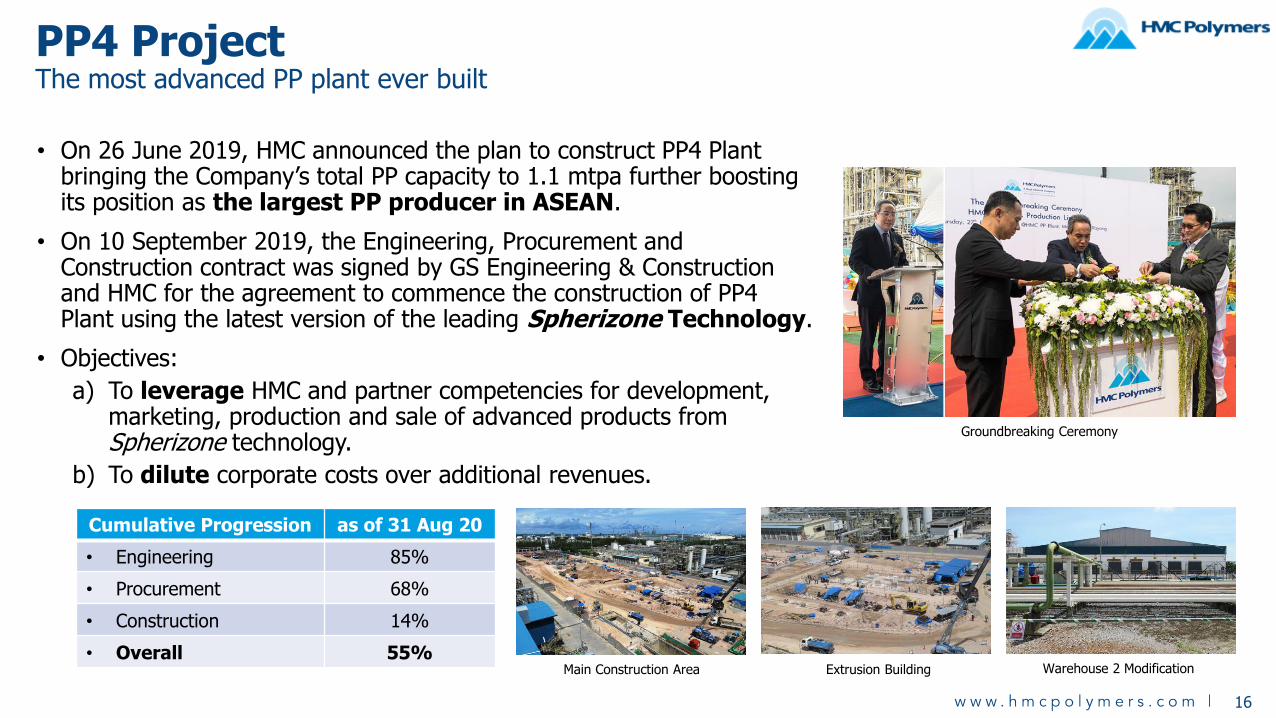

• On 26 June 2019, HMC announced the plan to construct PP4 Plant bringing the Company’s total PP capacity to 1.1 mtpa further boosting its position as the largest PP producer in ASEAN.

• On 10 September 2019, the Engineering, Procurement and Construction contract was signed by GS Engineering & Construction and HMC for the agreement to commence the construction of PP4 Plant using the latest version of the leading Spherizone Technology.

• Objectives:

a) To leverage HMC and partner competencies for development, marketing, production and sale of advanced products from Spherizone technology.

b) To dilute corporate costs over additional revenues.

PP4 ProjectThe most advanced PP plant ever built

Main Construction Area Extrusion Building Warehouse 2 Modification

Groundbreaking Ceremony

16

Cumulative Progression as of 31 Aug 20

• Engineering 85%

• Procurement 68%

• Construction 14%

• Overall 55%

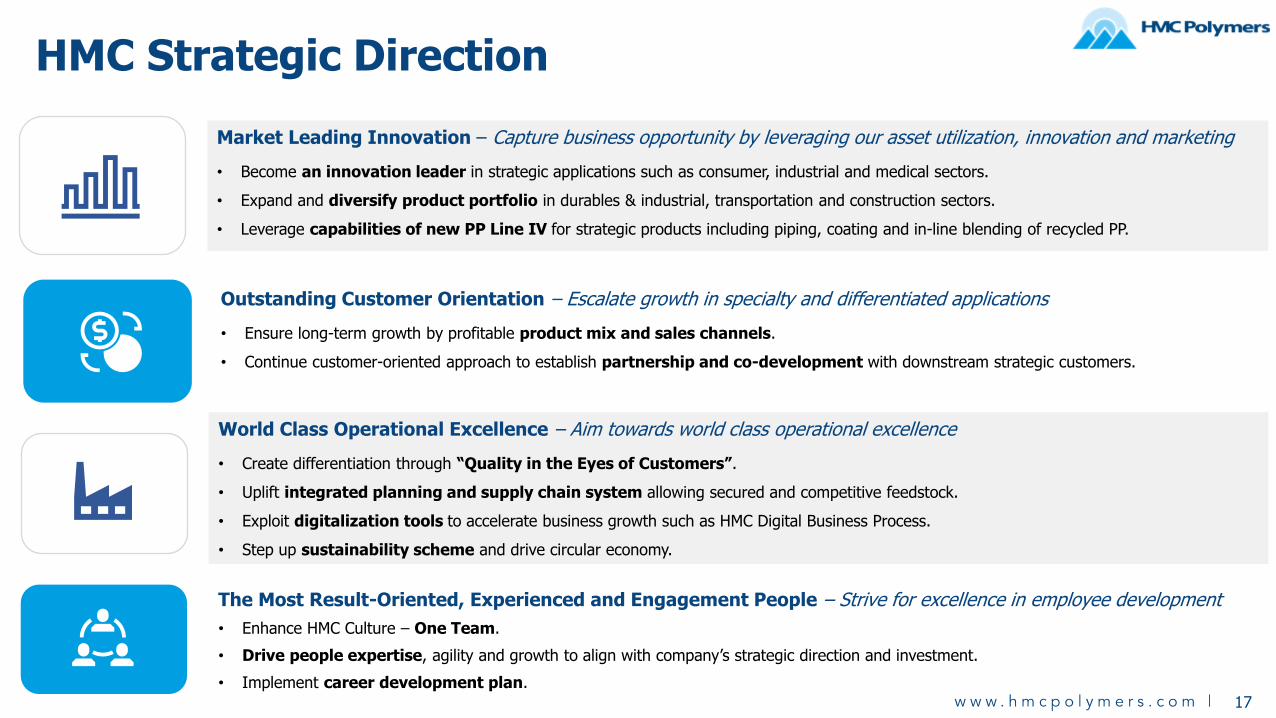

HMC Strategic Direction

Market Leading Innovation – Capture business opportunity by leveraging our asset utilization, innovation and marketing

• Become an innovation leader in strategic applications such as consumer, industrial and medical sectors.

• Expand and diversify product portfolio in durables & industrial, transportation and construction sectors.

• Leverage capabilities of new PP Line IV for strategic products including piping, coating and in-line blending of recycled PP.

Outstanding Customer Orientation – Escalate growth in specialty and differentiated applications

• Ensure long-term growth by profitable product mix and sales channels.

• Continue customer-oriented approach to establish partnership and co-development with downstream strategic customers.

The Most Result-Oriented, Experienced and Engagement People – Strive for excellence in employee development

• Enhance HMC Culture – One Team.

• Drive people expertise, agility and growth to align with company’s strategic direction and investment.

• Implement career development plan.

World Class Operational Excellence – Aim towards world class operational excellence

• Create differentiation through “Quality in the Eyes of Customers”.

• Uplift integrated planning and supply chain system allowing secured and competitive feedstock.

• Exploit digitalization tools to accelerate business growth such as HMC Digital Business Process.

• Step up sustainability scheme and drive circular economy.

17

18

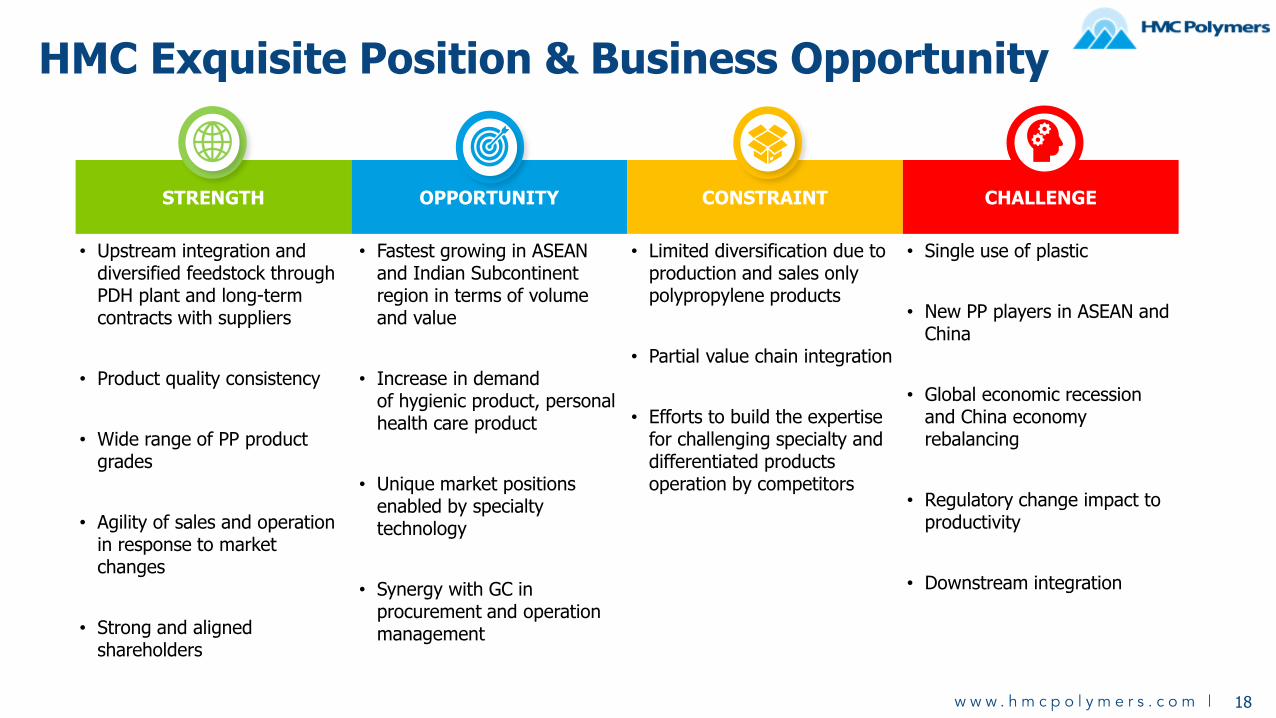

HMC Exquisite Position & Business Opportunity

STRENGTH OPPORTUNITY CONSTRAINT CHALLENGE

• Upstream integration and diversified feedstock through PDH plant and long-term contracts with suppliers

• Product quality consistency

• Wide range of PP product grades

• Agility of sales and operation in response to market changes

• Strong and aligned shareholders

• Fastest growing in ASEAN and Indian Subcontinent region in terms of volume and value

• Increase in demand of hygienic product, personal health care product

• Unique market positions enabled by specialty technology

• Synergy with GC in procurement and operation management

• Limited diversification due to production and sales only polypropylene products

• Partial value chain integration

• Efforts to build the expertise for challenging specialty and differentiated products operation by competitors

• Single use of plastic

• New PP players in ASEAN and China

• Global economic recession and China economy rebalancing

• Regulatory change impact to productivity

• Downstream integration

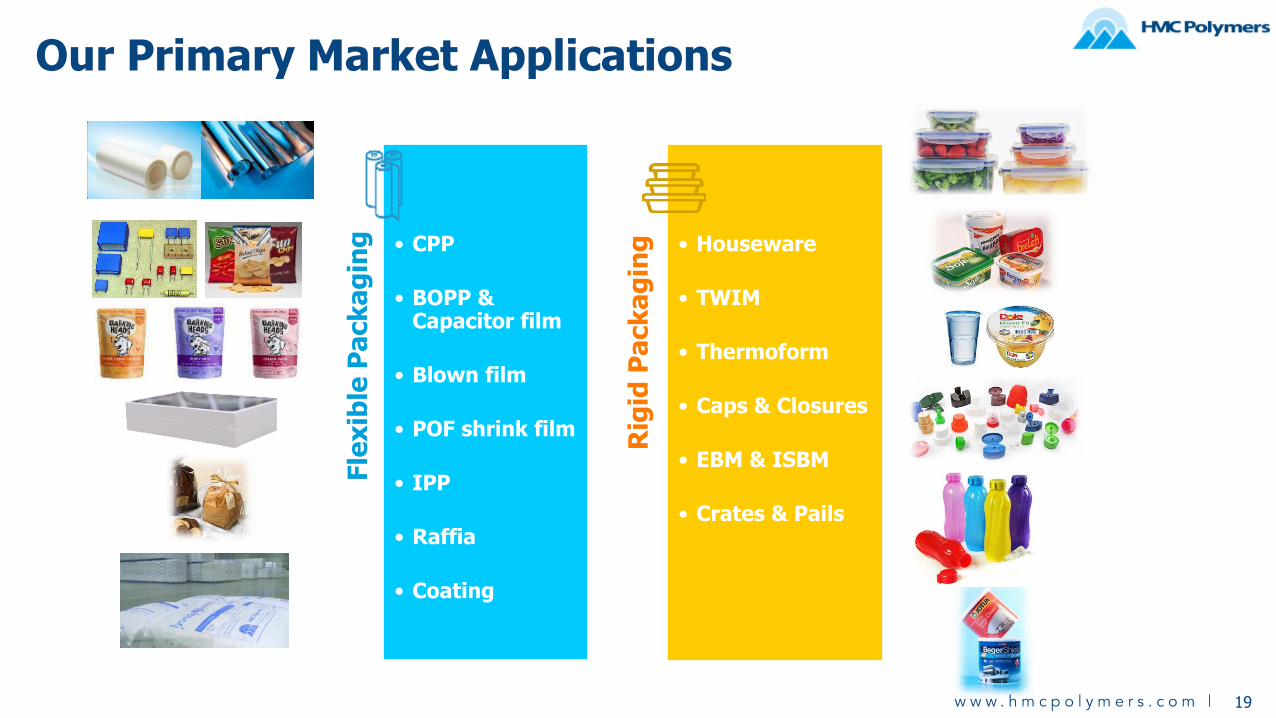

Our Primary Market Applications

Fle

xib

le P

ack

ag

ing • CPP

• BOPP & Capacitor film

• Blown film

• POF shrink film

• IPP

• Raffia

• Coating

Rig

id P

ack

ag

ing • Houseware

• TWIM

• Thermoform

• Caps & Closures

• EBM & ISBM

• Crates & Pails

19

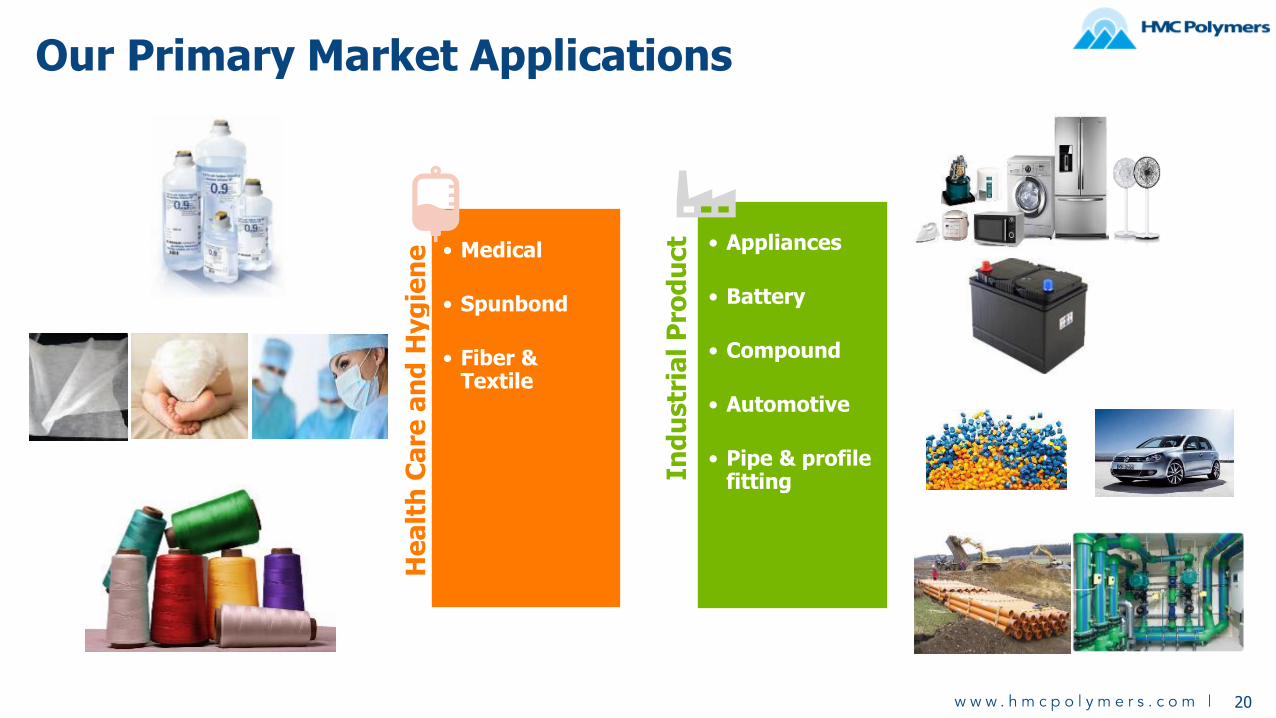

Our Primary Market Applications

He

alt

h C

are

an

d H

yg

ien

e • Medical

• Spunbond

• Fiber & Textile

Ind

ustr

ial P

rod

uct • Appliances

• Battery

• Compound

• Automotive

• Pipe & profile fitting

20

Good product aesthetics

Microwaveable

High transparency and gloss Food contact compliance

Good impact strengthat low temp

Preserve long shelf life

Advantages of PolypropyleneHMC Product’s value proposition through a variety of property

21

Light weight

High creep resistance

Soft & Hygiene High purity

Durable & Stack ability Excellent chemical resistance

Advantages of PolypropyleneHMC Product’s value proposition through a variety of property

22

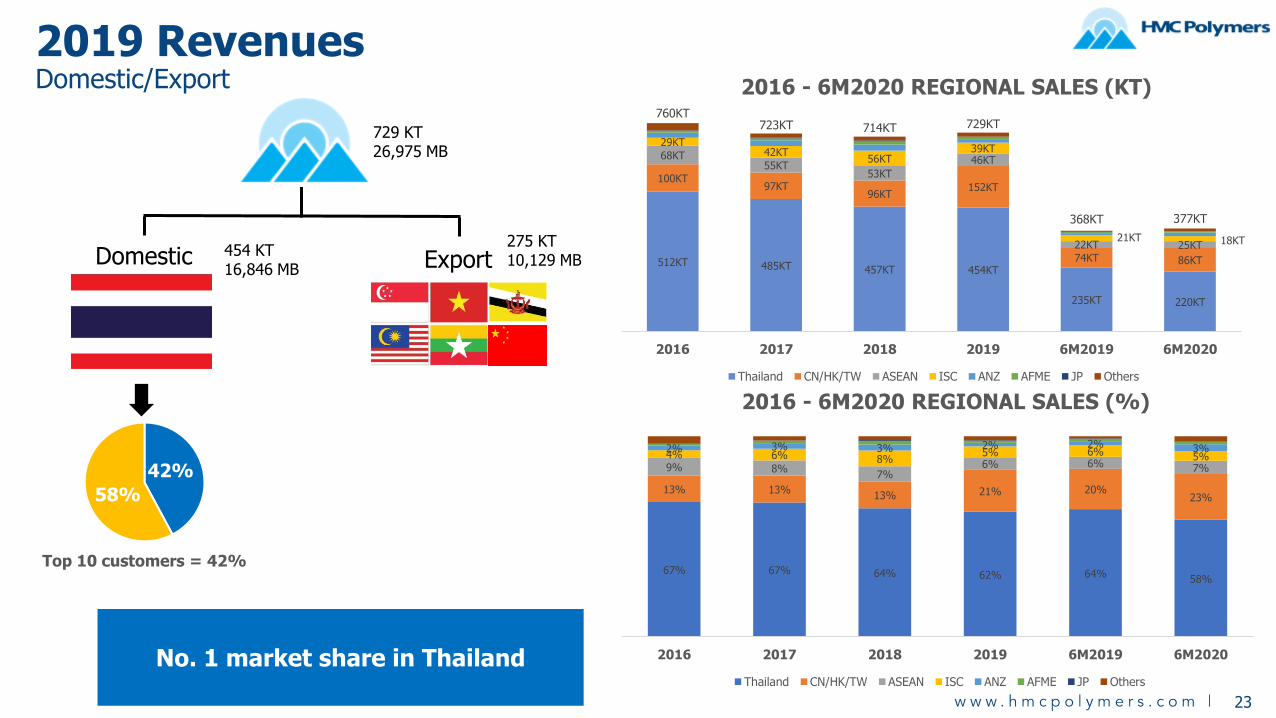

42%

58%

Domestic Export

Top 10 customers = 42%

729 KT26,975 MB

454 KT16,846 MB

275 KT10,129 MB

2019 RevenuesDomestic/Export

No. 1 market share in Thailand

23

512KT 485KT 457KT 454KT

235KT 220KT

100KT97KT

96KT152KT

74KT 86KT

68KT55KT

53KT

46KT

22KT 25KT

29KT42KT

56KT39KT

21KT 18KT

760KT723KT 714KT 729KT

368KT 377KT

2016 2017 2018 2019 6M2019 6M2020

Thailand CN/HK/TW ASEAN ISC ANZ AFME JP Others

67% 67% 64% 62% 64%58%

13% 13%13% 21% 20%

23%

9% 8%7%

6% 6% 7%

4% 6% 8%5% 6% 5%

2% 3% 3% 2% 2% 3%

2016 2017 2018 2019 6M2019 6M2020

Thailand CN/HK/TW ASEAN ISC ANZ AFME JP Others

2016 - 6M2020 REGIONAL SALES (KT)

2016 - 6M2020 REGIONAL SALES (%)

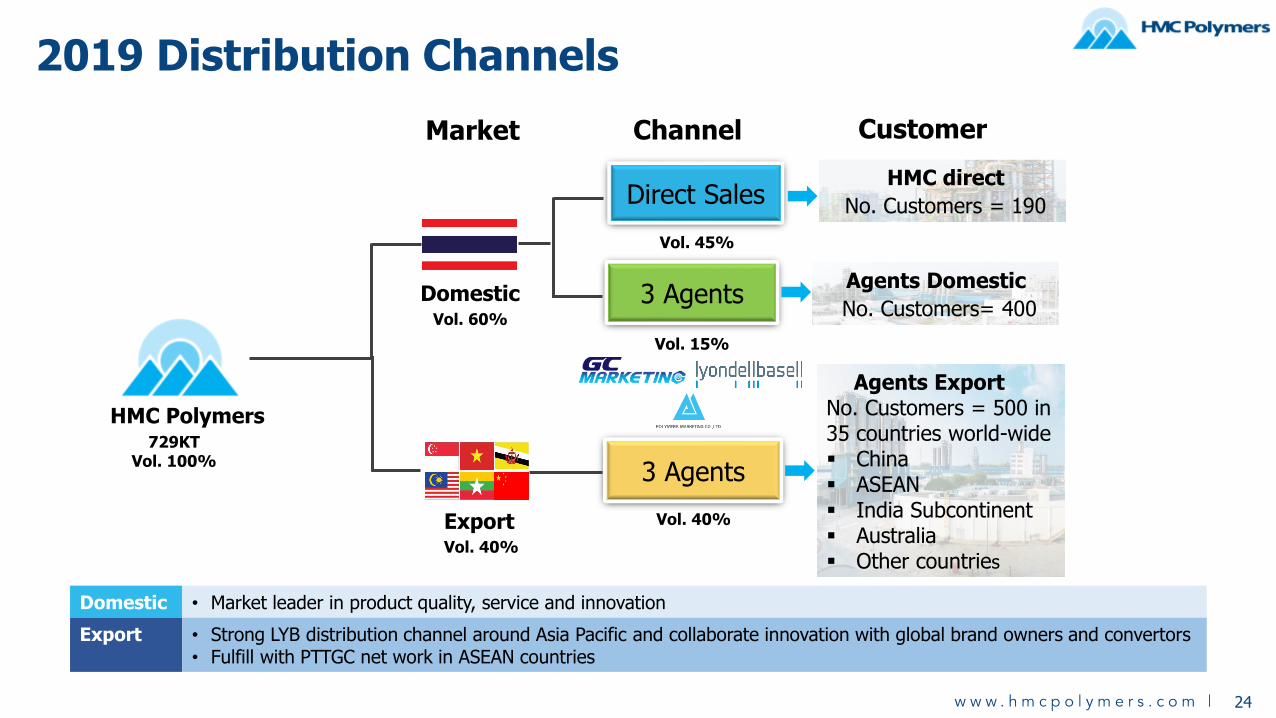

2019 Distribution Channels

729KTVol. 100%

HMC Polymers

Domestic

Market

Vol. 60%

Vol. 40%

Export

Direct Sales

Channel

3 Agents

Vol. 45%

Vol. 15%

3 Agents

Vol. 40%

Customer

HMC direct

No. Customers = 190

Agents Domestic

No. Customers= 400

Agents ExportNo. Customers = 500 in 35 countries world-wide▪ China▪ ASEAN▪ India Subcontinent▪ Australia▪ Other countries

Domestic • Market leader in product quality, service and innovation

Export • Strong LYB distribution channel around Asia Pacific and collaborate innovation with global brand owners and convertors• Fulfill with PTTGC net work in ASEAN countries

24

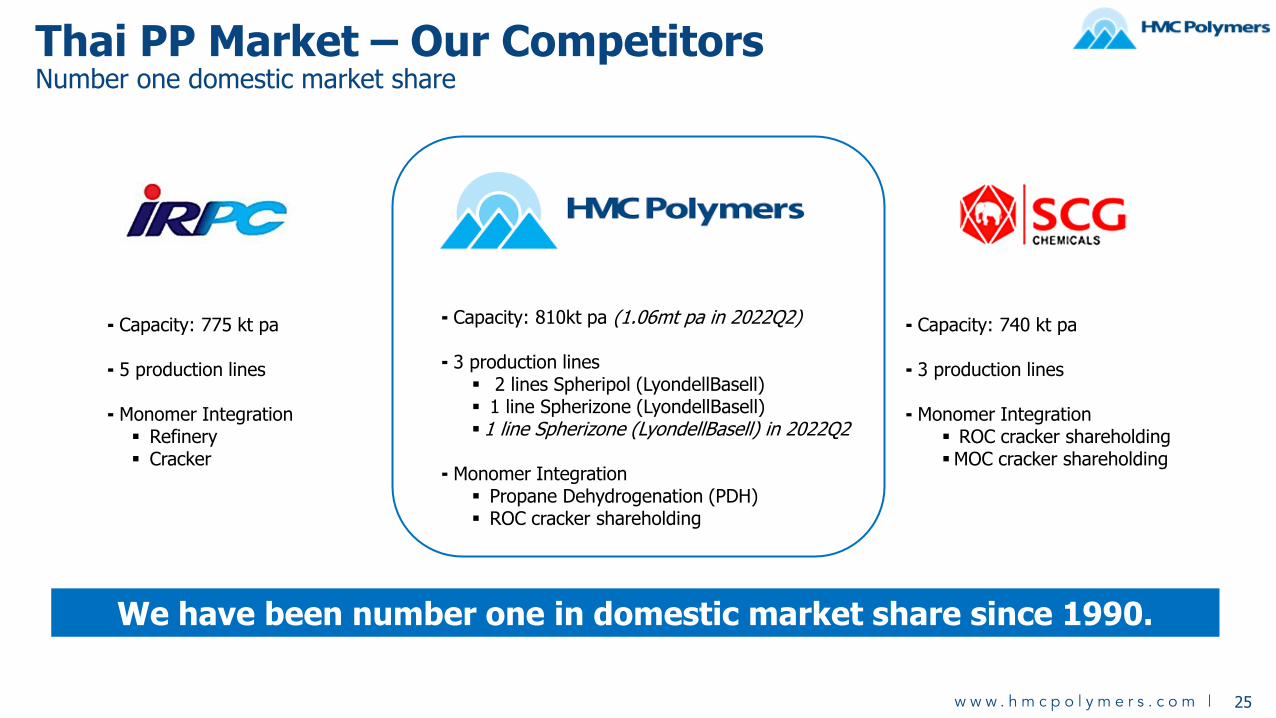

Thai PP Market – Our CompetitorsNumber one domestic market share

⁃ Capacity: 740 kt pa

⁃ 3 production lines

⁃ Monomer Integration▪ ROC cracker shareholding▪MOC cracker shareholding

⁃ Capacity: 775 kt pa

⁃ 5 production lines

⁃ Monomer Integration▪ Refinery▪ Cracker

We have been number one in domestic market share since 1990.

⁃ Capacity: 810kt pa (1.06mt pa in 2022Q2)

⁃ 3 production lines▪ 2 lines Spheripol (LyondellBasell)▪ 1 line Spherizone (LyondellBasell)▪ 1 line Spherizone (LyondellBasell) in 2022Q2

⁃ Monomer Integration▪ Propane Dehydrogenation (PDH)▪ ROC cracker shareholding

25

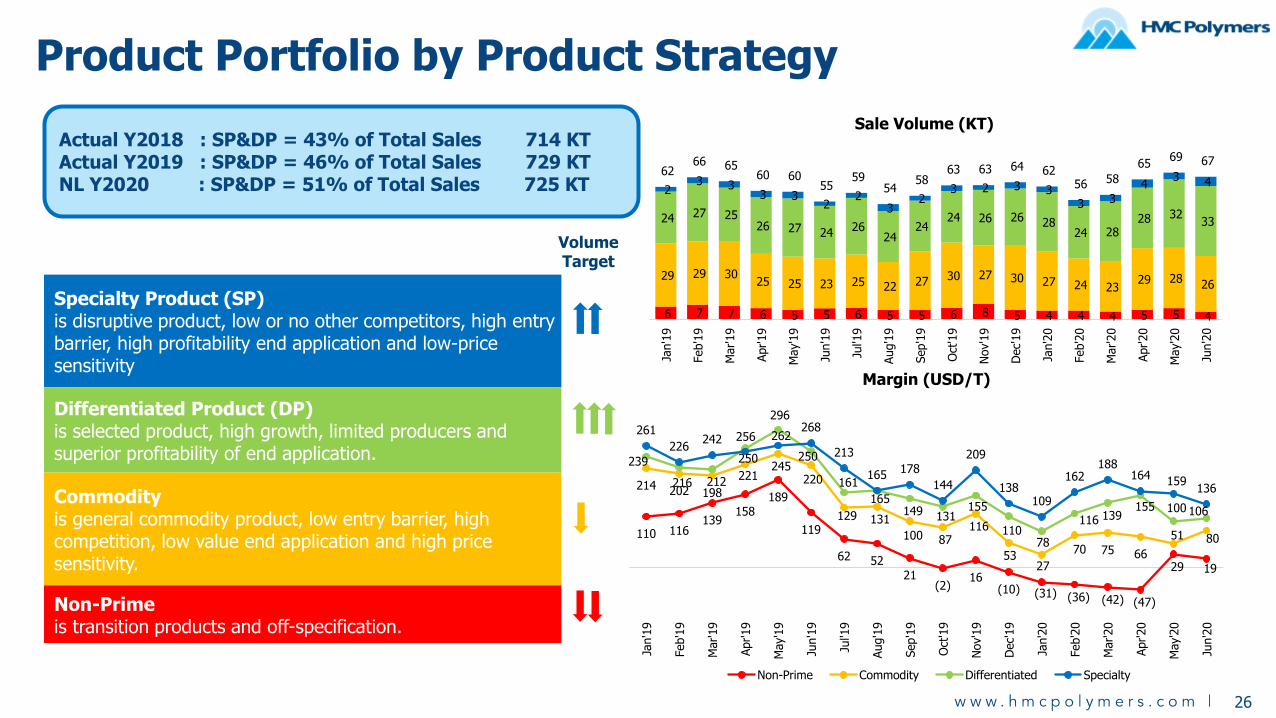

Product Portfolio by Product Strategy

Volume Target

Specialty Product (SP)is disruptive product, low or no other competitors, high entry barrier, high profitability end application and low-price sensitivity

Differentiated Product (DP)is selected product, high growth, limited producers and superior profitability of end application.

Commodityis general commodity product, low entry barrier, high competition, low value end application and high price sensitivity.

Non-Primeis transition products and off-specification.

6 7 7 6 5 5 6 5 5 6 8 5 4 4 4 5 5 4

29 29 30 25 25 23 25 22 27 30 27 30 27 24 23

29 28 26

24 27 25 26 27 24

26 24

24 24 26 26 28

24 28 28 32

33

2 3 3

3 3 2

2 3

2 3 2 3 3

3 3 4

3 4 62

66 65 60 60

55 59

54 58

63 63 64 62 56 58

65 69 67

Jan'1

9

Feb'1

9

Mar'19

Apr'19

May'1

9

Jun'1

9

Jul'1

9

Aug'1

9

Sep'1

9

Oct

'19

Nov'1

9

Dec'

19

Jan'2

0

Feb'2

0

Mar'20

Apr'20

May'2

0

Jun'2

0

Sale Volume (KT)

110 116 139

158 189

119

62 52 21

(2)16

(10) (31) (36) (42) (47)

29 19

214 202 198

221 245

220

129 131

100 87 116

53 27

70 75 66

51 80

239

216 212

256

296

250

161

165 149 131

155

110 78

116 139 155 100 106

261

226 242

250

262 268

213

165 178

144

209

138 109

162 188

164 159 136

Jan'1

9

Feb'1

9

Mar'19

Apr'19

May'1

9

Jun'1

9

Jul'1

9

Aug'1

9

Sep'1

9

Oct

'19

Nov'1

9

Dec'

19

Jan'2

0

Feb'2

0

Mar'20

Apr'20

May'2

0

Jun'2

0

Margin (USD/T)

Non-Prime Commodity Differentiated Specialty

26

Actual Y2018 : SP&DP = 43% of Total Sales 714 KTActual Y2019 : SP&DP = 46% of Total Sales 729 KTNL Y2020 : SP&DP = 51% of Total Sales 725 KT

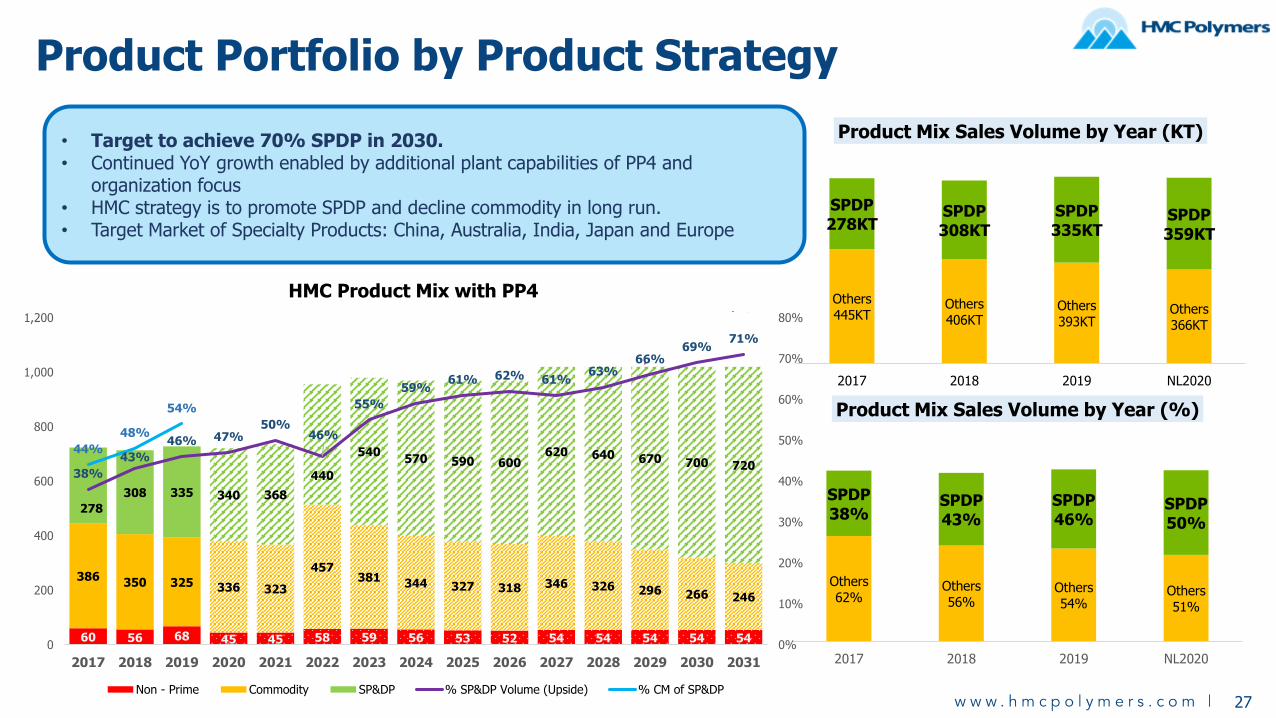

Product Portfolio by Product Strategy

Others

445KTOthers

406KTOthers

393KTOthers

366KT

SPDP278KT

SPDP308KT

SPDP335KT

SPDP359KT

2017 2018 2019 NL2020

Product Mix Sales Volume by Year (KT)

Others

62%Others

56%Others

54%Others

51%

SPDP38%

SPDP43%

SPDP46%

SPDP50%

2017 2018 2019 NL2020

Product Mix Sales Volume by Year (%)

27

• Target to achieve 70% SPDP in 2030.• Continued YoY growth enabled by additional plant capabilities of PP4 and

organization focus• HMC strategy is to promote SPDP and decline commodity in long run.• Target Market of Specialty Products: China, Australia, India, Japan and Europe

60 56 68 45 45 58 59 56 53 52 54 54 54 54 54

386350 325 336 323

457381

344 327 318 346 326 296 266 246

278

308 335 340 368

440

540570 590 600

620 640 670 700 72038%

43%

46% 47%50%

46%

55%

59%61% 62% 61%

63%66%

69%71%

44%

48%

54%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

200

400

600

800

1,000

1,200

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

HMC Product Mix with PP4

Non - Prime Commodity SP&DP % SP&DP Volume (Upside) % CM of SP&DP

Today’s Agenda

1. Company Profile

2. Financial Performance

3. Debentures Offering

28

Financial PerformanceProfit resilience amid the cyclicality of petrochemical business

29

Total Revenue (Unit: THB million)

EBITDA (Unit: THB million) Net Profit (Unit: THB million)

* Dividend Income derived by PTTGC & ROC investment.

6,503

3,697

20.08%13.56%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2018 2019EBITDA EBITDA Margin

-43.15% YoY 3,997

1,656

12.34%6.07%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2018 2019Net Profit Net Profit Margin

-58.57% YoY

19,57116,720

11,424

10,182

1,391

361

32,386

27,263

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2018 2019

Revenue from sale of goods (Domestic) Revenue from sale of goods (Export) Dividend Income & Other Income

-15.82% YoY • 2019 challenge as a result of global economic tensions and weak market conditions due to cyclicality of the industry

• We focus on high-value-added product resulting in decent performance and EBITDA margin around 14%o Sales volume +2% but declined in price at -11%

following the weaker PP market prices at -14%o Planned shutdown of PDH Planto Stronger THB against USDo Less dividends income

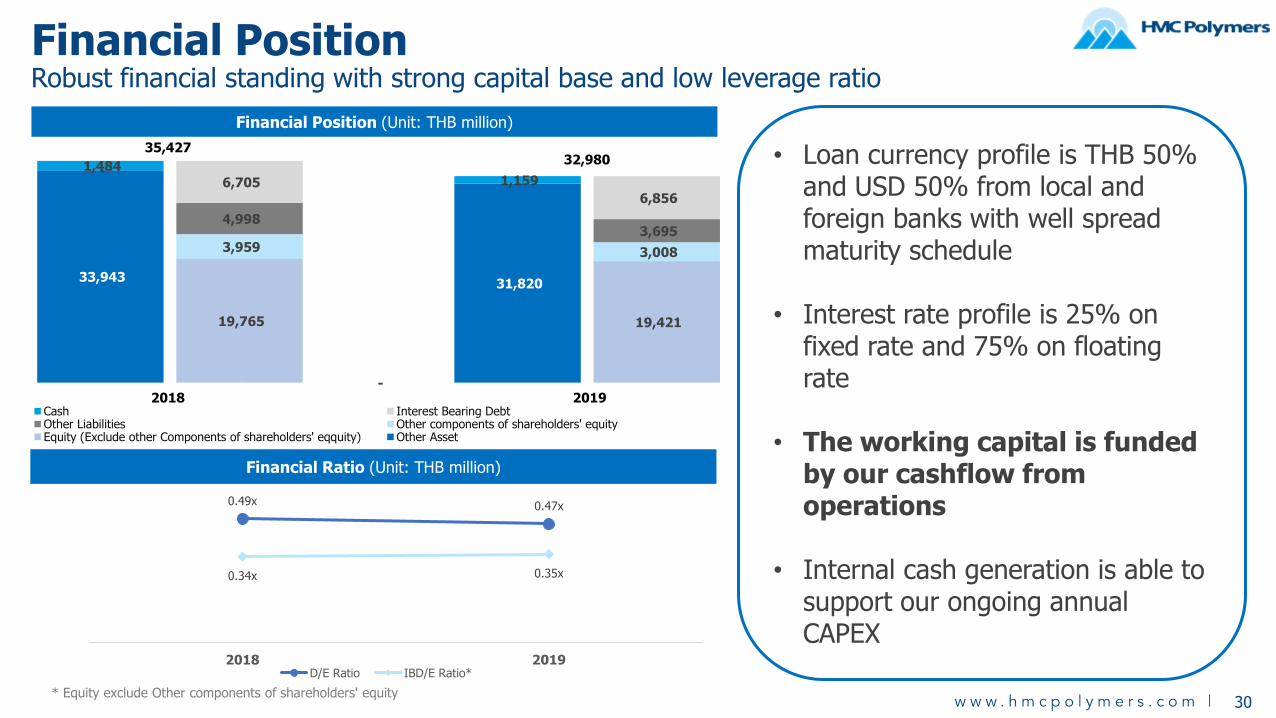

Financial PositionRobust financial standing with strong capital base and low leverage ratio

30

Financial Position (Unit: THB million)

Financial Ratio (Unit: THB million)

* Equity exclude Other components of shareholders' equity

0.49x 0.47x

0.34x 0.35x

2018 2019D/E Ratio IBD/E Ratio*

• Loan currency profile is THB 50% and USD 50% from local and foreign banks with well spread maturity schedule

• Interest rate profile is 25% on fixed rate and 75% on floating rate

• The working capital is funded by our cashflow from operations

• Internal cash generation is able tosupport our ongoing annual CAPEX

33,943

- -

31,820

19,765 19,421

3,959 3,008

-

4,998

-

-

3,695

6,705 6,856

1,484 1,159

Cash Interest Bearing DebtOther Liabilities Other components of shareholders' equityEquity (Exclude other Components of shareholders' eqquity) Other Asset

2018

35,427

2019

32,980

A-(tha)

31

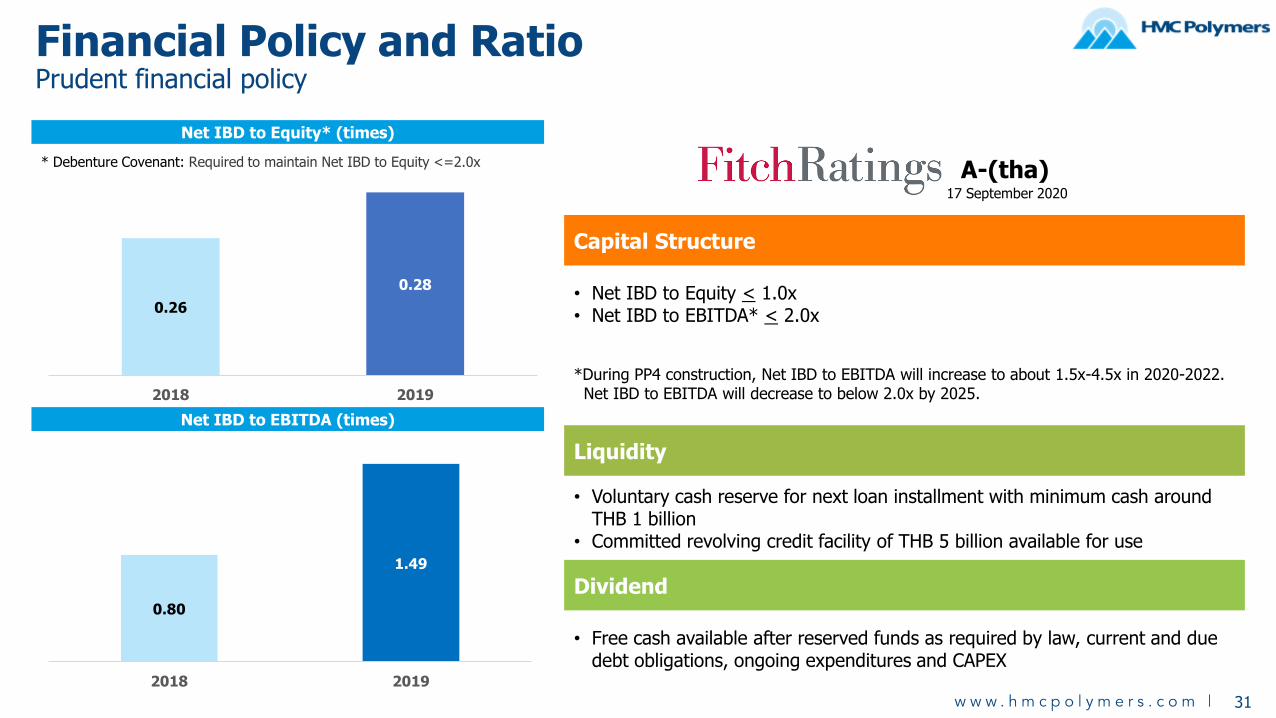

Financial Policy and RatioPrudent financial policy

17 September 2020

Net IBD to Equity* (times)

Net IBD to EBITDA (times)

* Debenture Covenant: Required to maintain Net IBD to Equity <=2.0x

0.80

1.49

2018 2019

Capital Structure

• Net IBD to Equity < 1.0x• Net IBD to EBITDA* < 2.0x

*During PP4 construction, Net IBD to EBITDA will increase to about 1.5x-4.5x in 2020-2022. Net IBD to EBITDA will decrease to below 2.0x by 2025.

Liquidity

• Voluntary cash reserve for next loan installment with minimum cash around THB 1 billion

• Committed revolving credit facility of THB 5 billion available for use

Dividend

• Free cash available after reserved funds as required by law, current and due debt obligations, ongoing expenditures and CAPEX

0.26

0.28

2018 2019

32

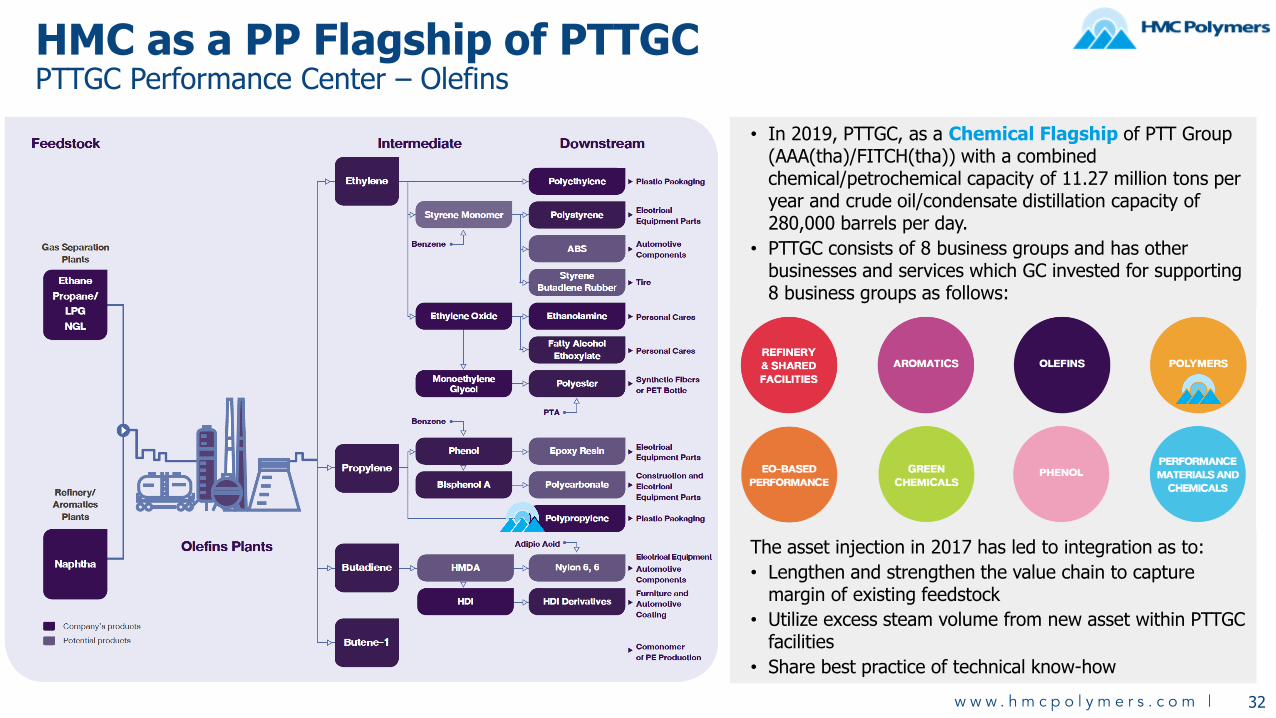

HMC as a PP Flagship of PTTGCPTTGC Performance Center – Olefins

• In 2019, PTTGC, as a Chemical Flagship of PTT Group (AAA(tha)/FITCH(tha)) with a combined chemical/petrochemical capacity of 11.27 million tons per year and crude oil/condensate distillation capacity of 280,000 barrels per day.

• PTTGC consists of 8 business groups and has other businesses and services which GC invested for supporting 8 business groups as follows:

The asset injection in 2017 has led to integration as to:

• Lengthen and strengthen the value chain to capture margin of existing feedstock

• Utilize excess steam volume from new asset within PTTGC facilities

• Share best practice of technical know-how

Today’s Agenda

1. Company Profile

2. Financial Performance

3. Debentures Offering

33

34

Investment Highlights

Focus on High-Value-Added Products:HMC focuses on differentiated and specialty products, which have lower competition and higher margins. The proportion of sales of these products increased to around 46% in 2019 from about 35% in 2015.

Leading Technology and Product Innovation:HMC is the leader in pipe grade and medical grade PP in Thailand, and is the world’s first producer of PP for dielectric film using modern PP technology from LyondellBasell.

Strong Linkage with Shareholders: HMC is a propylene off-taker of PTTGC. PTTGC considers HMC as its key vehicle in the PP business. HMC has a non-compete arrangement with PTTGC. PTTGC and LyondellBasell appoint the majority of HMC's directors and some key management personnel.

A Leader in South-East Asian PP Producer:HMC's capacity will increase to about 1.1 million tonnes per annum by 2022, making it the largest PP producer in the region after its new PP production line 4 is completed.

To be A Most Admired Company andAsia's Preferred Partner

35

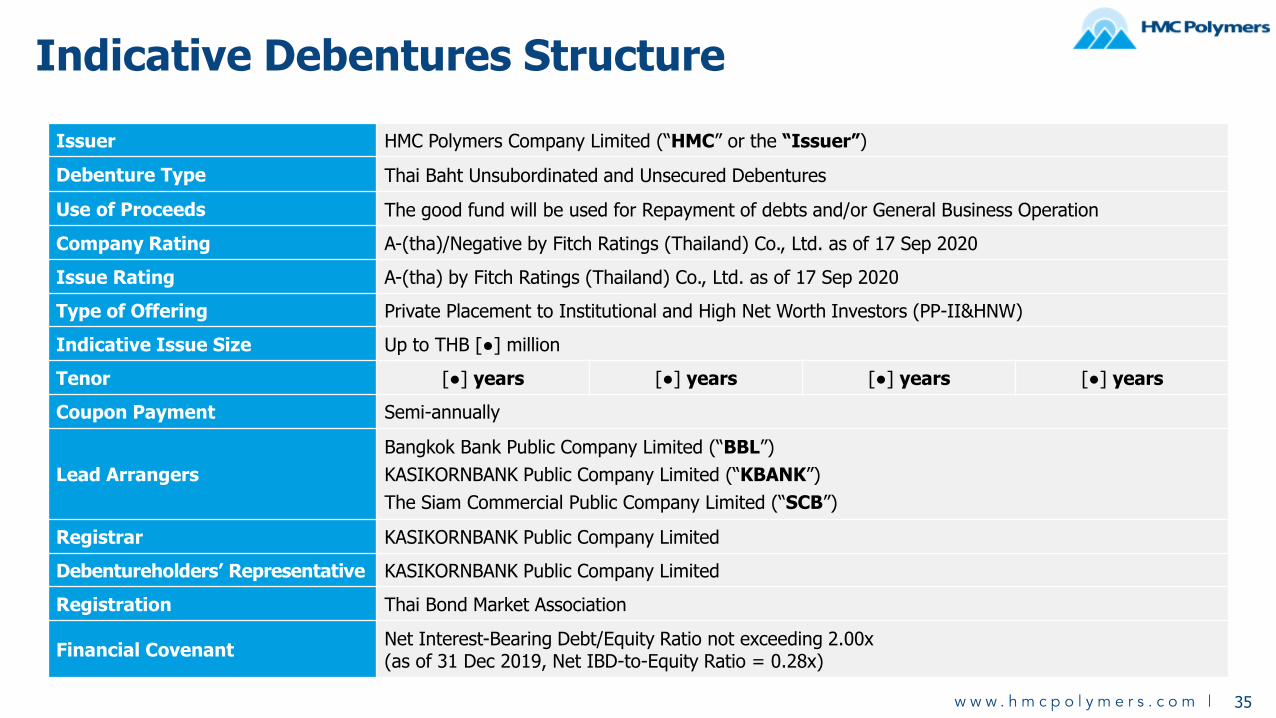

Indicative Debentures Structure

Issuer HMC Polymers Company Limited (“HMC” or the “Issuer”)

Debenture Type Thai Baht Unsubordinated and Unsecured Debentures

Use of Proceeds The good fund will be used for Repayment of debts and/or General Business Operation

Company Rating A-(tha)/Negative by Fitch Ratings (Thailand) Co., Ltd. as of 17 Sep 2020

Issue Rating A-(tha) by Fitch Ratings (Thailand) Co., Ltd. as of 17 Sep 2020

Type of Offering Private Placement to Institutional and High Net Worth Investors (PP-II&HNW)

Indicative Issue Size Up to THB [●] million

Tenor [●] years [●] years [●] years [●] years

Coupon Payment Semi-annually

Lead Arrangers

Bangkok Bank Public Company Limited (“BBL”)

KASIKORNBANK Public Company Limited (“KBANK”)

The Siam Commercial Public Company Limited (“SCB”)

Registrar KASIKORNBANK Public Company Limited

Debentureholders’ Representative KASIKORNBANK Public Company Limited

Registration Thai Bond Market Association

Financial CovenantNet Interest-Bearing Debt/Equity Ratio not exceeding 2.00x (as of 31 Dec 2019, Net IBD-to-Equity Ratio = 0.28x)

36

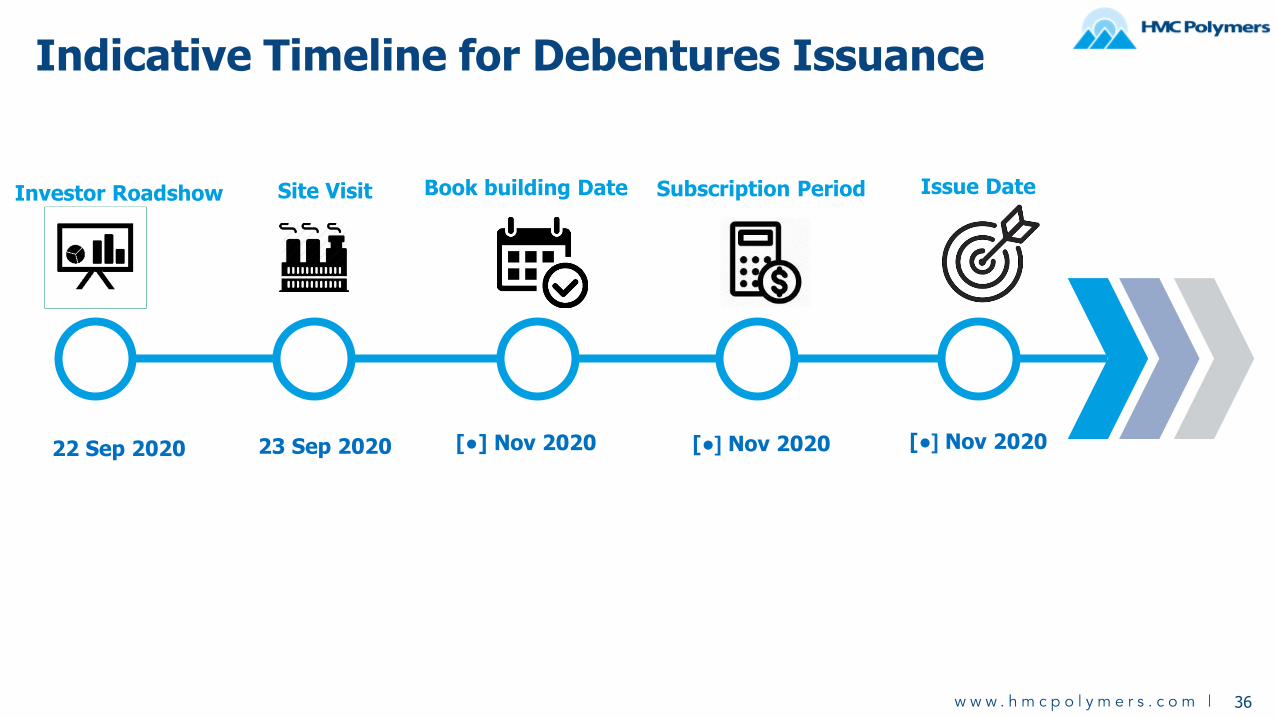

Indicative Timeline for Debentures Issuance

Investor Roadshow

22 Sep 2020

Site Visit

23 Sep 2020

Book building Date

[●] Nov 2020

Subscription Period

[●] Nov 2020

Issue Date

[●] Nov 2020

Disclaimer:

Before using a HMC Polymers product, customers and other users should make their own independent determination that the

product is suitable for the intended use. They should also ensure that they can use the HMC Polymers product safely and legally.

This document does not constitute a warranty, express or implied, including a warranty of merchantability or fitness for a particular

purpose. In addition, no immunity under HMC Polymers’, LyondellBasell's or third parties' intellectual property rights shall be implied

from this document. No one is authorized to make any warranties, issue any immunities or assume any liabilities on behalf of HMC Polymers

except in a writing signed by an authorized HMC Polymers employee. Unless otherwise agreed in writing, the exclusive remedy for all claims is

replacement of the product or refund of the purchase price at HMC Polymers’ option, and in no event shall HMC Polymers be liable for special,

consequential, incidental, punitive or exemplary damages.

Company Confidential

Q&A

Disclaimer:

Before using a HMC Polymers product, customers and other users should make their own independent determination that the

product is suitable for the intended use. They should also ensure that they can use the HMC Polymers product safely and legally.

This document does not constitute a warranty, express or implied, including a warranty of merchantability or fitness for a particular

purpose. In addition, no immunity under HMC Polymers’, LyondellBasell's or third parties' intellectual property rights shall be implied

from this document. No one is authorized to make any warranties, issue any immunities or assume any liabilities on behalf of HMC Polymers

except in a writing signed by an authorized HMC Polymers employee. Unless otherwise agreed in writing, the exclusive remedy for all claims is

replacement of the product or refund of the purchase price at HMC Polymers’ option, and in no event shall HMC Polymers be liable for special,

consequential, incidental, punitive or exemplary damages.

Company Confidential

Thank you