HMRC, CDS Programme Draft Export Tariff Completion Rules Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 1 of 95 Document name: Export Tariff Completion Rules Abstract: The total data element completion rules for export declaration data sets. Please note the formatting of this document has not be revised as this is how it will be officially published. Status: Draft Stability: Document indicate in 'yellow' highlighted text where there are still decisions or answers pending. Team: Customs Directorate Version reference Update Date V5.0 Export Tariff Completion Rules 30/11/17 V0.1 Draft Box Completion Rules 09/06/17

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 1 of 95

Document name: Export Tariff Completion Rules

Abstract: The total data element completion rules for export declaration data sets. Please note the formatting of this document has not be revised as this is how it will be officially published.

Status: Draft

Stability: Document indicate in 'yellow' highlighted text where there are still decisions or answers pending.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 2 of 95

General Notes on Reading Data Element Completion Rules:

Data element overview table

The table shown, at the start of each data item identifies in column:

1. Which types of declaration require the completion of the data element

2. The screen name as it appears on the CDS product

3. The number and type of characters allowed in the data element

4. The number of times the data element may be used at Header level

5. The number of times the data element may be used at Item level

6. The XML data schema path for the data element

For example:

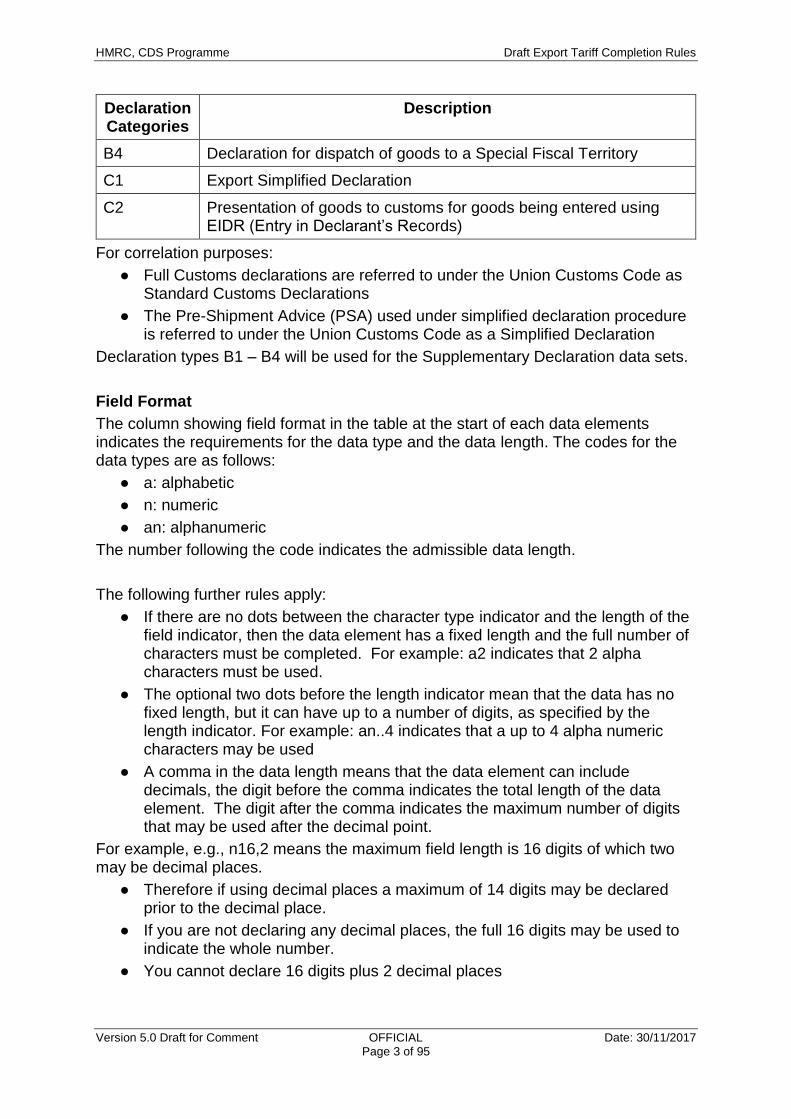

Declaration Categories

Screen name

Field format No. of occurrences

at header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3, B4, C1, C2

a2 1x 99x

XML Data Schema path

Declaration Categories:

The data element completion rules provided in this document indicate for which types of declarations the data element is required, e.g., data element 1/1 needs to be completed for types: C21, A1, A2, A3, B1, B2, B3, B4, C1 and C2

The table below explains which types of declarations these are, for example C1: Export Simplified Declaration

Declaration Categories

Description

C21 (Air) Port inventory release message

A1 Exit Summary Declaration

A2 Exit Summary Declaration for express consignments

A3 Re-export Notification

B1 Export Standard Declaration or Re-export Standard Declaration

B2 Special Procedures –Declaration for Outward Processing

B3 Declaration for Customs Warehousing of Union goods to claim repayment or remission of import duty. To note this declaration type is not currently used in the UK. This type will only be introduced if CAP export refunds are re-introduced.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 3 of 95

Declaration Categories

Description

B4 Declaration for dispatch of goods to a Special Fiscal Territory

C1 Export Simplified Declaration

C2 Presentation of goods to customs for goods being entered using EIDR (Entry in Declarant’s Records)

For correlation purposes:

● Full Customs declarations are referred to under the Union Customs Code as Standard Customs Declarations

● The Pre-Shipment Advice (PSA) used under simplified declaration procedure is referred to under the Union Customs Code as a Simplified Declaration

Declaration types B1 – B4 will be used for the Supplementary Declaration data sets.

Field Format

The column showing field format in the table at the start of each data elements indicates the requirements for the data type and the data length. The codes for the data types are as follows:

● a: alphabetic

● n: numeric

● an: alphanumeric

The number following the code indicates the admissible data length.

The following further rules apply:

● If there are no dots between the character type indicator and the length of the field indicator, then the data element has a fixed length and the full number of characters must be completed. For example: a2 indicates that 2 alpha characters must be used.

● The optional two dots before the length indicator mean that the data has no fixed length, but it can have up to a number of digits, as specified by the length indicator. For example: an..4 indicates that a up to 4 alpha numeric characters may be used

● A comma in the data length means that the data element can include decimals, the digit before the comma indicates the total length of the data element. The digit after the comma indicates the maximum number of digits that may be used after the decimal point.

For example, e.g., n16,2 means the maximum field length is 16 digits of which two may be decimal places.

● Therefore if using decimal places a maximum of 14 digits may be declared prior to the decimal place.

● If you are not declaring any decimal places, the full 16 digits may be used to indicate the whole number.

● You cannot declare 16 digits plus 2 decimal places

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 4 of 95

Examples of field lengths and formats:

● a1: 1 alphabetic character, fixed length

● n2: 2 numeric characters, fixed length

● an3 3 alphanumeric characters, fixed length

● a..4: up to 4 alphabetic characters

● n..5: up to 5 numeric characters

● an..6: up to 6 alphanumeric characters

● n..7,2: up to 7 numeric characters in total including maximum 2 decimals.

Data Groups:

The UCC data elements are grouped in sections:

Group Description

1 Message Information (including Procedure Codes)

2 References of messages, document, certificates and authorisations

3 Parties

4 Valuation information and taxes

5 Dates, times, periods, places, countries and regions

6 Goods identification

7 Transport information (modes, means and equipment)

8 Other data elements (statistical data, guarantees and tariff related data)

Notes

In several cases the following instructions indicate that Data Elements are to be left blank. Some of these data elements may have been completed on declarations arriving from other Member States. Where that is so and they are being used as export declarations in this country the information must be allowed to stand - it must not be deleted or erased.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 6 of 95

All Declaration Categories:

Used to indicate both the type of declaration and if the goods have arrived or not at the goods location. For electronic declarations the code used must be consistent with the CDS transaction being used.

For correlation purposes:

● Full Customs declarations are referred to under the Union Customs Code as Standard Customs declarations

● The Pre-Shipment Advice (PSA) used under simplified declaration procedure is referred to under the Union Customs Code as a Simplified Declaration

Code Type of declaration Goods Arrived or

not

A Standard customs declaration Goods arrived

B Simplified declaration on occasional basis Goods arrived

C Simplified declaration with regular use Goods arrived

D Standard customs declaration Goods not arrived

E Simplified declaration on occasional basis Goods not arrived

F Simplified declaration with regular use Goods not arrived

J C21 Goods arrived

K C21 Goods not arrived

X Supplementary declaration covered by types B and E Goods arrived

Y Supplementary declaration covered by types C and F Goods arrived

Z Supplementary declarations for Entry in Declarants Records

Goods arrived

Notes:

D.E. 1/2 must be left blank on paper declaration continuation sheets when used.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 7 of 95

For Declaration Category C2:

This is the number assigned to the goods in the EIDR records (Entry in Declarant’s Records).

All Declaration Categories:

Number of the item in relation to the total number of items contained in the declaration or notification.

Enter in sequential number order, up to a maximum of 999, the item number.

Notes:

If a declaration is amended and a goods item is removed, the goods item number relating to the removed item cannot be reused.

For example, if on a 12 item declaration, item number 11 is removed in an amendment, then item number 11 cannot be reused for a different goods item on the declaration. Item 12 would also not be re-numbered and remains as item 12.

For paper declarations: Enter the item number (in sequential number order), up to the total declared in D.E. 1/9 (ex-box 5).

D.E. 1/7: Specific Circumstance indicator

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

A2 an3 1x NA

XML Data Schema path

Status of D.E.

Finalised

For Declaration Category A2 only:

Enter code A20 in D.E. 1/7 to indicate that the Exit Summary Declaration relates to Express Consignments.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 8 of 95

D.E. 1/8: Signature / Authentication (Box 54 - place and date, signature and name of the declarant/representative)

Declaration Categories Screen name

Field format No. of occurrences

at header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3, B4, C1, C2

an..35 1x NA

XML Data Schema path

Status of D.E.

Finalised

All Declaration Categories:

Where, as a result of declaration processing, it is determined that customs will accept a declaration without the need for the presentation of the paper copy, the user identity used to lodge a declaration with CDS will replace the hand-written signature as the authentication credential for that declaration.

The CDS role identified by the user identity will determine the liability for all data transmitted in that declaration. In a paperless environment the user identity will have the same legal status as the hand-written signature on the paper declaration.

Individual liability will rest with the signatory within the company for the use of that credential (i.e., the user identity). If there is to be a change of person who will act as signatory, this must be notified immediately to HMRC in writing, whereupon its records will be updated

Where the declarant is completing the declaration themselves under ‘self-representation’, they shall be liable for the content of all declarations so completed and submitted.

Where the declarant is acting as a ‘direct’ representative, in the name of and on behalf of another person, and is transmitting the declaration under the declarant’s own user identity, the declarant must hold (and be able to produce on request to customs) written authority of their powers to act. Failure to do so will result in liability resting with the representative.

Where an agent delegates the making of a declaration to a sub- agent, and the sub-agent makes the declaration in a ‘direct’ capacity, in the name of and on behalf of the first agent, but using the sub-agent’s user identity as the authentication credential; the sub-agent must hold (and be able to produce on request to customs) written authority of their powers to act. Failure to produce written authority will result in liability resting with the sub-agent.

Where the declarant is acting as an ‘indirect’ representative in his/her own name, but on behalf of another person, both parties accept joint and several liability for all data transmitted under the user identity. A declarant failing to state the level of representation on the electronic declaration will be deemed to be acting in his/her own name and on his/her own behalf.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 9 of 95

Where an agent delegates the making of a declaration to a sub- agent, in an ‘indirect’ capacity on behalf of the first agent (but using the sub-agent’s user identity as the authentication credential), then the sub-agent becomes the customs debtor and is jointly and severally liable. The original agent ceases to be a customs debtor because they neither make the declaration nor have responsibility for performing the acts and formalities laid down by customs rules.

The declaration must be signed according to the following rules. If the exporter is:

● An individual, by that individual or an employee who has been authorised in writing

● A partnership, by one of the partners, or one of their employees authorised in writing by a partner

● A company incorporated in the UK under the companies acts, by a director or the secretary, or an employee of the company authorised in writing by a director or the secretary

● A corporation incorporated in the UK by statute, by a person authorised by law to sign for the corporation, or an employee of the corporation authorised in writing by such a person

● A foreign firm or company, or a corporation incorporated abroad by statute, by a person authorised by the law of the country in which the firm or company, is established.

Alternatively, the declaration may be signed on behalf of the exporter by any firm, company or individual to whom the exporter has given the authority to act as a declarant for customs purposes. The manner of authorisation is a matter of arrangement between exporters and their declarant but, in giving authority to a declarant, the exporter will be assumed to have given authority to the clerks and servants authorised by the agent to carry out all of the exporter’s customs business. Customs may at any time require evidence that a declarant has been authorised by an exporter to sign declarations on the exporter’s behalf.

Notes:

Where paper-based declarations are concerned, the original of the handwritten signature of the person concerned must be given on the copy of the declaration which is to remain at the office of export/ dispatch/ import, followed by the full name of that person. Where that person is not a natural person, the signatory should add his capacity after his signature and full name.

In signing D.E. 1/8, a legal declaration is being made that the details shown on the form and any continuation sheets are true and complete and that the requirements of any national or Union legislation have been met.

When a declaration partly completed in another member state is being used as the export declaration, the person signing D.E. 1/8 is committing themselves to the accuracy of all the information on the form, including that which was already completed when they received the document.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 10 of 95

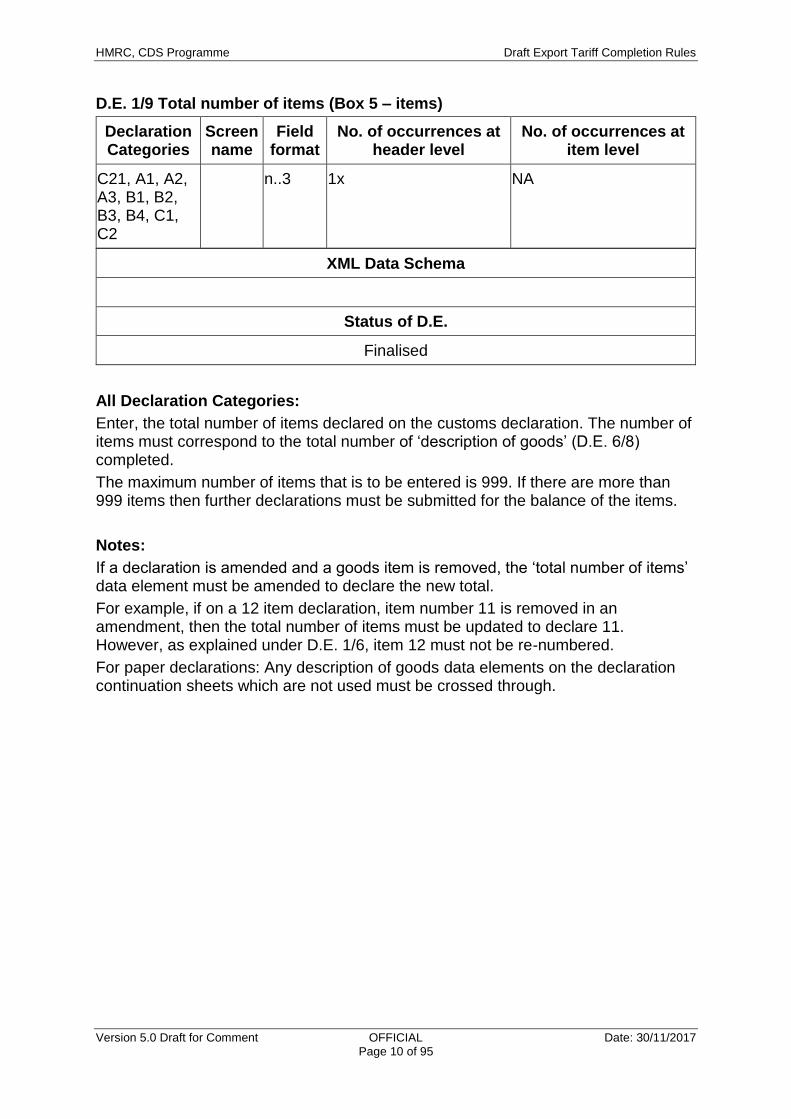

D.E. 1/9 Total number of items (Box 5 – items)

Declaration Categories

Screen name

Field format

No. of occurrences at header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3, B4, C1, C2

n..3 1x NA

XML Data Schema

Status of D.E.

Finalised

All Declaration Categories:

Enter, the total number of items declared on the customs declaration. The number of items must correspond to the total number of ‘description of goods’ (D.E. 6/8) completed.

The maximum number of items that is to be entered is 999. If there are more than 999 items then further declarations must be submitted for the balance of the items.

Notes:

If a declaration is amended and a goods item is removed, the ‘total number of items’ data element must be amended to declare the new total.

For example, if on a 12 item declaration, item number 11 is removed in an amendment, then the total number of items must be updated to declare 11. However, as explained under D.E. 1/6, item 12 must not be re-numbered.

For paper declarations: Any description of goods data elements on the declaration continuation sheets which are not used must be crossed through.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 11 of 95

D.E. 1/10 Procedure (Box 37 – procedure)

Declaration Categories

Screen name

Field format No. of occurrences

at header level

No. of occurrences at item level

C21, B1, B2, B3, B4, C1

an4 Requested procedure code: an2 +

Previous procedure code: an2

NA 1x

XML Data Schema

Status of D.E.

Finalised

All Declaration Categories:

Enter the appropriate (4 digit) Procedure Code from the list in Appendix D.E. 1/10 Procedure Codes, using the relevant procedure code description to help you complete the declaration.

Only one 4 digit procedure code can be declared against each item in D.E. 1/10.

The 4 digit Procedure Code is made up using:

Digits 1 and 2: Requested Procedure Code, e.g., 31 (Re-export)

Procedure Codes may only be declared on the relevant Declaration Category, as defined in the table below. Procedure Codes used on a single customs declaration must all be from the same Declaration Category, for example a Procedure Code from B1 may not be combined with a Procedure Code from B2.

Declaration Category

Declarations Requested Procedure Codes (Digits 1 and 2)

B1 Export declaration and re-export declaration

10, 11, 23, 31

B2 Special procedure — processing — declaration for outward processing

21, 22

B3 Declaration for Customs warehousing of Union goods

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 12 of 95

B4 Declaration for dispatch of goods in the context of trade with special fiscal territories

10

C1 Export Simplified declaration 10, 11, 23, 31

All the items on a declaration for re-export from warehousing must be subject to:

The same Procedure Code in D.E. 1/10 and

Removed from the same warehouse.

Separate declarations are required for goods subject to different warehousing Procedure Codes and/ or removed from different warehouses. The Procedure Code notes explain these restrictions in more detail.

Use of a Procedure Code in this data element constitutes a formal declaration that the conditions of relevant regulations will be complied with and legally binds the declarant accordingly.

Enter the appropriate (3 digit) Additional Procedure Code from the list in Appendix D.E. 1/11 Additional Procedure Codes, using the relevant Additional Procedure Code description to help you complete the declaration.

Up to 99 additional Procedure Codes may be declared against each item in D.E. 1/11. Declarants must follow the guidance on code compatibility in the UK Trade Tariff to prevent incompatible codes being declared, which will result in the rejection of a declaration.

Notes:

All the items on a declaration for re-export from warehousing must be subject to:

The same Procedure Code in D.E. 1/10 and

Removed from the same warehouse.

Separate declarations are required for goods subject to different warehousing D.E. 1/10 Procedure Codes and/ or removed from different warehouses. The D.E. 1/10 Procedure Code notes explain these restrictions in more detail.

Use of an Additional Procedure Code in this data element constitutes a formal declaration that the conditions of relevant regulations will be complied with and legally binds the declarant accordingly.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 15 of 95

First component: Document Category (a1)

The first component (a1) consists of a letter and is used to distinguish between the three categories mentioned below:

● the declaration for temporary storage represented by ‘X’

● the simplified declaration or the entry in the declarant’s records, represented by ‘Y’

● the previous document, represented by ‘Z’. For example: Y Second component: Previous document type (an..3)

The second component (an..3), consists of a combination of digits and/ or letters, serves to identify the type of document:

● Choose the Code from the list in Appendix D.E. 2/1 Simplified Declaration/ Previous Document Code.

For example, code: CLE

Third component: Previous document reference (an..35)

The third component (an..35) represents the data needed to recognise the document. Enter:

● The identification number or another recognisable reference of the document

● Followed by the Declaration UCR (DUCR) as appropriate.

For example, 20171001DUCR7GB000000000000-12345

See notes below for the format of the DUCR.

Fourth component: Goods item identifier (n..3)

The fourth component (n..3) is used to identify which item of the previous document is being referred to:

● The item number of the goods concerned as provided in D.E. 1/6 or the goods item number on the summary declaration or previous document.

For example: 1

The full code for D.E. 2/1 in this example would be YCLE20171001DUCR7GB000000000000-12345-1

Notes:

On paper declarations: the details are separated with a dash in the format <class>-<type>-<reference>-<DUCR>-<goods item number>

If removed from warehouse (other than by EIDR) or IP insert the document identity (for example, Customs export entry reference or DUCR/Part that entered the goods to that regime).

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 16 of 95

For a simplified declaration, enter class code:

X for goods removed from Temporary Storage, or

Z for other document

Followed by:

Type of document

The reference number of the previous document, followed by

The DUCR if appropriate

For an SDP supplementary declaration, enter class code ‘Y’, followed by:

SDE

The CDS simplified declaration entry number

The DUCR

For an EIDR supplementary declaration, enter the class code ‘Y’, followed by:

● Code CLE

● The date of the entry in the EIDR records (the date format should be yyyymmdd)

● The DUCR

References applicable to all items must be entered at header level, with a maximum number of 9,999 instances.

References not applicable to all items should be declared at item level, with a maximum number of 99 instances.

DUCR Completion Rules:

A DUCR and the optional part must be unique, and must comply with the rules and format as detailed in the ‘Format of the DUCR’ section below.

The declaration of a DUCR is mandatory for all NES declarations. The same DUCR must be supplied on all linked declaration parts, e.g., simplified declaration and supplementary declaration.

It is important that traders enter their own declaration UCR numbers into D.E. 2/1 Simplified Declaration/ Previous Document (third component) as these are recognised across the EU and remove the requirement to enter additional references into D.E. 2/4 (Reference Number/ UCR). (TBC)

When printing an EAD the DUCR number in D.E. 2/1 Simplified Declaration/ Previous Document (third component) should be printed into D.E. 2/4 (Reference Number/ UCR) of the paper EAD.

DUCR Part Numbers: TBC

Couriers and fast parcel operators, authorised under the MOU arrangements must supply a DUCR Part.

The declaration of a DUCR Part also enables the CDS system to detect duplicates and so identify potential problems at an early stage.

On supplementary declarations enter the related DUCR Part(s) for the linked simplified declarations(s). If a SD covers more than one simplified declaration, use

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 17 of 95

the DUCR of the first simplified declaration as the DUCR Part for the supplementary declaration.

The DUCR Parts of each of the other simplified declarations are to be declared as separate 9DCS documents.

Format of DUCR

The format of the reference number in the UK is the DUCR, which is created from the following components:

'Year' - is the year in which the DUCR was allocated. For example, '9' if allocated in 2009, '0' if allocated in 2010 and '1' if allocated in 2011. Therefore, for the year 2009, ensure the year component of the DUCR entered onto the Procedure for Electronic Application for Certificates (PEACH) advance notification contains the single '9' digit and not '09'. In 2010, enter the year as a single '0' digit and not '10'.

'Country' - is the country where the DUCR was allocated.

'EORI' - is the identity of the trader as known to HM Revenue & Customs (HMRC). In the UK this is the 12-character EORI number.

'-' - is a dash.

'Reference' - is a unique series of characters that the trader, whose EORI number is included in the DUCR, devises and which provides an audit trail within traders' commercial records. This component of the DUCR is restricted to numbers, upper case letters and certain special characters.

An example DUCR is as follows: ‘7GB000000000000-12345’

This example DUCR would have been issued in 2017, in the UK, for an EORI number ‘000000000000’, and with a trader reference number of ‘12345’.

D.E. 2/2 Additional information

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3,

B4, C1

Coded version (Union codes): an5 n1 + an4 OR (national codes): an5 a1 +an4 +

Free text description: an..507 or 512

NA 99x

XML Data Schema

Status of D.E.

TBC: field length of free text description segment

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 18 of 95

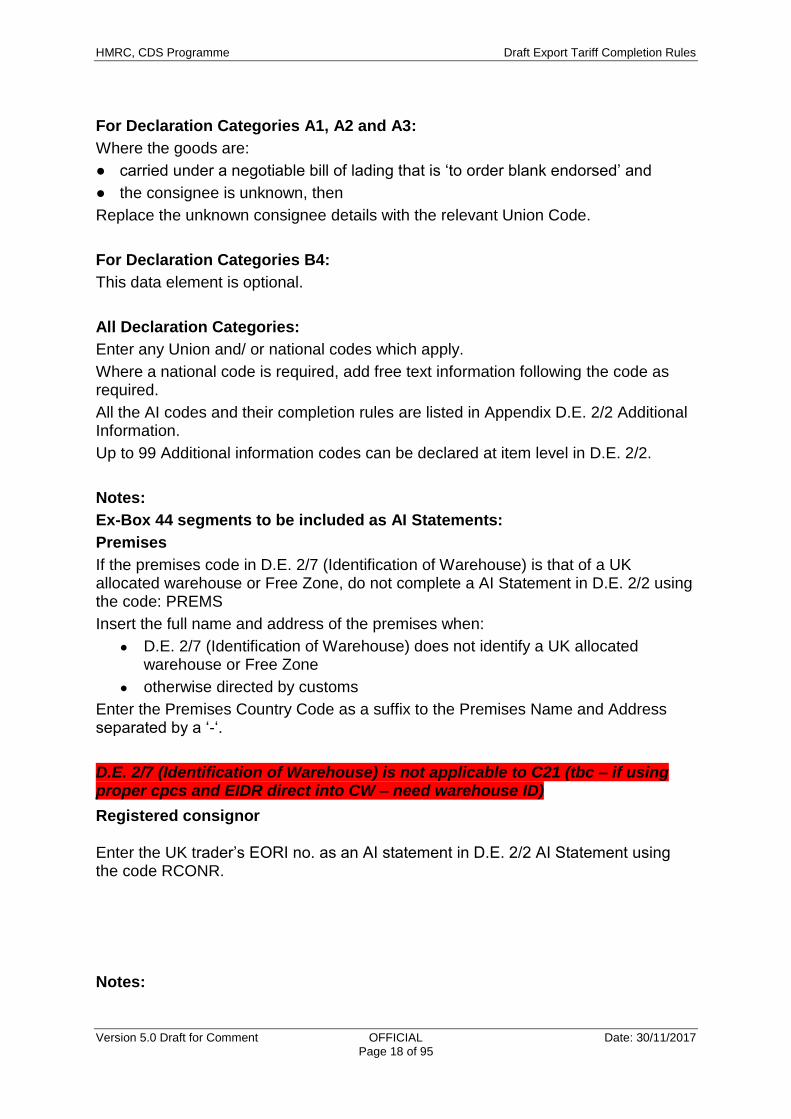

For Declaration Categories A1, A2 and A3:

Where the goods are:

● carried under a negotiable bill of lading that is ‘to order blank endorsed’ and

● the consignee is unknown, then

Replace the unknown consignee details with the relevant Union Code.

For Declaration Categories B4:

This data element is optional.

All Declaration Categories:

Enter any Union and/ or national codes which apply.

Where a national code is required, add free text information following the code as required.

All the AI codes and their completion rules are listed in Appendix D.E. 2/2 Additional Information.

Up to 99 Additional information codes can be declared at item level in D.E. 2/2.

Notes:

Ex-Box 44 segments to be included as AI Statements:

Premises

If the premises code in D.E. 2/7 (Identification of Warehouse) is that of a UK allocated warehouse or Free Zone, do not complete a AI Statement in D.E. 2/2 using the code: PREMS

Insert the full name and address of the premises when:

● D.E. 2/7 (Identification of Warehouse) does not identify a UK allocated warehouse or Free Zone

● otherwise directed by customs

Enter the Premises Country Code as a suffix to the Premises Name and Address separated by a ‘-‘.

D.E. 2/7 (Identification of Warehouse) is not applicable to C21 (tbc – if using proper cpcs and EIDR direct into CW – need warehouse ID)

Registered consignor

Enter the UK trader’s EORI no. as an AI statement in D.E. 2/2 AI Statement using the code RCONR.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 19 of 95

Where a foreign company (for example, one not registered in the UK) takes ownership of goods before export, although the foreign company will be responsible for the export (including obtaining customs clearance of the goods) it is the UK company who has to provide evidence of export to justify zero rating the supply for VAT purposes.

In these situations, to help the UK trader in obtaining this evidence of export, enter the UK traders EORI number (without any GB prefix) in this data element.

Excise Registered Consignor

Enter the Excise Registered Consignor’s identification number (e.g. EORI or other identifier) as an AI statement in D.E. 2/2 AI Statement using the code ECONR.

Notes:

Please refer to Notice 197 for more details

EMCS is an EU wide electronic system for recording and validating movements of duty-suspended excise goods within the EU. Authorised warehouse keepers and registered consignors moving duty-suspended excise goods must register and enrol for EMCS.

The e-AD (ARC) should be entered in D.E. 2/3 as a document code reference using code C651 and the TRANS Code entered in D.E. 2/2 as an AI statement.

D.E. 2/3 Documents produced, certificates and authorisations, additional references and D.E. 8/7 Writing Off

Declaration Categories

Screen name

Field format No. of occurrences

at header level

No. of occurrences at item level

C21, A1, A3, B1, B2, B3,

B4, C1

Document type (Union codes) a1 + an3 OR (national codes): n1 + an3 + Document identifier and part: an..40 + Document Status: a2 +

Reason: an..35 + Issuing authority name: an..70 +

Date of validity: an8 (yyyymmdd) +

Measurement unit and qualifier, if applicable: an..4 +

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 20 of 95

Status of D.E.

TBC – seventh component, location of third quantity

For Declaration Category B1:

D.E 2/3 and 8/7 requirements are combined for the purposes of completing the declaration. The details for writing off are to be declared alongside the document code details as a single data element.

Writing off details are only required on a B1 declaration.

All Declaration Categories:

All the document codes are listed in Appendix D.E. 2/3 Document Code.

D.E. 2/3 can only be declared at item level.

Up to 99 documents produced, certificates and authorisations, additional reference codes can be declared in D.E. 2/3 for each goods item..

Each document code has eight components:

First Component: Document Type Code (an4)

The first component is a 4 figure Document Type Code. See Appendix D.E. 2/3 Document Code for a list of document codes which should be declared in specific circumstances. The Document Code appendix should be read in conjunction with Appendices D.E. 1/10 Procedure Codes and D.E 1/11 Additional Procedure Codes for information on which Document Codes should be used in order to use specific customs procedures.

Second Component: Document Identifier and Part (an..40)

The second component comprises of two sub-components.

Sub-component 1: Document Identifier (an..35)

This sub-component is the document identifier. This is the reference number, as specified against the document type code in Appendix D.E. 2/3 Document Code. This must identify the unique document, authorisation, licence or certificate being declared.

Sub-component 2: Multi Line Document (Document Part) (an..5)

Enter the line item (part) as required for the particular document.

For example, some licences cover many products with each defined as a line. The document part sub-component is used to identify the line number when required.

If omitted it defaults to 1 and the attribution applies to the first (or only) line of the licence.

The line item number of the document is to be appended to the document identifier (completed in the first sub-component) separated by a dash (-).

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 21 of 95

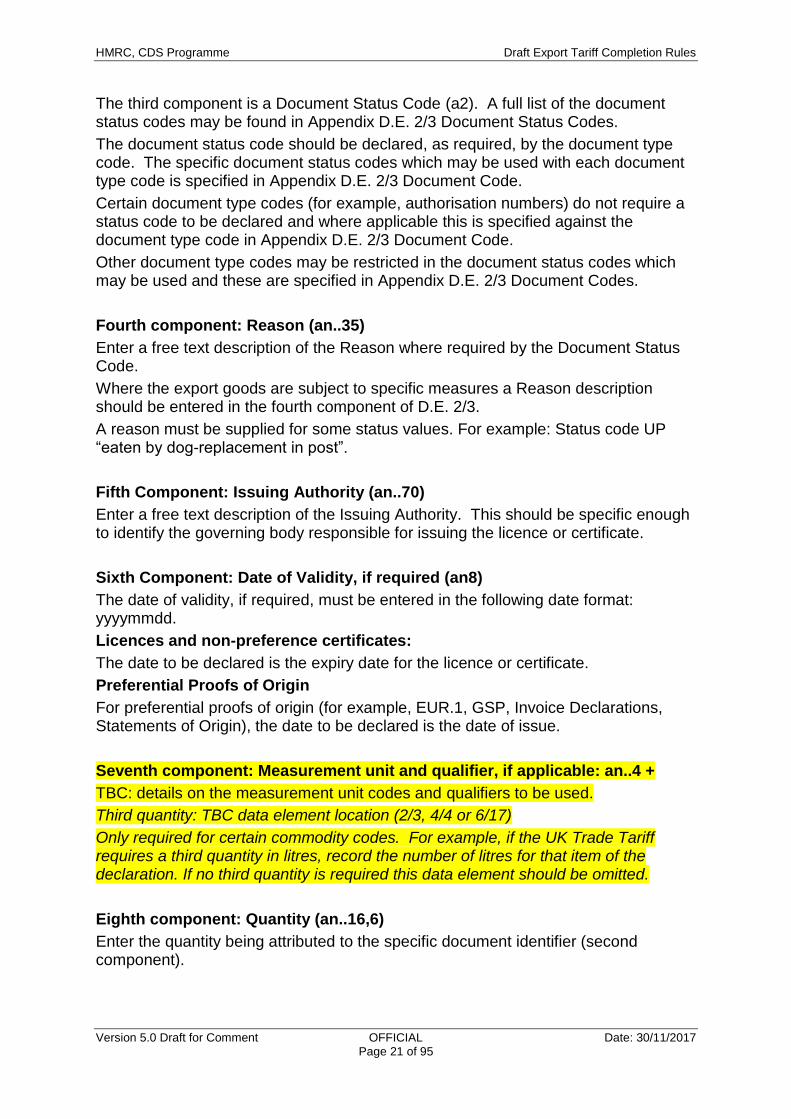

The third component is a Document Status Code (a2). A full list of the document status codes may be found in Appendix D.E. 2/3 Document Status Codes.

The document status code should be declared, as required, by the document type code. The specific document status codes which may be used with each document type code is specified in Appendix D.E. 2/3 Document Code.

Certain document type codes (for example, authorisation numbers) do not require a status code to be declared and where applicable this is specified against the document type code in Appendix D.E. 2/3 Document Code.

Other document type codes may be restricted in the document status codes which may be used and these are specified in Appendix D.E. 2/3 Document Codes.

Fourth component: Reason (an..35)

Enter a free text description of the Reason where required by the Document Status Code.

Where the export goods are subject to specific measures a Reason description should be entered in the fourth component of D.E. 2/3.

A reason must be supplied for some status values. For example: Status code UP “eaten by dog-replacement in post”.

Fifth Component: Issuing Authority (an..70)

Enter a free text description of the Issuing Authority. This should be specific enough to identify the governing body responsible for issuing the licence or certificate.

Sixth Component: Date of Validity, if required (an8)

The date of validity, if required, must be entered in the following date format: yyyymmdd.

Licences and non-preference certificates:

The date to be declared is the expiry date for the licence or certificate.

Preferential Proofs of Origin

For preferential proofs of origin (for example, EUR.1, GSP, Invoice Declarations, Statements of Origin), the date to be declared is the date of issue.

Seventh component: Measurement unit and qualifier, if applicable: an..4 +

TBC: details on the measurement unit codes and qualifiers to be used.

Third quantity: TBC data element location (2/3, 4/4 or 6/17)

Only required for certain commodity codes. For example, if the UK Trade Tariff requires a third quantity in litres, record the number of litres for that item of the declaration. If no third quantity is required this data element should be omitted.

Eighth component: Quantity (an..16,6)

Enter the quantity being attributed to the specific document identifier (second component).

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 22 of 95

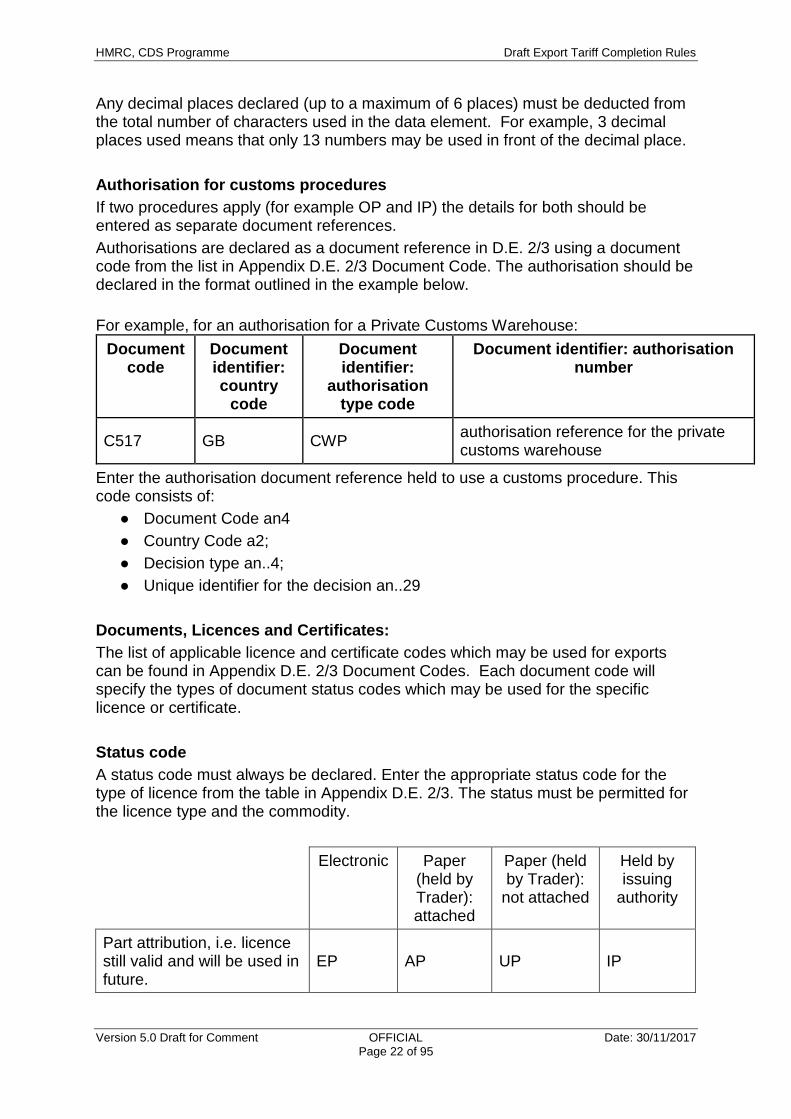

Any decimal places declared (up to a maximum of 6 places) must be deducted from the total number of characters used in the data element. For example, 3 decimal places used means that only 13 numbers may be used in front of the decimal place.

Authorisation for customs procedures

If two procedures apply (for example OP and IP) the details for both should be entered as separate document references.

Authorisations are declared as a document reference in D.E. 2/3 using a document code from the list in Appendix D.E. 2/3 Document Code. The authorisation should be declared in the format outlined in the example below.

For example, for an authorisation for a Private Customs Warehouse:

Document code

Document identifier: country

code

Document identifier:

authorisation type code

Document identifier: authorisation number

C517 GB CWP authorisation reference for the private customs warehouse

Enter the authorisation document reference held to use a customs procedure. This code consists of:

● Document Code an4

● Country Code a2;

● Decision type an..4;

● Unique identifier for the decision an..29

Documents, Licences and Certificates:

The list of applicable licence and certificate codes which may be used for exports can be found in Appendix D.E. 2/3 Document Codes. Each document code will specify the types of document status codes which may be used for the specific licence or certificate.

Status code

A status code must always be declared. Enter the appropriate status code for the type of licence from the table in Appendix D.E. 2/3. The status must be permitted for the licence type and the commodity.

Electronic Paper (held by Trader): attached

Paper (held by Trader):

not attached

Held by issuing

authority

Part attribution, i.e. licence still valid and will be used in future.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 23 of 95

Electronic Paper (held by Trader): attached

Paper (held by Trader):

not attached

Held by issuing

authority

Surrendered, i.e. licence still valid but will not be used in future.

ES AS US IS

Exhausted, i.e. nil balance. EE AE UE IE

Already attributed on simplified declaration.

EA JA UA IA

‘Late’ declaration after licence removed from CHIEF.

EL

Below de minimis. XB XB XB XB

Waiver claimed. XW XW XW XW

Goods covered by the commodity code don’t require a licence (ex-heading).

XX XX XX XX

Where a licence waiver is being claimed please enter XW as status code and details of the waiver claimed in data element 2/2 as an AI statement using the appropriate AI code from Appendix 2/2 AI Statements.

Department for International Trade

The declaration that the goods are subject to the Open General Export Licence is not required except for sensitive goods.

Rural Payments Agency (RPA) Common Agricultural Policy (CAP) export licences and certificates

It is necessary to declare separately the RPA authorisation and the licence/ certificate numbers.

In D.E. 2/2 enter the authorisation code RPTID followed by the RPA Registration Number.

The appropriate document code for the licence/certificate from Appendix D.E. 2/3 Document Codes must be declared with its associated reference number. This will need to be declared as a separate item in D.E. 2/3.

Document Reference/Identifier

All Declaration Categories:

Enter the Document Reference/Identifier, format: an..35.

The Document Reference for a licence is formatted: <country code > < licence type > < licence identifier >.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 24 of 95

Don’t enter any separator or space between the 3 parts. The licence identifier is not supplied when the status identifies that a particular licence is not being declared.

< country code > For all UK government department/agency issued licences/AFCs/ permits (including those which were originally issued in another member state but which were subsequently re-issued - including any ‘extracts’ - by a UK government department/agency) enter ‘GB’.

For licences issued in another member state enter the relevant country code, for example for France enter ‘FR’.

< licence type > as identified in Appendix D.E. 2/3 Document Codes.

< licence identifier > enter the licence identifier allocated by the issuing authority. If the licence does not have a reference enter the title of the licence. A licence identifier is not supplied when the status identifies that a particular licence is not being declared (i.e. status code is in the x-series).

Notes:

Beneficiary countries of the EU GSP will progressively start to apply the REX system, replacing the current system of origin certification based on Form A certificates or invoice declarations for low value consignments with Statements on origin. By 30 June 2020, all exporters who wish to benefit from the GSP preferential tariff treatments will have to make out statements of origin. Refer to the published guidance for more information.

D.E. 2/4 Reference Number (Box 7 - reference number)

Declaration Categories

Screen name

Field format

No. of occurrences at header level

No. of occurrences at item level

C21, A1, B1, B2, B3, B4, C1

an..35 1x 1x

XML Data Schema

Status of D.E.

Finalised

For all export declarations the DUCR must be declared in D.E. 2/1 as part of the Simplified Declaration/ Previous Document Identifier (third component).

For optional use by the declarant to record a commercial reference for their own purposes.

The format of the reference number may take the form of the WCO DUCR, which is created from the following components:

'Year' - is the year in which the DUCR was allocated. For example, '9' if allocated in 2009, '0' if allocated in 2010 and '1' if allocated in 2011. Therefore, for the year 2009, ensure the year component of the DUCR entered onto the Procedure for Electronic Application for Certificates (PEACH)

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 25 of 95

advance notification contains the single '9' digit and not '09'. In 2010, enter the year as a single '0' digit and not '10'.

'Country' - is the country where the DUCR was allocated.

'EORI' - is the identity of the trader as known to HM Revenue & Customs (HMRC). In the UK this is the 12-character EORI number.

'-' - is a dash.

'Reference' - is a unique series of characters that the trader, whose EORI number is included in the DUCR, devises and which provides an audit trail within traders' commercial records. This component of the DUCR is restricted to numbers, upper case letters and certain special characters.

An example DUCR is as follows: ‘7GB000000000000-12345’

This example DUCR would have been issued in 2017, in the UK, for an EORI number ‘GB000000000000’, and with a trader reference number of ‘12345’.

Notes:

This data element can be declared once at header and once at item level.

D.E. 2/5: LRN (No previous reference)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3, B4, C1, C2

an..22 1x NA

XML Data Schema

Status of D.E.

TBC: AEAC replacement message to shut MUCR

All Declaration Categories:

The Local Reference Number at export shall be the MUCR if used. See Notes section below for LRN format to be used where no MUCR applies.

This data element can only be declared once at header level.

Whereas a declaration UCR directly relates to an individual CDS declaration, master UCRs are normally used to associate or link several declaration UCRs. For example, when a container holds a number of consignments from different exporters, each of whom has a DUCR.

Rather than quoting many individual DUCRs for each consignment or consolidators, the inventory systems can advise CDS that each of the Declaration UCRs in the container is associated with a single Master UCR.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 26 of 95

Master UCRs can be associated with other Master UCRs. Although a Master UCR can be associated with one or many Declaration UCRs a Declaration UCR can only belong to one Master UCR.

Association can be done:

at the time of declaration by advising the declaration UCR and master UCR on the declaration

by authorised traders (such as consolidators and inventory systems) on arrival (anticipated and/or actual) at a customs controlled location-by providing the Declaration UCR and Master UCR in the arrival message

by an explicit association transaction through which one can also: o dis-associate a UCR from a Master UCR o associate a Master UCR or Declaration UCR with a (higher level)

The MUCR should only be completed according to the commercial rules for that type of traffic and/or location. It is typically used for groupage/consolidated consignments. For example, in the air environment would normally be the Master/Simple Air Waybill number or for approved courier traffic the CBV (Courier Baggage Voucher) reference.

If no MUCR is known/ applies, the LRN must be completed using the alternative format rules below.

Format of the MUCR

Master UCR (MUCRs) have one of the formats listed below

For Air

Use ‘A’ followed by:

either 3 alpha characters

a maximum of 8 numbers

a maximum length of 13 characters overall

For courier traffic

Use ‘C’ followed by:

3 alpha characters

at least 4 more alphanumeric

The courier MUCR must be at least 8 numbers long.

Other MUCR formats

GB/iii-s…s - GB = country, then followed by 3 characters identifying the inventory system and then at least another 5 alpha/numeric characters (minimum 12 characters in total)

GB/iiii-s…s - same as above yet with 4-character inventory reference (minimum 13 characters in total)

GB/EORI-s…s - GB, followed by the slash, then a valid EORI, hyphen and then at least one alpha or numeric character

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 27 of 95

Notes:

Export declarations where no MUCR applies:

If not in possession of a MUCR, the Local Reference Number should be created from the EORI number and a unique reference/ identifier as shown below:

'EORI' - is the identity of the trader as known to HM Revenue & Customs (HMRC). In the UK this is the two-digit Country Code followed by the12 character EORI number.

'-' - is a dash.

'Reference' - is a unique series of characters that the trader, whose EORI number is included in the LRN, devises and which provides an audit trail within traders' commercial records. This component of the LRN is restricted to numbers, upper case letters and certain special characters.

An example LRN is as follows: ‘GB000000000000-12345’

This example LRN would have been created by a trader with an EORI number ‘000000000000’, and with a trader reference number of ‘12345’.

Notes:

The rules about what other characters are allowed in a MUCR are the same as for DUCR, for example restricted to numbers, upper case letters and certain special characters viz. 0 to 9, A to Z, -, ( and ). If a MUCR is entered, then a DMS message xxxx (TBC AEAC equivalent message) must also be submitted to shut the consolidation once all the declarations have been associated with the MUCR.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 29 of 95

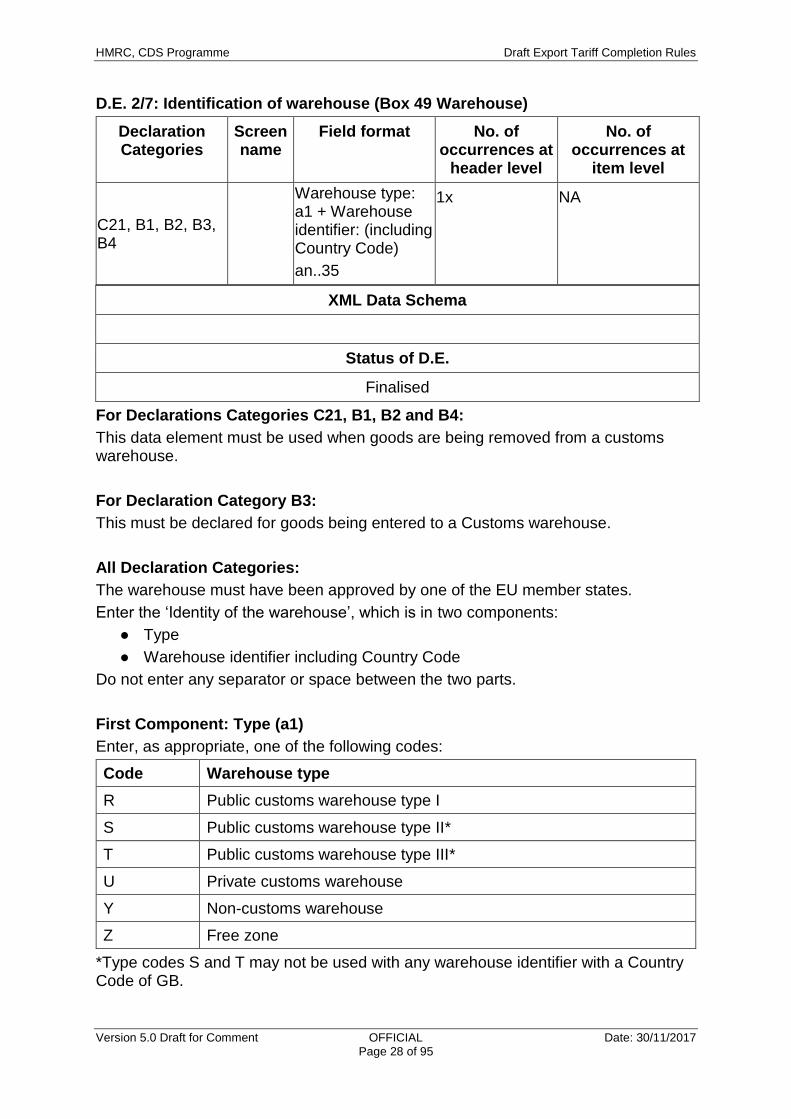

Second Component: Warehouse Identifier (including Country Code) (an..35)

The warehouse identifier consists of two parts:

The identification number for the warehouse issued by the authorising member state

The Country Code for the authorising member state

In the UK:

● customs warehouses have a 7-digit reference ● excise warehouses have a 13-digit reference ● the Free Zone is 0000006 - Isle of Man

If the warehouse identity is not a UK allocated code (suffixed by ‘GB’), the premises name and address must be supplied as an AI Statement in D.E. 2/2 Additional Information, using AI code ‘PREMS’.

Notes:

An example of a Customs Warehouse Identification reference number is R1234567GB:

Where R denotes a Type I public warehouse

1234567 denotes the authorisation number for the warehouse

GB denotes the authorising Member State

An example of an Excise warehouse identity is YGB00001234567GB:

Where Y denotes a non-customs warehouse

GB00001234567 is the 13-character excise warehouse identifier

GB denotes the authorising Member State

Group 3-Parties

D.E. 3/1 Exporter Name and Address (Box 2 - consignor/exporter)

Declaration Categories

Screen names

Field format No. of occurrences

at header level

No. of occurrences at item level

C21, A1, A2, A3, B1, B2, B3, B4, C1

Name: an..70 + Street and number: an..70 + Country: a2 + Postcode: an..9 +

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 30 of 95

All Declaration Categories:

The details of the exporter (as defined in Article 1(19) of the Delegated Regulation 2015/2446) are to be entered in D.E. 3/1.

The exporter name and address, and their identity details, if known, are to be provided.

Box 2 (Consignor/ Exporter) is now covered under six different data elements under CDS.

D.E 3/1 is used to declare the Exporter’s name and address and postcode. This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/2.

If the Exporter identifier reference number (EORI) quoted in D.E. 3/2 is recognised by CDS, then D.E. 3/1 should not be completed.

Name and address

Enter the full name and address of the exporter, including the postcode. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

Notes:

Exporter is defined (in Article 1(19) of the Delegated Regulation 2015/2446) as:

● the person established in the customs territory of the Union who, at the time when the declaration is accepted, holds the contract with the consignee in the third country and has the power for determining that the goods are to be brought to a destination outside the customs territory of the Union,

● the private individual carrying the goods to be exported where these goods are contained in the private individual’s personal baggage,

● in other cases, the person established in the customs territory of the Union who has the power for determining that the goods are to be brought to a destination outside the customs territory of the Union.

For paper and C21 declarations: only one exporter is to be declared.

For all other declarations:

If there is only one exporter then the exporter details are to be supplied at header level.

If there is more than one exporter then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual exporter details must be supplied at item level (one exporter per item).

Read about the completion rules for the multiple consignor procedure.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 31 of 95

D.E. 3/2 Exporter Identification Number (Box 2 - consignor/exporter)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at item level

C21, B1, B2, B3, B4, C1

an..17 1x 1x

XML Data Schema

Status of D.E.

Finalised

All Declaration Categories:

Enter the identification number (EORI) of the exporter (as defined in Article 1(19) of the Delegated Regulation 2015/2446) in D.E. 3/2

Where a valid EORI number is provided in D.E. 3/2, the exporters’ name and address does not need to be completed in D.E. 3/1.

Where the exporter does not have an EORI number, the customs administration may assign an ad hoc number for the declaration concerned.

For MoU approved fast parcel traders, insert GB888888811005 when details of individual exporters do not have to be supplied.

Notes:

For paper and C21 declarations: only one exporter is to be declared.

For all other declarations:

If there is only one exporter then the exporter details are to be supplied at header level.

If there is more than one exporter then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual exporter details must be supplied at item level (one exporter per item). Read about the completion rules for the multiple consignor procedure.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 32 of 95

D.E. 3/7 Consignor Name and Address (Box 2: Consignor/ Exporter)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

C21, A1, A2,

Name: an..70 +

Street and number: an..70 +

Country: a2 +

Postcode: an..9 +

City: an..35

1x 1x

XML Data Schema

Status of D.E.

Finalised

Declaration Categories A1 and A2:

This data element must be provided when the Consignor (D.E. 3/7) is different from the Declarant (D.E. 3/17).

When D.E. 3/7 is completed on the details must match those declared in D.E. 3/1 (Exporter).

Declaration Category C21:

The Consignor’s name and address, and their identity details, if known, are to be provided.

All Declaration Categories:

Box 2 (Consignor/ Exporter) is now covered under six different data elements under CDS.

D.E 3/7 is used to declare the Consignor’s name and address and postcode. This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/8.

If the Consignor’s identifier reference number (EORI) quoted in D.E. 3/8 is recognised by CDS, then D.E. 3/7 should not be completed.

Name and address

Enter the full name and address of the consignor, including the postcode. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

Notes:

For paper and C21 declarations: only one exporter is to be declared.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 33 of 95

If there is only one consignor then the consignor’s details are to be supplied at header level.

If there is more than one consignor then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual consignor details must be supplied at item level (one consignor per item). Read about the completion rules for the multiple consignor procedure.

D.E. 3/8 Consignor Identification Number (Box 2: Consignor/ Exporter)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at item level

C21, A1, A2 an..17 1x 1x

XML Data Schema

Status of D.E.

Finalised

Declaration Categories A1 and A2:

This data element must be provided when the Consignor Identification Number (D.E. 3/8) is different from the Declarant Identification Number (D.E. 3/18).

When D.E. 3/8 is completed on the details must match those declared in D.E. 3/2 (Exporter Identification Number).

Declaration Category C21:

Enter the identification number (e.g., EORI) of the party who is consigning the goods, in D.E. 3/8.

All Declaration Categories:

Box 2 (Consignor/ Exporter) is now covered under six different data elements under CDS.

Where a valid EORI number is provided in D.E. 3/8, the consignor’s name and address does not need to be completed in D.E. 3/7.

Where the consignor does not have an EORI number, the customs administration may assign him an ad hoc number for the declaration concerned.

For specifically MoU approved fast parcel traders insert GB888888811005 when details of individual consignors do not have to be supplied.

Notes:

For paper and C21 declarations: only one consignor is to be declared.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 34 of 95

If there is only one consignor then the consignor’s details are to be supplied at header level.

If there is more than one consignor then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual consignor’s details must be supplied at item level (one consignor per item). Read about the completion rules for the multiple consignor procedure.

D.E. 3/9 Consignee Name and Address (Box 8 - consignee)

Declaration Categories

Screen names

Field format No. of occurrences at

header level

No. of occurrences at

item level

C21, A1, A2, B1, B2, B3, B4, C1

Name: an..70 +

Street and number: an..70 +

Country: a2 +

Postcode: an..9 +

City: an..35 +

1x 1x

XML Data Schema

Status of D.E.

Draft: Confirm MoU completion of AI code 00200 in Notes

All Declaration Categories:

Box 8 (Consignee/ Importer) is now covered under six different data elements under CDS.

Enter the consignee’s name and address, and their identity details, if known.

This is the party to whom the goods are consigned/ shipped.

D.E 3/9 is used to declare the consignee’s name and address and postcode. This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/10.

Name and Address

Enter the full name and address of the consignee, including the postcode. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

If the Consignee’s identifier reference number (EORI) quoted in D.E. 3/9 is recognised by CDS, then D.E. 3/10 should not be completed.

Notes:

For paper and C21 declarations only one consignee is to be declared.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 35 of 95

For all other declarations, if there’s only one consignee then the consignee’s details are to be supplied at header level.

If there is more than one consignee then consignee details are to be supplied at item level.

If there is more than one consignee then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual consignee details must be supplied at item level (one consignee per item).

You need to be aware that:

● if the consignee is not known, enter the details of the firm or company responsible for taking delivery of the goods

● for traders authorised under the fast parcel MoU, or if directed by CPC instructions, consignee details can be supplied by entering 00200 in lieu of the name, street, city and postcode details and enter the country of ultimate destination of the goods in D.E. 5/8 (Country of Destination)

D.E. 3/10 Consignee Identification Number (Box 8 - consignee number)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at item level

C21, A1, A2, B1, B2, B3, B4, C1

an..17 1x 1x

XML Data Schema

Status of D.E.

Finalised

Declaration Category B3:

Where goods are subject to export refunds are entered to a customs warehouse, the EORI number of either:

● the person claiming the export refund or

● the ware housekeeper may be declared.

All Declaration Categories:

Enter the identification number of the party to whom the goods are consigned/ shipped. Where a valid EORI number is provided in D.E. 3/10, the consignee’s name and address should not be completed in D.E. 3/9.

Where a unique identification number is issued under third country trading partnership programmes that number may be declared in D.E. 3/10.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 36 of 95

Notes:

The identity of a consignee is a combination of the country code of the issuing country, and the identity reference allocated by that country. The identity reference must take the following form:

● agency code (an..3) as listed in UN/EDIFACT 3055

● consignee Identification code (an..13)

For example, JP1511234567890 for a Japanese consignee (country code: JP) whose identification number with Japanese customs (Agency Code 151) is 1234567890.

For paper and C21 declarations: only one consignee is to be declared.

For all other declarations:

If there is only one consignee then the consignee details are to be supplied at header level.

If there is more than one consignee then Additional Information Code 00200 is to be quoted in D.E. 2/2 and the individual consignee details must be supplied at item level (one consignee per item).

D.E. 3/15 Importer Name and Address (Box 8 - consignee)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

Name: an..70 +

Street and number: an..70 +

Country: a2 +

Postcode: an..9 +

City: an..35+

1x NA

XML Data Schema

Status of D.E.

Finalised

This data element is not used for (re)export purposes.

This data element is not used for (re)export purposes.

D.E. 3/17 Declarant Name and Address (Box 14 - declarant/representative)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

C21, B1, B2, B3, B4, C1

Name: an..70 + Street and number: an..70 + Country: a2 + Postcode: an..9 +

City: an..35

1x NA

XML Data Schema

Status of D.E.

Finalised

Box 14 (Declarant/ Representative) is now covered under five different data elements under CDS.

All Declaration Categories:

D.E 3/17 is used to declare the Declarant’s name and address and postcode. This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/18.

If the Declarant’s identifier reference number (EORI) quoted in D.E. 3/18 is recognised by CDS, then D.E. 3/17 should not be completed.

If the declarant’s identity has been entered in D.E. 3/18, then the full name and address of the declarant must be entered in D.E. 3/17 if:

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 38 of 95

●

Name and Address

Enter the full name and address of the Declarant, including the postcode. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

Notes:

This data element may only be declared once at header level.

Enter the appropriate code (see below) in D.E. 2/2 (Additional information), if, for example:

● Declarant and Exporter are the same, code 00400 is to be used. ● Declarant and Consignor are the same, code 00300 is to be used

On paper declarations: Enter the full name and address of the person or company concerned, and the telephone number of the signatory.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 39 of 95

Notes:

This data element may only be declared once at header level.

Where a sub-agent, acting as a direct representative (DR), is completing a NES declaration (Simplified declaration and/or Supplementary Declarations) on behalf of a NES authorised trader acting as an indirect representative (IR), the identity of the IR must be entered in D.E. 3/19 or 3/20 (box 14) and the sub-agent’s identity must be entered in D.E. 2/2 (Additional Information) using code: GEN46 followed by the sub-agents identification number.

D.E. 3/19 Representative Name and Address (Box 14 - declarant/representative and Box 50: Principal’s Representative)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

C21, B1, B2, B3, B4, C1

Name: an..70 + Street and number: an..70 + Country: a2 + Postcode: an..9 +

City: an..35 +

1x NA

XML Data Schema

Status of D.E.

Finalised

Box 14 (Declarant/ Representative) is now covered under five different data elements under CDS.

All Declaration Categories:

This information shall only be required if the Representative is different from D.E. 3/17 Declarant Name and Address.

This data element must be completed with the details of the Representative who will be responsible for the customs formalities at the Office of Exit where this differs from the Declarant declared in D.E. 3/17.

D.E 3/19 is used to declare the Representative’s name and address and postcode. This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/20.

If the Representatives identifier reference number (EORI) quoted in D.E. 3/20 is recognised by CDS, then D.E. 3/19 should not be completed.

If the Representative’s identity has been entered in D.E. 3/19, then the full name and address of the declarant must be entered in D.E. 3/20 if:

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 40 of 95

● it is a paper declaration.

Name and Address

Enter the full name and address of the Representative, including the postcode. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

Notes:

This data element may only be declared once at header level.

Where a sub-agent, acting as a direct representative (DR), is completing a NES declaration (Simplified declaration and/or Supplementary Declarations) on behalf of a NES authorised trader acting as an indirect representative (IR), the identity of the IR must be entered in D.E. 3/19 or 3/20 (box 14) and the sub-agent’s identity must be entered in D.E. 2/2 (Additional Information) using code: GEN46 followed by the sub-agents identification number.

On paper declarations: Enter the full name and address of the person or company concerned, and the telephone number of the signatory.

Box 14 (Declarant/ Representative) is now covered under five different data elements under CDS.

All Declaration Categories:

This information shall only be required if the Representative is different from D.E. 3/18 Declarant’s Identification Number.

This data element must be completed with the details of the Representative who will be responsible for the customs formalities at the Office of Exit where this differs from the Declarant declared in D.E. 3/18.

Enter the identification number (EORI) of the Representative (as defined in Article 18 of the Union Customs Code, EU Reg. No. 952/2013) in D.E. 3/20.

Where a valid EORI number is provided in D.E. 3/20, the Representative’s name and address does not need to be completed in D.E. 3/19.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 41 of 95

Where the Representative does not have an EORI number, the customs administration may assign an ad hoc number for the declaration concerned.

Notes:

This data element may only be declared once at header level.

Where a sub-agent, acting as a direct representative (DR), is completing a NES declaration (Simplified declaration and/or Supplementary Declarations) on behalf of a NES authorised trader acting as an indirect representative (IR), the identity of the IR must be entered in D.E. 3/19 or 3/20 (box 14) and the sub-agent’s identity must be entered in D.E. 2/2 (Additional Information) using code: GEN46 followed by the sub-agents identification number.

D.E. 3/21 Representative Status Code (Box 14 - declarant/representative)

Declaration Categories

Screen name

Field format

No. of occurrences at

header level

No. of occurrences at

item level

C21, A1, A2, A3, B1, B2, B3, B4, C1, C2

n1 1x NA

XML Data Schema

Status of D.E.

Finalised

Declaration Categories A1, A2 and A3:

This data element is not optional for these Declaration Categories under the Union Customs Code.

All Declaration Categories:

Enter the relevant code showing the status of the representative:

This data element must be completed, other than in the case of self-representation. Enter one of the following codes:

Code Representation

2 Direct representation

3 Indirect representation

Notes:

Any person may appoint a representative (agent) to perform the acts and formalities laid down by customs rules.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 42 of 95

A customs representative shall be established within the customs territory of the Union, except where the customs representative acts upon behalf of persons who are not required to be established within the customs territory of the Union.

Direct representation

Where an agent is acting as a ‘direct’ representative, in the name and on behalf of another person - the ‘declarant’, the agent must hold (and be able to produce on customs request), written authority of their powers to act as the declarant’s representative. Failure to produce written authority will result in liability resting with the agent.

Where an agent delegates the making of a declaration to a sub- agent and the sub-agent makes the declaration in a ‘direct’ capacity, in the name and on behalf of the first agent, the sub- agent must hold (and be able to produce on request to customs) written authority of their power to act. Failure to produce written authority will result in liability resting with the sub-agent.

Indirect representation

Where the declarant is acting as an ‘indirect’ representative in their own name, but on behalf of another person, both parties accept joint liability for all information provided.

Where an agent delegates the making of a declaration to a sub- agent in an indirect capacity on behalf of the first agent, then the sub-agent becomes the customs debtor. The original agent ceases to be a customs debtor because they neither make the declaration nor have responsibility for performing the acts and formalities laid down by customs rules.

D.E. 3/24 Seller Name and Address (Box 2: Consignor/ Exporter)

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

Name: an..70 +

Street and number: an..70 +

Country a2+

Postcode: an..9 +

City: an..35 +

Phone number: an..50

1x 1x

XML Data Schema

Status of D.E.

Finalised

This data element is not required for (re)export purposes.

This data element is not used for (re)export purposes.

D.E. 3/31: Carrier Name and Address

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

A1, A2, A3,

Name: an..70 +

Street and number: an..70 +

Country: a2 +

Postcode: an..9 +

City: an..35 +

Phone number: an..50

1x NA

XML Data Schema

Status of D.E.

Finalised

All Declaration Categories:

This information is only required where the Carrier is different from the Declarant (as declared in D.E. 3/17). Where the Carrier is different, the details of the Carrier are to be entered in D.E. 3/31.

D.E 3/31 is used to declare the Carrier’s name and address, postcode and phone number.

If the Carrier’s identifier reference number (EORI) quoted in D.E. 3/32 is recognised by CDS, then D.E. 3/31 should not be completed.

This D.E should only be completed where a recognised EORI number is not held and declared in D.E. 3/32.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 45 of 95

Enter the full name and address of the Carrier, including the postcode and phone number. Where a country does not use a postcode or equivalent code, (e.g. US zip code), enter ‘NA’ in this data element.

Notes:

This data element may only be declared once at header level.

D.E. 3/32: Carrier Identification number

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

A1, A2, A3, an..17 1x NA

XML Data Schema

Status of D.E.

Finalised

All Declaration Categories:

Enter the identification number (EORI) of the Carrier in D.E. 3/32.

Where a valid EORI number is provided in D.E. 3/32, the Carrier’s name and address does not need to be completed in D.E. 3/31.

Where the Carrier does not have an EORI number, the customs administration may assign an ad hoc number for the declaration concerned.

Notes:

This data element may only be declared once at header level.

Where a unique identification number is issued under third country trading partnership programmes that number may be declared in D.E. 3/32.

If used, enter the unique identification number assigned to an economic operator of a third country in the framework of a trade partnership programme developed in accordance with the World Customs Organization Framework of Standards to Secure and Facilitate Global Trade which is recognised by the European Union.

This data element comprises of two components:

First Component: Role Code (a..3)

Enter the role code specifying their role in the supply chain. The following parties can be declared:

Role Code

Party Description

CS Consolidator

Freight forwarder combining individual smaller consignments into a single larger consignment (in a consolidation process) that is sent to a counterpart who mirrors the consolidator’s activity by dividing the consolidated consignment into its original components

MF Manufacturer

Party which manufactures goods

FW Freight Forwarder

Party undertaking forwarding of goods

WH Warehouse Keeper

Party taking responsibility for goods entered into a warehouse

Second Component: Identification number of the party (an..17)

This should be an EORI number issued by a Member State, or a third country unique identifier recognised by the EU.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 48 of 95

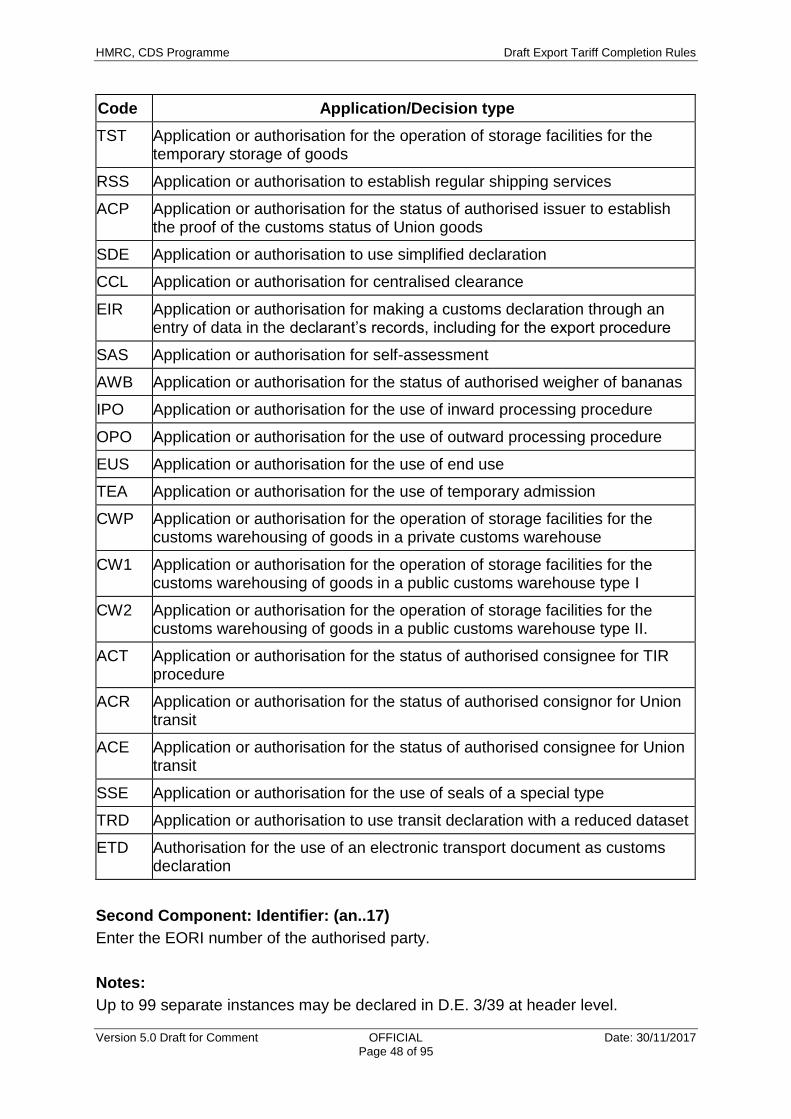

Code Application/Decision type

TST Application or authorisation for the operation of storage facilities for the temporary storage of goods

RSS Application or authorisation to establish regular shipping services

ACP Application or authorisation for the status of authorised issuer to establish the proof of the customs status of Union goods

SDE Application or authorisation to use simplified declaration

CCL Application or authorisation for centralised clearance

EIR Application or authorisation for making a customs declaration through an entry of data in the declarant’s records, including for the export procedure

SAS Application or authorisation for self-assessment

AWB Application or authorisation for the status of authorised weigher of bananas

IPO Application or authorisation for the use of inward processing procedure

OPO Application or authorisation for the use of outward processing procedure

EUS Application or authorisation for the use of end use

TEA Application or authorisation for the use of temporary admission

CWP Application or authorisation for the operation of storage facilities for the customs warehousing of goods in a private customs warehouse

CW1 Application or authorisation for the operation of storage facilities for the customs warehousing of goods in a public customs warehouse type I

CW2 Application or authorisation for the operation of storage facilities for the customs warehousing of goods in a public customs warehouse type II.

ACT Application or authorisation for the status of authorised consignee for TIR procedure

ACR Application or authorisation for the status of authorised consignor for Union transit

ACE Application or authorisation for the status of authorised consignee for Union transit

SSE Application or authorisation for the use of seals of a special type

TRD Application or authorisation to use transit declaration with a reduced dataset

ETD Authorisation for the use of an electronic transport document as customs declaration

Second Component: Identifier: (an..17)

Enter the EORI number of the authorised party.

Notes:

Up to 99 separate instances may be declared in D.E. 3/39 at header level.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 51 of 95

B1, B2

Union codes: a1 + n2

OR

National codes:

n1 + an2

NA 99x

XML Data Schema

Status of D.E.

Draft

All Declaration Categories:

The CDS system will populate this data element based upon the data declared elsewhere in the declaration, as required for CAP export refunds and CAP export licences.

This data element does not need to be completed by the Exporter/ Declarant.

For reference purposes, a list of tax type codes may be found in Appendix D.E. 4/3 Tax Type Codes.

D.E. 4/4: Calculation of taxes – Tax Base (Box 47b Tax Base)

Declaration Categories

Screen name

Field format No. of occurrences at header

level

No. of occurrences at item level

B1, B2, B3

Measurement unit and qualifier, if applicable: an..6 + Quantity: n..16,6

NA 99x

XML Data Schema

Status of D.E.

Draft

This data element does not require completion for (re)export purposes.

All Declaration Categories:

The CDS system will populate this data element based upon the data declared elsewhere in the declaration, as required for CAP export refunds and CAP export licences.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 52 of 95

Declaration Categories

Screen name

Field format No. of occurrences at

header level

No. of occurrences at

item level

B1, B2, n..17,3 NA 99x

XML Data Schema

Status of D.E.

Draft

This data element does not require completion for (re)export purposes.

All Declaration Categories:

The CDS system will populate this data element based upon the data declared elsewhere in the declaration, as required for CAP export refunds and CAP export licences.

This data element does not require completion for (re)export purposes.

All Declaration Categories:

The CDS system will populate this data element based upon the data declared elsewhere in the declaration, as required for CAP export refunds and CAP export licences.

Notes:

If a claim to a CAP Export Refund is made then CDS will show an estimate of the amount of potential CAP. This does not constitute a statement or guarantee that this is what will be paid, it is a figure provided for information only and does not take into account various factors about the circumstances of the export.

The final amount to be paid (if any) is entirely a matter for the RPA.

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 53 of 95

Further information about these requirements is contained in Notice 780.

D.E. 4/7: Calculation of taxes – Total

Declaration Categories

Screen name

Field format

No. of occurrences at

header level

No. of occurrences at item level

B1, B2 n..16,2 NA 1x

XML Data Schema

Status of D.E.

Draft

This data element does not require completion for (re)export purposes.

All Declaration Categories:

The CDS system will populate this data element based upon the data declared elsewhere in the declaration, as required for CAP export refunds and CAP export licences.

D.E. 4/8: Calculation of taxes – Methods of Payment (MOP) (Box 47e MOP)

Declaration Categories

Screen name Field format

No. of occurrences at

header level

No. of occurrences at

item level

B1, B2 a1 NA 99x

XML Data Schema

Status of D.E.

Draft – MOP code to be used for CAP export refunds TBC

This data element must only be completed for (re)export purposes when submitting a CAP export refund claim for the sole purpose of releasing security on a CAP export licence.

All Declaration Categories:

Enter method of payment code ‘L’. In all other cases leave blank.

D.E. 4/9 Additions and Deductions (Box 45 – adjustment)

Version 5.0 Draft for Comment OFFICIAL Date: 30/11/2017 Page 54 of 95

Code: a2 +

Amount: n..16,2 99x 99x

XML Data Schema