A step-by-step guide on how I represent you in the home buying process.

10

A GUIDE TO THE HOME BUYING PROCESS Finding the right home, in the perfect neighborhood and at a cost that is within your budget is no small task. That’s were I come in. As your Realtor®, I am committed to diligently seeking out potential homes for you, thoroughly researching your top candidates, and advocating strongly on your behalf to ensure you secure your next home at the best possible price. Making Sense of the Data. There’s lot’s of information available—on the web, in books and through friends—to assist you in your home search. So much that it’s sometimes overwhelming. I can help you navigate though the data, understand the relevant aspects and have clarity around the process and what to expect. •Knowledge. •Advocacy. •Experience.

Transcript

A GUIDE TO THE HOME BUYING PROCESS

Finding the right home, in the perfect neighborhood and at a cost that is within your budget is no small task. That’s were I come in. As your Realtor®, I am committed to diligently seeking out potential homes for you, thoroughly researching your top candidates, and advocating strongly on your behalf to ensure you secure your next home at the best possible price.

Making Sense of the Data. There’s lot’s of information available—on the web, in books and through friends—to assist you in your home search. So much that it’s sometimes overwhelming. I can help you navigate though the data, understand the relevant aspects and have clarity around the process and what to expect.

• Knowledge.

• Advocacy.

• Experience.

Peruse Homes and Neighborhoods. It’s helpful to start your search on a broad scale so that you become familiar with all of the options. You’ll quickly define style, floor plans and communities that resonate with you.

Explore the Market. Knowing data and the current offer environment help you become a better informed buyer and successfully compete in today’s market. I have the tools to help you make the best decisions.

Identify Mortgage Parameters. Meet with local mortgage lenders to find out what the best home loan programs for you are. This helps you evaluate options ahead of time and a lender “pre-approval” letter is a must have in today’s market.

RESEARCH. EXPLORE. PONDER.

• Neighborhood.

• Floor Plans & Styles.

• Condition.

• Price.

Define Criteria. Once you have clarity about the type of home, neighborhood and price range you are looking for, it helps to create a list of your “must have” and “nice to have” criteria for your new home and reevaluate it often through the search process.

Look at Homes that Meet Your Criteria. Together, we’ll scour the market to make sure you don’t miss anything. We’ll see potential homes and identify candidates for purchase. We will adjust criteria as needed based upon the knowledge you gain along the way.

The Top 3. We’ll keep a running Top 3 list of the homes that best fit your wants and needs. No home will be perfect, but if it meets most of your criteria, it might be worthy of consideration. We can then evaluate the facts and data to make a solid decision.

FINDING THE RIGHT HOME

Research and Review. We’ll thoroughly research and review your Top 3, including looking over the seller’s property disclosure statement (Form 17) to ensure you know about any known defects and accessing public records and permit history. I’ll relay any questions you may have to the seller’s broker for a response.

Consider Pre-Inspections. If you find yourself competing for the best homes in today’s multiple offer environment, you might give your offer a significant boost by conducting a pre-inspection of the home and eliminating your inspection contingency altogether. Based on the age of the home and potential concerns you may have, I’ll recommend further evaluation by professionals as appropriate (i.e. oil tank certification, sewer scopes, geo-tech surveys, etc.)

INVESTIGATE THE DETAILS

Supplemental Pieces. In additional to preparing a well-written agreement, I’ll outline the major components of your offer and highlight its strengths in a cover letter. Many buyers also opt to include a personal letter to the seller telling a little about themselves and why they chose to make on offer on the seller’s home. Sometimes this personal touch makes all the difference as most sellers would rather make a concession for a buyer they like.

Price. Before writing your offer, I’ll do a market evaluation to determine value so you can make knowledgeable decisions and avoid paying too much.

Contingencies. I will review optional clauses, financing, appraisal, inspection, and title contingencies with you and explain how they work. I’ll help you determine what you need to protect your interests.

Strategy. I’ll advise you on how to best structure a competitive offer based on your purchase objectives, and discuss strategy alternatives, so that I can best represent you at the offer presentation.

Evaluations. If not done already, I’ll recommend further evaluation by professionals as appropriate (i.e. oil tank certification, sewer scopes, geo-tech surveys, etc.)

OFFER CONSIDERATIONS

The Offer. You’ll sign the offer and write an earnest money check (typically 1-3% of the price) to show good faith. If possible, I’ll present your offer in person—creating a professional impression and personally explaining the merits of your offer.

Seller Decision. The seller can accept your offer, counter it, or reject it. In a multiple offer situation, the seller will typically chose to counter the strongest offer first.

Counteroffer Process. The most typical seller response is a counteroffer—which might address major hurdles such as a gap in price or minor tweaks such as a change in timing.

Buyer Decision. After evaluating the seller’s counteroffer, your choices are to accept it, counter it back, or reject it. I’ll walk you through the process and communicate your decision to the seller’s broker.

Mutual Acceptance. Mutual acceptance occurs when the buyer and seller have agreed, in writing, to all contract terms and signed documents are delivered to the other party with no further changes. Verbal agreements show a parties intent but are not legally binding.

Potential detours. If the seller accepts a different offer, or you decide this isn’t the right home to pursue, go back to your Top 3 or look at homes again until you find one you would be interested in making an offer on.

THE NEGOTIATION PROCESS

Loan Application. Make formal loan application (typically within 5 days) to meet the requirements of the financing contingency. Missing this deadline may put your earnest money at risk if you can’t get your loan…unless, of course, you are paying all cash!

Appraisal. An independent appraiser hired by the

lender visits the property to conduct an appraisal and verify the sales price

matches current values.

Title Review. You will receive a title report from the title insurance company. Together with the title officer, you’ll verify the property has no liens or encumbrances that would affect title.

Inspection. If you didn’t conduct a pre-inspection, you’ll schedule home inspection with a

licensed professional home inspector who works on your behalf to determine safety

and structural issues that would affect your ownership.

Information Verification. This contingency allows you to verify the

seller’s statements through public records, neighbors, or document review.

Evaluations and Insurance. Any professional evaluations you opted to have would be done at this time (i.e. oil tank certification, sewer scopes, geo-tech surveys, etc.). This is also a good time to call your insurance broker for a binder.

Now that you have come to terms with the seller, it’s time to conduct your due diligence under the contract. I’ll create a timeline checklist to provide clarity over what needs to

happen and when. Here are some of the typical contingencies that need to be addressed.

CONDUCTING YOUR DUE DILIGENCE

Piece of Mind. A big part of my job is providing you information to make sound decisions, making you aware of your rights and options, and managing the process so nothing is overlooked. Through each contingency and evaluation, I’ll help you prepare the appropriate notices and walk you through the options, protocol and process so you know exactly what to expect. Then I’ll timely communicate those notices to the seller’s broker and keep you informed of the status every step of the way.

• Financing

• HOA Review

• Verification

• Appraisal

• Lead Paint

• Utilities

• Inspection

• Feasibility

• Insurance

• Evaluation

• Title Review

• Form 17

NAVIGATING THE PROCESS

Your Advocate Every Step of the Way. When the unexpected complication arises, I’ll help you understand your options, communicate your decisions to the seller’s broker, and negotiate a resolution or termination based on your wishes. The bottom line: I want you to be happy in your home for years to come and I’d like you to think of me as your real estate resource for life. My goal isn’t to make a quick sale, it’s to help you secure the right home for your needs.

Evaluation concerns

Title issues Low appraisal

Financing challenges

WORKING THROUGH ISSUES

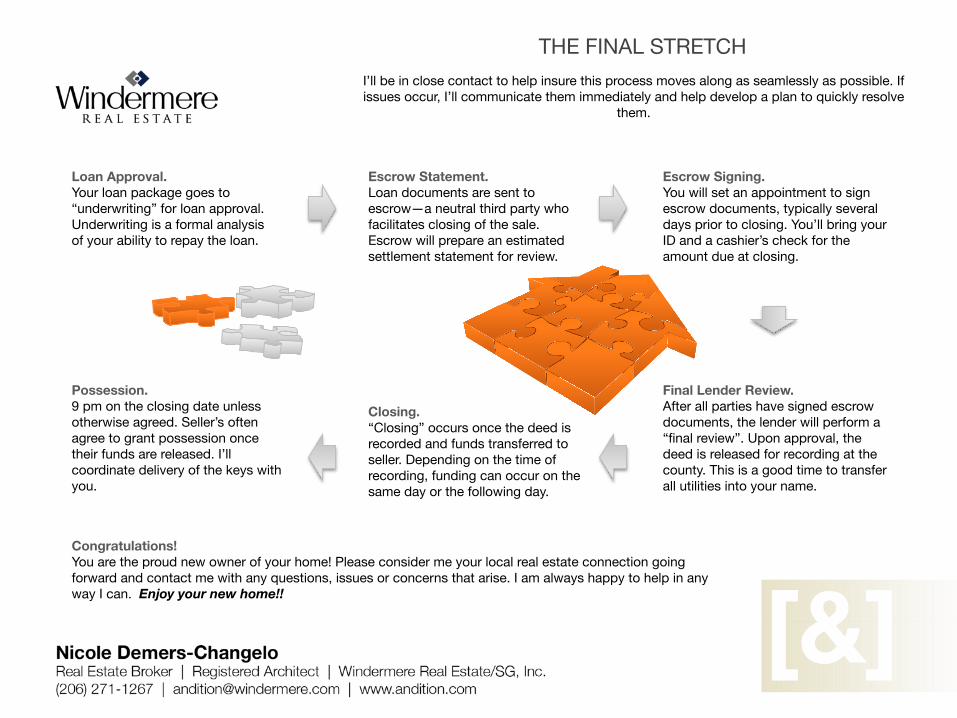

Loan Approval. Your loan package goes to “underwriting” for loan approval. Underwriting is a formal analysis of your ability to repay the loan.

Escrow Signing. You will set an appointment to sign escrow documents, typically several days prior to closing. You’ll bring your ID and a cashier’s check for the amount due at closing.

Escrow Statement. Loan documents are sent to escrow—a neutral third party who facilitates closing of the sale. Escrow will prepare an estimated settlement statement for review.

I’ll be in close contact to help insure this process moves along as seamlessly as possible. If issues occur, I’ll communicate them immediately and help develop a plan to quickly resolve

them.

THE FINAL STRETCH

Final Lender Review. After all parties have signed escrow documents, the lender will perform a “final review”. Upon approval, the deed is released for recording at the county. This is a good time to transfer all utilities into your name.

Closing. “Closing” occurs once the deed is recorded and funds transferred to seller. Depending on the time of recording, funding can occur on the same day or the following day.

Possession. 9 pm on the closing date unless otherwise agreed. Seller’s often agree to grant possession once their funds are released. I’ll coordinate delivery of the keys with you.

Congratulations! You are the proud new owner of your home! Please consider me your local real estate connection going forward and contact me with any questions, issues or concerns that arise. I am always happy to help in any way I can. Enjoy your new home!!