Home Firm Performance After ForeignInvestments and Divestitures

Dirk Engel1,2 and Vivien Procher2,31University of Applied Sciences Stralsund, Stralsund, 2Rheinisch-Westf€alisches Institut f€ur

Wirtschaftsforschung (RWI), Essen, and 3Jackst€adt Center of Entrepreneurship and Innovation Research,

Schumpeter School of Business and Economics, University of Wuppertal, Wuppertal

1. INTRODUCTION

EXPORTING and foreign direct investment (FDI) can be seen as alternative strategies to

serve foreign markets, and thus, switching from export to FDI might reduce home-based

export activities. Consequently, policymakers worry that FDIs imply a significant relocation

of jobs from home to host countries. However, existing papers do not provide substantial

empirical confirmation for any negative effects of FDI on home employment (e.g. Barba

Navaretti and Castellani, 2008; Becker and Muendler, 2008; Desai et al., 2009). Therefore,

this paper investigates the extent to which the FDI – export relationship can illuminate this

trend. Among others Head and Ries (2004) argue that the location of different stages of pro-

duction in different countries (i.e. vertical specialisation) and home centralisation of certain

products may matter for firms which in turn would point towards a positive association

between FDI and exporting.

Based on a large database for French firms and applying propensity score matching com-

bined with a difference-in-difference (DiD) estimator, we show that FDI and exporting often

constitute complementary activities. To the authors’ knowledge, there is no study that analy-

ses the FDI – export relationship and the relationship between FDI and domestic employment

simultaneously. While this relationship is not homogeneous across firms, any study should

address the important role of moderating factors like industry affiliation. We provide some

empirical evidence by differentiating between firms in high-tech and low-tech industries. The

imitation of knowledge-intensive products might have great consequences for the comparative

advantage of firms in high-tech industries, so that the latter might be more inclined to opt for

vertical specialisation and home centralisation of production processes. In contrast, firms in

low-tech industries might prefer to substantially replicate and relocate production process to

low-cost countries. As a result, we expect export activity of firms in high-tech industries are

affected to a larger extent by the FDI decision than firms in low-tech industries.

While many empirical studies analyse the role of investments and acquisitions on home

plant performance, we fail to detect any study which addresses the effects of divesting from

abroad on home firm employment, turnover and export activity. The meta-analysis of Lee and

Madhavan (2010) clearly confirms this research gap. Existing papers focus either on financial

accounting measures (e.g. return on investment) or stock price changes due to foreign divesti-

tures announcements. Driven by the globalisation of production processes, divestitures have

We would like to thank the anonymous referee who gave precise and helpful comments on an earlierversion sent to The World Economy. Furthermore, we appreciated the comments and suggestions madeby Christoph M. Schmidt. The financial support by the Ruhr Graduate School in Economics is gratefullyacknowledged.

become increasingly relevant in the last few decades. Moreover, business restructuring due to

the financial and economic crisis since 2008 will further raise the likelihood of divestitures in

the years to come. By analysing both the effects of investing abroad and divesting from

abroad, we finally provide a comprehensive analysis on the home performance of firms after

stepping in and out of foreign markets.

The remainder of the paper is organised as follows: Section 2 contains a brief review of

the FDI and divestiture literature with respect to firm performance. Section 3 describes the

data and methodological approach. Results are presented in Section 4. Section 5 presents the

conclusions drawn.

2. BACKGROUND

a. Effects of Investing Abroad

The debate of home market effects from FDI is often linked to the actual type of FDI.

Resource-seeking FDI might affect home plant output and employment negatively and pro-

ductivity positively in the short term, as some production processes are relocated to exploit

cost advantages at the foreign location. In the long term, however, positive effects on output

and employment based on reducing the cost of production may dominate which then allows

product prices to decrease and, thus, could induce higher demand at home. Furthermore,

extensive intra-firm trade between headquarters and foreign affiliates might curtail negative

effects of (partial) relocation when the firm prefers to concentrate some production stages

abroad (see Head and Ries, 2004).

Market-driven FDI with self-contained foreign production units might substitute some

home-based export activities so that domestic employment decreases. However, multinational

enterprises (MNEs) who concentrate on market-driven FDI are likely to exploit economies of

scale by accessing new markets, which in turn may have positive effects on the productivity

at home. Similarly, firms also experience performance gains through their exposure in foreign

markets (see the learning-by-exporting hypothesis e.g. Bernard and Jensen, 1999; Wagner,

2007; meta-analysis by Martins and Yang, 2009).

Recent empirical studies analyses intensively the effects of investing abroad on home

plant’s performance. Based on the extensive use of propensity score matching combined with

a DiD approach in the microeconometric programme evaluation (Heckman et al., 1998), this

kind of estimator has also received increasing attention in the FDI literature. Barba Navaretti

and Castellani (2008) apply this estimator and find significant positive effects of outward FDI

by Italian MNEs on turnover and productivity (TFP) at home, but the effect on employment

is insignificant. Based on a small sample of 47 German MNEs, Kleinert and Toubal (2007)

also observe an insignificant effect on employment and a significant increase in TFP in the

first year after investing abroad. J€ackle and Wamser (2010) use the same database and apply

Heckman’s (1978) parametric estimator for endogenous treatment effects. They find signifi-

cant positive effects of FDI on TFP for German MNEs up to three years after going abroad.1

For Japanese MNEs, Hijzen et al. (2007) observed a weak significant positive effect on

domestic factory TFP in the initial year and significant positive effects on output and employ-

1 Interestingly the OLS estimates are downward biased in this study which suggests that no significantdifferences in TFP growth and employment growth exist.

provide a more comprehensive understanding of average employment effects after foreign

divestitures.

3. DATA AND EMPIRICAL METHOD

a. Panel Structure

This paper utilises firm-level data from the European AMADEUS database which is

provided by Bureau van Dijk (BvD). The data collection by BvD is carried out by coun-

try-specific information providers, for example the credit insurer Coface Scrl in France.

These providers use published sources including annual reports and stock exchange infor-

mation. In addition, they contact companies directly to handle collection orders from com-

panies’ business partners (e.g. banks). The coverage ratio of AMADEUS data is 73.5 per

cent related to total sales of Sirene register which covers all French companies (see

INSEE, 2012).

Companies’ financial records are available for up to 10 years but information on the own-

ership and subsidiary structure is static and based on the latest annual report available in the

year of data compilation. Dynamics in the (foreign) subsidiary network can only be analysed

via the various updates of the AMADEUS database. We have access to six updates and focus

on changes in the international status of companies that take place between the years 2000

and 2002, 2002 and 2004, as well as 2005 and 2007, respectively. Consequently, we analyse

the post-entry and post-exit domestic performance of French exporters and MNEs that chan-

ged their status in 2001, 2003 or 2006.

Our data set is limited to unconsolidated firm-level accounts to analyse location- and

entity-specific performance effects. The data set includes companies of a wide range of

manufacturing and service industries.2 Table 1 provides an overview of the underlying

panel structure. The overall panel is unbalanced as the latest year for which key financial

data are available is 2010. Given the underlying data structure, the short-term analysis

(t + 1 and t + 2) is based on a larger sample of firms than the long-term analysis (t + 5

and t + 6).

We differentiate between two types of changers with exporting firms that become engaged

in FDI (i.e. new MNEs, DX-DI) and MNEs that divest all foreign affiliates to become pure

exporters (DI-DX). The number of observations, as depicted in Table 2, is obtained via probit

estimations with variables taken from the pre-change periods. In sum, the number of exporters

going abroad is much larger (884) than the number of MNEs that cease their foreign opera-

tions (279). In the majority of cases, a large pool of potential control firms (non-changers)

exists, which is a prerequisite for finding a comparable firm for each treated observation in

the subsequent matching procedure.

The number of firms used in the matching procedure and DiD analysis can be further

reduced if key performance variables are missing in the post-change period. Consequently,

the number of observations depends on the type of change, the year of change and the specific

2 Excluded from the analysis are the following industries (with the industry codes (NACE) in parenthe-ses): Agriculture, hunting and forestry (01, 02), fishing (05), mining and quarrying (10–14), managementactivities of holding companies (7,415), public administration and defence, compulsory social security(75) and activities of membership organisations (91). Values in the upper and lower 1st percentile of thedistribution are eliminated from the dataset in order to control for outliers and coding errors.

Notes:(i) Changes in the internationalisation status can occur between 2000 and 2002, 2002 and 2004, 2005 and 2007, wherethe first year refers to the pre-change period (t�1). For example, firms in the DX-DI group with the pre-change year2000 were exporters (DX) in 2000 who became multinational enterprises (DI) by 2004. (ii) The number of observa-tions is obtained from probit models on pre-change variables. (iii) The control groups refer to the potential number offirms that can function as control observations in the matching procedure. (iv) ‘Total’ refers to firm-year observations.

3 In principle there are 36 different sample sizes due to two changing modes (upward D/DX-DI anddownward DI-DX/D), three changing years (2001, 2003 and 2006) and six outcome variables (exportturnover, export share, number of employees, operating turnover, labour productivity and TFP). Valuesin the upper and lower 1st percentile of the distribution are eliminated from the dataset in order to con-trol for outliers and coding errors.

the propensity score matching to construct the sample of adequate control firms with the DiD

estimator (e.g. Heckman et al., 1998, 1999; Blundell and Costa Dias, 2000, 2002) to estimate

the average treatment effect on the treated (ATT).

As the number of observables used in the matching process increases, it becomes rather

difficult to find a suitable match for every firm; furthermore, every unmatched firm is tanta-

mount to data loss. The propensity score method suggested by the pioneer work of Rosen-

baum and Rubin (1983) constitutes a helpful solution by computing the probability of mode

change conditional on observables by applying a logit or probit estimation. We implement a

nearest neighbour matching with replacement to match each treated firm with one non-treated

firm with the closest probability of mode change.4 This procedure implies that a non-treated

firm can be matched to more than one treated firm. Therefore, a correction for standard errors

to draw conclusions on statistical inference is required. We follow Lechner (2001) and apply

his estimator for an asymptotic approximation of the standard errors.

When the matching method is completed, we can then apply DiD estimator to calculate

the ATT as follows:

ATTDiD ¼ E½Y1i;tþk � Y1

i;t�1� � E½Y0i;tþk � Y0

i;t�1�:The DiD estimator evaluates the average performance E½Y1

i;tþk � Y1i;t�1� of treated firms

between the year before (t�1) and k years after a mode change against the average perfor-

mance E½Y0i;tþk � Y0

i;t�1� for matched non-treated firms.

c. Outcome and Control Variables

All firm-specific state variables used in the probit model to explain changes in the mode of

internationalisation are taken from the pre-change period, t�1. Many theoretical and empirical

papers (e.g. Roberts and Tybout, 1997; Helpman et al., 2004) emphasise the important role of

basic firm characteristics like the number of employees, operating revenue, age and productiv-ity for bearing the sunk costs of investing abroad. We further include previous export turnoverand export share (export to total operating turnover), which might approximate international

experience and attractiveness of foreign markets. The productivity measures used in the probit

models refer to labour productivity, defined as operating revenue per employee. All these

quantitative variables are included as values in logarithm.5

A growing number of studies point out that multiunit and multinational characteristics as

well as ownership characteristics can also affect firm’s mode of internationalisation (e.g.

Roper et al., 2006; Bernard and Jensen, 2007; Greenaway et al., 2007). Therefore, firms’

ownership structure is used as a proxy for underlying strategic interests of its owners and is

captured by the dummy variables corporate shareholder, financial shareholder, state share-holder, individual shareholder and foreign shareholder for non-French investors. Only owners

with an ownership share of 10 per cent or more are taken into account to assure an effective

4 The matching procedure is carried out using software package psmatch2 in STATA 12 (see Leuvenand Sianesi, 2003).5 In previous estimations we also took into account the growth rate of employees, productivity and(export) turnover to check for the role of firm’s growth path. Since we detect no significant coefficientestimates for growth rates we decided to leave out these variables in the final estimations to prepare ourmatched samples.

voice in the management of a firm. The organisational structure is further accounted for by

the number of domestic subsidiaries.Financially constrained firms might be less likely to enter (Chaney, 2005) and more likely

to leave foreign markets. Companies can fail to finance their internationalisation because of a

liquidity shortage. Thus, following recent empirical papers on foreign market participation

(Greenaway et al., 2007; Stiebale, 2011), we include a liquidity ratio defined as the difference

of current assets and current liabilities to total assets.

Markusen (1995) highlights the positive correlation between the importance of intangible

assets in industries and the economic importance of MNEs. The ratio of intangible fixed assets to

tangible fixed assets is used as a proxy for the knowledge capital because no direct information is

available on corporate R&D expenses. Finally, up to 28 industry dummies based on the two-digit

NACE classifications attempt to capture any remaining industry-specific heterogeneity.

For evaluating the post-entry as well as post-exit performance, we concentrate on six out-

come variables. The main variables of interest are export share (i.e. export to total operating

revenue) and export turnover to analyse the extent to which exports serve as substitutes or

complements of FDI. Additionally, employment, operating revenue, labour productivity and

total factor productivity are taken into account.6 With exception of the export share, we com-

pute and compare growth rates of variables between the treatment and non-treatment group.

The computation of growth rates follows Evans (1987) approach by assuming an exponential

growth trend. Annual average growth rates are calculated as the difference between the loga-

rithm of outcome variables in any year t + k (with k � 1) and the pre-switching year t�1,divided by the number of years between t + k and t�1.

4. RESULTS

Separate probit regressions are carried out for each switching mode and year to obtain

matched samples of treated and suitably non-treated firms. In sum, we fail to detect any

significant differences between both groups of firms before the treated firms change the mode

of internationalisation.7 This in turn allows interpreting differences in outcome variables as

result of switching the mode of internationalisation.

a. Investing Abroad

The results from the DiD estimation for treated firm, which invest abroad for the first time,

are presented in Tables 3 and 4. The number of firm observations decreases over time as

complete outcome records are not available for all post-change periods.8 Our main variables

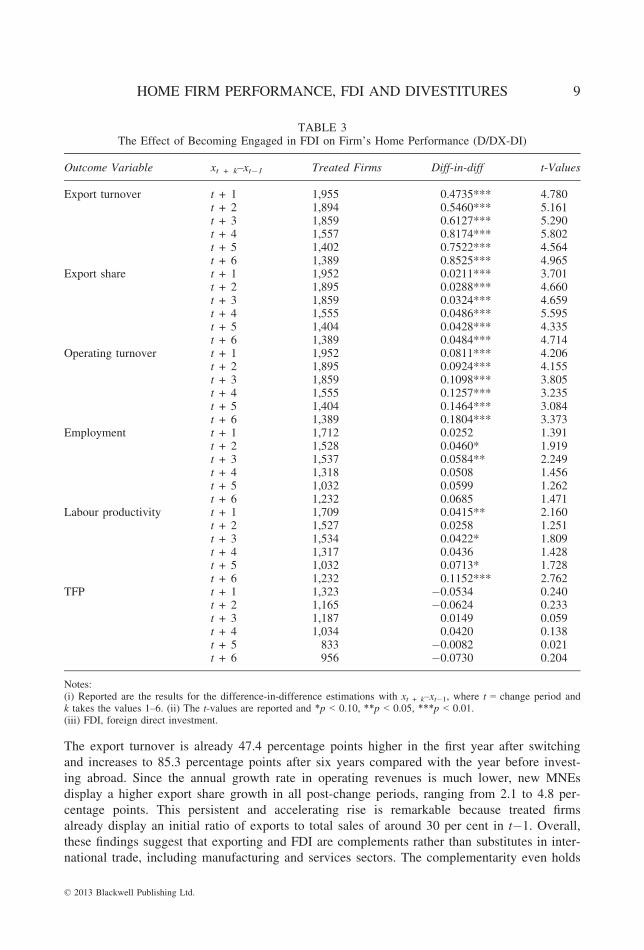

of interest are export turnover and export share. According to results depicted in Table 3, new

MNEs are affected by a significant increase in the absolute export turnover compared with

domestic firms and exporters that, in the same time frame, did not become engaged in FDI.

6 TFP is obtained by applying the STATA command (levpet). The TFP value corresponds to the residualobtained from a firm-specific Cobb-Douglas production function. In contrast to labour productivity, TFPhas no obvious scaling or natural base values thereby impeding a direct interpretation (see Levinsohnet al., 2003 for details).7 The results for the probit estimations and balancing tests are available on request.8 Robustness checks are carried out for firms with a complete outcome record in all post-changeperiods.

Notes:(i) Reported are the results for the difference-in-difference estimations with xt + k–xt�1, where t = change period andk takes the values 1–6. (ii) The t-values are reported and *p < 0.10, **p < 0.05, ***p < 0.01.(iii) FDI, foreign direct investment.

Notes:(i) Reported are the results for the difference-in-difference estimations with xt + k–xt�1, where t = change period andk takes the values 1–6. (ii) The t-values are reported and *p < 0.10, **p < 0.05, ***p < 0.01.

Notes:(i) Reported are the results for the difference-in-difference estimations with xt + k–xt�1, where t = change period andk takes the values 1–6. (ii) The t-values are reported and significance level is 10%.

Notes:(i) Reported are the results for the difference-in-difference estimations with xt + k–xt�1, where t = change period andk takes the values 1–6. (ii) The t-values are reported and significance level is 10%.

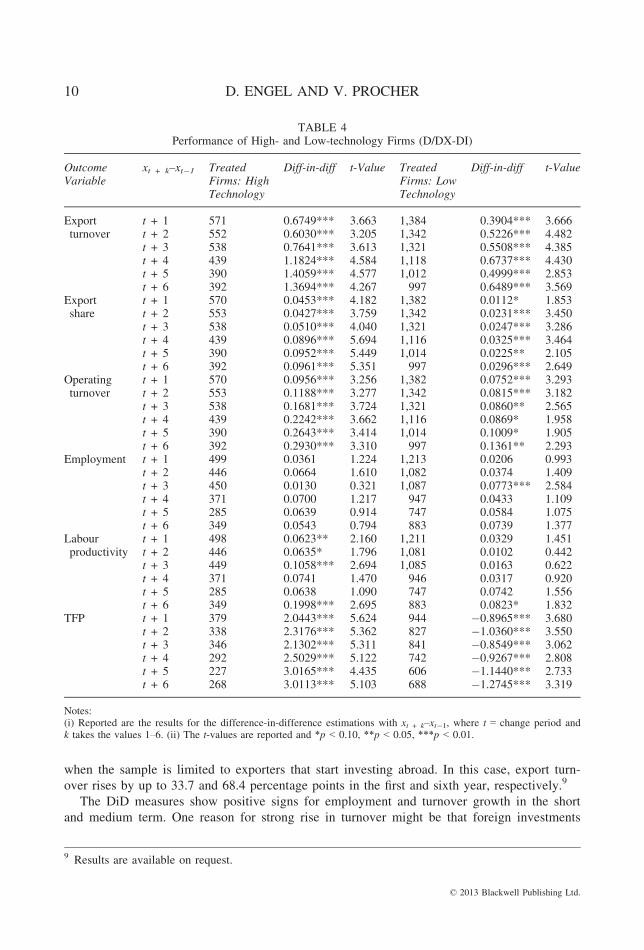

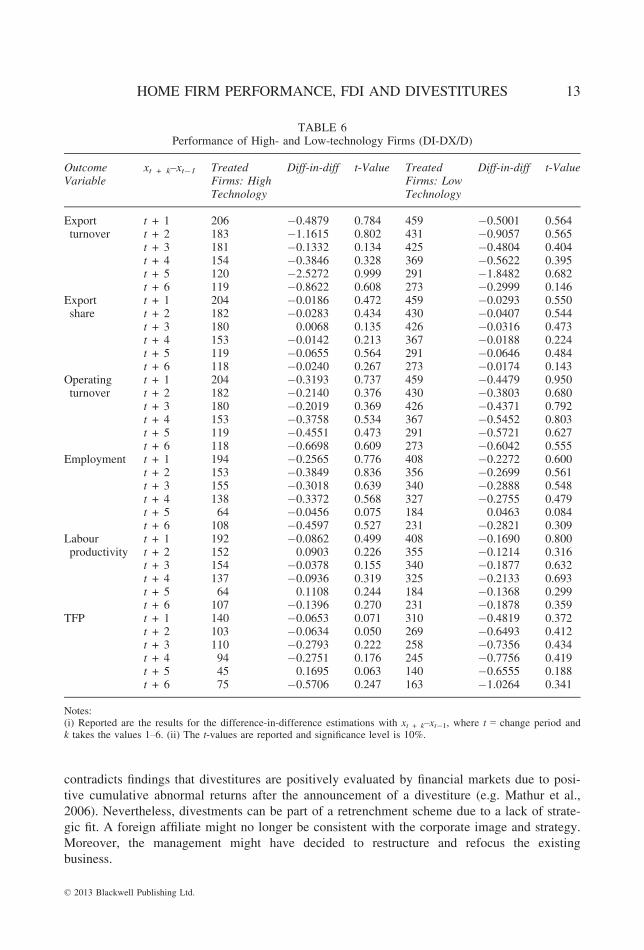

All the findings remain unchanged when the sample is split with respect to the industry

affiliation and general technology level. We fail to detect any significant effect on outcome

variables listed in Table 6. The overall results for divesting firms show no substantial perfor-

mance differences with respect to technology differences. Therefore, analysing reasons for

divestiture as well as transaction forms (selling, closing or spinning-off a foreign business)

might be essential in future research to further enhance the relationship between investment,

divestiture and subsequent corporate performance.

5. CONCLUSION

This paper analyses the effects of investing or divesting abroad on domestic enterprise per-

formance in a French context. A propensity score matching combined with a DiD estimator is

applied to derive empirical findings.

We find a substantial rise in the export share for firms becoming engaged in outward

investments indicating that FDI and exports are complements rather than substitutes. This

might explain why the annual employment and turnover growth is up to 18 percentage points

larger in the post-change periods for new MNEs compared with non-investing firms. The

complementarity between FDI and exports is stronger for switching firms in high-tech indus-

tries than for switching firms in low-tech industries, which might indicate that high-tech firms

opt to a larger extent for home centralisation of certain products and/or vertical specialisation

than low-tech firms. From a policy perspective, the step of firms to internationalise is very

positive because of the steady and strong business development at home in subsequent years.

Apart from FDI, foreign divestitures are a central part of global business dynamics. There-

fore, our study provides an unique contribution to the question on how divesting from abroad

affects home enterprise’ performance. Interestingly, the impact of real economic effects in

terms of export turnover, operating revenue, employment and productivity are negligible in

post-divestiture periods. Based on our findings, one can conclude that the home country does

not need not to fear negative repercussions from firms reverting to domestic operations, but

neither can it gain from foreign divestitures.

REFERENCES

Amador, J. and S. Cabral (2009), ‘Vertical Specialization Across the World: A Relative Measure’, NorthAmerican Journal of Economics and Finance, 20, 3, 267–80.

Barba Navaretti, G. and D. Castellani (2008), ‘Investment Abroad and Performance at Home: Evidencefrom Italian Multinationals’, in S. Brakman and H. Garretse (eds.), Foreign Direct Investment and theMultinational Enterprise (Cambridge, MA: MIT Press), 199–224.

Barba Navaretti, G., D. Castellani and A. C. Disdier (2010), ‘How Does Investing in Cheap LabourCountries Affect Performance at Home? Firm-level Evidence from France and Italy’, OxfordEconomic Papers, 62, 234–60.

Becker, S. O. and M.-A. Muendler (2008), ‘The Effect of FDI on Job Security’, The B.E. Journal ofEconomic Analysis & Policy, 8, Article 8.

Benito, G. R. G. (1997), ‘Divestment of Foreign Production Operations’, Applied Economics, 29, 10,1365–78.

Bernard, A. B. and J. B. Jensen (1999), ‘Exceptional Exporter Performance: Cause, Effect, or Both?’Journal of International Economics, 47, 1, 1–25.

Bernard, A. B. and J. B. Jensen (2007), ‘Firm Structure, Multinationals, and Manufacturing PlantDeaths’, Review of Economics and Statistics, 89, 1, 1–11.

Blundell, R. and M. Costa Dias (2000), ‘Evaluation Methods for Non-experimental Data’, Fiscal Studies,21, 4, 427–68.

Blundell, R. and M. Costa Dias (2002), ‘Alternative Approaches to Evaluation in EmpiricalMicroeconomics’, Portuguese Economic Journal, 1, 1, 1–38.

BvDEP. AMADEUS Database, Release 202, 168, 146, 136, 113 and 88 (Bureau van Dijk ElectronicPublishing, BvDEP). Available at: www.amadeus.bvdep.com (15 March 2012).

Cao, J., S. Owen and A. Yawson (2008), ‘Analysing the Wealth Effects of UK Divestitures: An Exami-nation of Domestic and International Sales’, Research in International Business and Finance, 22, 1,68–84.

Chaney, T. (2005), Liquidity Constrained Exporters. Mimeo (Chicago, IL: University of Chicago).Denis, D. K. and D. K. Shome (2005), ‘An Empirical Investigation of Corporate Asset Downsizing’,

Journal of Corporate Finance, 11, 3, 427–48.Desai, M. A., F. C. Foley and J. R. Hines (2009), ‘Domestic Effects of the Foreign Activities of US

Multinationals’, American Economic Journal. Economic Policy, 1, 1, 181–203.Evans, D. S. (1987), ‘The Relationship Between Firm Growth, Size, and Age: Estimates for 100 Manu-

facturing Industries’, Journal of Industrial Economics, 35, 2, 567–83.Greenaway, D., A. Guariglia and R. Kneller (2007), ‘Financial Factors and Exporting Decisions’,

Journal of International Economics, 73, 2, 377–95.Hanson, R. C. and M. H. Song (2003), ‘Long-term Performance of Divesting Firms and the Effect of

Managerial Ownership’, Journal of Economics and Finance, 27, 3, 321–36.Head, K. and J. Ries (2003), ‘Heterogeneity and the Foreign Direct Investment Versus Exports

Decision of Japanese Manufacturers’, Journal of the Japanese and International Economies, 17, 4,448–67.

Head, K. and J. Ries (2004), ‘Exporting and FDI as Alternative Strategies’, Oxford Review of EconomicPolicy, 20, 3, 409–23.

Heckman, J. J. (1978), ‘Dummy Endogenous Variables in a Simultaneous Equation System’, Econome-trica, 46, 4, 931–60.

Heckman, J. J., P. Ichimura and H. Todd (1998), ‘Matching as an Econometric Evaluation Estimator’,Review of Economic Studies, 65, 2, 261–94.

Heckman, J. J., R. J. LaLonde and J. A. Smith (1999), ‘The Economics and Econometrics of ActiveLabour Market Programs’, in A. Ashenfelter and D. Card (eds.), Handbook of Labour Economics(Amsterdam: Elsevier), Vol. 3A, 1866–2097.

Helpman, E., M. J. Melitz and S. R. Yeaple (2004), ‘Export Versus FDI with Heterogeneous Firms’,American Economic Review, 94, 1, 300–16.

Hering, L., T. Inui and S. Poncet (2010), ‘The Elusive Impact of Investing Abroad: Can an Analysis ofthe Motives for FDI Help?’, Working Paper 2010/12 (Florence: European University Institute).

Hijzen, A., T. Inui and Y. Todo (2007), ‘The Effects of Multinational Production on Domestic Perfor-mance: Evidence from Japanese Firms’, Discussion Paper Series 07-E-006 (Tokyo: Research Instituteof Economy, Trade and Industry).

INSEE – Institut national de la statistique et des �etudes �economiques (2012), ‘Principaux Resultats desEntreprises par Secteur en 2010’, Available at: http://www.insee.fr/fr/themes/tableau.asp?reg_id=0&ref_id=NATTEF09225 (15 March 2012).

J€ackle, R. and G. Wamser (2010), ‘Going Multinational: What are the Effects on Home Market Perfor-mance?’ German Economic Review, 11, 2, 188–207.

Jensen, M. C. (1986), ‘Agency Costs of Free Cash Flow, Corporate Finance and Takeovers’, AmericanEconomic Review, 76, 2, 323–29.

Kleinert, J. and F. Toubal (2007), ‘The Impact of Locating Production Abroad on Activities atHome: Evidence from German Firm-Level Data’, Discussion Paper 314 (Tubingen: University ofTubingen).

Krautheim, S. (2009), ‘Export-supporting FDI’, Working Paper, Economics Studies 20/2009 (Frankfurtam Main: Deutsche Bundesbank).

Lechner, M. (2001), ‘Identification and Estimation of Causal Effects of Multiple Treatments Under theConditional Independence Assumption’, in M. Lechner and F. Pfeiffer (eds.), Econometric Evaluationof Labour Market Policies (Heidelberg: Physica/Springer). 43–58.

Lee, D. and R. Madhavan (2010), ‘Divestiture and Firm Performance: A Meta-analysis’, Journal ofManagement, 36, 6, 1345–71.

Legler, H. and R. Frietsch (2007), ‘Neuabgrenzung der Wissenswirtschaft – forschungsintensiveIndustrien und wissensintensive Dienstleistungen (NIW/ISI-Listen 2006)’, in Bundesministerium fur

Bildung und Forschung (BMBF) (ed.), Studien zum deutschen Innovationssystem Nr. 22/2007(Hannover/Karlsruhe: NIW/Fraunhofer).

Leuven, E. and B. Sianesi (2003), ‘PSMATCH2: Stata Module to Perform Full Mahalanobis and Propen-sity Score Matching, Common Support Graphing, and Covariate Imbalance Testing’, Statistical Soft-ware Components, Boston College Department of Economics. This version: 3.1.4 17dec2008.

Levinsohn, J., A. Petrin and B. Poi (2003), ‘Production Function Estimation in Stata Using Inputs toControl for Unobservables’, Stata Journal, 4, 2, 113–23.

Markusen, J. (1995), ‘The Boundaries of the Multinational Enterprise and the Theory of InternationalTrade’, Journal of Economic Perspectives, 9, 2, 169–89.

Martins, P. S. and Y. Yang (2009), ‘The Impact of Exporting on Firm Productivity: A Meta-analysis ofthe Learning-by-exporting Hypothesis’, Review of World Economics, 145, 3, 431–45.

Mathur, I., K. C. Gleason and M. Singh (2006), ‘Foreign Asset Divestitures by U.S. firms: An Analysisof Motives and Valuation Consequences’, Available at SSRN: http://ssrn.com/abstract=891871(accessed 15 September 2009).

Nerlinger, E. (1998), ‘Standorte und Entwicklung junger innovativer Unternehmen: Empirische Ergeb-nisse fur West-Deutschland’, Dissertation University L€uneburg, ZEW Wirtschaftsanalysen, 27 (Baden-Baden: Nomos Verlag).

Roberts, M. J. and J. R. Tybout (1997), ‘The Decision to Export in Colombia: An Empirical Model ofEntry with Sunk Costs’, American Economic Review, 87, 4, 545–56.

R€oller, L.-H., J. Stennek and F. Verboven (2001), ‘Efficiency Gains from Mergers’, European Economy,5, 1, 31–128.

Roper, S., J. H. Love and D. A. Higon (2006), ‘The Determinants of Export Performance: Evidence forManufacturing Plants in Ireland and Northern Ireland’, Scottish Journal of Political Economy, 53, 5,586–615.

Rosenbaum, P. R. and D. B. Rubin (1983), ‘The Central Role of the Propensity Score in ObservationalStudies for Causal Effects’, Biometrika, 70, 1, 41–55.

Stiebale, J. (2010), ‘The Impact of Foreign Acquisitions on the Investors’ R&D Activities – Firm-LevelEvidence’, Ruhr Economic Papers No. 161 (Essen: RWI).

Stiebale, J. (2011), ‘Do Financial Constraints Matter for Foreign Market Entry? A Firm-Level Examina-tion’, The World Economy, 34, 1, 123–53.

Wagner, J. (2007), ‘Exports and Productivity: A Survey of the Evidence from Firm Level Data’,The World Economy, 30, 1, 60–82.