38

M. CRUZ DEL BARRIO HEAD OF HOME AND GARDEN RESEARCH 7 March 2015 HOMEWARES: TRENDS AND OPPORTUNITIES AROUND THE WORLD 2015 AND BEYOND

| Date post: | 19-Jul-2015 |

| Category: |

Business |

| Upload: | euromonitor-international |

| View: | 1,501 times |

| Download: | 3 times |

M. CRUZ DEL BARRIO

HEAD OF HOME AND GARDEN RESEARCH

7 March 2015

HOMEWARES: TRENDS AND OPPORTUNITIES AROUND THE WORLD 2015 AND BEYOND

© Euromonitor International

2

Our Services Syndicated Market Research Custom Research and Consulting Expansive Network On the ground researchers in 80 countries Cross-comparable data across every market Our Expertise Consumer Trends & Lifestyles Product Categories & Distribution channels Economics & Forecasting

Who Is Euromonitor International?

INTRODUCTION

© Euromonitor International

3

Euromonitor International’s Network and Coverage

INTRODUCTION

© Euromonitor International

4

Euromonitor International’s Research Methodology

INTRODUCTION

HOMEWARES: MARKET OVERVIEW

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

FUTURE CHALLENGES AND OPPORTUNITIES

KEY TAKEAWAYS

US$84bn GLOBAL RETAIL SALES OF

HOMEWARES (2014)

13%

GLOBAL GROWTH

(ANNUAL AVERAGE 2008-2013)

0.1%

OF TOTAL SALES

COME FROM THE US (2014)

© Euromonitor International

7

Homewares

US$84 bn

Dining

US$37 bn

Dinnerware

US$17bn

Beverageware

US$13 bn

Cutlery

US$7 bn

Kitchen

US$47 bn

Cookware

US$26 bn

Kitchenware

US$21 bn

The Building Blocks of the Global Homewares Industry

HOMEWARES: MARKET OVERVIEW

© Euromonitor International

8

Homewares value sales by region (2014)

Western Europe

32%

Australasia 1% Middle East and

Africa 4%

Asia Pacific

30%

Eastern Europe

8%

North America

16%

Latin America

8%

China Leads Growth in Emerging Economies…

HOMEWARES: MARKET OVERVIEW

© Euromonitor International

9

Homewares value sales by region (2014)

Developed

markets

48%

Middle East and

Africa 4%

Asia Pacific

30%

Eastern Europe

8%

Latin America

8%

… but Developed Countries Remain Key Players

HOMEWARES: MARKET OVERVIEW

© Euromonitor International

10

How does Homewares Compare with other Industries?

HOMEWARES: MARKET OVERVIEW

70

75

80

85

90

Global Retail Sales by Industry, US$ billion, 2014

US

$ B

illio

n

Coffee Laundry Care

Ice Cream

Vitamins and Dietary

Supplements

Traditional Toys and Games

Homewares

© Euromonitor International

11

Homes = Homewares: Rising Ownership Drives Sales

HOMEWARES: MARKET OVERVIEW

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

China Turkey Brazil Russia S. Korea US

Net New Housing Completion (Selected Markets, 2008-2013)

© Euromonitor International

12

-30 -25 -20 -15 -10 -5 0 5 10 15 20

Spain

Mexico

US

France

Brazil

Turkey

S. Korea

Russia

China

New Housing Completions Growth: Top and Bottom Countries, 2012-2014 % CAGR

2012-2014 % CAGR

Homes = Homewares: My Home is My Castle

HOMEWARES: MARKET OVERVIEW

Housing

construction

growing

fastest

Housing

construction yet

to recover to

pre-recession

levels

© Euromonitor International

13

Cooking is More than a Necessity HOMEWARES: MARKET OVERVIEW

-2

-1

0

1

2

3

-2

-1

0

1

2

3

Stove TopCookware

Food Storage KitchenUtensils

Ovenware Beverageware Cutlery Dinnerware

% A

nnual G

row

th

US

$ B

illio

n

Homewares Growth by Category (2008-2013)

2008-13 absolute 2008-13 CAGR %

© Euromonitor International

14

-3

-2

-1

0

1

2

3

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

% V

alu

e G

row

th

Homewares retail sales growth by category (World, 2013)

Beverageware Cutlery Dinnerware Cookware Kitchenware

Growing Cooking Interest Boosts Sales

Growth

Drivers

HOMEWARES: MARKET OVERVIEW

© Euromonitor International

15

15

20

25

2008 2009 2010 2011 2012 2013

US

$ p

er

ho

use

ho

ld

World: Dining and Kitchen Expenditure per Household, US$, 2008-2013

Dining Kitchen

Cooking Related Products Prove to Be More Resilient

HOMEWARES: MARKET OVERVIEW

US$105

US$94

US$90

© Euromonitor International

16

0%

25%

50%

75%

100%

Brazil Russia India Germany China France Japan UK US

Never prepare Less than 5 minutes 5-15 minutes 15-30 minutes 30+ minutes

How much time do you spend preparing lunch?

Euromonitor Survey on Eating Habits Around the World in 2013 (I)

HOMEWARES: MARKET OVERVIEW

% o

f re

sp

on

de

nts

© Euromonitor International

17

0%

25%

50%

75%

100%

China Japan India US UK Russia Brazil France Germany

Never prepare Less than 5 minutes 5-15 minutes 15-30 minutes 30+ minutes

How much time do you spend preparing dinner?

Euromonitor Survey on Eating Habits Around the World in 2013 (II)

HOMEWARES: MARKET OVERVIEW

% o

f re

sp

on

de

nts

© Euromonitor International

18

Stove Top Cookware vs Ovenware: Tale of Two Products

HOMEWARES: MARKET OVERVIEW

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

Asia Pacific

Latin America

Australasia

North America

Middle East and Africa

Eastern Europe

Western Europe

US$ billion

Stove Top cookware Vs. Ovenware absolute growth (2008-2013)

Stove Top Cookware Ovenware

© Euromonitor International

19

Roasting and Baking are Regional Preferences

HOMEWARES: MARKET OVERVIEW

93% of households have a microwave

0 20 40 60 80 100

China

Japan

Mexico

Chile

US

Brazil

Russia

UK

Ovens: Household penetration (2014)

0.1% of households have an oven

% o

f household

s

100%

© Euromonitor International

20

China Shows No Interest in Microwaves

HOMEWARES: MARKET OVERVIEW

93% of households have a microwave

0 20 40 60 80 100

China

Mexico

Russia

Brazil

Japan

Chile

UK

US

Microwaves: Household penetration (2014)

Negligible household penetration

91%

% o

f household

s

93%

HOMEWARES: MARKET OVERVIEW

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

FUTURE CHALLENGES AND OPPORTUNITIES

KEY TAKEAWAYS

© Euromonitor International

22

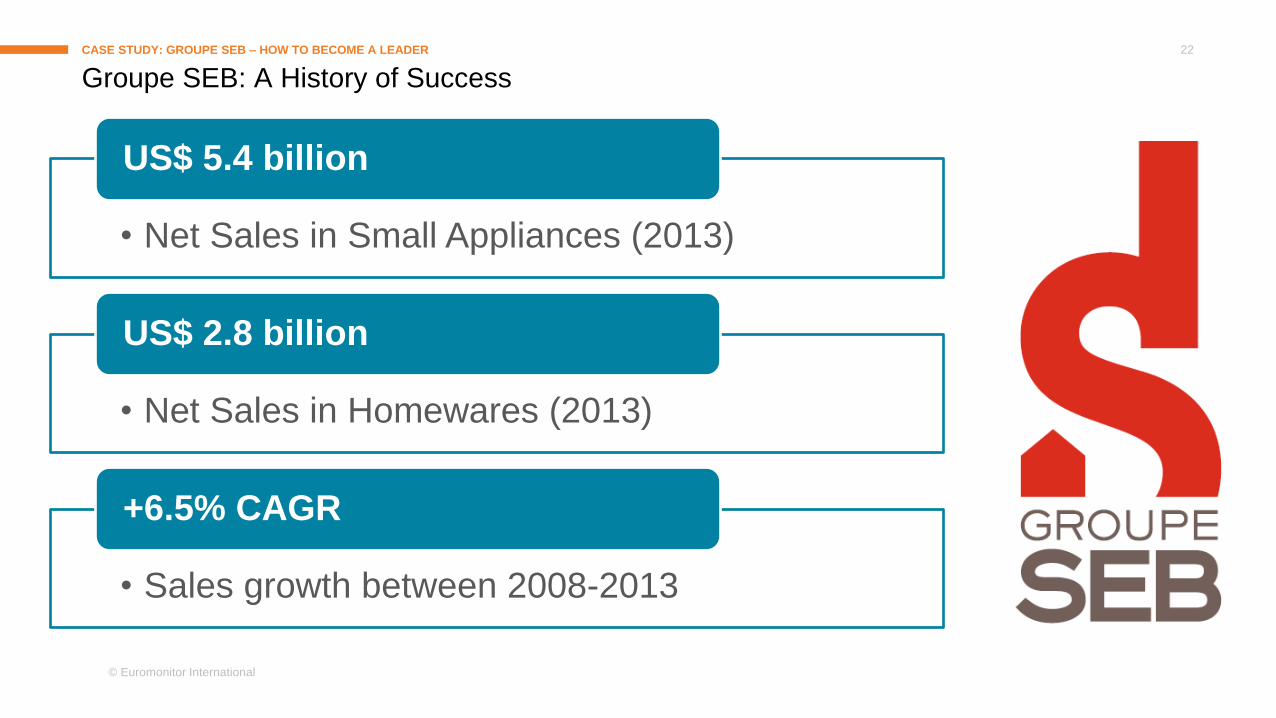

Groupe SEB: A History of Success

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

• Net Sales in Small Appliances (2013)

US$ 5.4 billion

• Net Sales in Homewares (2013)

US$ 2.8 billion

• Sales growth between 2008-2013

+6.5% CAGR

© Euromonitor International

23

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2009 2010 2011 2012 2013

US

$ m

illio

n

Groupe SEB Cookware Sales 2009-2013, US$ million, Retail Value RSP

Groupe SEB a leading player in cookware

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

© Euromonitor International

24

Acquisition of leading local brands

Control of retail network

Introduce other SEB brands to market

• Supor

• Imusa

• Maharaja Whiteline

• Company operated stores

• Third party retailers

• Imusa and Home & Cook outlets

Groupe SEB global strategy

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

© Euromonitor International

25

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014

Consumer Appliances: Imusa brand volume sales 2009-2014 (‘000 units)

Vo

lum

e s

ale

s (

‘00

0 u

nits)

Company

operated stores in

Colombia (2014)

22

Largest cookware

company in the

US by value sales (2014)

3rd

SEB’s Acquisitions to Bolster Retailing Presence (I): The Americas

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

Groupe SEB

takeover

© Euromonitor International

26

Company operated stores in China

+1,000

Cookware brand in China by sales,

2014

1st

SEB’s Acquisitions to Bolster Retailing Presence (II): China

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

0

100

200

300

400

500

600

2009 2010 2011 2012 2013 2014

Kitchen: Supor Brand Sales in China (US$ mn) 2009-2014

Va

lue

sa

les (

US

$ m

illio

n)

© Euromonitor International

27

Currency Fluctuations Hit SEB

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

-20

-15

-10

-5

0

5

10

Japan Russia Turkey

% y

-o-y

va

lue

gro

wth

Sales Growth Performance: Local Currency and Euro Y-o-Y Exchange Rates 2012-2013

Local Currency Euro Y-o-Y Exchange Rates

HOMEWARES: MARKET OVERVIEW

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

FUTURE CHALLENGES AND OPPORTUNITIES

KEY TAKEAWAYS

© Euromonitor International

29

Commoditization of homewares

Competition from private label

Unclear brand segmentation

The Future Comes with Many Challenges

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

30

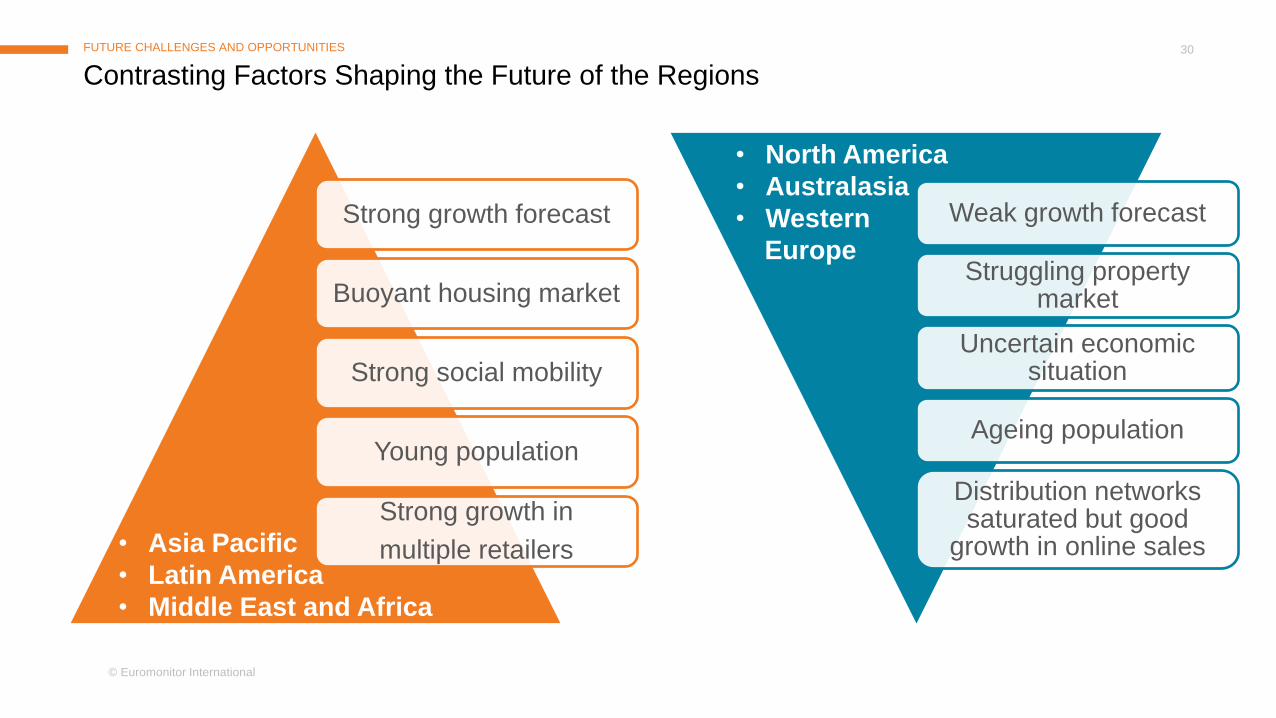

Strong growth forecast

Buoyant housing market

Strong social mobility

Young population

Strong growth in

multiple retailers

Contrasting Factors Shaping the Future of the Regions

Weak growth forecast

Struggling property market

Uncertain economic situation

Ageing population

Distribution networks saturated but good

growth in online sales • Asia Pacific

• Latin America

• Middle East and Africa

• North America

• Australasia

• Western

Europe

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

31

Fastest Growing Markets

-2

0

2

4

6

0

50

100

150

WesternEurope

Australasia NorthAmerica

EasternEurope

LatinAmerica

AsiaPacific

MiddleEast and

Africa

20

13

-18 C

AG

R%

US

$ p

er

household

(2013

)

Homewares: Inverse correlation between spend per household and forecast growth

2013 US$ per household spend 2013-18 CAGR%

China Indonesia

Brazil UAE

Thailand

Growth will Come from Emerging Economies

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

32

0

2

4

6

8

10

12

0

10

20

30

40

50

60

70

Brazil US Russia Germany South Korea Argentina

% s

ha

re

US

$ m

n

Highest growth countries in Ovenware and Share of Silicone in 2013

2009-13 absolute growth Ovenware 2013 silicone share in Ovenware %

Growth Through Innovation: Silicone in Ovenware

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

33

0

5

10

15

20

25

0

100

200

300

400

500

China Germany Russia US Canada South Korea

% s

hare

US

$ m

n

Highest growth countries in Kitchen Utensils and Share of Silicone in 2013

2009-13 absolute growth Kitchen Utensils 2013 silicone share in Kitchen Utensils %

Growth Through Innovation: Silicone in Kitchen Utensils

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

34

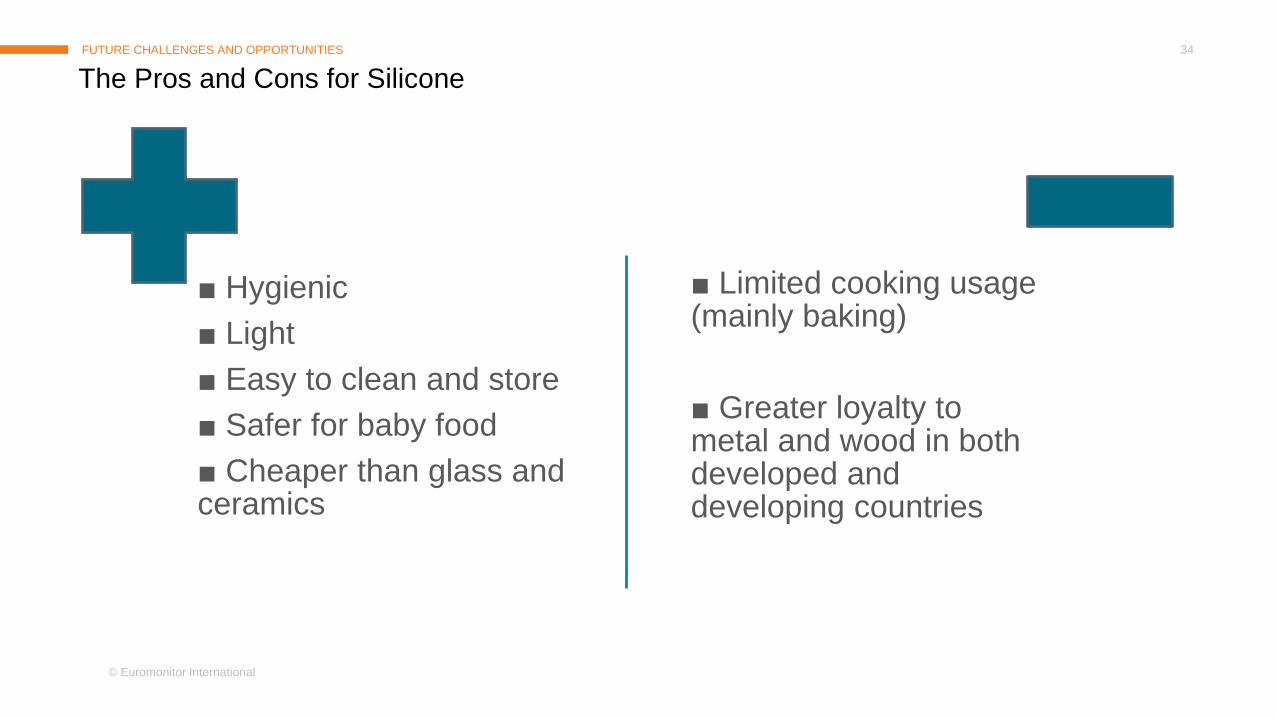

■ Hygienic

■ Light

■ Easy to clean and store

■ Safer for baby food

■ Cheaper than glass and ceramics

■ Limited cooking usage (mainly baking)

■ Greater loyalty to metal and wood in both developed and developing countries

The Pros and Cons for Silicone

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

35

Smart Objects and the Internet of Things

FUTURE CHALLENGES AND OPPORTUNITIES

US (2014)

SKE Lab Neo Smart Jar

112%

Tablet Penetration

162%

Smartphone Penetration

SEB Groupe: 40% of R&D allocated to

Smart Objects and Connectivity in 2014

Source: www.Indiegogo.com

HOMEWARES: MARKET OVERVIEW

CASE STUDY: GROUPE SEB – HOW TO BECOME A LEADER

FUTURE CHALLENGES AND OPPORTUNITIES

KEY TAKEAWAYS

© Euromonitor International

37

Key Takeaways

Emerging

Markets

• Growth potential

• Lower expenditure per household

Developed

Market

• Stagnant growth

• Higher expenditure per household

Creating Value

• New Product Development

• Materials and formats

Smart Home

• Homewares as part of the “Internet of Things”

FUTURE CHALLENGES AND OPPORTUNITIES

© Euromonitor International

38

THANK YOU FOR LISTENING

M. Cruz del Barrio

Head of Home and Garden Research

Euromonitor International

60-61 Britton Street

London EC1M 5UX

www.euromonitor.com

Note: 2013 figures are based on part-year estimates. 2014 data is preliminary. Both are subject to change. Final data to be published May 2015