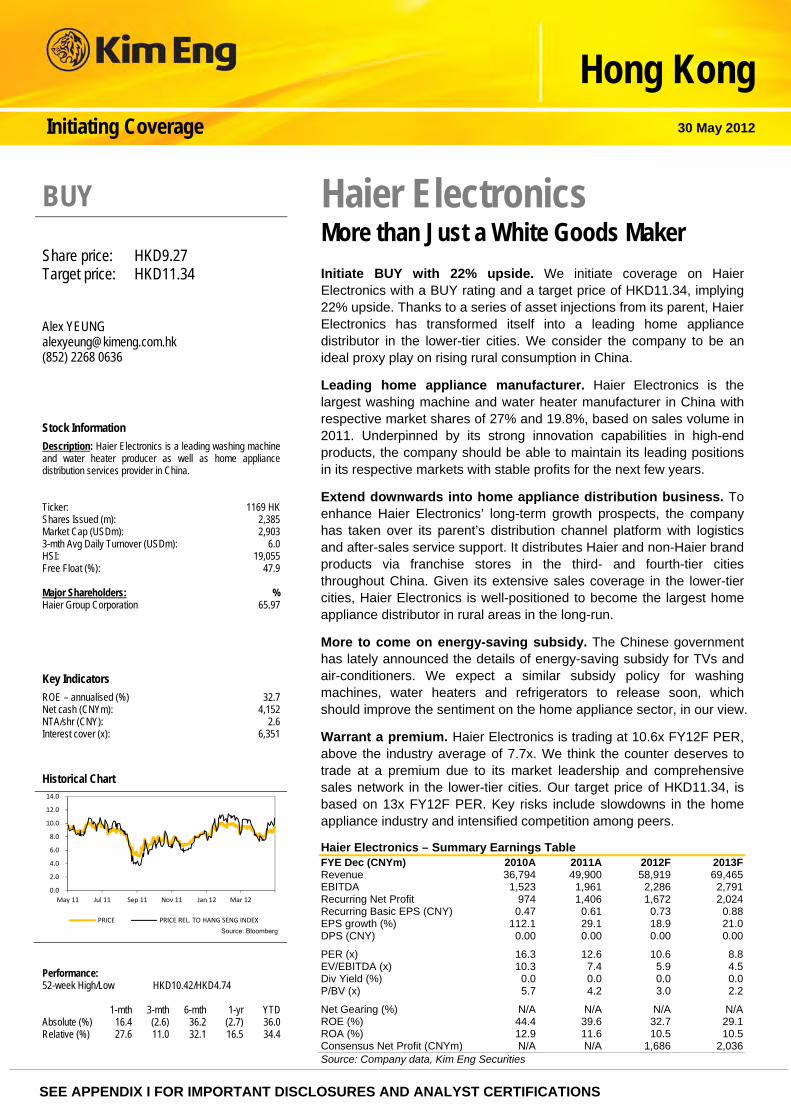

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS Hong Kong Initiating Coverage 30 May 2012 Haier Electronics More than Just a White Goods Maker Initiate BUY with 22% upside. We initiate coverage on Haier Electronics with a BUY rating and a target price of HKD11.34, implying 22% upside. Thanks to a series of asset injections from its parent, Haier Electronics has transformed itself into a leading home appliance distributor in the lower-tier cities. We consider the company to be an ideal proxy play on rising rural consumption in China. Leading home appliance manufacturer. Haier Electronics is the largest washing machine and water heater manufacturer in China with respective market shares of 27% and 19.8%, based on sales volume in 2011. Underpinned by its strong innovation capabilities in high-end products, the company should be able to maintain its leading positions in its respective markets with stable profits for the next few years. Extend downwards into home appliance distribution business. To enhance Haier Electronics’ long-term growth prospects, the company has taken over its parent’s distribution channel platform with logistics and after-sales service support. It distributes Haier and non-Haier brand products via franchise stores in the third- and fourth-tier cities throughout China. Given its extensive sales coverage in the lower-tier cities, Haier Electronics is well-positioned to become the largest home appliance distributor in rural areas in the long-run. More to come on energy-saving subsidy. The Chinese government has lately announced the details of energy-saving subsidy for TVs and air-conditioners. We expect a similar subsidy policy for washing machines, water heaters and refrigerators to release soon, which should improve the sentiment on the home appliance sector, in our view. Warrant a premium. Haier Electronics is trading at 10.6x FY12F PER, above the industry average of 7.7x. We think the counter deserves to trade at a premium due to its market leadership and comprehensive sales network in the lower-tier cities. Our target price of HKD11.34, is based on 13x FY12F PER. Key risks include slowdowns in the home appliance industry and intensified competition among peers. Haier Electronics – Summary Earnings Table FYE Dec (CNYm) 2010A 2011A 2012F 2013F Revenue 36,794 49,900 58,919 69,465 EBITDA 1,523 1,961 2,286 2,791 Recurring Net Profit 974 1,406 1,672 2,024 Recurring Basic EPS (CNY) 0.47 0.61 0.73 0.88 EPS growth (%) 112.1 29.1 18.9 21.0 DPS (CNY) 0.00 0.00 0.00 0.00 PER (x) 16.3 12.6 10.6 8.8 EV/EBITDA (x) 10.3 7.4 5.9 4.5 Div Yield (%) 0.0 0.0 0.0 0.0 P/BV (x) 5.7 4.2 3.0 2.2 Net Gearing (%) N/A N/A N/A N/A ROE (%) 44.4 39.6 32.7 29.1 ROA (%) 12.9 11.6 10.5 10.5 Consensus Net Profit (CNYm) N/A N/A 1,686 2,036 Source: Company data, Kim Eng Securities BUY Share price: HKD9.27 Target price: HKD11.34 Alex YEUNG [email protected](852) 2268 0636 Stock Information Description: Haier Electronics is a leading washing machine and water heater producer as well as home appliance distribution services provider in China. Ticker: 1169 HK Shares Issued (m): 2,385 Market Cap (USDm): 2,903 3-mth Avg Daily Turnover (USDm): 6.0 HSI: 19,055 Free Float (%): 47.9 Major Shareholders: % Haier Group Corporation 65.97 Key Indicators ROE – annualised (%) 32.7 Net cash (CNYm): 4,152 NTA/shr (CNY): 2.6 Interest cover (x): 6,351 Historical Chart Performance: 52-week High/Low HKD10.42/HKD4.74 1-mth 3-mth 6-mth 1-yr YTD Absolute (%) 16.4 (2.6) 36.2 (2.7) 36.0 Relative (%) 27.6 11.0 32.1 16.5 34.4 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 May 11 Jul 11 Sep 11 Nov 11 Jan 12 Mar 12 PRICE PRICE REL. TO HANG SENG INDEX Source: Bloomberg

Transcript

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Hong KongInitiating Coverage 30 May 2012

Haier Electronics More than Just a White Goods Maker Initiate BUY with 22% upside. We initiate coverage on Haier Electronics with a BUY rating and a target price of HKD11.34, implying 22% upside. Thanks to a series of asset injections from its parent, Haier Electronics has transformed itself into a leading home appliance distributor in the lower-tier cities. We consider the company to be an ideal proxy play on rising rural consumption in China.

Leading home appliance manufacturer. Haier Electronics is the largest washing machine and water heater manufacturer in China with respective market shares of 27% and 19.8%, based on sales volume in 2011. Underpinned by its strong innovation capabilities in high-end products, the company should be able to maintain its leading positions in its respective markets with stable profits for the next few years.

Extend downwards into home appliance distribution business. To enhance Haier Electronics’ long-term growth prospects, the company has taken over its parent’s distribution channel platform with logistics and after-sales service support. It distributes Haier and non-Haier brand products via franchise stores in the third- and fourth-tier cities throughout China. Given its extensive sales coverage in the lower-tier cities, Haier Electronics is well-positioned to become the largest home appliance distributor in rural areas in the long-run.

More to come on energy-saving subsidy. The Chinese government has lately announced the details of energy-saving subsidy for TVs and air-conditioners. We expect a similar subsidy policy for washing machines, water heaters and refrigerators to release soon, which should improve the sentiment on the home appliance sector, in our view.

Warrant a premium. Haier Electronics is trading at 10.6x FY12F PER, above the industry average of 7.7x. We think the counter deserves to trade at a premium due to its market leadership and comprehensive sales network in the lower-tier cities. Our target price of HKD11.34, is based on 13x FY12F PER. Key risks include slowdowns in the home appliance industry and intensified competition among peers.

Description: Haier Electronics is a leading washing machine and water heater producer as well as home appliance distribution services provider in China. Ticker: 1169 HK Shares Issued (m): 2,385 Market Cap (USDm): 2,903 3-mth Avg Daily Turnover (USDm): 6.0 HSI: 19,055 Free Float (%): 47.9 Major Shareholders: % Haier Group Corporation 65.97 Key Indicators

Haier dominates in China. Haier Electronics, together with its parent companies - Qingdao Haier (600690 CH) and Haier Group Corporation, is one of the largest white goods manufacturers in China with a 7.8% market share, based on revenue in 2011. Haier Electronics produces a comprehensive range of washing machines and water heaters to cater to the diverse needs of customers. Riding on the group’s strong execution ability and experienced management team, the Haier brand enjoys strong domestic recognition and decent global demand.

A pioneer among peer manufacturers to head downstream. Formerly a home appliance manufacturer, Haier Electronics has leveraged on its relationship with the parent to take over the Goodaymart distribution platform that distributes Haier brand and non-Haier (third-party) brand home appliance products in the third- and fourth-tier cities. Underpinned by its extensive network coverage with more than 7,000 Haier stores and 700 Goodaymart stores, Haier Electronics enjoys first-mover advantage. Thus, it is well-positioned to capture the strong growth of rural consumption in China, which should produce solid earnings growth for the company over the next few years.

New subsidy programme bolstering growth of home appliance industry. The China State Council has announced a new energy-saving subsidy programme (amounting to CNY26.5b) to be launched in five home appliance categories. We expect Haier Electronics’ high-end washing machines and water heaters to be eligible for the subsidy. Moreover, the new subsidy programme would also foster the development of its distribution business, on the back of government initiatives to improve the demand for energy-saving home appliance products. Overall, the company should be one of the chief beneficiaries of the new subsidy programme.

Potential M&A to strengthen distribution business. Haier Electronics has a strong balance sheet with an estimated net cash value of CNY4.2b as of the end of FY12F. Thus, the company is in a strong capital position to actively explore potential M&A opportunities, with an eye on accelerating its downstream distribution business. Potential earnings-enhancing activities include acquisitions of sizable regional distributors with strong third-party brands sourcing channels.

Initiating BUY with a target price of HKD11.34. Considering Haier Electronics’ leadership in the white goods manufacturing industry, the robust growth prospects of its distribution business in rural areas and its healthy balance sheet, Haier Electronics deserves to be trading at a premium valuation against its industry peers. Our TP of HKD11.34 is based on 13x FY12F PER, supported by an EPS CAGR of 20% for FY11-13F. Initiate coverage with BUY, with a 22% upside.

30 May 2012 Page 3 of 24

Haier Electronics Group Co., Ltd

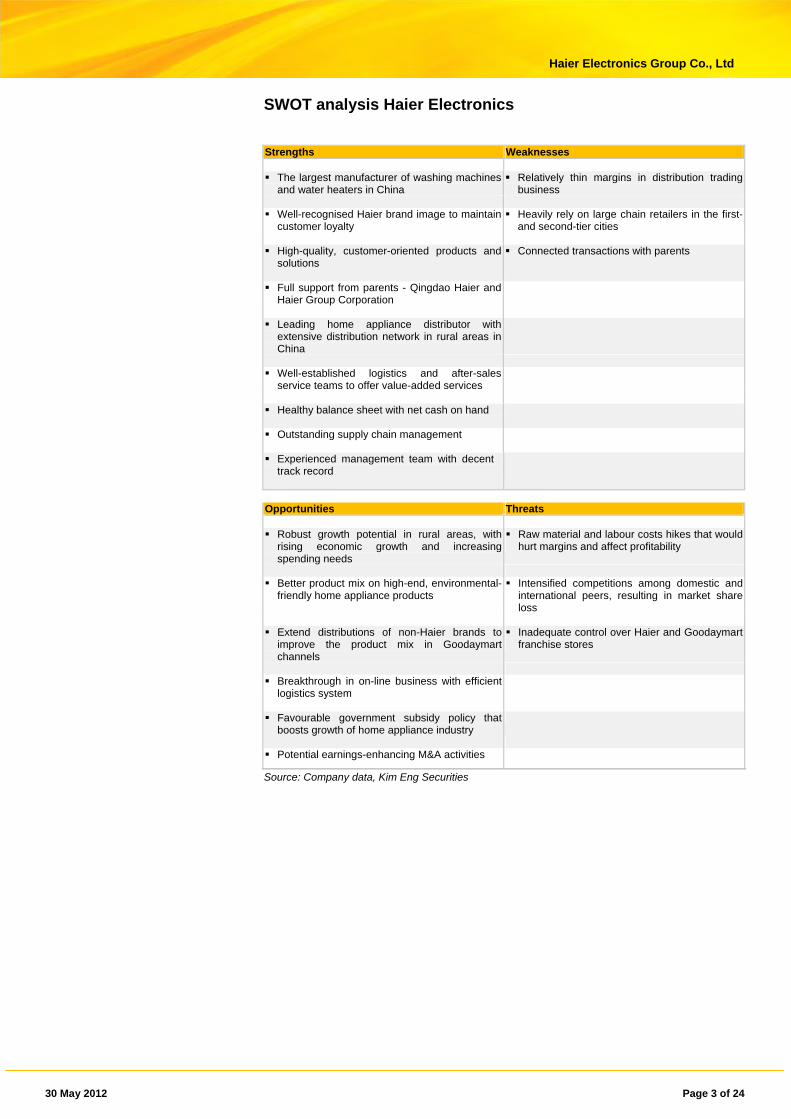

SWOT analysis Haier Electronics

Strengths Weaknesses The largest manufacturer of washing machines

and water heaters in China Relatively thin margins in distribution trading

business Well-recognised Haier brand image to maintain

customer loyalty Heavily rely on large chain retailers in the first-

and second-tier cities High-quality, customer-oriented products and

solutions Connected transactions with parents

Full support from parents - Qingdao Haier and

Haier Group Corporation

Leading home appliance distributor with

extensive distribution network in rural areas in China

Well-established logistics and after-sales

service teams to offer value-added services

Healthy balance sheet with net cash on hand

Outstanding supply chain management

Experienced management team with decent

track record

Opportunities Threats Robust growth potential in rural areas, with

rising economic growth and increasingspending needs

Raw material and labour costs hikes that would hurt margins and affect profitability

Better product mix on high-end, environmental-

friendly home appliance products Intensified competitions among domestic and

international peers, resulting in market share loss

Extend distributions of non-Haier brands to

improve the product mix in Goodaymart channels

Inadequate control over Haier and Goodaymart franchise stores

Breakthrough in on-line business with efficient

logistics system

Favourable government subsidy policy that

boosts growth of home appliance industry

Potential earnings-enhancing M&A activities

Source: Company data, Kim Eng Securities

30 May 2012 Page 4 of 24

Haier Electronics Group Co., Ltd

Company background

Brief history. Haier Electronics is a subsidiary of the Haier Group Corporation. After years of restructuring, with the business changing hands, Haier Electronics has become a leading producer of washing machines and water heaters in China. Most of its products are sold under the brand name of Haier. It has been the largest producer in the past decade, its market shares in washing machines and water heaters were 27% and 19.8%, respectively, in 2011, based on sales volume. In order to broaden its sources of revenue, Haier Electronics has spent the past two years acquiring its parent’s home appliance distribution, logistics and after-sales service businesses, as well as tapping into a new business, known as integrated channel services (ICS), with a focus on the third- and fourth-tier cities in China.

A-share listed Qingdao Haier. Qingdao Haier (600690 CH) has been listed on the Shanghai Stock Exchange since 1993. Apart from its washing machine and water heater businesses that are managed under the HK-listed Haier Electronics, Qingdao Haier also operates other white goods businesses including refrigerators, air-conditioners and some small home appliances. On a consolidated basis, about 68% of Qingdao Haier sales were derived from Haier Electronics in FY11. (please refer to the appendix section of the shareholding structure of Haier Electronics.)

Figure 1: Haier Electronics business structure

Source: Company data, Kim Eng Securities

30 May 2012 Page 5 of 24

Haier Electronics Group Co., Ltd

Integrated channel services segment

Expanding into downstream distribution business. As part of the Haier Group’s business strategy, Haier Electronics took over its parent’s channel service operation arm, Goodaymart, and started to operate a downstream distribution business in 2010, with a focus on the third- and fourth-tier cities in China. Additionally, Haier Electronics also acquired the logistics and after-sales service businesses from its parent, thus transforming Haier Electronics into an integrated channel service provider.

Figure 2: Evolution of integrated channel services for Haier Electronics

Source: Company data, Kim Eng Securities

Distribution channel arm Goodaymart. Since 2010, Haier Electronics has started to distribute home appliance products through its channel arm Goodaymart in the third- and fourth-tier cities of China. Goodaymart distributes a wide spectrum of products including Haier Electronics’ washing machines and water heaters, home appliance goods from Haier Electronics’ parents (Qingdao Haier and Haier Group Corporation), along with non-Haier brand products. Goodaymart’s distributors comprise more than 7,000 Haier franchise stores that carry Haier brand products exclusively and 700 Goodaymart franchise stores that sell both Haier and non-Haier brand products.

Figure 3: Haier Electronics distribution model

Source: Company data, Kim Eng Securities

30 May 2012 Page 6 of 24

Haier Electronics Group Co., Ltd

Figure 4: Examples of non-Haier brands in Goodaymart

Source: Company data, Kim Eng Securities

Fast and efficient logistics network. Haier Electronics has a strong nationwide logistics network in China with an extensive geographical coverage in rural areas. It offers suppliers and customers just-in-time logistics services by providing distribution, warehousing, as well as after-market and third party logistics. It has about 82 operational logistics centers and nine under construction, covering different provinces, regions, counties and towns as of the end of 2011. With a fleet of 16,000 delivery vehicles servicing China, fast delivery is guaranteed. The company is able to deliver products to locations within 150km in only 24 hours and locations within 250km in just 48 hours.

Quality after-sales service. Haier Electronics acquired the final piece of the ICS business with the successful acquisition of the after-sales service business from its parent in Jun 2011. This segment provides value-added services for customers in the areas of installation, maintenance and ordering of spare parts for the Haier brand. There are five call centres strategically located in Beijing, Qingdao, Wuhan, Guangzhou and Chongqing, which provide 24/7 quality services to customers throughout China. It also has 40,000 engineers stationed nationwide in China. Riding on the increasing needs of products repairing services in the lower-tier cities, the after-sales service unit should become increasingly popular, thus offering growing potential for Haier Electronics.

On-line sales channels. To tap into the fast-growing on-line sales demand, Haier Electronics acquired the e-Haier platform (www.ehaier.com) from its parents in Jun 2011. The e-Haier sells approximately 2,000 kinds of Haier brand products, it re-directs sales orders to nearby franchise stores that provide distribution, logistics and after-sales services. The e-Haier receives a platform fee in return. Over the medium-term, Haier Electronics will be able to forge positive synergies between its online sales platform and its solid logistics and distribution network.

Domestic brands

International brands

30 May 2012 Page 7 of 24

Haier Electronics Group Co., Ltd

Figure 5: Haier franchise store Figure 6: Goodaymart franchise store

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

Figure 7: Logistics center interior look Figure 8: Customer service center

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

Figure 9: Logistics vehicle Figure 10: The e-Haier website (www.ehaier.com)

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

30 May 2012 Page 8 of 24

Haier Electronics Group Co., Ltd

White goods manufacturing segment

Market leader in respective markets. The white goods manufacturing operation comprises sales of washing machines and water heaters. Its dominant market position aside, Haier Electronics is poised to achieve steady growth in the washing machine and water heater markets, the company has rolled out plans to improve its product mix to produce high-end environmental-friendly products continuously for its comprehensive brand portfolios. The portfolios are Haier, Casarte and Leader, with the latter two accounting for 30% of white goods sales.

Figure 11: Comprehensive white goods brands portfolio

Source: Company data, Kim Eng Securities

Washing machine business. Haier Electronics produces both top loading and front loading washing machines; it is the largest washing machine manufacturer in China. In 2011, the Haier brand led the domestic market with a 27% market share based on sales volume, according to market research China Market Monitor (CMM).

Sales of Haier Electronics’ washing machine business increased gradually to CNY12.2b (+6% yoy), accounting for 19.9% of total sales in FY11. Within the segment, about 60% of sales came through the Goodaymart channel, with the remaining 29% and 11% from domestic third-party retailers and the overseas market respectively. Owing to rising overseas sales that have a lower gross margin than the domestic market, gross margin fell slightly by 0.3ppt to 27.8% in FY11.

With its strong brand and R&D capabilities, Haier Electronics intends to shift its focus to high-end products. As a result, we expect the sales mix of higher-priced front-loading washing machines to increase.

Figure 12: Market shares for washing machine industry in 2010

Source: China IOL, Kim Eng Securities

Haier Electronics27.0%

Midea20.0%Panasonic

11.0%

Siemens11.0%

Sanyo8.0%

LG6.0%

Others17.0%

30 May 2012 Page 9 of 24

Haier Electronics Group Co., Ltd

Figure 13: Prices of Haier Electronics washing machines in 36 cities (CNY/ unit)

Source: CEIC, Kim Eng Securities

Water heater business. In addition to washing machines, Haier Electronics also offers a comprehensive mix of electric, gas and solar water heaters. China Market Monitor reiterated that Haier Electronics has maintained its leading position in the domestic market by holding a 19.8% market share in terms of sales volume in 2011. In particular, its market shares in electric and gas water heater had expanded to 27.1% and 7.6% from 20.3% and 6% in 2010 respectively.

Sales in the water heater business were solid, amounting to CNY3.8b (+22.5% yoy) and constituting 6.3% of total sales in FY11. Notably, about 85.7% of water heater sales were generated through the Goodaymart channel. Gross margin narrowed by 0.7ppt yoy to 41.9%, mainly due to rising raw material and labour costs.

With the government’s intensified efforts to save energy and reduce emissions, it is anticipated that consumer interest in energy-saving water heaters will increase. As a result, we believe that the sales contribution of solar water heaters should increase, which would raise the ASP and protect gross margins. In fact, the gross margin of water heaters has stayed at above 40% for the past few years, due to their relative newness and under-penetration in China.

Production base. In the past, most of the capital expenditures were linked to the washing machine segment, as the company was building up the washing machine productions capacities in Qingdao, Hefei, Shunde, Jiaonan and Chongqing. Haier Electronics can produce a total of 15.5m units of washing machines per annum. Separately, Haier Electronics manufactures water heaters in Qingdao, Wuhan and Chongqing with an estimated total capacity of 3.5m units per annum. Due to the company’s large sales volumes and high penetration rates in the markets, utilisation rates have been maintained at above 80%.

Figure 14: Washing machine and water heater production capacity

Source: Company data, Kim Eng Securities

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2,500

May 03 Mar 04 Jan 05 Nov 05 Sep 06 Jul 07 May 08 Mar 09 Jan 10 Nov 10 Sep 11

30 May 2012 Page 10 of 24

Haier Electronics Group Co., Ltd

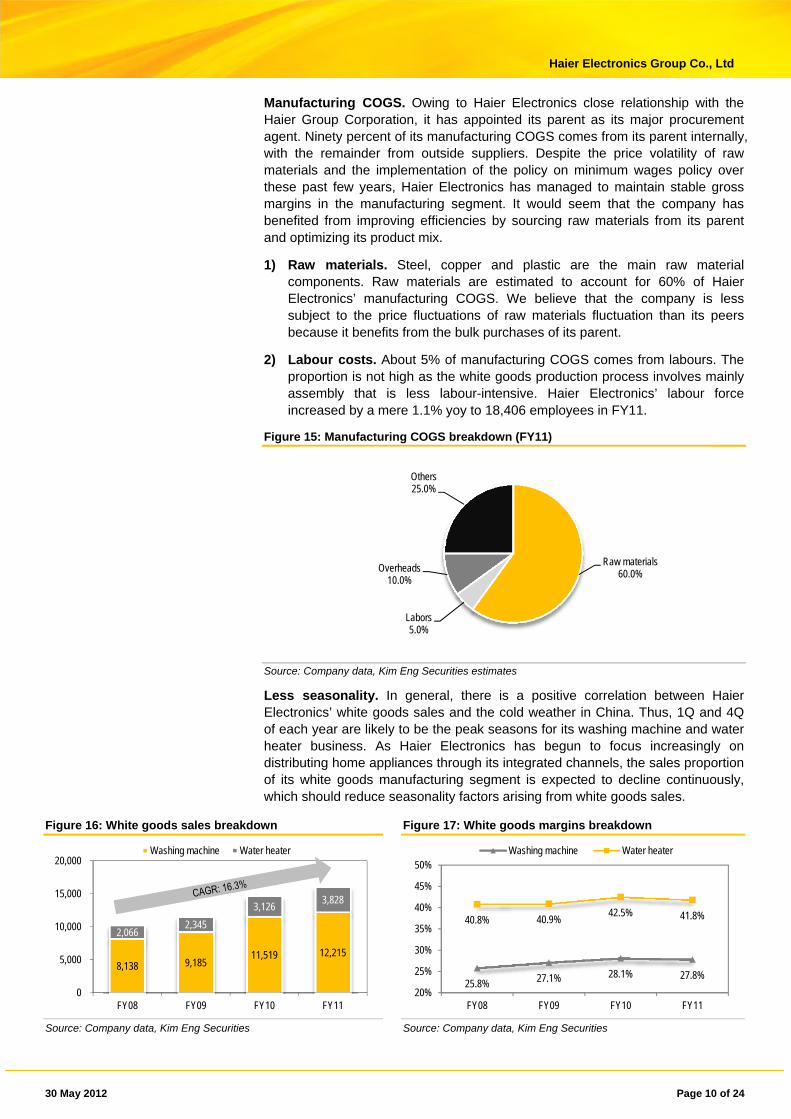

Manufacturing COGS. Owing to Haier Electronics close relationship with the Haier Group Corporation, it has appointed its parent as its major procurement agent. Ninety percent of its manufacturing COGS comes from its parent internally, with the remainder from outside suppliers. Despite the price volatility of raw materials and the implementation of the policy on minimum wages policy over these past few years, Haier Electronics has managed to maintain stable gross margins in the manufacturing segment. It would seem that the company has benefited from improving efficiencies by sourcing raw materials from its parent and optimizing its product mix.

1) Raw materials. Steel, copper and plastic are the main raw material components. Raw materials are estimated to account for 60% of Haier Electronics’ manufacturing COGS. We believe that the company is less subject to the price fluctuations of raw materials fluctuation than its peers because it benefits from the bulk purchases of its parent.

2) Labour costs. About 5% of manufacturing COGS comes from labours. The proportion is not high as the white goods production process involves mainly assembly that is less labour-intensive. Haier Electronics’ labour force increased by a mere 1.1% yoy to 18,406 employees in FY11.

Figure 15: Manufacturing COGS breakdown (FY11)

Source: Company data, Kim Eng Securities estimates

Less seasonality. In general, there is a positive correlation between Haier Electronics’ white goods sales and the cold weather in China. Thus, 1Q and 4Q of each year are likely to be the peak seasons for its washing machine and water heater business. As Haier Electronics has begun to focus increasingly on distributing home appliances through its integrated channels, the sales proportion of its white goods manufacturing segment is expected to decline continuously, which should reduce seasonality factors arising from white goods sales.

Figure 16: White goods sales breakdown Figure 17: White goods margins breakdown

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

Raw materials60.0%

Labors5.0%

Overheads10.0%

Others25.0%

8,138 9,185 11,519 12,215

2,066 2,345

3,126 3,828

0

5,000

10,000

15,000

20,000

FY08 FY09 FY10 FY11

Washing machine Water heater

25.8% 27.1% 28.1% 27.8%

40.8% 40.9%42.5% 41.8%

20%

25%

30%

35%

40%

45%

50%

FY08 FY09 FY10 FY11

Washing machine Water heater

30 May 2012 Page 11 of 24

Haier Electronics Group Co., Ltd

Growth strategies and drivers

White goods product mix optimisation. In order to maintain steady growth for the white goods manufacturing segment, Haier Electronics will persist in developing products with high added value including front loading washing machines and gas water heaters. The company will also capitalize on its multi-brand strategy involving the high-end Casarte brand and the rural-focused Leader brand to cater the needs for its diverse customers. In our view, Haier Electronics intends not to compete with peers on price, but on brand equity and R&D capabilities, to maintain its sales growth momentum.

Extend non-Haier brand portfolio. To fuel the future growth of its ICS business, Haier Electronics will introduce even more popular non-Haier brands to the Goodaymart franchise stores in the third- and fourth-tier cities as to attract more retailers to join the Goodaymart distribution network. Non-Haier brand products typically generate higher margins than its own Haier brand products; thus, the rising sales contributions of non-Haier brand products should strengthen overall margins and profitability in the long-run. In FY11, sales of Haier brand products contributed to 90% of its ICS business sales. Management is targeting a 50:50 sales split between Haier and non-Haier brand products for the ICS business in FY15F.

Expansion of franchise stores network. With its adoption of the franchise model, Haier Electronics will continue to expand the Goodaymart franchise stores. The company has about 700 Goodaymart stores at the county level; it plans to expand to 1,000 stores in FY12F. Meanwhile, Haier Electronics has no plans to expand its 7,000 Haier franchise stores further; instead, it will concentrate on standardisation and operational efficiency improvements in order to enhance the productivity of each store.

Strategic cooperation with the Carlyle Group. In Jul 2011, the Carlyle Group became a strategic investor in Haier Electronics through the subscription of convertible bonds and warrants at the exercise prices of HKD10.67 and HKD11.20 respectively. The holder can exercise the rights in Feb 2013. Upon a complete conversion, the dilution impact will be about 5.7%. In our view, Carlyle not only provides capital funds, but also experience in consumer goods, distribution management and M&A activities, which will likely accelerate Haier Electronics’ development of its distribution capabilities.

Major beneficiary of new government subsidy. In May 2012, the Chinese government announced that it would spend CNY26.6b in subsidies to promote five home appliance products with energy-saving features, including air-conditioners, flat-panel TVs, refrigerators, washing machines and water heaters, and the duration of the subsidy has been set tentatively at one year. We believe that Haier Electronics will be one of the beneficiaries under the new policy: a high proportion of its washing machines and water heaters is classified as environmentally-friendly. Moreover, its ICS business will also benefit from the improving demand for home appliance products within the industry.

30 May 2012 Page 12 of 24

Haier Electronics Group Co., Ltd

Financial analysis

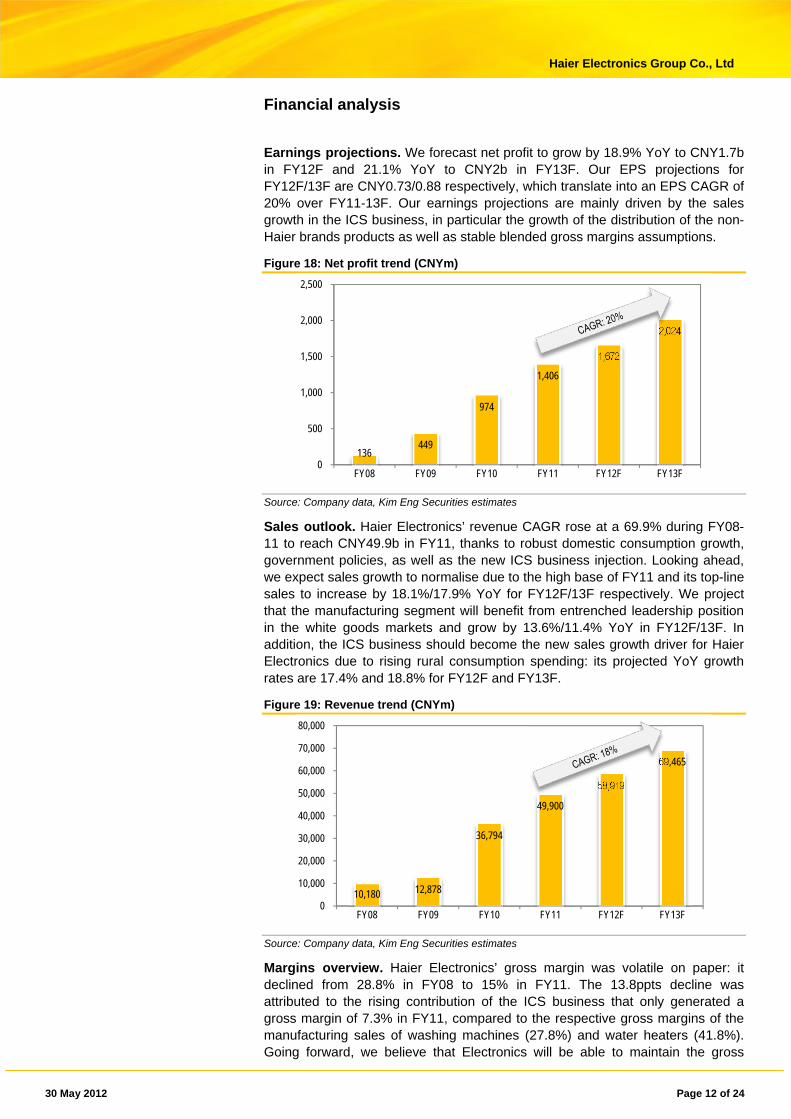

Earnings projections. We forecast net profit to grow by 18.9% YoY to CNY1.7b in FY12F and 21.1% YoY to CNY2b in FY13F. Our EPS projections for FY12F/13F are CNY0.73/0.88 respectively, which translate into an EPS CAGR of 20% over FY11-13F. Our earnings projections are mainly driven by the sales growth in the ICS business, in particular the growth of the distribution of the non-Haier brands products as well as stable blended gross margins assumptions.

Figure 18: Net profit trend (CNYm)

Source: Company data, Kim Eng Securities estimates

Sales outlook. Haier Electronics’ revenue CAGR rose at a 69.9% during FY08-11 to reach CNY49.9b in FY11, thanks to robust domestic consumption growth, government policies, as well as the new ICS business injection. Looking ahead, we expect sales growth to normalise due to the high base of FY11 and its top-line sales to increase by 18.1%/17.9% YoY for FY12F/13F respectively. We project that the manufacturing segment will benefit from entrenched leadership position in the white goods markets and grow by 13.6%/11.4% YoY in FY12F/13F. In addition, the ICS business should become the new sales growth driver for Haier Electronics due to rising rural consumption spending: its projected YoY growth rates are 17.4% and 18.8% for FY12F and FY13F.

Figure 19: Revenue trend (CNYm)

Source: Company data, Kim Eng Securities estimates

Margins overview. Haier Electronics’ gross margin was volatile on paper: it declined from 28.8% in FY08 to 15% in FY11. The 13.8ppts decline was attributed to the rising contribution of the ICS business that only generated a gross margin of 7.3% in FY11, compared to the respective gross margins of the manufacturing sales of washing machines (27.8%) and water heaters (41.8%). Going forward, we believe that Electronics will be able to maintain the gross

136 449

974

1,406

1,672

2,024

0

500

1,000

1,500

2,000

2,500

FY08 FY09 FY10 FY11 FY12F FY13F

10,180 12,878

36,794

49,900

58,919

69,465

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FY08 FY09 FY10 FY11 FY12F FY13F

30 May 2012 Page 13 of 24

Haier Electronics Group Co., Ltd

margins of its sales, thanks to its continuous upgrade of its product mix for high-end products. Separately, we expect the gross margin of the ICS business to expand gradually on the back of the increasing sales of non-Haier brand products that enjoy higher gross margins. However, we believe that the gross margin improvement will be negligible in the short-term as the company focuses on growing the scale of its ICS business, instead of increasing its margins. Overall, we expect the company’s blended gross margin to remain stable at 14.8%/14.7% for FY12F/13F.

Figure 20: Margins trend

Source: Company data, Kim Eng Securities estimates

Healthy balance sheet. Haier Electronics has a healthy balance sheet with CNY3.3b in net cash as of the end of FY11, which includes the proceeds of HKD1.1b from the issuance of a five-year convertible bond in Jul 2011. Aided by its increasing operating cash flows, Haier Electronics’ net cash position should be sustainable in the upcoming years. In our view, the company’s strong balance sheet gives it significant financial flexibility, thus, the company is well-positioned to make further acquisitions, without needing to raise additional capital from other financing methods.

Capital expenditure. We forecast that Haier Electronics’ FY12F CAPEX will be CNY1b, higher than the CNY317m in FY11. Based on our estimates, the company will spend CNY200m on doubling its production capacity of front loading washing machines from the current level, and another CNY600m for constructing new warehouses for the logistics segment, with the remaining CNY200m for potential M&A opportunities. Although Haier Electronics’ CAPEX has increased for FY12F, we believe that it can be funded by the company’s strong internal cash flows.

Dividend policy. Although it sits on a rich net cash balance, Haier Electronics does not have a consistent dividend policy. The company has not paid any dividends since 2009, in order to fund strategic acquisitions for its integrated channel services business in China. With the recent suspension in dividends and CAPEX needs ahead, we do not expect a change in the company’s dividend policy for the upcoming years.

28.8%

25.0%

13.1%15.0% 14.8% 14.7%

1.3%3.5% 2.6% 2.8% 2.8% 2.9%

0%

5%

10%

15%

20%

25%

30%

35%

FY08 FY09 FY10 FY11 FY12F FY13F

GPM NPM

30 May 2012 Page 14 of 24

Haier Electronics Group Co., Ltd

Valuation and recommendation

Re-rating has started. Haier Electronics has been trading in the PER range of 2x-19.6x over the past four years, with an average ratio of 7.8x since 2008 and 10.4x since 2010. There has been a re-rating of Haier Electronics in the recent two years, as the company’s downstream operation has been generating strong earnings growth.

Worth the premium. The stock is now trading at 10.6x FY12F PER, while other HK-listed and A-share listed home appliance players are trading in the respective ranges of 4.9x-10.6x and 8.6x-37.9x. Going ahead, we believe that the re-rating issue will continue. Haier Electronics deserves to trade at a premium compared to its peers, owing to its leadership in the white goods manufacturing segment, robust growth potential in its downstream distribution business and promising exposure to rising rural demand.

BUY with 22% upside. We initiate coverage on Haier Electronics with a BUY recommendation and a target price of HKD11.34, based on the PER methodology. Our target price is pegged on 13x FY12F PER which translates into 0.6x PEG, on the back of a two-year EPS CAGR of 20%.

Figure 21: Relative share price performance (%)

Source: Bloomberg, Kim Eng Securities

Figure 22: PER band Figure 23: PBR band

Source: Bloomberg, Kim Eng Securities estimates Source: Bloomberg, Kim Eng Securities estimates

The key risk factors that pose downside risks to our earnings forecasts are as follows:

Connected transactions. Owing to the organisational structure of Haier Electronics with Qingdao Haier and Haier Group Corporation, Haier Electronics had disclosed several connected transactions with the other two parties over the past few years. They are mainly related to products procurement, internal sales agreement as well as assets acquisitions/transfers. As Haier Electronics’ distribution business grows rapidly and becomes a major source of sales, we believe that the frequency of such connected transactions will decrease, which should improve investor confidence in Haier Electronics.

Macro environment. As the Chinese government persists with tightening its policy on lending and investments, the market has already expected China’s economic growth to slow down; in fact, it considers a moderate rate to be healthy in the long-term. However, a faster-than-expected decline in economic growth due to deteriorating macros around the could hurt consumer confidence and lead to a decline in consumer spending for home appliance products.

Intensified competition. The competition in the white goods manufacturing sector is keen and Haier Electronics may face challenges from other competitors within the same industry. Should anyone initiate a price war, Haier Electronics might have to follow suit in order to stay competitive or to maintain its the market share. As a result, Haier Electronics profitability may be affected adversely.

Threat from big retailers. Gome and Suning have initiated expansion plans into the lower-tier cities. With their strong execution capabilities in the top-tier cities, they could replicate their business models in the top-tier cities successfully in the lower-tier cities, thus undermining Haier Electronics’ distribution business and challenging our earnings projections.

Expiry of government’s subsidy programme. The “Home Appliances to Countryside” policy that subsidised consumers’ purchases has been phasing out gradually; in fact, it will expire completely by Jan 2013. Consumers may be purchasing products in advance in order to enjoy the subsidy, thus, demand for home appliance products after the subsidy programme could drop significantly.

Hikes in raw material and labour costs. As with other home appliance producers in China, surges in raw material and labour costs may put place Haier Electronics’ gross margins under pressure. Raw material and labour costs account for about 60% and 5% of COGS of its white goods manufacturing segment, respectively.

30 May 2012 Page 17 of 24

Haier Electronics Group Co., Ltd

Appendix I: Shareholding structure

Parent has the control. The Qingdao Haier Collective Asset Management Association (青島海爾集體資產管理協會) is the ultimate controlling shareholder of

Haier Electronics through the Haier Group Corporation that has a total stake of 65.97% in Haier Electronics. Shares are exercised through Qingdao Haier that owns a 51.81% stake in Haier Electronics. Haier Investment and Development, an investment company owned by the senior management in the Haier Group Corporation, holds the remaining 14.16% stake. It has served the entire Haier Group Corporation for a long time.

Figure 25: Corporate structure

Source: Company data, HKEx, Kim Eng Securities

30 May 2012 Page 18 of 24

Haier Electronics Group Co., Ltd

Appendix II: Corporate development

Figure 26: Haier Electronics corporate milestones Sept 2000 Haier Group Corporation and CCT Telecom established two JVs, Pegasus Telecom

(Hong Kong) and Pegasus Telecom (Qingdao), with respective stakes of 49:51 and 51:49, for the operation of the mobile handsets business.

Dec 2001 Both Haier Group Corporation and CCT Telecom injected the stakes of Pegasus Telecom (Hong Kong) into CCT Digital (1169), making Pegasus Telecom (Hong Kong) a wholly-owned subsidiary of CCT Digital. In addition, CCT Telecom also injected its 49% stake of Pegasus Telecom (Qingdao) into CCT Digital.

Jan 2002 CCT Digital was renamed Haier CCT.

Oct 2002 Haier Group Corporation injected the 15.5% stake of Pegasus Telecom (Qingdao) into Haier CCT.

Jan 2005 Haier Group Corporation injected the top loading washing machine business into Haier CCT. At the same time, it also injected the remaining 35.5% stakes of Pegasus telecom (Qingdao) into Haier CCT.

Mar 2005 Haier CCT was renamed Haier Electronics.

Jan 2006 Haier Electronics returned its mobile handset business back to Haier Group Corporation.

Dec 2006 Front loading washing machine and water heater businesses were injected into Haier Electronics from Haier Group Corporation.

Sept 2009 Haier Electronics established a wholly-owned subsidiary to participate in the distribution of home appliance products, as well as the provision of related value-added services that consist of logistics, agency, and post-sale services in China.

Jan 2010 Haier Electronics and Haier Group Corporation entered into a products procurement agreement and an internal sales agreement to distribute all Haier brand home appliance products in third- and fourth-tier cities.

Mar 2010 Haier Electronics completed the business and asset transfer of the distribution channel from Haier Group Corporation.

Aug 2010 Haier Electronics acquired the logistics business from Haier Group Corporation with a consideration of CNY763m.

Jun 2011 Haier Electronics acquired the after-sales service business with a consideration of CNY240m and the online sales platform business with a consideration of CNY30m from Haier Group Corporation.

Aug 2011 Haier Electronics introduced Carlyle Group as its strategic investor through the issuance of convertible bonds and warrants.

Oct 2011 Haier Electronics formed a JV with Home Retail Group with respective stakes of 51% and 49% to develop a general merchandise multi-channel retailing business under the brand name of Argos in China.

Source: Company data, Kim Eng Securities

30 May 2012 Page 19 of 24

Haier Electronics Group Co., Ltd

Appendix III: Management profile

Decent management. Haier Electronics is managed by a group of professionals with extensive experience in the home appliance industry; most of the senior managers have more than 20 years of experience in the industry. In fact, their execution ability has been proven by the company’s strong earnings growth over the past few years.

Figure 27: Key management team Name Age Title Current / Previous experience Education Ms. Yang Mian Mian 70 Chairman and Executive

Director Responsible for determining corporate strategies and overall management

Graduated from Shandong University in 1963

Mr. Zhou Yun Jie 45 Executive Director Has over 20 years of experience in sales management and enterprise management

Graduated from the Xian Jiaotong University with a Diploma in Management from the Doctoral courses

Mr. Li Hua Gang 42 Chief Operation Officer and Executive Director

Holds a number of senior positions in the sales and marketing functions with his expertise in the sales management in the third- and fourth-tier cities in China

Graduated from the Huazhong University of Science and Technology with a Bachelor’s degree in Economics in 1991

Mr. Sun Jing Yan 41 Executive Director Responsible for the operation of the water heater business; has over 18 years of experience in the water heater business

Graduated from Shangdong Institute of Light Industry with a Bachelor’s degree in Engineering in 1993

Mr. Wu Ke Song 61 Deputy Chairman and Non-executive Director

Responsible for worldwide business development and liaison with relevant government officials

Graduated from Shandong University in 1974

Mr Liang Hai Shan 45 Non-executive Director Responsible for identifying market opportunities and formulating white goods business strategies; has over 23 years of experience in the manufacturing of household electrical appliances

Graduated from the Xian Jiaotong University with a Bachelor’s degree in Industry

Ms. Janine Junyuan Feng

43 Non-executive Director Involved in many direct investments by the Carlyle Group in consumer, financial, and industrial companies in China

Graduated from Harvard Business School with an MBA degree in 1996

Mr. Wu Yinong 49 Independent Non-executive Director

Has been in the investment banking industry for more than 15 years

Graduated from Portland State University in the US with a Master’s degree in Business Administration

Mr. Yu Hon To, David 64 Independent Non-executive Director

Extensive experience in corporate finance No information

Dr. Liu Xiao Feng 49 Independent Non-executive Director

Solid experience in corporate finance Graduated from the University of Cambridge with Master’s degrees from the Faculty of Economics

Mr. Huang Xiao Wu 34 Deputy General Manager

Responsible for assisting the General Manager in implementing corporate development strategy

Graduated from the University of Hong Kong with a Master’s degree in Business Administration

Mr. Peng Jia Jun 34 Chief Financial Officer Holds a number of senior financial positions in the finance department, Haier Australia trading company

Graduated from the University of International Business and Economic with a Master’s degree in Business Administration

Mr. Shu Hai 45 General Manager Responsible for the sales, research and development and production management of the washing machine business

Graduated from Ocean University of China with a Master’s degree in International Trade

Mr. Wang Zheng Gang

39 General Manager Responsible for developing the logistics business and identifying related market opportunities; has over 16 years of experience in the manufacturing of household electrical appliances

Graduated from the Xian Jiaotong University with a Master’s degree in Logistics Engineering in 2007

Mr. Lu Pei Shi 48 General Manager Responsible for the research and development of the washing machine business

Graduated from Shandong Agricultural and Mechanical College with a Bachelor’s degree

Mr. Ng Chi Yin 46 Company Secretary Has over 23 years of experience in auditing, finance and company secretarial matters

Graduated from the Chinese University of Hong Kong with a Bachelor’s degree in Business Administration

Source: Company data, Kim Eng Securities

30 May 2012 Page 20 of 24

Haier Electronics Group Co., Ltd

Appendix IV: White goods

Figure 28: Front loading washing machine Figure 29: Top loading washing machine

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

Figure 30: Electric water heater Figure 31: Gas water heater

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

Figure 32: Solar energy heater Figure 33: Solar energy heater installation idea

Source: Company data, Kim Eng Securities Source: Company data, Kim Eng Securities

30 May 2012 Page 21 of 24

Haier Electronics Group Co., Ltd

INCOME STATEMENT BALANCE SHEET FYE Dec (CNYm) 2010A 2011A 2012F 2013F

VIETNAM Michael KOKALARI, CFA Head of Research +84 838 38 66 47 [email protected] Strategy Nguyen Thi Ngan Tuyen +84 844 55 58 88 x 8081 [email protected] Food and Beverage Oil and Gas Ngo Bich Van +84 844 55 58 88 x 8084 [email protected] Banking Nguyen Quang Duy +84 844 55 58 88 x 8082 [email protected] Rubber Dang Thi Kim Thoa +84 844 55 58 88 x 8083 [email protected] Consumer Nguyen Trung Hoa +84 844 55 58 88 x 8088 [email protected] Steel Sugar Macro

30 May 2012 Page 23 of 24

Haier Electronics Group Co., Ltd

Definition of Ratings Kim Eng Research uses the following rating system:

BUY Total return is expected to be above 15% in the next 12 months

HOLD Total return is expected to be between -15% to +15% in the next 12 months

SELL Total return is expected to be below -15% in the next 12 months

Applicability of Ratings The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not carry investment ratings as we do not actively follow developments in these companies. Some common terms abbreviated in this report (where they appear):

Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings BV = Book Value FV = Fair Value PEG = PE Ratio To Growth CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On Equity DPS = Dividend Per Share NTA = Net Tangible Asset ROSF = Return On Shareholders’ Funds EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date EV = Enterprise Value PBT = Profit Before Tax APPENDIX I: TERMS FOR PROVISION OF REPORT, DISCLOSURES AND DISCLAIMERS Disclaimer The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and you should consult an independent financial adviser before making any investments or entering into any transaction in relation to any securities mentioned in this report. The information, tools and material presented herein are not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject Maybank Kim Eng Holdings Limited and/or its subsidiaries or affiliates (collectively “Maybank Kim Eng”) to any registration or licensing requirement within such jurisdiction. Information and opinions presented in this report have been obtained or derived from sources believed by Maybank Kim Eng to be reliable, but Maybank Kim Eng makes no representation as to their accuracy or completeness and Maybank Kim Eng accepts no liability for loss arising from the use of the material presented in this report where permitted by law and/or regulation. This report is not to be relied upon in substitution for the exercise of independent judgment. Maybank Kim Eng may have issued other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them. The research analyst(s) primarily responsible for the preparation of this report confirms that (a) all of the views expressed in this report accurately reflects his or her personal views abut any and all of the subject securities or issuers; and (b) that no part of his or her compensation was, is or will be, directly or indirectly, related to the specific recommendations or views he or she expressed in this report. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Maybank Kim Eng, its directors and employees may have investments in securities or derivatives of any companies mentioned in this report, and may make investment decisions that are inconsistent with the views expressed in this report. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct its own investigation and analysis of the product and consult with its own professional advisers as to the risks involved in making such a purchase. General Disclosure Maybank Kim Eng and its officers, directors and employees, including persons involved in the preparation or issuance of this report, may, to the extent permitted by law, from time to time participate or invest in financing transactions with the issuer(s) of the securities mentioned in this report, perform services for or solicit business from such issuers, and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto. In addition, it may make markets in the securities mentioned in the material presented in this report. Maybank Kim Eng may, to the extent permitted by law, act upon or use the information presented herein, or the research or analysis on which they are based, before the material is published. One or more directors, officers and/or employees of Maybank Kim Eng may be a director of the issuers of the securities mentioned in this report. Maybank Kim Eng may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the previous 12 months, significant advice or investment services in relation to the investment concerned or a related investment. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information contained herein is believed to be reliable, its completeness and accuracy is however not guaranteed. Opinions expressed in this report are subject to change without notice, and no part of this publication is to be construed as an offer, or solicitation of an offer to buy or sell any securities or financial instruments whether referred therein or otherwise. We do not accept any liability whatsoever whether direct or indirect that may arise from the use of information contained in this report. Any transactions by US persons in any security discussed in this report must be carried out through Maybank Kim Eng Securities (USA) Inc which has distributed this report in the USA. In addition, this document has been distributed in the UK for information only and circulated only to existing customers of Maybank Kim Eng, who are not private customers as classified under FSA’s Rules.

30 May 2012 Page 24 of 24

Haier Electronics Group Co., Ltd

Malaysia Maybank Investment Bank Berhad (A Participating Organisation of Bursa Malaysia Securities Berhad) 33rd Floor, Menara Maybank, 100 Jalan Tun Perak, 50050 Kuala Lumpur Tel: (603) 2059 1888; Fax: (603) 2078 4194

Singapore Maybank Kim Eng Securities Pte Ltd Maybank Kim Eng Research Pte Ltd 9 Temasek Boulevard #39-00 Suntec Tower 2 Singapore 038989 Tel: (65) 6336 9090 Fax: (65) 6339 6003

London Maybank Kim Eng Securities (London) Ltd 6/F, 20 St. Dunstan’s Hill London EC3R 8HY, UK Tel: (44) 20 7621 9298 Dealers’ Tel: (44) 20 7626 2828 Fax: (44) 20 7283 6674

New York Maybank Kim Eng Securities USA Inc 777 Third Avenue, 21st Floor New York, NY 10017, U.S.A. Tel: (212) 688 8886 Fax: (212) 688 3500

Stockbroking Business: Level 8, Tower C, Dataran Maybank, No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888 Fax: (603) 2282 5136

Hong Kong Kim Eng Securities (HK) Ltd Level 30, Three Pacific Place, 1 Queen’s Road East, Hong Kong Tel: (852) 2268 0800 Fax: (852) 2877 0104

Indonesia PT Kim Eng Securities Plaza Bapindo Citibank Tower 17th Floor Jl Jend. Sudirman Kav. 54-55 Jakarta 12190, Indonesia

Tel: (62) 21 2557 1188 Fax: (62) 21 2557 1189

India Kim Eng Securities India Pvt Ltd 2nd Floor, The International 16, Maharishi Karve Road, Churchgate Station, Mumbai City - 400 020, India Tel: (91).22.6623.2600 Fax: (91).22.6623.2604

Philippines Maybank ATR Kim Eng Securities Inc. 17/F, Tower One & Exchange Plaza Ayala Triangle, Ayala Avenue Makati City, Philippines 1200 Tel: (63) 2 849 8888 Fax: (63) 2 848 5738

Thailand Maybank Kim Eng Securities (Thailand) Public Company Limited 999/9 The Offices at Central World, 20th - 21st Floor, Rama 1 Road Pathumwan, Bangkok 10330, Thailand Tel: (66) 2 658 6817 (sales) Tel: (66) 2 658 6801 (research)

Vietnam In association with

Kim Eng Vietnam Securities Company 1st Floor, 255 Tran Hung Dao St. District 1 Ho Chi Minh City, Vietnam Tel : (84) 838 38 66 36 Fax : (84) 838 38 66 39

Saudi Arabia In association with

Anfaal Capital Villa 47, Tujjar Jeddah Prince Mohammed bin Abdulaziz Street P.O. Box 126575 Jeddah 21352 Tel: (966) 2 6068686 Fax: (966) 26068787

South Asia Sales Trading Connie TAN [email protected] Tel: (65) 6333 5775 US Toll Free: 1 866 406 7447

North Asia Sales Trading Eddie LAU [email protected] Tel: (852) 2268 0800 US Toll Free: 1 866 598 2267