24

Investor Presentation August 2012 HORSEHEAD HOLDING CORP. HORSEHEAD HOLDING CORP. Cellhouse

Investor PresentationAugust 2012

HORSEHEAD HOLDING CORP.HORSEHEAD HOLDING CORP.

Cellhouse

2

Legal Disclaimers

Informational Purposes Only

This investor presentation is being furnished for informational purposes only, and does not and shall not constitute an offer to sellor a solicitation to buy any securities of the Company.

Third Party Information

This presentation has been prepared by the Company based on information we have or have obtained from sources we believeto be reliable. Summaries of the terms of certain documents may be contained in this presentation and may not be complete,and we refer you to such documents for a more complete understanding of what we discuss in this presentation. The informationin this presentation is current only as of the date on the cover, and our business or financial condition and other information inthis presentation may change after that date.

Forward Looking Statements

This presentation contains statements, estimates and projections with respect to the anticipated future performance ofthe Company that may be deemed to be “forward‐looking statements”. You should not place undue reliance uponthese statements. These statements relate to analyses and other information, which are based on forecasts of futureresults and estimates of amounts not yet determinable. These statements also relate to our future prospects, liquidity,possible or future results of operations, developments and business strategies. Although we believe that our plans,intentions and expectations reflected in or suggested by such forward‐looking statements are reasonable, we cannotassure you that we will achieve those plans, intentions or expectations.

Non-GAAP Financial Measures

We have included certain financial measures in this presentation, including EBITDA and Adjusted EBITDA, which are“non-GAAP financial measures” as defined under the rules of the Securities and Exchange Commission. Thispresentation includes reconciliations of the non-GAAP financial measures found in this presentation to the mostdirectly comparable financial measures calculated and presented in accordance with generally accepted accountingprinciples in the United States.

3

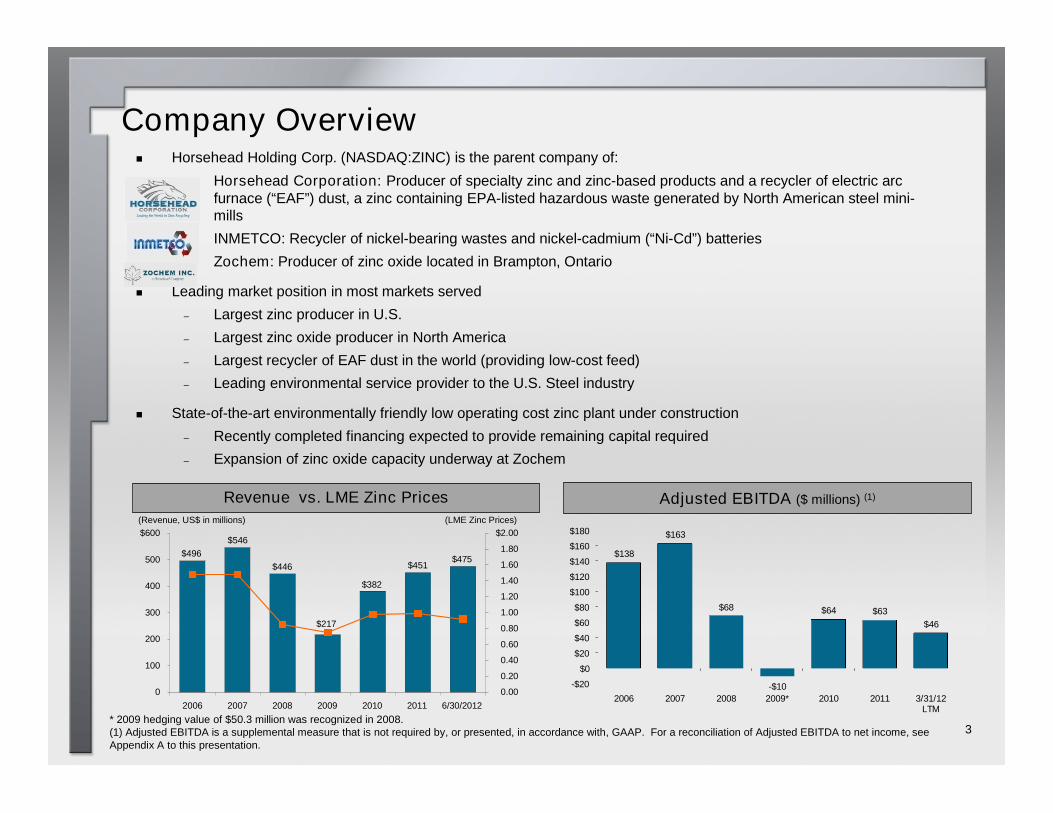

Company Overview Horsehead Holding Corp. (NASDAQ:ZINC) is the parent company of:

– Horsehead Corporation: Producer of specialty zinc and zinc-based products and a recycler of electric arcfurnace (“EAF”) dust, a zinc containing EPA-listed hazardous waste generated by North American steel mini-mills

– INMETCO: Recycler of nickel-bearing wastes and nickel-cadmium (“Ni-Cd”) batteries

– Zochem: Producer of zinc oxide located in Brampton, Ontario

Leading market position in most markets served

– Largest zinc producer in U.S.

– Largest zinc oxide producer in North America

– Largest recycler of EAF dust in the world (providing low-cost feed)

– Leading environmental service provider to the U.S. Steel industry

State-of-the-art environmentally friendly low operating cost zinc plant under construction

– Recently completed financing expected to provide remaining capital required

– Expansion of zinc oxide capacity underway at Zochem

Adjusted EBITDA ($ millions) (1)

$138

$163

$68

-$10

$64 $63

$46

-$20

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2006 2007 2008 2009* 2010 2011 3/31/12LTM

* 2009 hedging value of $50.3 million was recognized in 2008.(1) Adjusted EBITDA is a supplemental measure that is not required by, or presented, in accordance with, GAAP. For a reconciliation of Adjusted EBITDA to net income, seeAppendix A to this presentation.

$217

$496

$546

$446

$382

$451$475

0

100

200

300

400

500

$600

2006 2007 2008 2009 2010 2011 6/30/2012

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

$2.00

(Revenue, US$ in millions) (LME Zinc Prices)

Revenue vs. LME Zinc Prices

4

Operations Footprint

Calumet, IL

Recycling Facility:

EAFD: 169,000(1)

Tons

Pittsburgh, PA

Monaca, PA Facility

Finished Products:

PW Metal: 88,000 Tons

Zinc Oxide: 90,000 Tons

SSGH Metal: 15,000 Tons

Zinc Dust: 5,900 Tons

Palmerton, PA

Recycling Facility

Calcine: 130,000(2) Tons

EAFD: 273,000 Tons (1)

Zinc Powder: 5,000 -14,000(3)

Tons

Finished Products

Zinc Copper Base: 3,000Tons

Barnwell, SC

Recycling Facility:

EAFD: 180,000(1) Tons

Rockwood, TN

Recycling Facility:

EAFD: 148,000 Tons (1)

Ellwood City, PA

INMETCO Recycling Facility:

EAFD and other waste: 70,000 Tons

Cadmium: 5,000 tons

Under construction

Acquired in 2011

Built in 2010

Acquired in 2009

Other operating facilities

Rutherford Co., NC

New Zinc Plant

Under Construction

Projected Operating Level:

155,000 Tons of SHG, CGG& PW metal

Brampton, ON, Canada

Zochem Facility

Finished Products:

Zinc Oxide: 49,600 Tons

Horsehead has production and/or recycling operations at seven facilities in seven locations

Note: Number of tons denotes annual capacity.

EAF Recycling: 770,000 Tons

Smelting: 140,000 Tons

Existing Capacity

Note: Excludes New North Carolina Plant.

(1) Represents EAF dust and other metal-bearing wastes recycling and processing capacity.(2) Assumes that one of four kilns is operated to produce calcine and the other three kilns are operated to produce waelz oxide.(3) Depending upon grade.

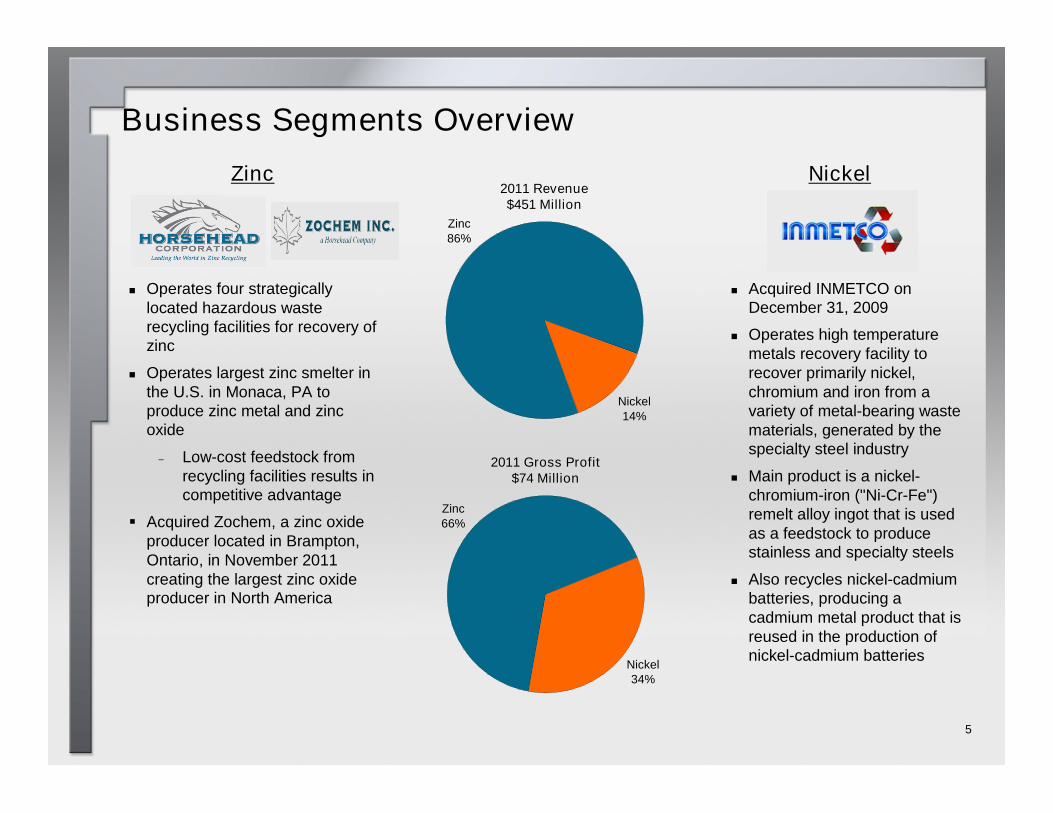

Business Segments Overview

Operates four strategicallylocated hazardous wasterecycling facilities for recovery ofzinc

Operates largest zinc smelter inthe U.S. in Monaca, PA toproduce zinc metal and zincoxide

– Low-cost feedstock fromrecycling facilities results incompetitive advantage

Acquired Zochem, a zinc oxideproducer located in Brampton,Ontario, in November 2011creating the largest zinc oxideproducer in North America

5

Acquired INMETCO onDecember 31, 2009

Operates high temperaturemetals recovery facility torecover primarily nickel,chromium and iron from avariety of metal-bearing wastematerials, generated by thespecialty steel industry

Main product is a nickel-chromium-iron ("Ni-Cr-Fe")remelt alloy ingot that is usedas a feedstock to producestainless and specialty steels

Also recycles nickel-cadmiumbatteries, producing acadmium metal product that isreused in the production ofnickel-cadmium batteries

Zinc Nickel

Nickel14%

Zinc86%

2011 Revenue$451 Million

2011 Gross Profit$74 Million

Nickel34%

Zinc66%

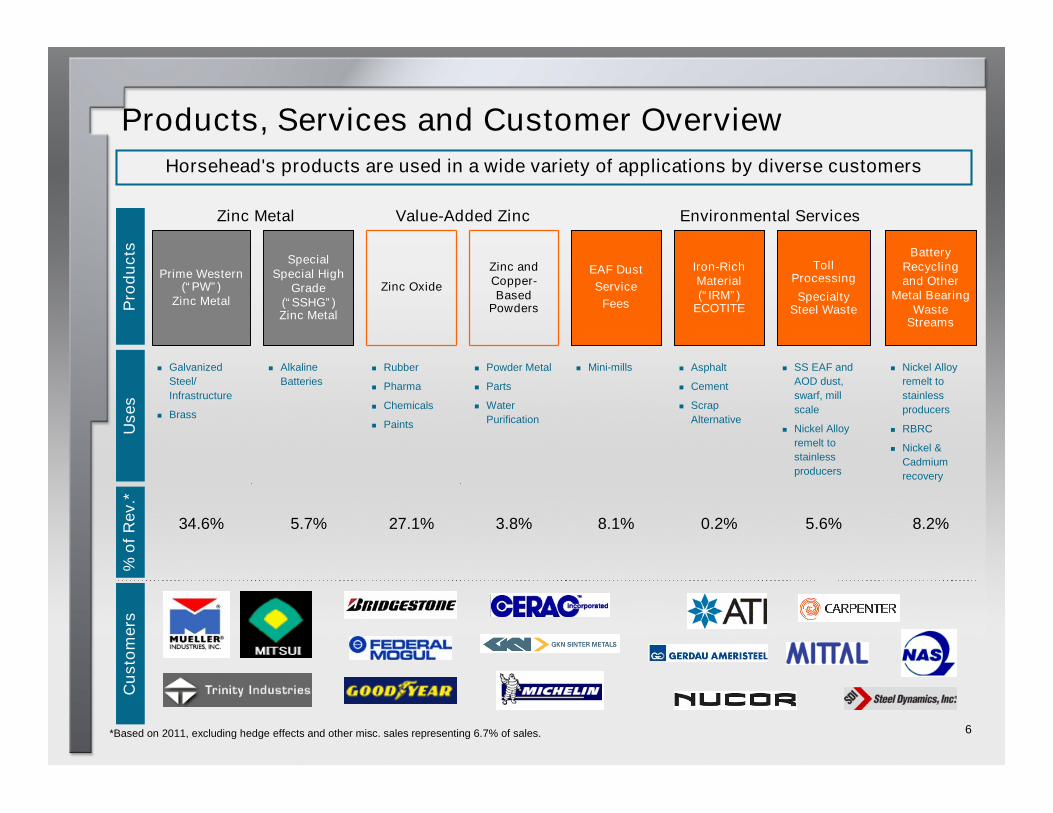

Products, Services and Customer Overview

Prime Western(“PW”)

Zinc Metal

SpecialSpecial High

Grade(“SSHG”)Zinc Metal

Zinc Oxide

Zinc andCopper-Based

Powders

EAF Dust

Service

Fees

Iron-RichMaterial(“IRM”)

ECOTITE

TollProcessing

SpecialtySteel Waste

BatteryRecyclingand Other

Metal BearingWaste

Streams

Galvanized

Steel/

Infrastructure

Brass

Alkaline

Batteries

Rubber

Pharma

Chemicals

Paints

Powder Metal

Parts

Water

Purification

Mini-mills Asphalt

Cement

Scrap

Alternative

SS EAF and

AOD dust,

swarf, mill

scale

Nickel Alloy

remelt to

stainless

producers

Nickel Alloy

remelt to

stainless

producers

RBRC

Nickel &

Cadmium

recovery

34.6% 5.7% 27.1% 3.8% 8.1% 0.2% 5.6% 8.2%

Value-Added Zinc Environmental ServicesZinc Metal

*Based on 2011, excluding hedge effects and other misc. sales representing 6.7% of sales.

Horsehead's products are used in a wide variety of applications by diverse customers

Pro

du

cts

Uses

%o

fR

ev.*

Cu

sto

me

rs

6

7

New Zinc Plant — Green Technology at a SubstantiallyLower Cost

Current 80 year old zinc smelter utilizes a high-cost electrothermic process which produces a limited product range andfaces increasing environmental pressures

New plant will utilize a state-of-the-art, “green” technology based on solvent extraction and electro-winning technology

Benefits:

– Lower energy usage, higher labor productivity and reduced maintenance costs

– Produces Special High Grade (“SHG”) and Continuous Galvanizing Grade (“CGG”) in addition to the PrimeWestern Grade produced by current smelter thus serving a much larger market with higher premiums

– Recovery of value from silver and lead in electric arc furnace (“EAF”) dust and higher premiums onSHG and CGG

Positions the Company among the global low cost producers when combined with our EAF-based feed

New facility is currently expected to expand EBITDA by approximately $90 to $110 million by 2014

(1) Due to cost reductions and higher zinc recoveries.

(2) For a reconciliation of Adjusted EBITDA to net income, see Appendix A to this presentation.

Existing Smelter New Zinc FacilityIncremental Annual Adj. EBITDA

Contribution ($ million)(2)

Manufacturing Conversion Cost ~$0.38/lb ~$0.22 — $0.24/lb $46 to $50

Reduced Feed Cost(1) $0.41/lb $0.35/lb 16 to 20

Higher Co-Product Value N/A Increased Revenue: $15 to $25 million/year 15 to 25

Higher SHG/CGG Premium N/A Increased Revenue: $8 to $10 million/year 8 to 10

Volume Expansion and Other 140,000 tpy contained zinc 155,000 tpy contained zinc 5 to 5

Total: $90 to $110

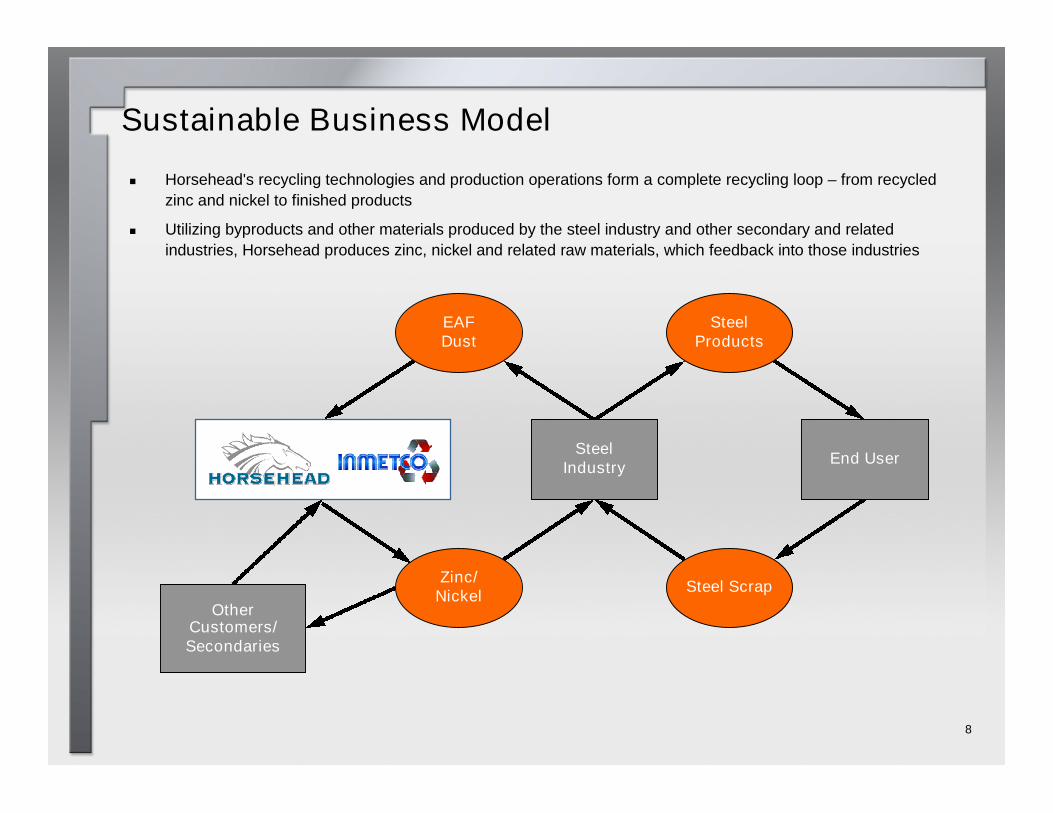

Horsehead's recycling technologies and production operations form a complete recycling loop – from recycled

zinc and nickel to finished products

Utilizing byproducts and other materials produced by the steel industry and other secondary and related

industries, Horsehead produces zinc, nickel and related raw materials, which feedback into those industries

8

Sustainable Business Model

EAFDust

SteelProducts

Steel Scrap

OtherCustomers/Secondaries

End UserSteel

Industry

Zinc/Nickel

9

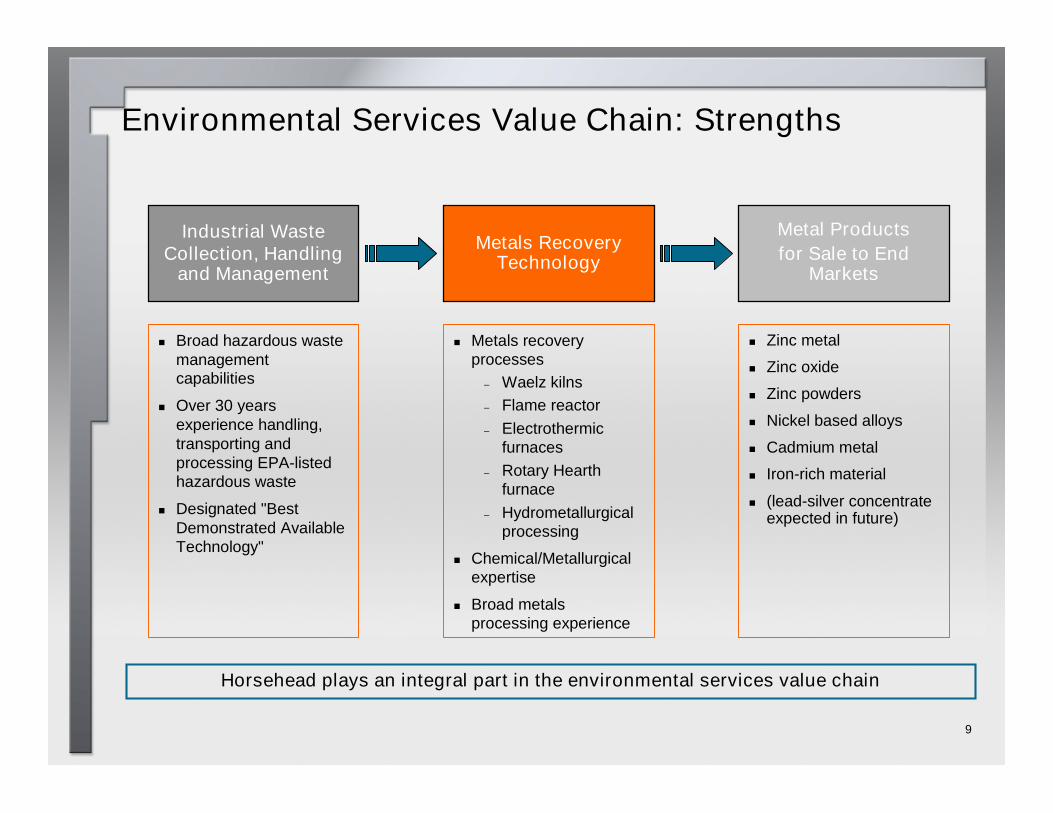

Environmental Services Value Chain: Strengths

Industrial WasteCollection, Handling

and Management

Metals RecoveryTechnology

Metal Products

for Sale to EndMarkets

Broad hazardous wastemanagementcapabilities

Over 30 yearsexperience handling,transporting andprocessing EPA-listedhazardous waste

Designated "BestDemonstrated AvailableTechnology"

Zinc metal

Zinc oxide

Zinc powders

Nickel based alloys

Cadmium metal

Iron-rich material

(lead-silver concentrateexpected in future)

Metals recoveryprocesses

– Waelz kilns

– Flame reactor

– Electrothermicfurnaces

– Rotary Hearthfurnace

– Hydrometallurgicalprocessing

Chemical/Metallurgicalexpertise

Broad metalsprocessing experience

Horsehead plays an integral part in the environmental services value chain

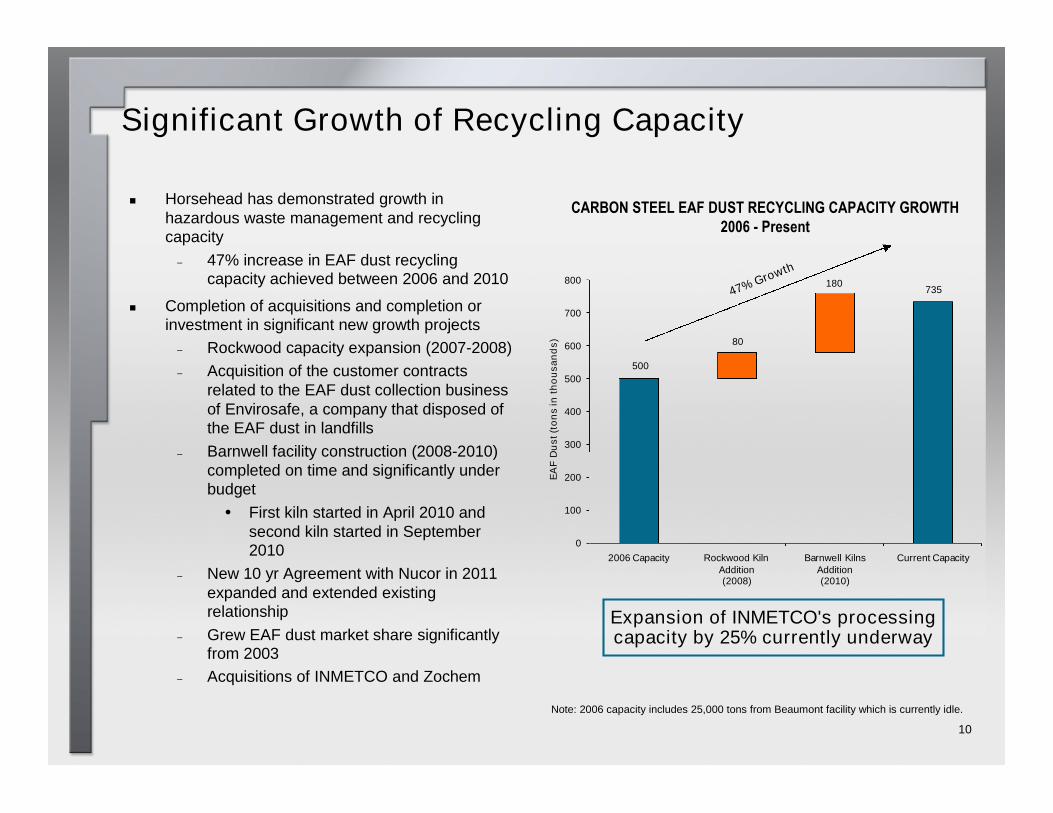

500

735

80

180

0

100

200

300

400

500

600

700

800

2006 Capacity Rockwood KilnAddition(2008)

Barnwell KilnsAddition(2010)

Current CapacityE

AF

Du

st

(to

ns

inth

ou

sa

nd

s)

Significant Growth of Recycling Capacity

Horsehead has demonstrated growth inhazardous waste management and recyclingcapacity

– 47% increase in EAF dust recyclingcapacity achieved between 2006 and 2010

Completion of acquisitions and completion orinvestment in significant new growth projects

– Rockwood capacity expansion (2007-2008)

– Acquisition of the customer contractsrelated to the EAF dust collection businessof Envirosafe, a company that disposed ofthe EAF dust in landfills

– Barnwell facility construction (2008-2010)completed on time and significantly underbudget

• First kiln started in April 2010 andsecond kiln started in September2010

– New 10 yr Agreement with Nucor in 2011expanded and extended existingrelationship

– Grew EAF dust market share significantlyfrom 2003

– Acquisitions of INMETCO and Zochem

47% Growth

CARBON STEEL EAF DUST RECYCLING CAPACITY GROWTH2006 - Present

Note: 2006 capacity includes 25,000 tons from Beaumont facility which is currently idle.

10

Expansion of INMETCO's processingcapacity by 25% currently underway

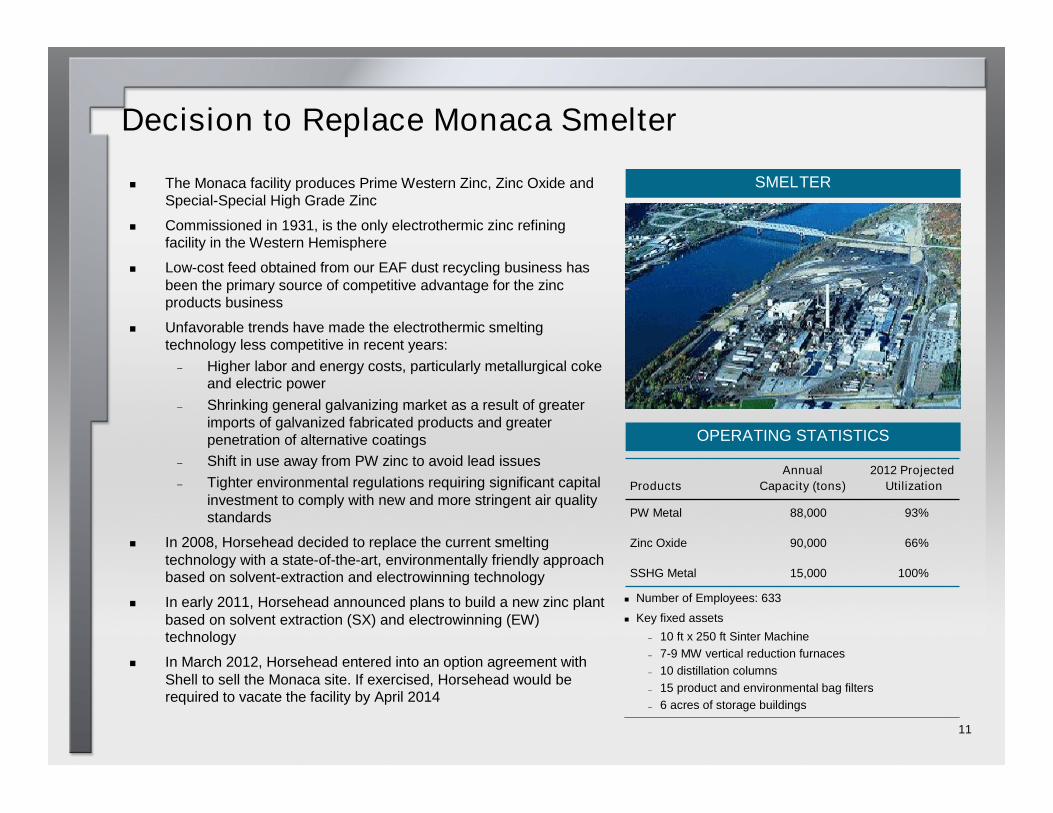

The Monaca facility produces Prime Western Zinc, Zinc Oxide andSpecial-Special High Grade Zinc

Commissioned in 1931, is the only electrothermic zinc refiningfacility in the Western Hemisphere

Low-cost feed obtained from our EAF dust recycling business hasbeen the primary source of competitive advantage for the zincproducts business

Unfavorable trends have made the electrothermic smeltingtechnology less competitive in recent years:

– Higher labor and energy costs, particularly metallurgical cokeand electric power

– Shrinking general galvanizing market as a result of greaterimports of galvanized fabricated products and greaterpenetration of alternative coatings

– Shift in use away from PW zinc to avoid lead issues

– Tighter environmental regulations requiring significant capitalinvestment to comply with new and more stringent air qualitystandards

In 2008, Horsehead decided to replace the current smeltingtechnology with a state-of-the-art, environmentally friendly approachbased on solvent-extraction and electrowinning technology

In early 2011, Horsehead announced plans to build a new zinc plantbased on solvent extraction (SX) and electrowinning (EW)technology

In March 2012, Horsehead entered into an option agreement withShell to sell the Monaca site. If exercised, Horsehead would berequired to vacate the facility by April 2014

SMELTER

OPERATING STATISTICS

11

Products

Annual

Capacity (tons)

2012 Projected

Utilization

PW Metal 88,000 93%

Zinc Oxide 90,000 66%

SSHG Metal 15,000 100%

Decision to Replace Monaca Smelter

Number of Employees: 633

Key fixed assets

– 10 ft x 250 ft Sinter Machine

– 7-9 MW vertical reduction furnaces

– 10 distillation columns

– 15 product and environmental bag filters

– 6 acres of storage buildings

New Zinc Plant Overview

13

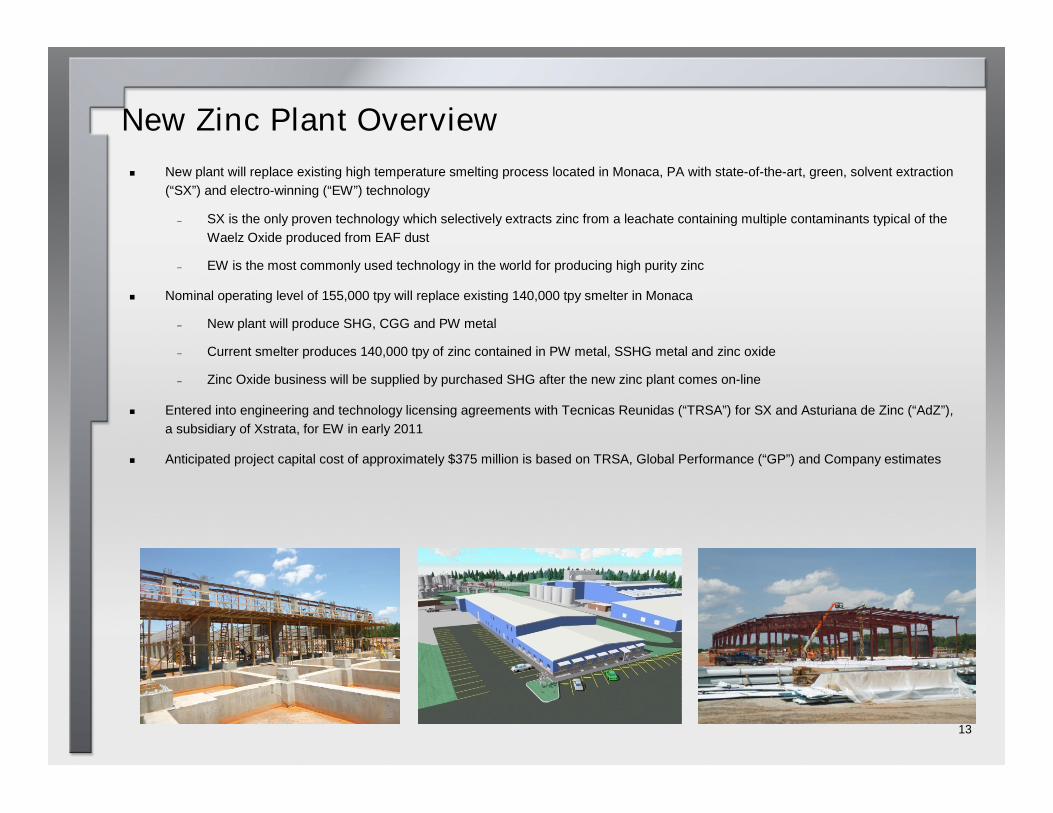

New Zinc Plant Overview

New plant will replace existing high temperature smelting process located in Monaca, PA with state-of-the-art, green, solvent extraction

(“SX”) and electro-winning (“EW”) technology

– SX is the only proven technology which selectively extracts zinc from a leachate containing multiple contaminants typical of the

Waelz Oxide produced from EAF dust

– EW is the most commonly used technology in the world for producing high purity zinc

Nominal operating level of 155,000 tpy will replace existing 140,000 tpy smelter in Monaca

– New plant will produce SHG, CGG and PW metal

– Current smelter produces 140,000 tpy of zinc contained in PW metal, SSHG metal and zinc oxide

– Zinc Oxide business will be supplied by purchased SHG after the new zinc plant comes on-line

Entered into engineering and technology licensing agreements with Tecnicas Reunidas (“TRSA”) for SX and Asturiana de Zinc (“AdZ”),

a subsidiary of Xstrata, for EW in early 2011

Anticipated project capital cost of approximately $375 million is based on TRSA, Global Performance (“GP”) and Company estimates

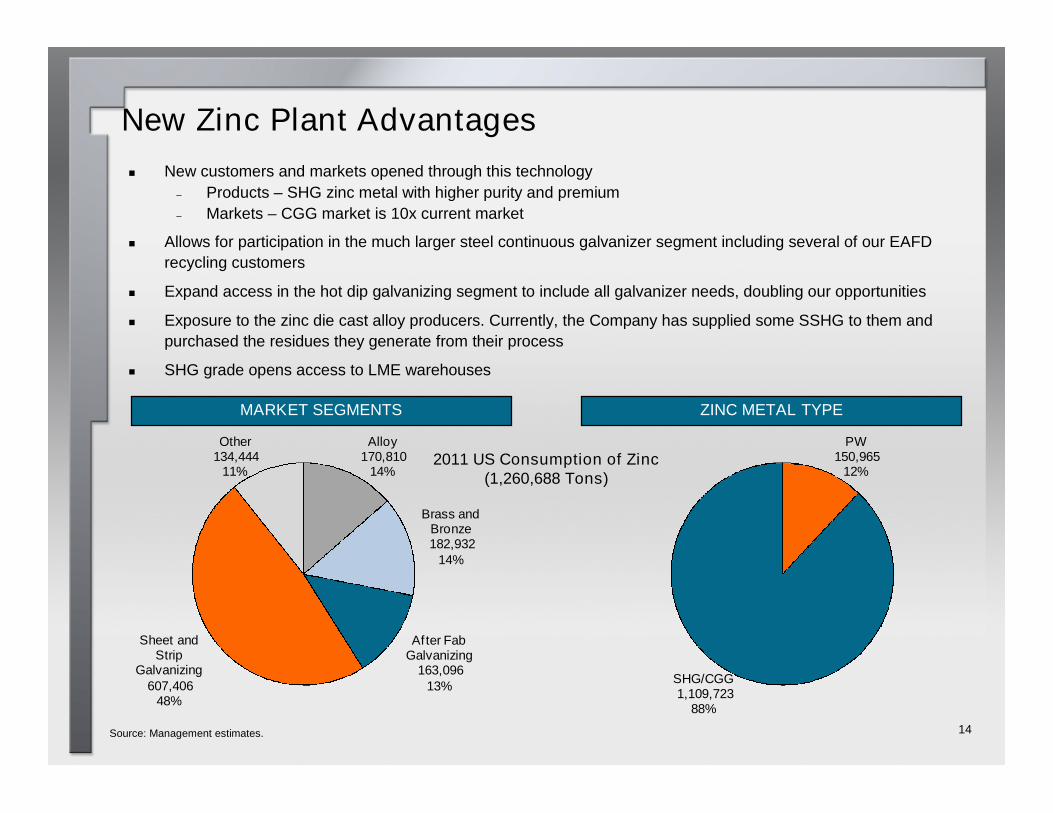

New customers and markets opened through this technology

– Products – SHG zinc metal with higher purity and premium

– Markets – CGG market is 10x current market

Allows for participation in the much larger steel continuous galvanizer segment including several of our EAFD

recycling customers

Expand access in the hot dip galvanizing segment to include all galvanizer needs, doubling our opportunities

Exposure to the zinc die cast alloy producers. Currently, the Company has supplied some SSHG to them and

purchased the residues they generate from their process

SHG grade opens access to LME warehouses

MARKET SEGMENTS ZINC METAL TYPE

New Zinc Plant Advantages

14

2011 US Consumption of Zinc(1,260,688 Tons)

Source: Management estimates.

Alloy170,810

14%

Brass andBronze182,932

14%

After FabGalvanizing

163,09613%

Sheet andStrip

Galvanizing607,406

48%

Other134,444

11%

PW150,965

12%

SHG/CGG1,109,723

88%

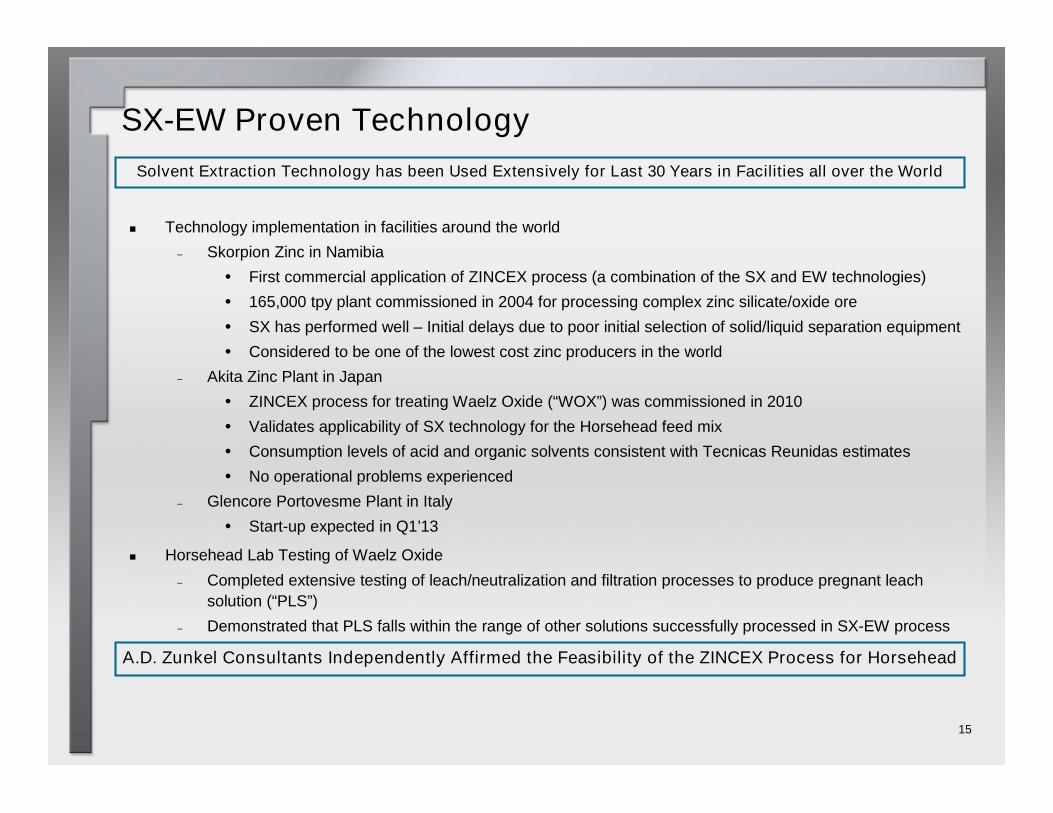

SX-EW Proven Technology

Technology implementation in facilities around the world

– Skorpion Zinc in Namibia

• First commercial application of ZINCEX process (a combination of the SX and EW technologies)

• 165,000 tpy plant commissioned in 2004 for processing complex zinc silicate/oxide ore

• SX has performed well – Initial delays due to poor initial selection of solid/liquid separation equipment

• Considered to be one of the lowest cost zinc producers in the world

– Akita Zinc Plant in Japan

• ZINCEX process for treating Waelz Oxide (“WOX”) was commissioned in 2010

• Validates applicability of SX technology for the Horsehead feed mix

• Consumption levels of acid and organic solvents consistent with Tecnicas Reunidas estimates

• No operational problems experienced

– Glencore Portovesme Plant in Italy

• Start-up expected in Q1’13

Horsehead Lab Testing of Waelz Oxide

– Completed extensive testing of leach/neutralization and filtration processes to produce pregnant leach

solution (“PLS”)

– Demonstrated that PLS falls within the range of other solutions successfully processed in SX-EW process

15

Solvent Extraction Technology has been Used Extensively for Last 30 Years in Facilities all over the World

A.D. Zunkel Consultants Independently Affirmed the Feasibility of the ZINCEX Process for Horsehead

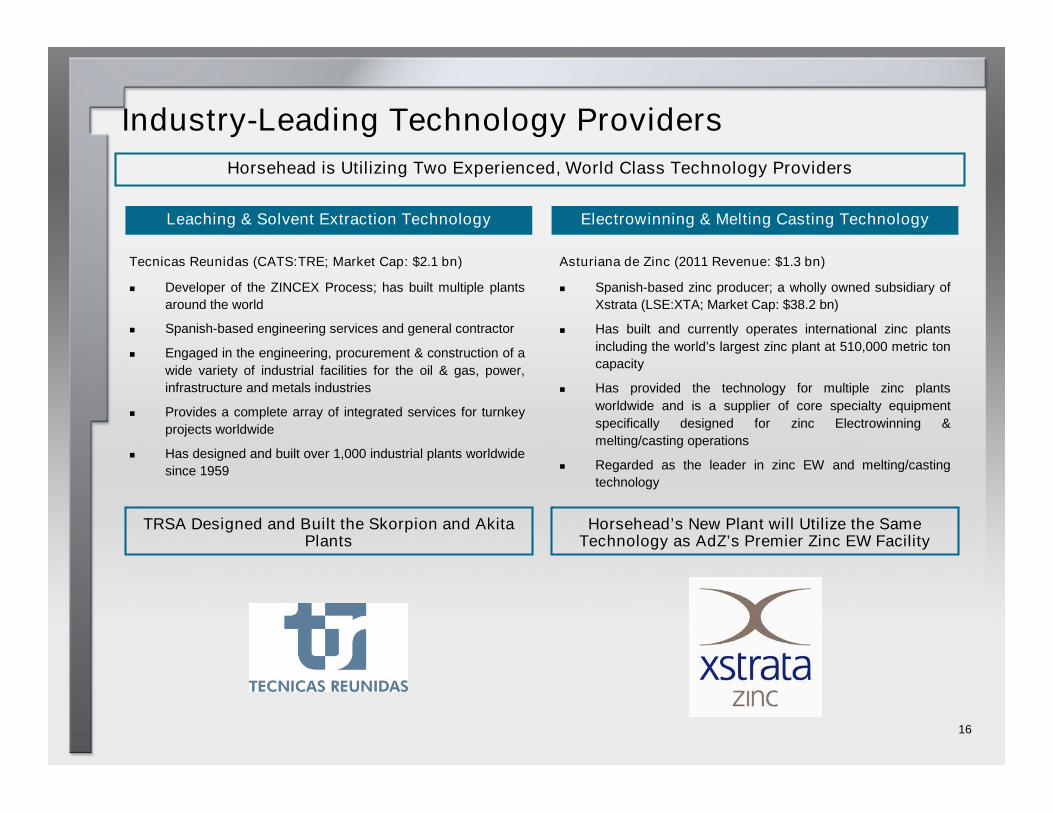

Industry-Leading Technology Providers

Tecnicas Reunidas (CATS:TRE; Market Cap: $2.1 bn)

Developer of the ZINCEX Process; has built multiple plants

around the world

Spanish-based engineering services and general contractor

Engaged in the engineering, procurement & construction of a

wide variety of industrial facilities for the oil & gas, power,

infrastructure and metals industries

Provides a complete array of integrated services for turnkey

projects worldwide

Has designed and built over 1,000 industrial plants worldwide

since 1959

Electrowinning & Melting Casting TechnologyLeaching & Solvent Extraction Technology

Asturiana de Zinc (2011 Revenue: $1.3 bn)

Spanish-based zinc producer; a wholly owned subsidiary of

Xstrata (LSE:XTA; Market Cap: $38.2 bn)

Has built and currently operates international zinc plants

including the world’s largest zinc plant at 510,000 metric ton

capacity

Has provided the technology for multiple zinc plants

worldwide and is a supplier of core specialty equipment

specifically designed for zinc Electrowinning &

melting/casting operations

Regarded as the leader in zinc EW and melting/casting

technology

TRSA Designed and Built the Skorpion and AkitaPlants

Horsehead’s New Plant will Utilize the SameTechnology as AdZ’s Premier Zinc EW Facility

Horsehead is Utilizing Two Experienced, World Class Technology Providers

16

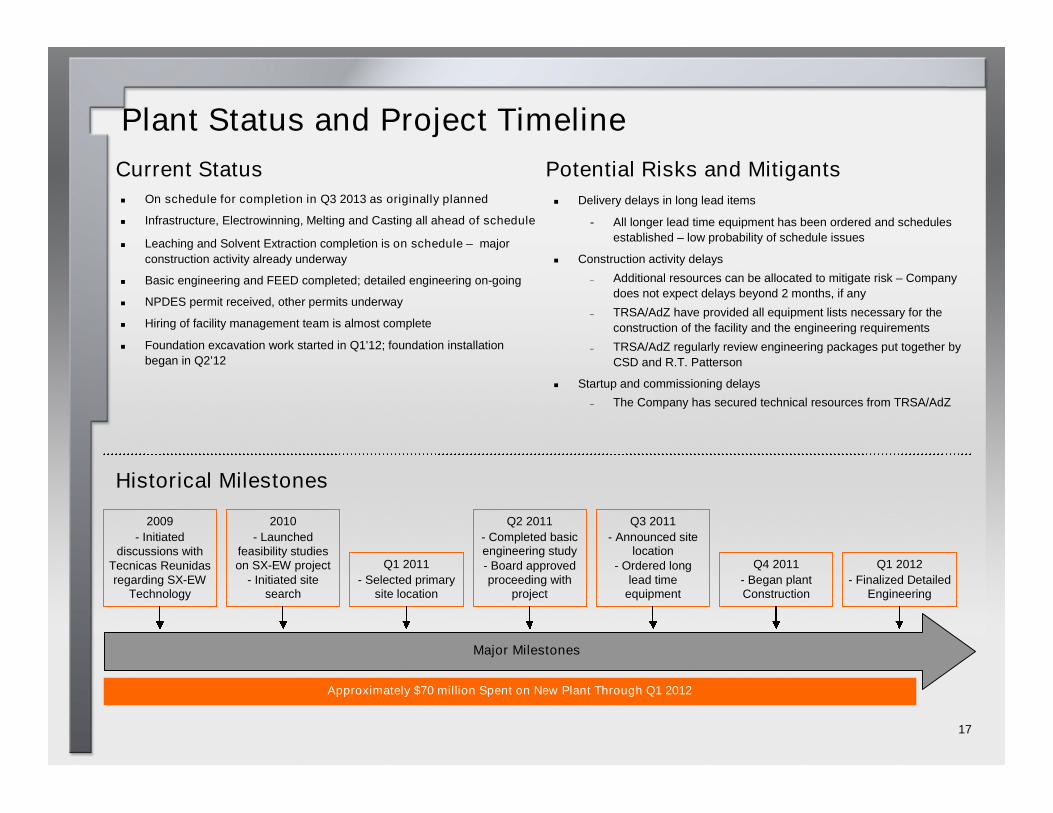

Historical Milestones

Plant Status and Project Timeline

17

Major Milestones

Q3 2011

- Announced sitelocation

- Ordered longlead time

equipment

Q4 2011

- Began plantConstruction

Q2 2011

- Completed basicengineering study- Board approvedproceeding with

project

2009

- Initiateddiscussions with

Tecnicas Reunidasregarding SX-EW

Technology

2010

- Launchedfeasibility studieson SX-EW project

- Initiated sitesearch

Q1 2011

- Selected primarysite location

On schedule for completion in Q3 2013 as originally planned

Infrastructure, Electrowinning, Melting and Casting all ahead of schedule

Leaching and Solvent Extraction completion is on schedule – major

construction activity already underway

Basic engineering and FEED completed; detailed engineering on-going

NPDES permit received, other permits underway

Hiring of facility management team is almost complete

Foundation excavation work started in Q1’12; foundation installation

began in Q2’12

Current Status

Q1 2012

- Finalized DetailedEngineering

Approximately $70 million Spent on New Plant Through Q1 2012

Delivery delays in long lead items

- All longer lead time equipment has been ordered and schedules

established – low probability of schedule issues

Construction activity delays

– Additional resources can be allocated to mitigate risk – Company

does not expect delays beyond 2 months, if any

– TRSA/AdZ have provided all equipment lists necessary for the

construction of the facility and the engineering requirements

– TRSA/AdZ regularly review engineering packages put together by

CSD and R.T. Patterson

Startup and commissioning delays

– The Company has secured technical resources from TRSA/AdZ

Potential Risks and Mitigants

Plant Status and Project Timeline (Cont.)

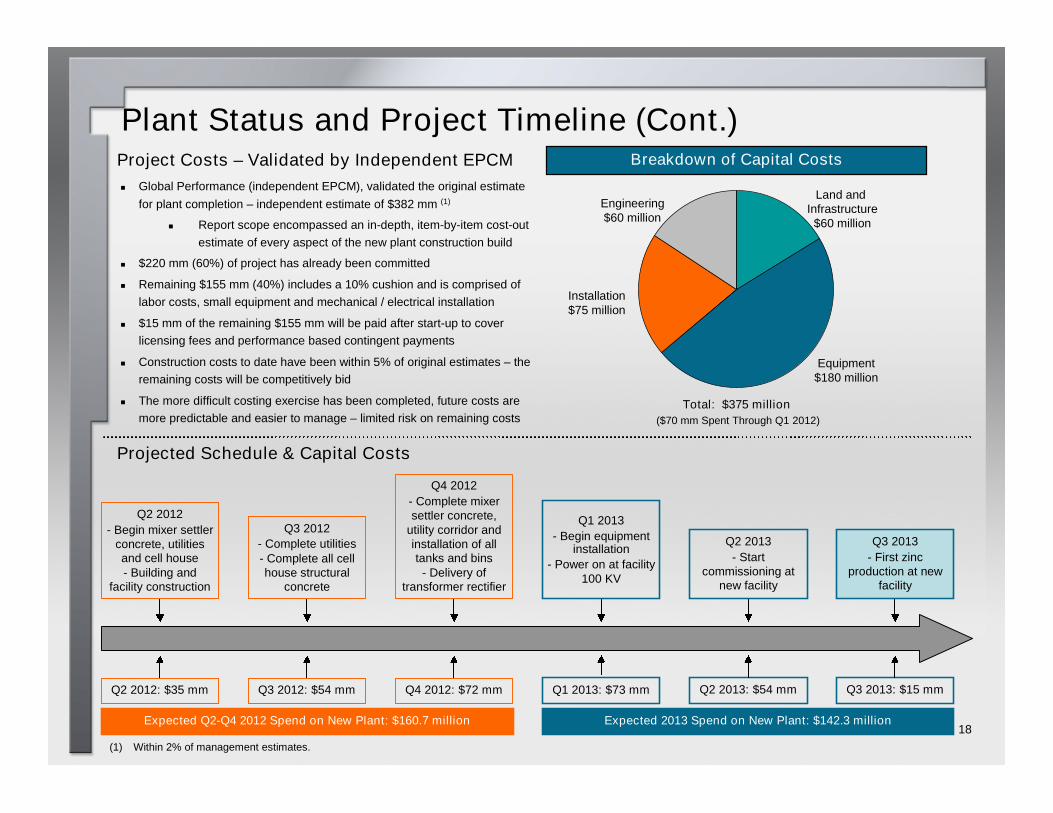

18

Global Performance (independent EPCM), validated the original estimate

for plant completion – independent estimate of $382 mm (1)

Report scope encompassed an in-depth, item-by-item cost-out

estimate of every aspect of the new plant construction build

$220 mm (60%) of project has already been committed

Remaining $155 mm (40%) includes a 10% cushion and is comprised of

labor costs, small equipment and mechanical / electrical installation

$15 mm of the remaining $155 mm will be paid after start-up to cover

licensing fees and performance based contingent payments

Construction costs to date have been within 5% of original estimates – the

remaining costs will be competitively bid

The more difficult costing exercise has been completed, future costs are

more predictable and easier to manage – limited risk on remaining costs

Project Costs – Validated by Independent EPCM

Q2 2012

- Begin mixer settlerconcrete, utilitiesand cell house- Building and

facility construction

Q3 2012

- Complete utilities- Complete all cellhouse structural

concrete

Q4 2012

- Complete mixersettler concrete,

utility corridor andinstallation of alltanks and bins

- Delivery oftransformer rectifier

Q1 2013

- Begin equipmentinstallation

- Power on at facility100 KV

Q2 2013

- Startcommissioning at

new facility

Q3 2013

- First zincproduction at new

facility

Q1 2013: $73 mm Q2 2013: $54 mm Q3 2013: $15 mmQ2 2012: $35 mm Q3 2012: $54 mm Q4 2012: $72 mm

Expected 2013 Spend on New Plant: $142.3 millionExpected Q2-Q4 2012 Spend on New Plant: $160.7 million

Total: $375 million

Engineering$60 million

Land andInfrastructure

$60 million

Equipment$180 million

Installation$75 million

Breakdown of Capital Costs

Projected Schedule & Capital Costs

($70 mm Spent Through Q1 2012)

(1) Within 2% of management estimates.

Financial Overview

Revenue vs. LME Zinc Prices

Adjusted EBITDA and Margin (1)

20

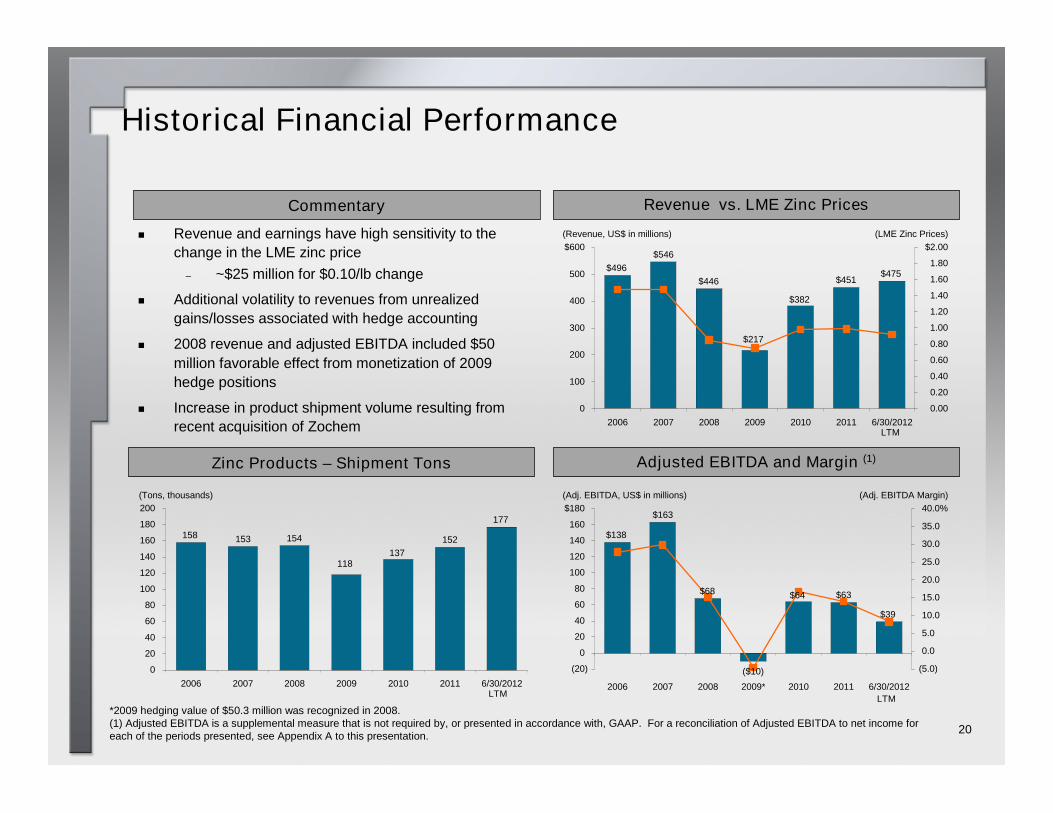

Historical Financial Performance

*2009 hedging value of $50.3 million was recognized in 2008.(1) Adjusted EBITDA is a supplemental measure that is not required by, or presented in accordance with, GAAP. For a reconciliation of Adjusted EBITDA to net income foreach of the periods presented, see Appendix A to this presentation.

Revenue and earnings have high sensitivity to the

change in the LME zinc price

– ~$25 million for $0.10/lb change

Additional volatility to revenues from unrealized

gains/losses associated with hedge accounting

2008 revenue and adjusted EBITDA included $50

million favorable effect from monetization of 2009

hedge positions

Increase in product shipment volume resulting from

recent acquisition of Zochem

Commentary

Zinc Products – Shipment Tons

118

177

152

137

154153158

0

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 6/30/2012

(Tons, thousands)

$217

$496

$546

$446

$382

$451$475

0

100

200

300

400

500

$600

2006 2007 2008 2009 2010 2011 6/30/2012

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

$2.00

(Revenue, US$ in millions) (LME Zinc Prices)

LTMLTM

LTM

($10)

$138

$163

$68 $64 $63

$39

(20)

0

20

40

60

80

100

120

140

160

$180

2006 2007 2008 2009* 2010 2011 6/30/2012

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0%

(Adj. EBITDA, US$ in millions) (Adj. EBITDA Margin)

21

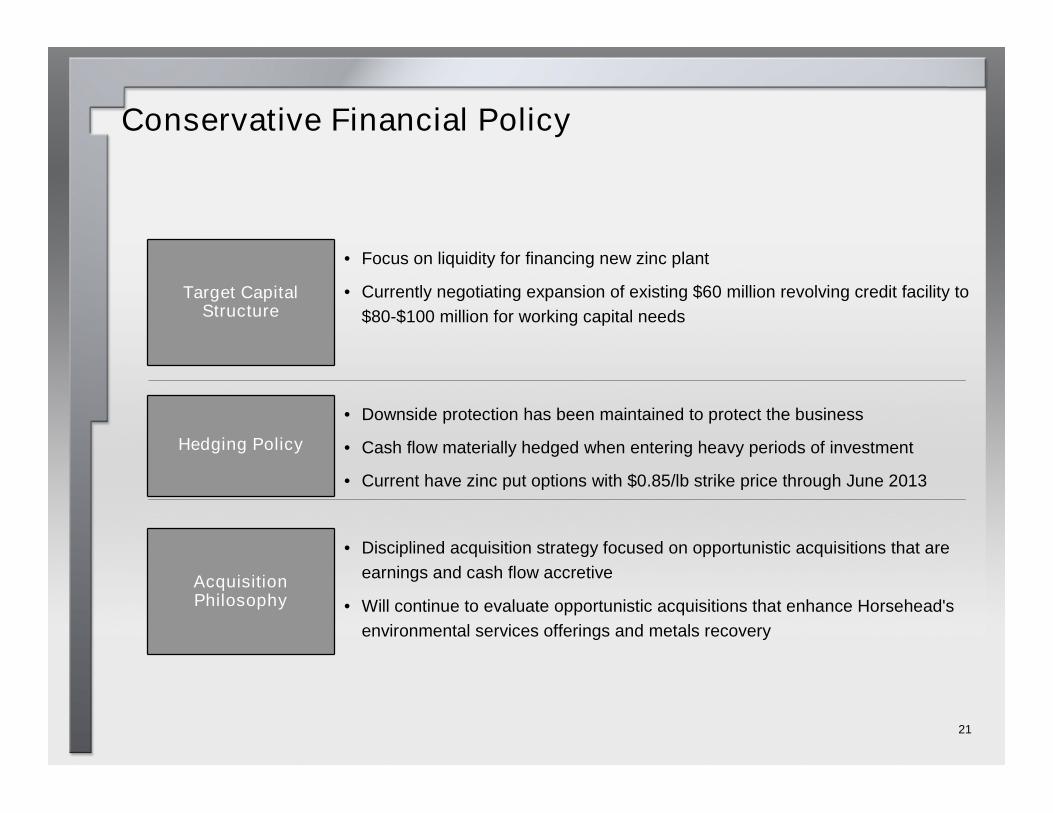

Conservative Financial Policy

Target CapitalStructure

• Focus on liquidity for financing new zinc plant

• Currently negotiating expansion of existing $60 million revolving credit facility to

$80-$100 million for working capital needs

Hedging Policy

• Downside protection has been maintained to protect the business

• Cash flow materially hedged when entering heavy periods of investment

• Current have zinc put options with $0.85/lb strike price through June 2013

AcquisitionPhilosophy

• Disciplined acquisition strategy focused on opportunistic acquisitions that are

earnings and cash flow accretive

• Will continue to evaluate opportunistic acquisitions that enhance Horsehead's

environmental services offerings and metals recovery

Illustrative EBITDA Sensitivity

22

Adj. EBITDA at Various Levels of LME Zinc Prices*

52-week High & Low Range of LME Zinc Prices$0.79 - $1.13

*The slide shows the illustrative effect of a change in the LME zinc price on Adj. EBITDA for zinc products from the current zinc production facility in Monaca, PA (“StatusQuo”) versus the new zinc production facility in North Carolina (“SX-EW”). The Status Quo scenario assumes 142,000 tons of zinc production versus 156,000 tons of zincproduction in the SX-EW scenario. The change in Adj. EBITDA does not include any price change for other metals (lead and silver) or contributions from INMETCO andZochem.

LME Zinc Prices

Ad

j.E

BIT

DA

Status Quo With SX-EW

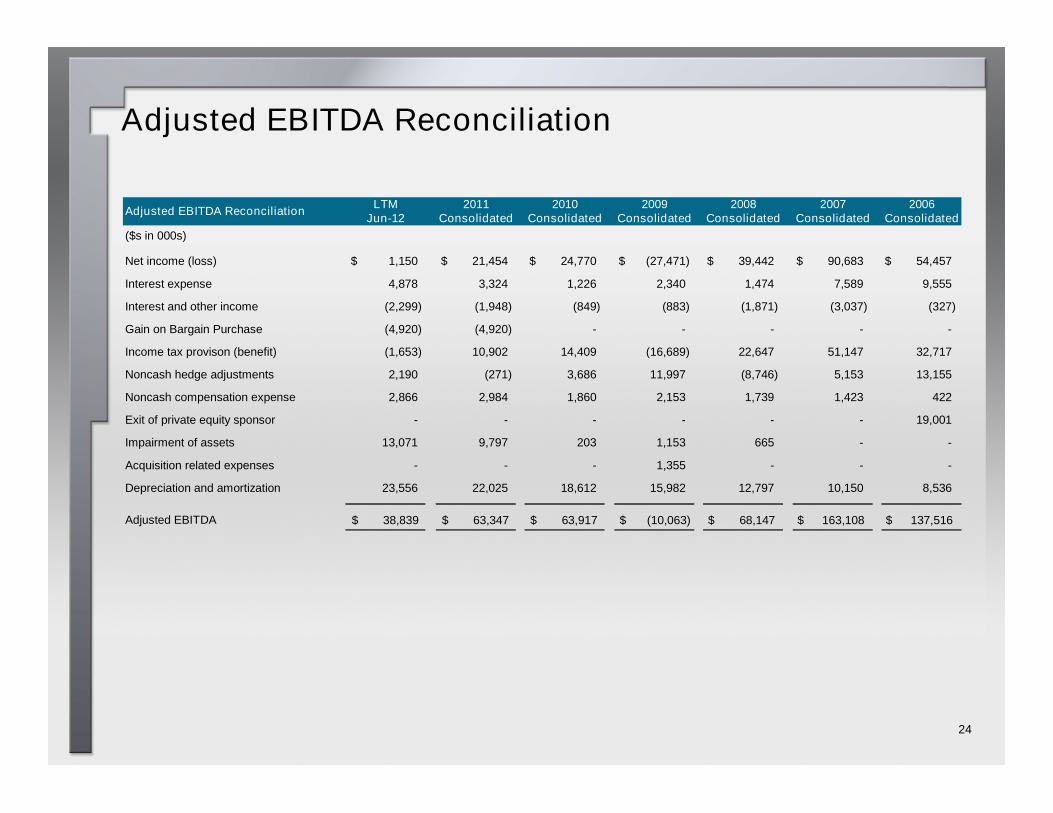

Appendix A

24

Adjusted EBITDA Reconciliation

LTM 2011 2010 2009 2008 2007 2006Jun-12 Consolidated Consolidated Consolidated Consolidated Consolidated Consolidated

($s in 000s)

Net income (loss) 1,150$ 21,454$ 24,770$ (27,471)$ 39,442$ 90,683$ 54,457$

Interest expense 4,878 3,324 1,226 2,340 1,474 7,589 9,555

Interest and other income (2,299) (1,948) (849) (883) (1,871) (3,037) (327)

Gain on Bargain Purchase (4,920) (4,920) - - - - -

Income tax provison (benefit) (1,653) 10,902 14,409 (16,689) 22,647 51,147 32,717

Noncash hedge adjustments 2,190 (271) 3,686 11,997 (8,746) 5,153 13,155

Noncash compensation expense 2,866 2,984 1,860 2,153 1,739 1,423 422

Exit of private equity sponsor - - - - - - 19,001

Impairment of assets 13,071 9,797 203 1,153 665 - -

Acquisition related expenses - - - 1,355 - - -

Depreciation and amortization 23,556 22,025 18,612 15,982 12,797 10,150 8,536

Adjusted EBITDA 38,839$ 63,347$ 63,917$ (10,063)$ 68,147$ 163,108$ 137,516$

Adjusted EBITDA Reconciliation