Hotels & Leisure Market in Minutes May 2015 Savills World Research Ireland Hotels Economic Overview Ireland was Europe’s fastest growing economy in 2014 with GDP expanding by 4.8%. This was the sharpest rate of increase since 2007 and reflects the combination of continued strong net exports growth (10.4%) in addition to a return of domestic demand growth (2.9%) for the first time in seven years. Moreover, according to the Dublin Economic Monitor, consumer sentiment in the city is at its highest point since the series began in 2003. In turn this has led to a strong improvement in the labour market with nearly 30,000 new jobs (net) created in Ireland in 2014. This brings the total number of new jobs added since the Q1 2012 trough to 114,000. The tourism sector has been a big winner in the recovery accounting for nearly a fifth of total employment growth since Q1 2012. Strong GDP growth in Ireland’s main tourist markets (2.4% in the US and 2.8% in the UK in 2014), a significant decline in the value of the Euro (-22.2% vs the Dollar and -13.1% vs Sterling in the year to April 22nd 2015) and the reduced VAT rate on tourism (13.5% to 9% in July 2011) have all contributed to increased numbers of foreign visitors. Over 7.6m non-residents visited Ireland in 2014, the highest number since 2008. In addition, a further 14% growth in visitor numbers was recorded in Q1 2015. In terms of trips taken by Irish residents, there has also been positive momentum. Improvements in the consumer economy including real wage (2.6%) and consumption growth (1.1%) contributed to 7.4m domestic trips in 2014, an increase of 3.4% on 2013 and the highest in five years. Moreover, the number of domestic trips was up a further 13.2% in Q1 2015. ■ GRAPH 1 Trips Taken in Ireland by Origin of Visitor Source: CSO 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 2008 2009 2010 2011 2012 2013 2014 No. of Trips (000s) Overseas Domestic Ballsbridge Hotel – Part of Project Trinity launched Q2 2015

Transcript

Hotels & Leisure Market in Minutes May 2015

Savills World Research Ireland Hotels

Economic OverviewIreland was Europe’s fastest growing economy in 2014 with GDP expanding by 4.8%. This was the sharpest rate of increase since 2007 and reflects the combination of continued strong net exports growth (10.4%) in addition to a return of domestic demand growth (2.9%) for the first time in seven years. Moreover, according to the Dublin Economic Monitor, consumer sentiment in the city is at its highest point since the series began in 2003. In turn this has led to a strong improvement in the labour market with nearly 30,000 new jobs (net) created in Ireland in 2014. This brings the total number of new jobs added since the Q1 2012 trough to 114,000.

The tourism sector has been a big winner in the recovery accounting for nearly a fifth of total employment growth since Q1 2012. Strong GDP growth in Ireland’s main tourist markets (2.4% in the US and 2.8% in the UK in 2014), a significant decline in the value of the Euro (-22.2% vs the Dollar and -13.1% vs Sterling in the year to April 22nd 2015) and the reduced VAT rate on tourism (13.5% to 9% in July 2011) have all contributed to increased numbers of foreign visitors. Over 7.6m non-residents visited Ireland in 2014, the highest number since 2008. In addition, a further 14% growth in visitor numbers was recorded in Q1 2015. In terms of trips taken by Irish residents, there has also been positive momentum. Improvements in the consumer economy including real wage (2.6%) and consumption growth (1.1%) contributed to 7.4m domestic trips in 2014, an increase of 3.4% on 2013 and the highest in five years. Moreover, the number of domestic trips was up a further 13.2% in Q1 2015. ■

GRAPH 1

Trips Taken in Ireland by Origin of Visitor

Source: CSO

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2008 2009 2010 2011 2012 2013 2014

No.

of T

rips (

000s

)

Overseas Domestic

Ballsbridge Hotel – Part of Project Trinity launched Q2 2015

02 Ireland Hotels

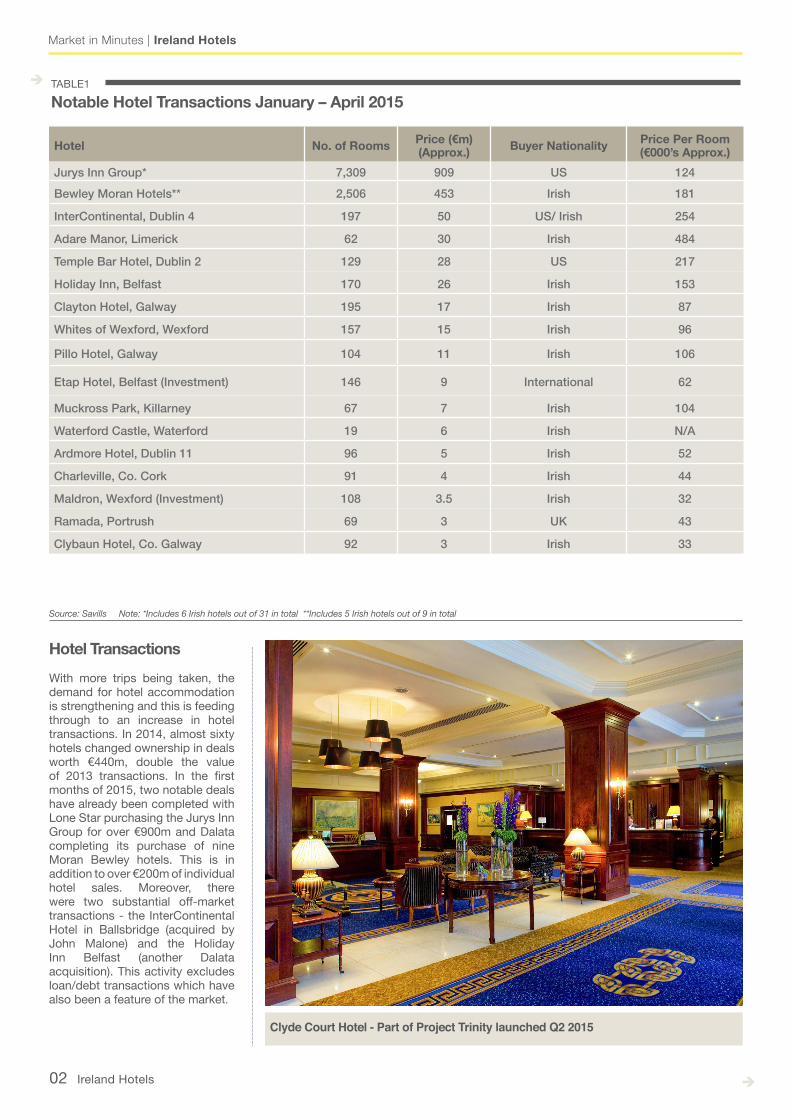

Hotel No. of Rooms Price (€m) (Approx.) Buyer Nationality Price Per Room

(€000’s Approx.)Jurys Inn Group* 7,309 909 US 124Bewley Moran Hotels** 2,506 453 Irish 181

InterContinental, Dublin 4 197 50 US/ Irish 254

Adare Manor, Limerick 62 30 Irish 484

Temple Bar Hotel, Dublin 2 129 28 US 217

Holiday Inn, Belfast 170 26 Irish 153

Clayton Hotel, Galway 195 17 Irish 87

Whites of Wexford, Wexford 157 15 Irish 96

Pillo Hotel, Galway 104 11 Irish 106

Etap Hotel, Belfast (Investment) 146 9 International 62

Muckross Park, Killarney 67 7 Irish 104

Waterford Castle, Waterford 19 6 Irish N/A

Ardmore Hotel, Dublin 11 96 5 Irish 52

Charleville, Co. Cork 91 4 Irish 44

Maldron, Wexford (Investment) 108 3.5 Irish 32

Ramada, Portrush 69 3 UK 43

Clybaun Hotel, Co. Galway 92 3 Irish 33

Market in Minutes | Ireland Hotels

Source: Savills Note: *Includes 6 Irish hotels out of 31 in total **Includes 5 Irish hotels out of 9 in total

TABLE1

Notable Hotel Transactions January – April 2015

Hotel TransactionsWith more trips being taken, the demand for hotel accommodation is strengthening and this is feeding through to an increase in hotel transactions. In 2014, almost sixty hotels changed ownership in deals worth €440m, double the value of 2013 transactions. In the first months of 2015, two notable deals have already been completed with Lone Star purchasing the Jurys Inn Group for over €900m and Dalata completing its purchase of nine Moran Bewley hotels. This is in addition to over €200m of individual hotel sales. Moreover, there were two substantial off-market transactions - the InterContinental Hotel in Ballsbridge (acquired by John Malone) and the Holiday Inn Belfast (another Dalata acquisition). This activity excludes loan/debt transactions which have also been a feature of the market.

Clyde Court Hotel - Part of Project Trinity launched Q2 2015

03 Ireland Hotels

Market in Minutes | Ireland Hotels

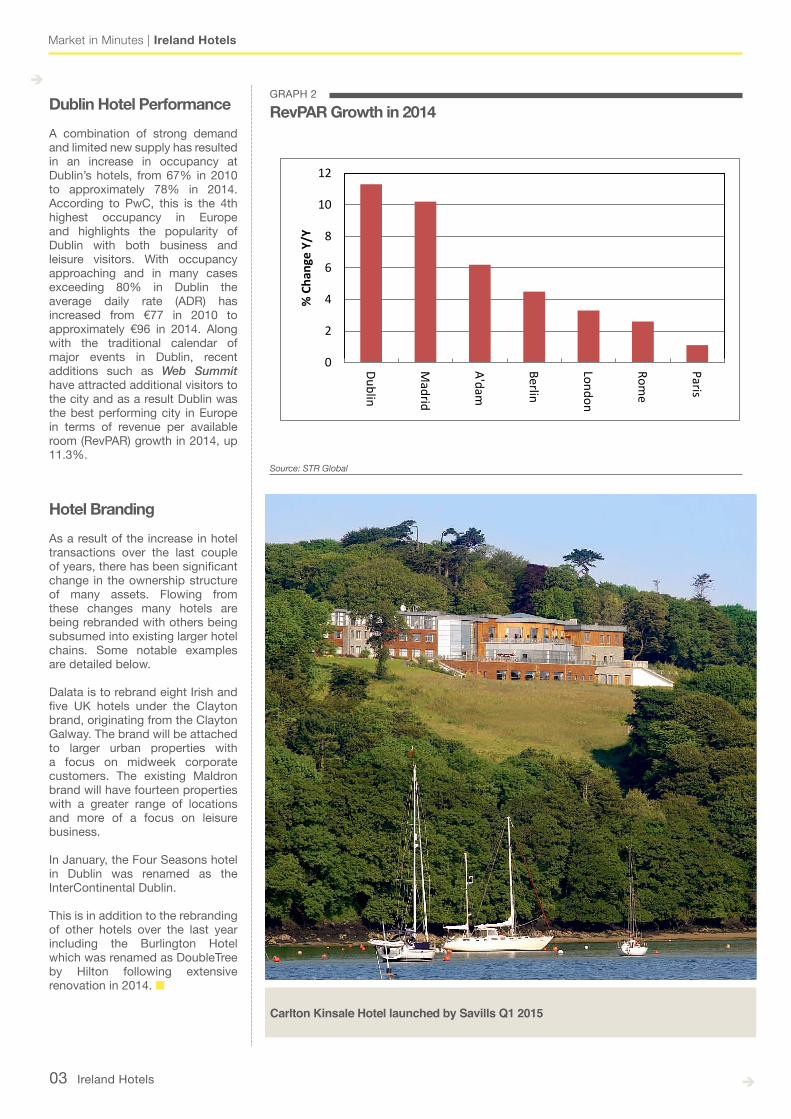

Dublin Hotel Performance A combination of strong demand and limited new supply has resulted in an increase in occupancy at Dublin’s hotels, from 67% in 2010 to approximately 78% in 2014. According to PwC, this is the 4th highest occupancy in Europe and highlights the popularity of Dublin with both business and leisure visitors. With occupancy approaching and in many cases exceeding 80% in Dublin the average daily rate (ADR) has increased from €77 in 2010 to approximately €96 in 2014. Along with the traditional calendar of major events in Dublin, recent additions such as Web Summit have attracted additional visitors to the city and as a result Dublin was the best performing city in Europe in terms of revenue per available room (RevPAR) growth in 2014, up 11.3%.

Hotel BrandingAs a result of the increase in hotel transactions over the last couple of years, there has been significant change in the ownership structure of many assets. Flowing from these changes many hotels are being rebranded with others being subsumed into existing larger hotel chains. Some notable examples are detailed below.

Dalata is to rebrand eight Irish and five UK hotels under the Clayton brand, originating from the Clayton Galway. The brand will be attached to larger urban properties with a focus on midweek corporate customers. The existing Maldron brand will have fourteen properties with a greater range of locations and more of a focus on leisure business.

In January, the Four Seasons hotel in Dublin was renamed as the InterContinental Dublin.

This is in addition to the rebranding of other hotels over the last year including the Burlington Hotel which was renamed as DoubleTree by Hilton following extensive renovation in 2014. ■

■ Forecasts for strong economic growth in Ireland (4.4%), the UK (2.5%) and the US (3.5%) in 2015 will support a further increase in trips taken in Ireland (both domestic and foreign).

■ Quantitative Easing (QE), in effect since March 9th 2015, will continue to put pressure on an already declining Euro. This will be particularly beneficial for visitors from non-Euro Area countries who will get better value for money when visiting Ireland.

■ As visitor numbers continue to increase, hotel occupancy, ADR and RevPAR are likely to continue to grow and this, in turn, will support hotel transactions going forward.

Savills Hotels & Leisure & Research TeamsPlease contact us for further information

Savills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 180 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East. A unique combination of sector knowledge and entrepreneurial flair give clients access to real estate expertise of the highest calibre. We are regarded as an innovative-thinking organisation backed up with excellent negotiating skills. Savills chooses to focus on a defined set of clients, therefore offering a premium service to organisations with whom we share a common goal. Savills takes a longterm view to real estate and works hard to invest in long term and strategic relationships and is synonymous with a high quality service offering and a premium brand. This bulletin is for general informative purposes only. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. All references to space and floor areas are approximate and apply to the greater Dublin area. The bulletin is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research. (c) Savills Ltd. 2015.