Page 1

1

Household Debt and Credit

2015 in Review

Andrew Haughwout

The views presented here are those of the authors and do not necessarily reflect

those of the Federal Reserve Bank of New York, or the Federal Reserve System.

Page 2

2

0

3

6

9

12

15

0

3

6

9

12

15Mortgage HE Revolving Auto Loan Credit Card Student Loan Other

Trillions of Dollars

Total Debt Balance and its Composition Trillions of Dollars

Source: FRBNY Consumer Credit Panel/Equifax

2015Q4 Total: $12.12 Trillion

2014Q4Total: $11.83 Trillion

(3%)

(10%)

(6%)

(9%)

(4%) (68%)

Page 3

3

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

03

:Q1

03

:Q3

04

:Q1

04

:Q3

05

:Q1

05

:Q3

06

:Q1

06

:Q3

07

:Q1

07

:Q3

08

:Q1

08

:Q3

09

:Q1

09

:Q3

10

:Q1

10

:Q3

11

:Q1

11

:Q3

12

:Q1

12

:Q3

13

:Q1

13

:Q3

14

:Q1

14

:Q3

15

:Q1

15

:Q3

Housing Auto CC Student

Auto and Student Debt Growth has Outstripped

Mortgage and CC

Page 4

4

75

80

85

90

95

100

75

80

85

90

95

100

03:Q1 04:Q1 05:Q1 06:Q1 07:Q1 08:Q1 09:Q1 10:Q1 11:Q1 12:Q1 13:Q1 14:Q1 15:Q1

Current 30 days late 60 days late 90 days late 120+ days late Severely Derogatory

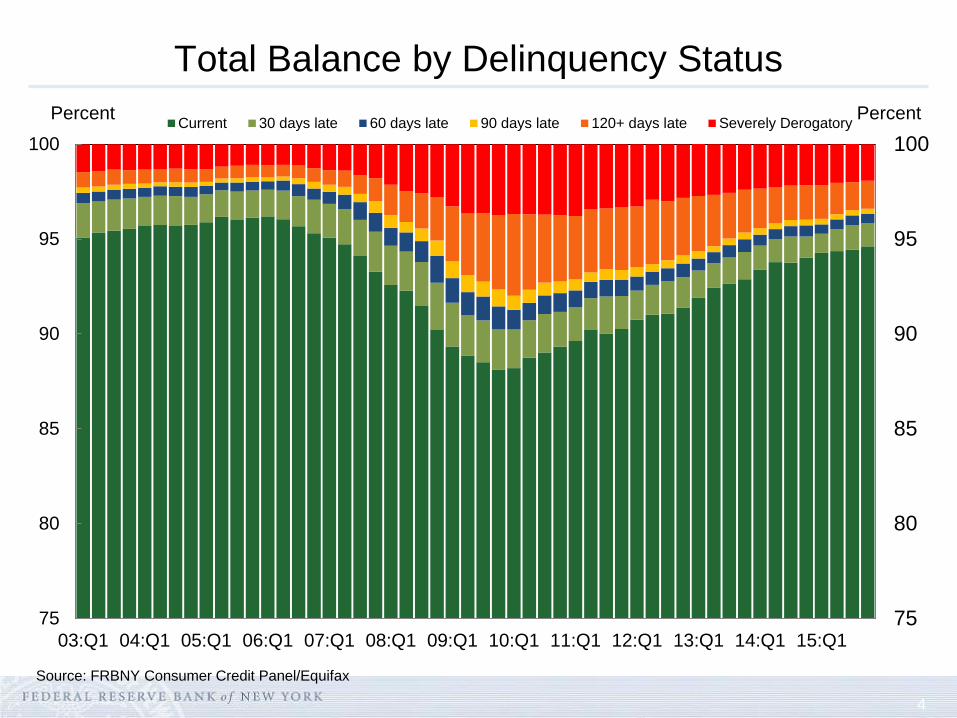

Total Balance by Delinquency Status

Percent

Source: FRBNY Consumer Credit Panel/Equifax

Percent

Page 5

5

Transition into delinquency for current mortgages

2015: 1.1%

2000-2005 avg: 1.45%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

00:Q1 02:Q1 04:Q1 06:Q1 08:Q1 10:Q1 12:Q1 14:Q1 16:Q1

Percent Percent

Source: FRBNY Consumer Credit Panel/Equifax

Page 6

6

Number of Consumers with New Foreclosures

and Bankruptcies

0

300

600

900

1,200

0

300

600

900

1,200

03:Q1 04:Q1 05:Q1 06:Q1 07:Q1 08:Q1 09:Q1 10:Q1 11:Q1 12:Q1 13:Q1 14:Q1 15:Q1

Foreclosures Bankruptcies

Thousands Thousands

Source: FRBNY Consumer Credit Panel/Equifax

Page 7

7

Notable in 2015

Delinquencies continued to decline

At year end 5.4% of debt was delinquent, lowest since early 2007

New foreclosures are at the lowest level we’ve seen

Data begin in 1999

Bankruptcies also trending down

Student loan delinquency remains high

Total household debt rose $289 billion, or 2.4%

Auto debt led the way, growing $109 billion (over 11%)

Outstanding auto debt crossed the $1 trillion mark in Q2

Other non-housing debt also grew strongly (4.7% - 6.5%)

Housing debt growth has been sluggish since end of deleveraging, and continued in 2015

Page 8

8

WHITHER MORTGAGES?

Page 9

9

Why has mortgage debt been so sluggish?

In spite of rising house prices, mortgage credit hasn’t expanded much

House prices up more than 1/3 since early 2012

But mortgage debt hasn’t grown (up less than 1%)

A stark contrast to last expansion

Both prices and debt roughly doubled 2000-2006

Why is this time different?

Page 10

3000

4000

5000

6000

7000

8000

9000

10000

60

80

100

120

140

160

180

200

2000 2002 2004 2006 2008 2010 2012 2014 2016

House Prices and Mortgage Debt

Index (Jan 2000 = 100) $ Billions

Source: FRBNY Consumer Credit Panel/Equifax and CoreLogic

CoreLogic HPI

(Left Axis)

Mortgage Debt

Outstanding

(Right Axis)

Page 11

11

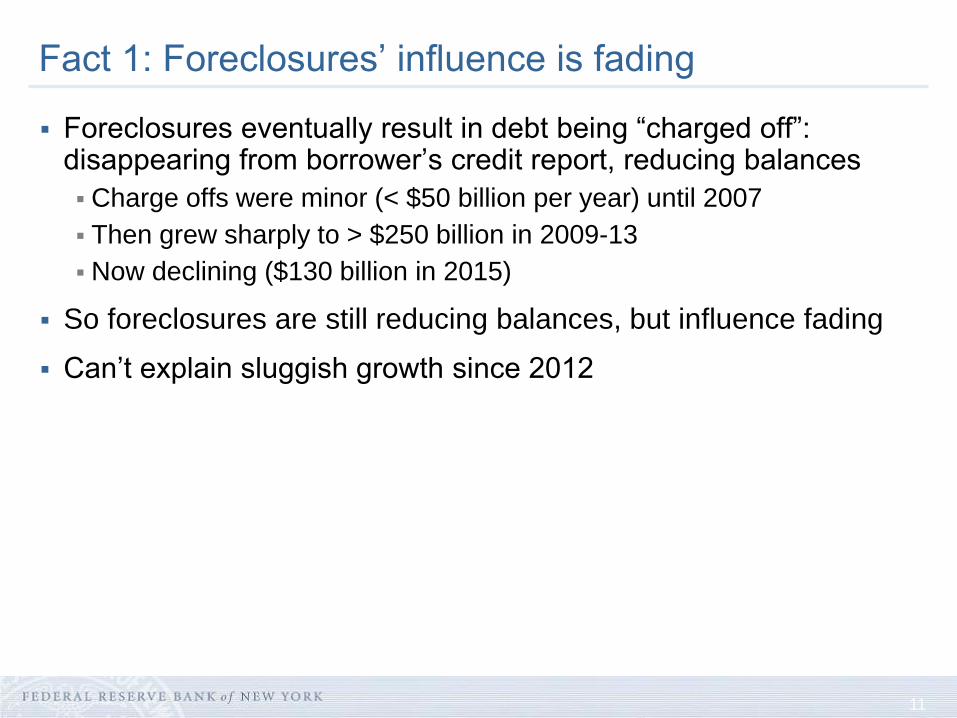

Fact 1: Foreclosures’ influence is fading

Foreclosures eventually result in debt being “charged off”: disappearing from borrower’s credit report, reducing balances

Charge offs were minor (< $50 billion per year) until 2007

Then grew sharply to > $250 billion in 2009-13

Now declining ($130 billion in 2015)

So foreclosures are still reducing balances, but influence fading

Can’t explain sluggish growth since 2012

Page 12

12

-400

-200

0

200

400

600

800

1,000

20

00

Q4

20

01

Q2

20

01

Q4

20

02

Q2

20

02

Q4

20

03

Q2

20

03

Q4

20

04

Q2

20

04

Q4

20

05

Q2

20

05

Q4

20

06

Q2

20

06

Q4

20

07

Q2

20

07

Q4

20

08

Q2

20

08

Q4

20

09

Q2

20

09

Q4

20

10

Q2

20

10

Q4

20

11

Q2

20

11

Q4

20

12

Q2

20

12

Q4

20

13

Q2

20

13

Q4

20

14

Q2

20

14

Q4

20

15

Q2

20

15

Q4

First and second lien charge offs

$ Billion

Source: FRBNY Consumer Credit Panel/Equifax

Fact 1: Foreclosures’ influence is fading

Page 13

13

Fact 2: Purchases not adding much

Housing transactions typically add to outstanding debt

Some new construction purchased with (net) new mortgages

Housing starts still well below boom levels

Sellers’ (paid off) mortgages are smaller than buyers’ (opened)

Sellers have paid down debt

Especially true when prices are rising, buyer must borrow more

In 2006 and 2007, transactions added $800B - $1T annually

$200B in 2009-11, now back to $350B

Much lower contribution to mortgage debt than during the boom

Page 14

14

-400

-200

0

200

400

600

800

1,000

20

00

Q4

20

01

Q2

20

01

Q4

20

02

Q2

20

02

Q4

20

03

Q2

20

03

Q4

20

04

Q2

20

04

Q4

20

05

Q2

20

05

Q4

20

06

Q2

20

06

Q4

20

07

Q2

20

07

Q4

20

08

Q2

20

08

Q4

20

09

Q2

20

09

Q4

20

10

Q2

20

10

Q4

20

11

Q2

20

11

Q4

20

12

Q2

20

12

Q4

20

13

Q2

20

13

Q4

20

14

Q2

20

14

Q4

20

15

Q2

20

15

Q4

First lien originations plus normal (non-charge-off) payoffs First and second lien charge offs

$ Billion

Source: FRBNY Consumer Credit Panel/Equifax

Fact 2: Purchases not adding much

Page 15

15

Fact 3: Much less cash out than in boom

Borrowers can take cash out of properties without moving

With a cash-out refinance

With a junior lien (eg, Home Equity Loans or Lines of Credit)

Very important during the boom

$300-$400 billion in cash withdrawn per year in 2003-2007

Declined sharply during the bust

$10-$40 billion annual rate since 2012

Much lower contribution to mortgage debt than during the boom

Page 16

16

Fact 3: Much less cash out than during the boom

-300

-200

-100

0

100

200

300

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

refinance second lien activity

Source: FRBNY Consumer Credit Panel/Equifax

$ Billion

Page 17

17

Fact 4: First-lien principal pay-down has grown a lot

2015Q4 outstanding mortgage debt is $8.25T

We’ve seen this level 3 times now (all Q4)

2006: $170 billion in annual pay-down (2.1%)

2011: $234 billion in annual pay-down (2.8%)

2015: $288 billion in annual pay-down (3.5%)

$118 billion or 70% increase since 2006 on same base

Page 18

18

-300

-200

-100

0

100

200

300

20

00

Q1

20

00

Q3

20

01

Q1

20

01

Q3

20

02

Q1

20

02

Q3

20

03

Q1

20

03

Q3

20

04

Q1

20

04

Q3

20

05

Q1

20

05

Q3

20

06

Q1

20

06

Q3

20

07

Q1

20

07

Q3

20

08

Q1

20

08

Q3

20

09

Q1

20

09

Q3

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

refinance first lien paydown second lien activity

Amortization has increased by $90 billion per year since 2009

Fact 4: First-lien principal pay-down has grown a lot

$ Billion

Page 19

19

Why is pay-down share increasing?

Three factors determine pay-down share

Interest rate

Loans with low rates have higher principal pay-down per dollar of payment

Loan age

Older loans have higher principal pay-down per dollar of payment

Term of loan

Loans with shorter terms have higher principal pay-down per payment

All of these factors are currently pushing principal share up

Page 20

20

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

11

32

53

74

96

17

38

59

71

09

12

11

33

14

51

57

16

91

81

19

32

05

21

72

29

24

12

53

26

52

77

28

93

01

31

33

25

33

73

49

Payment number

30-yr @ 6.8%

30-yr @ 3.5%

15-yr @ 2.7%

Source: Authors’ calculations

Interest rate, term and age determine principal share

Page 21

21

Savings from refinancing a $200,000 mortgage

30-yr @ 6.8%, pmt 78

Principal

Interest

Payment $1,303

Principal $ 263 (4.2% of income)

15-yr @ 2.7%, pmt 1

Principal

Interest

Payment $1,352 (+3.7%)

Principal $ 902 (14.4% of income)

Assumes borrower income of $75,000 finances all payments

Source: Authors’ calculations

Page 22

22

Stock of outstanding debt has aged since 2003

0

10

20

30

40

50

60

70

80

199

9Q

1

199

9Q

3

200

0Q

1

200

0Q

3

200

1Q

1

200

1Q

3

200

2Q

1

200

2Q

3

200

3Q

1

200

3Q

3

200

4Q

1

200

4Q

3

200

5Q

1

200

5Q

3

200

6Q

1

200

6Q

3

200

7Q

1

200

7Q

3

200

8Q

1

200

8Q

3

200

9Q

1

200

9Q

3

201

0Q

1

201

0Q

3

201

1Q

1

201

1Q

3

201

2Q

1

201

2Q

3

201

3Q

1

201

3Q

3

201

4Q

1

201

4Q

3

201

5Q

1

201

5Q

3

25th percentile 50th percentile

75th percentile average

Source: New York Fed Consumer Credit Panel / Equifax

Months since origination

Mean loan age rises from 23 to 50 months

Page 23

23

Mortgage rates much lower, especially for 15-year

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

0

1

2

3

4

5

6

7

8

9

20

00

- J

an

20

00

- A

ug

20

01

- M

ar

20

01

- O

ct

20

02

- M

ay

20

02

- D

ec

20

03

- J

ul

20

04

- F

eb

20

04

- S

ep

20

05

- A

pr

20

05

- N

ov

20

06

- J

un

20

07

- J

an

20

07

- A

ug

20

08

- M

ar

20

08

- O

ct

20

09

- M

ay

20

09

- D

ec

20

10

- J

ul

20

11

- F

eb

20

11

- S

ep

20

12

- A

pr

20

12

- N

ov

20

13

- J

un

20

14

- J

an

20

14

- A

ug

20

15

- M

ar

30-year 15-year Diff (right axis)7/06: 6.8%

12/12: 2.7%

Page 24

24

Median

25th percentile

10th percentile

500

550

600

650

700

750

800

500

550

600

650

700

750

800

99:Q2 01:Q2 03:Q2 05:Q2 07:Q2 09:Q2 11:Q2 13:Q2 15:Q2

Credit Score at Origination: Mortgages* Score Score

Source: FRBNY Consumer Credit Panel/Equifax

* Credit Score is Equifax Riskscore 3.0; mortgages include first-liens only.

Tight lending standards mean lower interest rates for average borrower

Page 25

25

Effective rate on outstanding mortgages has fallen

0

1

2

3

4

5

6

7

8

19

99

:Q1

19

99

:Q3

20

00

:Q1

20

00

:Q3

20

01

:Q1

20

01

:Q3

20

02

:Q1

20

02

:Q3

20

03

:Q1

20

03

:Q3

20

04

:Q1

20

04

:Q3

20

05

:Q1

20

05

:Q3

20

06

:Q1

20

06

:Q3

20

07

:Q1

20

07

:Q3

20

08

:Q1

20

08

:Q3

20

09

:Q1

20

09

:Q3

20

10

:Q1

20

10

:Q3

20

11

:Q1

20

11

:Q3

20

12

:Q1

20

12

:Q3

20

13

:Q1

20

13

:Q3

20

14

:Q1

20

14

:Q3

20

15

:Q1

20

15

:Q3

Percent

Source: Bureau of Economic Analysis

Down over 50% (380 bps) since 2000

Page 26

26

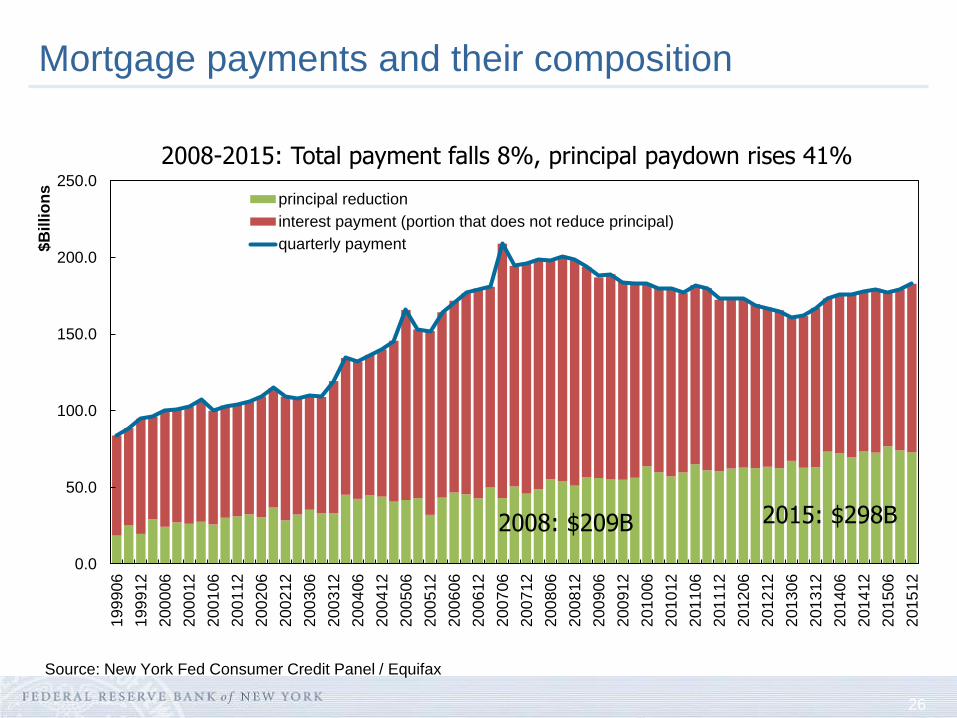

Mortgage payments and their composition

0.0

50.0

100.0

150.0

200.0

250.0

199

906

199

912

200

006

200

012

200

106

200

112

200

206

200

212

200

306

200

312

200

406

200

412

200

506

200

512

200

606

200

612

200

706

200

712

200

806

200

812

200

906

200

912

201

006

201

012

201

106

201

112

201

206

201

212

201

306

201

312

201

406

201

412

201

506

201

512

$B

illi

on

s

principal reduction

interest payment (portion that does not reduce principal)

quarterly payment

Source: New York Fed Consumer Credit Panel / Equifax

2008: $209B 2015: $298B

2008-2015: Total payment falls 8%, principal paydown rises 41%

Page 27

27

Summary

Between 2000-2006, house prices and mortgage debt both doubled

Since 2012 house prices have risen 34%, mortgage debt < 1%

Foreclosures’ effect on reducing debt is fading

Equity withdrawal and transactions adding only modestly to balances

$400 billion vs $1.4 trillion annual

Stable since 2012

A big change: increased principal paydown from aging stock of continuing debt and refinances into lower rate, shorter term debt

$300 billion in paydown annually

A major increase in savings for these households

Page 28

28

Explanations, implications and outlook

Some of this is easy to understand

When borrower doesn’t move or refinance, debt gets older and principal payment goes up

Lower rates and shorter terms refinances largely due to . . .

. . . decline in overall rates

. . . especially low 15-yr r

Tighter standards mean average borrower gets a lower rate

Some of it is less clear

Are less equity withdrawal and transactions due to . . .

. . . borrower caution

or

. . . tighter standards/supply?

Could be a sign of stress for some borrowers (eg young student borrowers)

Page 29

29

Explanations, implications and outlook

Whatever the causes, these factors are increasing personal savings for these borrowers

Existing stock of debt likely to “age in place”

If rates go up, strong incentives to continue in low rate mortgage

Leading to slow increase in pay-down/saving

Could be offset by increase in equity withdrawal or purchase borrowing

But little sign of that yet