68

Housewares in the UK & Steamer Trading Cookshop Ben Phillips IBC Global Forum Mexico City, June 2015

Housewares in the UK & Steamer Trading Cookshop

Ben Phillips

IBC Global Forum

Mexico City, June 2015

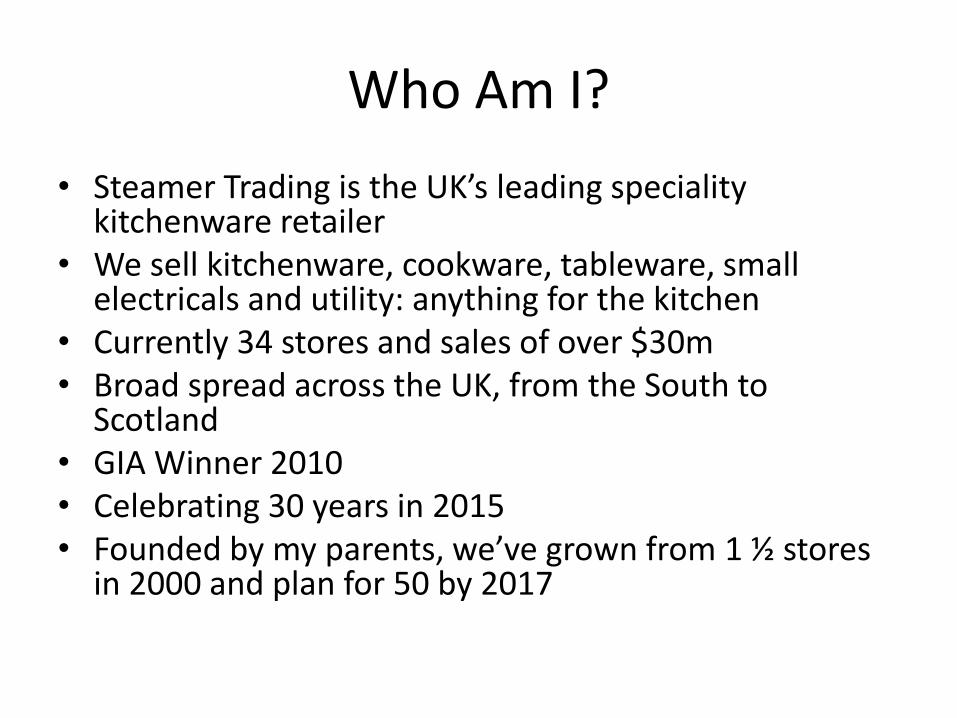

Who Am I?

• Steamer Trading is the UK’s leading speciality kitchenware retailer

• We sell kitchenware, cookware, tableware, small electricals and utility: anything for the kitchen

• Currently 34 stores and sales of over $30m • Broad spread across the UK, from the South to

Scotland • GIA Winner 2010 • Celebrating 30 years in 2015 • Founded by my parents, we’ve grown from 1 ½ stores

in 2000 and plan for 50 by 2017

Agenda

• The UK market: facts and figures

• Structure of the retail market for housewares

• Steamer Trading – what we’re about and our place in the market

• Supplying the UK market – distribution or direct?

• Working with Steamer Trading

• Questions

The UK Market

• The #3 market for US housewares exporters

• We’re “friendly, receptive, English-speaking and appreciate US innovation and branding”

• With 64 million people in an area the size of Michigan distribution is “relatively easy to plan”

• We “have ample spending power” with GDP per capita of $46k vs. US ($55k), Canada ($50k)

• 20 retailers account for over 60% of sales in the UK

• We have “sophisticated”, “price sensitive” consumers With acknowledgements to Laura Spingola and the IHA Blog!

The UK Consumer and Cooking

In the last year: 88% Prepared a family meal 60% Watched TV cookery shows 57% Looked up recipes online 31% Cooked for a dinner party 27% Bought a cook book 5% Took a cooking lesson

The UK Consumer and Eating

84% Eat breakfast at home 58% Have lunch at home 92% Take dinner at home 43% Eat at the dining table 18% Have dinner in the kitchen 50% Eat dinner on the sofa

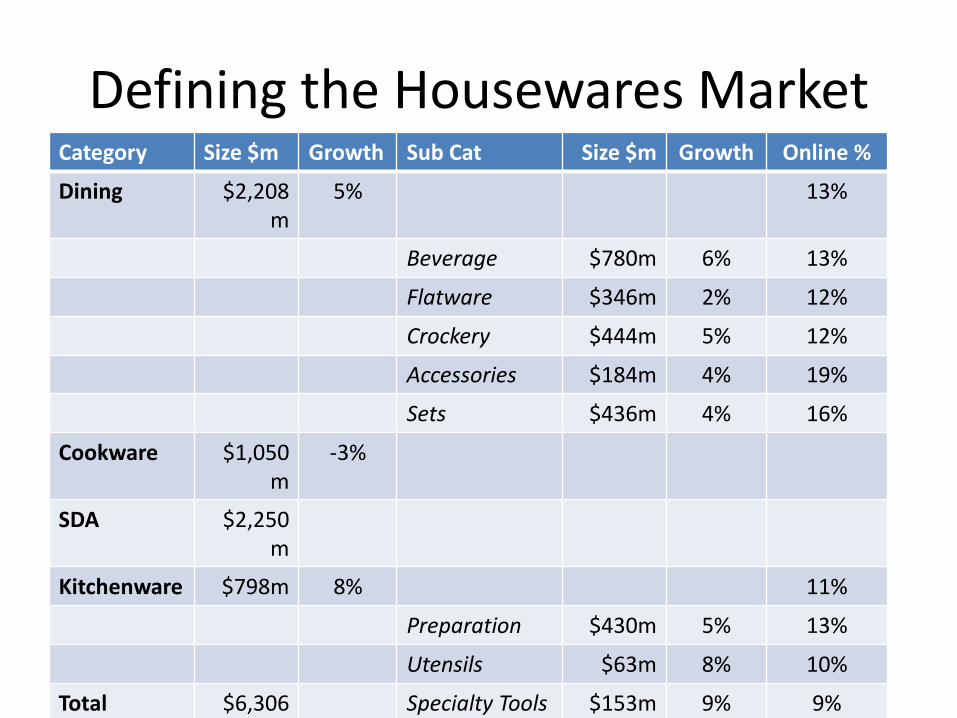

Defining the Housewares Market Category Size $m Growth Sub Cat Size $m Growth Online %

Dining $2,208m

5% 13%

Beverage $780m 6% 13%

Flatware $346m 2% 12%

Crockery $444m 5% 12%

Accessories $184m 4% 19%

Sets $436m 4% 16%

Cookware $1,050m

-3%

SDA $2,250m

Kitchenware $798m 8% 11%

Preparation $430m 5% 13%

Utensils $63m 8% 10%

Total $6,306m

Specialty Tools $153m 9% 9%

Figures 2015 est Source: Conlumino, other Boards $150m 10% 7%

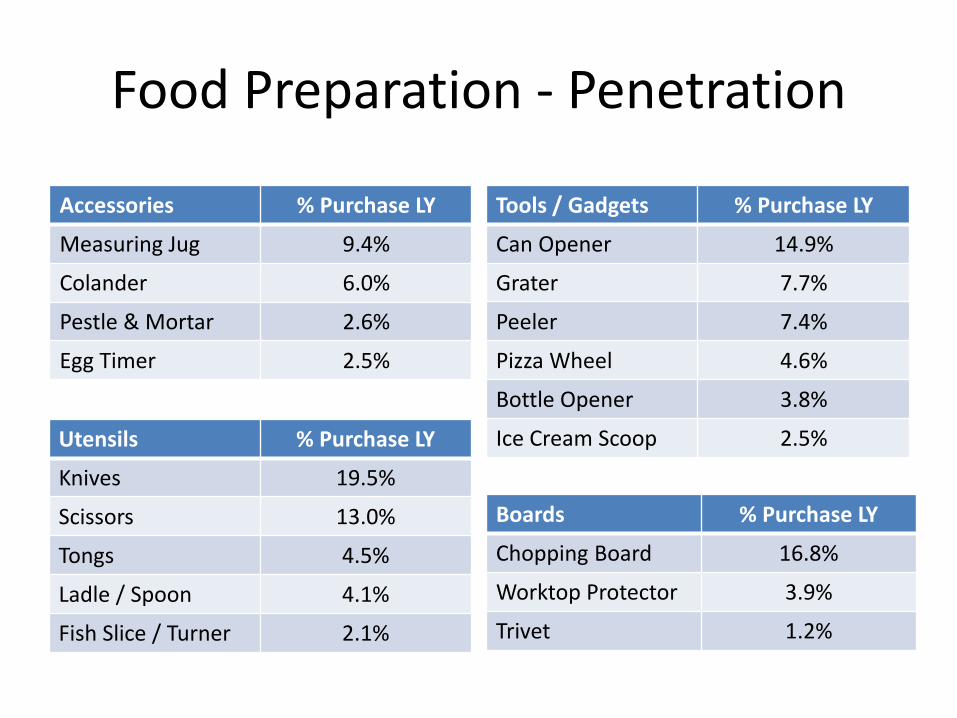

Food Preparation - Penetration

Accessories % Purchase LY

Measuring Jug 9.4%

Colander 6.0%

Pestle & Mortar 2.6%

Egg Timer 2.5%

Tools / Gadgets % Purchase LY

Can Opener 14.9%

Grater 7.7%

Peeler 7.4%

Pizza Wheel 4.6%

Bottle Opener 3.8%

Ice Cream Scoop 2.5% Utensils % Purchase LY

Knives 19.5%

Scissors 13.0%

Tongs 4.5%

Ladle / Spoon 4.1%

Fish Slice / Turner 2.1%

Boards % Purchase LY

Chopping Board 16.8%

Worktop Protector 3.9%

Trivet 1.2%

Tableware - Penetration

Accessories % Purchase LY

Salt/Pepper Pot 7.1%

Cheese Board 4.0%

Cake Stand 3.6%

Butter Dish 3.4%

Beverage % Purchase LY

Glasses 28.3%

Mugs 27.5%

Cups & Saucers 6.9%

Teapot 6.4%

Cafetiere 4.2%

Milk Jug 3.6% Crockery % Purchase LY

Bowls 14.2%

Dinner Plate 14.0%

Side Plate 9.3%

Egg Cups 4.2%

Serving Bowl 3.4%

Flatware % Purchase LY

Knives 12.8%

Teaspoons 11.8%

Spoons 9.8%

Why do Consumers Buy Kitchenware?

New Purchase

21.7% First time that the consumer has

purchased this product

Replacement

71.8% Replacing old (47%), broken (40%) or

disliked items (10%)

Upgrade /Complete

24.4% Purchase made for better

functionality (14%), a new look (12%) or to complete a set (4%)

Impulse

18.7% Reasons include a special offer (11%)

and pure impulse (6%)

Why Do Consumers Buy Tableware?

New Purchase

16.4% First time that the consumer has

purchased this product

Replacement

63.7% Replacing old (34%), broken (36%) or

disliked items (13%)

Upgrade /Complete

49.3% Purchase made to add to existing

items (33%), a new look (22%) or to complete a set (9%)

Impulse

33.5% Reasons include a special offer (17%)

and pure impulse (17%)

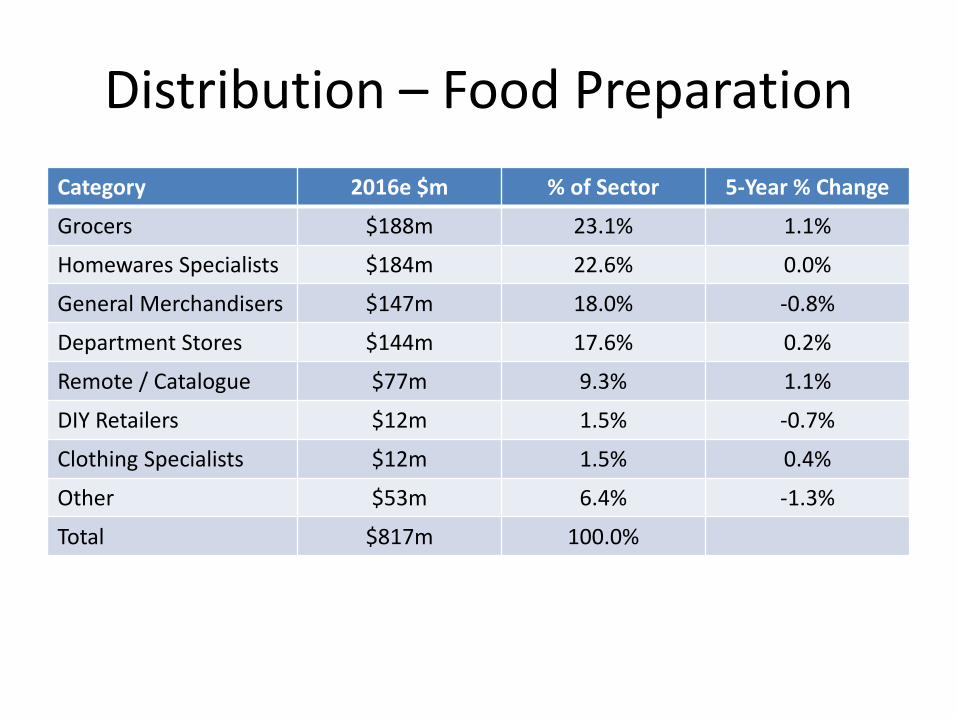

Distribution – Food Preparation

Category 2016e $m % of Sector 5-Year % Change

Grocers $188m 23.1% 1.1%

Homewares Specialists $184m 22.6% 0.0%

General Merchandisers $147m 18.0% -0.8%

Department Stores $144m 17.6% 0.2%

Remote / Catalogue $77m 9.3% 1.1%

DIY Retailers $12m 1.5% -0.7%

Clothing Specialists $12m 1.5% 0.4%

Other $53m 6.4% -1.3%

Total $817m 100.0%

Retailer Shares – Food Preparation

Retailer Market Share Type / Third Party Offer?

Tesco 9.4% Supermarket, limited

Wilkinsons 6.1% General, value, limited

Asda 5.9% Walmart, limited

John Lewis 5.8% Department store, c.50%

IKEA 5.1% Homewares, none

Lakeland 4.1% Specialist, c.50%

Argos 3.5% Generalist, value, some

Sainsburys 3.1% Supermarket, some

Debenhams 2.3% Department store, c.50%

Dunelm 2.0% Homewares, value, some

Marks & Spencer 0.8% Clothing, general, none

Total Top 11 48.1%

Distribution – Tableware

Category 2016e $m % of Sector 5-Year % Change

Department Stores $619m 27.5% 0.2%

Homewares Specialists $459m 20.4% -0.2%

Grocers $432m 19.2% 1.0%

General Merchandisers $372m 16.5% -0.9%

Remote / Catalogue $149m 6.6% 0.6%

Clothing Specialists $117m 5.2% 1.0%

DIY Retailers $63m 2.8% -0.2%

Other $41m 1.8% -1.5%

Total $2,252m 100.0%

Retailer Shares – Tableware

Retailer Market Share Type / Third Party Offer?

John Lewis 8.9% Department store, c.50%

Argos 6.8% Generalist, value, some

Tesco 6.1% Supermarket, none

Asda 5.9% Walmart, none

Debenhams 5.6% Department store, >50%

IKEA 5.2% Homewares, none

Wilkinsons 4.1% Generalist, value, limited

Marks & Spencer 3.9% Clothing, general, none

Total Top 8 46.5%

Why do Consumers Buy?

0 10 20 30 40 50 60 70

Low Prices

Convenient

Good Quality

In Stock

Wide Choice

Bargains

Get Product Immediately

Good Brand Selection

Pleasant Environment

Had Loyalty Card

Force of Habit

Innovative Products

Easily View Products

Good Customer Service

Offers Home Delivery

Good Guaranteed

Price Matching Scheme

Recommended by Friend

Ethical Credentials

Variations Between Retailers

Branded Housewares Market

The Steamer Trading Heritage

2001-2011: 10 Years of Growth

• 25 stores opened in 10 years (now 34)

• Mixed freehold/leasehold portfolio has provided exceptional stability

• 250,000 customer database (now 700,000)

• No closed or failing stores

• Industry reputation for staff knowledge, enthusiasm and friendliness

• Retained the feeling of ‘our’ local shop

Steamer Trading Sales

Steamer Trading Profits

Housewares Industry Awards • Specialist Multiple Retailer of the Year 2013, 2014 • Excellence in Training 2012 • Excellence in Display 2012 • Specialist Multiple Retailer of the Year 2010, 2011 • Global Innovator Award 2010 • Oracle / Retail Week Emerging Retailer of the Year 2009 • Excellence in Retail Display 2009 • Small Multiple Retailer of the Year 2007, 2008 • Multiple Retailer of the Year 2005, 2006 • Independent Retailer of the Year 2004 • Excellence in Retail Display 2003 • Global Innovator Award (UK Winner)2003 • Independent Retailer of the Year 2000

Growth Plan (2012)

• 5-Year objective to more than double Sales to $60m within 5 years

• Store numbers grown from 26 (2011) to 48 by 2017: over 35 by end 2015

• Same-store growth targeted against an assumed flat market

• Internet forecast as ‘largest store’ by 2016/7, doubling year-on-year

• Remain focussed on the UK market

What is the Steamer Trading Brand?

• We’re not a large, corporate retailer

• We’re family run, we’re enthusiastic and we care about our customers

• We’re about the kitchen – the heart of the home

• We’re a specialist retailer – we know our onions (and how to peel, slice, dice, cube and fry them)

• We’re about having fun in the kitchen, too

• …and never, ever, take ourselves too seriously

Strategy

• Develop position as a specialist, offering the very best for the kitchen

• Focus on developing key brands

• Enhance consumer awareness of the value of investing in the right equipment

• Set the highest standards in customer service

• Exceptional level of staff knowledge and engagement

what does this look like?

Photography by Oliver Perrott

what does this look like?

Photography by Oliver Perrott

what does this look like?

Photography by Oliver Perrott

Store Strategy

• Beautiful buildings in prime locations

• Market towns in good areas

• Never become a ‘chain’

• Offer a truly comprehensive range

• Excite and delight with new ideas, colour, quirkiness – and fun

• Invest in making shops look as good as they can – don’t focus on the short term

• Brands are key in a polarising market

Steamer Trading Store Locations

‘Typical’ Steamer Trading shops

Photography by Oliver Perrott

‘Typical’ Steamer Trading shops

Photography by Oliver Perrott

Guildford store

Photography by Oliver Perrott

Guildford interior

Bluewater – the First Mall Store

Steamer Trading Online

• Grow online revenue by 50% YoY

• Align store and online brand messages • We want to establish ourselves as 'foodies' and the experts in everything for the kitchen

• Onsite • Increasing content on all product pages – videos, images and unique written content

• Community site • Building a Steamer Trading blog site to help increase engagement and brand loyalty by

establishing ourselves as experts in our category

• Extra platform to engage with our customers about our brands (recipes, how to, experts choice, buying guides)

• Emails • Database is currently 200k with a focus to drive acquisition this year

• 2 weekly emails

• Continue to send content led emails i.e. recipes

www.steamer.co.uk

Brand Stories, Recipes

Expert’s Choice, Buying Guides

Engaging Emails

Steamer Trading – Product Strategy

• ‘Serious Cookshops with Style’

• 10,000+ lines from specialist to fun

• Focus on mid/upper end ranges

• Build, develop and support brands

• Own-label an opportunity to introduce variation and excitement – not an entry point

• Unique/different/seasonal products create interest

‘They sell things here

that I never knew

I didn’t have’

Steamer Trading Buying Team

Ben Phillips

Managing Director

Susan Millin

Interim B&M Director

Priti Merchant

Buying Manager

New Hire

Joanna Canham

Buying Admin

Melly Cooper

Buying Admin

Amy Wells

Buying Admin (Maternity Leave)

Neil Windsor

Merchandiser

New Hire

New Hire

Jennifer McCalvey

Project Merchandiser

Jess Taylor

Interim Retail Director

Nick O’Mahony

Head of Product Training

Lauren Nichol

Online and Marketing

Alastair Kerr

George Treves

Non-Executives

Sourcing Strategy

• Who we buy from: UK manufacturers/brand owners: 44% (25%)

UK subsidiaries/international brands: 25% (30%)

Multibrand distributors: 24% (40%)

Direct imports: 7% (5%)

• 200 active suppliers (from 300 ‘recent’) • Trade shows: Birmingham, Frankfurt, Chicago,

Paris, smaller UK events • Long-term, partner relationships with key

suppliers • All of our top 10 suppliers were represented

when we opened 30 years ago

Example Best Sellers

Example Key Suppliers

• Kitchencraft (Lifetime Brands) • Beam (KitchenAid distributor) • Le Creuset • Global • Dexam (Chef’n distributor) • PHA (Cuisipro distributor) • Eddingtons (multibrand distributor) • JosephJoseph • OXO Good Grips • Yaxell (Japanese specialty cutlery)

US Brands at Steamer Trading - 2009

KitchenAid OXO

Cuisipro Chef’n

Microplane Cuisinart

Chef’s Choice Tovolo

Danica Architec

Zak Nordic Ware

Meyer Epicurean

Fred + Friends

US Brands at Steamer Trading – 2015/6

Dash

True

Prepara

Vitamix

Blendtec

Pack-It

Olde Thompson

Aladdin

Stanley

Corkicle

KitchenAid

Cuisipro

Microplane

Chef’s Choice

Danica / NOW Designs

Zak

OXO

Chef’n

Cuisinart

Tovolo

Architec

Nordic Ware

Fred + Friends

Camelback

Mighty Mug

Full Circle

Zing Anything

MSC/Joie

Zoku

Bobble

That!

Anchor Hocking

Vinturi

Dealing with the UK Market

• Dominated by subsidiaries / distributors – virtually no UK-based manufacturing

• International brands have a great opportunity to enter and compete

• US principals seen as more supportive than Europeans – willing to take a long term view

• Importance of the independent sector – there is no ‘big box’ retailer to carry the success of a major product single-handedly

Key Market Differences

• Our ovens are smaller…

• …and so are our kitchens – before our customers buy, they have to think of where they’ll keep it

• We don’t do celebrations…

• …or have china for ‘best’

• We buy a lot more supermarket ready-meals

• We barbecue less and don’t have as much of an outdoor culture

Key Market Differences

• Induction is more important and essential future-proofing

• Our dishwashers are far more damaging to ‘dishwasher safe’ products

• We don’t eat together as a family as much • Seasonality – as determined by Crate & Barrel – is

a new discovery • Top end – introduced by Williams Sonoma to

every major town in the US – is a lonely place in the UK

What we look for from the US

• Product innovation and development – everyday products, better engineered

• Strong packaging and point of sale

• Brand communication

• ‘Unique’ products with limited UK presence

• Flexibility in sourcing

• Export pricing - £ for $ retail pricing rarely fools the internet-aware generation

• Awareness of export markets

Supplying the UK – A Distributor View

• ‘A good brand deserves a good distributor’

• Expect to carry c.50-60% of the range

• Give the brand its own ‘voice’

• Often uneconomic to ship from US – aim for factory volumes

• Take a view on timing – 1 year is too short

• A good export manager is key to the relationship

The Distributor’s Target Market

Retailer/Sector Possible % of Kitchenware Distribution

Independent Sector 25-30%

- Steamer Trading 3%+

- Fenwick (group) 2%+

John Lewis 15%

Lakeland 10%

Department Stores (other) 10%

Internet Retailers 10%

Other inc. Grocery 25%

A standard margin for independents will be 2.4x (including 20% taxes); larger retailers will expect 3x+; and department stores may demand 4x including support / rebates

Working with Steamer Trading

• Steamer Trading is the only growing retailer of scale in the UK that has a strategy of building brands

• Focus on strong, design and innovation-led products that offer a point of difference

• Tight focus on ‘the kitchen’ and the more aspirational consumer

• A brand must protect its routes to market – internet pricing cannot be policed in the UK

What we Offer

• A strong, highly respected and financially secure retail partner

• The highest levels of staff training, POS support and in-store demonstration

• Knowledgeable and passionate customer communication

• A database of over 700,000 customers reached through our Christmas catalogue

• Loyalty and openness to our key suppliers

Steamer Trading Christmas Catalogue

Brand Building