FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT HOUSING AUTHORITY OF NEW ORLEANS YEAR ENDED SEPTEMBER 30, 2005 Under provisions of state law, this report is a public document. A copy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court. _ / i D~'~- Release Date_

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

_ / iD~'~-Release Date_

Housing Authority of New Orleans

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS' REPORT 2

MANAGEMENT'S DISCUSSION AND ANALYSIS 5

BASIC FINANCIAL STATEMENTS

STATEMENT OF NET ASSETS 15

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NETASSETS 17

STATEMENT OF CASH FLOWS 18

NOTES TO FINANCIAL STATEMENTS 20

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND COMPLIANCE AND OTHER MATTERSBASED ON AN AUDIT OF THE FINANCIAL STATEMENTSPERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITINGSTANDARDS 38

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE WITHREQUIREMENTS APPLICABLE TO EACH MAJOR PROGRAM ANDINTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITHOMB CIRCULAR A-133 40

SCHEDULE OF FINDINGS AND QUESTIONED COSTS 43

SCHEDULE OF PRIOR YEAR AUDIT FINDINGS 50

SUPPLEMENTAL INFORMATION

FINANCIAL DATA SCHEDULE 54

SCHEDULE OF EXPENDITURES OF FEDERAL FINANCIAL AWARDS 58

MANAGEMENT LETTER 59

- 2 -

I ReZniCk Reznick Group, PC Tel: (704) 332-9100525 N.Tryon Street Fax; (704) 332-6444Suite 1000 www.reznidcgroup.comCharlotte, NC 28202

INDEPENDENT AUDITORS' REPORT

To the Board of CommissionersHousing Authority of New Orleans

We have audited the accompanying statement of net assets of the Housing Authority ofNew Orleans (HANO) and its discretely presented component units as of and for the year endedSeptember 30, 2005, and we were engaged to audit the related statements of revenue, expensesand changes in net assets, and cash flows, as listed in the table of contents for the year thenended. These basic financial statements are the responsibility of HANO's management. Ourresponsibility is to express an opinion on these financial statements. For the year endedSeptember 30, 2005, we did not audit the financial statements of the component units. Thosestatements were audited by other auditors whose reports have been furnished to us, and ouropinion, insofar as it relates to those entities, is based solely on the reports of the other auditors.

Except as explained by the following paragraph, we conducted out audit in accordancewith auditing standards generally accepted in the United States if America and the standardsapplicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States. Those standards require that we plan and perform theaudit to obtain reasonable assurance about whether the financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting the amountsand disclosures in the statement of net assets. An audit also includes assessing the accountingprinciples used and significant estimates made by management, as well as evaluating the overallfinancial statement presentation. We believe that our audit of the statement of net assets and thereports of other auditors provide a reasonable basis for our opinion.

We were unable to obtain records regarding potential liabilities for incurred but notreported claims, tenant income, and expenses. Additionally, HANO was unable to providesufficient documentation on the statement of net assets accounts that were deemed unverifiableby their consultants and written off to the statement of revenue, expenses and changes in netassets.

Because of the matter discussed in the preceding paragraph the scope of our work wasnot sufficient to enable us to express, and we do not express, an opinion on the statement ofrevenues, expenses and changes in net assets and cash flows for the year ended September 30,2005.

In our opinion, based on our audit and the reports of other auditors, except for the effectsof such adjustments, if any, as might have been determined to be necessary had there beendocuments analyzing the potential liabilities for incurred but not reported claims, the statementsof net assets presents fairly, in all material respects, the financial position of the HousingAuthority of New Orleans, as of September 30, 2005, in conformity with accounting principlesgenerally accepted in the United States of America.

-3-

Atlanta • Austin • Baltimore • Bethesda • Charlotte • Chicago • Los Angeles • Sacramento • Tysons Comer

In accordance with Government Auditing Standards, we have also issued our report datedSeptember 21, 2007, on our consideration of HANO's internal control over financial reportingand our tests of its compliance with certain provisions of laws, regulations, contracts and grantagreements and other matters. The purpose of that report is to describe the scope of our testingof internal control over financial reporting and compliance and the results of that testing, and notto provide an opinion on the internal control over financial reporting or on compliance. Thatreport is an integral part of an audit performed in accordance with Government AuditingStandards and should be considered in assessing the results of our audit.

The Management's Discussion and Analysis on pages 5 to 14 is not a required part of thebasic financial statements, but is supplementary information required by accounting principlesgenerally accepted in the United States of America and the Governmental Accounting StandardsBoard. We have applied certain limited procedures that consisted principally of inquiries ofmanagement regarding the methods of measurement and presentation of the supplementaryinformation. However, we did not audit the information and we express no opinion on it.

The accompanying supplemental information on pages 54 through 58, including theschedule of expenditures of federal awards as required by U.S. Office of Management andBudget Circular A-133, "Audits of States, Local Governments, and Non-Profit Organizations,"and the Financial Data Schedule required by the U.S. Department of Housing and UrbanDevelopment, are presented for purposes of additional analysis and are not a required part of thebasic financial statements. Since HANO was not able to provide evidence or corroboratingevidence in support of the accompanying supplemental information and we were not able toapply other auditing procedures to satisfy ourselves as to whether the supplemental informationis fairly stated, in all material respects, in relation to the basic financial statements, the scope ofour work was not sufficient to enable us to express, and we do not express, an opinion onwhether the supplemental information is fairly stated, in all material respects, in relation to thebasic financial statements taken as a whole.

Charlotte, North CarolinaSeptember 21,2007

-4-

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30, 2005(Unaudited)

This section of the Housing Authority of New Orleans (HANO)'s financial report representsmanagement's discussion and analysis of HANO's financial performance during the fiscal yearended September 30, 2005. Please read it in conjunction with HANO's financial statements,which follow this section.

FINANCIAL HIGHLIGHTS

• HANO's total net assets as of September 30, 2005 were approximately $142,189,148 ascompared to total net assets of approximately $217,534,244 at September 30, 2004. Thisrepresents a decrease from the prior year of approximately $75,345,096 or 35%.

• During the year, HANO's operating revenues were $10,343,272 less than the$157,951,431 expended on Housing Assistance Payments, General & Administrative,Repairs and Maintenance, Utilities, Tenant Services, Protective Services, andDepreciation Expense. This is better than last year, when expenses exceeded revenues by$29,125,993.

• For the fiscal year ended September 30, 2005, HANO recognized Low Income andSection 8 operating subsidies of $31,962,863 and $64,345,539, respectively. HANO alsorecognized $19,596,920 in HOPE VI grant revenues, $24,282,453 in capital grantrevenues, and $8,545,190 in dwelling rental revenues for the current fiscal year.

• HANO administers federal self-sufficiency programs that benefited 431 Section 8Housing Choice Voucher participants for the fiscal year ended September 30, 2005. Thegoal of these programs is to provide supportive services as well as job readiness andplacement programs. The programs emphasize life skills, education, training and othercomprehensive services. During fiscal year 2005, 12 participants completed the program.Total expenditures on program services for the year were $ 1 18,360.

• For the fiscal year ended September 30, 2005, HANO received a regulatory waiver of itsSEMAP submission. The most current submission in 2004 resulted in a score of (100)

HANO received a regulatory waiver of its FASS score issued by HUD REAC for thefiscal year ended September 30, 2005. HANO received a FASS score of 13 out of 30 forits audited electronic submission to HUD REAC for the fiscal year ended September 30,2004.

- 5 -

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30,2005(Unaudited)

• HANO administers HOPE VI grants that are being used to revitalize distressed propertiesin the West Bank and Ninth Ward communities of greater New Orleans. These grants aredesigned to provide residents of deteriorating public housing communities with newhousing and resident services and training programs. Demolition of 171 obsolete publichousing units and an acquired obsolete 82 unit apartment complex has been completed.These properties along with other acquisition in the development neighborhood are beingused to develop 126 new single-family homes and duplexes for home-ownership andrental. Phase 1 construction consisting of 21 homeownership and 27 rental units isunderway. An alternative financing plan for Phase 2 (78 units) has been approved byHUD. The HOPE VI Community Supportive Services Program (CSS) offers acomprehensive array of job training, educational and life skills programs as well assupport services. At the end of 2006, there were 30 households and 71 personsparticipating in the CSS Program. A Neighborhood Network grant, a state-of-the-artcomputer facility with training programs, and a Youthbuild grant, a youth education andjob training program, were implemented to compliment the CSS Program.

• For the fiscal year ended September 30, 2005, HANO received a regulatory waiver of itsMASS certification. The most current submission in 2004 resulted in a score of (26) outof 30 total points.

• During 2005, Hurricanes Katrina and Rita struck the Gulf Coast region with catastrophicresults. As part of the federal government's efforts to house families impacted by thestorm, HANO participated in the Katrina Disaster Housing Assistance Program(KDHAP). Under KDHAP, special vouchers were issued similar to the Housing ChoiceVoucher program and eligible families were provided assistance. Families began usingthese vouchers in November 2005. In December of 2005, through Congressional action,an appropriations bill was approved that provided funding for the Disaster VoucherProgram (DVP). Under DVP, HANO was to terminate assistance under the KDHAPprogram on February 28, 2006 and move the assisted families to DVP assistance.

Crescent Affordable Housing Corporation (CAHC) was formed in December of 2003, as acomponent unit of HANO. CAHC is a nonprofit membership corporation established for thepurpose of coordinating the development of safe, decent and affordable housing for the low andmoderate income citizens of New Orleans.

Lune <TOr Enterprises, LLC (Lune d'Or) was formed in March of 2004, as a component unitof HANO. Lune d'Or currently serves as the managing member of four Louisiana limited

-6 -

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30,2005(Unaudited)

liability companies. CAHC and HANO serve as co-developers with respect to the affordablehousing projects being constructed by the four LLC's.

Fischer I, LLC (Fischer I) was formed in March of 2004. Fischer I is a Louisiana limitedliability company that currently has 20 affordable housing units under construction.

Fischer III, LLC (Fischer III), Florida II-A (Florida), and Guste I, LLC (Guste) wereformed in December of 2003. Fischer III and Guste are limited liability companies that currentlyhave under construction 103, and 82 affordable housing units, respectively. Florida II-A is alimited liability company that had 168 units under construction prior to Hurricane Katrina.Because of the damages resulting from the hurricane, construction at Florida II-A has beenplaced on hold. The bonds issued for the Florida site have been deferred and HANO is currentlyevaluating how best to proceed with the site.

OVERVIEW OF FINANCIAL STATEMENTSThe annual report consists of three parts - management's discussion and analysis (this section),the basic financial statements, and required supplementary information. The basic financialstatements included in this annual report are those of a special-purpose government engaged in abusiness-type activity. The following statements are included:

• Statement of Net Assets - reports HANO's assets and liabilities at the end of theoperating year and provides information about the nature and amounts of investment ofresources and obligations to creditors.

• Statement of Revenue, Expenses, and Change in Net Assets - reports the results ofactivity over the course of the current year. It details the costs associated with operatingHANO and how those costs were funded. It also provides an explanation of the changein net assets from the previous operating period to the current operating period.

• Statement of Cash Flows - reports HANO's cash flows in and out from operating,investing, noncapital financing, and capital related financing and investing activities. Itdetails the sources of HANO's cash, what it was used for, and the change in cash over thecourse of the operating year.

• The notes to the financial statements explain some of the information in the financialstatements and provide more detailed data.

• The statements are followed by required supplementary information that presentsHANO's electronic data submitted to HUD's Real Estate Assessment Center.

- 7 -

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30, 2005(Unaudited)

Our analysis of HANO as a whole begins on this page. The most important question asked aboutHANO's finances is, "Is HANO, as a whole, better or worse off as a result of the year'sactivities?"

The attached analysis of entity wide net assets, revenue, and expenses are provided to assist withanswering the above question. This analysis includes all assets and liabilities using the accrualbasis of accounting.

Accrual accounting is similar to the accounting used by most private sector companies. Accrualaccounting recognizes revenue and expenses when earned or incurred regardless of when cash isreceived or paid.

Our analysis also presents HANO's net assets and changes in them. You can think of HANO'snet assets as the difference between what HANO owns (assets) to what HANO owes (liabilities).The change in net assets analysis will assist the reader with measuring the health or financialposition of HANO.

Net assets are categorized as one of three types.

I. Invested in capital assets, net of related debt - Capital assets, net of accumulateddepreciation and reduced by debt attributable to the acquisition of those assets;

II. Restricted - net assets whose use is subject to constraints imposed by law or agreement;III. Unrestricted - net assets that are neither invested in capital assets nor restricted.

Over time, significant changes in HANO's net assets are an indicator of whether its financialhealth is improving or deteriorating. To fully assess the financial health of any HousingAuthority, the reader must also consider other non-financial factors such as changes in familycomposition, fluctuations in the local economy, HUD mandated program administrative changes,and the physical condition of the Housing Authority's capital assets.

FINANCIAL ANALYSIS OF THE HANO AS A WHOLE

As noted earlier, net assets may serve over time as a useful indicator of HANO's financialposition. In the case of HANO, assets exceeded liabilities by $142,189,148 at the close of themost recent fiscal year.

By far the largest portion of HANO's net assets (72 percent) reflects the investment in capitalassets (e.g. land, buildings, machinery, and equipment), less any related debt used to acquire

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30,2005(Unaudited)

those assets that are still outstanding. HANO uses these capital assets to provide services to itsprogram participants. Although HANO's investment in capital assets is reported net of relateddebt, it should be noted that the resources needed to repay this debt must be provided from othersources since the capital assets themselves cannot be used to liquidate these liabilities.

Table A-l

Housing Authority of New Orleans Net Assets

2005 2004

Current AssetsRestricted AssetsCapital Assets (net)Other Assets

Total Assets

Current LiabilitiesTenant Security DepositsNon Current Liabilities

Total Liabilities

Invested In Capital Assets (net)Restricted Net AssetsUnrestricted Net Assets

Total Net Assets

$

$

451810371238

26

6896

1022910

142

,385,645,177,102,310

,725508,888,121

,492,535,160

,189

,020,505,828,574,927

,530,107,142,779

,894,641,613

,148

$ 36,201,20170,063,615

195,102,69423,014,346

324,381,856

33,656,471539,225

72,651,916106,847,612

195,102,69329,029,593(6,598,042)

$ 217,534,244

Variance

25.4%-73.4%-47.1%208.9%-26.5%

-20.6%-5.8%-5.2%

-10.0%

-47.5%1.7%

-254.0%

-34.6%

The remaining balance of unrestricted net assets $10,160,613 may be used to meet HANO'songoing obligations to program participants and creditors'.

At the end of the current fiscal year, HANO is able to report positive balances in all categories ofnet assets. The same situation did not hold true for its prior fiscal year where Unrestricted NetAssets had a deficit balance of $6,598,042.

HANO's net assets decreased by $75,345,096 during the current fiscal year. The decreasemainly represents the impact of the casualty loss recognized on capital assets as a result ofHurricane Katrina.

-9 -

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS

September 30, 2005(Unaudited)

HANO's current assets increased by $9,183,819. This increase resulted from the increase ininvestments that are held by component units in connection with development activity.

HANO's restricted assets decreased by $51,418,110. This decrease resulted mainly from thereclassification to unrestricted of the investments cited in the previous note.

HANO's capital assets decreased by $91,924,866. This decrease resulted from the wind andflood damage created by the Gulf Coast Hurricanes of 2005. In accordance with GovernmentalAccounting Standards Board Statement #42, Capital Asset Impairment and InsuranceRecoveries, HANO wrote off capital assets in accordance with the provisions outlined within thestatement.

HANO's other assets increased by $48,088,228. The major component of this increase, asreported, is the recognition of $42,220,000 of debt owed by the Component Units to the PrimaryGovernment unit.

HANO's current liabilities decreased by $6,930,941. This decrease resulted from the paydownof amounts owed to vendors and suppliers.

HANO's tenant security deposit balances decreased minimally by $31,118. This decreaseresulted mainly from normal operations and from the initial wave of the Katrina effect.

HANO's non-current liabilities decreased by $3,763,774 during the current fiscal year Thisdecrease reflects payment of long-term debt during the year.

-10-

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS - CONTINUED

September 3 0,2005(Unaudited)

Table A-2Housing Authority of New Orleans Changes in Net Assets

Nonoperating Revenues:Capital GrantsInvestment IncomeInterest In Notes Receivable

Total Revenues

Expenses:Housing Assistance PaymentsGeneral and AdministrativeRepairs and MaintenanceUtilitiesTenant ServicesProtection ServicesDepreciation and Amortization

Nonoperating Expenses:Interest ExpenseCasualty Loss

HANO's HAP revenues increased by $8,552,316. The increase resulted from increases in thehousing choice voucher program.

HANO's Administrative fee revenues decreased by $899,206. The decrease reflected changes inthe HUD method by which these fees were calculated.

HANO's Operating grant revenues increased by $7,825,380. The increase resulted fromincreases in cash applied to HOPE VI developments.

HANO's Other operating revenues increased by $4,812,649. The increase resulted fromincreased utilization of an infrastructure grant from the City of New Orleans.

HANO's Capital grant revenues decreased by $25,809,049. The decrease resulted from lowerutilization of funds on capital projects and the exhaustion of certain grants that were available inthe previous year.

HANO's Repairs and Maintenance expenses increased by $8,919,409. The increase resultedfrom various major undertakings that constituted extraordinary repairs but which, at the sametime, did not qualify as capital additions.

HANO's Utility expenses decreased by $2,716,122. The decrease resulted from the shutdown ofoperations during September combined with improved efficiency.

HANO's Protection services expenses decreased by $2,111,692. The decrease resulted fromcessation of the service contract with the New Orleans Police Department.

HANO incurred $82,964,252 in Casualty losses that it did not incur in the prior year. Theselosses resulted from the write off of capital assets, due to the storm events, net of insurancerecoveries.

Capital Asset and Debt Administration

Capital assets. HANO's investment in capital assets as of September 30, 2005, amounts to$102,492,894 (net of accumulated depreciation). This investment in capital assets includes land,buildings and improvements, furniture and equipment, and construction in progress. The totalnet decrease in HANO's investment in net capital assets for the current operating year was47.5%.

- 12-

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS - CONTINUED

September 30,2005(Unaudited)

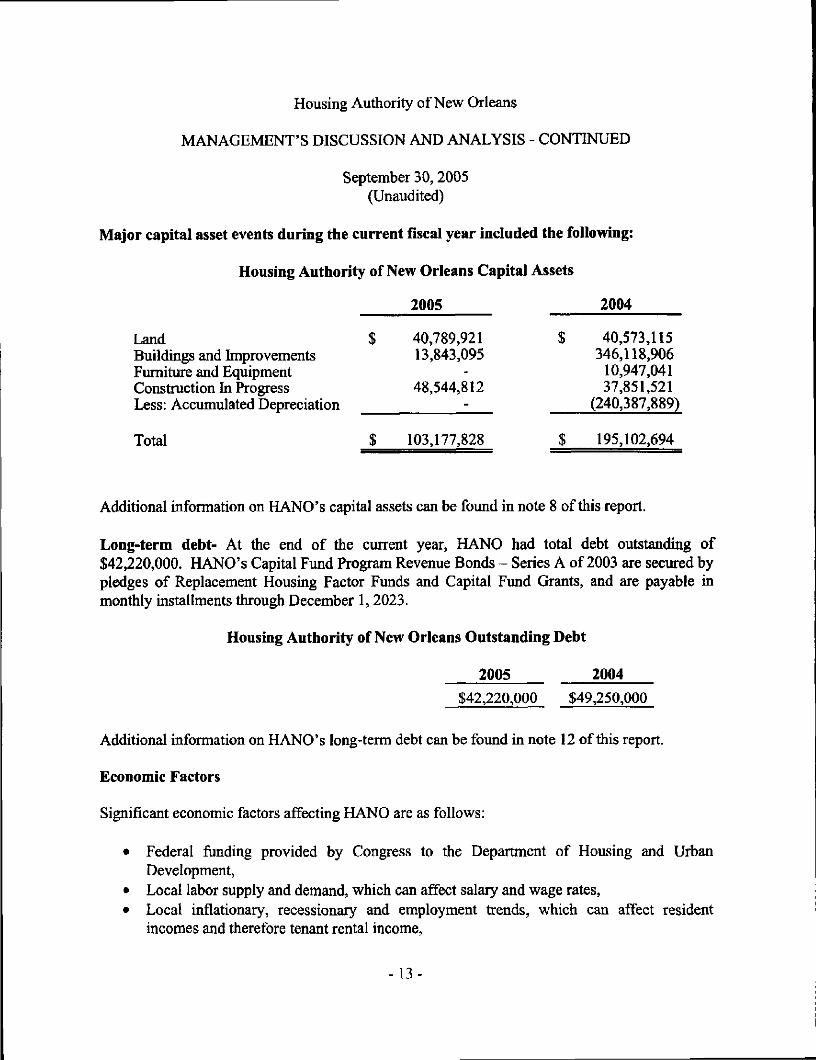

Major capital asset events during the current fiscal year included the following:

Housing Authority of New Orleans Capital Assets

2005 2004

Land $ 40,789,921 $ 40,573,115Buildings and Improvements 13,843,095 346,118,906Furniture and Equipment - 10,947,041Construction In Progress 48,544,812 37,851,521Less: Accumulated Depreciation - (240,387,889)

Total $ 103,177,828 $ 195,102,694

Additional information on HANO's capital assets can be found in note 8 of this report.

Long-term debt- At the end of the current year, HANO had total debt outstanding of$42,220,000. HANO's Capital Fund Program Revenue Bonds - Series A of 2003 are secured bypledges of Replacement Housing Factor Funds and Capital Fund Grants, and are payable inmonthly installments through December 1, 2023.

Housing Authority of New Orleans Outstanding Debt

2005 2004

$42,220,000 $49,250,000

Additional information on HANO's long-term debt can be found in note 12 of this report.

Economic Factors

Significant economic factors affecting HANO are as follows:

• Federal funding provided by Congress to the Department of Housing and UrbanDevelopment,

• Local labor supply and demand, which can affect salary and wage rates,• Local inflationary, recessionary and employment trends, which can affect resident

incomes and therefore tenant rental income,

-13-

Housing Authority of New Orleans

MANAGEMENT'S DISCUSSION AND ANALYSIS - CONTINUED

September 30, 2005(Unaudited)

• Natural disasters which can have a devastating impact on the local economy,• Locality issues which result from goods and services often being required to be imported,• Inflationary pressure on utility rates, supplies and other costs.

Requests for Information

The financial report is designed to provide a general overview of HANO's finances for all thosewith an interest in the Housing Authority's finances. Questions concerning any of theinformation provided in this report or requests for additional financial information should beaddressed to Chief Financial Officer, Housing Authority of New Orleans, 4100 Touro Street,New Orleans, Louisiana 70122.

-14-

Housing Authority of New Orleans

STATEMENT OF NET ASSETSEnterprise Fund and Discretely Presented Component Units

September 30, 2005

ASSETS

Current AssetsCash and cash equivalents - unrestrictedInvestmentsAccounts receivable - PHA projectsAccounts receivable - HUDAccounts receivable - otherPrepaid expenses

Total Current Assets

Restricted AssetsResident security depositsRestricted cashResident loan collateralRestricted bond and grant funds

Total Restricted Assets

Capital AssetsLandBuildings and improvementsFurniture, equipment and machinery -

administrationConstruction in progress

Less: Accumulated depreciation

Total Capital Assets

Other Noncurrent AssetsNotes receivable from component unitsNotes receivable- otherAccrued interest receivable - notes receivablePrepaid ground leaseOther assets

Total Other Noncurrent Assets

Total Assets

PrimaryGovernment

$ 28,289,4475,542,213

494,107802,453

9,602,423654,377

45,385,020

529,8276,571,945

11,543,733

18,645,505

40,789,92113,843,095

48,544,812

103,177,828

103,177,828

42,220,00026,891,652

1,990,922

71,102,574

238,310,927

ComponentUnits

$ 731,19035,676,345

1,742,612

38,150,147

28,287331,877

360,164

15,66114,306,436

14,322,097(15,661)

14,306,436

123,1862,143,189

2,266,375

55,083,122

TotalReporting

Entity

$ 29,020,63741,218,558

494,107802,453

11,345,035654,377

83,535,167

529,8276,600,232

331,87711,543,733

19,005,669

40,789,92113,843,095

15,66162,851,248

117,499,925(15,661)

117,484,264

42,220,00026,891,652

1,990,922123,186

2,143,189

73,368,949

293,394,049

(Continued)

-15-

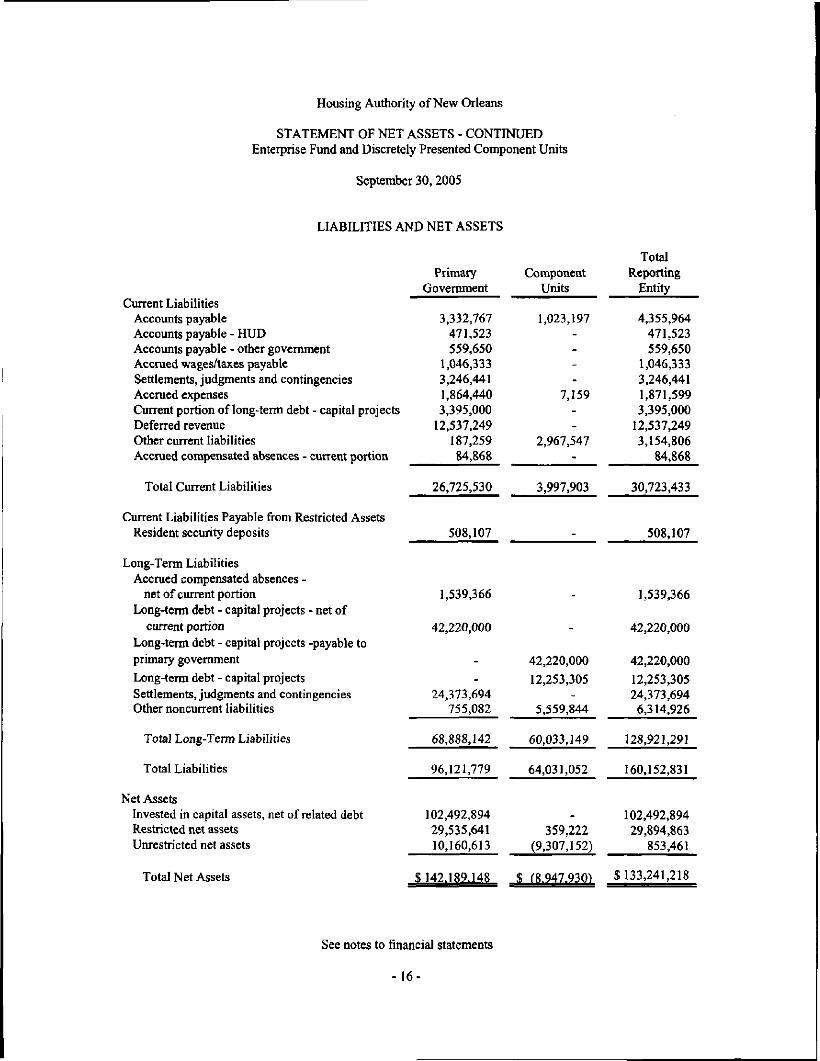

Housing Authority of New Orleans

STATEMENT OF NET ASSETS - CONTINUEDEnterprise Fund and Discretely Presented Component Units

September 30,2005

LIABILITIES AND NET ASSETS

Current LiabilitiesAccounts payableAccounts payable - HUDAccounts payable - other governmentAccrued wages/taxes payableSettlements, judgments and contingenciesAccrued expensesCurrent portion of long-term debt - capital projectsDeferred revenueOther current liabilitiesAccrued compensated absences - current portion

Total Current Liabilities

Current Liabilities Payable from Restricted AssetsResident security deposits

net of current portionLong-term debt - capital projects - net of

current portionLong-term debt - capital projects -payable toprimary governmentLong-term debt - capital projectsSettlements, judgments and contingenciesOther noncurrent liabilities

Total Long-Term Liabilities

Total Liabilities

Net AssetsInvested in capital assets, net of related debtRestricted net assetsUnrestricted net assets

Total Net Assets

PrimaryGovernment

3,332,767471,523559,650

1,046,3333,246,4411,864,4403,395,000

12,537,249187,25984,868

26,725,530

ComponentUnits

1,023,197----

7,159--

2,967,547-

3,997,903

TotalReporting

Entity

4,355,964471,523559,650

1,046,3333,246,4411,871,5993,395,000

12,537,2493,154,806

84,868

30,723,433

508,107 508,107

1,539,366

42,220,000

-

24,373,694755,082

68,888,142

96,121,779

102,492,89429,535,64110,160,613

-

42,220,000

12,253,305

5,559,844

60,033,149

64,031,052

359,222(9,307,152)

1,539,366

42,220,000

42,220,000

12,253,30524,373,6946,314,926

128,921,291

160,152,831

102,492,89429,894,863

853,461

(8.947.930) $133,241,218

See notes to financial statements

- 16-

Housing Authority of New Orleans

STATEMENT OF REVENUES, EXPENSES AND CHANGES IN NET ASSETSEnterprise Fund and Discretely Presented Component Units

Year ended September 30, 2005

Operating RevenueDwelling rentHUD operating subsidy and grant revenueOther income

Total Operating Revenue

Operating ExpensesAdministrativeTenant servicesUtilitiesMaintenance and operationsProtective servicesGeneralHousing assistance paymentsExtraordinary maintenanceDepreciation

Total Operating Expense

Operating Loss

Nonoperating Revenues (Expenses)Investment incomeInterest on notes receivableCasualty lossInterest expense

Total Nonoperating Revenues (Expenses)

Loss Before Capital Grants

Capital GrantsHUD capital grantsState and city grants

Total Capital Grants

Change in Net Assets

Net Assets - Beginning

Capital contributions

Net Assets - Ending

PrimaryGovernment

$ 8,545,190 $128,620,153

10,442,816

147,608,159

23,341,0344,755,982

10,212,43716,037,036

1,442,6943,579,810

62,906,02114,888,95020,787,467

157,951,431

(10,343,272)

768,7321,609,180

(82,964,252)(2,110,746)

(82,697,086)

(93,040,358)

11,647,7756,047,487

17,695,262

(75,345,096)

217,534,244

$ 142,189,148 $

ComponentUnits

i -

_

38,309

48,371

86,680

(86,680)

(10,493,472)

(10,493,472)

(10,580,152)

-

(10,580,152)

359,222

1,273,000

J8,947,930)

TotalReporting

Entity

$ 8,545,190128,620,15310,442,816

147,608,159

23,379,3434,755,982

10,212,43716,037,0361,442,6943,628,181

62,906,02114,888,95020,787,467

158,038,111

(10,429,952)

768,7321,609,180

(93,457,724)(2,110,746)

(93,190,558)

(103,620,510)

11,647,7756,047,487

17,695,262

(85,925,248)

217,893,466

1,273,000

$ 133,241,218

See notes to financial statements

- 17-

Housing Authority of New Orleans

STATEMENT OF CASH FLOWSEnterprise Fund

Year ended September 30,2005

Cash flows from operating activitiesDwelling rent receiptsOperating subsidy and grant receiptsOther income receipts

Total receipts

Payments to vendorsPayments to employeesHousing assistance payments

Total disbursements

Net cash provided by operating activities

Cash flows from investing activitiesInvestment incomeNotes receivable advancesDecrease in investments

Net cash provided by investing activities

Cash flows from capital and related financing activitiesCapital grants receipts - HUDCapital asset purchasesCapital grants - state and cityLong-term borrowingLoan costs paidInterest paid on long-term debt

Net cash provided by capital and related financing activities

NET INCREASE IN CASH

Cash and cash equivalents, beginning

Cash and cash equivalents, ending

Reconciliation to Statement of Net Assets:Cash and cash equivalents- unrestrictedRestricted cashResident security deposits

Increase (decrease) in liabilitiesAccounts payableAccounts payable - HUDAccrued wages/taxes payableSettlements, judgments and contingenciesHomebuyers reversersOther current liabilitiesDeferred revenueTenant security deposits payableAccrued compensated absences

Total adjustments

Net cash used by operating activities

PrimaryGovernment

$ (10,343,272)

20,787,46754,353

121,7522,629,024

(8,068,213)(369,650)934,593

1,950,493(572,979)266,653

(319,810)(304,739)148,608

(6,028,887)(31,118)

3,462

11,201,009

$ 857,737

See notes to financial statements

-19-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS

September 30, 2005

NOTE 1 - ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTINGPOLICIES

Organization

The Housing Authority of New Orleans (HANO) is a public body corporate and politicestablished on September 29, 1936 pursuant to the laws of the State of Louisiana to providelow-rent housing for qualified individuals in accordance with the rules and regulationsprescribed by the Department of Housing and Urban Development (HUD) and other FederalAgencies. The primary purpose of HANO is to provide safe, decent, sanitary, and affordablehousing to low-income, elderly, and disabled families in New Orleans, Louisiana.

Reporting Entity

GASB Statement No. 14, The Financial Reporting Entity, established criteria for determiningthe governmental reporting entity and component units that should be included within thereporting entity. Under the provisions of this Statement, HANO is considered a primarygovernment, since it is a special purpose government that has a separate governing body, islegally separate, and is fiscally independent of other state or local governments.

HANO is a related organization of the City of New Orleans since Commissioners areappointed by the Mayor of the City of New Orleans. The City of New Orleans is notfinancially accountable for HANO as it cannot impose its will on HANO and there is nopotential for HANO to provide financial benefit to, or impose financial burdens on, the Cityof New Orleans. Accordingly, HANO is not a component unit of the financial reportingentity of the City of New Orleans. HANO has been determined to be a "Troubled Agency"by HUD, and HUD has appointed a Receiver to act as the Executive Director and hasreplaced HANO's Board of Commissioners with its own appointed Board.

In determining how to define the reporting entity, management has considered all potentialcomponent units. The determination to include a component unit in the reporting entity wasmade by applying the criteria set forth in Section 2100 and 2600 of the Codification ofGovernmental Accounting and Financial Reporting Standards and GASB Statement No. 14(amended) and GASB Statement No. 39, Determining Whether Certain Organizations areComponent Units. These criteria include manifestation of oversight responsibility; includingfinancial accountability, appointment of a voting majority, imposition of will, financialbenefit to or burden on a primary organization, financial accountability as a result of fiscaldependency, potential dual inclusion, and organizations included in the reporting entityalthough the primary organization is not financially accountable.

-20-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

Reporting Entity

As part of a major redevelopment plan HANO formed a non-profit corporation and fiveseparate limited liability corporations during the fiscal year of 2004.

Crescent Affordable Housing Corporation (CAHC) was formed in December 2003 as a non-profit membership corporation in which HANO serves as the sole member, for the purpose ofcoordinating the development of safe, decent and affordable housing to low and moderateincome citizens of New Orleans. CAHC has applied for tax exempt status under Section501(c)(3) of the Internal Revenue Code (the Code) as a supporting organization underSection 509(a)(3) or the Code, the sole purpose of which is to carry out the affordablehousing mission of HANO.

Lune d'Or Enterprises, LLC (Lune d'Or), a Louisiana limited liability company, whose solemember is CAHC was formed in March 2004. Lune d'Or currently serves as the managingmember of four Louisiana limited liability companies, each of which will own a singleaffordable housing project qualified for low-income housing tax credits. The purpose of thefour LLC's is to redevelop or construct mixed income housing. CAHC and HANO willserve as co-developers with respect to these affordable housing projects.

Fischer I, LLC was formed in March 2004. The Fischer I project will be financed using taxcredit equity investments.

Fischer III, LLC, Florida II-A, LLC, and Guste I, LLC's were formed in December 2003.The Fischer III, Florida II-A and Guste I projects will be funded with mixed-financing whichwill include, but not be limited to, funds borrowed pursuant to the Trust Indenture betweenHANO, JP Morgan Trust Company, NA and the Industrial Development Board of the City ofNew Orleans, Louisiana, Inc (the Bond Issuer), from the proceeds of the Capital FundProgram Revenue Bonds, Series A of 2003 (the Bonds), tax credit equity investment funds,construction loans from a conventional lender, and Affordable Housing Program grant fundsfrom the Federal Home Loan Bank.

CAHC and Lune d'Or are component units of HANO and are reported as blended componentunits. Fischer I, Fischer III, Florida II-A and Guste I are reported as discreetly presentedcomponent units of HANO.

HANO has an additional subsidiary/affiliate organization, the HANO Resident LoanCorporation, Inc. Based upon the application of the criteria mentioned above, HANOResident Loan Corporation, Inc. is a discreetly presented component unit of HANO.

-21 -

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 3 0,2005

Programs Administered by HANQ

The main programs of HANO are as follows:

• Low-Rent Public Housing under Annual Contributions Contract FW-1190 and relatedprograms for development, modernization, community development, and residentassistance.

• Housing Choice Voucher Program (formerly Section 8 Rental Assistance Program):Rental Vouchers FW-2217Moderate Rehabilitation/Single Room Occupancy FW-2147New Construction FW-2201

• Locally Owned Homeownership Program

• Resident-Managed Low-Rent Public Housing

Basis of Presentations and Accounting

In accordance with both Louisiana State Reporting Law (LAS-R.S.24:514) and uniformfinancial reporting standards for HUD housing programs, the financial statements areprepared in accordance with United States generally accepted accounting principles (GAAP).The Governmental Accounting Standards Board (GASB) is the accepted standards settingbody for establishing accounting and financial reporting standards.

Based upon compelling reasons offered by HUD, HANO reports under the governmentalproprietary fund type (enterprise fund), which uses the accrual basis of accounting. Theenterprise fund emphasizes the flow of economic resources as a measurement focus. In thisfund, revenues are recorded when earned and expenses are recorded at the time the liabilitiesare incurred. Pursuant to the election option made available by GASB Statement No. 20,Accounting and Financial Reporting for Propriety Funds and Other Governmental EntitiesThat Use Proprietary Fund Accounting, pronouncements of the Financial AccountingStandards Board (FASB) issued after November 30, 1989 are applied in the preparation ofthe financial statements.

The enterprise method is used to account for those operations that are financed and operatedin a manner similar to private business, or where the Board has decided that thedetermination of revenues earned, costs incurred, and/or net income necessary formanagement accountability is appropriate. The intent of the governing body is that the costs

-22-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 3 0,2005

(expenses including depreciation) of providing services to the general public on a continuingbasis be financed or recovered primarily through funding from HUD and charges to residentsfor rent and other fees.

All of HANO's programs are accounted for as one business-type activity reported in a singleenterprise fund.

Budgets

Budgets are prepared on an annual basis for each major operating program and are used as amanagement tool throughout the accounting cycle. The capital fund budgets are adopted ona "project length" basis. Budgets are not, however, legally adopted nor legally required forfinancial statement presentation.

Operating Revenue and Expenses

Operating revenues and expenses consist of revenues earned and expenses incurred as aresult of the principal operations of HANO. Operating revenues consist of tenant rents andfees and HUD operating grants. Non-operating revenues consist of investment income andother non-operating revenues. Non-operating expenses consist of interest expense.

Cash Equivalents

Cash and cash equivalents include amounts in demand deposits, interest-bearing demanddeposits, and time deposits and other investments with original maturities of 90 days or less.Under state law, HANO may deposit funds in demand deposits, interest-bearing demanddeposits, or time deposits with state banks organized under Louisiana law or any other stateof the United States, or under the laws of the United States.

Investments

Investments are recorded at fair value. Investment instruments consist only of itemsspecifically approved for public housing agencies by the U.S. Department of Housing andUrban Development. Investments are either insured or collateralized using the dedicatedmethod. Under the dedicated method of collateralization, all deposits and investments overthe federal depository insurance coverage are collateralized with securities held by HANO'sagent in HANO's name. It is HANO's policy that all funds on deposit are collateralized inaccordance with both HUD requirements and requirements of the State of Louisiana.

-23-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30,2005

Inventories

Inventories are valued at cost using the First-In, First-Out (FIFO) method. If inventory fallsbelow cost due to damage, deterioration, or obsolescence, HANO establishes an allowancefor obsolete inventory. HANO uses the consumption method for expense recognition andrelies upon its periodic (annual) inventory for financial reporting purposes.

Prepaid Items

Payments made to vendors for services that will benefit periods beyond the fiscal year endare recorded as prepaid items.

Restricted Assets

Certain assets may be classified as restricted assets on the statement of net assets becausetheir use is restricted for modernization programs, security deposits held in trust, family self-sufficiency program escrows, and homebuyers' reserves, among others.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generallyaccepted in the United States of America requires management to make estimates andassumptions that affect the reported amounts of assets and liabilities and disclosure ofcontingent assets and liabilities at the date of the financial statements and reported amountsof revenues and expenses during the reporting period. Actual results could differ from thoseestimates.

Fair Value of Financial Instruments

The carrying amount of HANO's financial instruments at September 30, 2005 includingcash, investments, accounts receivable, and accounts payable closely approximates fairvalue.

Capital Assets

All purchased capital assets are valued at cost when historical records are available. Whenno historical records are available, capital assets are valued at estimated historical cost. Landvalues were derived from development closeout documentation. Donated capital assets arerecorded at their fair value at the time they are received. All normal expenditures of

-24-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

preparing an asset for use are capitalized when they meet or exceed the capitalizationthreshold.

Pursuant to the enterprise GAAP method, the cost of buildings and equipment is depreciatedover the estimated useful lives of the related assets on a composite basis using the straight-line method. Depreciation commences on modernization and development additions in theyear following completion, or in the fifth year if the program is 90% complete. The usefullives of buildings and equipment for purposes of computing depreciation are as follows:

Buildings 271/2 yearsBuilding modernization 10 yearsVehicles 5 yearsEquipment 5 years

Maintenance and repairs expenditures are charged to operations when incurred. Bettermentsin excess of $5,000 are capitalized. When land, buildings and equipment are sold orotherwise disposed of, the asset account and related accumulated depreciation account arerelieved, and any gain or loss is included in operations.

Costs of assets damaged by Hurricane Katrina were reduced by the impairment and theadjusted cost depreciated over the assets remaining life.

Impairment of Long-Lived Assets

In accordance with GASB No. 42, Accounting and Financial Reporting for Impairment ofCapital Assets and for Insurance Recoveries, the Authority has at September 30, 2005,recognized in the accompanying financial statements the impact of demolition activities andimpairment related to the hurricane. Under the provisions of the statement, prominent eventsor changes in circumstances affecting capital assets are required to be evaluated to determinewhether impairment of a capital asset has occurred. Impaired capital assets that will nolonger be used should be reported at the lower of carrying value or fair value. Impairment ofcapital assets with physical damage generally should be measured using the restoration costapproach, which uses the estimated cost to restore the capital asset to identify the portion ofthe historical cost of the capital asset that should be written-off. Impairment has beenrecorded on the majority of the Authority's capital assets.

-25-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

Compensated Absences

Compensated absences are those absences for which employees will be paid, such as annual/vacation and sick leave. A liability for compensated absences for annual/vacation leave thatis attributable to services already rendered and that is not contingent on a specific event,outside the control of HANO and its employees, is accrued as employees earn the rights tothe benefits. Compensated absences that relate to future services or that are contingent on aspecific event that is outside the control of HANO and its employees are accounted for in theperiod in which such services are rendered or in which such events take place.

Litigation Losses

HANO recognizes estimated losses related to litigation in the period in which the eventgiving rise to the loss occurs, the loss is probable, and the loss can be reasonably estimated.

Annual Contribution Contracts

Annual Contribution Contracts provide that HUD shall have the authority to audit andexamine the records of public housing authorities. Accordingly, final determination ofHANO's financing and contribution status for the Annual Contribution Contracts isdetermined by HUD based upon financial reports submitted by HANO.

Risk Management

HANO is exposed to various risks of loss related to torts; theft of, damage to, and destructionof assets; errors and omissions; injuries to employees; and natural disasters. HANO carriescommercial insurance for risks of loss regarding workers* compensation and employee healthand accident insurance. Settled claims resulting from these risks have not exceededcommercial insurance coverage in any of the past three fiscal years, with the exception ofautomobile liability insurance claims, which exceed coverage by $1,600,000. Additionally,there has been no significant reduction in insurance coverage from the prior year. For otherrisks regarding property and general liability, HANO is self-insured (see notes 9 and 10).

NOTE 2 - DEPOSITS AND INVESTMENTS

Cash and Cash Equivalents

It is the Authority's policy for deposits to be secured by collateral valued at market or par,whichever is lower, less the amount of the Federal Deposit Insurance Corporation (FDIC)insurance. It is HANO's policy to maintain collateralization in accordance with HUD

-26-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30,2005

requirements. All balances are collateralized at 102% in accordance with requirements ofcollateralization agreement.

Investments

Investments consist of certificates of deposits and government securities. It is the policy ofthe Authority that investments be secured by collateral valued at market or par, whichever islower, less the amount of FDIC insurance.

Risks

Interest rate risk - The Authority's policy does not address interest rate risk.

Credit rate risk - The Authority's investments consist of certificates of deposits, which do nothave credit ratings, and government securities; however, the Authority's policy does notaddress credit rate risk.

Custodial credit risk - This is the risk that in the event of a bank failure, the Authority'sdeposits and investments may not be returned to it. As of September 30, 2005, $56,186,284of the Authority's deposits and investments were exposed to this risk because the amountswere in excess of FDIC insurance limits and the accounts were collateralized with securitiesheld by the pledging financial institutions in the Authority's name. The following schedulesummarizes the custodial credit risk:

BalanceReported on the Balance

Authrity's Deposited with FDIC Insurance UnisuredFinancial the Financial Amount (Fully

Statements Institution Collateralized)Bank deposits $ 35,391,219 $ 39,690,338 $ 600,000 $ 39,090,338Funds held by trustees -

government securities 11,553,733 11,553,733 - 11,553,733Certificates of

Deposits 5,542,213 5,542,213 - 5,542,213

Total $ 52,487,165 $ 56,786,284 $ 600,000 $ 56,186,284

-27-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

Cash and cash equivalents are reported on the statement of net assets as follows:

Cash and cash equivalents - unrestricted $ 28,289,447Cash and cash equivalents - restricted 6,571,945Cash and cash equivalents - security deposit 529,827

Total cash and cash equivalents $ 35,391,219

Investments are reported on the statement of net assets as follows:

Investments - unrestricted $ 5,542,213Restricted bond and grant funds 11,543,733

NOTE 3 - RESTRICTED CASHRestricted cash as of September 30,2005 consisted of the following:

Orleans Parish School Board Escrow $ 308,122Family self-sufficiency 366,312Cash for modernization 5,484,016Program income 413,495

$ 6,571,945

-28-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30,2005

NOTE 4 - ACCOUNTS RECEIVABLE

Accounts receivable as of September 30,2005 consisted of the following:

Accounts receivable - tenants $ 316,710Allowance for doubtful accounts (316,710)

Net tenant receivables

HUD (see NOTE 5 for detail) 802,453Accounts receivable- Limited Partnership- development cost 1,291Advances to development projects 10,058,239Other 37,000

$ 10,898,983

NOTE 5 - DUE FROM/TO U.S. DEPARTMENT OF HOUSING AND URBANDEVELOPMENT

Amounts due from HUD as of September 30, 2005 were as follows:

2002 ROSS $ 2,4151994 HOPE VI - Desire 657,7381996 HOPE VI - St. Thomas 6,3052002 HOPE VI - Fischer 3,4872002 HOPE VI - Guste 3,9362002 HOPE VI - Florida 2,8802002 HOPE VI - B.W. Cooper 2,8802004 CFP 122,812

$ 802,453

Amounts due to HUD as of September 30, 2005 were as follows:

New Construction $ 415,185Mod/ Rehab 56,338

$ 471,523

-29-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

NOTE 6 - PREPAID EXPENSES

Prepaid expenses as of September 30,2005 consisted of prepaid insurance of $654,377.

NOTE 7 - NOTES RECEIVABLE

Abundance Square Associates

HANO has a note receivable with Abundance Square Associates, Limited Partnership in themaximum original amount of $2,577,025. The note was issued to partially finance theconstruction of public housing, which will be owned and operated by the borrower. Prior toConstruction Completion, each advance on the note bore interest at the long-term federal rateapplicable on the date of each advance. After Construction Completion, the rate of interestpayable on the outstanding principal shall be a blended rate, on a weighted basis, of theaverage interest rates applicable to each advance. Construction Completion occurred in June2003 and the blended rate is 4.78%. All principal and accrued interest is due atDecember 31, 2043. The balance outstanding at September 30, 2005 was $2,160,508, plusaccrued interest receivable of $ 186,031.

Treasure Village Associates

HANO has a note receivable with Treasure Village Associates, Limited Partnership in themaximum original amount of $1,100,000. The note was issued to partially finance theconstruction of public housing, which will be owned and operated by the borrower. Prior toConstruction Completion, each advance on the note bore interest at the long-term federal rateapplicable on the date of each advance. After Construction Completion, the rate of interestpayable on the outstanding principal shall be a blended rate, on a weighted basis, of theaverage interest rates applicable to each advance. Construction Completion occurred inMarch 2004 and the blended rate is 5.09%. All principal and accrued interest is due atDecember 31, 2053. The balance outstanding at September 30, 2005 was $1,100,000, plusaccrued interest receivable of $99,627.

St. Thomas HOPE VI

HANO has a note receivable with LCD Rental I, LLC in the original amount of $13,360,800.The note was issued to partially finance the rehabilitation and revitalization of HOPE VIapartment complexes. The note accrues interest at 1% per annum. Principal and accruedinterest are payable from cash flow, as defined. All principal and accrued interest is due at

-30-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

October 1, 2043. The balance outstanding at September 30, 2005 was $13,360,800 plusaccrued interest of $267,216.

HANO has a note receivable with LGD Rental I, LLC in the original amount of $10,519,620.The note was issued to partially finance the rehabilitation and revitalization of HOPE VIapartment complexes. The note accrues interest at 1% per annum. Principal and interest arepayable from cash flow, as defined. All principal and accrued interest is due at October 1,2043. The balance outstanding at September 30, 2005 was $4,616,230 plus accrued interestof $92,393.

Guste I. LLC

HANO has a construction mortgage note receivable with Guste I, LLC in the original amountof $ 10,634,315. The note accrues interest at 3% per annum. Principal and accrued interest isdue at February 1, 2007. The balance outstanding at September 30, 2005 was $10,634,315plus accrued interest of $312,221.

Florida IIA. LLC

HANO has a construction mortgage note receivable with Florida IIA, LLC in the originalamount of $20,876,450. The note accrues interest at 3% per annum. Principal and accruedinterest is due at February 1, 2007. The balance outstanding at September 30, 2005 was$20,876,450 plus accrued interest of $607,420.

-31-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30,2005

Florida III. LLC

HANO has a construction mortgage note receivable with Florida III, LLC in the originalamount of $14,710,628. The note accrues interest at 3% per annum. Principal and accruedinterest is due at February 1, 2007. The balance outstanding at September 30, 2005 was$14,710,628 plus accrued interest of $426,084.

Non-Current

Abundance SquareTreasure VillageGusteFlorida IIAFischer HIProgram income loansLCDLCD

NOTE 8 - LAND, BUILDINGS, AND EQUIPMENT

Notes Receivable$

$

2,160,5081,100,000

10,634,31220,876,45014,710,6281,652,724

13,360,8004,616,230

69,111,652

Accrued Interest$ 186,031

99,627312,221607,420426,084

-267,21692,393

$ 1,990,992

LandBuildingsEquipment - dwellingEquipment - administrationConstruction in progress

NOTE 9 - ACCRUED CONTINGENT LIABILITIES AND SETTLEMENTS

Current Long-term Total

Judgments and settled claims $ 2,059,795 $ 5,936,045 $ 7,995,840Interest payable on judgments and claims 1,186,646 99,446 1,286,092Pending claims - 18,338,243 18,338,243

$ 3,246,441 $ 24,373,734 $ 27,620,175

Reconciliation of Accrued Contingent Liabilities and Settlements to the FDS:

Line 324 Line 353 Total

Judgments and settled claims $ 2,059,795 $ 5,936,045 $ 7,995,840Interest payable on judgments and claims 1,186,646 99,446 1,286,092Pending claims

Other noncurrent liabilities:Homebuyers' reserve liability

-

3,246,441

.

$ 3,246,441

18,338,243

24,373,734

755,082

755,082

$ 25,128,816

18,338,243

27,620,175

755,082

755,082

$ 28,375,257

NOTE 10 - RISK MANAGEMENT

As stated in Note 1, HANO is exposed to various risks of loss related to torts; theft of,damage to, and destruction of assets for which HANO is self-insured for general liability,workers' compensation claims, fire and extended coverages.

Due to funding shortfalls, HANO has been unable to fund its self insurance fund inaccordance with state law requirements. Additionally, paragraph 22 of GASB Statement # 10"Accounting and Financial Reporting for Risk Financing and Related Insurance Issue", statesin part; A liability for unpaid claims costs, including estimates of costs related to incurredbut not reported (INBR) claims should be accrued when insured events occur. Due tobudgetary shortfalls, HANO has not had an analysis performed to identify IBNR nor has

- 3 3 -

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

HANO established a liability for these potential claims. With the events of HurricaneKatrina, HANO anticipates realization of significant losses associated with shortfalls incoverage as well as unfunded reserves. These amounts are expected to be recognized andrecorded for the fiscal year ended September 30,2006.

HANO is a defendant in various lawsuits in which a probable loss to HANO has beenestimated. This estimate has been recorded in the financial statements as shown in Note H,above.

HANO is also a defendant in various lawsuits related to accidents and injuries on HANOproperties, for which no probability of outcome has been determined. In addition, HANO isa defendant in a class action lawsuit regarding alleged lead-based paint poisoning. Noestimate of probable loss has been made in this regard.

NOTE 11 - COMPENSATED ABSENCES PAYABLE

HANO has established a policy (in accordance with State Civil Service) to pay eachemployee their accrued annual leave upon termination up to a maximum of 300 hours. Thecost of current leave privileges, computed in accordance with GASB codification SectionC60, is recognized as a current year expense in the period in which it is earned, inaccordance with generally accepted accounting principles.

At September 30, 2005 total leave to be paid upon termination is $1,624,233. Of thisamount, $84,868 is deemed to be a current liability.

NOTE 12 - LONG-TERM DEBT

Pursuant to a Trust Indenture between HANO, the Industrial Development Board of the Cityof New Orleans, Louisiana, Inc. and J.P. Morgan Trust Company, NA dated December 1,2003, bonds in the amount of $49,250,000 titled "Capital Fund Program Revenue BondsSeries A of 2003". The proceeds of the bonds were used to finance loans to fund a portion ofthe construction and development costs of three affiliated entities: Guste I, LLC, Florida II-A, LLC and Fischer III, LLC. The managing member of each of these affiliates is Lune d'orEnterprises, LLC, whose sole member is Crescent Affordable Housing Corporation. Asdiscussed in Note A, HANO is the sole member of Crescent Affordable HousingCorporation.

-34 -

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30, 2005

The bonds bear interest at a rate of 4.45% and require interest payable each June 1st andDecember 1st. Principal payments of varying amounts are due annually beginningDecember 1, 2004, with a final maturity date of December 1, 2023.

HANO, with the approval of HUD, has pledged a portion of its Replacement Housing Factorfunds (a component of its annual Capital Fund grants from HUD) as security for payment ofprincipal and interest on the bonds.

Aggregate annual debt service requirements for the bonds are as follows:

Year ending September 30,2006200720082009

2010-20142015-20192020-2023

NOTE 13 - DEFINED CONTRIBUTION PENSION PLAN

HANO provides pension benefits for all its full-time employees through a definedcontribution plan entitled "Housing Authority of New Orleans Pension Plan". The plan isadministered by the Pension Plan Committee and was revised in November 2004. ThePension Plan Committee consists of employees of HANO. As a defined contribution plan,benefits depend solely on amounts contributed to the plan plus investments earnings. TheBoard of Commissioners for HANO is authorized to establish and amend plan benefits.Employees are eligible to participate after one hour of service.

HANO contributes 5% of the employee's base salary each month, while the employeecontributes a mandatory 14 of 1% of their gross wages. HANO's contributions for eachemployee, and interest allocated to the employee's account, are fully vested after 3 years ofservice. Interest forfeited, either as a result of death or employees who leave employmentprior to being vested, is apportioned among all participants in the plan year in which theforfeiture occurs.

HANO's total payroll in fiscal year 2005 was $20,399,585. The contributions of HANO andemployees were calculated using $14,387,482. HANO and the employees madecontributions amounting to $610,266 and $120,842, respectively.

NOTE 14 - ECONOMIC DEPENDENCY

HANO received approximately 83% of its revenues from the U.S. Department of Housingand Urban Development (HUD) in the fiscal year. If the amount of revenues received fromHUD falls below critical levels, HANO's operating results could be adversely affected.

NOTE 15 - CONTINGENCIES

HANO is subject to possible examinations made by Federal and State authorities whodetermine compliance with terms, conditions, laws and regulations governing other grantsgiven to HANO in the current and prior years. There were no such examinations for the yearended September 30, 2005.

NOTE 16 - ANNUAL CONTRIBUTIONS CONTRACT FW-1190

Annual Contributions Contract FW-1190

Pursuant to the Annual Contributions Contract, HUD contributes an operating subsidyapproved in the operating budget. Operating subsidy contributions for the year endedSeptember 30, 2005, were $24,014,462 for HANO managed Low-Rent Public HousingProgram and $7,948,401 for the Resident Managed Low-Rent Public Housing Program.

Annual Contributions Contracts

Housing Choice Voucher Program Annual Contributions Contracts provide for housingassistance payments to private owners of residential units on behalf of eligible low or verylow-income families. The program provides for such payments with respect to existing andmoderately rehabilitated housing covering the difference between the maximum rental on adwelling unit, and the amount of rent contribution by a participating family and relatedadministrative expense.

-36-

Housing Authority of New Orleans

NOTES TO FINANCIAL STATEMENTS - CONTINUED

September 30,2005

HUD contributions for the year ended September 30,2005, were as follows:

HANO is engaged in a modernization and development program and has entered intoconstruction-type contracts with approximately $18,592,000 remaining until completion.

NOTE 18 - RESTRICTED NET ASSETS

Restricted net assets at September 30, 2005 consisted of the following:

Unspent proceeds from City of New OrleansTax Increment Financing Bonds $ 5,903,390

Unspent grant from the City of New Orleansplus accrued interest in excess ofdeferred revenue 96,792

Notes receivable plus accrued interest 23,535,459

$29.535.641

-37-

Reznick Group, RC Tel: (704) 332-9100

525 N. Tryon Street Fax; (704) 332-6444

Suite 1000 www.reznickgroup.com

Charlotte, NC 28202

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND COMPLIANCE AND OTHER MATTERS

BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMEDIN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of DirectorsThe Housing Authority of New Orleans

We have audited the accompanying statement of net assets of the Housing Authority ofNew Orleans (HANO) as of and for the year ended September 30, 2005, and we were engaged toaudit the related statements of revenue, expenses and changes in net assets, and cash flows, aslisted in the table of contents for the year then ended and have issued our report thereon datedSeptember 21, 2007 which report was qualified for the potential liabilities for incurred but notreported claims as described in the third paragraph therein.

We were unable to obtain records regarding tenant income and expenses and HANO wasunable to provide sufficient documentation on the statement of net assets accounts that weredeemed unverifiable by their consultants and written off to the statement of revenue, expensesand changes in net assets. We conducted our audit in accordance with auditing standardsgenerally accepted in the United States of America and the standards applicable to financialaudits contained in Government Auditing Standards, issued by the Comptroller General of theUnited States.

Internal Control Over Financial Reporting

As stated in the second paragraph above, many of the documents required for our auditwere unavailable. Therefore, we were unable to perform all procedures we considerednecessary. To the extent possible, we considered the Housing Authority of New Orleans'internal control over financial reporting hi order to determine our procedures for the purpose ofexpressing our opinion on the basic financial statements and not to provide an opinion on theinternal control over financial reporting. However, we noted certain matters involving theinternal control over financial reporting and its operation that we consider to be reportableconditions. Reportable conditions involve matters coming to our attention relating to significantdeficiencies in the design or operation of the internal control over financial reporting that, in ourjudgment, could adversely affect the Housing Authority of New Orleans' ability to record,process, summarize and report financial data consistent with the assertions of management in thefinancial statements. Reportable conditions are described in the accompanying Schedule ofFindings and Questioned Costs as items 2005-1, 2005-2, and 2005-4.

-38-

Atlanta • Baltimore • Bethesda • Charlotte • Chicago • Los Angeles • Sacramento • Tysons Corner

A material weakness is a reportable condition in which the design or operation of one ormore of the internal control components does not reduce to a relatively low level the risk thatmisstatements caused by error or fraud in amounts that would be material in relation to thefinancial statements being audited may occur and not be detected within a timely period byemployees in the normal course of performing their assigned functions. Our consideration of theinternal control over financial reporting would not necessarily disclose all matters in the internalcontrol that might be reportable conditions and, accordingly, would not necessarily disclose allreportable conditions that are also considered material weaknesses. However, of the reportableconditions described above, we considered items 2005-1, 2005-2, and 2005-4 to be materialweaknesses. We also noted other matters involving the internal control over financial reporting,which we have reported to the management of the Housing Authority of New Orleans in aseparate letter dated September 21,2007.

Compliance and Other Matters

As stated in the second paragraph above, many of the documents required for our auditwere unavailable. Therefore, we were unable to perform all procedures we considerednecessary. However, we were able to perform some tests of the Housing Authority of NewOrleans' compliance with certain provisions of laws, regulations, contracts and grants,noncompliance with which could have a direct and material effect on the determination offinancial statement amounts. However, providing an opinion on compliance with thoseprovisions was not an objective of those procedures and, accordingly, we do not express such anopinion. The results of our tests disclosed an instance of noncompliance that is required to bereported under Government Auditing Standards, which is described in the accompanyingSchedule of Findings and Questioned Costs as item 2005-3.

This report is intended solely for the information and use of the Board of Commissioners,management and federal awarding agencies and pass-through entities and is not intended to beand should not be used by anyone other than these specified parties.

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE WITH REQUIREMENTSAPPLICABLE TO EACH MAJOR PROGRAM AND INTERNAL CONTROL OVER

COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133

To the Board of DirectorsThe Housing Authority of New Orleans

Compliance

We were engaged to audit the compliance of the Housing Authority of New Orleans(HANO) with the types of compliance requirements described in the U.S. Office of Managementand Budget (OMB) Circular A-133 Compliance Supplement that are applicable to each of itsmajor federal programs for the year ended September 30, 2005. The Housing Authority of NewOrleans' major federal programs are identified in the summary of auditors' results section of theaccompanying Schedule of Findings and Questioned Costs. Compliance with the requirementsof laws, regulations, contracts and grants applicable to each of its major federal programs is theresponsibility of the Housing Authority of New Orleans' management.

All of HANO's public housing tenant lease files and voucher client files were destroyedby Hurricane Katrina. The records that remain are not sufficient to permit the application ofauditing procedures that would be adequate for us to express an opinion about whethernoncompliance with the types of compliance requirements referred to above that could have adirect and material effect on a major federal program occurred.

In performing those procedures that we could, we found instances of non-compliancedescribed in items 2005-5 to 2005-7 in the accompanying Schedule of Findings and QuestionedCosts, where the Housing Authority of New Orleans did not comply with requirements regardingmajor federal programs as follows:

Major Federal Program Compliance RequirementLow-Rent Public Housing Reporting

EligibilityEquipment and Rental Property Management

Housing Choice Voucher Eligibility

-40-

Atlanta • Baltimore • Bethesda • Charlotte • Chicago • Los Angeles • Sacramento • Tysons Corner

Compliance with such requirements is necessary, in our opinion, for the HousingAuthority of New Orleans to comply with requirements applicable to those programs.

Since HANO was not able to provide evidence or corroborating evidence documentingits compliance with the requirements of its major federal programs and we were not able to applyother auditing procedures to satisfy ourselves as to whether HANO did in fact comply with therequirements of its major federal programs, the scope of our work was not sufficient to enable usto express, and we do not express, an opinion as to whether the Housing Authority of NewOrleans complied, in all material respects, with the requirements referred to above that areapplicable to each of its major federal programs for the year ended September 30, 2005.

Internal Control Over Compliance

The management of the Housing Authority of New Orleans is responsible forestablishing and maintaining effective internal control over compliance with requirements oflaws, regulations, contracts and grants applicable to federal programs. In performing thoseprocedures that we could, we considered the Housing Authority of New Orleans' internal controlover compliance with requirements that could have a direct and material effect on a majorfederal program in order to determine our auditing procedures for the purpose of expressing ouropinion on compliance and to test and report on internal control over compliance in accordancewith OMB Circular A-133.

We noted certain matters involving the internal control over compliance and its operationthat we consider to be reportable conditions. Reportable conditions involve matters coming toour attention relating to significant deficiencies in the design or operation of the internal controlover compliance that, in our judgment, could adversely affect the Housing Authority of NewOrleans's ability to administer a major federal program in accordance with the applicablerequirements of laws, regulations, contracts, and grants. Reportable conditions are described inthe accompanying schedule of findings and questioned costs as items 2005-5 to 2005-7.

A material weakness is a reportable condition in which the design or operation of one ormore of the internal control components does not reduce to a relatively low level the risk thatnoncompliance with the applicable requirements of laws, regulations, contracts, and grantscaused by error or fraud that would be material in relation to a major federal program beingaudited may occur and not be detected within a timely period by employees in the normal courseof performing their assigned functions. Our consideration of the internal control over compliancewould not necessarily disclose all matters in the internal control that might be reportableconditions, and accordingly, would not necessarily disclose all reportable conditions that are alsoconsidered to be material weaknesses. However, of the reportable conditions described above,we consider items 2005-5 to 2005-7 to be material weaknesses.

-41-

ReznickGroup

This report is intended solely for the information and use of the Board of Commissioners,management and federal awarding agencies and pass-through entities and is not intended to beand should not be used by anyone other than these specified parties.

Charlotte, North CarolinaSeptember 21,2007

-42-

Housing Authority of New Orleans

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

Year ended September 30,2005

Summary of Auditors' Results

1. The auditors' report expresses a qualified opinion on the statement of net assets anddisclaims an opinion on the related statements of revenue, expenses and changes in netassets, and cash flows

2. Reportable conditions and material weaknesses were identified during the audit of thebasic financial statements.

3. An instance of noncompliance material to the basic financial statements of the HousingAuthority of New Orleans was disclosed during the audit.

4. Reportable conditions and material weaknesses were identified during the audit of themajor federal award programs.

5. The auditors' report on compliance for the major federal award programs for the HousingAuthority of New disclaims an opinion.

6. Audit findings relative to the major federal award programs for the Housing Authority ofNew Orleans are reported in this schedule.

7. The programs tested as major programs include:• CFDA #14.850 Low-Rent Public Housing• CFDA #14.866 HOPE VI - Urban Revitalization Program• CFDA #14.872 Capital Fund Program• CFDA #14.871 HCVP-Voucher

8. The threshold for distinguishing Type A and B programs was $3,000,000.

9. The Housing Authority of New Orleans did not quality as a low-risk auditee.

-43-

Housing Authority of New Orleans

SCHEDULE OF FINDINGS AND QUESTIONED COSTS - CONTINUED

Year ended September 30, 2005

Findings - Financial Statements Audit

2005 - 1 Cash Disbursement ProceduresType of finding: Internal control - reportable condition

Condition: Signed checks are in the custody of the individual that prepares manual checks.They should be handled by someone independent of all payable, disbursing, cash receivingand general ledger functions. This matter relates to finding 2004-1 and 2003-1, whichremain unresolved as of year-end.

Cause: The Authority's current policies allow for the same person preparing manual checksto check signed checks.

Criteria: In order to have safeguards over cash and prevent potential theft of federal fundsthere should be a segregation of duties that keeps the person preparing manual checks andthe person who keeps the signed checks separate.

Auditors' Recommendation: We recommend that after checks are signed, they be given to anindividual to mail that is independent of all payable, disbursing, cash receiving and generalledger functions.

Management's Response: