Housing Finance in Emerging Markets Washington DC – 16 March 2006 “Internationalisation of Covered bonds” Cristina Costa Senior Adviser - ECBC European Mortgage Federation. European Mortgage Federation. - PowerPoint PPT Presentation

19

1 Housing Finance in Emerging Housing Finance in Emerging Markets Markets Washington DC – 16 March 2006 Washington DC – 16 March 2006 “ “ Internationalisation of Internationalisation of Covered bonds” Covered bonds” Cristina Costa Cristina Costa Senior Adviser - ECBC Senior Adviser - ECBC European Mortgage Federation European Mortgage Federation

Transcript

1

Housing Finance in Emerging Housing Finance in Emerging MarketsMarkets

Washington DC – 16 March 2006Washington DC – 16 March 2006

European Mortgage FederationEuropean Mortgage Federation

2

European Mortgage European Mortgage FederationFederation

Founded in 1967 to represent mortgage lenders’ interests at EU level (retail & funding)

Groups national trade associations and credit institutions from EU Member States + acceding countries

New Member State membership: Czech Rep., Hungary, Latvia and Poland

Accession Country Membership: Romania

Just welcomed Ukraine as its latest member

Represents approx.75% of EU mortgage market

EU mortgage market amounts to approx. 49% of EU GDP

3

I.I. Mortgage Market TrendsMortgage Market Trends

II.II. Covered Bonds: an attractive Covered Bonds: an attractive funding sourcefunding source

III.III. Expansion of covered bondsExpansion of covered bonds

IV.IV. The Spanish ExperienceThe Spanish Experience

V.V. Case Study : HungaryCase Study : Hungary

VI.VI. OutlookOutlook

AgendaAgenda

4

EU Mortgage Market TrendsEU Mortgage Market Trends

Mortgages Outstanding: Total value of outstanding residential mortgage loans EUR 5.2 trillion at end 2005 (c. 49% of GDP)

Growth: Average annual growth rate approx. 8% per year over the last 10 years. Growth is much higher in the New MS

Interest Rates: The introduction of the Euro has resulted in significant falls in mortgage interest rates, which in turn has stimulated the markets

House prices: Big price increases in most countries over past few years, but there are signs of house price growth slowing down around Europe

Regulation: Capital adequacy and European retail FS integration dominate the regulatory agenda

Funding: Diversified access to capital market funding is increasingly important; EMF launches ECBC to represent covered bonds

5

Mortgage Funding in EuropeMortgage Funding in Europe

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Denmark

Hungary

Sweden

Czech Republic

Spain

Germany

France

Austria

Latvia

I reland

Poland

UKEU:17%

Covered bonds outstanding as % of mortgage debt outstanding (2004)

Source: European Mortgage Federation

6

Special character of covered bondsSpecial character of covered bonds

Covered Bonds

Specific legal framework/Contractual

provision

Strict supervision

High quality collateral

Quasi-bankruptcy remoteness

Preferential right of bondholders

Separated collateral pools

Source: ABN Amro

7

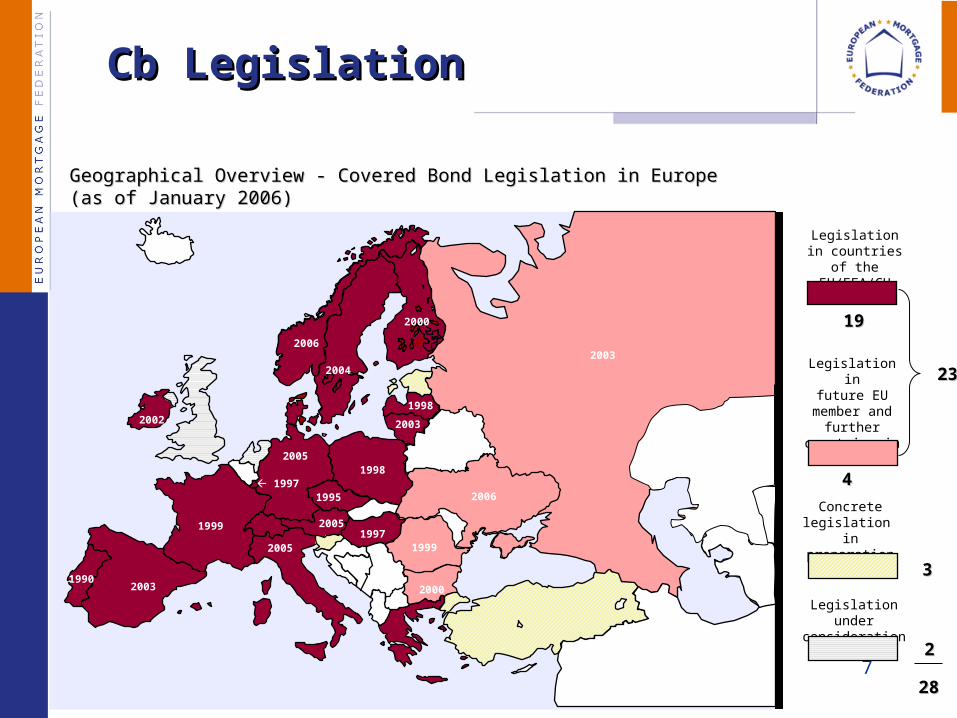

Cb LegislationCb Legislation

Geographical Overview - Covered Bond Legislation in EuropeGeographical Overview - Covered Bond Legislation in Europe(as of January 2006)(as of January 2006)

Legislation in countries of the

EU/EEA/CH

Legislation infuture EU

member and further

countries in transition

Concrete legislation

in preparation

Legislation under

consideration

33

22

2233

2288

1998

1997

1995

1998

1997

1999

2000

2000

2002

1999

2006

2004

19902003

2003

2003

1919

44

2005

2005

2005

2006

8

Covered BondsCovered Bonds

Most European countries have adopted cb legislation

Competition has driven legislation to ever higher (safety) standards without sacrificing funding flexibility

No trend towards lowest common denominator

Regulated at EU level (Art. 22(4) of UCITS):

Issued by a credit institution

Subject to special supervision

Investment of proceeds effected in eligible assets

Outstanding issues covered by eligible assets until maturity

Priority claim of bondholders on subset of assets Recently adopted CRD lists set of eligible assets

9

CB: an attractive funding sourceCB: an attractive funding source For issuersFor issuers

• Low funding costs• Flexible alternative to deposits and senior bonds• Possibility of extending the maturity profile of banks’

liability side to make it match with mortgage loans loan maturity

For investorsFor investors• Alternative to Government bonds (yield pick-up)• Secure instrument in case of issuer insolvency -

double protection (claim against issuer & cover pool) • Higher liquidity due to large issue sizes and market

maker commitments• Geographic and asset class diversification

10

Record supply in European jumbo Record supply in European jumbo covered bondscovered bonds

Source: HVB

Prior to 1976 (pre Franco), parallels with Eastern Europe Laws date back to 1872 which saw first law allowing

‘Cédulas hipotecarias’. Mortgage Law 1946 (legal & operational security) Moncloa Pact 1977 (removal of obstacles) 1982 Mortgage Market Law

Securitisation law introduced in 1991

Spanish Economy:

Steady fall in unemployment from 26% to around 10%

Falling interest rates (Eurozone membership)

Cut National debt; Big increase in per capita income

Result - Housing, construction and Mortgage Markets booming

The Spanish ExperienceThe Spanish Experience

Covered Bonds in SpainCovered Bonds in Spain

Almost 1/5 of mortgages funded by Cédulas, and 1/3 of new lending

In 2005, issuance highest in Europe surpassing that of Jumbo Pfandbriefe

Issuance open to all types of institutions (multi-sellers, direct)

80% LTV limit on residential or 70% for commercial property

Strengthening status & demand of cédulas through:

2004 Insolvency Act

2005 Modification to Withholding tax regime

Expected Jumbo issuance for 2006 is approximately EUR 58 Billion.

Lessons to be learnt from SpainLessons to be learnt from Spain

Spanish Experience Highest home ownership rate in Western World Lowest State Housing in Western World Thriving covered bond market and securitisation

market One of Europe’s fastest growing mortgage markets

Achieved by… Diversified Funding Strategy Building programme to ensure supply of quality housing Macro-economic reform Solid primary market laws to ensure safety of collateral Minimising State involvement

15

Housing & Mortgage Markets Housing & Mortgage Markets in in Hungary vs. EU 25 and CEECs-2004Hungary vs. EU 25 and CEECs-2004

EU 25 CEECs Hungary

Total value of residential loans, € million, (EU 25)

Growth rates of residential mortgage market 9.7% 34.4% 35.0%

Home ownership 63.5%Above 80% in manyCEECs 92.0%

Outstanding covered bonds as % of residential mortgage lending outstanding

17.0% N/A 63%

Source: European Mortgage Federation, Hypostat 2004

16

Regulatory Environment:

• Legal framework – Mortgage Banking Act (1997)

• State subsidy scheme (introduced 2001)

Well developed system of refinancing partner banks through purchasing mortgages

3 covered bond issuers - FHB, HVB, OTP

CB fastest growing market (6% of GDP) - total outstanding volume EUR4.9bn (EMTN Programme)

Since 2004: market based development

• High HUF interest rates have turned clients towards FX-based products

• Current monthly net growth (30-35 billion HUF) seems to be sustainable

Case Study: HungaryCase Study: Hungary

17

Size of the domestic market

• Crowding-out effect of Govies (growing budget deficit)

Liquidity concerns• Primary issues are relatively small (c. EUR50m)

• Secondary turnover is moderate

Less supportive macro environment• Volatile interest rates and FX market

Growing role of foreign EUR issuances but majority of outstanding cb volume were domestic issues and HUF denomination

Cut in subsidy scheme and growing FX lending decreased the incentive of cb funding for non mortgage bank lenders

Hungary: ChallengesHungary: Challenges

18

European Mortgage Markets show no signs of slowing, especially in new member states

Continued Growth of covered bonds

Emergence of new issuers: IT, PT, NL, UK….

FSA to implement EU compliant cb regime; NL next.

Increased level of investor interest (CEE, Asia)

Continued work of ECBC• Work on definition of common standards for covered bonds

European Commission working on European standard – funding likely to be one of the driving forces behind integration• Launch of Expert Group on Funding