NATIONAL COUNCIL OF APPLIED ECONOMIC RESEARCH How Households Save and Invest: Evidence from NCAER Household Survey Sponsored by Securities and Exchange Board of India (SEBI) July 2011 Main Report

Transcript

NATIONAL COUNCIL OF APPLIED ECONOMIC RESEARCH

How Households Save and Invest:Evidence from NCAER Household Survey

Sponsored by

Securities and Exchange Board of India(SEBI)

July 2011

Main Report

How Households Save and Invest:Evidence from NCAER Household Survey

Sponsored by

Securities and Exchange Board of India (SEBI)

July 2011

National Council of Applied Economic Research

MAIN REPORT

ii

iii

Report Prepared by

Hari K. Nagarajan (Project Advisor)

D.V. Sethi (Consultant)

Kailash C. Pradhan

Shrabani Mukherjee

Sudhir K. Singh

Survey

D.V. Sethi

J.P. Singh

Assistance1

Angelica Bharthi

Upasana Sharma

K.S. Urs

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

Study Team

1. Mr Anuj Sharma and Mr Rajender Singh provided assistance in certain stages of the survey.

All rights reserved, no part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any formor by any means, electronic, mechanical, photocopying, recording and/or otherwise, without the prior written permission ofthe publisher.

July 2011

Published byJatinder S. BediSecretary

National Council of Applied Economic ResearchParisila Bhawan11, Indraprastha EstateNew Delhi 110 002T +91 11 23379861-3F +91 11 23370164E [email protected] www.ncaer.org

Designed and printed atCirrus Graphics Pvt. Ltd.B-62/14, Phase II, Naraina Industrial Area, New Delhi 110 028T +91 9811026274

The global economy is on a recoverypath after the shocks of the severefinancial and economic crises of

2008 and 2009. The Indian financial sectorwas able to withstand the global shocksduring this period and emerge stronger.The foreign capital inflows have resumedand the capital markets have regained thedynamism. The experience has shown thatthe need for greater understanding andcareful monitoring of the financial sector isessential for designing policies for sustain-ing high rate of economic growth with sta-bility.

This study, third in this area supportedby Securities and Exchange Board of India(SEBI), has focused on understanding thebehaviour of households as investors invarious financial instruments which aretraded in markets regulated by SEBI. As in-vestors, the households evaluate a varietyof options available to them includingthose traded in formal markets under regu-lation. To this extent, the study has lookedat a range of financial saving instruments.

In this study, we have used a sample ofabout 38,000 households in 44 cities and40 villages across the states. It is estimatedthat there are 24.5 million investors in In-dia. The study points to the relatively lowrates of participation by the households inthe securities market, though there hasbeen growth in the investor populationover the past 10 years since the last surveycarried out by NCAER. Fifty four per centof all households treat commercial banksand insurance schemes as their primarychoice for savings at all India level. Thedegree of risk aversion is extremely high inIndian households. Households engagingin more risky instruments are only at themargin. Education plays a significant rolein influencing risk preferences. The degreeof risk was the highest among investorswith more than 15 years of schooling. Vil-lages that are close to urban centres signif-icantly participate in financial marketsparticularly in the mutual funds. Othercharacteristics of rural households, likemarital status and gender, do not signifi-cantly alter the distribution of investment.

I would like to place on record mydeep appreciation for the confidenceplaced in NCAER by Shri C.B. Bhave, for-mer Chairman, SEBI and Shri U.K. Sinha,present Chairman, SEBI for entrusting uswith this study. Shri Nagender Parakh,Chief General Manager and Dr Sarat Malik,Joint Director, SEBI participated in allstages of this study as partners. Theirknowledge of the securities market hasbeen invaluable in putting together this fi-nal report. A special word of thanks is alsodue to Shri Prashant Saran, Whole TimeMember of SEBI, for his valuable adviceand guidance. Dr Hari K. Nagarajan, SeniorFellow, directed the project at NCAER andShri D.V. Sethi provided constant supportas a Consultant throughout the study.

Thousands of households participatedin the sample survey and I am deeply in-debted to their voluntary engagement inthe data collection process. Without theircooperation, the survey would not havebeen possible.

I hope that the study will be found use-

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

Preface

Shekhar Shah

Director-GeneralNCAER

xii

ful in making the capital markets withinthe reach of millions of households who

will look for good and safe returns from thefinancial markets.

xiii

The third NCAER survey of house-holds in urban and rural India to ex-amine in detail the various aspects

of income, expenditure, savings, and in-vestments was recently completed. Inmany respects this survey differed from itspredecessors at NCAER in both its depthand diversity of information that was col-lected from households. Three points areworth noting: a) a comprehensive profile ofrisk taking ability of households as well asindividual earners, savers, and investorswas constructed, b) the expected and theextant role of the regulator, viz. SEBI wasarticulated from the point of view of thevarious constituents of the households,and c) an attempt was made to link the in-come profile with market participation,role of the regulator, information, and riskprofile.

The broad objectives of this surveywere: (1) to prepare a comprehensive pro-file of savings and investment behaviour inthe context of income and consumptionpatterns,(2 ) to create a profile of investors'preferences for various market instru-

ments like IPOs, securities and mutualfunds and its significance in the growth inprimary and secondary security markets.The study examines attitudes towards different types of savings and investmentalternatives, (3) to obtain the risk profile ofthe households and relate this to savingsand investment behaviour and (4) to understand the impact of rules and regulations framed by the Securities and Exchange Board of India (SEBI) on households’ choice of investment patterns.

The survey comprised of two parts.First a comprehensive listing of house-holds in various cities and villages was un-dertaken. The listing was done to selectsample of pure savers, investors, non-in-vestors, and non-savers. This exercise in-cluded identifying the distribution of fi-nancial market and non-financial instru-ments preferred by households to "park"part of their disposable income. The urbansample was selected through a three stageprocess where the cities and towns except-ing Mumbai, New Delhi, Kolkata, Hyder-

abad, Chennai, and Bangalore were select-ed randomly. From within the cities andtowns the urban blocks were next identi-fied and selected. Villages were selectedusing the following criteria: Twenty vil-lages within a close proximity (less than 20kilometres from urban centres) were se-lected for the sample. A second group oftwenty villages that were considered re-mote (more than 20 kilometres) from ur-ban centres were selected next. 70, 159households each were listed in the variousurban blocks and villages respectively.

The total sample was made up of38,412 households selected from 44 citiesand 40 villages. A detailed questionnairewas then administered to the selectedhouseholds. The process of listing was alsodone in villages. However, after repeatedlisting in more than 50 villages across thecountry, it was found that the extent of par-ticipation in financial markets was ex-tremely low. Hence it was decided to pres-ent the findings of investments and savingsseparately for rural households based on acarefully selected sample of 40 villages.

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

Executive Summary

The broad findings are as follows:

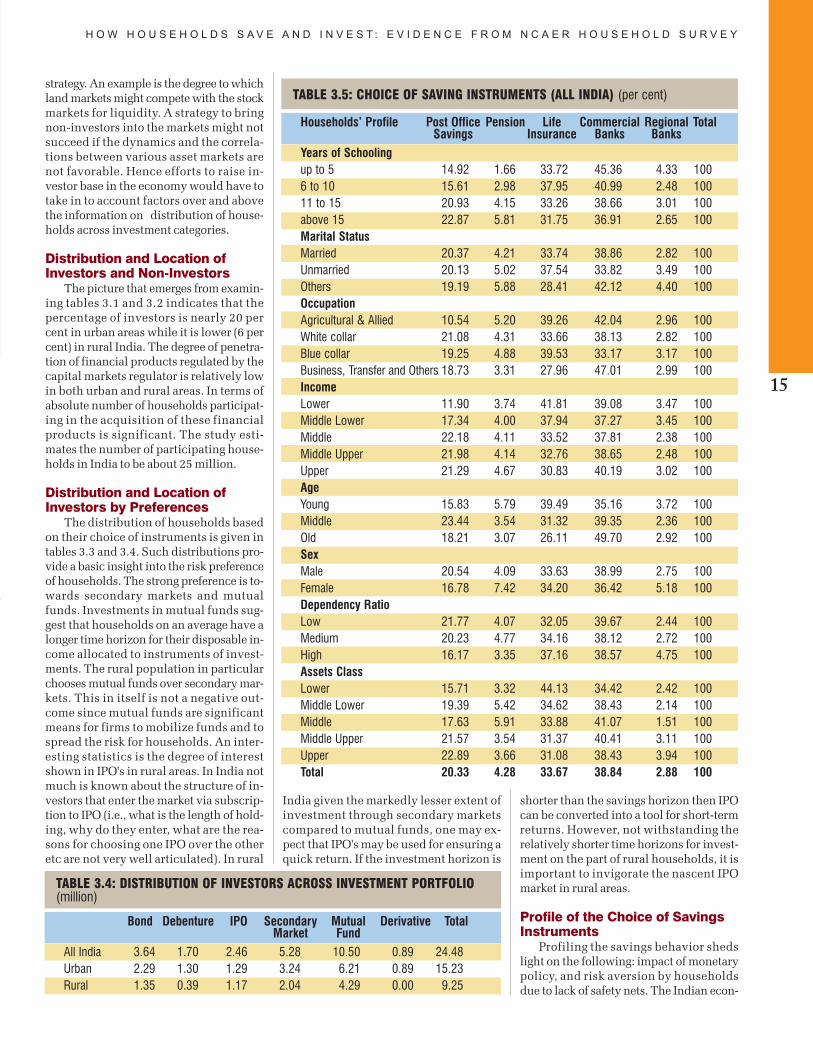

National Level The percentage of investors is nearly

20 in urban areas while it is much low-er (6 per cent) in rural India.

The estimated number of investorhouseholds in India is 24.5 millionwho constitute about 11 per cent of to-tal households.

The strong preference of investors is to-wards mutual funds (43 per cent) andsecondary markets (22 per cent). In ur-ban areas, 41 per cent of investors in-vest in mutual funds and 21 per centsecondary markets, whereas, 46 percent rural population chooses mutualfunds and 22 per cent secondary mar-kets.

There is a significant magnitude ofsmall savers among all households.Eleven to 25 per cent of all householdssave in post office savings schemes.

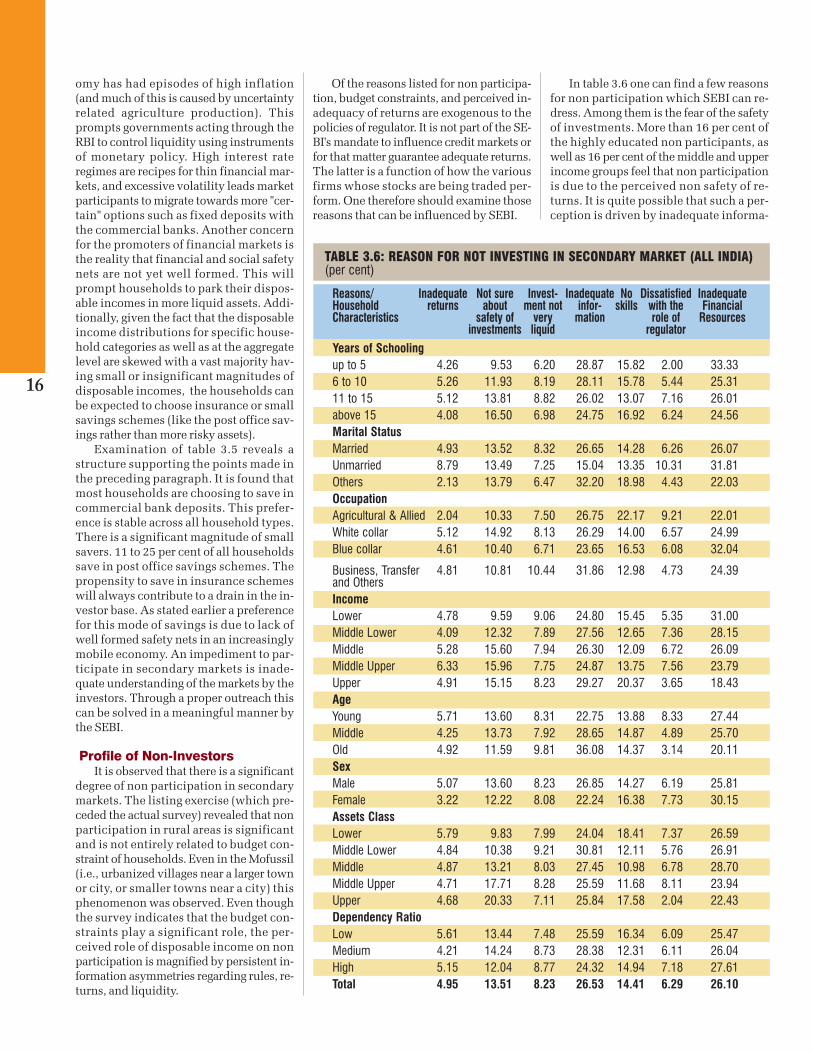

More that 16 per cent of the highly ed-ucated non-participants, as well as 16per cent of the middle and upper in-come groups feel that non-participa-tion is due to the perceived non-safetyof returns.

The survey reveals that a large propor-tion of non-participants is satisfiedwith the role of the regulator SEBI, inregulating markets. Only between 2 to10 per cent of the non-participantsacross selected household groups indi-cate dis-satisfaction with the role of themarket regulator.

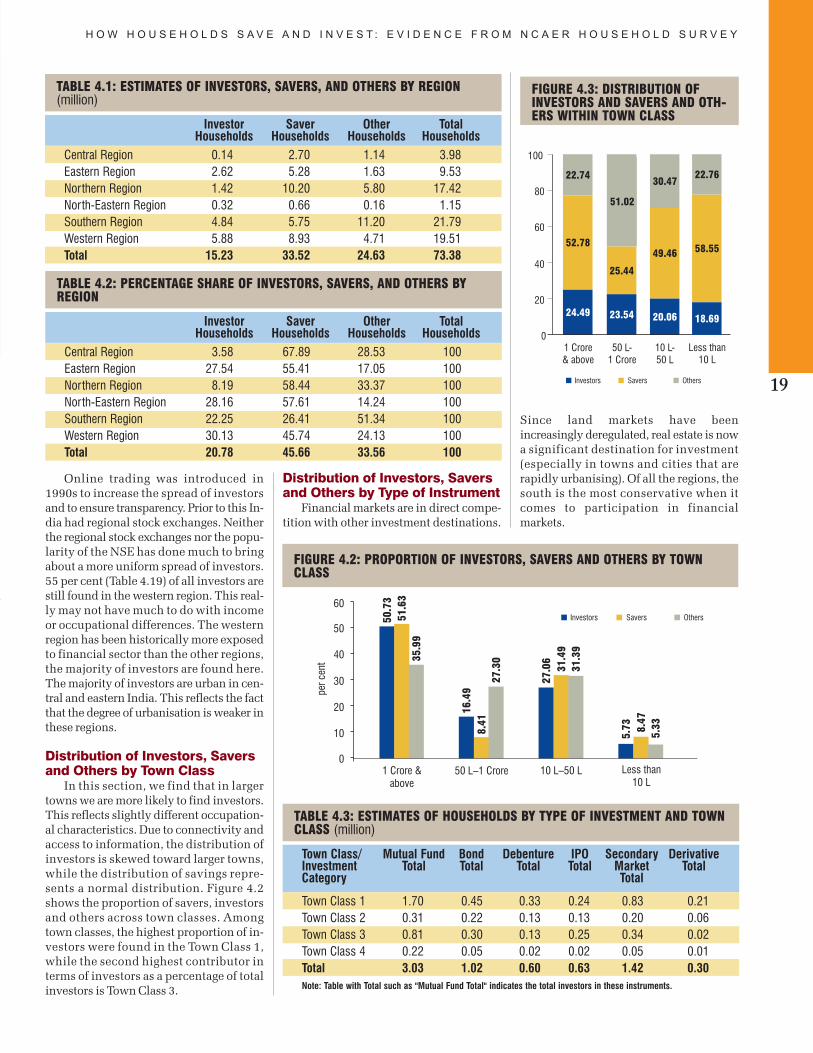

Urban India In the present study the estimated

number of urban investor householdsis 15.23 million which constitute 21per cent of all urban households. Theestimated saver households and otherhouseholds are 34 million (46 per cent)and 25 million (33 per cent), respec-tively.

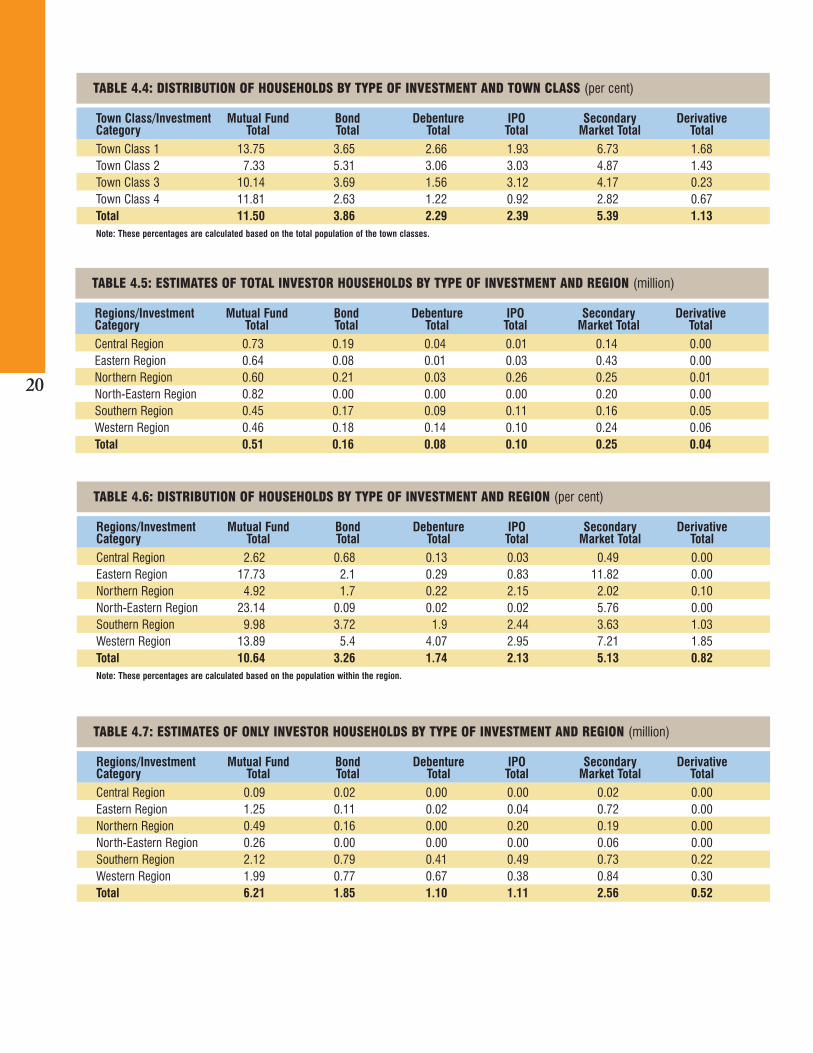

A majority of households do not partic-ipate in financial markets. The distri-bution of participation is not spatiallyeven. For instance, 55 per cent of all in-vestors are found in the western region.

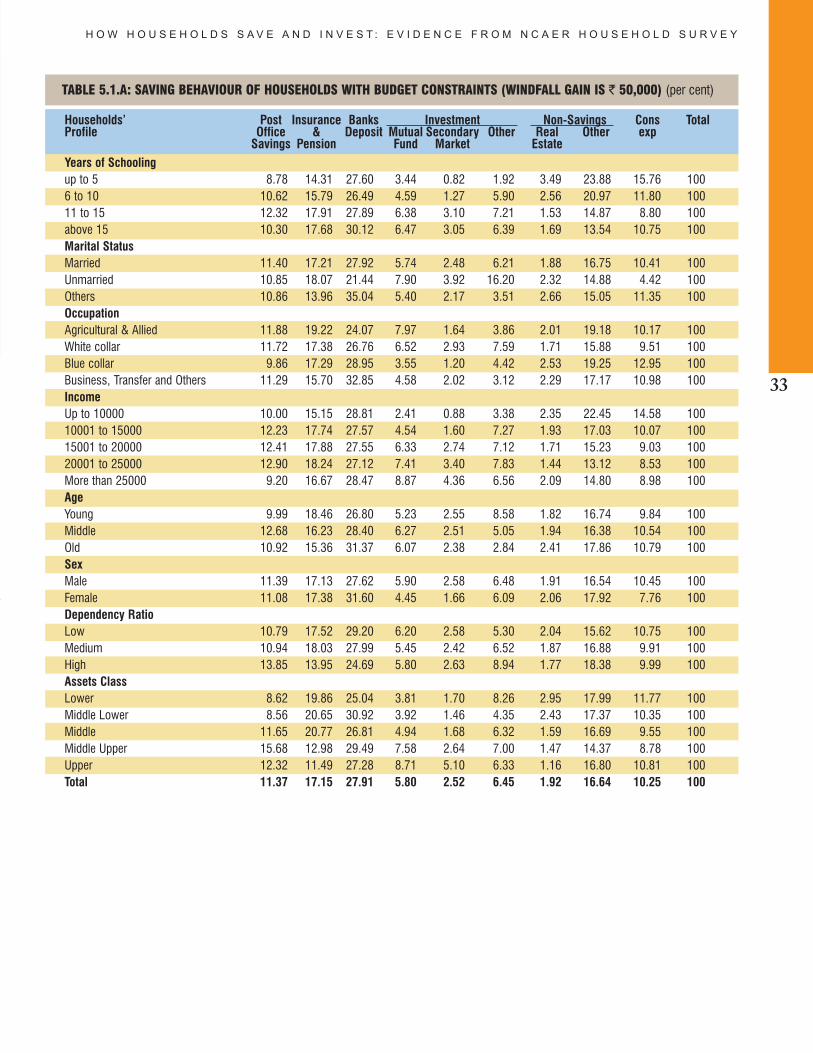

Relaxation of budget constraints doesnot lead to households taking higherlevels of risks. The allocations are stillin avenues such as commercial bankdeposits and real estate.

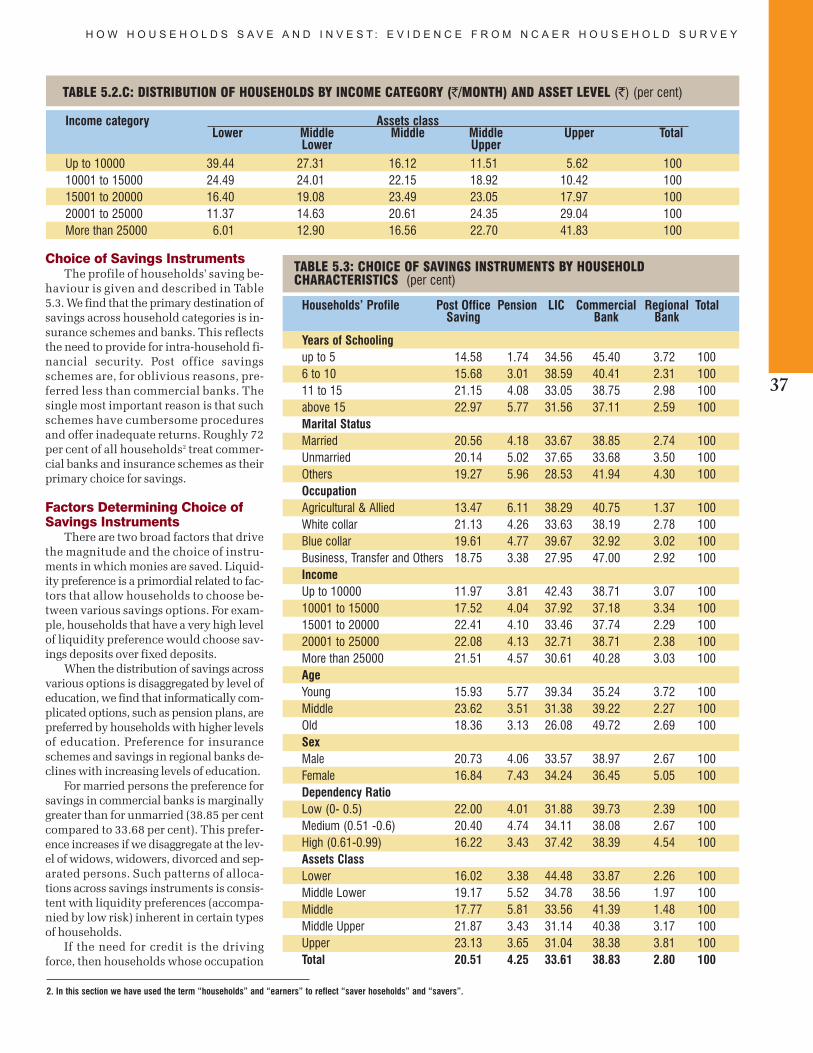

The primary destination of savingsacross household categories is insur-ance schemes and banks.

Post office savings schemes are, for ob-vious reasons, less preferred comparedto commercial bank deposits and ac-

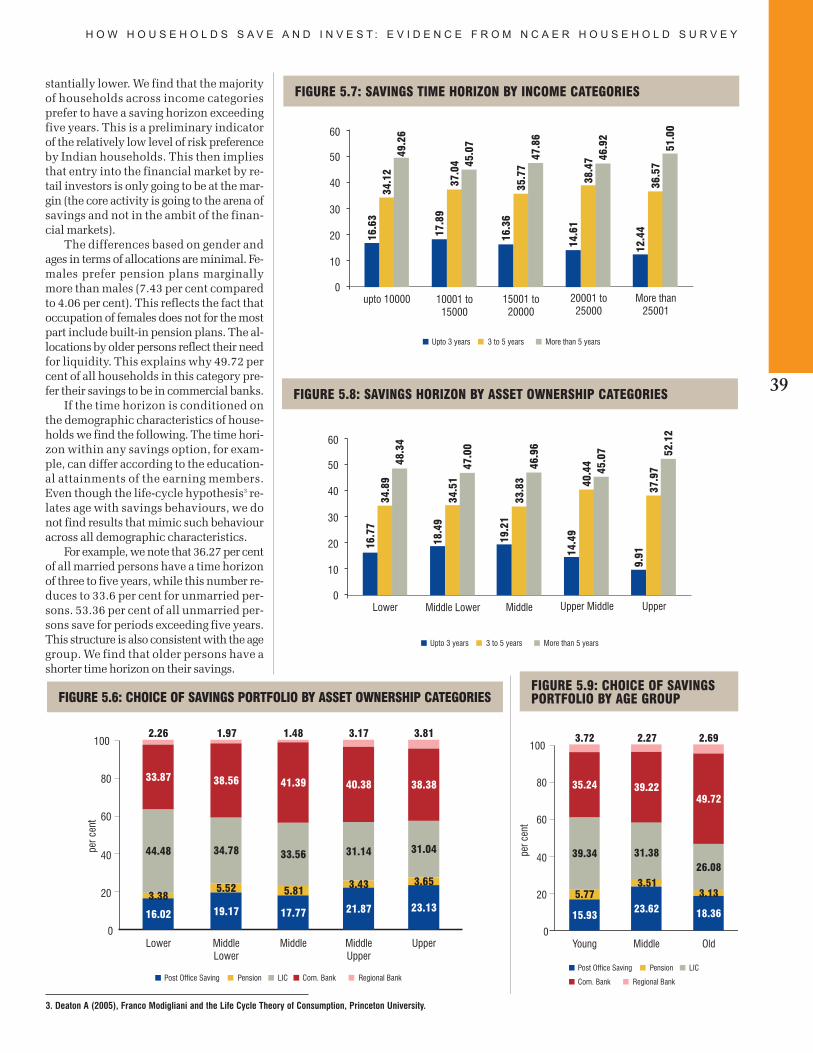

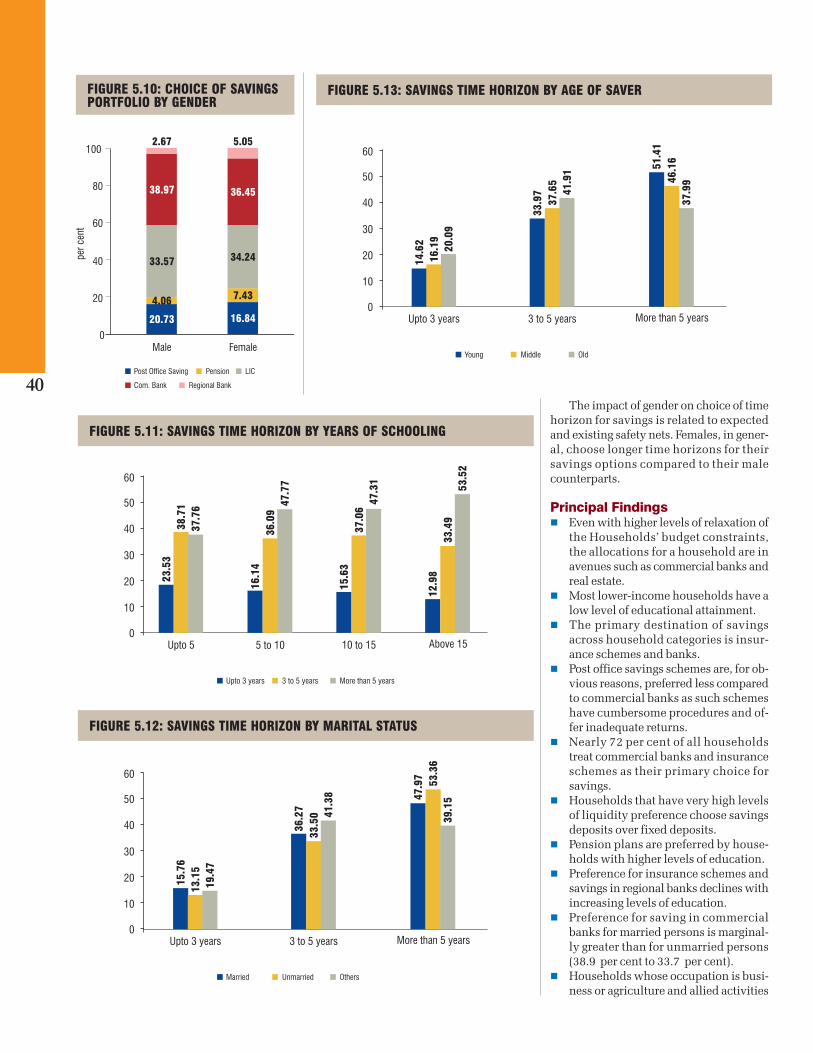

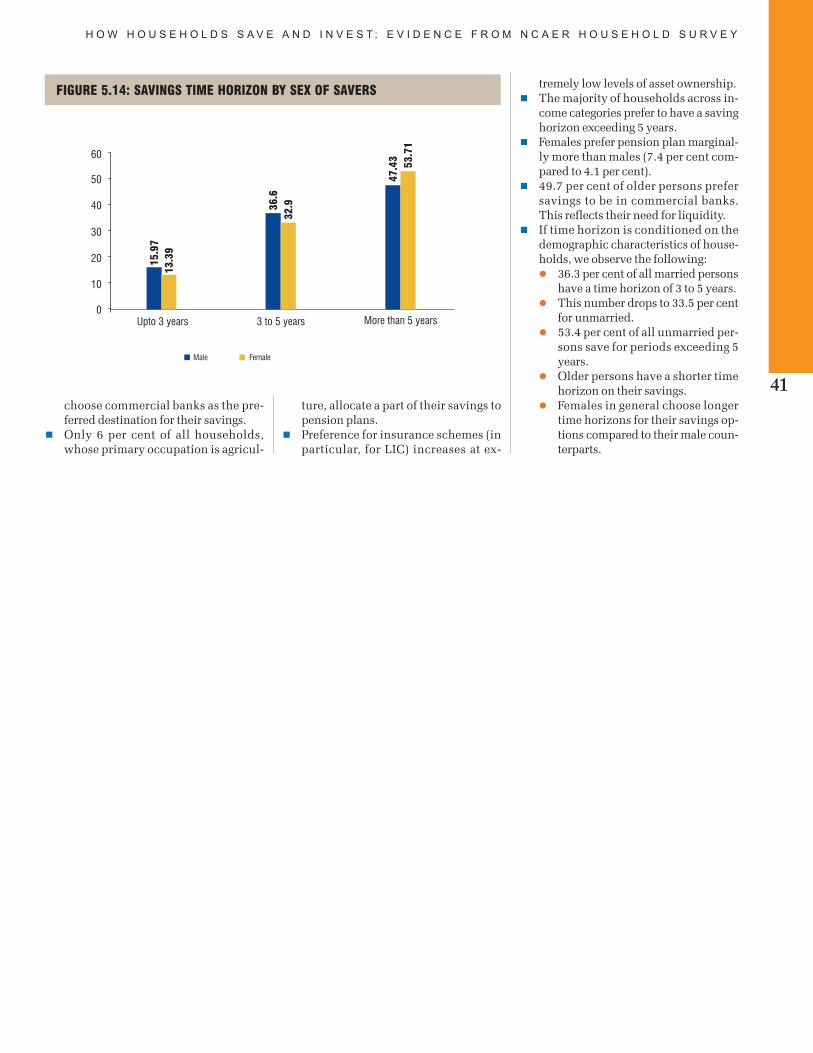

counts as such schemes have cumber-some procedures and offer inadequatereturns. Nearly 72 per cent of all house-holds treat commercial banks and in-surance schemes as their primarychoice for savings. Households thathave very high levels of liquidity pref-erence choose savings deposits overfixed deposits. Pension plans are pre-ferred by households with higher lev-els of education. Preference for insur-ance schemes and savings in regionalbanks decline with increasing levels ofeducation. Preference for saving incommercial banks for married house-holds is marginally greater than for un-married households (38.9 per cent to33.7 per cent). Households whose oc-cupation is business or agriculture andallied activities choose commercialbanks as the preferred destination fortheir savings. Only 6 per cent of allhouseholds, whose primary occupa-tion is agriculture, allocate a part oftheir savings to pension plans. Prefer-ence for insurance schemes (in partic-ular, for LIC) increases at extremelylow levels of asset ownership. The ma-jority of households across income cat-egories prefer to have a saving horizonexceeding 5 years. Females prefer pen-sion plan marginally more than males(7.4 per cent compared to 4.1) and 49.7per cent of older persons prefer savingsin commercial banks. This reflectstheir need for liquidity. If time horizonis conditioned on the demographiccharacteristics of households, we ob-serve the following: a) 36.3 per cent ofall married persons have a time hori-zon of 3 to 5 years. b) This numberdrops to 33.5 per cent for unmarriedpersons. c) 55.4 per cent of all unmar-ried persons save for periods exceeding5 years. d) Older persons have a short-er time horizon on their savings. e) Fe-males in general choose longer timehorizons for their savings options com-pared to their male counterparts.

Household income is a relatively minordeterminant of participation in finan-cial market. Instead, factors such as ed-ucation, information, as well as qualityinformation influence the magnitudeand extent of participation to a greaterextent.

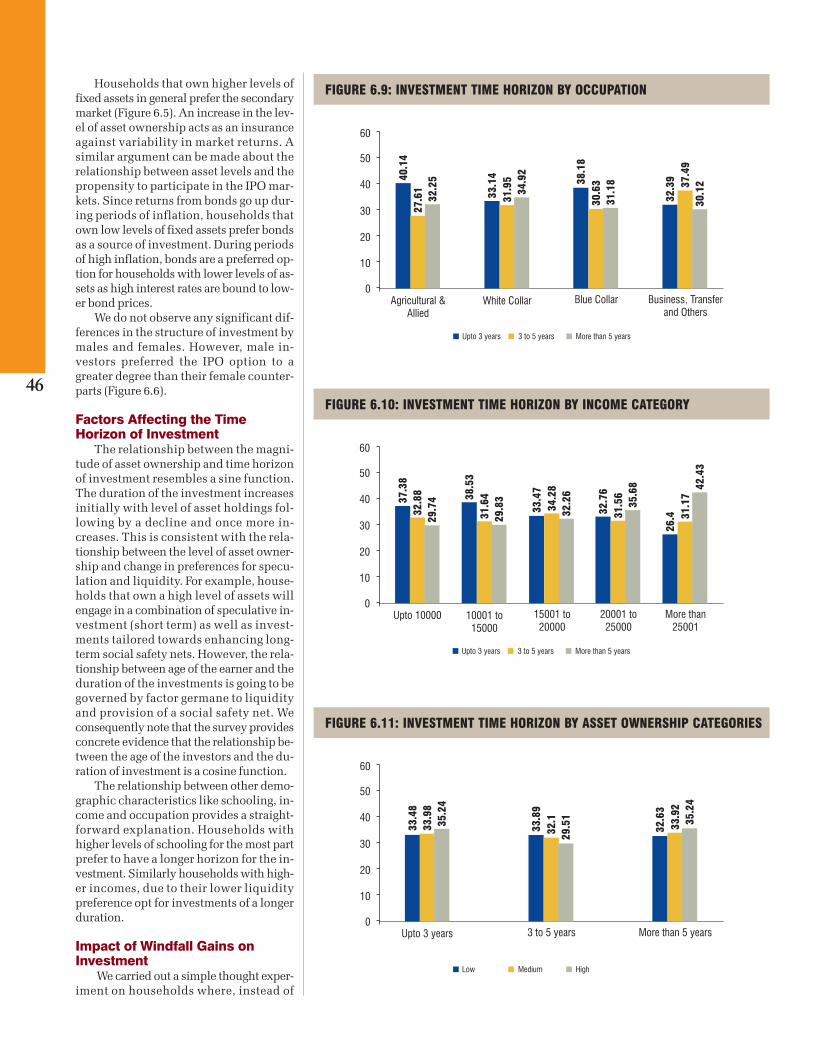

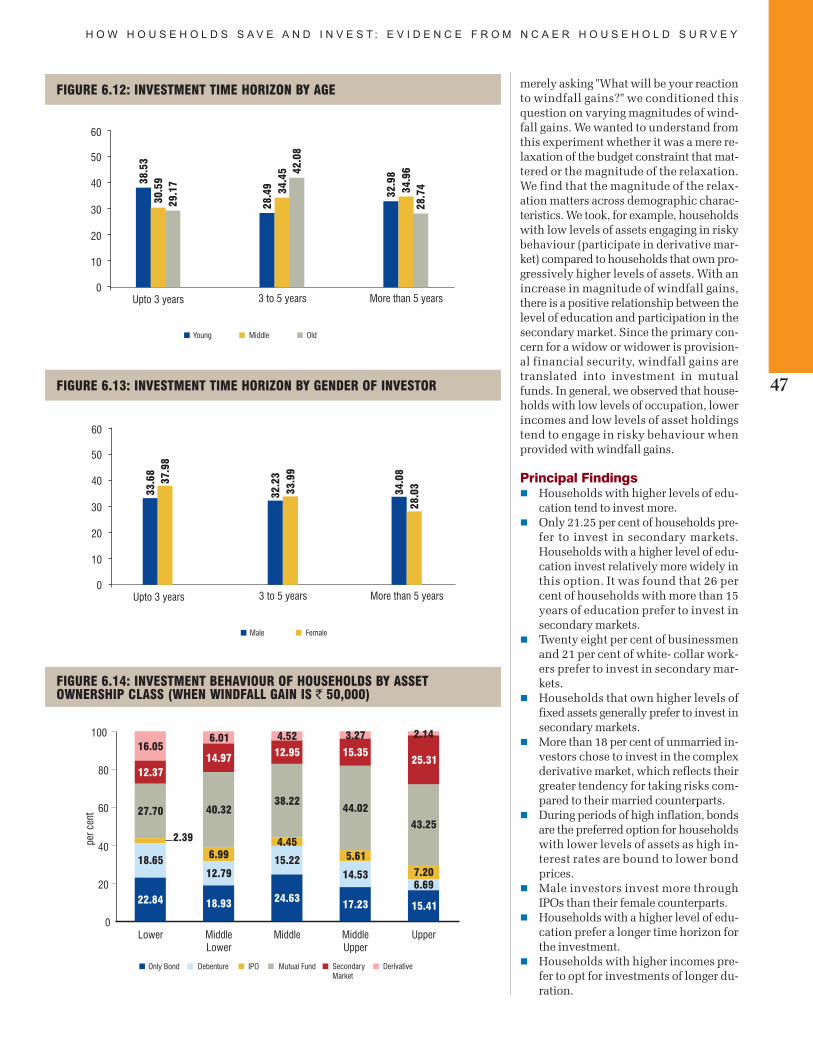

Only 21.25 per cent households preferto invest in secondary markets. House-holds with a higher level of educationinvest more in this option. It was foundthat 26 per cent households with morethan 15 years of education prefer to in-vest in secondary markets. Twenty

eight per cent of businessmen and 21per cent of white-collar workers preferto invest in this option. Householdsthat own higher levels of fixed assetsgenerally prefer to invest in secondarymarkets. More than 18 per cent of un-married households chose to invest inthe complex derivative market, whichreflects their greater tendency for tak-ing risks compared to their marriedcounterparts. During periods of highinflation, bonds are the preferred op-tion for households with lower levelsof assets as high interest rates arebound to lower bond prices. Male in-vestors invest more through IPOs thantheir female counterparts. Householdswith a higher level of education prefera longer time horizon for the invest-ment. Households with higher in-comes opt for investments of longerduration.

In case of windfall gains, householdswith low level of assets engaged inrisky behaviour (participated in the de-rivative market) compared to house-holds that own progressively higherlevel of assets. If windfall gains are in-creased in magnitude, there continuesto be a positive relationship betweenlevels of education and participation inthe secondary markets.

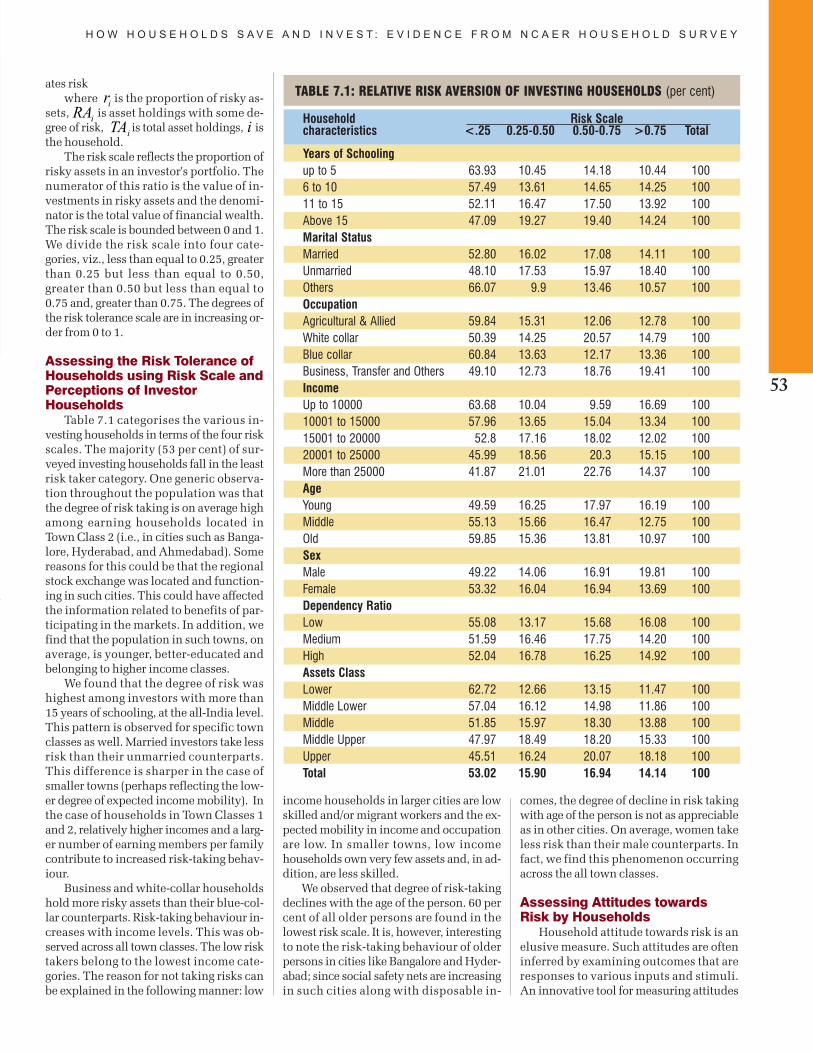

The degree of risk aversion is extreme-ly high in Indian households. It is onlyat the margin that households engagein risky ventures. We note that risk tak-ing increases only at very high incomelevels or if there is a significantly largewindfall gain.

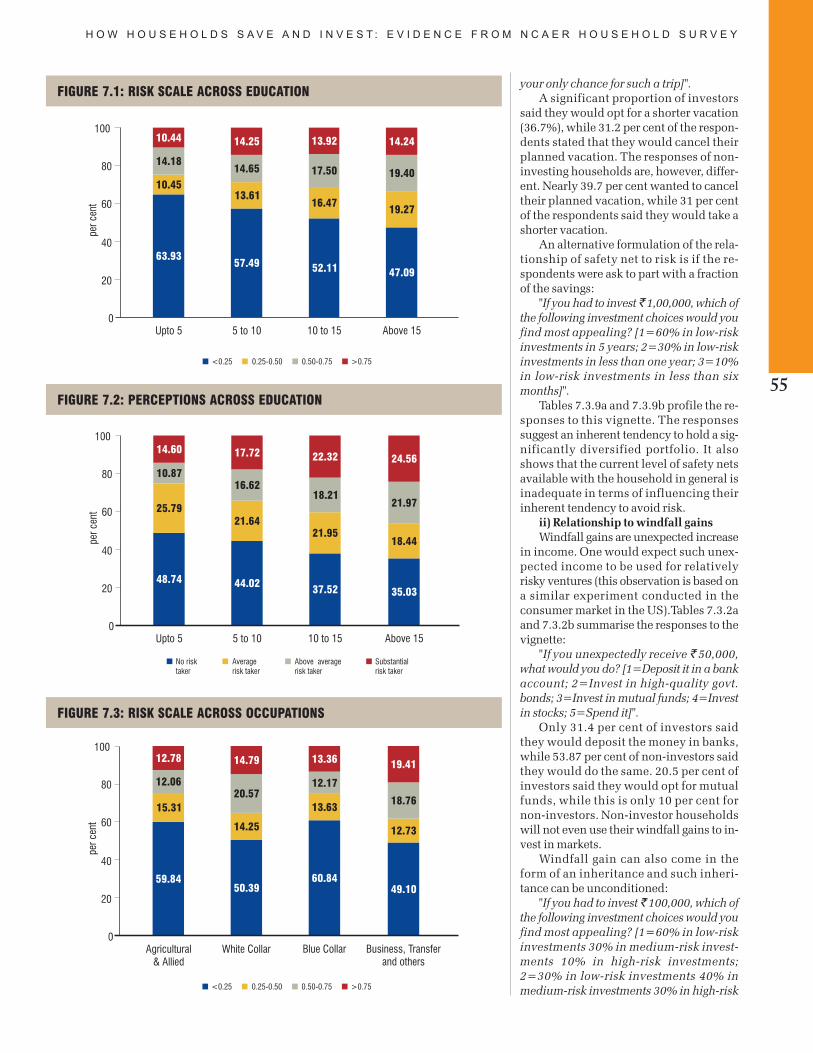

The majority (53 per cent) of surveyedinvesting households fall in the leastrisk taker category. The degree of risk-taking is, on average, high among earn-ing households located in cities such asBangalore, Hyderabad and Ahmed-abad (Town Class 2, where the popula-tion is between 50 lakh — 1 crore). Ed-ucation plays a significant role in risk-taking activity. The degree of risk wasthe highest among investors with morethan 15 years of schooling at the all-In-dia level. With the increase in educa-tional attainment, risk tolerance in-creases. Married investors take less riskaverse than their unmarried counter-parts. On average females take less riskthan their male counterparts. Businessand white-collar workers hold morerisky assets than their blue-collar coun-terparts. The degree of risk-taking is in-versely proportional to age; risk-takingdeclines with the age of the persons.And we find that nearly 60 per cent of

xiv

older persons fall in the lowest riskscale.

Quality and source of information sig-nificantly influence the extent of par-ticipation in financial markets. Oursurvey indicated that there is much tobe done to provide the current and po-tential participants with optimal levelsof information.

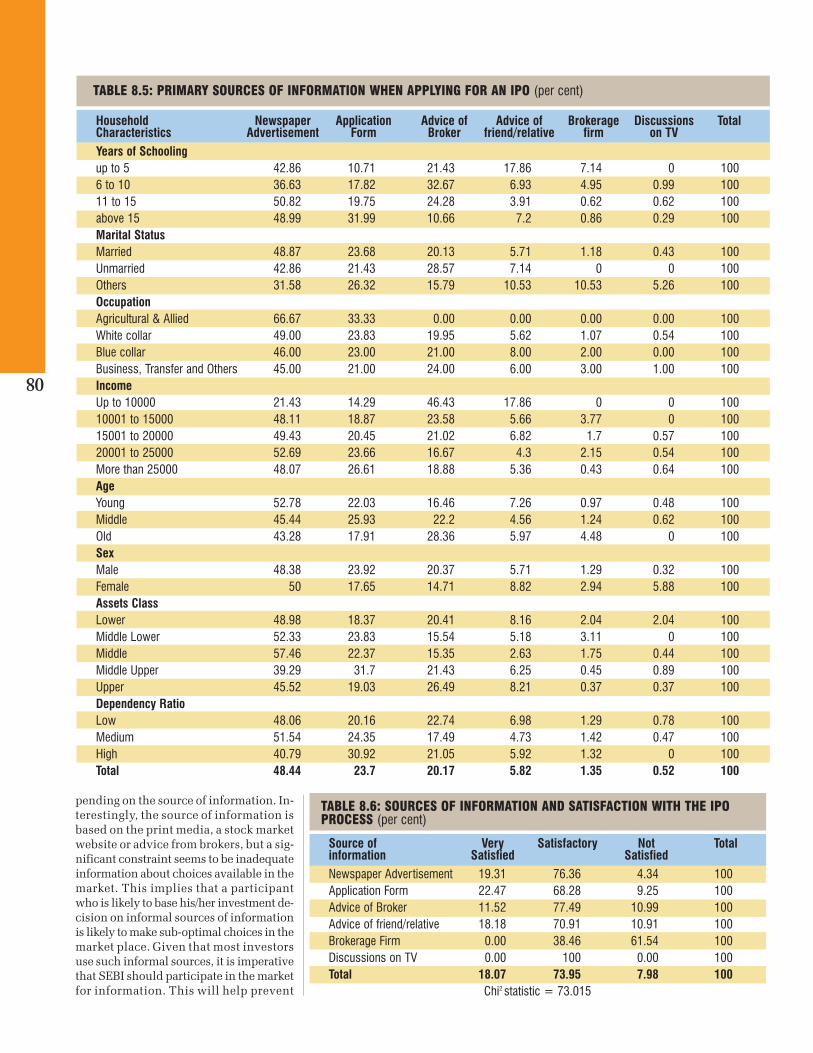

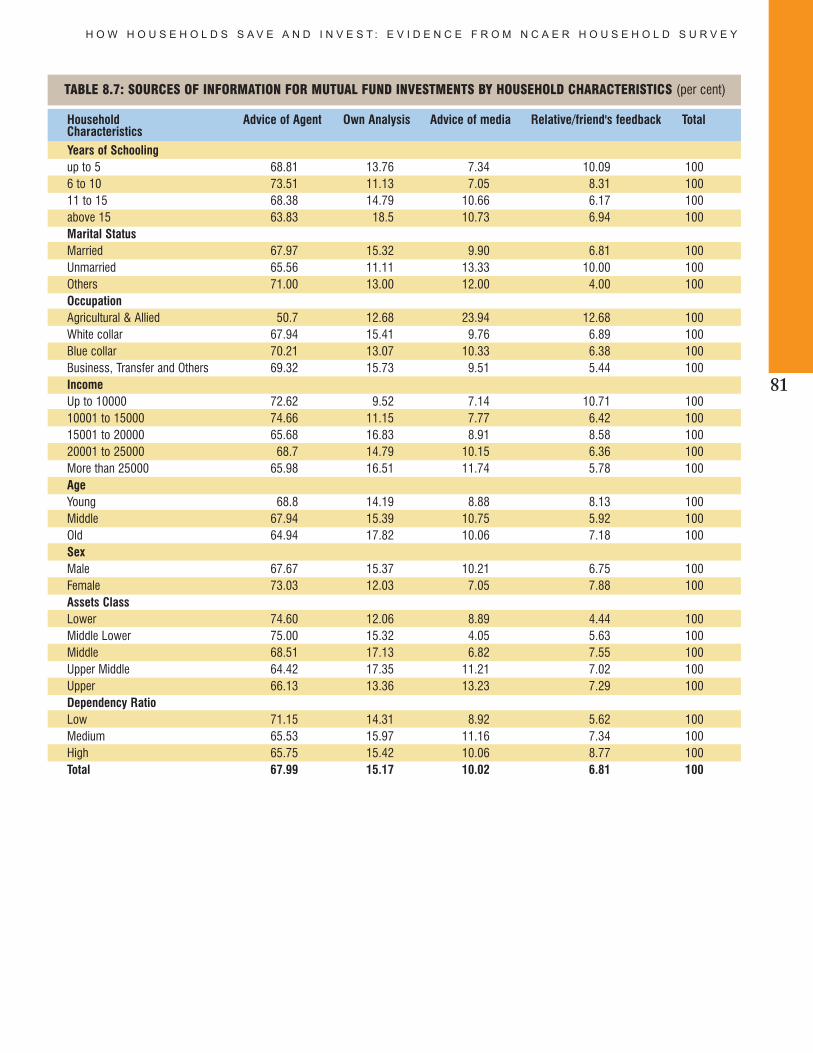

About 40 per cent investors are of theopinion that in the book buildingprocess, the prices of the IPO enteringthe market may not be transparentand the retail investors do not havesufficient knowledge about SEBI’srole. Around 32 per cent of partici-pants feel that the regulator SEBI andMCA may like to take additional stepsrelated to conflict between sharehold-ers and firms. Around 21 per cent ofall investors are not clear about therole of the regulator in preventing un-explained volatility, though it is theperceived role of SEBI to investigatesources of large fluctuations in price.It is the role of the regulator to de-listthe non-performing firms; yet, 24 percent of all investors are not aware ofthe role of the stock exchange or theregulator or the MCA in this process.Thirty nine per cent of all investorsexpect SEBI to undertake actionsagainst inadequate information aboutinvestment choices. Nearly 50 percent of all market participants feelthat exchanges/SEBI is required totake adequate measures to ensuresmooth functioning of the market.The source of retardation in the rate ofparticipation by Indian households inthe market is due to informationasymmetry and the poor quality of in-formation. While applying for an IPO,investors across all income/educationcategories list newspapers as the sin-gle source of information. A signifi-cant number of investors find the ad-vice of brokers more useful. The sur-vey reveals that while participation inmutual funds as well as in the sec-ondary market, a significant majoritydepends on the advise given by inter-mediaries and friends.

A significant source of retardation inthe rate of participation by Indianhouseholds in markets is due to infor-mation asymmetry and poor quality ofinformation. While applying for anIPO, investors across all income / edu-cation categories list newspapers as thesingle source of information. A signifi-cant number of investors find the ad-vice of brokers more useful. The survey

reveals that while participating in mu-tual funds as well as in the secondarymarket, a significant majority dependson the advice given by intermediariesand friends.

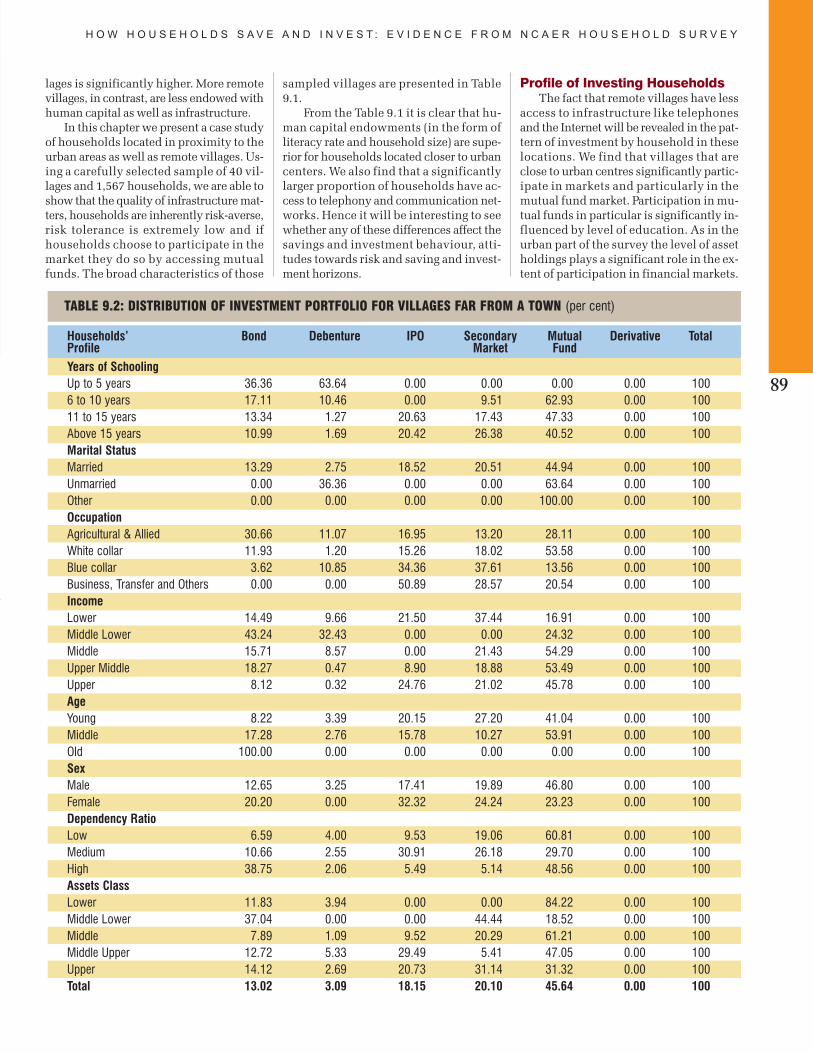

Rural India The rural survey reveals the following

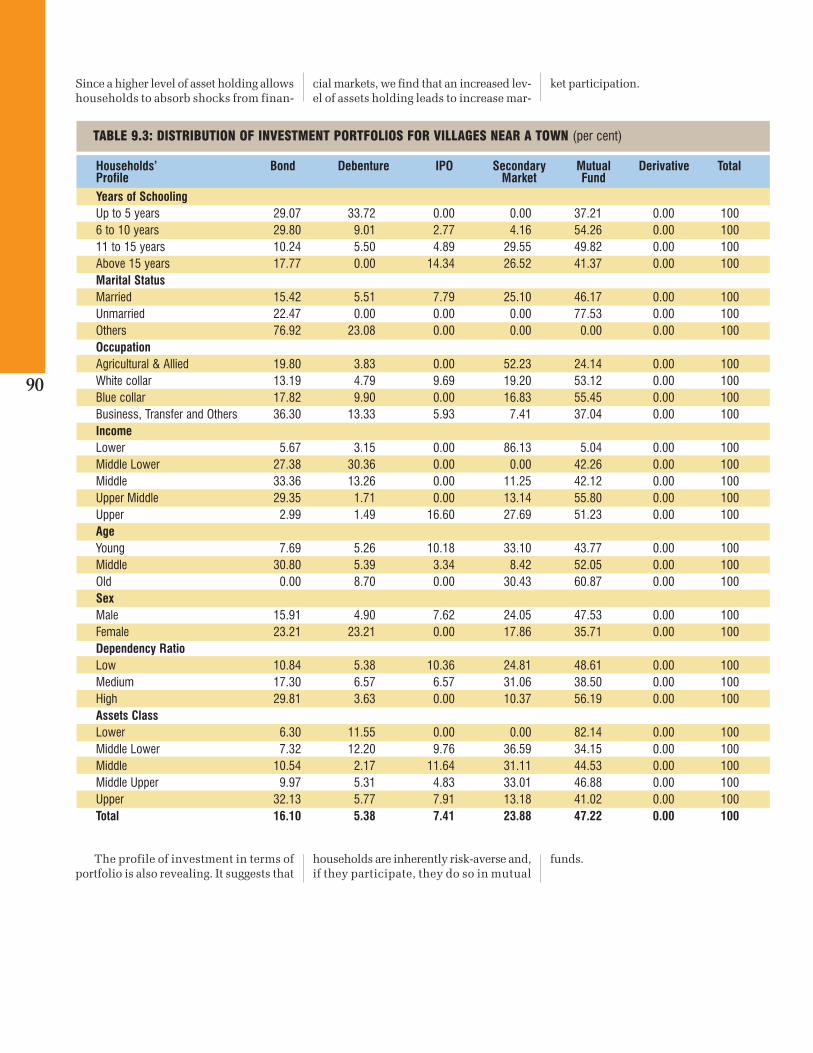

facets of households. The survey re-veals that human capital endowmentsin the form of literacy rate and house-hold size are superior for householdslocated closer to urban centers. A largeproportion of these households haveaccess to telephony and communica-tion networks.

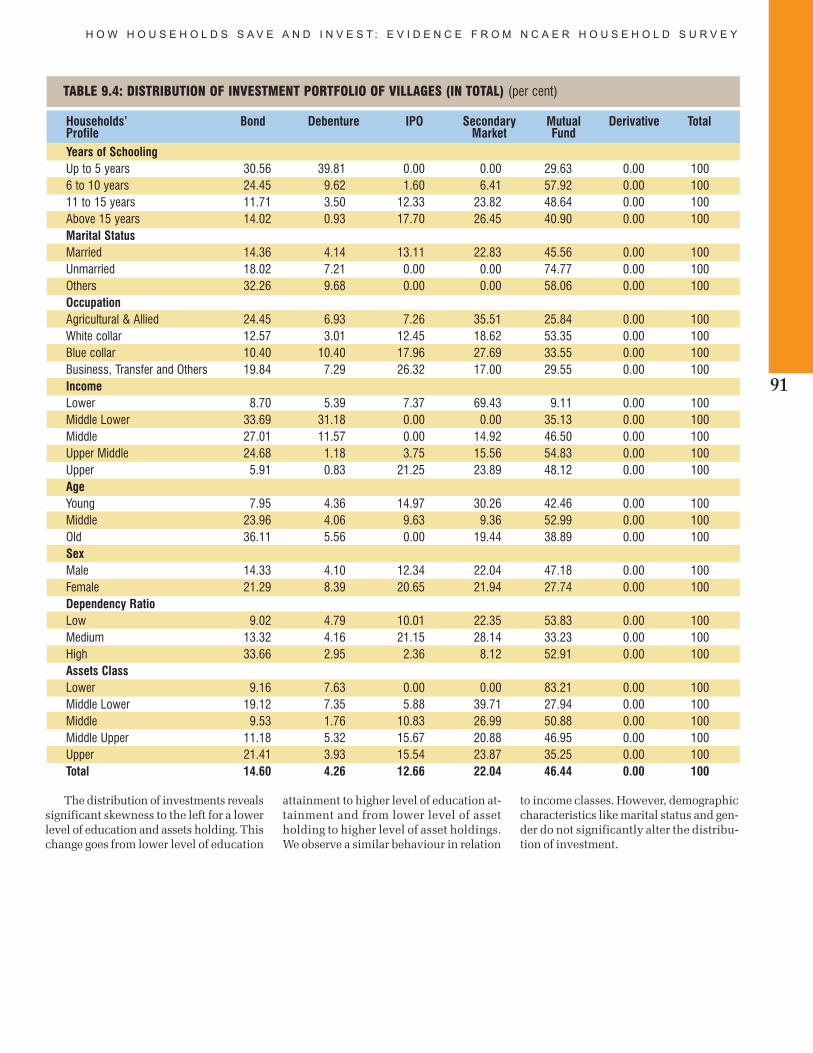

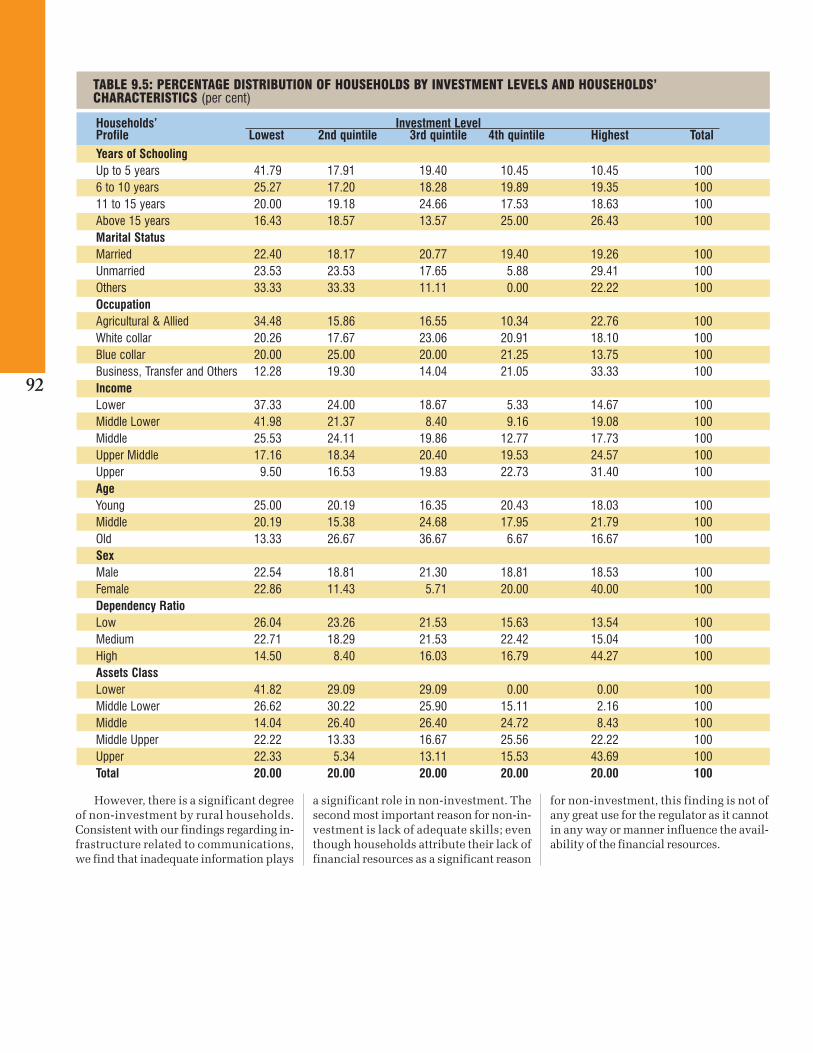

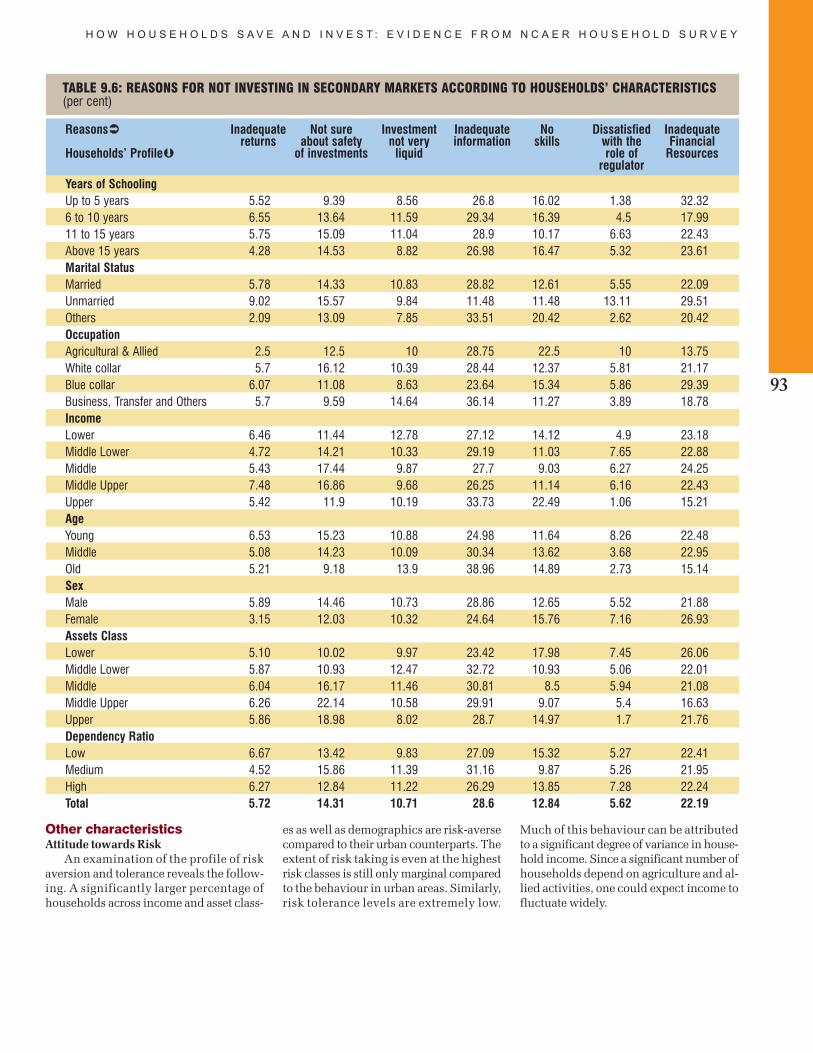

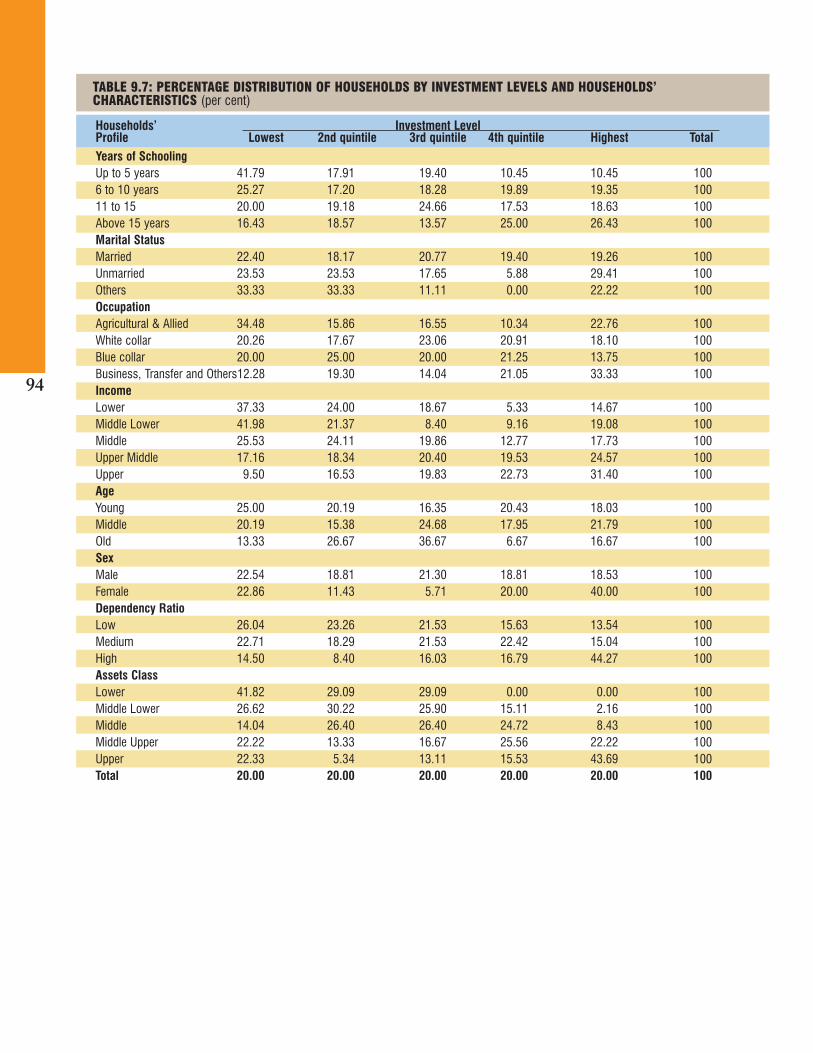

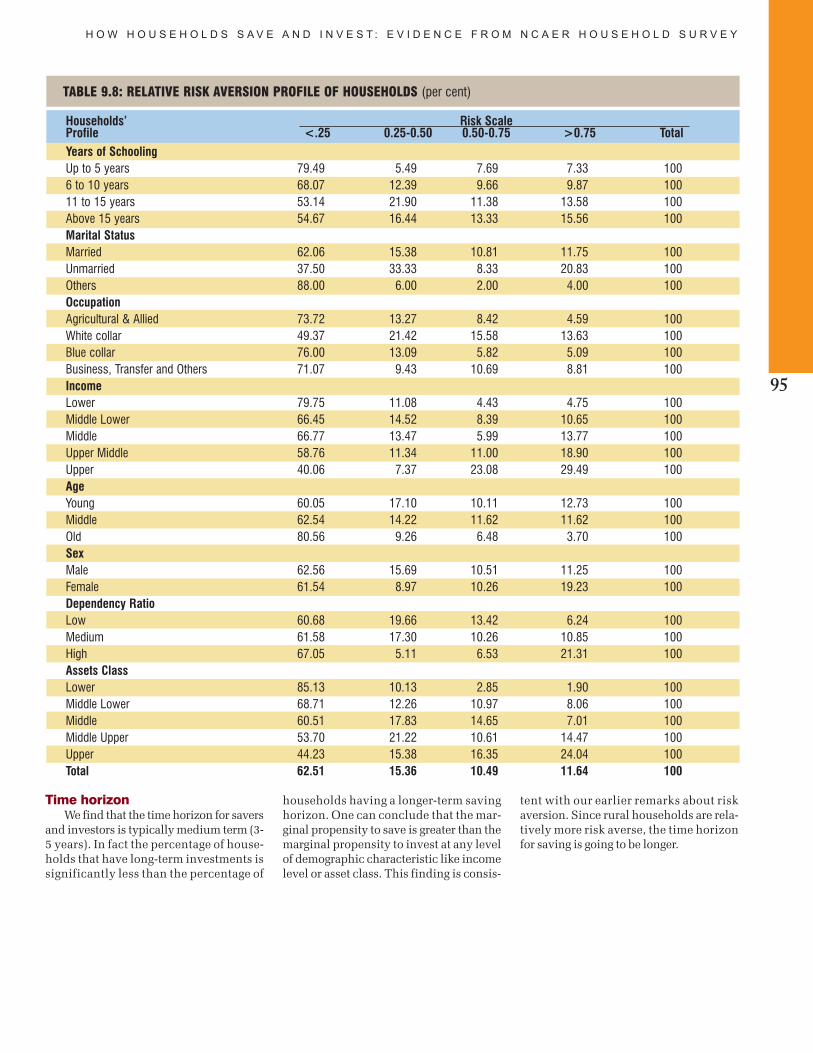

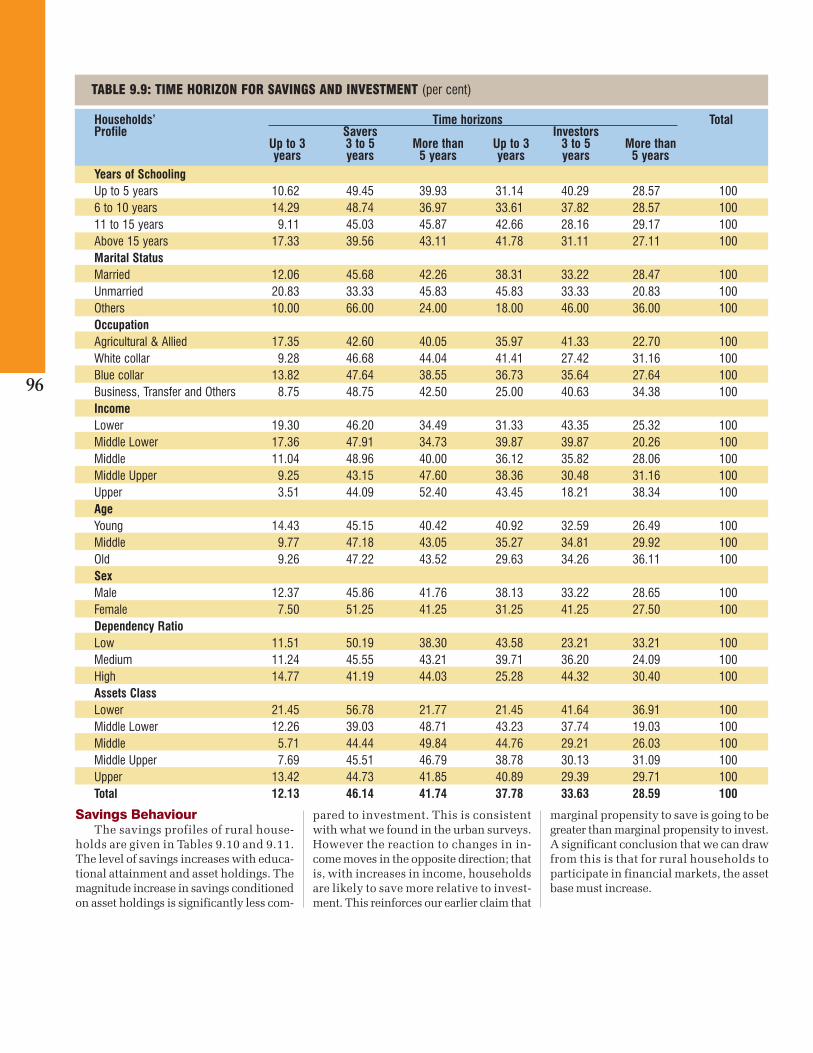

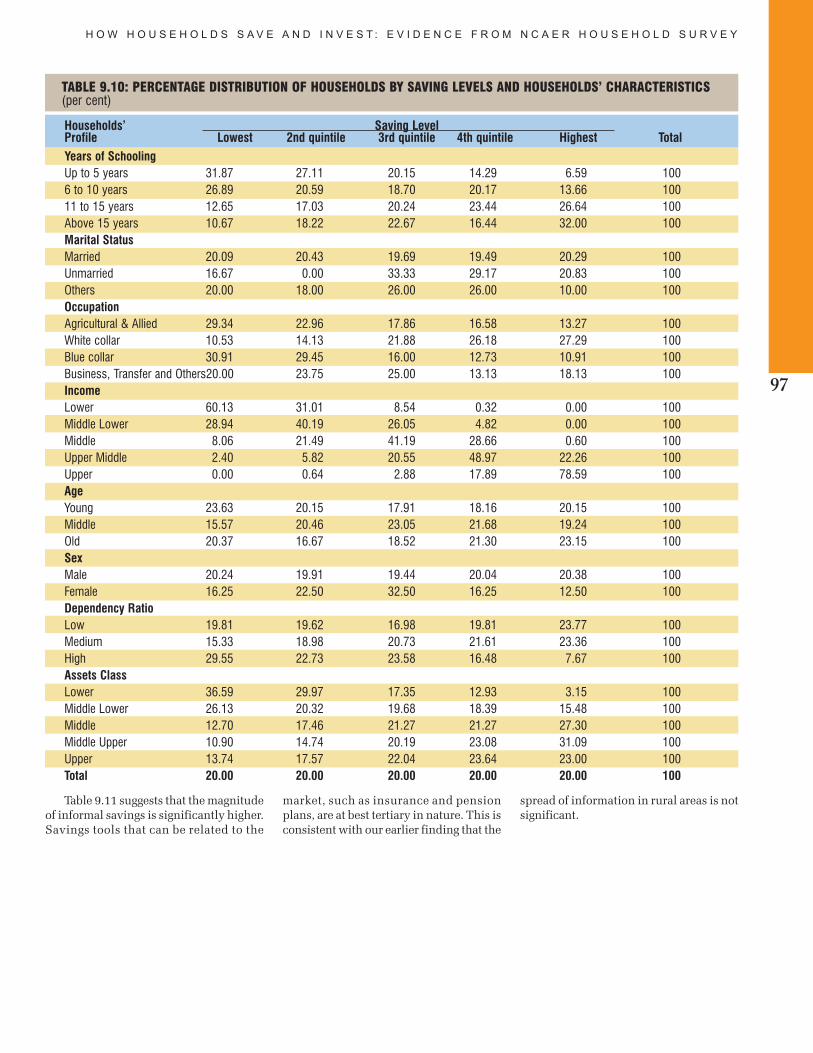

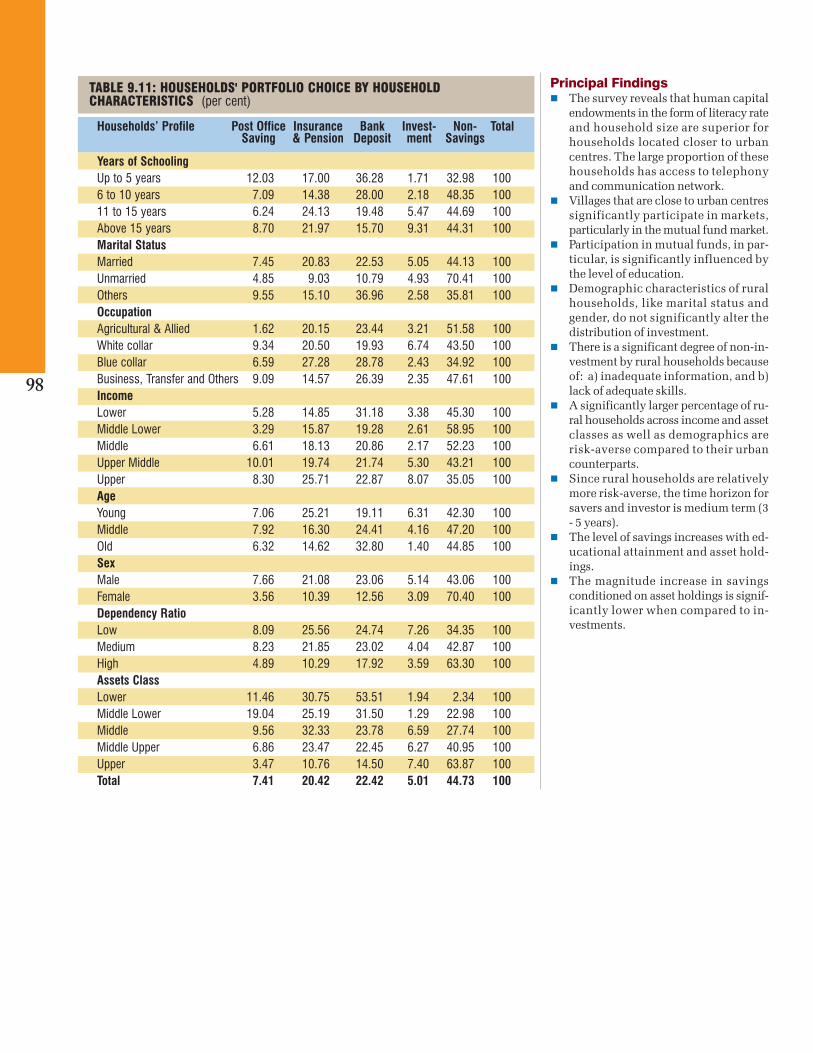

Households in villages that are close tourban centers significantly participatein markets, particularly in the mutualfund market. Participation in mutualfunds, in particular, is significantly in-fluenced by the level of education. De-mographic characteristics of ruralhouseholds, like marital status andgender, do not significantly alter thedistribution of investment. There is asignificant degree of non-investmentby rural households because of: a) in-adequate information, and b) lack ofadequate skills. A significantly largerpercentage of rural households acrossincome and asset classes as well as de-mographics are risk-averse comparedto their urban counterparts. Since ruralhouseholds are relatively more risk-averse, the time horizon for savers andinvestor is medium term (3–5 years).The level of savings increases with ed-ucational attainment and asset hold-ings. The magnitude increase in sav-ings conditioned on asset holdings issignificantly lower when compared toinvestments.

General ObservationsFurther examination of data lead to fol-

lowing observation on the savings and in-vestment profile of households, the struc-ture of savings and investment, the desti-nation of investment, the profile of in-vestors and savers and their perceptionsand motivations.

Households and individual investorssupply a pool of capital that creates liquid-ity in the market and make it dynamic.Thus, household income, its consumptionand its distribution are fundamental to anyeconomic analysis. These determine thenature and rate of saving in an economywhich, in turn, implies the rate of econom-ic growth. Sustained research in this fieldthus becomes imperative in order to un-derstand the patterns of savings and capi-

tal formation in our country. The observa-tions below are drawn from the responsesof the urban households as bulk of the in-vestor households is in the urban areas.

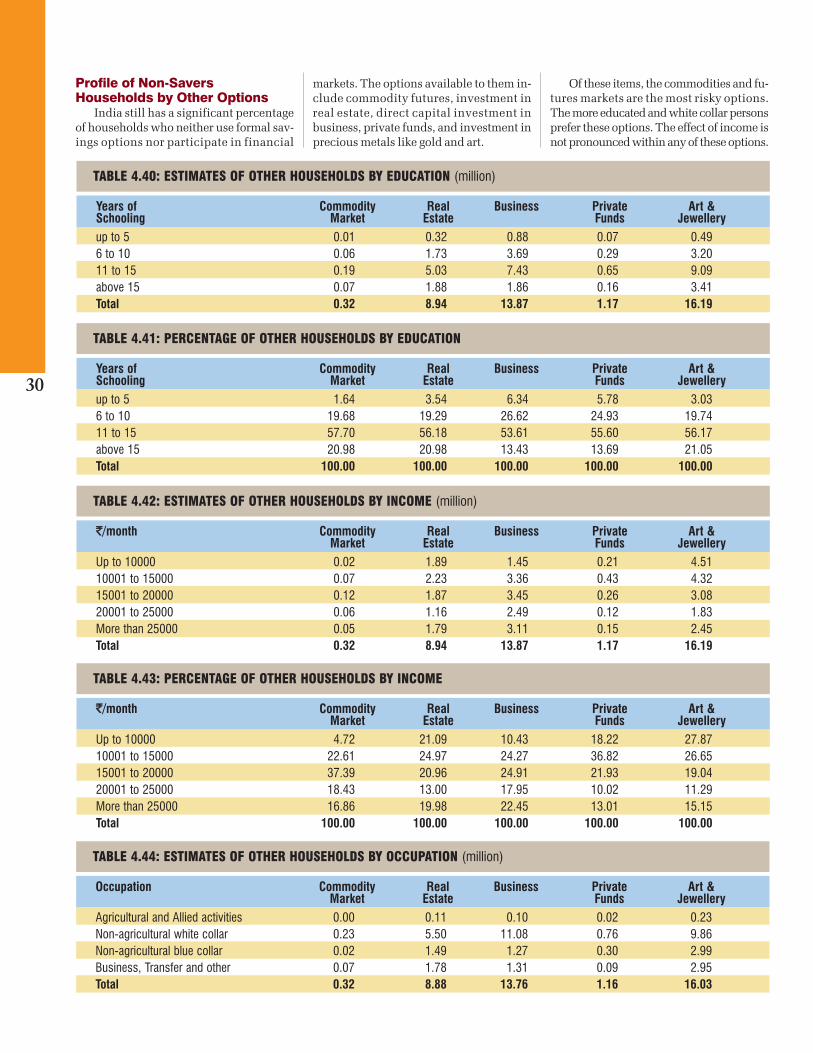

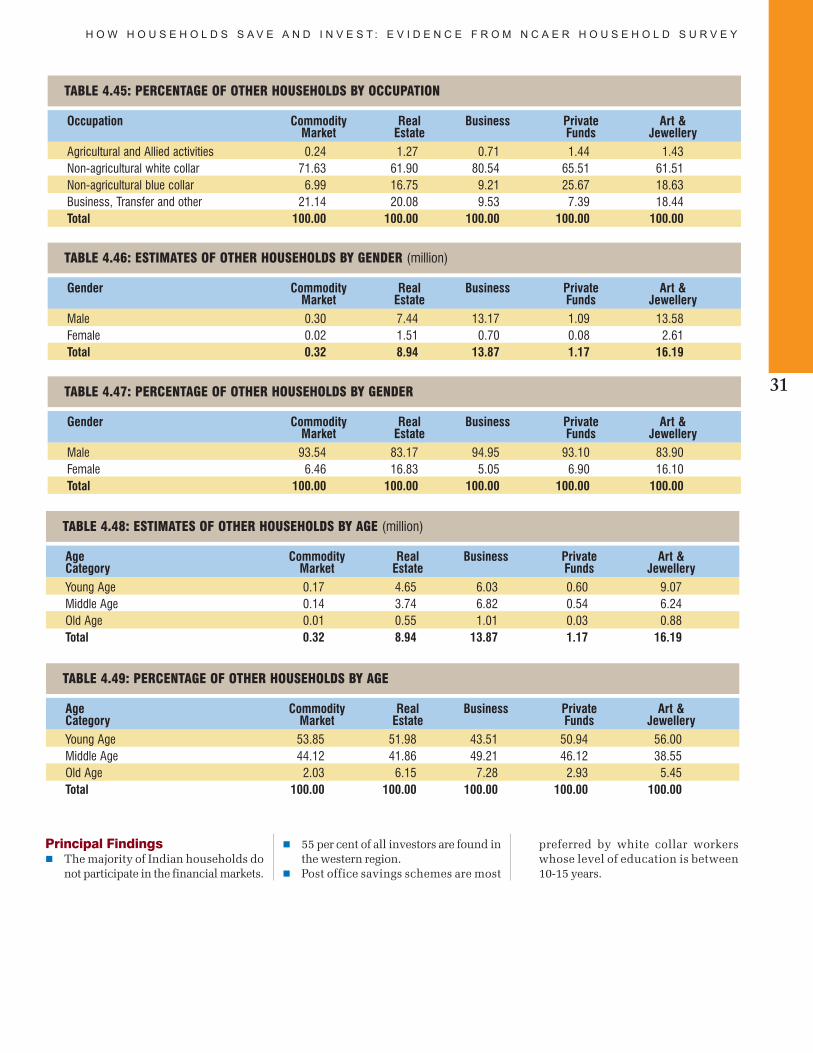

1. The majority of investors are urban incentral and eastern India. This reflectsthe fact that the degree of urbanizationis weaker in these regions. India stillhas a significant percentage of house-holds who neither use formal savingsoptions nor participate in financialmarkets. The options available to theminclude commodity futures, invest-ment in real estate, direct capital in-vestment in business, private funds,and investment in precious metals likegold and art.

2. Of these items, the commodities andfutures markets are the most risky op-tions. The more educated and whitecollar persons prefer these options. Theeffect of income is not pronouncedwithin any of these options. It is alsoimportant to understand the relation-ship between demographic character-istics and time horizon of investment,particularly for the regulator. If house-holds in general have short-term in-vestment horizons, then the regulatorcan expect to see a significant degree ofspeculative activities in the markets.

3. It is important for regulators to under-stand households' ability to take risk aswell as the general appetite for risk.The consequences of risk-taking activ-ity on the part of households are oftenobserved in the market place. For ex-ample, markets for stocks, derivativesand commodity futures are inherentlymore risky avenues for household. Onthe other hand, the market for mutualfunds and bonds are markedly lessrisky options available to households.A significant movement in the stockmarket and allied risky market can bean indication that households and in-stitutional investors are increasinglygoing to take risks.

4. Typically we would want to attributethe ability on the part of households toengage in risky behaviour (as it relatesto participation in market) to: a) a de-gree of information asymmetry in themarket place, b) the extent of regulationof markets (perceived water-tight meas-ures against big bulls, etc.) and c)household budget constraints. Themarket regulator can affect the first twofactors but can feel the consequences ofthe third in the market place. That is,due to macroeconomic forces the budg-et constraints of the household can get

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

xv

relaxed and this can lead previouslynon-participating households to partic-ipate and current participants to in-crease their allocation; risk-taking be-haviour could increase faced with theincrease in liquidity in the household.

5. Risk in finance and business is thevariability of returns from an invest-ment. This reflects the degree of uncer-tainty of returns on an asset. Thegreater the variability in return from in-vestments, the greater is the perceivedrisk. Risk tolerance is the degree of un-certainty that an investor is willing toabsorb with respect to a negativechange or variability in the value of his/her portfolio.

6. Though SEBI has put in place mecha-nisms for the smooth functioning ofthe IPO market, it is worrying to notefor example that about 40 per cent ofinvestors believe that in the bookbuilding process prices for the IPO en-tering the market are either not trans-parent or are not aware of SEBI's role.The magnitude of lack of awareness ofSEBI's role in various stages of an IPOis small but quite significant. Thirtytwo per cent of participants in the IPOprocess feel that the procedure for re-fund for non-allocation are either inad-equate or the role of SEBI in this is per-ceived to be non-transparent.

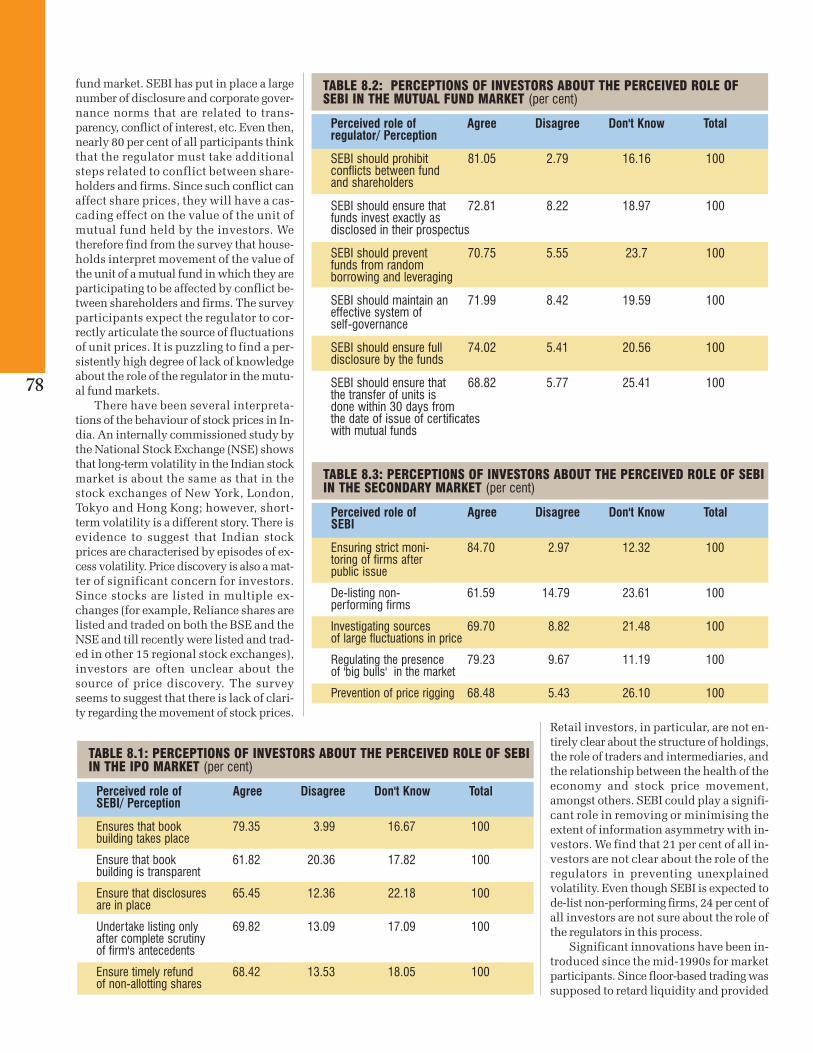

7. This survey clearly suggests that in-vestors expect SEBI to put in place a setof mechanisms that would enable in-vestors to effectively access the mutualfund market. SEBI has put in place alarge number of disclosure and corpo-rate governance norms that are relatedto transparency, conflict of interest, etc.Even then, nearly 80 per cent of all par-ticipants think that the regulator musttake additional steps related to conflictbetween shareholders and firms. Sincesuch conflict can affect share prices,they will have a cascading effect on thevalue of the unit of mutual fund heldby the investors. We therefore findfrom the survey that households inter-pret movement of the value of the unitof a mutual fund in which they are par-ticipating to be affected by conflict be-

tween shareholders and firms. The sur-vey participants expect the regulator tocorrectly articulate the source of fluc-tuations of unit prices. It is puzzling tofind a persistently high degree of lackof knowledge about the role of the reg-ulator in the mutual fund markets.

8. SEBI could play a significant role in re-moving or minimizing the extent of in-formation asymmetry with investors.We find that 21 per cent of all investorsare not clear about the role of the regu-lators in preventing unexplainedvolatility. Even though SEBI is expect-ed to de-list non-performing firms, 24per cent of all investors are not sureabout the role of the regulators in thisprocess.

9. Interestingly even with online tradinga significant percentage of current, pastand potential participants expect a de-gree of price rigging. To correct theseills, the survey suggests that a signifi-cant number of investors expect SEBIto take action, such as monitoring postpublic issues (39 per cent), de-listing(29 per cent) and investigating undueprice fluctuations (32 per cent). How-ever given the continued prevalence ofthe bullish market nearly 50 per cent ofall market participants say that SEBIhas not put in adequate mechanisms toprevent the recurrence of the big bulls(who drive up the market without fun-damental reasons) in the market.

10. Based on the findings of the survey, it isour opinion that the source of retarda-tion in the rate of participation by Indi-an households in the market is due toboth information asymmetry as well asthe poor quality of information. For ex-ample, we find that a single importantsource of information for investorsacross all income/education categorieswhile applying for an IPO is newspa-pers. This ought to be of serious signif-icant concern for the regulator sinceboth current and potential market par-ticipants are basing their judgment oninadequate source of information. SE-BI must undertake to fine-tune the in-vestor camps so that households avoidtheir unreliable sources of information.

Given the existing scenario related tothe provision of information, there isnothing surprising with the findingsthat most market participants are onlymoderately satisfied with the informa-tion provided by regulators and, in fact,find information from intermediariessuch as brokers more useful.

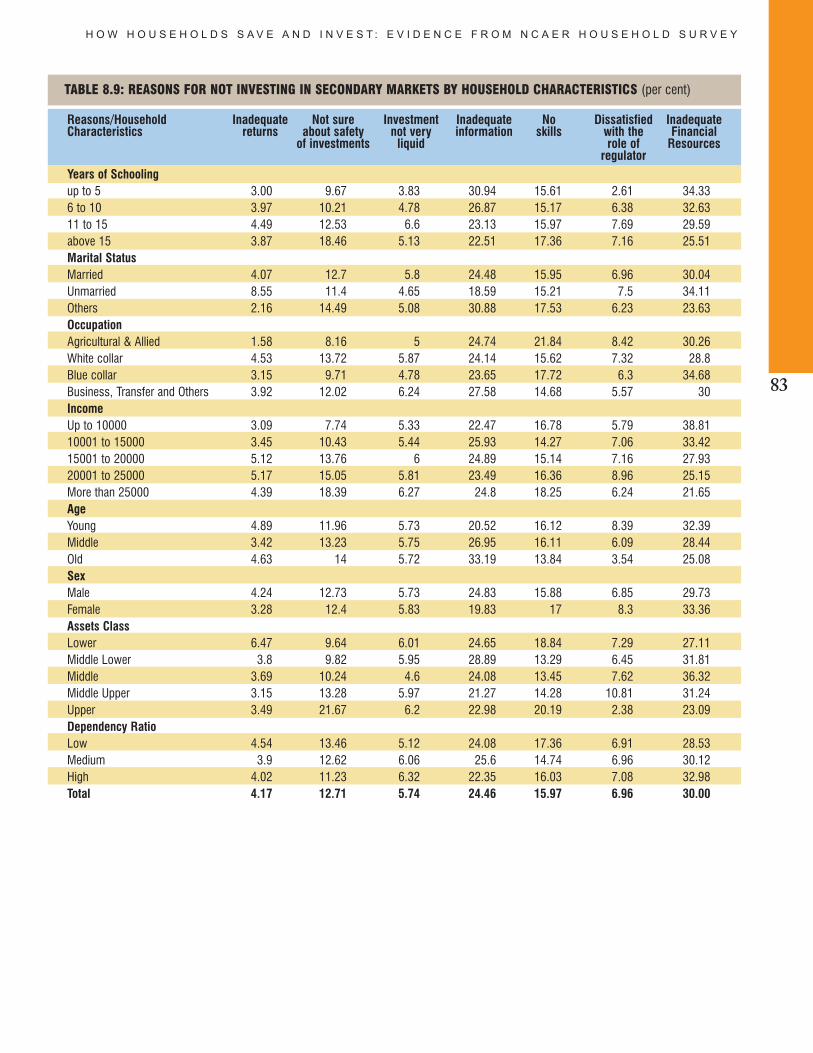

11. When we examine the reasons for notparticipating in markets we find that(in descending order) they are inade-quate information, lack of skills anduncertainty about safety of returns.Households have also identified inad-equate financial resources as con-straint on participation. However thisis not within the control of SEBI andwe therefore chose not to elaborate onthis aspect of non-participation at thispoint. It is evident that SEBI could takeadditional steps to impart skills, reducethe information asymmetry at the timeof participation and put in place morewater-tight measures to guarantee thesafety of returns.

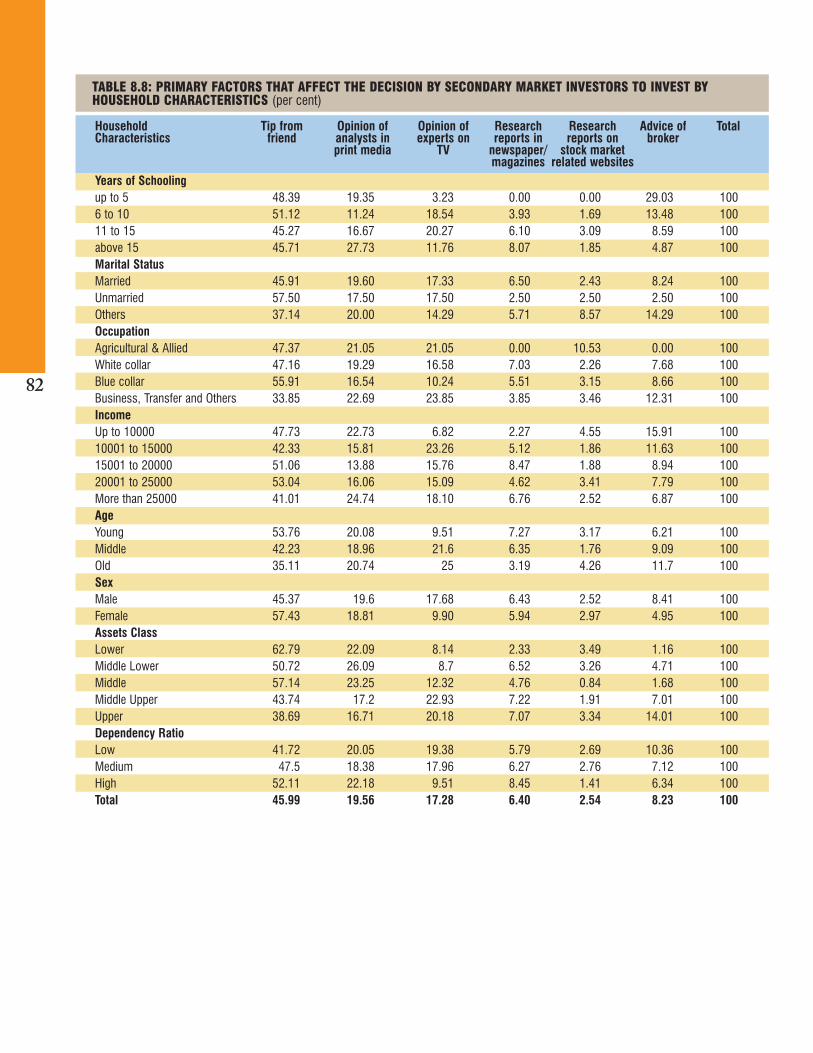

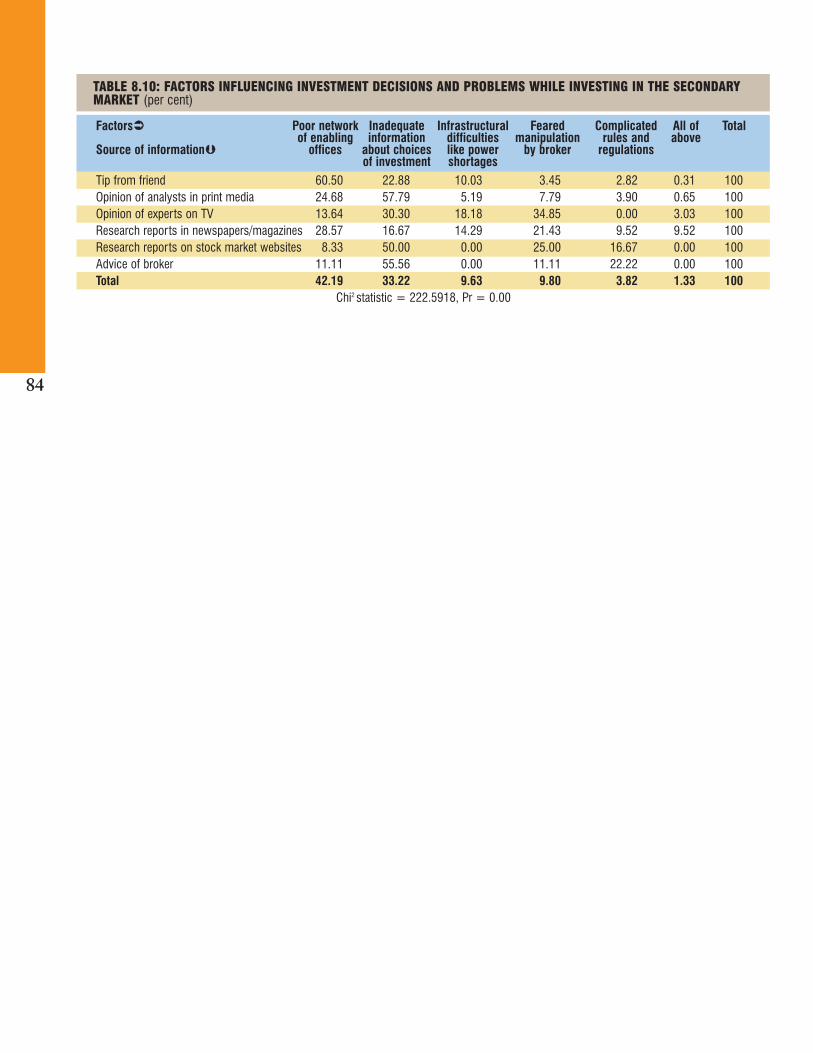

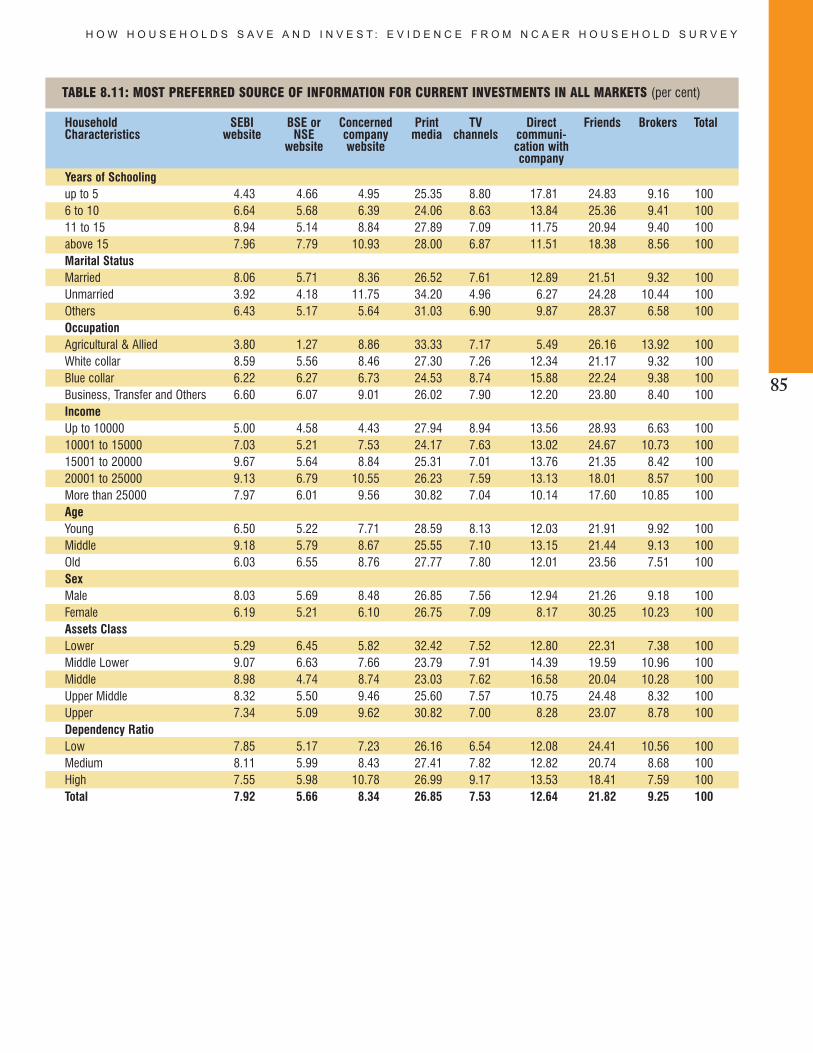

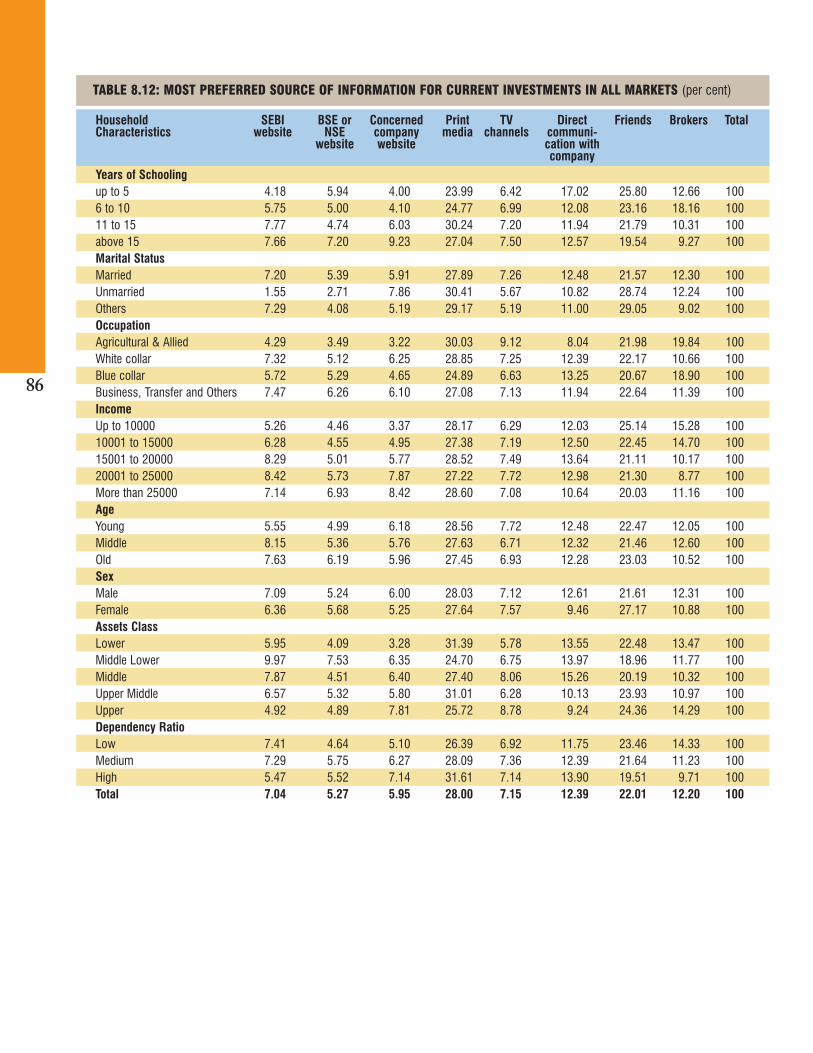

12. The constraints faced by participatingin the secondary market seem to varydepending on the source of informa-tion. Interestingly, we find that thesource of information is based on theprint media, a stock market website oradvice from brokers, but a significantconstraint seems to be inadequate in-formation about choices available inthe market. This implies that a partici-pant who is likely to base his/her in-vestment decision on informal sourcesof information is likely to make sub-op-timal choices in the market place. Giv-en that most investors use such infor-mal sources, it is imperative that SEBIshould participate in the market for in-formation. This will help prevent mar-ket participants from making sub-opti-mal choices as well as reduce existinginstitutional bottlenecks. At presentthe preferred source of information areindeed the print media, friends andbrokers. Both the SEBI and BSE/NSEwebsites are performing only a margin-al role in providing information.

xvi

1

BackgroundThe allocation of resources within

households has always been of interest toresearchers and policy makers. It is widelyaccepted that the development of a na-tion's productive capacity requires capitalformation which can be done either byutilising domestic resources or through ex-ternal assistance. Within domestic re-sources, a nation's savings and investmentpropensities play a key role in reaching tar-geted economic growth as well as dynam-ic stability in the capital market, but anunderstanding of aggregate propensityalone is not sufficient. What is required isa reasonably sound idea of the savings andinvestment profile of households, thestructure of savings and investment, thedestination of investment, the profile ofinvestors and savers and their perceptionsand motivations.

Households and individual investorssupply a pool of capital that creates liquid-ity in the market and make it dynamic.Thus, household income, its consumptionand its distribution are fundamental to any

economic analysis. These determine thenature and rate of saving in an economywhich, in turn, implies the rate of econom-ic growth. Sustained research in this fieldthus becomes imperative in order to un-derstand the patterns of savings and capi-tal formation in our country.

Except for a few household surveys inthe late 90s, very few studies estimate theprofile of households' saving and invest-ment for both rural and urban areas in In-dia. The Micro Impact of Macro and Ad-justment Policies in India (MIMAP) surveyin 1996 and the detailed report on "House-hold Savings and Investment Behaviour inIndia in 2003" by EPW Research Founda-tion and NCAER was an attempt in this di-rection. Although these studies describeIndia's saving performance in detail, theydo not sufficiently describe the analyticalframework of households' decision-mak-ing determinants and the factors that de-termine the propensity to save and invest,which are important from a policy per-spective.

To understand and assist in policy-

making, the Securities and ExchangeBoard of India (SEBI) has been promotingresearch in the Indian securities market.The NCAER–SEBI Survey (1999) provideddisaggregated data on household income,expenditure, asset holdings, savings andinvestment in the share market. Anotherstudy by NCAER on Compliance cost ofSEBI regulations in 2002 presented find-ings on the Indian capital markets. Whilethese surveys have been useful in report-ing distribution and investors' profiles, notmuch can be inferred about actual house-hold behaviour in terms of attitudes to-wards risk, the relationship of such atti-tudes with savings and investment pat-terns, liquidity preferences, etc.

In order to fill this research gap, thisstudy attempts to capture the details ofearning members of households, their per-ceptions about various investment andsavings options, the time horizon for sav-ing and investment, and financial risk tol-erance assessment along with total incomeand its distribution separately for the maincities, states and villages of India for the

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

Introduction and SamplingStrategy

1

year 2008-09. This survey examines in-comes, expenditures, savings, and invest-ments in detail by providing a suitablestructure (for example, vignettes on therisk profile of households). The survey al-so examines the risk worthiness of house-holds in investment in different types ofsecurity markets and their perceptionsabout the role of SEBI in this context.

Focus of the StudyThe objectives of the study are as fol-

lows:1. To prepare a comprehensive profile of

savings and investment behaviour inthe context of income and consump-tion patterns.

2. To create a profile of investors' prefer-ences for various market instrumentslike IPOs, securities and mutual fundsand its significance in the growth inprimary and secondary security mar-kets. The study examines attitudes to-wards different types of savings and in-vestment alternatives.

3. To obtain the risk profile of the house-holds and relate this to savings and in-vestment behaviour. The study assess-es the risk tolerance of investor andnon-investor households with an in-strument called a vignette.

4. To understand the impact of rules andregulations framed by the SecuritiesExchange Board of India (SEBI) on aHouseholds’ choice of investment pat-terns.This study presents a systematic and

stylised analysis of investing households'perceptions about financial market seg-ments regulated by SEBI and other savingsand investment options. Keeping this inmind, we created a listing and householdschedule to obtain detailed informationabout household earnings, savings and in-vestment profile, income-expenditure, fi-nancial and non-financial asset holdings,and aspirations and decisions in invest-ment depending on their perceptions ofvarious saving and investment options andthe role of the regulator, and their marketawareness.

Study Design, Concepts andDefinitions

The objective of this study is to preparea comprehensive profile of the savings andinvestment behaviour of households. Us-ing this profile we propose to understandtheir respective risk profiles and the barri-ers to participation in primary and second-ary markets as well as in instruments con-trolled by the regulations issued by SEBI.The study is also interested in determining

the steps that SEBI could take to enhanceparticipation in the markets, the sourcesand uses of information by households andthe role of information in mediating house-hold behaviour in markets.

The study also sheds light on the dis-tribution in markets of participants as wellas non-participants to understand the rateof growth of market participants. The sam-ple selected thus provides insights into thebehaviour of households and also de-scribes the distribution of householdsacross the economic space. For example, itwill be pertinent to see if market participa-tion is a purely urban phenomenon. Sucha finding is important to the regulator sothat it can fine-tune its outreach activities.

Based on the NCAER's previous expe-rience of conducting household-levelstudies and a comprehensive review ofsimilar studies of international repute, asuitable procedure was adopted to identi-fy the approach, concepts and definitions,create a sample design, select the samplesize, identify the content of the question-naire, etc.. This survey intends to generatea reliable explanation of household behav-iour besides arriving at a robust estimate ofthe number of savers, investors, and othertypes of households.

Survey DescriptionThe household is the basic unit of

analysis in the study. A household surveywas conducted in 25 major states/ UnionTerritories of India. The territories of Jam-mu & Kashmir, Arunachal Pradesh, Naga-land, Manipur, Mizoram, Tripura, An-daman & Nicobar Islands, Daman and Diu,Dadra and Nagar Haveli and Lakshadweepwere excluded due to operational difficul-ties.

The sample size is 38,412. The samplesize was proposed based on the degree ofprecision required to arrive at reliable pop-ulation estimates. However, a preliminaryround of listing showed that such a samplewould overestimate categories such asnon-investors or savers. We listed 70,159households in 44 cities and 40 villagesacross the states. The original listing had17 categories of investment and savings.We found that the occurrence of house-holds in the categories related to investorswas less than 2 per cent.

Hence, it was decided not to have afixed sample size; instead, we focussed onselected blocks from each city/ town. 100households were listed from each block(representing roughly 60 per cent of theblock population). This listing exerciseprovided a context for the study within theresearch site and, by breaking down the

households into saving/investment strata,it elucidated the need to make inferencesderived from comparing groups of demo-graphically homogenous cities. These esti-mates will illuminate household charac-teristics and benefit our attempt to under-stand household behaviour and risk per-ception.

The selected households were sur-veyed for their household income statusand preference for saving and investmentunder the 17 categories listed below.

Stratum I. Investors: Householdsthat invested in any of thefollowing options in the current/previous year Government bonds Bonds issued by government under-

takings, such as IDBI, SBI, GAIL andSAIL.

Debentures in private companies Equities in private companies Mutual Funds Derivatives

Stratum II. Savers: Householdsnot invested in the above but inthe options given below Post Office and other similar savings

schemes Pension schemes Public insurance schemes: LIC; private

insurance such as Max and Bajaj. Commercial/private/public sector

banks Co-operative/ regional rural banks

Stratum III. Other Savers:Households invested in theoptions below Commodities futures Real estate Businesses Private funds Precious metals & jewellery Art

Owing to non-responses in a numberof sub-categories, the original list of 17categories was reduced to reflect threecategories, viz., investors, savers, and oth-ers. A household was listed as an investorif it had undertaken any of the investmentoptions above irrespective of its savingsdecisions; a household was listed as asaver if it did not participate in any of theinvestment options but chose to save innon-risky sources; and a household wasclassified as Other Saver if it did not un-dertake any of the listed savings and in-vestment options but chose to savethrough other means. A household that

2

did not qualify under any of these threecategories was classified as 'None', andsince their proportion was very small,they were merged with Stratum III. Al-though during listing households were al-so categorised by income group, this wasamalgamated at the time of sample selec-tion in order to capture all income groupsfor unbiased estimation. Within each cat-egory a minimum admissible distributionwas arrived at. A total of 38,412 house-holds were selected from 652 urbanblocks in 44 cities, and 40 villages.

Selection of Urban SampleFollowing the purposive sampling de-

sign, all the state capitals were included inthe survey along with major urban ag-glomerations present in the states/UT.These were classified into town sizes pro-portional to the population. Following thisprocedure, a total of 44 cities were sampledfor this study, with populations rangingfrom over one crore to less than five lakh.In each of the selected cities, final house-holds to be sampled were selected ran-domly across the three strata.

Selection of Rural SampleDuring the listing for village-level

households, it was found that there was in-adequate representation of households inthe three strata, with almost all the house-holds falling into either Stratum III or the'none' category. Since the purpose of ourstudy is to understand rural householdsavings and investment behaviour and notthe magnitude of savings and investmenthouseholds, it was decided to undertake acase study of the savings and investmentbehaviour of rural households.

With the objective of understandinghousehold behaviour and the role of accessto information in a Households’ saving andinvestment decisions, the case study surveys 40 villages following equal proba-bility sampling from 10 states where an adequate representative sample was available. Four villages from every statewere selected randomly, with two villagesproximal to the urban city which was selected for the urban sample and two villages remote from the selected urbancentre. The assumption underlying this selection technique was that proximity toan urban centre is a proxy for access to in-formation. Therefore, our rural case studyattempts to elaborate how access to an ur-

ban centre and infrastructure affects thesaving/investment decisions of ruralhouseholds.

Organisation of the ReportThis report consists of ten chapters.

The Chapter 1 introduces the back-ground, objectives and sampling design ofthe study, while Chapter 2 describes thedevelopments in the Indian capital mar-kets. Subsequently, Chapter 3 focuses onthe estimation of numbers ofinvestors/non-investors and their profileat the national level. Chapter 4 focuses onthe estimated numbers of investors andsavers by location and household charac-teristics in urban India. The savings andinvestment patterns of the respondentsare described in detail in Chapters 5 and6. Chapter 7 profiles the risk behaviourand relative risk tolerance of the house-holds and Chapter 8 discusses the twomain factors affecting investment deci-sions, namely, the perceived role of SEBIand sources of information related to in-vestment. Chapter 9 presents the casestudy for rural India. Conclusions of thereport is assembled in Chapter 10.

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

3

4

The Indian securities market has ahistory of nearly 150 years. TheBombay Stock Exchange, the

Ahmedabad Stock Exchange and the Cal-cutta Stock Exchange are among Asia's old-est stock exchanges. However, the modernera in the Indian securities market and itstransformation began with the economicreforms in the early 1990s when the gov-ernment initiated a systemic shift to a moreopen economy with greater reliance onmarket forces in which the private sectorplays an important role. The Indian secu-rities market gained greater importanceand the SEBI Act, 1992 established the Se-curities and Exchange Board of India (SE-BI) as a statutory authority to oversee thesecurities market in India.

SEBI is mandated with three principalobjectives:

(i) To protect the interests of investors insecurities;

(ii) To promote the development of the se-curities market; and

(iii) To regulate the securities market.

Before the establishment of SEBI, ac-tivities in securities markets lacked a com-prehensive regulatory framework andwere opaque. Since the establishment ofSEBI, the securities market in India has de-veloped significantly. It led to a successfultransition from a highly controlled merit-based regulatory regime to market-orient-ed disclosure-based regulatory regime. SE-BI's focus has been on developing a well-regulated modern securities market in In-dia by adopting global standards and inter-national best practices. With the imple-mentation of various rules and regulationsprescribed by SEBI, access to informationhas increased, the risk of defaults has gonedown and overall governance and ambi-ence have become conducive for protec-tion of investors' interests and the devel-opment of the securities market in India.

The Quantitative Aspects ofMarket Transformation

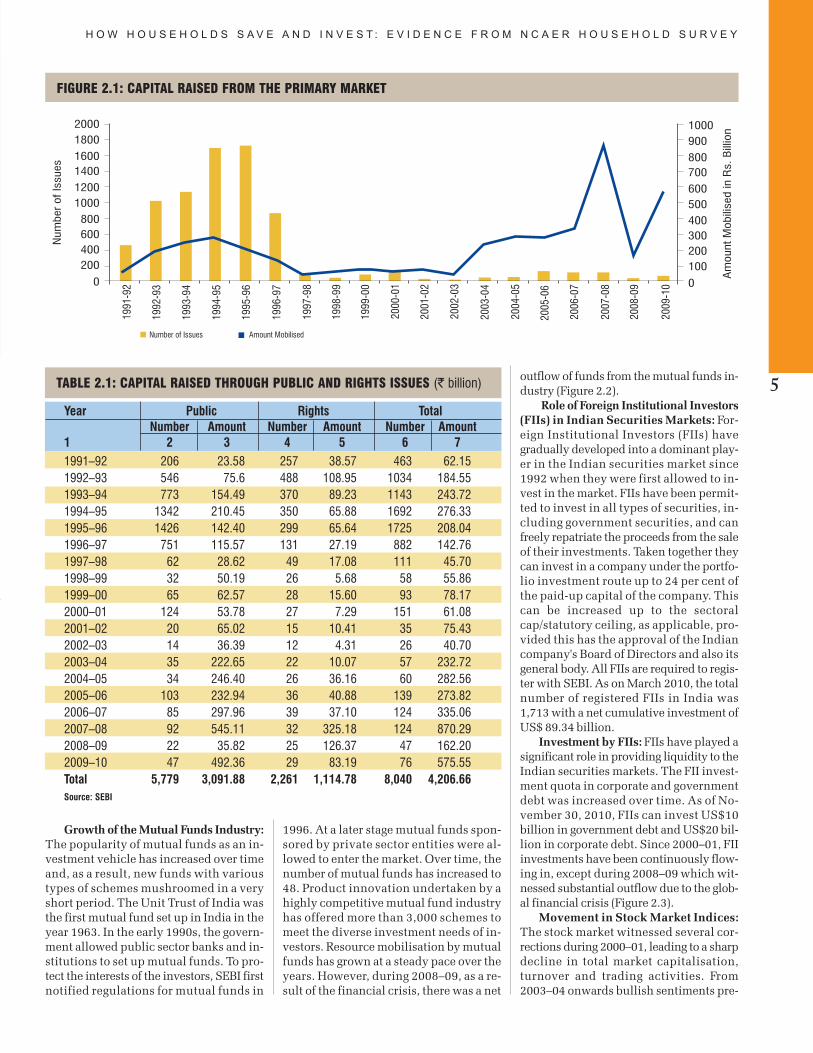

Development of Primary Securities

Market: An efficient primary market iscritical for resource mobilisation by corpo-

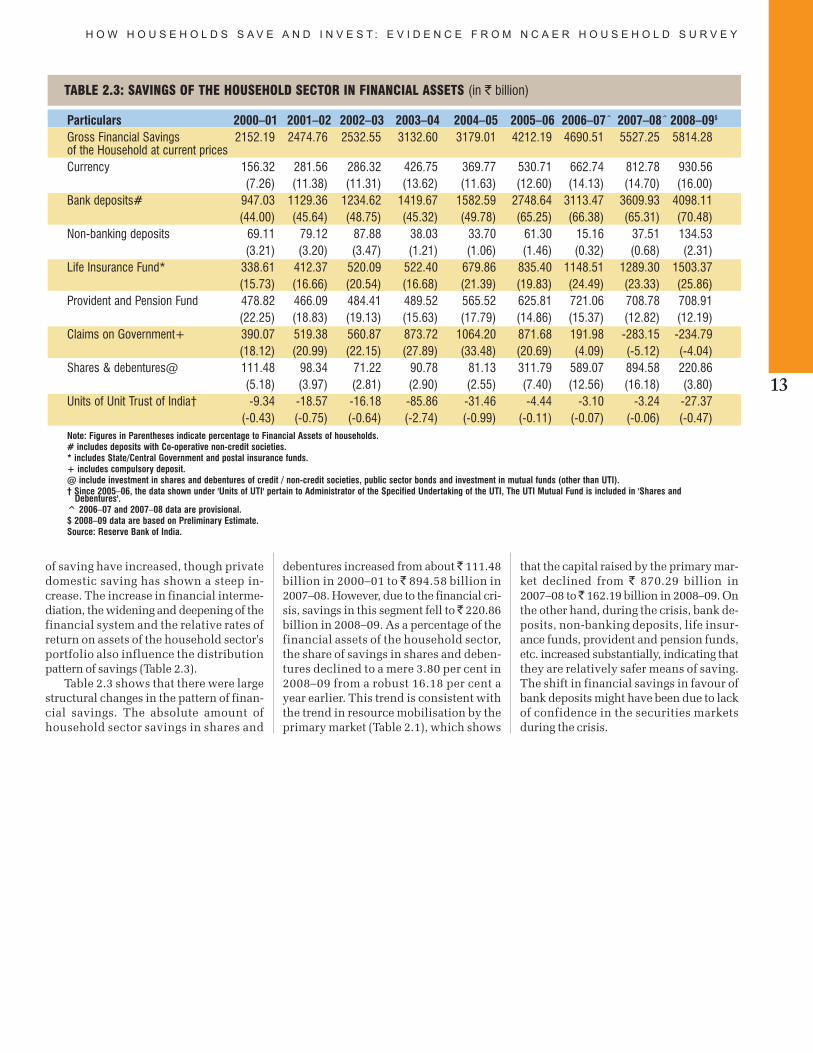

rate to meet their growth and expansionplans. The development of primary mar-kets in India has followed a unique pat-tern. While the number of issues in the ear-ly nineties was very high (more than1,000), the aggregate resources mobilisedwas not significant. However, in the firstdecade of the 21st century the trend gradu-ally reversed; the number of issues re-mained low (less than 200) but the amountmobilised increased significantly. The on-ly exception to this trend was during2008–09 when the US was hit by the sub-prime crisis leading to a global financialcrisis and the cascading effect was felt inemerging markets. Where in 2007–08 anamount of ̀ 870.29 billion was mobilisedthrough 124 public and rights issues, theamount mobilised fell to a mere ̀ 162.20billion through 47 issues in 2008–09. Withthe gradual waning of the sub-prime crisisin 2009–10, the market regained confi-dence and an amount of ̀ 575.55 billionwas mobilised through 76 issues (Figure2.1).

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

Developments in the IndianCapital Markets

2

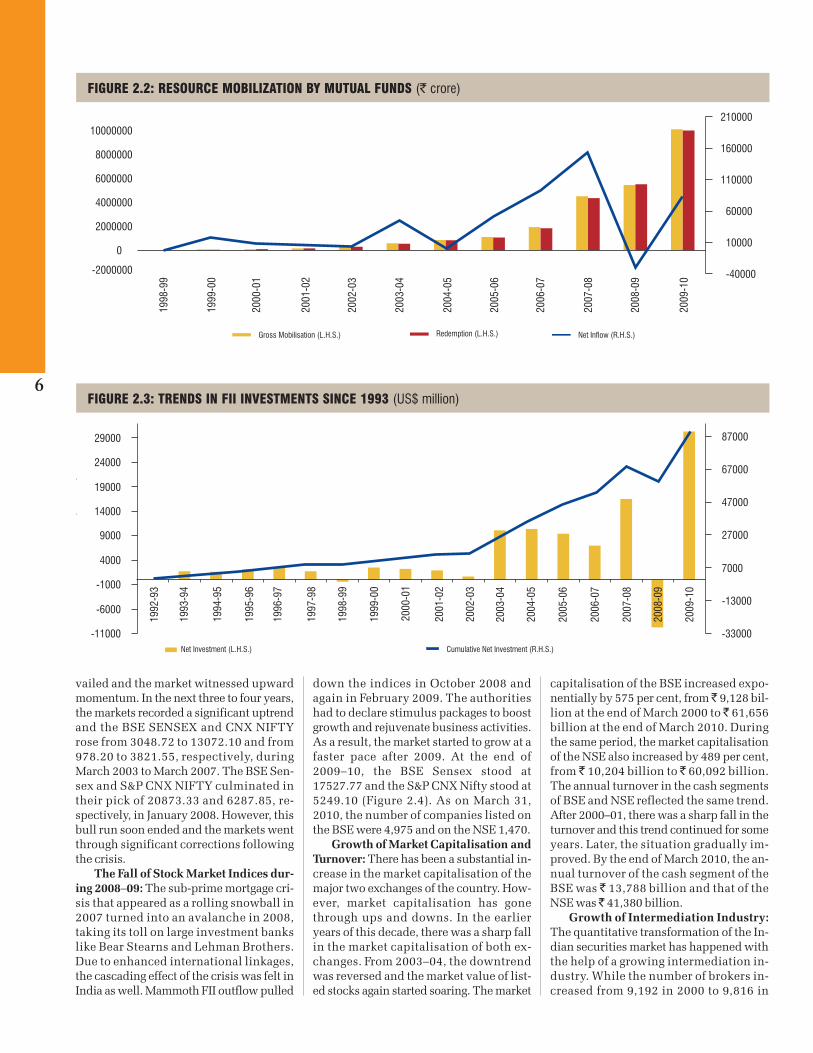

Growth of the Mutual Funds Industry:

The popularity of mutual funds as an in-vestment vehicle has increased over timeand, as a result, new funds with varioustypes of schemes mushroomed in a veryshort period. The Unit Trust of India wasthe first mutual fund set up in India in theyear 1963. In the early 1990s, the govern-ment allowed public sector banks and in-stitutions to set up mutual funds. To pro-tect the interests of the investors, SEBI firstnotified regulations for mutual funds in

1996. At a later stage mutual funds spon-sored by private sector entities were al-lowed to enter the market. Over time, thenumber of mutual funds has increased to48. Product innovation undertaken by ahighly competitive mutual fund industryhas offered more than 3,000 schemes tomeet the diverse investment needs of in-vestors. Resource mobilisation by mutualfunds has grown at a steady pace over theyears. However, during 2008–09, as a re-sult of the financial crisis, there was a net

outflow of funds from the mutual funds in-dustry (Figure 2.2).

Role of Foreign Institutional Investors

(FIIs) in Indian Securities Markets: For-eign Institutional Investors (FIIs) havegradually developed into a dominant play-er in the Indian securities market since1992 when they were first allowed to in-vest in the market. FIIs have been permit-ted to invest in all types of securities, in-cluding government securities, and canfreely repatriate the proceeds from the saleof their investments. Taken together theycan invest in a company under the portfo-lio investment route up to 24 per cent ofthe paid-up capital of the company. Thiscan be increased up to the sectoralcap/statutory ceiling, as applicable, pro-vided this has the approval of the Indiancompany's Board of Directors and also itsgeneral body. All FIIs are required to regis-ter with SEBI. As on March 2010, the totalnumber of registered FIIs in India was1,713 with a net cumulative investment ofUS$ 89.34 billion.

Investment by FIIs: FIIs have played asignificant role in providing liquidity to theIndian securities markets. The FII invest-ment quota in corporate and governmentdebt was increased over time. As of No-vember 30, 2010, FIIs can invest US$10billion in government debt and US$20 bil-lion in corporate debt. Since 2000–01, FIIinvestments have been continuously flow-ing in, except during 2008–09 which wit-nessed substantial outflow due to the glob-al financial crisis (Figure 2.3).

Movement in Stock Market Indices:

The stock market witnessed several cor-rections during 2000–01, leading to a sharpdecline in total market capitalisation,turnover and trading activities. From2003–04 onwards bullish sentiments pre-

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

5

2000

1800

1600

1400

1200

1000

800

600

400

200

0

1000

900

800

700

600

500

400

300

200

100

0

Num

ber

of

Issues

Am

ount M

obili

sed in R

s.

Bill

ion

1991-9

2

Number of Issues Amount Mobilised

1992-9

3

1993-9

4

1994-9

5

1995-9

6

1996-9

7

1997-9

8

1998-9

9

1999-0

0

2000-0

1

2001-0

2

2002-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007-0

8

2008-0

9

2009-1

0

FIGURE 2.1: CAPITAL RAISED FROM THE PRIMARY MARKET

TABLE 2.1: CAPITAL RAISED THROUGH PUBLIC AND RIGHTS ISSUES (` billion)

Year Public Rights TotalNumber Amount Number Amount Number Amount

vailed and the market witnessed upwardmomentum. In the next three to four years,the markets recorded a significant uptrendand the BSE SENSEX and CNX NIFTYrose from 3048.72 to 13072.10 and from978.20 to 3821.55, respectively, duringMarch 2003 to March 2007. The BSE Sen-sex and S&P CNX NIFTY culminated intheir pick of 20873.33 and 6287.85, re-spectively, in January 2008. However, thisbull run soon ended and the markets wentthrough significant corrections followingthe crisis.

The Fall of Stock Market Indices dur-

ing 2008–09: The sub-prime mortgage cri-sis that appeared as a rolling snowball in2007 turned into an avalanche in 2008,taking its toll on large investment bankslike Bear Stearns and Lehman Brothers.Due to enhanced international linkages,the cascading effect of the crisis was felt inIndia as well. Mammoth FII outflow pulled

down the indices in October 2008 andagain in February 2009. The authoritieshad to declare stimulus packages to boostgrowth and rejuvenate business activities.As a result, the market started to grow at afaster pace after 2009. At the end of2009–10, the BSE Sensex stood at17527.77 and the S&P CNX Nifty stood at5249.10 (Figure 2.4). As on March 31,2010, the number of companies listed onthe BSE were 4,975 and on the NSE 1,470.

Growth of Market Capitalisation and

Turnover: There has been a substantial in-crease in the market capitalisation of themajor two exchanges of the country. How-ever, market capitalisation has gonethrough ups and downs. In the earlieryears of this decade, there was a sharp fallin the market capitalisation of both ex-changes. From 2003–04, the downtrendwas reversed and the market value of list-ed stocks again started soaring. The market

capitalisation of the BSE increased expo-nentially by 575 per cent, from ̀ 9,128 bil-lion at the end of March 2000 to ̀ 61,656billion at the end of March 2010. Duringthe same period, the market capitalisationof the NSE also increased by 489 per cent,from ̀ 10,204 billion to ̀ 60,092 billion.The annual turnover in the cash segmentsof BSE and NSE reflected the same trend.After 2000–01, there was a sharp fall in theturnover and this trend continued for someyears. Later, the situation gradually im-proved. By the end of March 2010, the an-nual turnover of the cash segment of theBSE was ̀ 13,788 billion and that of theNSE was ̀ 41,380 billion.

Growth of Intermediation Industry:

The quantitative transformation of the In-dian securities market has happened withthe help of a growing intermediation in-dustry. While the number of brokers in-creased from 9,192 in 2000 to 9,816 in

6

10000000

8000000

6000000

-2000000

0

2000000

4000000

210000

-40000

10000

60000

110000

160000

1998-9

9

2006-0

7

2009-1

0

2008-0

9

2007-0

8

2005-0

6

2004-0

5

2003-0

4

2002-0

3

20

01

-02

2000-0

1

1999-0

0

Gross Mobilisation (L.H.S.) Net Inflow (R.H.S.)Redemption (L.H.S.)

FIGURE 2.2: RESOURCE MOBILIZATION BY MUTUAL FUNDS (` crore)

-11000

-6000

-1000

4000

9000

14000

19000

24000

29000

1995-9

6

2000-0

1

2001-0

2

1994-9

5

2009-1

0

2007-0

8

2008-0

9

1993-9

4

1992-9

3

2006-0

7

2005-0

6

2004-0

5

2003-0

4

2002-0

3

1999-0

0

1998-9

9

1997-9

8

1996-9

7

Net Investment (L.H.S.)

()

Cl

iN

I(U

SD

)

Cumulative Net Investment (R.H.S.)

87000

67000

47000

27000

7000

-13000

-33000

FIGURE 2.3: TRENDS IN FII INVESTMENTS SINCE 1993 (US$ million)

2010, that of sub-brokers increased bymore than fourteen-fold from 5,675 to75,744 during the same period signifyingthe reach and expansion of the Indian se-curities market. Supplementing this ex-pansion during the past decade, the num-ber of depository participants increasedfrom 205 to 758, the number of portfoliomanagers increased from 23 to 243, thenumber of venture capital funds increasedfrom 22 to 160 and foreign venture capitalfunds emerged as a new class of partici-pants in the market with their number in-creasing to 143 by 2010. On the otherhand, dematerialisation led to a reductionin the number of registrars and transferagents from 242 to 74 during the pastdecade.

Qualitative Aspects of MarketTransformation

Modernisation of Securities Market

Infrastructure: There has been a remark-able expansion and modernisation of in-frastructure to support the rapid growth ofthe securities market in India. The markethas transited from scream-based trading toscreen-based trading since the earlynineties, providing an electronic, screen-based, anonymous, order-driven tradingsystem for dealing in securities. The mar-ket can be accessed from anywhere in thecountry through the Internet. In order tofurther expand the reach of the market, ex-changes have started enabling tradingthough mobile telephones. Securities areno longer dealt with in physical form - theyare dematerialised and electronicallyrecorded to facilitate smooth trading andtransfer of ownership. All trades on ex-changes undergo the regulated trading,clearing and settlement processes. Theclearing house of the exchange or its sub-

sidiary clearing corporation undertakepost-trading activities like clearing and set-tlement of trades on exchanges. Theseclearing houses/ corporations act as thecounterparty to trades on exchanges andguarantee finality of settlement on thestrength of the Settlement Guarantee Fund(SGF)/ Trade Guarantee Fund (TGF). Thesettlement system has transited from ac-counting period trading settlement torolling settlement in a phased manner be-ginning on January 10, 2000 in selectedscrips to rolling settlement in all listedscrips with effect from December 31, 2001.The settlement cycle was reduced from theinitial T+5 to T+2 rolling settlement byApril 1, 2003. Apart from the introductionof book building mechanisms for public is-sues in the late nineties, several processeshave been streamlined to enhance effi-ciency and reduce the cost of the issueprocess in the primary market. One suchmeasure introduced in recent years is theprocess of subscription to initial public of-fering through the Applications Supportedby Blocked Amount (ASBA) facility. Theinvestor grievance redressal mechanismhas been overhauled by enabling onlineaccess to the redressal system to encourageretail investors to participate in the market.

Use of Technology: The Indian securi-ties markets have been at the forefront inembracing modern technology and globalbest practices. The adoption of V-SAT tech-nology extended the reach of the stock ex-changes from their trading halls to everynook and corner of the country whilescreen-based trading brought in trans-parency and fairness. India has no openoutcry system, unlike some developedcountries where this system is still fol-lowed. The National Stock Exchange of In-dia Limited (NSEIL) was the first to use

satellite-based communication technologyfor establishing connectivity. The NSE andBSE now offer access from 201 and 359cities and towns in India, respectively.

Dematerialisation: Gone are the dayswhen investors had to maintain a plethoraof documents. With the introduction of de-materialisation, which is automation ofshare ownership records in a central data-base, the problems of delays, bad deliver-ies and theft/forgery of share certificatesvanished. The depositories have set up anation-wide network with proper infra-structure to handle the securities deposit-ed or settled in dematerialised mode in theIndian stock markets. By the end of March2010, in NSDL and CDSL the number ofinvestor accounts were ̀ 105.85 lakh and` 65.86 lakh, respectively; the number ofcompanies available for dematerialisationwere 8,124 and 6,805, respectively; andthe value of dematerialised shares stood at` 56,17,842 crore and ̀ 8,38,928 crore, re-spectively. This progress happenedthrough the expansion in reach of the in-creasing number of Depository Partici-pants (DPs) which stood at 269 DPs of NS-DL and 489 DPs of CDSL by end-March2010.

Expansion and Globalisation of Indi-

an Securities Markets: India is home tomore than 4,900 domestically-listed com-panies in the BSE, making India secondonly to the US in terms of number of do-mestically-listed companies. With thechanged dynamics of global financialflows, emerging markets are attracting anincreased amount of foreign funds. In In-dia, the securities market has developed ata rapid pace. The domestic mutual fundindustry has been expanding by introduc-ing new products and has been receivingincreased allocation of the financial sav-

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

7

22000

20000

18000

16000

14000

12000

10000

8000

6000

4000

2000

6500

5500

4500

3500

2500

1500

500

SENSEX Index (L.H.S.) NIFTY Index (R.H.S.)

1/1

/20

00

1/1

/20

01

1/1

/20

02

1/1

/20

03

1/1

/20

04

1/1

/20

05

1/1

/20

06

1/1

/20

07

1/1

/20

08

1/1

/20

09

1/1

/20

10

7/1

/2000

7/1

/2001

7/1

/2002

7/1

/2003

7/1

/2004

7/1

/2005

7/1

/2006

7/1

/2007

7/1

/2008

7/1

/2009

7/1

/2010

FIGURE 2.4: TRENDS IN INDIAN INDICES

ings of domestic households. The regula-tory framework is in place for collective in-vestment schemes, domestic venture cap-ital funds and foreign venture capital in-vestors. The transformation has manifest-ed itself in the higher ranking of the Indiansecurities markets in the global arena.

Market Regulations: The SEBI Act em-powers SEBI to frame regulations to regu-late intermediaries and to ensure disclo-sures and investor protection by listedcompanies. SEBI has framed a number ofregulations for different intermediaries.Under these regulations, SEBI prescribeseligibility norms, viz., physical infrastruc-ture, professional competencies and mini-mum capital requirements for registeringintermediaries. SEBI also prescribes a codeof conduct and disclosure and compliancerequirements. SEBI monitors the activitiesof registered entities and takes penal actionif the regulations are violated. To ensurethat the perimeter of SEBI's regulations arein tune with the dynamic nature of the se-curities market, SEBI reviews its regula-tions from time to time and prescribes newregulations to regulate new activities in themarket. The regulatory framework for in-termediaries, which has been evolvingsince 1992, has stood the test of time andhas been able to ensure, by and large, qual-ity intermediation services in the market.

Economic ReformsEconomic liberalisation in India can be

traced to the late 1970s; however, full-fledged economic reforms began in July1991 when the government decided toopen the way for an International Mone-tary Fund (IMF) programme that led to theadoption of a major reform package to copewith a balance of payments crisis. As a re-sult, the foreign exchange reserves recov-ered quickly, enabling India to manage itsbalance of payments (BoP) problem. Theprocess of economic liberalisation has con-tinued till date. In this process, emphasiswas given to opening up the economy toaccess the international market and tomake way for private enterprises to takepart in market competition more freely.

The principal objective behind this re-form was to bring about a gradual shift to-wards a capitalistic system so as to achievehigh economic growth and industrialisethe nation. The internal liberalisationmeasures were based on deregulation, ini-tiation of privatisation, tax reforms, and fi-nancial sector reforms. These measures,inter alia, included the repeal of the Con-troller of Capital Issues (CCI) Act 1947, theintroduction of the SEBI Act of 1992 andthe Security Laws Amendment which gave

SEBI the legal authority to register and reg-ulate all security market intermediaries.The inception of the National Stock Ex-change (NSE) is also considered to be animportant development in the internal re-form process that helped enormous expan-sion of the stock market.

External liberalisation, on the otherhand, allowed foreign institutional in-vestors to invest in the stock markets andIndian companies to raise capital abroad.In this regard several measures were takensuch as allowing foreign direct investment(FDI) by increasing the ceiling on share offoreign capital in joint ventures, stream-lining procedures for FDI approvals, open-ing up India's equity markets to investmentby foreign institutional investors (FIIs) andpermitting Indian firms to raise capital ininternational markets by issuing GlobalDepository Receipts (GDRs) and AmericanDepository Receipts (ADRs), abolishingquantitative restrictions and reducing tar-iffs on imported goods and, last but notleast, a gradual transformation to fullerCapital Account Convertibility (FCAC).

The reforms in the financial sector andthe securities market have encouraged thecorporate sector by bringing about marketcompetition and providing easy access topublic money to finance new projects. Thesecurities market has gained enormous im-portance and has become an investmentavenue for investors.

SEBI and the Regulation ofSecurities Markets

From its inception, SEBI has endeav-oured to develop the securities marketsand simultaneously set up a benchmark inmarket regulation. While much of the ini-tial agenda in the early nineties is com-plete, the task of development and regula-tion of securities markets is an ongoingprocess. The work of investor protectionand education and development of mar-kets needs to be set in a new context peri-odically. Following is a brief review of SE-BI's achievements in the field of marketregulation in the past decade.

Streamlining Capital Raising: SEBIover time has introduced a number meas-ures aimed at enhancing efficiency and op-timising the cost of raising capital from thesecurities market. The transformation ofthe primary securities market has been onaccount of the introduction of the bookbuilding route for public issues, marginingand proportional allotment for all cate-gories of investors in book-built issues,mandatory IPO grading, qualified institu-tions placements (QIPs), fast-track issues,Applications Supported by Blocked Ac-

counts (ASBA) and significant reductionin the timeline for rights issues and bonusissues.

Reduction in Transaction Costs: Thegrowth in the categories of investors in themarket has kept pace with the types ofproducts. Transaction costs have comedown on account of the reduction in /ratio-nalisation of fees, commissions and marketimpact cost. The transaction cost chargedby depositories is the lowest in the world.Broking fees have plummeted in the pastdecade-and-a-half. The maximum broker-age chargeable by trading member in re-spect of trades in the equity cash segmentcan be up to 2.5 per cent of the contractprice, inclusive of statutory levies like se-curities transaction tax, SEBI turnover fee,service tax and stamp duty. However, theactual brokerage charged is as low as 0.10per cent, suggesting a competitive broker-age industry. Entry load has been abol-ished for investment in mutual funds.

Transparency: SEBI's regulatoryregime is primarily based on disclosuresand transparency. To make the process ofprice discovery in the primary marketsmore transparent, SEBI introduced thebook building process and mandated nec-essary disclosures in the offer documents.In the secondary markets, transparency isensured by introduction of screen-basedorder matching system which makes theprice and volume data instantly availableto an investor in the remotest corner of thecountry. To increase the accessibility of in-formation, SEBI's own activities are imme-diately put on the website, including theconsent orders, quasi-judicial orders andboard notes.

Disclosure-based Regulations: The es-tablishment of SEBI ushered disclosure-based regulation in the Indian securitiesmarket. Companies desiring to raise capi-tal from the securities market through pub-lic issues are required to disclose all mate-rial information so as to facilitate informedinvestment decision-making. This man-date applies to companies that propose tolist their securities, listed companies andall regulated entities. The legal frameworkhas often been fine-tuned to improve dis-closure norms and transparency stan-dards. The report of the Committee on Fi-nancial Sector Assessment (CFSA) has not-ed that all applicable transparency prac-tices are observed in India.

Promotion of Market Integrity: Thesurveillance, investigation and enforce-ment capability of SEBI has been strength-ened to deter violation of securities laws.To enhance the efficacy of the surveillancefunction, SEBI has put in place a compre-

8

hensive Integrated Market SurveillanceSystem (IMSS) which generates alerts aris-ing out of unusual market movements.IMSS is also being used to monitor the ac-tivities of market participants as well as toissue suitable instructions to stock ex-changes and market participants. The su-pervision and enforcement thus not onlycomplemented the fine-tuned legal frame-work but ensured better compliance.Processes have been introduced to expedi-tiously resolve cases of violations by pass-ing quasi-judicial orders, instituting legalproceedings or through the consentprocess. SEBI keeps a continuous vigil onthe activities of the stock exchanges to pro-mote an effective surveillance mechanismand also carries out inspections of the sur-veillance department of major stock ex-changes. Since 1992–93, SEBI has under-taken 1,359 investigation cases and 1,264cases investigations have been completed.During 2009–10, 71 new cases were takenup for investigation and 74 cases werecompleted.

Investor Assistance and Education:

SEBI has in place a comprehensive mech-anism to facilitate redressal of grievancesagainst intermediaries registered by it andagainst companies whose securities arelisted or proposed to be listed on stock ex-changes. Since its inception, SEBI has re-solved 25, 46,302 investor grievancesamounting to 94 per cent of the total of27,06,895 investor grievances received. Ason March 31, 2010, there were 1,60,593pending investor grievances and actionshad already been initiated in 1,22,713grievances. SEBI has taken several steps toaddress structural weaknesses in the sys-tem to eliminate the root cause of com-plaints. SEBI has evolved a procedurewhere class action suits filed by investorassociations in respect of violations will bereimbursed the cost of legal action. In-vestor education has received much atten-tion in the recent past.

Adoption of International Standards:

The legal and regulatory framework gov-erning the Indian securities market com-plies substantially with the InternationalOrganization of Securities Commission's(IOSCO) Principles of Securities Regula-tion. The assessment of IOSCO Principlesas regards regulation of the equity/corpo-rate bond market by the Committee on Fi-nancial Sector Assessment (CFSA) has re-vealed an overall significant level of com-pliance; out of 30 principles, India is fullycompliant on 20, broadly compliant on 8and partially compliant on the remaining2. SEBI has implemented a suitable KYCregime in accordance with the recommen-

dations of the Financial Action Task Force(FATF) on money laundering. In additionto its association with IOSCO, SEBI hasbeen actively co-operated with foreign reg-ulators, self-regulatory organisations, in-ternational financial institutions, interna-tional standards-setting bodies and otherinternational agencies of repute and rele-vance for the development and regulationof securities markets.

Risk Management: Various measureshave been taken to ensure a prudentialmarket structure. The establishment ofcentral counterparties, introduction ofcross-margining for all categories of in-vestors, straight-through processing, de-rivatives trading (including currency fu-tures), short selling, securities lending andborrowing, margining for institutional in-vestors in the equity cash segment, corpo-rate governance norms for listed compa-nies, know your customer (KYC) normsand minimum public float, etc., havebrought the Indian securities market at parwith the matured markets. Introduction ofrobust risk management systems have en-sured that there should be no defaults inthe system even when there are unprece-dented movements in the markets causedlargely by global factors. After the imple-mentation of these norms, activities in thesecurities market continued smoothly. Thesettlement of trades also continued at anuninterrupted pace.

Professional Intermediation: Interme-diaries bridge the gap between investorsand issuers in securities markets. There-fore, the way intermediaries deal with theirclients influences their trust and willing-ness to carry out business in the market. Inorder to enhance the quality of intermedi-ation, SEBI, apart from regulating their ac-tivities, has taken several steps to ensurethat intermediaries are adequatelyequipped, both in terms of physical infra-structure as well as professionally quali-fied staff, to discharge their responsibilitiesin a professional and cost-effective man-ner. Some of the steps by SEBI in this re-gard are SEBI's encouragement for corpo-ratisation of the brokerage industry, reviewof eligibility norms of intermediaries fromtime to time, certification of persons asso-ciated with securities markets, etc.

The key measures initiated by SEBI be-tween 2000–01 and 2009–10 are given be-low: Trading in Equity Derivatives: To pro-

vide liquidity to the market and to en-able the market to absorb larger shocks,derivatives trading were introduced. Tobegin with, trading was allowed in

June 2000 in index futures contractsbased on the S&P CNX Nifty and BSE-30 (Sensex) index at the NSE and theBSE, respectively. Trading in index op-tions, stock options and futures on in-dividual stocks commenced duringJune, July and November 2001, respec-tively.

Internet Trading: To provide added ad-vantage of convenience, transparencyand real time access to investors, Inter-net-based order entry was allowed forexecution of trades on stock exchanges.

Compulsory T+2 Rolling Settlement:

Rolling settlement was introduced on avoluntary T+5 basis in the demat seg-ment of the stock exchanges on January15, 1998 to expedite the trading andsettlement process and improve the ef-ficiency of the securities market. In2001–02, compulsory T+5 rolling set-tlement was introduced for all scripslisted and traded in any stock exchangein India. The rolling settlement cyclewas shortened from T+5 to T+3 witheffect from April 1, 2002. The clearingand settlement cycle time was furthercontracted to T+2 with effect fromApril 1, 2003 for quick settlement andlower settlement risk in the Indian cap-ital market.

Exchange Traded Derivatives Con-

tracts on Currency and Interest Rate:

To make the Indian capital marketmore efficient, transparent and worldclass, new products, namely, interestrate futures contracts (June 2003) andfutures and options contracts on sec-toral indices (August 2003) were intro-duced. FIIs and Non-Resident Indians(NRIs) were also permitted to invest inall exchange traded derivative con-tracts. Exchange-traded derivativescontracts on a notional 10-year govern-ment bond were allowed for trading.Stock brokers were allowed to trade incommodity derivatives. Based on therecommendation of the RBI–SEBIStanding Technical Committee on ex-change-traded currency futures, SEBIlaid down the framework for thelaunch of exchange-traded currencyfutures. This included eligibility normsfor existing and new exchanges andtheir clearing corporations/houses, eli-gibility criteria for members of such ex-changes/clearing corporations/ houses,product design, risk managementmeasures, surveillance mechanismsand other issues pertaining to ex-change-traded currency futures. TheNSE commenced trading in currencyfutures on August 29, 2008, the BSE

H O W H O U S E H O L D S S A V E A N D I N V E S T : E V I D E N C E F R O M N C A E R H O U S E H O L D S U R V E Y

9

commenced trading on October 1,2008 and the MCX-SX commencedtrading on October 6, 2008.

Implementation of STP: Mandatoryprocessing of all institutional trades ex-ecuted on the stock exchanges throughStraight-Through Processing (STP) wasintroduced with effect from July 1,2004. This was in continuation of theefforts made by SEBI to ensure inter-operability between STP serviceproviders through the setting up of acentralised STP hub.

Corporatisation and Demutualisation:

SEBI envisaged Corporatisation andDemutualisation (C&D) of exchanges todo away with conflicts of interest exist-ing in mutual stock exchanges whereownership, management and tradingrested with the same set of people. Inorder to expedite this, SEBI approvedand notified the C&D schemes of 19stock exchanges during 2005–06. TheNSE and OTCEI were already notifiedas corporatised and demutualisedstock exchanges vide the notificationsdated March 23, 2005 and September15, 2005, respectively.

Gold Exchange Traded Funds (GETF):

Pursuant to the announcement madeby the Finance Minister in his BudgetSpeech for 2005–06, SEBI (MutualFunds) Regulations, 1996 was amend-ed to permit mutual funds to introduceGETFs in India subject to certain in-vestment restrictions.

Dissemination of Filings: At the in-stance of SEBI, the BSE and the NSEjointly launched a common portal(www.corpfiling.co.in) on January 1,2007 to disseminate the filings madeby companies listed on these ex-changes, in terms of the listing agree-ment.

Permanent Account Number (PAN):

PAN was made mandatory for all de-mat accounts pertaining to all cate-gories including minors, trusts, foreigncorporate bodies, banks, corporates, FI-Is, and NRIs. SEBI stipulated that PANwould be the sole identification num-ber for all participants in the securitiesmarket, irrespective of the amount oftransaction with effect from July 2,2007. The objective was to strengthenthe Know Your Client (KYC) normsthrough a single identification.

Grading of IPOs: It has been mademandatory for IPOs to obtain gradingfrom at least one credit rating agencyregistered with SEBI. The grading is re-quired to be disclosed in the prospec-tus, abridged prospectus and in every

advertisement for IPOs. Short Selling and Securities Lending

and Borrowing (SLB): SEBI specifiedthe broad regulatory framework forshort selling by institutional investorsand a full-fledged securities lendingand borrowing scheme. Accordingly,relevant amendments were made toSEBI (FII) Regulations, 1995 and SEBI(Mutual Funds) Regulations, 1996, en-abling FIIs and mutual funds to partic-ipate in short selling and SLB.

Introduction of Direct Market Access:

With a view to increase liquidity, bringabout greater transparency, lower theimpact cost for large orders and reducethe risk of error associated with manu-al execution of client orders; the facili-ty of Direct Market Access (DMA) wasintroduced. This facility allows brokersto offer its clients direct access to theexchange trading system through thebroker's infrastructure without manu-al intervention by the broker.

Cross Margining across Exchange-

Traded Equity (Cash) and Exchange-

Traded Equity Derivatives (Deriva-

tives) Segments: In order to improvethe use of capital by market partici-pants, SEBI extended the facility ofcross-margining across the cash and de-rivatives segments to all categories ofmarket participants. To begin with, aspread margin of 25 per cent of the totalapplicable margin on the eligible off-setting positions is levied in the respec-tive cash and derivatives segments.

Transition from DIP Guidelines to

ICDR Regulations: SEBI (Issue of Cap-ital and Disclosure Requirements) Reg-ulations, 2009 replaced SEBI (Disclo-sure and Investor Protection) Guidelines.

Extension of Trading Hour: Exchangeswere allowed to set any trading hoursbetween 9 a.m. and 5 p.m., providedthey have in place a risk managementsystem and infrastructure commensu-rate to the trading hours.

Combating Financing of Terrorism:

During 2009–10, directions were is-sued to stock exchanges, depositoriesand all registered intermediaries tocomply with Combating Financing ofTerrorism (CFT) under the UnlawfulActivities (Prevention) Act, 1967.

Corporate Debt Market: SEBI directedthe BSE and the NSE to introduce atrade-reporting platform for corporatebonds in 2006–07. Continuing with therationalisation of disclosure norms forlisting debt issuances, the listing agree-ment for debt securities was further

simplified. All trades in corporatebonds between specified entities, viz.,mutual funds, foreign institutional in-vestors/sub-accounts, venture capitalfunds, foreign venture capital in-vestors, portfolio managers, and RBI-regulated entities as specified by theRBI had to be necessarily cleared andsettled through the National SecuritiesClearing Corporation Limited (NSCCL)or the Indian Clearing CorporationLimited (ICCL). The provisions of thiscircular apply to all corporate bondstraded Over-the-Counter (OTC) or onthe debt segment of stock exchanges onor after December 1, 2009.

Flexibility to Set Expiry Date/Day for

Equity Derivatives: Flexibility to setthe expiry date/ day for equity deriva-tive contracts was allowed to the stockexchanges.

Reforms in Mutual Funds Industry: Inorder to empower mutual funds in-vestors through transparency in pay-ment of commission and load struc-ture, entry load was abolished for allmutual fund schemes and investorswere allowed to pay commission sepa-rately to agents commensurate with theservices provided to them by the agent.In order to have parity among all class-es of unit holders, it was decided thatno distinction among unit holdersshould be made based on the amountof subscription while charging exitloads. Considering the importance ofsystems audit in the technology-drivenasset management activity, it was de-cided that mutual funds should have asystems audit conducted by an inde-pendent CISA/ CISM-qualified orequivalent auditor. In order to expandthe reach of investments in mutualfunds, units of mutual fund schemeswere permitted to be transactedthrough registered stock brokers ofrecognised stock exchanges.

Investor Protection and Education

Fund: For administration of the In-vestor Protection and Education Fundestablished by SEBI in 2007, SEBI (In-vestor Protection and Education Fund)Regulations, 2009 was notified.