29

How the new healthcare law impacts your bottom line Rhea Aguinaldo August 21, 2013 CAMEO webinar The Affordable Care Act and California Small Businesses

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | aubrey-cobb |

| View: | 213 times |

| Download: | 0 times |

How the new healthcare law impacts your bottom line

Rhea AguinaldoAugust 21, 2013CAMEO webinar

The Affordable Care Act and California Small Businesses

About Small Business MajorityAbout Small Business MajorityAbout Small Business MajorityAbout Small Business Majority

• Small business advocacy organization – founded and run by small business owners

• National–based in CA–with additional offices in Washington, DC, NY, OH, CO and MO

• Research and advocacy on issues of top importance to small businesses (<100 employees) and the self-employed

• Very focused on reducing healthcare costs over the past 6 years

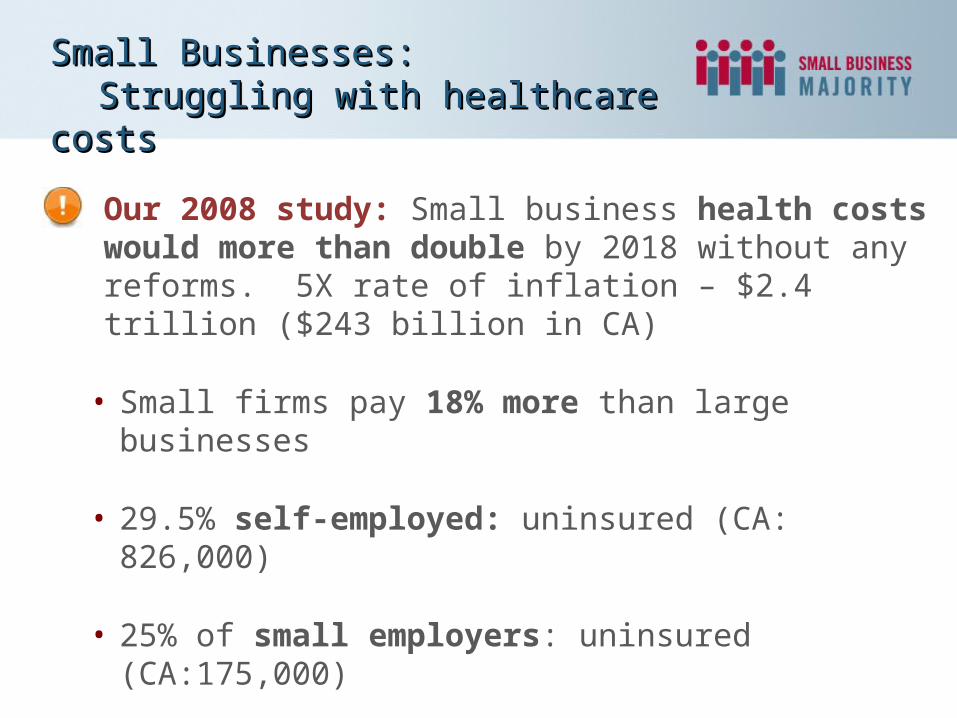

Small Businesses: Small Businesses: Struggling with healthcare costsStruggling with healthcare costs

Small Businesses: Small Businesses: Struggling with healthcare costsStruggling with healthcare costs

Our 2008 study: Small business health costs would more than double by 2018 without any reforms. 5X rate of inflation – $2.4 trillion ($243 billion in CA)

• Small firms pay 18% more than large businesses

• 29.5% self-employed: uninsured (CA: 826,000)

• 25% of small employers: uninsured (CA:175,000)

Our opinion survey: 86% of CA small businesses don’t offer because of cost; 70% of those who do offer say they are struggling to do so

Our opinion survey: 86% of CA small businesses don’t offer because of cost; 70% of those who do offer say they are struggling to do so

Small Businesses: Small Businesses: Struggling with healthcare costsStruggling with healthcare costs

Small Businesses: Small Businesses: Struggling with healthcare costsStruggling with healthcare costs

Topics for discussionTopics for discussion

• Affordable Care Act Consumer Protections

• Cost Containment Provisions

• Small Business Tax Credits

• Employer Responsibilities

• Individual Responsibility (incl. self-employed)

• Health Benefits Exchange

• Covered California

• Questions and Comments

The Affordable Care ActThe Affordable Care Act

• Builds on existing healthcare system

• Aims to rein in healthcare costs

• Upheld by U.S. Supreme Court

• Implementation primarily the responsibility of the states (small business input essential)

• Some important benefits went into effect immediately

• Others implementedfrom 2010-2014

Affordable Care Act ImprovementsAffordable Care Act Improvements

• No pre-existing conditions – Guaranteed Issue• Dependents can stay on parents plan until age 26• No gender based premiums• No lifetime caps on dollar value of services• All plans include 10 essential health benefits

1. Ambulatory patient services

6. Prescription drugs

2. Emergency services 7. Rehabilitative and habilitative services and devices

3. Hospitalization 8. Laboratory services

4. Maternity and newborn care

9. Preventive and wellness servicesand chronic disease management

5. Mental health and substance abuse disorder services, including behavioral health treatment

10.Pediatric services

Cost Containment – Cutting costs saves small businesses money

Cost Containment – Cutting costs saves small businesses money

• Exchanges leverage pooled purchasing power to lower premiums

• Ensure that more $$ go to medical care

o 80/20 Rule: Requires insurers to spend at least 80% of small business premiums on medical claims. Limits administrative costs to 20%. (Estimated $1.1B in rebates issued in 2012 nationally; 28% small business plans)

• Premium increases are now reviewed by state

• Incentives for prevention and wellness

o Grants for up to 5 years to small employers that establish new wellness programs

• Other incentives for administrative efficiency and modernization (e.g. pay for performance)

• Aims to reduce “hidden tax” of $1,000 per year

Small business tax creditsSmall business tax creditsSmall business tax creditsSmall business tax credits

• In effect now (as of tax year 2010)

o $40 billion in credits by 2019

• Which businesses & non-profits are eligible?

Fewer than 25 full-time employees

Average annual wages <$50,000

Employer pays at least 50% of the premium cost

Small business tax creditsSmall business tax credits

• Tax credits on a sliding scale:

o Up to 35% 2010–13

o Up to 50% any two years beginning in 2014

• Premium expenses: comprehensive medical coverage, incl. dental, vision, long-term care

• Tax credits do not cover premium expenses of owners or their families

• Can amend your taxes for past years

Small business tax creditsSmall business tax credits

Our report: 375,310 CA businesses are eligible (70% of all small businesses); 158,000 CA businesses eligible for the maximum credit

Our report: 375,310 CA businesses are eligible (70% of all small businesses); 158,000 CA businesses eligible for the maximum credit

• Businesses with fewer than 50 full-time workers – 96% of all businesses – are exempt from any requirement to offer insurance

Employer shared responsibilityFor larger employers - 2015Employer shared responsibilityFor larger employers - 2015

Employer Responsibility: For Larger Employers (>50 FTEs)Employer Responsibility: For Larger Employers (>50 FTEs)

• Am I above or below 50 full-time employee threshold?

– At least 50 full-time employees or combination of full-time/part-time employees equivalent to 50 full-time employees

– Full-time employees: at least 30 hours per week

– Part-time employees: add up total hours worked, divide by 30

– Seasonal employees (≤120 days per year) cannot put you over 50 FTE threshold

• Size of firm determined annually

• Fee (if any) determined monthly

Beginning January 1, 2015

•Failure to offer coverage: $2,000 per year for each full-time employee, excluding the first 30 full-time employees

o Firms only pay penalty if at least one worker qualifies for federal financial assistance in Exchange.

•Failure to offer “affordable” coverage: $3,000 per year for each full-time employee receiving federal financial assistance in exchange

o What is “affordable”?

o Employee’s required contribution exceeds 9.5% of employee income (not household);

o Plan covers less than 60% (average) of healthcare expenses

Employer Responsibility: For Larger Employers (>50 FTEs)Employer Responsibility: For Larger Employers (>50 FTEs)

• Two notices available: one for employers who do offer coverage, one for employers who do not.

• (<$500,000)

www.dol.gov/ebsa/healthreform• Employers required by the Fair Labor Standards Act (FLSA) to

notify employees of coverage options available through the Insurance Marketplace.

• Notifications to existing employees must be out by Oct 1, 2013 and all new employees beginning Oct 1 should receive this notice.

Employer Responsibility: Employee Notification

Employer Responsibility: Employee Notification

• Summary of health plan – Insurers provide employers a summary of benefits; employers must share info with workers (Sept. 2012)

• W2 reporting: informational only

o Allows workers to see how much employer is spending on health benefits

o Firms with fewer than 250 workers exempt until further notice

Employer Responsibility:W2 reporting

Employer Responsibility:W2 reporting

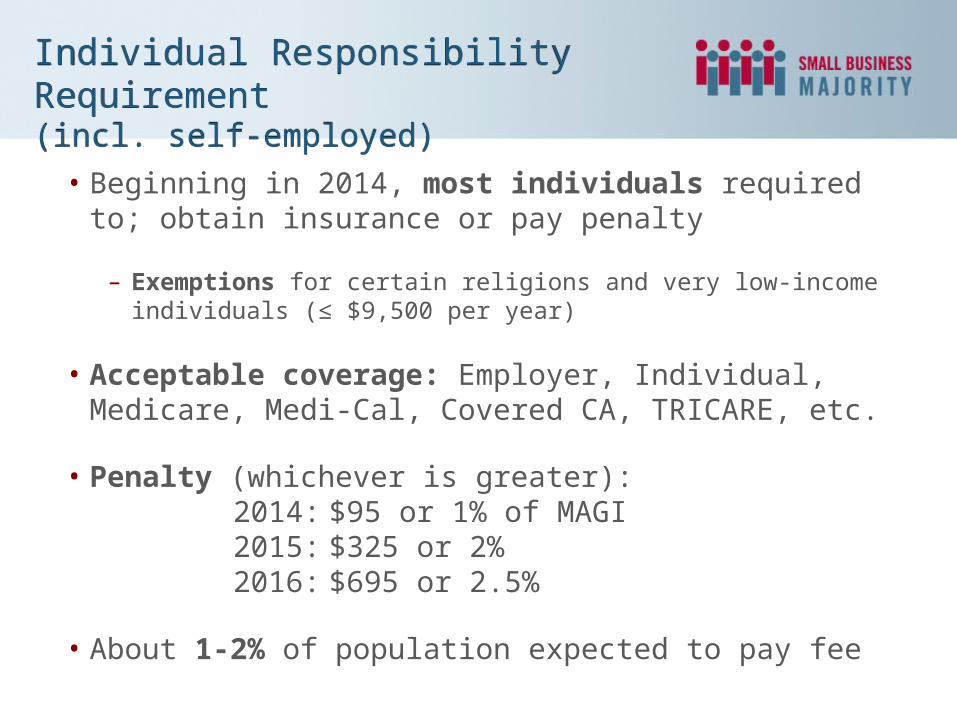

• Beginning in 2014, most individuals required to; obtain insurance or pay penalty

– Exemptions for certain religions and very low-income individuals (≤ $9,500 per year)

• Acceptable coverage: Employer, Individual, Medicare, Medi-Cal, Covered CA, TRICARE, etc.

• Penalty (whichever is greater):2014: $95 or 1% of MAGI 2015: $325 or 2% 2016: $695 or 2.5%

• About 1-2% of population expected to pay fee

Individual Responsibility Requirement(incl. self-employed)

Individual Responsibility Requirement(incl. self-employed)

• Tax Credits/Premium Assistance available to individuals (not offered min. coverage at work) with income between 138% to 400% of federal poverty level (family of 4 = $23,000 to $92,000)

– Ex: Family of 4; annual income $60,000; adults 40 yrs oldo Estimated premium: $880 per montho Tax credit: $471 per montho Family pays: $409 per month

• Not eligible for tax credits in Exchange if employer offers affordable insurance

• Open to citizens and legal immigrants

Individual Responsibility Requirement (incl. self-employed)

Individual Responsibility Requirement (incl. self-employed)

What is a Health Benefit Exchange?What is a Health Benefit Exchange?

• Two Exchanges: individuals; small businesses (2-50)• Plans begin January 1st, 2014 • Open enrollment: October 1st, 2013

• Voluntary • Members of Congress and staff required to use Exchange

• Exchanges designed by states–or by federal gov’t if a state so chooses

• State-based exchanges mean increased flexibility and more input from small businesses and other stakeholders

• Not a new concept - Business groups, non-profits and state gov’ts already run similar programs in CA, CT, MA, NY, UT

What is a Health Benefit Exchange?What is a Health Benefit Exchange?

One-stop shop web portal

Small business Health Options Program

INSURANCE PLANS

EXCHANGEChoice

ComparisonBilling

Tax Credits

SMALL BUSINESSES

• Marketplace to buy name brand commercial insurance policies

• Compare plans for information about price, quality and service

• Plans organized by metal tiers: bronze, silver, gold, platinum

• Calculator to compare costs across plan options

• Streamlined billing process

Covered California—California’s Health Benefit Exchange

Covered California—California’s Health Benefit Exchange

Covered California• First in the nation. Enacted in 2010 –

Bipartisan effort• Governed by independent public board • Hold dozens of public board meetings • Executive Director is a former business leader;

hiring more staff now• Received federal $$ for planning; Exchange self-

funding by 2015; no state dollars spent• Stakeholder advisory panels providing input

from small business owners and business organizations

Covered California—Key SHOP Decisions

Covered California—Key SHOP Decisions

• Small Business Health Options Program (SHOP) for businesses with 2-50 employees

• Active purchaser power means rates are negotiated on your behalf.

• Carriers in individual Exchange generally must also submit bid for SHOP

• Employee Choice: Employer selects “tier” of coverage; worker selects insurer; employer receives one bill

• Certified agents can sell Exchange products; will be paid market commission rates.

• HR Services: COBRA administration, HSAs, wellness plans, etc.

• Public-private partnership: Administrative management of SHOP by private-sector vendor

Covered California—2014 Individual Covered California—2014 Individual Providers (incl. self-employed)Providers (incl. self-employed)

Covered California—Covered California—2014 SHOP Providers2014 SHOP Providers

Covered California—Covered California—2014 Sample SHOP Rates2014 Sample SHOP Rates

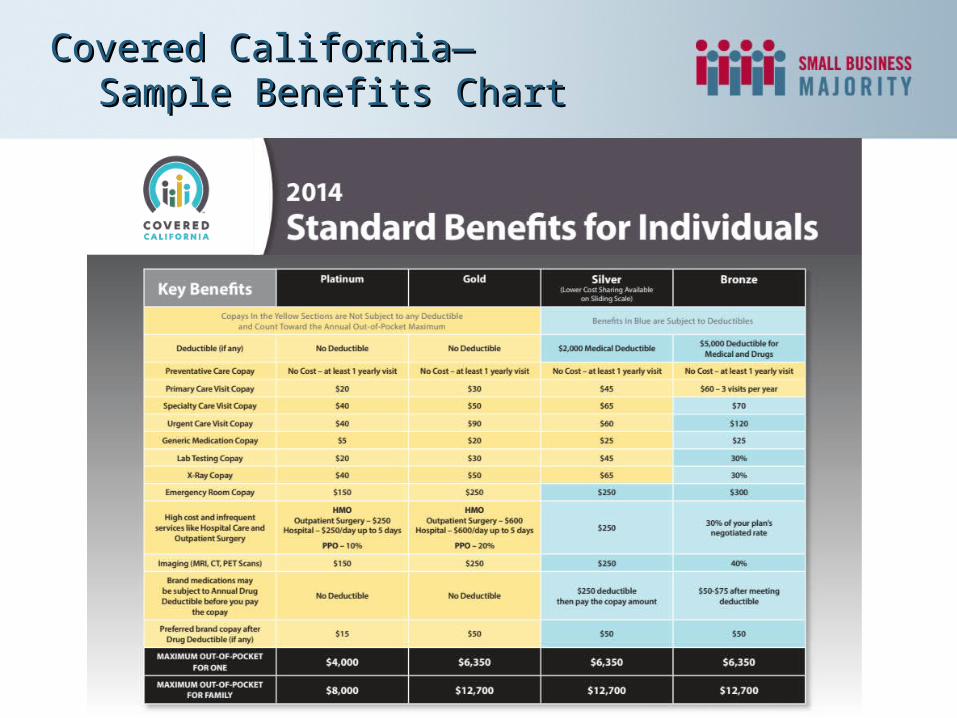

Covered California—Covered California—Sample Benefits ChartSample Benefits Chart

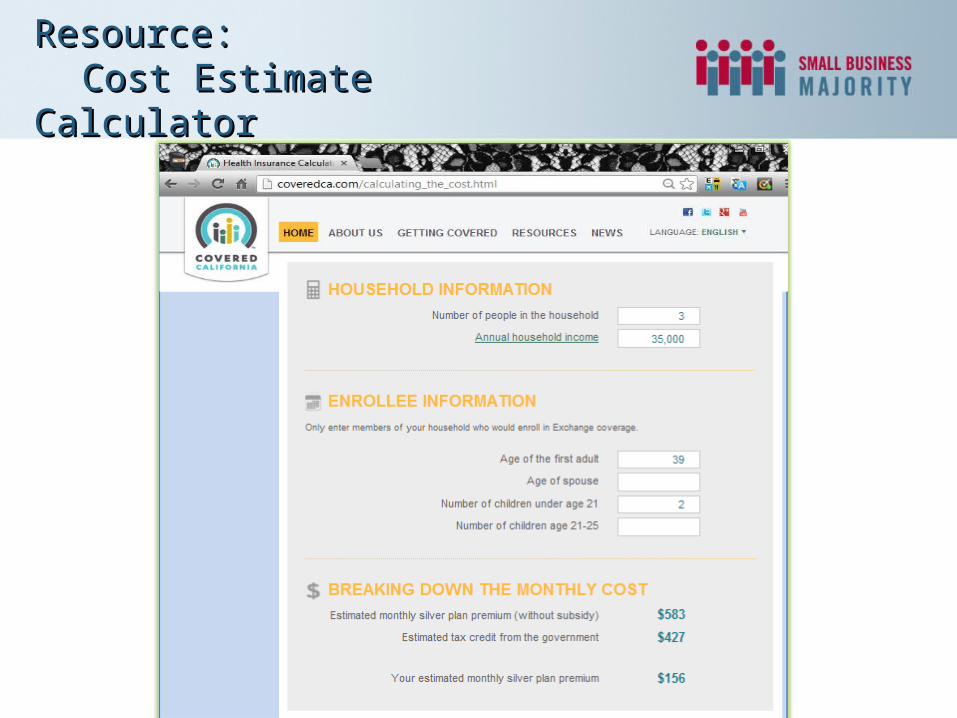

Resource:Resource:Cost Estimate CalculatorCost Estimate Calculator

Resource:Resource:SBM Health Coverage GuideSBM Health Coverage Guide

• Objective resource to navigate the new healthcare system

• Step-by-step guide if employers decide to offer coverage, alternative healthcare options if you don’t

• Tools like the Small Business Tax Credit calculator and action plan checklist

www.HealthCoverageGuide.org

For more informationFor more information

• SBM Website: www.SmallBusinessMajority.org– Detailed FAQ & Summary

– Tax Credit Calculator

• Covered California: www.CoveredCA.com

• CA Health Benefits Exchange:www.healthcare.ca.gov

• Healthcare Coverage Guide: www.HealthCoverageGuide.org

• Health Law Guide for Business: www.HealthLawGuideForBusiness.org

Rhea Aguinaldo

Northern CA Outreach Manager

Direct: (415) 654-4846

Contact Information

Connect with us!

@SmlBizMajority Small Business Majority

Ways to Get Involved with SBM:

• Receive a monthly newsletter

• Share your story for media requests

• Letters to the editor/Op-eds

• State events/Roundtables

• Webinars for business organizations