21

Joe Debtor: Marginalized by Debt 2015 Study of Insolvent Debtors www.hoyes.com

| Date post: | 02-Aug-2015 |

| Category: |

Economy & Finance |

| Upload: | hoyes-michalos |

| View: | 2,112 times |

| Download: | 2 times |

Joe Debtor: Marginalized by

Debt2015 Study of

Insolvent Debtors

www.hoyes.com

Table of ContentsWhy We Conduct Our Study

How We Gather Information

Causes of Insolvency in Canada

Meet Joe Debtor

At-Risk Groups for Filing Insolvency

Insolvent Senior (60+) Debtor Profile

Insolvent Student Debtor Profile

Insolvent Lone Parent Debtor Profile

What it Means for Canadians

Bankruptcy is Not Your Only Option

2

3

4

5

6

7

8

1215

1819

• Our Joe Debtor report has been published every two years, for the past eight years.

• We hope to inform the public about personal finance trends and to identify individuals at-risk for filing insolvency.

• The statistics collected in our study help us to better understand our clients so that we can offer advice that will benefit their unique situation.

3

Why We Conduct Our Study

• As required by law, Hoyes Michalos gathers information about each person that files with us, including: – income, family size, gender, age, assets and debts.

• Our current study is a review of almost 6,000 personal insolvencies between January, 2013 to December, 2014.

4

How We Gather Information

Causes of Insolvency in Canada

5

Throughout Canada, just over 118,000 individuals filed a consumer proposal or personal bankruptcy in 2014.1

The top reasons for financial difficulties include:

Cause of Financial Difficulty2 Rate

Overextension of credit, financial mismanagement and unexpected expenses

55%

Job related (unemployment, layoff, reduction in pay)

37%

Marital or relationship breakdown 19%

Illness, injury and health related problems 15%

1. Office of the Superintendent of Bankruptcy Canada, Insolvency Statistics in Canada

2. Tabulated from the reasons given by the debtors on the Statement of Affairs, when asked to give reasons for their financial difficulties. The numbers do not add to 100%

since some debtors give more than one cause for their insolvency.

Meet Joe Debtor

6

Contrary to popular belief, the average insolvent debtor is not unlike the average Canadian. Joe Debtor is:

• 44 years old • Male• Employed• Married with at least one child

Joe’s Debt Levels

Type of Debt Amount of Debt

Unsecured Debt $56,545

Mortgage Debt $197,137

Personal Loan Debt $19,266

Credit Card Debt $20,776

Tax Debt $9,114

Student Loan Debt $1,849

At-Risk Groups for Filing Insolvency

7

We’ve identified three at-risk groups:

1. Seniors2. Students3. Lone Parents

For each of these at-risk groups, unique factors push them further into debt.

We’ll take a look at each profile to determine specific causes for their high debt levels and offer solutions for dealing with debt.

8

Insolvent Senior (60+) Debtor Profile

• Seniors account for 10% of all files included in our study.

• Average Unsecured Debt: $69,031

When Compared to Other At-Risk Groups:

Highest Credit Card Debt at $33,355

Highest Tax Debt: $12,571

Highest Debt-to-Income Ratio: 260%

Highest Payday Loan Debt: $3,693 Carrying 3.7 payday loans on average

9

Senior Debtors on a Fixed Income

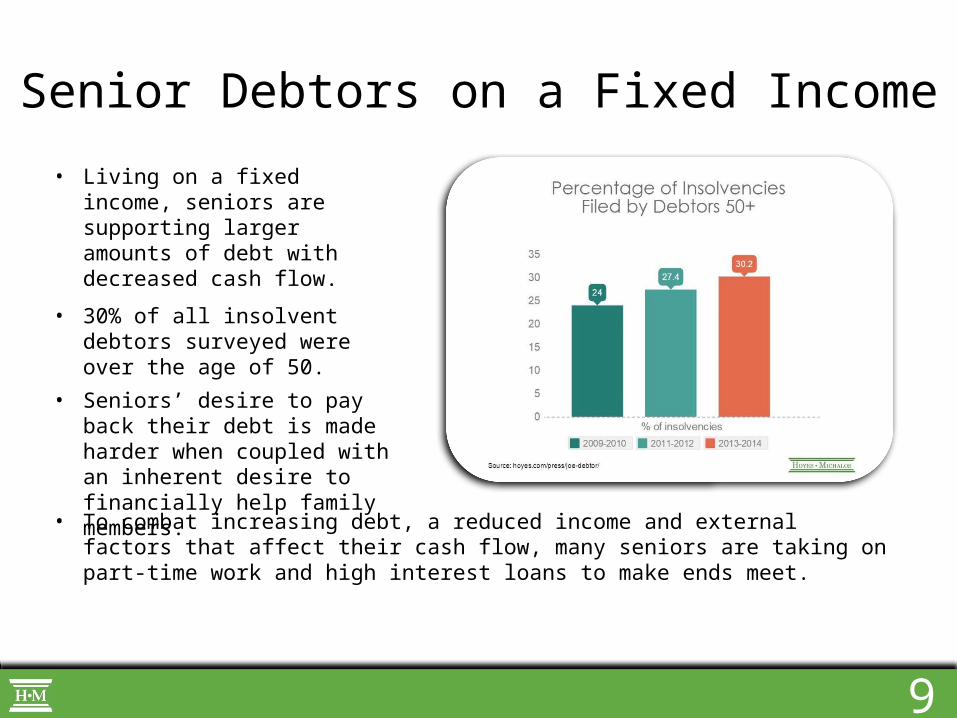

• Living on a fixed income, seniors are supporting larger amounts of debt with decreased cash flow.

• 30% of all insolvent debtors surveyed were over the age of 50.

• Seniors’ desire to pay back their debt is made harder when coupled with an inherent desire to financially help family members.

• To combat increasing debt, a reduced income and external factors that affect their cash flow, many seniors are taking on part-time work and high interest loans to make ends meet.

10

Senior Debtors Turning to Payday Loans

• With the highest unsecured debt load of all identified at-risk groups, averaging $68,677, seniors are turning to high interest loans in an attempt to pay down their debt.

• We found that 1 in 10 seniors (9%) carried at least one payday loan, but the average insolvent senior had 3.7 outstanding loans at the time of insolvency.

• Average payday loan debt: $3,693 (equal to 167% of their income)

11

Senior Debtor Solutions

1. Pre-retirees facing debt should review their options to eliminate that debt before they retire and shift to a lower fixed income.

2. Avoid cashing out savings plans like RRSPs that will be taxed upon withdrawal. If you’re struggling to pay off your debt and need professional help, laws in Ontario ensure that you keep your retirement savings. Learn more here.

3. Although you may want to help your children or grandchildren with their financial difficulties, it’s important that you deal with your own debts first so that you don’t solve one problem while making another far worse.

12

Insolvent Student Debtor Profile

• Student debtors account for 13.4% of those included in our study.• 60% of that demographic

are female.

• Average Student Loan Debt: $13,818

Jane Student Vs. Joe Student

Jane student owes $14,748 19% more than Joe Student

Jane and Joe Student earn a similar salary.

Joe Student is 91% employed compared to 83% for Jane Student.

13

Student Debtor More Likely to be Female

• 13% of all clients surveyed in the study had student loan debt. Of those clients, 6 in 10 (60 %) were female.

• Women are more likely to be out of work for factors such as maternity leave, disability and unemployment, making paying of student loan debt even harder.

• For the average female student debtor, student loans were listed as the primary financial problem leading to their insolvency.

14

Student Debtor Solutions

Be Pro-active: • Avoid using credit cards as a source of cash flow. Piling

debt on top of student debt is not the answer.• Take advantage of government repayment assistance

programs and negotiate new payment arrangements to help manage your finances once out of school.

• Create a budget and a timeline for dealing with your student loan debt.

Get Professional Help:• If student debt is affecting your debt levels, seeking help

from a Trustee in Bankruptcy might be the right choice.• The law states that once you have been out of school for

seven years or longer (The 7 Year Rule), student loan debt is dischargeable in a bankruptcy and consumer proposal.

15

Insolvent Lone Parent Debtor Profile

• Lone Parents account for 18% of all files in our study.• 75% are female.

• Average Unsecured Debt: $52,928

Lone Parent Debtors Vs. Joe Debtor

Average family size: 2.7 Joe Debtor’s family size: 2.2

86% are employed, but household income is 4% below Joe Debtor’s.

Less overall debt ($52,928 vs. $56,545), but struggle with student loans (19% vs. 13%), car loans (40% vs. 37%) and accounts in collection.

16

Lone Parent Debtors Struggling with the Cost of Living

• 1 in 5 debtors listed marital issues as cause of debt problems.

• 75% of lone parents are female and more likely to be off work for things like maternity leave or family sick leave.

• Lone parents are more likely to borrow to pay for ordinary costs such as car loan debt, mortgage debt and student loan debt.

“[Lone parents] are borrowing to live” – Doug Hoyes, Co-Founder Hoyes, Michalos & Associates

17

Lone Parent Debtor Solutions• Assess your income and expenses each month.

Use this information to create a budget.

• Lone parents are more likely to carry debt on necessary expenses (like a vehicle to get to work or a house). Review the cost of these items and find out whether changes can be made; such as trading in for a smaller/older car, downsizing your home or deciding to rent.

• Avoid using credit for every day expenses like groceries. It’s better to budget for these expenses and pay with cash or debit so that you’re using funds that you physically have in your account. The perception of free money can be enticing, but it comes with high interest.

• Finally, if your debt has become unmanageable, it’s time to seek help from a professional. They can review all of your options and come up with a solution that will work for you and your family.

18

What it Means for Canadians

• Canadians are not worried about high debt levels because interest rates are low, making the cost to carry debt more affordable.

• For those not overextend and not reliant on high cost credit options, low interest rates make debt manageable and explains the significant reduction in the overall amount of insolvencies filed since 2009.

• However, for those groups that we have identified from our study as at-risk for filing insolvency, they tend to be caught in a cycle of debt from which it is difficult to escape.

• The most worrisome trend that our study revealed is the use of high interest payday and quick cash loans by all of our at-risk groups. This pattern suggests that debt has become a survival tool for many Canadians feeling like they have no other option.

19

Bankruptcy is Not Your Only Option

• For those who are in need of professional help, you have options.

• Not only did our study identify at-risk groups for filing insolvency, but it also revealed that more Canadians are choosing to file consumer proposals as an alternative to bankruptcy.

• In our study, proposals accounted for 55% of insolvencies, while bankruptcies made up 45%.

Worrying about money and debts has a devastating effect on individuals and families, alike.

Recognizing the need for help and talking to a reputable professional, such as a trustee in bankruptcy (like Hoyes Michalos) for advice, is the first step toward eliminating overwhelming debt.

20

The Solution to Problem Debt!

Read the full Joe Debtor report

You have options.We can help.