52

HR Balance Sheet Do you have one ? If not, can you build one ? Ramakrishna Krovvidi, Senior Vice President – OD, du. Supported by Mahesh, Senior Director – Total Rewards, du

HR Balance Sheet

Do you have one ? If not, can you build one ?

Ramakrishna Krovvidi, Senior Vice President – OD, du.Supported by Mahesh, Senior Director – Total Rewards, du

Pay‐for‐Performance ?

What can’t be measured can’t be managed!!

Then……

Are we really managing well our Human Assets??

Pay‐for‐Performance ?

Pay‐for‐Performance ? Agenda

• HR Effectiveness

• Predictive Organization Performance

• HR Balance Sheet

Pay‐for‐Performance ? Key Topics

• HR Effectiveness

• Predictive Organization Performance

• HR Balance Sheet

Pay‐for‐Performance ?

• Does your HR Head report to CEO?

Structural Requirements to be effective HR ?

• How much time your HR head spends with CEO and on what topics?

• Is your HR Head at same job level and pay as of any Business UnitHead reporting to CEO?

• Does your HR Head interact with Board/Remco?

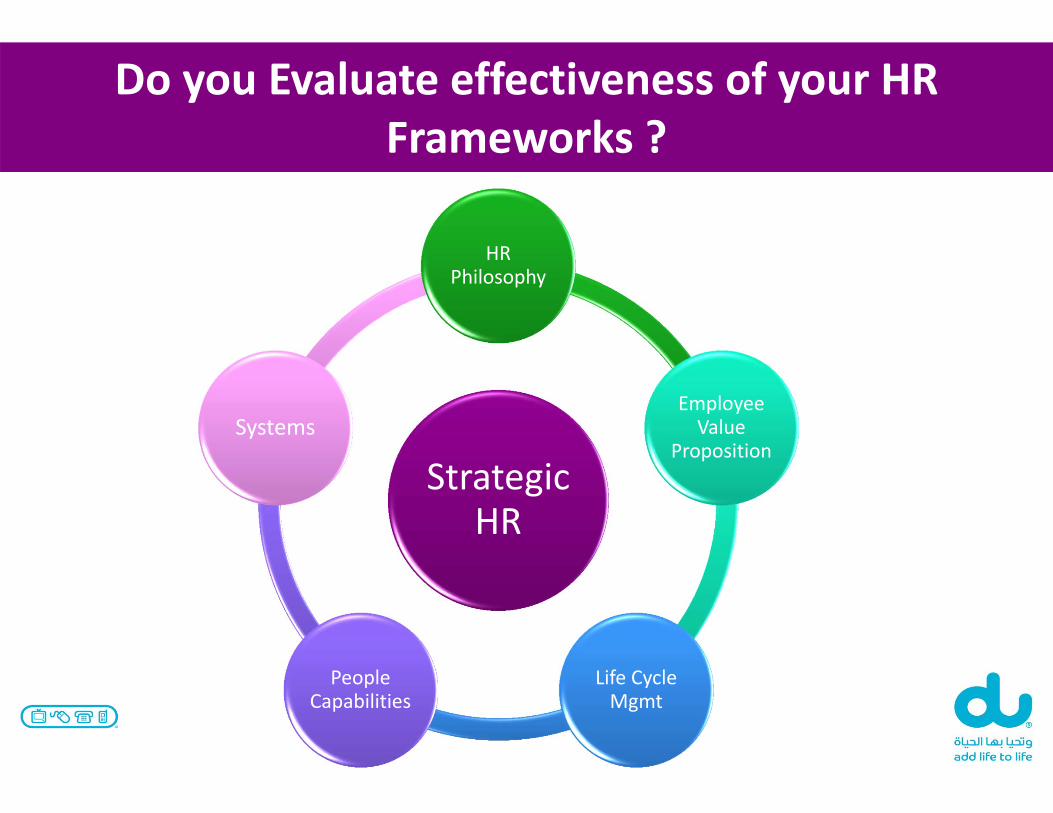

Pay‐for‐Performance ?Do you Evaluate effectiveness of your HR

Frameworks ?

Strategic HR

HR Philosophy

Employee Value

Proposition

Life Cycle Mgmt

People Capabilities

Systems

Pay‐for‐Performance ?Customer Centric Measures to Focus on…

• Employee Engagement Score

• Attrition Rate

• L&D ROI

• End to End cycle times

• Critical Roles Analysis & Succession Identification

• Growth Opportunities per Person

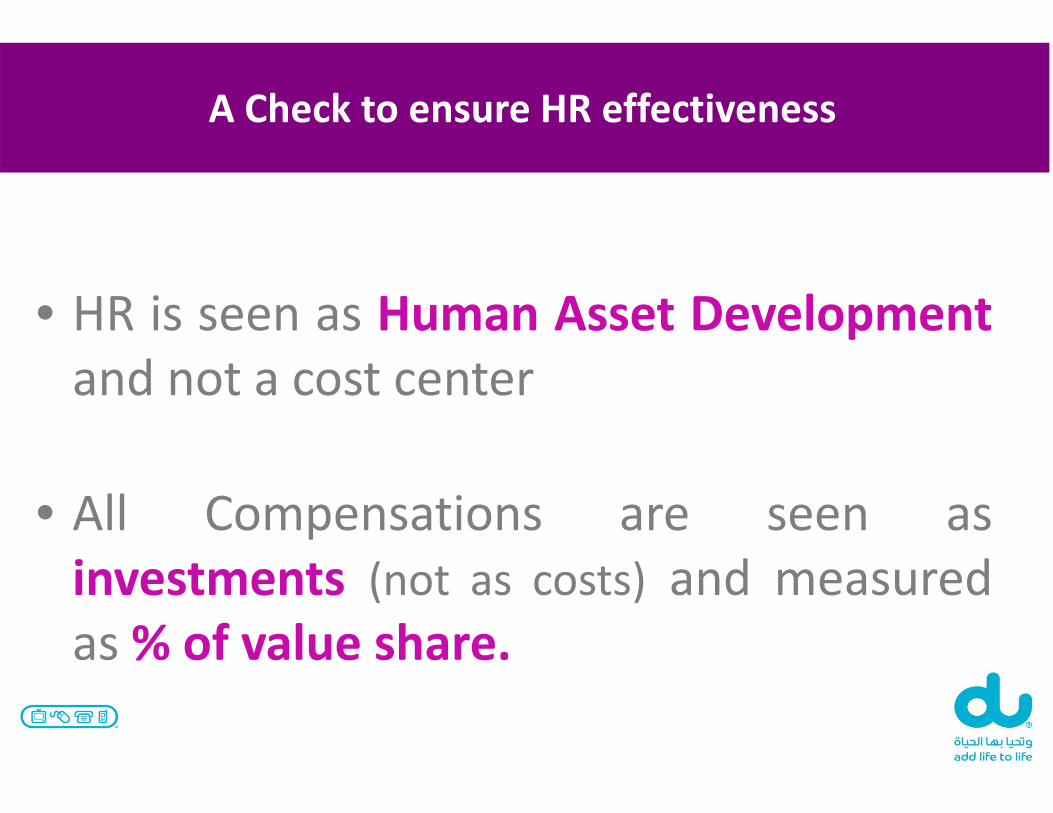

Pay‐for‐Performance ?A Check to ensure HR effectiveness

• HR is seen as Human Asset Developmentand not a cost center

• All Compensations are seen asinvestments (not as costs) and measuredas % of value share.

Pay‐for‐Performance ?BSC of Strategic HR’s, always ensures the balance

Less of More of

Pay‐for‐Performance ?

Pay‐for‐Performance ? Key Topics

• HR Effectiveness

• Predictive Organization Performance

• HR Balance Sheet

Pay‐for‐Performance ?Organization Architecture

Organization Architecture

Shareholding

Strategy

Structure & Sizing

Systems & Processes

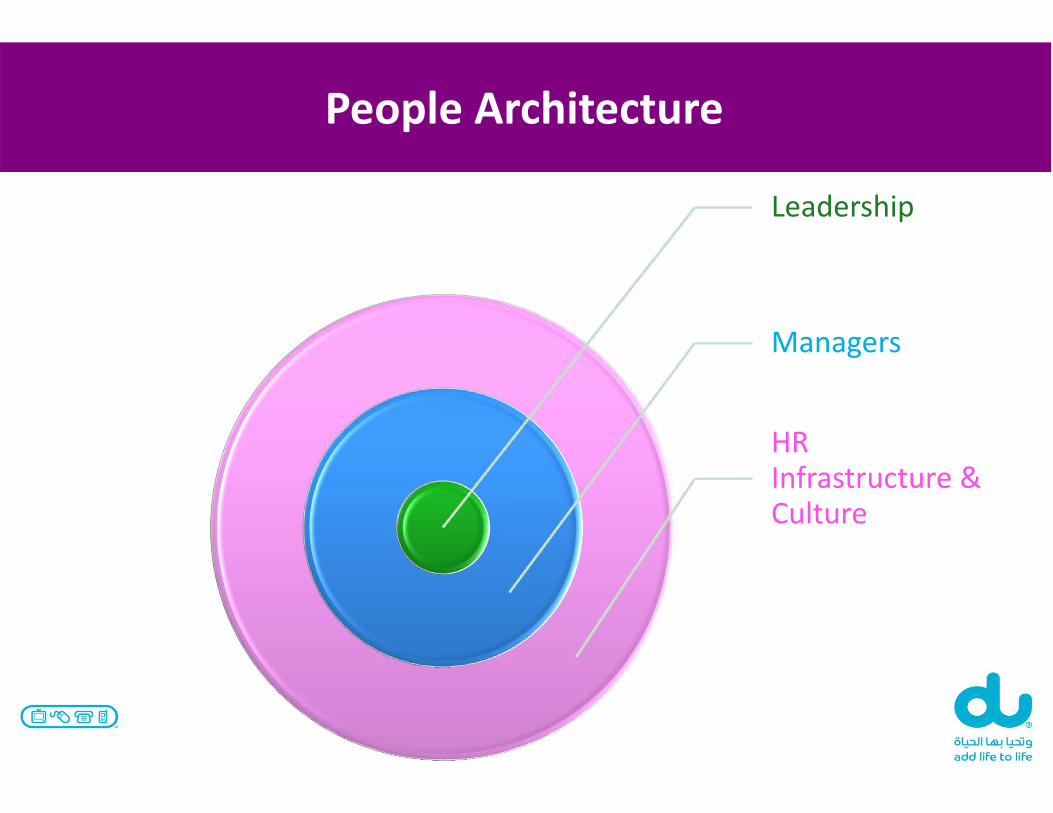

Pay‐for‐Performance ?People Architecture

Leadership

Managers

HR Infrastructure & Culture

Pay‐for‐Performance ?

Pay‐for‐Performance ?Understand your Organization’s Unique Performance Model

Organization Performance

Organization Architecture

People Architecture= X

+‐Environment

impact

Pay‐for‐Performance ? Key Topics

• HR Effectiveness

• Predictive Organization Performance

• HR Balance Sheet

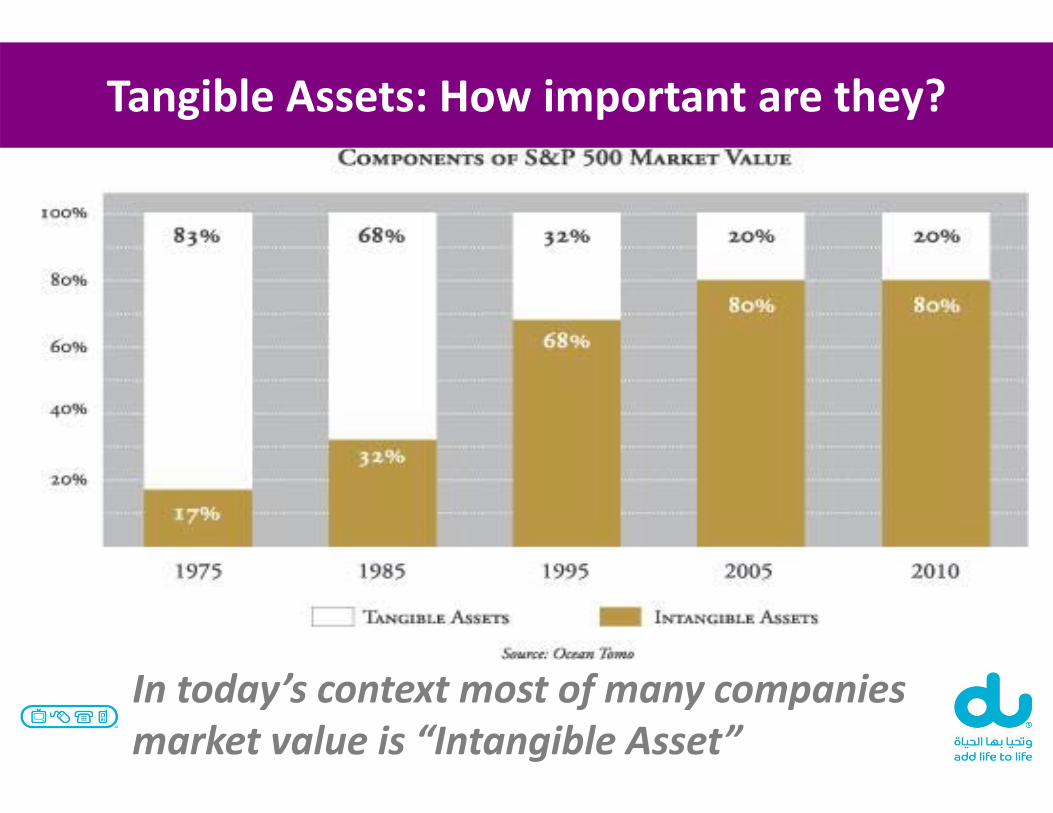

Pay‐for‐Performance ?Tangible Assets: How important are they?

In today’s context most of many companies market value is “Intangible Asset”

Pay‐for‐Performance ?Before we evaluate Human Capital….

If people are most important “Asset”….

Where are they on your Financial Statements?

• Expense side in Income statement!

• Liabilities (pensions..) in Balance sheet!!

Pay‐for‐Performance ?Before we evaluate Human Capital….

One Should exercise caution of the following:• Be clear of the “purpose”

• There is no right or wrong method but some principles prevail

• Some of the Accounting principles might not be valid in Human Asset Valuation

• Not Making it too complex

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation PrincipleOlder the Asset = Lower the book value

Always true in Accounting

Newer the Asset = Higher the book value

Generally experienced employees value is higher than fresh recruits…

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation Principle

5 $ note = Each note worth the same

Always true in Financial Accounting

Is value of each employee the same?…..

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation Principle

10 Employees Leaving Company = Headcount & cost less by 10 heads

Always true in Financial Accounting

What if these 10 employees are the most critical talent?…..

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation Principle4 + 4 = 8 Always true in Mathematics

& Accounting4 ‐ 4 = 0

Does this hold true in the context of Human Capital Dynamics?? (team dynamics, multiplier effect, environment & culture impact!)

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation PrincipleNon Performing Asset = Write‐off by same value

Always true in Accounting

DISENGAGED employee destroys value by many folds… also cost of disengagement is not linear…

Pay‐for‐Performance ?Some Complexity….How does the equation work?

Equation PrincipleFuture Value of Asset = Apportioned @rate of interest or cost of capital

Always true in Accounting

Human POTENTIAL is unlimited…….also INNOVATION breakthrough can enhance value exponentially…..

Pay‐for‐Performance ?Few Models for HC Valuation in Practice

• Historical Cost

• Replacement Cost

• Opportunity Cost

• The Lev‐Schwartz (PV of Future Earnings) Method

Pay‐for‐Performance ?Few Models for HC Valuation in Practice

Historical Cost

• All costs related to Acquiring, T&D and capitalized and

amortized

Major Limitations: Doesn’t take into effect value

created, not all costs of employee are considered (salaries!)

Pay‐for‐Performance ?Few Models for HC Valuation in Practice

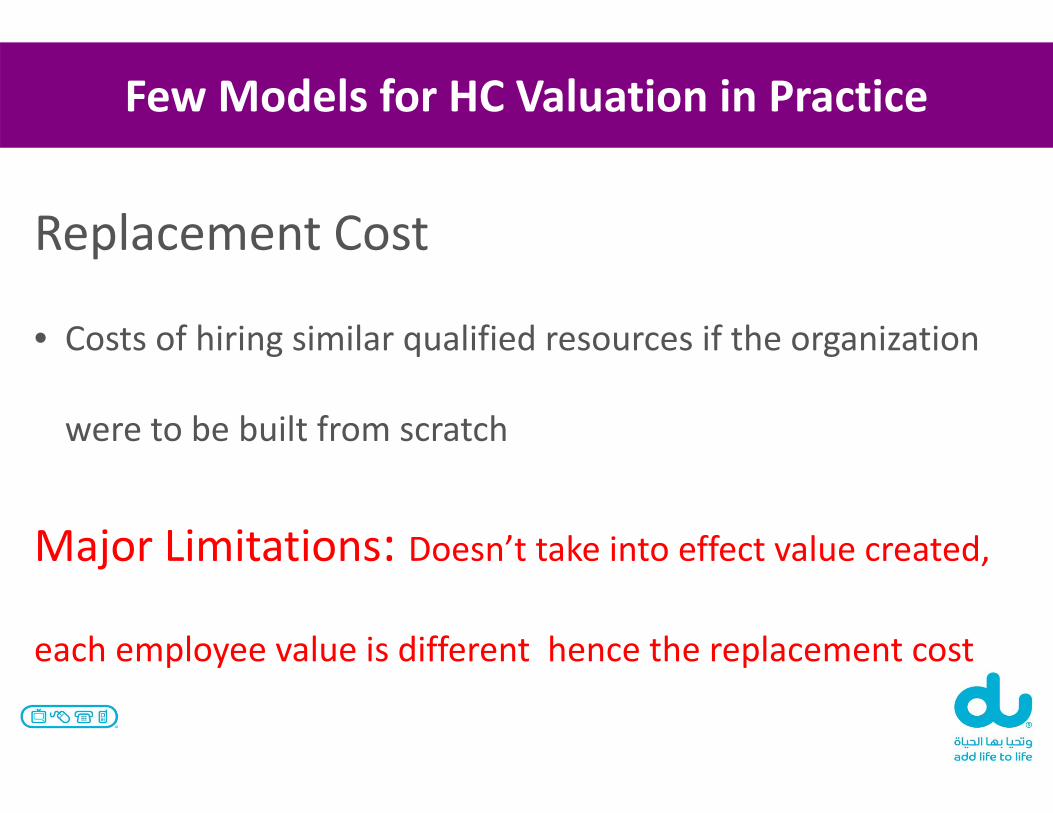

Replacement Cost

• Costs of hiring similar qualified resources if the organization

were to be built from scratch

Major Limitations: Doesn’t take into effect value created,

each employee value is different hence the replacement cost

Pay‐for‐Performance ?Few Models for HC Valuation in Practice

Opportunity Cost

• Divisional heads bidding for the services of various people

they need

Major Limitations: value of a person on a particular job is

different than another job in other division, Management costs

Pay‐for‐Performance ?Few Models for HC Valuation in Practice

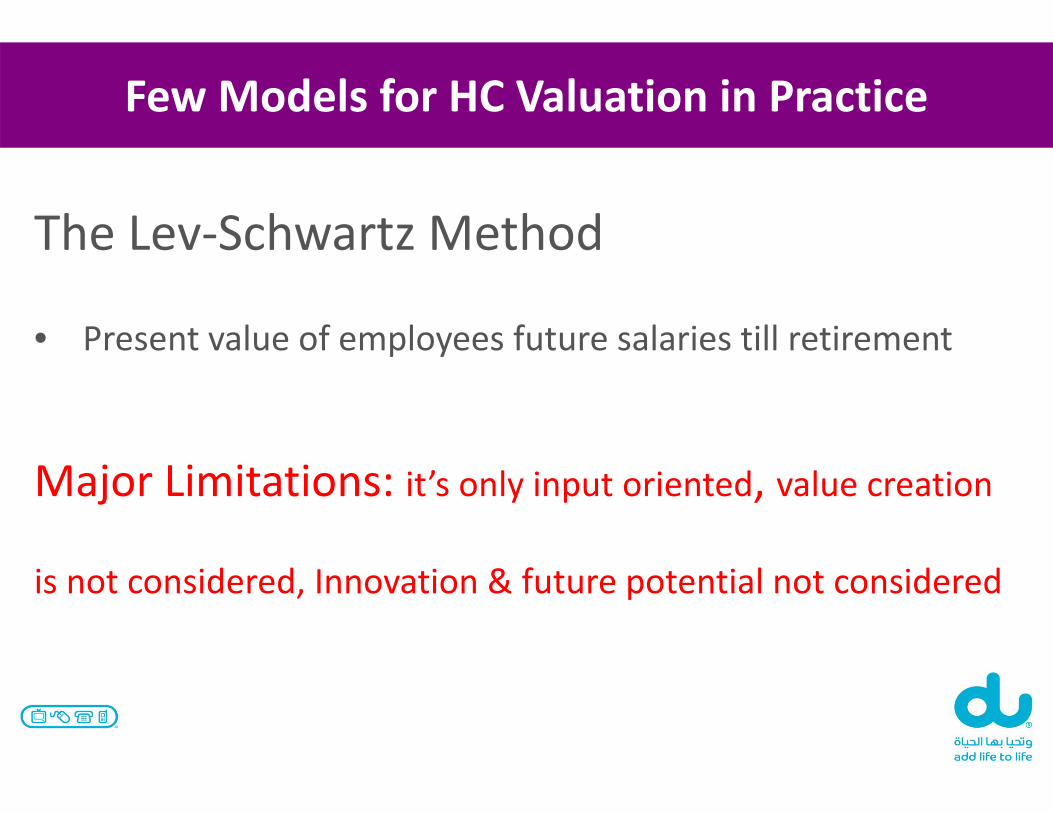

The Lev‐Schwartz Method

• Present value of employees future salaries till retirement

Major Limitations: it’s only input oriented, value creation

is not considered, Innovation & future potential not considered

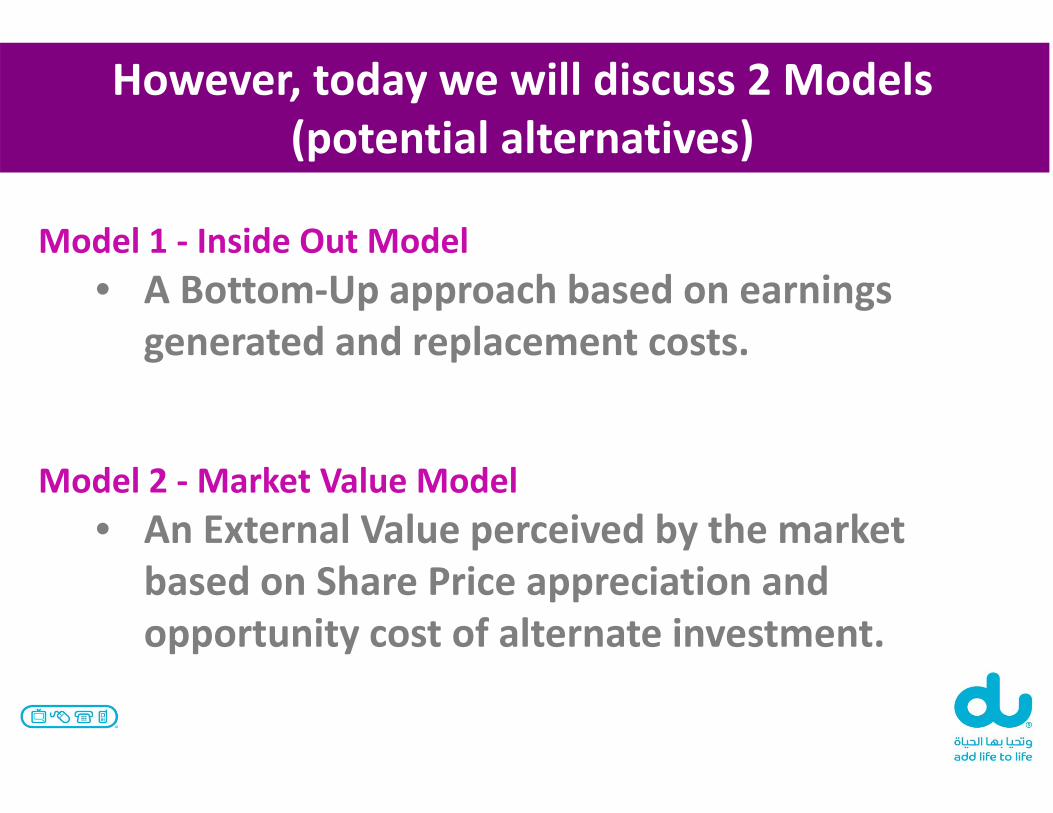

Pay‐for‐Performance ?However, today we will discuss 2 Models

(potential alternatives)

Model 1 ‐ Inside Out Model• A Bottom‐Up approach based on earnings

generated and replacement costs.

Model 2 ‐Market Value Model• An External Value perceived by the market

based on Share Price appreciation and opportunity cost of alternate investment.

Model 1 (Inside Out Model)

33

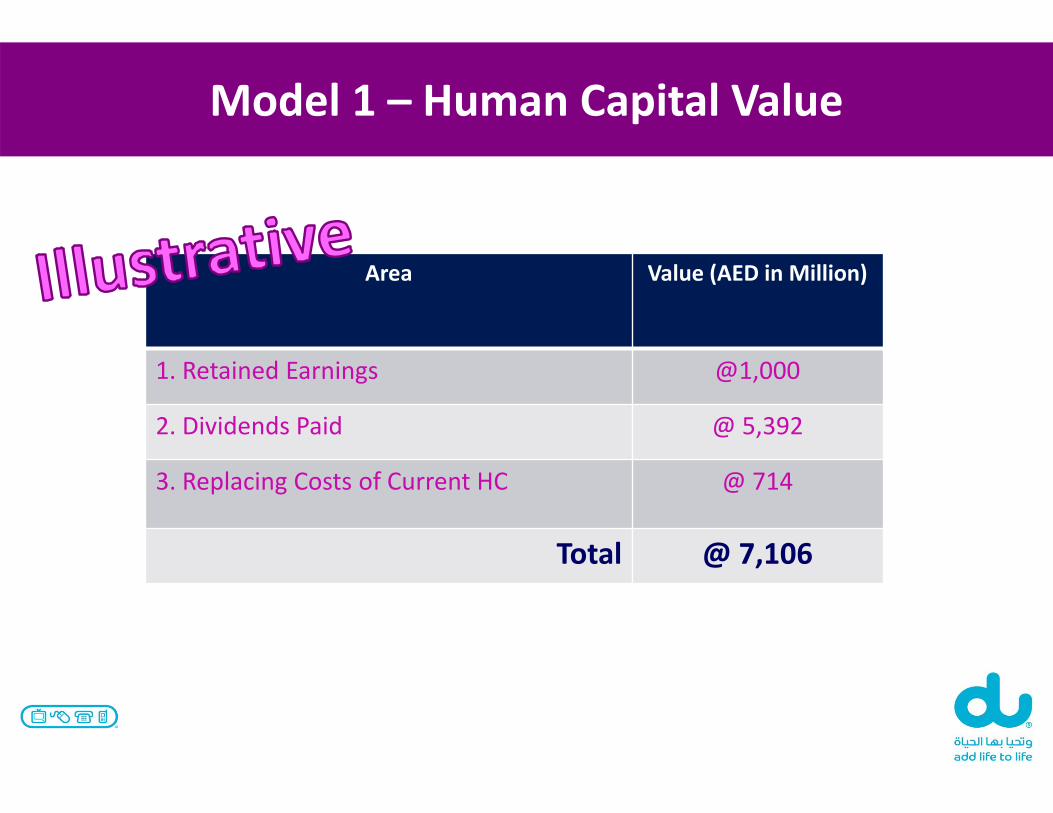

Pay‐for‐Performance ?Model 1 – Human Capital Value

Area Value (AED in Million)

1. Retained Earnings

2. Dividends Paid

3. Replacing Costs of Current HC

Total Human Capital Value = 1+2+3

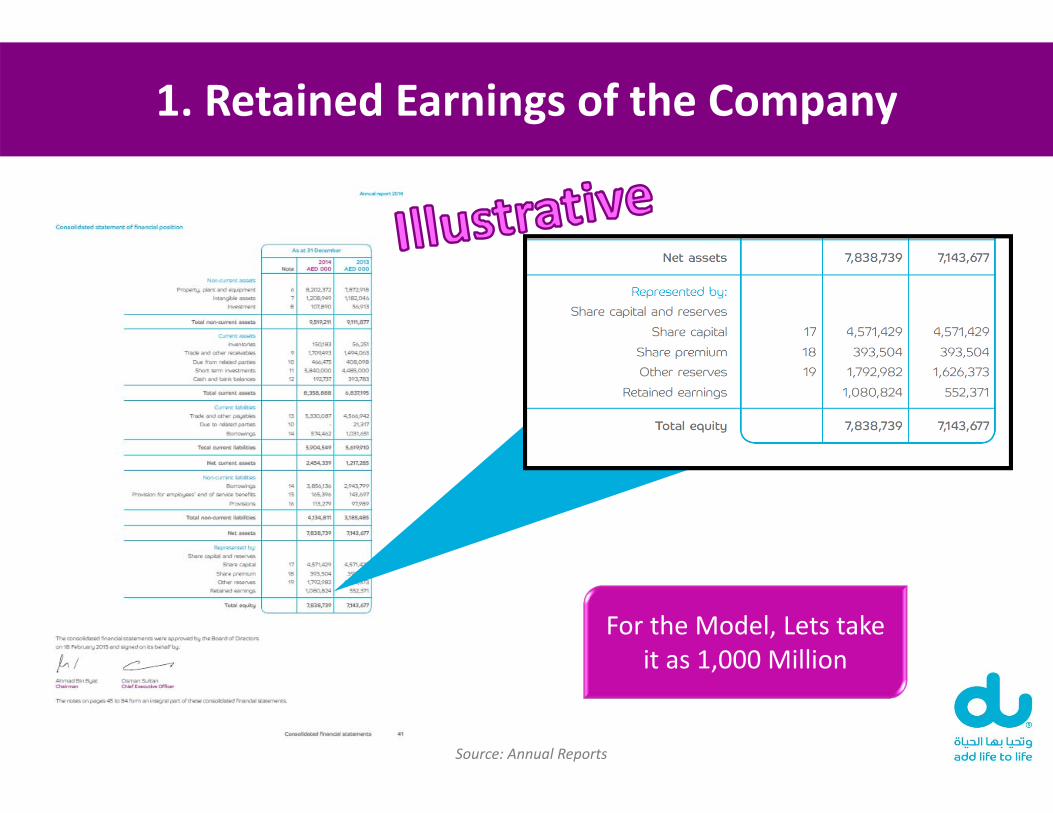

Pay‐for‐Performance ?1. Retained Earnings of the Company

For the Model, Lets take it as 1,000 Million

Source: Annual Reports

Pay‐for‐Performance ?2. Dividends Paid till date

Year Dividend (AED 000)

2011 @ 685

2012 @ 1,371

2013 @ 1,874

2014 @ 1,462

Total @5,392

Source: Annual Reports

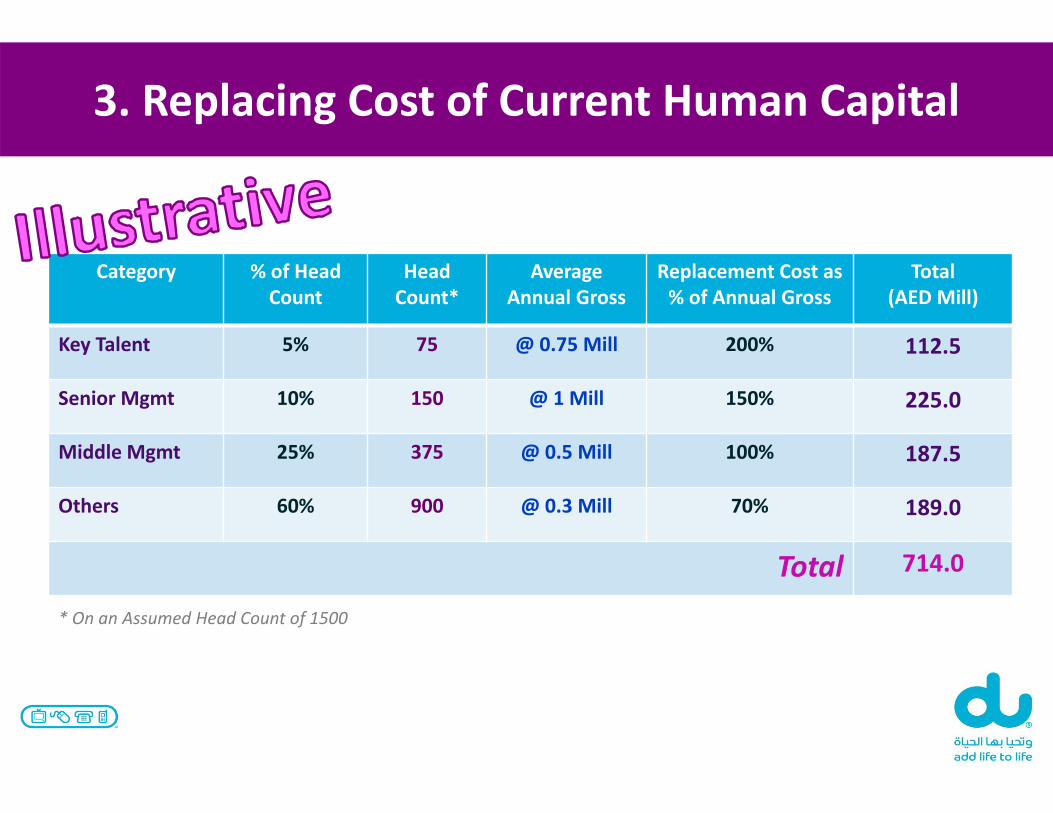

Pay‐for‐Performance ?3. Replacing Cost of Current Human Capital

Category % of Head Count

HeadCount*

Average Annual Gross

Replacement Cost as % of Annual Gross

Total(AED Mill)

Key Talent 5% 75 @ 0.75 Mill 200% 112.5

Senior Mgmt 10% 150 @ 1 Mill 150% 225.0

Middle Mgmt 25% 375 @ 0.5 Mill 100% 187.5

Others 60% 900 @ 0.3 Mill 70% 189.0

Total 714.0

* On an Assumed Head Count of 1500

Pay‐for‐Performance ?Model 1 – Human Capital Value

Area Value (AED in Million)

1. Retained Earnings @1,000

2. Dividends Paid @ 5,392

3. Replacing Costs of Current HC @ 714

Total @ 7,106

Pay‐for‐Performance ?Human Capital Asset Value Trend

0

1

2

3

4

5

6

7

8

HC Value

Y1 Y2 Y3 Y4

Model 2 (Outside‐In)

40

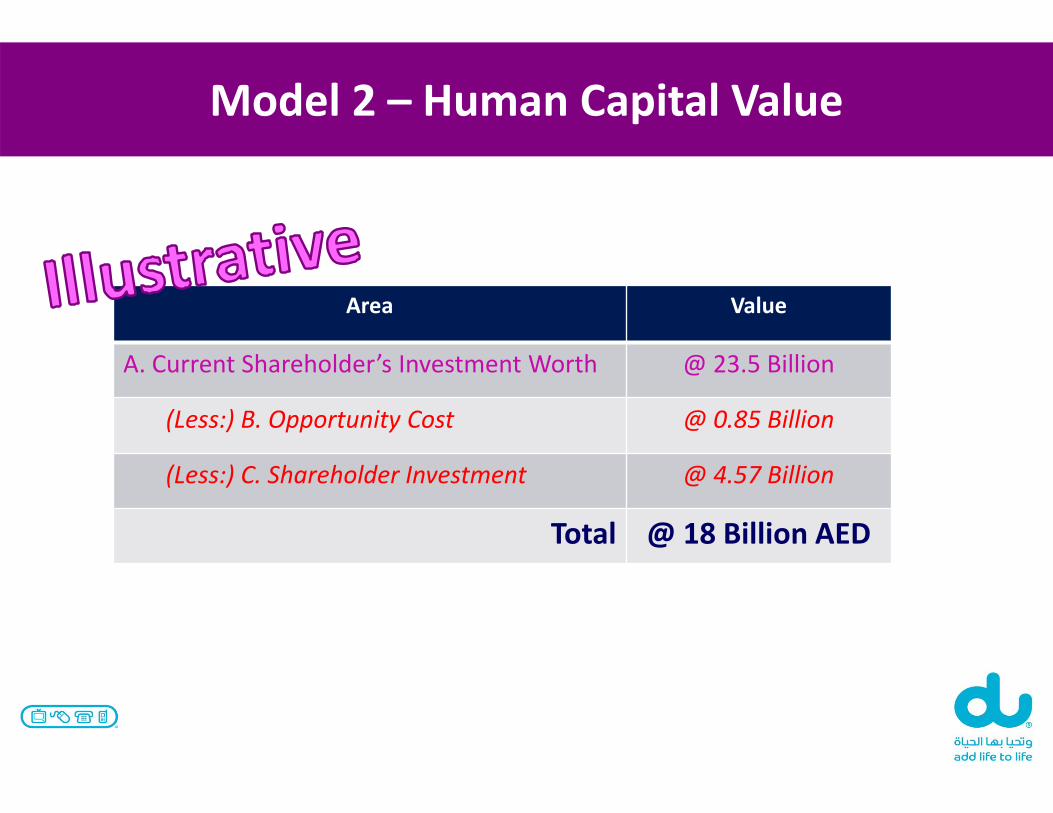

Pay‐for‐Performance ?Model 2 – Human Capital Value

Area Value

A. Current Shareholder’s Investment Worth

(Less:) B. Opportunity Cost

(Less:) C. Shareholder Investment

Total = A – (B+C)

Pay‐for‐Performance ?1. Shareholders Investment

Area Value

Total Number of Equity Shares @ 4,571 Mill AED

Face Value of 1 Share @1 AED

Total Shareholder Investment = 4,571 Million AED

Pay‐for‐Performance ?2. Opportunity Cost of Shareholder’s Investment

Area Value

Amount Invested @4,571 M AED

Potential Interest Rate @ 2%

Number of Years till 2014 9

Interest Gain = 4,571 M * 2% * 9

= 855 M AED

Pay‐for‐Performance ?3. Current Shareholder’s Investment Worth

Area ValueCurrent Share Price @5.15 AED

No of Shares @4,571 M

Shareholder Investment Worth @ 23.5 Billion

Pay‐for‐Performance ?Model 2 – Human Capital Value

Area Value

A. Current Shareholder’s Investment Worth @ 23.5 Billion

(Less:) B. Opportunity Cost @ 0.85 Billion

(Less:) C. Shareholder Investment @ 4.57 Billion

Total @ 18 Billion AED

Pay‐for‐Performance ?The Range of Human Capital Value

Model 1

AED 7.1 Billion

Model 2

AED 18 Billion

Pay‐for‐Performance ?Human Capital Valuation can be used for…

• Decisions in Investing in People

• Designing Pay for Performance Programs

• Business Cases for Retention Schemes

Pay‐for‐Performance ?Some Constraints for not reporting HC

• Companies don’t “Own Human resources”

• Is it because GAAP/FASB or IFRS doesn’t “Mandate”

• No established/widely accepted principles

• Not sufficient “R&D” to advance this topic

• Lack of intent from CFOs/CHROs/CEOs/Boards

Pay‐for‐Performance ?

Let us be “Roughly Right” by starting HC valuation & HR Balance Sheet

rather than….

“Grossly Wrong” by not measuring it

Pay‐for‐Performance ?Next Steps….

Can you Champion this cause?

and

Will your Company publish Human Capital Value & Balance Sheet??

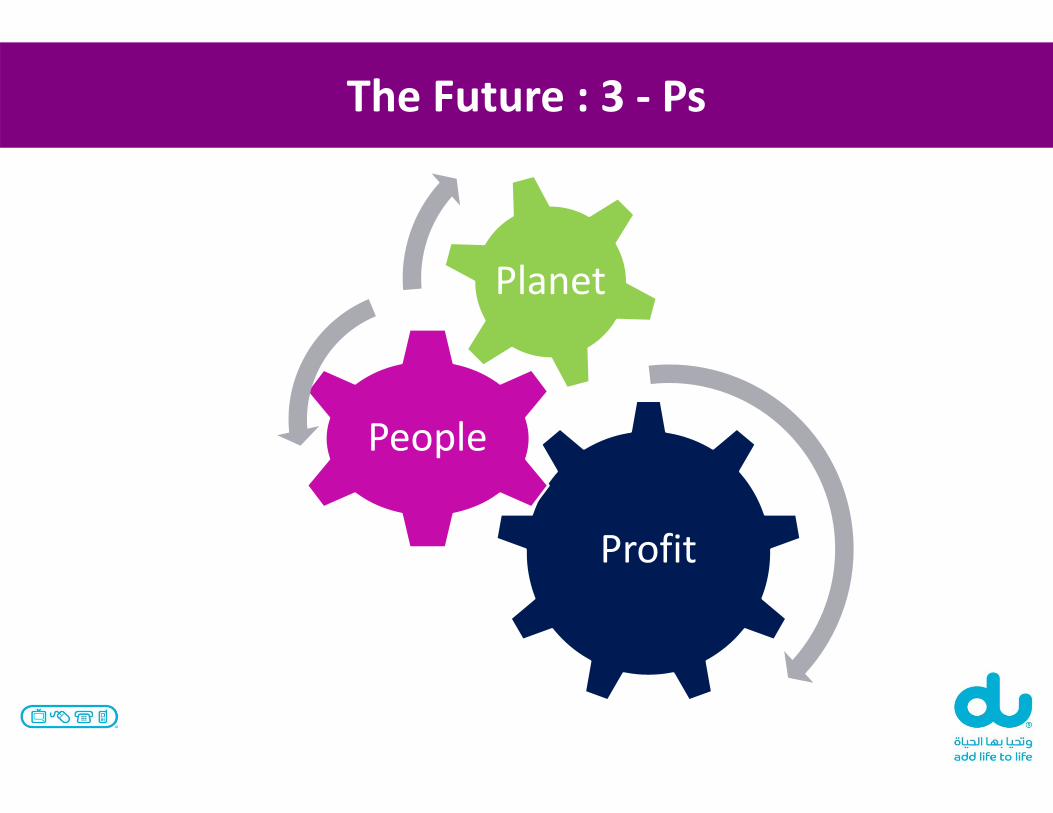

Pay‐for‐Performance ?The Future : 3 ‐ Ps

Profit

People

Planet

Thank You….