54

HSBC Asset Management (India) Private Limited Annual Report 2013 - 2014

HSBC Asset Management (India) Private Limited

Annual Report 2013 - 2014

HSBC Asset Management (India) Private Limited

DIRECTORS’ REPORT

FOR THE YEAR ENDED MARCH 31, 2014 The Directors have pleasure in submitting their report along with the audited financials for the Financial Year ended March 31, 2014. 1. FINANCIAL RESULTS

(Rs. 000s)

Particulars Current

financial year ended

March 31, 2014

Previous financial year ended

March 31, 2013

Gross income 720,696 431,810 Profit / (loss) before finance charges and depreciation 42,090 (191,661) Finance charges 2,036 1,994 Depreciation 13,758 18,503 Exceptional Items 101,715 - Profit / (loss) for the period (75,419) (212,158) Provision for Tax - -

Deferred Tax & Fringe benefit tax Credit / (Charge) - - Net Profit / (loss) for the period after adjustment of deferred tax credit (75,419) (212,158) Dividend, Dividend Distribution tax & Other Appropriations - - Net Profit / (loss) after taxes carried forward to the Balance Sheet (75,419) (212,158) Previous period figures have been regrouped and reclassified wherever necessary to confirm the current period’s presentation. 2 OPERATIONS a) Mutual Fund While the markets continued to remain challenging during the financial year ending March 31, 2014, we observed diverse trends in Assets under Management.

HSBC Asset Management (India) Private Limited

During the year, the following schemes were launched/matured by HSBC Mutual Fund:

Name of the Scheme Date of Launch

HSBC Capital Protection Oriented Fund April 18, 2013

HSBC Fixed Term Series 91 August 01, 2013

HSBC Fixed Term Series 94 August 16, 2013

HSBC Fixed Term Series 95 August 23, 2013

HSBC Fixed Term Series 98 October 14, 2013

HSBC Fixed Term Series 97 October 24, 2013

HSBC Fixed Term Series 99 November 08, 2013

HSBC Fixed Term Series 100 November 27, 2013

HSBC Fixed Term Series 101 January 15, 2014

HSBC Fixed Term Series 105 February 05, 2014

HSBC Fixed Term Series 106 February 24, 2014

HSBC Asia Pacific (Ex Japan) Dividend Yield Fund

February 03, 2014

HSBC Fixed Term Series 107 March 06, 2014

HSBC Fixed Term Series 109 March 24, 2014

HSBC Managed Solutions April 09, 2014

Name of Scheme Date of Maturity

HSBC Fixed Term Series 86 April 02, 2013

The Company earned Investment Management fees to the tune of Rs. 39.73 crores (net of Service Tax) for managing the assets of HSBC Mutual Fund. The fund under management of the Schemes of HSBC Mutual Fund as at March 31, 2014 was Rs. 6,976.47 crores. The Fund had 219898 live investor accounts as at March 31, 2014 in its various Schemes. b) Portfolio Management Services (PMS) The Company launched its Portfolio Management Services (PMS) offering on 27 March 2006. Portfolio Management Services is a customized proposition for high net worth clients. The service aims to provide personalized portfolio management services to select clientele depending on the investor's risk appetite, growth expectations and personal investment requirements. Currently the Company provides Discretionary and Advisory Portfolio Management Services to individual and institutional customers.

HSBC Asset Management (India) Private Limited

As on March 31, 2014, the PMS business had Assets under Management (AUM) of INR 83884.27 crores including the Employee Provident Fund Organization (EPFO) corpus. There were 128 (including EPFO) clients under Discretionary PMS and 1 client under Advisory PMS. 3. PERFORMANCE

The performance of the Schemes of HSBC Mutual Fund as on March 31, 2014 is presented below:

1) HSBC Equity Fund (HEF) – an open-ended diversified Equity Scheme

HEF seeks to generate long-term capital growth from an actively managed portfolio of equity and equity related securities. The net assets of HEF amounted to Rs. 453.11 crores as at March 31, 2014 as against Rs. 537.32 crores as at March 31, 2013. Around 97.81% of the net assets were invested in equities, 2.51% of the net assets were invested in reverse repos/CBLO and (- 0.32%) was in the net current assets as at March 31, 2014. HEF remained invested in a diversified portfolio across large capitalization stocks. The relative overweight in Technology resulted in outperformance against scheme benchmark for the period 2013-14.

Date Of Inception : 10 Dec 02 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Equity Fund – Growth 16.82 4.20 -8.90 24.34

S&P BSE 200 (Scheme Benchmark)

16.65 5.41 -9.55 18.72

CNX Nifty (Standard Benchmark)

17.53 6.93 -9.13 17.67

Rs. 10,000, if invested in HEF, would have become

11,682 10,420 9,110 118,277

Rs. 10,000, if invested in S&P BSE 200, would have become

11,665 10,541 9,045 69,977

Rs. 10,000, if invested in CNX Nifty, would have

11,753 10,693 9,087 63,309

HSBC Asset Management (India) Private Limited

Date Of Inception : 10 Dec 02 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

become

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparison purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 2) HSBC India Opportunities Fund (HIOF) – an open-ended flexi-cap Equity

Scheme HIOF seeks long term capital growth through investments across all market capitalizations, including small, mid and large cap stocks. It aims to be predominantly invested in equity and equity related securities. However, it could move a significant portion of its assets towards fixed income securities if the fund manager becomes negative on equity markets. The net assets of HIOF amounted to Rs. 177.60 crores as at March 31, 2014 as compared to Rs. 212.70 crores as at March 31, 2013. Around 98.47% of the net assets were invested in equities, 3.09 % of the net assets were invested in reverse repos/CBLO and (-1.56%) were in the net current assets as at March 31, 2014. HIOF outperformed its benchmark on a 1-year, 3-year basis and since its inception. The overweight in Technology resulted in outperformance against its benchmark for the period 2013-14. In addition, stock selections in sectors like Consumer Discretionary, Healthcare, Industrials, Materials and Utility contributed to the outperformance during this period.

HSBC Asset Management (India) Private Limited

Date Of Inception : 24 Feb 04 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC India Opportunities Fund – Growth 27.93 0.21 -3.60 15.97

S&P BSE 500 (Scheme Benchmark) 16.44 4.14 -9.47 13.76

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 13.77

Rs. 10,000, if invested in HIOF, would have become

12,793 10,021 9,640 44,698

Rs. 10,000, if invested in S&P BSE 500, would have become

11,644 10,414 9,053 36,805

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 36,822

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 3) HSBC Midcap Equity Fund (HMEF) – an open-ended diversified Equity Scheme HMEF seeks to generate long term capital growth from an actively managed portfolio of equity and equity related securities primarily being midcap stocks. However, it could move a portion of its assets towards fixed income securities if the fund manager becomes negative on the Indian equity markets. The net assets of HMEF amounted to Rs. 82.03 crores as at March 31, 2014 as compared to Rs. 82.29 crores as at March 31, 2013. Around 98.61 % of the net assets were invested in equities, 2.12% of the net assets were invested in reverse repos/CBLO and (-0.73 %) were in the net current assets as at March 31, 2014.

HSBC Asset Management (India) Private Limited

HMEF has done well in terms of outperformance v/s benchmark due to stock selection across various sectors for the period 2013-14. The focus on reasonable growth oriented companies available at attractive valuations (PB/ROE) paid off. HMEF continues to be overweight in Auto Ancillary, Agro Chemicals, Capital Goods, Pharma and underweight in FMCG sector.

Date Of Inception : 19 May 05 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Midcap Equity Fund – Growth 28.40 -8.82 -8.51 9.51

S&P BSE Midcap (Scheme Benchmark) 13.86 -4.30 -9.14 9.19

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 14.67

Rs. 10,000, if invested in HMEF, would have become

12,840 9,118 9,149 22,400

Rs. 10,000, if invested in S&P BSE Midcap, would have become

11,386 9,570 9,086 21,818

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 33,688

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 4) HSBC Progressive Themes Fund (HPTF) – an open-ended flexi-theme

Equity Scheme HPTF seeks to generate long term capital growth from an actively managed portfolio of equity and equity related securities by investing primarily in sectors, areas and themes that play an important role in, and / or benefit from, India's progress, reform process and economic development.

HSBC Asset Management (India) Private Limited

The net assets of HPTF amounted to Rs. 110.41 crores as at March 31, 2014 as compared to Rs. 130.40 crores as at March 31, 2013. Around 99.88% of the net assets were invested in equities, 0.93% of the net assets were invested in reverse repos/CBLO and (-0.81%) were in the net current assets as at March 31, 2014. HPTF is a theme based scheme. The focus of the scheme being on Infrastructure and Economic Reforms suffered due to delay in the government policy, high interest rates, etc. as against a more diversified benchmark. However, post-election the fund has managed to recover sharply on expectations of increased infrastructure thrust, improvement in investment cycle, easing of regulatory hurdles etc.

Date Of Inception : 23 Feb 06 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Progressive Themes Fund – Growth 4.65 -10.58 -4.28 1.06

S&P BSE 200 (Scheme Benchmark) 16.65 5.41 -9.55 9.56

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 10.15

Rs. 10,000, if invested in HPTF, would have become

10,465 8,942 9,572 10,896

Rs. 10,000, if invested in S&P BSE 200, would have become

11,665 10,541 9,045 20,962

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 21,900

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs.

HSBC Asset Management (India) Private Limited

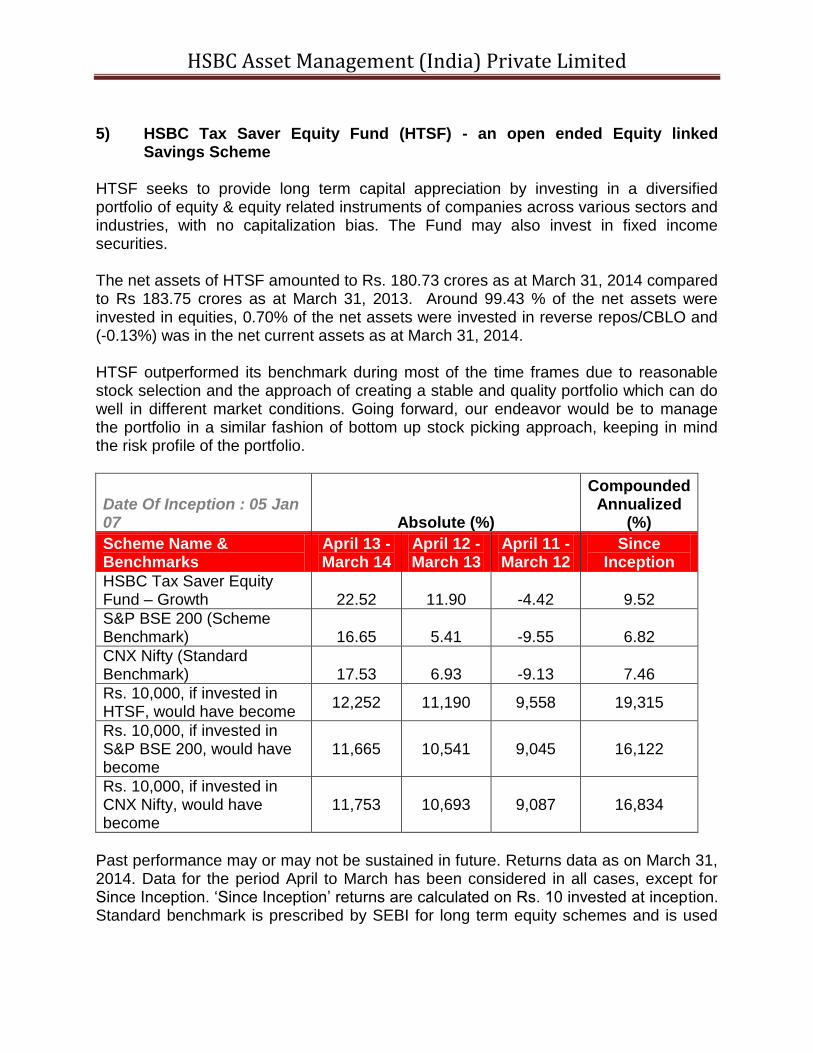

5) HSBC Tax Saver Equity Fund (HTSF) - an open ended Equity linked Savings Scheme

HTSF seeks to provide long term capital appreciation by investing in a diversified portfolio of equity & equity related instruments of companies across various sectors and industries, with no capitalization bias. The Fund may also invest in fixed income securities. The net assets of HTSF amounted to Rs. 180.73 crores as at March 31, 2014 compared to Rs 183.75 crores as at March 31, 2013. Around 99.43 % of the net assets were invested in equities, 0.70% of the net assets were invested in reverse repos/CBLO and (-0.13%) was in the net current assets as at March 31, 2014. HTSF outperformed its benchmark during most of the time frames due to reasonable stock selection and the approach of creating a stable and quality portfolio which can do well in different market conditions. Going forward, our endeavor would be to manage the portfolio in a similar fashion of bottom up stock picking approach, keeping in mind the risk profile of the portfolio.

Date Of Inception : 05 Jan 07 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Tax Saver Equity Fund – Growth 22.52 11.90 -4.42 9.52

S&P BSE 200 (Scheme Benchmark) 16.65 5.41 -9.55 6.82

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 7.46

Rs. 10,000, if invested in HTSF, would have become

12,252 11,190 9,558 19,315

Rs. 10,000, if invested in S&P BSE 200, would have become

11,665 10,541 9,045 16,122

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 16,834

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used

HSBC Asset Management (India) Private Limited

for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs.

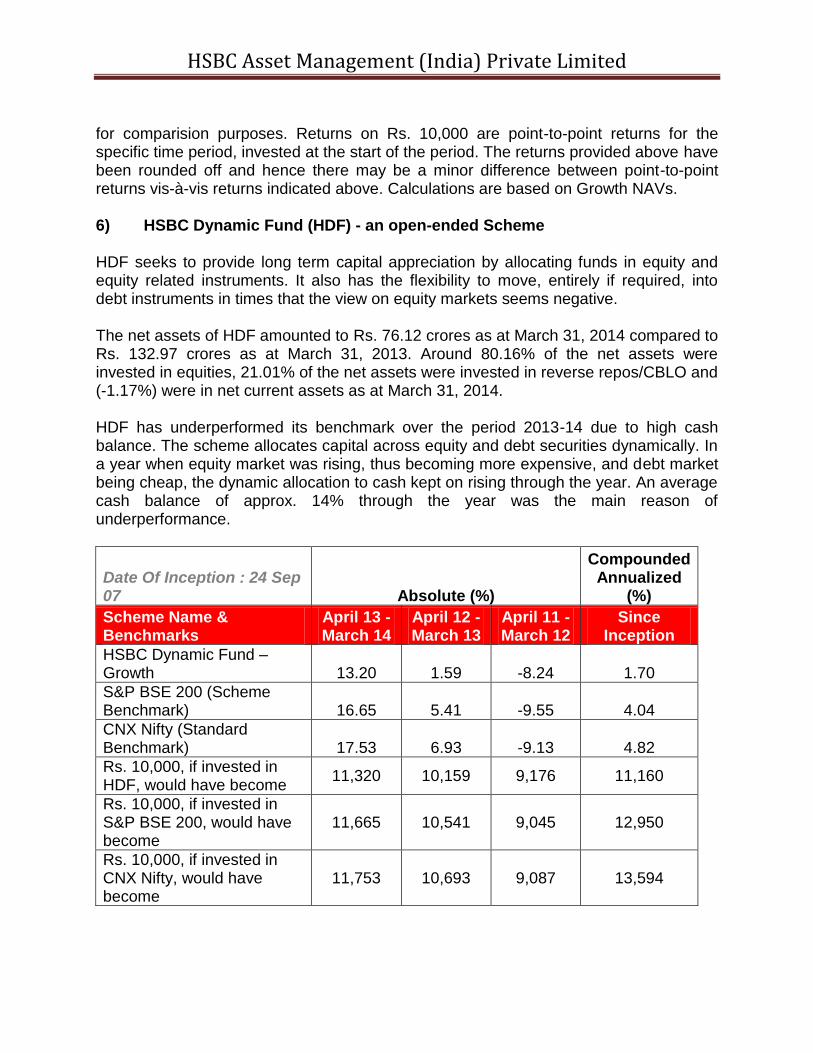

6) HSBC Dynamic Fund (HDF) - an open-ended Scheme HDF seeks to provide long term capital appreciation by allocating funds in equity and equity related instruments. It also has the flexibility to move, entirely if required, into debt instruments in times that the view on equity markets seems negative. The net assets of HDF amounted to Rs. 76.12 crores as at March 31, 2014 compared to Rs. 132.97 crores as at March 31, 2013. Around 80.16% of the net assets were invested in equities, 21.01% of the net assets were invested in reverse repos/CBLO and (-1.17%) were in net current assets as at March 31, 2014. HDF has underperformed its benchmark over the period 2013-14 due to high cash balance. The scheme allocates capital across equity and debt securities dynamically. In a year when equity market was rising, thus becoming more expensive, and debt market being cheap, the dynamic allocation to cash kept on rising through the year. An average cash balance of approx. 14% through the year was the main reason of underperformance.

Date Of Inception : 24 Sep 07 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Dynamic Fund – Growth 13.20 1.59 -8.24 1.70

S&P BSE 200 (Scheme Benchmark) 16.65 5.41 -9.55 4.04

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 4.82

Rs. 10,000, if invested in HDF, would have become

11,320 10,159 9,176 11,160

Rs. 10,000, if invested in S&P BSE 200, would have become

11,665 10,541 9,045 12,950

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 13,594

HSBC Asset Management (India) Private Limited

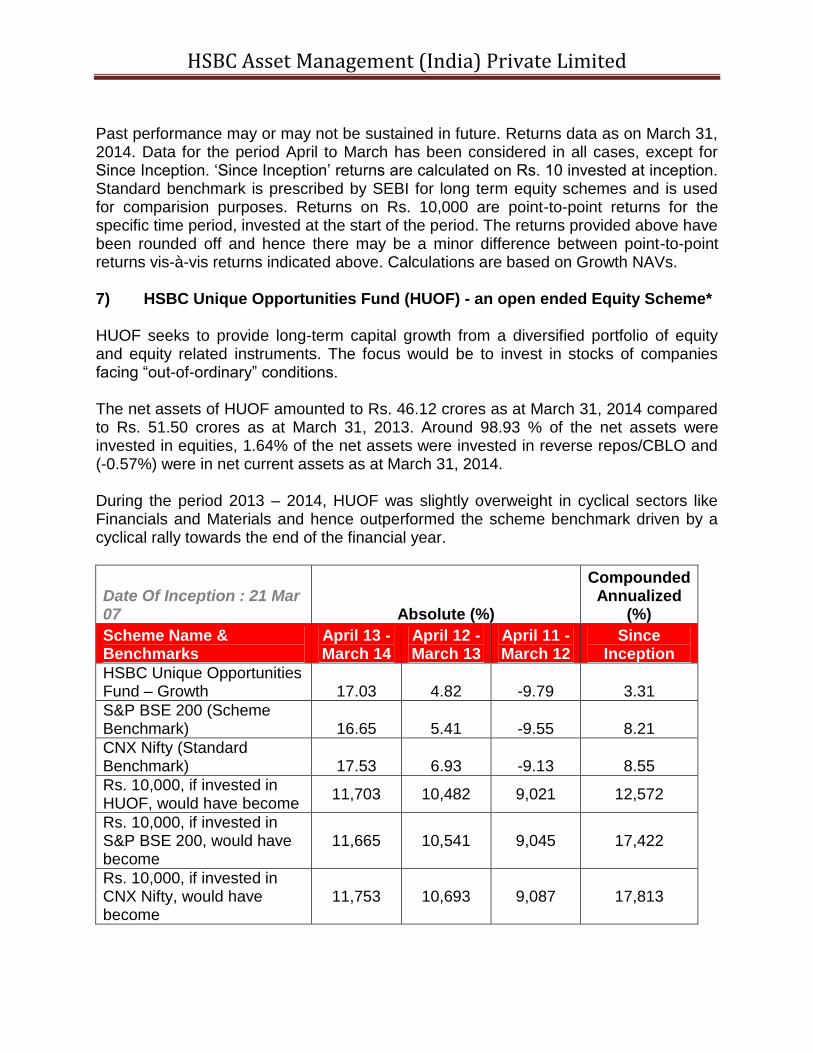

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 7) HSBC Unique Opportunities Fund (HUOF) - an open ended Equity Scheme* HUOF seeks to provide long-term capital growth from a diversified portfolio of equity and equity related instruments. The focus would be to invest in stocks of companies facing “out-of-ordinary” conditions. The net assets of HUOF amounted to Rs. 46.12 crores as at March 31, 2014 compared to Rs. 51.50 crores as at March 31, 2013. Around 98.93 % of the net assets were invested in equities, 1.64% of the net assets were invested in reverse repos/CBLO and (-0.57%) were in net current assets as at March 31, 2014. During the period 2013 – 2014, HUOF was slightly overweight in cyclical sectors like Financials and Materials and hence outperformed the scheme benchmark driven by a cyclical rally towards the end of the financial year.

Date Of Inception : 21 Mar 07 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Unique Opportunities Fund – Growth 17.03 4.82 -9.79 3.31

S&P BSE 200 (Scheme Benchmark) 16.65 5.41 -9.55 8.21

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 8.55

Rs. 10,000, if invested in HUOF, would have become

11,703 10,482 9,021 12,572

Rs. 10,000, if invested in S&P BSE 200, would have become

11,665 10,541 9,045 17,422

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 17,813

HSBC Asset Management (India) Private Limited

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. *HUOF is undergoing a change in its investment objective, investment strategy etc. and will be re-named as the HSBC Dividend Yield Equity Fund. The changes being in the nature of fundamental attribute changes, the investors have been notified of the same giving then an option to redeem from the Fund. The change will be effective from July 18, 2014. Kindly refer the notice dated May 26, 2014 (published in Financial Express and Navshakti newspapers dated May 27, 2014 and available on www.assetmanagement.hsbc.com/in) for more details. 8) HSBC Small Cap Fund (HSCF) – an open ended Equity Scheme* HSCF seeks to provide long-term capital appreciation primarily from a diversified portfolio of equity and equity related instruments of small cap companies. The net assets of HSCF amounted to Rs. 15.08 crores as at March 31, 2014 compared to Rs. 13.77 crores as at March 31, 2013. Around 98.21 % of the net assets were invested in equities, 3.92% of the net assets were invested in reverse repos/CBLO and (-2.13%) were in the net current assets as at March 31, 2014. HSCF had shown better performance across different time periods against its scheme benchmark. Stock selection had improved the performance vis-a-vis benchmark. Further, the valuation difference between large and small cap is not justified and unlikely to sustain, thus creating opportunities for better risk-return in mid-small cap segment.

Date Of Inception : 24 Mar 08 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Small Cap Fund – Growth 35.67 -6.02 -18.39 2.93

S&P BSE Small Cap (Scheme Benchmark) 19.09 -14.05 -20.74 0.29

HSBC Asset Management (India) Private Limited

Date Of Inception : 24 Mar 08 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 6.42

Rs. 10,000, if invested in HSCF, would have become

13,567 9,398 8,161 11,903

Rs. 10,000, if invested in S&P BSE Smallcap, would have become

11,909 8,595 7,926 10,175

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 14,546

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. * HSBC Small Cap Fund merged with HSBC Midcap Equity Fund with effect from April 26, 2014 and consequently ceases to exist. 9) HSBC Income Fund (HIF) – an open-ended Income Scheme HIF seeks to generate reasonable income through a diversified portfolio of fixed income securities. The AMC’s view of interest rate trends and the nature of the plans will be reflected in the type and maturities of securities in which the Short Term and Investment Plans are invested.

The Scheme has two plans – the Investment Plan and the Short Term Plan. The net assets of HSBC Income Fund – Investment Plan (HIF – IP) amounted to Rs. 61.65 crores as at March 31, 2014 as compared to Rs. 89.77 crores as at March 31, 2013. Around 94.86% of the net assets were invested in debt and money market instruments, 1.26% of the net assets were invested in reverse repos/CBLO and 3.88 % were in net current assets as at March 31, 2014. The net assets of HSBC Income Fund – Short Term Plan (HIF – STP) amounted to Rs. 727.27 crores as at March 31, 2014 as

HSBC Asset Management (India) Private Limited

compared to Rs. 1035.16 crores as at March 31, 2013. Around 96.70 % of the net assets were invested in debt and money market instruments, 0.23 % of the net assets were invested in reverse repos/CBLO and 3.07 % were in net current assets as at March 31, 2014.

HIF-IP and HIF – STP underperformed their benchmark due to higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency. Although the measures were gradually rolled back, long end of the curve remained anchored to 8.75-9% range due to supply and absence of open market operations.

HIF – IP

Date Of Inception : 10 Dec 02 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Income Fund - Investment Plan – Growth 1.85 11.19 8.86 6.65

Crisil Composite Bond Fund Index (Scheme Benchmark) 4.34 9.27 7.68 5.72

Crisil 10 Year Gilt Index (Standard Benchmark) -0.79 11.31 2.41 5.03

Rs. 10,000, if invested in HIF - IP, would have become

10,185 11,119 10,886 20,725

Rs. 10,000, if invested in Crisil Composite Bond Fund Index, would have become

10,434 10,927 10,768 18,767

Rs. 10,000, if invested in Crisil 10 Year Gilt Index, would have become

9,921 11,131 10,241 17,431

HIF – STP

Date Of Inception : 10 Dec 02 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Income Fund - S T P – Growth 7.23 9.26 8.41 6.80

Crisil Short Term Bond Fund Index (Scheme 8.79 9.09 8.28 6.64

HSBC Asset Management (India) Private Limited

Date Of Inception : 10 Dec 02 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

Benchmark)

Crisil 1 Year T-Bill Index (Standard Benchmark) 5.78 8.37 6.59 5.44

Rs. 10,000, if invested in HIF -ST, would have become

10,723 10,926 10,841 21,047

Rs. 10,000, if invested in Crisil Short Term Bond Fund Index, would have become

10,879 10,909 10,828 20,691

Rs. 10,000, if invested in Crisil 1 Year T-Bill Index, would have become

10,578 10,837 10,659 18,205

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 10) HSBC Gilt Fund (HGF) – an open-ended Gilt Scheme HGF seeks to generate reasonable returns through investments in Government Securities of various maturities. The AMC’s view of interest rate trends will be reflected in the maturities of securities in which the scheme is invested. The net assets of HGF amounted to Rs. 2.64 crores as at March 31, 2014 as compared to Rs. 2.20 crores as at March 31, 2013. Around 28.54% of the net assets were invested in reverse repos/CBLO and 69.24 % were invested in government securities and 2.22 % were in net current assets as at March 31, 2014. HGF underperformed its benchmark due to higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency. Although the measures were gradually rolled back, long end of the curve

HSBC Asset Management (India) Private Limited

remained anchored to 8.75-9% range due to supply and absence of open market operations.

Date Of Inception : 05 Dec 03 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Gilt Fund - Growth 1.99 12.37 8.15 4.30

I-Sec Composite Bond Fund Index (Scheme Benchmark) 3.95 11.71 6.77 6.50

Crisil 10 Year Gilt Index (Standard Benchmark) -0.79 11.31 2.41 4.20

Rs. 10,000, if invested in HGF, would have become

10,199 11,237 10,815 15,453

Rs. 10,000, if invested in I-Sec Composite Bond Fund Index, would have become

10,395 11,171 10,677 19,156

Rs. 10,000, if invested in Crisil 10 Year Gilt Index, would have become

9,921 11,131 10,241 15,295

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs 11) HSBC Floating Rate Fund – Long Term Plan (HFRF – LTP) – an open-ended

Income Scheme HFRF seeks to generate reasonable return with commensurate risk from a portfolio comprised of floating rate debt instruments and fixed rate debt instruments swapped for floating rate returns. The scheme may also invest in fixed rate money market and debt instruments. The net assets of the HFRF - LTP amounted to Rs. 112.48 crores as at March 31, 2014 as compared to Rs. 232.34 crores as at March 31, 2013. Around 99.94% of the net assets were invested in money market instruments, 0.48% was invested in reverse repos/CBLO and (-0.42%) were in net current assets as at March 31, 2014.

HSBC Asset Management (India) Private Limited

HFRF-LTP performed close to its benchmark by focusing on accruals and investing in the shorter-end of the yield curve. Short end yield curve also faced higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency.

Date Of Inception : 16 Nov 04 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC FRF - LTP – Growth 9.21 9.17 9.38 7.68

Crisil Liquid Fund Index (Scheme Benchmark) 9.46 8.22 8.45 6.96

Crisil 1 Year T-Bill Index (Standard Benchmark) 5.78 8.37 6.59 5.67

Rs. 10,000, if invested HFRF - LTP, would have become

10,921 10,917 10,938 20,014

Rs. 10,000, if invested in Crisil Liquid Fund Index, would have become

10,946 10,822 10,845 18,798

Rs. 10,000, if invested in Crisil 1 Year T-Bill Index, would have become

10,578 10,837 10,659 16,776

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 12) HSBC Cash Fund (HCF) – an open-ended Liquid Scheme* HCF aims to provide reasonable returns, commensurate with low risk while providing a high level of liquidity, through a portfolio of money market and debt securities. The net assets of HCF amounted to Rs. 1394.74 crores as at March 31, 2014 as compared to Rs. 469.01 crores as at March 31, 2013. The entire net asset remains

HSBC Asset Management (India) Private Limited

invested in debt and money market instruments including reverse repos/CBLO as at March 31, 2014. HCF performed broadly in line with its benchmark for a year due to conservative investments in line with the internal guidelines alongwith focus on accruals and credits.

Date Of Inception : 04 Dec 02 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

Last 7 Days as

on 31 March 2014

Last 15 Days as on

31 March 2014

Last 30 Days as

on 31 March 2014

April 13 - March

14 Since

Inception

HSBC Cash Fund – Growth 10.31 9.92 9.44 9.42 8.98

Crisil Liquid Fund Index (Scheme Benchmark) 13.20 12.94 11.69 9.46 8.76

Crisil 91 Day T-Bill Index (Standard Benchmark) 12.05 11.69 10.15 8.55 8.24

Rs. 10,000, if invested in HCF, would have become

10,020 10,041 10,078 10,942 12,802

Rs. 10,000, if invested in Crisil Liquid Fund Index, would have become

10,025 10,053 10,096 10,946 12,727

Rs. 10,000, if invested in Crisil 91 Day T-Bill Index, would have become

10,023 10,048 10,083 10,855 12,554

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs.

HSBC Asset Management (India) Private Limited

* Pursuant to SEBI circular dated Sept 13, 2012, certain plans/options within the schemes have been discontinued to comply with a single plan structure. Since there was no continuous NAV history available for the surviving plan prior to 19 May 2011, returns since the said date have been considered for calculating performance. The inception date of HSBC Cash Fund however is December 04, 2002.

13) HSBC Ultra Short Term Bond Fund (HUSBF) – an open ended Debt Scheme HUSBF seeks to provide liquidity and reasonable returns by investing primarily in a mix of short term debt and money market instruments. The net assets of HUSBF amounted to Rs. 153.71 crores as at March 31, 2014 as compared to Rs. 45.73 crores as at March 31, 2013. Around 95.64% of the net assets were invested in debt and money market instruments, 4.38% were invested in reverse repos/CBLO and (-0.02%) were in net current assets as at March 31, 2014. HUSBF outperformed its benchmark due to focus on better placed positions on the yield curve. HUSBF also faced higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency.

Date Of Inception : 17 Oct 06

Simple Annualized

(%) Compounded

Annualized (%)

Scheme Name & Benchmarks April 13 - March 14 Since Inception

HSBC Ultra Short Term Bond Fund - Growth $ 9.04 8.91

Customized Benchmark Index (Scheme Benchmark)* 8.60 8.18

Crisil 1 Year T-Bill Index (Standard Benchmark) 5.78 6.59

Rs. 10,000, if invested in HUSTBF, would have become

10,904 11,365

Rs. 10,000, if invested in Customized Benchmark Index, would have become

10,860 11,250

Rs. 10,000, if invested in Crisil 1 Year T-Bill Index, would have become

10,578 11,004

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used

HSBC Asset Management (India) Private Limited

for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. $Pursuant to SEBI circular dated Sept 13, 2012, certain plans/options within the schemes have been discontinued to comply with a single plan structure. Since there was no continuous NAV history available for the surviving plan prior to 1 October 2012, returns since the said date have been considered for calculating performance ‘Since Inception’. The inception date of HSBC Ultra Short Term Bond Fund however is October 17, 2006. *Composite index of Crisil Liquid Fund Index (90%) and Crisil Short Term Bond Fund Index (10%). 14) HSBC Flexi Debt Fund (HFDF) – an open ended Debt Scheme HFDF seeks to deliver returns in the form of interest income and capital gains, along with high liquidity, commensurate with the current view on the markets and the interest rate cycle, through active investment in debt and money market instruments. The net assets of HFDF amounted to Rs. 540.42 crores as at March 31, 2014 as compared to Rs.792.49 crores as at March 31, 2013. Around 97.11% of the net assets were invested in debt and money market instruments, 0.18% was invested in reverse repos/CBLO and 2.71% were in the net current assets as at March 31, 2014. HFDF underperformed its benchmark due to higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency. Although the measures were gradually rolled back, long end of the curve remained anchored to 8.75-9% range due to supply and absence of open market operations.

Date Of Inception : 05 Oct 07 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Flexi Debt Fund – Growth 3.69 11.26 9.54 8.38

Crisil Composite Bond Fund Index (Scheme Benchmark) 4.34 9.27 7.68 6.54

Crisil 10 Year Gilt Index (Standard Benchmark) -0.79 11.31 2.41 5.49

HSBC Asset Management (India) Private Limited

Date Of Inception : 05 Oct 07 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

Rs. 10,000, if invested in HFDF, would have become

10,369 11,126 10,954 16,862

Rs. 10,000, if invested in Crisil Composite Bond Fund Index, would have become

10,434 10,927 10,768 15,091

Rs. 10,000, if invested in Crisil 10 Year Gilt Index, would have become

9,921 11,131 10,241 14,147

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 15) HSBC MIP (HMIP) – an open-ended Fund (Monthly income is not assured and is subject to availability of distributable surplus.) HMIP is an open-ended fund which seeks to generate reasonable returns through investments in Debt and Money Market Instruments. The secondary objective of the scheme is to invest in equity and equity related instruments to seek capital appreciation. The scheme offers two plans: Regular Plan and Savings Plan. The Regular Plan can have up to 15% of the corpus invested in equities while the Savings Plan can have up to 25 % invested in equities. The net assets of HMIP – Regular Plan (HMIP – R) amounted to Rs. 111.44 crores as at March 31, 2014 as compared to Rs. 190.42 crores as at March 31, 2013. Around 82.16% of the net assets were invested in debt and money market instruments & 15.29% of the net assets were invested in equities as at March 31, 2014. The net assets of HMIP – Savings Plan (HMIP – S) amounted to Rs. 186.36 crores as at March 31, 2014 as compared to Rs. 317.36 crores as at March 31, 2013. Around 71.55% of the net assets were invested in debt and money market instruments & 26.60% % of the net assets were invested in equities as at March 31, 2014. HMIP-R and HMIP-S also faced higher volatility in rates during the year as RBI hiked the short end rates substantially in July 2013 to counter pressure on currency. Although

HSBC Asset Management (India) Private Limited

the measures were gradually rolled back, long end of the curve remained anchored to 8.75-9% range due to supply and absence of open market operations. HMIP – Regular Plan

Date Of Inception : 24 Feb 04 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC MIP - Regular Plan – Growth 6.60 10.07 5.20 7.67

Crisil MIP Blended Index (Scheme Benchmark) 6.42 9.09 5.26 7.12

Crisil 1 Year T-Bill Index (Standard Benchmark) 5.78 8.37 6.59 5.45

Crisil 10 Year Gilt Index (Standard Benchmark) -0.79 11.31 2.41 4.21

Rs. 10,000, if invested in HMIP - R, would have become

10,660 11,007 10,520 21,103

Rs. 10,000, if invested in Crisil MIP Blended Index, would have become

10,642 10,909 10,526 20,049

Rs. 10,000, if invested in Crisil 1 Year T-Bill Index, would have become

10,578 10,837 10,659 17,090

Rs. 10,000, if invested in Crisil 10 Year Gilt Index, would have become

9,921 11,131 10,241 15,170

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs.

HSBC Asset Management (India) Private Limited

HMIP – Savings Plan

Date Of Inception : 24 Feb 04 Simple Annualized (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC MIP - Savings Plan – Growth 8.99 10.74 4.94 9.30

Crisil MIP Blended Index (Scheme Benchmark) 6.42 9.09 5.26 7.12

Crisil 1 Year T-Bill Index (Standard Benchmark) 5.78 8.37 6.59 5.45

Crisil 10 Year Gilt Index (Standard Benchmark) -0.79 11.31 2.41 4.21

Rs. 10,000, if invested in HMIP - S, would have become

10,899 11,074 10,494 24,561

Rs. 10,000, if invested in Crisil MIP Blended Index, would have become

10,642 10,909 10,526 20,049

Rs. 10,000, if invested in Crisil 1 Year T-Bill Index, would have become

10,578 10,837 10,659 17,090

Rs. 10,000, if invested in Crisil 10 Year Gilt Index, would have become

9,921 11,131 10,241 15,170

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 16) HSBC Fixed Term Series – a close ended Income Scheme The scheme seeks to generate returns by investing in a portfolio of fixed income instruments which mature on or before the maturity date of the plans under the scheme.

HSBC Asset Management (India) Private Limited

Details of schemes launched during the period are provided below -

Name of Scheme Date of Launch

HSBC Fixed Term Series 91 August 01, 2013

HSBC Fixed Term Series 94 August 16, 2013

HSBC Fixed Term Series 95 August 23, 2013

HSBC Fixed Term Series 98 October 14, 2013

HSBC Fixed Term Series 97 October 24, 2013

HSBC Fixed Term Series 99 November 08, 2013

HSBC Fixed Term Series 100 November 27, 2013

HSBC Fixed Term Series 101 January 15, 2014

HSBC Fixed Term Series 105 February 05, 2014

HSBC Fixed Term Series 106 February 24, 2014

HSBC Fixed Term Series 107 March 06, 2014

HSBC Fixed Term Series 109 March 24, 2014

HSBC Fixed Term Series 102 April 28, 2014

Being close ended fixed maturity plans, the performance of these schemes are not provided. 17) HSBC Capital Protection Oriented Fund – a close ended Capital Protection

Oriented Scheme The scheme seeks protection of capital by investing a portion of the portfolio in high quality debt securities and money market instruments and also to provide capital appreciation by investing in equities through NIFTY (Index) Call Options. The scheme launched one plan namely, HSBC Capital Protection Oriented Fund – Series I – Plan I having a tenure of 790 days. HSBC Capital Oriented Protection Fund – Series I – Plan I was launched on April 18, 2013. The performance of the scheme is benchmarked against CRISIL MIP Blended Index. Being a close ended scheme, the performance of the scheme is not provided.

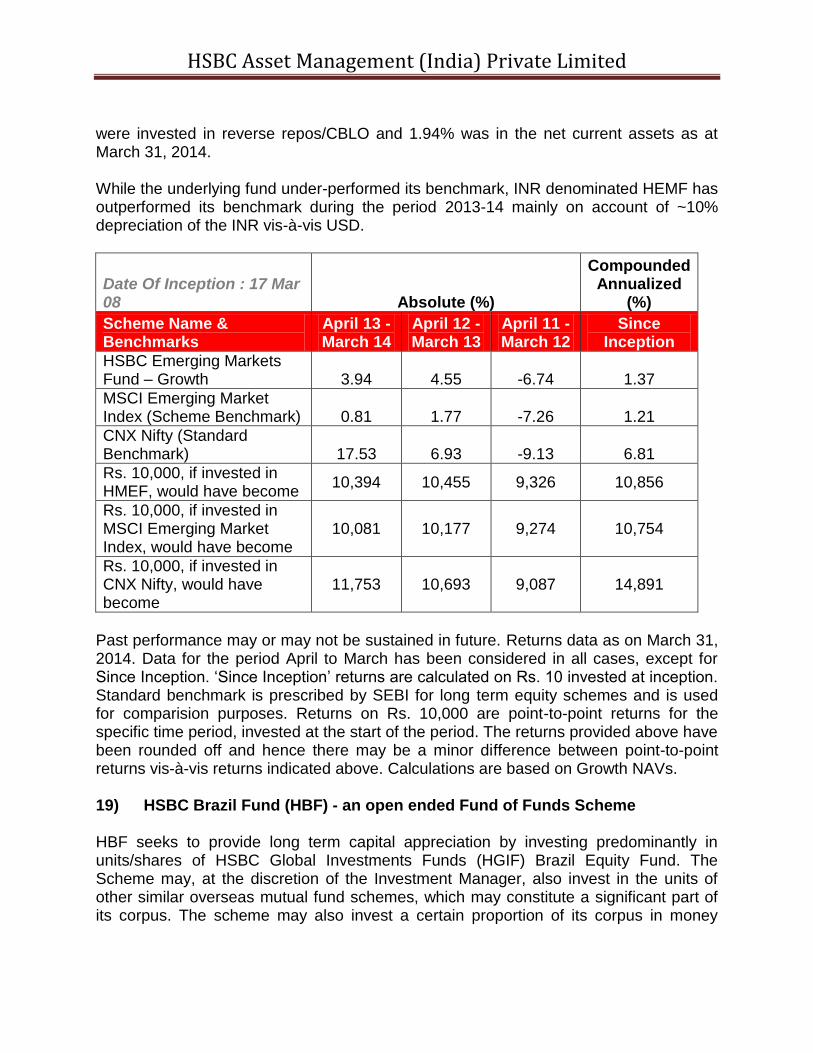

18) HSBC Emerging Markets Fund (HEMF) - an open-ended Scheme HEMF seeks to provide long term capital appreciation by investing in India and in the emerging markets, in equity and equity related instruments, share classes and units/securities issued by overseas mutual funds or unit trusts. The fund may also invest a limited proportion in debt and money market instruments. The net assets of HEMF amounted to Rs. 14.47 crores as at March 31, 2014 compared to Rs. 19.11 crores as at March 31, 2013. Around 97.56% of the net assets were invested in HSBC GEM Equity Fund (overseas mutual fund), 0.50% of the net assets

HSBC Asset Management (India) Private Limited

were invested in reverse repos/CBLO and 1.94% was in the net current assets as at March 31, 2014. While the underlying fund under-performed its benchmark, INR denominated HEMF has outperformed its benchmark during the period 2013-14 mainly on account of ~10% depreciation of the INR vis-à-vis USD.

Date Of Inception : 17 Mar 08 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks

April 13 - March 14

April 12 - March 13

April 11 - March 12

Since Inception

HSBC Emerging Markets Fund – Growth 3.94 4.55 -6.74 1.37

MSCI Emerging Market Index (Scheme Benchmark) 0.81 1.77 -7.26 1.21

CNX Nifty (Standard Benchmark) 17.53 6.93 -9.13 6.81

Rs. 10,000, if invested in HMEF, would have become

10,394 10,455 9,326 10,856

Rs. 10,000, if invested in MSCI Emerging Market Index, would have become

10,081 10,177 9,274 10,754

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 9,087 14,891

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. 19) HSBC Brazil Fund (HBF) - an open ended Fund of Funds Scheme HBF seeks to provide long term capital appreciation by investing predominantly in units/shares of HSBC Global Investments Funds (HGIF) Brazil Equity Fund. The Scheme may, at the discretion of the Investment Manager, also invest in the units of other similar overseas mutual fund schemes, which may constitute a significant part of its corpus. The scheme may also invest a certain proportion of its corpus in money

HSBC Asset Management (India) Private Limited

market instruments and /or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time. The net assets of HBF amounted to Rs. 94.05 crores as at March 31, 2014 compared to Rs. 184.79 crores as at March 31, 2013. Around 99.05 % of the net assets were invested in HSBC Brazil Equity Fund (overseas mutual fund), 1.11% of the net assets were invested in reverse repos/CBLO and (-0.16%) were in the net current assets as at March 31, 2014. HBF had outperformed its scheme benchmark during the period 2013-14 mainly on account of depreciation of the INR vis-à-vis the USD.

Date Of Inception : 06 May 11 Absolute (%)

Compounded Annualized

(%)

Scheme Name & Benchmarks April 13 - March 14

April 12 - March

13 Since

Inception

HSBC Brazil Fund – Growth -11.37 -2.50 -4.90

MSCI Brazil 10/40 Index (Scheme Benchmark) -14.46 -14.53 -13.38

CNX Nifty (Standard Benchmark) 17.53 6.93 6.71

Rs. 10,000, if invested in HBF, would have become

8,863 9,750 8,642

Rs. 10,000, if invested in MSCI Brazil 10/40 Index, would have become

8,554 8,547 6,587

Rs. 10,000, if invested in CNX Nifty, would have become

11,753 10,693 12,079

Past performance may or may not be sustained in future. Returns data as on March 31, 2014. Data for the period April to March has been considered in all cases, except for Since Inception. ‘Since Inception’ returns are calculated on Rs. 10 invested at inception. Standard benchmark is prescribed by SEBI for long term equity schemes and is used for comparision purposes. Returns on Rs. 10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be a minor difference between point-to-point returns vis-à-vis returns indicated above. Calculations are based on Growth NAVs. All returns have been sourced from Mutual Funds India Explorer software unless otherwise stated. With regard to equity schemes (including the equity component of MIPs), fund performance is calculated on a total return basis (i.e. it includes dividends re-invested) while the benchmark is calculated on a price return basis (i.e. it does not consider dividends re-invested).

HSBC Asset Management (India) Private Limited

20) HSBC Asia Pacific (Ex Japan) Dividend Yield Fund (HAPDF) – an open ended Fund of Funds Scheme

HAPDF seeks to provide long term capital appreciation by investing predominantly in units of HSBC Global Investment Funds (HGIF) Asia Pacific Ex Japan Equity High Dividend Fund (HEHDF). The Scheme may, also invest a certain proportion of its corpus in money market instruments and / or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time. However, there is no assurance that the investment objective of the Scheme will be achieved. The net assets of HADPF amounted to Rs. 56.26 crores as at March 31, 2014. Around 97.42 % of the net assets were invested in HSBC Global Investment Funds (HGIF) Asia Pacific Ex Japan Equity High Dividend Fund (overseas mutual fund), 2.78% of the net assets were invested in reverse repos/CBLO and (-0.20%) were in the net current assets as at March 31, 2014. The scheme was launched on February 03, 2014. The performance of the scheme is benchmarked against MSCI AC Asia Pacific Ex Japan. Performance data has not been provided as the scheme has not completed 1 year period from its launch. 21) HSBC Managed Solution (HMS) – an open ended Fund of Funds Scheme HMS seeks to provide long term total return primarily by seeking capital appreciation through an active asset allocation with diversification commensurate with the risk profile of investments by investing predominantly in units of equity mutual funds as well as in a basket of debt mutual funds gold exchange traded funds (ETFs) and other ETFs, offshore mutual funds and money market instruments. The scheme has three plans namely, HMS – Growth Plan, HMS – Moderate Plan and HMS – Conservative Plan. The scheme was launched on April 09, 2014. The performance of HMS – Growth Plan is benchmarked against Composite Index constituting 80% of BSE 200 Index and 20% of CRISIL Composite Bond Index while the performance of HMS – Moderate Plan is benchmarked against CRICIL Balanced Fund Index. The performance of HMS – Conservative Plan is benchmarked against Composite Index constituting of 90% into CRISIL Composite Bond Index and 10% of BSE 200 Index. Performance data has not been provided as the scheme has not completed 1 year period from its launch. 4. INVESTOR SERVICES The number of official points of acceptance of transactions is 198 locations. In addition to the offices of the Registrar & Transfer agents, the AMC has Investor Service Centres in 5 locations at its own offices - namely Mumbai, New Delhi, Kolkata, Bangalore and

HSBC Asset Management (India) Private Limited

Chennai. With a view to enhance customer convenience, the AMC has extended the facility of priority based servicing to key distributors through the enhancement of the Interactive Voice Reponses. Call Center number has now been converted to a single Toll Free number which can be dialed from anywhere in India. The call center service is being managed by the Registrar and Transfer Agents. The AMC continues to retain the outsourced back office services with HSBC Electronic Data Processing India Private Limited. On the distribution front, the number of empanelled distributors was 664 as on March 31, 2014. During the year, the AMC initiated tie-ups for online distribution of the Mutual Fund’s schemes with several channel partners taking the total number of such tie-ups to 46. 5. DIRECTORS Mr. Dinesh Kumar Mittal was appointed as a Director of HSBC Asset Management (India) Private Limited w.e.f. February 05, 2014. As required by the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, the Board of Directors of the Company comprises 50% directors who are not associate of or associated in any manner with, the Sponsor of HSBC Mutual Fund (HSBC Securities and Capital Markets (India) Private Limited) or any of its subsidiaries or the Trustees of HSBC Mutual Fund. Directors’ Responsibility Statement The Directors confirm that: (i) in the preparation of the annual accounts, the applicable accounting standards

have been followed along with proper explanation relating to material departures; (ii) the accounting policies have been consistently applied and reasonable and

prudent judgement and estimates have been made so as to give a true and fair view of the state of affairs of the Company as at March 31, 2014 and of the profit or loss of the Company for the Financial Year ended March 31, 2014;

(iii) proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of the Companies Act, 1956 has been taken for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities; and

(iv) the annual accounts have been prepared on a going concern basis.

HSBC Asset Management (India) Private Limited

6. PERSONNEL Particulars of employees required under section 217(2A) of the Companies Act, 1956 read with the Companies (Particulars of Employees) Rules, 1975 are given in the Annexure forming part of this Report. 7. CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION AND

FOREIGN EXCHANGE EARNINGS AND OUTGO As the Company is the asset management company to HSBC Mutual Fund and provides portfolio management services, no reporting in respect of conservation of energy and technology absorption is required. Information regarding foreign exchange earnings and outgo is contained in points 20.2 and 20.3 of the Notes to the financial statements. 8. AUDITORS M/s B S R & Associates retire as auditors at the ensuing annual general meeting and are eligible for reappointment. By authority of the Board Sd/- Sd/-

Naina Lal Kidwai Puneet Chaddha Chairperson Whole Time Director & Chief Executive Officer Place: Mumbai Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

HSBC Asset Management (India) Private Limited

Financial statementstogether with Auditors’ Reportfor the year ended 31 March 2014

HSBC Asset Management (India) Private Limited

Financial statements together with Auditors’ Reportfor the year ended 31 March 2014

Contents Pages

Auditors’ Report 3 – 7

Balance sheet 8

Statement of profit and loss 9

Cash flow statement 10 – 11

Schedules to the financial statements 12 – 25

Independent Auditors’ Report

To the Members of HSBC Asset Management (India) Private Limited Report on the Financial Statements

We have audited the accompanying financial statements of HSBC Asset Management (India) Private Limited (‘the Company’), which comprises the balance sheet as at 31 March 2014, the statement of profit and loss and the cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

The Management is responsible for the preparation of these financial statements that give a true and fair view of the financial position, financial performance and cash flows of the Company in accordance with the Accounting Standards referred to in sub-section (3C) of section 211 of the Companies Act, 1956 (‘the Act’). This responsibility includes the design, implementation and maintenance of internal control relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with the Standards on Auditing issued by the Institute of Chartered Accountants of India. Those Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Company’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of the accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion and to the best of our information and according to the explanations given to us, the financial statements give the information required by the Act in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India: (a) in the case of the balance sheet, of the state of affairs of the Company as at 31 March 2014; (b) in the case of the statement of profit and loss, of the loss for the year ended on that date;

and (c) in the case of the cash flow statement, of the cash flows for the year ended on that date.

3

Independent Auditors’ Report (Continued) HSBC Asset Management (India) Private Limited Report on Other Legal and Regulatory Requirements

1. As required by the Companies (Auditor’s Report) Order, 2003 (“the Order”), as amended, issued by the Central Government of India in terms of sub-section (4A) of section 227 of the Act, we give in the Annexure a statement on the matters specified in paragraphs 4 and 5 of the said Order.

2. As required by section 227(3) of the Act, we report that:

a. we have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purpose of our audit;

b. in our opinion proper books of account as required by law have been kept by the Company so far as appears from our examination of those books;

c. the balance sheet, the statement of profit and loss and the cash flow statement dealt with by this report are in agreement with the books of account;

d. in our opinion, the balance sheet, the statement of profit and loss and the cash flow statement comply with the Accounting Standards referred to in subsection (3C) of section 211 of the Companies Act, 1956; and

e. on the basis of written representations received from the directors as on 31 March 2014, and taken on record by the Board of Directors, none of the directors is disqualified as on 31 March 2014, from being appointed as a director in terms of clause (g) of sub-section (1) of section 274 of the Companies Act, 1956.

For B S R & Associates LLP Chartered Accountants Firm's Registration No: 116231W/W-100024 Sd/- N Sampath Ganesh Mumbai Partner 11 August 2014 Membership No: 042554

4

HSBC Asset Management (India) Private Limited Annexure to Independent Auditors’ Report - 31 March 2014 (Referred to in our report of even date)

(i) (a) The Company has maintained proper records showing full particulars, including quantitative details and situation of fixed assets.

(b) The Company has a regular programme of physical verification of its fixed assets by which all fixed assets are verified on yearly basis. In our opinion, this periodicity of physical verification is reasonable having regard to the size of the Company and the nature of its assets. No material discrepancies were noticed on such verification.

(c) Fixed assets disposed during the year do not affect the going concern assumption.

(ii) The Company is a service company primarily rendering asset management services and portfolio management services. Accordingly it does not hold any physical inventories. Thus, paragraph 4(ii) of the Order is not applicable.

(iii) The Company has neither granted nor taken any loans, secured or unsecured, to or from Companies, firms or other parties covered in the register maintained under Section 301 of the Companies Act, 1956.

(iv) In our opinion, and according to the information and explanations given to us, there is an adequate internal control system commensurate with the size of the Company and the nature of its business, with regard to purchase of fixed assets and sale of services. We have not observed continuing failure by the Company to correct major weakness in the internal control system in regard to above, during the course of the audit.

(v) (a) In our opinion and according to the information and explanation given to us, the particulars of contracts or arrangements referred to in Section 301 of the Companies Act, 1956 have been entered in the register required to be maintained under that section.

(b) In our opinion, and according to the information and explanations given to us, the transactions made in pursuance of contracts and arrangements referred to in (a) above and exceeding the value of Rs. 5 lakh with a party during the year have been made at a price which is reasonable having regard to the prevailing market prices at the relevant time.

(vi) According to the information and explanations given to us, the Company has not accepted any deposits from the public to which the directives issued by the Reserve Bank of India and the provisions of Section 58A, Section 58AA or any other relevant provisions of the Act and the rules framed there under apply.

(vii) In our opinion, the Company has an internal audit system commensurate with its size and nature of business.

(viii) The Central Government has not prescribed the maintenance of cost records under section 209(1) (d) of the Act for any of the activities conducted/services rendered by the Company. Accordingly para 4(viii) of the Order is not applicable.

5

HSBC Asset Management (India) Private Limited Annexure to Independent Auditors’ Report - 31 March 2014 (Continued) (ix) (a) According to the information and explanations given to us and on the basis of our

examination of the records of the Company, amounts deducted/accrued in the books of account in respect of undisputed statutory dues including provident fund, income tax, professional tax, service tax and other material statutory dues have been generally regularly deposited during the year except for few instances of delays in depositing dues of income taxes of an employee with the appropriate authorities. As explained to us, the Company did not have any dues on account of employees’ state insurance, sales tax, wealth tax, custom duty, excise duty, cess and investor education and protection fund.

(b) According to the information and explanations given to us, no undisputed amounts payable in respect of provident fund, income tax, professional tax, service tax, other material statutory dues were in arrears as at 31 March 2014 for a period of more than six months from the date they became payable.

(c) According to the information and explanations given to us, the following dues of Income-tax have not been deposited by the Company on account of disputes:

Name of the statute

Nature of dues

Amount (rupees in‘000)

Period to which the amount

relates

Forum where dispute is pending

Income Tax Act, 1961

Income tax 1,341 A.Y 2004-05 Appellate Tribunal

Income Tax Act, 1961 Income Tax Act, 1961

Income tax Income tax

15,042

5,034

A.Y 2007-08

AY 2008-09

Appellate Tribunal Appellate Tribunal

(x) The accumulated losses of the Company are less than fifty percent of the Company’s net worth. The Company has incurred cash losses during the current financial year and in the immediately preceding financial year of Rs. 61,660 thousand and Rs. 193,655 thousand respectively.

(xi) In our opinion and according to the information and explanations given to us, the Company did not have any outstanding dues to any financial institution, banks or debenture holders during the year.

(xii) The Company has not granted any loans and advances on the basis of security by way of pledge of shares, debentures and other securities.

(xiii) In our opinion and according to the information and explanation given to us, the Company is not a chit fund or a nidhi /mutual benefit fund/ society. Accordingly paragraph 4(xiii) of the Order is not applicable.

(xiv) According to the information and explanations given to us, the Company is not dealing or trading in shares, securities, debentures and other investments.

6

HSBC Asset Management (India) Private Limited Annexure to Independent Auditors’ Report - 31 March 2014 (Continued)

(xv) According to the information and explanations given to us, the Company has not given any guarantee for loans taken by others from banks or financial institutions.

(xvi) Based on our examination of the records of the Company and based on the information and explanation given to us, the Company has not taken any term loans during the year and accordingly paragraph 4 (xvi) of the order is not applicable to the Company.

(xvii) According to the information and explanations given to us and on an overall examination of the balance sheet of the Company, the Company has not raised any funds on short-term basis for the purpose of long-term investments.

(xviii) The Company has not made any preferential allotment of shares to companies/ firms/parties covered in the register maintained under Section 301 of the Act.

(xix) According to the information and explanations given to us, the Company has not issued any debentures during the year.

(xx) The Company has not raised any money by public issues during the year.

(xxi) According to the information and explanations given to us, no fraud on or by the Company has been noticed or reported during the year.

For B S R & Associates LLP Chartered Accountants Firm's Registration No: 116231W/W-100024 Sd/- N Sampath Ganesh Mumbai Partner 11 August 2014 Membership No: 042554

7

HSBC Asset Management (India) Private Limited

Balance Sheetas at 31 March 2014

(Currency: Indian Rupees in thousands)

Note 31 March 2014 31 March 2013EQUITY AND LIABILITIESShareholders' fundsShare capital 3 542,000 542,000Reserves and surplus 4 (10,885) 64,533

531,115 606,533

Non-current liabilitiesLong-term borrowings 5 3,824 4,096Long-term provisions 7 14,175 13,354

17,999 17,450

Current liabilitiesTrade payables 8 149,329 120,244Other current liabilities 9 79,743 61,787Short-term provisions 7 8,009 6,377

237,081 188,408

TOTAL 786,195 812,391

ASSETSNon-current assetsFixed assetsTangible assets 10.1 25,274 29,670Intangible assets 10.2 - -Long-term loans and advances 11 393,775 397,211

419,049 426,881

Current assetsCurrent investments 12 149,780 277,448Trade receivables 13 170,869 54,054Cash and bank balances 14 1,111 15,055Short-term loans and advances 11 45,386 38,953

367,146 385,510

TOTAL 786,195 812,391

Significant accounting policies 2 (0.10) 0.03

The notes referred to above form an integral part of the financial statements.As per our report of even date attached

For B S R & Associates LLP For and on behalf of the Board of Directors ofChartered Accountants HSBC Asset Management (India) Private LimitedFirm Registration No. 116231W/W-100024

Sd/- Sd/- Sd/-N Sampath Ganesh Naina Lal Kidwai Puneet ChaddhaPartner Chairperson Director &Membership No: 042554 Chief Executive OfficerMumbai

Sd/-

Denny ThomasCompany SecretaryMumbai11 August 2014

11 August 2014

8

HSBC Asset Management (India) Private Limited

Statement of Profit and Lossfor the year ended 31 March 2014

(Currency: Indian Rupees in thousands)

Note 31 March 2014 31 March 2013REVENUERevenue from operations 15 683,965 416,436Other income 16 36,731 15,374

Total revenue 720,696 431,810

EXPENSESEmployee benefits expenses 17 375,147 327,864Finance costs 18 2,036 1,994Depreciation and amortization 10 13,758 18,503Other expenses 19 303,458 295,607

Total expenses 694,399 643,968

Profit/ (Loss) before exceptional items and tax 26,297 (212,158)Exceptional items 19.3 101,715 -

Loss before tax (75,419) (212,158)Tax expense:

Deferred tax 6 - -

Loss for the year (75,419) (212,158)

Earnings per equity share [face value of share Rs 10]Basic and diluted 20.5 (1.39) (4.40)

Significant accounting policies 2

The notes referred to above form an integral part of the financial statements.As per our report of even date attached

For B S R & Associates LLP For and on behalf of the Board of Directors ofChartered Accountants HSBC Asset Management (India) Private LimitedFirm Registration No. 116231W/W-100024

Sd/- Sd/- Sd/-N Sampath Ganesh Naina Lal Kidwai Puneet ChaddhaPartner Chairperson Director &Membership No: 042554 Chief Executive OfficerMumbai11 August 2014 Sd/-

Denny ThomasCompany SecretaryMumbai11 August 2014

9

HSBC Asset Management (India) Private Limited

Cash flow statementfor the year ended 31 March 2014(Currency: Indian Rupees in thousands)

31 March 2014 31 March 2013

A Cash flow from operating activities

(Loss) before tax (75,419) (212,158)Adjustments for

Depreciation 13,758 18,503Interest expenses 1,036 933Loss on sale of fixed assets 652 1,131Unrealised foreign exchange losses 3,429 70Profit on sale of investments (30,446) (13,949)Dividend income - (587)

(11,571) 6,101

Operating (loss) before working capital changes (86,989) (206,057)

(Decrease) / increase in trade receivables (117,554) (9,216)(Decrease) / increase in loans and advances and other current assets (5,711) 23,635Increase / (decrease) in current liabilities and provisions 46,428 (748)

Cash generated from / (used in) operations (163,826) (192,387)

Income taxes paid (43,912) (39,697)Income tax refund received 46,631 -

Net cash used by operating activities ( A ) (161,107) (232,083)

B Cash flow from investing activitiesPurchase of fixed assets (10,056) (24,472)Proceeds from sale / (cost incurred for sale) of fixed assets 42 865Purchase of Mutual fund units (589,546) (1,199,419)Proceeds from sale of Mutual fund units 747,654 1,013,205Dividend income - 587

Net cash provided/ (used) by investing activities ( B ) 148,094 (209,234)

C Cash flow from financing activitiesPrincipal payment under finance leases (3,045) (3,670)Proceeds from finance leases 3,150 5,785Finance cost paid (1,036) (933)Proceeds from issue of equity shares - 452,000

Net cash provided/ (used) by financing activities ( C ) (931) 453,181

10

HSBC Asset Management (India) Private Limited

Cash flow statementfor the year ended 31 March 2014(Currency: Indian Rupees in thousands)

31 March 2014 31 March 2013

Net (decrease) / increase in cash and cash equivalents (A) + (B) + (C) (13,944) 11,864

Cash and cash equivalents at the beginning of the year 15,055 3,191Cash and cash equivalents at the end of the year 1,111 15,055

Net (decrease) / increase in cash and cash equivalents (13,944) 11,864

(0.40) (0.88)NoteCash and cash equivalents comprise of cash on hand, balances with banks in current accounts.

(Refer Note 14 of the financial statements)

The notes referred to above form an integral part of the financial statements.

As per our report of even date attached

For B S R & Associates LLP For and on behalf of the Board of Directors of

Chartered Accountants HSBC Asset Management (India) Private Limited

Firm Registration No. 116231W/W-100024

Sd/- Sd/- Sd/-

N Sampath Ganesh Naina Lal Kidwai Puneet Chaddha

Partner Chairperson Director &

Membership No: 042554 Chief Executive Officer

Mumbai

11 August 2014 Sd/-

Denny Thomas

Company Secretary

Mumbai

11 August 2014

11

HSBC Asset Management (India) Private Limited

Notes to financial statementsfor the year ended 31 March 2014(Currency: Indian Rupees in thousands)

1. Background

2. Significant Accounting Policies

2.1 Basis of preparation of financial statements

2.2 Use of estimates

2.3 Current-non-current classification

All assets and liabilities are classified into current and non-current.

AssetsAn asset is classified as current when it satisfies any of the following criteria:

(a) it is expected to be realised in, or is intended for sale of consumption in, the company's normal operating cycle;(b) it is held primarily for the purpose of being traded;(c) it is expected to be realised within 12 months after the reporting date; or(d) it is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least 12 months after the reporting date.

Current assets include the current portion of non-current financial assets.All other assets are classified as non-current.

LiabilitiesA liability is classified as current when it satisfies any of the following criteria:

(a) it is expected to be settled in the company’s normal operating cycle;(b) it is held primarily f or the purpose of being traded(c) it is due to be settled within 12 months after the reporting date; or

Current liabilities include current portion of non-current financial liabilities. All other liabilities are classified as non-current.

Operating cycleOperating cycle is the time between the acquisition of assets for processing and their realisation in cash or cash equivalents.

2.4 Fixed assets and depreciation

Motor Cars As per the lease tenure or on the basis of technical evaluation of the useful life whichever is less

Computers 40.00%

Office Equipment 25.00%

Furniture and Fittings 25.00%

Assets costing less than Rs. 10,000 are fully depreciated in the year of purchase.

2.5 Impairment of assets