39

HSBC Holding plc Account Development Plan For Client A

HSBC Holding plc

Account Development Plan

For Client A

2 © Evalueserve. All rights reserved.

Contents

01 A Brief Summary 3

02 Sector & Company Overview 6

03 Organization Structure 17

04 Strategy 23

05 ICT Landscape 29

06 Opportunities for Client A 33

A Brief Summary

4 © Evalueserve. All rights reserved.

HSBC – A Brief Summary (1/2)

HSBC Business Strategy• Founded in 1865, HSBC serves 47m customers in 71 countries through its ~4,700 offices• As part of its business restructuring plan, HSBC sold its operations in Brazil during 2016. It is also reducing its retail branches in India and

concentrating on the most profitable regions.• For geographic expansion, HSBC plans to target Asia (especially China), the US, and Mexico.• For cost savings, the company has disposed off its low-returning portfolios. It also has planned heavy reduction in its workforce, relying on IT

automation– HSBC has started an initiative to re-engineer IT and operations to target cost saving of USD4.5-5.0bn over 2015–2017. It includes FTE

reduction by 22,000–25,000 over the period.

IT Organization & Outlook• The company follows a decentralized IT structure and IT decisions are led by the CIOs of the respective geographies.• The IT stakeholders within the company, are currently fairly happy with their current set of vendors, including those in Storage, Virtualization,

Cloud, Application Software and others.• Stickiness to the current vendors and disinterest in pursuing new vendors such as Veeam and Splunk highlights their conservative approach

towards IT

Focus Areas• The company started pursuing a Digital Transformation agenda and is hoping that Social Network Banking, BlockChain Technology will be the

next drivers for its growth.• Analytics is another area of focus for the company to improve its processes for customer acquisition and customer experience.• To improve collaboration among employees, HSBC NOW 2.0 and Social Directory are in place. The company plans to further invest in tools and

applications to assist employees in productivity gains• Cybersecurity has gained importance owing to the cyber attacks in Aug-2015 and Jan-2016

5 © Evalueserve. All rights reserved.

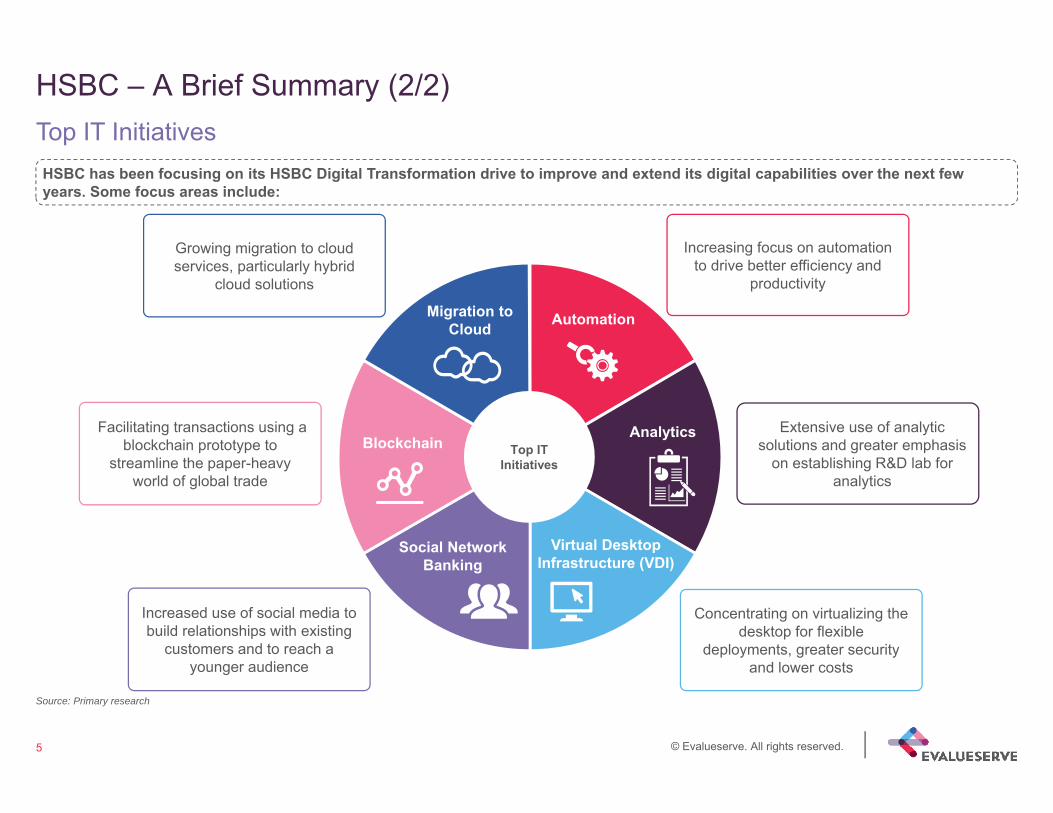

HSBC – A Brief Summary (2/2)

HSBC has been focusing on its HSBC Digital Transformation drive to improve and extend its digital capabilities over the next fewyears. Some focus areas include:

Top IT Initiatives

AnalyticsBlockchain

Migration to Cloud

Social Network Banking

Automation

Virtual Desktop Infrastructure (VDI)

Top IT Initiatives

Growing migration to cloud services, particularly hybrid

cloud solutions

Facilitating transactions using a blockchain prototype to

streamline the paper-heavy world of global trade

Increased use of social media to build relationships with existing

customers and to reach a younger audience

Increasing focus on automation to drive better efficiency and

productivity

Extensive use of analytic solutions and greater emphasis

on establishing R&D lab for analytics

Concentrating on virtualizing the desktop for flexible

deployments, greater security and lower costs

Source: Primary research

Sector & Company Overview

7 © Evalueserve. All rights reserved.

Sector Overview: Market Size, Growth and Key Players

Source: Various company annual reports / MarketLine industry reports / OneSource / Yahoo Finance, accessed on 02 Nov 2016

Global sector size, growth and outlook• Over 2009–2014, overall assets in the global banking sector increased steadily at a CAGR of 4.9%. Return on average equity of global banks

increased 2.6 pp to 10.3% in 2015 from 2008. • Over 2015–2018, the asset value of banks is expected to grow at a CAGR of 7.2%, from USD139.2tn to USD171.7tn. In 2013,

– Europe accounted for USD57.3tn of the banking assets the highest in the world. Within Europe, France and the UK hold the majority of the assets.

• Global investment banking services fees increased 7% y-o-y to reach USD90.1bn in 2014. This is the strongest annual period for fees since 2007 (USD104.2bn).

• As per Moody’s Global Banking Outlook 2016, European and US banks will continue to tighten their bad loan portfolio causing a reduction in early-stage delinquencies for most asset classes. The report also anticipated moderate asset quality deterioration in some Asian banking systems.

Firmographics

Other prominent banking companies globally include Wells Fargo, ICBC, China Construction Bank, Banco Santander, Mitsubishi UFJ Financial, Royal Bank of Canada, Lloyds Banking Group, UBS Group, ING Group, Deutsche Bank, Credit Suisse Group, Standard Chartered, SocieteGenerale and Royal Bank of Scotland.

Market cap comparison of leading banking companies globally (USDbn)

41.464.1

139.5157.1

168.2249.1

Sector definition

Banking sector comprises activities of banks and similar institutions, which offer savings, loans, mortgages, and related financial services to consumers and businesses. The value of the market is calculated in terms of the value of the assets held by the banks.It includes financial institutions that offer investment banking and brokerage services. The value of the market is calculated in terms of the revenue generated.

8 © Evalueserve. All rights reserved.

Banking Sector: ICT spending trends and growth drivers

Source: Industry reports / * The banking industry is part of the financial services sector

ICT Spending will continue to grow moderately in the banking sectorICT spending trends for the global banking sector

• The total IT spending for banking institutions across N. America, Europe, Asia-Pacific, and Latin America is expected to grow to USD241bn in 2016, 3.9% higher than in 2015.

• Retail and wholesale banking in N. America is expected to experience a steady increase in amount of money spent on technology.

• In Europe, IT spending is expected to grow across all banking solutions.

• In Asia, banks are continuing to update their business models to adapt to new regulations and employ innovative technologies.

Growth drivers for ICT in retail banking sector• Growth in new technologies for business optimization: A large number of banks plan to invest in agile analytics solutions, data

warehousing/marts, and real-time business intelligence and CRM applications in the next two years. They also plan to integrate offline distribution channels with online ones. Both these factors would increase their ICT spending.

• Adoption of hybrid cloud: Banks are increasingly moving to cloud-based services through partnerships with vendors such as IBM, Microsoft, and HP. They plan to use public cloud services for less critical applications and keep critical applications in a private cloud.

• Catering to changing consumer preferences: Traditional banking methods have become outdated. To cater to changing consumer preferences, banks have been developing new products and services, and restructuring and streamlining operations. This is increasing the demand for IT systems and capabilities.

• Increased focus on operational efficiency and cost reduction: Many major global banks are trying to reduce their operating costs by increasing their ICT expenditure. Select key investment areas are data warehousing, claims and policy administration systems, time-to-market, and staff costs.

220.9231.6

241.0250.6

261.4

2014 2015 2016e 2017e 2018e

ICT Spending in Global Banking Sector, USDbn

ICT

spen

ding

in g

loba

l ba

nkin

g se

ctor

9 © Evalueserve. All rights reserved.

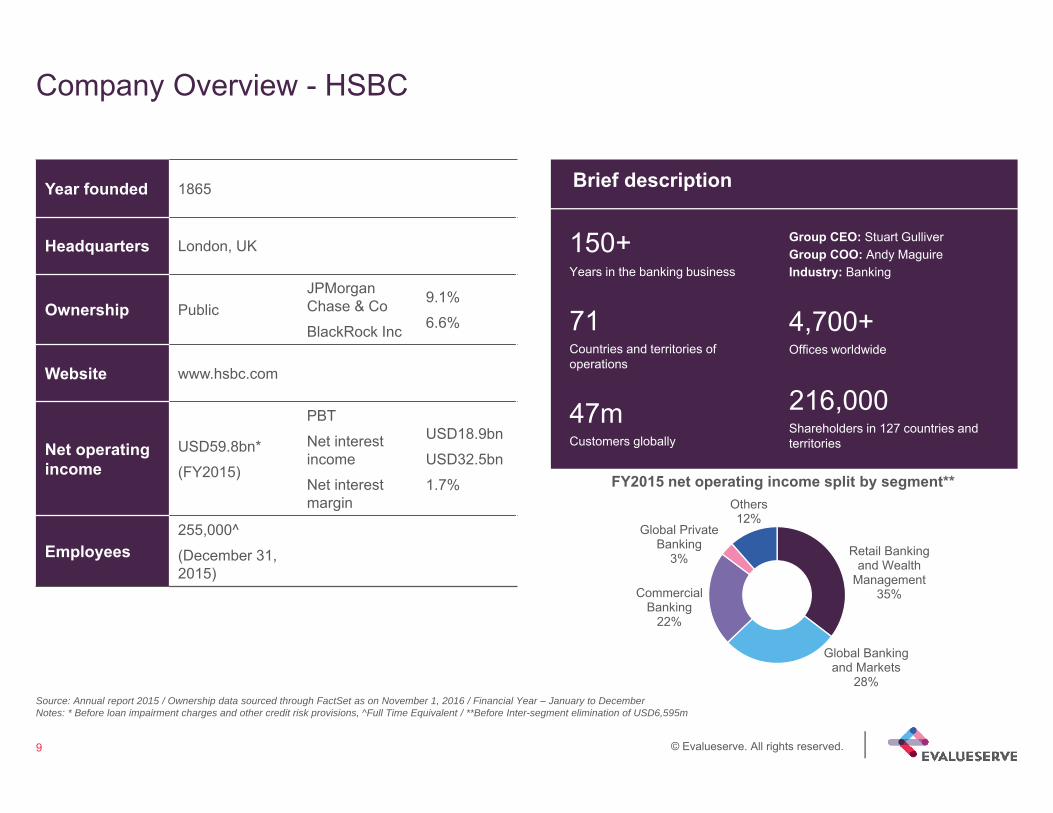

Company Overview - HSBC

Source: Annual report 2015 / Ownership data sourced through FactSet as on November 1, 2016 / Financial Year – January to DecemberNotes: * Before loan impairment charges and other credit risk provisions, ^Full Time Equivalent / **Before Inter-segment elimination of USD6,595m

Year founded 1865

Headquarters London, UK

Ownership PublicJPMorgan Chase & CoBlackRock Inc

9.1%6.6%

Website www.hsbc.com

Net operating income

USD59.8bn*(FY2015)

PBTNet interest incomeNet interest margin

USD18.9bnUSD32.5bn1.7%

Employees255,000^(December 31, 2015)

Brief description

Countries and territories of operations

71

150+Years in the banking business

Group CEO: Stuart GulliverGroup COO: Andy MaguireIndustry: Banking

216,000Shareholders in 127 countries and territories

47mCustomers globally

Offices worldwide

4,700+

Retail Banking and Wealth

Management35%

Global Banking and Markets

28%

Commercial Banking

22%

Global Private Banking

3%

Others12%

FY2015 net operating income split by segment**

10 © Evalueserve. All rights reserved.

HSBC – Business Segments

Source: Annual report 2015*Revenue and OPEX mentioned are the adjusted revenue taking into consideration currency translation and significant items.

Retail Banking and Wealth Management (RBWM) Commercial Banking (CMB) Global Banking and Markets

(GB&M)Global Private Banking (GPB)

Overview

Provides a range of personal banking and wealth management products and services to individual clients.

Provides banking solutions to address the need of its corporate clients. The segment has a presence in about 55 countries and territories.

Provides financial products and services to the corporate and institutional clients across 50 countries.

Offers banking and investment solutions to high net worth clients.

Products and Services

Retail banking, wealth management, asset management and insurance

Working capital, term loans, payment services and international trade facilitation, among other services such as professional services around M&A, and provide access to financial markets

Transaction banking, financing, advisory, capital markets and risk management

Tailored private banking, investment and wealth management services

Key figures

Net Operating Income: USD23.5bn

OPEX: USD12.1bn

Net Operating Income:USD14.9bn

OPEX: USD4.3bn

Net Operating Income:USD18.2bn

OPEX: USD7.1bn

Net Operating Income:USD2.1bn

OPEX: USD1.2bn

11 © Evalueserve. All rights reserved.

HSBC – Geographic Footprint

Source: Strategic report 2015*Net operating income excludes Intra-HSBC items worth USD3,375m

47.1%

26.5%

15.6%

7.7%3.2%

40.0%

33.0%

12.0%

4.0%10.0%

No. of employees – FY2015 Net operating income – FY2015*

EuropeAsia

Latin AmericaNorth AmericaMiddle East and Africa

Canada

US

Mexico

UK

France

Germany

Egypt

Saudi Arabia

UAE

India

Mainland China

Taipei, Taiwan

Hong Kong

Australia

IndonesiaSingapore

Singapore

HeadquartersPriority Markets

12 © Evalueserve. All rights reserved.

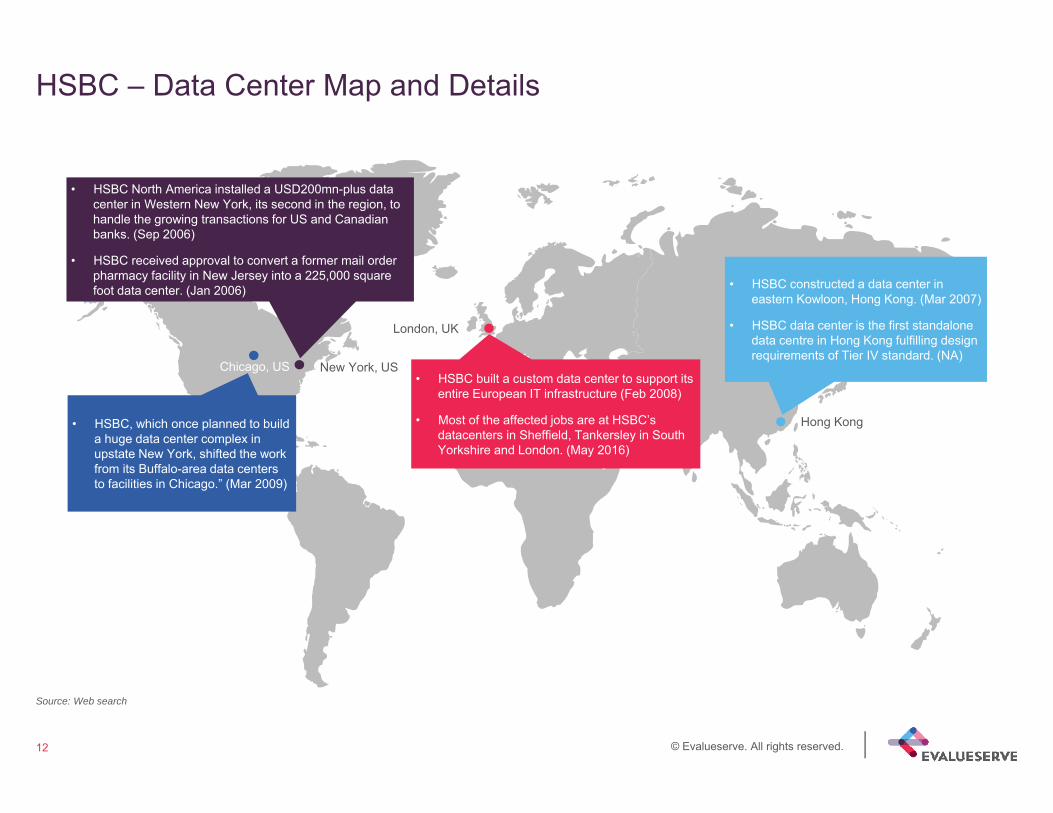

HSBC – Data Center Map and Details

Source: Web search

Hong Kong

London, UK

• HSBC built a custom data center to support its entire European IT infrastructure (Feb 2008)

• Most of the affected jobs are at HSBC’s datacenters in Sheffield, Tankersley in South Yorkshire and London. (May 2016)

New York, USChicago, US

• HSBC North America installed a USD200mn-plus data center in Western New York, its second in the region, to handle the growing transactions for US and Canadian banks. (Sep 2006)

• HSBC received approval to convert a former mail order pharmacy facility in New Jersey into a 225,000 square foot data center. (Jan 2006)

• HSBC, which once planned to build a huge data center complex in upstate New York, shifted the work from its Buffalo-area data centers to facilities in Chicago.” (Mar 2009)

• HSBC constructed a data center in eastern Kowloon, Hong Kong. (Mar 2007)

• HSBC data center is the first standalone data centre in Hong Kong fulfilling design requirements of Tier IV standard. (NA)

13 © Evalueserve. All rights reserved.

HSBC – Detailed Financials (1/2)

Revenue Overview, 2013-2016, USD Billion Financial Stability Overview

• Revenue in FY15 was USD59.8bn, 2% lower when compared with the 2014 number

• FY16 revenue is expected to decline due to deteriorating economic conditions in Hong Kong and the UK, two of the bank’s main markets

• Revenue in FY15 benefited from a favorable movement in significant items but was offset by the adverse effect of currency translation amounting to USD4.8bn– USD1.4bn gain in revenue was achieved as a result of the partial

sale of shareholding in Industrial Bank– Also, a lower provisions and charges relating to the ongoing

review of compliance with the Consumer Credit Act in the UK resulted in revenue gain in FY15

FY15 Results – Key Highlights• HSBC reported a moderate increase in its operating margins,

implying an improvement in its ability to cater to fixed expenses• RoE shows a steady decline in line with a decrease in net margins –

many financial institutions (who were earlier invested in HSBC) have revisited their positions as a result of this

• NII remained stable when compare with in FY14; however, a negative NII implies bank’s interest expenses were more than returns produced as a result of weak investment climate in its areas of operation

• EPS decreased during 2013-15 period, as dividend per ordinary share increased during the period

64.6 61.2 59.8 52.1

17.8

14.7 15.1

0

5

10

15

20

0.0

20.0

40.0

60.0

80.0

100.0

FY13 FY14 FY15 FY16 - Estimate

Revenue Net Income

Profitability ratios* FY13 FY14 FY15Operating Margin (%) 25.8 21.6 22.9Net Margin (%) 25.1 18.4 17.7Free Cash Flow Growth (%) 1953.0 -99.6 35.3Return on Equity (RoE) (%) 9.2 7.3 7.2Net Int Inc & Other (NII) (%) -7.5 -5.2 -5.2Other ratios 2013 2014 2015EPS (USD) 0.84 0.69 0.65

Free Cash Flow/Sales (%) 14.7 13.8 12.8Operating Margin (%) 25.8 21.6 22.9

Source: Annual report, Web search / Financial year: Jan - Dec

14 © Evalueserve. All rights reserved.

HSBC – Detailed Financials (2/2)

Source: Annual report, Web search

Revenue by Business Segment, FY14 vs FY15 PBT by Business Segment, FY14 vs FY15 (USD mn)

Segments FY14 FY15 Trend

RBWM 5,581 4,967 11.0%

CMB 8,814 7,973 9.5%

GB&M 5,889 7,910 34.3%

GPB 626 344 45.0%

Others -2,230 -2,327 4.3%

0%20%40%60%80%

100%

FY14 FY15OthersGlobal Private Banking (GPB)Global Banking & Markets (GB&M)Commercial Banking (CMB)Retail Banking & Wealth Management (RBWM)

5.6%

2.6%

8.6%

19.5%YoY Growth

6.5%

YoY decline is depicted in Red font

Revenue by Geography, FY15 Revenue by Geography, FY14 vs FY15

21,058

25,303

2,565

7,657

6,592

Europe Asia Middle East and North Africa North America Latin America

0%

20%

40%

60%

80%

100%

FY14 FY15Europe Asia MENA N. America Latin America

6.9%

0.7%

6.1%

20.3%

YoY Growth

2.4%

YoY decline is depicted in Red font

$61.2bn $59.8bn

15 © Evalueserve. All rights reserved.

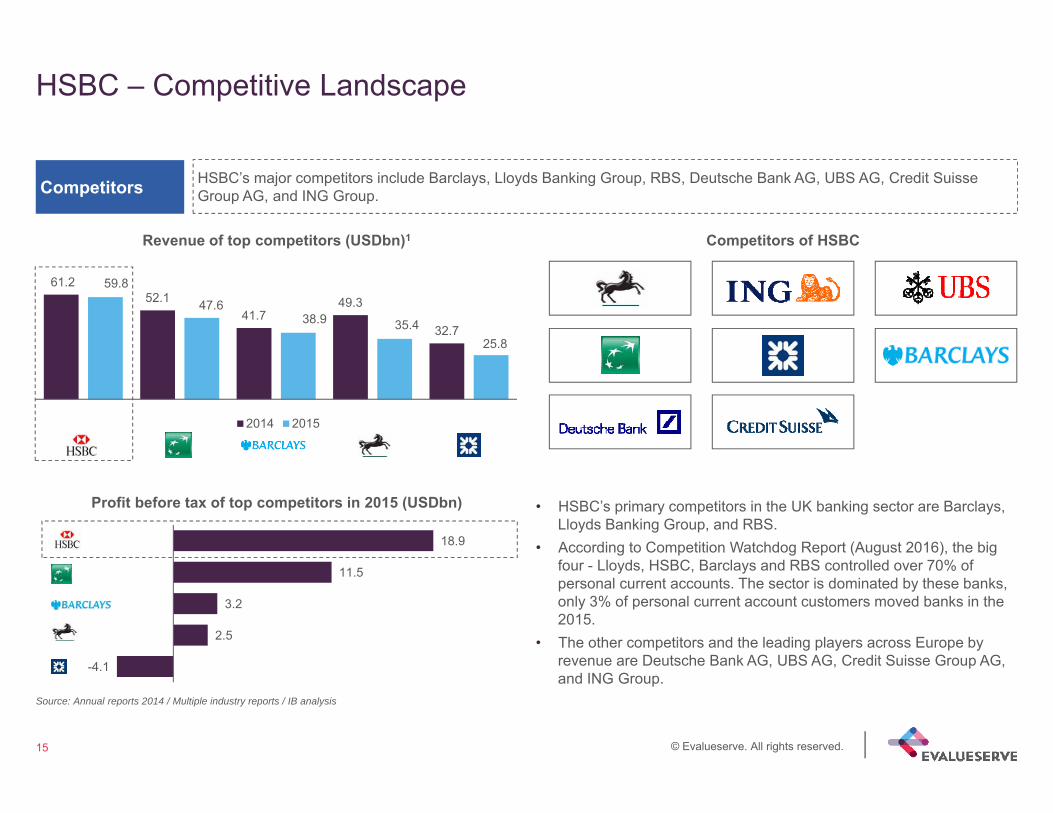

HSBC – Competitive Landscape

Competitors HSBC’s major competitors include Barclays, Lloyds Banking Group, RBS, Deutsche Bank AG, UBS AG, Credit Suisse Group AG, and ING Group.

61.2 52.1

41.749.3

32.7

59.8

47.638.9 35.4

25.8

2014 2015

Revenue of top competitors (USDbn)1 Competitors of HSBC

Profit before tax of top competitors in 2015 (USDbn)

-4.1

2.5

3.2

11.5

18.9

• HSBC’s primary competitors in the UK banking sector are Barclays, Lloyds Banking Group, and RBS.

• According to Competition Watchdog Report (August 2016), the big four - Lloyds, HSBC, Barclays and RBS controlled over 70% of personal current accounts. The sector is dominated by these banks, only 3% of personal current account customers moved banks in the 2015.

• The other competitors and the leading players across Europe by revenue are Deutsche Bank AG, UBS AG, Credit Suisse Group AG, and ING Group.

Source: Annual reports 2014 / Multiple industry reports / IB analysis

16 © Evalueserve. All rights reserved.

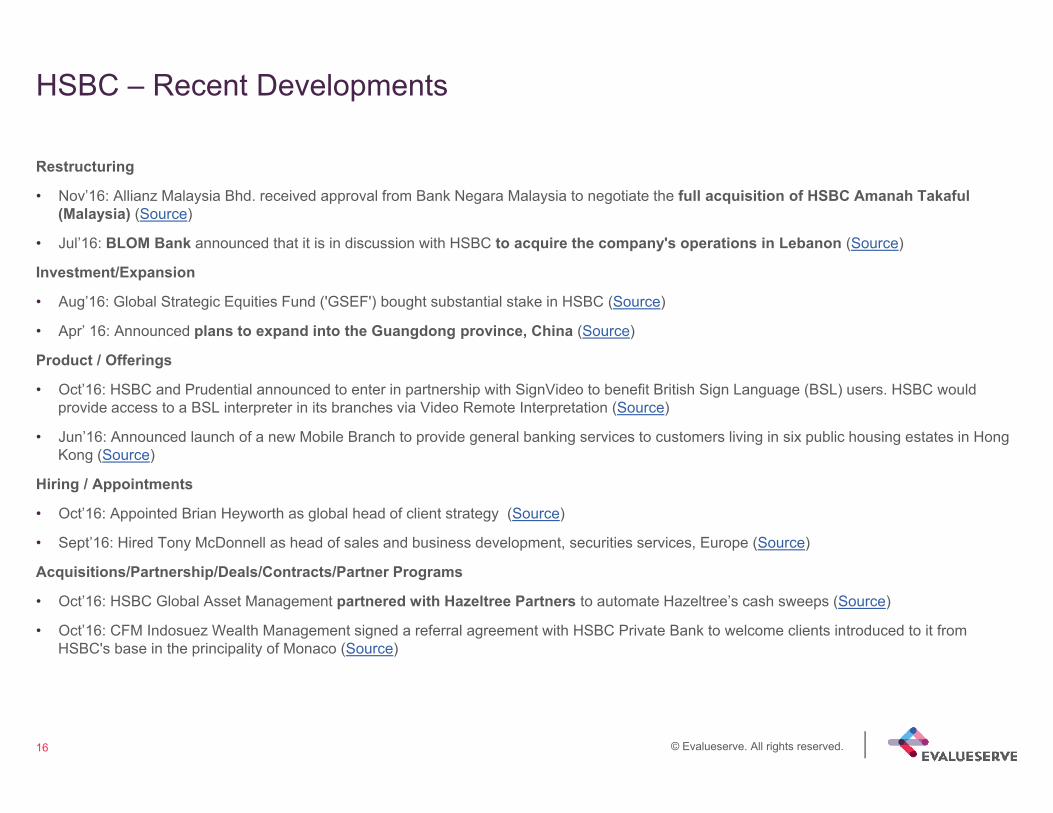

HSBC – Recent Developments

Restructuring

• Nov’16: Allianz Malaysia Bhd. received approval from Bank Negara Malaysia to negotiate the full acquisition of HSBC Amanah Takaful (Malaysia) (Source)

• Jul’16: BLOM Bank announced that it is in discussion with HSBC to acquire the company's operations in Lebanon (Source)

Investment/Expansion

• Aug’16: Global Strategic Equities Fund ('GSEF') bought substantial stake in HSBC (Source)

• Apr’ 16: Announced plans to expand into the Guangdong province, China (Source)

Product / Offerings

• Oct’16: HSBC and Prudential announced to enter in partnership with SignVideo to benefit British Sign Language (BSL) users. HSBC would provide access to a BSL interpreter in its branches via Video Remote Interpretation (Source)

• Jun’16: Announced launch of a new Mobile Branch to provide general banking services to customers living in six public housing estates in Hong Kong (Source)

Hiring / Appointments

• Oct’16: Appointed Brian Heyworth as global head of client strategy (Source)

• Sept’16: Hired Tony McDonnell as head of sales and business development, securities services, Europe (Source)

Acquisitions/Partnership/Deals/Contracts/Partner Programs

• Oct’16: HSBC Global Asset Management partnered with Hazeltree Partners to automate Hazeltree’s cash sweeps (Source)

• Oct’16: CFM Indosuez Wealth Management signed a referral agreement with HSBC Private Bank to welcome clients introduced to it from HSBC's base in the principality of Monaco (Source)

Organization Structure

18 © Evalueserve. All rights reserved.

HSBC – Corporate Structure

Source: Company website / *MENA – Middle East and North AfricaNote: At 31 Dec 2015. All entities wholly owned unless shown otherwise (part ownership rounded down to nearest per cent) / Excludes other Associates, Insurance companies and Special Purpose Entities

AsiaMENA*EuropeN. AmericaLatin America

HSBC Holdings plc

HSBC Latin America

Holdings (UK) Limited

HSBC Latin America BV

HSBC Overseas

Holdings (UK) Limited

HSBC Bank Canada

HSBC Bank plc

HSBC Private Banking Holdings

(Suisse) S.A.

HSBC Bank Egypt S.A.E

HSBC Holdings BV

HSBC Bank Argentina S.A.

HSBC North America

Holdings Inc.

HSBC Private Bank (Suisse)

S.A.

The Saudi British Bank

HSBC Mexico SA

HSBC Investments

(North America) Inc.

HSBC Finance Corporation HSBC France

HSBC Bank Middle East

Limited

HSBC Asia Holdings (UK)

Limited

The Hongkong and Shanghai

Banking Corporation

Ltd

HSBC Bank (China) Co.

Limited

HSBC Securities (USA) Inc.

HSBC Trinkaus &

Burkhardt AG

HSBC Bank Malaysia Berhad

HSBC Bank (Taiwan) Limited

HSBC USA Inc.

HSBC Bank USA, N.A.

HSBC Bank Australia Limited

Bank of Communi-cationa Co

Limited

Hang Seng Bank Limited

Hang Seng Bank (China)

Limited

Holding company

Intermediate holding company

Operating company

Associate

62% PRC

HK

19%

HK

94%

40%

Germany

80%

99%

UK

USA

99%

UK

19 © Evalueserve. All rights reserved.

HSBC – Executive committee

Source: Company website

Executive and CEO Leadership

Douglas FlintGroup Chairman

Peter BoylesChief Executive, Global Private

Banking

Samir AssafChief Executive, Global Banking

and Markets

Patrick J BurkePresident and

CEO, HSBC US

Simon CooperChief Executive,

Global Commercial

Banking

Stuart GulliverGroup CEO

Iain MackayGroup Finance

Director

Ben MathewsGroup Company

Secretary

Andy MaguireGroup COO

Pam KaurGroup Head ofInternal Audit

Pierre GoadGroup Head of

employee insight & communications

Stuart Levey Chief Legal Officer

John Flint Chief Executive, Retail Banking

and Wealth Management

Peter WongChief Executive, The Hong Kong and Shanghai Banking Corp

Marc MosesExecutive Director and

Group Chief Risk OfficerExec

utiv

e Le

ader

ship

CEO

Lea

ders

hip

Antonio SimoesCEO, HSBC

Bank plc

Paulo MaiaCEO, Latin

America, HSBC and Executive

Chairman, HSBC Mexico

Noel QuinnChief Executive,

Global Commercial

Banking

20 © Evalueserve. All rights reserved.

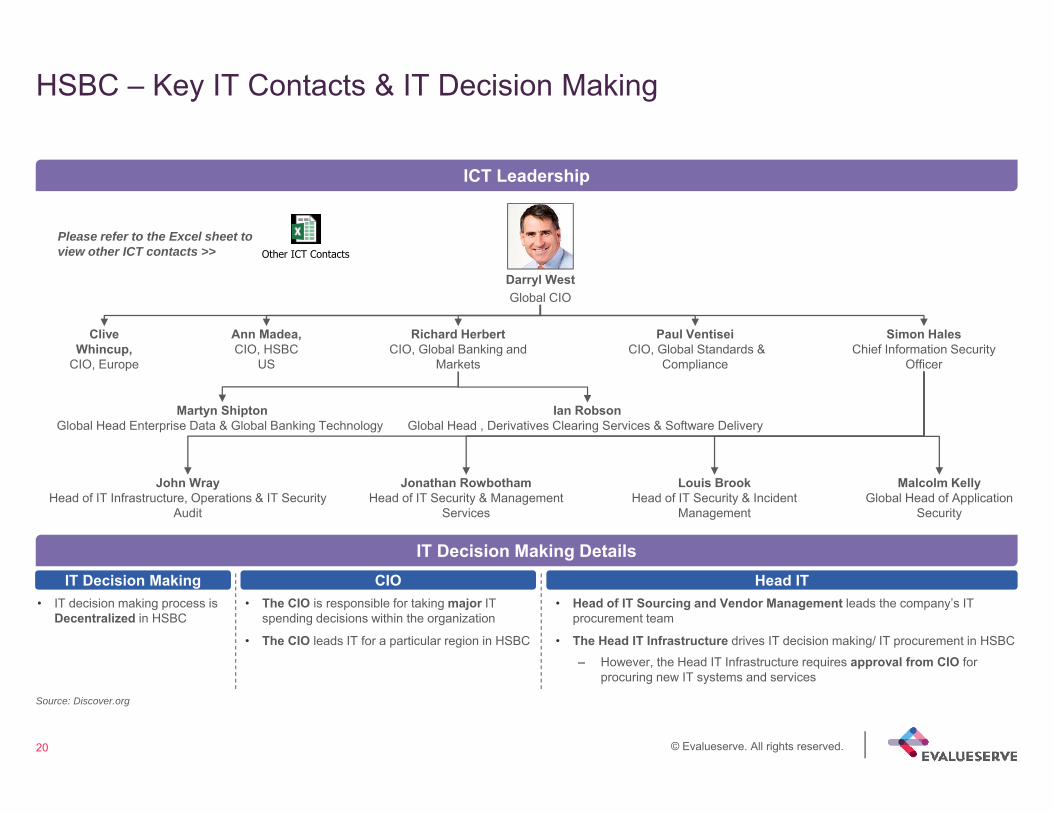

HSBC – Key IT Contacts & IT Decision Making

Source: Discover.org

ICT Leadership

Clive Whincup,

CIO, Europe

Darryl WestGlobal CIO

Please refer to the Excel sheet to view other ICT contacts >>

Ann Madea, CIO, HSBC

US

Other ICT Contacts

Richard Herbert CIO, Global Banking and

Markets

Ian Robson Global Head , Derivatives Clearing Services & Software Delivery

Martyn ShiptonGlobal Head Enterprise Data & Global Banking Technology

Paul VentiseiCIO, Global Standards &

Compliance

Simon HalesChief Information Security

Officer

John WrayHead of IT Infrastructure, Operations & IT Security

Audit

Jonathan RowbothamHead of IT Security & Management

Services

Malcolm KellyGlobal Head of Application

Security

Louis BrookHead of IT Security & Incident

Management

• The CIO is responsible for taking major IT spending decisions within the organization

• The CIO leads IT for a particular region in HSBC

• Head of IT Sourcing and Vendor Management leads the company’s IT procurement team

• The Head IT Infrastructure drives IT decision making/ IT procurement in HSBC– However, the Head IT Infrastructure requires approval from CIO for

procuring new IT systems and services

• IT decision making process is Decentralized in HSBC

IT Decision Making DetailsIT Decision Making CIO Head IT

21 © Evalueserve. All rights reserved.

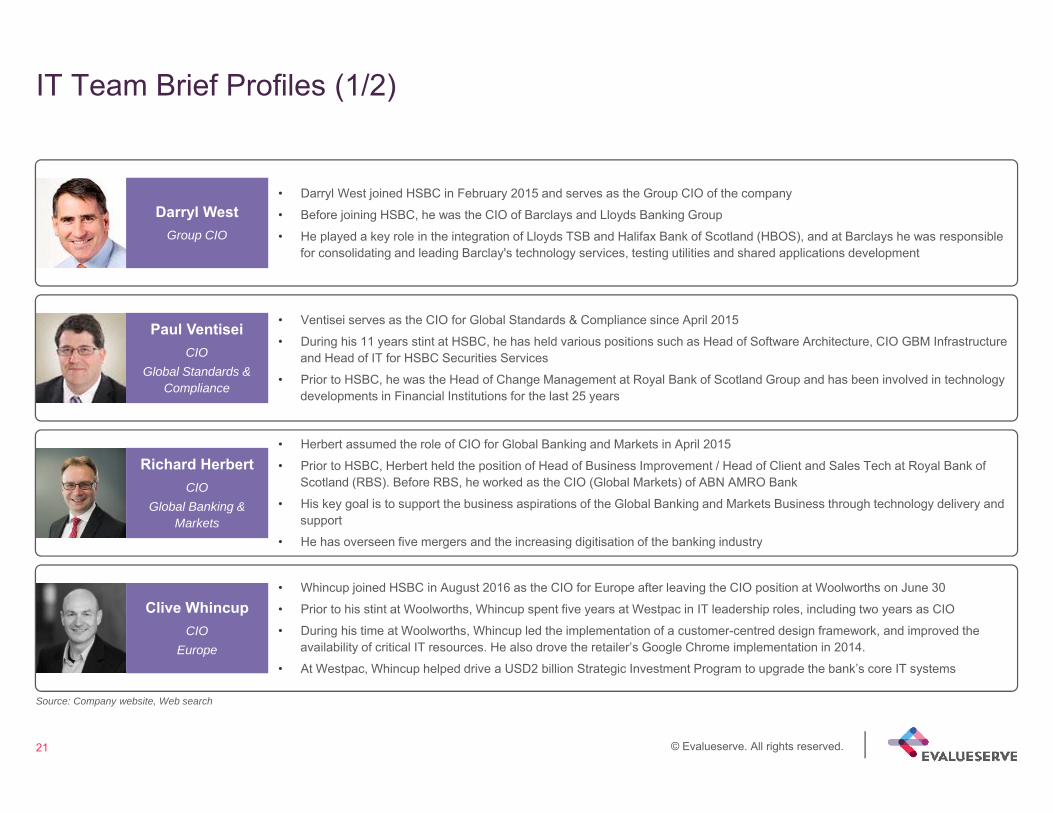

Paul VentiseiCIO

Global Standards & Compliance

IT Team Brief Profiles (1/2)

• Darryl West joined HSBC in February 2015 and serves as the Group CIO of the company

• Before joining HSBC, he was the CIO of Barclays and Lloyds Banking Group

• He played a key role in the integration of Lloyds TSB and Halifax Bank of Scotland (HBOS), and at Barclays he was responsiblefor consolidating and leading Barclay's technology services, testing utilities and shared applications development

Darryl WestGroup CIO

• Ventisei serves as the CIO for Global Standards & Compliance since April 2015

• During his 11 years stint at HSBC, he has held various positions such as Head of Software Architecture, CIO GBM Infrastructure and Head of IT for HSBC Securities Services

• Prior to HSBC, he was the Head of Change Management at Royal Bank of Scotland Group and has been involved in technology developments in Financial Institutions for the last 25 years

• Herbert assumed the role of CIO for Global Banking and Markets in April 2015

• Prior to HSBC, Herbert held the position of Head of Business Improvement / Head of Client and Sales Tech at Royal Bank of Scotland (RBS). Before RBS, he worked as the CIO (Global Markets) of ABN AMRO Bank

• His key goal is to support the business aspirations of the Global Banking and Markets Business through technology delivery and support

• He has overseen five mergers and the increasing digitisation of the banking industry

Richard HerbertCIO

Global Banking & Markets

• Whincup joined HSBC in August 2016 as the CIO for Europe after leaving the CIO position at Woolworths on June 30

• Prior to his stint at Woolworths, Whincup spent five years at Westpac in IT leadership roles, including two years as CIO

• During his time at Woolworths, Whincup led the implementation of a customer-centred design framework, and improved the availability of critical IT resources. He also drove the retailer’s Google Chrome implementation in 2014.

• At Westpac, Whincup helped drive a USD2 billion Strategic Investment Program to upgrade the bank’s core IT systems

Clive WhincupCIO

Europe

Source: Company website, Web search

22 © Evalueserve. All rights reserved.

Key IT Executives in Media

Source: Company Website, Web search

Our voices and fingerprints are unique, with physical and behavioral characteristics almostimpossible to mimic. While this is the largest roll out of voice ID in the U.K. banking, otherindustries will soon follow our lead

In February 2016 On deploying biometric security tools

~Tracy Garrad, CEO, First Direct Online Banking Division, HSBC

We’re going to restructure the cost base of the bank by digitising everything. We are on amission to take every customer interaction and every process of the bank and digitise thewhole thing. There will be no paper

In September 2016 On the progress towards digitalization

~Darryl West, CIO, HSBC

We’ve done some amazing things already, we’ve focused on ‘mobile first’ strategy for ourcustomer interactions, we’ve launched Apple Pay and Android Pay which have provedenormously popular in the markets where they’re available. We have WeChat integrationunderway in the Pearl River Delta

In September 2016 On the progress towards digitalization ~Darryl West, CIO, HSBC

The new R3 globally accessible lab environment is enabling both R3 and member banks tocollaborate technically on experiments related to shared ledger and smart contractstechnology. As demonstrated by the first project that is already up and running, this labplatform will aid faster experimentation, provide technical agility and aid learning greatly

In January 2016 On teaming up for cloud-based distributed ledger ~Richard Herbert, CIO, Global Banking and Markets, HSBC

“

“

“““

““

“Media Quotes and Priority

Strategy

24 © Evalueserve. All rights reserved.

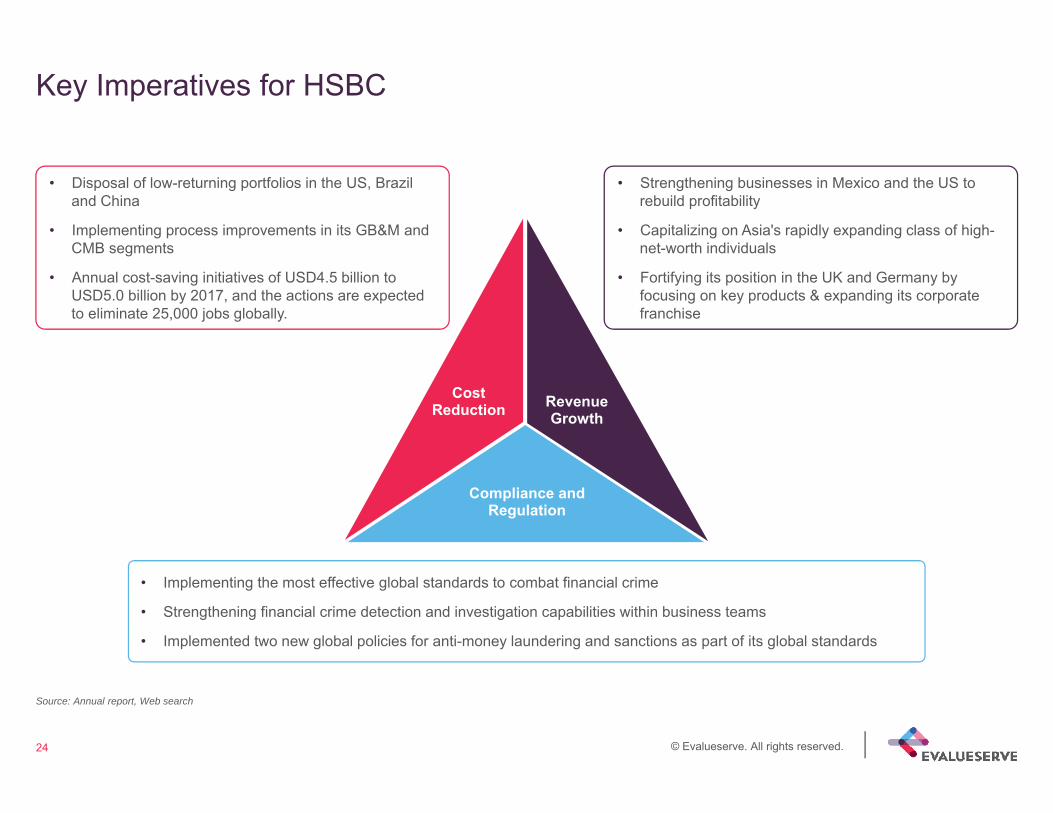

Key Imperatives for HSBC

Cost Reduction Revenue

Growth

Compliance and Regulation

• Disposal of low-returning portfolios in the US, Brazil and China

• Implementing process improvements in its GB&M and CMB segments

• Annual cost-saving initiatives of USD4.5 billion to USD5.0 billion by 2017, and the actions are expected to eliminate 25,000 jobs globally.

• Strengthening businesses in Mexico and the US to rebuild profitability

• Capitalizing on Asia's rapidly expanding class of high-net-worth individuals

• Fortifying its position in the UK and Germany by focusing on key products & expanding its corporate franchise

• Implementing the most effective global standards to combat financial crime

• Strengthening financial crime detection and investigation capabilities within business teams

• Implemented two new global policies for anti-money laundering and sanctions as part of its global standards

Source: Annual report, Web search

25 © Evalueserve. All rights reserved.

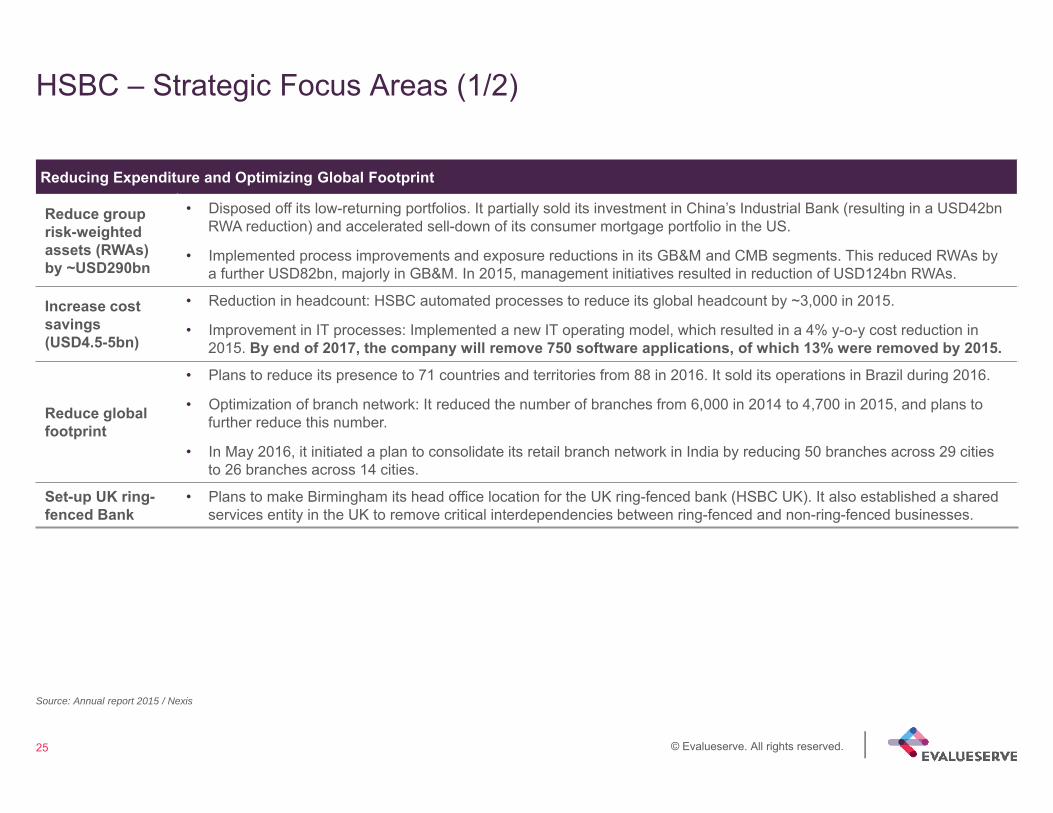

HSBC – Strategic Focus Areas (1/2)

Source: Annual report 2015 / Nexis

Reducing Expenditure and Optimizing Global Footprint

Reduce group risk-weighted assets (RWAs) by ~USD290bn

• Disposed off its low-returning portfolios. It partially sold its investment in China’s Industrial Bank (resulting in a USD42bn RWA reduction) and accelerated sell-down of its consumer mortgage portfolio in the US.

• Implemented process improvements and exposure reductions in its GB&M and CMB segments. This reduced RWAs by a further USD82bn, majorly in GB&M. In 2015, management initiatives resulted in reduction of USD124bn RWAs.

Increase cost savings(USD4.5-5bn)

• Reduction in headcount: HSBC automated processes to reduce its global headcount by ~3,000 in 2015.

• Improvement in IT processes: Implemented a new IT operating model, which resulted in a 4% y-o-y cost reduction in 2015. By end of 2017, the company will remove 750 software applications, of which 13% were removed by 2015.

Reduce global footprint

• Plans to reduce its presence to 71 countries and territories from 88 in 2016. It sold its operations in Brazil during 2016.

• Optimization of branch network: It reduced the number of branches from 6,000 in 2014 to 4,700 in 2015, and plans to further reduce this number.

• In May 2016, it initiated a plan to consolidate its retail branch network in India by reducing 50 branches across 29 cities to 26 branches across 14 cities.

Set-up UK ring-fenced Bank

• Plans to make Birmingham its head office location for the UK ring-fenced bank (HSBC UK). It also established a shared services entity in the UK to remove critical interdependencies between ring-fenced and non-ring-fenced businesses.

26 © Evalueserve. All rights reserved.

HSBC – Strategic Focus Areas (2/2)

Source: Annual report 2015 / Nexis

Increased focus on key growth markets and Asia

Invest in key growth markets

• UK and Hong Kong: The bank aims to strengthen and develop its position in the UK and Hong Kong, its home market, focusing on key products, such as mortgages and personal lending.

• China: Mainland China continues to be of strategic significance to the bank. It is therefore continuing to invest in organic growth, particularly in Guangdong and other economically important regions.

• US and Germany: The bank continues to improve its position in the US and Germany by expanding its corporate franchise. In 2014, it broadened its customer base by enhancing products, widening its geographical coverage, and adjusting its risk appetite.– In the US, it is focusing on selling transaction banking products. It witnessed a 9% increase in Global Trade and

Receivables Finance in 2015. – Along with the segment focus, it is consolidating data centers and moving to lower-cost office locations.

• Mexico: In Mexico, it is concentrating on RBWMs as its revenue grew by 7% y-o-y in 2015. The growth is faster than expected in the cards, mortgages, and personal loans markets.

Expand in Asia

• HSBC plans to capitalize on Asia's rapidly expanding class of high-net-worth individuals and grow its asset management and insurance businesses.

• The bank aims to capture market in China’s Pearl River Delta (PRD) and also in the ASEAN region especially in Singapore, Malaysia, and Indonesia.– In Dec. 2015, the bank announced plans to establish a management team in Guangdong and appointed He Shunhua

as the Executive President. – Also, in November 2015, HSBC agreed to set up an onshore JV securities firm with Shenzhen Qianhai Financial

Holdings. Through the JV, it plans to engage in securities and investment banking business in China.

27 © Evalueserve. All rights reserved.

HSBC – Go-to-Market Strategy

Source: Web search

Go-to-market strategy

Proactive use of social media for Marketing

• HSBC leverages social media to increase their presence in key growth markets and aims to increase customers for its Advance account.

• It launched Social Hub to showcase digital content on social media and attract new customers by allowing them to create their own film to thank their family and friends on Social Hub.

Leverage digital marketing to boost customer retention

• Bank uses search engine optimization (SEO) and pay-per-click to direct people to its website and use banner ads that will enable prospective customers to get quotes within the ads without having to leave the site.

• In 2015, it launched TV campaign for its Advance Account aimed to show how people’s support networks can help to achieve their ambitions, backed up with message to promote the benefits of its products and improve brand advocacy

Use Sponsored content to establish key global connections

• HSBC leverages sponsored content to promote its interactive Trade Forecast tool which provide latest trends in world trade– Uses the 1-7-30-4-2-1 rule in which HSBC use the combination of daily articles from the Global Connections

community combined with quarterly releases of the Trade Forecast tool

Host events, conferences and roadshows to promote products and services

• In 2016, the bank hosted roadshows such as Pearl River Delta Investor and Analyst Roadshow, Global Banking and Markets - Investor update, ESG update to update their investors on company’s financial performance and recent product launch

• In 2016, it attended Retail Banking and Wealth Management - Goldman Sachs European Financials Conference

28 © Evalueserve. All rights reserved.

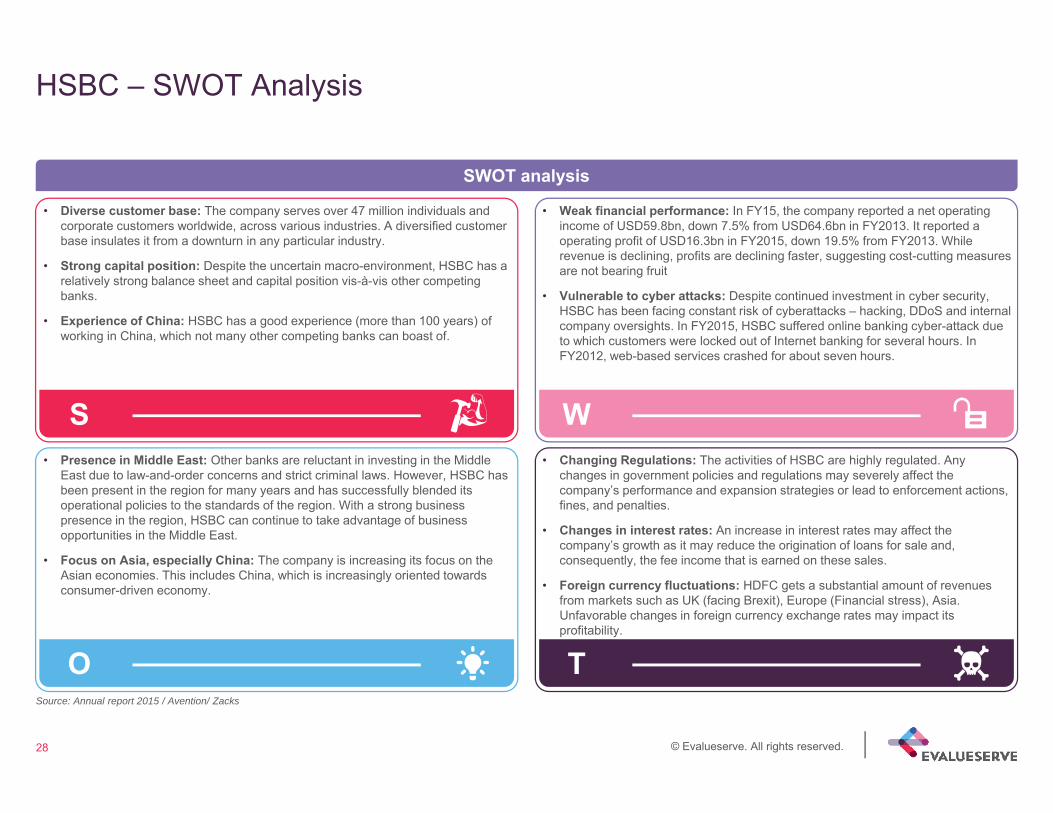

HSBC – SWOT Analysis

Source: Annual report 2015 / Avention/ Zacks

S

O

W

T

• Diverse customer base: The company serves over 47 million individuals and corporate customers worldwide, across various industries. A diversified customer base insulates it from a downturn in any particular industry.

• Strong capital position: Despite the uncertain macro-environment, HSBC has a relatively strong balance sheet and capital position vis-à-vis other competing banks.

• Experience of China: HSBC has a good experience (more than 100 years) of working in China, which not many other competing banks can boast of.

• Presence in Middle East: Other banks are reluctant in investing in the Middle East due to law-and-order concerns and strict criminal laws. However, HSBC has been present in the region for many years and has successfully blended its operational policies to the standards of the region. With a strong business presence in the region, HSBC can continue to take advantage of business opportunities in the Middle East.

• Focus on Asia, especially China: The company is increasing its focus on the Asian economies. This includes China, which is increasingly oriented towards consumer-driven economy.

• Weak financial performance: In FY15, the company reported a net operating income of USD59.8bn, down 7.5% from USD64.6bn in FY2013. It reported a operating profit of USD16.3bn in FY2015, down 19.5% from FY2013. While revenue is declining, profits are declining faster, suggesting cost-cutting measures are not bearing fruit

• Vulnerable to cyber attacks: Despite continued investment in cyber security, HSBC has been facing constant risk of cyberattacks – hacking, DDoS and internal company oversights. In FY2015, HSBC suffered online banking cyber-attack due to which customers were locked out of Internet banking for several hours. In FY2012, web-based services crashed for about seven hours.

• Changing Regulations: The activities of HSBC are highly regulated. Any changes in government policies and regulations may severely affect the company’s performance and expansion strategies or lead to enforcement actions, fines, and penalties.

• Changes in interest rates: An increase in interest rates may affect the company’s growth as it may reduce the origination of loans for sale and, consequently, the fee income that is earned on these sales.

• Foreign currency fluctuations: HDFC gets a substantial amount of revenues from markets such as UK (facing Brexit), Europe (Financial stress), Asia. Unfavorable changes in foreign currency exchange rates may impact its profitability.

SWOT analysis

ICT Landscape

30 © Evalueserve. All rights reserved.

HSBC – ICT budget and key ICT facts

Source: Press search / IB analysis

ICT budget

HSBC’s estimated ICT budget is USD5.5bn.(9.2% of net operating income in 2015)

Key ICT facts• IT Layoffs: In May 2016, the company started the process of laying off 840 IT employees, in the UK. These jobs will be outsourced to Poland, China and India. The

restructuring is planned to be completed by end of 2017.• Development work migration to low cost markets: In 2015, 50% of the software development at HSBC was done in India and China. Under the bank’s new strategy, the

percentage is expected to rise to 75%.• Vendor Consolidation: By June 2015, five tech suppliers accounted for 50% of HSBC’s business, while about 4,000 providers accounted for the remaining 50%. The bank aims

to have four key suppliers that would account for over 80% of its business.• In 2014–2015, HSBC’s compliance team developed new processes for vendor management and risk management. The team planned the strategy and analytics for the

company's US regulatory compliance area and developed new regulatory compliance systems.

% o

f tot

al IC

T sp

end

Communications / Networking

40.2%

Services & Outsourcing

24.0%

Software17.0%

Hardware16.8%

Storage1.6%

Other0.4%

Key ICT facts – Procurement• The day-to-day procurement of goods and services is managed by HSBC’s Procurement Department. • In 2009, the company updated its supplier code of conduct to lay emphasis on social, environmental, and economic aspects of sustainability.• Its suppliers are required to fill in a Supplier Registration Form as a part of its supplier relationship management process.• The company favors partnerships with local suppliers.

31 © Evalueserve. All rights reserved.

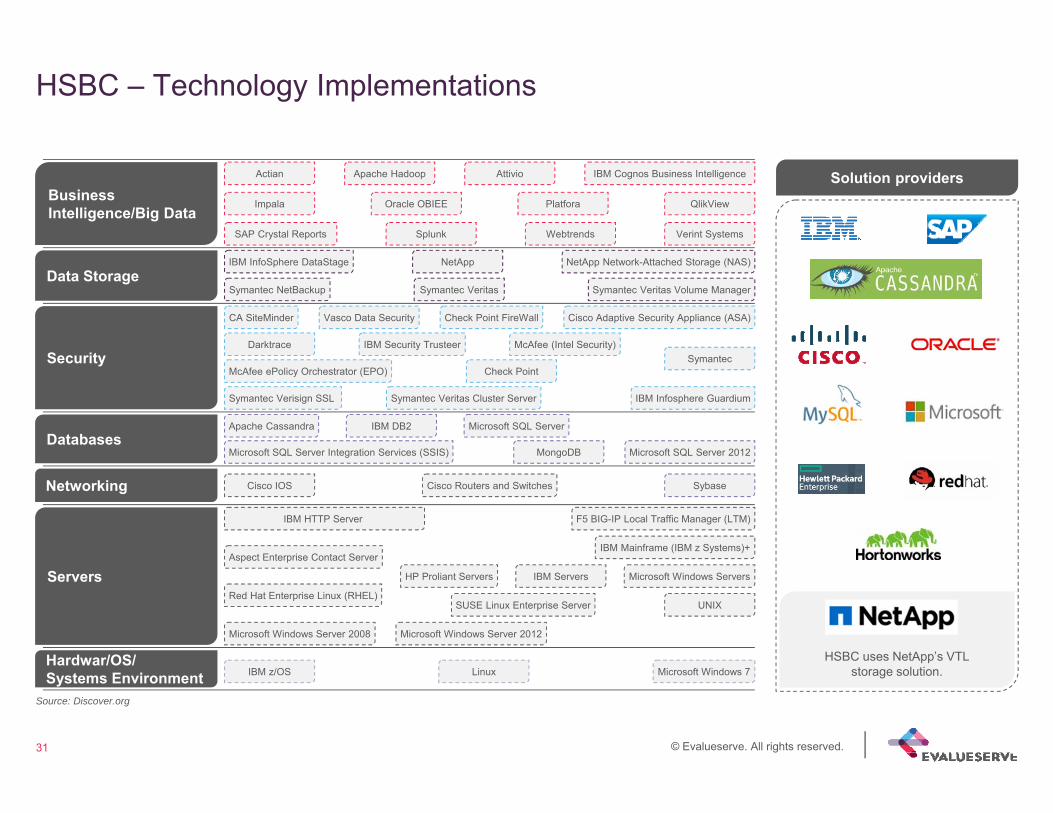

HSBC – Technology Implementations

Source: Discover.org

Solution providers

HSBC uses NetApp’s VTL storage solution.

BusinessIntelligence/Big Data

Data Storage

Security

Databases

Networking

Servers

Hardwar/OS/Systems Environment

McAfee ePolicy Orchestrator (EPO)

Cisco IOS

IBM z/OS

Actian

Linux

McAfee (Intel Security)

IBM Servers

Red Hat Enterprise Linux (RHEL)SUSE Linux Enterprise Server

Microsoft Windows 7

Platfora

IBM InfoSphere DataStage

HP Proliant Servers

Apache Cassandra IBM DB2 Microsoft SQL Server

Microsoft SQL Server 2012Microsoft SQL Server Integration Services (SSIS)

Sybase

Aspect Enterprise Contact Server

UNIX

Microsoft Windows Servers

Apache Hadoop Attivio

Impala Oracle OBIEE QlikView

SAP Crystal Reports

IBM Cognos Business Intelligence

Splunk Verint Systems

MongoDB

SymantecDarktrace

IBM Infosphere Guardium

IBM Security Trusteer

NetApp Network-Attached Storage (NAS)NetApp

Symantec Veritas Volume ManagerSymantec VeritasSymantec NetBackup

Webtrends

Cisco Adaptive Security Appliance (ASA)CA SiteMinder

Check Point

Check Point FireWallVasco Data Security

Cisco Routers and Switches

F5 BIG-IP Local Traffic Manager (LTM)IBM HTTP Server

IBM Mainframe (IBM z Systems)+

Microsoft Windows Server 2008 Microsoft Windows Server 2012

Symantec Verisign SSL Symantec Veritas Cluster Server

32 © Evalueserve. All rights reserved.

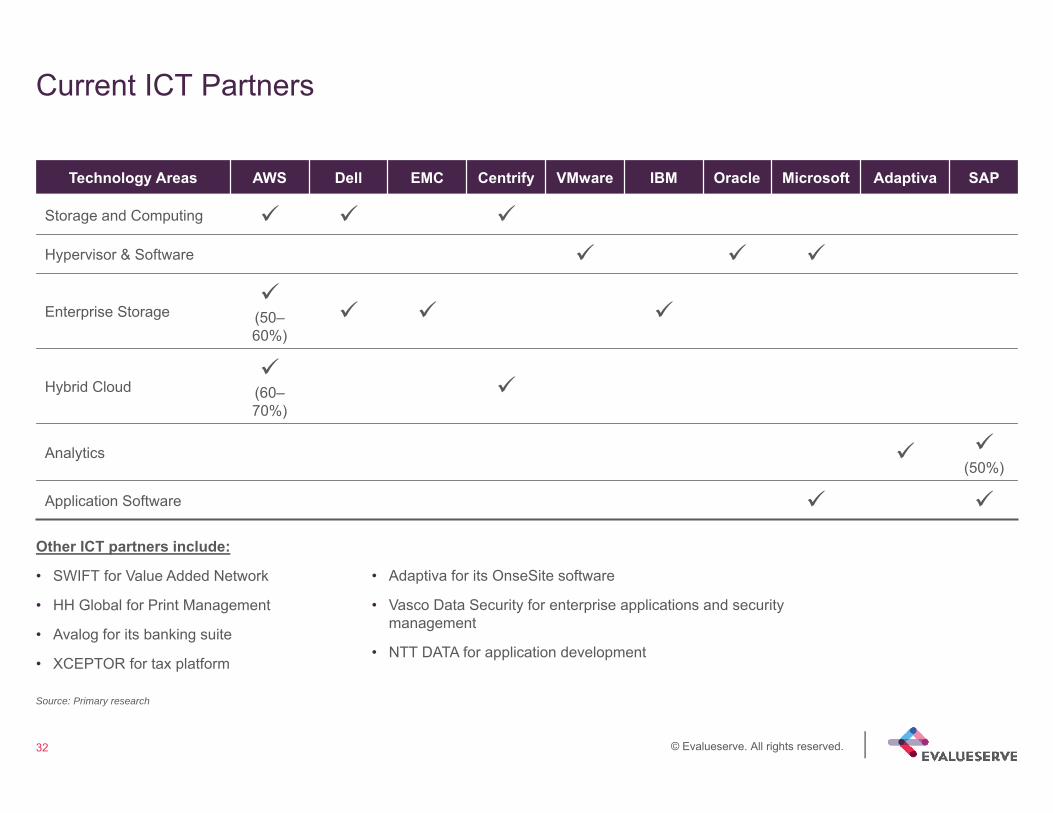

Current ICT Partners

Source: Primary research

Technology Areas AWS Dell EMC Centrify VMware IBM Oracle Microsoft Adaptiva SAP

Storage and Computing

Hypervisor & Software

Enterprise Storage

(50–60%)

Hybrid Cloud

(60–70%)

Analytics (50%)

Application Software

Other ICT partners include:

• SWIFT for Value Added Network

• HH Global for Print Management

• Avalog for its banking suite

• XCEPTOR for tax platform

• Adaptiva for its OnseSite software

• Vasco Data Security for enterprise applications and security management

• NTT DATA for application development

Opportunities for Client A

34 © Evalueserve. All rights reserved.

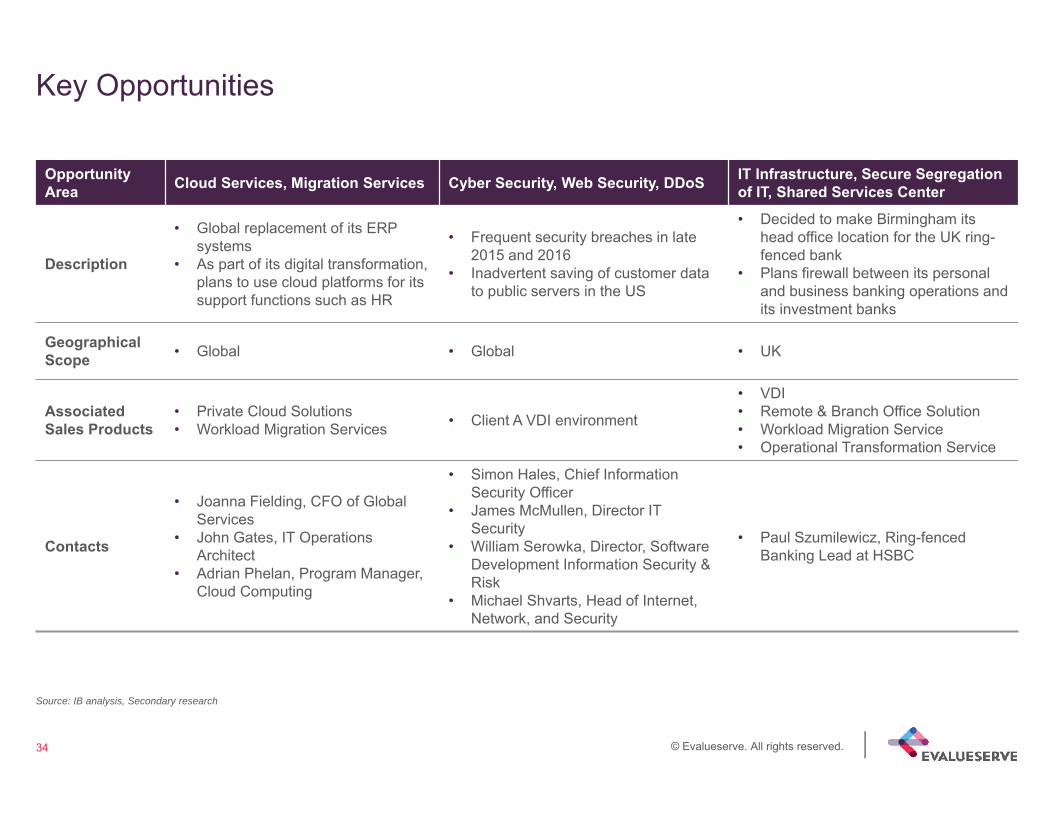

Key Opportunities

Source: IB analysis, Secondary research

Opportunity Area Cloud Services, Migration Services Cyber Security, Web Security, DDoS IT Infrastructure, Secure Segregation

of IT, Shared Services Center

Description

• Global replacement of its ERP systems

• As part of its digital transformation, plans to use cloud platforms for its support functions such as HR

• Frequent security breaches in late 2015 and 2016

• Inadvertent saving of customer data to public servers in the US

• Decided to make Birmingham its head office location for the UK ring-fenced bank

• Plans firewall between its personal and business banking operations and its investment banks

Geographical Scope • Global • Global • UK

Associated Sales Products

• Private Cloud Solutions• Workload Migration Services • Client A VDI environment

• VDI• Remote & Branch Office Solution• Workload Migration Service• Operational Transformation Service

Contacts

• Joanna Fielding, CFO of Global Services

• John Gates, IT Operations Architect

• Adrian Phelan, Program Manager, Cloud Computing

• Simon Hales, Chief Information Security Officer

• James McMullen, Director IT Security

• William Serowka, Director, Software Development Information Security & Risk

• Michael Shvarts, Head of Internet, Network, and Security

• Paul Szumilewicz, Ring-fenced Banking Lead at HSBC

35 © Evalueserve. All rights reserved.

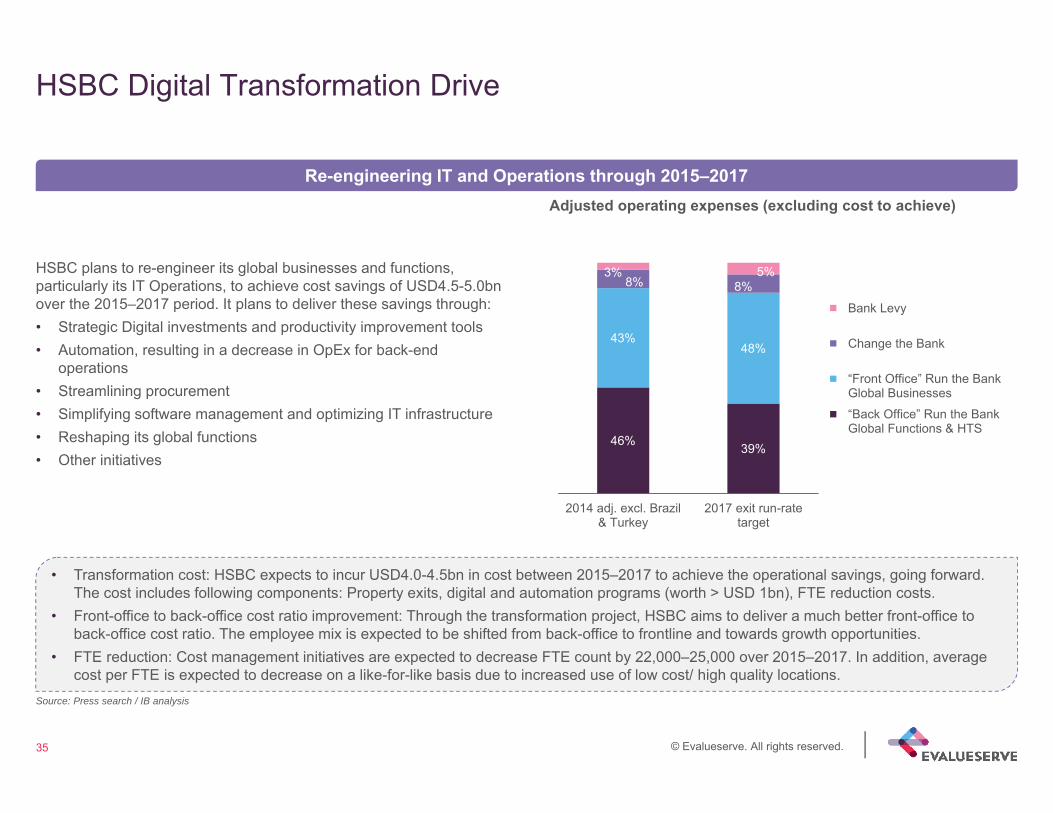

HSBC Digital Transformation Drive

Source: Press search / IB analysis

Re-engineering IT and Operations through 2015–2017

HSBC plans to re-engineer its global businesses and functions, particularly its IT Operations, to achieve cost savings of USD4.5-5.0bn over the 2015–2017 period. It plans to deliver these savings through:• Strategic Digital investments and productivity improvement tools• Automation, resulting in a decrease in OpEx for back-end

operations• Streamlining procurement • Simplifying software management and optimizing IT infrastructure• Reshaping its global functions• Other initiatives

46% 39%

43%48%

8% 8%3% 5%

2014 adj. excl. Brazil& Turkey

2017 exit run-ratetarget

Bank Levy

Change the Bank

“Front Office” Run the Bank Global Businesses“Back Office” Run the Bank Global Functions & HTS

• Transformation cost: HSBC expects to incur USD4.0-4.5bn in cost between 2015–2017 to achieve the operational savings, going forward. The cost includes following components: Property exits, digital and automation programs (worth > USD 1bn), FTE reduction costs.

• Front-office to back-office cost ratio improvement: Through the transformation project, HSBC aims to deliver a much better front-office to back-office cost ratio. The employee mix is expected to be shifted from back-office to frontline and towards growth opportunities.

• FTE reduction: Cost management initiatives are expected to decrease FTE count by 22,000–25,000 over 2015–2017. In addition, average cost per FTE is expected to decrease on a like-for-like basis due to increased use of low cost/ high quality locations.

Adjusted operating expenses (excluding cost to achieve)

36 © Evalueserve. All rights reserved.

Other HSBC Initiatives (1/2)

Source: Press search / IB analysis

Use of Data Analytics• Uses data analysis to provide tablet-based tools to frontline staff, develop digital product origination, and enhance trading of foreign currencies.

Usage extended to identify inconsistent processes, benchmark performance, and map the customer journey.• Deployed data analysis to improve customer service. It combined data from channel analytics with information about when to contact a customer

and what to contact them about. The tool helped the bank acquire new customers, enhance existing customer relationships, and retain profitable customers over the long term.

• Extended the use of SAS Fraud Management for real-time credit and debit card fraud detection to the UK and Asia. • Tested a new consumer mobile app using real-time analytics and 'nudge theory’ to identify trends in user spending habits. The app will use this

data to send targeted nudges, or alerts, to inform users about their expenditure patterns.• In 2015, invested in Platfora, for data cleansing. It then processes the data in an in-memory database and provides a visualization layer.• In 2015, Douglas Flint, group chairman, announced that HSBC will increase investment in data analytics to prevent regulatory failings.

HSBC NOW 2.0 – A Collaborative Project• Multi-lingual internal Web application available for employees around the globe. This project is composed of multiple portals focused on one

synchronized user experience leveraging the SSO feature of SharePoint. Besides allowing the employees to track their tasks and work hours, the system is also a document repository with out of-the-box (OOTB) and custom workflows for document approvals.

• Includes migration of the existing internal application, developed using IBM’s Lotus Notes, to Microsoft’s SharePoint 2013.• Includes Yammer to provide an enterprise social network for employees. In 2014, the company started offering additional online authentication to

improve its security system.

Social Directory• A read-only ASP.NET MVC 5 Web application that uses the SharePoint User Profile Service (UPS) as the data source. It enables employees to

search for a colleague anywhere in the globe based on the employee’s first name, last name, email address, department or branch location.

37 © Evalueserve. All rights reserved.

Other HSBC Initiatives (2/2)

Source: Press search / IB analysis

BlockChain Project• Partnered with Bank of America and Singapore government’s IT and telecom agency, Infocomm Development Authority of Singapore (IDA) , on a

project that applies blockchain to trade finance.• The planned blockchain application uses Hyperledger protocol to replicate the letter of credit (LC) transaction process between banks, exporters

and importers.• The proof-of-concept involves a seven-step process showcasing data authentication using distributed-ledger system.

Cybersecurity• In Feb 2016, the company introduced voice pattern recognition for online banking for its retail banking operation and First Direct customers in the

UK• The company’s Financial System Vulnerabilities Committee mentions cybersecurity as one of its key focus areas owing to recent incidents such

as– In Jan 2016, HSBC online banking crashed after a cyber attack. The attack was a denial of service attack, in which the attackers prevented

people from using the online service by overloading it with huge numbers of requests and web traffic, forcing the system to crash. – In Apr 2015, HSBC Finance Corporation acknowledged that its database of mortgage customers has been breached and personal account

information was exposed.

38 © Evalueserve. All rights reserved.

The information contained in this report has been obtained from reliable sources. The output is in accordance with the information available on such sources and has been carried out to the best of our knowledge with utmost care and precision. While Evalueserve has no reason to believe that there is any inaccuracy or defect in such information, Evalueserve disclaims all warranties, expressed or implied, including warranties of accuracy, completeness, correctness, adequacy, merchantability and / or fitness of the information.

Evalueserve Disclaimer

39 © Evalueserve. All rights reserved.

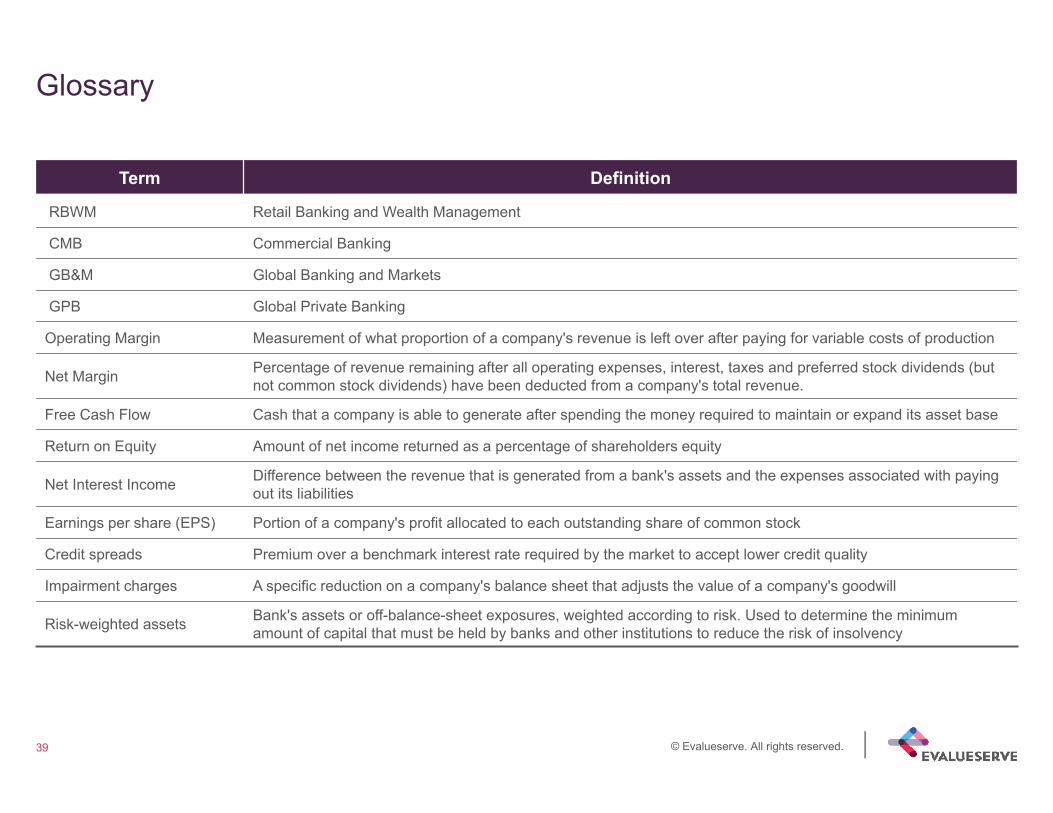

Glossary

Term Definition

RBWM Retail Banking and Wealth Management

CMB Commercial Banking

GB&M Global Banking and Markets

GPB Global Private Banking

Operating Margin Measurement of what proportion of a company's revenue is left over after paying for variable costs of production

Net Margin Percentage of revenue remaining after all operating expenses, interest, taxes and preferred stock dividends (but not common stock dividends) have been deducted from a company's total revenue.

Free Cash Flow Cash that a company is able to generate after spending the money required to maintain or expand its asset base

Return on Equity Amount of net income returned as a percentage of shareholders equity

Net Interest Income Difference between the revenue that is generated from a bank's assets and the expenses associated with paying out its liabilities

Earnings per share (EPS) Portion of a company's profit allocated to each outstanding share of common stock

Credit spreads Premium over a benchmark interest rate required by the market to accept lower credit quality

Impairment charges A specific reduction on a company's balance sheet that adjusts the value of a company's goodwill

Risk-weighted assets Bank's assets or off-balance-sheet exposures, weighted according to risk. Used to determine the minimum amount of capital that must be held by banks and other institutions to reduce the risk of insolvency