47

General Mathematics HSC Mathematics General 2 Course Stage 6 FM5 Annuities and loan repayments Distance Education Mathematics Network, Rural and Distance Education

FM5 Annuities and loan repayments 0

General Mathematics

HSC Mathematics General 2 Course

Stage 6

FM5 Annuities and loan repayments

Distance Education Mathematics Network, Rural and Distance Education

FM5 Annuities and loan repayments 0

Acknowledgements

Writer: Mandi Sutherland, Sydney Distance Education High School Editors: Mathematics staff at Camden Haven High School, Dubbo School of Distance Education, Karabar High School, Southern Cross School and Sydney Distance Education High School © Distance Education Mathematics Network, Rural and Distance Education, NSW Department of Education and Communities, April 2013. We thank the following owners of copyright material for permission to reproduce their work.

• Board of Studies Mathematics General Stage 6 Syllabus 2012

• Learning Materials Production, Open Training and Education Network - Distance Education, NSW Department of Education and Training 2002

FM5 Annuities and loan repayments 1

Introduction ...................................................................................................... 3 1.1 Annuities ................................................................................................. 4

1.2 Future value annuities ............................................................................. 5 Future value of an annuity formula .................................................................................. 7

Future value interest factor tables .................................................................................... 8

1.3 Present value annuities ......................................................................... 13 Present value of an annuity formula .............................................................................. 15

Present value interest factor tables ................................................................................ 16

1.4 Paying off a loan ................................................................................... 19 1.5 Home loans ........................................................................................... 21 1.6 Graphing loan repayments .................................................................... 25 Increasing repayments ................................................................................................... 25

A sudden windfall ........................................................................................................... 26

Monthly vs. fortnightly repayments ................................................................................ 27

1.7 Additional fees and charges .................................................................. 31 Stamp duty ..................................................................................................................... 31

Assignment – Annuities and loans ................................................................. 34

Appendix ........................................................................................................ 39

Terminology ................................................................................................... 43

Student evaluation.......................................................................................... 44

Answers ......................................................................................................... 45

Contents

FM5 Annuities and loan repayments 2

Strand: Financial Mathematics A sound understanding of credit, the responsible use of, and costs associated with, credit cards, and borrowing and investing money are important in developing students’ ability to make informed financial decisions. This includes a sound understanding of annuities, which represent fixed payments into an investment account or for the repayment of a loan. In the Financial Mathematics Strand in the HSC Mathematics General 2 course, the principal focus is on the mathematics of borrowing money and making informed decisions about financial situations. Outcomes addressed

A student:

MG2H-1 uses mathematics and statistics to evaluate and construct arguments in a range of familiar and unfamiliar contexts

MG2H-3 makes predictions about situations based on mathematical models, including those involving cubic, hyperbolic or exponential functions

MG2H-6 makes informed decisions about financial situations, including annuities and loan repayments

MG2H-9 chooses and uses appropriate technology to locate and organise information from a range of contexts

MG2H-10 uses mathematical argument and reasoning to evaluate conclusions drawn from other sources, communicating a position clearly to others, and justifies a response.

Content summary

FM4 Credit and borrowing

FM5 Annuities and loan repayments

FM5 Annuities and loan repayments 3

The principal focus of this topic is the nature and mathematics of annuities, the processes by which they accrue, and ways of maximizing their value as an investment. Annuity calculations are also used to calculate the present value of a series of payments and to calculate the repayment amount of a reducing-balance loan. Emphasis should be placed on using tables of interest factors to facilitate calculations.

Outcomes addressed: MG2H-1, MG2H-3, MG2H-6, MG2H-9, MG2H-10

Students develop the following knowledge, skills and understanding

• recognise that an annuity is a financial plan involving periodical, equal contributions to an account, with interest compounding at the conclusion of each period

• calculate (i) the future value of an annuity (FVA) and (ii) the contribution per period, using a table of future value interest factors for calculating a single future value of an annuity stream

• recognise that the values in a table of future value interest factors can be obtained using the formula for the future value of an annuity

• calculate (i) the present value of an annuity (PVA) and (ii) the contribution per period, using a table of present value interest factors for calculating a single present value of an annuity stream

• recognise that the values in a table of present value annuity interest factors can be obtained using the formula for the present value of an annuity

• use a table of interest factors for the present value of an annuity to calculate loan instalments, and hence the total amount paid over the term of a loan

• investigate the various processes for repayments of loans

• calculate the monthly repayment for a home loan from a table, given the principal, rate and term

• calculate the fees and charges that apply to different options for borrowing money in order to make a purchase

• interpret graphs that compare two or more repayment options for home loans.

For students in Distance Education Centres only: there is an evaluation page at the back of this part; fill it in when you have finished the work; say how easy/hard/interesting you find this work; ask relevant questions and return your comments to your teacher.

Introduction

FM5 Annuities and loan repayments 4

An annuity is a series of regular payments made over a number of periods. These payments may be made either by an individual or to an individual.

Examples of annuities include: • dividends • loan repayments • Austudy payments • mortgage repayments • rental payments • social security benefits • superannuation payments.

If payments are made at the end of a period the annuity is called an ordinary annuity.

If they are made at the beginning of a period, the annuity is called an ordinary annuity due.

In the previous booklet FM4 Credit and borrowing we learnt the terms future value and present value. This terminology is also used when working with annuities.

The future value of an annuity is the total value of the investment at the end of the last payment period.

The present value of an annuity is the single sum of money which, if invested today at the rate of compound interest which applies to the annuity, would produce the same financial result over the same period of time.

It is important to remember that payments/withdrawals are made at the end of each period in an ordinary annuity.

In the next two sections you will be shown how to use formulas to calculate the future value and present value of an annuity.

1.1 Annuities

FM5 Annuities and loan repayments 5

The future value of an annuity is the total of all payments plus the compound interest earned over the term of the annuity. (Revise FM4 Credit and borrowing if you have forgotten your work on the compound interest formula)

To find the total returned, you can use repeated applications of the compound interest formula since the principal is different each period.

EXAMPLE 1

You deposit $100 at the end of each month into a savings account earning 6% p.a., compounded monthly for four months. What is the future value of your annuity?

Solution

Using

A = P 1+ r( )n and r = 6% p.a.

= 0.5% per month (Don’t forget to change this value to a decimal!)

The first $100 is invested for three months so it amounts to:

A = 100(1 + 0.005)3

= $101.51

The second $100 is invested for two months so it amounts to:

A = 100(1 + 0.005)2

= $101.00

The third $100 is invested for one month so it amounts to:

A = 100 (1 + 0.005)1

= $100.50

The fourth $100 is deposited at the end of the fourth month with $0 interest.

Value of the annuity is $101.51 + $101.00 + $100.50 + $100 = $403.01

1.2 Future value annuities

FM5 Annuities and loan repayments 6

EXAMPLE 2

Complete the following table, showing the future value of each $200 deposited at the end of each month for 6 months at and interest rate of 12% p.a., compounded monthly. Then find the future value of the annuity.

Number of months, n, invested

Amount invested, P

Future Value, A

5 $200

4 $200

3 $200

2 $200

1 $200

0 $200

Total = $

Solution

Number of months, n, invested

Amount invested, P

Future Value, A

5 $200 $210.20

4 $200 $208.12

3 $200 $206.06

2 $200 $204.02

1 $200 $202

0 $200 $200

Total = $1230.40

Note that there is not a sum of $200 invested for 6 months. This is because the money is deposited at the end of each month.

This tells us that if we were to deposit $200 into an account at the end of every month for 6 months, at the end of this time the future value of the annuity is $1230.40.

FM5 Annuities and loan repayments 7

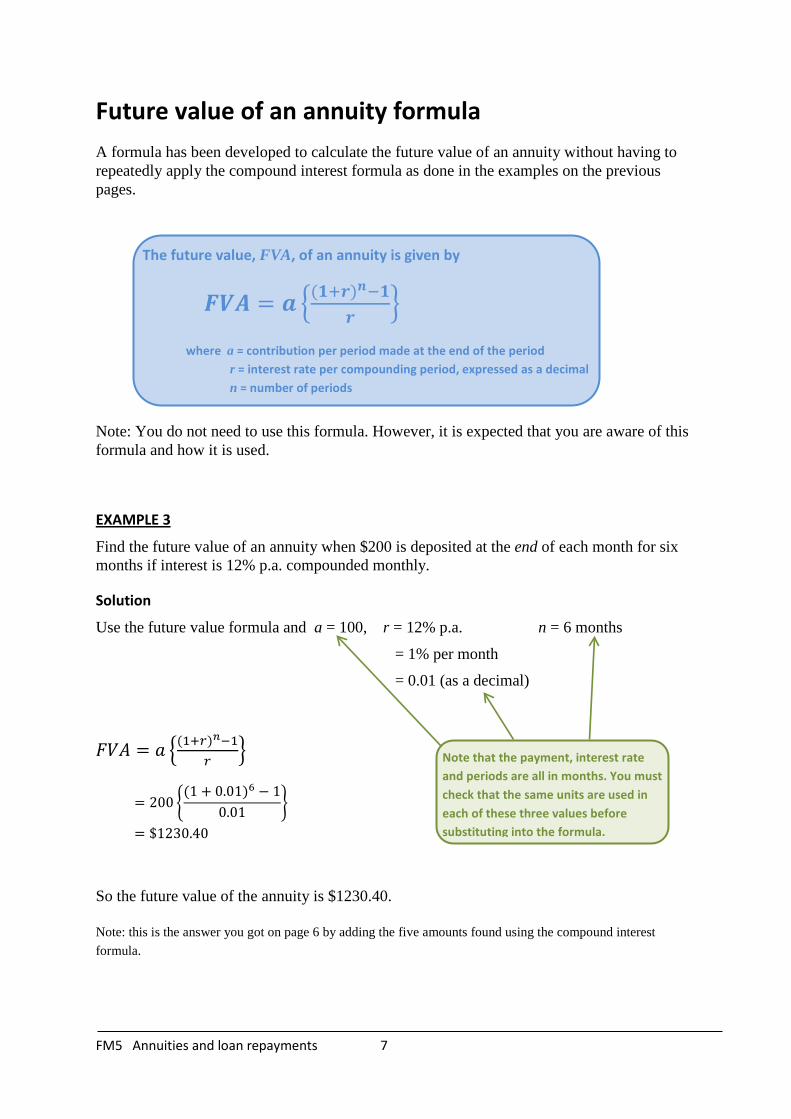

Future value of an annuity formula A formula has been developed to calculate the future value of an annuity without having to repeatedly apply the compound interest formula as done in the examples on the previous pages.

Note: You do not need to use this formula. However, it is expected that you are aware of this formula and how it is used.

EXAMPLE 3

Find the future value of an annuity when $200 is deposited at the end of each month for six months if interest is 12% p.a. compounded monthly.

Solution

Use the future value formula and a = 100, r = 12% p.a. n = 6 months

= 1% per month

= 0.01 (as a decimal)

𝐹𝑉𝐴 = 𝑎 �(1+𝑟)𝑛−1𝑟

�

= 200 �(1 + 0.01)6 − 1

0.01 �

= $1230.40

So the future value of the annuity is $1230.40.

Note: this is the answer you got on page 6 by adding the five amounts found using the compound interest formula.

The future value, FVA, of an annuity is given by

𝑭𝑭𝑭 = 𝒂 �(𝟏+𝒓)𝒏−𝟏𝒓

�

where a = contribution per period made at the end of the period r = interest rate per compounding period, expressed as a decimal n = number of periods

Note that the payment, interest rate and periods are all in months. You must check that the same units are used in each of these three values before substituting into the formula.

FM5 Annuities and loan repayments 8

EXAMPLE 4

Shelley wants to buy an apartment in five years. She estimates it will cost $250 000 and she needs a 10% deposit. She makes monthly deposits to a bank earning 12% p.a., compounded quarterly until she is ready to buy.

a) How much deposit does Shelley need for the apartment?

b) How much should she set aside each month to reach her deposit goal?

Solutions

a) The deposit is

10% × $250 000 = $25 000

b) FVA = 25 000, r = 12% p.a., n = 20 quarters = 3% per quarter = 0.03

𝐹𝑉𝐴 = 𝑎 �(1 + 𝑟)𝑛 − 1

𝑟 �

25000 = 𝑎 �(1 + 0.03)20 − 1

0.03 �

25000 = 𝑎 × 26.87037 …

𝑎 =25000

26.87037 …

= $930.39

So $930.39 should be deposited each quarter to have a deposit of $25 000 in five years time.

Future value interest factor tables As mentioned earlier, you are not expected to apply the future value annuity formula yourself. Instead, you will be using annuity tables, otherwise known as future value interest factor tables.

These tables are often used by those working in finance as it allows them to make quick calculations without the use of the future value annuity formula we have just seen.

An example of such a table is given on the following page. You will see that all values in the table are rounded to five decimal places.

FM5 Annuities and loan repayments 9

This table gives the future value (FVA) of an annuity with a contribution of $1 per period.

A larger version of this table is given on page 39 of the Appendix.

Let us now reconsider EXAMPLE 3, from page 7:

Find the future value of an annuity when $200 is deposited at the end of each month for six months if interest is 12% p.a. compounded monthly.

Here we already know that our interest rate is 1% per period, and we have 6 periods.

Looking at the table to where these values meet (as shown circled in red) we have a value of $6.15202.

Remembering that the future value table gives the future value of an annuity with a contribution of $1 per period, this tells us that if we were to contribute $1 per month at 1% per month for six months it would grow to $6.15. However, since we are investing $200 per month:

200 × $6.15202 = $1230.40 which is the same answer as earlier.

You can calculate each value in the table above by using the future value annuity formula and substituting in the different interest rates and periods, and setting a = 1.

FM5 Annuities and loan repayments 10

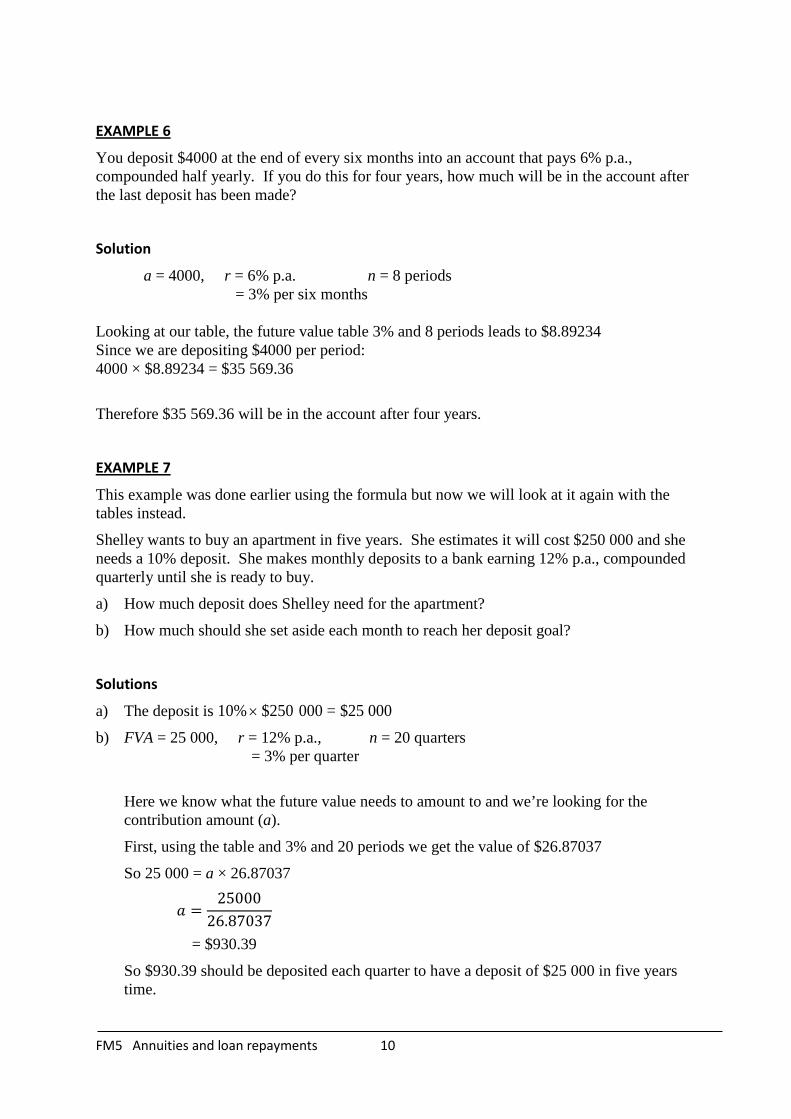

EXAMPLE 6

You deposit $4000 at the end of every six months into an account that pays 6% p.a., compounded half yearly. If you do this for four years, how much will be in the account after the last deposit has been made?

Solution

a = 4000, r = 6% p.a. n = 8 periods = 3% per six months Looking at our table, the future value table 3% and 8 periods leads to $8.89234 Since we are depositing $4000 per period: 4000 × $8.89234 = $35 569.36

Therefore $35 569.36 will be in the account after four years.

EXAMPLE 7

This example was done earlier using the formula but now we will look at it again with the tables instead.

Shelley wants to buy an apartment in five years. She estimates it will cost $250 000 and she needs a 10% deposit. She makes monthly deposits to a bank earning 12% p.a., compounded quarterly until she is ready to buy.

a) How much deposit does Shelley need for the apartment?

b) How much should she set aside each month to reach her deposit goal?

Solutions

a) The deposit is

10% × $250 000 = $25 000

b) FVA = 25 000, r = 12% p.a., n = 20 quarters = 3% per quarter

Here we know what the future value needs to amount to and we’re looking for the contribution amount (a).

First, using the table and 3% and 20 periods we get the value of $26.87037

So 25 000 = a × 26.87037

𝑎 =25000

26.87037

= $930.39

So $930.39 should be deposited each quarter to have a deposit of $25 000 in five years time.

FM5 Annuities and loan repayments 11

Use the table of future value interest factors on page 39 of the Appendix to answer the following questions. 1 An annuity is organised so that $1000 is deposited at the end of each month into an

account earning 9% p.a. compounding monthly for two and a half years.

a) What is the interest rate per month?

b) What is the value of an annuity at the end of the two and a half years.

c) How much of this is interest?

2 a) What is the value of an annuity at the end of ten years if $5000 is deposited every six months into an account earning 8% p.a., compounded half yearly.

b) What amount is interest?

3 To provide for the purchase of a car, Alexis deposits $1200 at the end of every quarter into an account earning 12% p.a. compounded quarterly.

a) How much does Alexis have at the end of four years?

b) How much more does she need to save before she can buy a car costing $25 000?

c) Will she have enough for this car if she saves for four and a half years?

4 Jim is planning to take an overseas trip in two and a half years time. He estimates the cost will be $10 000. He has been advised to put $300 each month into an account which pays 9% p.a., compounded monthly.

a) How much will he have saved, including interest, at the end of two and a half years?

b) Will he have enough money in two and a half years for his trip?

c) By how much will he fall short or overshoot his goal?

5 Mary wants to renovate her kitchen in three years time and will need $10 000. Starting in one month, she will begin making regular monthly deposits into an account earning 9% p.a., compounded monthly. How much should she deposit each month? Write your answer correct to the nearest dollar. Note: Since she missed the first monthly payment Mary will only be making 35 deposits.

6 A self-employed person has a retirement plan. If $7500 is paid each year into an account earning 12% p.a., how much will be in the retirement account after 20 years?

Exercise 1.2

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

FM5 Annuities and loan repayments 12

7 Starting on her 21st birthday and continuing on every birthday up to and including her 60th, Hariklea deposits $5000 into a fund as savings towards her retirement. How much, to the nearest dollar, will be in the fund when she retires (aged 60 years) if the fund earns:

a) 6% p.a., compounded annually?

b) 9% p.a., compounded annually?

8 The camping gear William wants will cost him $12 000. He will buy it in two years time and finds a bank willing to offer him interest of 3% p.a., compounded monthly. How much must he contribute each month?

9 The parents of a newborn child decide that on each birthday from the 1st to the 17th inclusive, they will deposit a certain amount into an investment account to save towards the child’s education. The account offers 6% p.a. interest. How much should they put away each year to have $16 000 after the seventeenth deposit?

10 A company estimates it will need $250 000 in eight years to replace its computer system. If it establishes a sinking fund by making fixed six-monthly payments into an account paying 12% p.a., compounded six-monthly, how much should each payment be? Note: a sinking fund is any account that is established to accumulate funds to meet future obligations or debts.

FM5 Annuities and loan repayments 13

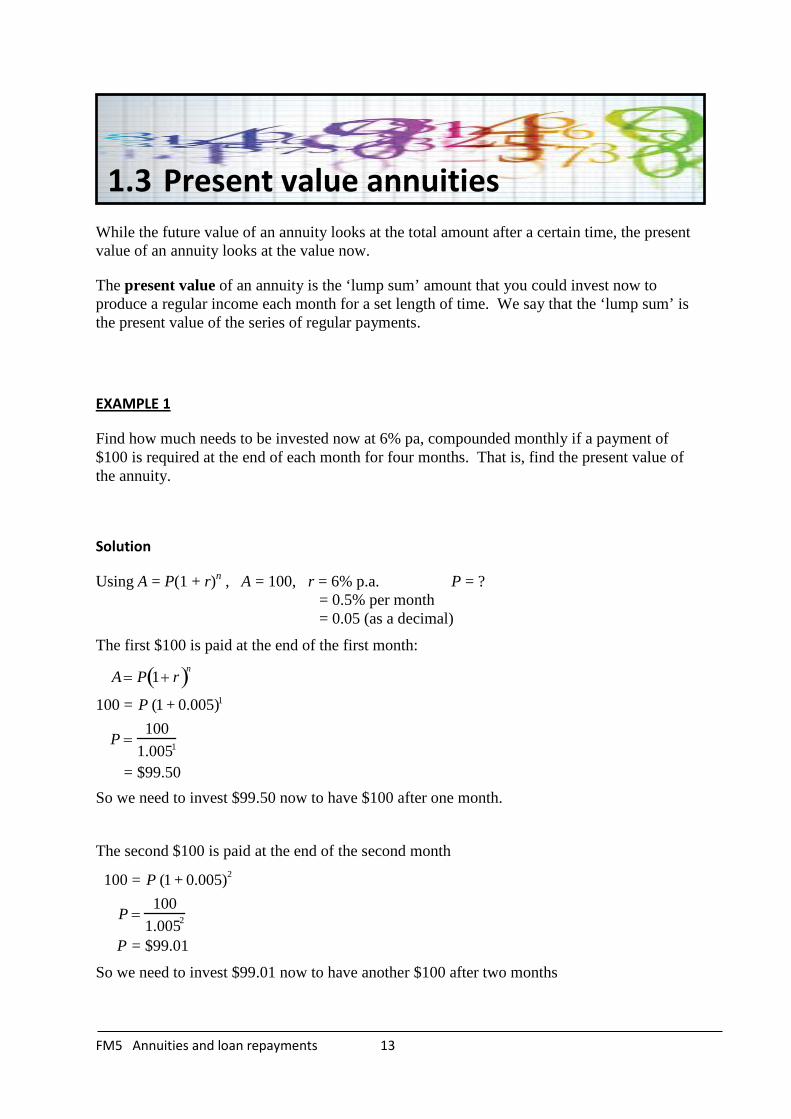

While the future value of an annuity looks at the total amount after a certain time, the present value of an annuity looks at the value now.

The present value of an annuity is the ‘lump sum’ amount that you could invest now to produce a regular income each month for a set length of time. We say that the ‘lump sum’ is the present value of the series of regular payments.

EXAMPLE 1

Find how much needs to be invested now at 6% pa, compounded monthly if a payment of $100 is required at the end of each month for four months. That is, find the present value of the annuity.

Solution

Using A = P(1 + r)n , A = 100, r = 6% p.a. P = ? = 0.5% per month = 0.05 (as a decimal)

The first $100 is paid at the end of the first month:

A = P 1+ r( )n

100 = P (1 + 0.005)1

P =100

1.0051

= $99.50

So we need to invest $99.50 now to have $100 after one month.

The second $100 is paid at the end of the second month

100 = P (1 + 0.005)2

P =100

1.0052

P = $99.01

So we need to invest $99.01 now to have another $100 after two months

1.3 Present value annuities

FM5 Annuities and loan repayments 14

The third $100 is paid at the end of the third month

100 = P (1 + 0.005)3

P =100

1.005( )3

= $98.51

So we need to invest $98.51 now to have another $100 after three months.

The fourth $100 is paid at the end of the fourth month

100 = P (1 + 0.005)4

P =100

1.005( )4

= $98.02

So we need to invest $98.02 now to have another $100 after four months

Present value of the annuity = $99.50 + $99.01 + $98.51 + $98.02 = $395.04

This means that $395.04 must be deposited now to be able to produce the four monthly payments of $100.

FM5 Annuities and loan repayments 15

Present value of an annuity formula A formula has been developed to calculate the present value of an annuity without having to repeatedly apply the compound interest formula as done in the examples on the previous pages.

Note: You do not need to use this formula. However, it is expected that you are aware of this formula and how it is used.

EXAMPLE 2 What amount needs to be deposited in an account now so you can withdraw $100 at the end of each month for four months if interest is 6% p.a., compounded monthly?

Solution

a = $100, r = 6% p.a. n = 4 months

= 0.5% per months

𝑃𝑉𝐴 = 𝑎 �(1 + 𝑟)𝑛 − 1𝑟(1 + 𝑟)𝑛

�

= 100 �(1 + 0.005)4 − 1

0.005(1 + 0.005)4�

= $395.05

The present value is $395.04, that is, you need to deposit $395.04 now to be able to withdraw $400 over the next four months.

Note: this is the same amount you obtained in EXAMPLE 1 where you totalled four amounts, each calculated using the compound interest formula.

The present value, N, of an annuity is given by

𝑷𝑭𝑭 = 𝒂 �(𝟏+𝒓)𝒏−𝟏𝒓(𝟏+𝒓)𝒏

�

where a = contribution per period made at the end of each period r = interest rate per per compounding period, expressed as a decimal n = number of periods

FM5 Annuities and loan repayments 16

Present value interest factor tables As mentioned earlier, you are not expected to apply the present value annuity formula yourself. Instead, you will be using annuity tables, otherwise known as present value interest factor tables. These are very similar to the future value interest factor tables looked at in the previous section.

Let’s reconsider EXAMPLE 3 above, using the present value table on the following page.

We already know that r = 0.5% and there are 4 periods.

Looking at where these values meet (as circled in red) they give a value of $3.95050

As we wish to be able to withdraw $100 each month: 100 × $3.95050 = $395.05 which is the same answer as both previous methods.

A larger version of this table is provided in the Appendix on page 40.

You can calculate each value in the table above by using the present value annuity formula and substituting in the different interest rates and periods, and setting a = 1.

FM5 Annuities and loan repayments 17

EXAMPLE 3

A computer is sold on the terms that it will be repaid in monthly instalments of $75 for the next two and a half years. Interest is charged at 18% p.a., compounded monthly. What is the equivalent cash price of the computer? Solution

Here r = 1.5% per month and there are 30 periods.

Using the table given on page 40 of the Appendix we get a value of $24.01584

75 × $24.01584 = $1801.19

Therefore the equivalent cash price of the computer is $1801.19

EXAMPLE 4

John establishes an annuity by depositing $100 000 into an account that pays 10% p.a., compounded quarterly. Equal quarterly withdrawals will be made for the next five years. At the end of this time the account will have zero balance. Calculate the amount of each withdrawal.

Here PVA = 100 000, r = 2.5% per quarter and there are 20 periods.

Looking at our table, this gives a value of $15.58916

100 000 = a × 15.58916

𝑎 =100000

15.58916

= $6414.71

Therefore John is able to withdraw $6414.71 every quarter for the next five years before he runs out of money.

FM5 Annuities and loan repayments 18

Use the table of present value interest factors on page 40 of the Appendix to answer the following questions. 1 How much should you deposit now into an account paying 6% p.a., compounded

quarterly, in order to withdraw $1500 each quarter (three months) for the next five years?

2 What is the present value of an annuity that pays $500 a month for two years given that interest is 9% p.a., compounded monthly?

3 Arthur is able to repay $3000 at the end of each six month period for the next fifteen years. If interest is 8% p.a. compounded six-monthly, how much can he borrow on these conditions?

4 Shelley pays off her car loan at $325 per month for four years and two months. There is no down payment and she is charged 1.5% interest per month on the unpaid balance:

a) What was the original cost of the car to the nearest dollar?

b) What total interest will be paid, correct to the nearest dollar?

5 Trent establishes an annuity by depositing $250 000 into an account that pays 8% p.a., compounded six-monthly. Equal six-monthly withdrawals will be made for the next fifteen years. At the end of this time the account will have zero balance. Calculate the amount of each withdrawal. Write your answer correct to the nearest dollar.

Exercise 1.3

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

FM5 Annuities and loan repayments 19

The loan amount is the present value of the series of loan repayments. For reducing balance loans, the present value formula (and hence the present value table) can be used to calculate both loan repayments (a) and the total loan amount (PVA).

EXAMPLE 1

Kris borrows $2000 and repays it in four equal monthly instalments. If interest is charged at 24% p.a., compounded monthly, find

a) the monthly instalment

b) the total repaid

c) the interest paid

Solutions

a) PVA = 2000, r = 2% per month and there are 4 periods.

Using the interest rate and periods in the present value table on page 40 of the Appendix, we have a value of $3.80773

2000 = a × 3.80773

𝑎 =2000

3.80773

= $525.25

Therefore the monthly instalment is $525.25.

b) The total repaid = 4 × $525.25

= $2101

c) Interest paid = $2101 – $2000

= $101

1.4 Paying off a loan

FM5 Annuities and loan repayments 20

Use the table of present value interest factors on page 40 of the Appendix to answer the following questions. 1 A company buys fax machines for its office for $15 000 and finances them at 12% p.a.,

compounded monthly. If the loan is to be repaid in two years with equal monthly payments:

a) how much is each payment?

b) what is the total repaid?

c) how much interest will be paid?

2 Suppose you take out a loan for a fridge valued at $1450 and agree to pay for it in 18 equal monthly instalments at interest of 0.75% per month.

a) How much is each payment?

b) How much interest will be paid?

3 A car loan for $68 000 is taken out over a 10 year period .

a) If the repayments are made six-monthly, at an interest rate of 10% p.a. compounded six-monthly find

i) the six-monthly repayments

ii) the total repaid

iii) the total interest paid.

b) If the repayments are made quarterly, at an interest rate of 8% p.a. compounded quarterly find

i) the quarterly repayments

ii) the total repaid

iii) the total interest paid.

c) Which is the better loan repayment option? Justify your answer with mathematical reasoning.

Exercise 1.4

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

FM5 Annuities and loan repayments 21

Most home loans are reducing balance loans. A reducing balance loan is a loan where interest calculated each period is less than for the previous period (provided that you are making regular repayments of course). This is because some of the principal has been repaid.

It is not unusual when taking out a home loan over 20 – 30 years to end up repaying two or three times as much as you originally borrowed. This is why it is important to understand exactly what you are signing yourself up for.

In this section, you will use tables to determine monthly repayments on a reducing balance loan.

The table in the Appendix on page 41 shows the monthly repayments for differing loan amounts over 20 years at various interest rates.

Even though repayments are generally made monthly, interest rates are quoted as yearly amounts. Financial institutions quote yearly rates to customers but convert to a monthly rate to fit with monthly repayments.

EXAMPLE 1

Kelly takes out a home loan of $350 000 over 20 years at an interest rate of 6% p.a.

a) Use Table A in the Appendix to find the monthly repayment.

b) How much is paid back altogether for this loan?

c) How much interest was paid?

Solutions

a) A section of the table is provided on the following page:

From the table, go across the $350 000 row and down the 6% p.a. column. This is circled for you in green. A value of $2507.51 is obtained.

Therefore the monthly repayment is $2507.51.

1.5 Home loans

FM5 Annuities and loan repayments 22

b) Monthly repayment is $2507.51

Total repaid = $2507.51 × 240 = $601 802.40

c) Interest = amount repaid – loan amount = $601 802.40 – $350 000 = $251 802.40

EXAMPLE 2

Luke takes out a home loan of $460 000 over 25 years at an interest rate of 7% p.a.

a) Use Table B in the Appendix on page 42 to find the monthly repayment.

b) How much is paid back altogether for this loan?

c) How much interest was paid?

Solutions

a) The table is provided on the following page:

From the table, go across the 7% p.a. row and down the 25 year column. This is circled for you in green. A value of $7.07 is obtained.

Note that this table shows the monthly repayments per $1000 borrowed.

As Luke has borrowed $460 000: $460 000 ÷ 1000 = 460

Therefore 460 × $7.07 = $3252.20

Hence Luke’s monthly repayment is $3252.20

FM5 Annuities and loan repayments 23

Monthly repayments per $1000 borrowed

b) $3252.20 × 300 = $975 660

c) Interest = $975 660 – $460 000 = $515 660

FM5 Annuities and loan repayments 24

Use Table A in the Appendix on page 41 to answer the following questions 1 Find the monthly repayment over 20 years for a loan of:

a) $305 000 at 8% p.a.

b) $490 000 at 12% p.a.

c) $335 000 at 10% p.a.

2 a) What is the monthly repayment for a loan of $390 000 over 20 years at 11% p.a.?

b) What is the total repaid on this loan?

c) How much interest is charged?

Use Table B in the Appendix on page 42 to answer the following questions. 3 Jane takes out a home loan for $600 000 over a 30 year period at an interest rate of

8% p.a.

a) What is her monthly repayment?

b) What is the total repaid on this loan?

c) How much interest is charged?

4 Jane’s friend Joan also takes out a home loan for $600 000 at an interest rate of 8% p.a. However Joan takes out her loan over a 20 year period.

a) What is her monthly repayment?

b) What is the total repaid on this loan?

c) How much interest is charged?

5 Compare your answers to 3 c) and 4 c)

a) What difference was there between the two loans that Jane and Joan had?

b) Who paid more interest, and how much more?

c) What conclusions can you draw about what effect the period of a home loan has on the total interest paid?

6 a) What is the monthly repayment for a loan of $195 000 for 25 years at 6% p.a.?

b) If the borrower repaid the loan over 15 years what would the monthly repayment be?

c) In each case, how much is repaid over the life of the loan?

d) How much could be saved by paying off the loan in 15 years?

Exercise 1.5

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

FM5 Annuities and loan repayments 25

Increasing repayments A home loan can be paid off faster by increasing the repayment. We have seen in Exercise 1.5 how reducing the period of a loan can significantly reduce the total interest paid.

Suppose, if instead of paying back $600 per month you were able to pay back $750 per month. You could pay the loan off faster and save on interest.

The graph below shows the amount outstanding on a $300 000 loan at 6% p.a. comparing monthly repayments of $2400 and $1800.

As you can see, repaying the minimum of $1800 per month means the loan is repaid over the full 30 year period. However, if the monthly repayments are increased to $2400 per month the loan is repaid in approximately 17 years.

As a side note, repaying the loan in 17 years results in paying $171 968 interest whereas repaying the loan over 30 years results in paying $346 644 in interest. That is a massive saving of $174 767 by repaying an extra $600 per month.

EXAMPLE 1

Use the graph above to find a) the amount owing on each loan after 10 years. _ b) the time it takes for each loan to fall under $50 000 (50k)

1.6 Graphing loan repayments

$2400 per month

$1800 per month

FM5 Annuities and loan repayments 26

Solutions

a) After 10 years there is $150 000 still owing on the loan with the monthly repayment of $2400 and $250 000 still owing on the loan with the monthly repayment of $1800.

b) The loan with the monthly repayment of $2400 falls under $50 000 after approximately 15 years. It takes the loan with the monthly repayment of $1800 approximately 27.5 years to reach this value.

A sudden windfall

Most people pay off a loan by putting in a certain amount each month because that is all they can comfortably, or are willing to, afford.

Suppose you came into a sudden windfall of, say, $5000. Should you put this towards paying off a loan or should you use it to go on a holiday or buy a jet ski? While such a decision has a lot to do with your own value system and preferences, here you will consider it purely from a mathematical point of view.

Suppose in paying off that $50 000 loan at $600 a month, you came into a $5000 windfall and put all of that $5000 towards paying off the loan.

The following diagram shows the original path the loan would have taken (without the one-off $5000 payment) and the modified path after $5000 was put towards it.

By contributing the additional $5000 towards the home loan before continuing with your regular $600 payments results in repaying the loan approximately 45 months earlier than expected.

FM5 Annuities and loan repayments 27

EXAMPLE 2

Use the graph on the previous page to answer the following: a) How long does it take to repay each loan i) with making the $5000 contribution? _ ii) without making the $5000 contribution?

b) How much is owing on each loan after 6 years?

Solutions

a) i) 8 years 3 months ii) 12 years

b) with contribution: $17 500 without contribution: $32 500

Monthly vs. fortnightly repayments The graph shows the progress of a $200 000 loan at 6.7% p.a. reducible interest over 30 years for monthly and fortnightly repayments.

Here the overall monthly repayment does not change. But instead of repaying $2000 once a month, $1000 is paid every two weeks.

As you can see, making a fortnightly repayment reduces the period of the loan, and hence the interest paid. This is due to the fact that financial institutions calculate their interest daily. Which means that every fortnight your loan balance decreases slightly, leading to less interest being charged. This will be looked at further in the following exercise.

FM5 Annuities and loan repayments 28

1 The graph below shows the amount outstanding on two loans valued at $250 000 with interest charged at 6% p.a. One loan has a monthly repayment of $2000, and the other $1600, as shown on the graph.

a) How long does it take to repay each of the loans? b) How much is owing on each loan after 5 years has elapsed? c) After how many years does the amount owing on each loan fall under $75 000?

2 Below is a graph used in one of the earlier examples.

a) How long into the loan was the additional $5000 put toward the home loan? b) What is the difference in the amount owing at 5 years between the two options? c) List one positive and one negative aspect of putting the additional $5000 towards the loan.

Exercise 1.6

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

$2000 per month

$1600 per month

FM5 Annuities and loan repayments 29

3 The graph shows the progress of a $200 000 loan at 6.7% p.a. reducible interest over 30 years for monthly and fortnightly repayments.

a) How much sooner can you repay the loan if you make fortnightly repayments?

b) For both repayment methods, how long does it take for the amount owing to fall under $60 000?

c) Why would some people prefer to pay monthly as opposed to fortnightly?

4 The graph below shows the amount outstanding on two loans valued at $200 000 with interest charged at 6% p.a. One loan has a monthly repayment of $2400, and the other $1500, as shown on the graph.

Draw a curve on the graph representing what you think a monthly repayment of $1800

would look like.

$2400 per month $1500 per month

Remember to return this sheet to your teacher with your solutions.

FM5 Annuities and loan repayments 30

FM5 Annuities and loan repayments 31

The amount of the loan, cost of the loan (interest), term of the loan and repayment amount will vary for different borrowers and lenders.

There are additional costs when borrowing for a mortgage. These include: bank fees, solicitor’s fees, stamp duty and home loan insurance. Depending on the property you plan to purchase, it is often beneficial to also get pest and building inspections carried out. This all comes at an additional cost to your home loan.

Stamp duty Stamp duty is a general tax imposed by the Office of State Revenue on title transfers as a result of selling real estate, vehicles and other property. You may recall that we looked at Stamp Duty for motor vehicles in the Preliminary course (FSDr1 Costs of purchase and insurance)

Below is a table showing the stamp duty rates for NSW

Property value Stamp duty payable

$0 – $14 000 1.25% of value

$14 001 – $30 000 $175 + 1.5% of value over $14 000

$30 001 – $80 000 $415 + 1.75% of value over $30 000

$80 001 – $300 000 $1 290 + 3.5% of value over $80 000

$300 001 – $1 million $8 990 + 4.5% of value over $300 000

$1 million – $3 million $40 490 + 5.5% of value over $1 million

Over $3 million $150 490 + 7% of value over $3 million

EXAMPLE 1

Using the table above, calculate the stamp duty payable on a house valued at

a) $190 000

b) $450 000

1.7 Additional fees and charges

FM5 Annuities and loan repayments 32

Solutions

a) Stamp duty = $1 290 + 3.5% of value over $80 000

= $1 290 + 0.035 × (190 00 – 80 000)

= $1 290 + $3850

= $5 140

b) Stamp duty = $8 990 + 4.5% of value over $300 000

= $8 990 + 0.045 × (450 000 – 300 000)

= $8 990 + $6 750

= $15 740

EXAMPLE 2

Ursula purchased a property valued at $320 000. In addition she also had to pay the following: Solicitor fees $1250, Building report $275, Land title fees $160, Pest inspection $120.

Calculate the total Ursula had to pay in additional costs.

Solution

Stamp duty = $8 990 + 0.045 × (320 000 – 300 000)

= $9 890

Total costs = $9 890 + $1 250 + $275 + $160 + $120

= $11 695

FM5 Annuities and loan repayments 33

1 Using the table on page 31, calculate the stamp duty payable on property’s valued at

a) $79 000

b) $620 000

c) $287 000

d) $1.8 million

2 Gervasse purchased a property valued at $2.3 million. In addition to the stamp duty he also had to pay the following: Solicitor fees $2750, Building report $475, Land title fees $195, Pest inspection $280, survey report $370 and a loan application fee of $700.

Calculate the total Gervasse had to pay in additional costs.

Exercise 1.7

Please complete all exercises on your own lined A4 paper. Make sure each question is labelled clearly.

FM5 Annuities and loan repayments 34

Use the tables on pages 39 and 40 in the Appendix to answer the following. 1 Anastasia is planning to take the trip of a lifetime in ten years time and estimates that she

will need $30 000. She is advised to contribute $2500 at the end of each year into an account that pays 5% p.a., compounded annually.

a) Will she have enough money for her trip in ten years time?

b) By how much will she fall short of, or overshoot, her goal?

2 A company estimates that it will have to replace a piece of equipment in two years time at a cost of $85 000. To have the money available at this time, a sinking fund is established by making fixed monthly payments into an account paying 12% p.a., compounded monthly. How much should each payment be?

3 Find the value of the following investments after 20 years;

a) a lump sum of $100 000 invested today at 12% p.a., compounded annually or

b) a six-monthly payment of $6000, commencing today, with interest of 12% p.a., compounded six-monthly.

c) Which would give the better financial result at the end of the 20 year period?

4 Matilda invested $2500 at the end of each year for the first 15 years of her working life. The interest rate was 7% p.a.

a) How much money did Matilda invest during this time?

b) By using the table, find the total value of her investment after 15 years.

After 15 years she stopped these regular payments, withdrew the annuity amount and deposited it in a long-term investment account at 9% p.a., compounded monthly for the next ten years.

c) What was the value of this investment after the further ten years?

Ronald, on the other hand, saved $1500 at the end of each year for the whole 25 years. He began saving at the same time Matilda did at an interest rate of 7% p.a., compounded annually.

d) How much did Ron have at the end of 25 years?

e) Comment on who is the better saving strategy.

Assignment – Annuities and loans

FM5 Annuities and loan repayments 35

5 The author of a leading textbook anticipates royalties of $3450 at the end of each six month period for the next ten years. What single amount should the author accept now instead of the periodic payments if money is worth 6% p.a., compounded six-monthly?

6 At the end of twelve years a netball club will need to replace goal posts and other club equipment. It is estimated these replacement costs will be $10 000. How much will the club need to deposit each year at 5% p.a., compounded annually, for this purpose?

Use the loan repayment tables in the Appendix on pages 41 and 42 for these questions.

7 What is the monthly repayment for a loan of $420 000 over 20 years at an interest rate of 7% p.a.?

8 a) What is the monthly repayment for a loan of $355 000 over 20 years at 10% p.a.?

b) What is the total repaid?

c) How much interest was paid?

9 Calculate the monthly repayments for the following loans:

a) $326 000 for 10 years at 5% p.a.

b) $890 000 for 25 years at 9% p.a.

10 Ian takes out a home loan valued at $563 000 over a 15 year period at 6% p.a.

a) What is his monthly repayment?

b) How much will he pay in total with his monthly repayments?

c) How much interest is Ian charged over the 15 year period?

11 Belinda pays $750 a month towards her loan. If she can afford to put in more per month, what is your advice for her? Explain.

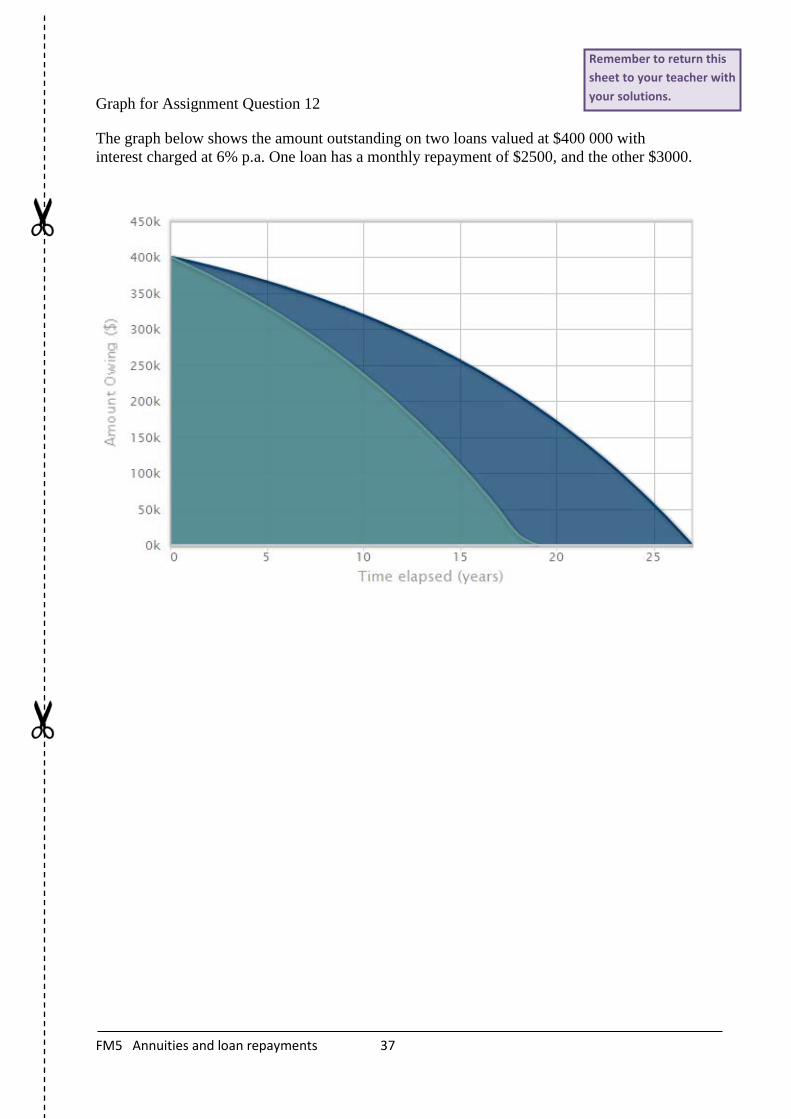

Use the graph on page 37 to answer the questions below. 12 a) Label which curve represents the monthly repayment of $2 500, and which represents the monthly repayment of $3 000.

b) How long does it take to repay each loan.

c) What is amount owing on each of the loans after 5 years?

d) When does the amount owing fall under $100 000 for each repayment option?

e) Draw a line on the graph showing where a monthly repayment of

i) $4 000 would be.

ii) $2 700 would be.

FM5 Annuities and loan repayments 36

FM5 Annuities and loan repayments 37

Graph for Assignment Question 12

The graph below shows the amount outstanding on two loans valued at $400 000 with interest charged at 6% p.a. One loan has a monthly repayment of $2500, and the other $3000.

Remember to return this sheet to your teacher with your solutions.

FM5 Annuities and loan repayments 38

FM5 Annuities and loan repayments 39

Appendix

Future value of an annuity with a contribution of $1 per period.

FM5 Annuities and loan repayments 40

Present value of an annuity with a contribution of $1 per period.

FM5 Annuities and loan repayments 41

Table A: Loan repayment table (term of loan 20 years)

Amount

borrowed Annual percentage interest rate

$ 4 5 6 7 8 9 10 11 12

305 000 1848.23 2012.86 2185.11 2364.65 2551.19 2744.16 2943.31 3148.17 3358.31 310 000 1878.53 2045.86 2220.94 2403.42 2593.01 2789.15 2991.56 3199.78 3413.37 315 000 1908.83 2078.86 2256.76 2442.18 2634.84 2834.14 3039.81 3251.39 3468.42 320 000 1939.13 2111.86 2292.58 2480.95 2676.66 2879.12 3088.06 3303.00 3523.48 325 000 1969.43 2144.86 2328.40 2519.71 2718.48 2924.11 3136.31 3354.61 3578.53 330 000 1999.73 2177.85 2364.22 2558.48 2760.30 2969.10 3184.56 3406.22 3633.58 335 000 2030.03 2210.85 2400.04 2597.24 2802.13 3014.08 3232.81 3457.83 3688.64 340 000 2060.33 2243.85 2435.87 2636.01 2843.95 3059.07 3281.06 3509.44 3743.69 345 000 2090.62 2276.85 2471.69 2674.77 2885.77 3104.05 3329.32 3561.05 3798.75 350 000 2120.92 2309.84 2507.51 2713.54 2927.60 3149.04 3377.57 3612.66 3853.80 355 000 2151.22 2342.84 2543.33 2752.30 2969.42 3194.03 3425.82 3664.27 3908.86 360 000 2181.52 2375.84 2579.15 2791.07 3011.24 3239.01 3474.07 3715.88 3963.91 365 000 2211.82 2408.84 2614.97 2829.83 3053.06 3284.00 3522.32 3767.49 4018.96 370 000 2242.12 2441.84 2650.79 2868.60 3094.89 3328.99 3570.57 3819.10 4074.02 375 000 2272.42 2474.83 2686.62 2907.36 3136.71 3373.97 3618.82 3870.71 4129.07 380 000 2302.72 2507.83 2722.44 2946.13 3178.53 3418.96 3667.07 3922.32 4184.13 385 000 2333.02 2540.83 2758.26 2984.89 3220.35 3463.94 3715.32 3973.93 4239.18 390 000 2363.32 2573.83 2794.08 3023.66 3262.18 3508.93 3763.57 4025.54 4294.24 395 000 2393.61 2606.82 2829.90 3062.42 3304.00 3553.92 3811.83 4077.14 4349.29 400 000 2423.91 2639.82 2865.72 3101.19 3345.82 3598.90 3860.08 4128.75 4404.34 405 000 2454.21 2672.82 2901.55 3139.95 3387.65 3643.89 3908.33 4180.36 4459.40 410 000 2484.51 2705.82 2937.37 3178.72 3429.47 3688.88 3956.58 4231.97 4514.45 415 000 2514.81 2738.82 2973.19 3217.48 3471.29 3733.86 4004.83 4283.58 4569.51 420 000 2545.11 2771.81 3009.01 3256.25 3513.11 3778.85 4053.08 4335.19 4624.56 425 000 2575.41 2804.81 3044.83 3295.01 3554.94 3823.84 4101.33 4386.80 4679.62 430 000 2605.71 2837.81 3080.65 3333.78 3596.76 3868.82 4149.58 4438.41 4734.67 435 000 2636.01 2870.81 3116.48 3372.54 3638.58 3913.81 4197.83 4490.02 4789.72 440 000 2666.30 2903.81 3152.30 3411.30 3680.41 3958.79 4246.08 4541.63 4844.78 445 000 2696.60 2936.80 3188.12 3450.07 3722.23 4003.78 4294.33 4593.24 4899.83 450 000 2726.90 2969.80 3223.94 3488.83 3764.05 4048.77 4342.59 4644.85 4954.89 455 000 2757.20 3002.80 3259.76 3527.60 3805.87 4093.75 4390.84 4696.46 5009.94 460 000 2787.50 3035.80 3295.58 3566.36 3847.70 4138.74 4439.09 4748.07 5065.00 465 000 2817.80 3068.79 3331.40 3605.13 3889.52 4183.73 4487.34 4799.68 5120.05 470 000 2848.10 3101.79 3367.23 3643.89 3931.34 4228.71 4535.59 4851.29 5175.10 475 000 2878.40 3134.79 3403.05 3682.66 3973.16 4273.70 4583.84 4902.90 5230.16 480 000 2908.70 3167.79 3438.87 3721.42 4014.99 4318.68 4632.09 4954.50 5285.21 485 000 2938.99 3200.79 3474.69 3760.19 4056.81 4363.67 4680.34 5006.11 5340.27 490 000 2969.29 3233.78 3510.51 3798.95 4098.63 4408.66 4728.59 5057.72 5395.32 495 000 2999.59 3266.78 3546.33 3837.72 4140.46 4453.64 4776.84 5109.33 5450.38 500 000 3029.89 3299.78 3582.16 3876.48 4182.28 4498.63 4825.09 5160.94 5505.43

FM5 Annuities and loan repayments 42

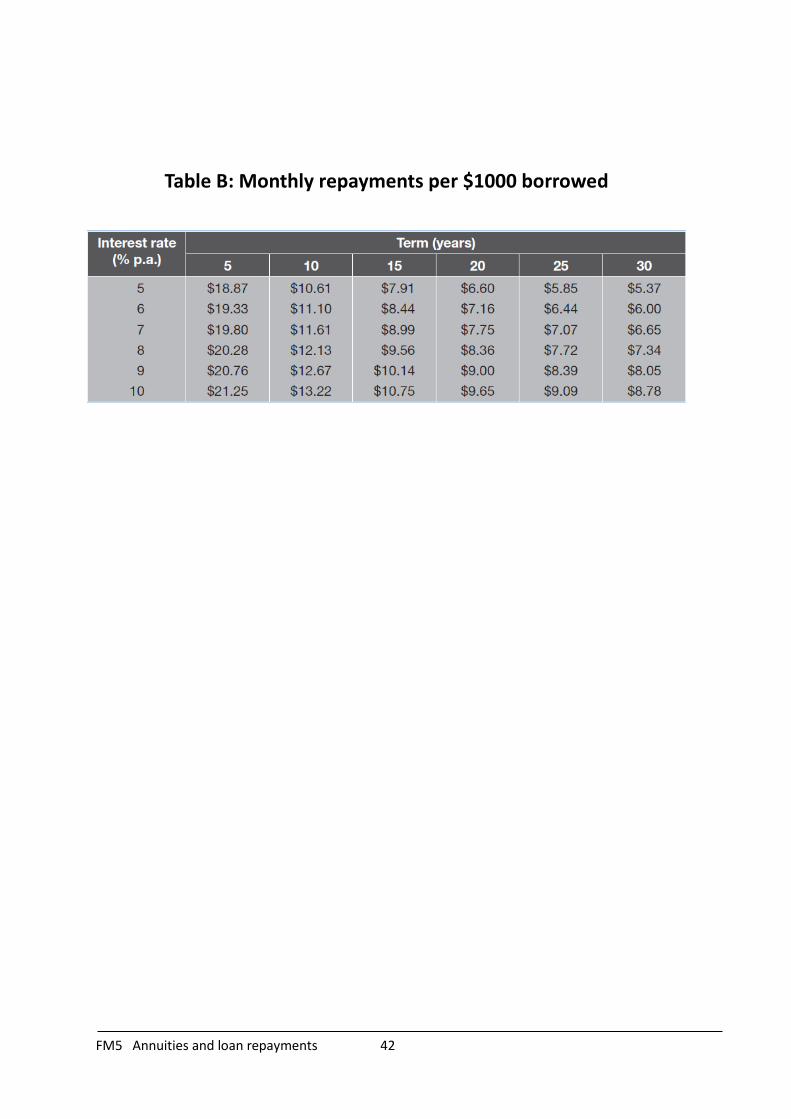

Table B: Monthly repayments per $1000 borrowed

FM5 Annuities and loan repayments 43

Do you understand the following words or expressions? Look back in your notes, if necessary, and give your explanations here.

future value annuity _____________________________________________________

_____________________________________________________________________

present value annuity ____________________________________________________

_____________________________________________________________________

loan repayments ________________________________________________________

_____________________________________________________________________

additional fees _________________________________________________________

_____________________________________________________________________

stamp duty ____________________________________________________________

_____________________________________________________________________

Terminology

FM5 Annuities and loan repayments 44

When you have finished this unit of work see if you can do these things.

can do with confidence ↓

need more help ↓

Tick if you can do them with confidence:

• recognise that an annuity is a financial plan involving periodical equal contributions to an account, with interest compounding at the conclusion of each period.

• calculate the future value of an annuity and the contribution per period using a table of future value interest factors

• calculate the present value of an annuity and the contribution per period using a table of future value interest factors

• recognise that the values in a table of future and present value interest factors can be obtained using the formula

• use a table of interest factors to calculate loan instalments and hence the total amount paid over the term of a loan.

• investigate the various processes for repayment of loans

• calculate the monthly repayment for a home loan from a table

• calculate the fees and charges that apply to different options for borrowing money in order to make a purchase

• interpret graphs that compare two or more repayment options for home loans.

Ask for further help with any concepts you feel unsure about.

Please write your questions and any other comments below.

_______________________________________________________________

_______________________________________________________________

_______________________________________________________________

_______________________________________________________________

_______________________________________________________________

_______________________________________________________________

_______________________________________________________________

Student Evaluation

FM5 Annuities and loan repayments 45

Exercise 1.2 1. a) 0.75% b) $33 502.90 c) $3502.90 2. a) $148 890.40 b) $48 890.40 3. a) $24 188.26 b) $811.74 c) Yes 4. a) $10 050.87 b) Yes c) $50.87 over 5. $251 6. $540 393.30 7. a) $773 810 b) $1 689 412 8. $485.77 9. $567.12 10. $9738.04 Exercise 1.3 1. $25 752.96 2. $10 944.58 3. $51 876.09 4. a) $11 375 b) $4875 5. $14 458 Exercise 1.4 1. a) $706.10 b) $16 946.40 c) $1946.40 2. a) $86.42 b) $105.56 3. a) i) $5456.50 ii) $109 130 iii) $41 130 b) i) $2485.79 ii) $99 431.60 iii) $31 431.60 c) The quarterly repayments as you pay almost $10 000 less in interest. Exercise 1.5 1. a) $2551.19 b) $5395.32 c) $3232.81 2. a) $4025.54 b) $966 129.60 c) $576 129.60

Exercise 1.5 cont’d 3. a) $4404 b) $1 585 440 c) $985 440 4. a) $5016 b) $1 203 840 c) $603 840 5. a) The loan period. b) Jane, $381 600. c) The longer the period of the loan, the more interest charged. 6. a) $1225.80 b) $1645.80 c) $376 740, $296 244 b) $80 496 Exercise 1.6 1. a) 17 years and 26 years b) $200 000 and $225 000 c) 13 years and 21 years 2. a) ≈26 months b) ≈$13 000 c) Positive: Loan is repaid quicker and hence less interest is charged. Negative: The money could be used on other necessities. 3. a) 6 years b) 21 years, 26 years c) The have other financial commitments, or their wages are paid monthly. 4.

Exercise 1.7 1. a) $1272.50 b) $23 390 c) $8535 d) $84 490 2. $116 760

Answers