Regionality, customer proximity & sustainability Solid core earnings based on sustainable business model 'HETA solution' positively impacts 2016 financial profitability Substantial profit retention further strengthens already sound capitalisation Continued significant growth in customer deposits E | May 2017 HYPO NOE Investor Presentation

Transcript

Regionality, customer proximity & sustainability

Solid core earnings based on sustainable business model

Substantial profit retention further strengthens already sound capitalisation

Continued significant growth in customer deposits

E | May 2017

HYPO NOE Investor Presentation

2

Section Slide

I. Group Business Strategy 3

II. Business Outlook for 2017 14

III. Financial Figures 15

IV. Funding 19

V. Contacts 26

Appendix Key Financial Statements and Further Details 27

Content

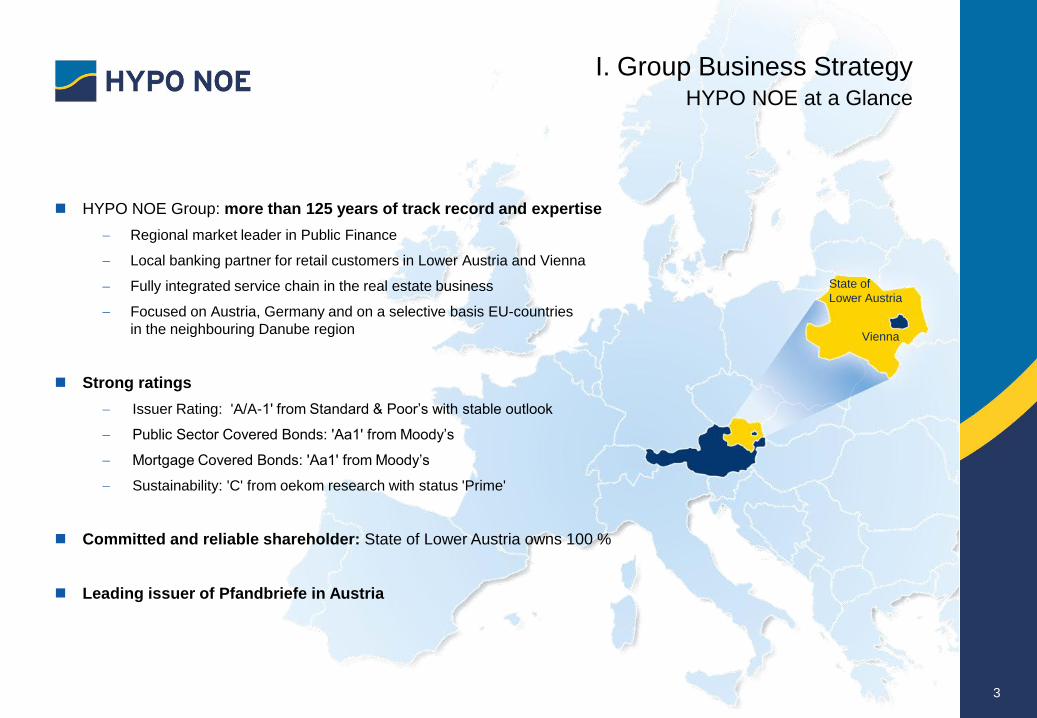

3

State of

Lower Austria

Vienna

I. Group Business Strategy HYPO NOE at a Glance

HYPO NOE Group: more than 125 years of track record and expertise

Regional market leader in Public Finance

Local banking partner for retail customers in Lower Austria and Vienna

Fully integrated service chain in the real estate business

Focused on Austria, Germany and on a selective basis EU-countries

in the neighbouring Danube region

Strong ratings

Issuer Rating: 'A/A-1' from Standard & Poor’s with stable outlook

Public Sector Covered Bonds: 'Aa1' from Moody’s

Mortgage Covered Bonds: 'Aa1' from Moody’s

Sustainability: 'C' from oekom research with status 'Prime'

Committed and reliable shareholder: State of Lower Austria owns 100 %

Leading issuer of Pfandbriefe in Austria

4

I. Group Business Strategy Recent Developments

Proposed Merger of HYPO NOE Landesbank AG and HYPO NOE Gruppe Bank AG

Schedule

June 29, 2016: Supervisory Board of HYPO NOE Gruppe Bank AG initiated a project to prepare a merger

with its 100 % subsidiary HYPO NOE Landesbank AG

Merger is scheduled for completion by autumn 2017 with retroactive effect from January 1st, 2017

Objective

Reintegration of the retail and housing finance businesses into the core universal bank

Primary purpose is an increase in efficiency of the banking group by lowering complexity of the

organisation and realising operational synergies

Process

Preparatory measures were started in 2016, and the merger progress is proceeding on schedule

Change management process has been initiated – with employee involvement and participation at the

heart of overall project success

5

I. Group Business Strategy Core Market: Competitive Economy

Austria

Positive GDP development

2016e + 1.5 % (EU19: 1.7 %)

2017f + 1.8 % (EU19: 1.6 %)

GDP per capita1 above average

2016e EUR 46,822 (EU19: EUR 38,986)

2017f EUR 48,617 (EU19: EUR 40,398)

One of the lowest unemployment rates within the EU

2016e 6.0 % (EU19: 9.9 %)

2017f 5.8 % (EU19: 9.4 %)

Public debt below EU average

2016e 84.6 % (EU19: 91.7 %)

2017f 82.4 % (EU19: 90.6 %)

Level of corporate and household indebtedness substantially

below Euro-zone average

Attractive yield spreads relative to Germany

Housing market: no oversized construction sector and low level of

household indebtedness

Lower Austria / Vienna

40 % of Austria‘s population live and work in

Lower Austria and Vienna

Region with highest population growth potential

2015-2075

41 % of Austrian GDP is generated in Lower Austria and Vienna

Highest gross income from employment

Lower Austria (# 1) EUR 33,118

Vienna (# 3) EUR 31,330

Highest purchase power per inhabitant

Lower Austria (# 1) EUR 21,048

Vienna (# 3) EUR 20,870

Fiscal equalisation scheme secures strong and prudent

framework for investors

Privileged access to international financial markets through

Federal Financing Agency (ÖBFA)

1 EIU, GDP per capita at purchase price parity; 03/2017

6

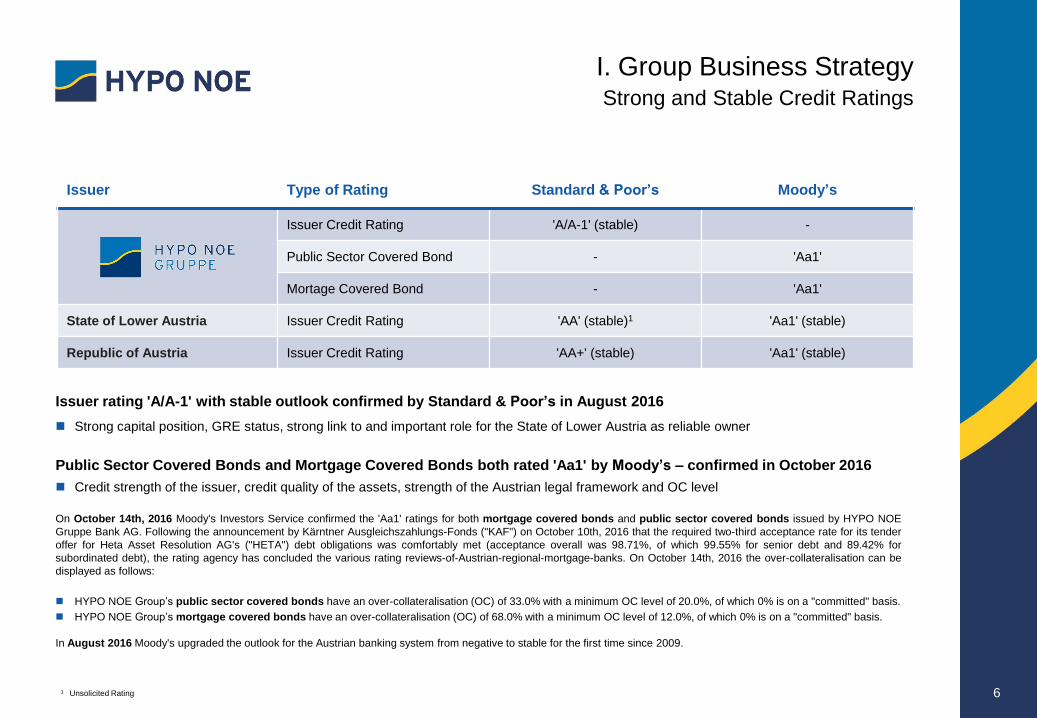

Issuer rating 'A/A-1' with stable outlook confirmed by Standard & Poor’s in August 2016

Strong capital position, GRE status, strong link to and important role for the State of Lower Austria as reliable owner

Public Sector Covered Bonds and Mortgage Covered Bonds both rated 'Aa1' by Moody’s – confirmed in October 2016

Credit strength of the issuer, credit quality of the assets, strength of the Austrian legal framework and OC level

On October 14th, 2016 Moody's Investors Service confirmed the 'Aa1' ratings for both mortgage covered bonds and public sector covered bonds issued by HYPO NOE

Gruppe Bank AG. Following the announcement by Kärntner Ausgleichszahlungs-Fonds ("KAF") on October 10th, 2016 that the required two-third acceptance rate for its tender

offer for Heta Asset Resolution AG's ("HETA") debt obligations was comfortably met (acceptance overall was 98.71%, of which 99.55% for senior debt and 89.42% for

subordinated debt), the rating agency has concluded the various rating reviews-of-Austrian-regional-mortgage-banks. On October 14th, 2016 the over-collateralisation can be

displayed as follows:

HYPO NOE Group’s public sector covered bonds have an over-collateralisation (OC) of 33.0% with a minimum OC level of 20.0%, of which 0% is on a "committed" basis.

HYPO NOE Group’s mortgage covered bonds have an over-collateralisation (OC) of 68.0% with a minimum OC level of 12.0%, of which 0% is on a "committed" basis.

In August 2016 Moody's upgraded the outlook for the Austrian banking system from negative to stable for the first time since 2009.

1 Unsolicited Rating

Issuer Type of Rating Standard & Poor’s Moody’s

Issuer Credit Rating 'A/A-1' (stable) -

Public Sector Covered Bond - 'Aa1'

Mortage Covered Bond - 'Aa1'

State of Lower Austria Issuer Credit Rating 'AA' (stable)1 'Aa1' (stable)

Republic of Austria Issuer Credit Rating 'AA+' (stable) 'Aa1' (stable)

I. Group Business Strategy Strong and Stable Credit Ratings

7

Sustainability ratings are an important evaluation with regards to corporate social responsibility performance and as such for a

holistic and future-orientated corporate governance. Therefore, sustainability ratings become an increasingly important aspect of

socially responsible investment decisions.

The corporate social responsibility performance of HYPO NOE Group is currently assessed by the sustainability rating agencies

oekom research, imug and rfu.

As part of a successful sustainability programme HYPO NOE Group was in 2015 awarded for

the first time a 'C' rating with the status of 'Prime' .

'Prime' is awarded for an above-average commitment in the areas of environmental and social

responsibility.

HYPO NOE Group was rated in 2016 by the Austrian rating agency rfu and awarded with the

status of "rfu qualified" (rating result: ba ). rfu is an Austrian company specialising in

sustainable investment and in particular sustainability analysis .

The best performing companies are awared with the status "rfu qualified“ and added to the rfu

sustainable investment universe.

I. Group Business Strategy Top Sustainability Ratings from oekom & rfu

8

HYPO NOE Group is in the upper quarter of all rated issuers of Public Pfandbriefe (Public Sector

Covered Bonds) .

HYPO NOE Group is the best of all rated issuers of Public Pfandbriefe in the savings bank

sector .1

1 As an issuer HYPO NOE is assigned to the savings bank sector (incl. Landesbanks and mortgage banks).

HYPO NOE Group is in the upper quarter of all rated issuers of mortgage bonds (Mortgage

Covered Bonds).

HYPO NOE Group is the best of all rated issuers in the savings bank sector.1

HYPO NOE Group is in the upper quarter of all rated financial institutions (including development

banks).

HYPO NOE Group is the best of all rated issuers in the savings bank sector.1

I. Group Business Strategy Top Sustainability Ratings from imug

9

Public Finance

Corporate & Structured Finance

Religious Communities,

Special Interest

Groups & Agriculture

Real Estate Finance

Real Estate Services

Retail Customers

I. Group Business Strategy Competence and Experience Drive Business Focus

Strategic Business Units

Public Finance

Financing and leasing solutions for the public sector

Corporate & Structured Finance

Corporate and structured finance solutions

Project and infrastructure finance

Local SMEs

Religious Communities, Special Interest Groups &

Agriculture

Financing solutions

Ethical investments

Property & facility management

Real Estate Finance

Financing of commercial projects and housing developers

Real Estate Services

Project development and management

Property management

Facility management

Retail Customers

Experts on mortgages and housing for private customers

and special services for professionals

10

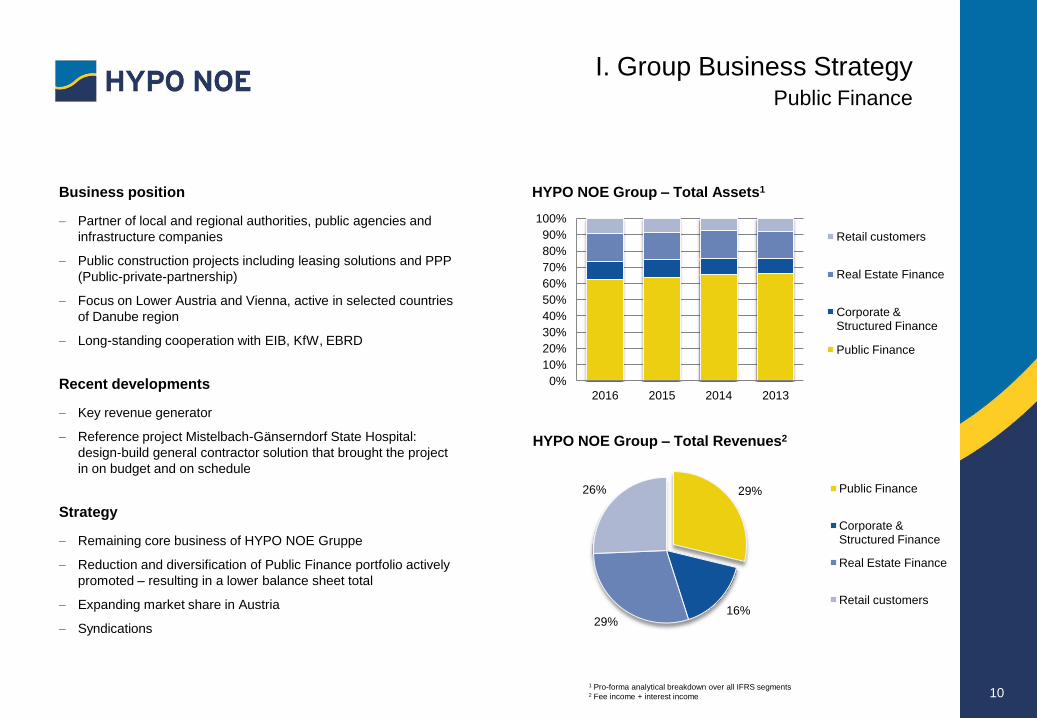

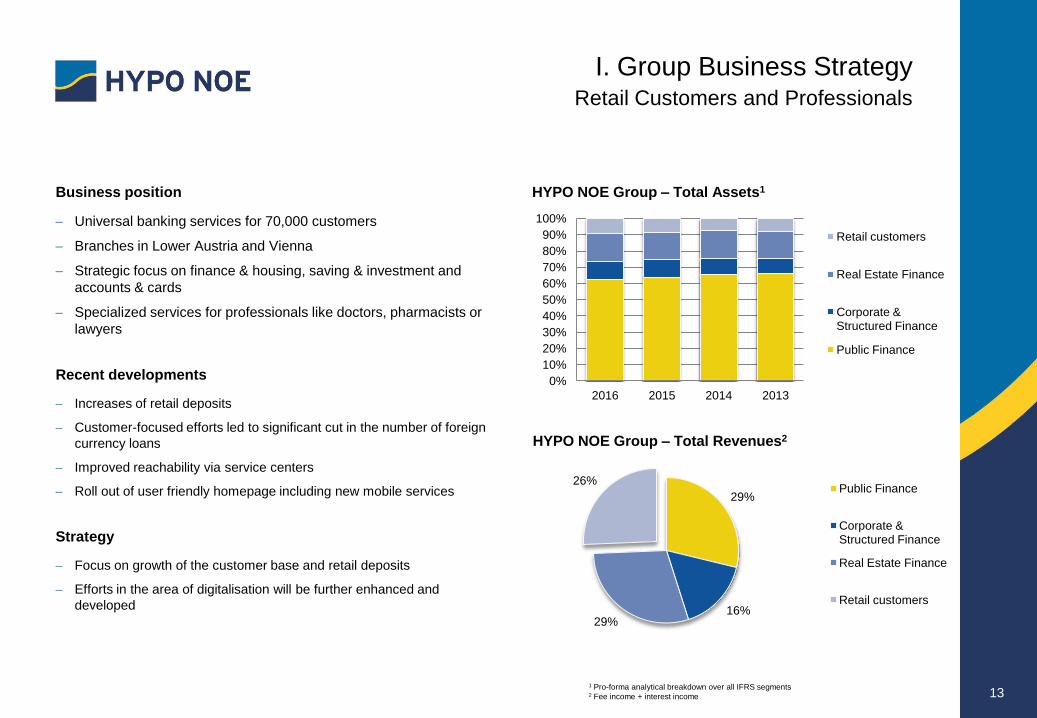

Business position

Partner of local and regional authorities, public agencies and

infrastructure companies

Public construction projects including leasing solutions and PPP

(Public-private-partnership)

Focus on Lower Austria and Vienna, active in selected countries

of Danube region

Long-standing cooperation with EIB, KfW, EBRD

Recent developments

Key revenue generator

Reference project Mistelbach-Gänserndorf State Hospital:

design-build general contractor solution that brought the project

in on budget and on schedule

Strategy

Remaining core business of HYPO NOE Gruppe

Reduction and diversification of Public Finance portfolio actively

promoted – resulting in a lower balance sheet total

Expanding market share in Austria

Syndications

1 Pro-forma analytical breakdown over all IFRS segments 2 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16% 29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Public Finance

11

Business position

Corporate and structured corporate finance solutions for the mid-cap

and large corporate segments

Regional focus Austria, Germany and defined markets of the Danube

region

International business focus on infrastructure and corporates of

strategic relevance.

Specialized team for target group religious communities, interest

groups and agriculture

Recent developments

Intense competition and subdued credit demand

Focus on SME business in core markets

Financing of the renovation of sacral buildings

Selective financing of renewable energy projects

Strategy

Structured corporate lending will remain a high priority

Drive Danube strategy forward by partnering with Austrian and local

businesses in the region

Build up a range of ethical investment products

1 SME business (33% of corporate portfolio) is part of HYPO NOE Landesbank

2 Pro-forma analytical breakdown over all IFRS segments 3 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16% 29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Corporate & Structured Finance1

12

Business position

Financing solutions for the asset classes:

office, logistics, warehouse and residential property, shopping

Pfandbriefe remain outstanding in case of issuers‘s bankruptcy YES YES

NPV matching YES1 YES

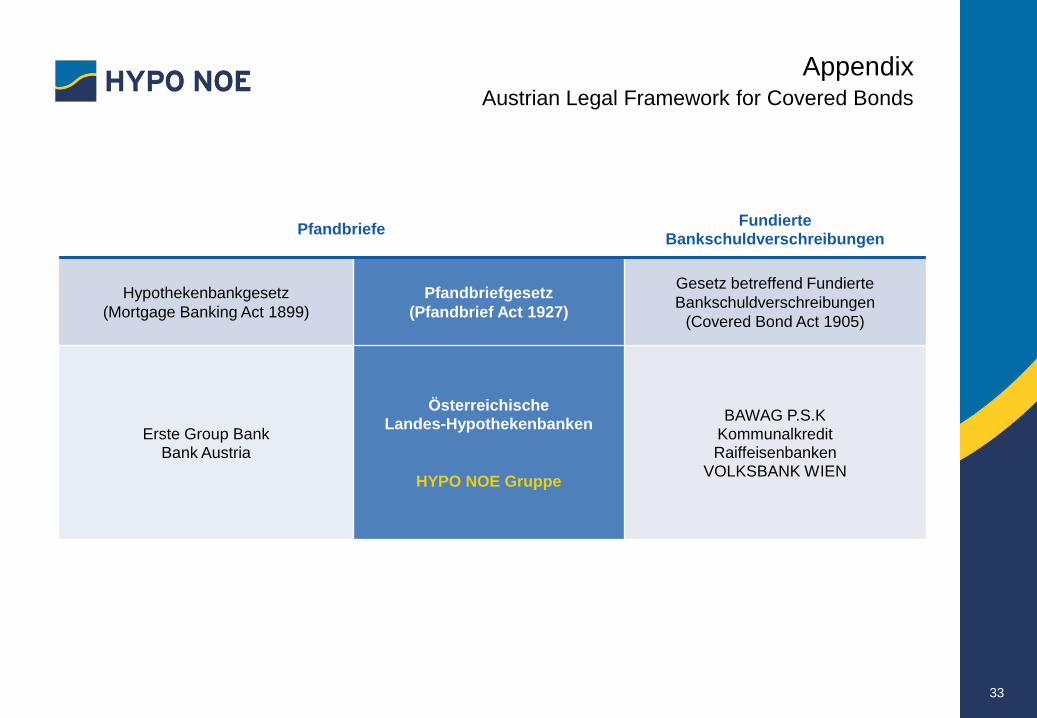

Austrian Pfandbrief law was initially based on German legislation

Important changes to the German Pfandbrief law were followed by Austrian legislation

Main differences: Germany allows collateral from non-European countries; NPV matching is compulsory in Germany and voluntary

in Austria (self-commitment by issuing bank in Articles of Association)

1 if included in the Articles of Association of the respective credit institution

Appendix Comparison of Austrian vs. German Pfandbrief Law

35

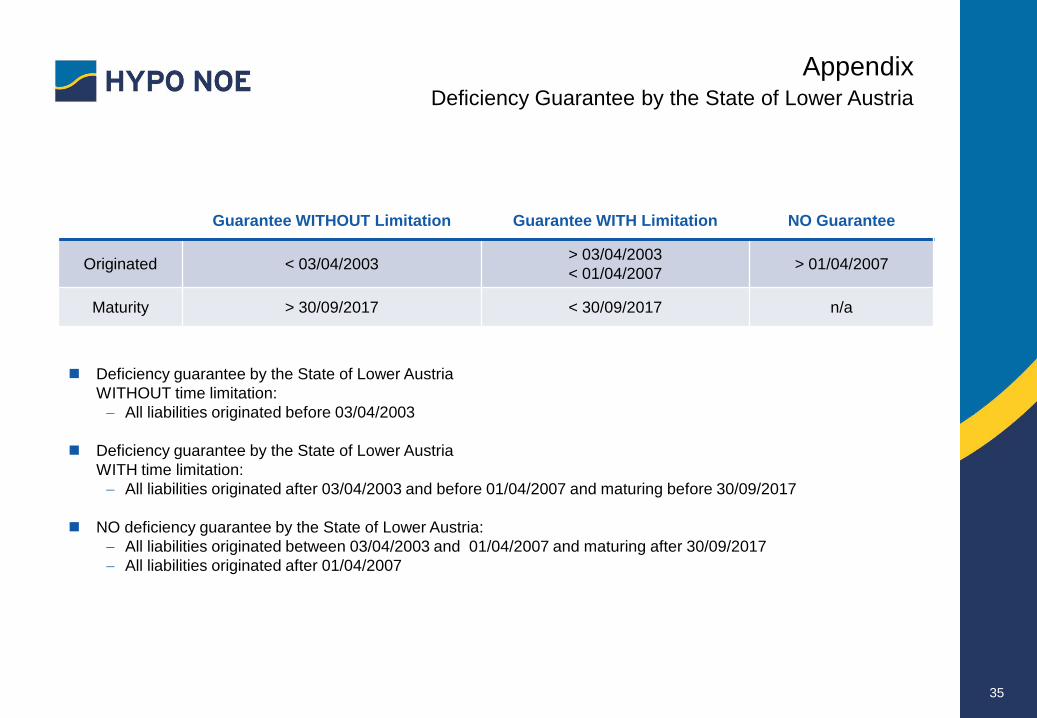

Deficiency guarantee by the State of Lower Austria

WITHOUT time limitation:

All liabilities originated before 03/04/2003

Deficiency guarantee by the State of Lower Austria

WITH time limitation:

All liabilities originated after 03/04/2003 and before 01/04/2007 and maturing before 30/09/2017

NO deficiency guarantee by the State of Lower Austria:

All liabilities originated between 03/04/2003 and 01/04/2007 and maturing after 30/09/2017

All liabilities originated after 01/04/2007

Guarantee WITHOUT Limitation Guarantee WITH Limitation NO Guarantee

Originated < 03/04/2003 > 03/04/2003

< 01/04/2007 > 01/04/2007

Maturity > 30/09/2017 < 30/09/2017 n/a

Appendix Deficiency Guarantee by the State of Lower Austria

36

HETA moratorium directly

Moratorium on HETA debt repayments imposed by the Austrian

Financial Market Authority on March 1, 2015

HYPO NOE held EUR 225mn of HETA debt securities on its own

portfolio

Cumulated write-down in 2014-2015 based on model calculations:

EUR 87.1 mn including impairment hedge adjustment

(35.85 % of face value EUR 225 mn)

Significant non-recurring income in 2016 from the sale of Carinthian

Compensation Payment Fund (KAF) zero-coupon bonds received

under the exchange for HETA securities incl. unwinding: EUR 59.5 mn

Pfandbriefbank (Österreich) AG – formerly Pfandbriefstelle

All eight member banks and their guarantors –

Austria’s federal states – bear joint and several liability

All members agreed on providing sufficient liquidity,

i.e. 1/8 each (= 12.5 % or approx. EUR 155mn)

HYPO NOE received explicit backing of the State of Lower Austria for

its part of joint and several liability for “Pfandbriefstelle“ issues,

therefore was no risk provisioning nor regulatory capital required

Appendix HETA moratorium – credit risk dimensions

37

Financial Market Authority (FMA)

The FMA issued a special notice imposing a moratorium on debt repayments by HETA until 31 May 2016.

By decision of 10 April 2016 a haircut was imposed by the FMA .

Tender & exchange offer and buy back offer

Tender offer for repurchase of HETA bonds at an envisaged discounted value (75% of face value) by Carinthian Compensation

Payment Fund (KAF) was denied by the creditors and did not reach a necessary two-third majority in March 2016.

On 18 May 2016, the Republic of Austria and a majority of HETA creditors underwent a MoU to create an out-of-court

settlement. A new tender offer of approx. 90% of the nominal value was expected to be disclosed in autumn 2016, which

required a significantly lower depreciation compared to the FMA haircut mentioned above.

Under the new tender offer which was announced by KAF on 6 September 2016, and which was valid until 7 October, creditors

had a choice between a cash payment totalling around EUR 7.8bn and an or zero-coupon notes with a total nominal value of

EUR 10.4bn.

Following the announcement by KAF on 10 October 2016 that the required two-third acceptance rate for its tender offer for

HETA Asset Resolution AG's debt obligations was comfortably met (acceptance overall was 98.71%, of which 99.55% for

senior debt and 89.42% for subordinated debt).

HYPO NOE Group accepted the exchange for a zero-coupon bond with an abstract, explicit, unconditional and irrevocable

guarantee by the Federal Republic of Austria upon first demand.

In December 2016, the zero-coupon bond was sold back to KAF for net proceeds of EUR 59.5 mn incl. unwinding.

HYPO NOE Group no longer holds any HETA or KAF bonds. Therefore, HYPO NOE Group is no longer subject to any

exposure-related risks with regards to HETA or KAF.

Appendix HETA moratorium – legal implications

38

This document does not constitute an offer to sell, or the solicitation of an offer to subscribe for or buy, any securities, investments or any other financial instruments, in or of HYPO

NOE Gruppe Bank AG, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision. This

document does not constitute an investment analysis or a recommendation to buy or to sell and is not intended to substitute any individual investment advice. Any such offers will

only be made when a prospectus in relation to the Offering is published in due course. This presentation will only be part of an offer, when it is explicitly referenced in the respective

offer.

No reliance may be placed for any purposes whatsoever on the information contained in this document or on its completeness. No representation or warranty, expressed or implied,

is given by or on behalf of HYPO NOE Gruppe Bank AG or the banks represented in this presentation or any of such institutions’ affiliates, directors, officers or employees, advisors

or any other person as to the accuracy or completeness of the information or opinions contained in this document and no liability whatsoever is accepted for any such information or

opinions or any use which may be made of them.

This document is intended for distribution in the United Kingdom only to persons who have professional experience in matters relating to investments falling within Article 19(5) of the

Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended, or to those persons to whom it may otherwise lawfully be distributed. Neither this document

nor any copy of it may be taken or transmitted in or into the United States or to any US person (as defined by Regulation S of the US Securities Act of 1933 (the “Securities Act”)) or

transmitted in or into Australia, Canada or Japan or to Australian, Canadian or Japanese persons. Securities of HYPO NOE Gruppe Bank AG have not been and – as of the date of

this presentation – will not be registered under the Securities Act and may not be offered or sold in the United States absent registration under the Securities Act or exemption from

the registration requirements thereof. There will be no public offer of securities of HYPO NOE Gruppe Bank AG in the United States. The distribution of this document in or into other

jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about and observe, any such restrictions. Any failure to

comply with this restriction may constitute a violation of applicable securities law and regulations.

Certain market data and financial and other figures (including percentages) in this document were rounded in accordance with commercial principles. Figures rounded in this manner

may not in any and all cases add up to the stated totals or the statements made in the underlying sources. For the calculation of percentages used in the text, the actual figures,

rather than the commercially rounded figures, were used. Accordingly, in some cases, the percentages provided in the text may deviate from percentages based on rounded figures.

Certain statements in this presentation are forward-looking statements. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that

could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions could

adversely affect the outcome and financial effects of the plans and events described herein. HYPO NOE Gruppe Bank AG does not undertake any obligation to update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on forward-looking statements, which speak as

only of the date of this presentation. Statements contained in this presentation regarding past trends or activities should not be taken as a representation that such trends or activities

will continue in the future.

Although due care has been taken in compiling this document it cannot be excluded that it is incomplete or contains errors.

HYPO NOE Gruppe Bank AG, its shareholders, advisors and employees are not liable for the accuracy and completeness of the statements, estimations and the conclusions

contained in this document. Possible errors or incompleteness do not constitute any grounds for liability, neither with regard to indirect nor direct damages. For the avoidance of

doubt HYPO NOE Gruppe Bank AG points out that it is not liable for any losses, damages or disadvantages including direct, indirect, financial, immaterial, special or consequential

loss or damage (whether for loss of profit or otherwise) due to this document or any of the statements contained therein.

By reading / downloading this presentation, you explicitly agree to be bound by the above.

NOT FOR DISTRIBUTION IN THE UNITED STATES OF AMERICA, AUSTRALIA, CANADA AND JAPAN.