I. Intro........................................................................ 2 A. URI v. Ram Holdings.........................................................2 B. Background..................................................................2 II. Acquisition mechanics....................................................... 6 A. Three basic state-law structures............................................6 1. Statutory Merger (Stock for Stock)........................................7 2. Asset Acquisition (Cash for Assets).......................................8 3. Stock Acquisition (Cash for Stock)........................................9 B. Alternative structures.....................................................10 1. Stock for Assets Acquisition.............................................10 2. Reverse Asset Acquisition................................................10 3. Stock for Stock Acquisition..............................................11 4. Two-Stage Acquisition....................................................11 5. Triangular Structure.....................................................11 B. Summary....................................................................13 C. Reorgs, Recaps, Reincorps, and Conversions.................................15 D. Appraisal remedy...........................................................17 E. Securities law issues – Williams Act.......................................23 III. Successorship............................................................. 25 A. Transfers of assets........................................................25 B. Successor liability........................................................26 1. State law................................................................26 2. Federal law..............................................................27 C. Liability avoidance strategies.............................................29 1. Dissolution provisions of state corporate codes..........................30 2. Legal capital statutes...................................................31 3. Fraudulent conveyance law................................................31 4. Breach of fiduciary duties...............................................34 IV. Deal Issues................................................................ 34 A. Documents..................................................................34 1. Preliminary documents....................................................34 1

Transcript

I. Intro....................................................................................................................................................................................2

A. URI v. Ram Holdings......................................................................................................................................................2

B. Background...................................................................................................................................................................2

II. Acquisition mechanics.......................................................................................................................................................6

A. Three basic state-law structures...................................................................................................................................6

1. Statutory Merger (Stock for Stock)............................................................................................................................7

2. Asset Acquisition (Cash for Assets)............................................................................................................................8

3. Stock Acquisition (Cash for Stock).............................................................................................................................9

B. Alternative structures..................................................................................................................................................10

1. Stock for Assets Acquisition.....................................................................................................................................10

3. Stock for Stock Acquisition......................................................................................................................................11

B. Summary.....................................................................................................................................................................13

C. Reorgs, Recaps, Reincorps, and Conversions..............................................................................................................15

D. Appraisal remedy........................................................................................................................................................17

E. Securities law issues – Williams Act.............................................................................................................................23

III. Successorship.................................................................................................................................................................25

A. Transfers of assets......................................................................................................................................................25

B. Successor liability........................................................................................................................................................26

1. State law..................................................................................................................................................................26

2. Federal law..............................................................................................................................................................27

C. Liability avoidance strategies......................................................................................................................................29

1. Dissolution provisions of state corporate codes......................................................................................................30

2. Legal capital statutes...............................................................................................................................................31

4. Breach of fiduciary duties........................................................................................................................................34

IV. Deal Issues.....................................................................................................................................................................34

A. Documents..................................................................................................................................................................34

B. Litigation.....................................................................................................................................................................35

V. Legal Duties of Owners & Managers...............................................................................................................................37

A. Board’s duties in negotiated deals..............................................................................................................................37

1. Duty of care.............................................................................................................................................................39

2. Duty of loyalty.........................................................................................................................................................41

B. Board’s decision to block hostile takeover..................................................................................................................42

I. Intro

A. URI v. Ram Holdings Forthright negotiator principle

o One party has subjective intent and the other party knows (or should know) about ito This is dumb and doesn’t really exist- merger agmt is about advantage-taking

Reverse break-up feeo Buyer agrees to pay fee if they don’t consummate purchaseo Less typical than break-up fee paid by sellers (to prevent shopping in name of fid duty)

Constraints on opportunismo Judge trying to limit opportunism re lawyering, reputation, law, etc.

B. Background Capitalist arc

o Form a firmo Raise moneyo Build a businesso Sell Control

IPO – more popular in 90s Merger or acquisition – way more popular now

Catalysts of merger activityo Regulatory change – Telecom Act of 1996o Technological change – Interneto Healthy capital markets – Bull market w low interest rateo Egoo Random walko Way to cash out

Reasons for firm combinationso Grow or die (build v. buy)

2

Grow existing business Create new business Buy new business

o A thinks it can make more value w T’s assets than T can Efficiency motives (increase size of pie)

Economies of scale/scope – manufacturing efficiencies, extending management talent to larger asset base

Reduce production costs – McDonalds buying meat processing firm Replacing bad management – lower agency costs, new blood, better strategy Diversification Change capital structure Race to size – economies of scale – need to match upstream or downstream size –

WalMart factor Facilitates entry

o Speeds entry into new markets – products, geographyo Allows entry without adding to industry capacity

Changes in gov’t policy – altering distribution and payment systems Need for global reach – airline mergers/alliances Satisfy various stakeholders

Redistributive motives Shifting value from gov’t (NOLs) creditors (LBOs), or consumers (monopoly

pricing) All about tax

Bad motives Market power Overestimation of synergies Empire building (driven by poor economic incentives) Social prestige Boredom Hubris Bootstrap game

o T has lower growth prospectso Conglom is worth 2x T – can buy T’s 100K shares by issuing 50K shareso No synergistic value in mergero Earnings double but shares increase only by 50%o T shareholders trade cash for growth

o Questions to ask Competitiveness, fragmentation, and pace of marketplace for industry Access to capital Cost of capital Capabilities of management Capabilities of advisors Strength of core skills and competencies

3

Customer and supplier loyalty Degree to which speed to market and scale are critical

Do acquisitions create value?o Shareholder value

Net gains are modest (1%) Target shareholders do very well (20-50% premia) Acquirer shareholders lose in short and long run Best deals are those w cash, serial acquirers, and privately held targets

o Societal concerns Job losses from mergers High cost of lawyers Potential for exploitation – bootstrap game

o Key drivers of profitable acquisitions Synergies

Sale or redeployment of underperforming assets positively rec’d by investors Building market power does not pay

Studies show gain from M&A do not come from anticompetitive combinations Payment w stock is costly, cash is neutral

Signal that firm stock price is overvalued Discipline of cash

Regulation Costs of Williams Act

o Management efficiencies Ts are by and large decent performers T managers are displaced in less than 50% of cases As usually lose $ or break even Surviving firms generally NOT better managed

What causes failure?o Inspection problem

Winner’s curse – thrill of chase blinds pursuers of consequences of catch Lemons problem Most common in conglomerate mergers – 85% in tire industry were failures

o Interaction problem Poor integration of businesses Inability to make cuts as promised Culture clash Departure of key personnel Change as result of merger process

Deal time-tableo Discussion phase

CEO-CEO information understanding4

Letter of intent or term sheet Mostly internal advice – some outside opinions

o Discovery phase Confidentiality agmt Due diligence begins

o Mating dance phase Negotiations about price, structure, and documentation Draft Acquisition or Merger Agmt

o Approval phase Prepare notices and disclosures Both Boards of Directors Approve (sign Exec Agmt) Shareholders approve

o Closing phase T&R list – closing agenda Exchange accomplished

Lawyers’ roleo Can really mess things upo Have monopoly over litigationo Other profs can render good merger advice for cheapero Need to not just divide pie, but expand pie

Deal Valuationo Gain from deal = value of combined firm – sum of value of individual firms on owno Cost = amount paid less value of firm boughto Only do deal if gain > cost

Risk-shifting strategieso Collar - range of acceptable variation in deal terms

Price collar - fixed to exchange ratio deals Share collar - floating exchange ratio deals

o Walk-away right - gives T the right to walk away from merger if A’s stock price falls below certain level (not common bc don’t want to ruin deal w temp market fluctuation and shareholder vote gives de facto walk-away right)

Single trigger – if stock down 15%, T can walk away Double trigger – if stock down 15% and 15% relative to pre-defined industry peer group,

T can walk away Post-closing adjustments

o True-ups Adjust purchase price based on status of T’s balance sheet at closing Set amount specified for working capital and payments made by either buyer or seller for

difference from amounto Earnouts

Delayed payment schedule A pays part of price as % of post-closing profits

5

Used mostly for small, closely held firmso Contingent valuation rights

Securities issued to target shareholders If A firm stock price trades below target price for specific time post-closing, holder of

CVRs get consideration to make them wholeo Other delay problems (bt inking & closing the deal)

Depletion of physical assets, including cash Departure of key personnel Misbehavior of outgoing executives – final period problems

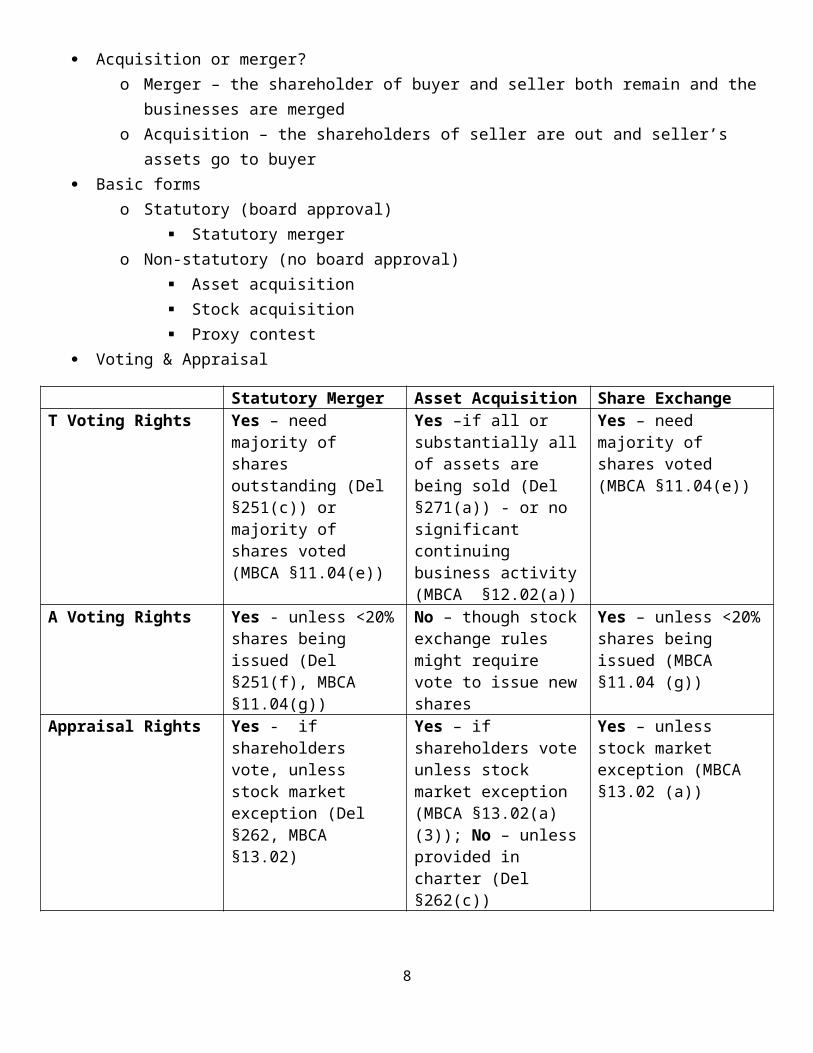

II. Acquisition mechanics

A. Three basic state-law structures Types of mergers

o Horizontal merger Direct competitors K-Mart & Sears

o Vertical merger Firms in different stages of production in same market Intel & TSMC

o Conglomerate merger Neither direct rival nor producers in same production chain Textron & Cessna

Acquisition or merger?o Merger – the shareholder of buyer and seller both remain and the businesses are mergedo Acquisition – the shareholders of seller are out and seller’s assets go to buyer

Basic formso Statutory (board approval)

Statutory mergero Non-statutory (no board approval)

Asset acquisition Stock acquisition Proxy contest

Voting & Appraisal

Statutory Merger Asset Acquisition Share ExchangeT Voting Rights Yes – need majority of

shares outstanding (Del §251(c)) or majority of shares voted (MBCA §11.04(e))

Yes –if all or substantially all of assets are being sold (Del §271(a)) - or no significant continuing business activity (MBCA §12.02(a))

Yes – need majority of shares voted (MBCA §11.04(e))

6

A Voting Rights Yes - unless <20% shares being issued (Del §251(f), MBCA §11.04(g))

No – though stock exchange rules might require vote to issue new shares

Yes – unless <20% shares being issued (MBCA §11.04 (g))

Appraisal Rights Yes - if shareholders vote, unless stock market exception (Del §262, MBCA §13.02)

Yes – if shareholders vote unless stock market exception (MBCA §13.02(a)(3)); No – unless provided in charter (Del §262(c))

o Del § 251 – Agreement, Board Approval, Shareholder Approvalo MBCA § 11.01 et seq – Share Exchanges

Stepso A & T boards approve the mergero Proxy materials distributed to shareholders as neededo Shareholder voting

T shareholders ALWAYS vote per §251(c) A shareholders vote if A stock outstanding increases by > 20 % per §251(f)

o If majority of shares outstanding approves, T assets merge into A and T shareholders get back A stock – certificate of merger is then filed w Secy of State

o Dissenting shareholders who had a right to vote have appraisal rights Impact

o A continues in existence, likely as NewCoo T ceases to existo All property and contract rights of T & A are now vested into NewCoo All liabilities of T & A are vested in NewCo (who steps into their shoes in litigation)o Articles of incorporation and bylaws of A are amended as provided in merger agmt)o Shares of T & A are coverted into new form (cash, stock, etc) as provided in Merger Agmt

Voting – basic procedure that both corp’s holder ratifyo Who votes?

Del: only voting shares, but can be altered in K MBCA §11.04: class voting mandatory

o Type of majority required? Old rule: unanimity Del: majority of outstanding holders MBCA §11.04(e): majority of those present, if quorum

o Exceptions to shareholder voting Short-form mergers – Del §253: parent holds >90% of each class of voting stock in sub

7

Small-scale mergers – Del §251(f): 20% dilution rule – A shareholders must hold 83% of voting shares at conclusion of trans (also applies to cash-out mergers)

Holding company reorganizations – Del §251(g)

2. Asset Acquisition (Cash for Assets) Basics

o DGCL §271: sale; lease or exchange of assets; consideration, procedure – corp may sell all or substantially all of its assets when the holders of majority of stock vote thereon

o MBCA §12.01 et seq Steps

o Boards of A & T approve the dealo Only T’s shareholders get voting and (outside DE) appraisal rights (only T is being bought) –

and only if selling substantially all assetso Trans costs generally higher because title to actual physical assets of T must be transferred to Ao After transfer, selling T usually liquidates the consideration rec’d (cash) to its stockholders – also

requires vote Impact

o T continues to exist, with all directors and shareholders – no automatic operation by law (raises costs)

o All property must be transferred to A individually – documents of transfer prepared, docs filed w gov’t (raises trans costs again)

o Consideration for assets sale must be distributed to T’s shareholders (raises costs)o A doesn’t assume T’s liabilities unless written assumption of liabilities or tort exceptionso Parties often try to opt of stay in private K, but this will not be enforcedo Lots in stay legislation that doesn’t have to do with Cs, so get many exceptions

Appraisal rights exceptions (general rule in DE = no appraisal rights)o New York – appraisal rights in asset sales if consideration in stock, but not cash (if seller

dissolves w in 1 year)o CA – appraisal rights in assets sales if consideration is stocko MBCA

1984: very liberal – full link bt voting and appraisal 1999: de-links voting and appraisal in several areas

No appraisal rights if securities not altered No appraisal rights on amendments to charter (unless reverse stock split) Market out exception Appraisal rights for cash for assets acquisition

Substantially all of assetso Cases

Katz v. Bregman (Del, 1981) Sale of business making steel drums representing >50% of assets to go into plastic

drum business IS sale of substantially all the firm’s assets Qualitative – 50%

8

Qualitative – switch to new business that could be radical departure Hollinger v. Hollinger Int’l (Del, 2004)

Issue is whether trans leaves stockholder w investment that in economic terms is qualitatively different than the one they now possess

Gimbel Brothers (Del, 1974) Don’t invest for stuff other than money Economic value to corp as new entity is what matters

o Rules of thumb DE

>75% is substantially all <25% is NOT substantially all

MBCA Sale OK w out shareholder vote unless would leave the corp w out significant

business activity 1999 amendment creates 25% safe harbor rule

Reasons for votingo Other “bet the company” stuff doesn’t require voteo But M&A looks more like investment decisions than management decisionso Special agency problems of final period for incumbent managers

3. Stock Acquisition (Cash for Stock) Basics

o Del §203 – anti-takeover provisiono Negotiated or open market purchaseo Tender offer

Williams Act (federal) Schedule 13D filing (5% rule) §16 of ’34 Act (10% rule)

Stepso No voting rights for either A or T’s holders – vote w your feeto Boards agree on transo A pays cash to B and B sends its stock over to Ao A is now the parent of B, which is a wholly or partially owned subsidiaryo Old B shareholders hold cash and no stocko This is a taxable trans

Shidler v. All-American (Iowa, 1980)o In merger, common shares are cashed out – exchange of stock for casho One day, the owner of the common stock owns a part of an ongoing enterprise, the next he has $o Statute trumps charter languageo Class voting in some stateso Many ways to structure a trans, each w different consequences

9

B. Alternative structures

1. Stock for Assets Acquisition Steps

o Asset acquisition A shareholders have no voting rights B shareholders vote to ratify B assets and liabilities go to A, and A sends stock over to B as consideration

o B corp dissolves A corp has the assets and liabilities of B B dissolves and is extinguished

o This is is a tax-free acquisition (C reorg) Benefits

o Voting and appraisal DE: A shareholders get no voting or appraisal rights MBCA: gives voting rights, but not appraisal rights for A shareholders Some states: give both voting and appraisal rights

o De facto merger argument usually loser Disgruntled shareholders of A sue claiming stock-for-assets is really a merger NJ courts will apply it in some cases, though

Heilbrunn v. Sun Chemical (Del, 1959)o Purpose of the appraisal remedy

Stockholder forced against will to accept investment in foreign enterprise Compensation for former right to prevent merger (old unanimity rule)

o A firm shareholders do NOT get votes or appraisal in asset purchaseso Purchasing shareholders are DENIEDo No de facto merger doctrine

Leaves open minnow-swallow-whale case, though Hariton v. ARCO Electronics (Del, 1963)

o Trans was same as merger of seller into buyero Equal dignity rule: §251 and §257 deserve equal dignityo Attempt to distinguish would create uncertainty and invite litigationo Selling shareholders are DENIED

2. Reverse Asset Acquisition Steps

o Asset acquisition A shareholder have to vote to ratify; B shareholders do NOT get voting rights B moves a controlling block of its shares to A A sends assets and liabilities over to B as consideration

o A corp dissolves A shareholders, who had vote, now have controlling block of B shares

10

o Post-transaction A&B shareholders have stock in B corp B changes its name to A corp Holds B assets/liabilities and old A assets/liabilities

3. Stock for Stock Acquisition Steps

o Stock acquisition A shareholders have no voting rights A corp sends stock to B shareholders and B shareholders send stock back to A corp

o Post-transaction A corp is now the parent of B corp, which is wholly owned subsidiary of A This is a tax-free acquisition (B reorg)

Advantageso DE: A shareholders no voting or appraisal rightso MBCA: gives voting but not appraisal for A shareholderso CA, NJ, OH, RI: give both

4. Two-Stage Acquisition Steps

o Stock acquisition B shareholders give shares to A corp; A corp gives cash to B shareholders B is partially-owned subsidiary of A - A corp now owns 51% or more of outstanding B

shares, while old B shareholders own 49% or less of outstanding B shareso Squeeze-out merger

A shareholders have no vote; Old B shareholder do vote A drops down a new wholly owned sub and mergers B into the new sub – so B’s assets

and liabilities go to the new sub, who sends cash to old B shareholders B shares are then canceled and B corp is extinguished A shareholders now have A, which is the parent to the wholly owned sub, which now

changes its name to B corp Irving Bank Corp. v. Bank of New York (NY, 1988)

o Two-stage acquisition plan involving 1) acquisition of stock, not assets; and 2) a delay in the second step is NOT a merger

o Defacto merger doctrine only in cases where selling corp quickly ceases to existo Distinction bt asset sale (leaving only a shell) and stock purchase

Purposeo Speedo Reduce risk of competing bido Avoid “entire fairness” standard of review – requires stock acquisition for over 90% of T shares,

following by back-end short form merger

11

5. Triangular Structure Merger v. Asset sale

o Transfer of control – merger process much easiero Transfer of assets – merger process much easiero Transfer of consideration – merger process much easiero Successor liability – asset sale more flexibility o Shareholder voting – generally no voting by acquirer shareholders (Del)o Appraisal rights – no appraisal rights for seller (Del)

Triangle basicso Want ease of merger AND flexibility of asset saleo Two types (also used for asset and stock acquisitions)

Forward – T merges into sub Reverse – sub mergers into T

Advantageso A shareholders don’t vote or get appraisal rightso Sub shareholders must vote, but only has one holder (A) w one share voted by boardo Limits timely, costly, and uncertain voting; ex post litigation over appraisalo Isolates sub in limited liability position

State treatmento CA

A shareholders vote in asset and stock acquisitions if consideration is stock Attempts to apply rights equally when substance transaction is the same – equivalency of

rights based on substance (NYSE agrees only on voting) Shareholder voting and appraisal rights stuff apply to foreign corps w minimal contacts in

CA – does not apply to publicly traded corpso NY

Imposes appraisal process on all companies doing biz in NY Steps (forward triangular merger)

o Drop down Sub A files certificate of incorp for Sub; capitalizes Sub with A shares B is just chillin w its shareholders

o T merges into Sub A shareholders have no voting votes; B holders must vote to ratify B corp gives assets and liabilities to Sub; Sub gives A shares to B holders (§251 merger) B stock is cancelled and B corp is extinguished at this point

o Post-trans A shareholders not include B holders – still hold Sub Sub changes name to B Corp; holders B Corp assets and obliged on B’s liabilities

Rauch v. RCA Corp (2nd Cir, 1988)o GE sub merges into RCA to avoid liquidation of RCA, and therefore obligation to pay

dissolution premium to preferred holderso Conversion of shares for merger is legally distinct from redemption of shares

12

o Minority stock interests may be eliminated under a merger – where merger permitted by law, holders should know of this right when they buy preferred shares

Rothschild Int’l v. Liggetto Two-step transaction not a liquidation requiring payment of preference – no liquidation bc

reverse cash-out merger did not liquidate the assets – stockholders know of this possibility Equity Group Holdings (SD FL, 1983)

o Minnow swallows whale to get tax benefito Complaints of purchasing firm holders (no voting/appraisal rights) fall on deaf ears outside of

CA, etc.o No de facto merger – business judgment of minnow swallowing whale fineo Would need breach of fid duty to hold otherwise

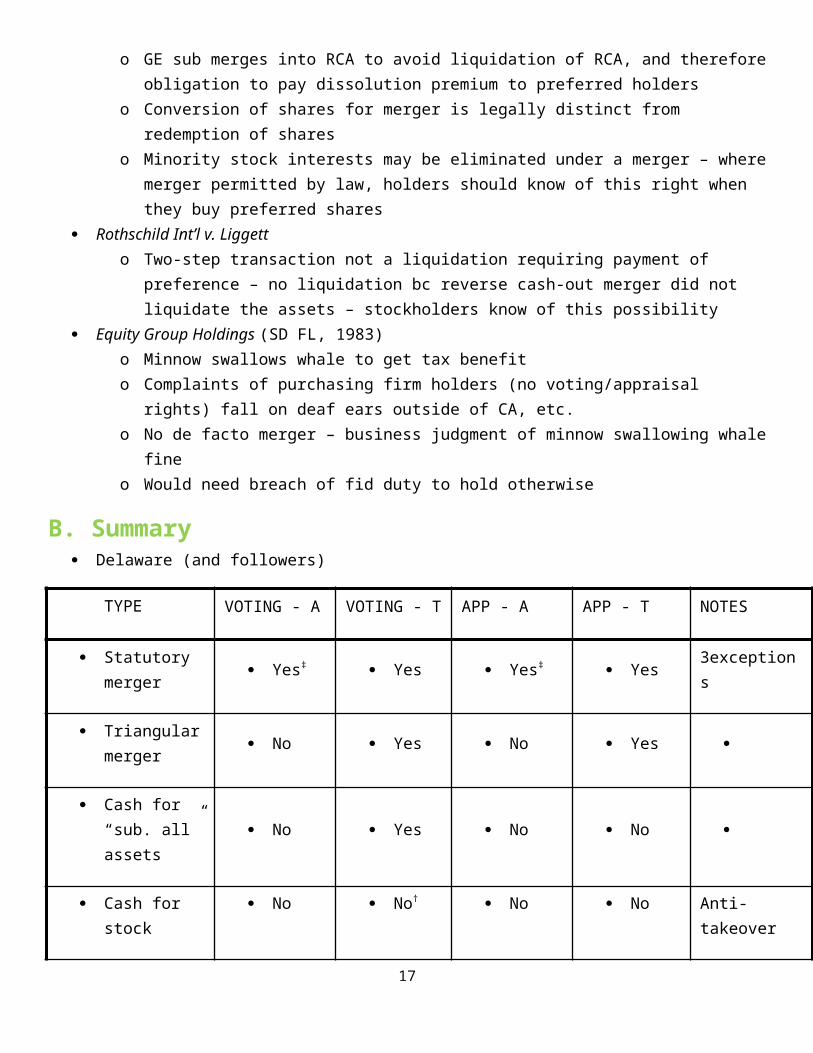

B. Summary Delaware (and followers)

TYPE VOTING - A VOTING - T APP - A APP - T NOTES

Statutory merger

Yes‡ Yes Yes‡ Yes 3exceptions

Triangular merger

No Yes No Yes

Cash for “sub. all” assets

No Yes No No

Cash for stock No No† No No

Anti-takeover statute § 203

Stock for assets No Yes No No

Reverse stock for assets acq.

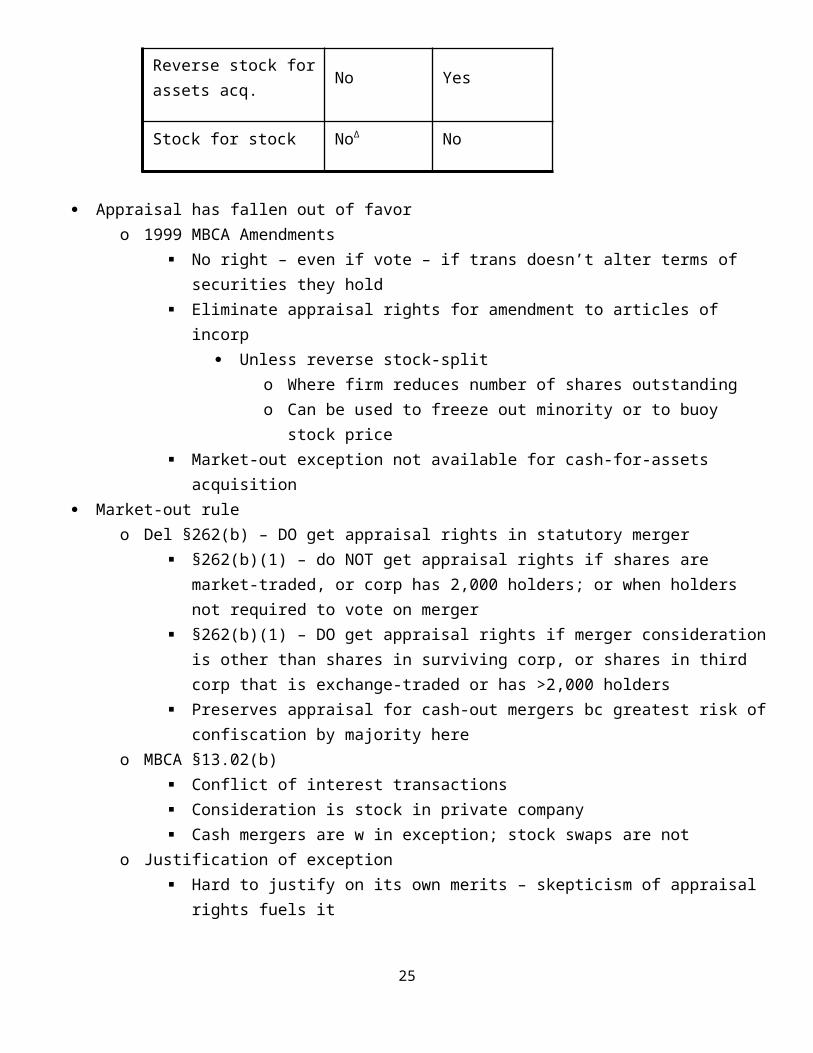

Yes No No No

Stock for stock No No† No No

Anti-takeover statute § 203

MBCA – 1984 (and followers)

13

TYPE VOTING - A VOTING - T APP - A APP - T NOTES

Statutory merger Yes* Yes Yes Yes

Triangular merger Yes* Yes Yes Yes

Cash for “sub. all” assets No Yes No No‡

Cash for stockNo No† No No

Anti-takeover statutes

Stock for assets Yes* Yes No∆ Yes

Reverse stock for assets acq.

Yes Yes No Yes

Stock for stockYes* No† No∆ No

Anti-takeover statutes

Advantages and disadvantageso Asset acquisition over statutory merger

A shareholders do not vote (except MBCA – CA – in stock-for-asset) B shareholders – no class vote – DE gives no appraisal rights

o Triangular deals over straight mergers A shareholders do not vote (except MBCA – CA – in stock-for-asset)

o Triangular merger over stock acquisition 100% ownership But, B shareholders vote and have appraisal rights A shareholders do not vote in either (except MBCA – CA)

o Two-step acquisition over triangular merger 100% ownership Vote is a formality Speed (avoid bidding war) If A has 90% ownership, B holders do not vote A shareholders do not vote (except MBCA – CA)

o De facto merger doctrine Dead w rare exceptions (NJ, Ark – require corp to dissolve immediately)

14

Always possible for inequitable transactions

C. Reorgs, Recaps, Reincorps, and Conversions Single-form reorganizations

o Recapitalizations Stage 1 – A corp drops down wholly owned sub

A has common and preferred holders Stage 2 – Statutory merger

A common have vote; A preferred don’t have vote A corp merges into sub – A is extinguished and both types of stock cancelled Sub changes its name to A corp

Example – eliminate preferred shares Amend Articles of Incorporation Using merger as alternative to charter amendment

o Reincorporations Example – reincorporate as a Del. Corp Amend Articles of Incorporation; Re-file Create a shell; merge into shell

o Conversions Example – change from an LLC to C Corp Conversion statutes Merger Reorganizations for going public

Exampleo LLC wants to go publico Creates C-Corp shell, merges into C, and exterminates the LLC

DE (and others) - allow business combination transactions among various typeso DE LLC or business trust, or LP can convert to DE Corpo Original entity must file certificate of conversion w DE Secy of Stateo Conversion will not affect any obligations incurred prior to conversiono Conversion does not constitute a dissolution – liabilities are tacking

Two-stage structureso Goals

Redistribute from one class of shareholders to another Achieve amendments to charter (or action that would require amendment or vote) w out

process of §242o Cases

Federal United Corp v. Havender (Del, 1940) Holding

o DE Court adopts highly literal and technical reading of corporate codeo Allows firms to eliminate dividend arrearages of preferred stockholders

15

o Shareholders on notice that corp may be merged w another if majority agree

o Merger, although legal, violated fid duties to preferred shareholders Some courts prevent common from discriminating preferred Del courts find duties largely only to common bc protect self w K

Resulto Preffereds w arrears are cashed out on the cheap

Impacto Advise clients to invest only in corps w charter provisions providing for

preferred voteo Must check provisions of individual investment contracts for these

protections Warner Comm v. Chris-Craft Industries (Del, 1989)

Holdingo Adverse effects from merger, not amendment – so no class voteo “Alter or change” in certificate only refers to process of amending

certificateo §251 merger that cancels stock in disappearing entity and modifies does

NOT mean an alteration of the outstanding stocko Court thinks that class voting (giving each class a veto) would lead to

opportunistic behavior by a class that would defeat mergers that are in the best interest of the firm

Resulto Same as Havender – preferreds are cashed out on cheapo But this time there was contractual attempt to address the problem

Elliot Assoc v. Avatex (Del, 1998) Holding

o A creates sub, mergers into sub, and changes its name back to Ao Need 2/3 vote if amendment to charter by merger, consolidation,

otherwiseo A says not surviving, so charter provision doesn’t applyo Court says parties must have had voting in mind also for cases in which A

disappears – gives voting right Result

o Here, contract language to protect preferreds is effective VGS, Inc. v. Castiel (Del, 2000)

Secret meeting and decision to merge to divest C of power – did they have to tell?o LLC Act §18-404: managers may do w out meeting as long as they have

enough votes to do the actiono LLC Operating Agmt: silent on notice/meeting/voting – no unanimity

requirement Court still finds obligation to tell C about meeting

16

o Written-consent allows for quick action where minority views irrelevanto Not meant to secretly deprive third managero Grounded in fid duty to majority equity owners – weapon in merger cases

for self interested transactions C appointed managers to protect him rather than statutory default

o Court says this means he gets more protection on boardo But didn’t C really trade control rights for the VC funding?

D. Appraisal remedy1. Policy arguments

Policy arguments foro Wertheimer – shareholders may depress price in order to cash out minority at discounto Pareto optimal – price floor makes sure that no one is made worse off by transaction

Policy arguments againsto Most stock-for-stock deals contain walk right if 3-5% or more of selling holders notify firm that

they will assert rightso So even if 95% of holders believe it’s a good deal, small minority can veto (in cash –poor deals)

2. Transactions supporting the right

Forms of dealso Selling firm shareholders

Statutory mergers (including short-form mergers) Asset acquisitions (except Del) Sale of control block (Mich, Fla, SC)

Appraisal has fallen out of favoro 1999 MBCA Amendments

No right – even if vote – if trans doesn’t alter terms of securities they hold Eliminate appraisal rights for amendment to articles of incorp

Unless reverse stock-split18

o Where firm reduces number of shares outstandingo Can be used to freeze out minority or to buoy stock price

Market-out exception not available for cash-for-assets acquisition Market-out rule

o Del §262(b) – DO get appraisal rights in statutory merger §262(b)(1) – do NOT get appraisal rights if shares are market-traded, or corp has 2,000

holders; or when holders not required to vote on merger §262(b)(1) – DO get appraisal rights if merger consideration is other than shares in

surviving corp, or shares in third corp that is exchange-traded or has >2,000 holders Preserves appraisal for cash-out mergers bc greatest risk of confiscation by majority here

o MBCA §13.02(b) Conflict of interest transactions Consideration is stock in private company Cash mergers are w in exception; stock swaps are not

o Justification of exception Hard to justify on its own merits – skepticism of appraisal rights fuels it

3. Procedural requirements

Shareholders must dissent (NOT vote “yes”) Must hold shares through date of merger close Must notify corp 20 days BEFORE the date of the vote (per §262(d)(1)) Must file petition w court after the vote

o Del: file within 120 days (per §262(e)) – trial can take yearso MCBA

Firm sends notice to dissenters w in 10 days Dissenter must return form to firm in 40 days Payment within 30 days – firm’s estimate of value + interest If dissatisfied, demand within 30 days – corp pays or files petition w in 60days

Court holds valuation proceeding to “determine shares’ fair value exclusive of any element of value arising from accomplishment/expectation of merger (§262(h))”

Atty fees and costso Del: charged against recovery pool

Firm does NOT pay for dissenters’ expenses even if dissenters prove they deserved more Want to discourage marginal claims

o MBCA: charged against firm

4. Exclusive remedy?

Main alternative = Injunctive relief o Available (pre-Weinberger) where merger “lacked proper business purpose” or “was not entirely

fair (Singer v. Magnavox)”o Choice bt property rules (injunction) and liability rules (damages)

19

Indifferent WHEN trans costs are zero Two types of claims in these cases– fair price AND fair dealing

o Weinberger (Del, 1983) – appraisal IS exclusive remedy UNLESS Fraud, misrepresentation Self-dealing Deliberate waste or corporate assets Gross and palpable overreaching

o Rabkin (Del, 1985) – P class actions (outside appraisal) appropriate IF breach of duty of fair dealing

Appraisal IS exclusive only when claims go solely to adequacy of price

5. Determination of “fair value”

§262(h)o Fair value exclusive of any element of value arising from mergero Court should take into account “all relevant factors”

Two main issueso Battle of experts – value of shares using “modern valuation techniques”o Should dissenting holders participate in gains of firm?

WHEN is value determined?o Value as minority shares – minority discount (least desirable for dissenters)o Value as pro rata claim on going concern value – no minority discount, but no claim on benefits

of dealo Value as pro rata claim on going concern value, including benefits of deal (most desirable for

dissenters) Valuation techniques

o Old method – “block method” or “DE block” – weighted average of: Net asset value (fair value of all assets, not necessarily book value) based on liquidation

value Capitalized earnings (multiple earnings per share x price/earnings ratio to get price per

share) – use comparables to get firm’s “price” Market value

Comparables – firm/market prices, mergers Share price – other publicly traded corps - use multiples of comps Company price (other acquisitions) – use multiples of comps

Discounted cash flow – primary methodology STEP 1 - Estimate yearly cash flow for 10 years – use historic earnings figures,

adjusting for market conditions and firm maturity

20

STEP 2- Estimate terminal value – firm value 10 years out (discounting dividends w zero or constant growth)

STEP 3 - Discount 11 figures in above steps and aggregate – select discount rate application to firm risk and market conditions

STEP 4 - Apply control premium to sum of 2 and 3 Option pricing method Free cash flow – best measure of financial performance (“cash is king”)

Operating cash flow minus capital expenditures Total Value methods

Liquidation value – book value or earning value of assets Sale of business Stable growth

o Cross-exam material of opposing experts Market value – liquidity and market anomalies Multiples – selection of comparable firms Discounted cash flow – estimate of future returns (based on averages) & selection of

discount rate Caselaw

o Cavalier Oil v. Harnett (Del, 1989) Holding

Ps say minority discount good bc low liquidity firms = minority shares trade for less

Court says NO minority discount - says §262 appraisal is “value of corp itself, as distinguished from specific fraction of its shares as they may exist in hands of particular shareholder”

Statute §262(a) – entitled to court’s fair value appraisal of holder’s shares of stock §262(h) – Court shall determine shares’ value exclusive of merger

Reasoning Leads to too much uncertainty and litigation Unjust enrichment for majority, who is already freezing out minority

BUT There is no obligation to share premiums w minority per corp law

o MG Bancorporation, Inc. v. Le Beau (Del, 1999) Ps say that valuation based on minority stake and not pro rata – experts say two different

things Court accepts Comparative Acquisitions analysis and removes minority discount –

applies ontrol premium applied to controlled banks Valuation based on operative reality at time of merger, assuming dissenters would be

willing to keep investment position had merger not occurred (assumes market price is that of minority shares)

Find MGB’s last 12 mos earnings and book value Identify comparable cos sold recently

21

Find multiples of earnings and book value for which comps were sold Apply multiple to MGB’s past earnings and book value Do NOT include control premium bc included an implicit premium

Litigation costs (DE) Interest only in extraordinary ccs Otherwise – parties bear own costs (unless equitable exception)

Avoiding extreme valuations Baseball – chose most reasonable estimate Night baseball – pick estimate closest to court’s estimate

o Weinberger v. UOP, Inc. (Del, 1983) What is Fair value

Holder entitled to be paid for that which has been taken from him Determination made on date the merger closes

What is relevant? Any facts which were known or could be ascertained as of date of merger which

sheds light on future prospects of corp Only speculative elements of value that may arise from accomplishment or

expectation of merger are excluded Elements of future value which are known or susceptible of proof as of date of

merger and not product of speculation may be consideredo Cede & Co. v. Technicolor, Inc (Del, 1996)

Two-step merger and dissenters of T want plans of new majority owners re target to be taken into account for the minority shares to be cashed out w second step

Chancery Court Plans of buyer (before or after first step) are NOT part of fair value - value of new

management after merger is in connection w the accomplishment/expectation of merger

Supreme Court Value added during interregnum is an element of fair value of dissenter’s shares –

value added to going concern by majority acquirer during transient period of two-step merger accrues to benefit of ALL shareholders and must be included in appraisal process

Impact There was a business that got over-diversified and a purchaser sees this and plans

to buy bad corp, sell of bad assets, and retain value of core business – taking considerable risks w funding to do this

Dissenters are getting normal takeover premium AND value from purchasers future plans

If preexisting shareholders of bad biz get to share these profits, purchasers will be less likely to do these deal at the margins

Now costs will be higher and bad behavior is encourages (hide plans until after second step to avoid dissenters sharing the profits from the expected plans)

Alternatives

22

Could do triangular merger – but slower than two-step and invited rival bids Could contract around – specific value for preferred shares in event of appraisal

has been enforced - Ford Holdings Preferred Stock (Del, 1997)o Wouldn’t work for common bc they get all upside – could use floating

cap, though, like 120% of purchase price History of Appraisal Statute

o Version 1 (1899) – value set by panel of three appraisers (1 from diss, 1 from dir, 1 joint) Valuation is dispositive

o Version 2 (1943) – value set by one appraiser (court appoints) Valuation not dispositive, but accorded weight

o Version 3 (1976) – court shall appraise shares Two-step procedure of past is waste

E. Securities law issues – Williams Act Williams Act Impetus

o Congress and SEC originally took hand’s off approach - Rule 133: stock-for-stock merger did not involve offer and sale of securities subject to registration

Rule 145: REVERSED 133 – most business combos that result in T shareholders owning securities in surviving corp are offer and sale subject to registration

o Hostile takeovers virtually unregulated – these were rare until 1960s when tech decreased cost of buying on open market – bidders owed NO common law duties of disclosure to T shareholders and were NOT company insiders so had no duties of disclosure period – bidders could get substantial positions quickly

1968 Williams Act: raiders seen as looters and wanted to protect good old companies from looting – NOW, investors need disclosures to make decisions

Elementso §13(d) – Early Warning System

Requires disclosure whenever anyone acquires more than 5% of stock – investor must file within 10 days after acquiring

Partial exemptions for Institutional Investors and passive investors Each group member deemed to beneficially own each member’s stock – group is anyone

acting together to buy, vote, or sell stocko §14(d)(1) – General Disclosure

Requires tender offeror to disclose identity and future plans, including subsequent going-private transactions (if investors getting cash, why do they care?)

Tender offer must be made to all holders (purchases must all be made at best price) – no sweetheart deals

If bid oversubscribes, shares take up pro rata – end rush to tender – can’t leave any holders out

Holders who tender can withdraw while offer open – buyer’s remorseo §14(e) – Anti-fraud provision

23

Prohibits any fraudulent, deceptive, or manipulative practices in connection w a tender offer

Tender offer must be open for 20 biz days to give time for deliberation – bidder cannot buy outside tender offer

o §14(d)(4-7) – Terms of the Offer Governs the substantive terms of the tender offer (duration, equal treatment, etc) Exception to general rule that securities law are about disclosure

Special issueso All Holders Rule

Can golden parachutes violate the rule – best price rule…o Definition of tender offer

Conventional - Rule 14d-2(a) When published in newspaper and distributed to shareholders (formal)

Unconventional – flexible factors test Active and widespread solicitation of public holders Substantial percentage of stock Bought at premium On non-negotiable terms With floor and ceiling Offer open for limited time Putting pressure on offerrees to sell Using public announcements

Policy debateo Goals

T holders more educated, less pressured Equal treatment

o Critics No just disclosure, but substance – contrary to philosophy of securities law Messy and leads to lots of litigation – doesn’t even define tender offer Increases price, reduces number of bids – better decision making or just more costs? Disclosure rewards free riders, second bidders

If bidder prospects bad, T holders will take cash up front If bidder’s prospects good, free riders can defeat bid

Time delay enables T manager’s defenses Reduces tender offer power as check on poor management

III. Successorship

A. Transfers of assets Successorship questions

o Statutory merger - automatic for assets and liabilities (exception for patent licenses)

24

o Stock sales – not a transfer of title or assignment or delegation of any K rightso Assets sales – case by case question – contract interpretation on each particular asset

Case lawo PPG Industries, Inc. v. Guardian Industries Corp (6th Cir, 1979)

General rule w respect to assets and liabilities of T in statutory merger – pass to surviving corp as matter of law

Court rejects this for transfers of patent licenses in mergers Patent license that is silent on assignability is non-assignable and does NOT transfer in

merger – but real estate license that is expressly non-assignable DOES transfer in merger Patents are personal bc payments based on royalties – shared by competitors –

want incentives for invention, new ideas, keeping info in public domain, etc. Contractual solution to this type of problem

Control change clauses Competition clauses – right to approve or terminate Scope restrictions – limit to specific business units or products Fees and royalties – adjustments based on volume Geographic exclusivity – market carve outs

o Branmar Theatre Co v. Branmar, Inc. (Del, 1970) D says that transfer of stock not assignment, but performance was personal like patent

licenses, so ordinary rule shouldn’t apply A stock acquisition without a control change clause is NOT a transfer of title or

assignment or delegation of any contract rights With whom negotiations were conducted is irrelevant Personal nature relevant Restraints on alienation disfavored for real estate

o Sharon Steel Corp v. Chase Manhattan Bank (2d Cir, 1982) Clause in K says UV could transfer bond obligations to successor who purchased all or

substantially all of its assets Court says this protects lenders and borrowers by assuring degree of continuity of assets

- other transactions protected by self-interested equity holders Sale of metals business (41% of assets) - >75% is substantially all; <25% is NOT

substantially all – lawyers give opinions authorizing sales up to 55% (also look to qualitative – whether trans leaves holders w economically different investment)

Court penalizes liquidations in favor of extraordinary dividends when liquidation is less likely to injure creditors

o Chemetall v. ZR Energy (7th Cir, 2003) C is owner of M’s assets and wants to enforce trade secret agreement bt M & F Court allows Q of intent to go to jury – other provisions in K show intent of secrecy

B. Successor liability Successor liability in asset acquisitions

o Facts EC makes tons of cash, but has lots of liabilities in the form of future tort claims

25

OC pays cash to EC for its assets and trade creditor liability EC keeps the tort liability – makes extraordinary dividend and survives as shell before

dissolving – sweetheart deal for insiders who walk away w huge severance packageo Issue

Can EC’s creditors follow the assets and sue OC?o Answer

Sometimes – depends on claim, jurisdiction, and details of acquisition

1. State law Black letter law

o Merger – successor firm automatically liable for debtso Stock sale – buyer not liable absent veil piercing or enterprise liability theoryo Asset sale – generally, liabilities stay w seller

Reasoning Cash available – if arm’s length, the indifferent Potential windfall – more security than bargained for Preference for going concern sales over liquidation

Exceptions Consent (express or implied) Intent to defraud Mere continuation of seller – catches asset sales to shell corps created for

transactions (new firms w same owners and managers) De facto merger – attempt to stop old liquidation game where seller retains debt,

dissolves, and passes sales proceeds back to selling firm’s holders, who consume or subdivide, flee, and make collection prohibitively expensive

o Continuity of selling firm (management, assets, location)o Continuity of stockholders

Cargo Partners v. Albatrans (2d Cir, 2003)o Issue is whether the buyer of all firm’s assets is liable for trade debts of selling firmo Court finds NO de facto merger – no continuity of ownership bc seller stockholder got cash and

went awayo Expanding successor liability to trade creditors would make it more difficult for insolvent

business to be sold as going concern (which would increase likelihood of piecemeal sales of assets at lower price, reducing the amour available to Cs)

o Result is to penalize stock-for-asset deals Ruiz v. Blentech Corp (7th Cir, 1996)

o Ray Insulation from its predecessor’s liabilities promotes availability & transferability of

capital - outweighed here by the considerations favoring protection for injured users of defective products

P would have no other remedy bc of liquidation New corp had knowledge to gauge risks of injury from old products If new corp enjoys old corp’s good will, needs to have liability for its defects too

26

CA rule: five exceptions Assume De facto merger Mere continuation Fraudulently escaping liability Products line – limited to tort claims where

o Purchaser lacks adequate remedy against seller/manufacturero Purchaser knows of risk of products line it continueso Seller transfer goodwill associated w products line

o Domine Similar deal but old corp still had money and was not insolvent and successor only

bought SOME of the assets, not everything – Court found successor NOT liable Ray NOT in conformity w strict liability in IL – will not impose strict liability on D who

is outside the original purchasing and marketing chain (corp successor to manufacturer of allegedly defective product who takes after product left manufacturer control is NOT liable)

Corp successor can’t exert pressure to make product better, did not market product, did not get most of the profits, etc.

IL rule: four exceptions Assume De facto merger Mere continuation Fraudulently escaping liability

o Court decides to apply CA law to corp issue (bc based in CA) but IL law to tort issue (bc accident happened in IL) – issue is now whether products line exception sounds in corp or tort law

Tort issue, so IL law – Ruiz loses bc no exception for products line in IL

2. Federal law Golden State Bottling Corp v. NLRB (US, 1973)

o New test in private claims labor cases – notice test – buyer knew of unfair labor practice – want to protect employees from the following

Employees may perceive successor’s failure to remedy the predecessor’s unfair practices Successor could benefit from unfair practices of predecessor if collective action not taken Board may fire employees w high union activity

o Policy objective can be achieved at minimal cost to successor Generally in best position to remedy Also benefits from the unfair practices Paid less bc of practices or got indemnity clause

Fall River Dyeing & Finishing Corp v. NLRB (US, 1987)o FR had duty to bargain w union that represented employees at predecessor company bc

Continuity of business - substantial continuity Same factories,

27

Same jobs/supervisors Same products and customers (mostly)

Continuity of employeeso Dissent says no continuity of business

Completely separate entities – no shell game Bought assets only on open market – no product name or goodwill Business w old customers won competitively (no transfer of lists) Arbitrary date for determine employee count – doubled employees 3 mos after

Duty to bargain v. duty to arbitrateo Successor must bargain (statutory) if meets Fall River Dyeing test

Continuity of business Continuity of employees (successor can’t avoid by discriminating in hiring) Notice

o Duty to bargain very important bc Without, union must organize With duty, mandatory bargaining and possibly of strike With duty, disclosure requirements and bargain to impase needed before some changes

can be madeo Successor bound by arbitration clause (contractual) under certain ccs

John Wiley & Sons v. Livingston (US, 1964) Successor required to arbitrate w union under CBA where

o Biz entity sameo Wholesale transfer of merged employer’s employees to corp employer’s

plant, ando Union had made its position known well before merger and never departed

from it NLRB v. Burns Intern Sec Serv Inc (US, 1972)

No assumption of K bc o Not merger case, ando Not case about compelling arbitration

o Seems court has backed off transferring duty to arbitrate to purchaser and concentrated on less onerous duty to bargain

Few courts force CBAs on unwilling purchaser (w out mere continuation) Makes no sense to apply duty to arbitrate and not carry over substantial terms of CBA

NY v. NSI (2d Cir, 2003)o District court

Substantial continuity test NSI operations were substantial continuation

o Purchased all customer contracts, customer lists, service inventory, accounts receivable, trucks, insulated jackets bearing same name

o Employed drivers and used name on letter head, and used same phone number

28

NSI subject to successor liability for environmental infractionso Court of appeals

Mere continuation/identity test Requires existence of single corp after transfer of assets w identity of stock,

holders, directors bt the predecessor and successor corps Different from “substantial continuation (Golden State)

This test held that successor maintains same biz, with same employees, doing same jobs, under same supervisors, conditions, etc. while producing same products for same customers

o Concurrence Eliminates substantial continuity test for fear it will be adopted by others - offers

alternative of manipulation requirement Substantial continuity may unfairly penalize bona fide purchaser - may do all

research, etc. and then learn of hidden liability after purchase Harmful to society – leads to more liquidations and lowers asset values

Law and economicso Want corp to internalize cost of cleanup w price (either consumers pay price and corp can

cleanup or they don’t and then have to run cleaner cheaper biz) and want seller of firm to internalize cost by (discounting price of cleanup to buying firm)

Strategies to minimize exposureo Due diligenceo Warranty and indemnification clauses in acquisition agmto Triangular asset acquisition structure o No continuity of businesso Choice of law clause – do NOT elect Cal, Mich, NJ

C. Liability avoidance strategies Three scams (for managers/shareholders to steal from creditors)

o Liquidate and dissolve seller, distributing sale proceeds to shareholderso Extraordinary dividend or stock repurchase o Sweetheart deals w shareholders/milk assets

Excessive salary payments Sales of assets for less than fair market value Loans to shareholders at less than market interest rates Guarantees of shareholder debt on which shareholder defaults

Many ways for law to protect creditors

1. Dissolution provisions of state corporate codes In re RegO Company (Del, 1992)

o Issue is whether Claimants Trust provides security that will be sufficient for claims of present claims and will likely be sufficient for future claims based on knowledge of corp

o Appointed guardian ad litem pursuant to §280 to rep interests of future claimants

29

Fact that claims exceed assets does NOT prohibit RegO from dissolution under statute Trust is NOT sufficient under statute – declines to approve discrimination among

claimants of same class based on relatives time at which any claims mature or are reduced to judgment

o Appointed special master to help evaluate parties’ claims Permitted ongoing suit alleging extraordinary dividend was fraudulent conveyance Said nothing in order intended to alter existing equitable rights of legit claimants to

pursue relief Del law

o §275 – dissolution Requires approval of majority of outstanding shares

o §278 – continuation Body corporation continues 3 yrs (or longer if court approves) for defending suits –

continues indefinitely to cover these suits filed w in 3 yearso §279 – trustee/receiver

Can be appointed by court upon showing of good cause by holder, creditors, or director – may be continued in discretion of court

o §282 – liability of stockholders Liability shall not exceed amount distributed to such stockholder in dissolution

Delaware’s two formso §280 – notice wind-up (judicial)

Publish notice in paper for 2 weeks and send notice to each known claimant Claims barred if given actual notice and do not present claim Corp or successor may reject claim w in 90 days Claimant may revive if commence action w in120 days of rejection; otherwise, barred Must provide security sufficient to provide compensation if claim matures Petition court to determine security necessary for pending or unknown but likely claims

o §281 0 private wind-up (extrajudicial) If firm doesn’t do above, must adopt plan to make reasonable provison to pay all claims Reasonably likely to be sufficient to provide compensation for claims that have not been

made known to corp but are likely w in 10 years after dissolution based on facts corp does know

Directors not personally liable if comply Del v. MBCA

o Del – escrow approach Reasonable plan of distribution for all claims in 5-10 yrs – shareholders may be liable

under claim (limited to pro rata share of payments) – directors liable if plan not reasonable

Safe harbor – petition court of chancery (no shareholder liability after 3 years; no director liability)

o MBCA – different rules for dissolution 1979 – authorizes suit against firm for 2 yrs after dissolution 1984 – extends life of body corporate for suits to 5 yrs, defines as SOL

30

1999 – reduces term to 3 yrs

2. Legal capital statutes Legal capital/insolvency statutes

o Limits on corp distributions to shareholders Dividends Redemptions

o Modern – insolvency triggers Balance sheet test – net liabilities exceed net assets Equity test – not able to pay debts as they become due

State bulk transfer statuteso New Bulk Sales Act – waiver and indemnity; escrow

Largely unnecessary and avoidable

3. Fraudulent conveyance law Fraudulent conveyance statutes

o Voids transfers that injure creditors Dividends, redemptions, sweetheart deals, liquidation payments

o Actual fraud – actual intento Constructive fraud – constructive intent

No reasonably equivalent value in exchange and remaining assets unreasonably small, seller knew firm could not pay debts, or firm was insolvent or became insolvent

LBOso Process

Step 1 – fund creates acquisition shell corp T borrows cash from institutional investors

Step 2 – shell purchases controlling block of stock of T Step 3 – Shell merges into T

A’s holders receive all outstanding common stock in T T’s minority holders exchange voting stock for debt securities in T A’s massive debts attach by operation of law to T

Step 4 – T manipulates its assets and capital structure to generate cash to pay off acquisition financing

o Fraudulent conveyance? Basic fraudulent conveyance is intentional fraud or badges of fraud – LBOs are not trying

to create a bankrupt firm – not trying to loot Only 9th Cir seems to think that fraudulent transfer law should NOT apply to LBOs

In re PNP Holdings (9th Cir, 1998)o Issue is whether PNP rec’d something of fairly equivalent value for the transfer – jury found that

non-monetary benefits were there and thought there was equivalent value – appealing, saying that should have been decided not value as matter of law

o Court agrees w jury that yes value – trade Cs were paid for three years and would have been great deal if not for crazy competition and sudden bad market

31

o Most cases turn on solvency – and are found for defense per solvency letters, etc. Subsidiaries

o Problem Corp in bankruptcy sells a sub and wants that sale to be free and clear of 3rd party claims But sub is not in bankruptcy, so sale is not protected by §363 of B Code So sub is not immunized from 3rd party claims and Buyer can be sued

o Solution Insist that sub become party to asset purchase agmt as “seller” and also become a

“debtor” (asset sale, not stock sale) If sub can’t or shouldn’t go bankrupt, buyer should do more due diligence – adjust price

based on claims and/or negotiate holdbacks or indemnification Could also get “channeling injunction” requiring that claims against sub instead by

brought solely against proceeds of the sale Environmental exceptions

o Successor liability for CERCLA claims Owner of land liable for CERCLA clean up costs regardless of whether bought after

bankruptcy cleansing Fact that asset sale in this case took place in context of B is NOT determinative of

liabilityo Ninth Avenue Remedial Group v. Allis-Chalmers Corp. (Ind, 1996)

DC B court approves sale free and clear or all liens, claims, taxes, etc. per §363(f) Court chooses substantial continuity (Golden State) test for successor liability

where one corp has to remain w same owners and dirs – does not use mere continuity (one corp, same owners and dirs) – bc environmental requires broadened successor liability

o Retention of same employeeso Retention of same supervisorso Retention of same production facilities at same locationo Production of same producto Retention of same nameo Continuity of assetso Continuity of general business operationso Whether successor holds itself out as continuation of previous enterpriseo Whether transfer is a scam to avoid liability

Timing of claim – sale free and clear does not include future claims that did not arise until after B proceedings ended

o Discharge if claimants had actual or constructive knowledge that release happened and could tie the D to the release prior to the B reorg

o Claim exists not when it is brought, but when potential claimant knew or should have known that claim existed – if claimant could not have presented claim in B proceeding, it is NOT barred

32

Court refuses to respect K provision that covers future claims to override CERCLA

o Other rule would encourage piecemeal liquidations instead of going concern sales

o Would allow some USCs to line jump in violation of absolute priority rule 7th Cir

Don’t want to encourage filing B by treating bankrupt sellers different than otherso Purchasers can demand lower price to account for pending liabilitieso Purchasers not held liable if they had no noticeo BUT, it’s very hard to price these liabilities

Creditor can get second chance w successor liabilityo Priority rules are irrelevant after a B proceeding is over

If predecessor viable, then no reason to hold successor liableo CERCLA v. Bankruptcy

CERCLA – facilitate cleanup of environmental contamination by distributing cost among broad category of parties directly and indirectly responsible

B Code – maximize payments to Cs while giving fresh start to Ds and preserving valuable going concerns - court has power to preclude claims not filed during B proceeding

Can reduce risks of successor liability by Giving adequate notice to potential claimants of hearing where court will be asked

to approve sale free & clear Getting specific finding by B court that sale is free and clear of claims Getting a decree in the order approving the sale enjoining claimants from

pursuing the buyer of purchased assets Shut down debtor for period of time

o Schmoll v. AC&S, Inc (Ore, 1988( Seven-step trans to separate asbestos liability from biz originally held as division that was

unrelated to asbestos and a viable asset – asset sale of asbestos divisions to litigation group for unsecured note

DC judge says knows what they are up to and won’t let them do it – this is affirmed by 9th

Cir w one sentence – court does not want to allow form over substance – can’t design transaction to escape asbestos liabilities

Court hated how selling firm was left insolvent by selling its profitable divisions – court says they should have filed for B instead bc they are trying a B-like reorg w out protection for creditors

o US v. Bestfoods (US, 1998) Dumping law – any person who at time of disposal owned or operated facility where

dumping occurred Court says standard is NOT whether the parent operates the sub, but whether parent

operates the FACILITY as evidenced by participation in activities of facility rather than the sub

33

Operation must manage, direct, or conduct operations specifically related to pollution

More than mechanical activation of pumps and valves – must be direction over facility’s activities

Activities consistent w parent’s investor status – monitoring sub performance, supervision or capital and budgetary decisions, and articulation of policies and procedures – do NOT give rise to direct liability

Notice that triangular structure will not always insulate the buyer from the liabilities of the selling firm as wholly-owned sub

Parent must nor direct of manage the environmental practices of the sub

4. Breach of fiduciary duties Creditors can show that board can breached its fiduciary duties

o Can then create successor liability

IV. Deal Issues

A. Documents

1. Preliminary documents Confidentiality agmts – not much litigation

o Breaches hard to establisho Damages from breaches hard to prove

Letters of intento Legal status – can be binding (w essential terms supplemented by open-ended terms), binding

agmt to bargain, or non-bindingo Clients want them and lawyers do NOT – sellers want them more than buyerso Pros

Preliminary (moral) commitment before spending lots on drafting final deal Laying out deal terms reduces uncertainty and potential for surprise/mistake Helps acquirer line up financing

o Cons Courts may use letter to give disgruntled party relief Impacts bargaining leverage before information asymmetries are reduced

2. Acquisition agreement This is the binding doc

3. Supplemental documents Disclosure letter (Schedules or Exhibits) Employment or non-competition agmt Due diligence checklists

34

Earnouts

4. Closing documents Supplement to Disclosure letter Counsel opinions Comfort letters & fairness opinions Release Non-negotiable promissory note Escrow Agmts Bill or Sale and Assumption Agreements

B. Litigation IG Acquisition Corp v. Alaska Indus Hardware, Inc (NY, 2994)

o Letter of intent had “best efforts” clause, but was NOT binding bc it references stock purchase agmt that must be signed

o Court finds evidence for specific performance anyway even though SPA not signed Lawyer told other sign that they had reached final agmt Lawyers said changes fine and agmt looks final to us Shook hands in person, said deal was done, and would sign SPA later that night

o Uses agency theory (D told agents he had a deal who made representation to P to this effect) & promissory estoppel (clear promise to sign, reasonable reliance on promise, injury sustained by reliance)

Texaco, Inc v. Pennzoil Co (Tex, 1987)o NY standard is intent, not form – if parties intend to be bound only when they sign a formal agmt

later, then initial agmt NOT binding – if not, and if all substantial terms are agreed to, then bound by initial agmt – look to factors

(1) whether party expressly reserved right to be bound only when written agmt signed; Court says conditions subsequent, not precedent here

(2) whether any partial performance by one party that party disclaiming K accept; Court says issue of press release was slight partial performance

(3) whether all essential terms had been agreed on; and Court says press release had lots of same terms as unsigned MOA

(4) whether the complexity and magnitude of trans was such that formal, executed writing would normally be expected

Court says yes, huge scope here, but could be that approved and just waitingo Court looked to previous draft, and custom/practice to fill in missing deal terms – result is largest

jury verdict in history of the world (at the time) Jury believed that a handshake was a deal

ConAGRA, Inc v. Cargill, Inc (Neb, 1986)o Merger agmt bt A and T and then someone else jumps in and does cash-out mergero Court says “best efforts” clause is unenforceable despite including fiduciary out – does NOT

relieve the board of their duties to shareholders Per §251(b) – Dirs have to determine that combo is in best interests of holders

35

Del reaches same result in Omnicare Jewel Cos Inc v. Pay less Drug Stores Northwest, Inc (9th Cir, 1984)

o Tender offer for PayLess after they have stock merger agmt w best efforts clause w Jewelo Best efforts clause stopped negotiation w other bidders but did not decide whether board, having

rec’d higher bid, could bind itself to recommend initial lower proposal O’Tool v. Genmar Holdings, Inc (10th Cir, 2004)

o Purchase for $2.3M cash w earnout consideration (joint bargaining gains when seller believes higher future value than buyer) – jury gave award for breach when didn’t go through w it

o Court implied covenant of good faith and fair dealing – to interpret and to act reasonably – can’t use oppressive techniques to deny other side even when you don’t expressly violate the terms

o Ds have burden of proof – what isn’t expressly in agmt seen in P’s favoro Earnout lessons

W out specific drafting, assets purchased under earnout provision must be segmented until earnout expires

Makes things even more detailed now in intent in attempt to recapture predictive function of K – makes things too complicated and literal words can be ignored

AES Corp v. Dow Chemical Co (3d Cir, 2003)o No-reliance clause limits ability to recover under the Act, so it is VOID – reliance factors are

(1) whether fid relationship existed bt parties (2) whether P had opportunity to detect fraud (3) the sophistication of the P (4) existence of long standing relationships; and (5) P’s access to relevant information

o 2d Cir goes other way – respects contractual limits of sophisticated parties IBP v. Tyson Foods (Del, 2001)

o MAC is a backstop protecting acquirer from occurrence of UNKNOWN events that substantially threaten overall earnings potential of target in durationally-significant manner

Undisclosed problem – yes MAC Unknown consequences of disclosed problem – prob NOT MAC

o Most important thing is whether company has suffered MAC that is consequential to corp’s earning power over years rather than mos

Strategic investors do not view over short-term! MAC factors = Size, duration, expectedness, buyer-specific

V. Legal Duties of Owners & Managers

A. Board’s duties in negotiated deals Typical timeline

o Management negotiationo Board approval (sig on merger agmt)o Board recommendation to holders – vote yes

36

o Shareholder voteo Closing

Board power to say no or change terms of agmto Can reject management proposal

Can accept alternative overture Deal can be presented to holders anyway – tender offer, proxy fight

o Has power to abandon after holders vote Subject to contractual rights of other party Allowed by DGCL, so most contracts include it

o Can amend after shareholder vote only in limited ccs – no amendments for Changing consideration paid Changing articles of incorporation Materially changing the terms and conditions of plan to adversely affect a ratifying group

of shareholderso Can agree to terms that vary w future events

Doesn’t run afoul of “illusory promises” doctrine Deal protection covenants

o Types Performance promises

Typeso Best effortso No-shop clauseso No-merger clauses (can negotiate but can’t recommend until vote on 1st)o No talk/no negotiation clauseso Go shop clauses

Levelso Strict – board must recommend deal to holders even if higher offer has

been made – may not negotiate at all w other bidders 9th Cir enforces these Del does not enforce if violates board’s fid duties

o Leeway – board must recommend deal if no higher offers – board can’t solicit other offer nor can it give confidential info to other buyers (“no-shop/no-talk” clauses)

Cancellation payments Lock-ups

o Asset – if we walk away, you get to buy X asset for Y price (cheap)o Stock – if we walk away, you get to buy X number of shares at Y price

(cheap) Termination/topping fees - if we walk away, we you $X (typically 1-5%)

Others Voting agmt Golden and tin parachutes

37

o Arguments Pro

Max flexibility to boards Boards encourage reluctant first bidders

o Encourages money spent on due diligence, prof serviceso Provide economic compensation for jilted purchaser n event that target

chooses not to closeo Obstruct disruption of deal by another purchaser – no “stalking horse” –

initial bidder proves floor for negotiations and proof of firm’s extrinsic value

Does not stop all other bids Courts can stop abuses

Con Boards abuse this power to favor bidders offering personal advantages Well-intentioned boards will make mistakes – buyers are repeat and smart, while

one-time seller CEOs may be overconfident and ignorant Risk of locking in low price

Standards of review for board actionso Deferential

Business judgment rule Gross negligence

Duty of care – duty to be informed; may rely on experts Duty of loyalty – entire fairness analysis; not all conflicts, but only where interested dir

controls board or where fails to disclose conflict to other dirso Enhanced scrutiny

Unocal test – when board adopts defensive mechanisms in response to threat to corp control or policy, burden on board to meet enhanced test by showing following (if shown, BJR applies)

Reasonable grounds for believing that danger to corp policy and effectiveness existed (show by board’s good faith and reasonable investigation)

Defensive measure were reasonable in relation to threat posed (shown by objective reasonableness)

Revlon duties – transactions involving sale of control – board’s legally mandated goal is to achieve highest value for holders

Once board sells control, dirs role changes from defenders of corp to auctioneers charged w getting best price for holders at sale

Sale of control - cases turn on whether the trans involves a sale of controlo Cash deal – YES enhanced duties likely applyo Stock-for-stock deals

Most deals NOT a sale of control – BJR applies – no control when remains in large fluid market

If sale of control, Revlon applies – if sale of majority stake with control over buyer

38

1. Duty of care Smith v. Van Gorkom (Del, 1985)

o Legal standard Breach of duty of care

BRJ does not apply – board NOT informed Reliance on experts – NOT reasonable Ratification by shareholders – NOT informed

Entire Fairness test – Burden of proof on boardo Decision to sell – what did the target board know?

Stock trading in $30-38 range Bid was for $55, a 50% premium Friendly Deal Premiums average 10-20% Rail car business was in decline A would not engage in auction – sell now or he’s gone

o Court was upset by Casual board posture No expert appraisal No formal market vetting Flippancy – happened at the Opera Priced from an LBO study

o Impact More formal board procedures – no quick decisions Fairness opinions Shop the firm?

Technicolor sagao Perelman offers $23/share for Technicolor, 100% premium – board approves w out getting

credible valuable and there is evidence of casual attitude and procedural irregularity – Cinerama votes NO and perfects appraisal rights – court says that T stock is worth $21.60/share – board didn’t: