39

IAB/PwC mobile ad spend study Guy Phillipson – CEO, IAB Jon Mew - head of mobile, IAB Eva Berg Winters - PwC

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | jana-bryant |

| View: | 26 times |

| Download: | 0 times |

IAB/PwC mobile ad spend studyGuy Phillipson – CEO, IAB

Jon Mew - head of mobile, IAB

Eva Berg Winters - PwC

In today’s presentation

1. Introduction

2. Methodology

3. Mobile in 2008

4. The figures

5. Outlook

1. Introduction

50% of the world’s population is on mobile

But how many in the UK are

actually using the mobile internet?

The UK economy is in reverse but

technology is in top gear

We call it a phone, but it does everything!

Marketers and media are obsessed!

IAB has successfully integrated mobile

Research

Workshops

PR + Comms Presentations

Guides

Events

Education

So how much is mobile advertising worth?

? ?

?

Now

we

know!

2. MethodologyEva Berg Winters - PwC

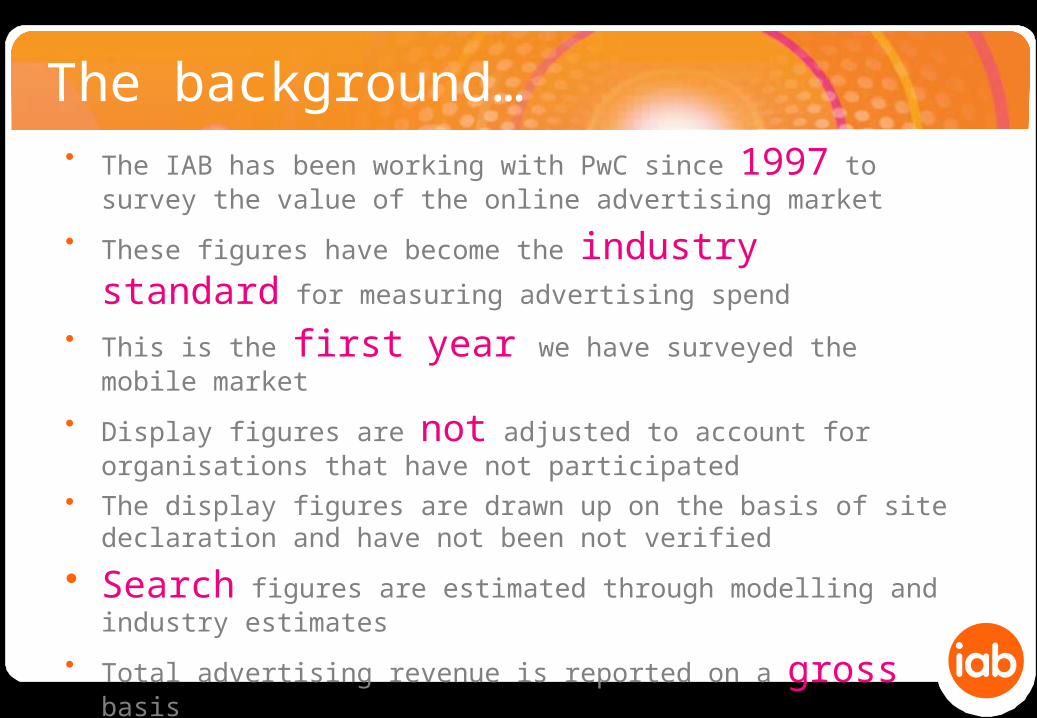

• The IAB has been working with PwC since 1997 to survey the value of the online advertising market

• These figures have become the industry standard for measuring advertising spend

• This is the first year we have surveyed the mobile market

• Display figures are not adjusted to account for organisations that have not participated

• The display figures are drawn up on the basis of site declaration and have not been not verified

• Search figures are estimated through modelling and industry estimates

• Total advertising revenue is reported on a gross basis

The background…

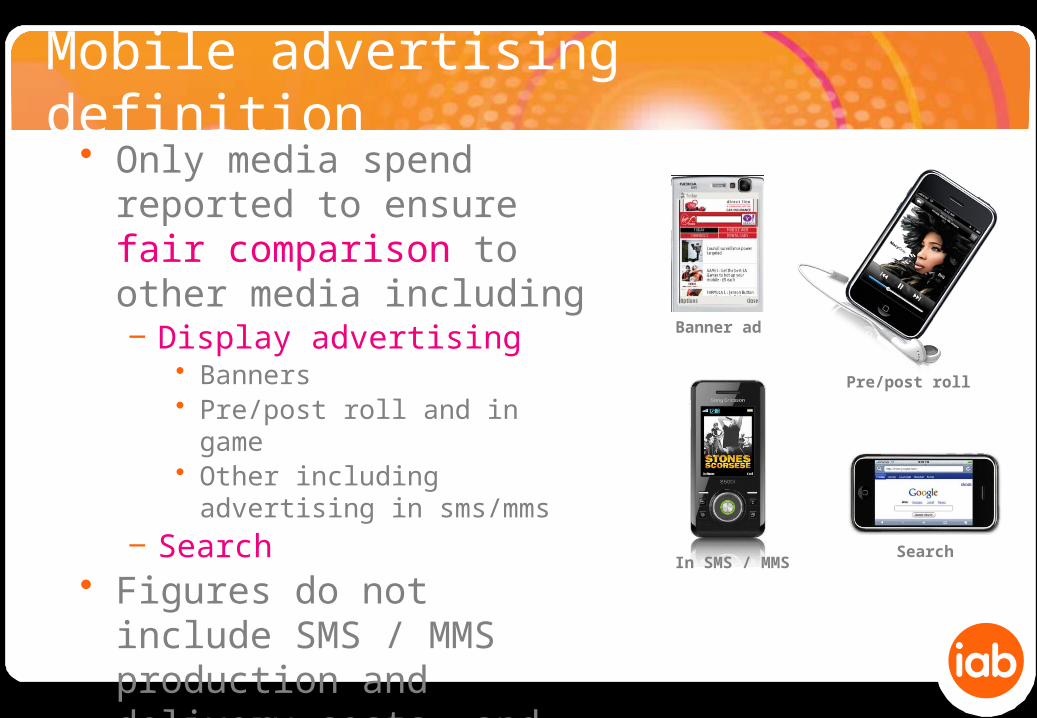

Mobile advertising definition• Only media spend reported

to ensure fair comparison to other media including‒ Display advertising

• Banners• Pre/post roll and in game• Other including advertising in

sms/mms

‒ Search• Figures do not include

SMS / MMS production and delivery costs, and other mobile marketing revenues

Banner ad

Pre/post roll

SearchIn SMS / MMS

Research participants

3. Mobile in 2008Jon Mew - head of mobile, IAB

Handsets

MobileContent

OperatorPricing

Measurement

Education

Proof

Big trends driving uptake

MobileAd

Uptake

Changing Consumer behaviour

Key trends – handsets improve

Source: Comscore 3 month average ending October 2008

Total 3G penetration

+36% yr on yr

Key trends - content

Source: Comscore 3 month average ending October 2008

total market unlimited data plan subscribers

4.6%

20.2%

% Accessing social networking sites daily

Key trends - pricing

Source: Comscore 3 month average Feb 2009

+ 109% growth in customers on

unlimited data plans in 2008

+ 340%

Mobile internet usage grows in 2008

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

12,000,000De

c-05

Jan-

06Fe

b-06

Mar

-06

Apr-

06M

ay-0

6Ju

n-06

Jul-0

6Au

g-06

Sep-

06O

ct-0

6N

ov-0

6De

c-06

Jan-

07Fe

b-07

Mar

-07

Apr-

07M

ay-0

7Ju

n-07

Jul-0

7Au

g-07

Sep-

07O

ct-0

7N

ov-0

7De

c-07

Jan-

08Fe

b-08

Mar

-08

Apr-

08M

ay-0

8Ju

n-08

Jul-0

8Au

g-08

Sep-

08O

ct-0

8N

ov-0

8De

c-08

Source: Comscore 3 month rolling average

+28% growth in 2008

4.The figures

Total mobile advertising revenue 2008

£28.6m

Source: IAB / PwC mobile display ad spend survey 2008; search spend figure derived from modelling and industry estimates

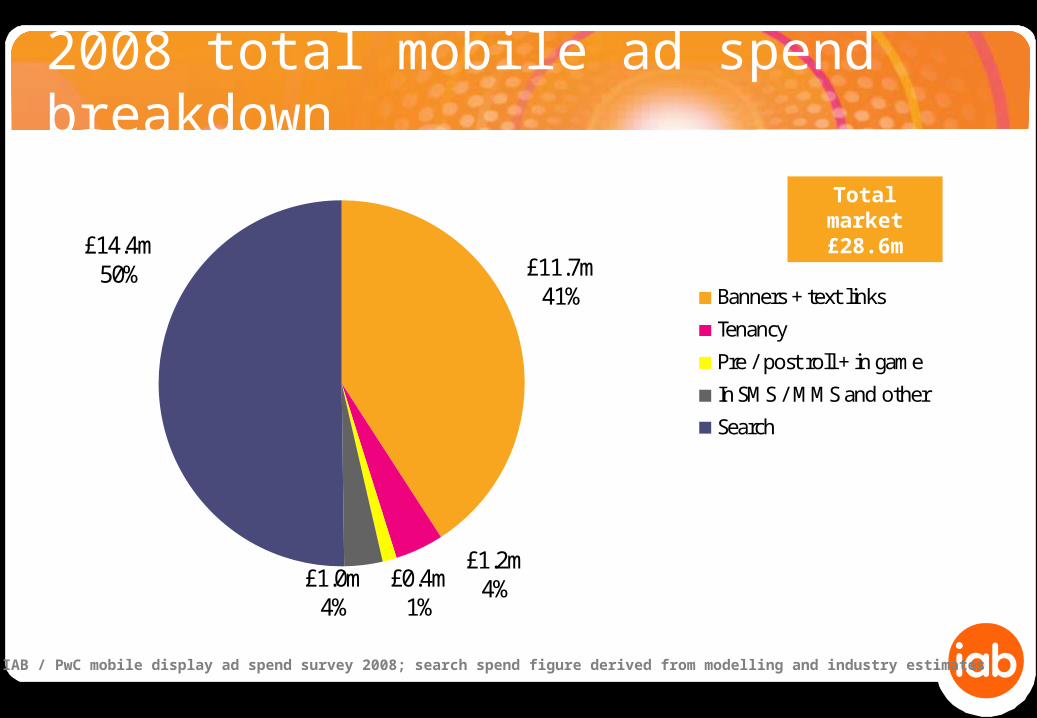

2008 total mobile ad spend breakdown

£11.7m41%

£1.2m4%£0.4m

1%£1.0m

4%

£14.4m50%

Banners + text links

Tenancy

Pre / post roll + in game

In SMS / MMS and other

Search

Total market £28.6m

Source: IAB / PwC mobile display ad spend survey 2008; search spend figure derived from modelling and industry estimates

2008 total display breakdown

£11.7m82%

£1.2m9%

£0.4m2%

£1.0m7%

Banners + text links

Tenancy

Pre / post roll + in game

In SMS / MMS, classified and other

Total market £14.2m

Source: IAB / PwC mobile display ad spend survey 2008; search spend figure derived from modelling and industry estimates

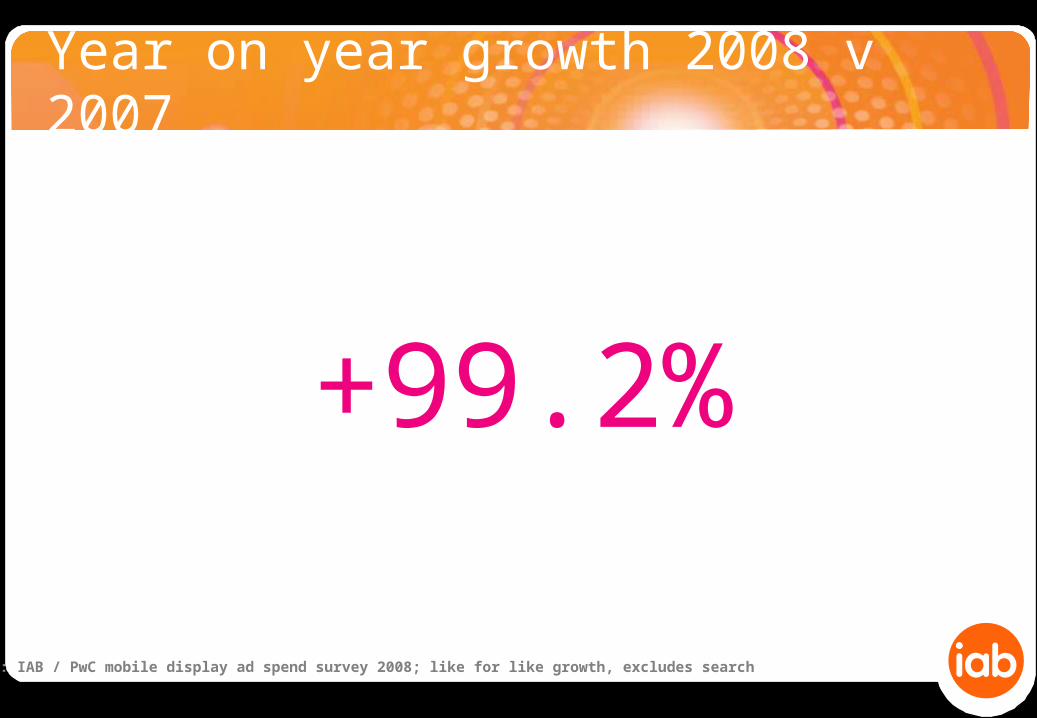

Year on year growth 2008 v 2007

+99.2%

Source: IAB / PwC mobile display ad spend survey 2008; like for like growth, excludes search

Consistent growth through 2008

+ 15.4%

+ 9.4%

+ 17.5%

Quarterly total display revenue 2008

Source: IAB / PwC mobile display ad spend survey 2008; search spend figure derived from modelling and industry estimates

H1 2008 v H2 2008

+27.4% growth from H1 to H2

Source: IAB / PwC mobile display ad spend 2008 – like for like growth, excludes search

Mobile shows similar trend to online

6.37.4 7.1

8.3

9.810.4 10.3

11.8

13.4

14.614

15.816.8

17.817.2

18.1

0

5

10

15

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q40

20

40

60

80

100

120

140

160

180

Onl

ine

ad s

pend

£ m

illio

ns

Source: PricewaterhouseCoopers / Internet Advertising Bureau / WARC

Onl

ine

audi

ence

(m

illio

ns)

£51m

£153.1m

£165.7m

1998 1999 2000 2001

9.4m* £28.6m

*Source: Comscore 12 month average 2008

£19.4m

Mobile audience

and spend 2008

5.Outlook

Carat/Aegis -7%

Group M -11%

Enders -13%

Average forecast -10%

Current forecasts for total 2009 advertising

In the toughest year for advertising,

mobile is forecast to grow

while traditional media declines

Outlook – continued growth expected

x

Initially we will run the study

annually and publish 2009 figures

in early 2010

Key headlines

• Total market beats expectations at £28.6m

• Impressive growth year on year at 99.2%

• Consistent growth throughout year despite market

conditions

• Close parallels to early online figures

• Hard to forecast accurately but we expect growth in

2009

New mobile initiatives from IAB

Mobile innovators award – 21st May

ThanksFor more information email [email protected]

Questions?

ThanksFor more information email [email protected]

Disclaimer

The IAB retained PricewaterhouseCoopers LLP (the UK firm) (‘PwC’) to compile the mobile adspend figures collected by the IAB from its members in January through April 2009 and to deliver to the IAB the topline figures collated from this review; PwC has not verified the information which it received from the IAB, and provides no opinion or other form of assurance with respect to such information.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, neither the Interactive Advertising Bureau UK (the ‘IAB’) nor any of the IAB’s

contributors/subcontractors accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information

contained in this publication or for any decision based on it.