IAS 39 Impairment principles applied in less-developed markets/economies: case of Macedonia Marija Efremova Advisor to the Governor for IFRS National Bank of the Republic of Macedonia Vienna, 6-7 September 2010

Transcript

IAS 39 Impairment principles applied in less-developed markets/economies:

case of Macedonia

Marija Efremova Advisor to the Governor for IFRS National Bank of the Republic of Macedonia

Vienna, 6-7 September 2010

Content: IAS 39 Impairment principles Regulation for credit risk management for banks

operating in R.Macedonia Case study – work on an example Discussion

This session will talk about impairment on: • loan receivables • individually significant items

IAS 39 Impairment principles

IAS 39 Impairment principles (1/4)

existence of objective evidence of impairment – impairment

triggering events

measure/assess the amount of impairment loss

recognise impairment loss in the books

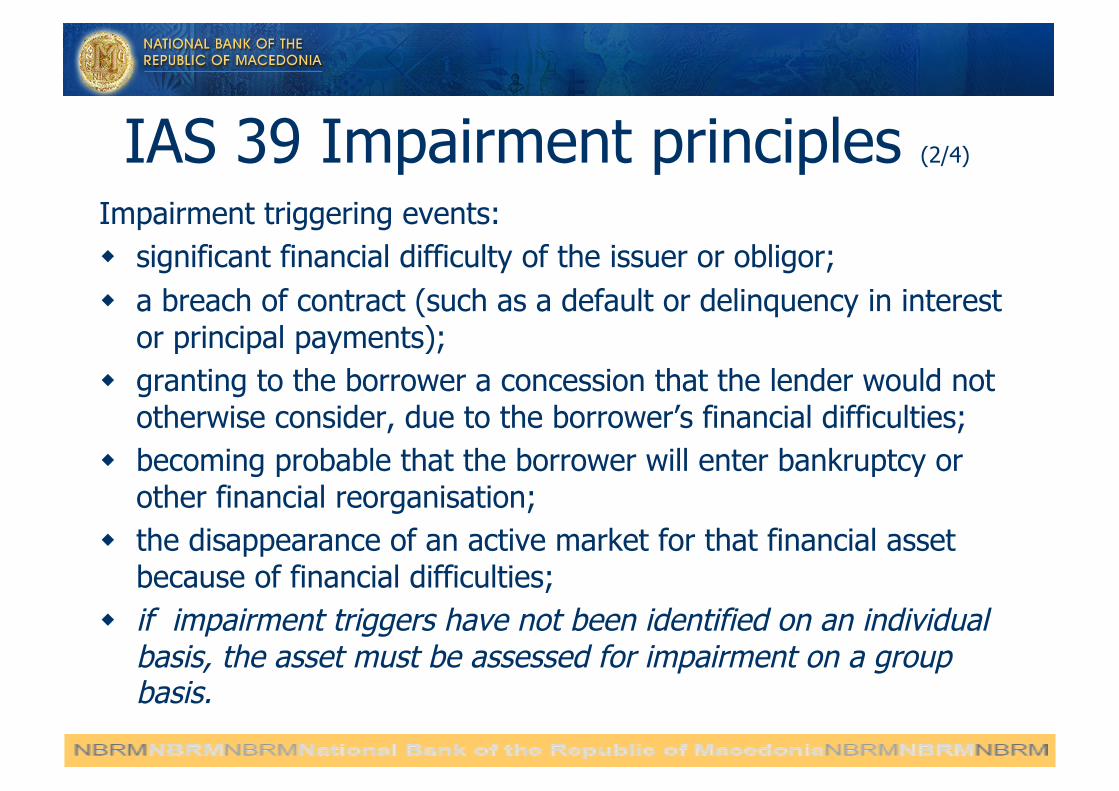

IAS 39 Impairment principles (2/4) Impairment triggering events: significant financial difficulty of the issuer or obligor; a breach of contract (such as a default or delinquency in interest

or principal payments); granting to the borrower a concession that the lender would not

otherwise consider, due to the borrower’s financial difficulties; becoming probable that the borrower will enter bankruptcy or

other financial reorganisation; the disappearance of an active market for that financial asset

because of financial difficulties; if impairment triggers have not been identified on an individual

basis, the asset must be assessed for impairment on a group basis.

IAS 39 Impairment principles (3/4) If, and only if, one or more impairment triggering events (“loss event”) has happened after the initial recognition of the asset and that loss event has impact on estimated future cash flows of the asset

Impairment incurred

Measure the amount of impairment loss

IAS 39 Impairment principles (4/4)

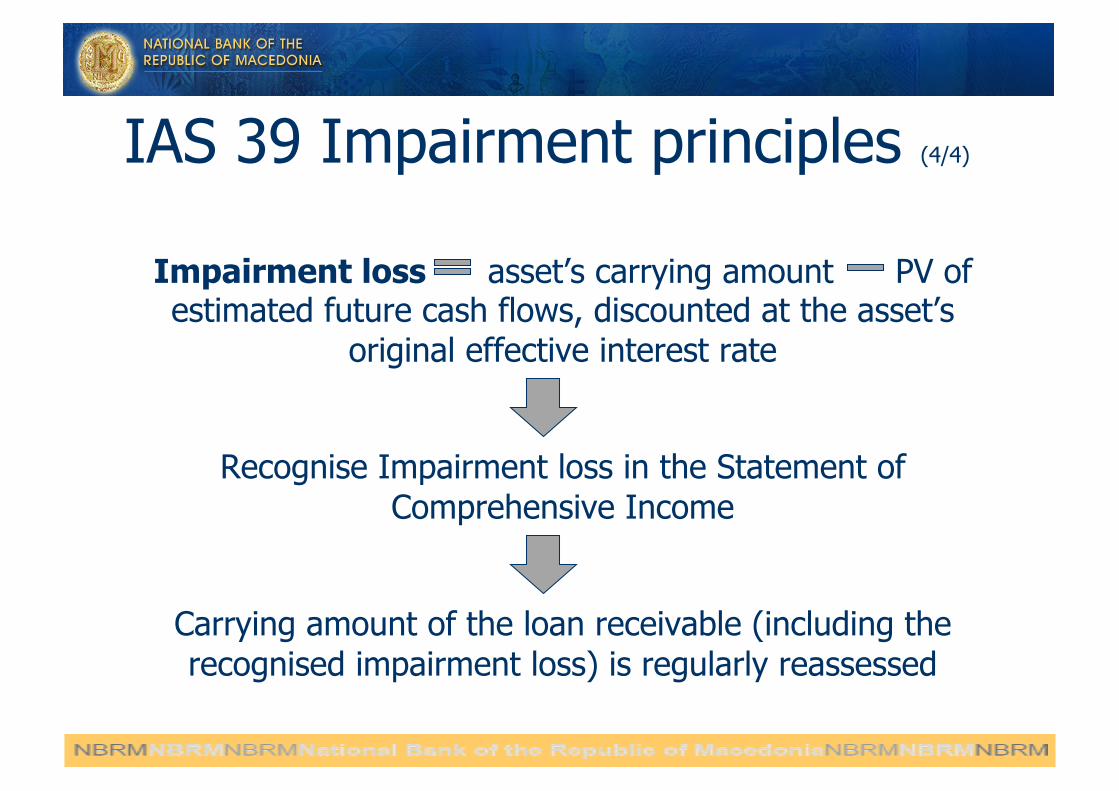

Impairment loss asset’s carrying amount PV of estimated future cash flows, discounted at the asset’s

original effective interest rate

Recognise Impairment loss in the Statement of Comprehensive Income

Carrying amount of the loan receivable (including the recognised impairment loss) is regularly reassessed

Content: IAS 39 Impairment principles Regulation for credit risk management for banks

operating in R.Macedonia Case study – work on an example Discussion

Regulation for credit risk management for banks operating in R.Macedonia

Regulation for credit risk management for banks operating in R.Macedonia (1/20)

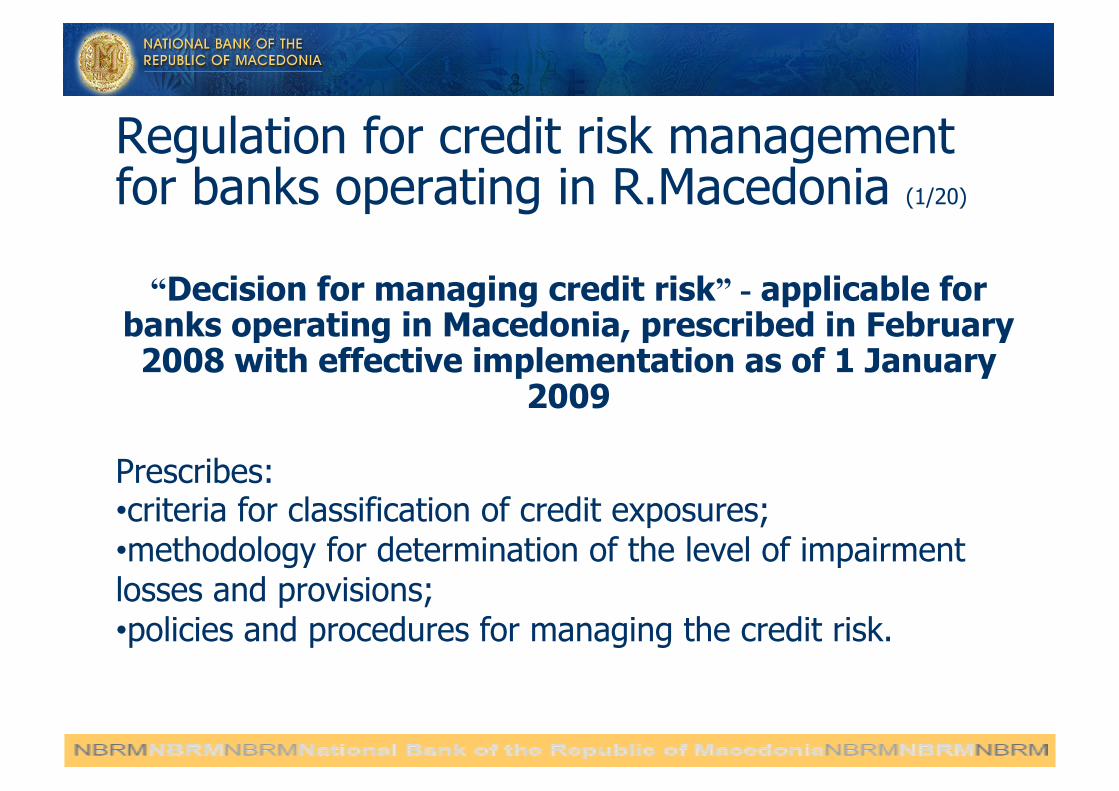

“Decision for managing credit risk” - applicable for banks operating in Macedonia, prescribed in February 2008 with effective implementation as of 1 January

2009

Prescribes: • criteria for classification of credit exposures; • methodology for determination of the level of impairment losses and provisions; • policies and procedures for managing the credit risk.

Regulation for credit risk management for banks operating in R.Macedonia (2/20)

step 1: classification of the loan receivable into the prescribed risk categories (A, B, C, D, E); step 2: determining the present value of the estimated future cash flows of the receivable; step 3: assessment of the amount of the impairment loss, as a difference between the carrying amount of the loan and the present value of the estimated future cash flows (as determined in step 2)

Regulation for credit risk management for banks operating in R.Macedonia (3/20) Alternative: If the bank does not determine the present value of the estimated future cash flows (step 2 is not applied)

step 3 (alternative): Impairment loss carrying amount of the receivable upper level of impairment loss of the risk category in which the receivable has been classified (A, B, C, D, E)

Regulation for credit risk management for banks operating in R.Macedonia (4/20) step 1: Classification of credit exposures

General principles for classification of credit exposures: • creditworthiness of the client; • servicing the liabilities to the bank; • quality of the collateral.

Impairment triggering events, as prescribed by IAS 39 (each developed per separate risk categories)

Regulation for credit risk management for banks operating in R.Macedonia (5/20) step 1: Classification of credit exposures

Risk category Days overdue

A up to 30 days

B 31 to 60 days (exceptionally 61 to 90)

C 61 to 120 days (exceptionally 121 to 180)

D 121 to 270 days (exceptionally over 270)

E over 270 days

trigger: “breach of contract”

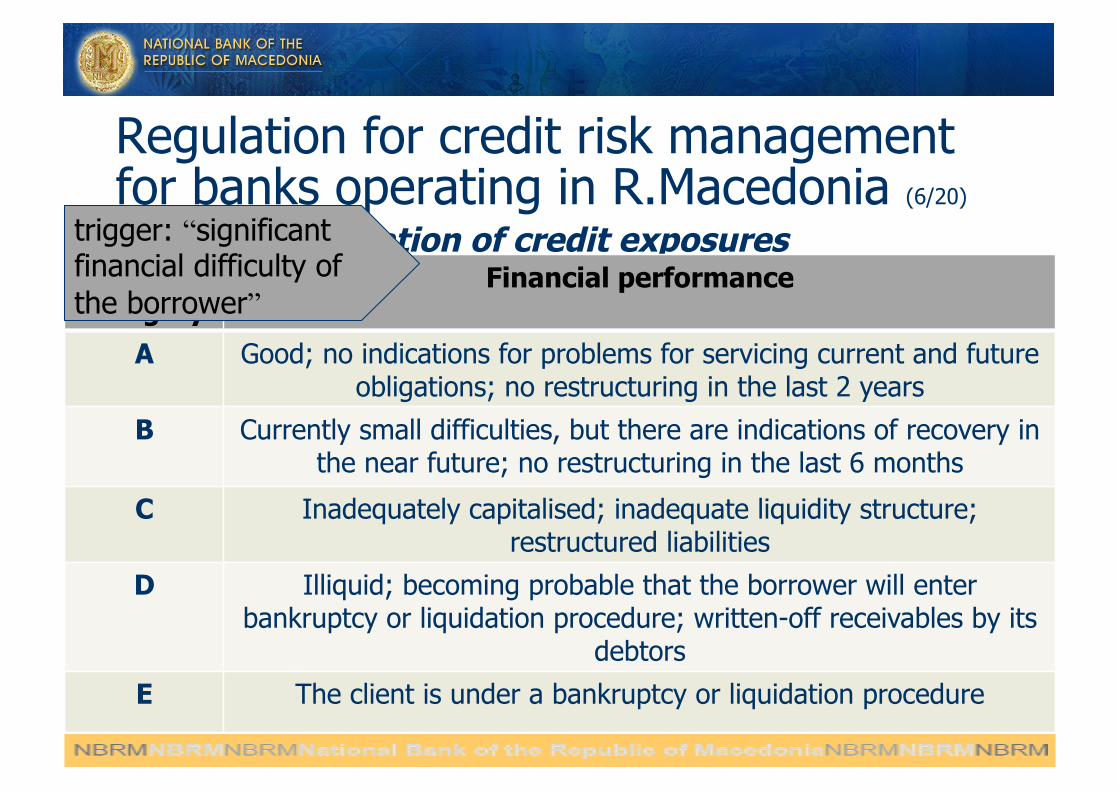

Regulation for credit risk management for banks operating in R.Macedonia (6/20) step 1: Classification of credit exposures Risk

category Financial performance

A Good; no indications for problems for servicing current and future obligations; no restructuring in the last 2 years

B Currently small difficulties, but there are indications of recovery in the near future; no restructuring in the last 6 months

C Inadequately capitalised; inadequate liquidity structure; restructured liabilities

D Illiquid; becoming probable that the borrower will enter bankruptcy or liquidation procedure; written-off receivables by its

debtors

E The client is under a bankruptcy or liquidation procedure

trigger: “significant financial difficulty of the borrower”

Regulation for credit risk management for banks operating in R.Macedonia (7/20) step 1: Classification of credit exposures

Risk category

Financial performance

A No restructuring in the last 2 years

B No restructuring in the last 6 months

C Restructured liabilities

D

E

trigger: “granting a concession, due to the borrower’s financial difficulties”

Regulation for credit risk management for banks operating in R.Macedonia (8/20) step 1: Classification of credit exposures

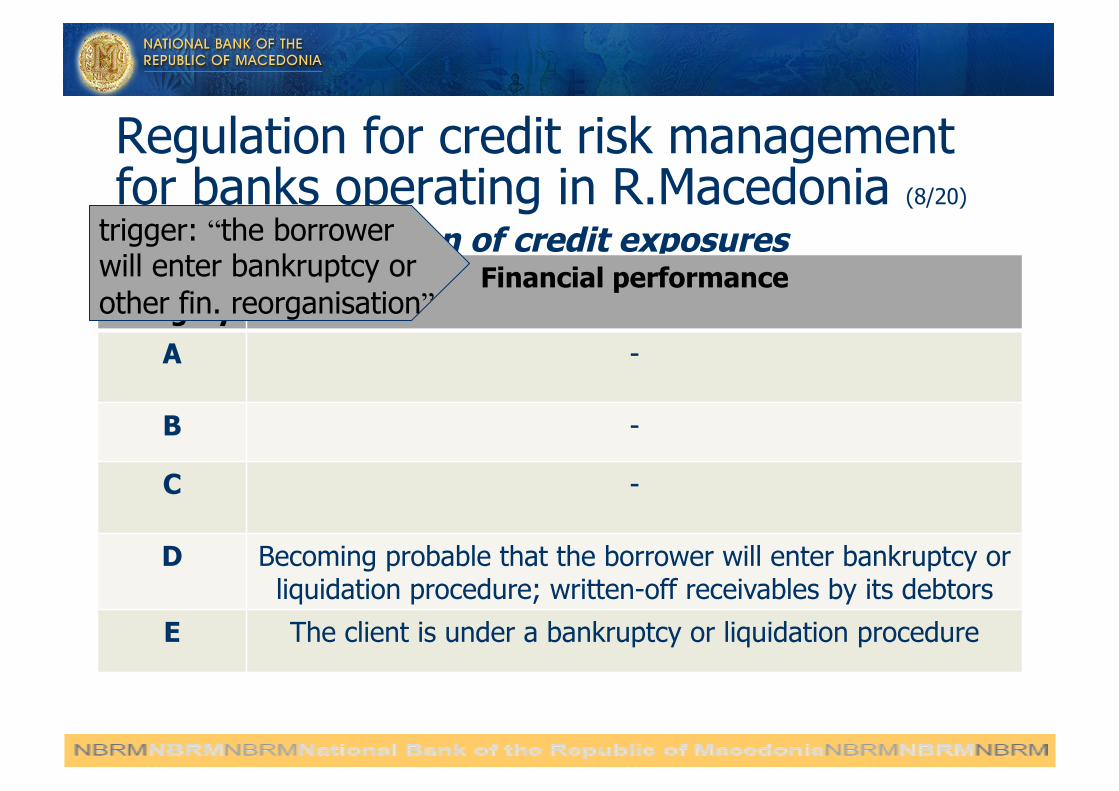

Risk category

Financial performance

A -

B -

C -

D Becoming probable that the borrower will enter bankruptcy or liquidation procedure; written-off receivables by its debtors

E The client is under a bankruptcy or liquidation procedure

trigger: “the borrower will enter bankruptcy or other fin. reorganisation”

Regulation for credit risk management for banks operating in R.Macedonia (9/20) step 2: Determining the present value of the estimated future cash flows of the receivable: Determine the recoverable amount of the receivable by calculating the present value of the estimated future cash flows of the receivable, discounted with the original effective interest rate.

Composition of the estimated future cash flows is a key determinant of the

amount of impairment losses.

Regulation for credit risk management for banks operating in R.Macedonia (10/20) step 2: Determining the present value of the estimated future cash flows of the receivable: Estimated future cash flows of the receivable can be comprised of: for regularly performing loans – ex.: contractual repayment amounts (principal and interest) for loans for which there is any uncertainty about the timing and amount of the cash flows; or for which there is a risk that payments will not be made when due expected – ex.: reduced and/or delayed contractual repayment amounts; expected value of the collateral upon the loan, to be collected (when regular repayment is no more expected).

There are certain conditions in respect of the inclusion of the value of collateral

in the estimated future cash flows of the receivable.

Regulation for credit risk management for banks operating in R.Macedonia (11/20)

In Macedonia: liquid market exists for some equity shares (companies operating in

Macedonia) and for treasury and government bills and bonds (maturity ranges from 1 month to 3 years);

there is an active market for residential and commercial property, but it is not easily observable;

transactions for purchase and sale of industrial property are occurring irregularly (predominantly for privatisation purposes).

In addition: the time needed to overtake a collateral-property is between 6 months and

2 years. the time needed to sold the foreclosed collateral-property is usually more

than 18 months.

How to measure the “fair value” of assets when there are no observable active and liquid markets?

Regulation for credit risk management for banks operating in R.Macedonia (12/20)

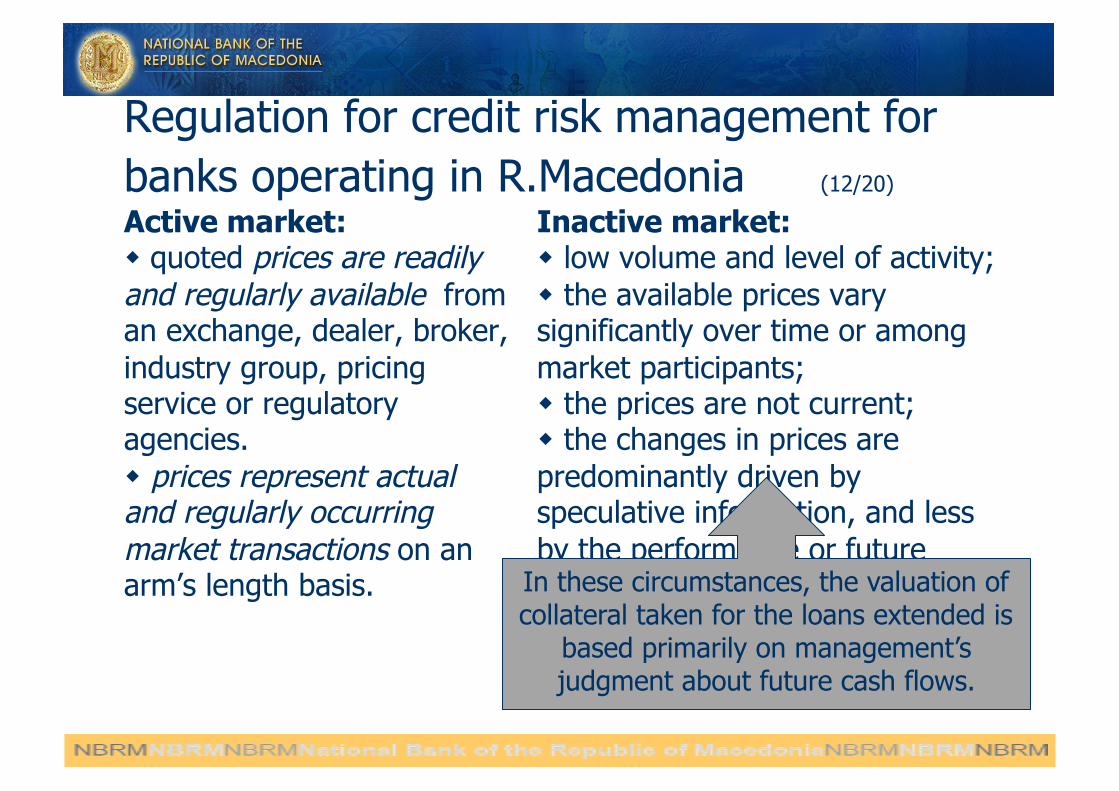

Active market: quoted prices are readily and regularly available from an exchange, dealer, broker, industry group, pricing service or regulatory agencies. prices represent actual and regularly occurring market transactions on an arm’s length basis.

Inactive market: low volume and level of activity; the available prices vary significantly over time or among market participants; the prices are not current; the changes in prices are predominantly driven by speculative information, and less by the performance or future plans of the market participants In these circumstances, the valuation of

collateral taken for the loans extended is based primarily on management’s judgment about future cash flows.

Regulation for credit risk management for banks operating in R.Macedonia (13/20)

Regulator’s perspective: How to measure the “fair value” of assets when there are

no observable active and liquid markets?

Regulator’s action: Prescribe the minimum characteristics of the market to be

fulfilled, in order the value of the asset - collateral to be taken into account when calculating impairment losses.

Regulation for credit risk management for banks operating in R.Macedonia (14/20) step 2: Determining the present value of the estimated future cash flows of the receivable

The value of the collateral is taken into consideration only if: • “first-class” collateral risk category “A” • unconditional irrevocable guarantee issued by non-banking financial or non-financial institution with a good credit standing (“A-” Standard&Poor’s; “A3” Moody’s) • the asset taken as collateral presents an “appropriate” asset for collection of the receivable

Regulation for credit risk management for banks operating in R.Macedonia (15/20)

step 2: Determining the present value of the estimated future cash flows of the receivable The asset taken as collateral presents an “appropriate” asset for collection of the receivable, if: • there is a functional market for the asset or similar assets; • there is information available for the realised transactions with the same or similar assets in the last 3 months; • the information about the realised prices is publicly available; • proceeds from eventual sale of the collateral are expected to be collected in a period less then 12 months from the date of foreclosure of the collateral. • ....some administrative/documentary criteria.......

if these criteria are met, the value of the collateral can be included in the estimated future cash flows of the receivable, up to the amount of the outstanding receivable.

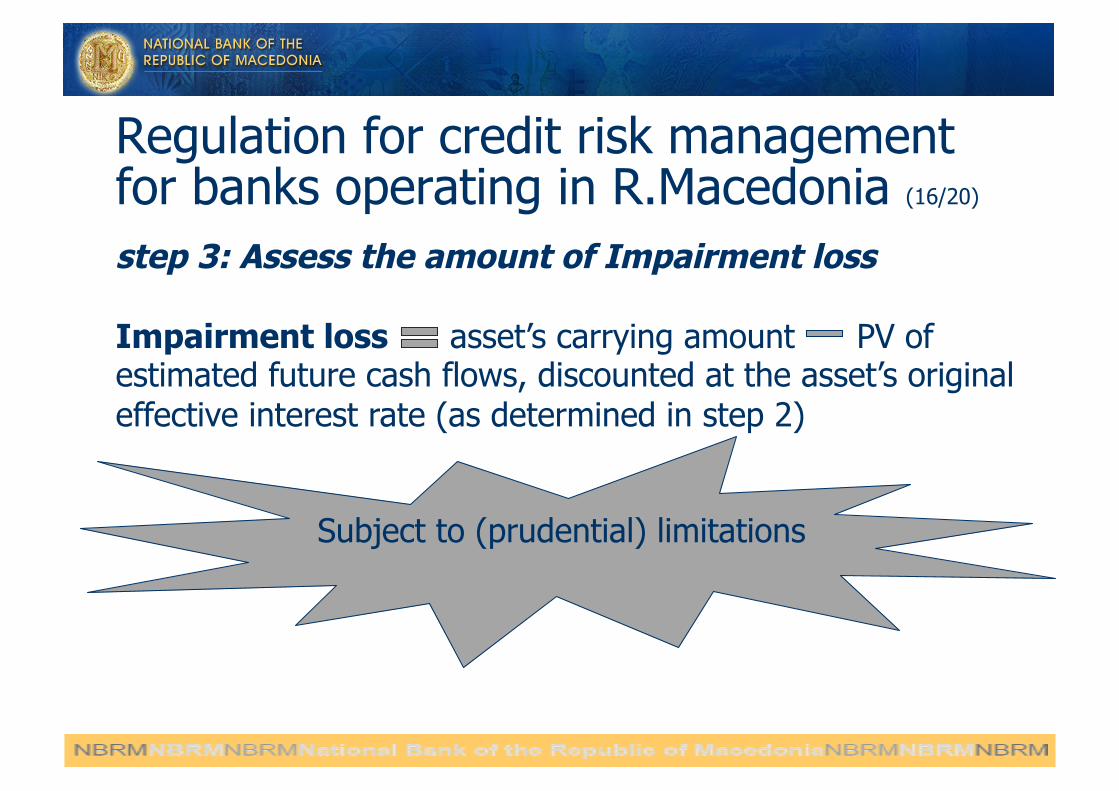

Regulation for credit risk management for banks operating in R.Macedonia (16/20) step 3: Assess the amount of Impairment loss

Impairment loss asset’s carrying amount PV of estimated future cash flows, discounted at the asset’s original effective interest rate (as determined in step 2)

Subject to (prudential) limitations

Regulation for credit risk management for banks operating in R.Macedonia (17/20)

Regulation for credit risk management for banks operating in R.Macedonia (18/20)

Risk category

Rang of % of impairment loss

A 0% - 10%

B 10.1% - 25%

C 25.1% - 50%

D 50.1% - 75%

E 75.1% - 100%

step 1 vs step 3:

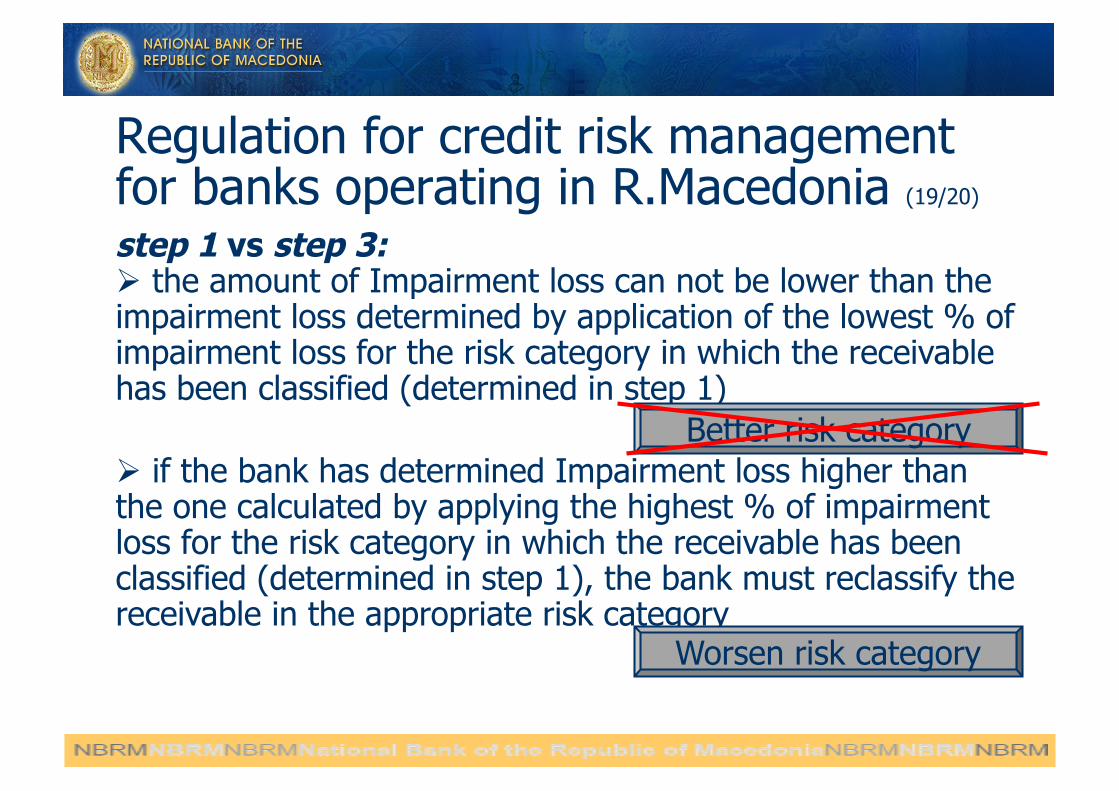

Regulation for credit risk management for banks operating in R.Macedonia (19/20) step 1 vs step 3: the amount of Impairment loss can not be lower than the impairment loss determined by application of the lowest % of impairment loss for the risk category in which the receivable has been classified (determined in step 1)

if the bank has determined Impairment loss higher than the one calculated by applying the highest % of impairment loss for the risk category in which the receivable has been classified (determined in step 1), the bank must reclassify the receivable in the appropriate risk category

Better risk category

Worsen risk category

Regulation for credit risk management for banks operating in R.Macedonia (20/20)

Effects / Differences in the recognised Impairment losses due to: (Non-)Inclusion of the value of collateral in the calculation of the recoverable amount Impairment loss can not be lower than the one calculated when applying the lowest % of impairment loss for the respective risk category Firstly, step 1: Classification; then calculation of Impairment loss, subject to prudential limitations

Content: IAS 39 Impairment principles Regulation for credit risk management for banks

operating in R.Macedonia Case study – work on an example Discussion

Case study – work on an example

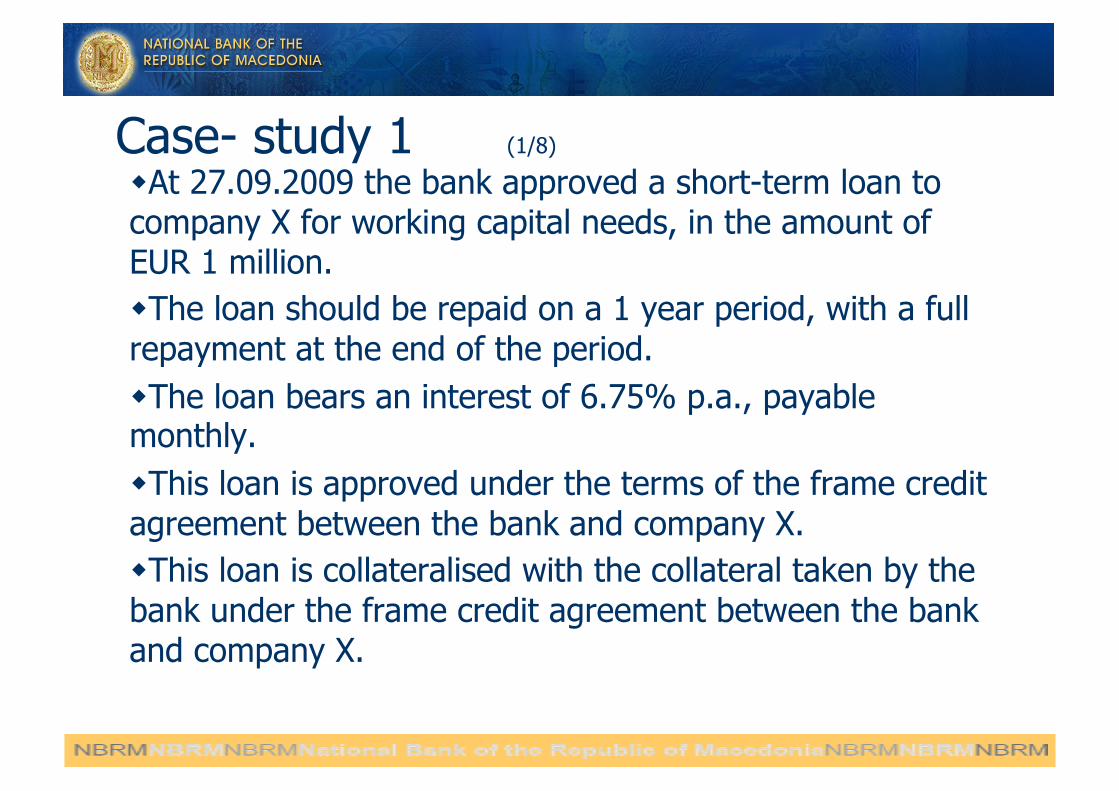

Case- study 1 (1/8) At 27.09.2009 the bank approved a short-term loan to company X for working capital needs, in the amount of EUR 1 million. The loan should be repaid on a 1 year period, with a full repayment at the end of the period. The loan bears an interest of 6.75% p.a., payable monthly. This loan is approved under the terms of the frame credit agreement between the bank and company X. This loan is collateralised with the collateral taken by the bank under the frame credit agreement between the bank and company X.

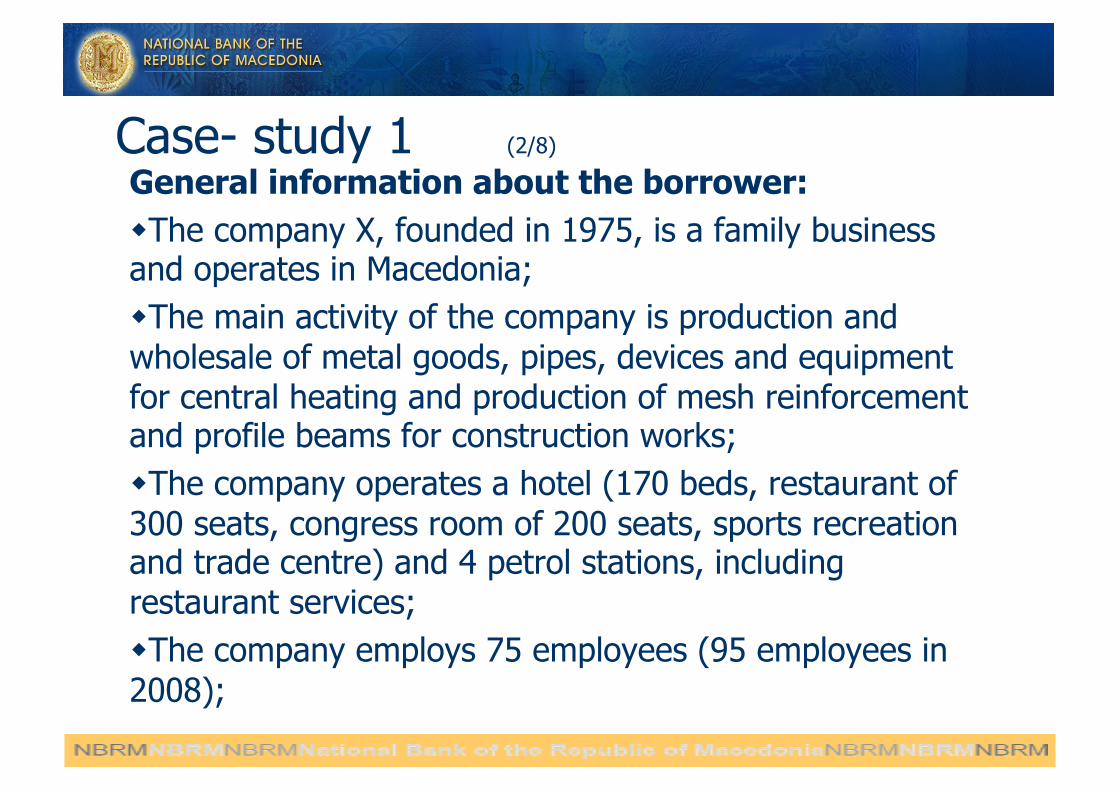

Case- study 1 (2/8) General information about the borrower: The company X, founded in 1975, is a family business and operates in Macedonia; The main activity of the company is production and wholesale of metal goods, pipes, devices and equipment for central heating and production of mesh reinforcement and profile beams for construction works; The company operates a hotel (170 beds, restaurant of 300 seats, congress room of 200 seats, sports recreation and trade centre) and 4 petrol stations, including restaurant services; The company employs 75 employees (95 employees in 2008);

Case- study 1 (3/8) The company has a frame loan agreement for utilizing different credit facilities from the Bank, within maximum credit exposure of EUR 8.4 million. Collateral:

In millions of Euro Value of the

collateral Date of

valuation

Collateral

Petrol station 0.8 02.09.2009

Petrol station 0.2 02.09.2009

Petrol station 0.1 02.09.2009

Hotel 4.8 02.09.2009

Pledge on raw materials 2.1 02.09.2009

Pledge on production equipment

1.2 02.09.2009

Total: 9.2

Case- study 1 (4/8) Credit facilities used by the borrower:

In millions of Euro 30.06.2010 31.12.2009 31.12.2008

Credit exposure

Principal 7.8 7.8 8.2

Interest 0.04 0.02 -

Off-Balance Sheet exposure

0.5 0.1 0.08

Total credit exposure:

8.3 7.9 8.3

Number of credit

facilities used

Short-term 6 12 8

Long-term 3 3 3

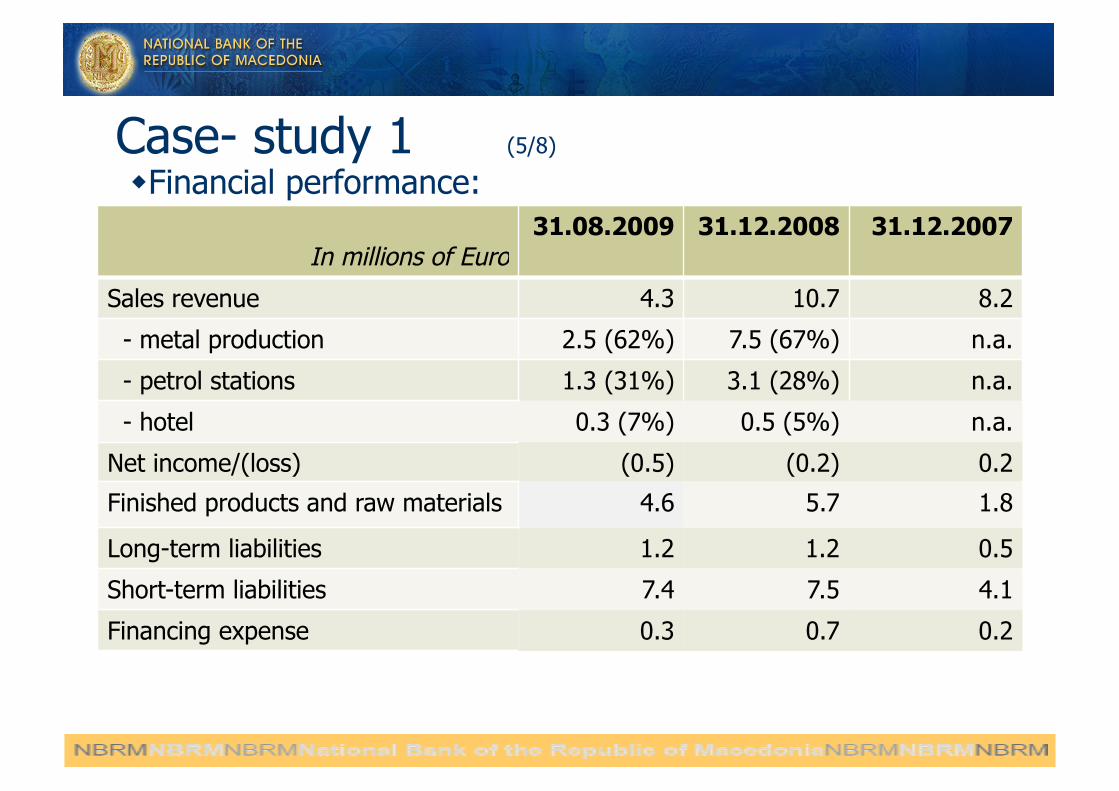

Case- study 1 (5/8) Financial performance:

In millions of Euro 31.08.2009 31.12.2008 31.12.2007

Sales revenue 4.3 10.7 8.2

- metal production 2.5 (62%) 7.5 (67%) n.a.

- petrol stations 1.3 (31%) 3.1 (28%) n.a.

- hotel 0.3 (7%) 0.5 (5%) n.a.

Net income/(loss) (0.5) (0.2) 0.2

Finished products and raw materials 4.6 5.7 1.8

Long-term liabilities 1.2 1.2 0.5

Short-term liabilities 7.4 7.5 4.1

Financing expense 0.3 0.7 0.2

Case- study 1 (6/8) Financial performance:

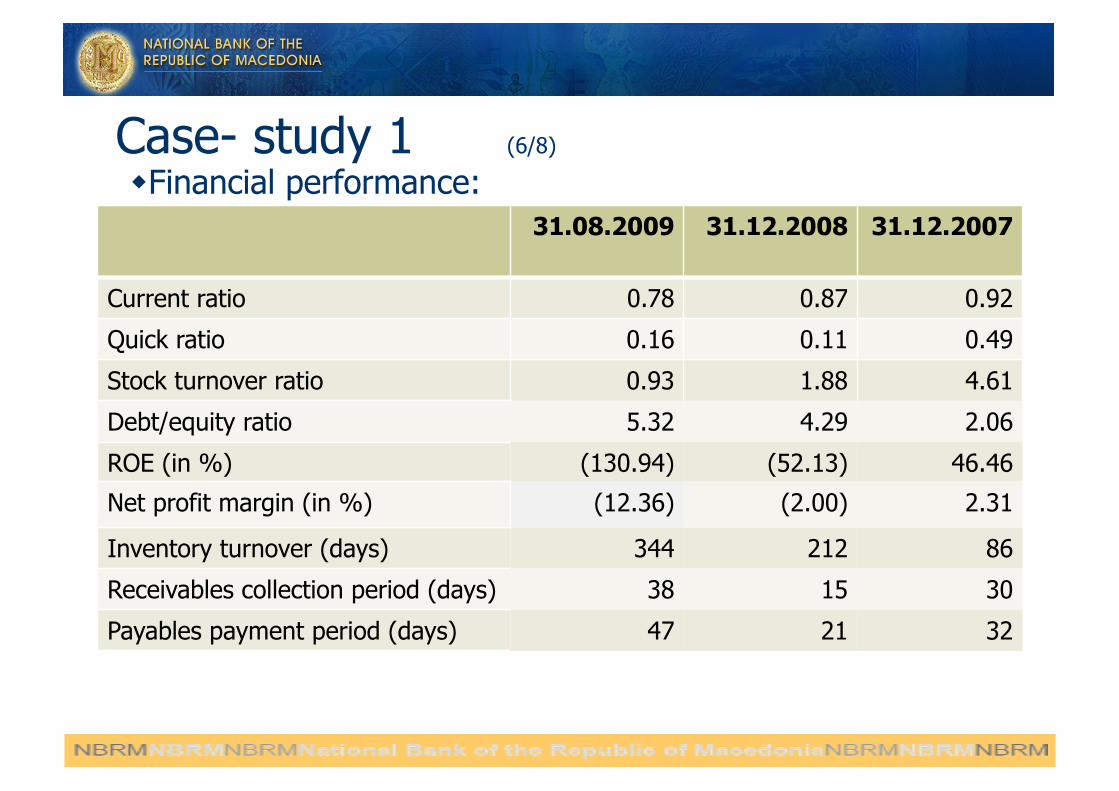

31.08.2009 31.12.2008 31.12.2007

Current ratio 0.78 0.87 0.92

Quick ratio 0.16 0.11 0.49

Stock turnover ratio 0.93 1.88 4.61

Debt/equity ratio 5.32 4.29 2.06

ROE (in %) (130.94) (52.13) 46.46

Net profit margin (in %) (12.36) (2.00) 2.31

Inventory turnover (days) 344 212 86

Receivables collection period (days) 38 15 30

Payables payment period (days) 47 21 32

Case- study 1 (7/8) Due to the global crisis, that impacted the metal industry as well, the company faces financial difficulties: realised loss in 2008 and 2009; deteriorated operating profit; deteriorated liquidity position in the second half of 2009; increase of inventory of both finished goods and raw materials; canceled purchase agreements from the company’s customers from Greece, Serbia, Croatia, Slovenia.

The external auditor issued qualified Audit opinion for the FS 2008, for the value of inventories (overstated for EUR 0.6 million)

Case- study 1 (8/8) The company services its liabilities to the bank regularly (source for repayment: revenues from the other businesses of the company (hotel and petrol stations) and by drawing new facilities from the bank for repayment of the previous facilities) In the 1st quarter 2010 the company requested a rescheduling of the short-term facilities into one long-term facility on a 7 years period, with regular monthly repayment schedule

Case- study 2 (1/8) At 11.08.2009 the bank approved a long-term loan to company Y for investment purposes (for expansion and modernization of the production process), in the amount of EUR 7.6 million. The loan has a grace period up to 30.06.2010. The loan is repayable on a monthly basis during 8 years (96 months) period after the grace period (up to 30.06.2018). The loan bears an interest of 6.75% p.a., payable monthly. This loan is collateralised with the collateral taken by the bank under the frame credit agreement between the bank and company Y. The company’s participation in the investment is 20%.

Case- study 2 (2/8) General information about the borrower: The company Y is the largest producer of steel and slabs in Macedonia and the only producer of hot rolled plates in the region; The major shareholder of the company is an international steel production and wholesale company; One part of the company’s business refers to processing activities for the major shareholder and the other part is own production and sale of company Y; The company is listed on the Macedonian Stock Exchange; The company employs more than 1,000 employees;

Case- study 2 (3/8) The company has a frame loan agreement for utilizing different credit facilities from the bank, within maximum credit exposure of EUR 39.5 million. Collateral:

In millions of Euro Value of the

collateral Date of

valuation

Collateral

Production facilities and administrative building

24.2 24.11.2009

Pledge over the production equipment, raw materials and finished products

75.1 24.11.2009

Future pledge on equipment (to be purchased under the investment project)

3.2 n.a.

Total: 102.5

Case- study 2 (4/8) Credit facilities used by the borrower:

In millions of Euro 30.06.2010 31.12.2009 31.12.2008

Credit exposure

Principal 23.9 23.9 13.2

Interest and other receivable

0.09 0.1 0.03

Off-Balance Sheet exposure

0.3 0.9 11.7

Total credit exposure:

24.4 24.9 24.9

Number of credit

facilities used

Short-term 20 12 13

Long-term 9 11 7

Case- study 2 (5/8) Financial performance:

In millions of Euro 30.06.2010 31.12.2009 31.12.2008 31.12.2007

Sales revenue 42.7 70.3 102.9 89.9

Net income/(loss) (0.2) 0.02 1.1 3.4

Finished products and raw materials

15.0 19.4 15.9 19.9

Long-term liabilities 18.6 12.5 8.8 4.1

Short-term liabilities 52.4 54.7 55.6 54.8

Financing expense 0.6 1.0 0.5 0.7

Case- study 2 (6/8) Financial performance:

30.06.2010 31.12.2009 31.12.2008 31.12.2007

Current ratio 0.47 0.43 0.44 0.59

Quick ratio 0.11 0.11 0.15 0.23

Stock turnover ratio 4.39 4.05 6.43 4.50

Debt/equity ratio 3.90 4.15 3.78 3.69

ROE (in %) (0.23) 0.04 1.73 5.22

Net profit margin (in %) (0.39) 0.04 1.08 3.74

Inventory turnover (days)

n.a. n.a. 74 110

Receivables collection period (days)

n.a. n.a. 25 44

Payables payment period (days)

n.a. n.a. 49 49

Case- study 2 (7/8) Due to the global crisis, that impacted severely the metal industry, the company faces financial difficulties: realising loss in 2010 and significantly decreased profit in 2009; change in the structure of the company’s activities – own production and sales significantly reduced (previously around 70% of production), while increased processing activities for the major shareholder; fall in sale prices on the international markets for more than 60% and sharp fall in demand since 2008; deteriorated liquidity position in the second half of 2009 and 2010 (part of it due to the investment project).

The external auditor draws attention to the going concern of the company, due to its large dependence on the major shareholder.

Case- study 2 (8/8) No redundancies, but salaries decreased for 15%. There is an agreement that the major shareholder will cover the company’s generated losses on a quarterly basis (in 2009: covered EUR 4.7million). The major shareholder extended a short-term interest-free loan in the amount of EUR 26 million, considered as permanent financing. The company services its liabilities to the bank regularly (source for repayment: by drawing new facilities from the bank for repayment of the previous facilities and by the financial support from the major shareholder). The company’s share price on the Macedonian Stock Exchange has decreased for around 32% in 2009 and 2010.

Case- study 1 and 2 You are required to: identify the impairment triggers, if any estimate the impairment loss as of 30.06.2010 classify the loan receivable in risk category, in accordance with the credit risk management regulation in R.Macedonia and estimate the level of impairment losses

Content: IAS 39 Impairment principles Regulation for credit risk management for banks

operating in R.Macedonia Case study – work on an example Discussion Discussion